国际结算全集合(英文版)

国际结算全集合(英文版)

3. 4.

5. 6. 7.

Correspondent banking relationship

Correspondent bank 代理行 the basis for cooperation of commercial banks all over the world to fulfill international settlement “a bank having direct connection or friendly service relations with another bank.” Selecting a correspondent bank: reputation and creditworthiness; size and financial status; location; services offered by it; polices and strength of it

forms of circulation

过户转让(assignment)非流通

特点:书面形式 转让通知原债务人或登记过户 受让人权利受前手缺陷的影响 当事人:转让人、受让人、原始债务人

交付转让(transfer) 准流通或半流通

特点:交付背书转让 不通知原债务人 受让人的权利受前手权利缺陷的影响 当事人:转让人,受让人

to maximize revenues; credit risks associated with financing extended to buyers or sellers

Factors in the payment decision

To exporters: protection against non-payment risks by the importers, such as: commercial risks, financial risks; political risks; risks in control of title to the goods,etc. convenience; cost; commercial competitiveness

国际结算(双语)教学全套课件1

Payment methods

Documents

remittances,

collPeactyimonesn,tlemtteetrhsods

of credit, standby lbeatnrcotkeoefmlrlgceiurotcaefttrdaiocanitnrnc,este,dessei,tltesa,,tntdebrys intleertntaetrioonfalcredit, facbtaonrkingguaanrdantees, forifnateitrinagtional

policies, certificates of origin, etc

Traditional payment method

case

• 1.The supplier agrees that the buyer will effect payments under the term of T/T against receipt of B/L by fax.

✓ UK Bills of Exchange Act of 1882; ✓《英国票据法》 ✓ US Uniform Commercial Code of 1962; ✓《美国统一商法》

• For documentary collections, documentary credits, standby credits, or guarantees, the applicable international customs and practices are:

factoring and forfaiting

commercial invoice,

pacDkoincgumlisetn,ts:

bilclsomofmleardciniagl, insinurvaoniccee,poplaiccikeisn,g celritsitf,icbailtlessooff orliagidni,nge,tcinsurance

国际结算英文版讲义

Comparison

among the three kinds of

remittances:

T/T It is in a form of dispatching cable or telex or SWIFT Authentication is made by test key. It is a safe method of remittance. The cost of remittance is higher. It is the fastest and most prevalent method of remittance. M/T D/D It is in a form of mail It is in a form of banker’s advice or payment order demand draft By signature (on payment order Not as safe as T/T lower Owing to its slower speed, banks reduce the use of M/T in the remittance the By signature (on draft) Not as safe as T/T lower It may be purchased by a bank other than drawee bank. It is a useful method of remittance. the

Banker’s Demand Draft, D/D

Remitter

① 票 汇 申 请 书 交 款 付 费 ④ 汇款通知书(票根) ② 银 行 即 期 汇 票

资金

③ 银行即期汇票 ⑤ 银 行 即 期 汇 票

国际结算(英文版)清华大学出版社-答案

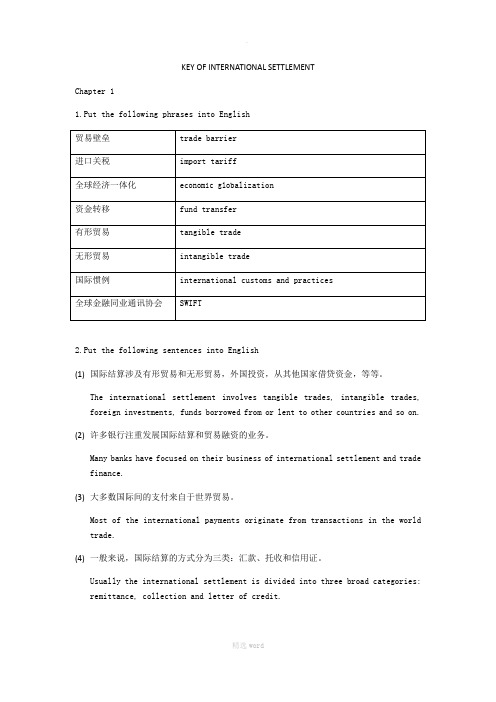

KEY OF INTERNATIONAL SETTLEMENTChapter 11.Put the following phrases into English2.Put the following sentences into English(1)国际结算涉及有形贸易和无形贸易,外国投资,从其他国家借贷资金,等等。

The international settlement involves tangible trades, intangible trades, foreign investments, funds borrowed from or lent to other countries and so on.(2)许多银行注重发展国际结算和贸易融资的业务。

Many banks have focused on their business of international settlement and trade finance.(3)大多数国际间的支付来自于世界贸易。

Most of the international payments originate from transactions in the world trade.(4)一般来说,国际结算的方式分为三类:汇款、托收和信用证。

Usually the international settlement is divided into three broad categories: remittance, collection and letter of credit.3. True or False1)International payments and settlements are financial activities conducted inthe domestic country. (F)2)Fund transfers are processed and settled through certain clearing systems.(T)3)Using the SWIFT network, banks can communicate with both customers andcolleagues in a structured, secure, and timely manner.(T)4)SWIFT can achieve same day transfer.(T)4.Multiple Choice1)SWIFT is __B__A.in the united statesB. a kind of communications belonging to TT system for interbank’s fundtransferC.an institution of the United NationsD. a governmental organization2)SWIFT is an organization based in __A___A.BrusselsB.New YorkC.LondonD.Hong Kong3) A facility in fund arrangement for buyers or sellers is referred to __A___A.trade financeB.sale contractC.letter of creditD.bill of exchange4)Fund transfers are processed and settled through __C___A.banksB.SWIFTC.clearing systemD.telecommunication systems5)__C__is the reason why international trade first began.A.Uneven distribution of resourcesB.Patterns of demandC.Economic benefitsparative advantages5. Answer the following questions1)Where are the medium of exchange originated from?Tracing back the history of international settlement, the medium of exchange originated from coins to notes.2)What will inevitably lead to under the international political, economic andcultural exchanges?The international political, economic and cultural exchange inevitably leads to credits and debts owed by one country to another.3)Why do banks focus on the development of the businesses of internationalsettlement?Banks focus more and more on the development of the businesses because it isa major resource of profits.4)What will banks do to meet the higher and higher demand of the internationalmarket?Banks need to develop innovative products and deliver the best services possible in whatever way they can.Chapter 21.Put the following phrases into English2.Put the following sentences into English(1)用于国际结算的货币是可兑换的货币。

国际结算 英文版2.3-2.4 Notes and Cheques

Copyright by Fei Zhonglin School of Economics and Management, NJUT12.3 Promissory notes (P/N)UBEA :A promissory note isan unconditional promise in writingmade by one person to another signed by the maker engaging to payon demand or at a fixed or determinable future timea sum certain in money to the payee, or to the order of, a specified person or to bearer.中国票据法定义:本票是出票人签发的、承诺自己在见票时或在指定的日期无条件支付确定金额给收款人或持票人的票据。

Copyright by Fei Zhonglin School of Economics and Management, NJUT 2本票实质是出票人和付款人为同一人的汇票。

①Issue ②present forpaymentDrawer (Maker)PayeeCopyright by Fei Zhonglin School of Economics and Management, NJUT3Specimen of a noteGeneral Promissory Note ( Trader ’s note )Promissory Note for USD12,345.00 Tianjin,12 Nov.2001At 60 days after sight, we promise to pay to the order of ABC Trade Co.the sum of US Dollars Twelve Thousand Three Hundred and Forty Five only.For Tianjing Textile Co.signedCopyright by Fei Zhonglin School of Economics and Management, NJUT 42.3.4 Differences between a bill and a noteUnconditional order vs. unconditional promise Basic partiesIn fact, most of acts relating to bills are also of relevance to notes, but there ’re some exceptions:acceptance;presentment for acceptance (Geneva Uniform Law: visa); acceptance for honor supra protest; bills in a set; Specimen of a billsee P.74Copyright by Fei Zhonglin School of Economics and Management, NJUT 52.3.5 Types of notesBased on the maker :The maker is a trader --Trader ’s note 商业本票/一般本票The maker is a banker--Banker ’s note 银行本票 Usually it is payable on demand and iscustomarily called “Casher ’s order ”出纳指示; China: Promissory notes = banker ’s notesCopyright by Fei Zhonglin School of Economics and Management, NJUT 6Other banker ’s noteInternational money order 国际小额本票Central banker ’s note 中央银行本票e.g. Treasury bills 国库券Negotiable certificate of deposit 流通存单Copyright by Fei Zhonglin School of Economics and Management, NJUT72.4 ChequesUBEA :A cheque is a bill of exchange drawn on a banker payable on demand.A three-party instrument, the drawee is a bank Payable on demand中国票据法定义:支票是出票人签发的,委托办理支票存款业务的银行在见票时无条件支付确定金额给收款人或持票人的票据。

国际结算 中英文终极版

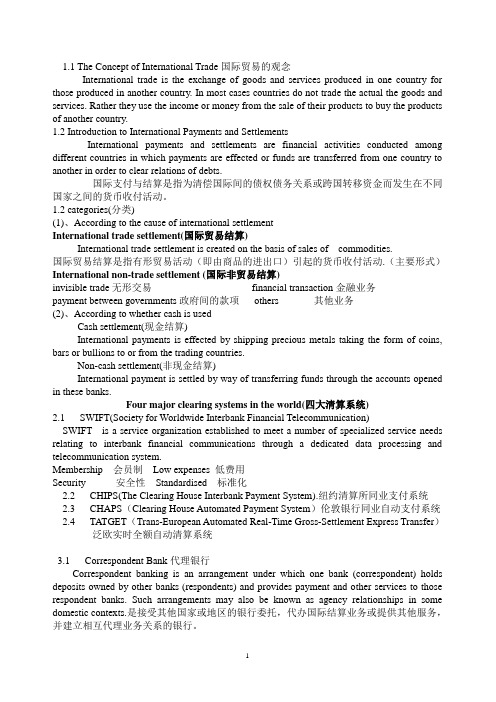

1.1 The Concept of International Trade国际贸易的观念International trade is the exchange of goods and services produced in one country for those produced in another country. In most cases countries do not trade the actual the goods and services. Rather they use the income or money from the sale of their products to buy the products of another country.1.2 Introduction to International Payments and SettlementsInternational payments and settlements are financial activities conducted among different countries in which payments are effected or funds are transferred from one country to another in order to clear relations of debts.国际支付与结算是指为清偿国际间的债权债务关系或跨国转移资金而发生在不同国家之间的货币收付活动。

1.2 categories(分类)(1)、According to the cause of international settlementInternational trade settlement(国际贸易结算)International trade settlement is created on the basis of sales of commodities.国际贸易结算是指有形贸易活动(即由商品的进出口)引起的货币收付活动.(主要形式)International non-trade settlement (国际非贸易结算)invisible trade无形交易financial transaction金融业务payment between governments政府间的款项others 其他业务(2)、According to whether cash is usedCash settlement(现金结算)International payments is effected by shipping precious metals taking the form of coins, bars or bullions to or from the trading countries.Non-cash settlement(非现金结算)International payment is settled by way of transferring funds through the accounts opened in these banks.Four major clearing systems in the world(四大清算系统)2.1 SWIFT(Society for Worldwide Interbank Financial Telecommunication)SWIFT is a service organization established to meet a number of specialized service needs relating to interbank financial communications through a dedicated data processing and telecommunication system.Membership 会员制Low expenses 低费用Security 安全性Standardised 标准化2.2 CHIPS(The Clearing House Interbank Payment System).纽约清算所同业支付系统2.3 CHAPS(Clearing House Automated Payment System)伦敦银行同业自动支付系统2.4 TATGET(Trans-European Automated Real-Time Gross-Settlement Express Transfer)泛欧实时全额自动清算系统3.1 Correspondent Bank代理银行Correspondent banking is an arrangement under which one bank (correspondent) holds deposits owned by other banks (respondents) and provides payment and other services to those respondent banks. Such arrangements may also be known as agency relationships in some domestic contexts.是接受其他国家或地区的银行委托,代办国际结算业务或提供其他服务,并建立相互代理业务关系的银行。

国际结算英文课件chapter 5

5.3 Payment Transaction by T/T

一、Cover Payment Method

5.3 Payment Transaction by T/T

一、Cover Payment Method 1、Only One “Instruction” Received 2、Properly Match the MT202 with the MT100

Payer (Creditor)

2、Procedure

Remitter (Debtor)

1.Remittance Application

3.Effect Payment

2.Payment Order by post

Remitting bank

Paying bank

5.2 Means of Remittance

5.Effect Payment

Remitting bank

6.Claim

Paying bank

5.3 Payment Transaction by T/T

一、Cover Payment Method 二、Serial Payment Method 三、Guideline to Interbank Compensation

5.2 Means of Remittance

T/T

[EXERCISE]: TEST_____ VALUE (DATE)________ OUR REF_________ PLEASE DEBIT OUR A/C OR ____________BRANCHES’A/C OR OUR HO A/C PAY AMOUNT _________ TO ________BANK FOR CREDIT OF _____BANK IN FAVOUR OF _____________A/C NO.__________ REMARKS___________

国际结算双语教材英语版

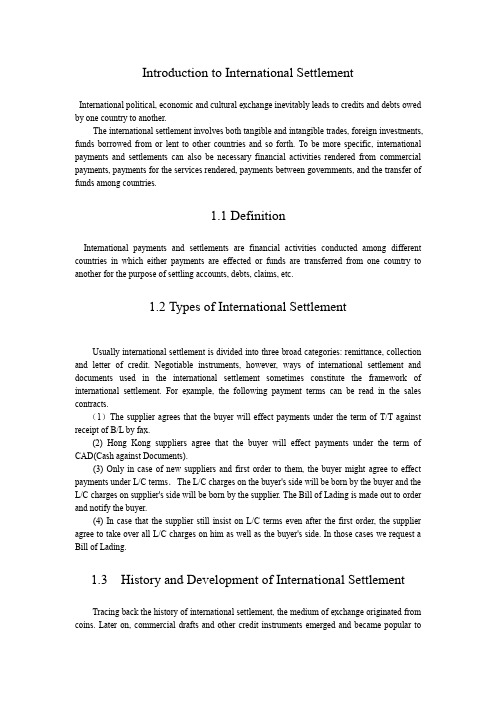

Introduction to International SettlementInternational political, economic and cultural exchange inevitably leads to credits and debts owed by one country to another.The international settlement involves both tangible and intangible trades, foreign investments, funds borrowed from or lent to other countries and so forth. To be more specific, international payments and settlements can also be necessary financial activities rendered from commercial payments, payments for the services rendered, payments between governments, and the transfer of funds among countries.1.1 DefinitionInternational payments and settlements are financial activities conducted among different countries in which either payments are effected or funds are transferred from one country to another for the purpose of settling accounts, debts, claims, etc.1.2 Types of International SettlementUsually international settlement is divided into three broad categories: remittance, collection and letter of credit. Negotiable instruments, however, ways of international settlement and documents used in the international settlement sometimes constitute the framework of international settlement. For example, the following payment terms can be read in the sales contracts.(1)The supplier agrees that the buyer will effect payments under the term of T/T against receipt of B/L by fax.(2) Hong Kong suppliers agree that the buyer will effect payments under the term of CAD(Cash against Documents).(3) Only in case of new suppliers and first order to them, the buyer might agree to effect payments under L/C terms.The L/C charges on the buyer's side will be born by the buyer and the L/C charges on supplier's side will be born by the supplier. The Bill of Lading is made out to order and notify the buyer.(4) In case that the supplier still insist on L/C terms even after the first order, the supplier agree to take over all L/C charges on him as well as the buyer's side. In those cases we request a Bill of Lading.1.3History and Development of International SettlementTracing back the history of international settlement, the medium of exchange originated from coins. Later on, commercial drafts and other credit instruments emerged and became popular tomeet the needs of the constantly increasing business activities in both geographical regions and volume of the international trade.Depending on the creditability of financial institutions, both buyers and sellers are usually willing to complete their settlement through banks respectively, and a financial arrangement could be reached then. Therefore, many banks have focused on their business of international settlement and trade finance.Most of the international payments originate from transactions in the world trade. With the enormous amount of international trade activities, the volume of the international settlement has reached trillions of US dollars nowadays. Banks; as a result, are focusing more and more on the development of the business because it is a major resource of profit.1.4 International Customs and PracticesThe International Chamber of Commerce is the world business organization. It is the only representative body that speaks with authority on behalf of enterprises from all services in every part of the world.(1)International Practices concerning Bills: Bill of Exchange Act, 1882, Jeva Uniform Bill Act.(2) International Practices concerning Settlement:(Uniform Rules for Collection, ICC Publication No: 522), Uniform Customs and Practice for Commercial Documentary Credits,1993 Revision, ICC Publication No. 500).(3) International Practices concerning Documents: Hague Rules, Hamburg Rules, International Convention Concerning the Transport of Goods by Rail, Agreement on International Rail-Road through Transport of Goods, Uniform Rules for a Combined Transport Documents, Institute Cargo Clauses, ICC, International Rules for Interpretation of Trade Terms, Incoterms2000 and UNCITRAL Arbitration Rule.Instruments2.1General IntroductionBills of Exchange, cheques, and promissory notes are all known as negotiable instruments. It is a fundamental principle of property law that we cannot obtain a better title than that possessed by the person from whom we received it. There is always the risk that that person has no title to the property because he has stolen it or obtained it from some other person who got improperly. The true owner, on discovering the property and proving his right to it, can demand the property be restored to him. Our remedy is to look for the person from which we received the property and try to get our money back. That person will in turn claim from his immediate transferor, this tracing right goes on up to the unfortunate one who bought the property from the thief.2.2 Bills of Exchange2.2.1 DefinitionA Bill of Exchange (draft) is a commercial instrument. It is an unconditional order in writing, addressed by one person to another,signed by the person giving it,requiring the person to whom it is addressed to pay on demand,or at a fixed or determinable future time,a sum certain in money,to or to the order of a specified person or to the bearer.A typical Bill of Exchange is drawn in this manner(see Specimen 2.1)·Note:●An unconditional order in writing.●Addressed by one person (the drawer).●To another (the drawee).●Signed by the person giving it.●Requiring the person to whom it is addressed.、、●To pay.●On demand or at a fixed or determinable future time.● A sum certain in money:●To or to the order of a specified person or the bearer.2.2.2 Liability on Bills of ExchangeThe liability on a Bill of Exchange is by signature only: no signature, no liability. In another words, no person is liable as drawer, endorser or acceptor of a bill who has not signed.2.2.3 Endorsement of Bills of ExchangeFor many commercial contracts, the benefits of the contract may be transferred from one person to another. With a Bill of Exchange, this transfer is effected by delivery, or by endorsement and delivery. Endorsement is a signature and a signature must be the same with the transferor's name as stated on the bill. It is normally on the back of the document. There are four types of endorsement: blank, special, restrictive or conditional.2 .2.4 Acceptance of Bills of Exchange The drawee has no liability on the bill until he signs the bill in ,such a way as to signify acceptance of liability to pay the money stated on the bill. The acceptance of a bill is the signification by the drawee of his assent to the order of the drawer. An acceptance is invalid unless it complies with the following conditions, namely:(1)It must be written on the bill and signed by the drawee. The mere signature of the drawee, without additional words, is sufficient.(2) It must not express that the drawee will perform his promise by any other means than the payment of money.Acceptance may be made before signature by the drawer. It may also be accepted when overdue or when previously by non-acceptance or non-payment.2.2.5 Holders of Bills of Exchange.A holder for value is the holder of bill for which value has been given: he is a holder for value as regards all parties prior to himself. Once value is given for a bill, the-holder giving value and all subsequent holders are holders for value. A holder for value has the right of transferability conferred upon him by the common law. He has exactly the same rights together, with faults andfailings, if any, of the person who transferred the bill to him.2.2.6Duties of Holders of a Bill of ExchangeA Bill of Exchange holder must do two things:present the bill for acceptance and present the bill for payment. The holder must carry out his duties. Alternatively, he can transfer the bill to another person, within a "reasonable time" of receiving the bill.Presenting the bill for acceptance is personal. The bill is presented to the drawee personally for acceptance, wherever he is. In so doing, the holder gains an extra signature and thereby an extra liability on the bill. If the drawee refuses to accept the bill, the bill is then dishonored by non-acceptance and the holder can immediately sue all prior parties to the bill.Presentment for payment is local, meaning that the bill must be presented at the right place whether or not the person liable on the bill is at that place. The right place is the place stated on the bill as being the place of payment, otherwise the bill should be presented at the place of business or the place of the drawee/acceptor. The payment should be presented during business hours.2.2.7 Liability of Drawers,Drawees and Endorsers(1)Liability of DrawersBy drawing the bill the drawer commits himself to the following:a. That it will be duly accepted or paid on presentment, andb. That if it is dishonored he will compensate the holder or any endorser for any loss suffered.(2) Liability of DraweesBefore acceptance, the drawee is not liable to any holder (though he may be personally liable to the drawer if he dishonors a bill properly drawn upon him).After acceptance, the drawee becomes the person primarily liable on the bill, and engages that he will pay the bill according to the terms of his acceptance.(3) Liability of EndorsersAny person who endorses a bill makes a commitment that it will be duly paid upon presentment. If the bill is dishonored he will compensate the holder who is compelled to pay it.2.2.8 Dishonor of Bills of ExchangeIf a bill is dishonored by non-acceptance or non-payment, the holder must inform all prior parties that the bill has been dishonored. If such notice has not been given within a reasonable time, all prior parties except the person primarily liable on the bill will cease to be liable to the holder. The person primarily liable on the bill is the drawer. Once the bill is accepted, the acceptor assumes primary liability.2.3 Cheques2.3.1 DefinitionA cheque is an unconditional order in writing, addressed by a person to a bank, signed by the person making it, requiring the bank to pay on demand a sum certain in money to onto the order ofa specified person or to the bearer.2.3.2Parties to a ChequeThree parties are essentially involved:●The Payee, a person to whom a cheque is expressed to be payable.●The Drawer, the person who writes the cheque.●The Drawee, the bank on whom the cheque is drawn and to whom the order to pay isgiven.2.3.3 SignatureAn agent may sign a cheque if he is authorized. For example; a bank officer may sign on behalf of the bank for which he works provided he is an authorized signatory.2.3.4 ForgeryIf the drawer has not signed (and he cannot truly have done that if his signature has been forged), then the document without the drawer's signature is not a cheque.For example, if John Black steals Wolf Smith's cheque book, forges Mr. Smith's signature to a cheque USDS,000 and presents it to the bank on which it is drawn and obtained payment, the bank cannot debit Mr. Smith's account with it, for the bank's only authority to debit the account is Mr. Smith's genuine signature. The bank would lose the money unless the forgery was immediately discovered after payment. However, if the bank had paid the forger John Black,then its only right would be against the forger, for what it was worth.2.4 Promissory Notes2.4.1 DefinitionA promissory note is an unconditional promise in writing, made by one person (the maker)to another (the payee or the holder), signed by the maker, engaging to pay on demand or at a fixed or determinable future time a sum certain in money, to or to the order of a specified person or to bearer.A promissory note is a promise, and a bill is an order. There is no need to protest a dishonored note. And as the maker of a promissory note is the person primarily liable on it, there can be no acceptance.A promissory note is not complete when the maker signs it. It must also be delivered to the payee or bearer.A typical promissory note is made in this manner (see Specimen 2.3).Note:●An unconditional promise in writing.●The maker.●The payee or the holder.●Engaging to pay.●On demand or at a fixed or determinable future time.● A sum certain in money.2.4.2 Liability of MakersThe maker of a promissory note should be engaged in the payment according to its tenor, and is precluded from denying to a holder in due course the existence of the payee and his then capacity to endorse.2.4.3 Banker's DraftsA banker's draft is a negotiable instrument drawn payable to order by a bank as drawer on the same bank as' drawee, in another word, the drawer and drawee are the same person. It is issued by a bank for certain fixed amounts, always payable to bearer and on demand. Even though the draft may be drawn by a branch of head office or another branch; and the bank is considered as one entity for this purpose. It is also a legal tender.It goes without saying that a banker's draft is as good as cash for many commercial purposes, dishonor of it being unheard of unless it is known that the presenter is not entitled to it.Remittance and Collections3.1 DefinitionRemittance refers to the transfer of funds from one party to another among different countries through banks. At the request of its customer, a bank transfers a certain sum of money to its overseas branches or correspondent banks and instructs them to pay a named person or corporation in that country.3.2 Means or Instruments of RemittanceThe remittance will be done by several means or instruments such as mail transfer, demand draft and telegraphic transfer. The instruments mentioned above bear their characteristics, which will be discussed later.3.2.1 Mail Transfer (M/T)A mail transfer is to transfer funds by means of a payment order or a mail advice, or sometimes a debit advice issued by a remitting bank, at the request of a remitter. Either of a payment order, mail advice or debit advice must be authenticated with tested key or the authorized signatures of the remitting bank. It instructs the paying bank to pay a certain sum of money to the beneficiary. Upon receipt of the payment order, the paying bank verifies the tested key or the authorized signature, notifies the beneficiary, pays to him and claims reimbursement from the remitting bank. In practice, the remitting bank credits the account for the paying bank in the remitting bank.3.2.2 Demand Drafts(D/D)A demand draft is often used when the customer wants to transfer the funds to his beneficiary by himself. The remitter will make a written request of issuance to the remitting bank. Then the remitting bank debits the remitter's account, issues a bank draft and forwards it to the remitter who may send or carry it abroad to the payee. Upon receipt of the draft, the payee can either present it for payment to the drawee’s bank or sell it to his own bank crediting his account. The drawee's bank verifies the signature, pays the draft and claims back the amount paid in accordance with itsagency arrangement with the remitting bank.3.2.3Telegraphic Transfer(T/T)Telegraphic transfer refers to remittance by SWIFT. It is exactly the same as a mail transfer, except that instruction from the remitting bank to the paying bank is transmitted by cable/telex/SWIFT instead of by mail. Therefore, it is faster, but more expensive than the mail transfer. It is often used when the remittance amount is large and the transfer of funds is subject to a time limit. Thus, 90% remittance is done through T/T.Table 3.1 Comparison among T/T,MT and D/D3.2.3 Collections3.3.1 DefinitionAfter the exporter has shipped the goods or rendered services to his customers abroad, he draws a Bill of Exchange on the latter with or without shipping documents attached thereto and then gives the draft to his bank together with his appropriate collection instructions. Thus, a collection on the basis of commercial credit is usually processed through banks acting as the intermediary.3.3.2 Workflow(1)The exporter ships goods and obtains documents of title from the shipping line.(2) The exporter, known as the principal, delivers the following documents to his bank (remitting bank): a. a Bill of Exchange drawn on the importer; b. documents for goods of title and c. a collection order which contains the exporter's instructions to the remitting bank.(3) The remitting bank completes its own collection order addressed to the importer's bank.(4) If the instructions are D/P (documents against payment), the importer's bank will release the documents to the importer only against payment. If the instructions are D/A(documents against acceptance), the importer's bank will release the documents against acceptance of the Bill of Exchange by the importer.(5) The bank credits the proceeds to the principal's account.3.3.3 Documentary Collections(1)DefinitionA documentary collection is an operation in which a bank collects payment on behalf of the seller (the principal) by delivering documents to the buyer.Documentary collections are suitable in cases where the exporter is reluctant to supply the goods on an open account basis, but does not need the strong security provided by a documentary credit. A documentary collection is more secure than settlement on open account, because the importer can take possession of the goods with either making payment or accepting a Bill of Exchange. The banks concerned are under no obligation to pay. The exporter is relieved of a large part of the administrative work connected with the collection of documents, and benefits from the banks’worldwide network of contacts. Thanks to the less stringent formal requirements, this service is cheaper and more flexible than a documentary credit.With a documentary collection, however, the exporter is not certain, at the time of dispatch of the goods whether the buyer will actually make the full payment. This form of settlement is therefore most appropriate in the following cases:●the exporter has little doubt about the buyer's willingness and ability to pay;●the political, economic and legal environment in the importing country is considered tobe stable;●the buyer's country has placed no restrictions on imports (e.g. exchange controls).(2) Types of Documentary Collectionsa. Documents against Payment (D/P)The presenting bank is authorized to release the documents to the drawee only against immediate payment. That means the payment should be effected on first presentation of the documents. Sometimes there is no draft in the documentary collection due to the levy of stamp duty.b. Documents against Acceptance (D/A)The presenting bank releases the documents to the importer against his acceptance of a Bill of Exchange, which is usually payable 30-180 days after sight or at a fixed future date. The presenting bank must ensure that the acceptance of the Bill of Exchange is complete and correct. However, the presenting bank bears no responsibility for the authenticity of the signature, the authority of the signatory to sign or the creditworthiness of the acceptor.With a D/A arrangement, the importer takes possession of the goods before payment is actually effected. Once the goods have been released, the exporter's only safeguard is the Bill of Exchange accepted by the importer.c. Acceptance with, Documents against PaymentWith this type of documentary collections, the exporter gives instructions that the importer, when presented with the documents, shall accept a Bill of Exchange drawn at, say, 60 days aftersight. The documents may not, however, be released to the importer until the bill has been paid. In other words, the release of documents is made against payment of tenor drafts.Acceptance. with documents against payment is not encouraged by International Chamber of Commerce.3.3.4 Uniform Rules for Collections(URC)The Uniform Rules for Collections (URC) form an internationally accepted code of practice covering documentary collections. URC are not incorporated any national or international law, but are normally binding on all parties because all bank authorities (especially the collection instruction) will state that the collection is subject to URC (ICC Publication No: 522, URC522).URC522 will apply unless the collection instruction states otherwise or the laws in one of the countries concerned specifically contradict them.3.3.5 Collection InstructionsHaving dispatched the goods and prepared the documents, the exporter is ready to request his bank to arrange a collection. The specimen of collection. instruction is a standard form which enables the exporter to include specific instructions to his bank regarding the documentary collection. The collection instruction must be clear and complete, since the handling of the transaction by the remitting and collecting banks will be governed solely by the instructions contained in the collection instruction. The most important parts included in the collection instruction are instructions regarding documents and payments.(1)Instructions to Release Documentsa. D/A refers to the release of documents against acceptance of tenor drafts. The collecting bank will fulfill his obligation when the documents are delivered upon the acceptance of the draft.b. D/P refers to the release of documents against payment of sight drafts or simply against payment.c. D/P at xx days after sight refers to the release of documents against payment of tenor drafts. In order to avoid confusion with the operation of D/A, the statement "Deliver documents only after payment was effected" should be written into the collection instruction.(2) Instructions to Effect PaymentOne of the following three options of collection instructions may be chosen:a. When the remitting bank has an account with the collecting bank, the collection instruction will be “please credit our account with you under you SWIFT/airmail advice to us".b. When the collecting bank has an account with the remitting bank, the collection instruction will be "please collect the proceeds and authorize us by SWIFT/airmail to debit your account with us".c. When there is no account relationship between the remitting bank and the: collecting bank, the collection instruction will be "please collect and remit the proceeds to X Bank for credit our account with them under their SWIFT/airmail advice to us".(3) Additional Instructionsa. The collection instruction should give specific instructions about whether or not to protest in the event of non-payment or non-acceptance. If the importer refuses to pay or to accept the Bill of Exchange when the documents are presented, the presenting bank must send notice of this to the exporter through the remitting bank.The bank will not institute a protest unless expresslyinstructed to do so.b. The exporter should give the name and address of a representative or agent in the country of importer who will be responsible for the warehousing and resale of goods in the event of non-payment. The collection instruction should specify if there is a party known as the "case of need". If a case of need is named, the collecting bank will refer to him in the event of dishonor for guidance or instruction.3.3.6 Legal Position of Banks(1)Duties of Remitting BanksThe bank's legal liability is set out in the Uniform Rules for Collections. Banks must verify that the documents received comply with the one specified in the collection instruction, and carryout the instructions given by the principal.a. Documents ProcessingBanks have no responsibility to examine the documents thoroughly. The remitting bank will make additional checks before sending them to collecting bankb. International Practice in Conducting the BusinessFor matters not mentioned in the collection instruction, the remitting bank should handle the collection business in compliance with the international practice in terms of those unmentioned in the collection instruction. For instance, under URC522, Article 5 (d),remitting bank may choose collecting bank for the principal if no collecting bank is named in the collection instruction.In addition, banks assume no liability in case the instructions they transmit are not carried out, even if they have taken the initiative in choosing such banks according to URC522, Article11(b).Moreover, according to URC522, Article 4(a), all the documents sent for collection must contain complete and precise collection instructions, including one specifying that the collection is subject to URC522.c. Liability for NegligenceUnder URC522, banks shall act in good faith and excise reasonable care. Banks will be liable for the loss caused by negligence on the part of the bank: For example, the remitting bank fails to inform the principal of the refusal of payment from the collecting bank in time, and thus causes loss to the principal. Also, the remitting bank is responsible for the documents sent to the collecting bank by wrong address.(2) Duties of Collecting Banksa. Implementation of Collection InstructionsUsually there is a correspondent relationship between remitting bank and collecting bank, and correspondent agreements are signed by them. Collecting bank handles the collection business according to the collection instruction. According to URC522, Article 4, collecting banks are only permitted to act upon the instructions given in such collection instruction and in accordance with URC522.Any deviation from these instructions at the request of importer will be at the peril of the collecting bank.If the collection instruction is unclear, the collecting bank should contact the remitting bank timely and wait for the further instruction. If the collecting bank finds it difficult to follow up the instruction given by the remitting bank, e.g. goods consigned to the collecting bank without prior agreement, the collecting bank can ignore it. The collecting bank has no obligation to take delivery of goods, which remain at the risk and responsibility of the party dispatching the goods uponURC522, Article 10.b. Documents HandlingAccording to URC522, Article 12, the collecting bank must verify that the documents received are in order as they are listed in the collection instruction and must advise by telecommunication or, if that is not possible, by other expeditious means without delay, the party from whom the collection instruction was received of any documents missing or found to be other than listed. The collecting bank has no further obligation in this respect. Documents are to be presented to the importer in the form in which they are received according to URC522,Article 5.The advice from the collecting bank which forwards to the importer is accompanied by photocopies of the documents. These provide the importer with essential facts about the goods that have been sent and tell him whether the documents received by the bank will enable him to take delivery of the goods and clear them through customs. The importer may go to the bank's offices and examine the papers. The bank, however, is not allowed to let him inspect the goods at the place of destination without authorization from the exporter.With a D/A transaction, the accepted Bill of Exchange either remains with the collecting bank or is returned to the remitting bank, depending on the instructions given by the exporter. In the latter case, the remitting bank delivers the bill to the exporter, who can either discount it or have it collected at maturity. In the case of medium-term maturity, there may be the possibility of selling the bill to a forfeiter or using it as security for a bank advance. The collecting bank should be responsible for keeping the accepted Bill of Exchange and the documents before the payment is effected by the importer:c. Protection of GoodsAccording to URC522, Article 10, in the event that goods are dispatched directly to the address of a collecting bank or to the order of a collecting bank for release to an importer against payment or acceptance or upon other terms and conditions without prior agreement on the part of that bank, such bank will have no obligation to take delivery of the goods, which remain at the risk and responsibility of the party dispatching the goods. Even when specific instructions are given to the collecting bank to take actions in respect of the goods to which a documentary collection relates, including storage and insurance of the goods, the collecting bank has no obligation to do so, and it should advise the remitting bank accordingly. However, in the case that the collecting bank takes action for the protection of the goods, whether instructed or not, it assumes no liability with regard to the condition of the goods, or any acts and omissions on the part of any third parties entrusted with the custody or protection .of the goods. But the collecting bank must inform without delay the bank from which the collection instruction was received of any such action taken.(3) Liability of Collecting Banksa. Documents ReleaseUnder URC522, Article 19, partial payment in documentary collections will be accepted only if specifically authorized in the collection instruction. Otherwise, the collecting bank will release the documents to the importer only after full payment has been received, and the collecting bank will not be responsible for any consequences arising out of any delay in the delivery of documents.b. Completeness and Correctness of Bill AcceptanceThe collecting bank is responsible for ensuring that the form of the acceptance of a Bill of。

国际结算(双语)

EXW

FCA

EX WORKS(…named place)工厂交货条件

FREE CARRIER(… named place)交至承运人条件

FAS

FOB

FREE ALONGSIDE SHIP (… named port of shipment)船边交货条件

FREE ON BOARD (… named port of shipment)装运港船上交货条件

A Bank

Current a/c XXX

B Bank

B Bank‟s currency

Nostro A/C XXX is A Bank‟s __________________a/c

Exercise:

Current a/c XXX

A Bank

B Bank

A Bank‟s currency

Vostro A/C XXX is A Bank‟s __________________a/c,

Establish a correspondent relationship between two banks.

Agency arrangement Control documents

What do control documents include?

Control Documents

Lists of specimen of authorized signatures 印鉴 是银行列示的所有有权签字的人的有权签字额度、签字范围、 有效签字组合方式以及亲笔签字字样。代理行可凭其核对对 Verify the messages, letters(airmailed) are 方银行发来的电报、电传等的真实性。 authentic Telegraphic test keys密押 Verify the telex and cable are authentic 是两家代理行之间事先约定的专用押码,在发送电报时,由

国际结算英文课件Chapter 2

2.6.1 SWIFT Address/BIC Standard

SWIFT BIC Structure: a. Bank Code PNBP b. Country Code US c. Location Code 33 d. Branch Code PNBP US 3N NYC COMM CN SH NJG

Message Type

MT752 MT754 MT756 MT760 MT767

Transaction

Payment authorization Advice of payment/acceptance Advice of reimb. Or payment Guarantee Guarantee amendment Advice of receipt of guarantee Advice of release Advice of debit Advice of credit

2.3 EUR Clearing Systems

2.3.1 Euro

Euro is the name given by the European Council of Madrid to the new single European currency.

2.3.2 Two Key Clearing Systems:TARGET and Euro 1

security, only member banks have access to the network through the use of secure logon key.

2.6.1 SWIFT Address/BIC Standard

Bank Identifier Codes(BIC) are a universal method of identifying financial institutions in order to facilitate automated processing of telecommunication message in banking and related financial environments.

国际结算(双语版)

2.1.1 Definition of Remittance 2.1.2 Basic parties of Remittance

1. Remitter and payee 2. Remitting bank and paying bank 2.1.3 Characteristics of Remittance 1. High risk. 2. Fast speed and low cost.

Chapter Chapter Chapter Chapter Chapter Chapter Chapter Chapter Chapter Chapter Chapter

1 Negotiable Instrument 2 Remittance 3 Collection 4 Letter of credit 5 Types of letter of credit 6 Introduction of UCP600 7 Documents in credit 8 Standby letter of credit 9 Letter of Guarantee 10 Forfaiting 11 International Factoring

3.2.2 Documents against Acceptance (D/A)

3.3.1 The risk of collection. 1. Risk for seller 2. Risk for buyer 3.3.2 The risk management of collection 3.3.3 Financing under collection 1. Outward bill purchasing 2. Trust Receipt (T/R) 3. Delivery against Bank Guarantee

国际结算 英文版3 Remittance

III Payment techniques• What are payment techniques?– Under certain circumstance, use some methods and instruments to settle claims and debts. – How to settle claims and debts? – Contents of payment techniques: when, where, under what kind of condition, use which currency, instrument and transfer procedure.Different payment techniques• Remittance • Collection • • • • •on the basis of Business CreditLetter of credit Standby letter of credit Bank guarantee International factoring International forfaitingon the basis of Bank CreditCopyright by Fei Zhonglin School of Economics and Management, NJUT1Copyright by Fei Zhonglin School of Economics and Management, NJUT2Factors in payment decision• • • • Protection Convenience Cost Commercial competitivenessTrade-offs among above four criteria3. Remittance3.1What is a remittance?– A bank, at the request of its customer, transfers a certain sum of money to its overseas branch or correspondent bank, instructing it to pay a named person domiciled in that country.BuyerSellerCopyright by Fei Zhonglin School of Economics and Management, NJUT3Copyright by Fei Zhonglin School of Economics and Management, NJUT43.2 Basic parties to a remittance• • • • Remitter / Payer (汇款人) Remitting Bank(汇出行) Paying Bank(汇入行/解付行) Payee or Beneficiary(收款人/受益人)3.3 Types of remittance• Mail Transfer (M/T, 信汇)– Cheap and slow, typically used for remittance of small sums or of little urgency• Telegraphic Transfer (T/T,电汇)– Safe and fast, the most popular way of remitting funds• Remittance by Bank’s Demand Draft (D/D,票汇) – Payment is guaranteed by the remitting bank, and demand draft is payable to the specified payee who can transfer the draft before it is presented for payment. Usually used for non‐trade settlement.Copyright by Fei Zhonglin School of Economics and Management, NJUT 5 Copyright by Fei Zhonglin School of Economics and Management, NJUT 61APPLICATION FOR OUTWARD REMITTANCEProcedures of M/T and T/T□T/T电汇(汇款申请书)□M/T信汇 □D/D票汇AMOUNT(金额)Remitter contract Payee /Beneficiary (buyer) (seller) A. Submit E. Provide remittance D. Notify and B. Receipt payment application, make payment receipt proceeds , commission C. Send payment order by mail or telegraphic Remitting Paying bank bank F. Send debit advice and payment receiptCopyright by Fei Zhonglin School of Economics and Management, NJUT 7AMOUNT IN WORDS(大写金额)BENEFICIARY’S NAME (收款人姓名) BENEFICIARY’S BANK ACCOUNT NUMBERS (收款人往来行帐户) BENEFICIARY’S ADDRESS(收款人地址)REMITTER’S NAME&ADDRESS TEL.(汇款人姓名)MESSAGE(汇款人附言)Copyright by Fei Zhonglin School of Economics and Management, NJUT 8The obligations of remitting bank• Carefully examine the contents of the remittance application; • Carefully examine the authenticity and coherence of related documents provided by remitter; • Make sure there are enough funds in remitter’s account; • Make Payment Order (P.O.) according to the remittance application, choose reasonable remitting route; • The ways of reimbursement of remittance cover should be expressed on the P.O. definitely, if necessary, use Bank Transfer (B.T.) to inform the third bank effecting reimbursement to paying bank.Copyright by Fei Zhonglin School of Economics and Management, NJUT 9The obligations of paying bank• Authenticate the signature or test key of payment order to ensure its genuineness; • Notify the payee and request the latter to perform related procedures in compliance with the policies of foreign exchange; • Follow the instruction of P.O. to effect payment; • Get the payment receipt from payee and send it to the remitting bank with the debit advice.Copyright by Fei Zhonglin School of Economics and Management, NJUT10Procedures of D/DRemitter (buyer) A. Submit remittance application, proceeds and commission Payee /Beneficiary (seller) D. Send the demand draft E. Present F. Make the demand payment draft contractRemittance & Reverse remittancepayment instrument seller funds payment instrument sellerPaying bankbuyer顺汇B. Draw a demand draftbuyer逆汇Remitting bankC. Send D/D advice G. Send debit advicefunds• 判断标准:支付工具和资金的流向是否一 致,买方付款是否主动11 Copyright by Fei Zhonglin School of Economics and Management, NJUT 12Copyright by Fei Zhonglin School of Economics and Management, NJUT2Outward remittance and Inward remittance• Outward remittance: The remittances which are handled by the home remitting bank • Inward remittance: The remittance which are handled by foreign paying bankVostro account and Nostro accountVostro account: B’s account with A Nostro account: A’s account with B Bank ABank BVostro account: A’s account with B Nostro account: B’s account with ACopyright by Fei Zhonglin School of Economics and Management, NJUT13Copyright by Fei Zhonglin School of Economics and Management, NJUT143.4 Reimbursement of remittance cover• The paying bank has maintained an USD account with the remitting bank, suppose an outward remittance in USD is made:There’s a Vostro account of USD• The remitting bank has maintained a GBP account with the paying bank, suppose an outward remittance in GBP is made:There’s a Vostro account of GBPIn cover, we have credited your account with us.In cover ,please debit our account with youRemitting bank Remitting bank Paying bank15Paying bankCopyright by Fei Zhonglin School of Economics and Management, NJUTCopyright by Fei Zhonglin School of Economics and Management, NJUT16• Both paying bank and remitting bank have maintained USD account with XYZ Bank, suppose an outward remittance in USD is made :In cover, we have authorized XYZ Bank to debit our account and credit your account with them.Remitting bankPaying bankXYZ bankCopyright by Fei Zhonglin School of Economics and Management, NJUT 17 Copyright by Fei Zhonglin School of Economics and Management, NJUT 183• Remitting bank and paying bank have not maintained account with each other, nor have kept accounts with same third Bank , suppose an outward remittance is made, remitting bank should write “cover instruction” as follows:– In cover, we have instructed Bank X to remit proceeds to your account with Bank Y.3.5 Application of remittance in international trade• Characteristics of remittance– Efficient, timely and cost effective; – The transfer of funds is independent of transfer of goods, so it is risky; – The financial burden is not same to the buyer and seller, so it is unfair.Copyright by Fei Zhonglin School of Economics and Management, NJUT19Copyright by Fei Zhonglin School of Economics and Management, NJUT20• Payment in Advance (cash in advance, 预付货款) • Payment upon arrival of goods (C.O.D.货到付款)– Consignment – Open account • Other charges, esp. for services – freight charges, insurance premium – ad-rate, packing charges, interest for deferred payment,etc. – commission, refundment, indemnity, etc.汇款撤消与挂失• 汇款能否撤销?– M/T, T/T撤消条件:退汇必须在解付之前做出• 汇款人退汇 • 收款人退汇– D/D 撤消条件:退汇必须在汇款人寄出汇票前做出• 票汇时,汇票遗失如何处理?– 向汇入行出具担保书以防重付 – 汇入行向汇出行做出挂失止付指示 – 退汇或补发汇票Copyright by Fei Zhonglin School of Economics and Management, NJUT21Copyright by Fei Zhonglin School of Economics and Management, NJUT224。

国际结算双语课程标准--英文版

Practice 2. TT process operation

4

Collection

To understand the definition of collection,be familiar with the international practice,parties and application of collection

International settlement(bilinguacoluisrsme) standard

First, summary of course

It is the core course of international economic and trade major, based on the operating skills’ cultivation about methods of international settlement, combining theory with reality, emphasising on positional operation, paying attention to the cultivation of comprehensive ability about finding, analyzing and solving problems, etc.

1.Definition of standby letter of credit

2.Characteristics of standby letter of credit

3.Differences between standby letter of credit and documentary letter of credit

INTERNATIONAL SETTLEMENT CHAPTER 1国际结算第一章

International

settlement

Instruments

• Bills of exchange

• Cheques

Payment Methods

• Promissory Note

• Remittance

• Collection

• Letter of Credit

• Bank Guarantee &Standby Credit

《国际结算(理论,实务,案例)》, 蒋琴儿,秦定编著,清华大学出版 社,2006年

《国际结算》张东祥主编 武汉大学出版社出版,2004年

《国际贸易结算与融资》, 程祖伟 韩玉军 编中国人民大学出版社, 2004 年5月第二版

《金融专业英语证书考试教材(现代银行业务)》中国金融出版社,2002 年

Packing list

Weight memo

Certificate of Original

All kinds of Certificates

Rules URC

UCP URG

课程成绩

平时:30%,考勤,回答问题,课堂练习, 作业等

期末:70%,闭卷考试,英文试卷

课 程 教 材:

教材名称:《国际结算(英文版)》

主 编:秦定、高蓉蓉 出 版 社:清华大学出版社 出版年份:2010年2月

参考文献:

《International Settlements 国际结算》,邵新力,机械工业出版社, 2012年

学习指导:

在学习国际结算方式时,注重理论联系实际,要求学生用 所学的国际结算基本原理来分析和处理每一种结算方式中 的案例,掌握开立信用证,审单,制单,电汇和票汇等基 本技能。同时让学生了解国际结算与国际贸易,贸易融资 和出口信贷的相互之间的关系与区别,以及综合运用的能 力。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

From cash settlement to non-cash settlement From goods trading to documents trading From direct payment between traders to payment effected through a financial intermediary

to maximize revenues; credit risks associated with financing extended to buyers or sellers

Factors in the payment decision

To exporters: protection against non-payment risks by the importers, such as: commercial risks, financial risks; political risks; risks in control of title to the goods,etc. convenience; cost; commercial competitiveness

Characteristics and developing trend

1. 2. the scale and scope of international settlement get greater and greater International lending and financing is closely combined with international payments On the basis of international customs and practice International guarantees applied to international settlement More diversified vehicle currencies The proportion of commercial credit in international settlement gets bigger A much facilitated international banking network connected with electronic telecommunication

Correspondent banking relationship

Meaning of International Settlement

the financial activities conducted among different countries in which payments are effected or funds are transferred from one country to another in order to settle claims and debts,emerged in the course of political ,economic or cultural contacts among them.

International Settlement

Chapter One Introduction

Concept

Category Evolution

Players and theirs roles

Factors in payment decisions Characteristics and developing trend

Negotiable intsruments(票据):

bills of exchange, promissory notes, checks

Payment techniques:

remittances,collections, letters of credit, bank guarantees, international factoring and forfaiting

safety, high efficiency, low cost, standardization

Electronic settlement

SWIFT CHIPS CHAPS FEDWIRE TARGET

SWIFT(Society for worldwide interbank financial telecommunication)环球同业银行金融电讯协会 特点:标准化;安全可靠,自动加核密押;高速度,低费用. 业务分类:客户汇款(customer transfer);银行头寸调拨 (bank transfer);外汇业务(foreign exchange confirmations);托收业务(collections);证券业务 (securities);贵金属和银团贷款业务(precious metals and syndication);信用证和保函(documentary credits and guarantees);旅行支票(travelers cheques);银行帐单处理 业务(statements).

Documents:

bills of lading,insurance policies, certificates of origin, etc

Category of international settlement

Trade settlement: payments for visible trades Non-trade settlement: 1、invisible trade settlement: payments for services, technology transfer, patents and copyright contracts, etc 2、financial transaction settlement: buying and selling of financial assets, overseas money-raising and investing 3、payments between governments:aids and grants 4、others: overseas remittances, inheritances, etc

Players and their roles

Exporter

to get prompt payment; minimize non-payment risks

Importer

to receive goods as ordered; pay as late as possible

Financial intermediary