F6 taxation-57

2019年ACCA考试科目及内容

2019年ACCA考试科目及内容第一部分为基础阶段,主要分为知识课程和技能课程两个部分。

知识课程主要涉及财务会计和管理会计方面的核心知识,也为接下去实行技能阶段的详细学习搭建了一个平台。

知识课程的三个科目同时也是FIA方式注册学员所学习的FAB、FMA、FFA三个科目。

技能课程共有六门课程,广泛的涵盖了一名会计师所涉及的知识领域及必须掌握的技能。

具体课程为:第二部分为专业阶段,主要分为核心课程和选修(四选二)课程。

该阶段的课程相当于硕士阶段的课程难度,是对第一部分课程的引申和发展。

该阶段课程引入了作为未来的高级会计师所必须的更高级的职业技能和知识技能。

选修课程为从事高级管理咨询或顾问职业的学员,设计了解决更高级和更复杂的问题的技能。

具体课程为:所有学生必须完成三门核心课程。

ACCA科目内容介绍(中文版)基础阶段:知识课程F1会计师与企业F1《会计师与企业》是P1《公司治理,风险管理与职业道德》和P3《商务分析》的基础。

涵盖:企业组织,公司管理,会计和报告体系,内部财务控制,人力资源管理,会计职业道德您将会学到:企业是如何运作的,会计师和审计师在企业中的作用,如何使用科学的人力资源管理方式,如何使企业和财务的各个环节的处理符合职业道德和价值观。

F2管理会计F2《管理会计》是F5《业绩管理》和P5《高级业绩管理》的基础。

涵盖:管理会计,管理信息,成本会计,预算和标准成本,业绩衡量,短期决策方法。

您将会学到:如何使学员能够处理基本的成本信息,并能向管理层提供能用作预算和决策的信息。

F3财务会计F3《财务会计》是F7《财务报告》和P2《公司报告》的基础。

涵盖:财务会计,财务信息,复式记账法,会计系统,试算平衡表,业务交易,会计事项的记录以及合并报表基础知识。

您将会学到:如何利用财务会计相关的原则和概念,使用复式记账法,编制基本的财务报表。

基础阶段:技能课程F4公司法与商法F4《公司法》与F7《财务报告》、F8《审计与认证业务》、P1《公司治理,风险管理与职业道德》、P2《公司报告》都有着一定的联系。

ACCAF6TXTaxation(TX)ACCA复习笔记13时间专题

ACCAF6TXTaxation(TX)ACCA复习笔记13时间专题ACCA F6 TX Taxation (TX) ACCA复习笔记 13 时间专题ACCA Taxation-United Kingdom - 13时间专题与时间有关的个税、企税内容1. UK ResidentAutomatic overseas tests ⼀定是①过去3年没有交过UK个税,税务年度中在UK时间<46天②过去3年⾄少1年交过UK个税,税务年度中在UK时间<16天③在UK外有full-time⼯作,税务年度中在UK时间<90天Automatic UK tests ⼀定不是①该税务年度中在UK居住满183天②Has a home in UK, no home overseas③Work full-time in UK during the tax yearSufficient UK ties test 可能是(表格不⽤背诵,考试会给出)5 UK ties①有⼈: spouse/civil partner配偶或伴侣, child under 18②有住: 在UK有房且在tax year中住过③有实质性⼯作: full-time/part-time/self-employed④过去两个税务年度中⾄少1年在UK居住超过90天⑤本税务年度中居住在UK的时间最久(可能在多个国家和地区居住过)2. Individual Tax 个税【Review: TX复习笔记2】1)可在计税时减除的Travel Expense:只减除与temporary workplace(≤24months)的部分2)Taxable Benefit: Living accommodationAdditional Charge若第⼀次居住⽇距离购⼊⼤于6年,ori. Cost → MV@⼊住⽇计算3) PAYE Forms①P11D: provide to employee by 6 July②P60: Provide to employee by 31 May③P45: 给年中离职的职员 3 copiesPenalty (late filling PAYE within 3 months)Over 3 months, additional penalty:5%*tax and NIC due----------------------------------------------------------【Review: TX复习笔记4】1)Marketing cost开始贸易经营之前7年内发⽣的⼴告费⽤可以减除2)Capital allowancea. Short life asset life < 8year 单列资产b. Assets life ≥ 25 years (aircraft) --SRP----------------------------------------------------------【Review: TX复习笔记5】1) Begining period 1~3注意BP2 有3种情况2) Closing/Cessation year①结业时间早于5 April, 与上⼀tax year合并计算②结业时间晚于5 April,最后⼀段全部计⼊*计算Closing year记得减去期初的overlap relief3) Early trade loss relief开始trade的前4年中产⽣loss, 可以按FIFO的顺序抵减之前三年的Total net income Before PA.4) 注意terminal loss的分段:结业⽇往前推12个⽉,以 6 April 分为两半----------------------------------------------------------【Review: TX复习笔记7】Payment of CGT----------------------------------------------------------【Review: TX复习笔记8】1) Wasting Chattelsestimated remaining useful life ≤ 50 years2) PPR ReliefPeriod of Occupation (分⼦)①Actual occupation②Last 18 months 销售⽇之前18个⽉中的未居住的部分③Work overseas 视同居住④Work in other place of UK→最多48 months⑤Any reason: 36 months*③④⑤前和后须存在actual occupation3) PPR for Business use⽐如:利⽤房⼦1楼开商店①During whole period: last 18 month不送②Partial period: last 18 month 依然送----------------------------------------------------------【Review: TX复习笔记9】1) Gift relief Notification DateFor Year 2019/20, both parties should notify HMRC Before 5 April 2024 (within 4 years)2) Deferred Gain 缴税⽇3)计提 Investors' Relief 的条件a). investor:不是该企业的 employee 或 director;b). dispose 的是购⼊时未上市公司的股票(可<5%)c). 必须在 6 April 2016 年后获得这些股票d). 这些股票的获取必须通过认购(subscribe)获得e). 持有满 3 年3. Self-assessment and Payment of Tax – Individuals 常考2’客观题,很重要1) Amendment for tax return: 修改期12 months after the due date of Electronic return.2) Compliance Check 审核、抽查期a)正常交:The first anniversary上交后的⼀周年内b)晚交:上交后的⼀周年+1个季度⽇Quarter dates (31 Jan, 30 Apr, 31 July, 31 Oct)3) Payment of tax4) Penalty & Interest 参照笔记104. Corporate Tax【Review: TX复习笔记11】1) 资产购⼊时间在Dec. 2017之前才有资格计IA2) Matching Rules for shares卖出shares的顺序:①Same day②销售⽇前9天③FA1985 pool: 1 April 1982~销售⽇前10天(考虑IA的计算)5. 企税的计算与缴纳期限 (Task 23)Review Task 22 Augmented profit 判断公司⼤⼩1. Non-Large Company#Interest to HMRC#Interest from HMRCTaxable under Investment Income2. Large Company分4期缴税#Short Accounting Period (AP<12 months)前3期:AP开始⽇后的第7、10、14个14号第4期:AP结束⽇后的第4个14号第4期:多退少补*可能出现第4期⽇期在第3期之前的情况,删掉第3期#Transitional Relief成为Large company 的第⼀年:若Augmented Profit≤£10 million则本年度可以使⽤Non-large Co. 的缴税⽅法做。

特许公认会计师 F6考试常用计算公式与答题方法介绍

特许公认会计师 F6考试常用计算公式与答题方法介绍ACCA F6的标准格式的确很复杂,所以有很多同学就会自己创造一种新的格式,或者是直接使用恒等式得出计算结果。

确实最后那个数字是正确的,但是在F6的考试中那个数字恰巧不是很重要。

那么临考前有什么办法能够帮助自己多拿几分呢?浦江财经为你介绍特许公认会计师F6考试常用计算公式与答题方法。

大家在做题的时候发现考官给的标准答案后面附带了很多的“NOTE”。

这些“NOTE”其实并不是ACCA考试答案的一部分,而只是考官关于题目考点的解释。

那么我们应该在什么时候写“NOTE”呢?通常情况下在计算中遇到“exempt income”, “exempt benefit”以及capital gain计算的“exempt asset”的时候才需要写“NOTE”。

NOTE不需要写的长篇大论,通常推荐用一句话把事情表达清楚就可以了,毕竟通常这些条目只有half Mark。

Adjustment of trading profit Trading profit 的调整是考试当中的重要考点,但是考生的得分率通常都不尽人意,为什么会这样呢?1、格式书写不符合规范如下是案列trading profit 调整的固定提问方式:Where a question requires the adjustment of profits, candidates will be told in there quire ments what figure to start their computation with (normally the net profit figure for an unincorporated business, or the profit before taxation figure for a limited company). They will also be told that they should list all of the items referred to in the notes to the question, indicating by the use of zero (0) any items, which do not require adjustment. Please see the end of this article for different wording used in variant papers.考生会被要求从一个固定的数字开始调整。

浅谈对acca的认识

浅谈对acca的认识ACCA在国内受到热捧,是非常适合大学生考取的国际高端财经证书。

下面就带大家认识一下ACCA比较重要的几点。

1)全面完善的课程体系。

ACCA课程使学员全面掌握财务、财务管理、审计、税务及经营战略等方面的专业知识,提升分析能力并拓宽战略思维。

2)理论与实际的密切结合。

ACCA的专业资格是理论知识与实际经验的高度紧密结合。

新考试大纲充分表达了雇主和专业人士的意见,反映了现代商务社会对财会人员的要求。

3)对专业价值和职业操守的重点强调。

ACCA创举性地开设了在线职业操守训练课程,它给予学员一系列的职业操守的理念,并设置了多个自我测试题,检验学员职业操守的价值观和行为。

取得ACCA会员资格要完成三个“E”,即通过考试、完成在线职业操守训练课程、并取得三年相关工作经验。

4)国际标准与本地实情的和谐统一。

ACCA考试大纲以国际会计准则/国际财务报告准则和国际审计准则作为依据设计考试内容,并提供了包括中国在内的40多种不同国家和地区的法律与税务方面的试卷,这使得ACCA成为最切合中国实际的国际性会计师资格。

5)公平一致的考试标准。

ACCA的专业资格考试采用全球统一标准,即统一教材、统一考试、统一评卷,最后会员取得全球统一的证书。

6)遍布全球的考点网络。

学员在一个国家向ACCA注册后,可根据需要在全球350多个考点中选择、更换适合自己的考试中心。

7)认证与学位的相互补充。

ACCA在全球范围内寻求与优秀院校的广泛合作。

满足一定的条件后,ACCA学员将有机会获得英国牛津-布鲁克斯大学应用会计理学士学位。

8)灵活的学习方式。

学员可以根据自己的实际情况,选择参加培训班或自修以及网上培训来完成ACCA考试。

急速通关计划 ACCA全球私播课大学生雇主直通车计划周末面授班寒暑假冲刺班其他课程。

ACCA F6 常用计算及格式

Income tax 计算格式Non‐savings income Savings income Dividend income Trading profit X X Employment income X X Property business income X X Savings (x100/80)X X Dividends (x100/90)X X Total income X X X X Less: qualifying interest paid(X)(X) Net income X X X X Less: personal allowance(10000+‐)(X) Txable income X X X X Income tax liability X Less tax suffered at sourceDividends (10%)XSavings (20%)XPAYE (20‐45%)X(X) Income tax payable X Trading Profit(only for self‐employed)个税Profit Before Taxation X Add: Non‐deductible expenditure X Less: Income under other schedules(X)Interest Income(X)Dividend Income(X)Rent Income(X)Profit on disposal of non‐current(X) Less: Capital Allowance (私用扣WDA; AIA asset; FYA; BC/BA(X) Tax adjusted Trading Profit X Employment Income X Salary货币收入X Bonus货币收入XCommission货币收入X Add:Benefit in kind非货币收入X Less: Allowable deduction如OPC职位养老金(X) Employment Income XTaxable benefit on not‐job related living accommodation X General Charge = Annual value & Rent paid by the employer,取高值X Add:Additional charge = (Cost ‐ £75,000) * official interest rate X这里,如购买日‐第一次出租<6年,取Cost;>6年,取第一次出租时MV Less: Job related part(X) Less: Rent paid by employee(X)XMileage AllowanceEmployer Paid X Less: HMRC 10,000 at 45p; > 10,000 at 25p(X) Taxable benefit X Or Allowable deduction(X) Capital Gain TaxGross proceeds X Less: Incidental costs of disposal(X) Net proceeds X Less: Cost(X) Less: Enhancement expenditure包括诉讼费,建围栏(X) Capital gain/(capital loss) X/(X) Less: Individual annual exemptio11000如果已经为loss,不再扣(X) Taxable gain X/0 Capital LossCurrent gains XCY capital losses先抵扣当年损失(X)1X Capital losses b/fwd再抵扣去年损失(X)2X Less: Individual annual exemptio11000(X) Taxable gain如net loss,可带去次年X Part disposalProceeds of part disposal A Less: selling costs(X) Net proceeds X Less: Original cost of whole asseA/(A+B) = C(C) Chargeable gain X Gift Relief (纯赠送)A: Disposal proceeds MVLess: Cost(X)Capital Gain X'Less: Gift Relief(X')Chargeable Gain (Donor No gain/No loss) 00 B:Base cost of asset = MV – Gift Relief(Rest of the gain is rolled over into the base cost for a subsequent disposal of the asset) Gift Relief for sale under value (半卖半送)A: Disposal proceeds MVLess: Cost (X)Capital Gain X1先算X2,倒退得X1X1Less: Gift Relief for sale at under value (Balancing Figure)(X)Chargeable Gain X2(X2=Actual consideration ‐ cost)X2 B:Base cost of asset = MV – Gift Relief for sale at under value = consideration(Rest of the gain is rolled over into the base cost for a subsequent disposal of the asset)Gift of shares 难点!Free hold property CBA & CALeasehold property CBA & CAStock流动资产,都不是Debtors T/R,流动资产,都不是Investments CAPlant (cost & proceeds <6000Non wasting chattel, exemptCreditors T/P, Liability,都不是Lifetime tax: proformaGift X Less: AE (X) Less: AE b/f (X) Net gift after exemptions X Less: Nil band remaining:Nil band at date of gift X*less: CLTs in last 7 years be(X)(X)X Tax@20% (or 20/80) X * Nil band for 2014/15 is 325,000Death tax: proformaGross CLT/PET X Less: nil band remaining: Nil band on death325000Less: GCTs in 7 years before gift(X)Nil band remaining(X)X Tax @ 40% IHT IHT Less: taper relief% × IHT (X)(X)XLess: lifetime tax (on CLT) (X) Death tax due X Death estate: proformaCHARGEABLE ESTATE XLess: nil band remaining: Nil band on death325000Less: GCTs in 7 years before death(X)Nil band remaining(X)X Tax @ 40% IHT IHT Corporation tax 计算格式Trading Profits(accruals)X Investment Income (accruals)(accruals)X Property Business Income (accruals)(accruals)X Net chargeable gains (receipts)(cash basis)X Less: Qualifying charitable donations (payments)(cash basis)(X) Taxable total profits X PLUS: Franked Investment In非关联企业(<50%)分红X Augmented Profits (for tax rate only)X Trading profit企税Profit before taxation X Add: Non‐deductible expenditure X Less:Income under other schedules(X) Less: Capital allowance – P&M(X) Trading Profit X Investment IncomeInterest income (actual cash amount received gross by companies)Less: Interest payable for underpaid / overdue taxLess: Property loan interest*所有非经营活动产生的利息,都从Invest income下减去Chargeable Gains ₤Proceeds X Less: Incidental cost on disposal (X) Allowable expenditure X Less: cost (X) Less: incidental cost on purchase(X) Less: improvement (X) Unindexed Gain X Less: Indexation allowance (IA)(% increase in RPI to 3 d.p. x Allowable expenditure) (X) Indexed gain X Less: Rollover relief (X) Less: Capital loss – current period (X) – carried forward (X) Chargeable Gain X PAYE tax codeAllowances:Personal allowances XHigher rate relief XExpense deductions X X Less: DeductionsBenefits XUntaxed income XTax under payments b/f gross up (x100/20 or 100/4上一年少交的税X(X) Allowance to set against pay XL ‐ Tax code for born after 5 Apr 1948P ‐ Tax code for born between 6 Apr 1938 ‐ 5 Apr 1948Y ‐ Tax code for born before 6 Apr 1938。

F6 (MLA) Taxation说明书

This presentation will start with an overview of the F6(MLA) Taxation syllabus, as well as of the examinable legislation and details of the exam format.In the second part of the presentation, I will discuss some areas where candidates typically do well/struggle based on my experience of candidates’performance in this paper.The purpose of the F6 (MLA) Taxation syllabus is to introduce candidates to the Maltese tax system and to cover the core areas of the main taxes in Malta as they affect both individuals and companies.The F6 (MLA) Taxation syllabus and study guide can be found on the ACCA website at the following link:/uk/en/student/exam-support-resources/fundamentals-exams-study-resources/f6/syllabus-study-guide/f6-syllabus-study-guide-malta-mla.html#More specifically,the key areas of the F6 (MLA) Taxation syllabus are the following:•The Maltese tax system and its administration•Individual income tax•Corporate income tax•Tax liabilities on the disposal of capital assets•Social security contributions•Value added taxWhile the exam will always touch upon each of these areas to some degree, and therefore none of these areas ought to be overlooked, it is of course immediately apparent from past papers that certain areas of the syllabus carry more weight than others. For instance, income tax as it applies to individuals and companiesinvariably features far more prominently than social security contributions.This diagram is reproduced from the F6 (MLA) Taxation syllabus and study guide, and illustrates in diagrammatical form the key syllabus areas covered by thepaper.The tax rates and allowances tables provide the tax rates which candidates are to use in a given exam sitting.The 2016 tax rates and allowances tables to be used for F6 (MLA) Taxation exams in June and December 2017 are published on the ACCA global website at the following link:-/content/dam/acca/global/PDF-students/acca/f6/examdocs/f6-mla-examdocs-2017.pdfAs an example of the application of the cut-off rules, on 8 August 2017 legal notice 205 of 2017 was published, whereby a number of updates were effected to the Fringe Benefit Rules. As these amendments were passed before 30 September 2017, they will become examinable as from the June and December 2018 papers. Anything enacted after 30 September 2017 will not be examinable until the 2019 papers.Usually, questions in F6 (MLA) Taxation will refer to the current year. However, even if an earlier and/or later year is tested, candidates shouldapply the same legislation.The F6 (MLA) Taxation exam is predominantly computational. However, there will still be narrative elements where candidates will be required to explain or discuss tax issues.No changes are envisaged to the “new” exam format that has come into effect as from the 2015 papers, which will remain as 15 x 2 mark multiple-choice questions, 4 x 10 mark questions and 2 x 15 mark questions in line with what ispublished in the study guide.ACCA has removed the restriction relating to the 15 additional minutes of reading time, so that while the time considered necessary to complete these exams remains at 3 hours, candidates may use the additional 15 minutes as they choose. ACCA encourages students to take time to read questions carefully and to plan answers but once the exam time has started, there are no additional restrictions as to when candidates may start writing in their answer books.Time should be taken to ensure that all the information and exam requirements are properly read and understood.Proper time management is of course essential, and candidates are advised not to spend disproportionate amounts of time on any single question. Having said that, it is my personal view as examiner that the F6 (MLA) Taxation paper is notunduly time pressured.The multiple choice questions (MCQs) should be given due attention and treated as mini-questions in their own right. They account for 30% of the overall mark and therefore typically make a key contribution to thecandidate’s overall exam success or failure.There is a useful article on the ACCA global website in relation to Multiple choice questions, which is available at the following link:/uk/en/student/exam-support-resources/fundamentals-exams-study-resources/f4/technical-articles/mcq-dec14.htmlThis gives candidates important generic information on answering multiple choicequestions (Section A of this paper), so they should be encouraged to read it.It is of course very important that candidates use up-to-date learning materials applicable to the exam session that they are preparing for.Therefore, an annual revision / update exercise to the learning materials ought to be conducted. It is important to note that although the syllabus and study guide document might indicate that there have been no updates to the syllabus, the actual content of the syllabus areas will likely be subject to changes at least to some degree e.g. new / updated tax rates and computational rules.To link back to the previous example of the new legal notice amending the Fringe Benefit Rules, the syllabus and study guide for 2018 will most likely not show any changes for 2018 in this respect (because what is examinable i.e. the application of the Fringe Benefit Rules in this case, has not itself changed) –however the learning materials must of course be updated to take into account the rules asamended.Candidates that attend courses at tuition providers certainly do have the advantage of covering the exam material from expert tutors. It is not enough, however, to participate in such a course. Self-study and regular practice are of key importance.Candidates should be reminded that, in order to maximise one’s success in the exam, study and question practice time at home are necessary and indeedindispensable.While transfers of controlling share interests have been an area of weakness in several exam sessions, a marked improvement was noted inthe last exam session (June 2017).Failing to read the requirement can result in some candidates wasting valuable time providing calculations for things the requirement specifically said to ignore (such as inflation allowance for capital gains computations). Likewise, in section B, if for example the requirement verb is “state”, candidates should just provide a very succinct answer (typically no more than one sentence) rather than wasting time by writing more, for which no marks will be awarded.Candidates should also refer to the mark allocation as an indicative guide as to how much they should write in their answer.Also for section B, some candidates fail to present organised answers with workings clearly shown. Candidates should be reminded that the answer to each question in Section B should be started on a new page, with workings properly numbered so that it is clear to which question part they relate. Also, candidates should be advised to give careful thought to the layout and organisation of their answers during the examination.Sometimes, candidates have illegible handwriting which makes theiranswers difficult to mark.Finally, this slide sets out some basic advice for those who are new to teaching F6.First of all, I would encourage tutors to make the most of the resources available on the ACCA website.You should be guided by the syllabus and study guide in particular to make sure that you are using up to date learning materials. As previously mentioned, learning materials should cover both the taught phase (namely the core knowledge) as well as the revision phase (including exam-standard questions based on past papers and guidance on exam technique). As tutors, you should also ensure that the course you are running again provides for sufficient time for candidates to learn the core knowledge as well as to practice exam-standard questions.As regards exam-standard questions, a particularly useful resource is the past exams with suggested answers and marking scheme that are available on the ACCA website. It is particularly important that you familiarise yourself with thecurrent exam format, which has been in place since the June 2015 paper.I would also advise you not to underestimate Section A of the exam, consisting of multiple choice questions, as this represents 30% of the overall mark and can make all the difference between a pass and a fail.Finally, I reiterate the point made earlier that as tutors you should reinforce the message that attending the course alone is not enough for success. Candidates need to revise at home and make time to practice exam-standard questions in order to be successful.Q&A time。

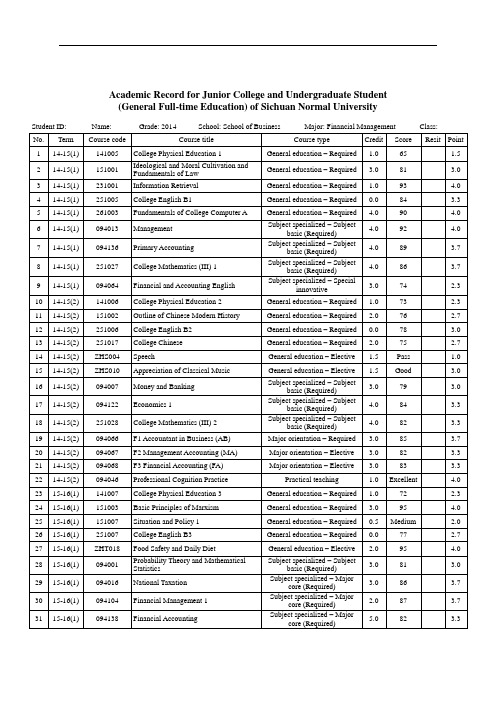

成绩单-四川师范大学-专科-商学院-竖版9列

Medium

2.0

46

16-17(1)

094023

Marketing

Subject specialized – Major core (Required)

3.0

85

3.7

47

16-17(1)

094106

Financial Markets

Subject specialized – Major core (Required)

1.0

65

1.5

2

14-15(1)

151001

Ideological and Moral Cultivation and Fundamentals of Law

General education – Required

3.0

81

3.0

3

14-15(1)

231001

Information Retrieval

3.0

16

14-15(2)

094007

Money and Banking

Subject specialized – Subject basic (Required)

3.0

79

3.0

17

14-15(2)

094122

Economics 1

Subject specialized – Subject basic (Required)

General education – Required

4.0

90

4.0

6

14-15(1)

094013

Management

Subject specialized – Subject basic (Required)

Deloitte 的提问

Deloitte 的提问1.Please prepare a short paragraph to describe why you are interested in your selected job position and what career objectives you want to achieve in Deloitte. (no more than 300 words ) 我在学习ACCA的课程中对F6税务(英国)特别感兴趣,而且在F6的考试中取得高分。

后来在课下对中国税务也做了一些了解。

而德勤在税务方面的业务做得非常成功,所以我对德勤的税务很关注,也特别有意向进德勤工作。

现在我正在学习中国的税务,在未来的工作中,我想学更多关于中国税务方面的专业知识,希望自己能在税务上有很明显的进步,而德勤在税务方面的服务很全面,能为我提供一个很好的学习平台,并且德勤的客户来自各个行业,能让我广泛涉猎各个行业的税务。

我勤奋且学习能力很棒,在工作中能很快适应各个项目并高效完成任务,为德勤创造价值。

在未来我计划在税务方面取得一番成就,努力成为3i人才,(insightful洞见,integreated融合和创新innovative).I was very interested in taxation when I was learning F6-taxation(UK) of ACCA, and I got a high marks in the F6 test. After that I also do some understanding of China tax code. Deloitte has got a great success in the tax business, so I am very interested in the tax services of Deloitte and have the intention to work for Deloitte.Now I'm learning China tax code. In the future, I want to gain knowledge in the Chinese taxation system, and hope I can learn even more. The tax services of Deloitte are very comprehensive, so this job position can provide me with a good learning platform. And Deloitte’s customers come from various industries, which will allow me to come into contact with the tax laws of various industries. I am diligent and have a great learning ability, so that I can quickly adapt to the various projects in the work and efficiently complete tasks, to create value for Deloitte. In the future I hope to make achievements in taxation and be for you a 3i talent (insightful, integrated and innovative).2.A client s CEO wants your recommendation on how to grow their business profitability. How will you prepare for this?For those of client‘s Co who have built successful businesses, they may be wondering how to take the next step and grow their business beyond its current status. There are several possibilities:1. Open another location- However,physical expansion isn't always the best growth answer without carefulresearch, planning and number-planning2. Form an alliance-Aligning themselves with a similar type of business can be a powerful way to expandquickly3. License their product-This can be an effective, low-cost growth medium, particularly if they have a serviceproduct or branded product4. Diversify-Diversifying their product or service lineDepend on the type of business they own, their available resources, and how much money, time and sweat equity they're willing to invest all over again, I’ll choose the proper one (or ones) for their business.。

ACCA16门科目简介

ACCA F阶段与P阶段共16门科目简介第一部分为基础阶段,主要分为知识课程和技能课程两个部分。

知识课程主要涉及财务会计和管理会计方面的核心知识,也为接下去进行技能阶段的详细学习打下坚实的地基。

知识课程的三个科目同时也是FIA方式注册学员所学习的FAB、FMA、FFA三个科目。

技能课程共有六门课程,广泛的涵盖了一名注册会计师所涉及的知识领域及必须掌握的技能。

知识课程FUNDAMENTALS——KNOWLEDGEF1 会计师与企业Accountant in Business (AB)F2 管理会计Management Accounting (MA)F3 财务会计Financial Accounting (FA)技能课程FUNDAMENTALS——SKILLSF4 公司法与商法Corporate and Business Law (CL)F5 业绩管理Performance Management (PM)F6 税务Taxation (TX)F7 财务报告Financial Reporting (FR)F8 审计与认证业务Audit and Assurance (AA)F9 财务管理Financial Management (FM)第二部分为专业阶段,主要分为核心课程和选修(选二)课程。

该阶段的课程相当于硕士阶段的课程难度,是对第一部分课程的引申和发展。

该阶段课程引入了作为未来的高级会计师所必须的更高级的职业技能和知识技能。

选修课程为从事高级管理咨询或顾问职业的学员,设计了解决更高级和更复杂的问题的技能。

核心课程PROFESSIONAL——ESSENTIALSP1 专业会计师Professional Accountant (PA)P2 公司报告Corporate Reporting (CR)P3 商务分析Business Analysis (BA)选修课程PROFESSIONAL——OPTIONS(四门任选二门)P4 高级财务管理Advanced Financial Management (AFM)P5 高级业绩管理Advanced Performance Management (APM)P6 高级税务Advanced Taxation (ATX)P7 高级审计与认证业务Advanced Audit and Assurance (AAA)Written by first intuition China(第一直觉教育ACCA)。

非货币性资产交换

万元旳设备,并支付25万元补价 ⑤ 以公允价值为200万元旳房产换取一台运送设

备并收取24万元补价

1.2 非货币性资产交换旳确认和计量

问题提出:怎样计量非货币性资产旳价 格?为何要计量?

1.2 非货币性资产交换旳确认和计量

1.确认和计量旳原则

(一)公允价值 应该以公允价值和应支付旳有关税费作为换 入资产旳成本,公允价值与换出资产账面价 值旳差额计入当期损益。 (二)账面价值 应该以账面价值和应支付旳有关税费作为换 入资产旳成本,不确认损益。

1.2 非货币性资产交换旳确认和计量

措• 施问旳题合提用出条:件既强然调有:两互种换可是供否选具择有旳商确业 实 能认 ?质 够、以可计及靠量换地方入计法且 量,换 。那出么资选产择旳何公种允计价量值方是法否 难点:对互换是否具有商业实质旳判 断及资产公允价值旳可靠计量。

够可靠计量:跃 •无市同场类或类似资产可比市场旳,

采用估值技术拟定公允价值

1.3 会计处理

一、以公允价值计量旳会计处理

•在换入资产基于公允价值计价旳情况下,换入资产旳入账金 额原则上应基于换出资产旳公允价值予以拟定,除非有确凿 证据表白换入资产旳公允价值比换出资产旳公允价值愈加可 靠。

(一)换入资产入账价值确实定

课堂作业:10% 课堂纪律:10%

本书主要内容

主讲内容:

非货币性资产互换 债务重组 外币折算 租赁 所得税 资产减值 企业合并 合并财务报表 分部报告与中期财务报告

第1章 非货币性资产互换

一、本章主要内容:

(1)非货币性资产互换旳认定(要 点);

(2)非货币性资产互换旳计量; (3)非货币性资产互换旳会计处理

关于ACCA的感想

关于ACCA的感想据了解,ACCA-特许公认会计师公会(The Association of Chartered Certified Accountants,简称ACCA)成 立于1904年,是目前世界上领先的专业会计师团体,也是国际上海外学员最多、学员规模发展最快的专业会计师组织。

自二十世纪三十年代起,ACCA将其专业资格考试推向海外,目前在170多个国家和地区拥有29.6万多名学员和11.5万多名会员。

ACCA的宗旨是为那些愿意在财会、金融和管理领域一展宏图的能人志士,在其职业生涯的全程提供高质量的专业机会,并推广最高的道德和管理标准,为公众利益服务。

它在全球拥有近80个代表处和服务中心(ACCA总部设在伦敦,在美国洛杉矶、加拿大多伦多、澳大利亚悉尼及中国香港建有分会,在格拉斯哥、都柏林、新德里、吉隆坡、新加坡、内罗毕、约翰内斯堡、北京、上海和广州等世界上70多个城市均设有代表处),并设有350多个考点,通过这个网络,为40多万ACCA学员和会员的职业生涯全程提供强有力的支持。

ACCA在全球于50多家组织和机构建立了会计方面的合作伙伴关系,与全球470多家注册的培训机构、近8500家ACCA认证雇主有密切的合作。

英国立法许可ACCA会员从事审计、投资顾问和破产执行的工作。

ACCA会员资格得到欧盟立法以及许多国家公司法的承认。

ACCA在欧洲会计专家协会(FEE)、亚太会计师联合会(CAPA)和加勒比特许会计师协会(ICAC)等会计组织中起着非常重要的作用。

在国际上,ACCA是国际会计准则理事会(IASB)的创始成员,也是国际会计师联合会(IFAC)的成员。

在2000年 ACCA和牛津·布鲁克斯大学(Oxford Brookes University)建立了合作关系,使学员在学习ACCA专业资格的同时,有机会获得该校应用会计的(荣誉*)理学士学位。

此项全球性的创举进一步突出了ACCA作为全球会计和培训领域领导者的地位。

必看!读了MPAcc你可以享受的免考政策!

必看!读了MPAcc你可以享受的免考政策!近年来考研越来越热,会计专硕成为考研一大热门专业,这不仅仅是因为会计专硕在培养模式上的双导师制和侧重社会实践的教学理念,还有很大程度上会计专硕(MPAcc)免考政策。

下面凯程青青老师给大家整理了MPAcc免考政策相关内容。

一、免考CPA(4门)1、CPA会计硕士修完指定科目,可直接注册入读香港会计师公会专业资格课程(QP),QP课程毕业生可获豁免中国注册会计师全国统一考试的“会计”、“审计”、“财务成本管理”和“公司战略与风险管理”四门科目。

CPA免考政策为会计专硕的包括注入极大的活力,也为会计专硕增加了无限的诱惑力,很多考生开始为此选择会计专硕。

在这里,提醒广大考生,并不是所有的学校都会拥有CPA免考的资格,同时在拥有CPA免考资格的学校中也并不是所有的都适合应届本科生,所以建议广大考生慎重选择。

Qp课程:即香港会计师公会的专业资格课程(QP),它是以自修为主的英语学习课程考试,考试内容包括财务汇报、企业财务、业务鉴证、税务共4个单元和一个期终考试。

QP学员可透过公会提供的教材吸收专业知识,并参加公会举办的工作坊,巩固专业及通识技能。

在CPA免考条件中,只有通过了该项课程,才会获得CPA的免考资格。

2、考试科目一共6门、免考4门。

考试科目:会计,审计,财务成本管理,公司战略与风险管理,经济法,税法6个科目;免考科目:会计,审计,财务成本管理,公司战略与风险管理,四门科目。

3、免考要求会计硕士修完指定科目,可直接注册入读香港会计师公会专业资格课程(QP),QP课程毕业生可获豁免中国注册会计师全国统一考试的《会计》《审计》《财务成本管理》《公司战略与风险管理》四门科目。

4、Qp课程即香港会计师公会的专业资格课程(QP),它是以自修为主的英语学习课程考试,考试内容包括财务汇报,企业财务,业务鉴证,税务共4个单元和一个期终考试。

QP学员可透过公会提供的教材吸收专业知识,并参加公会举办的工作坊,巩固专业及通识技能。

诺基亚智能手机使用指南说明书

C

Capacities Chart .................... 344, 346 Carbon Monoxide Hazard .............. 52 Carrying Cargo .............................. 202 Cassette Player

Charging System Indicator .... 58, 328 Checklist, Before Driving............. 206 Child Safety ...................................... 20 Child Seats........................................ 25

Before Driving ............................... 191 Belts, Seat ..................................... 8, 41 Beverage Holder............................ 101 Body Repair .................................... 310

Maintenance............................... 279 Usage .................................. 111, 117 Air Outlets (Vents)................ 110, 115 Air Pressure, Tires ........................ 282 Alcohol in Gasoline........................ 350 Aluminum Wheels, Cleaning........ 305 Antifreeze ....................................... 253 Anti-lock Brakes (ABS) Indicator................................ 59, 219 Operation .................................... 218 Anti-theft, Audio System............... 179 Anti-theft Steering Column Lock .. 76

ACCA F阶段知识整理

ACCA F阶段知识整理ACCA考试科目一共有13门,其中F阶段考试科目一共占了9门课程,其中的重要性不言而喻,那么F阶段和P阶段有什么关联呢?P阶段应该如何选择呢?带着这些疑问一起和高顿ACCA来看看吧。

给大家整理了一套电子版ACCA备考资料,里面有很多ACCA考试资料可供大家选择。

而且在对于上班族来说,电子版的也很适合在地铁上查阅:电子版ACCA 备考资料F1 Accountant in Business这一门倾向于管理方面,课程难度不大,很多常识性的知识点,但是毕竟是ACCA第一门考试,所以刚开始大多数同学都会对很多专业词汇的英文表述不熟悉,加上F1中的知识点比较细碎,因此加大了学习的难度。

建议大家把每章的知识点自己做一个梳理总结,每一章节整理出大框架,可以很好地帮助本科的学习。

F2 Mangement Accounting这一门课是管理会计,课体总体难度不大,差异分析的部分可能有些难度,另外一些财务比率的计算需要掌握,为以后的学习打好基础。

F3 Financial Accounting这一门课是财务会计,属于基础会计学,其中会涉及到会计科目、会计分录、丁字账、试算平衡表等等一系列会计基础知识,对于没有会计基础的同学一开始会觉得一头雾水,但是入了门之后这门课程难度并不算大。

这一门课程是之后F7和P2的学习基础,一定要掌握知识点,同时积累英语专业词汇。

F4 Corporate and Business Law英美法系和大陆体系的不同在于他们使用的是判例法,因此F4中涉及到不同年代各种法律案例,并且有很多专业词汇。

以判例法为主考试难度感觉是在上升,但是通过率在上升F5 Performance Management这门课是管理会计的进阶,对于F2基础打得好的同学拿下这门课应该不在话下。

这门课程总体难度不大,重点在于掌握不同成本法及业绩评价方法的应用。

F6 Taxation这门课90%以上都是计算,是中国考生最拿手的地方。

acca科目分类

acca科目分类ACCA科目分类ACCA(Association of Chartered Certified Accountants,特许公认会计师协会)是一家提供国际专业会计资格认证的机构。

ACCA 认证是会计和财务领域的国际金字招牌,被公认为国际上最具影响力和公信力的会计师资格之一。

ACCA考试分为基础阶段和专业阶段,基础阶段主要是财务与管理会计的基础知识,而专业阶段则涵盖了更加深入和专业的会计领域。

下面将对ACCA科目进行详细分类和介绍。

基础阶段1. F1 - Accountant in Business该科目主要涵盖了会计专业人士所需的商业理解和组织管理的基本知识。

学习者将了解组织结构、管理层决策、财务管理等方面的基础知识。

2. F2 - Management Accounting管理会计是管理层通过分析和评估各种会计数据来支持管理决策的过程。

学习者将学习成本估算、预算编制、组织绩效评估等管理会计的基本原理。

3. F3 - Financial Accounting财务会计是一门重要的会计学科,专注于公司财务报表的准备和分析。

学习者将学习资产负债表、利润表和现金流量表等财务报表的编制和解读。

4. F4 - Corporate and Business Law该课程主要涵盖商法和公司法方面的内容。

学习者将了解法律对商业和公司运营的影响,以及相关法律规定下的商业伦理问题和道德要求。

专业阶段1. Essentials Module - 必修科目F5 - Performance Management该科目主要涵盖了管理会计和业绩管理的高级概念和技术。

学习者将学习如何使用会计数据和管理信息来评估和改善组织的绩效。

F6 - Taxation税务是一个重要的财务领域,涉及到纳税义务和税务计划。

学习者将学习不同国家的税法、个人和公司的税务义务以及相应的优化措施。

F7 - Financial Reporting财务报告为公司和利益相关方提供了有效的财务信息。

acca英语词汇书

acca英语词汇书

以下是一些推荐的ACCA英语词汇书:

1. "ACCA F4 Corporate and Business Law (English): Passcards"

by BPP Learning Media

2. "ACCA F5 Performance Management: Passcards" by BPP Learning Media

3. "ACCA F6 Taxation (UK): Passcards" by BPP Learning Media

4. "ACCA F7 Financial Reporting: Passcards" by BPP Learning Media

5. "ACCA F8 Audit and Assurance: Passcards" by BPP Learning Media

6. "ACCA F9 Financial Management: Passcards" by BPP Learning Media

这些书籍由BPP Learning Media出版,专为ACCA考试编写,旨在帮助考生掌握ACCA的必备英语词汇。

每本书都包含了

大量的ACCA相关词汇和术语,并提供了示例和练习,以帮

助考生巩固所学内容。

无论您是想提升ACCA考试的英语能力,还是想扩展ACCA课程中的词汇知识,这些书籍都是不

错的选择。

请注意,这只是一些建议,您还可以在其他书店或在线市场上寻找其他ACCA英语词汇书的选择。

accatx科目考试内容

accatx科目考试内容ACCA是全球最著名的财会职业资格认证之一,因其在全球范围内的认知度和影响力而备受关注。

该认证涵盖了各种财务和会计职位所需的技能和知识,旨在提高专业人士的职业水平和市场竞争力。

ACCA的考试由14门科目组成,每门科目都涵盖了不同的领域和主题,以下是ACCA科目考试内容简介:1. F1 - Accountant in Business (AB): 认识企业和商业环境,了解商业决策和财务报告的基础知识。

2. F2 - Management Accounting (MA): 理解管理会计的基本原则和技术,能够应用它们以制定和实施管理决策。

3. F3 - Financial Accounting (FA): 掌握财务报告的基本原则和标准,能够编制和解释财务报表。

4. F4 - Corporate and Business Law (LW): 了解商业法律和法规,能够理解并应用公司法和商业合同。

5. F5 - Performance Management (PM): 能够分析和解释成本和绩效数据,并能根据结果制定和实施管理决策。

6. F6 - Taxation (TX): 理解个人和公司税务,掌握税务计算和纳税申报的基本原则。

7. F7 - Financial Reporting (FR): 掌握国际财务报告准则(IFRS),能够编制和解释复杂的财务报表。

8. F8 - Audit and Assurance (AA): 理解审计的基本原则和程序,能够评估企业的财务报表和内部控制。

9. F9 - Financial Management (FM): 能够制定和实施财务策略,并理解企业投资和融资的基本原则。

10. P1 - Governance, Risk and Ethics (GRE): 理解公司治理、风险管理和商业道德的基本原则和实践。

11. P2 - Corporate Reporting (CR): 掌握国际财务报告准则(IFRS)和企业合并的相关知识,能够编制和解释复杂的财务报表。

accaf阶段考试顺序

ACCA(特许公认会计师)考试的阶段包括三个主要的考试级别:基础阶段、应用阶段和专业阶段。

以下是一般情况下ACCA 考试阶段的顺序:1. 基础阶段(Fundamentals Level):- AB(F1)- Accountant in Business- MA(F2)- Management Accounting- FA(F3)- Financial Accounting- LW(F4)- Corporate and Business Law- PM(F5)- Performance Management- TX(F6)- Taxation- FR(F7)- Financial Reporting- AA(F8)- Audit and Assurance- FM(F9)- Financial Management2. 应用阶段(Applied Knowledge and Applied Skills):在完成基础阶段的所有九门考试后,您将获得ACCA 的知识模块证书(Knowledge Module Certificate)和技能模块证书(Skills Module Certificate)。

接下来,您可以选择应用阶段的考试顺序,选择适合自己的顺序考试。

- SBL(P1)- Strategic Business Leader- SBR(P2)- Strategic Business Reporting- APM(P3)- Advanced Performance Management- ATX(P6)- Advanced Taxation- AAA(P7)- Advanced Audit and Assurance3. 专业阶段(Strategic Professional):在完成应用阶段的所有考试后,您将获得ACCA 的技能模块证书(Skills Module Certificate)。

接下来是专业阶段的考试,其中包含两门必修考试和两门选修考试:- SBR(P2)- Strategic Business Reporting(如果在应用阶段未选择考试)- SBL(P4)- Strategic Business Leader(如果在应用阶段未选择考试)- Options Modules(从以下选项中选择两门考试):- AFM(P4)- Advanced Financial Management- APM(P5)- Advanced Performance Management- ATX(P6)- Advanced Taxation- AAA(P7)- Advanced Audit and Assurance请注意,考试的顺序并非固定的,您可以根据自己的需求和兴趣选择适合自己的考试顺序。

ACCA简介

ACCAACCA(特许公认会计师公会(The Association of Chartered Certified Accountants ,简称ACCA)成立于1904年,是目前世界上最大及最有影响力的专业会计师组织之一,也是在运作上通向国际化及发展最快的会计师专业团体。

目前已在世界上各主要国家都设立了分部、办事处及联络处。

在160多个国家共设有300多个考点,拥有学生和会员超过二十五万人。

ACCA课程全面、完善及先进兼备,现已被联合国采用作为全球会计课程的蓝本。

特许公认会计师公会简介自1990年开始,ACCA便积极参与中国会计专业人才的培训工作。

已在全国十三个城市开设了十四个考点,每年都有过千名学生参加ACCA考试。

十一个城市分别是:上海,北京,天津,武汉,大连,广州,深圳,南昌,长沙,南京,福州,成都和沈阳。

ACCA还在上海,天津,武汉,大连及广州与当地大学合作开设了培训班,赞助及辅导学生参加ACCA课程考试。

全国现有万余名学生,会员超过千人。

获取ACCA会员资格ACCA在英国、欧洲及许多主要国家为法定之会计师资格,其会员可成为执业会计师,会计师事务所合伙人。

受法律许可从事审计、税务、破产执行及投资顾问等专业会计师工作。

作为一个国际认可的专业会计师,我们的会员遍布于政府、公共机构及各行各业之领导职位如财务总监、总经理及董事等。

要成为ACCA的会员,学生必须通过ACCA十四门专业考试并获取三年财务及会计相关工作经验。

此三年相关工作经验可在考试之前、中、后累积,并且不限地域、行业、公司/机构性质等。

获取学位本科学位:根据ACCA和牛津布鲁克斯大学达成的学分互认协议,通过ACCA前9门课程后,提交一篇论文通过后,就可获得该校应用会计学本科学位。

英国牛津布鲁克斯大学是英国国立大学,在校生超过 1.7 万名。

该大学名列中国教育部承认的英国大学名单。

无论在北京还是在英国学习ACCA,都可以拿到该大学学位。

ACCA F6 Exam Tips December 2016

ACCA F6 Exam Tips December 2016ACCA F6 Taxation,这是ACCA F阶段第一次涉及到税法部分,所以大家在刚开始学的时候有点不知所措,这也是F6考试的一个难点。

关于F6的考试tips,接下来会给大家主要列举一些F6的考试重点,希望大家在考前关注一下。

1.Remember to learn your income tax and corporation tax proformas.2.Calculations which require no more than two or three entries into your calculator can be included on the face of your proformas(eg.Grossing up dividends/interest).Calculations which are more complex(pany car benefits)need separate workings which are properly referenced(W1,W2 etc and with a heading).3.Actually attempt the narrative parts of the requirement–aim for as many sentences as there are marks with each sentence containing something technical.Keep your paragraphs to no more than 3 sentences long(4 at an absolute maximum).4.In both numerical and narrative answers leave plenty of space on the page.So in proformas–leave a gap between each line(you will definitely need to add something in).In narrative answers leave a line or two between each paragraph just in case you remember something later.Well-spaced answers are also easier to mark–and you ALWAYS WANT TO KEEP YOUR MARKER HAPPY.We know that the two longest questions will focus on income tax and corporation tax.This is likely to include the following.·Employment benefits·Property income·Relief for pension contributionsAdjustments to profit to arrive at trading income for both companies and sole traders–in past sitting we have seen a number of questions whereby you have to correct errors in computations included in the scenarioCapital allowance computationsIt is also likely that section C will include a ten mark question on VAT,inheritance tax or capital gains tax.So remember to cover the whole syllabus in the practice and revision kit.Finally,remember the pass mark is 50%you don’t need to be perfect.If you don’t know something have a guess and move on.Sometimes you have to do that in order to get follow through marks in section C questions.If you make a mistake but then have to use that incorrect figure later on in a subsequent calculation then that’s fine you can only lose the mark once.In section A and B never leave an OT unanswered,have a guess if need be.大家要记住这些tips,祝大家考试顺利。