Chapter3 Accounting Equation and Illustration

Accounting Equation

/accounting/fin/equation/

2010-11-26

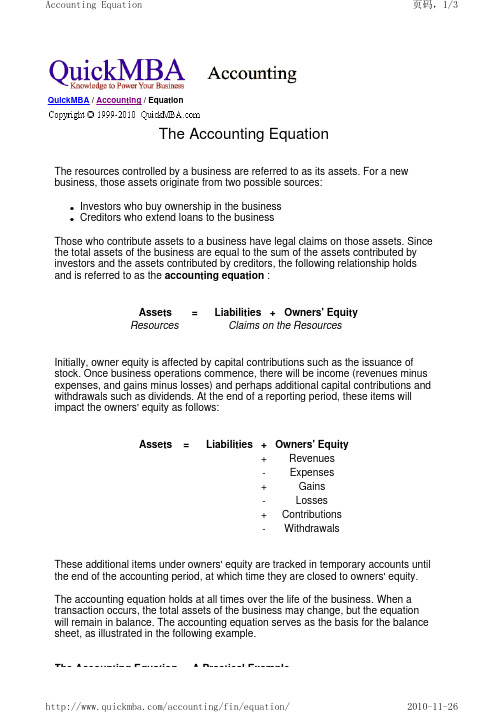

Accounting Equation

Assets = Liabilities + Owners' Equity

Resources

Claims on the Resources

Initially, owner equity is affected by capital contributions such as the issuance of stock. Once business operations commence, there will be income (revenues minus expenses, and gains minus losses) and perhaps additional capital contributions and withdrawals such as dividends. At the end of a reporting period, these items will impact the owners' equity as follows:

Accounting Equation

页码,1/3

QuickMBA / Accounting / Equation

The Accounting Equation

The resources controlled by a business are referred to as its assets. For a new business, those assets originate from two possible sources:

unit 3会计英语

maintain v. 保持,维持

【例】The increase in sales is being maintained. 【搭配】maintain quality/standard 保持质量/标准

Exercises

• Ⅱ. Finish the crossword puzzle with the help of the clues below:

Task 1 & 2

3. Newtech Co. Ltd sells a software and receives a check from the customer for $400 for the service provided. Analysis: The assets are and the owner's equity is .

经济业务对会计要素的影响,可以归纳为4大类: (1)资产增加,负债、所有着权益增加; (2)资产减少,负债、所有者权益减少; (3)一个资产项目减少,另一个资产项目增加; (4)一个负债、所有者权益项目减少,另一个负债、所有者权 益项目增加。 每一种业务都不会改变会计恒等式的成立。

Any increase in the amount of total assets is necessarily accompanied by an equal increase on the other side of the equation, that is, by an increase in either the liabilities or owner’s equity.

Task 1 & 2

3. Newtech Co. Ltd sells a software and receives a check from the customer for $400 for the service provided. Analysis: The assets are increased and the owner's equity is increased.

会计学原理双语142AccountingPrinciplesSYLLABUS

Jiangxi University of Finance and EconomicsSchool of International Trade and Economics SYLLABUSCourse Title: Principles of AccountingCourse Code: 02016Semester: 142Class No.: AE1Credits: 6Teaching Hours: 64Class Times: Tuesday 8:00am-9:40am, Friday 10:20am-12:00pm Prerequisites: NoneLecturer's InformationName: Dr. Ling JiangEmail : ljiang@Course Description and ObjectivesThis is an introductory financial accounting course. In today's economy, basic accountingknowledge is useful to students of various disciplines, especially those who are in the businessfield. This course is an opportunity of gaining an understanding of the many details ofoperation of a business entity from a financial information perspective. The focus is on thepreparation of corporate financial statements and interpreting the information by simple analyses.It is a prerequisite to more advanced accounting and business courses.Learning OutcomesUpon completion of the course, a student should achieve the following learning outcomes:Understand the operation of the accounting cycle.Understand how to account for business transactions.Understand how to prepare financial statements.Understand how to analyze a business entity's financial condition and operating results by usingfinancial statement information.Develop accounting-related critical thinking, problem solving, and ethical reasoning skills.1Teaching MethodsTeaching methods include formal lecture, group work, individual exercise, and class discussion.AssessmentFinal Examination 50%20% Mid-Term Examination10% Test 110% Test 210% Homework assignments, attendance, and class participation100%TotalTo obtain a passing grade, a student should achieve at least 60% in total.Tests and ExaminationsTests and Examinations will be held when the related learning content has been completed. Test1 covers chapters 1-4, Mid-Term Exam covers chapter 1-7, Test2 covers chapters 8-11, and theFinal Exam will focus on chapters 8-14, plus limited coverage on chapters 1-7. Homework, Attendance, and Class ParticipationIn-class exercises are opportunities to put chapter knowledge to practice. These can includegroup work, individual exercises, and case discussions. Homework problems are assigned toprovide additional exercises.Your InputYou will be expected to:Participate actively in group work, individual exercises, and class discussions. Complete homework assignments, and submit printed copies when they are due. Review textbook chapters, PowerPoint slides, and other study materials.Course outlineChapter 1 Accounting in BusinessChapter 2 Analyzing and Recording Transactions2Chapter 3 Adjusting Accounts and Preparing Financial StatementsChapter 4 Completing the Accounting CycleChapter 5 Accounting for Merchandising OperationsChapter 6 Inventories and Cost of SalesChapter 7 Accounting Information SystemChapter 8 Cash and Internal ControlsChapter 9 Accounting for ReceivablesChapter 10 Plant Assets, Natural Resources, and IntangiblesChapter 11 Current Liabilities and Payroll AccountingChapter 12 Long-Term LiabilitiesChapter 13 Investments and International OperationsChapter 14 Accounting for CorporationsTextbookJohn J. Wild, Ken W. Shaw, and Barbara Chiappetta, “Fundamental Accounting Principles,”21stedition, revised by Xuegang Cui and Qing Rao, English language reprint edition, McGraw-HillEducation (Asia) Co. and China Renmin University Press, 2013.Tentative Schedule34。

BASICACCOUNTINGEQUATION(Chapter2and3)…

Order of Preparation Date1. Income statement Period (e.g., year, quarter, month) ended date2. Statement of retained earnings Period (e.g., year, quarter, month) ended date3. Balance sheet As at end of period date4. Statement of cash flows Period (e.g., year, quarter, month) ended date Income Statement (perpetual inventory system)NameIncome StatementPeriod Ended DateSales revenuesSales$ XLess: Sales returns and allowances XNet sales$ X Cost of goods sold X Gross profit X Operating expensesSelling expenses(Examples: store salaries, advertising, delivery)$ X Administrative expenses(Examples: rent, amortization, utilities, insurance)X X Income from operations X Other revenues and gains(Examples: interest, gains)$ XOther expenses and losses(Examples: interest, losses)X X Net income$ X Income Statement (periodic inventory system)NameIncome StatementPeriod Ended DateSales revenuesSales$ XLess: Sales returns and allowances XNet sales$ X Cost of goods soldBeginning inventory$ XPurchases$ XLess: Purchase returns and allowances XNet purchases XAdd: Freight in XCost of goods purchased XCost of goods available for sale XLess: Ending inventory X Cost of goods sold X Gross profit X Operating expensesSelling expenses(Examples: store salaries, advertising, delivery)$ XAdministrative expenses(Examples: rent, amortization, utilities, insurance)X X Income from operations X Other revenues and gains(Examples: interest, gains)$ XOther expenses and losses(Examples: interest, losses)X X Net income X Statement of Retained EarningsNameStatement of Retained EarningsPeriod Ended DateRetained earnings, beginning of period$ X Add:Net income (or deduct net loss)XX Deduct: Dividends X Retained earnings, end of period$ X Balance SheetNameBalance SheetAs At DateAssetsCurrent assets(Examples: cash, temporary investments, accountsreceivable, merchandise inventory, prepaids)$ X Capital assets(Examples: property, plant, and equipment,natural resources, intangible assets)$ XLess: Accumulated amortization X X Total assets$ X Long-term investments(Examples: investment in bonds, investment in stock)X Liabilities and Shareholders’ EquityLiabilitiesCurrent liabilities(Examples: notes payable, accounts payable, accruals,unearned revenues, current portion of notes payable)$X Long-term liabilities(Examples: notes payable, bonds payable)X Total liabilities X Shareholders’ EquityShare capital X Retained earnings X Total liabilities and shareholders’ equity$ XNote:The equity section of the balance sheet would be presented as partners’ equity in a partnership and owner’s equity in aproprietorship.Statement of Cash FlowsNameStatement of Cash FlowsPeriod Ended DateCash flows from operating activitiesNote: May be prepared using the direct or indirect methodCash provided (used) by operating activities$ X Cash flows from investing activities(Examples: purchase / sale of long-term assets)Cash provided (used) by investing activities X Cash flows from financing activities(Examples: issue / repayment of long-term liabilities,issue or redemption of shares, payment of dividends)Cash provided (used) by financing activities X Net increase (decrease) in cash X Cash, beginning of period X Cash, end of period$ XSTOP AND CHECK:Statement of Retained Earnings – net income (loss) must equal net income (loss) presented on Income Statement.Balance Sheet – ending retained earnings must equal ending retained earnings presented on Statement of Retained Earnings; total assets must equal total liabilities and shareholders’ equity.Statement of Cash Flows: Cash, end of period must equal cash pre-sented on the Balance Sheet.REPORTSCONCEPTUAL FRAMEWORK OF ACCOUNTING (Chapter 1,2,4,6,7)CharacteristicsAssumptionsPrinciples ConstraintsUnderstandability (1)Going concern (7)Revenue recognition (4)Cost-benefit (1)Relevance (1)Monetary unit (6)Matching (2,4)Materiality (1)Reliability (1)Entity (1)Full disclosure (1)Comparability (1)Cost (4)SHAREHOLDERS’ EQUITY (Chapter 11)Comparison of Equity AccountsNo Par Value vs. Par Value Shares Journal EntriesDIVIDENDS (Chapter 11)Comparison of Dividend EffectsDebits and Credits to Retained EarningsPresentation of Non-Typical ItemsBONDS (Chapter 10)Computation of Annual Bond Interest ExpenseInterest expense 5Interest paid (payable) 1amortization of discount (OR 2amortization of premium)STATEMENT OF CASH FLOWS (Chapter 5)Cash flows from operating activities (indirect method)Net income Add: Decreases in current assets $ XIncreases in current liabilities X Amortization X Losses on disposals of assets XDeduct:Increases in current assets ( X)Decreases in current liabilities ( X)Gains on disposals of assets ( X)Cash provided (used) by operating activities$ XCash flows from operating activities (direct method)Cash receipts(Examples: from sales of goods and services to customers, from receipts of interest and dividends on loans and investments)$ XCash payments(Examples: to suppliers, for operating expenses, for interest, for taxes) ( X)Cash provided (used) by operating activities$ XACCOUNTING CYCLE (Chapter 3)Proprietorship Partnership CorporationOwner’s equityPartners’ equityShareholders’ equityName, CapitalName, Capital Capital stockName, CapitalRetained earningsNo Par Value Par ValueCashCashCommon sharesCommon shares (par value)Contributed capital in excess of par valueCashCommon SharesRetained EarningsCash Dividend No effectStock Dividend No effect Stock SplitNo effectNo effectNo effectRetained EarningsDebits (Decreases)Credits (Increases) loss. income.2.Cash dividends.3.Stock dividends.Discontinued operationsIncome statement (presented separately after income from continuing operations)Extraordinary itemsIncome statement (presented separately after income before extraordinary items)Premium Market Interest Rate < Contractual Interest Rate Face Value Market Interest Rate 5Contractual Interest Rate DiscountMarket Interest Rate > Contractual Interest RateStraight-line amortizationBond discount (premium)Number of interest periodsEffective-interest amortization Bond interest expense 2Bond interest paid (preferred method)Carrying value of bonds Face amount of bonds X at beginning of period x contractual interest ratemarket interest rate↑↓↓↓7Adjusted trial balance4Postings6Adjusting Entries3Journal entries2Transactions analysis1Transactions or eventsCHART OF ACCOUNTS 9Closing Entries8Preparation of financial statements5Trial BalanceOPENING BALANCESUSING THE INFORMATION IN THE FINANCIAL STATEMENTS(Chapter 12 and throughout the book)Ratio Formula Purpose or Use Performance Ratios1.Return on Assets (ROA)Income before interest Measures overall profitability of assets.Average total assetsOrNet income + [Interest expense x (1 – tax rate)]Average total assetsOrNet income + [interest expense x (1 – tax rate)] x Sales revenueSales revenue Average total assetsOrprofit margin ratio x total asset turnover2.Return on Equity (ROE)Net income – preferred dividends Measures profitability of shareholders’ investment.Average shareholders’ equityTurnover Ratios3.Accounts Receivable Turnover Sales on account Measures liquidity of receivables.Average accounts receivableDays to Collect365 days Measures number of days receivables outstanding.Accounts receivable turnover4.Inventory Turnover Cost of goods sold Measures liquidity of inventory.Average InventoryDays Inventory Held365 days Measures number of days stock is on hand.Inventory turnover5.Accounts Payable Turnover Credit Purchases Measures how many times old accounts are paid and newAverage accounts payable accounts incurred.Days to Pay Cost of goods soldAverage accounts payableShort-Term Liquidity Ratios6.Current Ratio Current assets Measures short-term debt paying ability.Current liabilitiesQuick Ratio Current assets – inventories – prepaid expenses Measures immediate short-term liquidity.Current liabilitiesLong-Term Liquidity Ratios7.Debt/Equity (I)Total liabilities Measures the proportion of financing that comes from debt.Total liabilities + Shareholders’ equityDebt/Equity (II)Total liabilities Measures debt as a percentage of capital.Total shareholders’ equityDebt/Equity (III)Total long-term liabilities Measures long-term liabilities as a percentage of long-term financing.Total long-term liabilities + shareholders’ equity8.Times Interest Earned Income before income taxes and interest expenseInterest expenseEarnings per Share Ratios9.Earnings per Share Net income – preferred dividends Measures net income earned on each share of common stock.Weighted average number of common shares10.Price-Earnings Ratio Market price per share of stock Measures ratio of the market price per share to earnings per share.Earnings per share。

会计学原理英文版

会计学原理英文版Accounting PrinciplesIntroductionAccounting principles refer to the fundamental concepts and guidelines that underpin the field of accounting. These principles provide a framework for recording, reporting, and analyzing financial transactions and information. They help ensure consistency and comparability in financial statements, enabling stakeholders to make informed decisions.The Accounting EquationAt the core of accounting principles is the accounting equation, which states that assets equal liabilities plus owner's equity. This equation forms the basis for maintaining balance in financial records. It expresses the relationship between resources owned by the business (assets), the sources of funding for those resources (liabilities), and the owners' claims to those resources (equity).Double-Entry SystemThe double-entry system is another key accounting principle. It requires that every transaction be recorded with equal debits and credits in the accounting records. This system ensures that the accounting equation remains in balance and enables the detection and correction of errors.Revenue RecognitionRevenue recognition is an important accounting principle used to determine when and how to recognize revenue. According to this principle, revenue should be recognized when it is both earned and realizable. This means that revenue is recognized when the company has fulfilled its obligations to provide goods or services and can reasonably expect to receive payment.Expense RecognitionExpense recognition, also known as matching principle, requires that expenses be recorded in the same period as the related revenues. This principle ensures that expenses are matched with the revenues they help generate, providing a more accurate depiction of the financial performance of a business.ConservatismThe principle of conservatism guides accountants to be cautious and to err on the side of understating rather than overstating assets and revenues. This principle helps prevent overvaluing assets and inflating financial results, promoting transparency and reliability. MaterialityThe materiality principle suggests that financial information should be reported if its omission or misstatement could influence the economic decisions of users. This principle recognizes that not all information is equally significant and allows for the omission of immaterial details to avoid unnecessary clutter in financialstatements.Going ConcernThe going concern principle assumes that a business will continue to operate indefinitely unless there is evidence to the contrary. This principle allows accountants to prepare financial statements under the assumption that the company will continue its operations in the foreseeable future, except when liquidation or cessation of operations is imminent.ConclusionAccounting principles provide a foundation for accurate and reliable financial reporting. By adhering to these principles, accountants ensure consistency, comparability, and transparency in financial statements, enabling stakeholders to evaluate a company's financial position and make informed decisions. Understanding and applying these principles is essential for anyone involved in the field of accounting.。

Chap_3_Small_Business_Accounting

13-2

e s b

Why Accounting Matters

Proves what your business did financially

Shows how much your business is worth

Banks, creditors, development agencies, and investors

13-11

e s b

Financial Reports

Five common financial statements: Income statement Statement of retained earnings Statement of owner’s equity Balance sheet Cash flow statement

CHAPTER

3

Small Business Accounting:

Projecting and Evaluating Performance

Objectives

Review the basic concepts of accounting Understand the requirements for a

13-5

Basic Concepts to determine accounting procedures

Business entity concept: a business has an existence separate from that of its owners. Going concern: business is expected to continue in existence for the foreseeable future

Accounting Equation and Accounting Circle

Exercises

4. Posting reclassifies the data from the journal’s chronological format to an account classification format in the ledger, which is a collection of the formal accounts.

v. 推迟,延期

14. liquidation [;lɪkwɪ'deɪʃn] n. 破产,清偿

15. residual [rɪ'zɪdjʊəl]

a. 剩余的

16. accumulate [ə'kjuːmjʊleɪt] v. 积聚,累积

Section Accounting Equation and Accounting Circle

· · ·

Complete the dialogue according to the Chinese hints·

1 会计等式是理解复式记账系统的基础。

_________________________________________________________产 解决债务 应付票据 应付账款 应计费用 应付债券 租赁债务

Section Accounting Equation and Accounting Circle

9

Part 2 Intensive Reading

Accounting Elements and Accounting Equation

————————————————————————————————————

Section Accounting Equation and Accounting Circle

会计平衡等式的英文作文

会计平衡等式的英文作文The Accounting Equation。

The accounting equation is a fundamental concept in the field of accounting. It is used to represent therelationship between a company's assets, liabilities, and equity. The equation is as follows:Assets = Liabilities + Equity。

This equation is also known as the balance sheet equation because it is used to create the balance sheet, which is a financial statement that shows a company's assets, liabilities, and equity at a specific point in time.Assets are the resources that a company owns that have value and can be used to generate revenue. Examples of assets include cash, inventory, property, and equipment.Liabilities are the obligations that a company owes toothers. Examples of liabilities include loans, accounts payable, and taxes owed.Equity is the residual interest in the assets of a company after deducting liabilities. Equity represents the ownership interest of the owners of the company. Examples of equity include common stock, retained earnings, and dividends.The accounting equation must always balance. This means that the total value of a company's assets must equal the sum of its liabilities and equity. If the equation does not balance, it indicates that there is an error in the company's financial records.The accounting equation is used in every aspect of accounting, from recording transactions to creating financial statements. It is a fundamental concept that every accountant must understand in order to properly record and report a company's financial information.In conclusion, the accounting equation is a fundamentalconcept in accounting that represents the relationship between a company's assets, liabilities, and equity. It is used to create the balance sheet and must always balance. Understanding the accounting equation is essential for anyone working in the field of accounting.。

会计等式英文作文

会计等式英文作文Accounting equation is a fundamental concept in accounting. It states that the assets of a business are equal to the liabilities plus the owner's equity. This equation must always be in balance, which means that the total value of assets must always equal the total value of liabilities and owner's equity.Assets are the resources that a business owns, such as cash, inventory, equipment, and property. These are the things that the business uses to generate revenue and operate the business.Liabilities are the debts and obligations of a business, such as loans, accounts payable, and other debts. These are the amounts that the business owes to others.Owner's equity represents the owner's investment in the business, as well as any profits that have been retained in the business. It is the residual interest in the assets ofthe business after deducting liabilities.The accounting equation is the foundation of double-entry accounting, which is the system used by most businesses to record their financial transactions. In double-entry accounting, every transaction affects at least two accounts, with the total debits always equaling the total credits.The accounting equation is a key tool for understanding the financial position of a business. By using this equation, businesses can ensure that their financial records are accurate and complete. It also helps in analyzing the financial health of a business and making informed decisions about its operations. In conclusion, the accounting equation is a crucial concept in accounting that helps businesses keep track of their financial position and make sound financial decisions.。

3 Accounting Equation

Capital

_

Owner’s Withdrawals

Withdrawals

+

Revenues

_ Expenses

Expenses

Revenues

Debit Credit

-

Debit Credit

+

Debit Credit

Debit Credit

+

+

-

-

+

-

Normal Balances

+

N o rm a l

-

-

Ⅱ. Business transactions

Business transactions ------- economic events directly change an entity’s financial condition or directly affect its results of operations. Result: All business transactions can be stated in terms of changes in the elements of the accounting equation.

2 On Nov.5, Exchange $20000 cash for land. Dr. Land $20000 Cr. Cash $20000

3 On Nov.7, If A had purchased a van for $28000, paying $8000 cash and signing a loan agreement for $20000. Dr. Van $28000 Cr. Cash $8000 Notes payable

(高职)商务英语(上海东海第三章会计与财务报表

实用商务英语导读教案

2020/2/12

1

Chapter 3 Accounting & Financial Statements

❖3.1 Accounting—the Language of Business ❖3.2 Basic Elements of Financial Position and

2020/2/12

3

3.1 Accounting—the Language of Business

❖ Relationship of Accounting to Other Fields: ✓ Finance ✓ Production ✓ Marketing ✓ Personnel ✓ General management

Click to edit company slogan .

23

the Accounting Equation ❖3.3 Generally Accepted Accounting Principles ❖3.4 Double-Entry System ❖3.5 Financial Statements

2020/2/12

2

Hale Waihona Puke 3.1 Accounting—the Language of Business

cash flows; and ④ the effects of cash and non-cash transactions on

the entity’s financial position.

3.5 Financial Statements

3.5 Financial Statements

Accounting Equation

Accounting EquationThe accounting system reflects two basic aspects of a company: what it owns and what it owes. Assets are resources with future benefits that are owned or controlled by a company. Examples are cash, supplies, equipment, and land. The claims on a company’s assets---what it owes---are separated into owner and no owner claims. Liabilities are what a company owes equity its no owners (creditors) in future payments, products, or services. Equity (also called owner’s equity or capital) refers to the claims of its owner(s). Together, liabilities and equity are the source of funds to acquire assets. The relation of assets, liabilities, and equity is reflected in the following accounting equation:Assets= Liabilities + Equity会计制度反映一个公司的两个基本方面:它所拥有的资产,所欠的债务。

资产是公司所拥有或控制的资源与未来的收益。

例如现金,物资,设备,土地等。

国外主流教材会计学章节安排供参考

Weygandt, Kieso, Kimmel: Accounting Principles, 9th Edition Chapter 1: Accounting in Action.Feature Story: Knowing the Numbers.What Is Accounting?The Building Blocks of Accounting.The Basic Accounting Equation.Using the Basic Accounting Equation.Financial Statements.All About You: Ethics: Managing Personal Financial Reporting.Appendix: Accounting Career Opportunities.Chapter 2: The Recording Process.Feature Story: Accidents Happen.The Account.Steps in the Recording Process.The Recording Process Illustrated.The Trial Balance.All About You: Your Personal Annual Report.Chapter 3: Adjusting the Accounts.Feature Story: What Was Your Profit?Timing Issues.The Basics of Adjusting Entries.The Adjusted Trial Balance and Financial Statements.Appendix: Alternative Treatment of Prepaid Expenses and Unearned Revenues.Chapter 4: Completing the Accounting Cycle.Feature Story: Everyone Likes to Win.Using a Worksheet.Closing the Books.Summary of the Accounting Cycle.The Classified Balance Sheet.All About You: Your Personal Balance Sheet.Appendix: Reversing Entries.Chapter 5: Accounting for Merchandising Operations.Feature Story:Who Doesn’t Shop at Wal-Mart?Merchandising Operations.Recording Purchases of Merchandise.Recording Sales of Merchandise.Completing the Accounting Cycle.Forms of Financial Statements.Appendix 5A: Periodic Inventory System.Appendix 5B: Worksheet for a Merchandiser.Chapter 6: Inventories.Feature Story: Where Is That Spare Bulldozer Blade?Classifying Inventory.Determining Inventory Quantities.Inventory Costing.Inventory Errors.Statement Presentation and Analysis.All About You: Employee Theft—An Inside Job.Appendix 6A: Inventory Cost Flow Methods in Perpetual Inventory Systems. Appendix 6B: Estimating Inventories.Chapter 7: Accounting Information Systems.Feature Story: QuickBooks® Helps This Retailer Sell Guitars.Basic Concepts of Accounting Information Systems.Subsidiary Ledgers.Special Journals.Chapter 8: Fraud, Internal Control, and Cash.Feature Story: Minding the Money in Moose Jaw.Fraud and Internal Control.Cash Controls.Control Features: Use of a Bank.Reporting Cash.All About You: Protecting Yourself from Identity Theft.Chapter 9: Accounting for Receivables.Feature Story: A Dose of Careful Management Keeps Receivables Healthy. Types of Receivables.Accounts Receivable.Notes Receivable.Statement Presentation and Analysis.All About You: Should You Be Carrying Plastic?Chapter 10: Plant Assets, Natural Resources, and Intangible Assets. Feature Story: How Much for a Ride to the Beach?Section 1: Plant Assets.Determining the Cost of Plant Assets.Depreciation.Expenditures During Useful Life.Plant Assets Disposals.Section 2: Natural Resources.Section 3: Intangible Assets.Accounting for Intangible Assets.Research and Development Costs.Statement Presentation and Analysis.All About You: Buying a Wreck of Your Own.Appendix: Exchange of Plant Assets.Chapter 11: Current Liabilities and Payroll Accounting.Feature Story: Financing His Dreams.Accounting for Current Liabilities.Contingent Liabilities.Payroll Accounting.All About You: Your Boss Wants to Know If You Jogged Today.Appendix: Additional Fringe Benefits.Chapter 12: Accounting for Partnerships.Feature Story: From Trials to Top Ten.Partnership Form of Organization.Basic Partnership Accounting.Liquidation of a Partnership.Appendix: Admission and Withdrawal of Partners.Chapter 13: Corporations: Organization and Capital Stock Transactions. Feature Story: "Have You Driven a Ford Lately?"The Corporate Form of Organization.Accounting for Issues of Common Stock.Accounting for Treasury Stock.Preferred Stock.Statement Presentation.Chapter 14: Corporations: Dividends, Retained Earnings, and Income Reporting. Feature Story: Owning a Piece of the Action.Dividends.Retained Earnings.Statement Presentation and Analysis.All About You: Corporations Have Governance Structures—Do You?Chapter 15: Long-Term Liabilities.Feature Story: Thanks Goodness for Bankruptcy.Bond Basics.Accounting for Bond Issues.Accounting for Bond Retirements.Accounting for Other Long-Term Liabilities.Statement Presentation and Analysis.Appendix 15A: Present Value Concepts Related to Bond Pricing.Appendix 15B: Effective-Interest Method of Bond Amortization.Appendix 15C: Straight-Line Amortization.Chapter 16: Investments.Feature Story: "Is There Anything Else We Can Buy?"Why Corporations Invest.Accounting for Debt Investments.Accounting for Stock Investments.Valuing and Reporting Investments.Chapter 17: Statement of Cash Flows.Feature Story: Got Cash?The Statement of Cash Flows: Usefulness and Format.Preparing the Statement of Cash Flows—Indirect Method.Using Cash Flows to Evaluate a Company.All About You: Where Does the Money Go?Appendix 17A: Using a Work Sheet to Prepare the Statement of Cash Flows—Indirect Method. Appendix 17B: Statement of Cash Flows—Direct Method.Chapter 18: Financial Statement Analysis. Feature Story: It Pays to Be Patient.Basics of Financial Statement Analysis. Horizontal Analysis.Vertical Analysis.Ratio Analysis.Earning Power and Irregular Items.Quality of Earnings.Chapter 19: Managerial Accounting.Feature Story: What a Difference a Day Makes. Managerial Accounting Basics.Managerial Cost Concepts.Manufacturing Costs in Financial Statements. Managerial Accounting Today.All About You: Outsourcing and Jobs.Chapter 20: Job Order Costing.Feature Story:"…And We’d Like It in Red". Cost Accounting Systems.Job Order Cost Flow.Reporting Job Cost Data.Under- or Over applied Manufacturing Overhead. All About You: Minding Your Own Business.Chapter 21: Process Costing.Feature Story: Ben & Jerry’s Tracks Its Mix-Ups. The Nature of Process Cost Systems. Equivalent Units.Comprehensive Example of Process Costing.Contemporary Developments.Appendix: Example of Traditional Costing versus Activity-Based Costing.Chapter 22: Cost-Volume-Profit.Feature Story: Growing by Leaps and Leotards.Cost Behavior Analysis.Cost-Volume-Profit Analysis.All About You: A Hybrid Dilemma.Appendix: Variable Costing.Chapter 23: Budgetary Planning.Feature Story: The Next ? Not Quite.Budgeting Basics.Preparing the Operating Budgets.Preparing the Financial Budgets.Budgeting in Non-Manufacturing Companies.All About You: Avoiding Personal Financial Disaster.Chapter 24: Budgetary Control and Responsibility Accounting. Feature Story: Trying to Avoid an Electric Shock.The Concept of Budgetary Control.Static Budget Reports.Flexible Budgets.The Concept of Responsibility Accounting.Types of Responsibility Centers.Chapter 25: Standard Costs and Balanced Scorecard.Feature Story: Highlighting Performance Efficiency.The Need for Standards.Setting Standard Costs—A Difficult Task.Analyzing and Reporting Variances from Standards.Balanced Scorecard.Appendix 25A: Standard Cost Accounting System.Appendix 25B: A Closer Look at Overhead Variances.Chapter 26: Incremental Analysis and Capital Budgeting.Feature Story: Soup Is Good Food.Section 1: Incremental Analysis.Management’s Decision-Making Process.Types of Incremental Analysis.Section 2: Capital Budgeting.Evaluation Process.Annual Rate of Return.Cash Payback.Discounted Cash Flow.All About You: What Is a Degree Worth?Appendix A: Specimen Financial Statements: PepsiCo, Inc.Appendix B: Specimen Financial Statements: The Coca-Cola Company. Appendix C: Time Value of Money.Appendix D: Using Financial Calculators.Appendix E: Standards of Ethical Conduct for Management Accountants.Accounting, 3rd EditionPaul D. Kimmel, University of Wisconsin, MilwaukeeJerry J. Weygandt, University of Wisconsin, MadisonDonald E. Kieso, Northern Illinois UniversityISBN: 978-0-470-37785-7 ©20091. Introduction to Financial Statements.Forms of Business Organization 4Users and Uses of Financial Information.Business Activities.Communicating with Users.A Quick Look at Tootsie Roll’s Financial Statements.2. A Further Look at Financial Statements.The Classified Balance Sheet.Using the Financial Statements.Financial Reporting Concepts.3. The Accounting Information System.The Accounting Information System.Accounting Transactions.The Account.Steps in the Recording Process.The Recording Process Illustrated.The Trial Balance.4. Accrual Accounting Concepts.Timing Issues.The Basics of Adjusting Entries.The Adjusted Trial Balance and FinancialStatements.Closing the Books.Quality of Earnings.Appendix. Adjusting Entries in an Automat.5. Merchandising Operations and the Multiple-Step Income Statement. Merchandising Operations.Recording Purchases of Merchandise.Recording Sales of Merchandise.Income Statement Presentation.Evaluating Profitability.Appendix. Periodic Inventory System.6. Reporting and Analyzing Inventory.Classifying Inventory 276Determining Inventory Quantities.Inventory Costing.Analysis of Inventory.Appendix 6A. Inventory Cost Flow Methods in Perpetual Inventory Systems. Appendix 6B. Inventory Errors.7. Internal Control and Cash.Fraud and Internal Control.Cash Controls.Control Features: Use of a Bank.Reporting Cash.Managing and Monitoring Cash.Appendix. Operation of the Petty Cash Fund.8. Reporting and Analyzing Receivables.Types of Receivables.Accounts Receivable.Financial Statement Presentationof Receivables.Managing Receivables.Notes Receivable.9. Reporting and Analyzing Long-Lived Assets.Section One. Plant Assets.Determining the Cost of Plant Assets.Accounting for Plant Assets.Analyzing Plant Assets.Section Two. Intangible Assets.Accounting for Intangible Assets.Types of Intangible Assets.Financial Statement Presentation of Long-Lived Assets. Appendix. Calculation of Depreciation Using Other Methods.10. Reporting and Analyzing Liabilities.Reporting and Analyzing Liabilities.Current Liabilities.Bonds: Long-Term Liabilities.Accounting for Bond Issues.Accounting for Bond Retirements.Financial Statement Presentation and Analysis.Appendix 10A. Straight-Line.Appendix 10B. Effective-Interest.Appendix 10C. Accounting for Long-Term.Notes Payable.11. Reporting and Analyzing Stockholders' Equity.The Corporate Form of Organization.Stock Issue Considerations.Accounting for Treasury Stock.Preferred Stock.Retained Earnings.Financial Statement Presentation of Stockholders’ Equity. Measuring Corporate Performance.Appendix. Entries for Stock Dividends.12. Statement of Cash Flows.The Statement of Cash Flows: Usefulness and Format. Preparation of the Statement of Cash Flows—Indirect Method. Using Cash Flows to Evaluate a Company.Appendix. Statement of Cash Flows—Direct Method.13. Performance Measurement.Sustainable Income.Comparative Analysis.Ratio Analysis.Quality of Earnings.Appendix. Comprehensive Illustration of Ratio Analysis. 14. Managerial Accounting.Managerial Accounting Basics.Managerial Cost Concepts.Manufacturing Costs in Financial Statements.Managerial Accounting Today.Appendix. Accounting Cycle for a Manufacturing Company.15. Job Order Costing.Cost Accounting Systems.Job Order Cost Flow.Reporting Job Cost Data.16. Process Costing.The Nature of Process Cost Systems.Equivalent Units.Comprehensive Example of Process Costing.Costing Systems—Final Comments.Appendix. FIFO Method.17. Activity-Based Costing.Traditional Costing and Activity-Based Costing. Example of Traditional Costing versus ABC.Activity-Based Costing: A Closer Look.Activity-Based Costing in Service Industries. Appendix. Just-in-Time Processing.18. Cost-Volume-Profit.Cost Behavior Analysis.Cost-Volume-Profit Analysis.19. Variable Costing: A Decision-Making Perspective. Cost-Volume-Profit (CVP) Review.Sales Mix.Cost Structure and Operating Leverage.20. Budgetary Planning.Budgeting Basics.Preparing the Operating Budgets.Preparing the Financial Budgets.Budgeting in Nonmanufacturing Companies.21. Budgetary Control and Responsibility Accounting.The Concept of Budgetary Control.Static Budget Reports.Flexible Budgets.The Concept of Responsibility Accounting.Types of Responsibility Centers.Appendix. Residual Income—Another Performance Measurement.22. Standard Costs and Balanced Scorecard.The Need for Standards.Setting Standard Costs—A Difficult Task.Analyzing and Reporting Variances from Standards.Balanced Scorecard.Appendix 22A. The Standard Cost Accounting System.Appendix 22B. A Closer Look at Overhead Variance.23. Incremental Analysis and Capital Budgeting.Section one. Incremental Analysis.Management’s Decision-Making Process.Appendix A: Specimen FinancialStatements: Tootsie Roll Industries, Inc. Appendix B: Specimen Financial Statements: Hershey Foods Corporation. Appendix C: Time Value of Money.Appendix D: Payroll Accounting.Appendix E: Subsidiary Ledgers & Special Journals.Appendix F: Accounting for Sole Proprietorships.Appendix G: Accounting for Partnerships.Appendix H: Reporting and Analyzing Investments.Photo credits.Company index.Subject index.MP Fundamental Accounting Principles (1-25) and Circuit City Annual Report, 18th EditionJohn J Wild, UNIV OF WISC MADISONKermit D. Larson, UNIV OF TEXAS AT AUSTINBarbara Chiappetta, NASSAU COMMUNITY COLLEGEHardcover with softcover (unboxed)©2007, ISBN-13 9780073271101MHID 00732711011. Accounting in Business2. Analyzing and Recording Transactions3. Adjusting Accounts and Preparing Financial Statements4. Completing the Accounting Cycle5. Accounting for Merchandising Operations6. Inventories and Cost of Sales7. Accounting Information Systems8. Cash and Internal Controls9. Accounting for Receivables10. Plant Assets, Natural Resources, and Intangibles11. Current Liabilities and Payroll Accounting12. Accounting for Partnerships13. Accounting for Corporations14. Long-Term Liabilities15. Investments and International Operations16. Reporting the Statement of Cash Flows17. Analysis of Financial Statements18. Managerial Accounting Concepts and Principles19. Job Order Cost Accounting20. Process Cost Accounting21. Cost Allocation and Performance Measurement22. Cost-Volume-Profit Analysis23. Master Budgets and Planning24. Flexible Budgets and Standard Costs25. Capital Budgeting and Managerial DecisionsFinancial & Managerial Accounting, 15th EditionJan Williams, UNIV OF TENNESSEE-KNOXVILLESue Haka, MICHIGAN STA TE U-EAST LANSINGMark S Bettner, BUCKNELL UNIVERSITYJoseph V Carcello, University of Tennessee---KnoxvilleHardcover, 1264 pages©2010, ISBN-13 9780073526997MHID 0073526991Chapter 1: Accounting: Information for Decision MakingChapter 2: Basic Financial StatementsChapter 3: The Accounting Cycle: Capturing Economic EventsChapter 4: The Accounting Cycle: Accruals and DeferralsChapter 5: The Accounting Cycle: Reporting Financial ResultsChapter 6: Merchandising ActivitiesChapter 7: Financial AssetsChapter 8: Inventories and the Cost of Goods SoldChapter 9: Plant and Intangible AssetsChapter 10: LiabilitiesChapter 11: Stockholders' Equity: Paid-in CapitalChapter 12: Income and Changes in Retained EarningsChapter 13: Statement of Cash FlowsChapter 14: Financial Statement AnalysisChapter 15: Global Business and AccountingChapter 16: Management Accounting: A Business PartnerChapter 17: Job Order Cost Systems and Overhead AllocationsChapter 18: Process CostingChapter 19: Costing and the Value ChainChapter 20: Cost-Volume-Profit AnalysisChapter 21: Incremental AnalysisChapter 22: Responsibility Accounting and Transfer PricingChapter 23: Operational BudgetingChapter 24: Standard Cost SystemsChapter 25: Rewarding Business Performance Comprehensive Problem 6: Utease Corporation Chapter 26: Capital BudgetingPrinciples of Accounting w/Annual Report, 1st EditionRobert Libby, CORNELL UNIVERSITY-ITHACAPatricia Libby, ITHACA COLLEGEFred Phillips, University of SaskatchewanStacey M Whitecotton, ARIZONA STA TE UNIV-TEMPEHardcover©2009, ISBN-13 9780077251031MHID 00772510321 Accounting and Starting a Business2 Establishing a Business and the Balance Sheet3 Operating a Business and the Income Statement4 Completing the Accounting Cycle5 Accounting Systems6 Merchandising Operations7 Inventories8 Internal Control and Cash9 Receivables10 Long-lived Tangible and Intangible Assets11 Current Liabilities and Payroll12 Partnerships13 Accounting for Corporations14 Long-term Liabilities15 Accounting for Investments16 Reporting and Interpreting Statement of Cash Flows17 Financial Statement Analysis18 Managerial Accounting19 Job Order Costing20 Process Costing and Activity Based Costing21 Cost Behavior and Cost-Volume-Profit Analysis22 Incremental Analysis and Capital Budgeting23 Budgeting and Planning24 Budgetary Control25 Decentralized Performance Evaluation。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1 Liabilities from past transactions or events. 2 Liability as a present obligation of the enterprise. 3 The settlement of liabilities is expected to lead to an outflow of economic benefits.

性质不同。负债是在经营或其他事项中发生的债 务,是债权人对其债务的权利;所有者权益是对 投入的资本及其运用所产生的盈余(或亏损)的 权利。

Differences in Owners' equity and Liabilities

3 Different repayments. Corporate Liabilities usually have agreed repayment date; Owner's equity does not exist agreed repayment date, which is an enterprise fund long-term used can only be repaid until liquidation.

1 Liabilities from past transactions or events.

负债是由过去的交易或事项形成的。 负债应当由企业过去的交易或者事项所形成。换 句话说。只有过去的交易或者事项才形成负债。 企业将在未来发生的承诺、签订的合同等交易或 者事项,不形成负债。

2 Liability as a present obligation of the enterprise

Definition of Liabilities

Liabilities as present obligations of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits. Characters:

负债是企业承担的现时义务。 负债必须是企业承担的现时义务。现时义务是指 企业在现行条件下已承担的义务:未来发生的交 易或者事项形成的义务,不属于现时义务,不应 当确认为负债。

3 The settlement of liabilities is expected to lead to an outflow of economic benefits. 负债的清偿预期会导致经济利益流出企业。 预期会导致经济利益流出企业也是负债的一个本 质特征只有企业在履行义务时会导致经济利益流 出企业的,才符合负债的定义,如果不会导致企 业经济利益流出的,就不符合负债的定义。在履 行现时义务清偿负债时,导致经济利益流出企业 的形式多种多样,例如用现金偿还或以实物资产 形式偿还;以提供劳务形式偿还;部分转移资产、 部分提供劳务形式偿还等。

Definition of Assets

Assets as resources controlled by the enterprise as a result of past events and from which economic benefits are expected to flow to the enterprise. Characters:

对象不同。负债是对债权人负担的经济责任;所 有者权益是对投资人负担的经济责任。

Differences in Owners' equity and Liabilities

2 Different characters. Liabilities are debt incurred in the operations or other matters, which is the right of creditors to its debt; owner's equity is the right of earnings (or losses) on invested capital arising from its use.

Differences in Owners' equity and Liabilities

1 Different objects. Liabilities shoulder the economic responsibility for creditors.Owner's equity shoulders the economic responsibility for investors.

Long-term assets

are those which should be realized or consumed after more than 12 months or longer than an accounting cycle such as prepaid expenses, land, buildings, equipment and so on.

实质重于形式以融资租赁的形式租入的固定资产,虽然从法律

形式来讲企业并不拥有其所有权,但是由于租赁合同中规定的租赁期 相当长,接近于该资产的使用寿命;租赁期结束时承租企业有优先购 买的选择权,在租赁期内承租企业有权支配资产并从中受益。所以, 从实质上看,企业控制了该项资产的使用权及受益权。所以在算会计 核算上,将融资租赁的固定资产视为企业的资产。

Liabilities

Current liabilities

are those amounts which are repayable within a period of less than 12 months or within an accounting cycle such as notes payable, accounts payable and so on .

Classification

Assets

Current assets

are those amounts which are realized or consumed within a period of less than 12 months or within an accounting cycle such as cash, inventory, notes receivable, accounts receviable and so on .

For Example

Goods or Services bought on credit

Borrowed Money

Liabilities

Salaries and wages owed to employees

Taxes owed to the Government

Classification

2 Assets are the economic resources owned or controlled by a business.

资产必须由企业拥有或控制。 由企业拥有或者控制,是指企业享有某项资产的所有权, 或者虽然不享有某项资产的所有权,但该资源能被企业所 控制。例如,融资租入的固定资产,按照实质重于形式的 要求,也应将其作为企业资产予以确认。

3 Assets can benefit future operations for the business.

资产预期会给企业带来经济利益。 预期会给企业带来经济利益,是指直接或间接导致现金和 现金等价物流入企业的潜力。资产必须具有交换价值和使 用价值。没有交换价值和使用价值、不能给企业带来未来 经济利益的资源不能确认为企业的资产。 例如,待处理财产损失或已失效、已毁损的存货,他们已 经不能给企业带来未来经济利益,就不应该再作为资产出 现在资产负债表中。

Chapter 3

Accounting Equation and illustration

Lecturer : Grade 11 Accounting CHEN Ling

Contents

1

2 Accounting Equation Assets

3

4 5

Liabilities

Owner’s Equity The Expand Accounting Equation

Text

Long-term liabilities

are those which should be repaid after more than 12 months or longer than an accounting cycle such as bonds payable, mortgages payable and so on.

6

Illustrative Transaction

Accounting Equation

Economic resources ↙ ↘ Owner Creditor ↘ ↙ Equities ↓↓(Accounting Equation) Assets Economic resources =Equities ↑ (Liabilities) ↖ ↓↓ Economic resources =Creditors’ equity + Owner’s equity ↓↓ Assets=Liabilities + Owner’s equity

Text

Definition of Owner’s Equity

Owner’s equity refers to the claims by the owner on the net assets of the business such as paidup capital (or equity) and retained earnings and so on. Owner’s equity=Assets - Liabilities