英文版财经新闻

国外频道原版英文播放

1、 E-TALK 26、DW TV

2、 ABS-CBN 27、TV 5 亚洲

3、 NBN 4 28、Studio 23

4、 ABC 5 29、ABC 亚太

5、 GMA 7 30、JCTV

6、 RPN 9 31、TBN

7、 EWTN 32、Net 25

8、 IBC 13 33、彭勃财经亚洲频道

9、民视 34、21世纪电影台

10、卡拉OK 35、Dream 电影1

11、索尼动作影视娱乐频道(AXN) 36、LIVING ASIA

12、CINEMAX亚洲频道 37、4UTV

13、福克斯新闻 38、Nickelodeon 菲律宾

14、家庭影院亚洲频道(HBO) 39、娱乐体育节目网亚洲频道(ESPN)

15、卫视电影台 40、卫视体育台

16、卫视国际电影台 41、贺曼娱乐电视网电影台

17、TCM 42、国家地理亚洲频道

18、日本广播协会收费娱乐电视频道 43、Adventure 1

19、Cartoon Network 44、ETC

20、迪斯尼频道 45、美国有线电视新闻网亚洲 (cNN)

21、Pinoy Box Office 46、ANIMAX动画频道

22、卫视合家欢台 47、Sports Plus体育频道

23、MTV 菲律宾 48、Soho Features

24、全国广播公司亚太财经频道(CNBC) 49、Dream 电影2

25、英国广播公司世界频道。

财经报道的特点

财经报道的特点财经报道主要汇集新华社视频记者的财经类报道,播报国内外最新财经新闻资讯,分析社会关注的财经热点话题,包括股市、汇市、油市、粮市、车市、房市等。

接下来小编为大家整理了财经报道的特点,希望对你有帮助哦!一、英文财经报道的特点——遣词造句英文财经报道属于一种专业性的新闻报道,因此,其语言运用的最大特征就是专业名词和专业术语多,而且许多常用词被赋予特殊的含义,例如: long(多头)、 short(空头)、 rally(价格回稳)、call(看涨)、put(看跌)等等。

如果不了解这些词在专业上的含义,就可能无法真正彻底读懂有关的报道和消息。

另一方面英文财经报道为了体现新颖、通俗,也经常用一些外来语、俗俚语、口语表达形式以及比较生动、灵活的小词,例如:"President Clinton said he is 'confident' Congress will approve …even as the plan continue to draw heavy fire from Republicans and Democrats on Capitol Hill."(这里的" to draw heavy fire"是俗语,意为"招致猛烈抨击"。

)"At the same time, Ortiz threw cold water on the idea advanced by several U.S. lawmakers…"("throw co ld water"意为"泼冷水",也是通俗的表达方式。

) "The weak dollar … has hammered the earnings of the big exporters at the heart of Japan's economy."( "hammer"原本指"用锤子钉…",是一个很形象的小词,这里转意为"严重影响"。

运用功能语法分析英文财经新闻报道特征

I ii m h d h p d f r a l v n h h u e c e . r d u a o e o n e e e t — o r r s u r

除 了 以上 这 种 直 接 引 述 外 ,英 文 财 经报 道 的 正 文 中还 有 更多的 间接 引述 。这类引述通常 以一些 常用的表达法引导 , 如 :“ a ”( ) e p e s 表 示 ) t l ”( s y 说 ,“ x r s ”( ,“ e l 告诉 ) , a cr i gt … ”( c o d n o 根据 …)等等 。所有这些 引述都 旨在体 现报道 的客观性 和真 实性 。 综 上 所 述 ,除 需 具 备 一 定 的 专 业 知 识 外 , 我 们 还 应 该 对 英 文财 经报道 的语言运用 规律和篇章特 征有所 认识,只有这 样 ,才 能 发 挥 财 经 济 报 道 传 递 信 息 的主 要 功 能 , 才 能 及 时 了 解 、准 确 掌 握 英 文 经 济 报 道 的信 息 内容 。

【 摘 要 】英文财经新闻报道从个别字词的选用到全篇 内容的 陈述都体现 了新 闻报道惯有的及时、客观、新颖的特点。文 章从专业需求 出发 ,全面介绍 了经济报 道在词汇及语篇两方面所表现 出的独有特征。

【 键 词 】财 经 新 闻 ;词 汇 特 点 ;语 篇 特 点 关 【 中图分类号 】G 1 . 2 22 【 文献标识码】A

Y h o!B y c m e a . E t a e a d o h r p o n n ao u.o.by r d n t e r mi e t s t s w r a al z d f r h u s a i e l s e k w e i e e ep r y e o o r tat m a tw e h n h c e v r o d d t e i h a e t a f c a k r o e l a e h m w t f k r f i .

财经类有用网址

尔街日报中文版/gb/index.asp路透中文网/marketwatch即时资讯/story/newsviewer一新浪财经/如果英文不太好没法阅读marketwatch的朋友,国内我认为新浪财经的美股和外汇频道都很不错。

彭博资讯英文版/shibor利率/shibor/web/html/index.html美国国债收益率/resource-center/data-chart-center/interest-ra tes/Pages/TextView.aspx?data=yield(二)查询股票详细信息上交所上市公司公告/sseportal/ps/zhs/ggts/ssgsggqw_full.shtml深交所上市公司公告/m/drgg.htmGoogle财经/finance纽交所和纳斯达克股票即时走势MSN money /纽交所和纳斯达克股票财务数据晨星公司/纽交所和纳斯达克股票数据纽交所/about/listed/lc_ny_overview.html可以按照国别或者行业或者规模查找公司雅虎财经/intlindices?e=americas全球主要指数走势(三)有价值的博客李驰新浪博客/lichi深圳市同威投资创始人,价值投资者,博文大约每月两篇朱平新浪博客/zhuping广发基金投资总监,博文每月一篇陶冬新浪博客/taodong瑞士信贷董事总经理、亚洲区首席经济分析师,每周一篇对全球市场的简评刘军洛新浪博客/liujunluo老刘应该不用介绍了,我甚至认为他的人气比上面三位要高段永平网易博客/老段也是价值投资者啊海宁的马甲新浪博客/hainingdemajia海宁的经济学功底很扎实如松新浪博客/msqygz对气候很有研究哈克新浪博客/guanmisheng数据和图形很丰富俞非和讯博客/。

[《环球时报》英文版经营管理初探]环球时报英文版

![[《环球时报》英文版经营管理初探]环球时报英文版](https://img.taocdn.com/s3/m/746da9ca482fb4daa48d4b25.png)

《[《环球时报》英文版经营管理初探]环球时报英文版》摘要:2009年4月20日《环球时报》英文版(报头为英文的Global Times)正式创刊,这是继1981年China Daily诞生后20多年来又一份全国性的大型综合性英文日报,《环球时报》中文版的日常版面设置为:头版、新闻背景、环球扫描、关注中国、深度报道・记者调查、军事、异国风情、台湾传真、国际论坛、娱乐与体育、漫画与文摘、环球财经、要闻等,《环球时报》英文版的联动市场竞争战略摘要:《环球时报》英文版逆全球金融危机之流、在报业不景气的大背景下创刊已近一年。

英文版《环球时报》不仅帮助报社实现了跨越式发展,还为中国开辟了新的国际舆论阵地。

在过去的半年里,报纸新生的喜悦伴随着成长期的阵痛,而其引入的英文报纸新发展模式也值得我们从媒介经营管理的角度进行分析和探索。

关键词:《环球时报》英文版经营管理2009年4月20日《环球时报》英文版(报头为英文的Global Times)正式创刊,这是继1981年China Daily诞生后20多年来又一份全国性的大型综合性英文日报。

与China Daily不同的是,英文版Global Times以中文《环球时报》为母体和依托,两者共享一个报名和报纸品牌(不同的仅是语言的差异),从而形成了国内“一报两刊”的新发展模式。

《环球时报》英文版创刊的媒介经营管理背景老牌西方媒体的操作经验认为,做媒体就是三部曲:第一,要有很深的口袋(即大的投资);第二,需要有一支很强的采编团队;第三,要有很先进的市场意识。

①这些经验对于《环球时报》英文版这样一份新兴的报纸而言,其重要性显然不言自明。

然而我们也应该看到,雄厚的资金是获取精英人才的基础,如果没有资金作为保障,高质量的采编团队和先进的市场意识也就无从谈起。

鉴于英文报纸的特殊性及其对采编人员更高的要求,《环球时报》英文版在创刊筹备之初就“面向全球招聘英才”:执行主编、执行副主编各1名;编辑部主管3名;英语新闻记者、编辑60名;外籍专家10名;并宣称“提供具有竞争力的薪酬待遇”。

《环球时报》中文版和英文版特色比较

类 英 浯报 纸 《环 球 时 报 》英 文 版 和 中 文 版 本 I州源 . 保持 一 致 的 传 播 L]径 , 部 是 代 表 一fII玉l就 际 问 题 向 世 发 声 自英 文 版 创 刊 以 来 , 《环 球 时 报 》形 成 了 ,Is、英 文 版 和 环 球 M 并 存 的 “三位 一 体 ” “网 报 结 合 ” 的发 展格 局

块 没 汁 、语 言 Jx【格 、排 版特 色 四 个 际 时政 类报 刊 ,从 刨 ru之 H起就 具 重 , “海 外 商 机 ”板 块 为他 fI、J 找

方 面 分 析 了 《环 球 时 报 》 ll_l、英 文 有党 媒性 质 ,针 对 I~精 英阶 层和 中 海 外投 资 机 会 提 供 1I,参 考 ; cfI文 版

些 不 的 传 播 策 略 ? 呈 现 哪 些 不 同 的 一 个基 本 出发 点 币¨. 牌特 色 差异 的 阶 层 男 性 读 者 的 渎 喜 好 豁 】:·I-

的 传 播 内 容 ? 笔 者 从 受 众 群 体 、板 根 源 l}1文 版 是 《人 K H报 》 旗 F的 文 版 受 众 巾 商 务 人 1二。 fH 1比

球 时 报 》 l}I、英 文版 的 板

英 文 版 受 众 青 年 人 。 大 多

从 表 1可 以 看 出 , }I文版 的受 众 块 没 汁和 大 部 分 综 合 类 报 纸 卡H似 , 数 ,这 决 定 了 英 文 版 娱 乐 干¨体 育 板

群体 数量 远远 大 f英文版 ,受众 年 龄 都 没 有 要 闻 、评 论 、lJj寸经 、体 育 、 块 总 共 有n版之 多 英文 版 的 lJj寸经

版的 差 异化

产 阶 层 ,受 众群 体 晓夫 ;而 蜒文版 则 受 众 }t, 14)岁 以 卜男 性 中 年 人 I 比

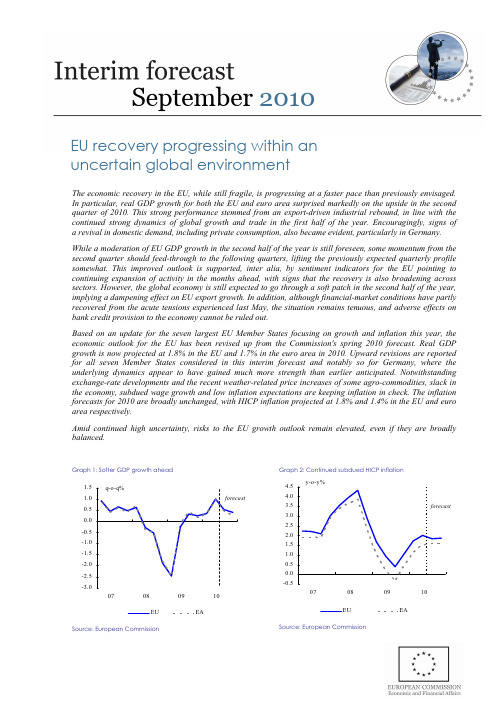

2010-09-13欧元区经济预测 英文版

[suggested new layout using the text of IF Sep 09]September 2010EU recovery progressing within an uncertain global environmentThe economic recovery in the EU, while still fragile, is progressing at a faster pace than previously envisaged. In particular, real GDP growth for both the EU and euro area surprised markedly on the upside in the second quarter of 2010. This strong performance stemmed from an export-driven industrial rebound, in line with the continued strong dynamics of global growth and trade in the first half of the year. Encouragingly, signs of a revival in domestic demand, including private consumption, also became evident, particularly in Germany. While a moderation of EU GDP growth in the second half of the year is still foreseen, some momentum from the second quarter should feed-through to the following quarters, lifting the previously expected quarterly profile somewhat. This improved outlook is supported, inter alia, by sentiment indicators for the EU pointing to continuing expansion of activity in the months ahead, with signs that the recovery is also broadening across sectors. However, the global economy is still expected to go through a soft patch in the second half of the year, implying a dampening effect on EU export growth. In addition, although financial-market conditions have partly recovered from the acute tensions experienced last May, the situation remains tenuous, and adverse effects on bank credit provision to the economy cannot be ruled out.Based on an update for the seven largest EU Member States focusing on growth and inflation this year, the economic outlook for the EU has been revised up from the Commission's spring 2010 forecast. Real GDP growth is now projected at 1.8% in the EU and 1.7% in the euro area in 2010. Upward revisions are reported for all seven Member States considered in this interim forecast and notably so for Germany, where the underlying dynamics appear to have gained much more strength than earlier anticipated. Notwithstanding exchange-rate developments and the recent weather-related price increases of some agro-commodities, slack in the economy, subdued wage growth and low inflation expectations are keeping inflation in check. The inflation forecasts for 2010 are broadly unchanged, with HICP inflation projected at 1.8% and 1.4% in the EU and euro area respectively.Amid continued high uncertainty, risks to the EU growth outlook remain elevated, even if they are broadly balanced.Graph 1: Softer GDP growth aheadSource: European CommissionGraph 2: Continued subdued HICP inflationSource: European Commission2Interim forecast September 2010Global recovery loosing momentumThe world economy recovered by more than expected in the first half of 2010, led by strong growth in emerging market economies, particularly in Asia. World trade also performed strongly, with trade in goods returning to pre-recession levels by mid-year. Despite some loss of momentum in the second quarter, annual growth in global trade (excl. EU) is now expected to average around 12% in 2010 in volume terms, up from about 10% in the spring forecast.Looking ahead, the global economy is set to moderate somewhat in the second half of 2010, although a 'double-dip' seems unlikely. This follows from the expected weaker support from inventory building going forward and the phasing out of stimulus measures. Leading indicators, such as the global Purchasing Managers' Index (PMI) for manufacturing, though remaining in expansion territory, have declined in recent months, suggesting that the global manufacturing cycle has peaked in the second quarter. Despite the expected soft patch, global GDP (excl. EU) is projected to grow by some 5% in 2010, up by ¼ pp. compared to the spring forecast.Graph 3: Softening global growth and trade-15-10-55100001020304050607080910113035404550556065World trade, CPB (ma3, LHS)Global PMI - manufacturing output (ma3, RHS)Source: CPB - Netherlands Bureau for Economic Policy Analysis, European CommissionThe global recovery is still expected to be uneven and is surrounded by major uncertainties. On the one hand, growth in emerging economies remainsrobust, supported by the rebound in global trade, commodity price developments and solid domestic demand. On the other hand, the recovery is still fragile in several advanced economies. While investment in equipment should continue to benefit with some lag from the increase in global demand, consumption remains constrained in these economies. Moreover, the resurfacing of global imbalances, high debt levels and lingering tensions in sovereign-debt markets are also weighing on the outlook.Financial markets affected by a retreat from riskOver the last few months, financial markets have partly recovered from the sovereign-debt crisis, though significant challenges remain in place. With concerns about the strength of the economic recovery increasing in some parts of the world, a retreat from risk has become a key determinant of financial-market developments.While sovereign-bond spreads in most European countries have narrowed somewhat since May 2010, they are still significantly above the levels seen at the beginning of the year. More recently, benchmark sovereign-bond yields have fallen to historic lows in the EU, with spreads vis-à-vis German bunds widening again in some Member States. Similarly, corporate-bond spreads have narrowed since May, but also remain substantially above their levels of early 2010. New bond issuance has resumed on the back of mostly better-than-expected corporate results. With concerns about sovereign debt receding, markets' attention has shifted from banks' solvency positions to banks' refinancing risk.Bank credit provision to the economy has come into focus over the past months. So far lending growth to households has remained very moderate in the euro area and the UK, whereas bank credit to non-financial corporations continued to shrink over the summer. The latest ECB survey provides evidence of renewed tightening of bank credit standards, at least for enterprises. The reported factors behind this are renewed constraints in banks' access to funding and liquidity management, owing to tensions in sovereign-debt markets. These developments suggest that support from the credit side to the economic recovery could materialise somewhat later than envisaged in the spring.3Interim forecast September 2010Improved prospects for the EU economyThe recovery of the EU economy gained ground in the second quarter of 2010. GDP growth picked up sharply, by 1.0% q-o-q in both regions, after growth of just 0.3% in the first quarter. This outcome was above the consensus estimate (which was 0.6% for the euro area) and the Commission's spring forecast (0.4%).While exports continued to support the recovery, expanding by a sizeable 4%, the second quarter also saw a rebalancing of growth towards domestic demand. Indeed, the contribution of private investment and consumption to GDP growth (0.6 pp. in the EU and euro area) exceeded the combined contributions of inventories and net exports (0.3 pp.). As expected in the spring, the second quarter figure also partly reflects temporary factors, such as a technical rebound in construction activity following the harsh winter.Graph 4: A rebalancing of EU growth across demandcomponents-2.5-2.0-1.5-1.0-0.50.00.51.01.507Q108Q109Q110Q1Inventories Net exportsDomestic demand (excl. inventories)GDP (q-o-q%)Source: European CommissionLooking ahead, GDP growth is set to moderate in the second half of the year. This stems from the expected softening in the global economy, along with the fading of the temporary factors that kick-started the recovery.Based on an update of the outlook for the seven largest Member States, GDP is now expected to expand by 0.5% in the EU and euro area in the third quarter, and by 0.4% and 0.3% respectively in the fourth. This represents a slight upward revisioncompared to the quarterly profile presented in the spring forecast, on account of some spill-over of the momentum from the second quarter.High-frequency indicators support the improved outlook for the EU economy. For instance, the Commission's Economic Sentiment Indicator (ESI) has recovered from the adverse impact of tensions in financial and sovereign-bond markets in May-June, to currently stand above its long-term average. Similarly, the composite PMI remains firmly in the zone that indicates expansion, despite a slight easing in August. As for sectoral patterns, the broad-based nature of the latest survey readings is also encouraging. It suggests that the expected spill-over from the export-led industrial rebound to the rest of the economy is gradually materialising.Graph 5: Brighter prospects for EU equipment investment-12-10-8-6-4-20240001020304050607080910-7-6-5-4-3-2-1012Equipment investment (LHS)Industrial confidence (ma3, RHS)*ma3=3 months moving averageSource: European CommissionFurther support to the view that the recovery is broadening can be found in data that are closely correlated with developments in private investment and consumption. For example, the degree of capacity utilisation is approaching a level (just above 80) which traditionally implies expanding equipment investment in the euro area. At the same time, the profit situation of firms has improved. On the consumption side, while disposable income remains weak, the decline in the household saving rate from its peak during the crisis, subdued inflation and stabilising labour-market conditions bode well for consumer spending in the near term.4Interim forecast September 2010Graph 6: Private consumption expanding again in the euroarea-0,9-0,6-0,30,00,30,60,91,21,51,80001020304050607080910121314151617Private consumption (LHS)Source: European CommissionGrowth forecast for the EU economy revised upFor 2010 as a whole, GDP growth is now forecast at 1.8% in the EU and 1.7% in the euro area. This represents a sizeable upward revision compared to the spring forecast (1.0% for the EU and 0.9% for the euro area), reflecting a higher carry-over from the first half of the year and the elements discussed above. However, this aggregate picture masks uneven developments across Member States, confirming the Commission's expectation of a multi-speed recovery within the EU. This is not surprising given differences in the scale of adjustment challenges and ongoing rebalancing within the EU and euro area.Inflation in the EU to remain moderateConsumer price inflation increased moderately in the first half of 2010. This upward trend reflected an increase in global commodity prices, as well as the impact of upward base effects from the food and energy components.Euro-area headline HICP inflation rose to 1.5% in the second quarter of 2010, in line with the spring forecast. Core inflation (i.e. HICP inflation excluding energy and unprocessed food) appears to have bottomed out at 0.8% in the same period, decreasing from 1.5% one year earlier. In the EU, headline inflation was 2.0% in the second quarter, 0.3 pp. higher than in the spring forecast, largely due to a surprise in the UK.Weak labour-market conditions kept wage growth subdued in the euro area in the first quarter of 2010. At the same time, annual unit-labour-cost growth was negative, reflecting improving productivity and only modest growth in compensation per employee.Looking ahead, the headline inflation rate for 2010 is expected to hold at 1.8% in the EU, while in the euro area it is marginally revised down to 1.4% (-0.1 pp. compared to the spring forecast). However, within the euro area, projected developments are somewhat divergent, with France being the only Member State with an upward revision, following increases in administered prices. Outside the euro area, inflation has been revised up, in particular in the UK on account of a stronger-than-expected pass-through to the headline inflation rate from exchange-rate and commodity-price developments, as well as due to changes in indirect taxation.Graph 7: EU underlying inflation remains subdued1.01.21.41.61.82.02.22.42.62.83.000010203040506070809106.57.07.58.08.59.09.510.0Core inflation (HICP excl. energy and unproc. food, LHS)Unemployment rate (RHS)y-o-y%% of labour force (inverted scale)Source: European CommissionDespite revisions at the Member State level, the underlying inflation trends identified in the spring forecast remain valid. The remaining slack in the economy and weak labour market conditions are expected to keep core inflation at historically low levels, while the headline rate may prove to be volatile in the second half of 2010, driven both by changes in commodity prices related to the outlook in advanced economies and base effects.Interim forecast September 2010Brighter growth outlook bodes well for the labour market and public financesIn keeping with the usual pattern – whereby labour- market developments follow those of GDP with a time lag of half a year or more – the labour-market situation has started to stabilise in recent months. The first quarter of 2010 saw job shedding ease to 0.2% q-o-q in the EU (from some 0.8% a year earlier) and come to an end in the euro area. Similarly, the unemployment rate has held steady since the spring, at 9.6% in the EU and 10.0% in the euro area.As for the outlook, survey indicators of firms' employment expectations point to moderate job creation going forward, as does the PMI employment index which crossed the 50-mark in May. Taken together with the strong upward revision to economic growth in 2010, it seems that the labour market may hold up somewhat better this year than expected at the time of the spring forecast. Nonetheless, conditions are set to remain weak, reflecting, inter alia, the partial unwinding of support measures and ongoing structural adjustment across sectors and firms. At Member State level, a continuation of the divergence observed to date in labour-market performance is also expected. Turning to public finances, additional consolidation measures taken since the publication of the spring forecast and the better-than-expected growth outlook will help improve the 2010 budgetary position in the EU and euro area.A full assessment of prospects for public finances and the labour market will be carried out in the Commission's upcoming autumn forecast.High uncertainty, but broadly balanced risks Uncertainty at the current juncture is high, with non-negligible risks to the EU growth outlook clearly evident. While these risks go in both directions, they appear broadly balanced for 2010. On the upside, the impetus from the export-led industrial rebound to private consumption could prove stronger than assumed in the baseline, as was the case in the first half of the year. The broad-based improvement in sentiment indicators of late bodes well for a similar outcome in the period ahead. Moreover, in so far as the labour market continues to surprise on the upside – as it has done for some time now – the feed-through to private consumption could be even more pronounced. The materialisation of these risks would add to the self-sustainability of the EU recovery. Likewise, the spill-over to be expected from the pick-up in activity in Germany to other Member States may materialise to a greater extent than expected at present, further strengthening the recovery.On the downside, softening global demand in the second part of 2010 – beyond that allowed for in the baseline – poses a risk for EU export growth. Second, the still relatively fragile financial-market situation remains a concern. While markets have recovered somewhat from the recent crisis, renewed turbulence in sovereign-debt markets could trigger further increases in funding costs and additional credit tightening, with adverse consequences for confidence and economic activity. A third downside risk relates to the fiscal consolidation underway in a number of Member States. This should help dissipate market concerns about fiscal sustainability, but may weigh more on domestic demand in the short term than currently envisaged. Regarding the inflation outlook, risks also appear to be broadly balanced for 2010. While strengthening activity and a weaker than previously assumed euro represent upside risks, weak labour-market conditions, as well as low inflation expectations, suggest that these pressures are likely to be offset in the near term.5Interim forecast September 2010Growth and inflation prospects in the seven largest Member States1. Germany – strong recovery becoming more broad-basedThe German economy has rebounded vigorously from the crisis, posting five consecutive quarters of robust growth since the second quarter of 2009. Despite the harsh weather conditions around the turn of 2009-10, the underlying growth momentum remained largely intact and turned out considerably stronger than projected in the Commission's spring forecast. A brisk rebound in world trade and expansionary monetary and fiscal policy were the main driving forces behind this turnaround. The initially largely export-driven recovery is increasingly becoming more broad-based with domestic demand contributing more strongly to growth in the second quarter than net exports.In the second quarter of 2010 real GDP growth culminated at over 2%, the highest quarterly rate since reunification. A particularly sharp increase in exports and a surge in construction activity – reflecting a rebound after the impact of severe winter weather and the kicking-in of public infrastructure projects as part of the fiscal stimulus – contributed to this exceptionally brisk pace. The weaker economic outlook for the US and a possible moderation of growth in Asia are likely to imply a softening of the export dynamics in the second half of the year. However, domestic demand components are set to gather further strength and to sustain a relatively lively recovery. The robust labour market which, despite the scope of the downturn, was barely affected should boost household confidence. Thus, private consumption will continue to be buoyed by falling unemployment, stronger wage growth as working hours are being extended again, still moderate inflation and fiscal relief measures. Rising capacity utilisation, low interest rates and the strong financial position of the corporate sector should support private investment activity, which will additionally be boosted by the expiry of favourable depreciation rules at the end of the year. Hence, despite some slowdown in the quarterly growth rates, real GDP is projected to grow by close to 3½% in 2010. Despite higher energy prices and a depreciation of the euro, HICP inflation has remained contained so far and is expected to accelerate only moderately in the coming months. Annual average HICP inflation is projected at just above 1.0% this year.2. Spain – temporary setback in mid-2010 Economic activity in 2010 is forecast to decline by 0.3% following a fall of3.7% in the previous year. Specifically, the first and second quarters of 2010 recorded positive quarterly growth, largely driven by temporary factors, though these positive effects will fade over the second half of the year.The VAT-rate increase which became effective on 1 July, led to a front-loading of consumption plans from the second to the first half of 2010, which seems consistent with the deterioration observed in retail sales in the third quarter. After growing significantly in the beginning of the year, car sales are also dropping sharply in the third quarter, reflecting the end of the car-scrapping schemes. Thus, private consumption is projected to contract in the second half of the year. Investment will remain weak: while the ongoing adjustment in the housing sector is projected to continue, public investment is set to fall as a result of the cut in public spending scheduled for the second half of 2010. Therefore, quarterly GDP growth is expected to record a temporary fall in the third quarter, but should turn positive in the fourth. For the year as a whole, domestic demand is set to lower GDP growth by nearly 1¼ pps.In the external sector, exports recorded better-than-expected growth at the beginning of 2010, consistent with the recovery of world demand. However, the growth contribution of net exports is expected to be close to 1 pp. compared to 2.7 pps. in 2009 as a result of an important rebound of imports in 2010, driven by a positive evolution of final demand.The inflation rate continued to increase, to 1¼% and above 1½% in the two first quarters of 2010 respectively. It is expected to rise to 1¾% at the end of the year, with an annual average of just above 1½% for 2010, on the back of higher oil prices and the VAT hike. After a significant increase in 2009, real wages are expected to stagnate in 2010,67Interim forecast September 2010following higher inflation and lower nominal wage increases included in recent agreements.Graph 8: Commission's Economic Sentiment Indicators (ESI) and components: differences from the long-term averages(last obs. Aug. 2010)-50-40-30-20-1001020ES NL IT PL FR EA UK EU DEManufacturing Services Consumers Construction Retail ESISource: European Commission3. France – gradual recovery on the back of subdued demandThe French economy has been gradually recovering from recession since the second quarter of last year. For 2009 as a whole, however, it experienced a significant decline of GDP (-2.6%), though less so than the euro area (-4.1%). This was mainly due to the absence of major domestic imbalances, relatively large economic stabilisers, the comparatively low degree of openness of the economy, combined with the limited size of the manufacturing sector, as well as the resilience of private consumption. Unlike the case in several other EU countries, there has been almost no acceleration in growth in the first half of 2010, with GDP expanding at an average quarter-on-quarter rate of 0.4%. In the second quarter of 2010, activity grew by 0.6% q-o-q. As before, domestic demand was the main driver of growth, complemented by the impact of a deceleration in destocking. In spite of the recovery in world trade and the depreciation of the euro, net trade was a drag on growth, as imports expanded strongly.The same structural features that partly shielded the French economy during the crisis will continue to contain the pace of expansion. Although business climate indicators are close to their long-termaverage, they have recently levelled off and remain below their historical recovery levels. This suggests a slowdown of economic expansion compared to the second quarter of 2010. Domestic demand is also set to grow at a moderate pace because the inventory cycle is becoming less supportive. Private consumption will mirror the weakness of disposable income and the after-effects of the car-scrapping premium. Investment growth should be limited given still large spare capacity. The still favourable developments in world trade combined with the euro depreciation are expected to have a positive but limited effect . All in all, GDP is likely to grow by 0.4% and 0.3% in the third and fourth quarter respectively, implying an annual growth rate of 1.6% for 2010 as a whole.HICP inflation reached 1.8% in the second quarter as the rise in oil prices was amplified by a base effect from last year. In 2010, inflation is set to average 1.6% while core inflation is expected to remain subdued. The high unemployment rate and the need for firms to remain competitive in an export-led recovery are likely to weigh on prices.4. Italy – exports contribute to a moderate upturnItaly's real GDP expanded by almost ½ pp. in both the first and the second quarter of 2010 and is expected to grow by 1.1% in the year as a whole. The 0.3 pp. upward revision compared with the Commission's spring 2010 forecast is explained by the better-than-anticipated growth impulse from external demand and a revised 2009 quarterly growth profile.The moderate recovery of the Italian economy is projected to be mainly driven by the industrial sector, thanks to the rebound in exports after the collapse recorded in 2009. The upturn in external demand is providing some support to investment in equipment, which also benefited from tax incentives that expired at the end of June. By contrast, investment in construction is expected to remain weak in the coming quarters. Finally, the still fragile labour-market situation is set to continue weighing on the dynamics of private consumption.As regards the quarterly profile of GDP growth, the most recent data on industrial production andInterim forecast September 2010business confidence suggest economic expansion in the third quarter of 2010 to continue at broadly the same pace as in the first two quarters of the year. The recovery is then projected to ease somewhat in the last quarter of 2010, due to the expected deceleration in global demand.The short-term outlook for the Italian economy appears subject to both upside and downside risks. On the one hand, global demand could prove stronger than anticipated, with positive spillovers also for firms' investment. On the other hand, possible renewed tensions and uncertainty in financial markets might affect economic agents' confidence.After declining markedly in 2009, HICP inflation picked up in the first half of 2010, due to the fading of favourable base effects from energy prices. In 2010 as a whole, inflation is projected to increase to 1.6% on average. This is 0.2 pp. lower than in the Commission's spring 2010 forecast, mainly because of less dynamic commodity prices.5. The Netherlands – maintaining moderate momentumThe recovery of the Dutch economy, which started in the second half of 2009, gained momentum in the first half of 2010, resulting in quarter-on-quarter GDP growth of 0.5% and 0.9% in the first and second quarter, respectively. Economic activity benefitted from a strong upswing in the inventory cycle and a rebound of investment in the second quarter, due mainly to a replacement of equipment. Although exports proved to be an important growth driver again – taking advantage of the acceleration in world trade and reflecting the sensitivity of the Dutch economy to external demand – net exports were a drag on growth, as imports posted even stronger growth in both the first and the second quarter of 2010. Private consumption showed some signs of recovery, especially in the first quarter, but this was in large part due to the low temperatures boosting households' energy consumption.The momentum of economic growth created in the second quarter is expected to continue partially in the third quarter, leading to quarter-on-quarter growth of 0.4%. With the fading of some temporary growth drivers, such as stock building, real GDP growth is expected to weaken again in the fourth quarter to 0.3% q-o-q, so that annual real GDP growth is projected to reach 1.9% in 2010. Private consumption is likely to remain subdued throughout the second half of 2010, given a strong and rapid decline in wage growth, as reflected in recent wage agreements. Additionally, limited support for private consumption is expected to stem from labour-market developments, in spite of the latter having outperformed expectations. The positive growth dynamics of investment displayed in the second quarter are likely to slow down, especially towards the end of 2010, reflecting a loss of demand momentum and a below-average capacity utilisation. Net trade is most likely to contribute to growth only moderately, given the expected softening of world-trade growth.The annual HICP inflation rate was historically low in the first half of 2010, reaching 0.4% in the second quarter. It is projected to increase in the third quarter, mainly as a result of a positive contribution of energy prices coming from a base effect. Overall, for 2010, inflation is expected to reach 1.1%.Graph 9: Uneven GDP developments across Member StatesSource: European Commission6. Poland – manufacturing sector leads the recoveryEconomic activity continued to be strong in the second quarter of 2010, with GDP growth reaching 1.1% q-o-q. The upswing was driven by a strong manufacturing sector (industrial production (s.a.) grew by 10.5% y-o-y in the second quarter of 2010)8。

英语财经报道翻译分析

2016.3黑龙江教育·理论与实践一、财经报道的功能(一)传递财经信息同其他类型的新闻相比较而言,财经报道提供的信息更具有专业性,更能够直接影响群众的经济行为,人们不只是需要通过财经报道所传达出的信息来满足自己了解社会的欲望,更要通过财经报道所提供的信息给出在市场中的投资及决策建议。

(二)剖析财经现象财经报道之间的新闻往往不是纯粹某件事的新闻,而有可能是一些经过长期的积累才发生的财经现象。

因经验和专业知识的局限,人们为了了解这些经济现象必须要借助专业人士报道,并对英文财经信息进行有针对性的解释及剖析。

英文财经报道译者要追溯财经事件的本质和研究其发生背景,将英文信息翻译给国人,使国人明晰经济现象。

(三)传播财经知识每一种经济现象背后都蕴含着丰富的经济学知识,这些专业性较强的经济学知识对于普通读者来说晦涩难懂。

而现阶段的中国社会,专业经济学知识的获得仍然需要通过学校教育的方式进行传播,而且拥有专业经济知识的人又相对较少,这就要求财经报道人员在报道财经现象时,要引入简单易懂的例子来帮助读者理解,这在一定程度上起到了传播财经知识的效果,使人们的经济素养得到提高。

二、财经报道的特点(一)抽象性在一个完整的社会系统中,经济是一个系统化的整体,由实时变动的一系列相互关联的进程、状态和指标构成,这就造就了财经报道很少是具体的某一事件的单纯性报道,而是相关的多方面的信息综合,报道内容本身就是抽象的。

财经类相关电视节目中,“即期交易”“持仓量”“BVI 股权”等财经方面的专业术语是十分常见的,这些术语的使用增添了财经报道的抽象性,晦涩难懂。

这就要求财经报道翻译人员在进行财经新闻报道时,化抽象为具体,内容上专业,表现形式上通俗,将抽象的财经信息贴切地表达出来。

(二)指示性财经新闻是经济状况的晴雨表,具有一定程度的指示性。

财经报道所涉及的指示性特指受众在接收到具体的财经信息后所付诸的有效行为。

即使财经报道并没有明确给出相应的做法,但读完报道后,读者就可以比较清楚地知晓自己应该在什么时间去怎么做。

第一财经介绍英文版

Throuh the postoffice network CBN Daily covers whole mainland.

As the domestic first finance and economics class daily paper, CBN already set up the big brand influence around the 3 big economic areas in China from its influence. Circulated from Monday to Saturday per week.

Derivatives

Money&Boud&Currency Institution Equity Fund&Disclosure

B7

B8

Data

Overseas

Layout of China Business News

C:Company News

Company & Sectors (Mon to Fri,8 pages) C1 C2 C3 C4 C5-8 Industry Headlines Industries Consumption Startups Industry Weekly

Core Coverage Yangtze River delta, Zhu River delta and Beijing around trading area,covering all the first line city of China. Five Values Fiancial News、Investment Guidance、Plan-making Reference、Policy Analysis、Life Style

全球热门报刊双语阅读精选

全球热门报刊双语阅读精选在信息爆炸的时代,我们可以通过互联网轻松获取到各种各样的新闻和资讯。

然而,对于想要提高自己的英语水平的人来说,阅读双语报刊是一个非常有效的方法。

通过阅读双语报刊,我们不仅可以了解到全球各地的新闻,还可以提高自己的语言能力。

下面是一些全球热门报刊的双语阅读精选。

首先,我们来看看《纽约时报》。

作为全球最有影响力的报纸之一,《纽约时报》每天都会报道各种各样的新闻,从政治到经济,从文化到科技,无所不包。

在它的双语版中,你可以看到英文原文和中文翻译,这样你就可以通过对比两种语言来提高自己的阅读能力。

接下来,我们来看看《卫报》。

作为英国最受欢迎的报纸之一,《卫报》以其深入的报道和独立的观点而闻名。

在它的双语版中,你可以看到英文原文和中文翻译,这样你就可以更好地理解文章的内容和作者的观点。

除了这些传统的报纸,还有一些新兴的媒体平台也提供了双语阅读的选项。

比如,《金融时报》和《经济学人》这样的财经媒体,它们的双语版可以帮助你了解全球经济的最新动态。

另外,一些新闻应用程序和网站也提供了双语阅读的功能,比如《今日头条》和《新浪新闻》,你可以根据自己的兴趣选择阅读的内容。

通过阅读双语报刊,我们可以不仅了解到全球各地的新闻,还可以提高自己的语言能力。

首先,通过对比英文原文和中文翻译,我们可以学习到更多的词汇和表达方式。

其次,通过阅读不同类型的文章,我们可以了解到不同领域的专业术语和表达习惯。

最后,通过阅读不同作者的观点,我们可以提高自己的思维能力和批判思维。

当然,阅读双语报刊也有一些挑战。

首先,对于初学者来说,阅读双语报刊可能会比较困难,因为其中可能会有一些生词和复杂的句子结构。

其次,由于翻译的不同,有时候中文翻译可能会与英文原文有所出入,这就需要我们有一定的英文基础来理解原文的意思。

总的来说,阅读双语报刊是提高英语水平的一种有效方法。

通过阅读全球热门报刊的双语版,我们可以了解到全球各地的新闻,提高自己的语言能力,拓宽自己的视野。

财经作文写作英文

财经作文写作英文英文:As a financial writer, I believe that staying up-to-date with the latest economic news and trends is crucial.It not only helps me write better articles, but it also allows me to make informed decisions about my own finances.One of the most important things to keep an eye on is the stock market. Understanding how it works and what factors can affect it can help you make smart investment choices. For example, if you see that a company's stock is consistently rising, it may be a good time to invest inthat company.Another important aspect of personal finance is budgeting. Creating a budget and sticking to it can help you save money and avoid overspending. It's important to track your expenses and identify areas where you can cut back. For example, if you notice that you're spending a lotof money on eating out, you may want to start cooking at home more often.中文:作为一名财经作家,我认为及时了解最新的经济新闻和趋势至关重要。

英文频道介绍

另外,在每晚八点的娱乐节目板快中,《华人电影志》填 补了上海在电影赏析节目上的空白;《不完全爵士》则是全 国唯一一家以爵士乐为主题的音乐深度赏析节目,专业的主 持人,丰富的影视资料,第一手的采访,给广大爵士乐爱好 者带来一个全新的视听盛宴。

除了英语节目之外,每周日外语频道还有两个小时的日 语板块,名牌栏目《中日之桥》在这里继续延伸,同时每周 推出一部日语原版电视剧,众多日本影视明星在这里展现他 们的“原音”风采。《音乐物语》则继续带给观众日本流行 乐坛的最新动态。

由于时间关系,我简短地介绍一 下CCTV9的其中两个突出的新闻 工作者:

杨锐和丙成钢

作为中央电视台英语频道访谈节目

DIALOGUE《今日话题》主持人兼制片人的

杨锐,以独特的主持风、主持人格,深厚的

文化底蕴,赢得了中外观众的称赞。 1980

年江苏南通市高考外语类状元被上海外国语

学院录取,但就读成绩一般,90%时间用于

同时,频道还引进大批原版影视节目,为喜爱观看原版 电影的观众每天奉上电影大餐,其中既包括《指环王》、 《傲慢与偏见》和《蜘蛛侠》等经典大片,也包括《三峡好 人》、《图雅的婚事》和《夜。上海》等优秀国产艺术电影, 以满足电影爱好者的要求。

明珠台(英语:Pearl)

明珠台(英语:Pearl)是电视广播有限公司的英 语电视频道,于1967年11月19日成立,主要的节目 以英语广播,部分节目加粤语作丽音广播。主要对手 为亚洲电视国际台。1991年,明珠台开始采用丽音 广播服务,提供多语言声音广播,观众可自行选择广 播语言。基本上,明珠台于部份节目提供了粤语和英 语作广播(主要在连续剧、电影及纪录片等,其他综 艺类型节目比较少)。而中文字幕在下午6时20分后, 于大部份节目提供。

财经英语怎么说

财经英语怎么说财经是指财政、金融、经济。

财经类专业是指经济类和管理类专业,常见的专业包括市场营销、会计、人力资源管理、金融、国际贸易、企业管理、统计、财税等,是近几年来人才市场上的热门专业。

那么,你知道财经的英文怎么说吗?财经的英文释义:finance and economics财经的英文例句:美元突然贬值,财经专家无不大伤脑筋。

The sudden fall in the value of the dollar has puzzled financial experts.一些财经记者的确拥有明显对口的学历背景。

Some financial journalists do have obviously relevant qualifications.我帮助他摆脱了财经困难。

I help him climb out of his financial hole.我终于发现财经调查结果具有约束力。

I finally find that the financial findings are binding.他的部分观点对于跟踪财经新闻的任何人来说都不会是陌生的。

Part of his argument will be familiar to anyone who follows the financial news.许多男人也读体育版和财经版。

Many men also read the sports pages and the financial pages.我知道你是财经专家。

I know that you are an expert in finance.《财经》作为其旗舰刊物,一直是其最大的收入来源。

Caijing is its flagship publication and one of its biggest money makers.财经新闻是一个竞争日益激烈的行业。

Financial news is an increasingly competitive industry.美元突然贬值,财经专家无不大伤脑筋。

英语新闻及对应翻译网站

之前每天BBC加VOA加CHINA DAIL Y的翻译日子已经结束,在痛苦的翻译过程中找到了有这些新闻相对应的翻译的网站,自己翻不准确的时候可以对照回中文,为了避免收藏夹因为某次中毒被洗掉,整理于此。

BBC/article.php?articleid=81 普特每日听力的页面,每天都有5min的BBC 新闻更新,现在一周还有两到三次访谈节目/forumdisplay.php?fid=27 standard的听力训练版块,可以找到前一天接近原稿的英文听写稿。

/chinese/simp/hi/default.stm BBC中文网,从右上角的搜索框查找你想要的那段新闻的关键词,一般能找到5min新闻的详细版,里面有绝大部分听力的内容,且用句几乎是一样的。

VOA/article.php?articleid=81 普特每日听力的页面,每天都有5min的VOA 新闻更新。

另推荐先听每日的VOA Special English,对应回STANDARD,会容易听懂很多。

/forumdisplay.php?fid=27 standard的听力训练版块,可以找到前一天接近原稿的英文听写稿。

Special English版里也有相应听写稿,不过听的人没有STANDARD 多。

/list-1597-1601.shtml VOA双语新闻,有MP3,一段英文稿配一段中文翻译,是最简单明了直接的一个网站了,有兴趣也可以GOOGLE VOA自己的中文网,我觉得这个已经够用了。

CHINA DAIL Y/ 中国日报网/hqgj/ 环球在线,它是中国日报网的中文网站,首页更新比较慢,但新闻却是更新了的,所以要从右上角新闻那里搜,然后找和中国日报网标题相似日期相同的新闻,就会发现几乎就是那篇的翻译了。

/language_tips/index.html 中国日报英语,英语点津。

如果不是非要听国际新闻的,这个网站上面会挑一些中国日报的新闻中的知识点进行讲解,另有许多非常好的学习内容和资源,可以慢慢去看。

财经新闻英语文体

2007年第5期总第65期JournalofFujianRadio&TVUniversityNo.5,2007General,No.65收稿日期:2007-07-13作者简介:徐琪(1979-),女,福建医科大学基础医学院英语教学部助教。

一、引言新闻英语(JournalisticEnglish)一般指英文报刊、电视和广播等大众传媒使用的英语。

依照报导的内容对其进行划分,一般可分为十一个种类:政治新闻(politicalnews),财经新闻(economicnews),科技新闻(technologi-calnews),文化新闻(culturalnews),体育新闻(sportsnews),暴力犯罪新闻(violenceandcrimenews),灾难新闻(disasternews),天气新闻(weathernews),讣闻(obit-uary),娱乐新闻(entertainment)及杂闻(miscellanies)。

随着中国在世界范围内越来越密切、频繁的经济交流活动,财经新闻英语也日益成为人们日常经济生活中不可或缺的重要组成部分。

作为新闻英语的一个分支,财经新闻英语除了具备新闻英语的共同特点,如倒金字塔式结构,运用字母缩写形式等等外,还具有其自身的特点。

本文将通过例证法对新闻财经从句法和词汇两个角度进行分析。

二、句法特点语言学上一般把语言的功能分为五类:信息功能in-formational,表情功能expressive,指示功能directive,寒暄功能phatic,以及美学功能aesthetic.对于财经新闻而言,毫无疑问,其主要功能是信息功能。

为达到在最短时间内向目标受众最大量地传递信息,新闻必须以最短的篇幅包含最大量的信息。

同时,由于时间的限制,要斟字酌句也不现实。

财经新闻与一般的新闻相比而言,更加具有实时性,否则就无法反映瞬息万变的财经世界,更无从谈及传递信息了。

这些在句法上主要表现为惯用扩展的简单句、常省略名词性从句中的关系代词、较多使用数字和比较结构、大量使用引语等四大特征:1.惯用扩展的简单句(expandedsimplesentences)例1.“NEWYORK-Stocksroared,withthetech-nology-ladenNasdaqmarketpostingitsbiggestgainever,aftertheFederalReservethrewalifelinetoWallStreetwithanunexpectedinterest-ratecuttokeeptheworld'slargesteconomyfromslowingtoomuch.”(纽约———股市上扬,高科技股集中的纳斯达克股市在美联储向华尔街出乎意料地抛出突然宣布降息这根救生索后迎来了其最大一次涨幅,美联储此次降息旨在防止美国经济发展进一步滞缓。

论英语财经新闻的译名统一

文 针 对 网络 对 外

误 商 机 。 果 报 道者 能 把 译 名统 一 原 则提 如

高 到 这 个 角 度 来对 待 , 前 网 络 对外 财经 当 英 语 新 闻 报 道 中译 名 不 统 一 的 问 题 就 会 大 大 改善 甚 至 消 除 。 新 闻 报 道 者 要 加 强 学 习和 积 累正 确

^ 厂

^ .I A O ̄ gE 2 1 ・ ( 半 月 ) 厂 .H 4 - I 0 0 1下

的标 志 ,是 国 家 国 际 经 贸 运 作 能 力 的体

论乒 语幼 崭 的 译名 饶 一

摘要 : 着 网 随

不 统 一 的译 名 主 要 出现 在 经 贸 财 经

络 的普 及 和发 展 ,

必 须 用 统 一 的 、 用 的 、 定 的 译 名 来 传 通 既

些 建议 : 道 者 要 报

提 高 对 译 名 统 一

英文简称都是 U D 。 N C

财 经 新 闻报 道 中 国 外 一 些 重 要 合 同

的 重视 态度 、 强 加 学 习和 积 累 , 将 并

和协 议 的译 名 不 统 一 。 许 多 重 要 合 同 、 条 约 和 协 议 的名 称 具 有 法 律 效 力 和 严 格 的 规 范 性 , 语 表 达 差 别 一 个 词 , 用 和 所 英 效

口 吴

久

经 贸 英 语 财 经 新

闻 报 道 中 出 现 的

译 名 不 统 一 问题 .

分 析 了 当 前 网 络

对 外 经 贸 英 语 财

很 容 易误 导 读 者 弄 错 阅读 对 象 。

外 文 缩 写 词 . 常 不 加 注释 , 英 文 常 用 缩 写 词 造 成意 义不 明 、 解 混 乱 。 如 : 理 例 联 合 国裁 军 审 议 委 员 会 U i d N t n i nt ai sD s e o —

英文版财经新闻

US planemaker Boeing has announced an "historic" order from United Airlines for 150 Boeing 737s, in a deal worth up to $14.7bn.美国飞机制造商波音公司宣布接到联合航空公司一份“历史性”订单,该订单涉及150架波音737s,价值147亿美元。

The order comprises 100 of the new Boeing 737 Max 9 planes and 50 Next Generation 737-900ER aircraft. Boeing said the deal meant it had now received more than 10,000 orders overall for aircraft from the 737 family.Boeing said the 737 was the "undisputed best-selling jetliner in the world".It said the Next Generation 737 was "the mostfuel-efficient and reliable" single-aisle plane in the market.The 737 Max, which is a new-engine variant on the Next Generation 737, builds on these strengths, Boeing said, reducing fuel use and carbon dioxide emissions by 13%.Modern features"United and Boeing share a rich history together and we are delighted United has chosen the 737 for its future fleet, renewing our partnership for decades to come," said Ray Conner, chief executive of Boeing Commercial Airplanes.Jeff Smisek, chief executive of United, said: "We look forward to offering our customers the modern features and reliability of new Boeing airplanes, while also making our fleet more fuel-efficient and environmentally friendly."United Continental, the parent company of United Airlines, said it would begin taking delivery of the 737 Max 9 planes in 2018.The 737-900ERs will be delivered from late 2013.Both planes feature a quieter cabin and brighter lighting, designed to give the impression of more space. The deal is valued at $14.7bn at list prices, although major airlines like United do not pay list prices.United Airlines is the world's biggest carrier. In 2011, it flew more than two million flights, carrying 142 million passengers.Earlier on Thursday, Boeing's European rival Airbus announced a further $6.35bn of potential orders at the Farnborough airshow.The four deals Airbus has announced so far this week, if completed, would total $16.9bn for 115 aircraft. Inflation has eased sharply in China, giving policymakers more room to spur economic growth amidst a global slowdown.中国通货膨胀率急剧下降,这使决策者有更多刺激经济增长的空间。

从目的论的角度探讨财经英语英汉翻译——以《华尔街日报》翻译为例

2332020年31期总第523期ENGLISH ON CAMPUS从目的论的角度探讨财经英语英汉翻译——以《华尔街日报》翻译为例文/刘东旭翻译技巧的选择是由翻译的目的决定,而不是由翻译的原文决定的。

译者在翻译时要注重译文的功能,灵活采取多种翻译策略和技巧,不必拘泥于原文的句法结构。

本文就英语财经新闻中存在的专业词汇和长难句,以及文化差异等,结合笔者的翻译实践进行分析。

1. 词汇的翻译。

词汇是理解文章的基础,由于新闻报道涉及的专业领域和范围较广,因此在翻译的过程中首先要对新闻词汇进行准确把握和理解。

在本节中将会举例展开解释部分专有名词、数学单位和动词的翻译。

(1)专有名词翻译。

英语财经新闻虽然注重可读性,但仍会有些专业词汇,或者一些常见的普通词汇在这里有其专门的用法和释义。

①But the further paring down of SoftBank' s Alibaba stake, as well as the departure of Mr. Ma from SoftBank' s board mark aturning point in a relationship that dates to the 1990s.②Mr. Ma brought Mr. Son onto Alibaba ' s board in 2005, a position he still holds.例①②中,Board作名词时指“板,木板等”;作动词时指“上(船、车或飞机)”,而在财经英语中指董事会。

如在本文例句中,SoftBank ' s board在句中表软银董事会,Alibaba ' s board 即阿里巴巴董事会。

③The market showed it was open to giant publicstock sales last week when PNC Financial Services Inc., the Pittsburgh-based regional bank, sold its stake in money manager BlackRock Inc. for about $13 billion.例③中,在新闻文章中我们常看到Inc.,Corp.和Co. Ltd 等公司的缩写形式。

英文报纸版面结构

英文报纸版面结构英文报纸的版面结构通常包括以下几个主要部分:1. 头版(Front Page):头版通常是报纸的正面,包含当天最重要的新闻、图片和标题。

这里通常放置最引人注意的内容,以吸引读者。

2. 要闻(Headlines):在头版或页面顶部,通常是粗体、大字体的标题,简洁地概括了当天最重要的新闻事件。

3. 新闻版块(News Sections):报纸的主要内容区域,包括政治、国际、国内、商业、文化等各类新闻板块。

每个板块都有不同的标题和副标题。

4. 专栏和评论(Opinion and Editorial Sections):这些部分包括专栏作家和评论员的观点、分析和评论,涵盖各种话题,如政治、社会、经济等。

5. 文化和娱乐(Arts and Entertainment):报道艺术、文化、娱乐圈的新闻,包括书评、电影评价、音乐、艺术展览等。

6. 体育版块(Sports Section):报道体育新闻、赛事结果、运动员采访等内容。

7. 财经版块(Business and Finance Section):涵盖股市、经济、企业新闻等内容,包括股票市场行情和商业趋势。

8. 公告栏和分类广告(Classifieds and Announcements):发布个人、商业和招聘广告,以及公告、通知等信息。

9. 生活版块(Lifestyle Section):包括食品、健康、家庭、旅行等生活相关的文章和建议。

10. 补充内容(Supplementary Content):可能包括杂志式的专题报道、附录、特别报道等。

这些部分组成了报纸的整体结构,在版面设计上通过标题、图片、字体等排版元素来吸引读者、突出重点和提供丰富的信息。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

US planemaker Boeing has announced an "historic" order from United Airlines for 150 Boeing 737s, in a deal worth up to $14.7bn.美国飞机制造商波音公司宣布接到联合航空公司一份“历史性”订单,该订单涉及150架波音737s,价值147亿美元。

The order comprises 100 of the new Boeing 737 Max 9 planes and 50 Next Generation 737-900ER aircraft.Boeing said the deal meant it had now received more than 10,000 orders overall for aircraft from the 737 family.Boeing said the 737 was the "undisputed best-selling jetliner in the world".It said the Next Generation 737 was "the most fuel-efficient and reliable"single-aisle plane in the market.The 737 Max, which is a new-engine variant on the Next Generation 737, builds on these strengths, Boeing said, reducing fuel use and carbon dioxide emissions by 13%.Modern features"United and Boeing share a rich history together and we are delighted United has chosen the 737 for its future fleet, renewing our partnership for decades to come," said Ray Conner, chief executive of Boeing Commercial Airplanes.Jeff Smisek, chief executive of United, said: "We look forward to offering our customers the modern features and reliability of new Boeing airplanes, while also making our fleet more fuel-efficient and environmentally friendly."United Continental, the parent company of United Airlines, said it would begin taking delivery of the 737 Max 9 planes in 2018.The 737-900ERs will be delivered from late 2013.Both planes feature a quieter cabin and brighter lighting, designed to give the impression of more space.The deal is valued at $14.7bn at list prices, although major airlines like United do not pay list prices.United Airlines is the world's biggest carrier. In 2011, it flew more than two million flights, carrying 142 million passengers.Earlier on Thursday, Boeing's European rival Airbus announced a further $6.35bn of potential orders at the Farnborough airshow.The four deals Airbus has announced so far this week, if completed, would total $16.9bn for 115 aircraft.Inflation has eased sharply in China, giving policymakers more room to spur economic growth amidst a global slowdown.中国通货膨胀率急剧下降,这使决策者有更多刺激经济增长的空间。

Consumer price rises cooled in June to 2.2% compared to the previous year, China's statistics bureau said.That is down from 3% in May and is well below the government target of 4%. China has taken steps to bolster(支持) growth as the global economic crisis weighs on demand for its goods.Analysts said lower food prices was the main driver of the slowing inflation.Pork prices, one of the biggest contributors to skyrocketing inflation last year, fell 12.2% from 2011.Growth stepsChina's central bank has cut key interest rates twice since the start of June, with benchmark lending rates down to 6%.It has also cut the amount of money banks must keep in reserve in an effort to boost lending.Analysts said they expected more such moves to boost growth from the government going forward."A lower consumer price index opens room for further policy easing, which we expect will pick up," said Zhang Zhiwei, chief China economist at Nomura in Hong Kong.International Monetary Fund (IMF) chief Christine Lagarde has said that the organisation's next forecast for global economic growth would be down from the 3.5% predicted in April.国际货币基金组织主席克里斯蒂娜·拉加德称,其组织对全球经济增长的预期将低于四月份预测的3.5%。

She also hailed EU leaders' efforts to solve the debt crisis.She said "significant steps" had been taken, but further reforms and strong implementation were needed.Christine Lagarde was speaking at an economic symposium(讨论会) in Tokyo as part of a week-long tour of Asia.Referring to measures adopted by eurozone leaders in Brussels last week, she said: "From the IMF perspective, we believe that more needs to be done in order to complete [the reform]."It's also a question of implementation - diligent(勤勉的) , rigorous, steady implementation."She particularly praised moves towards banking union.But she added that more would need to be done both inside and outside the eurozone, with renewed attempts at increased co-operation between countries.She said they should work together to restore trust in sovereign debt, reform the financial sector and achieve sustained growth.'Certainly lower'She warned that the IMF's forecast for global economic growth, which is due out later this month, would be lowered."What I can tell you is that it will be tilted to the downside and certainly lower than the forecast that was published three months ago," she said.Japanese Prime Minister Yoshihiko Noda complained that Europe's debt problems were hurting the Japanese economy because they were causing unjustified rises in the value of the yen."Market jitters on eurozone problems, especially one-sided yen rises that do not reflect Japan's economic fundamentals, are inflicting severe damage on economic sentiment(感情) ," he said.Credit ratings agency Moody's also said on Friday that the short-term risks to the eurozone economy had reduced.But it warned there would be a high cost to wealthier eurozone countries.The Bank of France has cut its forecast for the French economy.法国银行降低了今年法国经济发展的预期。