会计循环1

会计循环

汇总表”的有关栏内,然后再分别加计全部会计科目的借方本 期发生额和贷方本期发生额,填写到“合计”栏内。根据借贷 必相等原理,两个合计金额必然相等。“记账凭证汇总表”的 具体格式,如图表11-54,11-55所示。

三、记账凭证汇总表账务处理程序的核算步骤 记账凭证汇总表账务处理程序的具体核算步骤是:

第一节 会计循环概述

一、会计循环的意义 所谓会计循环是指企业将一定时期内发生的所有经济业务, 依照一定步骤、方法加以记录、归类、汇总直至编制会计报表, 这样一个周而复始循环往复的过程。在会计实务中,科学地组 织会计循环,对于有效地保证会计信息质量;连续、系统地记 录和反映各项经济业务的发生和完成情况,提供连续、全面的 会计信息具有重要意义。 二、会计循环的基本步骤 一个典型的会计循环过程,一般包括以下基本步骤: 1、会计事项的发生。会计主体在发生对内对外经济业务时,不论 是买卖、借贷或其他往来事项,只要经过双方同意,并议定公平 价格或承诺的,即构成会计事项发生。因此,会计事项必须是具 有经济活动内容、并可以计价结算的经济业务。

二、记账凭证账务处理程序的核算步骤 记账凭证账务处理程序的核算步骤是:

1. 根据原始凭证或原始凭证汇总表填制记账凭证。

2. 根据收款凭证和付款凭证逐日逐笔登记现金日记账和银行 存款日记账。 3. 根据各种记账凭证结合其所附原始凭证逐笔登记各种明细 分类账。 4. 根据各种记账凭证逐笔登记总分类账。

第二,可以正确、及时地提供会计信息,保证会计工作的质量, 更好地发挥会计在经营管理中的作用。

第三,可以简化会计核算手续,节约人力、物力和财力。

二、组织账务处理程序的要求

账务处理程序的确定,一般应符合以下基本要求: 1.要适应本单位的经济活动特点。会计核算必须从客观实际出发,根据 本单位经济活动的性质、经济管理的要求、规模的大小、业务的繁简、 人员的多少、管理水平的高低等,选择适合本单位特点的核算组织程序, 以有利于建立岗位责任制。 2.要满足经济管理的需要。会计是经济管理的重要工具,因此,会计核 算必须与经济管理的要求密切配合,贯彻国家的统一规定,符合财政部 门制定的会计制度,为国民经济的综合平衡、为本单位的经济管理和国 家及其有关部门监督经济活动提供正确、及时和完整的会计资料,以促 进单位改进和提高经济管理工作。 3.要能够提高核算工作质量与效率。帐务处理程序的建立,一方面要能 如实地反映经济活动情况,提供有用的会计信息;另一方面要在保证会 计资料正确、真实和完整的前提下,力求简化核算手续,提高会计工作 效率,节约人力物力,使日常会计核算工作得到最佳的协调配合。

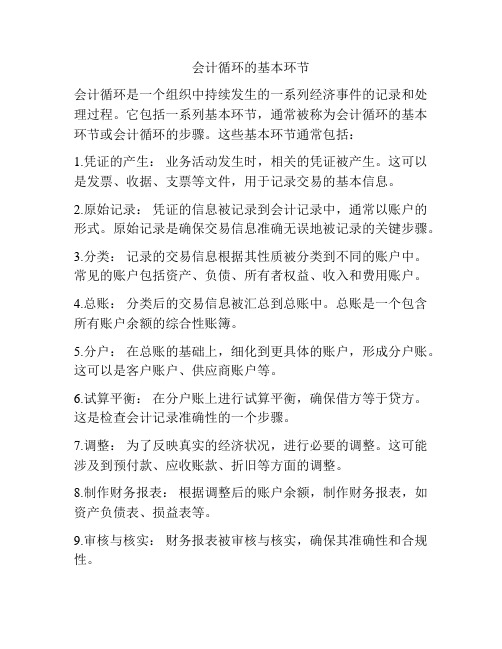

会计循环的基本环节

会计循环的基本环节

会计循环是一个组织中持续发生的一系列经济事件的记录和处理过程。

它包括一系列基本环节,通常被称为会计循环的基本环节或会计循环的步骤。

这些基本环节通常包括:

1.凭证的产生:业务活动发生时,相关的凭证被产生。

这可以是发票、收据、支票等文件,用于记录交易的基本信息。

2.原始记录:凭证的信息被记录到会计记录中,通常以账户的形式。

原始记录是确保交易信息准确无误地被记录的关键步骤。

3.分类:记录的交易信息根据其性质被分类到不同的账户中。

常见的账户包括资产、负债、所有者权益、收入和费用账户。

4.总账:分类后的交易信息被汇总到总账中。

总账是一个包含所有账户余额的综合性账簿。

5.分户:在总账的基础上,细化到更具体的账户,形成分户账。

这可以是客户账户、供应商账户等。

6.试算平衡:在分户账上进行试算平衡,确保借方等于贷方。

这是检查会计记录准确性的一个步骤。

7.调整:为了反映真实的经济状况,进行必要的调整。

这可能涉及到预付款、应收账款、折旧等方面的调整。

8.制作财务报表:根据调整后的账户余额,制作财务报表,如资产负债表、损益表等。

9.审核与核实:财务报表被审核与核实,确保其准确性和合规性。

10.决策:最后,基于财务报表的信息,组织可以做出决策,进行财务规划和经营管理。

这些基本环节构成了一个完整的会计循环,确保了组织的经济活动得以记录、分析和报告,为管理层提供了决策的基础。

每个环节都是会计体系中不可或缺的一部分。

会 计 循 环

应计费用的期末调整将同时等额地影响 费用和负债 。

【例7--2】华泰公司2009年12月1日向

银行借入一笔6个月的短期借款80,000元,年 利率6%。 分析:这项经济业务发生后,形成借款利息 费用2,400元,分6个月摊销。根据权责发生 制这一记账基础,应该在2009年12月底计提 当年已经发生但是尚未支付的利息费用。

编制以下调整分录: 借:财务费用 400 贷:应付利息 400

(三)预收收入的账项调整

预收收入是指以前会计期间已经收到入 账,但应归属本期或以后各期的收入。

企业在平时的一些交易中,会发生先收 取收入并已入账,但尚未向付款单位提供商 品或劳务或财产物资使用权,按照权责发生 制原则,这种收入不属于或不完全属于本期 收入。因此,每期的期末都要对预收收入账 项进行调整,将已实现的部分转为本期的收 入,未实现的部分递延到下期。

一、账项调整的意义

账项调整有助于正确地反映企业期末财 务状况。

期末账项调整即期末结账前,按照权责 发生制原则,确定本期的应得收入和应负担 的费用,并据以对账簿记录的有关账项进行 必要调整的会计处理方法。主要是为了在利 润表中正确地反映本期的经营成果以及正确 地反映企业期末的财务状况。

二、账项调整的内容

借方发生额

贷方发生额

合计

◆在实际工作中,企业一般将“总分类账户 本期发生额试算平衡表”和“总分类账户 期末余额试算平衡表”合并在一张表上

如图表7-3: 总分类账户本期发生额及余额试算平衡表

账户名称 期初余额 本期发生额 期初余额 借方 贷方 借方 贷方 借方 贷方

合计

第三节 账项调整

● 账项调整就是按照权责发生制这一标准, 合理地反映相互连接的各会计期间应得的 收入和应负担的费用,使各期的收入和费 用能在相关的基础上进行配比,从而比较 正确地确定出各期的盈亏。

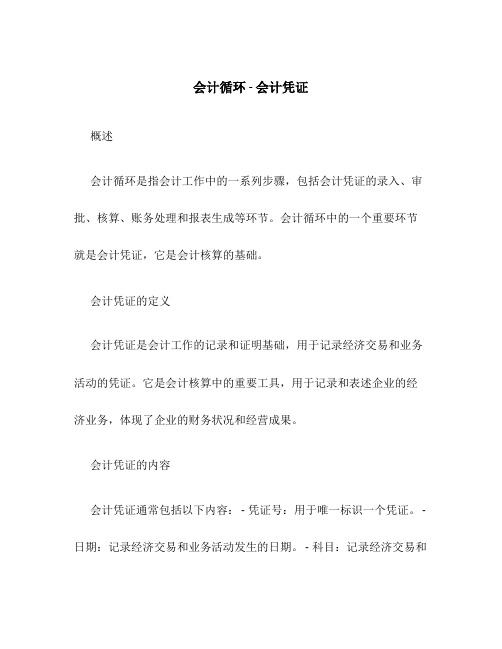

会计循环-会计凭证

会计循环 - 会计凭证概述会计循环是指会计工作中的一系列步骤,包括会计凭证的录入、审批、核算、账务处理和报表生成等环节。

会计循环中的一个重要环节就是会计凭证,它是会计核算的基础。

会计凭证的定义会计凭证是会计工作的记录和证明基础,用于记录经济交易和业务活动的凭证。

它是会计核算中的重要工具,用于记录和表述企业的经济业务,体现了企业的财务状况和经营成果。

会计凭证的内容会计凭证通常包括以下内容: - 凭证号:用于唯一标识一个凭证。

- 日期:记录经济交易和业务活动发生的日期。

- 科目:记录经济交易和业务活动涉及的会计科目。

- 借方金额:记录经济交易和业务活动的借方金额。

- 贷方金额:记录经济交易和业务活动的贷方金额。

- 摘要:简述经济交易和业务活动的内容和目的。

- 制证人:记录制证人的姓名。

会计凭证的种类根据不同的经济交易和业务活动,会计凭证可以分为多种类型。

常见的会计凭证类型包括: 1. 收款凭证:记录企业收到的款项。

2. 付款凭证:记录企业支付的款项。

3. 收入凭证:记录企业获得的收入。

4.销售凭证:记录企业销售产品或提供服务的凭证。

5. 购买凭证:记录企业购买商品或服务的凭证。

6. 资产凭证:记录企业购置或处置资产的凭证。

7. 负债凭证:记录企业借款或偿还债务的凭证。

8. 资产损益凭证:记录企业决策和行为引起的资产和负债的损益变动。

会计凭证的流程会计凭证的处理流程包括以下步骤: 1. 录入凭证:将经济交易和业务活动的相关信息录入凭证中,包括凭证号、日期、科目、借贷金额和摘要等。

2. 审批凭证:对录入的凭证进行审查和审批,确保凭证的准确性和合规性。

3. 核算凭证:根据凭证的科目和金额进行会计核算,包括借贷平衡、科目余额等。

4. 账务处理:根据核算结果,更新会计账簿和账户余额。

5. 报表生成:根据账务处理的结果,生成各类财务报表,如资产负债表、利润表等。

会计凭证的重要性会计凭证是财务会计工作中的核心,对企业的财务管理、决策和报告起着至关重要的作用: - 记录交易和活动:会计凭证记录了企业的经济交易和业务活动,体现了企业的经营情况和财务状况。

简述会计循环及其基本步骤

简述会计循环及其基本步骤会计循环是指会计工作中的一系列连续性操作和过程,主要包括了会计核算、报表编制和决策分析等环节。

它是一种持续循环的过程,通过不断的记录和分析,使企业能够及时了解自身的财务状况,为经营决策提供准确的数据支持。

下面将简要介绍会计循环的基本步骤。

第一步:凭证的登记和分类凭证是会计循环的基础,它记录了企业的经济活动和交易。

在这一步骤中,会计人员需要根据企业的经济活动,将相关的凭证进行登记和分类。

登记是指将凭证上的各项经济业务按照一定的规则,记录到会计账簿中。

分类是指根据凭证上的经济业务性质,将其归类到相应的会计科目中。

第二步:账户的核算和汇总在这一步骤中,会计人员需要对各项会计账户进行核算和汇总。

核算是指根据凭证上的经济业务,按照一定的规则进行账户的计算和调整。

汇总是指将各项账户的核算结果进行统计和合并,得出企业的总账和各项明细账。

第三步:报表的编制和分析在这一步骤中,会计人员需要根据会计核算的结果,编制各种财务报表。

常见的财务报表有资产负债表、利润表和现金流量表等。

编制财务报表是为了反映企业的财务状况和经营成果,为企业的经营决策提供依据。

同时,在编制财务报表的过程中,会计人员还需要对报表进行分析,以评估企业的经营状况和财务风险。

第四步:决策分析和调整在这一步骤中,会计人员需要对财务报表进行分析,以提供决策参考。

通过对财务报表的分析,可以了解企业的盈利能力、偿债能力和经营效益等情况,从而为企业的经营决策提供支持。

同时,会计人员还需要根据分析结果,对企业的会计核算和报表编制进行调整和修正,以确保财务信息的准确性和可靠性。

以上就是会计循环的基本步骤。

通过这一循环过程,企业能够及时了解自身的财务状况,为经营决策提供准确的数据支持。

同时,会计循环也是企业经营管理的基础,对于企业的经营和发展具有重要意义。

因此,加强会计循环的管理,提高会计工作的质量和效率,对于企业的可持续发展具有重要意义。

会计循环的内容

会计循环的内容我呀,跟你说这会计循环的内容,那可真是有点意思又有点麻烦。

你看啊,首先得有这么个交易或者事项发生。

就像我去菜市场买菜,我从兜里掏出钱给菜贩子,这就是个交易,在会计上呢,这就是会计循环的开端。

这时候,就得开始记账了。

记账那得有专门的本子,就像会计有账本一样。

我得把买了啥菜,花了多少钱,明明白白地写下来。

会计呢,他就得把这个交易按照规定的格式,借方写啥,贷方写啥,规规矩矩地记好。

这借方贷方啊,就像是两个人在拉一个锯,你这边多点,我那边就得少点,得平衡着来。

比如说我买了一把青菜,两块钱。

那在会计的账本里,可能就是库存现金减少两块,这是贷方;而食材的成本增加两块,这就是借方。

这账本上的数字啊,得写得清清楚楚的,那些个会计,戴着个眼镜,眼睛死死地盯着账本,那认真的模样,就像在审视世界上最珍贵的宝贝。

那小笔尖在账本上“沙沙沙”地写着,每一笔都像是在刻画一个故事。

记完账了,还不算完呢。

接着就得做分录汇总了。

这就好比把我今天买的所有菜的花销啊,归拢归拢。

会计也是把一段期间里的那些借方贷方的账目,都整理到一块儿,看看总的是个啥情况。

这个过程啊,就像是把散落在地上的珠子,用线串起来,变成一条漂亮的项链,整整齐齐的。

然后就是试算平衡。

这就像走钢丝一样,得两边都平衡了才行。

要是不平衡啊,那会计可就头疼了。

他就像热锅上的蚂蚁,在那账本里翻来覆去地找,到底是哪里出了错呢?那眉头皱得能夹死苍蝇,眼睛里满是疑惑和焦急。

试算平衡之后,就该调整账目了。

有时候啊,有些事儿不是当时就清楚的,就像我买的菜里有个烂叶子,当时没发现,后来才看到,这就得调整菜的成本了。

会计也是,有些费用或者收入可能之前没记对,或者有新的情况出现,就得调整账目。

最后就是编制财务报表了。

这报表就像是一张大地图,把公司的财务状况都清清楚楚地展示出来。

利润多少啊,资产多少啊,负债多少啊,都在这上头。

那些个老板啊,就看着这报表,就像看着自己的家底儿一样,脸上的表情也是随着报表上的数字变来变去的。

《会计循环》课件

B

C

成本计算与结转

根据企业生产、经营和管理需要,进行成本 计算和结转,为决策提供依据。

财产清查与报告

定期或不定期进行财产清查,编制财产清查 报告,确保账实相符。

D

会计循环的重要性

提高会计信息质量

通过规范化的会计循环,能够提高会 计信息的质量,保证会计信息的真实 、完整、准确。

03 会计循环实务操作

填制和审核原始凭证

总结词

原始凭证是经济业务发生时的第一手资料,是会计记录的主要依据。

详细描述

原始凭证的填制要求真实、完整、规范,包括发票、收据、入库单等。审核原 始凭证时,需要核对凭证的日期、金额、数量等信息,确保其真实性和准确性 。

编制记账凭证

总结词

记账凭证是会计记录的载体,是按照会计制度规定对原始凭证进行处理和分类的 结果。

分类

按照所反映的经济内容可分为收 款凭证、付款凭证和转账凭证。

内容

包括凭证的名称、填制日期、编 号、经济业务内容摘要、会计科

目、金额等。

总账与明细账

总账

01

总账是按照总分类账户分类登记交易或事项的账簿,是编制会

计报表的主要依据。

明细账

02

明细账是按照明细分类账户分类登记交易或事项的账簿,是对

总账的补充和具体化。

对账与结账的注意事项

对账注意事项

对账是会计循环中重要的环节,需要 核对账目是否一致,确保账务处理的 正确性。在对账过程中,需要注意核 对金额、科目、日期等信息,避免出 现误差。

结账注意事项

结账是会计循环的最后一个环节,需 要将本期所有经济业务进行总结和结 算。在结账时,需要注意核对本期发 生额和期末余额,确保财务报表的准 确性。

(word完整版)会计循环1习题精选含答案,推荐文档

True / False Questions1. Accounts that appear in the balance sheet are often called temporary (nominal) accounts.FALSE2. Income Summary is a temporary account only used for the closing process. TRUE3. Revenue accounts should begin each accounting period with zero balances. TRUE4. Closing revenue and expense accounts at the end of the accounting period serves to make the revenue and expense accounts ready for use in the next period.TRUE5. The closing process takes place after financial statements have been prepared. TRUE6. Revenue and expense accounts are permanent (real) accounts and should not be closed at the end of the accounting period.FALSE7. Closing entries result in revenues and expenses being reflected in the owner's capital account.TRUE8. The closing process is a step in the accounting cycle that prepares accounts for the next accounting period.TRUE9. The closing process is a two-step process. First revenue, expense, and withdrawals are set to a zero balance. Second, the process summarizes a period's assets and expenses.FALSE10. Closing entries are required at the end of each accounting period to close all ledger accounts.FALSE11. Closing entries are designed to transfer the end-of-period balances in the revenue accounts, the expense accounts, and the withdrawals account to owner's capital. TRUE12. The Income Summary account is a permanent account that will be carried forward period after period.FALSE13. Closing entries are necessary so that owner's capital will begin each period with a zero balance.FALSE14. Permanent accounts carry their balances into the next accounting period. Moreover, asset, liability and revenue accounts are not closed as long as a company continues in business.FALSE15. The first step in the accounting cycle is to analyze transactions and events to prepare for journalizing.TRUE16. The accounting cycle refers to the sequence of steps in preparing the work sheet. FALSE17. The first five steps in the accounting cycle include analyzing transactions, journalizing, posting, preparing an unadjusted trial balance, and recording adjusting entries.TRUE18. The last four steps in the accounting cycle include preparing the adjusted trial balance, preparing financial statements and recording closing and adjusting entries. FALSE19. A classified balance sheet organizes assets and liabilities into important subgroups that provide more information to decision makers.TRUE20. An unclassified balance sheet provides more information to users than a classified balance sheet.FALSE21. Current assets and current liabilities are expected to be used up or come due within one year or the company's operating cycle whichever is longer.TRUE22. Intangible assets are long-term resources that benefit business operations that usually lack physical form and have uncertain benefits.TRUE23. Assets are often classified into current assets, long-term investments, plant assets, and intangible assets.TRUE24. Current liabilities are cash and other resources that are expected to be sold, collected or used within one year or the company's operating cycle whichever is longer.FALSE25. Long-term investments can include land held for future expansion.TRUE26. Plant assets and intangible assets are usually long-term assets used to produce or sell products and services.TRUE27. Current liabilities include accounts receivable, unearned revenues, and salaries payable.FALSE28. Cash and office supplies are both classified as current assets.TRUE29. Plant assets are also called fixed assets or property, plant, and equipment. TRUE30. The current ratio is used to help assess a company's ability to pay its debts in the near future.TRUEMultiple Choice Questions64. Another name for temporary accounts is:A. Real accounts.B. Contra accounts.C. Accrued accounts.D. Balance column accounts.E. Nominal accounts.65. When closing entries are made:A. All ledger accounts are closed to start the new accounting period.B. All temporary accounts are closed but not the permanent accounts.C. All real accounts are closed but not the nominal accounts.D. All permanent accounts are closed but not the nominal accounts.E. All balance sheet accounts are closed.66. Revenues, expenses, and withdrawals accounts, which are closed at the end of each accounting period are:A. Real accounts.B. Temporary accounts.C. Closing accounts.D. Permanent accounts.E. Balance sheet accounts.67. Which of the following statements is incorrect?A. Permanent accounts is another name for nominal accounts.B. Temporary accounts carry a zero balance at the beginning of each accounting period.C. The Income Summary account is a temporary account.D. Real accounts remain open as long as the asset, liability, or equity items recorded in the accounts continue in existence.E. The closing process applies only to temporary accounts.68. Assets, liabilities, and equity accounts are not closed; these accounts are called:A. Nominal accounts.B. Temporary accounts.C. Permanent accounts.D. Contra accounts.E. Accrued accounts.69. Closing the temporary accounts at the end of each accounting period:A. Serves to transfer the effects of these accounts to the owner's capital account on the balance sheet.B. Prepares the withdrawals account for use in the next period.C. Gives the revenue and expense accounts zero balances.D. Causes owner's capital to reflect increases from revenues and decreases from expenses and withdrawals.E. All of these.70. Journal entries recorded at the end of each accounting period to prepare the revenue, expense, and withdrawals accounts for the upcoming period and to update the owner's capital account for the events of the period just finished are referred to as:A. Adjusting entries.B. Closing entries.C. Final entries.D. Work sheet entries.E. Updating entries.71. The closing process is necessary in order to:A. calculate net income or net loss for an accounting period.B. ensure that all permanent accounts are closed to zero at the end of each accounting period.C. ensure that the company complies with state laws.D. ensure that net income or net loss and owner withdrawals for the period are closed into the owner's capital account.E. ensure that management is aware of how well the company is operating.72. Closing entries are required:A. if management has decided to cease operating the business.B. only if the company adheres to the accrual method of accounting.C. if a company's bookkeeper forgets to prepare reversing entries.D. if the temporary accounts are to reflect correct amounts for each accounting period.E. in order to satisfy the Internal Revenue Service.73. The recurring steps performed each reporting period, starting with analyzing and recording transactions in the journal and continuing through the post-closing trial balance, is referred to as the:A. Accounting period.B. Operating cycle.C. Accounting cycle.D. Closing cycle.E. Natural business year.74. Which of the following is the usual final step in the accounting cycle?A. Journalizing transactions.B. Preparing an adjusted trial balance.C. Preparing a post-closing trial balance.D. Preparing the financial statements.E. Preparing a work sheet.75. A classified balance sheet:A. Measures a company's ability to pay its bills on time.B. Organizes assets and liabilities into important subgroups.C. Presents revenues, expenses, and net income.D. Reports operating, investing, and financing activities.E. Reports the effect of profit and withdrawals on owner's capital.76. The assets section of a classified balance sheet usually includes:A. Current assets, long-term investments, plant assets, and intangible assets.B. Current assets, long-term assets, revenues, and intangible assets.C. Current assets, long-term investments, plant assets, and equity.D. Current liabilities, long-term investments, plant assets, and intangible assets.E. Current assets, liabilities, plant assets, and intangible assets.77. The usual order for the asset section of a classified balance sheet is:A. Current assets, prepaid expenses, long-term investments, intangible assets.B. Long-term investments, current assets, plant assets, intangible assets.C. Current assets, long-term investments, plant assets, intangible assets.D. Intangible assets, current assets, long-term investments, plant assets.E. Plant assets, intangible assets, long-term investments, current assets.78. A classified balance sheet differs from an unclassified balance sheet in thatA. a unclassified balance sheet is never used by large companies.B. a classified balance sheet normally includes only three subgroups.C. a classified balance sheet presents information in a manner that makes it easier to calculate a company's current ratio.D. a classified balance sheet will include more accounts than an unclassified balance sheet for the same company on the same date.E. a classified balance sheet cannot be provided to outside parties.79. Two common subgroups for liabilities on a classified balance sheet are:A. current liabilities and intangible liabilities.B. present liabilities and operating liabilities.C. general liabilities and specific liabilities.D. intangible liabilities and long-term liabilities.E. current liabilities and long-term liabilities.80. The current ratio:A. Is used to measure a company's profitability.B. Is used to measure the relation between assets and long-term debt.C. Measures the effect of operating income on profit.D. Is used to help evaluate a company's ability to pay its debts in the near future.E. Is calculated by dividing current assets by equity.81. The current ratio:A. Is calculated by dividing current assets by current liabilities.B. Helps to assess a company's ability to pay its debts in the near future.C. Can reveal problems in a company if it is less than 1.D. Can affect a creditor's decision about whether to lend money to a company.E. All of these.AACSB: CommunicationsAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: HardLearning Objective: A182. The Unadjusted Trial Balance columns of a company's work sheet show the balance in the Office Supplies account as $750. The Adjustments columns show that $425 of these supplies were used during the period. The amount shown as Office Supplies in the Balance Sheet columns of the work sheet is:A. $325 debit.B. $325 credit.C. $425 debit.D. $750 debit.E. $750 credit.83. A 10-column spreadsheet used to draft a company's unadjusted trial balance, adjusting entries, adjusted trial balance, and financial statements, and which is an optional tool in the accounting process is a(n) :A. Adjusted trial balance.B. Work sheet.C. Post-closing trial balance.D. Unadjusted trial balance.E. General ledger.84. Accumulated Depreciation, Accounts Receivable, and Service Fees Earned would be sorted to which respective columns in completing a work sheet?A. Balance Sheet or Statement of Owner's Equity-Credit; Balance Sheet or Statement of Owner's Equity Debit; and Income Statement-Credit.B. Balance Sheet or Statement of Owner's Equity-Debit; Balance Sheet or Statement of Owner's Equity-Credit; and Income Statement-Credit.C. Income Statement-Debit; Balance Sheet or Statement of Owner's Equity-Debit; and Income Statement-Credit.D. Income Statement-Debit; Income Statement-Debit; and Balance Sheet or Statement of Owner's Equity-Credit.E. Balance Sheet or Statement of Owner's Equity-Credit; Income Statement-Debit; and Income Statement-Credit.85. Which of the following statements is incorrect?A. Working papers are useful aids in the accounting process.B. On the work sheet, the effects of the accounting adjustments are shown on the account balances.C. After the work sheet is completed, it can be used to help prepare the financial statements.D. On the work sheet, the adjusted amounts are sorted into columns according to whether the accounts are used in preparing the unadjusted trial balance or the adjusted trial balance.E. A worksheet is not a substitute for financial statements86. A company shows a $600 balance in Prepaid Insurance in the Unadjusted Trial Balance columns of the work sheet. The Adjustments columns show expired insurance of $200. This adjusting entry results in:A. $200 decrease in net income.B. $200 increase in net income.C. $200 difference between the debit and credit columns of the Unadjusted Trial Balance.D. $200 of prepaid insurance.E. An error in the financial statements.87. Statements that show the effects of proposed transactions as if the transactions had already occurred are called:A. Pro forma statements.B. Professional statements.C. Simplified statements.D. Temporary statements.E. Interim statements.88. If in preparing a work sheet an adjusted trial balance amount is mistakenly sorted to the wrong work sheet column. The Balance Sheet columns will balance on completing the work sheet but with the wrong net income, if the amount sorted in error is:A. An expense amount placed in the Balance Sheet Credit column.B. A revenue amount placed in the Balance Sheet Debit column.C. A liability amount placed in the Income Statement Credit column.D. An asset amount placed in the Balance Sheet Credit column.E. A liability amount placed in the Balance Sheet Debit column.89. If the Balance Sheet and Statement of Owner's Equity columns of a work sheet fail to balance when the amount of the net income is added to the Balance Sheet and Statement of Owner's Equity Credit column, the cause could be:A. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Debit column.B. A revenue amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.C. An asset amount entered in the Income Statement and Statement of Owner's Equity Debit column.D. A liability amount entered in the Income Statement and Statement of Owner's Equity Credit column.E. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.Problems129. In the table below, indicate with an "X" in the proper column whether the account is a (nominal) temporary account or a (real) permanent account.132. Based on the adjusted trial balance shown below, prepare a classified balance sheet for Focus Package Delivery.* $2,000 of the long-term note payable is due during the next year.135. Use the following partial work sheet from Matthews Lanes to prepare its income statement, statement of owner's equity and a balance sheet (Assume the owner did not make any investments in the business this year.)137. A partially completed work sheet is shown below. The unadjusted trial balance columns are complete. Complete the adjustments, adjusted trial balance, income statement, and balance sheet and statement of owner's equity columns.140. The adjusted trial balance of Sara's Web Services follows:(a) Prepare the closing entries for Sara's Web Services.(b) What is the balance of Sara's capital account after the closing entries are posted?Problems159. The unadjusted trial balance of Quick Delivery is entered on the partial work sheet below. Complete the work sheet using the following information:(a) Salaries earned by employees that are unpaid and unrecorded, $5,000.(b) An inventory of supplies showed $1,000 of unused supplies still on hand.(c) Depreciation on delivery vans, $24,000.(d) Services paid in advance by customers of $10,000 have now been provided tocustomers.。

中级财务会计——会计循环

1、收到银行通知,用银行存款支付到期的商业承兑汇票100 000元。

2、购入原材料一批,用银行存款支付货款150 000元,以及购入材料支付的增值税额为25 500元,款项已付,材料未到。

3、收到原材料一批,实际成本100 000元,计划成本95 000元,材料已验收入库,货款已于上月支付。

4、用银行汇票支付采购材料价款,公司收到开户银行转来银行汇票多余款收账通知,通知上填写的多余款234元,购入材料及运费99 800元,支付的增值税额16 966元,原材料已验收人库,该批原材料计划价格100 000元。

5、销售产品一批,销售价款300 000元(不含应收取的增值税),该批产品实际成本180 000元,产品已发出,货款未收到。

6、公司将短期投资(全部为股票投资)15 000元兑现,收到本金15 000元,投资收益1 500元,均存入银行。

7、购入不需安装的设备1台,价款85 470元,支付的增值税14 530元,支付包装费、运杂费1 000元。

价款及包装费、运杂费均以银行存款支付。

设备已交付使用。

8、购入工程物资一批,价款150 000元(含已缴纳的增值税),已用银行存款支付。

9、工程应付工资200 000元,应付职工福利费28 000元,其他应交款100 000元。

10、工程完工,计算应予资本化的长期借款利息150 000元。

该项借款本息未付。

11、一项工程完工,交付生产使用,已办理竣工手续,固定资产价值1 400 000元。

12、基本生产车间1台机床报废,原价200 000元,已计提折旧180 000元,清理费用500元,残值收入800元,均通过银行存款收支。

该项固定资产已清理完毕。

13、从银行借入3年期借款400 000元,借款已存入银行账户,该项借款用于构建固定资产。

14、销售产品一批,销售价款700 000元,应收的增值税额119 000元,销售产品的实际成本420 000元,货款银行已收妥。

会计循环及会计业务流程讲解

会计循环及会计业务流程讲解会计循环是指会计工作的循环性质,包括会计核算循环和财务报告循环。

会计业务流程则是指在会计循环中,涉及到的具体会计业务的流程和步骤。

下面将对会计循环和会计业务流程进行详细讲解。

一、会计循环会计循环是指会计工作按照一定的时序和逻辑进行的循环性质,主要包括会计核算循环和财务报告循环。

1.会计核算循环会计核算循环是指会计从发生交易开始,到编制内部财务报表结束的全过程。

它包括以下几个步骤:(1)捕捉业务活动:会计核算循环的第一步是捕捉业务活动,即对企业内外部的交易和事件进行记录和登记。

这一步骤主要包括采集业务凭证和原始凭证的分析。

(2)分类和处理:捕捉业务活动之后,需要对其进行分类和处理。

即根据会计准则和规定,对业务活动进行分类,并进行账务处理,包括分录、核算、计算和归集等。

(3)编制财务报表:分类和处理之后,需要根据会计法规和财务会计准则,编制内部财务报表。

这一步骤包括编制资产负债表、利润表、现金流量表等报表。

2.财务报告循环财务报告循环是指财务报告的编制和发布的全过程。

它包括以下几个步骤:(1)财务报表编制:根据会计核算循环的结果,编制各类财务报表,如资产负债表、利润表、现金流量表等。

(3)财务报表发布:经过审核后,财务报表可以进行发布,向内外部利益相关方提供财务信息。

这一步骤包括制定发布计划、编制报表摘要、发布报表等。

二、会计业务流程会计业务流程是指在会计循环中,涉及到的具体会计业务的流程和步骤。

1.业务活动记录流程业务活动记录流程是指对企业内外部的交易和事件进行记录和登记的流程。

它包括以下几个步骤:(1)采集业务凭证:根据实际业务活动,采集相关的业务凭证和原始凭证。

(2)原始凭证分析:对采集到的业务凭证和原始凭证进行分析,理清业务活动的基本情况。

(3)凭证录入:根据原始凭证和分析情况,将相关数据录入会计系统,形成凭证。

2.会计核算流程会计核算流程是指对业务活动进行分类和处理的流程。

会计循环练习题

会计循环练习题一、选择题1. 会计循环的第一步是:A. 记录日记账B. 编制试算平衡表C. 编制财务报表D. 确定会计政策2. 以下哪项不是会计循环的组成部分?A. 确认B. 计量C. 报告D. 预测3. 在会计循环中,记录日记账的目的是:A. 记录交易的详细信息B. 确定交易的会计分录C. 编制财务报表D. 进行试算平衡4. 会计循环中,调整分录的目的是:A. 记录交易B. 调整账簿余额C. 编制试算平衡表D. 编制财务报表5. 会计循环的最终目的是:A. 编制日记账B. 编制分类账C. 编制财务报表D. 进行审计二、填空题6. 会计循环的四个主要步骤包括:________、________、________和________。

7. 会计循环中的调整分录通常发生在_________期末,用以调整_________。

8. 会计循环中,_________账是记录所有交易的初步记录。

9. 会计循环的最终产物是一套_________,包括资产负债表、利润表和现金流量表。

10. 会计循环中,_________是确保所有交易都被记录并且没有错误的一种方法。

三、简答题11. 简述会计循环的四个主要步骤,并解释每个步骤的作用。

12. 什么是调整分录?为什么在会计循环中需要进行调整分录?13. 会计循环中,为什么需要编制试算平衡表?试算平衡表的作用是什么?14. 会计循环中,财务报表的编制包括哪些内容?它们各自的作用是什么?15. 描述会计循环中,如何从原始凭证到财务报表的整个流程。

四、计算题16. 假设一家公司在2023年1月1日购买了价值10000元的办公用品,款项尚未支付。

请根据会计循环的步骤,列出该公司应该进行的会计分录。

17. 如果上述公司在2023年12月31日进行了年末调整,发现办公用品的使用寿命为12个月,需要进行折旧。

请计算折旧额,并列出相应的会计分录。

18. 假设上述公司在2023年12月31日的应收账款余额为20000元,估计坏账准备为1000元。

第三章会计循环1

制的差旅费报销单等。

第三章 会计循环

第二节 经济业务与会计凭证

会 计 学

第三章 会计循环

第二节 经济业务与会计凭证

会 计 学

第三章 会计循环

第二节 经济业务与会计凭证

会 计 学

第三章 会计循环

第二节 经济业务与会计凭证

外来原始凭证是指在经济业务发生或完成时, 从外部单位或个人取得的原始凭证。 会 例如,购买货物从销货单位取得的发货票、增 计 值税专用发票等。 学

第三章 会计循环

第二节 经济业务与会计凭证

会 计 学

第三章 会计循环

第二节 经济业务与会计凭证

会 计 学

第三章 会计循环

第二节 经济业务与会计凭证

(2)原始凭证按其填制手续和方法的不同,可

分为一次凭证、累计凭证、汇总原始凭证和记账

编制凭证。

一次凭证是指只反映一项经济业务,或者同时

会 计

反映若干项同类性质的经济业务,填制手续是一

制度的规定对原始凭证进行审核、对不真实、 不合法的原始凭证有权不予接受。并向单位负 责人报告;对记载不准确、不完整的原始凭证 予以退回,并要求按照国家统一的会计制度的 规定更正、补充。

第三章 会计循环

(二)记账凭证 记账凭证又称记账凭单,是指由会计人员根据审核无

误的原始凭证或汇总原始凭证编制的,用来确定会计分 录,作为登记账簿直接依据的会计凭证。 (1)记账凭证按其适用的经济业务,可分为专用记账凭

3.经济业务 内容摘要

大方公司记账凭证

22.填.填制制日日期期 和和编编号号

√

应交税费

4.应记帐户的名称和金额(会计分录)

23400

23400

7.有关责任人的签名或盖章

会计经验会计循环的基本步骤是什么

会计经验会计循环的基本步骤是什么会计循环的基本步骤包括:记录原始凭证、分类账簿、总账、试算平衡、调整分录、编制财务报表、检查和审计、结束报告、闭环。

1.记录原始凭证:会计循环的第一步是记录原始凭证。

原始凭证是指反映经济业务发生情况且能作为会计处理的依据,如收据、发票、合同等。

原始凭证的记录要求准确、完整、及时。

2.分类账簿:将原始凭证按照经济业务的性质和记账规则归类,分别记录在不同的分类账簿中。

常见的分类账簿包括现金日记账、银行存款日记账、应收账款账簿、应付账款账簿、固定资产账簿等。

3.总账:将分类账簿中的账务综合起来,按照会计科目的顺序进行汇总记录,形成总账。

总账是会计核算的基础,反映了企业在特定时期内的财务状况和经营成果。

4.试算平衡:在编制总账时,应对会计科目的借贷发生额进行试算平衡,即借贷双方金额是否相等。

如果不平衡,需要进行核对和调整,直到试算平衡。

5.调整分录:通过审查账簿和财务报表,发现存在未能准确反映和计量的事项,需要进行调整分录。

调整分录主要涉及预提费用、递延收益、无形资产摊销、坏账准备等。

6.编制财务报表:根据总账和调整分录,编制各种财务报表,包括资产负债表、利润表、现金流量表等。

财务报表是向外界展示企业财务状况和经营成果的重要工具。

7.检查和审计:对编制完成的财务报表进行检查和审计,确保其真实、准确、完整。

检查和审计的目的是发现和纠正可能存在的错误、欺诈和违规行为,保证财务报表的可靠性。

8.结束报告:在完成财务报表的检查和审计后,会计人员需要编制结束报告。

结束报告总结了会计循环的结果,包括财务状况、经营成果和问题与建议等内容。

9.闭环:会计循环的最后一步是闭环。

闭环是指将财务报表和结束报告反馈给企业管理者,作为管理决策和经营分析的重要参考依据。

同时,企业管理者也需要根据财务报表和结束报告提出相关决策和建议,促进企业的长期发展。

以上是会计循环的基本步骤,每个步骤都需要严格按照会计准则和规定进行操作,以确保会计信息的准确性和可靠性。

会计循环过程的具体内容

会计循环过程的具体内容会计循环过程是指在会计系统中进行日常业务处理的一系列步骤。

这个过程涉及到了多个环节,包括账务记录、分类、总账和试算平衡等。

以下是会计循环过程的具体内容,供参考。

1.业务发生会计循环过程的第一步是业务的发生。

这些业务可以是购买商品或服务、销售产品、支付工资、收取租金等。

每个业务都会产生会计凭证,用于记录相关的会计信息。

2.原始凭证记录原始凭证是记录业务发生的最初记录,如发票、收据、支票等。

在会计循环过程中,需要将原始凭证进行逐笔记录和编号,确保凭证的准确性和完整性。

这些原始凭证将成为后续会计处理的依据。

3.凭证录入在凭证录入阶段,会计人员将原始凭证中的信息转化为会计凭证,并将其输入到会计系统中。

每个会计凭证通常包含日期、摘要、借方金额和贷方金额等核心信息。

会计人员需要仔细检查每个会计凭证的录入准确性和完整性。

4.账务分类在凭证录入后,会计人员需要对会计科目进行分类。

会计科目是用于记录和汇总特定类型的交易和资金流动的账户。

根据事先设定的会计科目分类体系,会计人员将每个会计凭证中的借贷金额分别归类到相应的会计科目中。

5.总账总账是记录所有会计科目余额和交易明细的主要账簿。

在会计循环过程中,会计人员需要将每个会计凭证的分类信息和借贷金额更新到总账中的相应科目下。

这样可以确保每个会计科目的余额准确反映其收支情况。

6.辅助账簿除了总账外,会计人员还可能使用一些辅助账簿来记录特定的业务或账务细节。

例如,现金日记账用于记录现金交易,销售日记账用于记录销售收入和应收账款等。

这些辅助账簿帮助会计人员更好地管理和跟踪特定业务的相关信息。

7.试算平衡试算平衡是会计循环过程中的重要步骤之一。

在这一阶段,会计人员对总账和辅助账簿进行核对和平衡。

他们会计算每个会计科目的借贷差额,确保总账和辅助账簿之间的余额一致,并与总账平衡。

8.财务报表编制最后,会计人员使用总账和辅助账簿中的信息编制财务报表。

这些报表包括资产负债表、利润表和现金流量表等。

2第二章 会计分录与会计凭证

(二)会计凭证的分类

按填制的程序和用途的不同分为: 原始凭证 会计凭证 记账凭证

二、原始凭证及其填制与审核

原始凭证:是记录经济业务已经发生、执行或完成,用 以明确经济责任,作为记账依据的最初的书面证明文 件。

(一)原始凭证的种类

1、按取得的途径和来源不同,分为自制原始凭证和 外来原始凭证。 2、按填制手续的完成情况可分为一次原始凭证和累 计原始凭证。

例1:采购员预借差旅费2300元,以现金支付。 借:其他应收款 2300 贷:现金 2300

根据不同账户的结构计算填列下表空格数字:

账户名称 期初余额 现金 短期投资 应收票据 库存商品 短期借款 应付账款 应交税金 实收资本 1250 30000 ? 36000 23000 32000 2000 ? 本期发生额 期末余额 借方 贷方 1450 ? 1400 10000 15000 ? 4100 5600 900 ? 76000 22000 13000 20000 ? 12000 ? 40000 ? 1000 0 5000 10000 850000

账户名称 现金 短期投资 应收票据 库存商品 短期借款 应付账款 应交税金 实收资本

期初余额 250 30000 2400 36000 23000 32000 2000 845000

本期发生额 借方 贷方 1450 1300 10000 15000 4100 5600 62000 76000 13000 20000 12000 20000 3000 1000 5000 10000

期末余额=期初余额+本期增加发生额-本期减少发生额

第四节 复式记账

一、复式记账原理 (一)单式记账法 (二) 复式记账法 1、定义:复式记账法是对发生每一笔经济业 务所引起会计要素的增减变动,以相等的金额 同时在两个或两个以上相互联系的账户中进行 登记的方法。 2、产生:佛罗伦萨式、热那亚式、威尼斯式 3、 复式记账法的基本特征 1、会计记录的双重性 2、自成体系的全部账簿记录的平衡性

第11章 会计循环《基础会计》PPT课件

1.预收收入 预收收入是指企业本期或前期已收到现金并已入账,但 要待以后会计期间才能确认的收入。随着时间的推移,预收 收入会逐渐转为已实现的收入,因此,在会计期末要将已实 现的预收收入确认为本期收入,未实现的收入递延到以后各 期等待确认。

第二节 账项调整

(二)递延项目的调整 2.预付费用 预付费用是指本期或前期已付出现金,但受益期要延续

第一节 会计循环的含义与步骤

一、会计循环的含义

会计循环,是指企业在一ຫໍສະໝຸດ 会计期间内,从取得或填制 反映经济业务发生的原始凭证起,到编制出会计报表为止的 一系列会计处理程序。

二、会计循环的基本步骤

第二节 账项调整

一、账项调整的含义

账项调整,就是在每个会计期末结账前,按照权责发生 制原则对部分会计事项预以调整的行为。账项调整时所编制 的会计分录,就是调整分录。

二、应予以调整的项目

(一)应计项目的调整 1.应计收入 应计收入是指本期期末已获得但尚未收到款项的各种收入,

如应收租金、应收利息等。

第二节 账项调整

(二)递延项目的调整

所谓递延,就是指将已支付的费用或已收到的收入推迟 到以后期间予以确认。这些已经收到的收入即为预收收入, 已支付的费用即为预付费用。

会计循环1习题精选含答案

会计循环1习题精选含答案True / False Questions1. Accounts that appear in the balance sheet are often called temporary (nominal) accounts.FALSE2. Income Summary is a temporary account only used for the closing process. TRUE3. Revenue accounts should begin each accounting period with zero balances. TRUE4. Closing revenue and expense accounts at the end of the accounting period serves to make the revenue and expense accounts ready for use in the next period.TRUE5. The closing process takes place after financial statements have been prepared. TRUE6. Revenue and expense accounts are permanent (real) accounts and should not be closed at the end of the accounting period.FALSE7. Closing entries result in revenues and expenses being reflected in the owner's capital account.TRUE8. The closing process is a step in the accounting cycle that prepares accounts for the next accounting period.TRUE9. The closing process is a two-step process. First revenue, expense, and withdrawals are set to a zero balance. Second, the process summarizes a period's assets and expenses. FALSE10. Closing entries are required at the end of each accounting period to close all ledger accounts.FALSE11. Closing entries are designed to transfer the end-of-period balances in the revenue accounts, the expense accounts, and the withdrawals account to owner's capital. TRUE12. The Income Summary account is a permanent account that will be carried forward period after period.FALSE13. Closing entries are necessary so that owner's capital will begin each period with a zero balance.FALSE14. Permanent accounts carry their balances into the next accounting period. Moreover, asset, liability and revenue accounts are not closed as long as a company continues in business.FALSE15. The first step in the accounting cycle is to analyze transactions and events to prepare for journalizing.TRUE16. The accounting cycle refers to the sequence of steps in preparing the work sheet. FALSE17. The first five steps in the accounting cycle include analyzing transactions, journalizing, posting, preparing an unadjusted trial balance, and recording adjusting entries.TRUE18. The last four steps in the accounting cycle include preparing the adjusted trial balance, preparing financial statements and recording closing and adjusting entries. FALSE19. A classified balance sheet organizes assets and liabilities into important subgroups that provide more information to decision makers.TRUE20. An unclassified balance sheet provides more information to users than a classified balance sheet.FALSE21. Current assets and current liabilities are expected to be used up or come due within one year or the company's operating cycle whichever is longer.TRUE22. Intangible assets are long-term resources that benefit business operations that usually lack physical form and have uncertain benefits.TRUE23. Assets are often classified into current assets, long-term investments, plant assets, and intangible assets.TRUE24. Current liabilities are cash and other resources that are expected to be sold, collected or used within one year or the company's operating cycle whichever is longer.FALSE25. Long-term investments can include land held for future expansion.TRUE26. Plant assets and intangible assets are usually long-term assets used to produce or sell products and services.TRUE27. Current liabilities include accounts receivable, unearned revenues, and salaries payable.FALSE28. Cash and office supplies are both classified as current assets.TRUE29. Plant assets are also called fixed assets or property, plant, and equipment. TRUE30. The current ratio is used to help assess a company's ability to pay its debts in the near future.TRUEMultiple Choice Questions64. Another name for temporary accounts is:A. Real accounts.B. Contra accounts.C. Accrued accounts.D. Balance column accounts.E. Nominal accounts.65. When closing entries are made:A. All ledger accounts are closed to start the new accounting period.B. All temporary accounts are closed but not the permanent accounts.C. All real accounts are closed but not the nominal accounts.D. All permanent accounts are closed but not the nominal accounts.E. All balance sheet accounts are closed.66. Revenues, expenses, and withdrawals accounts, which are closed at the end of each accounting period are:A. Real accounts.B. Temporary accounts.C. Closing accounts.D. Permanent accounts.E. Balance sheet accounts.67. Which of the following statements is incorrect?A. Permanent accounts is another name for nominal accounts.B. Temporary accounts carry a zero balance at the beginning of each accounting period.C. The Income Summary account is a temporary account.D. Real accounts remain open as long as the asset, liability, or equity items recorded in the accounts continue in existence.E. The closing process applies only to temporary accounts.68. Assets, liabilities, and equity accounts are not closed; these accounts are called:A. Nominal accounts.B. Temporary accounts.C. Permanent accounts.D. Contra accounts.E. Accrued accounts.69. Closing the temporary accounts at the end of each accounting period:A. Serves to transfer the effects of these accounts to the owner's capital account on the balance sheet.B. Prepares the withdrawals account for use in the next period.C. Gives the revenue and expense accounts zero balances.D. Causes owner's capital to reflect increases from revenues and decreases from expenses and withdrawals.E. All of these.70. Journal entries recorded at the end of each accounting period to prepare the revenue, expense, and withdrawals accounts for the upcoming period and to update the owner's capital account for the events of the period just finished are referred to as:A. Adjusting entries.B. Closing entries.C. Final entries.D. Work sheet entries.E. Updating entries.71. The closing process is necessary in order to:A. calculate net income or net loss for an accounting period.B. ensure that all permanent accounts are closed to zero at the end of each accounting period.C. ensure that the company complies with state laws.D. ensure that net income or net loss and owner withdrawals for the period are closed into the owner's capital account.E. ensure that management is aware of how well the company is operating.72. Closing entries are required:A. if management has decided to cease operating the business.B. only if the company adheres to the accrual method of accounting.C. if a company's bookkeeper forgets to prepare reversing entries.D. if the temporary accounts are to reflect correct amounts for each accounting period.E. in order to satisfy the Internal Revenue Service.73. The recurring steps performed each reporting period, starting with analyzing and recording transactions in the journal and continuing through the post-closing trial balance, is referred to as the:A. Accounting period.B. Operating cycle.C. Accounting cycle.D. Closing cycle.E. Natural business year.74. Which of the following is the usual final step in the accounting cycle?A. Journalizing transactions.B. Preparing an adjusted trial balance.C. Preparing a post-closing trial balance.D. Preparing the financial statements.E. Preparing a work sheet.75. A classified balance sheet:A. Measures a company's ability to pay its bills on time.B. Organizes assets and liabilities into important subgroups.C. Presents revenues, expenses, and net income.D. Reports operating, investing, and financing activities.E. Reports the effect of profit and withdrawals on owner's capital.76. The assets section of a classified balance sheet usually includes:A. Current assets, long-term investments, plant assets, and intangible assets.B. Current assets, long-term assets, revenues, and intangible assets.C. Current assets, long-term investments, plant assets, and equity.D. Current liabilities, long-term investments, plant assets, and intangible assets.E. Current assets, liabilities, plant assets, and intangible assets.77. The usual order for the asset section of a classified balance sheet is:A. Current assets, prepaid expenses, long-term investments, intangible assets.B. Long-term investments, current assets, plant assets, intangible assets.C. Current assets, long-term investments, plant assets, intangible assets.D. Intangible assets, current assets, long-term investments, plant assets.E. Plant assets, intangible assets, long-term investments, current assets.78. A classified balance sheet differs from an unclassified balance sheet in thatA. a unclassified balance sheet is never used by large companies.B. a classified balance sheet normally includes only three subgroups.C. a classified balance sheet presents information in a manner that makes it easier to calculate a company's current ratio.D. a classified balance sheet will include more accounts than an unclassified balance sheet for the same company on the same date.E. a classified balance sheet cannot be provided to outside parties.79. Two common subgroups for liabilities on a classified balance sheet are:A. current liabilities and intangible liabilities.B. present liabilities and operating liabilities.C. general liabilities and specific liabilities.D. intangible liabilities and long-term liabilities.E. current liabilities and long-term liabilities.80. The current ratio:A. Is used to measure a company's profitability.B. Is used to measure the relation between assets and long-term debt.C. Measures the effect of operating income on profit.D. Is used to help evaluate a company's ability to pay its debts in the near future.E. Is calculated by dividing current assets by equity.81. The current ratio:A. Is calculated by dividing current assets by current liabilities.B. Helps to assess a company's ability to pay its debts in the near future.C. Can reveal problems in a company if it is less than 1.D. Can affect a creditor's decision about whether to lend money to a company.E. All of these.AACSB: CommunicationsAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: HardLearning Objective: A182. The Unadjusted Trial Balance columns of a company's work sheet show the balance in the Office Supplies account as $750. The Adjustments columns show that $425 of these supplies were used during the period. The amount shown as Office Supplies in the Balance Sheet columns of the work sheet is:A. $325 debit.B. $325 credit.C. $425 debit.D. $750 debit.E. $750 credit.83. A 10-column spreadsheet used to draft a company's unadjusted trial balance, adjusting entries, adjusted trial balance, and financial statements, and which is an optional tool in the accounting process is a(n) :A. Adjusted trial balance.B. Work sheet.C. Post-closing trial balance.D. Unadjusted trial balance.E. General ledger.84. Accumulated Depreciation, Accounts Receivable, and Service Fees Earned would be sorted to which respective columns in completing a work sheet?A. Balance Sheet or Statement of Owner's Equity-Credit; Balance Sheet or Statement of Owner's Equity Debit; and Income Statement-Credit.B. Balance Sheet or Statement of Owner's Equity-Debit; Balance Sheet or Statement of Owner's Equity-Credit; and Income Statement-Credit.C. Income Statement-Debit; Balance Sheet or Statement of Owner's Equity-Debit; and Income Statement-Credit.D. Income Statement-Debit; Income Statement-Debit; and Balance Sheet or Statement of Owner's Equity-Credit.E. Balance Sheet or Statement of Owner's Equity-Credit; Income Statement-Debit; and Income Statement-Credit.85. Which of the following statements is incorrect?A. Working papers are useful aids in the accounting process.B. On the work sheet, the effects of the accounting adjustments are shown on the account balances.C. After the work sheet is completed, it can be used to help prepare the financial statements.D. On the work sheet, the adjusted amounts are sorted into columns according to whether the accounts are used in preparing the unadjusted trial balance or the adjusted trial balance.E. A worksheet is not a substitute for financial statements86. A company shows a $600 balance in Prepaid Insurance in the Unadjusted Trial Balance columns of the work sheet. The Adjustments columns show expired insurance of $200. This adjusting entry results in:A. $200 decrease in net income.B. $200 increase in net income.C. $200 difference between the debit and credit columns of the Unadjusted Trial Balance.D. $200 of prepaid insurance.E. An error in the financial statements.87. Statements that show the effects of proposed transactions as if the transactions had already occurred are called:A. Pro forma statements.B. Professional statements.C. Simplified statements.D. Temporary statements.E. Interim statements.88. If in preparing a work sheet an adjusted trial balance amount is mistakenly sorted to the wrong work sheet column. The Balance Sheet columns will balance on completing the work sheet but with the wrong net income, if the amount sorted in error is:A. An expense amount placed in the Balance Sheet Credit column.B. A revenue amount placed in the Balance Sheet Debit column.C. A liability amount placed in the Income Statement Credit column.D. An asset amount placed in the Balance Sheet Credit column.E. A liability amount placed in the Balance Sheet Debit column.89. If the Balance Sheet and Statement of Owner's Equity columns of a work sheet fail to balance when the amount of the net income is added to the Balance Sheet and Statement of Owner's Equity Credit column, the cause could be:A. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Debit column.B. A revenue amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.C. An asset amount entered in the Income Statement and Statement of Owner's Equity Debit column.D. A liability amount entered in the Income Statement and Statement of Owner's Equity Credit column.E. An expense amount entered in the Balance Sheet and Statement of Owner's Equity Credit column.Problems129. In the table below, indicate with an "X" in the proper column whether the account is a (nominal) temporary account or a (real) permanent account.132. Based on the adjusted trial balance shown below, prepare a classified balance sheet for Focus Package Delivery.* $2,000 of the long-term note payable is due during the next year.135. Use the following partial work sheet from Matthews Lanes to prepare its income statement, statement of owner's equity and a balance sheet (Assume the owner did not make any investments in the business this year.)137. A partially completed work sheet is shown below. The unadjusted trial balance columns are complete. Complete the adjustments, adjusted trial balance, income statement, and balance sheet and statement of owner's equity columns.。

会计循环和会计核算形式

凭证 收、付、转账凭证和汇总记账凭证 账簿 同前 三、流程p317 四、适用范围 优点 减少了登记总账的工作量;汇总记账凭证能够反映 出账户之间的对应关系,便于分析和检查经济业务的发生 情况。 缺点 转账业务较多时,编制汇总记账凭证的工作量大; 经济业务较少的单位如果采用这种方法,会加大工作量。 适用范围 规模大、经济业务量较多的单位。

三、会计核算形式的种类 在我国,常用的会计核算形式有:

记账凭证核算形式 科目汇总表核算形式 汇总记账凭证核算形式 日记总帐核算形式

第三节 记账凭证核算形式 一、记账凭证核算形式的概念和特点 记账凭证核算形式,是根据记账凭证直,都是以它为基础发展演变而成的。 特点 记账凭证无需通过汇总,直接逐笔登记总分类账。

并过入相应的分类账,再进行第二次试算平衡。 第六步,进行财产清查、对账,作出结账分录,结清所有收入、费用等虚账户。 第七步,编制会计报表。

一个完整的会计循环过程,至少要编制三次试算平 衡表: 第一次 在根据有关记账凭证登记分类账后进行的, 称之为调整前试算; 第二次是在期末的调整分录登账以后进行的试算平衡, 称之为调整后试算; 第三次是在结账后即结清所有虚账户后进行的试算。 在实际工作中,这些试算表是通过工作底稿来完成的。 常用的工作底稿的格式如下:

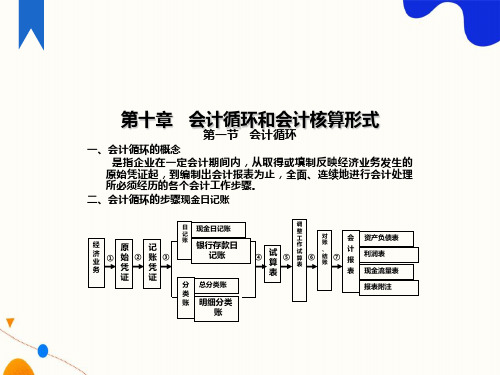

第十章 会计循环和会计核算形式

第一节 会计循环

一、会计循环的概念

是指企业在一定会计期间内,从取得或填制反映经济业务发生的 原始凭证起,到编制出会计报表为止,全面、连续地进行会计处理 所必须经历的各个会计工作步骤。

第108讲第29章会计循环-第1节及第2节

第二十九章 会计循环【本章考情分析】【本章教材结构】【本章考点详解】第一节 会计确认【本节知识点】【知识点1】会计确认主要解决的问题及一般标准【本节知识点详解】【知识点1】会计确认主要解决的问题及一般标准会计上将按照确认、计量、记录和报告为主要环节的会计基本程序及相应的方法称为会计循环。

会计确认是会计数据进入会计系统时确定如何进行记录的过程,即将某一会计事项作为会计要素正式列入会计报表的过程。

会计确认主要解决三个问题:1.确定某一经济业务是否需要进行确认;2.确定该业务应在何时进行确认;3.确定该业务应确认为哪个会计要素。

会计确认的三大标准:1.被确认的项目是通过经济业务活动所产生的,其交易性质符合会计要素的要求。

2.与该项目有关的未来经济利益流入或流出企业的不确定性能明确的评估;3.该项目应有可以计量的属性,如价值、成本等,并能可靠的进行计量【提示】根据上述标准,在确认收入时,应当及时、并坚持权责发生制;在确认费用时,应按照收入和对应发生的费用配比的要求操作。

确认收入和费用时需要在“持续经营”“会计分期”前提下,按照权责发生制要求来合理确认,即收入的确认要建立在取得收入权利的交易或事项发生时,费用的确认应是在承担费用的交易或事项出现时。

相应地,资产的确认要建立在取得资产所有权的交易发生之时,负债的确认要建立在确认负债成立的有关业务发生时。

可见,权责发生制构成了确认收入和费用的基础,也进一步构成了资产和负债的确认基础。

例题精讲【真题•2011多选】会计确认主要解决的问题包括()。

A.确定某一经济业务是否需要进行确认B.确定一项经济业务的货币金额C.确定某一经济业务应在何时进行确认D.确定某一经济业务应确认为哪个会计要素E.为编制财务报告积累数据【答案】ACD【解析】通过本题掌握会计确认需解决的三个问题,即是否需要确认、何时确认及确认在哪个要素中。

本题B选项是会计计量的含义;E选项是会计记录的含义。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计循环--财务会计的日常程序与方法Part I 教材导读(供预习使用)一.名词解释会计循环账户会计科目过账对账结账总分类账户明细分类账户永久性账户临时性账户复式记账法借贷记账法会计分录会计凭证原始凭证记账凭证生产成本累计折旧盈余公积利润分配会计账簿序时账簿辅助账簿平行登记二、判断题1、对于一个新创办的企业来说,会计循环程序开始于设置明细账。

()2、某企业期初资产总额100万元,本期取得借款6万元,收回应收账款7万元,用银行存款8万元偿还应付款,该企业期末资产总额为105万元。

()3、会计准则是会计核算的规范,是企业进行价值确认、计量、记录和报告必须遵循的标准。

()4、不能编制多借多贷的会计分录。

()5、企业可根据实际情况自行设计会计科目。

()6、更正错账的方法一般有三种:划线更正法、红字更正法和补充登记法。

()7、“有借必有贷,借贷必相等”是复式记账法的记账规则。

()8、企业已经预付,但应由本期和以后各期分别负担的费用称为预提费用。

()9、借贷记账法,借方表示增加,贷方表示减少,余额在借方。

()10、资产、负债和所有者权益之间,在任何情况下都保持平衡。

()11、原始凭证是记账凭证的填制依据,记账凭证是编制报表的直接依据。

()12、登账后,结账前或后发现据以登记的记账凭证应记科目和(或)金额发生错误,因此账簿记录也错误,此时,应采用划线更正法进行改正。

()13、现金日记账只需根据现金收、付款凭证填制。

()14、“生产成本”账户属于资产类账户,用来归集和分配产品生产过程中发生的各项生产费用,正确地计算产品生产成本。

()Part II 练习提高一、单项选择1、在会计实务中,记账凭证按其所反映的经济内容不同,可以分为()A、单式凭证和复式凭证B、通用凭证和专用凭证C、收款凭证,付款凭证和转证凭证D、一次凭证,累计凭证和汇总凭证2、账户的对应关系是指(D)A、总分类账与明细分类账之间的关系B、总分类账与日记账之间的关系C、总分类账与备查账之间的关系D、有关账户之间的应借应贷关系3、下列项目中不属于产品成本项目的有()A、直接材料B、制造费用C、直接人工费D、管理费用4、“借贷”记账符号表示()A 、债权债务关系的变化 B、记账金额 C、平衡关系 D、记账方向5、不属于长期资产的是()A、交易性金融资产B、长期投资C、固定资产D、无形资产6、企业用银行存款购买原材料,则企业资产()。

A、增加B、减少C、不变D、无法确定7、“应付账款”账户的期初余额为8 000元,本期增加额为12 000元,期末余额为6 000元,则该账户本期减少额为()。

A、10 000B、14 000C、2 000D、4 0008、在会计核算中,运用复式记账、填制会计凭证、登记账簿和编制报表等环节,都要以()为依据。

A、会计科目B、账户C、总分类账D、一级科目9、下列各项属于流动负债的是()。

A、应付债券B、预收账款C、预付账款D、其他应收款10、某会计人员根据记账凭证登记入账时,发现记账凭证的金额错误,实际金额大于记账凭证上记录的金额,那么会计人员应采用( C)更正错误。

A.划线更正法B. 红字更正法C.补充登记法D.编制相反分录冲减11、某会计人员根据记账凭证登记入账时,误将1000元填写为10000元,而记账凭证没有错误,应采用的更正方法为(C)。

A.红字更正法B.补充登记法C.划线更正法D.蓝字更正法12、以下选项中不属于账账核对的有()。

A.银行存款日记账余额和银行对账单的核对B.银行存款日记账余额与其总账的核对C.总账借方发生额合计数与其明细账借方发生额合计数的核对D.总账账户贷方余额与其明细账户贷方余额的核对13、企业采取永续盘存制时,财产清查的主要目的是()。

A.检查账实是否相符B.检查账证是否相符C.检查账账是否相符D.检查账表是否相符14、存货在财产清查中发现短缺,那么批准处理前应记入()。

A.待处理财产损溢B.期间费用C.营业外支出D.其它应收款15、各种账务处理程序的主要区别在于()。

A.登记总账的依据不同B.登记日记账的依据不同C.登记明细账的依据不同D.编制会计报表的依据不同16、某企业六月份销售甲产品一批,取得商业承兑汇票一张,价款10 000元,销售乙产品一批,取得转账支票一张,价款5 000元,收到5月份欠货款5 000元,按收付实现制确定该企业六月份销售收入(C )A.20 000B.15 000C.10 000D.5 00017、根据借贷记账法的账户结构,账户借方登记的内容有()。

A.收入的增加B.所有者权益的增加C.费用的增加D.负债的增加18、费用(成本)类账户的结构与资产类账户的结构()。

A.一致 B.相反 C.无法确定 D.无关19、“应收账款”账户的期初余额为7 000元,本期借方发生额为5 000元,本期贷方发生额为9 000元,该账户期末余额为()元。

A.3 000 B.12 000 C.16 000 D.14 00020、下列各项中,不属于原始凭证要素的是()。

A.经济业务发生日期 B.经济业务内容C.会计人员记账标记 D.原始凭证附件21、企业销售库存商品一批,商品已经发出,货款已存入银行,根据这笔业务的有关原始凭证应该填制的记账凭证是()。

A.收款凭证 B.付款凭证C.转账凭证 D.累计凭证22、下列各项,属于累计凭证的是()。

A.工资费用分配表 B.领料单C.进料单 D.限额领料单23、下列做法中,不符合《会计基础工作规范》规定的是()。

A.外来原始凭证金额错误,需要由原出具单位重新开具B.结账前凭证正确,账簿记录金额错误,可以采用“划线更正法”予以更正C.自制原始凭证须经办人签名或盖章D.销售商品3510.23元,销货发票大写金额为:叁仟伍佰壹拾元贰角叁分整24、原始凭证不得涂改、刮擦、挖补。

对于金额有错误的原始凭证,正确的处理方法是()。

A.由出具单位在凭证上更正并由经办人员签名B.由出具单位重开C.由出具单位在凭证上更正并由出具单位负责人签名D.由出具单位在凭证上更正并加盖出具单位印章25、对于真实、合法、合理但填写有错误的原始凭证,按规定应()。

A.拒绝办理会计手续 B.自行更正后办理会计手续C.上报有关部门 D.退回重新填制26、下列明细账中,应采用多栏式明细分类账的是 ( )。

A. 管理费用明细账B. 库存商品明细账C. 原材料明细账D. 固定资产明细账27、下列各明细分类账,可以采用定期汇总登记方式的是()。

A.固定资产 B.预付账款C.预收账款 D.库存商品28、在结账前发现账簿记录有文字或数字错误,而记账凭证没有错误,可以采用()。

A.划线更正法 B.红字更正法 C.补充登记法 D.使用褪色药水29、根据《会计档案管理办法》,企业应当永久保管的会计档案为()。

A.日记账 B.明细账C.会计移交清册D.会计档案保管清册30、某企业在遭受洪灾后,对其受损的财产物资进行的清查,属于()。

A.局部清查和定期清查 B.全面清查和定期清查C.局部清查或不定期清查 D.全面清查和不定期清查二、多项选择1、在借贷记账法下,账户贷方记录的内容是()。

A、资产的增加B、资产的减少C、负债及所有者权益的增加D、负债及所有者权益的减少E、收入的减少及费用的增加2、以下()事项,属于企业收入。

A、售后回购方式下销售商品的经济利益流入B、提供劳务的经济利益流入C、出租固定资产的经济利益流入D、出售固定资产的经济利益流入3、企业在编制财务报表之前,应完成()工作。

A、账项调整B、对账C、调整未达账项D、结账4、下列项目中,应作为企业长期资产核算和管理的有()。

A、购入准备随时变现的股票B、购入生产用机器C、购入准备持有至到期的债券投资D、购入办公用文具E、购入准备出售的商品5、以下( )不会影响借贷的平衡关系。

A.重记某项业务B.漏记某项业务C.颠倒借贷方向D.某项经济业务记错账户6、通常情况下,企业销售商品的出库单应传递的部门有( )。

A.销售部门B.行政部门C.会计部门D.仓库E.生产部门7、以下业务企业应该在备查账簿中记录的有( )。

A.发行股票的股数,股东所占的比例B.企业经营租赁租入的固定资产C.固定资产的使用期限D.应收票据的种类和金额8、任何会计主体都必须设置的账簿有()。

A.现金日记账 B.银行存款日记账C.总分类账簿 D.备查账簿E.明细分类账簿9、数量金额式明细分类账的账页格式适用于()。

A.库存商品明细账 B.应交税金明细账C.应付账款明细账 D.原材料明细账E.应收账款明细账10、下列表格可以作为原始凭证的有(ABD)。

A.实存账存对比表B.现金盘点报告表C.未达账项登记表D.结算款项合计登记表E.银行存款于额调节表11、采用明细分类账登记的依据是()。

A.原始凭证 B.汇总记账凭证C.记账凭证 D.经济合同E.购销协议12、下列各项工作以会计等式为理论基础的是()。

A.复式记账 B.成本计算C.编制资产负债表 D.试算平衡13、下列各项中,不属于账户的对应关系的是()。

A.总分类账户与明细分类账户之间的关系 B.有关账户之间的应借应贷关系C.资产类账户与负债类账户之间的关系 D.成本类账户与损益类账户之间的关系14、复式记账凭证的优点有()。

A.能全面反映账户的对应关系 B.便于按会计科目进行汇总C.有利于检查会计分录的正确性 D.便于分工记账15、下列错误中,无法通过试算平衡发现的有()。

A.一项经济业务被漏记了贷方金额 B.借贷双方同时少计了金额C.借方多计了金额 D.应借应贷科目的方向颠倒16、下列经济业务中,不应填制转账凭证的是()。

A.用银行存款偿还短期借款 B.收回应收账款C.用现金支付工资 D.生产领用原材料17、按照用途不同,账簿可以分为()。

A.序时账簿 B.分类账簿C.备查账簿 D.数量金额式18、下列明细账中,应采用数量金额式明细分类账的是 ( )。

A.库存商品明细账 B.包装物明细账C.原材料明细账 D.管理费用明细账19、下列各项,( ) 的单位适宜设置普通日记账。

A.规模较大,业务量较多但较为简单 B.规模较大,业务量较多且较复杂C.规模较小,业务量较多但较为简单 D.规模较小,业务量较少20、下列各项,属于应收票据对账内容的是()。

A.应收票据账簿记录与其会计凭证的核对B.应收票据明细账与总账的核对C.应收票据账簿记录与对方单位账簿记录的核对D.应收票据账簿记录与本单位销售收入总额的核对21、账簿按其外形特征的不同,可以为()。

A.订本账 B.活页账 C.序时账 D.卡片账22、在下列各类错账中,应采用红字更正法进行更正的错账有()。

A.记账凭证没有错误,但账簿记录有数字错误B.因记账凭证中的会计科目有错误而引起的账簿记录错误C.记账凭证中的会计科目正确但所记金额大于应记金额所引起的账簿记录错误D.记账凭证中的会计科目正确但所记金额小于应记金额所引起的账簿记录错误23、根据《会计档案管理办法》,企业应当永久保管的会计档案为()。