欧洲非上市企业采用国际财务报告准_省略_与启示_基于英国和德国的实证分析_杨丹

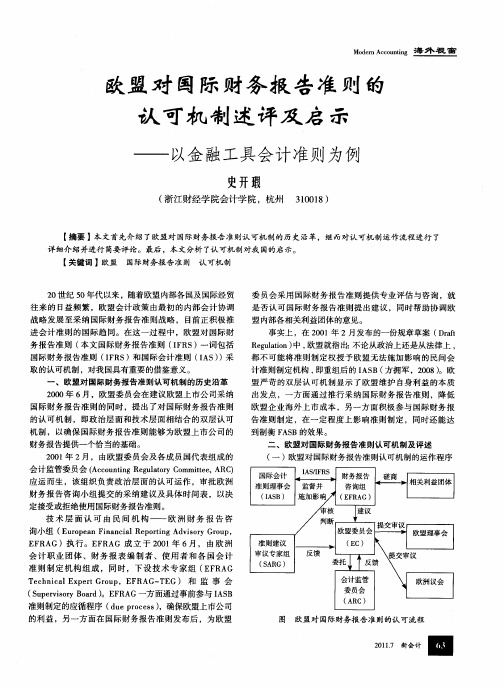

欧盟对国际财务报告准则的认可机制述评及启示——以金融工具会计准则为例

欧盟对国际财务报告准则的认可机制述评及启示——以金融工具会计准则为例首先,欧盟的认可机制能够提高国际财务报告准则的可信度和权威性。

欧盟作为全球最大的经济体之一,对IFRS的采用和应用给予认可,将为其他国家和地区奠定了一个权威的基准。

这不仅对欧盟内部企业来说具有重要意义,也为全球范围内的企业提供了一个参考。

其次,欧盟的认可机制能够促进国际财务报告准则的一致性和稳定性。

欧盟对IFRS的认可需要进行详细的审核和评估,以确保IFRS与欧盟内部的法规和要求相一致。

这种一致性和稳定性有助于减少不同国家和地区之间在财务报告中出现的差异,提高了跨境投资的透明度和稳定性。

另外,欧盟的认可机制还起到了监管和监督的作用。

欧盟对IFRS的审核和评估将确保财务报告的准确性和透明度,并可以对违反报告准则的企业采取相应的法律措施。

这将帮助维护欧盟内部市场的秩序和公平竞争,保护投资者的权益。

然而,欧盟对国际财务报告准则的认可机制也存在一些问题和挑战。

首先,审核和评估流程可能较为复杂和耗时,需要大量的人力和物力投入。

其次,不同国家和地区对IFRS的理解和应用可能存在差异,会导致一些争议和误解。

再次,IFRS的更新和变化较为频繁,需要及时跟进和调整。

最后,欧盟的认可机制虽然能够提高财务报告的准确性和透明度,但是否能完全避免欺诈行为仍然存在一定的风险。

对于其他国家和地区,欧盟对国际财务报告准则的认可机制提供了一些有益的启示。

首先,需要建立起一个权威和可信的组织或机制来对国际财务报告准则进行审核和评估。

其次,强调一致性和稳定性是确保财务报告准确、透明和可比性的重要因素。

再次,要加强监管和监督机制,对违反报告准则的企业采取相应的法律措施。

最后,需要及时跟进和调整准则,以适应不断变化的经济环境和市场需求。

总而言之,欧盟对国际财务报告准则的认可机制为保障财务报告的准确性、透明度和可比性提供了重要保障,同时也存在一些挑战和问题。

其他国家和地区可以通过借鉴欧盟的经验和做法,建立起一个有效的审核和评估机制,提高财务报告的质量和可信度。

国外政府财务信息披露的借鉴与启示

国外政府财务信息披露的借鉴与启示作者:王冰洁殷文玺胥辰辰来源:《知识文库》2019年第11期政府财务报告既是国家决策机关和政府主管部门作出宏观经济决策、制定公共政策、进行公共管理的重要信息来源,也是政府外部的利益相关者了解政府财务状况、衡量政府绩效并作出相关决策的重要信息来源。

本文分析了具有代表性的发达国家进行财务信息披露改革的具体实践,并探讨了发达国家政府财务信息披露体系值得我国学习和借鉴的地方。

1.1 法国法国采用日历年度作为财政年度,每年10月初到12月中旬,两院国会对财政部编制的下一年度预算案《财政法》进行审议通过,然后中央政府各项财政收入和支出都要依据《财政法》执行。

中央政府预算采用收付实现制基础编制,会计采用修正的收付实现制基础,预算和会计在分类上有较大不同。

财政部主要负责编制预算、税收征管、收付现金与会计核算,不同法国财政部内也设有国库司,其主要职能是管理中央政府的投资,组织和监督金融市场、保险市场等。

在法国政府会计系统之中,支出单位自行进行会计记录,另外政府也会分派会计师是进行记录,二者分开独立,互不影响。

公共部门在预算支出时一般分为四个步骤进行:承诺、发票核对、委托支付和支付。

由于国会无法完全地控制预算的形成和执行,加上不断增长公共支出,因此要求财政提高透明度,进行中央政府预算和会计改革的呼声越发强烈。

2001年8月颁布的新法案提出,法国中央政府将建立预算会计系统、财务会计系统以及成本会计系统。

三种会计系统将目前的收付实现制与新引入的权责发生制相结合,对所有政府经济活动进行核算,大部分政府业务以权责发生制为基础,同时强化了政府成本管理和费用核算。

法国中央政府每年要向国会提交一套完整的年度财政管理总报告,其中包含中央政府预算执行表和中央政府财务报表(资产负债表、净收益表、附注)。

法国地方政府的改革先行一步,目前市镇已经基本完成了预算和会计的权责发生制改革,地方政府会计改革主要是为了实现三方面目标:①技术性改进;②改进财务报表的内容;③改进财务分析工具。

采用国际会计准则财务报表的影响:德国的情况【外文翻译】

外文翻译Financial statement effects of adopting international accounting standards: the case of Germany Material Source: /Author: Mingyi Hung· K. R. Subramanyam1 IntroductionAs of January 1, 2005, all listed companies in the European Union are required to prepare their financial statements in accordance with International Accounting Standards (IAS) (Hofheinz 2002). IAS adoption by the European Union is one of the biggest events in the history of financial reporting, making IAS the most widely accepted financial accounting model in the world. Accordingly, there is an urgent need for managers and investors to understand the implications of IAS adoption. This is especially true in European countries with stakeholder-oriented accounting systems (such as Germany and France), as IAS is heavily influenced by the shareholder-oriented Anglo-Saxon accounting model, whereas local standards in many European countries have a greater contracting orientation and are driven by tax-book conformity considerations.The objective of our paper is to examine the financial statement effects of adopting IAS in European countries with stakeholder-oriented accounting systems. We conduct our investigation using a sample of 80 German firms that adopt IAS for the first time during the 1998 through 2002 period. Specifically, we investigate the effects of IAS adoption on financial statements by (1) documenting the financial statement changes precipitated by IAS adoption and (2) examining the effects of these changes on the properties of financial statement information. Examining financial statement implications is important because, while IAS adoption might lead to indirect economic consequences such as higher market liquidity or lower cost of capital, the only direct effects of adopting IAS are changed financial statements (and related footnote disclosures).We limit our investigation to Germany primarily to overcome problems associated with comparing across countries with different institutional environments. In addition, Germany is particularly well suited for our empirical investigation for several reasons. First, Germany provides an ideal natural experiment for examiningthe financial statement effects of IAS adoption in countries with stakeholder-oriented accounting systems because, unlike IAS, German CAAP or the German Commercial Code (Handelsge.setzbuch; henceforth, HGB) emphasizes a "prudent" approach to asset valuation and liability recognition to facilitate contracting among stakeholders (Harris et al. 1994; Leuz and Wustemann 2004).2 Second, because Germany has a strong rule of law tradition and an efficient judicial system, we can be assured that there is adequate enforcement of accounting rules (La Porta et al. 1998).3 Third, a relatively large number of German companies have adopted IAS, which provides us a reasonably large sample.4Our research design allows us to directly compare accounting numbers (and their properties) prepared under HGB with those prepared under IAS. A direct comparison is possible because German firms adopting IAS are required to restate their prior-year results under IAS during the adoption year; that is, IAS-adopting firms are required to issue financial statements prepared under both IAS and HGB for the year before adoption. Accordingly, our research design controls for cross-sectional and time-series differences between IAS and HGB firm-years. In addition, we restrict our sample to firms adopting IAS in 1998 or thereafter. Two important events occurred in 1998: (1) the core IAS standards were completed, and (2) IAS adopters were mandated to fully comply with the IAS standards (before 1998, companies could choose to implement only a subset of IAS standards). 5 Hence, examining post-1997 adoptions ensures that our IAS firm-years are representative.Our empirical investigation comprises two basic sets of analyses. Our first set of analyses documents the major accounting differences between HGB and IAS as well as the effects of IAS adoption on key accounting measures such as book value of equity and net income. Based on the book value and net income reconciliation adjustments that a subset of our sample firms report in their annual reports, we find that switching to IAS results in widespread and significant changes to deferred taxes, pensions, PP&E, and loss provisions. In addition, we find that total assets and book value of equity are significantly larger under IAS than under HGB and that cross-sectional variation in book value and net income are significantly higher under IAS than under HGB. Overall, our results are consistent with HGB emphasizing the prudence principle (balance sheet conservatism) and income smoothing-for example, limited recognition of assets and frequent use of discretionary loss provisions-and IAS emphasizing fair values and balance sheet valuation-for example,the use of fair value for financial instruments and recognition of internally developed intangibles.Our second set of analyses investigates the effects of IAS adoption on the relative and incremental value relevance of book values and net income as well as the asymmetric timeliness of net income. Since our sample companies voluntarily adopt IAS and therefore do not represent a random selection of German firms, we implement the two-stage regression procedure suggested by Heckman (1979) to control for the effect of self-selection in these tests. We measure value relevance in terms of the ability of accounting measures to explain contemporaneous stock prices. Our relative value relevance analysis finds no evidence that IAS improves the value relevance of book value or net income. However, we find that book value (net income) is accorded a significantly larger (smaller) valuation coefficient under IAS than under HGB, consistent with IAS markedly reducing income persistence (Ohlson 1995). In addition, our incremental value relevance results show that while the IAS adjustments to book value are value relevant, they add noise (measurement error) to income. Overall, our value relevance results are consistent with IAS being balance sheet- and fair value-orientated and HGB being income smoothing- and historical cost-oriented.Finally, we compare the timeliness and asymmetric timeliness of income measured under HGB and IAS. As in Ball et al. (2000), we estimate both timeliness and asymmetric timeliness (conditional conservatism) by regressing income on returns interacted with a variable that measures the sign of returns. Our results are consistent with IAS recognizing economic losses in a timelier manner than HGB, which suggests that IAS income is more conditionally conservative than its HGB counterpart. However, these results are not statistically significant.Two factors could potentially bias our results. First, we conduct our analyses in the year before IAS adoption, when IAS numbers are unavailable to the market. It is possible that our results are driven by the inability of the market to price IAS information at the time we conduct our tests. Accordingly, we conduct additional analyses using future prices and returns as proposed by Aboody et al. (2002). The results of these analyses suggest that the unavailability of IAS information is not likely to affect our inferences. Second, it is possible that our sample companies gradually narrowed differences between HGB and IAS before IAS adoption that is, gradually transitioned to IAS, potentially lowering the power of our tests (Barth et al. 2005). However, our additional analyses find little evidence of such gradualtransition, which suggests that our results are robust to this alternative explanation.' Our paper's primary contributions to the literature are threefold. First, we provide evidence on the likely financial statement effects of IAS adoption throughout the European Union, arguably one of the biggest events in the history of financial reporting. Unlike Barth et al. (2005), who study a large sample of firms from many different countries, we conduct a detailed examination on a small sample of German firms that voluntarily adopt IAS using a design that provides superior experimental control.Second, we contribute to the literature examining the valuation properties of IAS (for example, Ashbaugh and Olsson 2002; Harris and Muller 1999) by focusing our investigation on the period after both the adoption of the core standards by the IASC and the requirement of full compliance. Thus, our paper is arguably the first to examine the financial statement effects of truly representative IAS. Consequently, we are the first to document the substantial fair-value orientation of IAS and its implications for the value relevance and timeliness of financial statement information.Third, we contribute to the debate on the relative superiority of the Anglo- Saxon shareholder-oriented versus the continental European stakeholder-oriented accounting models. Prior studies using cross-country comparisons conclude that the shareholder-oriented model is more value relevant (Ali and Hwang 2000) but are unable to disentangle the effects of accounting standards from other institutional factors such as shareholder protection or market development. In contrast, we implement a design that allows us to examine the effects of accounting differences under a ceteris paribus condition and find no significant differences in value relevance between stakeholder-oriented (HGB) and share- holder-oriented (IAS) accounting models, although we do find suggestive evidence that IAS income may recognize economic losses in a timelier manner. While speculative in nature, our results are consistent with Ball et al. (2003), who show that institutional factors such as shareholder protection may play a more important role than accounting standards in explaining cross-country variation in the valuation properties of accounting data.The rest of the paper proceeds as follows. Section 2 describes the sample. Section 3 discusses accounting differences between HGB and IAS. Section 4 presents our procedure to correct for potential self-selection bias. Section 5 provides the results on the value relevance of HGB and IAS measures, while Section 6examines differences in asymmetric timeliness. Section 7 discusses several robustness tests. Finally, Section 8 concludes.The average effects of net income reconciliation items are generally in the same direction as those of book value reconciliation items, except for the adjustments related to provisions and deferred taxes. We note that the accounting differences do not necessarily change book value and net income in the same direction because book value captures the cumulative effect of accounting differences whereas net income captures the effect during the fiscal year. For example, while the change from tax-based accelerated depreciation methods to straight-line depreciation methods will increase book value of PP&E and therefore increase book value of equity, it will generally decrease (increase) depreciation expense and therefore increase (decrease) net income in the earlier (later) stage of PP & E's useful life.Since the net income adjustments result from the same accounting differences described in Sect. 3.1.1, we only provide a brief description of the five most frequent adjustment items: Deferred Taxes. As expected, deferred taxes represent the most frequent net income adjustment item, reported in 81% of observations. In addition, IAS expense adjustments related to defer taxes on average reduce net income by, 7 million. Property, Plant, and Equipment (PP&E) IAS adjustments related to PP&E on average increase net income by, 19 million, indicating a decrease depreciation expense related to PP&E during the reporting period. Leases, IAS adjustments related to leases on average increase net income by, 28 million, indicating a decrease in expenses (such as interest and depreciation expenses related to the lease) during the reporting period Pensions. While IAS adjustments related to pensions are relatively frequent, the average effect on net income is miniscule (the mean and median are both less than one Euro million). The small effect in net income suggests that most of the increase in pension liability is reflected in its opening balance for the reporting period, Goodwill.IAS adjustments related to goodwill on average increase net income by €2 million, indicating a decrease in goodwill amortization expense during the reporting period.译文采用国际会计准则财务报表的影响:德国的情况资料来源:/作者:MingyiHung·K.R.Subramanyam1 简介截至2005年1月1日,在欧洲联盟的所有上市公司被要求准备依据国际会计准则(IAS)(霍夫海因茨2002)来编制其财务报表。

欧盟对国际财务报告准则的认可机制述评及启示——以金融工具会计准则为例

委员会采用国际财务报告准则提供专业评估与咨询 ,就

是 否认 可 国际财 务 报 告准 则 提 出建 议 , 同时 帮助 协 调欧 盟 内部 各相 关利 益 团体 的意 见 。 事 实上 ,在 2 0 年 2月 发布 的一份规 章草 案 ( r t 01 D a f

进会计准则的国际趋同。在这一过程 中,欧盟对 国际财

的意见 , 并就是否予以认可和采纳 向E 提出建议 。 C 同时 , E R G与 E F A C合作 ,就既定会计 准则在欧洲的潜在经

T c nc l x et o p F e h ia p r Gr u ,E RAG— E E T G) 和 监 事 会

准—一I 则—( 交 建— 审 议 I lE 及C 议 馈) —\ 三

会计 监管

委员会 ( C) AR

欧洲议会

( u evsr or F A S p ri yB ad oE R G一 方面通 过事 前参 与 I S o AB

务报 告 准则 ( 文 国际财 务报 告 准 则 (F S 一 词包 括 本 IR ) 国际 财务 报 告准 则 ( F S I R )和 国际会 计 准则 (A ) 采 IS )

R gl i ) , euao 中 欧盟就指出: tn 不论从政治上还是从法律上 , 都不可能将准则制定权授予欧盟无法施加影响的民间会 计 准则 制定 机构 , 即重组 后 的 I S 方拥 军 ,20 ) A B( 0 8 。欧

详 细介 绍并进行 简要评 论 。最后 ,本 文分析 了认 可机 制对 我 国的启示 。

【 关键词 】 欧盟

国际财务报告准则 认可机制

2 世纪 5 年代 以来 ,随着欧盟内部各国及国际经贸 O O

往来 的 日益 频 繁 ,欧盟 会 计政 策 由最初 的 内部会 计 协 调 战 略发 展 至 采纳 国际 财务 报 告 准则 战 略 , 目前正 积 极 推

1.1 强制采用国际财务报告准则对欧洲权益资本成本的影响

Certified Accountants Educational Trust (London)

The Council of the Association of Chartered Certified Accountants consider this study to be a worthwhile contribution to discussion but do not necessarily share the views expressed, which are those of the authors alone. No responsibility for loss occasioned to any person acting or refraining from acting as a result of any material in this publication can be accepted by the authors or publisher. Published by Certified Accountants Educational Trust for the Association of Chartered Certified Accountants, 29 Lincoln’s Inn Fields, London WC2A 3EE.

by Dr. Edward Lee, Manchester Business School, University of Manchester Professor Martin Walker, Manchester Business School, University of Manchester Dr. Hans B. Christensen, Graduate School of Business, University of Chicago

欧盟采纳国际财务报告准则引发的思考

□·92·财会月刊(理论).2002年9月,欧洲议会和欧盟委员会发动了一场较大的财务报告变革,即颁布会计协调新法规,要求所有欧盟上市公司自2005年起,遵照国际财务报告准则(IFRS )编制财务报表。

这项法规对整个欧盟经济区28个国家的公司产生了重大影响,而颁布这项新法规的主要原因在于欧盟制定了金融服务行动计划(FSAP ),要求在2005年或者此后一段时间内建立欧盟统一金融服务市场,从而把欧盟各国培育成统一的经济实体,提高其在国际上的竞争力。

遵照IFRS 编制财务报表最终将有助于提高欧盟各国上市公司的财务报表透明度,提高市场效率,降低融资成本,进而消除跨境贸易障碍。

欧盟对IFRS 的采纳,带来了世界范围内财务报告制度的迅速变化。

根据德勤会计公司的报告,截至2006年1月10日,全世界已有70个国家要求上市公司按照IFRS 编制本国财务报表,25个国家允许上市公司按照IFRS 编制本国财务报表。

随着IFRS 在全球范围内的普遍实施,它对美国一般公认会计原则(GAAP )的影响日益增强,全球会计模式趋同化发展成为不可抗拒的潮流。

一、欧盟采纳IFRS 的历程回顾欧盟各成员国的经济状况差别很大,会计和财务报告实务在形式和定位上也存在明显差异。

20世纪70年代末至80年代,为推进区域会计协调化进程,欧盟颁发了一系列会计指令,以立法形式要求各成员国公司执行。

会计指令的颁布和实施,在一定程度上促进了欧盟各成员国之间的经济贸易交流,推动了欧盟的会计协调进程。

然而,会计指令仅为宽泛的指南,其本身存在不完善性,加之指令只是各种不同会计方法的汇合,未能真正减弱各国会计行为的多样性,因而未能带来欧盟各成员国财务报告的统一和质量提高,即使在欧洲范围内也不能保证公司财务报表的可比性和透明性,更难以适应资本市场全球化的要求。

20世纪90年代,经济全球化和竞争的加剧促使欧盟各成员国公司积极寻求在国外市场融资。

在欧洲银行业的国际财务报告准则的价值相关性【外文翻译】

外文翻译原文The value relevance of IFRS in the European banking industry Material Source: Review of Quantitative Finance and Accounting, Online Firs t™, 20 June 2010Author: Mariarosaria Agostino·Danilo Drago·Damiano B. SilipoAbstractThe main purpose of the paper is to investigate the market valuation of accounting information in the European banking industry before and after the adoption of IFRS, the latest version of International Accounting Standards. In a value relevance framework, we apply panel methods to a multiplicative interaction model, in which the partial effects of earnings and book value on share prices are conditional on the adoption of IFRS. According to our evidence, the IFRS introduction enhanced the information content of both earnings and book value for more transparent banks. By contrast, less transparent entities did not experience significant increase in the value relevance of book value.1 IntroductionWe investigate whether the value relevance increased after the adoption of IAS/IFRS by listed banks in Europe. Using a standard value-relevance model, we examine the value relevance of earnings and book value for 221 listed banks from 2000 to 2006.A number of papers have studied the value relevance of IAS/IFRS, sampling companies that complied with international standards voluntarily. The literature shows that voluntary movement towards international accounting harmonization has varied with developments in local and international accounting regulations, indicating a certain degree of opportunism on the part of management (e.g., Stolowy and Ding 2003; Kao 2007), so these findings may be affected by selection bias. Our analysis, by contrast, considers the impact of mandatory introduction of IAS/IFRS.We use panel rather than cross-section data, the latter used in most of the value-relevance literature. Indeed, notwithstanding harmonization, most of the political and economic factors influencing financial reporting practices remain localand differentiated(Ball 2006). With panel data, combined to country-level clusterization, we can control for individual and country characteristics that may be unobservable or hard to measure, such as legal systems, financial systems, or alignment between tax and financial reporting, and that differ across our sample.On the whole, our empirical results provide clear evidence that the impact of accounting earnings on the price of bank stocks increased following the compulsory introduction of IFRS. On the other hand, in most estimations, no significant influence of book value on the stock price was found.2 Related literatureA number of studies compare the value relevance of IAS, US-GAAP and local GAAP in other countries.Most are based on the model of Ohlson (1995) and subsequent refinements,which represents the value of the firm as a linear function of the book value of equity and the current value of any expected abnormal earnings (extra profit).3 Value relevance is estimated by the degree of explanatory power of the model. Barth et al. (2006), on a sample of 428 firms applying IAS from 1990 to 2004, found that the accounting quality of IAS is lower than US GAAP but higher than other domestic GAAP. Finally, introducing IAS reduces the difference in accounting quality between the IAS and US firms. By contrast,Harris and Muller (1999), based on a sample of 31 IAS firms cross-listed on US markets over the period 1992–1996, found limited evidence that reconciliation with US-GAAP,even in respect of IAS, provides relevant information to the market.Another way of appraising the relative performance of IAS and US GAAP is suggested by Leuz (2003) and Bartov et al. (2005). These authors compare the value relevance for German companies traded on German stock exchanges before and after their switch from German accounting rules to either US GAAP or IAS. Leuz measures information asymmetry for firms on Germany’s New Market, finding little evidence in bid/ask spreads or trading volume of differing value relevance of the switch to US GAAPS compared with a switch to IAS. Bartov et al. (2005) gets similar results by comparing value relevance measured as the slope coefficient of the returns/earnings regression. Ashbaugh and Olsson (2002) examine non-US firms listed on London’s SEAQ and find that IAS and US GAAP earnings and book values of equity are equally value-relevant, but that the degree of value relevance depends on the valuation model used.The qualitative results for the banking sector are similar. Barth et al. (1996) offer evidence that fair value estimates of loans, securities and long-term debt in theUnited States under SFAS 107 have significant explanatory power with respect to the prices of bank stocks, greater than that of book values. But Nissim (2003) raises doubts about the reliability of banks fair value disclosures for loans and Eccher et al. (1996) and Nelson (1996) found that the value relevance of SFAS 107 disclosures for bank shares have no incremental explanatory power, except in respect of investment securities. Park et al. (1999) also found evidence of value relevance for fair value accounting of investment securities.Barth et al. (2008) consider three indicators of accounting quality: earnings management, prompt loss recognition and value relevance; they posit that accounting quality is higher when earnings management is less, loss recognition prompter and the value relevance of the amounts entered greater. And in fact according to their estimations following the adoption of IAS firms display less earnings management, more timely loss recognition,and greater value relevance of the accounting amounts. That is, their results sustain the thesis that international standards produce better accounting quality than local GAAP outside the US.To date, however, there has very few papers on the value relevance of IFRS as endorsed by the European Union. Among them, Morais and Curto (2007), which lends support to the thesis that the value relevance of European list ed firms’ accounting amounts increased with adoption of IFRS. They also found that the impact of the adoption of the international standards is greater in civil code than in common law countries. However, their data include the period 2000–2005 and do not distinguish between voluntary and compulsory adoption. By contrast, Daske et al. (2008) in a very recent paper deal with voluntary and compulsory adoption of IFRS. They provide an extensive analysis of the early effects of mandatory adoption of IAS around the world. Among other things, they proved that there are modest but economically significant capital-market benefits around the introduction of mandatory IAS reporting. But these benefits are more pronounced for firms that voluntarily switched to IFRS before the mandatory adoption. However, capital-market benefits occur only in countries with relatively strict enforcement regimes and in countries where the institutional environment provides strong incentives to firms to be transparent. In the other adopting countries market liquidity and the cost of capital remain largely unchanged around the mandate. With respect to the previous work our paper focuses on a different issue (the value-relevance of the compulsory adoption of IFRS), and considers a more homogeneous context with respect to the institutional, environmental and firms’ characteristics.3 Empirical questions and methodologyThe conventional wisdom, corroborated by some empirical studies (see, for instance Barth,et al. 2006, 2008), has it that replacing local GAAP with IAS/IFRS should improve the quality of accounting amounts. Here we test this prediction on European listed banks, for which IFRS became mandatory in 2005. Using data from 2000 to 2006, we investigate whether the new standards are in fact more value-relevant by estimating a panel valuation model to see whether the value-relevance of accounting information changed.Formally, building on the well-known Ohlson (1995) framework, we estimate the following model:t it t it it it postIAS BVPS postIAS EPS BVPS P ⨯++++=43210αααααit t it dT postIAS EPS εα++⨯+5where it P is the stock price 6 months after the end of the fiscal year, it BVPS is per-share book value, it EPS is earnings per share, and postIAS is a dummy coded 1 when IFRS become mandatory, namely for the years 2005 and 2006, and 0 otherwise. Previous studies using the same dependent variable are Barth et al. (2008, 2006). As a robustness check,however, we also employ the price of the stock 3 months after the end of the year (see Sect. 5). Finally, the T variable is a trend, and it i it μνε+= is a composite error, in which the individual effect (i ν) summarizes unobserved time-invariant bank characteristics and the second term (it μ) captures idiosyncratic shocks to market value. The reason for disaggregating this error term is that this enables us to control properly for unobserved heterogeneity of banks, factoring out a different fixed effect for each one.4 DataOur sample includes banks whose shares are traded on a stock exchange in one of the EU-15 countries (Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland,Italy, Luxembourg, Netherlands, Portugal, Spain, Sweden, United Kingdom). Information on share prices, book value and earnings are drawn from Bankscope –Bureau van Djik. In our sample, earnings are never negative.After adjusting for data availability for different variables, we have a final sample of 1,201 annual observations for 221 European listed banks. The panel is unbalanced and spans the years 2000–2006. Table 2 arranges the banks by nationality. Denmark, Italy,France, Germany and Britain have the most banks in the sample, Luxembourg the fewest.5 Results5.1 Unbalanced panel estimates5.2 Balanced panel estimates5.3 Segmentations by capitalization, legal form, and rating5.4 Further robustness checks6 Concluding remarksOur intention was to determine whether the mandatory application of IFRS increased the value relevance of accounting information to the prices of bank shares in the European Union. As we expected, the marginal effect (value relevance) of earnings increased for the entire sample. This result is robust to different specifications of the model and to different samples. The largest incremental effect was in Germany and Italy, the smallest in the United Kingdom. This is consistent with the accepted view that IAS/IFRS requires more disclosure than local regulations in the Continental European countries.For equity book value, our results are less clear-cut. The results for the unbalanced panel indicate that the marginal effect of this variable is negative in the years following the introduction of the new standards. However, they are not robust to different specifications.For the balanced panel (banks reporting data in all the sample years) the marginal effect of book value is never significant in the post-adoption period.Generally speaking, it may be not surprising that book value is less value-relevant. Empirical work (Collins et al. 1999) suggests that this variable is more important when current earnings do not provide a good proxy for future earnings or when there is a heightened increased danger of bankruptcy or abandonment. However, these conditions do not apply to our sample banks, which realized positive and relatively stable profits over the survey period.In fact, the pattern differs considerably between small and large banks, and between rated and non-rated banks. For the smaller (and the non-rated) institutions, the impact of earnings increases while that of book value tends to decrease and become statistically insignificant. For the larger (and the rated) banks, the coefficients of both earnings and book value increase after 2005, and both variables exert a positive and significant marginal effect on share prices. These results suggest that the overall result on book value may reflect the weight of less transparent banks, which do not appear to have overcome their problems of opaqueness, even after the introduction of the new international accounting standards.It is also possible that small and non-rated banks are more opaque because theyare owned by shareholders operating in local markets. To inquire into this question, we split the sample according to legal form, i.e. into cooperative banks and public limited companies. Cooperative banks have closer and longer-term relationships with their member-customers (owners). Therefore, they do not need great transparency. The results for the cooperative banks confirm those for the entire sample. By contrast, for the banks organized as public limited companies, the book value continues to have a positive, though decreasing, impact on the share price even after the adoption of IFRS.Summing up according to our evidence, the introduction of the new accounting standards seems to have enhanced the information content of both earnings and book value for more transparent intermediaries. Less transparent entities, by contrast, seem not to have experienced significant increase in the value relevance of book value. Possible explanations for this phenomenon may provide interesting avenues for future research.译文在欧洲银行业的国际财务报告准则的价值相关性资料来源: 审查财务和会计计量,在线第一™,2010年6月20日作者:Mariarosaria Agostino·Danilo Drago·Damiano B. Silipo摘要本文的主要目的是探讨欧洲银行业之前和之后的国际财务报告准则,国际会计标准的最新版本采用了会计信息的市场价值。

国际财务报告准则的内容比较分析

国际财务报告准则的内容比较分析随着全球经济的快速发展和跨国合作的频繁进行,国际贸易的规模不断扩大,国际公司的数量也随之增加。

财务报告是企业与股东、投资人、债权人等外部利益相关者进行信息沟通和交流的工具,其质量和准确性对于企业的发展和外部利益相关者的决策具有重要意义。

因此,对于不同国家和地区的企业而言,制定一套统一的财务报告准则十分必要。

本文将对美国、欧洲和中国的财务报告准则进行比较分析,探讨它们的异同点。

一、美国财务报告准则(US GAAP)美国财务报告准则(US GAAP)是美国证券交易委员会(SEC)所要求的外部财务报告标准。

US GAAP的主要特点是细则严密、注重细节和规则化,强调遵循指引和规则来编制财务报告。

与此同时,US GAAP的应用范围广泛,几乎覆盖了所有行业。

US GAAP对于会计报表的结构和内容要求十分详细和严谨,包括资产负债表、利润表、现金流量表和所有者权益变动表等。

此外,US GAAP对于合并财务报表、坏账准备的计提、长期投资估值、收入判定和金融工具会计处理等方面也有专门的规定。

二、欧洲财务报告准则(IFRS)欧洲财务报告准则(IFRS),又称国际财务报告准则,由国际会计准则理事会(IASB)制定,是全球最为广泛采用的财务报告准则之一。

IFRS的主要特点是原则为基础、市场化和灵活性强,其目的是为了规范全球公司财务报告的标准和原则,使投资者能更直观地了解企业的财务状况。

IFRS对于会计报表的要求要比US GAAP简单,只要求包括资产负债表、利润表和现金流量表。

IFRS与US GAAP不同的是,它注重财务报告的真实和公正,强调会计师事务所的独立性和审计质量的保证。

在具体的财务报告制度上,IFRS与US GAAP的规定十分相似。

尽管IFRS仅适用于上市公司,但已成为全球范围内企业财务报告的最主要标准。

三、中国财务报告准则(CAS)中国财务报告准则(CAS)是中国证监会颁布的财务报告准则,由中国会计准则制定委员会制定,与IFRS和US GAAP相比,CAS更为注重企业的资产负债表的真实性和可靠性,强调披露和公告,以更好地维护公众利益。

财务管理制度的国际比较与借鉴

财务管理制度的国际比较与借鉴在全球化的背景下,各个国家的财务管理制度起到至关重要的作用,直接影响着国家经济的发展和稳定。

本文将通过比较不同国家的财务管理制度,分析其特点与局限,并探讨如何借鉴他国的经验来完善我国的财务管理制度。

一、美国财务管理制度美国作为全球经济的引领者,其财务管理制度堪称世界级标杆。

美国政府机构与企业间严格分离,财务报表透明度高,审计制度完善,企业财务信息公开程度高,监管规范全面,有力地维护了市场秩序和投资者权益。

然而,美国财务管理制度也存在一些问题,如大规模金融诈骗案件屡屡发生,企业盈余管理等情况,这为其他国家提供了教训。

二、德国财务管理制度德国的财务管理制度强调长期稳健而不是短期利益,注重企业的可持续发展。

其企业主要侧重于长期投资,少涉足金融衍生品市场。

财务报表以公允价值为基础,注重市场价值与企业价值的匹配,同时注重对中小企业的支持与促进。

然而,这种制度也存在刚性过强、对市场需求反应不及时等问题。

三、日本财务管理制度日本的财务管理制度以保护投资者权益和维护金融稳定为核心目标。

其市场监管机构严格,企业财务信息披露透明度高。

在企业盈余管理方面,日本设立了“金融会计问题研究小组”,定期审查企业财务报表,以防止企业进行财务造假。

然而,日本财务管理制度也面临着缺乏国际化、创新性不足等挑战。

四、我国财务管理制度我国的财务管理制度自改革开放以来取得了巨大的进步,但与发达国家相比,仍存在一定差距。

我国重视企业自主经营,推行市场化改革,提倡信息披露,但由于市场监管不到位、监管手段不够灵活等问题,仍有可能出现诸如虚假财务报表、内幕交易等违规行为。

实施财务管理制度的国际比较是我们借鉴和改进我国财务管理制度的重要手段。

在借鉴国外经验的同时,我们也应该注意到每个国家的具体情况、文化背景等因素对财务管理制度的影响,避免照搬照抄。

同时,我们还可以参考国际上一些成功的财务管理制度改革案例,如新加坡的金融监管模式和澳大利亚的信息披露制度等,从中吸取经验,加以改进。

中小企业财务制度的国际比较与借鉴经验

中小企业财务制度的国际比较与借鉴经验随着全球经济的快速发展,中小企业在各个国家中扮演着重要的角色。

在这种背景下,中小企业财务制度的比较与借鉴变得尤为重要。

本文将对世界各地中小企业财务制度进行比较,并从中找到可供借鉴的经验。

一、中小企业财务制度的定义中小企业是指规模适中、资金相对较少、在市场竞争中扮演着重要角色的企业。

中小企业财务制度是指为中小企业制定的适用于其财务管理和报告的规则和制度。

二、中小企业财务制度的国际比较1. 欧洲国家欧洲国家对中小企业财务制度给予了较高的重视。

例如,德国采用了双重会计制度,对中小企业采取了简化的财务报告要求,使得中小企业能够更加便捷地开展财务管理。

而英国则采用了灵活的财务报告制度,允许中小企业按照自身的特点进行财务报告。

2. 北美国家在北美国家,尤其是美国和加拿大,中小企业财务制度相对较为灵活。

美国采用了统一的财务报告标准,但对于中小企业可以选择性地执行一些规定,以方便企业的财务管理。

加拿大则建立了适用于中小企业的特殊财务报告标准,对中小企业提供了更加简化的财务管理方式。

3. 亚洲国家在亚洲国家中,中小企业财务制度的情况各不相同。

日本对中小企业财务报告设定了较为严格的要求,同时提供了相应的指导和支持,促进了中小企业的发展。

中国的中小企业财务制度也在不断完善中,通过推出适用于中小企业的会计准则,为中小企业提供了更加规范和便捷的财务管理方式。

三、中小企业财务制度的借鉴经验1. 简化财务报告要求各国都普遍认识到中小企业相对于大型企业而言,资源和能力有限。

因此,在制定中小企业财务制度时,应尽量简化财务报告要求,减轻企业的负担。

2. 提供指导和支持国家应积极提供中小企业财务管理的指导和支持,例如制定财务报告准则、提供培训和咨询服务等,帮助中小企业更好地开展财务管理工作。

3. 强调透明度和规范性中小企业财务制度应注重透明度和规范性,确保中小企业的财务报告真实、准确。

同时,加强财务监管,打击财务造假行为,维护市场的公平竞争环境。

财务报告的国际比较与借鉴分析

班有“神仙”作文500字

我们班有三位“无所不能”的“神仙”,什么,你不信?那么我就说给你听吧!

“呼……呼……”课堂上传出了一阵呼噜声,那是谁呀?那是我们班的“睡神”老三。

你瞧,才上午第一节课,他就又发挥了强势的睡功,与周公下棋去了,就连一年一次的“磨刀”(期末)考,他也不例外,卷子还没做完,他又呼呼大睡了。

“作业呢?又没做,叫家长!”我们五(1)班的教室里传出了一阵喊叫,路过的人还以为是发生了什么大事了,可我们班的同学们都习以为常了,不就是“菜”伦的后代“小菜”吗?他是“缺神”老二,从不自觉完成回家作业,老师也拿他没有办法。

“呯——”啊,不好!老大“脏神孙”来了,快跑……按理说,他姓孙,他的祖先孙子(孙子兵法)是位名人,人见人爱,可他咋这么讨厌呢?他只要一过来,大家都抱头鼠蹿,谁叫他这么脏呢!早上,他妈给他穿了新买的一件衣服,到了下午,这衣服已变得“面目全黑”了,上面涂满了,红、黑、蓝笔的印记,还有好多不知道哪儿搞来的泥巴!而且,不仅如此,他的座位也又脏又乱,您瞧!嘿,桌子斜了,椅子倒了,东西撒了一地,书包倒在地上,吃饭用手抓,不愧为三神中的老大“脏神”。

怎么样?我们班的三大神仙是不是无所不能,法力无边?什么?神太少?呀!下次你来我们班,我把玉皇大帝等大神都介绍给你!。

欧盟会计国际化进程与启示

欧盟会计国际化进程与启示一、前言欧盟(European;Union,EU)是当今世界上区域合作最为紧密并逐步从经济一体化走向一体化的国家间联盟。

它的前身是1957年成立的欧洲经济共同体EEC,后改称欧共体EC,1993年11月才改组为欧盟。

欧共体EC自成立后一直致力于在地区范围内进行协调。

欧共体有关财务与会计指令的颁布与实施,一定程度上促进了欧盟内部各成员国之间经济贸易交流。

但是由于各国存在着差异,以及指令本身的不完善,随着世界经济的一体化和资本市场的全球化,欧盟不得不进一步采取有效措施,加强会计国际化协调。

采纳国际会计准则是欧盟市场一体化的一个重要里程碑。

根据欧盟制定的关于采纳国际会计准则的决议,要求所有的欧盟上市公司从2005年起必须按国际会计准则(Intemational;Accounting;Standards,IAS)以及未来的国际财务报告标准(International;Financial;Reporting;Standards,IFRS)编制合并会计报表。

欧盟之所以采用IAS和IFRS,主要原因是欧盟制定了金融服务行动计划(Aktionsplan;fuer;Finanzdienstleistungen,FSAP),即在2005年或者之后一段时间里建立欧盟统一的金融市场。

1999年制定的FSAP打算采取43条措施,以扫除欧洲金融市场一体化进程中一切障碍,尽快把欧盟各国造就成一个统一的经济实体,尤其是金融实体,以提高在国际上的竞争力。

毕业论文二。

欧盟会计协调的现状和存在的1.欧盟自70年代以来所做的协调努力。

欧盟自20世纪70年代起就一直致力于会计协调工作。

协调的主要形式是制定各种会计指令。

指令具有很强的约束力,要求各成员国将其写入本国相关的法律法规中,因此,取得了良好效果。

欧盟于1978年7月25日首次发布了关于公司年度财务报告规定格式的第四号指令(78/660/EWG)和在1983年6月13日发布了关于合并报告第七号指令(83/349/EWG),对欧盟会计协调产生了重大。

国际财务报告准则在欧洲的采用

国际财务报告准则在欧洲的采用

Paul Powter;崔华清;毛新述

【期刊名称】《新理财-公司理财》

【年(卷),期】2005(000)010

【摘要】根据2002年《欧盟法令1606/2002》,在欧盟境内监管市场上市的

公司将自2005年1月113起按照国际财务报告准则(IFRSs)编制合并财务报表,约有9000家上市公司和更多子公司将因此受到影响。

欧盟采用IFRSs将会遇到哪些问题,其影响是什么?德勤会计公司资深专家Paul Pacter先生在2005年4月《the Hong Kong Accountant》一文中回答了这些问题。

近年来,我国公司开

始迈出国门,走向世界,采用IFRSs编制财务报表将成为不争的事实。

了解国外

公司采用IFRSs的有关情况,将有助于我国公司更好地走向世界。

【总页数】3页(P61-63)

【作者】Paul Powter;崔华清;毛新述

【作者单位】不详;中国人民大学博士研究生

【正文语种】中文

【中图分类】F233

【相关文献】

1.国际板会计准则选择初探——允许海外证券发行人采用国际财务报告准则的国际经验 [J], 魏雯

2.化危机为机遇以星火成燎原——当前国际财务报告准则在全球的采用情况(上)

[J], 财政部会计司

3.化危机为机遇以星火成燎原——当前国际财务报告准则在全球的采用情况(下) [J], 财政部会计司

4.11.欧洲证券和市场管理局要求上市发行人必须关注2017年度财务报告中的新国际财务报告准则 [J],

5.国际会计师联合会建议全球范围内采用国际财务报告准则 [J],

因版权原因,仅展示原文概要,查看原文内容请购买。

欧盟采纳国际财务报告准则引发的思考

欧盟采纳国际财务报告准则引发的思考

孔宁宁

【期刊名称】《财会月刊(理论版)》

【年(卷),期】2007(000)007

【摘要】本文通过深入分析欧盟采纳国际财务报告准则的原因及产生的效应,得出了以下结论:在当今国际环境下,我们应该立足于自身的会计环境和国家利益进行博弈选择,主动参与国际会计准则的制定工作,积极推进我国会计准则的国际化进程.【总页数】3页(P92-94)

【作者】孔宁宁

【作者单位】对外经济贸易大学国际商学院,北京,100029

【正文语种】中文

【中图分类】F2

【相关文献】

1.国际财务报告准则采纳悖论研究 [J], 胡成

2.司法辖区直接采纳国际财务报告准则的现实与反思 [J], 胡成;李心合

3.欧盟对国际财务报告准则的认可机制述评及启示——以金融工具会计准则为例[J], 史开瑕

4.《首次采纳国际财务报告准则》简介 [J], 唐晓玉

5.国际财务报告准则的成就、挑战与未来——国际财务报告准则基金会受托人主席米歇尔·普拉达于2012年6月27日在国际财务报告准则基金会法兰克福论坛上的演讲 [J], 陆建桥;陆琦林

因版权原因,仅展示原文概要,查看原文内容请购买。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

欧洲非上市企业采用国际财务报告准则的研究与启示———基于英国和德国的实证分析*杨丹(北京师范大学经济与工商管理学院100875)【摘要】非上市企业的国际财务报告准则应用模式是目前国际会计的研究热点,也是各国会计准则制定者关注的焦点。

本文以英国和德国非上市企业为样本,研究当欧洲全部上市公司强制使用国际财务报告准则的情境下,非上市企业是否会增加国际财务报告准则应用的期望。

研究发现,企业规模、资本结构、组织形式、盈利能力和本土会计准则质量显著影响其会计准则选择的倾向性,企业特征影响因素存在国家差异,但处于不同国家并不会加剧或减弱某一企业特征的影响程度。

由于欧洲国家对国际财务报告准则发展方向具有影响作用,本研究所得结果对国际财务报告准则未来在非上市企业层面进一步应用提供方向性支持。

【关键词】国际财务报告准则IFRS非上市企业比较会计一、引言2011年全球G20峰会上各国首脑认可了随着国际资本市场的深入发展,全球需建立统一的会计准则,以满足不同国家企业之间的会计信息可比性,提高国际资本投资效益。

国际会计准则理事会①(IASB,International Accounting Standards Board)近年来致力于制定国际财务报告准则(IFRS,International FinancialReporting Standards)并推动其在全球范围内广泛采用,正是基于这一观点。

IFRS的大范围使用最早发生在地域和贸易都不断一体化的欧洲。

自2005年起,欧盟委员会(EU,European Union)强制要求欧盟国家全部上市公司使用IFRS编制并报告合并财务报表。

随后,加拿大、澳大利亚等许多国家也逐渐采用IF-RS。

根据IASPlus2013年统计,全世界已有近120个国家要求或允许上市公司使用IFRS。

随着越来越多的国家和地区要求上市公司采用IFRS编制并披露财务报表,IASB开始着力制定适用于中小型私有企业的IFRS,并倡导和推动非上市企业逐步启用IFRS。

虽然全球建立统一的会计准则是大势所趋,但对于如何继续推动IFRS在各国企业,尤其是非上市企业的应用,是各国政策制定者需深入思考的问题。

是否如欧洲国家对上市公司一样,强制要求非上市企业使用IFRS?实际上,对于IFRS的强制性采用,国际职业界与学术界一直存在争议。

2007年,美国证券监督管理委员会(SEC,Securities and Exchange Commission)认为国际会计准则发展是必然趋势,并开始允许在美国上市的外国公司以IFRS披露财务报表。

同时SEC在2008年路线图中指出,将考虑允许美国上市公司使用IFRS的可能性(SEC,2008)。

然而,美国会计协会财务报告准则委员会的Jamal et al.(2010)提出会计准则竞争会产生优势,全球范围内采用统一会计准则未必是最优,允许美国公司在IFRS和美国会计准则(U.S.GAAP,Generally Accepted Accounting Principles)之间进行选择可能有助于得到更高质量的会计信息。

据此,SEC对U.S.GAAP和IFRS进行理论对比,并从2009年世界五百强中选取183家采用IFRS编制财务报表的上市公司进行实证考察。

2011年11月SEC发布研究结果,认为IFRS在部分准则内容上仍处于发展完善阶段,决定暂时不要求美国公司使用IFRS,待IFRS逐步提高和完善后,再考虑允许美国公司自愿选择是否使用IFRS(SEC,2011)。

SEC的决定为IFRS的继续发展提供了可能的方向,在国际会计准则发展初期,是否应允许企业根据自身需求自72*①本文英文版刊发于中国会计学会英文期刊China Journal of Accounting Studies2014年第2卷第2期。

本研究受教育部人文社会科学研究青年基金项目(14YJC790149)、国家社科基金青年项目(13CGL036)及中央高校基本科研业务费专项资金(SKZZX2013036)资助。

IASB的前身是国际会计准则委员会(International Accounting Standards Committee,简称IASC),2000年全面重组后更名。

愿选择采用IFRS 而不是强制要求其使用?由于企业从本土会计准则转而使用IFRS 存在转换成本,被强制要求使用IFRS 的企业未必能从中受益,但却需要承担这项转换成本。

基于此,本文对欧洲非上市企业自愿选择IFRS 的情况进行分析,研究当欧洲全部上市公司采用IFRS 编制财务报表的情境下,非上市企业是否会增加IFRS 应用能使其受益的期望,因为自愿选择IFRS 的企业认为应用IFRS 是有利的策略,并预期应用IFRS 所带来的收益会大于变更会计准则所产生的成本(Soderstrom and Sun ,2007;Drake et al.,2010)。

本文同时选取英国和德国大中型非上市企业为研究样本,深入调查这两个国家的非上市企业中哪一类型企业预期会从IFRS 应用中受益。

之所以选择英国和德国,首先由于这两国拥有较多非上市企业,可提供较充足的数据支持,其次英国和德国具有差异化的制度背景,这使得本文结果将同时反映微观企业特征和宏观制度背景对非上市企业会计准则选择倾向性的影响。

本研究在以下几方面可能存在贡献。

第一,与以往大多数考察上市公司选择会计准则行为的研究不同,本文的落脚点在于非上市企业,现有关于此类的研究寥寥无几。

而大部分国家的企业中,绝大多数是非上市企业,因此,对非上市企业的财务报告行为进行探讨更具研究意义。

第二,本文提供了非上市企业在会计准则选择方面的决定因素,丰富了相关研究文献。

第三,本文考察欧洲企业选择会计准则的倾向性,具有现实意义。

欧洲国家对于IFRS 的应用政策一直处于引领位置,IASB 总部设在伦敦,因此欧洲国家对于IFRS 的发展方向具有影响作用。

此外,欧洲国家政策制定者对于欧洲全部上市公司强制使用IFRS 的应用效果也存在争议,这会直接决定其对于非上市企业使用IF-RS 的要求。

那么,对欧洲非上市企业进行研究可以提供未来IFRS 如何在世界范围内进一步应用的方向性支持。

二、制度背景(一)欧洲国家非上市企业自愿选择IFRS 的整体情况表1列示了2010年欧洲国家非上市企业自愿选择IFRS 的描述性统计。

本文中,非上市企业与非上市公司、私有企业和中小企业的定义均不同。

非上市企业包括非上市的公司及其他组织形式的企业。

在欧洲,非上市企业不仅包括私有企业(Private firm ),也包括公开发行股票但不在证券交易所挂牌交易的企业(Public firm )(Nobes ,2010),比如英国的PLC 类企业、德国的AG 类企业和法国的SA 类企业。

此外,非上市企业既包括中小企业,也包括大企业,此处对于中小企业(SME )的界定,根据欧盟定义,量化指标体现为企业总资产、营业收入和员工的数量规模。

因此,非上市企业比非上市公司、私有企业和中小企业包含的企业范围更广泛。

表中统计数据来自于Orbis 数据库②。

表中的非上市企业仅包括按照欧盟4号指示(the FourthEU Directive )规定的大中型非上市企业,即满足下列条件:(1)资产总额超过250万欧元,(2)营业收入超过500万欧元,(3)员工人数超过50人。

同时,考虑到若企业为其他企业的子公司,出于合并报表需要,控股股东会影响企业对IFRS 的选择,使企业无法按照自己意愿选择会计准则,因此表中非上市企业不包括身为子公司的企业,即(4)如果企业50%以上的股权被另一个企业控制,则予以剔除。

表1的描述性统计结果支持本文选择英国和德国大中型非上市企业作为研究样本。

首先,英国和德国拥有较多非上市企业,这为本研究提供充足的数据支持。

其次,英国和德国具有差异化的制度背景,英国是英美法系(也称普通法法系Common Law System )的代表,而德国(与意大利、西班牙、法国等类似)是大陆法系(也称成文法法系Code Law System )的代表,两者不同的司法系统使得其与会计相关的制度背景存在较大差异,这为本研究提供宏观制度背景方面的数据。

表1欧洲国家大中型非上市企业自愿选择IFRS 的描述性统计(2010年)欧洲国家a自愿选择IFRS 的非上市企业b不含金融业金融业合计该国非上市企业数所占比例(%)英国31205162870.81意大利351061415457 2.58西班牙29221833105310799.94c 德国4830782746 2.84法国032321566 2.04葡萄牙0337670.39希腊6497362911.61比利时0224800.42芬兰0223560.56瑞典123145 2.07奥地利13484 4.76荷兰01162 1.61卢森堡221910.53注:a :自愿选择IFRS 的非上市企业数为0的国家,不在此处列示。

b :此处非上市企业仅为按照欧盟4号指示(the Fourth EU Directive )规定的大中型非上市企业。

c :西班牙几乎全部非上市企业使用IFRS 编制财务报表,根据对西班牙监管机构人员的访谈所得信息,主要原因为西班牙非上市企业使用的本土会计准则与IFRS 相差甚微,企业本身已默认其按照IFRS 编制财务报表。

(二)英国和德国的相关制度背景表2列示了英国和德国非上市企业会计准则选择的相关制度背景。

在英国,非上市企业可以在本土会计准则和82②Orbis 数据库由Bureau van Dijk 公司运营,该公司运营的另一个Amadeus 数据库,被许多研究私有企业(Private firm )的文献所使用,例如Coppens and Peek (2005)以及Peek et al.(2010)。

IFRS之间进行选择。

其中,非上市公司可以使用IFRS或者会计准则委员会(ASB,Accounting Standards Board)颁布的相关准则,包括财务报告准则(FRS,FinancialRepor-ting Standards)、会计实务准则公报(SSAPs,Statements of Standard Accounting Practice)和紧急问题工作小组摘要(UITF Abstracts,Urgent Issues Task Force Abstracts);小型非上市企业可以在IFRS、ASB准则或小企业准则(FRSSE,FinancialReporting Standard for Smaller Entities)中选择其一编制财务报表。

然而近年,英国无论是监管机构还是会计准则都经历着重大变革。