会计英语第四章作业

会计英语Chapter 4 Current Assets

会计英语

出版社 经管分社

会计英语Chapter 4 Current Assets

会计英语

出版社 经管分社

4.1 Cash

Accountants define cash as money on deposit in banks and any items that banks will accept for deposit. These items include not only coins and paper money, but also checks, money orders and travelers’ checks. Banks also accept drafts signed by customers using bank credit cards, such as Visa and MasterCard. Thus sales to customers using bank cards are cash sales, not credit sales, to the enterprise that makes the sale.

会计英语4,8,9章练习题

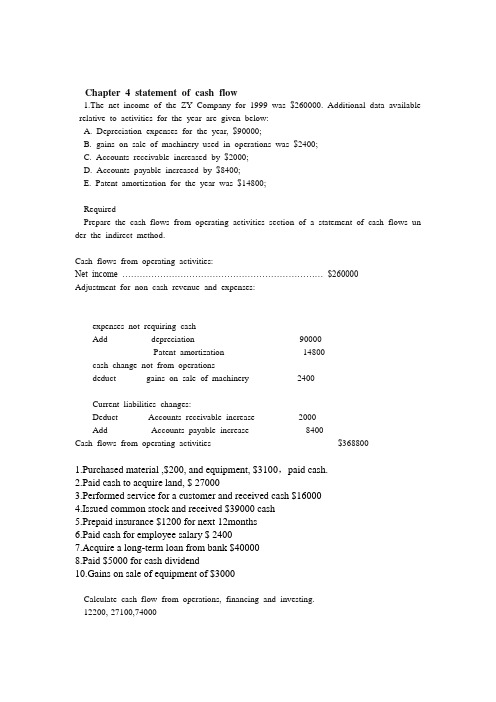

Chapter 4 statement of cash flow1.The net income of the ZY Company for 1999 was $260000. Additional data available relative to activities for the year are given below:A. Depreciation expenses for the year, $90000;B. gains on sale of machinery used in operations was $2400;C. Accounts receivable increased by $2000;D. Accounts payable increased by $8400;E. Patent amortization for the year was $14800;RequiredPrepare the cash flows from operating activities section of a statement of cash flows un der the indirect method.Cash flows from operating activities:Net income …………………………………………………………… $260000Adjustment for non cash revenue and expenses:expenses not requiring cashAdd depreciation 90000Patent amortization 14800cash change not from operationsdeduct gains on sale of machinery 2400Current liabilities changes:Deduct Accounts receivable increase 2000Add Accounts payable increase 8400Cash flows from operating activities $3688001.Purchased material ,$200, and equipment, $3100,paid cash.2.Paid cash to acquire land, $ 270003.Performed service for a customer and received cash $160004.Issued common stock and received $39000 cash5.Prepaid insurance $1200 for next 12months6.Paid cash for employee salary $ 24007.Acquire a long-term loan from bank $400008.Paid $5000 for cash dividend10.Gains on sale of equipment of $3000Calculate cash flow from operations, financing and investing.12200,-27100,74000Chapter 8 accounts receivable1.T/FAn account receivable that has been determined to be uncollectible is still an asset.(F) We should debit bad debts expense and credit allowance for doubtful accounts for write off bad debts.(F)Allowance for doubtful accounts is contra-asset account that offsets account receivable.(T)Gross accounts receivable appears on the balance sheet.(F)When we write off a worthless receivables, the net accounts receivable is less than before.(F)2.When we use the allowance method to record bad debts,there are three methods to estimate the amount of bad debtsPercentage of total accounts receivable outstanding(应收账款余额百分比法)Aging method(账龄分析法)Percentage-of-sales method(销货百分比法)(一)余额百分比法这是按照期末应收账款余额的一定百分比估计坏账损失的方法。

全英文初级会计第四章

-Indirect cost allocated to A = $2 × 3000 = $6000

-Indirect cost allocated to B = $2 × 2000 = $4000

To accompany Cost Accounting 12e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved.

4-6

Costing Approaches

• Actual Costing – allocates indirect costs based on the actual indirect-cost rates times the actual activity consumption

100 hours

Overhead Allocation

Rate:

$1,000 ÷ 100 DLhrs

= $10/DLhr

Overhead Applied to Job #123:

$10/DLhr X

5 hours used in Job #123

= $50

The Cost Object:

Job #123

DM DL OH

$100 $200

$50

Total Cost: $250

To accompany Cost Accounting 12e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved.

会计英语chapter 4

Example ----perpetual system ----perpetual

On Jan.1, the inventory account balance was $7,000, the whole year sales revenue was $10,000, on Dec.31, Inventory account balance was $2,000, and when its actual counted value was $1,000. cost: 7000 – 2000 = 5000 profit 10000 – 5000 = 5000 2000 – 1000 = 1000 ------- operating expenses

Service enterprise VS merchandising concern

Service enterprise Net income is then calculated by deducdeducting expenses from commissions earned or fees earned. net income = fees (commission) revenue - operating expenses.

Purchase, sales revenue and cost of goods sold

Merchandise purchases

gross purchase & net purchase net purchase = gross purchase – any purchase discounts – any purchase returns and allowances + transportation costs (paid by the buyer)

会计英语,第四章

C4 - 14

Advantages of Using Periodic Inventory

• The accounting records for inventory and

cost of goods sold are updated only at the end of the accounting period (month, year, etc.). • Thus, in the middle of the period, there is no record that shows how much inventory is on hand or how much has been sold (COGS). • This is an easy, inexpensive method.

C4 - 10

COGS Schedule

Assume that each unit cost $6

Units

Beg. Inventory + Purchases = Goods Available - End. Inventory = Cost of Goods Sold 3 8 11 5 6

Cost

C4 - 12

4-2 Two inventory systems

P110

• Two main systems for keeping merchandise inventory records:

–Perpetual inventory system - a system that keeps a running, continuous record that tracks inventories and the cost of goods sold on a day-to-day basis –Periodic inventory system - a system in which the cost of good sold is computed periodically by relying solely on physical counts without keeping day-to-day records of units sold or on hand.

会计英语——用英语了解会计的定义和运用

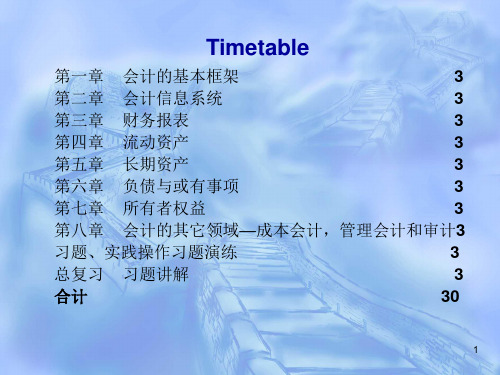

第一章 会计的基本框架

3

第二章 会计信息系统

3

第三章 财务报表

3

第四章 流动资产

3

第五章 长期资产

3

第六章 负债与或有事项

3

第七章 所有者权益

3

第八章 会计的其它领域—成本会计,管理会计和审计3

习题、实践操作习题演练

3

总复习 习题讲解

3

合计

30

1

Chapter 1

I. New words: 1. Account n. statement of money paid or owed for goods or services --The accounts show a profit of $9000. Open/close an account、account payable, account receivable, On account (1) pay part of the money (2)on credit --I will give you$30 on account. --buy things on account.

bank account -- Credit $8 to a customer / an account. Credit n. (1)permission to delay payment for goods and

services --No ~ is given at this shop. Payment must be in

prediction. --There is a lack of ~ between his promises

and his actions. ~ college, ~ column, ~course, ~school Corresponding a. more or less the same ~ fingerprints, the ~ period last year

国际会计第四章练习PPT课件

•

January 1, 2012

December 31, 2012

• Monetary assets 500 000

1 700 000

• Monetary liabilities 300 000

1 110 000

• General price level index:

•

January 1, 2012

• A. The nature of the products or services

• B. The nature of the production processes

• C. Relationship between operations in different geographic areas

changes in the general purchasing power of the reporting currency

over time.

(X)

2020/2/16

9

• Case Problem

• 1、The monetary assets and liabilities of Cowboy U.S. are as follows:

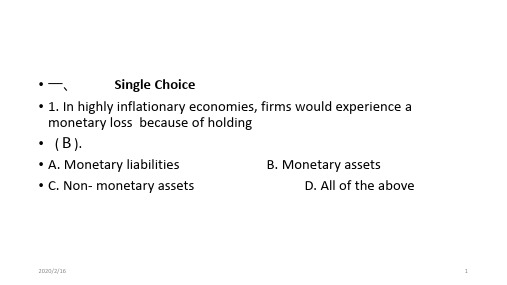

• 一、 Single Choice

• 1. In highly inflationary economies, firms would experience a monetary loss because of holding

• (B).

• A. Monetary liabilities

ቤተ መጻሕፍቲ ባይዱ

B. Monetary assets

• 1. In high-inflation environment, countries use inflation-adjusted models to

会计专业英语 第4章 Current Assets

A proper internal control system over cash is usually comprised of the following procedures:

◦ (1) Individuals who receive cash cannot disburse cash. ◦ (2) Individuals who handle cash cannot access

4.1 Monetary Capital

4.1.1 Cash

Cash includes cash on hand, checks, money orders and cash in bank or bank deposit that can be unconstrained withdrew from banks and other financial institutions.

It’s debited with cash shortages and credited th cash overages.

At the end of the accounting period, if there is a debit balance in the Cash Over and Short account, it should be transferred to the Miscellaneous Expense in the income statement.

◦ Second, cash is the most liquid asset and it is full of temptation to others. If cash is not well protected, it may be easily stolen or misappropriated.

会计英语第4章

◦ (5) Check the cash on hand every day to ensure that it’s in line with the accounts.

Many companies combine cash and cash equivalents on their balance sheets. Cash equivalents are highly liquid short-term investments that can be easily and quickly converted into cash.

◦ These two adjusted balances must be equal.

4.1.3 Internal Control Over Cash

A proper internal control system over cash is usually comprised of the following procedures:

4.2.3 Estimation of Bad Debts

Under the allowance method, there are two common methods to estimate the amount of bad debts:

① The percentage of credit sales method

unit 4会计英语

The words “debit” and “credit” should not be confused with “increase” and “decrease”.

confuse v. 搞乱, 使糊涂

【搭配】be confused with 与……混淆,弄错 【例句】I confused her with her sinter because they are so alike.

Task 1 & 2

2. Newtech Co. Ltd sells a software for $1 000 and sends their customer an invoice. They allow their customer 30 days to pay them for this software (on account). Analysis: The assets are increased and the owner's equity is increased.

Task 1 & 2

6. Newtech Co. Ltd pays the computer company $2000 with a check for the computers that they bought. Analysis: The assets are decreased and the liabilities are decreased.

Task 1 & 2

7. Newtech Co. Ltd receives a check from the customer who they billed (invoiced) $5 000 for services and allowed 30 days to pay. Analysis: One asset is increased and another asset is decreased.

《会计英语》Accounting04

16

Reconciling the Bank Balance(银行账户余 额的调节)

What's the bank statement?

17

Bank Statements(银行对账单)

Shows the beginning bank balance, deposits made, checks paid, other debits and credits in the month, and the ending bank balance.

14

Example of Petty Cash Payments

• Jose also spent $20 for delivery charges and $60 for coffee and other miscellaneous expenses. • What is the journal entry to record the Reimbursing of the frrency (纸币)

Cash is defined as any deposit banks will accept.

Checks

Money orders (汇票)

A cash equivalent is an investment that is readily convertible to a known amount of cash and is sufficiently close to its maturity date so that its market value is relatively insensitive to interest rate changes. 现金等价物是指企业持有至到期,容易兑换成确定金额的现 金,并且市场价值不随利率的变化有较大波动的一项投资。

2012CPA会计英语第四单元(完整版)

Unit 4 Financial Statement Elements-RevenuesRevenueDefinitionRevenue is an inflow of economic benefits during the period arising in the course of ordinary activities of an entity when those inflows result in increases in equity other than increases relating to contributions from equity participants.Inflow of economic benefits: 经济利益的流入Increase in equity: 所有者权益的增加Contributions from equity participants: 所有者投入MeasurementRevenue is measured at the fair value of the consideration received or receivable.收入以将要收到或已收到对价的现值来计量If the inflow of cash or cash equivalents is deferred (递延), the fair value of the consideration receivable is less than the nominal amount of cash and cash equivalents to be received, and discounting(折现)is appropriate.Identification of the transactionNormally, each transaction can be looked at as a whole. Sometimes, it is necessary to break atransaction into its component parts. E.g. a sale include both the transfer of goods and the provision of future servicing, the revenue for which should be deferred over the period the service is performed.On the other hand, seemingly separate transactions must be considered together if apart theylose their commercial meaning. E.g. sale and repurchase.Sale of goodsRevenue is recognized when:(a)all significant risks and rewards of ownership have been transferred to the buyer企业已将商品所有权上的主要风险和报酬转移给购货方(b)the entity has no continuing managerial involvement to the degree usually associated withownership, and no longer has effective control over the goods sold.企业既没有保留通常与所有权相联系的继续管理权,也没有对已售出的商品实施有效控制(c)both revenue and the associated costs of the transaction can be measured reliably收入的金额和相关的成本能够可靠地计量(d)probable that economic benefits will flow to the enterprise相关的经济利益很可能流入企业The passing of risks and rewards is critical to revenue recognition. The normal critical event is when goods are delivered to the buyer i.e. pass of position or transfer of legal title.通常情况下,转移所有权凭证并交付实物后,商品所有权上的主要风险和报酬随之转移。

IntermediateAccountingChapter4中级会计学第四章课后习题答案

Chapter 4The Income Statement and Statement of Cash FlowsQUESTIONS FOR REVIEW OF KEY TOPICSQuestion 4-5The term earnings quality refers to the ability of reported earnings (income) to predict a company’s future earnings. After all, an income statement simply reports on events that already have occurred. The relevance of any historical-based financial statement hinges on its predictive value.Question 4-7The process of intraperiod tax allocation matches tax expense or tax benefit with each major component of income, specifically continuing operations and any item reported below continuing operations. The process is necessary to achieve the desired result of separating the total income effects of continuing operations from the two separately reported items - discontinued operations and extraordinary items, and also to show the after-tax effect of each of those two components.Question 4-9Extraordinary items are material gains and losses that are both unusual in nature and infrequent in occurrence, taking into account the environment in which the entity operates.Question 4-11GAAP permit alternative treatments for similar transactions. Common examples are the choice among FIFO, LIFO, and average cost for the measurement of inventory and the choice among alternative revenue recognition methods. A change in accounting principle occurs when a company changes from one generally accepted treatment to another.In general, we report voluntary changes in accounting principles retrospectively. This means revising all previous periods’ financial statements as if the new method were used in those periods. In other words, for each year in the comparative statements reported, we revise the balance of each account affected. Specifically, we make those statements appear as if the newly adopted accounting method had been applied all along. Also, if retained earnings is one of the accounts whose balance requires adjustment (and it usually is), we revise the beginning balance of retained earnings for the earliest period reported in the comparative statements of shareholders’ equity (or statements of retained earnings if they’re presented instead).Then we create a journal entry to adjust all account balances affected as of the date of the change. In the first set of financial statements after the change, a disclosure note would describe the change and justify the new method as preferable. It also would describe the effects of the change on all items affected, including the fact that the retained earnings balance was revised in the statement of shareholders’ equity along with the cumulative effect of the change in retained earnings.An exception is a change in depreciation, amortization, or depletion method. These changes are accounted for as a change in estimate, rather than as a change in accounting principle. Changes in estimates are accounted for prospectively. The remaining book value is depreciated, amortized, or depleted, using the new method, over the remaining useful life.Question 4-15Comprehensive income is the total change in equity for a reporting period other than from transactions with owners. Reporting comprehensive income can be accomplished with a separate statement or by including the information in either the income statement or the statement of changes in shareholders’ equity.Question 4-22U.S. GAAP designates cash outflows for interest payments and cash inflows from interest and dividends received as operating cash flows. Dividends paid to shareholders are classified as financing cash flows. IFRS allows more flexibility. Companies can report interest and dividends paid as either operating or financing cash flows and interest and dividends received as either operating or investing cash flows. Interest and dividend payments usually are reported as financing activities. Interest and dividends received normally are classified as investing activitiesBRIEF EXERCISESBrief Exercise 4-6*$850,000 x 40%Note: Restructuring costs, interest revenue, and loss on sale of investments are included in income before income taxes and extraordinary item.Brief Exercise 4-9*$5,800,000 x 30%** Loss from operations of discontinued component:Impairment loss ($8 million book value less$7 million net fair value) $(1,000,000) Operating loss (3,600,000) Total before-tax loss $(4,600,000)EXERCISES Exercise 4-3* 30% x $440,000Pretax income from continuing operations $14,000,000Income tax expense (5,600,000) Income from continuing operations 8,400,000 Less: Net income 7,200,000 Loss from discontinued operations $1,200,000 $1,200,000 60%* = $2,000,000 = before tax loss from discontinued operations.*1-tax rate of 40% = 60%Pretax income of division $4,000,000 Add: Loss from discontinued operations 2,000,000 Impairment loss $6,000,000 Fair value of division’s assets$11,000,000 Add: Impairment loss 6,000,000 Book value of division’s assets$17,000,000Requirement 1This is a change in accounting estimate.Requirement 2$2,400,000 Cost$240,000 Previous annual amortization ($2,400,000 ÷ 10 years) x 21/2 yrs. 600,000 Amortization to date (2009-2011)1,800,000 Book value÷ 5 yrs. Estimated remaining life(given)$ 360,000 New annual amortizationTiger EnterprisesStatement of Cash FlowsFor the Year Ended December 31, 2011($ in thousands)Cash flows from operating activities:Net income $ 900Adjustments for noncash effects:Depreciation expense 240Changes in operating assets and liabilities:Decrease in accounts receivable 80Increase in inventory (40)Increase in prepaid insurance (30)Decrease in accounts payable (60)Decrease in administrative and other payables (100)Increase in income taxes payable 50Net cash flows from operating activities $1,040 Cash flows from investing activities:Purchase of plant and equipment (300) Cash flows from financing activities:Proceeds from issuance of common stock 100Proceeds from note payable 200Payment of dividends (1) (940)Net cash flows from financing activities(640)Net increase in cash 100 Cash, January 1 200 Cash, December 31 $ 300(1)Retained earnings, beginning $540+ Net income 900- Dividends x x = $940Retained earnings, ending $500The T-account analysis of the transactions related to operating cash flows is shown below. To derive the cash flows, the beginning and ending balances in the related assets and liabilities are inserted, together with the revenue and expense amounts from the income statements. In each balance sheet account, the remaining (plug) figure is the other half of the cash increases or decreases.Based on the information in the T-accounts above, the operating activities section of the SCF for Tiger Enterprises would be as shown next.Exercise 4-23 (concluded)Tiger EnterprisesStatement of Cash FlowsFor the Year Ended December 31, 2011($ in thousands)Cash flows from operating activities:Collections from customers $ 7,080Prepayment of insurance (130)Payment to inventory suppliers (3,460)Payment for administrative & other exp. (1,900)Payment of income taxes (550)Net cash flows from operating activities $ 1,040CPA / CMA REVIEW QUESTIONSCPA Exam Questions1. c. U.S. GAAP requires that discontinued operations be disclosed separatelybelow income from continuing operations.2. d.Other than sales, COGS, and administrative expenses, only the gain or lossfrom disposal of equipment is considered part of income from continuingoperations. Income from continuing operations was ($5,000,000 - 3,000,000- 1,000,000 + 200,000) = $1,200,000.3. a. In a single-step income statement, revenues include sales as well as otherrevenues and gains.Sales revenue $187,000Interest revenue 10,200Gain on sale of equipment 4,700Total $201,900The discontinued operations and the extraordinary gain are reported belowincome from continuing operations.4.a.The $400,000 impairment loss and the $1,000,000 loss from operationsshould be combined for a total loss of $1,400,000.5.d. The change in the estimate for warranty costs is based on new informationobtained from experience and qualifies as a change in accounting estimate. Achange in accounting estimate affects current and future periods and is notaccounted for by restating prior periods. The accounting change is a part ofcontinuing operations.6. a. Dividends paid to shareholders is considered a financing cash flow, not anoperating cash flow.7. c. Issuing common stock for cash is considered a financing cash flow, not aninvesting cash flow.CMA Exam Questions1.d. Discontinued operations and extraordinary gains and losses are shownseparately in the income statement, below income from continuing operations.The cumulative effect of most voluntary changes in accounting principle isaccounted for by retrospectively revising prior years’ financial statements.2.c.The operating section of a retailer’s income statement includes all revenuesand costs necessary for the operation of the retail establishment, e.g., sales,cost of goods sold, administrative expenses, and selling expenses.3 a. Extraordinary items should be presented net of tax after income fromoperations.PROBLEMSProblem 4-9Requirement 1Diversified Portfolio CorporationStatement of Cash FlowsFor the Year Ended December 31, 2011Cash flows from operating activities:Collections from customers (1)$880,000Payment of operating expenses (2)(660,000)Payment of income taxes (3)(85,000)Net cash flows from operating activities $135,000Cash flows from investing activities:Sale of investments 50,000Net cash flows from investing activities 50,000Cash flows from financing activities:Proceeds from issue of common stock 100,000Payment of dividends (80,000)Net cash flows from financing activities 20,000Increase in cash 205,000Cash and cash equivalents, January 1 70,000Cash and cash equivalents, December 31 $275,000(1)$900,000 in service revenue less $20,000 increase in accounts receivable.(2) $700,000 in operating expenses less $30,000 in depreciation less $10,000 increase in accounts payable.(3)$80,000 in income tax expense plus $5,000 decrease in income taxes payable.Problem 4-9 (concluded)Requirement 2Diversified Portfolio CorporationStatement of Cash FlowsFor the Year Ended December 31, 2011Cash flows from operating activities:Net income $120,000Adjustments for noncash effects:Depreciation expense 30,000Changes in operating assets and liabilities:Increase in accounts receivable (20,000)Increase in accounts payable 10,000Decrease in income taxes payable (5,000)Net cash flows from operating activities $135,000。

会计英语实训教程(第四章)

10. money order

11. electronic funds transfer

落后,缓慢 快递 补充,补足 即时支付 汇票 电子资金转账

Section 1 Cash and Accounts Receivable

9

Part 2 Intensive Reading

Cash

New Words and Special Terms

Section 1 Cash and Accounts Receivable

4

Part 1 Workplace Spoken English

Follow the Samples

Dialogue 1

A:Lucy, perhaps you need to set up a petty cash fund. B:Why? A:All businesses should have a petty cash fund for small various purchases. B:How much should we keep in it? A:There should not be a lot of money kept in the petty cash and it should

Section 1 Cash and Accounts Receivable

8

会计英语课后题答案Answer for lesson4

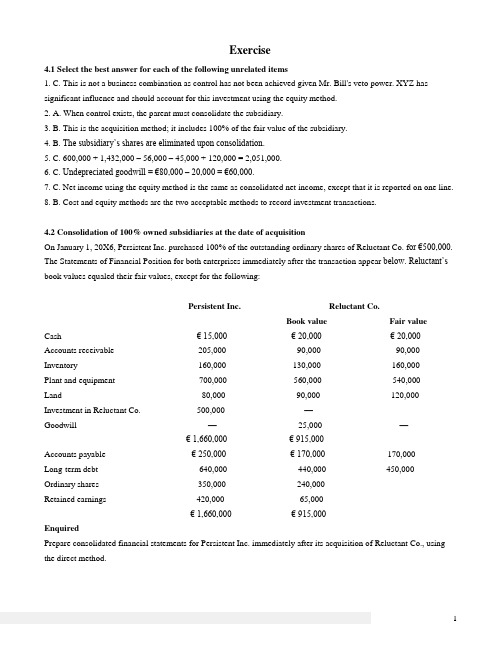

Exercise4.1 Select the best answer for each of the following unrelated items1. C. This is not a business combination as control has not been achieved given Mr. Bill's veto power. XYZ has significant influence and should account for this investment using the equity method.2. A. When control exists, the parent must consolidate the subsidiary.3. B. This is the acquisition method; it includes 100% of the fair value of the subsidiary.4. B. The subsidiary’s shares are eliminated upon consolidation.5. C. 600,000 + 1,432,000 – 56,000 – 45,000 + 120,000 = 2,051,000.6. C. Undepreciated goodwill = €80,000 –20,000 = €60,000.7. C. Net income using the equity method is the same as consolidated net income, except that it is reported on one line.8. B. Cost and equity methods are the two acceptable methods to record investment transactions.4.2 Consolidation of 100% owned subsidiaries at the date of acquisitionOn January 1, 20X6, Persistent Inc. purchased 100% of the outstanding ordinary shares of Reluctant Co. f or €500,000. The Statements of Financial Position for both enterprises immediately after the transaction appear below. Reluctant’s book values equaled their fair values, except for the following:Persistent Inc. Reluctant Co.Book value Fair valueCash € 15,000€ 20,000 € 20,000 Accounts receivable 205,000 90,000 90,000 Inventory 160,000 130,000 160,000Plant and equipment 700,000 560,000 540,000Land 80,000 90,000 120,000 Investment in Reluctant Co. 500,000 —Goodwill — 25,000 —€ 1,660,000 € 915,000Accounts payable € 250,000 € 170,000 170,000Long-term debt 640,000 440,000 450,000 Ordinary shares 350,000 240,000Retained earnings 420,000 65,000€ 1,660,000€ 915,000EnquiredPrepare consolidated financial statements for Persistent Inc. immediately after its acquisition of Reluctant Co., using the direct method.Calculation and allocation of purchase discrepancyCost of investment in Reluctant Co.: € 500,000Notice that goodwill that existed on Reluctant’s books at the date of acquisition had a fair value of €0 at the date of acquisition. The amount provides evidence of a previous acquisition of another enterprise by Reluctant. From Persistent’s point of view, this intangible asset has no value and represents a decrease in Reluctant’s net asset value. This issue will be covered in more depth in the next topic.4.3Consolidation less than 100% owned subsidiaries after the date of acquisition using working paper approach On January 1, 20X5, Pascal Ltd. purchased 90% of Socrates Co. for €1,655,000 cash. At that time, Socrates had the following Statement of Financial Position.SOCRATES CO.Statement of Financial PositionAt January 1, 20X5Book value Fair valueCash € 165,000€ 165,000Accounts receivable 285,000 270,000Inventory 300,000 345,000Plant and equipment — Net 2,250,000 2,400,000€ 3,000,000Accounts payable € 270,000 270,000Long-term debt 1,200,000 1,150,000Ordinary shares 600,000Retained earnings 930,000€ 3,000,000The long-term debt is payable in 10 years. The plant and equipment have an average remaining useful life of 10 years and are being depreciated on a straight-line basis. The annual goodwill impairment tests revealed a €2,000 loss in 20X5 and a €5,100 loss in 20X6. (These losses pertain to Pascal’s 90% ownership of Socrates. As such, the full amounts should be deducted from the consolidated earnings.) The following occurred in 20X5: Socrates earned €1,300,000 and paid dividends of €75,000.Pascal uses the equity method to record its investment in Socrates but must report on a consolidated basis. At December 31, 20X6, the following financial statements were available:Statements of Financial PositionAt December 31, 20X6Pascal SocratesCash € 371,600€ 239,000Accounts receivable 252,500 517,500Inventory 1,455,000 562,500Plant and equipment — Net 3,946,500 2,994,500Investment in subsidiary 2,876,400€ 8,902,000€ 4,313,500Accounts payable € 675,000€ 73,500Long-term debt — 1,200,000Future income taxes 160,000 75,000Ordinary shares 1,500,000 600,000Retained earnings 6,567,000 2,365,000€ 8,902,000€ 4,313,500Statements of Income and Retained EarningsFor the year ended December 31, 20X6Pascal SocratesSales €14,609,550€ 2,475,000Investment income 183,900 —Other income — 100,000Cost of sales 11,500,000 1,710,000Depreciation 159,000 156,000Other expenses 606,750 421,500Income tax expense 506,250 57,50012,772,000 2,345,000Net income 2,021,450 230,000Beginning balance, retained earnings 5,045,550 2,155,000Dividends (500,000) (20,000)Ending balance, retained earnings € 6,567,000 € 2,365,000Assume that Pascal elects to value the non-controlling interest in Socrates’ at the NCI’s percentile interest in the identifiable net assets of the subsidiary.Required1. Complete the calculation and allocation of purchase discrepancy and non-controlling interest.2. Complete the purchase discrepancy and adjustment schedule.3. Prepare eliminating entries for 20X6. Be sure to include appropriate commentary in support of each entry. Solution:1. Calculation and allocation of purchase discrepancy and non-controlling interestCost of 90% of Socrates at January 1, 20X5 € 1,655,000Fair value of identifiable net assets(€1,760,000 ×90%) 1,584,000Balance — Goodwill € 71,000Purchase discrepancy allocated toAccounts receivable –15,000Inventory 45,000Plant and equipment 150,000Long term debt 50,000 € 230,000TOTAL € 301,000Non-controlling interest: €1,760,000 ×10% = €176,0002.Purchase discrepancy adjustment schedule3. Eliminating entries#1 Investment income (230,000 ×90% – 23,100) ............ 183,900Dividends — S ........................................................ 18,000Investment in subsidiary ......................................... 165,900To eliminate 20X6 equity basis investment income and the parent’s share of Socrates’ 20X6 dividends against the investment account#2 Ordinary shares ............................................................. 600,000Retained earnings, January 1, 20X6 ............................. 2,155,000Purchase discrepancy .................................................... 249,000Investment in subsidiary ......................................... 2,710,500Non-controlling interest .......................................... 293,500To eliminate start-of-the-year retained earnings and ordinary shares of Socrates against the start-of-the-year balance of the investment account and to establish the purchase discrepancy and non-controlling interest at the end of December 31, 20X5#3 Other expenses (interest) .............................................. 5,000Depreciation expense .................................................... 15,000Goodwill impairment loss ............................................ 5,100Plant and equipment ..................................................... 120,000Goodwill ....................................................................... 63,900Long-term debt ............................................................. 40,000Purchase discrepancy .............................................. 249,000To allocate the purchase discrepancy amount at the end of 20X5, to record depreciation of purchase discrepancies for 20X6, and to set up the undepreciated purchase discrepancy balances at the end of 20X6#4 Non-controlling interest — I/S ..................................... 21,000Non-controlling interest — SFP ............................. 21,000To allocate the non-controlling interest’s share of 20X6 net income#5 Non-controlling interest — SFP ................................... 2,000Dividends — I/S ..................................................... 2,000To allocate non-controlling interest’s percentage of dividends paid by Socrates in 20X64.4Consolidation less than 100% owned subsidiaries after the date of acquisition using direct method and working paper methodOn January 1, 20X2, Ping Inc. acquired 75% of Sing Co. for €1,500,000. Sing’s condensed balance sheet and fair values immediately before the acquisition were as follows:SING CO. Statement of Financial PositionAt December 31, 20X1Book value Fair valueCash and accounts receivable € 540,000 € 540,000Inventory 250,000 270,000Plant and equipment (net) 1,435,000 1,575,000€ 2,225,000 € 2,385,000Current liabilities € 785,000€785,000Ordinary shares 1,200,000Retained earnings 240,000€ 2,225,000•Sing’s inventory turns over 6 times in a year.•Plant and equipment have an estimated useful life of 10 years.•Ping’s annual goodwill impairment test revealed a €30,000 loss for 20X3. The impairment is attributed to economic decline.•On December 31, 20X3, Ping owes Sing €18,000 related to an intercompany interest-free loan.The separate entity financial statements for the two companies at December 31, 20X3, are as follows:Income StatementsFor the year ended December 31, 20X3PING SINGSales € 3,600,000€ 2,800,000Investment income 237,000 —Total revenue 3,837,000 2,800,000Cost of goods sold 1,600,000 1,500,000Amortization expense 294,000 730,000Administration and other expenses 600,000 200,000Total expenses 2,494,000 2,430,000Net income € 1,343,000€ 370,000Statements of Changes in EquityFor the year ended December 31, 20X3Balance, January 1 — Retained earnings € 2,504,000€ 1,546,000Net income 1,343,000 370,0003,847,000 1,916,000Dividends 400,000 200,000Balance, December 31 — Retained earnings € 3,447,000€ 1,716,000Statements of Financial PositionAt December 31, 20X3Cash € 100,000€ 40,000Accounts receivable 960,000 840,000Inventory 1,200,000 500,000Plant and equipment (net) 1,914,000 1,956,000Investment in Sing Co. 2,541,000 —€ 6,715,000€ 3,336,000Current liabilities € 1,068,000€ 420,000Ordinary shares 2,200,000 1,200,000Retained earnings 3,447,000 1,716,000€ 6,715,000€ 3,336,000Additional information:(1) Company PING selected to value the NCI at NCI’s share of the fair value of the identifiable net asset of Sing.(2) Parent amortizes 100% of goodwill, FVI is amortized according to the proportionate share the parent and NCI own Required1. Prepare the Year 3 consolidated statements for Ping Inc. for the year ended December 31, Year 3, using the direct approach.2. Prepare a schedule of the changes in non-controlling interest since acquisition.3. Prepare the five entries necessary for the working paper approach and provide descriptions.Solutions:1.1112。

财务会计英语unit4 Owner’s Equity

Section 1 Partnership Accounting

Financial Accounting English (Second Edition)

Section 1 Partnership Accounting

Financial Accounting English (Second Edition)

Section 1 Partnership Accounting

Example 4.10 Assume that each partner of L & L Co. was to receive 15% interest on his capital balance, the remaining net income was to be shared equally. The calculations would be:

Lott ($88,000 ×60%) $52,800 Lambert ($88,000 ×40%) $35,200

$88,000

Financial Accounting English (Second Edition)

Section 1 Partnership Accounting

The closing entry to show the distribution was: 2007 Mar. 31 Income Summary 88000

Totals $38,000 50,000 $88,000

Financial Accounting English (Second Edition)

Section 1 Partnership Accounution would be:

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计英语第四章作业

Matching Questions

115. Match the following terms with the appropriate definition.

1. Temporary accounts

2. Pro forma statements

3. Closing entries

4. Work sheet

5. Accounting cycle

6. Post-closing trial balance

7. Permanent accounts

8. Operating cycle of a business

9. Income summary

10. Working papers

Accounts that reflect on activities related to one or

more future periods; they include all balance sheet

accounts.

Recurring steps performed each accounting period, starting with analyzing and recording of transactions in the journal and continuing through the post-closing trial

balance (or reversing entries).

Accounts that are used to record transactions and

events for one accounting period only; they include

revenues, expenses, and withdrawals.

Analyses and other informal reports prepared by accountants when organizing the information presented in

reports and financial statements.

A temporary account used only in the closing process

and to where the balances of revenue and expense

accounts are transferred.

A spreadsheet used to draft an unadjusted trial balance,

adjusting entries, adjusted trial balance, and financial

statements.

Entries recorded at the end of each accounting period to transfer end-of-period balances in revenue, expense, and withdrawals accounts to the permanent owner's capital

account.

A list of permanent accounts and their balances from

the ledger after all closing entries are journalized and

posted. The time span from when cash is used to acquire goods and services until cash is received from the sale of those

goods and services.

Statements that show the effects of proposed transactions as if the transactions had already occurred.

136. The unadjusted trial balance of E.Pace, Consultant is entered on the partial work sheet below. Complete the work sheet using the following information:

(a) Salaries earned by employees that are unpaid and unrecorded, $500.

(b) An inventory of supplies showed $800 of unused supplies still on hand.

(c) Depreciation on equipment, $1,300.。