ACCAF4学习

ACCA F4知识点:Charge抵押详解

在ACCA F4课程中有一个非常重要的知识点:Charge抵押。

这里所提到的抵押合同就是从属合同,从属于主合同,也就是我们常说的借款合同。

如果主合同消失,附属合同也就不复存在了。

给大家举个例子说明,一家公司遇到了财务危机,需要向银行贷款,但是银行并不信任这家公司的资信,要求该公司提供一份抵押担保。

在这个案例里,公司向银行的贷款合同就是主合同,抵押担保合同就是从属合同。

那么抵押是什么呢?为什么要设立抵押担保?抵押通常是在不动产或个人资产上增设的一项负担,使得债权人对抵押物拥有一项权利;一般情况下,如果有抵押,那么债权人可以在公司资不抵债、破产清算的时候优先接受赔偿,如果借款人不能如期还款,就会被要求买卖该抵押物,清偿债权人的债务。

抵押的设立方式根据抵押权设立时抵押物是否固定,将抵押分为固定抵押和浮动抵押。

固定抵押:一旦设立抵押物,抵押权就和抵押物贴合在一起,在抵押期间抵押物保持不变。

此类型抵押物通常是land,factory or other non-current assets。

这种抵押方式的特点是债务人不能随时处置抵押物,必须要征得债权人同意;如果债务人无法到期还款,则债权人可以变卖该项抵押物,用于清偿债权;在公司破产清算时,债权人最先受偿。

浮动抵押:在抵押期间,公司可以任意处置抵押物,从而获得现金流,用于清偿债权人的债务。

如果债权人不能清偿其债务。

或是公司停业,进入破产清算阶段的话,公司要将目前的抵押物拿去变卖,清偿债权人的债务。

什么是有效抵押要想债权人要求设立的债权有效,必须去到公司注册机关注册,时间是在抵押权设立后的21天内。

否则无效,抵押担保债权人会变成无抵押担保债权人,丧失优先受偿的权利。

X。

【ACCA paper F4】(PartB2)

1.Consideration对价,又可称为约因,其含义为“法律意 1.Consideration对价,又可称为约因,其含义为“法律意 义上的对价既可以由属于某一方当事人的权利、利益、利 润或收益所构成,也可以由另一方所遭受或承担的忍耐、 损害、损失或责任、义务所构成”,或“一方之行为,或 容忍或所为之诺言,乃换取对方诺言之代价,此项诺言既 有对价关系,自属有效。” 对价的意义在于:一般来说,一项允诺须有对价支持才具 有法律约束力,或一项合同须有对价支持才可成立生效。 简单地说, 简单地说,对价是”将欲取之,必先予之”,或为获得某种利 益所应付出的代价,这种代价可以是作为(积极的行为, 如承诺支付货款)或不作为(消极的行为,如承诺不从事 某种行为) 对价也可以视为“为购买允诺所支付的成本”。对价是相 对于允诺而言的。

Formation of contracts II

禁止反言原则的适用应注意: 该原则只能用于抗辩,而不能用作起诉的理由; Combe v Combe 1951 decree nisi (non-absolute ruling,离婚暂准判令) is (nonruling,离婚暂准判令) a ruling by a court that does not have any force until such time that a particular condition is met. Once the condition is met the ruling becomes decree absolute and is binding. Typically, the condition is that no new evidence or further petitions with a bearing on the case are introduced to the court.

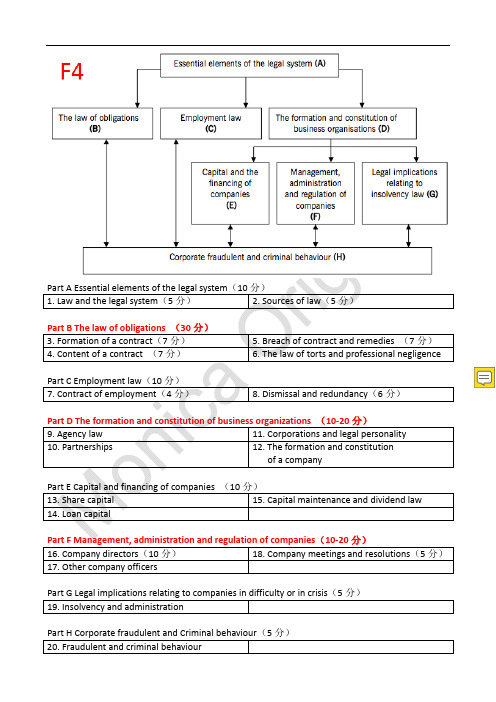

ACCA资料 f4-syllabus

Corporate and Business Law (GLO) (F4) September 2014 to August 2015( PAPER EXAM SESSIONS IN DEC 2014 AND JUN 2015. START DATE FOR CBE NOVEMBER 19 2014.)This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed inany examination session.THE STRUCTURE OF THE SYLLABUS AND STUDY GUIDERelational diagram of paper with other papersThis diagram shows direct and indirect links between this paper and other papers preceding or following it. Some papers are directly underpinned by other papers such as Advanced Performance Management by Performance Management. These links are shown as solid line arrows. Other papers only have indirect relationships with each other such as links existing between the accounting and auditing papers. The links between these are shown as dotted line arrows. This diagram indicates where you are expected to have underpinning knowledge and where it would be useful to review previous learning before undertaking study.Overall aim of the syllabusThis explains briefly the overall objective of the paper and indicates in the broadest sense the capabilities to be developed within the paper.Main capabilitiesThis paper’s aim is broken down into several main capabilities which divide the syllabus and study guide into discrete sections.Relational diagram of the main capabilitiesThis diagram illustrates the flows and links between the main capabilities (sections) of the syllabus and should be used as an aid to planning teaching and learning in a structured way.Syllabus rationaleThis is a narrative explaining how the syllabus is structured and how the main capabilities are linked. The rationale also explains in further detail what the examination intends to assess and why.Detailed syllabusThis shows the breakdown of the main capabilities (sections) of the syllabus into subject areas. This is the blueprint for the detailed study guide.Approach to examining the syllabusThis section briefly explains the structure of the examination and how it is assessed.Study GuideThis is the main document that students, learning and content providers should use as the basis of their studies, instruction and materials. Examinations will be based on the detail of the study guide which comprehensively identifies what could be assessed in any examination session.The study guide is a precise reflection and breakdown of the syllabus. It is divided into sections based on the main capabilities identified in the syllabus. These sections are divided into subject areas which relate to the sub-capabilities included in the detailed syllabus. Subject areas are broken down into sub-headings which describe the detailed outcomes that could be assessed in examinations. These outcomes are described using verbs indicating what exams may require students to demonstrate, and the broad intellectual level at which these may need to be demonstrated(*see intellectual levels below).INTELLECTUAL LEVELSThe syllabus is designed to progressively broaden and deepen the knowledge, skills and professional values demonstrated by the student on their way through the qualification.The specific capabilities within the detailed syllabuses and study guides are assessed at one of three intellectual or cognitive levels:Level 1: Knowledge and comprehensionLevel 2: Application and analysisLevel 3: Synthesis and evaluationVery broadly, these intellectual levels relate to the three cognitive levels at which the Knowledge module, the Skills module and the Professional level are assessed.Each subject area in the detailed study guide included in this document is given a 1, 2, or3 superscript, denoting intellectual level, marked at the end of each relevant line. This gives an indication of the intellectual depth at which an area could be assessed within the examination. However, while level 1 broadly equates with the Knowledge module, level 2 equates to the Skills module and level 3 to the Professional level, some lower level skills can continue to be assessed as the student progresses through each module and level. This reflects that at each stage of study there will be a requirement to broaden, as well as deepen capabilities. It is also possible that occasionally some higher level capabilities may be assessed at lower levels.LEARNING HOURS AND EDUCATION RECOGNITIONThe ACCA qualification does not prescribe or recommend any particular number of learning hours for examinations because study and learning patterns and styles vary greatly between people and organisations. This also recognises the wide diversity of personal, professional and educational circumstances in which ACCA students find themselves.As a member of the International Federation of Accountants, ACCA seeks to enhance the education recognition of its qualification on both national and international education frameworks, and with educational authorities and partners globally. Indoing so, ACCA aims to ensure that its qualifications are recognized and valued by governments, regulatory authorities and employers across allsectors. To this end, ACCA qualifications are currently recognized on the education frameworks in several countries. Please refer to your nationaleducation framework regulator for further information.Each syllabus contains between 23 and 35 main subject area headings depending on the nature of the subject and how these areas have been brokendown.GUIDE TO EXAM STRUCTUREThe structure of examinations varies within and between modules and levels.The Fundamentals level examinations contain 100% compulsory questions to encouragecandidates to study across the breadth of each syllabus.The Knowledge module is assessed by equivalent two-hour paper based and computer based examinations.The Skills module examinations F5-F9 are all paper based three-hour papers containing a mix ofobjective and longer type questions. The Corporate and Business Law (F4) paper is a two- hourcomputer based objective test examination which isalso available as a paper based version from the December 2014 examination session.The Professional level papers are all three-hour paper based examinations, all containing two sections. Section A is compulsory, but there will be some choice offered in Section B.For all three hour examination papers, ACCA has introduced 15 minutes reading and planning time.This additional time is allowed at the beginning of each three-hour examination to allow candidates to read the questions and to begin planning their answers before they start writing in their answer books. This time should be used to ensure that all the information and exam requirements are properly read and understood.During reading and planning time candidates may only annotate their question paper. They may not write anything in their answer booklets until told to do so by the invigilator.The Essentials module papers all have a Section A containing a major case study question with all requirements totalling 50 marks relating to this case. Section B gives students a choice of two from three 25 mark questions.Section A of both the P4 and P5 Options papers contain one 50 mark compulsory question, and Section B will offer a choice of two from three questions each worth 25 marks each.Section A of each of the P6 and P7 Options papers contains 60 compulsory marks from two questions; question 1 attracting 35 marks, and question 2 attracting 25 marks. Section B of both these Options papers will offer a choice of two from three questions, with each question attracting 20 marks. All Professional level exams contain four professional marks.The pass mark for all ACCA Qualification examination papers is 50%. GUIDE TO EXAMINATION ASSESSMENTACCA reserves the right to examine anything contained within the study guide at any examinationsession. This includes knowledge, techniques, principles, theories, and concepts as specified.For the financial accounting, audit and assurance, law and tax papers except where indicated otherwise, ACCA will publish examinable documents once a year to indicate exactlywhat regulations and legislation could potentially be assessed within identified examination sessions.. For paper based examinations regulation issued or legislation passed on or before 31st August annually, will be examinable from 1st September of the following year to 31st August t of the year after that. Please refer to the examinable documents for the paper (where relevant) for further information.Regulation issued or legislation passed in accordance with the above dates may be examinable even if the effective date is in the future. The term issued or passed relates to when regulation or legislation has been formally approved. The term effective relates to when regulation or legislation must be applied to an entity transactions and business practices.The study guide offers more detailed guidance on the depth and level at which the examinable documents will be examined. The study guide should therefore be read in conjunction with the examinable documents list.SyllabusAIM To develop knowledge and skills in the understanding of the general legal framework within which international business takes place, and of specific legal areas relating to business, recognising the need to seek further specialist legal advice where necessary. MAIN CAPABILITIES On successful completion of this paper candidates should be able to: A Identify the essential elements of different l egal systems including the main sources of l aw, the relationship between the different b ranches of a state’s constitution, and the need f or international legal regulation, and e xplain the roles of international organisations in the promotion and regulation of international trade, and the role of international arbitration as an alternative to court adjudicationB Recognise and apply the appropriate legal rules applicable under the United Nations Convention on Contracts for the International Sale of Goods, and explain the various ways in which international business transactions can be fundedC Recognise different types of international business formsD Distinguish between the alternative forms and constitutions of b usiness organisationsE Recognise and compare types of capital and the financing of companiesF Describe and explain how companies are managed, administered and regulatedG Recognise the legal implications relating to insolvency lawH Demonstrate an understanding of corporate and fraudulent behaviourRELATIONAL DIAGRAM OF MAIN CAPABILITIES(A) Essential elements of legal systems(B) International business transactions transactions (E) Capital and the financing of companies (H) Corporate fraudulent and criminal behaviour(F) Management, administration and regulation of companies (C) Transportation and payment of international business transactions (D) The formation and constitution of business organisations(G) Insolvency law FR (F7) CR (P2) CL (F4) AA (F8)RATIONALECorporate and Business Law Global is divided into eight areas. The syllabus starts with an introduction to different legal systems, different types of law and those organisations which endeavour to promote internationally applicable laws. It also introduces arbitration as an alternative to court adjudication.It then leads into an examination of the substantive law as stated in UN Convention on Contracts for the International Sale of Goods, which relates to the formation, content and discharge of international contracts for the sale of goods.The syllabus then covers a range of specific legal areas relating to various aspects of international business of most concern to finance professionals. These are the law relating to the financing of international transactions, and the various legal forms through which international business transactions may be conducted. Particular attention is focused on the law relating to companies. Aspects examined include the formation and constitution of companies, the financing of companies and types of capital, and the day–to-day management, the administration and regulation of companies and legal aspects of insolvency law.The final section links back to all the previous areas. This section deals with corporate fraudulent and criminal behaviour.DETAILED SYLLABUSA Essential elements of legal systems1. Business, political and legal systems2.International trade, international legalregulation and conflict of laws3. Alternative dispute resolution mechanismsB International business transactions1. Introduction to the UN Convention onContracts for the International Sale of Goodsand ICC Incoterms2. Obligations of the seller and buyer, andprovisions common to bothC Transportation and payment of internationalbusiness transactions1. Transportation documents and means ofpaymentD The formation and constitution of businessorganisations1. Agency law2.Partnerships3. Corporations and legal personality4. The formation and constitution of a companyE Capital and the financing of companies1.Share capital2. Loan capital3. Capital maintenance and dividend lawF Management, administration and the regulationof companies1. Company directors2. Other company officers3. Company meetings and resolutions G Insolvency law1.Insolvency and administrationH Corporate fraudulent and criminal behaviour1. Fraudulent and criminal behaviourAPPROACH TO EXAMINING THE SYLLABUSThe syllabus is assessed by a two-hour paper-based examination, and is also offered as a computer-based examination.The examination consists of:Section A-25 x 2 mark objective test questions 50%-20 x 1 mark objective questions 20% Section B- 5 x 6 mark multi-task questions 30% 100%All questions are compulsory.NOTE ON CASE LAWCandidates should support their answers on the paper-based multi-task questions withanalysis referring to cases or examples. There is no need to detail the facts of the case. Remember, it is the point of law that the case establishes that is important, although knowing the facts of cases can be helpful as sometimes questions include scenarios based on well-known cases. Further it is not necessary to quote section numbers of Acts.Study GuideA ESSENTIAL ELEMENTS OF LEGAL SYSTEMS1. Business, political and legal systemsa)Explain the inter-relationship of economic and political and legal systems.[2]b)Explain the doctrine of the separation ofpowers and its impact on the legal system.[2] c)Explain the distinction between criminal andcivil law.[1]d)Outline the operation of the following legalsystems:[1]i) Common lawii) Civil lawiii) Sharia law.2. International trade, international legalregulation and conflict of lawsa)Explain the need for international legalregulation in the context of conflict of laws.[1] b)Explain the function of international treaties,conventions and model codes.[1]c)Explain the roles of international organisations,such as the UN, the ICC, the WTO, the OECD, UNIDROIT, UNCITRAL and courts in thepromotion and regulation of internationaltrade.[1]3. Alternative dispute resolution mechanismsa)Explain the operation, and evaluate the distinctmerits, of court-based adjudication andalternative dispute resolution mechanisms.[2] b)Explain the role of the international courts oftrade including the International Court ofArbitration .[1]c) Explain and apply the provisions of theUNCITRAL Model Law on InternationalCommercial Arbitration.[2]d) Describe the arbitral tribunal. [2]e) Explain arbitral awards. [2]B INTERNATIONAL BUSINESS TRANSACTIONS1. Introduction to the UN Convention onContracts for the International Sale of Goodsand ICC Incotermsa)Explain the sphere of application and generalprovisions of the Convention.[1]b)Explain and be able to apply the rules forcreating contractual relations under theConvention.[2]c)Explain the meaning and effect of the ICCIncoterms.[1]2. Obligations of the seller and buyer, andprovisions common to botha)Explain and be able to apply the rules relatingto the obligations of the seller under theConvention:[2]i) delivery of goods and handing overdocumentsii) conformity of the goods and third partyclaimsiii) remedies for breach of contract by theseller.b) Explain and be able to apply the rules relatingto the obligations of the buyer under theConvention:[2]i) payment of the priceii) taking deliveryiii) remedies for breach of contract by thebuyer.c) Explain and be able to apply the rules relatingto the provisions common to both the sellerand the buyer under the Convention:[2]i) anticipatory breach and instalmentcontractsii) damagesiii) interestiv) exemptionsv) effects of avoidancevi) preservation of the goods.d) Explain and be able to apply the rules relatingto the passing of risk under the Convention.[2]C TRANSPORTATION AND PAYMENT OFINTERNATIONAL BUSINESS TRANSACTIONS 1. Transportation documents and means ofpaymenta) Define and explain the operation of bills oflading.[1]b) Explain the operation of bank transfers.[1]c) Explain and be able to apply the rules ofUNCITRAL Model Law on International CreditTransfer.[2]d) Explain and be able to apply the rules of theUN Convention on International Bills OfExchange And International PromissoryNotes.[2]e) Explain the operation of letters of credit andletters of comfort.[12D FORMATION AND CONSTITUTION OFBUSINESS ORGANISATIONS1. Agency lawa)Define the role of the agent and give examplesof such relationships paying particular regardto partners and company directors.[2]b) Explain the formation of the agencyrelationship.[2]c) Define the authority of the agent.[2]d) Explain the potential liability of both principaland agent.[2]2. Partnershipsa)Demonstrate a knowledge of the legislationgoverning the partnership, both unlimited andlimited.[1]b)Discuss the formation of a partnership .[2]c)Explain the authority of partners in relation topartnership activity.[2]d)Analyse the liability of various partners forpartnership debts.[2]e)Explain the termination of a partnership, andpartners’ subsequent rights and liabilities.[2]3. Corporations and legal personalitya)Distinguish between sole traders, partnershipsand companies.[1]b)Explain the meaning and effect of limitedliability.[2]c)Analyse different types of companies,especially private and public companies.[1] d)Illustrate the effect of separate personality andthe veil of incorporation.[2]e)Recognise instances where separatepersonality will be ignored (lifting the veil ofincorporation).[2]4. The formation and constitution of a companya)Explain the role and duties of companypromoters, and the breach of those duties and remedies available to the company.[2]b)Explain the meaning of, and the rules relatingto, pre-incorporation contracts.[2]c)Describe the procedure for registeringcompanies, both public and private.[1]d)Describe the statutory books, records andreturns that companies must keep or make.[1] e) Analyse the effect of a company’sconstitutional documents.[2]f) Describe the contents of the model articles ofassociation.[1]g) Explain how the articles of association can bechanged.[2]h) Explain the control over the names thatcompanies may or may not use.[2]E CAPITAL AND THE FINANCING OFCOMPANIES1. Share capitala)Examine the different types of capital.[2]b)Illustrate the difference between variousclasses of shares, including treasury shares,the procedure for altering class rights.[2]c)Explain allotment of shares, and distinguishbetween rights issue and bonus issue ofshares.[2]d)Examine the effect of issuing shares at either adiscount, or at a premium.[2]2. Loan capitala)Define companies’ borrowing powers.[1]b)Explain the meaning of loan capital anddebenture.[2]c)Distinguish loan capital from share capital andexplain the different rights held by shareholders and debenture holders.[2]d)Explain the concept of a company charge anddistinguish between fixed and floatingcharges.[2]e)Describe the need, and the procedure for,registering company charges.[2]3. Capital maintenance and dividend lawa)Explain the doctrine of capital maintenanceand capital reduction.[2]b)Explain the rules governing the distribution ofdividends in both private and publiccompanies.[2]F MANAGEMENT, ADMINISTRATION ANDREGULATION OF COMPANIES1. Company directorsa)Explain the role of directors in the operation ofa company, and the different types of directors,such as executive/ non-executive directors orde jure and de facto directors .[2]b)Discuss the ways in which directors areappointed, can lose their office and thedisqualification of directors.[2]c)Distinguish between the powers of the board ofdirectors, the managing director/chief executive and individual directors to bind theircompany.[2]d)Explain the duties that directors owe to theircompanies.[2]2. Other company officersa)Discuss the appointment procedure relating to,and the duties and powers of, a companysecretary.[2]b)Discuss the appointment procedure relating to,and the duties and rights of, a companyauditor, and their subsequent removal orresignation.[2]3. Company meetings and resolutionsa)Distinguish between types of meetings:general meetings and annual generalmeetings.[1]b)Distinguish between types of resolutions:ordinary, special and written.[2]c)Explain the procedure for calling andconducting company meetings.[2]G INSOLVENCY LAW1 Insolvency and administrationa)Explain the meaning of, and procedureinvolved, in voluntary liquidation, includingmembers’ and creditors’ voluntaryliquidation.[2]b)Explain the meaning of, the grounds for andthe procedure involved, in compulsoryliquidation.[2]c)Explain the order in which company debts willbe paid off on liquidation .[2]d) Explain administration as an alternative toliquidation.[2]e) Explain the way in which an administrator maybe appointed, the effects of such appointment,and the powers and duties of anadministrator.[2]H CORPORATE FRAUDULENT AND CRIMINALBEHAVIOUR1 Fraudulent and criminal behavioura)Recognise the nature and legal control overinsider dealing .[2]b)Recognise the nature and legal control overmarket abuse.[2]c)Recognise the nature and legal control overmoney laundering.[2]d)Recognise the nature and legal control overbribery.[2]e)Discuss potential criminal activity in theoperation, management and liquidation ofcompanies.[2]f)Recognise the nature and legal control overfraudulent and wrongful trading.[2]11© ACCA 2014 All rights reserved.SUMMARY OF CHANGES TO F4 GLOACCA periodically reviews its qualification syllabuses so that they fully meet the needs of stakeholders such asemployers, students, regulatory and advisory bodies and learning providers.The main areas that have been deleted from the syllabus are shown in Table 1 below:Table 1 – Deletions to F4 GLOSection and subject area Syllabus contentG1d) Insolvency The rules in the 1997 UNCITRAL Model Law on Cross-Border InsolvencyG2b) Administration Comparison of administration and Chapter 11protectionH1a) Corporate governance The idea of corporate governanceH1b) Corporate governance The extra-legal codes of corporate governanceH1c) Corporate governance The legal regulation of corporate governance:12© ACCA 2014 All rights reserved.。

ACCA

一,ACCA对中国学员的免试政策金融专业免试5门课程(F1-F5)会计学–获得学士学位免试5门课程(F1-F5)会计学–辅修专业免试3门课程(F1-F3)二,ACCA目前的科目设置如下,共16门(学员需通过12门必修科目及2门选修科目共14门课程)(F只需有四级水平,P需要更高的英语能力)1.知识课程FUNDAMENTALS--KNOWLEDGEF1 会计师与企业 Accountant in Business (AB)F2 管理会计 Management Accounting (MA)F3 财务会计 Financial Accounting (FA)2.技能课程 FUNDAMENTALS—SKILLSF4 公司法与商法 Corporate and Business Law (CL)F5 业绩管理 Performance Management (PM)F6 税务 Taxation (TX)F7 财务报告 Financial Reporting (FR)F8 审计与认证业务 Audit and Assurance (AA)F9 财务管理 Financial Management (FM)专业阶段3.职业核心课程 PROFESSIONAL—ESSENTIALSP1 公司治理、风险和职业道德 Governance, Risk & Ethics (GRE)P2 公司报告 Corporate Reporting (CR)P3 商务分析 Business Analysis (BA)4.职业选修课程 PROFESSIONAL-- OPTIONS(四门任选二门)P4 高级财务管理Advanced Financial Management (AFM)P5 高级业绩管理 Advanced Performance Management。

有心企业高层P6 高级税务 Advanced Taxation (ATX)。

ACCA-(F4)知识点之议会主权(Parliamentary sovereignty)

高顿财经ACCA ACCA-(F4)知识点之议会主权(

Parliamentary sovereignty )

本文由高顿ACCA 整理发布,转载请注明出处 ACCA-(F4)知识点之议会主权(Parliamentary sovereignty )

议会主权带来了如下的结果。

议会可以撤销之前的法规;否决或者更改由法庭发展而来的案例法;制作新的法条。

但是在实践中,议会同样会遵守一定的传统和惯例,这也在很大程度上限制了它的自由。

例如,没有一届议会可以通过立法来防止将来的议会来改变法律;法官需要陈述成文法中的条文并且从中找出适合正在解决的案例的说法;议会立法的效力和合法性是不容置疑的,但是法官也可以利用欧洲人权法对其进行“抵抗”。

更多ACCA 资讯请关注高顿ACCA 官网:。

【分享】【最新】ACCA LW(F4)专业词汇中英对照

【分享】【最新】ACCA LW(F4)专业词汇中英对照中国学生刚刚接触ACCA时面临的困难主要来自两方面:一个是英文教材的使用,二是长期以来形成的针对中国考试固有的思维方式。

第二个问题需要经过一段时间的学习和做题慢慢掌握英文考试的解题思路,熟悉ACCA的作答模式。

对于提高英语水平这个问题,我们可以先从掌握ACCA 词汇入手,逐渐了解专业名词的表达方式,进而能够在阅读教材时减少一些障碍,方便理解知识内容。

本文和大家分享的是ACCA初级阶段F4涉及的词汇,帮助大家快速入门高效学习。

(一)1. Apparent authority:表面权限Apparent authority is the authority which an agent appears to have to a third party. A contract made within the scope of such authority will bind the principal even though the agent was not following their instructions.2. Appeal court:上诉法院The appeal court is the court to which an appeal is made against the ruling or the sentence.3. Ante-natal care:产前护理Ante-natal care is an employee has a right not to be unreasonably refused time off for ante-natal care during working hours.4. Civil court:民事法庭In a civil suit, one party who feels they were harmed brings a complaint against another party.5. Civil law:民法Civil law exists to regulate disputes over the rights and obligations of persons dealing with each other and seeks to compensate injured parties.6. Collateral contract:附属合同A collateral contract is a contract where consideration is provided by the making of another contract. For example, if there are two separate contracts, one between A andB and one between A and C, on terms which involve some concerted action between B and C, there may be a contract between B and C.7. Common law:习惯法Common law is the body of legal rules common to the whole country which is embodied in judicial decisions.8. Consideration:对价Consideration is an essential part of most contracts. It is what each party brings to the contract.9. Constructive dismissal:推定解雇Constructive dismissal is where the employer commits a breach of contract, thereby causing the employee to resign. By implication, this is also dismissal without notice.10. Contextual rule:关联规则The contextual rule means that a word should be construed in its context: it is permissible to look at the statute as a whole to discover the meaning of a word in it.11. Contributory negligence:共同过失A court may reduce the amount of damages paid to the claimant if the defendant establishes that they contributed to their own injury or loss, this is known as contributory negligence.12. Counter-offer:反要约A counter-offer is a final rejection of the original offer. If a counter-offer is made, the original offeror may accept it, but if they reject it, their original offer is no longer available for acceptance.(二)13. County Court:地方法院County Courts hear claims in contract and tort, equitable matters and land and probate disputes among others.14. Court of Appeal:上诉法院The Court of Appeal hears appeals from the County Court, the High Court, the Restrictive Practices Court and the Employment Appeal Tribunal.15. Criminal law:刑法In criminal cases, the state prosecutes the wrongdoer.16. Crown Court:刑事法庭The Crown Court hears appeals from Magistrates' Courts.17. Declaration of solvency:有偿付能力的声明A voluntary winding up is a members' voluntary winding up only if the directors make and deliver to the Registrar a declaration of solvency.18. Duty of care:谨慎义务In the landmark case of Donoghue v Stevenson 1932 the House of Lords ruled that a person might owe a duty of care to another with whom they had no contractual relationship at all. The doctrine has been refined in subsequent rulings, but the principle is unchanged.19. Equity:衡平法Equity is a term which applies to a specific set of legal principles which were developed by the Court of Chancery to supplement (but not replace) the common law. It is based on fair dealings between the parties. It added to and improved on the common law by introducing the concept of fairness.20. Exclusion clause:除外条款An exclusion clause may attempt to restrict one party's liability for breach of contract or for negligence.21. Express authority:明示权限Express authority is a matter between principal and agent. This is authority explicitly given by the principalto the agent to perform particular tasks, along with the powers necessary to perform those tasks.22. Exemption clauses:免责条款An exclusion clause may attempt to restrict one party's liability for breach of contract or for negligence.23. Executed consideration:已履行的对价Executed consideration is an act in return for a promise such as paying for goods when the shopkeeper hands them over.24. Executory consideration:待履行的对价Executory consideration is a promise given for a promise, such as promising to pay for goods that the shopkeeper puts on order for you.25. liquidation:清算Liquidation means that the company must be dissolved and its affairs 'wound up', or brought to an end.。

ACCA F4知识要点 第9章

第9章 Agency law 代理合同1.代理的角色The Principal is the person who has legally empowered the Agent to enter into contractual relations with a Third Party. 代理是作为法定第三方,介入合同中。

The contract itself though is between the Principal and the third party. Two specific examples of agency relationships:•(a) Partners–per the Partnership Act 1890 all partners are deemed to be agents of the firm and are hence able to bind all co‐partners and make them jointly and severally liable for business transactions。

Accountancy practices are run as partnerships by partners. 所有的合伙人都是合伙企业的代理人,一个合伙人的行为,也会约束到其他合伙人,共同承担责任/也承担连带责任。

对外负责,对内可以向其他合伙人追偿。

•(b) Company Directors –the board of directors are deemed to be the agent of the company (though not the shareholders) and can therefore bind the company without personal liability. Individual directors do not have the power to bind the company unless they have derived any of the powers of agency. 公司的董事会成员未必是公司的股东,其行为公司承担责任,个人无需承担责任(正常情况下)。

ACCA F4-F9模拟题及解析(5)

ACCA F4-F9模拟题及解析(5)1. (a) In order for auditors to operate effectively and to provide an opinion on an entity’s financial statements, they are given certain rights.Required:State THREE rights of an auditor, excluding those related to resignation and removal. (3 marks) (b) HKSA 315 Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment requires auditors to obtain an understanding of control activities relevant to the audit.Control activities are the policies and procedures that help ensure that management directives are carried out;and which are designed to prevent and detect fraud and error occurring. An example of a control activity is themaintenance of a control account.Required:Apart from maintenance of a control account, explain FOUR control activities a company may undertake to prevent and detect fraud and error. (4 marks)(c) Describe THREE limitations of external audits. (3 marks)(10 marks)2. Sunflower Stores Co (Sunflower) operates 25 food supermarkets. The company’s year end is 31 December 2012.The audit manager and partner recently attended a planning meeting with the finance director and have provided you with the planning notes below.You are the audit senior, and this is your first year on this audit. In order to familiarise yourself with Sunflower, the audit manager has asked you to undertake some research in order to gain an understanding of Sunflower, so that you are able to assist in the planning process. He has then asked that you identify relevant audit risks from the notes below and also consider how the team should respond to these risks.Sunflower has spent $1·6 million in refurbishing all of its supermarkets; as part of this refurbishment programme their central warehouse has been extended and a smaller warehouse, which was only occasionally used, has been disposed of at a profit. In order to finance this refurbishment, a sum of $1·5 million was borrowed from the bank.This is due to be repaid over five years.The company will be performing a year-end inventory count at the central warehouse as well as at all 25 supermarkets on 31 December. Inventory is valued at selling price less an average profit margin as the finance director believes that this is a close approximation to cost.Prior to 2012, each of the supermarkets maintained their own financial records and submitted returns monthly to head office. During 2012 all accounting records have been centralised within head office. Therefore at the beginning of the year, each supermarket’s opening balances were transferred into head office’s accounting records. The increased workload at head office has led to some changes in the finance department and in November 2012 the financial controller left. His replacement will start in late December.Required:(a) List FIVE sources of information that would be of use in gaining an understanding of Sunflower Stores Co,and for each source describe what you would expect to obtain. (5 marks)(b) Using the information provided, describe FIVE audit risks and explain the auditor’s response to each risk in planning the audit of Sunflower Stores Co. (10 marks)(c) The finance director of Sunflower Stores Co is considering establishing an internal audit department.Required:Describe the factors the finance director should consider before establishing an internal audit department.(5 marks)(20 marks)3.(a) Identify and explain each of the FIVE fundamental principles contained within ACCA’s Code of Ethics and Conduct. (5 marks)(b) Rose Leisure Club Co (Rose) operates a chain of health and fitness clubs. Its year end was31 October 2012.You are the audit manager and the year-end audit is due to commence shortly. The following three matters have been brought to your attention.(i) Trade payables and accruals Rose’s finance director has notified you that an error occurred in the closing of the purchase ledger at the year end. Rather than it closing on 1 November, it accidentally closed one week earlier on 25 October. All purchase invoices received between 25 October and the year end have been posted to the 2013 year-end purchase ledger. (6 marks) (ii) Receivables Rose’s trade receivables have historically been low as most members pay monthly in advance. However, during the year a number of companies have taken up group memberships at Rose and hence the receivables balance is now material. The audit senior has undertaken a receivables circularisation for the balances at the year end; however, there are a number who have not responded and a number of responses with differences. (5 marks)(iii) Reorganisation The company recently announced its plans to reorganise its health and fitness clubs. This will involve closing some clubs for refurbishment, retraining some existing staffand disposing of some surplus assets. These plans were agreed at a board meeting in October and announced to their shareholders on 29 October. Rose is proposing to make a reorganisation provision in the financial statements. (4 marks)Required:Describe substantive procedures you would perform to obtain sufficient and appropriate audit evidence in relation to the above three matters.Note: The mark allocation is shown against each of the three matters above.(20 marks)4.(a) Explain the purpose of, and procedures for, obtaining written representations. (5 marks)(b) The directors of a company have provided the external audit firm with an oral representation confirming that the bank overdraft balances included within current liabilities are complete. Required:Describe the relevance and reliability of this oral representation as a source of evidence to confirm the completeness of the bank overdraft balances. (3 marks)(c) You are the audit manager of Violet & Co and you are currently reviewing the audit files for several of your clients for which the audit fieldwork is complete. The audit seniors have raised the following issues:Daisy Designs Co (Daisy)Daisy’s year end is 30 September, however, subsequent to the year end the company’s sales ledger has been corrupted by a computer virus. Daisy’s finance director was able to produce the financial statements prior to this occurring; however, the audit team has been unable to access the sales ledger to undertake detailed testing of revenue or year-end receivables. All other accounting records are unaffected and there are no backups available for the sales ledger. Daisy’s revenue is $15·6m, its receivables are $3·4m and profit before tax is $2m.Fuchsia Enterprises Co (Fuchsia)Fuchsia has experienced difficult trading conditions and as a result it has lost significant market share. The cash flow forecast has been reviewed during the audit fieldwork and it shows a significant net cash outflow.Management are confident that further funding can be obtained and so have prepared the financial statements on a going concern basis with no additional disclosures; the audit senior is highly sceptical about this. The prior year financial statements showed a profit before tax of $1·2m; however, the current year loss before tax is $4·4m and the forecast net cash outflow for the next 12 months is $3·2m.Required:For each of the two issues:(i) Discuss the issue, including an assessment of whether it is material;(ii) Recommend procedures the audit team should undertake at the completion stage to try to resolve the issue; and(iii) Describe the impact on the audit report if the issue remains unresolved.Notes: 1 The total marks will be split equally between each issue.2 Audit report extracts are NOT required. (12 marks)(20 marks)试题及答案1.(a)Auditors’ rights– Right of access at all times to the company’s books, accounts and vouchers.– Right to require from an officer of the company such information or explanations as they think necessary for the performance of their duties as auditors.– Right to receive all communications relating to written resolutions.– Right to receive all notices of, and other communications relating to, any general meeting which a member of the company is entitled to receive.– Right to attend any general meeting of the company.– Right to be heard at any general meeting which an auditor attends on any part of the business of the meeting which concerns them as auditor.(b) Control activities Segregation of duties – assignment of roles/responsibilities to different people, thereby reducing the risk of fraud and error occurring.Information processing – computer controls including general IT controls, which cover a range of applications and support the overall IT environment and application controls which are manual or automated controls which operate on a cycle/business process level.Authorisation – approval of transactions by a suitably responsible official to ensure transactions are genuine.Physical controls – restricting access to physical assets such as cash, inventory and plant and equipment, thereby reducing the risk of theft.Performance reviews – comparison or review of the performance of the business by looking at areas such as budget v actual results.Arithmetical controls – controls which check the arithmetical accuracy of accounting records. Account reconciliations – comparison of an account balance with another source; often this source is from a third party, such as the bank, with differences being investigated.(c)Limitations of external auditsAn external audit has a number of limitations which reduce its usefulness:Sampling – it is not practical for an auditor to test 100% of transactions and so they have to apply sampling methodologies in selecting balances/transactions to test. Therefore, there could be an error in an item not selected for testing by the auditor.Subjectivity – financial statements include judgemental and subjective areas and therefore the auditor is required to use their judgement in assessing whether the financial statements are true and fair.Inherent limitations of internal control systems – an internal control system is operated by people and hence is liable to human error. In addition, there is the possibility of controls override by management and of collusion and fraud. It is impossible to remove all of these inherent limitations and as the auditor relies on the internal control systems, this can reduce the usefulness of the audit.Evidence is persuasive not conclusive – the opinion is based on audit evidence gathered; however, while this evidence can indicate possible issues affecting the audit opinion, evidence involves estimates and judgements and hence does not give a definite conclusion.Audit report format – the format of the opinion is determined by International Standards on Auditing. However, the terminology used is not usually understood by non-accountants. This means that users may not actually understand the audit opinion given.Historic information – the audit report is often issued some time after the year end, and so the financial information can be quite different to the current position. In the current marketplace where companies’ financial positions can change quite quickly, the audit opinion may no longer be relevant as it is out of date.2 (a)Understanding an entitySource of information Information expect to obtainPrior year audit file Identification of issues that arose in the prior year audit and howthese were resolved. Also whether any points brought forward were noted for consideration for this year’s audit.Prior year financial statements Provides information in relation to the size of the entity as well as the key accounting policies and disclosure notes.Accounting systems notes Provides information on how each of the key accounting systems operates.Discussions with management Provides information in relation to any important issues which havearisen or changes to the company during the year.Current year budgets and management Provides relevant financial information for the year to date. Will help accounts of Sunflower Stores Co (Sunflower) the auditor to identify whether Sunflower has changed materially since last year. In addition, this will be useful for preliminary analytical review and risk identification.Permanent audit file Provides information in relation to matters of continuing importancefor the company and the audit team, such as statutory books information or important agreements. Sunflower’s website Recent press releases from the company may provide background on changes to the business during the year as this could lead to additional audit risks.Prior year report to management Provides information on the internal control deficiencies noted in the prior year; if these have not been rectified by management then theycould arise in the current year audit as well.Financial statements of competitors This will provide information about Sunflower’s competitors, in relation to their financial results and their accounting policies. This will be important in assessing Sunflower’s performance in the year and also when undertaking the going concern review.(b)Audit risks and auditor responses Audit risk Auditor response Sunflower has spent $1·6m on refurbishing its 25 food supermarkets. This expenditure needs to be reviewed to assess whether it is of a capital nature and should be included within non-current assets or expensed as repairs. Review a breakdown of the costs and agree to invoices to assess the nature of the expenditure and, if capital, agree to inclusion within the asset register and, if repairs, agree tothe income statement.During the year a small warehouse has been disposed of at a profit. The asset needs to have been correctly removed from property plant and equipment to ensure the non-current asset register is not overstated, and the profit on disposal should be included within the income statement. Review the non-current asset register to ensure that the asset has been removed. Also confirm the disposal proceeds as well as recalculating the profit on disposal.Consideration should be given as to whether the profit on disposal is significant enough to warrant separate disclosure within the income statement.Sunflower has borrowed $1·5m from the bank via a five year loan. This loan needs to be correctly split between current and non-current liabilities.In addition, Sunflower may have given the bank a charge over its assets as security for the loan. There is a risk that the disclosure of any security given is not complete.During the audit the team would need to confirm that the $1·5m loan finance was received. In addition, the split between current and non-current liabilities and the disclosures for this loanshould be reviewed in detail to ensure compliance with relevant accounting standards.The loan agreement should be reviewed to ascertain whether any security has been given, and this bank should be circularised as part of the bank confirmation process.Sunflower will be undertaking a number of simultaneous inventory counts on 31 December including the warehouse and all 25 supermarkets. It is not practical for the auditor to attend all of these counts; hence it may not be possible to gain sufficient appropriate audit evidence over inventory counts.The team should select a sample of sites to visit. It is likely that the warehouse contains most goods and therefore should be selected. In relation to the 25 supermarkets, the team should visit those with material inventory balances and/or those with a history of inventory count issues.(c)Internal audit departmentPrior to establishing an internal audit (IA) department, the finance director of Sunflower should consider the following:(i) The costs of establishing an IA department will be significant, therefore prior to committing to these costs and management time, a cost benefit analysis should be performed.(ii) The size and complexity of Sunflower should be considered. The larger, more complex and diverse a company is, then the greater the need for an IA department. At Sunflower there are 25 supermarkets and a head office and therefore it would seem that the company is diverse enough to gain benefit from an IA department.(iii) The role of any IA department should be considered. The finance director should consider what tasks he would envisage IA performing. He should consider whether he wishes them to undertake inventory counts at the stores, or whether he would want them to undertake such roles as internal controls reviews.(iv) Having identified the role of any IA department, the finance director should consider whether there are existing managers or employees who could perform these tasks, therefore reducing the need to establish a separate IA department.(v) The finance director should assess the current control environment and determine whether there are departments or stores with a history of control deficiencies. If this is the case, then it increases the need for an IA department.(vi) If the possibility of fraud is high, then the greater the need for an IA department to act as both a deterrent and also to possibly undertake fraud investigations. As Sunflower operates 25 food supermarkets, it will have a significant risk of fraud of both inventory and cash.3. (a)Fundamental principlesIntegrity –to be straightforward and honest in all professional and business relationships. Objectivity–to not allow bias, conflict of interest or undue influence of others to override professional or business judgements.Professional Competence and Due Care – to maintain professional knowledge and skill at the level required to ensure that a client receives competent professional services, and to act diligently and in accordance with applicable technical and professional standards.Confidentiality – to respect the confidentiality of information acquired as a result of professional and business relationships and, therefore, not to disclose any such information to third parties without proper authority, nor use the information for personal advantage. Professional Behaviour – to comply with relevant laws and regulations and avoid any action that discredits the profession.15Audit risk Auditor response Sunflower’s inventory valuation policy is selling price less average profit margin. Inventory should be valued at the lower of cost and net realisable value (NRV) and if this is not the case, then inventory could be under or overvalued.HKAS 2 Inventories allows this as an inventory valuation method as long as it is a close approximation to cost. If this is not the case, then inventory could be under or overvalued.Testing should be undertaken to confirm cost and NRV of inventory and that on a line-by-line basis the goods are valued correctly.In addition, valuation testing should focus on comparing the cost of inventory to the selling price less margin to confirm whether this method is actually a close approximation to cost. The opening balances for each supermarket have been transferred into the head office’s accounting records at the beginning of the year. There is a risk that if this transfer has not been performed completely and accurately, the opening balances may not be correct.Discuss with management the process undertaken to transfer the data and the testing performed to confirm the transfer was complete and accurate.Computer-assisted audit techniques could be utilised by the team to sample test the transfer of data from each supermarket to head office to identify any errors.There has been an increased workload for the finance department, the financial controller has left and his replacement will only start in late December.This increases the inherent risk within Sunflower as errors may have been made within the accounting records by the overworked finance team members. The new financial controller may not be sufficiently experienced to produce the financial statements and resolve any audit issues.The team should remain alert throughout the audit for dditional errors within the financedepartment.In addition, discuss with the finance director whether he will be able to provide the team with assistance for any audit issues the new financial controller is unable to resolve.(b)Substantive procedures(i)Trade payables and accruals– Calculate the trade payable days for Rose Leisure Clubs Co (Rose) and compare to prior years, investigate any significant difference, in particular any decrease for this year.– Compare the total trade payables and list of accruals against prior year and investigate any significant differences.– Discuss with management the process they have undertaken to quantify the understatement of trade payables due to the cut-off error and consider the materiality of the error.– Discuss with management whether any correcting journal entry has been included for the understatement.– Select a sample of purchase invoices received between the period of 25 October and the year end and follow them through to inclusion within accruals or as part of the trade payables journal adjustment.– Review after date payments; if they relate to the current year, then follow through to the purchase ledger or accrual listing to ensure they are recorded in the correct period.– Obtain supplier statements and reconcile these to the purchase ledger balances, and investigate any reconciling items.– Select a sample of payable balances and perform a trade payables’ circularisation, follow up any non-replies and any reconciling items between the balance confirmed and the trade payables’ balance.– Select a sample of goods received notes before the year end and after the year end and follow through to inclusion in the correct period’s payables balance, to ensure correct cut-off. (ii)Receivables– For non-responses, with the client’s permission, the team should arrange to send a follow up circularisation.– If the receivable does not respond to the follow up, then with the client’s permission, the senior should telephone the customer and ask whether they are able to respond in writing to the circularisation request.– If there are still non-responses, then the senior should undertake alternative procedures to confirm receivables.– For responses with differences, the senior should identify any disputed amounts, and identifywhether these relate to timing differences or whether there are possible errors in the records of Rose.– Any differences due to timing, such as cash in transit, should be agreed to post year-end cash receipts in the cash book.– The receivables ledger should be reviewed to identify any possible mispostings as this could be a reason for a response with a difference.– If any balances have been flagged as disputed by the receivable, then these should be discussed with management to identify whether a write down is necessary.(iii)Reorganisation– Review the board minutes where the decision to reorganise the business was taken, ascertain if this decision was made pre year end.– Review the announcement to shareholders in late October, to confirm that this was announced before the year end.– Obtain a breakdown of the reorganisation provision and confirm that only direct expenditure from restructuring is included.– Review the expenditure to confirm that there are no retraining costs included.– Cast the breakdown of the reorganisation provision to ensure correctly calculated.– For the costs included within the provision, agree to supporting documentation to confirm validity of items included.– Obtain a written representation confirming management discussions in relation to the announcement of the reorganisation.– Review the adequacy of the disclosures of the reorganisation in the financial statements to ensure they are in accordance with HKAS 37 Provisions, Contingent Liabilities and Contingent Assets.4.(a)Written representationsWritten representations are necessary information that the auditor requires in connection with the audit of the entity’s financial statements. Accordingly, similar to responses to inquiries, written representations are audit evidence.The auditor needs to obtain written representations from management and, where appropriate, thosecharged with governance that they believe they have fulfilled their responsibility for the preparation of the financial statements and for the completeness of the information provided to the auditor.Written representations are needed to support other audit evidence relevant to the financial statements or specific assertions in the financial statements, if determined necessary by theauditor or required by other Hong Kong Standards on Auditing.This may be necessary for judgemental areas where the auditor has to rely on management explanations. Written representations can be used to confirm that management have communicated to the auditor all deficiencies in internal controls of which management are aware.Written representations are normally in the form of a letter, written by the company’s management and addressed to the auditor. The letter is usually requested from management but can also be requested from the chief operating officer or chief financial officer. Throughout the fieldwork, the audit team will note any areas where representations may be required.During the final review stage, the auditors will produce a draft representation letter. The directors will review this and then produce it on their letterhead.It will be signed by the directors and dated as at the date the audit report is signed, but not after.(b) Oral representationA representation from management confirming that overdrafts are complete would be relevant evidence. Overdrafts are liabilities and therefore the main focus for the auditor is completeness.With regards to reliability, the evidence is oral rather than written and so this reduces its reliability. The directors could in the future deny having given this representation, and the auditors would have no documentary evidence to prove what the directors had said.This evidence is obtained from management rather than being auditor generated, and is therefore less reliable. Management may wish to provide biased evidence in order to reduce the amount of liabilities in the financial statements. The auditors are unbiased and so evidence generated directly by them will be better.External evidence obtained from the company’s banks could be used to confirm the bank overdraft balances and this would be more independent than relying on management’s internal confirmations.(c)Daisy Designs Co (Daisy)(i)Daisy’s sales ledger has been corrupted by a computer virus; hence no detailed testing has been performed on revenue and receivables. The audit team will need to see if they can confirm revenue and receivables in an alternative manner.If they are unable to do this, then two significant balances in the financial statements will not have been confirmed.Revenue and receivables are both higher than the total profit before tax (PBT) of $2m; receivables are 170% of PBT and revenue is nearly eight times the PBT; hence this is a very material issue. (ii) Procedures to be adopted include:– Discuss with management whether they have any alternative records which detail revenue andreceivables for the year.– Attempt to perform analytical procedures, such as proof in total or monthly comparison to last year, to gain comfort in total for revenue and for receivables.(iii)The auditors will need to modify the audit report as they are unable to obtain sufficient appropriate evidence in relation to two material and pervasive areas, being receivables and revenue. Therefore a disclaimer of opinion will be required.A basis for disclaimer of opinion paragraph will be required to explain the limitation in relation to the lack of evidence over revenue and receivables. The opinion paragraph will be a disclaimer of opinion and will state that we are unable to form an opinion on the financial statements. Fuchsia Enterprises Co (Fuchsia)(i)Fuchsia is facing going concern problems as it has experienced difficult trading conditions and it has a negative cash outflow. However, the financial statements have been prepared on a going concern basis, even though it is possible that the company is not a going concern. The prior year financial statements showed a profit of $1·2m and the current financial statements show a loss before tax of $4·4m, the net cash outflow of $3·2m represents 73% of this loss(3·2/4·4m) and hence is a material issue.(ii) Management are confident that further funding can be obtained; however, the team is sceptical and so the following procedures should be adopted:– Discuss with management whether any finance has now been secured.– Review the correspondence with the finance provider to confirm the level of funding that is to be provided and this should be compared to the net cash outflow of $3·2m.– Review the most recent board minutes to understand whether management’s view on Fuchsia’s going concern has altered.– Review the cash flow forecasts for the year and assess the reasonableness of the assumptions adopted.(iii) If management refuse to amend the going concern basis of the financial statements or at the very least make adequate going concern disclosures, then the audit report will need to be modified. As the going concern basis is probably incorrect and the error is material and pervasive, then an adverse opinion would be necessary.A basis for adverse opinion paragraph will be required to explain the inappropriate use of the going concern assumption.The opinion paragraph will be an adverse opinion and will state that the financial statements do not give a true and fair view.。

accaf4知识点总结

Chapter11.民法(civil law)和刑法(criminal law)的划分Civil law: an form of private law,used by individuals to assert rights against other individualsCriminal law: an aspect of public law to regulate crimesand to punish offendersIssue Civil CriminalWho brings the action Claimant/plaintiff原告Prosecutor/cps/stateBurden of proof Claimant/plaintiff原告Prosecutor/cps/stateStandard of proof Balance ofprobabilitiesBeyond reasonabledoubtDecisions Liable/not(judge)Guilty or notAims Compensatory Punitive/to punishRemedies纠正damages Imprisonment/fines1.Case law: made by judge/ statute law成文法: primarylegislation(made by the Parliament)/secondarylegislation( in exercise of law-making powers delegatedby Parliament). [注:Necessity for delegatedlegislation/secondary legislation :more convenient ;canhand over the task of specifying the law in detail toexperts]2.在case law中:common law普通法[created by judgesthrough the application of the principle of judicialprecedent. common law drew on customs/equity law衡平法:to resolve disputes where damages are not asuitable remedy and to introduce fairness into the legalsystem.]2.不同法院管辖事件的类型只受理民事案件County court只受理刑事案件Crown court民刑通吃Magistrate’s court , high court, court ofappeal, supreme court只受理一审County court, magistrate’s court只受理上诉Court of appeal , supreme court一审上诉通吃High court , crown courtChapter2Chapter21.Doctrine of Precedence(遵循先例制度的一般规则): somedecisions made by a court are binding and similar subsequent legal cases should be decided on the basis ofthe law established in earlier cases.2.可以创立判例法规则: Supreme Court/Court ofAppeal/High Court;不可以创立:Crown, Magistrates, County Courts cannot create precedent.3.Elements of judicial decision(影响法庭判决的因素):rationdecidendi判决理由[the reason for the decision]/Obiterdicta附带说明[statement made by the way, not binding,but merely of persuasive authority]4.法官又可以因为那些理由拒绝先例(disregarding judicialprecedent): Overrule取代[the procedure whereby a courthigher in the legal hierarchy sets aside a legal ruling established in a previous case]/Reverse推翻[a procedure whereby a court higher in the hierarchy reverses the decision of a lower court in the same case]/Distinguishing法官的自由裁决[a precedent is avoided by a judge demonstrating that the material facts of two cases are notthe same]5.Rules of Statutory Interpretation(法的解释):①the literalapproach :the literal rule[means that words in the Act should be given their literal and grammatical meaning rather than what the judge thinks they mean./the goldenrule :this rule is applied in circumstances where the application of the literal rule is likely to result in an obviously absurd result. ②the purposive approach :the judge should ,where necessary ,look beyond the words ofstatute to find out the reason/purpose for its enactment,and that meaning should be interpreted in the light of thepurpose[Mischief rule :purposive approach的具体表现形式/where a statute is designed to remedy a weakness inthe law, the correct interpretation is the one which achieves it.]6.语言处理规则(法律没有追溯力 a statute does not haveretrospective effect)Chapter3 合同法(IMP)1.合同的概念 a legally binding agreement enforceable in law2.从要约到承诺是否达成agreement [invitations to treat要约邀请--offer要约--acceptance承诺----agreement]3.Termination of an offer:express rejection/counter off反要约/lapse of time/revocation of an off/death/if the off is suject toa condition,it will lapse on failure of that condition4.Privity of Contract合同相对性原则: the common law doctrinethat only those are party to the contract---have rights or liabilities under the contract/ have the right to enforce the contract,contracts cannot give rights or obligations to othersChapter41.分类标准Express and lmplied terms:某个条款是否经过双方当事人协商同意(agreed by the parties)Condition,warranties and innominate terms 核心,从属和无名条款:根据条款重要性2.免责条款(三观概念)Any clause that attempts to exempt , or limit, the liabilityof one party for breach of contract or negligence3 test: correctly incorporated into the contract形式正确/worded clearly to exclude the breach措辞清晰/reasonable per statute内容合理Chapter51.type of breachRepudiatory breach根本性违约:refusal to perform拒绝履行/failure to perform an entire obligation不履行某项/incapacitation无力履行/breach ofcondition 违反核心条款/breach of an innominateterm违反无名条款Anticipatory breach预期违约:未到合同履行时间,当事人提前说明无法履行;收到预期违约通知可立即追究违约责任,也可等到履行合同时间追究责任Lawful excuses for non-performance开脱责任:performance is impossible因不可预见的事情发生不可履行/尝试履行被拒绝/ the other party make it impossible for him to performance/contract is discharged through frustration情势变更/the party have been agreement permitted non-performance2.Remedies : when a breach occurs, the court has to decidewhat the appropriate remedy should be.Common law Damage赔偿金, action forthe price, quantum meruit Equitable law 衡平法Specific performance实际履行,injunction禁令,rescission of the contract撤销合同3.Liquidated damage违约金: a genuine pre-estimate ofthe loss在订立合同前已经商定了,有利于解纠纷,如果违约金过高(远大于loss)判为惩罚性,则不可执行4.specific performance :the court directs a party tocomplete their contractual obligations以下几种情况法官不会让合同继续履行:courts cannot supervise法官无力监督履行/personal service/minors involvedChapter6 Tort侵权法A wrongful act against an individual which gives rise to a civilclaim.1.过失侵权的4个证明环节(概念标准内容)Negligence:It arises when one person suffers damage or injury though the negligent act(or omission to act)of another person.①Duty of care注意义务(三步走原则)1.Reasonable foreseeability合理预见原则2.Proximity关联性原则3.Justness and fairness of imposing a duty of care公平合理地强加注意义务②A breach of that duty违反注意义务1.general rule:The test for establishing breach of duty is an objective one:a breach of duty occurs if the defendant:”...fails to do something which a reasonable man...would do.”2.Special factors to considera.The probability of injuryb.The seriousness of the risk造成伤害的严重性c.Cost and practicability成本可行性mon practice证明是行业误差范围内e.Skilled persons/professionalsf.Social benefit③The breach of duty caused harm to the claimant违反义务是导致损失的原因1.The but for test2.No break in the chain of causation切断因果关系链的要素a.A natural eventb.Act of a third party 原侵权人不承担责任c.Act of the claimant④The loss ware not too remote主张的赔偿合理Reasonable foresight只赔偿违法者可以合理预见的部分2.抗辩事由①Contributory negligence共同过失(一般只是减少赔偿额,个别情况全部免除)②Volenti non fit injuria同意不生违法(彻底免除)Chapter7 劳动法1.身份判别①Control test :The amount of control that one person hadover the other②Integration test不会外包给他人的,不可或缺的③Multiple test/Economic reality testa. The regularity and method of payment报酬支付频率,支付方式b. The ownership of tools and equipment是否提供工具c. The regularity of hours of work工作时间d. The ability to delegate all the work/to provide substitute是否代理2.义务①Common Law Duties-Employers’ common law duties1)Duty of mutual trust and confidence2)To provide work for workers3)To pay wages/remuneration4)To indemnify employee against expenses and losses5)To provide for the care and safety of the employee6)No duty to provide reference when employees leave-Employees’ common law duties1) To obey reasonable and lawful orders2) To act faithfully/duty of faithful service/duty to accountfor all money and property3) To exercise reasonable skill and care in any activity intheir role as an employee/reasonable competence to do his job4) Personal service亲自完成交付的责任②Statutory Duties1)Pay and equality不能低于国家平均2) Time off work3)Trade union officials工会组织罢工可以参加,还要给工资4) Every woman has a right to maternity leave and someare entitled to maternity pay5) Health and safety6)Working time:17week,not exceed 48 hours for each 7 days除非员工书面同意多工作7) Flexible workingChapter81.解雇通知时间的计算1m-2Y: not less than 1 week2y-12y:1 week for each year≥12y: not less than 12 week劳动者离职要提前一周通知,合同期满不续则每工作一年折合一个月工资2.自动正当参加非法集合罢工unofficial industrial action/对国家安全有威胁自动不正当怀孕pregnancy/员工参加工会活动/收购并购时的解雇dismissal on transfer of an undertaking/工作存在安全问题/最低工作标准/作息时间/员工在周天拒绝工作3.用人单位解雇不当Chapter9 代理法1.代理关系建立方式Express agreement between the agent and principal达成委托代理协议合同,口头书面皆可Implied agreement默认没有代理协议但默认存在关系Ratification追任代理人先履行合同,事后委托人建立合同关系Without consent of principal 没有征得委托人同意就建立关系necessity/Estoppel2.代理权限(3)Express authority明示代理权限Implied authority默认代理权限Apparent/ostensible authority看起来有代理权限,实际上并没有Chapter10 合伙企业法1.合伙企业(概念):the relationships that subsists betweenpersons carrying on a business in common with a view toprofit. standard partnership is not s separate legal entityand its partners have full personal liability for the debtsof partnership.2.Termination/dissolution合伙企业解散的债务处理:payingoff external debts/repaying to the partners any loans oradvances/repaying the partner’s capital contribution/anything left over is then repaid to the partners in the profit sharing ratio .3.Termination/dissolution合伙企业解散的条件:expiry of afixed period stipulated in the partnershipagreement/completion of the express purpose for whichthe partnership was formed/partner gives notice to leave/a new partner is admitted into the partnership/death or bankruptcy of partner/happening ofany event which makes company can’t carry on/onapplication by a partner the Court may decree a dissolution of the partnership4.Sole trade宏观特征:is not a separate legal entity, theperson and business are viewed as the same legal entity5.Authority合伙人的代理权限:express authority明示代理权限[from partnership agreement]/implied authority默示代理权限/apparent authority表面代理权限[已经退伙但其他人不知道]6. A partner’s liability usually extends to the period forwhich were actually a partner of a firm. 合伙人只对担任合伙人期间合伙企业产生的债务有清偿责任7.Limited Partnership(LP)特征:the partnership must beregister with the Company Registry/one or more of thepartners must bear full,unlimited liability/partners with limited liability may not take part in management and cannot usually bind the business in contract/limitedpartner cannot withdraw their capital8.Limited Liability Partnership(LLP)特征:must be registeredwith the the Registrar of Companies, with formationdocuments signed by at least two members/has a legal personality separate/ the name of partnership must endwith LLP/partners are known as members, of which theremust be at least two/LLPs must file annual returns and accounts/all members are agents of LLP/all members’liability is limited/a designated member is responsible foradministration and filing/LLP is not subject to corporationtaxChapter121.设立pre-incorporation contacts谁来履行?Promoters发起人2.交什么文件①Memorandum of association公司章程(89年)②Application for registration注册申请书③A statement of capital and initial shareholdings关于公司资本坏人原始持有股份的状况说明④Statement of compliance遵从声明⑤A statement of company’s proposed officers拟任命谁为公司管理人员⑥A copy of any proposed articles of association自拟公司章程(06年)不是必须提交,没交使用默认模版3.2个证书的功能①Certificate of incorporation注册许可证Private company 只需要注册许可证,是形式审查②Trading certificate营业许可证Public company需要两个证,申领到注册许可证后一年内要申领到营业许可证,否则强制清算,是实质审查a.Allotted share capital is at least £50,000(允许股东分批缴纳)b.At least one quarter of the nominal value of the allottedshare capital has been paid up(minimum £12,500)首次不低于票面的1/4,为确保一开始不会有资金困难c.Details of promoters’ expenses设立费用具体怎么产生d.A statement of compliance in respect of payment of nominal values and share premium4.章程修改的程序和内容-Contentsa. Directors’ powers and responsibilityb. Decisions making by directorsc. Appointment of directorsd. Organization and conduct of general meetingse. Issue and transference of sharesf. Payment of dividendsg. Exercise of members’ rights-Alteringa. Passing a special resolution通过股东会的特别决定,3/4以上同意批准b. Providing the alteration has been made “bona fide in the interest of the company as a whole”内容符合全体股东的意愿5.各个公司名称缩写代表含义-Ltd:Limited-plc:public limited companyChapter131.capital的分类Issued已发行股本Shares already issued, including share taken on formation by subscribers to the memorandumCalled up 已催缴股本Amount which the company has required shareholders to payPaid up 以催Amount which shareholders have付股本actually paidEquity share Equity share capital is a company’sissued share capital less capital whichcarries preferential rights. It normallycomprises ordinary shares.2.普通股优先股的概念和差异feature ordinary Preferencedividends variable Fixed, usually,cumulative Voting rights Yes restrictedGeneralmeetingsMay attend andvoteRestricted liquidation Rank last/entitled torepayment ofcapital andshare of surplusRank aboveordinary share/entitled torepayment ofcapital only3.Bonus issue红利股发行The capitalization of the reserves if a company by the issue if additional shares to existing shareholders, in proportion to their holdings. Such shares are normally fully paid-up with no cash called for from the shareholders4.Share premium概念shares may be issued at a price above their nominalvalue, the difference between the issue price and the nominal value is a share premium用途the issue of fully paid bonus share/writing off the preliminary expenses of company formation/writing off the discount on the issue of debentures/repurchase of debenturesat a premiumChapter11 公司法The consequences of separate legal personality for the company are as follows:(1897年案例引出的规则)1: members' liability is limited.2: perpetual succession become possible as the company willneed to be formally wounded-up.3: the company itself can own property.4 :the company can use, and be sued in its own name.Types of company (公司的分类)Features Ltd Plc Minimum number of directors 1 2 Minimum number of members 1 1 Minimum share capital One share £500000 Advertise share/debentures to public No YesTime to hold accounting records 3 years 6 years Annual general meeting Optional Compulsory Company secretary Optional Compulsory File accounts after year-end 9 months 6 months。

ACCA-F4知识要点汇总(精简版)

ACCA-F4知识要点汇总(精简版)1. 公司法律结构及管理公司的法律结构包括公司章程、股东协议、公司登记簿、董事会、股东大会、公司秘书等。

管理层需要遵守法律法规,同时也应该关注公司的社会责任和企业道德。

2. 公司财务及税务公司的财务部门需要负责编制财务报表、管理公司资金、进行预算和决策分析等。

税务部门需要负责申报税务、缴纳税款以及规划税务策略。

3. 合同法律框架合同是商业交易的基础,具有法律约束力。

合同的成立需要满足合同要素、合同内容的充分和明确、合同手续正确等条件。

合同的违约应该依法承担相应的法律责任。

4. 卖方和买方的权利与义务在商品的交易中,卖方需要履行交货、履行义务、提供货物信息等职责;买方需要履行付款、接收货物、检验货物、通知卖方等职责。

同时,卖方和买方也有权利保护自己的利益。

5. 银行融资银行融资是常见的企业融资方式,包括贷款、信用证、保函等。

企业在申请银行融资时需提供充分的资料和合理的担保措施,并在合同履行期内按期还款。

6. 国际贸易国际贸易的主体包括进出口商、代理商、货代、保险公司等。

在国际贸易中,涉及到的问题有贸易商信用、运输保险、海关手续等。

企业需要制定适应国际贸易的商业策略。

7. 合并与收购合并与收购是企业快速扩张的一种方式。

在进行合并与收购时,需要考虑战略目标、财务风险、员工合法权益等问题,并进行充分的财务、法律尽职调查。

8. 会计和审计会计和审计是公司财务管理的重要组成部分。

会计部门需要负责制定会计政策、编制财务报表等。

审计部门需要进行内部审核、外部审核等工作,并对财务报表的真实性和准确性进行评估。

2019ACCA考试科目 F4备考攻略丨浅析基本法解释规则

2019ACCA考试科目 F4备考攻略丨浅析基本法解释规则2019ACCA考试科目 F4备考攻略丨浅析基本法解释规则 2019年01月04日F4阶段的“成文法解释规则”这一知识点比较容易混淆,Alisa老师为大家整合一下知识点,帮助大家全面理解。

在刚开始学习F4的时候,同学们会学习到成文法解释规则,关于如何区分成文法解释规则,很多同学都会感到吃力,不过不用担心,在这里,Alisa老师就来分享给大家如何正确区分这些恼人的解释规则。

对于英国普通法的成文法解释规则而言,文义规则(literal rule),黄金规则(golden rule),除弊原则(mischief rule)是三种历史最久的成文法解释规则。

而在当代普通法司法实践中,除弊原则已经流变成为目的规则(purposive rule),所以去区分mischief rule以及purposive rule是没有意义的。

那么在这篇文章中,我们会对这三种历史最悠久的解释规则进行区分。

(一)文义规则解释成文法的第一首要假设就是要尊重文义,所以文义规则是法官首先会适用的规则,文义规则是指在法律条文文本清晰,不模糊的情况下,依照其平直,通常,自然的字面意义予以及时的方法。

(二)黄金规则黄金规则可以理解为文义规则额的例外情况,正如我们在书上学到的,文义规则的解释下常常会出现不合理结果,而且也不能这个结果也明显不符立法机构的原意,故而,这个成文法就应该变通地去解释,以避免不合理的结果。

(三)目的规则目的规则是指首先确定立法机构指定该成文法的目的,然后以此目的为指导,对该成文法进行解释。

这个规则也是目前被法官更加倾向于使用的规则。

那么该如何完全区分(一)与(二),同学们可以掌握一个原则,黄金规则适用的前提是,使用黄金规则解释的结果不能够使得出的成文法意义超出文本本身的意义,但是目的规则则没有这样的前提,比如书上 Corkery v Carpenter 1950 案例中,在目的规则是适用下,使得醉酒骑车也符合禁止醉酒驾驶马车的成文条款的情况,这样的解释结果就超过了原本文本自身的含义。

ACCA F4知识点:Criminal law and Civil law

ACCA F4知识点:Criminal law and Civil law今天给大家来说一说ACCA F4中关于Criminal law和Civil law,即刑法和民法。

首先我们先来看一下它们的定义。

Civil law sets out the rights and duties of persons as between themselves. The person whose rights have been infringed can claim a remedy from the wrongdoer. 民法主要关注的是人的权利和责任以及对其的补偿。

Criminal law is concerned with the conduct that is considered so undesirable that the State punishes persons who transgress. 刑法主要关注的是一个违法的人对其的违法行为的惩罚。

关于Burden of proof,即举证责任,有相似的部分。

The necessity of proof normally lies with the person who lays charges, i.e. the claimant. 举证责任由原告承担。

这两者之间的区别主要体现在四个方面。

(1)Aim. Civil law is aimed to provide compensation for an injured party, whereas criminal law is to regulate society by the threat of punishment.(2)Parties. In a civil action, the claimant sues the defendant, while in a criminal action, the State prosecutes the defendant.(3)Standard of proof. In Civil law, if the claimant can prove the wrong on the balance of probabilities, his litigation is successful and the defendant is held liable. 民法中,要保持可能性的平衡。

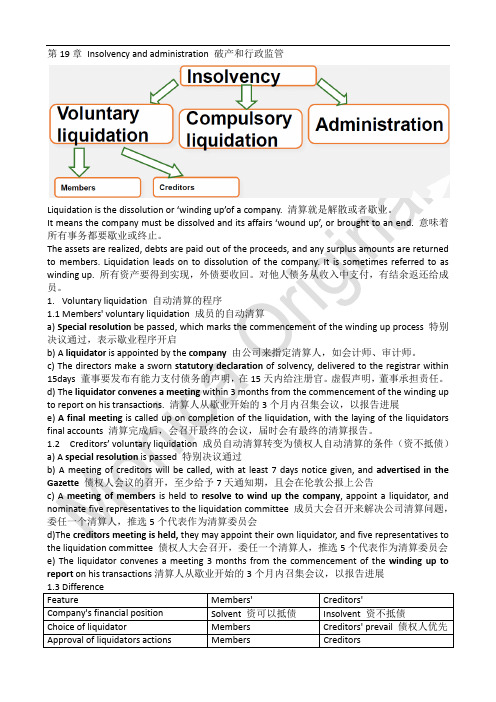

ACCA F4知识要点 第19章

第19章 Insolvency and administration 破产和行政监管Liquidation is the dissolution or ‘winding up’of a company. 清算就是解散或者歇业。

It means the company must be dissolved and its affairs ‘wound up’, or brought to an end. 意味着所有事务都要歇业或终止。

The assets are realized, debts are paid out of the proceeds, and any surplus amounts are returned to members. Liquidation leads on to dissolution of the company. It is sometimes referred to as winding up. 所有资产要得到实现,外债要收回。

对他人债务从收入中支付,有结余返还给成员。

1.Voluntary liquidation 自动清算的程序1.1Members' voluntary liquidation 成员的自动清算a) Special resolution be passed, which marks the commencement of the winding up process 特别决议通过,表示歇业程序开启b) A liquidator is appointed by the company 由公司来指定清算人,如会计师、审计师。

c) The directors make a sworn statutory declaration of solvency, delivered to the registrar within 15days 董事要发布有能力支付债务的声明,在15天内给注册官。

ACCA《F4公司法与商法》精选讲义第一章(3)

ACCA《F4公司法与商法》精选讲义第一章(3)本文由高顿ACCA整理发布,转载请注明出处Session 3 Types of cost and cost behaviorMain contents:1. Classifying costs2. Cost objects, cost and cost centers3. Analysis of costs into fixed and variable elements3.1 Classifying costsCosts can be classified in a number of different ways:· Element – costs are classified as materials, labor or expenses (overheads)· Nature – costs are classified as being direct or indirect.a. Direct cost is expenditure that can be directly identified with a specific cost unit or cost center.(1)。

Direct material is all material becoming part of the product unless used in negligible amount and/or having negligible cost. (component parts, part finished work and primary packing material)(2)。

Direct wages – are wages paid for labor either as basic hours or as overtime expensed on the product line.(3)。

ACCAF4知识点总结

ACCAF4知识点总结ACCA F4(全称为Corporate and Business Law,企业与商法)是ACCA(特许公认会计师协会)的考试科目之一,该科目旨在培养学生对法律和道德标准在商业环境中的应用能力。

下面是ACCA F4考试的重要知识点的总结。

1.法律体系与法律制度-法律体系的分类:普通法系、大陆法系、伊斯兰法系。

-各种法律制度的特点和适用范围。

2.法律规则与制度-法律的层级:宪法、立法、裁判法、平行法、国际法。

-法律规则的优先级和适用原则。

3.国家和政府-国家和国家主权的概念和要素。

-不同行政体制和政府机构的职责和权力。

4.法人与商法-法人的种类和特征:公司法主体、合伙公司、有限责任公司等。

-公司注册和运营的法律要求。

-公司治理的原则和实践。

5.合同法-合同法的定义和要素。

-合同的形成、要约的接受和契约的生效。

-合同的履行、违约和争议解决。

6.担保法与信托法-法律担保的种类和特点:抵押、质押、保证等。

-信托的定义、要素和种类。

-信托的设立、运作和终止。

7.货物买卖与供货合同-货物买卖合同的要素和合同条款。

-瑕疵物品的权利和救济。

-供货合同的要求和责任。

8.雇佣法与劳动法-雇佣合同的要素和权利义务。

-雇佣关系的终止:辞退、解聘和离职。

-劳动法的基本原则和劳动者权益保护。

9.公司法与企业管理-公司法的基本原则和要求。

-公司规章制度和内部控制的建立与遵守。

-公司法违规行为和违规惩罚。