金融服务贸易

中国金融服务贸易的国际竞争力分析_中国金融服务贸易国际竞争力分析

中国金融服务贸易的国际竞争力分析_中国金融服务贸易国际竞争力分析关键词服务贸易金融服务贸易国际竞争力。

一、金融服务和国际金融服务贸易的界定金融服务是服务的一种,是指金融机构运用货币交易手段融通有价物品,向金融活动参与者和顾客提供的共同受益、获得满足的活动。

关贸总协定乌拉圭回合谈判中对金融服务作了如下定义:金融服务是指由一成员方的金融服务提供者所提供的任何有关金融方面的服务,包括所有保险和与保险有关的服务及所有银行和其他金融服务。

本文所指的金融服务是指除保险服务外的金融服务。

国际金融服务贸易就是以提供金融服务为目的的国际性商业服务活动,有四种形式:(1)跨境交付,从一成员方境内向任何其他成员方境内提供金融服务,如一国消费者购买境外外国金融机构的金融服务。

(2)境外消费,在一成员方境内向任何其他成员方的服务消费者提供金融服务,如一国银行对外国人的旅行支票进行支付。

(3)商业存在,成员方的服务提供者通过在任何其他成员方境内的商业存在提供金融服务,如外国金融机构在东道国投资设立分支机构。

(4)自然人存在,一成员方的服务提供者通过在任何其他成员方境内的自然人存在提供金融服务,如一国从事金融服务的个人到另一成员国提供风险评估和金融咨询等服务。

当前我国的金融服务贸易也是以商业存在和跨境交付为主,其中以商业存在为最主要的形式。

这是因为服务贸易的无形性,以及其生产和消费同时进行的特殊性,使得服务交易通常需要服务提供者和消费者的直接接触,进行信息完全沟通。

此外,与众多跨国企业对外直接投资来规避东道国的贸易壁垒的动因一样,金融服务贸易以商业存在的形式出现同样可以规避服务贸易壁垒,获得信息优势,从而降低交易成本。

二、中国金融服务贸易的国际竞争力指数分析(一)国际市场占有率分析国际市场占有率是指一个国家某个产业或某种产品的出口总额占世界市场该产业或产品出口总额的比率。

该指标从一个国家整体的规模和产业整体实力的基础上简洁清楚地反映了该国该产业的整体国际竞争力。

我国金融服务贸易出口分析及影响因素研究

04

提升我国金融服务贸易出口的对策建议

优化金融服务贸易出口结构

完善金融监管体系,确保金融市场的稳定和安全。

加强金融机构内部管理,提高金融服务效率和质量。 加强金融行业人才培养,提高金融服务专业水平。

加强金融创新和支持政策调整

加强金融创新和支持政策调整是提升我国金融服务贸 易出口的重要手段。

加强政府对金融创新的支持力度,提高金融创新的能 力和水平。

推进金融制度创新,完善金融服务贸易的法律和政策 环境。

政策因素

政策支持力度

政策支持是促进金融服务贸易出口的重要因素。政府可以通过出台税收优惠、财 政补贴等政策措施来鼓励金融机构开展跨境服务,提高金融服务贸易出口的竞争 力。

监管政策

监管政策对金融服务贸易出口的影响不可忽视。过度的监管可能会限制金融服务 的市场准入和限制金融机构的经营范围,从而影响金融服务贸易出口的发展。因 此,适当的监管政策是促进金融服务贸易出口的重要因素。

《我国金融服务贸易出口 分析及影响因素研究》

xx年xx月xx日

目录

• 研究背景和意义 • 我国金融服务贸易出口现状分析 • 影响因素分析 • 提升我国金融服务贸易出口的对策建议 • 研究结论与展望

01

研究背景和意义

研究背景

金融服务贸易出口概 述

金融服务贸易出口是指一国(地区) 向另一国(地区)提供金融产品或服 务,并从中获取收入的过程。随着全 球经济一体化的深入发展,金融服务 贸易出口已成为各国(地区)经济竞 争的重要领域。

金融服务贸易发展现状及对策

THANKS FOR WATCHING

感谢您的观看

推动金融服务贸易创新发展

支持金融机构开展数字化转型,利用 大数据、人工智能等技术提升服务效 率和客户体验。

加强与科技企业的合作,推动金融科 技的创新和应用,探索新的商业模式 和增长点。

鼓励金融机构开展国际合作,推动金 融服务贸易的深度融合和发展。

加强金融服务贸易人才培养

加强教育和培训,培养具有国际 视野和专业技能的金融服务贸易 人才。

市场准入壁垒

一些国家对金融服务贸易的市场准入设置壁垒,阻碍 了金融服务贸易的发展。

金融服务贸易的监管问题

监管体系不完善

一些国家的监管体系未能跟上金融服务贸易的 发展步伐,导致监管漏洞和风险。

监管标准不统一

不同国家对金融服务贸易的监管标准不统一, 增加了监管难度和成本。

监管合作不足

各国之间的监管合作不足,导致跨国金融服务的监管混乱。

中国金融服务贸易发展概况

01

中国金融服务贸易规 模

中国的金融服务贸易规模不断扩大, 对外开放程度不断提高,尤其是在“ 一带一路”倡议的推动下,跨境金融 服务贸易发展迅速。

02

中国金融服务贸易结 构

银行业在中国金融服务贸易中占据主 导地位,但保险、证券等金融行业也 在不断发展壮大。

03

中国金融服务贸易特 点

02

金融服务贸易发展现状

全球金融服务贸易发展概况

全球金融服务贸易规模

近年来,全球金融服务贸易规模持续增长, 尤其是跨境金融服务贸易的快速增长。

全球金融服务贸易结构

银行、保险、证券等金融行业在金融服务贸易中占 据主导地位,而新兴的互联网金融行业也在迅速崛 起。

全球金融服务贸易特点

国际服务贸易金融

机器学习技术通过自主学习和优化算法,能够实现精准预测和决策支持等功能 ,为国际服务贸易金融中的市场分析、投资决策等提供重要支持。

05

国际服务贸易金融监管与合规

跨境金融监管体系

跨境金融监管合作

加强各国监管机构间的合作,共 同制定跨境金融市场的监管规则 ,确保跨国金融机构遵守各国监

管要求。

详细描述

某区块链平台为国际支付提供了一种新型解决方案, 通过智能合约等技术实现跨境支付的自动化和高效化 。相较于传统支付方式,该平台具有更低的成本、更 高的效率和更强的安全性。同时,该平台还就合规性 、监管要求等方面进行了考虑和设计。

案例四:人工智能在金融服务中的创新应用

要点一

总结词

要点二

详细描述

04

国际服务贸易金融技术

电子支付与区块链技术

电子支付技术

电子支付技术是国际服务贸易金融中 重要的支撑技术之一,能够实现快速 、便捷、安全的资金转移和支付。

区块链技术

区块链技术通过去中心化、可信任等 特点,为国际服务贸易金融提供了更 加安全、透明和高效的交易和清算方 式。

数据挖掘与风险管理技术

数据挖掘技术

详细描述

某出口企业与进口企业签订了出口合同,考虑到进口国的政治、经济风险,该企业选择 了预收货款的方式进行结算。同时,为降低汇率风险,该企业还选择了固定汇率的方式

进行结算。此外,该企业还就货物运输保险、信用证开立等环节进行了风险管理。

案例三:区块链技术在国际支付中的应用

总结词

区块链技术具有去中心化、安全性高、交易效率高等 特点,在国际支付领域具有广阔的应用前景。

统一监管标准

推动各国监管机构采用统一的监 管标准,降低跨境金融市场的监 管差异,提高市场透明度和稳定

中国金融服务贸易分析

市场需求

随着中国经济的快速发展和金融增加 ,为金融服务贸易提供了广阔的

市场空间。

02

中国金融服务贸易现状分析

金融服务贸易规模与结构

金融服务贸易规模

近年来,中国金融服务贸易规模不断 扩大,金融服务贸易额逐年增长。中 国已经成为全球金融服务贸易的重要 参与国之一。

金融服务贸易政策环境

政策环境概述

中国政府高度重视金融服务贸易的发展,出台了一系列政策措施,为金融服务 贸易提供了良好的政策环境。

政策环境具体内容

中国政府通过放宽市场准入、推动金融创新、加强监管合作等措施,促进金融 服务贸易的发展。同时,中国政府还积极推动金融市场的开放和国际化,为金 融服务贸易提供了更多的机遇和空间。

加强金融监管和风险防范,确保中国 金融服务贸易的健康稳定发展。

THANKS

谢谢您的观看

03

中国金融服务贸易面临的挑战 与机遇

面临的挑战

金融服务贸易全球化趋势

金融服务创新能力不足

随着全球金融市场的不断开放,中国 金融服务贸易面临着来自国际市场的 竞争压力。

中国金融服务创新能力相对较弱,缺 乏具有国际竞争力的金融产品和服务 。

金融服务监管体系不完善

中国金融服务监管体系尚不完善,存 在监管漏洞和不足,容易引发金融风 险。

中国金融服务贸易分析

汇报人: 日期:

目录

• 引言 • 中国金融服务贸易现状分析 • 中国金融服务贸易面临的挑战

与机遇 • 中国金融服务贸易发展趋势预

测与展望 • 结论与建议

01

引言

金融服务贸易概述

金融服务贸易定义

金融服务贸易是指一国或地区向 另一国或地区提供金融服务的过 程,包括跨境支付、跨境融资、 跨境保险、跨境证券投资等。

金融服务贸易

n 成员可对核准商业机构的设立和扩展附加条件和程 序要求,但不得违背在GATS项下的义务。

金融服务贸易

关于金融服务承诺的谅解

市场准入方面的规定

n 新的金融服务

n 各成员应允许其他成员在其境内建立的金融服 务机构提供新的金融服务,这是指尚未在该成 员境内提供但已在另一成员境内提供的具有金 融特性的服务及其相关服务。

加入后1年 开放广州、珠海、青岛、南京、武汉

加入后2年 开放济南、福州、成都、重庆;允许外国金融机构向中国企业提 供人民币业务的服务。

加入后3年 开放昆明、北京、厦门

加入后4年 开放汕头、宁波、沈阳、西安

加入后5年

取消所有地域限制;允许外国金融机构向所有中国客户提供人民 币业务服务;取消现在的限制所有权、经营及外国金融机构法律 形式的任何非审慎性措施;满足一定条件的外国金融机构可在华 设立独资、合资银行或财务公司,设立外国银金融行服的务贸分易行。

金融服务贸易

关于金融服务承诺的谅解 市场准入方面的规定

n 跨境服务

n 应允许非居民金融服务提供者根据国民待遇条款提 供如下服务:

n 海运和商业性航空航天运输及运费风险的保险;对 于运输的货物、运输货物的工具和由此产生的责任 保险、以及处于国际运输中的货物的保险;再保险、 恢复和咨询、保险统计、风险评估和索赔清算服务 等保险辅助性服务;

金融服务贸易

深入金融体制改革,促进中资银行的发展

n 第五,提高技术水平和工作效率。

n 运用国际通用准则或国际通用标准对银行的财务会计等资本 制度和授权、授信管理等基本业务操作规程进行规范。

n 逐步实现商业银行经营管理的电子化,特别要建立和完善市 场信息系统和决策支持系统。

国际服务贸易之金融服务贸易

一、金融服务贸易概述GA TS 框架下的金融服务贸易主要包括跨境交付境外消费商业活跃和自然人流动,而我国对金融领域的开放已不限于此2002年,我国主动实施了QFII 制度,允许合格的境外机构投资者进入A 股市场; 2006年实行的QDII 制度,允许合格的境内机构投资者到境外投资;2007年我国又宣布取消了QDII对外投资的限制在资本项目进一步开放的同时,一系列推动投资贸易便利化鼓励人民币跨境使用的制度也在紧锣密鼓地制定与实施。

可见,我国金融服务贸易的开放程度在不断提高。

PS:QDII,是“Qualified Domestic Institutional Investor”的首字缩写,合格境内机构投资者,是指在人民币资本项下不可兑换、资本市场未开放条件下,在一国境内设立,经该国有关部门批准,有控制地,允许境内机构投资境外资本市场的股票、债券等有价证券投资业务的一项制度安排。

设立该制度的直接目的是为了“进一步开放资本账户,以创造更多外汇需求,使人民币汇率更加平衡、更加市场化,并鼓励国内更多企业走出国门,从而减少贸易顺差和资本项目盈余”,直接表现为让国内投资者直接参与国外的市场,并获取全球市场收益。

QFII(Qualified Foreign Institutional Investors)合格的境外机构投资者的英文简称,QFII 机制是指外国专业投资机构到境内投资的资格认定制度。

(不用做在PPT里,但是如果要讲,需要解释一下这两个缩写)二、金融服务贸易发展概况1、我国金融服务贸易总量增加,进出口差额扩大尽管10年来我国金融服务贸易在总体规模上不断增长,但一直处于出口逆差状态,且逆差日益扩大。

2、我国金融服务贸易结构性失衡问题突出(1)内部结构失衡首先,保险服务和其他金融服务的进出口贸易总额相差悬殊。

通过整理数据发现,保险服务贸易进出口总额为其他金融服务贸易的数倍。

其次,保险服务进出口贸易总额平稳增长,其他金融服务进出口贸易总额时增时减,呈波动状。

国际金融服务贸易

5.1.3 关于金融服务贸易谈判 1.谈判的背景

国际服务贸易不断增长,在增长速度 上超过了与之对应的货物贸易的增长速 度。

1997-2006服务贸易出口与货物贸易出口对比 单位:亿美元

年份 项目 服务贸 易出口 额 货物贸 易出口 额 货物贸 易年均 增速 服务贸 易出口 年均增 速 服务贸 易出口 /货物 贸易出 口 13199 13515 14064 14936

4.14%

4.85%

16.85 %

21.50 %

13.70%

15.38 %

2.39%

4.06%

0.35%

7.31%

14.58 %

20.08 %

11.11%

12.08 %

23.61 24.57% %

24.63 %

23.14 %

24.23 %

24.79 %

24.31 %

24.03 %

23.48%

22.81 %

5、多哈回合金融服务贸易谈判最新进展

发达国家希望通过谈 判寻求更深更广的市 场开放和金融自由化。 不主张建立ESM 积极推动政府采购议 题的谈判。 发展中国家提出如果 不考虑他们的特殊发 展要求和执行困难, 将很难做出进一步的 市场准入承诺。 希望通过建立ESM, 实现金融开放的过渡。 对政府采购议题持保 留态度。

2003年金融服务行业前20位出口和进口国家和地区情况 单位:百万美元

2004年世界部分主要国家金融服务贸易进出口情况 单位:十亿美元

2.金融服务贸易国际化

金融服务贸易国际化的含义

金融服务贸易国际化是指金融服务贸 易涉及的主体、客体等日益国际化发展的 趋势。

金融服务贸易国际化的表现

中国金融服务贸易发展现状及对策分析

2009.6一、中国金融服务业进出口现状金融服务业是现代服务业的重要内容,而金融服务贸易也是服务贸易很重要的组成部分。

在国际收支平衡表统计中,金融行业的服务贸易进出口分为“保险服务”和“金融服务”两类。

其中,“保险服务”包括所有货物保险、直接保险(寿险和非寿险)和再保险;“金融服务”则包括所有金融中介服务和其他辅助服务,如信用证佣金和手续费、金融租赁服务、外汇交易服务、商业和消费信贷服务等,大致可归于“银行服务”和“证券服务”两类。

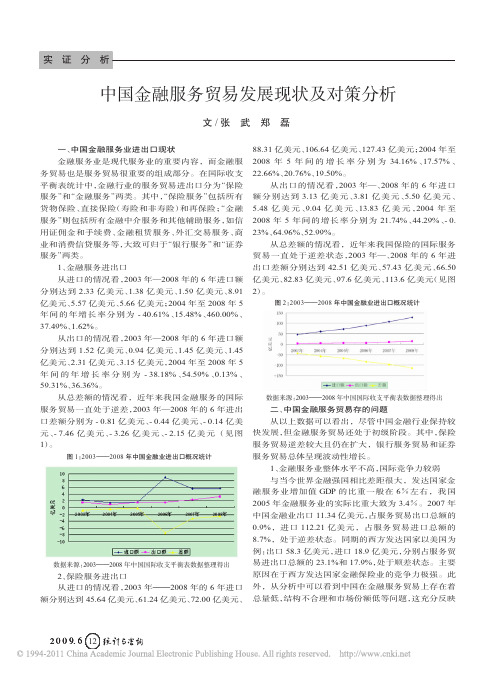

1、金融服务进出口从进口的情况看,2003年—2008年的6年进口额分别达到2.33亿美元、1.38亿美元、1.59亿美元、8.91亿美元、5.57亿美元、5.66亿美元;2004年至2008年5年间的年增长率分别为-40.61%、15.48%、460.00%、37.49%、1.62%。

从出口的情况看,2003年—2008年的6年进口额分别达到1.52亿美元、0.94亿美元、1.45亿美元、1.45亿美元、2.31亿美元、3.15亿美元,2004年至2008年5年间的年增长率分别为-38.18%、54.59%、0.13%、59.31%、36.36%。

从总差额的情况看,近年来我国金融服务的国际服务贸易一直处于逆差,2003年—2008年的6年进出口差额分别为-0.81亿美元、-0.44亿美元、-0.14亿美元、-7.46亿美元、-3.26亿美元、-2.15亿美元(见图1)。

图1:2003———2008年中国金融业进出口概况统计数据来源:2003———2008年中国国际收支平衡表数据整理得出2、保险服务进出口从进口的情况看,2003年———2008年的6年进口额分别达到45.64亿美元、61.24亿美元、72.00亿美元、88.31亿美元、106.64亿美元、127.43亿美元;2004年至2008年5年间的增长率分别为34.16%、17.57%、22.66%、20.76%、19.50%。

国资委三类贸易的定义

国资委三类贸易的定义1. 引言国资委三类贸易是指国务院国有资产监督管理委员会(以下简称国资委)所监管的三类特殊贸易形式。

这些特殊贸易形式在中国的经济发展中扮演着重要角色,对于推动产业升级、促进经济增长具有重要意义。

本文将对国资委三类贸易进行全面详细、完整且深入的阐述。

2. 国资委三类贸易的概述国资委三类贸易主要包括资源性商品贸易、技术服务贸易和金融服务贸易。

这些不同类型的贸易在性质、范围和规模上存在一定差异,但它们都是以国有资产为主体开展的。

2.1 资源性商品贸易资源性商品包括石油、天然气、矿产品等自然资源及其衍生品。

资源性商品贸易是指以资源性商品为主要交易对象的进出口活动。

这种贸易形式在中国经济中占据重要地位,对于满足国内市场需求和推动经济发展具有重要作用。

2.2 技术服务贸易技术服务贸易是指以技术为核心,涉及技术转让、技术咨询、技术合作等形式的国际贸易活动。

这种贸易形式在中国的经济发展中起到了重要的推动作用。

通过引进先进技术和知识,提高我国产业水平,加快产业升级和创新发展。

2.3 金融服务贸易金融服务贸易是指以金融产品和金融服务为主要内容的跨国经济活动。

这种贸易形式包括银行、证券、保险等金融机构提供的各类金融服务。

金融服务贸易对于促进国内金融市场开放、吸引外资和提升国际竞争力具有重要意义。

3. 国资委三类贸易的特点3.1 资源性商品贸易的特点资源性商品贸易具有以下特点:•需求旺盛:随着中国经济的快速发展,对于能源和矿产品等资源性商品的需求持续增长。

•价格波动大:国际市场上资源性商品价格波动较大,对贸易活动带来一定的风险。

•政府干预多:由于资源性商品的战略重要性,政府会对其进行一定的管理和监管。

3.2 技术服务贸易的特点技术服务贸易具有以下特点:•高附加值:技术服务贸易涉及高新技术和知识产权,具有较高的附加值。

•创新驱动:技术服务贸易能够促进创新发展,提升我国产业竞争力。

•跨国合作:技术服务贸易需要跨国企业之间的合作与交流。

文献综述范文

文献综述范文国外学者对金融服务贸易的研究始于20世纪80年代初,但相关文献甚少,对哪种贸易理论适用于金融服务贸易也存在很多不同观点。

其中,外生比较优势模式认为传统贸易理论适用于服务贸易,比较优势理论可以解释国际金融服务贸易的动因;内生比较优势模式认为比较优势可以通过后天专业化研究获得或通过投资创新与经验累积人为创造出来;规模经济模式则认为规模经济是金融服务贸易的主要动因。

二)国内学者关于金融服务贸易的研究现状我国学者对金融服务贸易的研究起步较晚,近年来逐渐得到关注。

其中,有学者从金融服务贸易的贸易模式、开放程度、贸易结构等方面进行了探讨;有学者从金融服务贸易的政策环境、制度建设、风险管理等方面进行了研究。

但总体来说,我国学者对金融服务贸易的研究还比较薄弱,需要进一步深入探讨。

二、战略性贸易政策在我国金融服务贸易中的应用研究一)战略性贸易政策的概念战略性贸易政策是指政府为了促进国内产业发展和提高国际竞争力而采取的一系列贸易政策措施。

这些措施主要包括:关税和非关税壁垒、进口配额、出口补贴、汇率政策、技术壁垒等。

战略性贸易政策的目的是通过保护国内产业、促进技术创新、提高国际竞争力等手段,实现国家经济发展和贸易平衡。

二)战略性贸易政策在我国金融服务贸易中的应用我国金融服务贸易的国际竞争力相对较低,需要采取战略性贸易政策来促进其发展。

具体来说,可以采取以下措施:一是通过关税和非关税壁垒保护国内金融服务业,避免外资的过度进入;二是通过出口补贴等手段扶持国内金融服务业的出口,提高其国际竞争力;三是通过技术壁垒等手段促进国内金融服务业的技术创新和提高,提高其国际竞争力。

当然,这些措施需要在国际贸易规则的范围内进行,不能违反XXX等国际贸易组织的规定。

三、结论与启示金融服务贸易是我国服务贸易的重要组成部分,也是我国未来发展的重点领域之一。

为了促进我国金融服务贸易的发展,需要采取一系列战略性贸易政策措施。

同时,我国学者还需要加强对金融服务贸易的研究,不断提高其研究水平和质量,为我国金融服务贸易的发展提供有力的理论支持。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

The financial services cultural orientation matrixDeborah Stephenson a ,Steve Worthington b ,1,Rebekah Russell-Bennett a ,⇑a School of Advertising Marketing and Public Relations,QUT Business School,Queensland University of Technology,Brisbane,Queensland,Australia bDepartment of Marketing,Monash University,Melbourne,Australiaa r t i c l e i n f o Article history:Received 24October 2011Revised 1June 2012Accepted 3July 2012Available online 10October 2012Keywords:Financial services CultureMarketing strategies Market entrya b s t r a c tWith saturation within domestic marketplaces and increased growth opportunities overseas,many finan-cial service providers are investing in foreign markets.However,cultural attitudes towards money can present market entry challenges to financial service providers.The industry would therefore benefit from a strategic model that helps to align financial marketing mixes with the cultural dimensions of a foreign market.The Financial Services Cultural Orientation (FSCO)Matrix has therefore been designed,with three cultural dimensions identified which influence preference for financial products;preference for cash,aversion to debt and savings orientation.Based on a combination of these dimensions and their relative strength within a culture,eight different consumer segments for financial products are identified,and marketing strategies for each consumer segment are then proposed.Three cultural clusters from the GLOBE Project House et al.(2002)are used to highlight possible geographic markets for each of these con-sumer segments.In particular,this paper focuses on GLOBE’s Confucian Asia,Southern Asia and Anglo cultural clusters,as these clusters represent the most well established financial markets in the world and the fastest growing financial markets for the future.The FSCO Matrix provides the financial services industry with an innovative and practical tool for addressing cross-cultural challenges and developing successful marketing strategies for entry into foreign markets.Ó2012Australian and New Zealand Marketing Academy.Published by Elsevier Ltd.All rights reserved.1.IntroductionCorporations are facing an increasingly global business world (Javidan and House,2002)and Saturation in the domestic market and increased growth opportunities overseas are encouraging many financial service providers to invest in foreign markets.As an example following China’s entry into the World Trade Organiza-tion in 2001,major United States (US)and European banks made inroads into the Chinese credit card market as part of their efforts to strengthen their retail banking business (Mollet,2004).With domestic growth stagnating in the early 2000s,Japan Credit Bureau (JCB),the largest credit card brand in Japan,has expanded into Chi-na by forming an alliance with the Bank of China (Mollet,2004).More recently,India has also started to open up its financial sector to foreign investment.Credit Suisse recently received in-principle approval for a banking license in India,with other global players now lined up for entry,including Goldman Sachs,Morgan Stanley,ICBC and National Australia Bank (Leahy,2010;The Financial Express,2010).However,entry into a new financial market is challenging,as consumer culture influences the success or failure of specific prod-ucts (Solomon et al.,2007).Culture is the accumulation of shared meanings,rituals,norms and traditions among the members of a society and ‘‘consumption choices simply cannot be understood without considering the cultural context in which they are made:culture is the ‘lens’through which people view products’’(Solomon et al.,2007,p.468).However the whole area of consumer culture theory (CCT)is not,‘a unified,grand theory,nor does it aspire to such nomothetic claims’(Arnould and Thompson,2005).Nonethe-less these authors claim that CCT researchers share a common theoretical orientation towards the study of cultural complexity,that links their research efforts.Furthermore CCT theorists study consumption in its contexts,in order to generate new constructs and theoretical insights.These research aspirations have high-lighted that the ‘real world’for any given consumer,is neither unified,monolithic nor transparently rational.This research ‘lens’then leads to the proposition that cultural attitudes toward money,present challenges in marketing financial products,within foreign markets.In China,for example,negative perceptions of borrowing through formal channels have created a resistance to bank loans (Worthington,2010).Instead,Chinese consumers prefer to borrow through family and friends and tend to pay cash,even for ‘big ticket’items,such as cars and houses (Worthington,2010).More1441-3582/$-see front matter Ó2012Australian and New Zealand Marketing Academy.Published by Elsevier Ltd.All rights reserved./10.1016/j.ausmj.2012.07.001⇑Corresponding author.Tel.:+61731382894;fax:+61731381811.E-mail addresses:debluey@ (D.Stephenson),steve.worthington@.au (S.Worthington),Rebekah.bennett@.au (R.Russell-Bennett).1Tel.:+61399032754;fax:+61399032900.recent research(Worthington et al.,2011)into credit cards in a Chinese cultural context has focused on the attitudes of the young, affluent Chinese,to the adoption and subsequent use of credit cards.This study highlighted the notion of guilt felt in China when using credit cards instead of cash.The research also introduced the term’future money’to describe the pay later facility that a credit card offers.Another aspect favoring the continued use of cash in this culture is that it is a means of signaling wealth,which is an important status aspect in China and this was thought to influence the relatively low level of credit card use in China.The research also revealed a generational issue that was believed to impede credit card adoption.Thus whilst most of the respondents in the qualitative phase of the research,felt that they belonged to a new generation,one that is different to that of their parents and grandparents,nevertheless,the young affluent Chinese,still felt guilty using‘future money’and spending rather than saving.In-deed earlier research by Smith and Hill(2009),found that whilst there had been recent rapid socio-economic change within China, there was evidence to suggest strong value system continuity, hence the young,affluent Chinese tend to gravitate towards the familiar,whilst generally resisting that which is unfamiliar.As a basic marketing rule,financial service providers must under-stand the attitudes of their customers to better tailor their market-ing and communication programs(Kanyak and Harcar,2001). Different cultural attitudes towardfinancial products may therefore require changes to the marketing mix,such as new branding and positioning strategies,new product developments or new incentive schemes.Previous academic literature has explored the different cultural perceptions of money around the world(Al-Moharby and Khatib,2007;Bonsu,2008;Chui and Kwok,2008;Falicov,2001; Kwok and Tadesse,2006).However,few studies have addressed how the current state offinancial services within a market has been influenced by the cultural attitudes towards money.A theoretical framework has also yet to be developed that explains what impact different cultural perceptions of money have on the consumption offinancial products.This information would be useful forfinancial service providers looking to expand into new foreign markets.Financial institutions need a strategic model that helps align their product offerings with the cultural dimensions of a foreign market.Cultural dimensions are a useful way of classifying behav-ior and identifying market segments.Three cultural dimensions have been identified in this paper as relevant to the consumption offinancial ing these dimensions,this paper will pres-ent a conceptual strategy matrix forfinancial institutions,profiling eight consumer segments forfinancial products.The Financial Ser-vices Cultural Orientation(FSCO)Matrix will outline thefinancial preferences for each of the consumer segments and propose effec-tive marketing strategies for reaching them.2.Literature ReviewThe purpose of the literature review is to present a conceptual background to the FSCO Matrix that will be presented.The FSCO Matrix has been designed using three major cultural dimensions identified in the literature as having an effect on the consumption offinancial products in foreign markets.These three cultural dimensions will helpfinancial service providers to understand how cross-cultural influences can impact on their marketing strat-egies(Assael et al.,2007).Cultural clusters identified in the GLOBE Project(House et al.,2002)are used to highlight possible geo-graphic markets where each consumer segment of the FSCO Matrix may be found.Thefinancial services industry is one that has evolved over cen-turies,from the clay tokens of Ancient Mesopotamia5000years ago,to the hedge funds of today(Ferguson,2008).This long history makes thefinancial services industry a mature market that needs to continuously expand in order to grow.Historically,western financial institutions have undertaken this expansion,often through entry into eastern markets.The westernfinancial model wasfirst spread in the guise of imperialism and then through glob-alization(Ferguson,2008).However,‘‘the globalization offinance has now...blurred the old distinction between developed and emerging markets,turning China into America’s banker-the Communist creditor to the capitalist debtor’’(Ferguson,2008,p.4).The economic development of eastern countries has seen many easternfinancial institutions now entering western markets.In 2009,China Construction Bank opened itsfirst branch in the US, joining four other Chinese banks already present within this mar-ket(The Information Company,2009).The China Construction Bank’s entry into a western market demonstrates that the tradition of westernfinancial institutions entering eastern markets is fast becoming obsolete and that,whilst cultural factors may influence consumer demand,foreign market entry is no longer bound by tradition.The GLOBE Project(House et al.,2002)has been selected as a relevant theoretical framework to guide research into the cultural perceptions of money within two targeted cultural clusters.The GLOBE Project,the most recent global attempt to classify cultural differences,studied sixty-one nations and grouped them into ten cultural clusters based on their similarities along nine dimensions. GLOBE is considered by many academics to offer superior benefitsTable1Nine cultural dimensions of GLOBE Project.1.Uncertainty Avoidance The extent to which members of an organization or society strive to avoid uncertainty by reliance on social norms,rituals,and bureaucratic practices to alleviate the unpredictability of future events2.Power Distance The degree to which members of an organization or society expect and agree that power should be unequally shared.3.Collectivism I Societal Collectivism reflects the degree to which organizational and societal institutional practices encourage and rewardcollective distribution of resources and collective action.Low scores reflect individualistic emphasis and high scores reflectcollectivistic emphasis by means of laws,social programs or institutional practices.4.Collectivism II In-Group Collectivism reflects the degree to which individuals express pride,loyalty and cohesiveness in their organizations or families.5.Gender Egalitarianism The extent to which an organization or a society minimizes gender role differences and gender discrimination.6.Assertiveness The degree to which individuals in organizations or societies are assertive,confrontational,and aggressive in social relationships*7.Future Orientation The degree to which individuals in organizations or societies engage in future-oriented behaviors such as planning,investingin the future,and delaying gratification.8.Performance Orientation The extent to which an organization or society encourages and rewards group members for performance improvement and excellence.(This dimension includes the future oriented component of the dimension called Confucian Dynamism by Hofstede and Bond,1988).9.Humane Orientation The degree to which individuals in organizations or societies encourage and reward individuals for being fair,altruistic,friendly,generous,caring,and kind to others.(This dimension is similar to the dimension labeled Kind Heartedness byHofstede and Bond,1988).(House et al.,2002,p.6).*Thefirst six culture dimensions had their origins in the dimensions of culture identified by Hofstede(1980).Thefirst three scales are intended to reflect the same constructs as Hofstede’s dimensions labeled Uncertainty Avoidance,Power Distance,and Individualism.2 D.Stephenson et al./Australasian Marketing Journal21(2013)1–9to Hofstede’s(1980)cultural factors(Javidan et al.,2006;Smith, 2006).GLOBE’s cultural clusters can provide useful informationtofinancial service providers,who mayfind it less risky and more profitable to expand into similar cultures to their own,rather than those that are drastically different(Javidan and House,2002).The definitions of the nine dimensions are shown in Table1.This paper will focus on the expansion offinancial institutions in Anglo countries into foreign markets belonging to GLOBE’s Southern Asia and Confucian Asia cultural clusters(see Table2). These two clusters offer some of the greatest future growth oppor-tunities in the world for both eastern and westernfinancial service providers.The Indian credit card market,for example,is growing at an annual rate of35%(Euromonitor International,2010b).Many financial institutions from GLOBE’s Anglo cluster are therefore increasing their presence within this market.Recently the,Australian and New Zealand(ANZ)bank received approval for a banking licence in India,with other global names also lined up for entry, including Goldman Sachs,Morgan Stanley and National Australia Bank(Leahy,2010;The Financial Express,2010).The growing importance of these two cultural clusters to thefinancial services industry makes it essential to understand their cultural orientation in order to succeed within them(Gupta et al.,2002a).Henry (2010),makes the point in his review of consumer rights and responsibilities in the credit card setting,that this requires con-stant trade-offs that mirror the struggle between liberal and liber-tarian political positions,that dominate the GLOBE‘s Anglo cluster. In the Southern Asian and Confucian Asian clusters,there may well be other political positions that need to be understood and dealt with,if market entry is to be successfully achieved.3.Cultural dimensions that influence the consumption offinancial productsFrom the literature and industry evidence,three important cultural dimensions have emerged as having a significant influence on the consumption offinancial products(refer to Fig.1).These dimensions are preference for cash(Worthington,2005;Euromon-itor International,2010b),aversion to debt(Shintani,2000;Euro-monitor International,2010b)and the overall importance placed upon saving(savings orientation)(Terpstra and Sarathy,2000; Beck&Webb,2003).These three dimensions are relevant to the consumption offinancial products across all cultures and are not limited to the specific cultural explorations of this paper.Thus cultures that possess high and low levels of each dimension are shown in Table3.The literature and industry evidence for cultural perceptions of money and the impact onfinancial service offerings are shown in Table3.An analysis of this research revealed three dominant ultural dimensions relevant tofinancial services;preference for cash,aversion to debt and savings orientation.Culture can be used to explain the cross-country variation of life insurance consump-tion.Kwok and Tadesse(2006)find that individualism has a posi-tive effect on the consumption of market-based life insurance, whilst collectivist cultures are more likely to rely on the support of their social networks.The low uptake of life insurance in the Philippines,classified within GLOBE’s Southern Asia cluster,which scored high on group collectivism,further supports thesefindings (Valerio,2010;Gupta et al.,2002a).The strong collectivist culture of China has meant that many consumers often seekfinancial support through informal channels,such as family and friends, resulting in a very underdeveloped tradition of credit,with banks seen mainly as a place for saving(Worthington,2005).Other literature discusses the role of cash within cultures and the over-riding preference for this payment method over others. Worthington(1998)compares thefinancial payment preferences of Japan and the UK,finding that whilst the UK has become one of the most card-centric countries in the world,cash still remains the predominate mode for transactions in Japan.Strong prefer-ences for cash are also still prevalent within China,where consum-ers will always carry enough cash with them to avoid losing face if their credit card or debit card is rejected(Worthington,2005).The cultural perception of money in China has led to an aversion to debt and borrowing,with a strong emphasis placed on saving and living within ones means(Worthington,2005;Thompson and Worthington,2010).Negative perceptions of debt have pre-sented similar obstacles in Japan to the widespread use of credit cards(Shintani,2000).Other examples of how the perception of money impacts onfinancial product offerings is presented in Table3.3.1.Dimension1:Preference for cashOne of the predominant cultural influences affecting the con-sumption offinancial products is the preference for cash(payment through the physical forms of money,such as notes or coins)within a culture.In some cultures there is still an over-riding preference for cash over other forms of payment,which has negatively influ-enced the uptake and use of more advancedfinancial products such as credit cards(Worthington,2005;Worthington,1998;Shapiro, 1993).Preference for cash appears to be driven by a trust in this commodity,or perhaps a lack of trust in the alternatives or institu-tions(Euromonitor International,2010c;Thompson and Worthing-ton,2010;Worthington,2005).Cultures that demonstrate a high preference for cash also appear to have high uncertainty avoidance (Worthington,2005).A preference for cash may manifest a reliance on social norms,rituals,and bureaucratic practices to alleviate the unpredictability of future events(House et al.,2002).Trust in cash,and its historical presence within a culture,means that its relevance may remain strong.Many older Iranians,for example,are still attached to cash and seeing the physical transac-tion of money(Euromonitor International,2010c).Furthermore, many Chinese consumers will always carry enough cash with them to avoid losing face if their credit card or debit card is rejected (Worthington,2005).Financial service providers need to be aware of an underlying cultural preference for cash,as this may dictate whatfinancial products will be accepted in the market.3.2.Dimension2:Aversion to debtAn aversion to debt is a significant cultural factor that can affect the consumption offinancial products.Negative perceptions ofTable2GLOBE Project’s cultural clusters.Cultural cluster CountriesSouthern Asia India,Indonesia,Philippines,Malaysia,Thailand,Iran Confucian Asia Taiwan,Singapore,Hong Kong,South Korea,China,Japan Anglo England,Australia,Canada,New Zealand,Ireland,USA.Source:House et al.(2002).Preference forcashAversion todebtSavingsorientationConsumption of financial productsD.Stephenson et al./Australasian Marketing Journal21(2013)1–93debt can hinder the acceptance of products that are designed to accumulate debt,such as loans and credit cards(Gong,2003; Thompson and Worthington,2010;Shintani,2000;Worthington, 2005).Cultures that demonstrate high aversion to debt may also a strong humane orientation(House et al.,2002).Cultures that have a strong humane orientation encourage and reward individu-als for being generous,caring and kind to others(House et al., 2002).This humane orientation may therefore lead to consumers lending and borrowing from one another,rather than through for-mal channels.In India,for example,a high humane orientation,together with an overall negative perception of debt,has impacted on thefinan-cial services sector.Debt has traditionally been associated with poverty and poor money management.Many Indians have there-fore preferred to borrow through informal channels,such as family and friends,rather thanfinancial institutions(Euromonitor Inter-national,2010b).An aversion to debt can also affect the traditional use offinan-cial products(Cards International,2007;Shintani,2000;Worthing-ton,1998).For instance,the way in which credit cards are used in Japan is substantially different to how they are used in western countries.Japanese consumers tend to use their credit cards for larger,less frequent purchases and are more likely to pay off their credit card in full(Shintani,2000;Worthington,1998).Australians, however,are more likely to use their credit cards in place of cash, with70%of cardholders regularly using revolving credit(Cards International,2007;Euromonitor International,2010a).An aversion to debt can influence both the adoption offinancial products as well as the way in whichfinancial products are used. Financial service providers may therefore need to adapt their marketing strategies.For example,Japan’s low use of revolving credit may alter the way in which revenue is generated within this market(Shintani,2000;Worthington,1998).3.3.Dimension3:Savings orientationThe importance of saving within a culture impacts on the con-sumption offinancial products.An individual who has a strong preference for saving may also have a strong future orientation (House et al.,2002).Individuals in countries such as Japan and Chi-na engage in future-oriented behaviors,such as planning,investing in the future,and delaying gratification(Terpstra and Sarathy, 2000;Beck&Webb,2003).A high savings orientation is antici-pated to be related to a preference for products that encourage saving or the spending of one’s own money(Clemes et al.,2010; Worthington,2010).External motivations,such as cultural traditions and future uncertainties appear to influence an individual’s preference for saving(Worthington,2010).This is most evident in China,where the cultural pressure to climb the‘three mountains’-education, accommodation and healthcare-has led to a personal savings rate of around25%(Euromonitor International,2010e;Worthington, 2005).A strong savings orientation has led to the acceptance of debit cards and in China and in2010,there were2.1billion debit cards(also known as bankcards)in circulation,many of them based on a savings account held by a Chinese individual,in a Chinese bank.(Worthington et al.,2011).A low emphasis on saving within a culture can also impact on the adoption(or non-adoption)offinancial products.In the Philip-pines,only1in10people regularly save a sufficient amount ofTable3Cultural perceptions of money and impact onfinancial service offerings.Cultural Dimension Financial product Country Financial consumption impact ReferenceAversion to debt Credit cards China Borrowing money is perceived as a sign of being incapable to provide,a sign ofliving beyond one’s means-avoidance of formal loan options Worthington,2005; Gong,2003Aversion to debt Credit cards Japan Credit cards seen as debt and thus used for larger,less frequent purchases.Consumers more likely to pay off credit card in full,rather than use revolvingcredit.Credit cards used to withdraw cash Shintani,2000; Worthington,1998Aversion to debt Other loans China Borrowing money perceived as a sign of being incapable to provide,a sign ofliving beyond one’s means.More likely to borrow through informal channelssuch as relatives Worthington,2005; Gong,2003Aversion to debt Life insurance Various Countries high on individualism purchase more market-based life insurance,rather than relying on fellow kinsmen to providefinancial supportChui and Kwok,2008Aversion to debt Mortgages UK(Islamicsub-culture)Accumulation of interest forbidden under Islamic law.Development of newinterest-free mortgages,where rent,as opposed to interest,is paid back to thelender,in addition to monthly mortgage repayments.Casciani,2002;BBC Online,2003Aversion to debt Other loans UK(Islamicsub-culture)Development of new product offerings compliant with Islamic law that avoidaccumulation of interest(e.g.car insurance)Pigott,2009;Brignall,2008Preference for cash Credit cards China Consumers prefer to borrow through‘informal’channels either at low or nointerest rate,borrowing relies on pre-established and trustworthy relationships(Guanxi)Worthington,2010 Preference for cash Credit cards UK One of the world’s largest card-centric countries,increasing cashless society Worthington,1998Preference for cash Cash Japan Cash still the predominate mode of payment.High amount of ATMs and highwithdrawal limits reinforces consumer preference for cash Worthington,1998; Shapiro,1993Preference for cash Cash China Consumers always carry enough cash with them to avoid losing face if theircredit card or debit card is rejectedWorthington,2005Preference for cash Cash China Most common method of payment for online purchases is cash upon delivery-impacts online business transactionsBin,Chen&Sun,2003Savings culture Life insurance Japan favorable:favourable attitude towards saving and providing for the future.Oneof the largest insurance markets in the world,90%of households have lifeinsurance coverage.Policies protecting against cancer growing in popularity Terpstra and Sarathy, 2000;Beck& Webb,2003Savings culture Savings accounts China High personal savings due to uncertainty about long-term welfare.Financialproducts encouraging saving are popular(e.g.savings accounts,debit cards)Worthington,2005Savings culture Life insurance UK High uncertainty avoidance means increased planning for the future.Britishcitizens invested more than40%in life insurance from1986–1990Beck&Webb,2003Savings culture Life insurance Philippines Low uncertainty avoidance has resulted in a low uptake of life insurance as‘‘fate will provide’’Valerio,2010Savings orientation Savings accounts UK(Islamicsub-culture)Development of new product offerings compliant with Islamic law.Savingsaccount with no overdraft or credit card facility,no interest generatedBBC Online,20034 D.Stephenson et al./Australasian Marketing Journal21(2013)1–9their income(Euromonitor International,2010d).As a result,the insurance market has struggled to take off,with a2008Citibank survey revealing that32%of respondents had no insurance policy whatsoever(Euromonitor International,2010d;Valerio,2010). The low level of acceptance of insurance products in the Philip-pines has impacted on the product offerings offinancial institu-tions,such as ANZ,which has cut insurance from their portfolio in this region(ANZ,2010).These three dominant cultural dimensions therefore provide a framework to the development of the FSCO Matrix.A combination of these dimensions and their relative strength within a culture lead to a predisposition for certainfinancial products.By under-standing these cultural preferences,financial service providers will be able to introduce more relevant products to the marketplace.4.Proposed FSCO MatrixThe three cultural dimensions previously identified can be used to develop marketing strategies for entering foreignfinancial markets.The FSCO Matrix(see Table4)can used by anyfinancial service provider seeking to enter a foreign market that is culturally different from their own.The FSCO Matrix is therefore applicable to both eastern and westernfinancial institutions.Different combi-nations of the three cultural dimensions are used to develop eight consumer segments forfinancial products.The application of this matrix involves two steps;step one,diagnose current attitudes and step two,select consumer segments.5.Step1:Diagnose current attitudes towards money and profile foreign marketIn order to develop effective marketing strategies for a foreign market,first,the cultural disposition of this market must be mea-sured.To do this,a sample of consumers in the target country should be assessed for their preference to cash,aversion to debt and savings orientation.Based on their responses,individuals should be classified into one of the eight consumer segments in the FSCO matrix.Once all respondents have been assigned to a consumer segment, the organization can then identify the most attractive target mar-kets within the foreign market and conduct a survey of these poten-tial customers.Based on their scores for the three dimensions,all respondents would be assigned to a consumer segment and the proportion of consumers in each segment calculated.The most attractive segments of the Chinese market would then emerge. For example,if35%of respondents were classified as free-spirited spenders this may represent the largest segment of the Chinese market.This segment may be an attractive market if the organiza-tion has products that appeal to this market which offer competitive advantage.Financial institutions seeking to enter the Chinese mar-ket would therefore focus their marketing efforts on this segment.6.Step2:Select consumer segment and develop targeted marketing strategyThis paper proposes that each combination of cultural dimen-sions requires a different marketing strategy forfinancial products.For each of the eight consumer segments,we define the character-istics based on prior research and suggestfinancial services marketing strategies that may appeal.We then conclude the sec-tion with a summary of suggested marketing strategies for each consumer segment.A summary of the suggested marketing strate-gies for each consumer segment of the FSCO Matrix is shown in Table5.We also suggest in which of the GLOBE’s cultural cluster the majority of each consumer segment might be found.6.1.Free-spirited spendersFree-spirited spenders have a low preference for cash,a low aversion to debt and a low savings orientation,thus they like cred-it,are comfortable with debt and prefer to spend rather than save. They are therefore open to sophisticatedfinancial products that may lead them into debt,such as credit cards and personal loans. Free-spirited spenders may generally belong to GLOBE’s Anglo cul-tural cluster(refer to Table1).The GLOBE Project found this cluster to score high on power distance,meaning that a high emphasis of consumption is placed on status and authority(House et al.,2002).A free-spirited attitude towards spending and accumulating debt may be a symptom of the need to demonstrate status or an inabil-iyy to control spending.Financial products that appeal to this category include those that allow consumers to borrow money at a low interest rate,as low savings may inhibit the ability to pay back debt quickly(Euro-monitor International,2010a).Such products include debit cards with overdraft facilities and credit cards with revolving credit. However,as a result of the economic downturn,free-spirited spenders are increasingly curbing their spending and attempting to pay off their debt.Manyfinancial service providers have there-fore introduced credit cards with balance transfers that allow consumers to consolidate their debt onto one card.HSBC,Citibank and ANZ are just some of the banks that have introduced these cards,competing on low interest rates or longer interest free repayment periods(Credit Card Offers,2010).Free-spirited spend-ers are also increasingly using debit cards in place of credit cards. This has led to the introduction of debit cards with e-commerce capabilities that consumers can use in place of credit cards for online purchases.The success of the Visa debit card highlights the popularity of this new technology,with more than741million cards in worldwide circulation(Visa,2010).Financial products that will succeed amongst free-spirited spenders include those that offer the ability to consolidate debt or pay off debt quicker.Price will become an increasingly impor-tant factor to this segment,withfinancial institutions competing on interest rates or longer repayment periods.Free-spirited spend-ers may also respond to reward schemes,such as bonus shopping points and gift vouchers,in return for using their debit cards.6.2.Plastic fantasticsPlastic fantastics have a low preference for cash,low aversion to debt and a high savings orientation.They are considered to be‘fan-tastic’byfinancial service providers because they are open to mod-ernfinancial products that may generate debt(e.g.credit cards), but have thefinancial capabilities to repay what they owe,as they have being culturally conditioned to save.Plastic fantastics areTable4Financial Services Cultural Orientation Matrix.Low preference for cash High preference for cashLow aversion to debt High aversion to debt Low aversion to debt High aversion to debtLow savings orientation Free-spirited spenders Cautious optimists Optimistic laggards Back to basics High savings orientation Plastic fantastics Sensible savers Cashed-up sensible spenders Cashed-up scepticsD.Stephenson et al./Australasian Marketing Journal21(2013)1–95。