最新会计报表附注中英文对照

会计报表科目中英文对照

一、企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流动资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due within one year减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivable due within one year减:短期投资跌价准备Less: Impairment for current investment短期投资净额Net bal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账准备Less: Bad debt provision for Account receivable应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账准备Less: Bad debt provision for Other receivable其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less: Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due within one year一年内到期的应收融资租赁款Finance lease receivables due within one year其他流动资产Other current assets流动资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment委托贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值准备Less: Impairment for long-term equity investment 减:长期债权投资减值准备Less: Impairment for long-term debt investment 减:委托贷款减值准备Less: Provision for entrusted loan receivable长期投资净额Net bal of long-term investment其中:合并价差Include: Goodwill (Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less: Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less: Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值准备Less: Impairment for construction in progress在建工程净额Net bal of construction in progress固定资产清理Liquidation of Fixed assets固定资产合计Total fixed assets无形资产及其他资产Other assets & Intangible assets无形资产Intangible assets减:无形资产减值准备Less: Impairment for intangible assets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease –Unguaranteed residual values融资租赁——应收融资租赁款Finance lease –Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets & intangible assets递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability & Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advance from customers Deposit Received应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Other payable预提费用Accrued Expense预计负债Anticipation Liabilities递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year其他流动负债Other current liability流动负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants & Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益)Owners’Equity实收资本(或股本)Paid in capital减;已归还投资Less: Capital redemption实收资本(或股本)净额Net bal of Paid in capital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include: Statutory reserves未确认投资损失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include: Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability & Equity三、利润及利润分配表Income statement and profit appropriation一、主营业务收入Revenue减:主营业务成本Less: Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit ( - means loss) 加:其他业务收入Add: Other operating income减:其他业务支出Less: Other operating expense减:营业费用Selling & Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列)Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列)Add: Investment income补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less: Non-operating expense四、利润总额(亏损总额以“—”填列)Profit before Tax减:所得税Less: Income tax少数股东损益Minority interest加:未确认投资损失Add: Unrealised investment losses五、净利润(净亏损以“—”填列)Net profit ( - means loss)加:年初未分配利润Add: Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution( - means loss)减:提取法定盈余公积Less: Appropriation of statutory surplus reserves提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and welfare fund提取储备基金Appropriation of reserve fund提取企业发展基金Appropriation of enterprise expansion fund利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners' distribution减:应付优先股股利Less: Appropriation of preference share's dividend提取任意盈余公积Appropriation of discretionary surplus reserve应付普通股股利Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital 八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses from natural disaster3.会计政策变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting policies4.会计估计变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting estimates5.债务重组损失Losses from debt restructuring另一个版本。

财务报表附注翻译-新版.pdf

****** CO., LTDNOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31, 2013(All amounts in RMB Yuan)I. Company Profile******* Co., Ltd. (hereinafter referred to as the "Company") is a limited liability company (Sino-foreign joint venture) jointly invested and established by **** Co., Ltd. and ******* Limited on 24 June 2013. On December 26, 2013, the shareholders have been changed to ***** CO., LTD and ******* LIMITED.Business License of Enterprise Legal Person License No.:Legal Representative:Registered Capital: RMB (Paid-in Capital: RMB )Address:Business Scope: Financing and leasing business; leasing business; purchase of leased property from home and abroad; residue value treatment and maintenance of leased property; consulting and guarantees of lease transaction (articles involved in the industry license management would be dealt in terms of national relevant stipulations) II. Declaration on following Accounting Standard for Business EnterprisesThe financial statements made by the Company are in accordance with the requirements of Accounting Standard for Business Enterprises, which reflects the financial position, financial performance and cash flow of the Company truly and completely.III. Basic of preparation of financial statementsThe Company implements the Accounting Standards for Business Enterprises (,Finance and Accounting [2006] No. 3”) issued by the Ministry of Finance on February 15, 2006 and the successive regulations. The Company prepares its financial statements on a going concern basis, and recognizes and measures i ts accounting items in compliance with the Accounting Standards for Business Enterprises – Basic Standards and other relevant accounting standards, application guidelines and criteria for interpretation of provisions as well as the significant accounting policies and accounting estimates on the basis of actual transactions and events.IV. The main accounting policies, accounting estimates and changesFiscal yearThe Company adopts the calendar year as its fiscal year from January 1 to December 31.Functional currencyRMB was the functional currency of the Company.Accounting measurement attributeThe Company adopts the accrual basis for accounting treatments and double-entry bookkeeping of borrowing for financial accounting. The historical cost is generally as the measurement attribute, and when accounting elements determined are in line with the requirements of Accounting Standards for Enterprises and can be reliably measured, t he replacement cost, net realizable value and fair value can be used for measurement.Accounting method of foreign currency transactionsThe Company?s foreign currency transactions adopt approximate spot exchange rate of the transaction date to convert into RMB in accordance with systematic and rational method; on the balance sheet date, the foreign currency monetary items use the spot exchange rate of the balance sheet date. All balances of exchange arising from differences between the balance sheet date spot exchange rate and the initial recognition or the former balance sheet date spot exchange rate, except that the exchange gains and losses arising by borrowing foreign currency for the construction or production of assets e ligible for capitalization are transacted i n accordance w ith capitalization principles, are included in profit or loss in this period; the foreign currency non-monetary items measured at historical cost will still be converted with the spot exchange rate of the transaction date.The standard for recognizing cash equivalentWhen making the cash flow statement, cash on hand and deposits readily to be paid will be recognized as cash, and short-term (usually no more than three months), highly liquid and readily convertible to known amounts of cash with insignificant riskof changes in value are recognized as cash equivalent.Financial InstrumentsClassification, recognition and measurement of financial assets- The company at the time of initial recognition of financial assets divides it into the following four categories: financial assets measured at fair value with changes included in the profit or loss of this period, loans and receivables, financial assets available for sale and held-to-maturity investments. Financial assets are measured at fair value when initially recognized. Relevant transaction costs of financial assets measured at fair value with changes included in the profit or loss of this period are recognized in profit or loss of this period, and relevant transaction costs of other categories of financial assets are recognized in the amount initially recognized.-- Financial assets measured at fair value with changes included in the profit or loss of this period refer to the short-term sales financial assets, including financial assets held for trading or financial assets measured at fair value with changes i ncluded in the profit or loss of this period designated upon initial recognition by the management. Financial assets measured at fair value with changes included in the profit or loss of this period are subsequently measured at fair value, and the interest or cash dividends obtained during the holding period will be recognized as investment income, and the gains or losses of the change in fair value at the end of this period are recognized in the profit or loss in this period. When it is disposed, the difference between the fair value and the initial recorded amount is recognized as investment income, while adjusting gains from changes in the fair value.--Loans and receivables: the non-derivative financial assets w ithout the price in an active market and with fixed and determinable recovery cost are classified as loans and receivables. Loans and receivables adopt the effective interest method and take amortized cost for subsequent measurement, and gains or losses arising from derecognition, impairment or amortization are included in the profit or loss of this period.-- Financial assets available for sale: including non-derivative financial assets available for sale recognized initially and other non-derivative financial assets except for loans and receivables, held-to-maturity investments and trading financial assets. Financial assets available for sale are subsequently measured at fair value, and interest or cash dividends obtained during the holding period will be recognized as investment income, and gains or losses arising from the changes in fair value at the end of this period are recognized directly in owners' equity until the financial asset is derecognized or impaired and then is recognized as the profit or loss in this period.-- Held-to-maturity investments: the non-derivative financial assets with clear intention and ability to hold to maturity by the management of the company, a fixed maturity date and fixed or determinable payments are classified as held-to-maturity investments. Held-to-maturity investments adopt the effective interest method and take amortized cost for subsequent m easurement, a nd gains or losses arising from derecognition, impairment or amortization are included in the profit or loss of this period.Classification, recognition and measurement of financial liabilities- The company at the time of initial recognition of financial liabilities divides it intothe following two categories: financial liabilities measured at fair value with changes included in the profit or loss of this period and other financial liabilities. Financial liabilities are measured at fair value when initially recognized. Relevant transaction costs of financial liabilities measured at fair value with changes included in the profitor loss of this period are recognized in profit or loss of this period, and relevant transaction costs of other financial liabilities are recognized in the amount initially recognized.-- Financial liabilities measured a t fair value with changes included in the profit or loss of this period include the trading financial liabilities and financial liabilities measured at fair value with changes included in the profit or loss of this period designated upon initial recognition. Financial liabilities are subsequently measured at fair value, and the gains or losses of the change in fair value are recognized in the profit or loss in this period.-- Other financial liabilities: adopting the effective interest method and taking amortized cost for subsequent measurement. The gains or losses arising from derecognition or amortization is included in the profit or loss of this period. Requirements for derecognition of financial liabilitiesFinancial liabilities shall be entirely or partially derecognized if the present obligations derived from them are entirely or partially discharged. Where the Company enters into an agreement with a creditor so as to substitute the current financial liabilities with new ones, and the contract clauses of which are substantially different from those of the current ones, it shall recognize the new financial liabilitiesin place of the current ones. Where substantial revisions are made to some or all of the contract clauses of the current financial liabilities, the Company shall recognize the new financial liabilities after revision of the contract clauses in place of the currentones entirely or partially.Upon entire or partial derecognition of financial liabilities, differences between thecarrying amounts of the derecognized financial liabilities and the consideration paid (including non-monetary assets surrendered or new financial liabilities assumed) are charged to profit or loss for the current period.Where the Company redeems part of its financial liabilities, it shall allocate the carrying amounts of the entire financial liabilities between the relative fair values ofthe parts that continue to be recognized and the derecognized parts on the redemption date. Differences between the carrying amounts allocated to the derecognized parts and the consideration paid (including non-monetary assets surrendered and the new financial liabilities assumed) are charged to profit or loss for the current period. Recognition and measurement for transfer of financial assetsIf the Company has transferred nearly all of the risks and rewards relating to the ownership of the financial assets t o the transferee, they shall be derecognized. I f it retains nearly all of the risks and rewards relating to the ownership of the financial assets, they shall not be derecognized and will be recognized as a financial liability. If the Company has not transferred nor retained nearly all of the risks and rewards relating to the ownership of the financial assets:(1) to give up the control of the financial assets to be derecognized; (2) not giving up control of the financial asset to be recognized based on the extent of its continuing involvement in the transferred financial assets and liabilities are recognized accordingly.If the transfer of entire financial assets satisfy the criteria for derecognition, differences between the amounts of the following two items shall be recognized in profit or loss for the current period: (1) the carrying amount of the transferred financial asset; (2) the aggregate consideration received from the transfer plus the cumulative amounts of the changes in the fair values originally recognized in the owners? equity. If the partial transfer of financial assets satisfy the criteria for derecognition, the carrying amounts of the entire financial assets transferred shall be split into the derecognized and recognized parts according to their respective fair values and differences between the amounts of the following two items are charged to profit or loss for the current period: (1) the carrying amounts of the derecognized parts;(2) The aggregate consideration for the derecognized parts plus the portion of the accumulative amounts of the changes in the fair values of the derecognized parts which are originally recognized in the owners? equity.Determination of the fair value of financial instruments- If financial instruments trade in an active market, the quoted price in an active market determines its fair value; if financial instrument trade not in an active market, the valuation techniques determine the fair value. Valuation techniques include recent market transaction price reference to the familiar situation and volunteer transaction, current fair value reference to other substantially similar financial instruments, discounted cash flow method and option pricing model and so on.Test and Provisions for impairment loss on financial assets--Except trading financial assets, the Company makes assessment o n the carrying values of financial assets at the balance sheet date. If there is evidence that the fair value of specific financial asset has been impaired, provisions for impairment loss is made accordingly.-- Measurement of impairment of financial assets measured at amortized costIf there is objective evidence that the financial asset measured at amortized cost has been impaired, the carrying amount of the financial asset is written down to the present value of estimated future cash flows (excluding future credit losses that have not yet occurred), and the amount of reduction is recognized as impairment loss and is recognized in the profit or loss of this period. The Company carries out the impairment test of significant single financial asset separately, carries out the impairment test on insignificant single financial asset from a single or combination of angles, and carries out the impairment test on single asset without objective evidence of impairment along with the financial assets with similar credit risk characteristics to constitute a combination, but does not carry out the impairment test on the provisionfor impairment of financial assets based on the single in the portfolio. In the subsequent period, if there is objective evidence that the value of financial asset has been restored and recognized relevant to the objective matters occurring after the impairment, previously recognized impairment loss shall be reversed and charged into the profit or loss of this period. But the book value after the reversal should not exceed the amortized cost at the reversal date of the financial assets supposed no provision for impairment. When the financial assets measured at amortized cost actually occur loss, offset against the related provision for impairment.--Available for sale financial assetsIf there is objective evidence that an impairment of available for sale financial assets occurs, even though the financial asset has not been derecognised, the cumulative loss of decrease o f the faire value originally recorded in the owner's equity should be transferred out and charged into the current profit and loss. The cumulative loss is the initial acquisition cost of available for sale financial assets, deducting the fair value of the withdrawing principal and amortization amount and impairment loss as well as net impairment amount originally charged into the profit or loss.Recognition and provision for bad debts of accounts receivableIf there is objective evidence that receivables are impaired at the end of this period,the carrying value will be written down to its present value of estimated future cash flows, and the amount of reduction is recognized as impairment loss and is recognized in the current profit or loss. Present value of estimated future cash flows is determined through future cash flows (excluding credit losses that have not been incurred) discounted at the original effective interest rate, taking into account the value of related collateral (less estimated disposal costs, etc.). Original effective interest rate is the actual interest rate when the receivables are recognized initially. The estimated future cash flows of short-term receivables have small difference from the present value, and the estimated future cash flows are not discounted in determining the related impairment loss.The significant single receivables are separately carried out impairment test at the end of this period, and if there is objective evidence that the impairment has occurred, based on the difference of the present value of future cash flows less than the book value, the impairment loss is recognized and the provision of bad debts is done. The significant single amount refers to top five receivable balances or the sum ofpayments accounting for more than 10% of receivable balances.If there is objective evidence that the individual non-significant receivables impairment has occurred, separate impairment test is done, the impairment loss is recognized and the provision for bad debts is done; other individual non-significant receivables and receivables not impaired after separate test are together divided into several combinations for impairment testing with aging as the similar credit risk characteristics, to determine the impairment loss and do provision for bad debts.In addition to separate provision for impairment of receivables, the company is based on the actual loss rate of receivable portfolio with the same or similar to the previous year and aging as the similar credit risk characteristics, and combines the current situation to determine the ratio of provision for bad debts as follows:Aging Ratio of provisionWithin one year 5%1 –2 years 20%2 –3 years 50%Over 3 years 80%Fixed assets and depreciation accounting methodRecognition criteria of fixed assets: fixed assets refer to tangible assets held for the purpose of producing commodities, providing services, renting or business management with useful lives exceeding one accounting year and high unit value. Classification of fixed assets: buildings and constructions, machinery equipment, transport equipment and office equipment.Fixed assets pricing and depreciation method: the fixed assets is priced based on actual cost and depreciated in a straight-line method. The estimated useful lives, estimated residual rate and annual depreciation rate of various categories of fixed assets are listed as follows:Category of fixed assets Estimateduseful lives(year)Estimated residualrate (year)Annualdepreciation rate(%)Buildings andconstructions20 10 4.5machinery equipment 10 5 9.5transport equipment 5 5 19office equipment 5 5 19Impairment of fixed assets: the Company checks the fixed assets term by term at the end of the reporting period, and if the market continuing to fall or technological obsolescence, damage, long-term idle and other reasons result in fixed assets recoverable amount lower than its book value, in accordance with the difference provision for impairment of fixed assets, the impairment loss is recognized in fixed assets a nd can not be reversed in a subsequent a ccounting period. The recoverable amount is recognized based on the fair value of the assets deducting the net amount after disposal expenses a nd the present value of cash flows of the estimated future assets. The present value of the future cash flows of the asset is determined in accordance with the resulting estimated future cash flows in the process of continuoususe and final disposal to select its appropriate discount rate and the amount of the discount.Accounting method of construction in progressThe construction in progress is priced on the actual cost, to temporarily transfer to fixed assets when reaching the intended use state in accordance with the project budget and the actual cost of the project, and to adjust the book value of fixed assets according to the actual cost after handling final settlement of accounts. Acquisition, construction or production of assets eligible for capitalization borrowed specifically or the interest on general borrowing costs and auxiliary expenses of specific borrowings occurred can be included in the cost of capital assets and subsequently recognized in the current profit or loss before the acquisition, construction or production of the qualifying asset reaches the intended use state or the sale state.Impairment of construction in progress: the Company conducts a comprehensive inspection of construction in progress at the end of the reporting period; if the construction in process is stopped for long time and will not be constructed in the next three years and the construction in progress brings great uncertainty to the economic benefits of enterprises due to backward performance or techniques and the construction in progress occurs impairment, the balance of recoverable amount of single construction in progress lower than the book value of construction in progressis for impairment provisions of construction in progress. Impairment loss on the construction in progress shall not be reversed in subsequent accounting periods once recognized.The pricing and amortizing of intangible assetsPricing of the intangible assets---The cost of outsourcing intangible assets shall be priced based on the actual expenditure directly attributable to intangible assets for the expected purpose.--- Expenditure on internal research and development projects is charged into the current profit or loss, and expense in the development stage can be recognized as intangible costs if meeting the criteria for capitalization.--- Intangible assets of investment is in accordance with the agreed value of the investment contract or agreement as costs, excluding not fair agreed value of the contract or agreement.--- Intangible assets of the debtor obtained in the non-cash asset cover debt method can be accepted; if the receivable creditor?s right is changed into intangible assets, then record according to the fair value of intangible assets.--- For non-monetary transaction intangible assets, t he fair value and related taxes payable of non-monetary assets should be the accounting cost.Amortization of intangible assets: as for the intangible assets with limited service life, it is amortized by straight-line method when it is available for use within the service period. As for unforeseeable period of intangible assets bringing future economic benefits to the company, it is regarded as intangible assets with uncertain service life, and intangible assets with uncertain service life can not be amortized. The Company?s intangible assets include land use rights, forest land use rights and the production and marketing information management software. The land use rights are amortizedaveragely in accordance with 50 years of service life, forest land use rights are amortized averagely in accordance with 30 years of service life, and the production and marketing information management software are amortized averagely in accordance with 5 years of service life.Expenditures arising from development phase on internal research and development projects can be recognized as intangible assets w hen satisfying all of the following conditions: (1) there is technical feasibility of completing the intangible assets so that they will be available for use or sale; (2) there is intention to complete and use or sell the intangible assets; (3) the method that the intangible assets g enerate economic benefits, including existence of a market for products produced by the intangible assets or for the intangible assets themselves, shall be proved. Or, if to be used internally, the usefulness of the intangible assets shall be proved; (4) adequate technical, financial, and other resources are available to complete the development of intangible assets, and the Company has the ability to use or sell the intangible assets;(5) the expenditures arising from development phase of the intangible assets can be measured reliably.Impairment of intangible assets: the Company conducts a comprehensive inspection on intangible assets a t the end of the reporting period. If the intangible assets h ave been replaced by other new technologies so as to seriously affect its capacity to create economic benefits for the enterprise, the market value of certain intangible assets sharply fall and is not expected to recover in the remaining amortization period, certain intangible asset has exceeded the legal time limit but still has some value in use as well as the intangible asset impairment has occurred, the provision for impairment is done according to the difference between the individual estimated recoverable amount and the book value. Impairment loss on the intangible asset shall not be reversed in subsequent accounting periods once recognized.Accounting method of capitalization of borrowing costsBorrowing costs that are directly attributable to the acquisition, construction or production of qualifying assets for capitalization should be charged into the relevant costs of assets and therefore should be capitalized. Borrowing costs incurred after qualifying assets for capitalization reaches the estimated use state are charged to profit or loss in the current period. Other borrowing costs are recognized as expenses based on the accrual and are charged to profit or loss in the current period.Capitalization of borrowing costs should meet the following conditions: expenditures are being incurred, which comprise disbursements incurred in the form of paymentsof cash, transfer of non-monetary assets o r assumption of interest-bearing debts for the acquisition, construction or production of qualifying assets for capitalization; borrowing costs are being incurred; purchase, construction or manufacturing activities that are necessary to prepare the assets for their intended use or sale are in progress. Capitalization amount of borrowing interest: the borrowing interest incurred from the acquisition, construction or production of assets eligible for capitalization borrowed specifically or generally should be determined the capitalization amount according to the following method before the acquisition, construction or production of a qualifying asset reaching its intended use or sale state:---Where funds are borrowed specifically for purchase, construction or manufacturingof assets eligible for capitalization, costs eligible for capitalization are the actual interest costs incurred in current period less the interest income of unused borrowing funds deposited in the bank or any income earned on the temporary investment of such borrowings.---Where funds allocated for purchase, construction or manufacturing of assets eligible for capitalization are part of a general pool, the eligible capitalization interest amounts are determined by multiplying a capitalization rate of general borrowing bythe weighted average of accumulated capital expenditures over those on specific borrowings. The capitalization rate will be determined based on the weighted average rate of the borrowing costs applicable to the general pool.Suspension for capitalization: Capitalization of borrowing costs should be suspended during periods in which purchase, construction or manufacturing of assets eligible for capitalization is interrupted abnormally with the interruption time exceeding three months continuously. Borrowing costs incurred during the interruption should be charged to profit or loss for the current period, and should continue to be capitalized when purchase, construction or manufacturing of the relevant assets resumes. If the interruption is the necessary procedure to prepare the assets purchased, constructed or manufactured eligible for capitalization for their intended use or sale, the borrowing costs should continue to be capitalized.Recognition criteria and measurement method of estimated liabilities Recognition criteria of estimated liabilities: when the external security, pending litigation or arbitration, product quality assurance, layoffs, loss of contracts, restructuring obligations, fixed asset retirement obligations and other pertinent business meet the following conditions, it can be recognized as the liability: (1) the obligation is a present obligation of the Company; (2)it is probable that settlement of such an obligation will result in the economic benefit to flow out from the Company; (3) the amount of the obligation can be measured reliably.Measurement method of estimated liabilities: The Company?s estimated liabilities shall be initially measured at the best estimates of the necessary expenditures for the fulfillment of the present obligations. To determine the best estimates, the Company shall take into full account the risks, uncertainties, time value of money, and other factors relating to the contingencies. If the time value of money is significant, the best estimates shall be determined after discounting the relevant future cash outflows. If there is a continuous range for the necessary expenses, and probabilities of occurrence of all the outcomes within this range are equal, the best estimate shall be determinedat the average amount within the range. The best estimates shall be determined as follows in other circumstances: (1) if the contingency involves a single item, the best estimate shall be determined at the most likely outcome; (2) if the contingency involves two or more items, the best estimate should be determined according to allthe possible outcomes with their relevant probabilities; (3) when all or part of the expenses necessary f or the settlement of estimated liabilities of the Company are expected to be compensated by a third parties, the compensations should be separately recognized as assets only when it is virtually certain that the compensations will be。

财务报表常用词汇中英文对照

财务报表常用词汇中英文对照财务报表常用词汇中英文对照一、企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流动资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due within one year减:一年内到期委托贷款减值准备Less:Impairment for Entrusted loan receivable due within one year减:短期投资跌价准备Less:Impairment for current investment 短期投资净额Net bal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账准备Less:Bad debt provision for Account receivable应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账准备Less:Bad debt provision for Otherreceivable其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less:Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due within one year 一年内到期的应收融资租赁款Finance lease receivables due within one year 其他流动资产Other current assets 流动资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment委托贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值准备Less:Impairment for long-term equity investment 减:长期债权投资减值准备Less:Impairment for long-term debt investment 减:委托贷款减值准备Less:Provision for entrusted loan receivable长期投资净额Net bal of long-term investment其中:合并价差Include:Goodwill(Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less:Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less:Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值准备Less:Impairment for construction in progress在建工程净额Net bal of construction in progress固定资产清理Fixed assets to be disposed of固定资产合计Total fixed assets无形资产及其他资产Other assets&Intangible assets无形资产Intangible assets减:无形资产减值准备Less:Impairment for intangible assets 无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease–Unguaranteed residual values 融资租赁——应收融资租赁款Finance lease–Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets&intangible assets 递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability&Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advance from customers应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Other payable预提费用Accrued Expense预计负债Provision递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year 其他流动负债Other current liability流动负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants&Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益)Owners’Equity实收资本(或股本)Paid in capital减;已归还投资Less:Capital redemption实收资本(或股本)净额Net bal of Paid in capital 资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include:Statutory reserves 未确认投资损失Unrealised investment losses 未分配利润Retained profits after appropriation 其中:本年利润Include:Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability&Equity三、利润及利润分配表Income statement and profit appropriation 一、主营业务收入Revenue减:主营业务成本Less:Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit(-means loss)加:其他业务收入Add:Other operating income减:其他业务支出Less:Other operating expense减:营业费用Selling&Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列)Profit from operation(-means loss)加:投资收益(亏损以“—”填列)Add:Investment income 补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less:Non-operating expense四、利润总额(亏损总额以“—”填列)Profit before Tax减:所得税Less:Income tax少数股东损益Minority interest加:未确认投资损失Add:Unrealised investment losses五、净利润(净亏损以“—”填列)Net profit(-means loss)加:年初未分配利润Add:Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution(-means loss)减:提取法定盈余公积Less:Appropriation of statutory surplus reserves提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and welfare fund提取储备基金Appropriation of reserve fund提取企业发展基金Appropriation of enterprise expansion fund 利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners'distribution减:应付优先股股利Less:Appropriation of preference share's dividend提取任意盈余公积Appropriation of discretionary surplus reserve应付普通股股利Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses from natural disaster3.会计政策变更增加(或减少)利润总额Increase(decrease)in profit due to changes in accounting policies4.会计估计变更增加(或减少)利润总额Increase(decrease)in profit due to changes in accounting estimates。

会计报表项目中英文对照帖(基本完成)

会计报表项目中英文对照帖(基本完成)Balance sheet(audited) 资产负债表Assets 资产Current assets 流动资产、Cash 货币资金Short—term investment 短期投资Notes receivable 应收票据Dividends receivable 应收股利Interest receivable 应收利息Account receivable 应收帐款Other receivable 其他应收款Advanced to suppliers 预付帐款Subsidies receivable 应收补贴款Inventories 存货Prepaid expenses 待摊费用Long-term investments maturing within one year 一年内到期的长期投资Other current assents 其他流动资产Total current assets 流动资产合计Long-term investments 长期投资Long—term equity investment 长期股权投资Long-term debt investment 长期债权投资Total long—term investment 长期投资合计Fixed assets 固定资产Fixed assets-cost 固定资产原价Less:accumulated depreciation 减:累计折旧Fixed assets net value 固定资产净值Less:impairment of fixed assets 减:固定资产减值准备Fixed asset-book value 固定资产净值Materials for projects 工程物资Construction in progress 在建工程Disposal of fixed assets 固定资产清理Total fixed assets 固定资产合计Intangible assets and other assets 无形资产及其他资产Intangible assets 无形资产Long-term deferred expenses 长期待摊费用Other long-term assets 其他长期资产Total intangible assets and other assets 无形资产及其他资产合计Deferred tax: 递延税项Deferred tax debit 递延税款借项Total assets 资产总计Liabilities and owners' equity 负债及所有者权益Current liabilities : 流动负债Short-term loans 短期借款Notes payable 应付票据Account payable 应付帐款Advance from customers 预收帐款Accrued payroll 应付工资Accrued employee’s welfare expenses应付福利费Dividends payable 应付股利Taxes payable 应交税金Other taxes and expense payable 其他应交款Other payable 其他应付款Accrued expenses 预提费用Provisions 预计负债Long—term liabilities due within one year 一年内到期的长期负债Other current liabilities 其他流动负债Total current liabilities 流动负债合计Long-term liabilities:长期负债Long—term loans 长期借款Bonds payable 应付债券Long-term accounts payable 长期应付款Specific account payable 专项应付款Other long-term liabilities 其他长期负债Total long-term liabilities 长期负债合计Deferred tax:递延税项Deferred tax credits 递延税款贷项Total other liabilities : 负债合计Owner’s equity:所有者权益(股东权益)Paid-in capital 实收资本Less :investment returned 减:已归还投资Pain—in capital-net 实收资本净额Capital surplus 资本公积Surplus from profits 盈余公积Including:statutory public welfare fund 其中:法定公益金Undistributed profit 未分配利润Total owner’s equity所有者权益(股东权益)Total liabilities and owner’s equities负债及所有者权益Total liabilities and owner’s equitie s 负债及所有者权益Income statement (audited) 利润表(已审)Item 项目Sales 产品销售收入Including :export sales 其中:出口产品销售收入Less: sales discounts and allowances 减:销售折扣与折让Net sales 产品销售净额Less:sales tax 减:产品销售税金Cost of sales 产品销售成本Including :cost of export sales 出口产品销售成本Gross profit 产品销售毛利Less : selling expense 减:销售费用General and administrative expense 管理费用Financial expense 财务费用Including :interest expense(less interest income) 其中:利息支出(减利息收入)Exchange loss (less exchange gain) 汇兑损失(减汇兑收益)Income from main operation 产品销售利润Add :income from other operations 加:其他业务利润Operating income 营业利润Add :investment income 加:投资收益Non—operating expense 营业外收入Less:non—operating expense 减:营业外支出Add:adjustment to pripr year's income and expense 加:以前年度损益调整Income before tax 利润总额Less:income tax 减:所得税Net income 净利润Statement of profit apropriation and distribution (audited)利润分配表(已审)Item 项目Net income 净利润Add:undistributed profit at beginning of year 加:年初未分配利润Other transferred in 其他转入Profit available for distribution 可供分配的利润Less:statutory surplus from profits 减:提取法定盈余公积Statutory public welfare fund 提取法定公益金Staff and workers’ bonus and welfare fund职工奖励及福利基金Reserve fund 提取储备基金Enterprise expansion fund 提取企业发展基金Profit capitalized on return of investments 利润归还投资Profit available for distribution to owners 可供投资者分配的利润Less:dividends payable for preferred stock 应付优先股股利V oluntary surplus from profits 提取任意盈余公积Dividends payable for common stock 应付普通股股利Dividends transferred to capital 转作股本的普通股股利Undistributed profit 未分配利润Cash flows statement 现金流量表项目 Item NO。

中英文对照的财务报表(资产负债表,损益表)

中英文对照的财务报表(资产负债表,损益表)中英文对照的财务报表(资产负债表,损益表)1 资产 assets11~ 12 流动资产 current assets111 现金及约当现金 cash and cash equivalents1111 库存现金 cash on hand1112 零用金/周转金 petty cash/revolving funds1113 银行存款 cash in banks1116 在途现金 cash in transit1117 约当现金 cash equivalents1118 其它现金及约当现金 other cash and cash equivalents 112 短期投资 short-term investment1121 短期投资 -股票 short-term investments - stock1122 短期投资 -短期票券 short-term investments - short-term notes and bills1123 短期投资-政府债券short-term investments - government bonds1124 短期投资 -受益凭证 short-term investments - beneficiary certificates1125 短期投资-公司债short-term investments - corporate bonds1128 短期投资 -其它 short-term investments - other1129 备抵短期投资跌价损失 allowance for reduction of short-term investment to market113 应收票据 notes receivable1131 应收票据 notes receivable1132 应收票据贴现 discounted notes receivable1137 应收票据 -关系人 notes receivable - related parties1138 其它应收票据 other notes receivable1139 备抵呆帐-应收票据allowance for uncollec- tible accounts- notes receivable114 应收帐款 accounts receivable1141 应收帐款 accounts receivable1142 应收分期帐款 installment accounts receivable1147 应收帐款 -关系人 accounts receivable - related parties 1149 备抵呆帐-应收帐款allowance for uncollec- tible accounts - accounts receivable118 其它应收款 other receivables1181 应收出售远汇款 forward exchange contract receivable 1182 应收远汇款 -外币 forward exchange contract receivable - foreign currencies1183 买卖远汇折价 discount on forward ex-change contract 1184 应收收益 earned revenue receivable1185 应收退税款 income tax refund receivable1187 其它应收款 - 关系人 other receivables - related parties 1188 其它应收款 - 其它 other receivables - other1189 备抵呆帐- 其它应收款allowance for uncollec- tible accounts - other receivables121~122 存货 inventories1211 商品存货 merchandise inventory1212 寄销商品 consigned goods1213 在途商品 goods in transit1219 备抵存货跌价损失 allowance for reduction of inventory to market1221 制成品 finished goods1222 寄销制成品 consigned finished goods1223 副产品 by-products1224 在制品 work in process1225 委外加工 work in process - outsourced1226 原料 raw materials1227 物料 supplies1228 在途原物料 materials and supplies in transit1229 备抵存货跌价损失 allowance for reduction of inventory to market125 预付费用 prepaid expenses1251 预付薪资 prepaid payroll1252 预付租金 prepaid rents1253 预付保险费 prepaid insurance1254 用品盘存 office supplies1255 预付所得税 prepaid income tax1258 其它预付费用 other prepaid expenses126 预付款项 prepayments1261 预付货款 prepayment for purchases1268 其它预付款项 other prepayments128~129 其它流动资产 other current assets1281 进项税额 VAT paid ( or input tax)1282 留抵税额 excess VAT paid (or overpaid VAT)1283 暂付款 temporary payments1284 代付款 payment on behalf of others1285 员工借支 advances to employees1286 存出保证金 refundable deposits1287 受限制存款 certificate of deposit-restricted1291 递延所得税资产 deferred income tax assets1292 递延兑换损失 deferred foreign exchange losses1293 业主(股东)往来 owners(stockholders) current account 1294 同业往来 current account with others1298 其它流动资产-其它 other current assets - other13 基金及长期投资 funds and long-term investments131 基金 funds1311 偿债基金 redemption fund (or sinking fund)1312 改良及扩充基金 fund for improvement and expansion 1313 意外损失准备基金 contingency fund1314 退休基金 pension fund1318 其它基金 other funds132 长期投资 long-term investments1321 长期股权投资 long-term equity investments1322 长期债券投资 long-term bond investments1323 长期不动产投资 long-term real estate in-vestments1324 人寿保险现金解约价值cash surrender value of life insurance1328 其它长期投资 other long-term investments1329 备抵长期投资跌价损失 allowance for excess of cost over market value of long-term investments14~ 15 固定资产 property , plant, and equipment141 土地 land1411 土地 land1418 土地-重估增值 land - revaluation increments142 土地改良物 land improvements1421 土地改良物 land improvements1428 土地改良物 -重估增值 land improvements - revaluation increments1429 累积折旧 -土地改良物 accumulated depreciation - land improvements143 房屋及建物 buildings1431 房屋及建物 buildings1438 房屋及建物 -重估增值 buildings -revaluation increments 1439 累积折旧-房屋及建物accumulated depreciation - buildings144~146 机(器)具及设备 machinery and equipment1441 机(器)具 machinery1448 机(器)具 -重估增值 machinery - revaluation increments 1449 累积折旧-机(器)具accumulated depreciation - machinery151 租赁资产 leased assets1511 租赁资产 leased assets1519 累积折旧 -租赁资产 accumulated depreciation - leased assets152 租赁权益改良 leasehold improvements1521 租赁权益改良 leasehold improvements1529 累积折旧- 租赁权益改良accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments for equipment1561 未完工程 construction in progress1562 预付购置设备款 prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation - miscellaneous property, plant, and equipment16 递耗资产 depletable assets161 递耗资产 depletable assets1611 天然资源 natural resources1618 天然资源-重估增值natural resources -revaluation increments1619 累积折耗-天然资源accumulated depletion - natural resources17 无形资产 intangible assets171 商标权 trademarks1711 商标权 trademarks172 专利权 patents1721 专利权 patents173 特许权 franchise1731 特许权 franchise174 著作权 copyright1741 著作权 copyright175 计算机软件 computer software1751 计算机软件 computer software cost176 商誉 goodwill1761 商誉 goodwill177 开办费 organization costs1771 开办费 organization costs178 其它无形资产 other intangibles1781 递延退休金成本 deferred pension costs1782 租赁权益改良 leasehold improvements1788 其它无形资产-其它 other intangible assets - other18 其它资产 other assets181 递延资产 deferred assets1811 债券发行成本 deferred bond issuance costs1812 长期预付租金 long-term prepaid rent1813 长期预付保险费 long-term prepaid insurance1814 递延所得税资产 deferred income tax assets1815 预付退休金 prepaid pension cost1818 其它递延资产 other deferred assets182 闲置资产 idle assets1821 闲置资产 idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables1841 长期应收票据 long-term notes receivable1842 长期应收帐款 long-term accounts receivable1843 催收帐款 overdue receivables1847 长期应收票据及款项与催收帐款-关系人 long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项 other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产 assets leased to others1851 出租资产 assets leased to others1858 出租资产 -重估增值 assets leased to others - incremental value from revaluation1859 累积折旧-出租资产accumulated depreciation - assets leased to others186 存出保证金 refundable deposit1861 存出保证金 refundable deposits188 杂项资产 miscellaneous assets1881 受限制存款 certificate of deposit - restricted1888 杂项资产 -其它 miscellaneous assets - other2 负债 liabilities21~ 22 流动负债 current liabilities211 短期借款 short-term borrowings(debt)2111 银行透支 bank overdraft2112 银行借款 bank loan2114 短期借款 -业主 short-term borrowings - owners2115 短期借款 -员工 short-term borrowings - employees2117 短期借款 -关系人 short-term borrowings- related parties 2118 短期借款 -其它 short-term borrowings - other212 应付短期票券 short-term notes and bills payable2121 应付商业本票 commercial paper payable2122 银行承兑汇票 bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价 discount on short-term notes and bills payable213 应付票据 notes payable2131 应付票据 notes payable2137 应付票据 -关系人 notes payable - related parties2138 其它应付票据 other notes payable214 应付帐款 accounts pay able2141 应付帐款 accounts payable2147 应付帐款 -关系人 accounts payable - related parties216 应付所得税 income taxes payable2161 应付所得税 income tax payable217 应付费用 accrued expenses2171 应付薪工 accrued payroll2172 应付租金 accrued rent payable2173 应付利息 accrued interest payable2174 应付营业税 accrued VAT payable2175 应付税捐 -其它 accrued taxes payable- other2178 其它应付费用 other accrued expenses payable218~219 其它应付款 other payables2181 应付购入远汇款 forward exchange contract payable2182 应付远汇款 -外币 forward exchange contract payable - foreign currencies2183 买卖远汇溢价 premium on forward exchange contract 2184 应付土地房屋款payables on land and building purchased2185 应付设备款 Payables on equipment2187 其它应付款 -关系人 other payables - related parties2191 应付股利 dividend payable2192 应付红利 bonus payable2193 应付董监事酬劳 compensation payable to directors and supervisors2198 其它应付款 -其它 other payables - other226 预收款项advance receipts2261 预收货款 sales revenue received in advance2262 预收收入 revenue received in advance2268 其它预收款 other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债 corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债 other current liabilities2281 销项税额 VAT received(or output tax)2283 暂收款 temporary receipts2284 代收款 receipts under custody2285 估计售后服务/保固负债 estimated warranty liabilities2291 递延所得税负债 deferred income tax liabilities2292 递延兑换利益 deferred foreign exchange gain2293 业主(股东)往来 owners current account2294 同业往来 current account with others2298 其它流动负债-其它 other current liabilities - others23 长期负债 long-term liabilities231 应付公司债 corporate bonds payable2311 应付公司债 corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款 long-term loans payable2321 长期银行借款 long-term loans payable - bank2324 长期借款 -业主 long-term loans payable - owners2325 长期借款 -员工 long-term loans payable - employees 2327 长期借款-关系人long-term loans payable - related parties2328 长期借款 -其它 long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据 long-term notes payable2332 长期应付帐款 long-term accounts pay-able2333 长期应付租赁负债 long-term capital lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties2338 其它长期应付款项 other long-term payables234 估计应付土地增值税accrued liabilities for land value increment tax2341 估计应付土地增值税estimated accrued land value incremental tax pay-able235 应计退休金负债 accrued pension liabilities2351 应计退休金负债 accrued pension liabilities238 其它长期负债 other long-term liabilities2388 其它长期负债-其它 other long-term liabilities - other28 其它负债 other liabilities281 递延负债 deferred liabilities2811 递延收入 deferred revenue2814 递延所得税负债 deferred income tax liabilities2818 其它递延负债 other deferred liabilities286 存入保证金 deposits received2861 存入保证金 guarantee deposit received288 杂项负债 miscellaneous liabilities2888 杂项负债-其它miscellaneous liabilities - other/Article/english/englishacc/200509/1556.html参考资料:/vbb/attachment.php?attachmentid=1629回答者:你心里只有我 - 举人四级 3-8 17:26评价已经被关闭目前有 1 个人评价好0% (0)不好100% (1)其他回答共 7 条资产负债表 Balance Sheet资产 ASSETS流动资产: Current asset货币资金 Cash(currency fund)Bank短期投资 Short-term investment应收票据 Notes receivable应收股利 Dividends receivable应收利息 Interests receivable应收账款 Accounts receivable其他应收款 Other receivable预付账款 Advances to suppliers应收补贴款 Subsidies receivable存货 Inventories待摊费用 Prepaid expenses一年内到期的长期债券投资Long-term investments maturing within one year其他流动资产 Other current assets流动资产合计 Total current assets长期投资: LONG TERM INVESTMENTS长期股权投资 Long-term equity investment长期债权投资 Long-term debt investment长期投资合计 Total long term investment固定资产: FIXED ASSETS:固定资产原值 Fixed assets-cost减:累计折旧 Less:Accumulated depreciation固定资产净值 Fixed assets-net value减:固定资产减值准备 Less: Impairment of fixed assets固定资产净额 Fixed assets-book value工程物资 Materials for projects在建工程 Construction in progress固定资产清理 Disposal of fixed assets固定资产合计 Total Fixed Assets无形资产及其它资产 INTANGIBLE ASSETS AND OTHER ASSETS: 无形资产 Intangible assets长期待摊费用 Long-term deferred expenses其他长期资产 Other long-term assets无形资产及其他资产合计Total intangible assets and other assets递延税项 Deferred tax递延税款借项 Deferred tax debit资产总计 TOTAL ASSETS负债及所有者权益(或股东权益)LIABILITIES AND OWNER`S EQUITY流动负债: CURRENT LIABILITIES短期借款 Short-term loans应付票据 Notes payable应付账款 Accounts payable预收账款 Advances from customers应付工资 Accrued payroll应付福利费Accrued Employee’s welfare expenses应付股利 Dividends payable未交税金 Taxes payable其他应交款 Other taxes and expenses payable其他应付款 Other payables预提费用 Accrued expenses预提负债 Provisions一年内到期的长期负债Long-term liabilities due within one year其他流动负债 Other current liabilities流动负债合计 Total current liabilities长期负债: LONG-TERM LIABILITIES:长期借款 Long-term loans应付债券 Bonds payable长期应付款 Long-term accounts payable专项应付款 Specific accounts payable其他长期负债 Other long-term liabilities长期负债合计 Total long-term liabilities递延税项: Deferred tax递延税款贷项 Deferred tax credit负债合计 Total other liabilities所有者权益:(或股东权益) OWNER`S EQUITY实收资本(或股本) Paid-in capital减:已归还投资 Less:Investments returned实收资本(或股本)净额 Paid-in capital-net资本公积 Capital surplus盈余公积 Surplus from profits其中:法定公益金 Including:statutory public welfare fund 未分配利润 Undistributed profit所有者权益(或股东权益)合计 T otal owner`s equity负债及所有者权益(或股东权益)合计 TOTAL LIABILITIES AND OWNER`S EQUITY损益表 Profit and Loss Statement项目 ITEMS一、营业收入 Income from main减:营业成本 Less:Cost of main operation营业税金及附加 Tax and additional expense二、经营利润 Income from main operation加:其他业务利润 Add:Income from other operation减:营业费用 Less:Operating expense管理费用 General and administrative expense财务费用 Financial expense三、营业利润 Operating Income加:投资收益 Add:Investment income补贴收入 Income from subsidies营业外收入 Non-operating income减:营业外支出 Less:Non-operating expense四、利润总额 Income before tax减:所得税 Less:Income tax五、净利润 NET INCOME回答者:sxtdc - 助理三级 3-8 13:57从下面的链接下载吧.如果不行,请给我发EMAIL:***************参考资料:/vbb/attachment.php?attachmentid=1629回答者:laneyre - 试用期一级 3-8 15:10这位朋友,我的QQ是82584953,你可以告诉我你的传真号,我传真给你.或者你可以找你们的国税征管员拿,他那肯定有的.回答者:shyupan - 助理二级 3-8 16:57资产负债表 Balance Sheet资产 ASSETS流动资产: Current asset货币资金 Cash(currency fund)Bank短期投资 Short-term investment应收票据 Notes receivable应收股利 Dividends receivable应收利息 Interests receivable应收账款 Accounts receivable其他应收款 Other receivable预付账款 Advances to suppliers应收补贴款 Subsidies receivable存货 Inventories待摊费用 Prepaid expenses一年内到期的长期债券投资Long-term investments maturing within one year其他流动资产 Other current assets流动资产合计 Total current assets长期投资: LONG TERM INVESTMENTS长期股权投资 Long-term equity investment长期债权投资 Long-term debt investment长期投资合计 Total long term investment固定资产: FIXED ASSETS:固定资产原值 Fixed assets-cost减:累计折旧 Less:Accumulated depreciation固定资产净值 Fixed assets-net value减:固定资产减值准备 Less: Impairment of fixed assets固定资产净额 Fixed assets-book value工程物资 Materials for projects在建工程 Construction in progress固定资产清理 Disposal of fixed assets固定资产合计 Total Fixed Assets无形资产及其它资产 INTANGIBLE ASSETS AND OTHER ASSETS: 无形资产 Intangible assets长期待摊费用 Long-term deferred expenses其他长期资产 Other long-term assets无形资产及其他资产合计Total intangible assets and other assets递延税项 Deferred tax递延税款借项 Deferred tax debit资产总计 TOTAL ASSETS负债及所有者权益(或股东权益)LIABILITIES AND OWNER`S EQUITY流动负债: CURRENT LIABILITIES短期借款 Short-term loans应付票据 Notes payable应付账款 Accounts payable预收账款 Advances from customers应付工资 Accrued payroll应付福利费Accrued Employee’s welfare expenses应付股利 Dividends payable未交税金 Taxes payable其他应交款 Other taxes and expenses payable其他应付款 Other payables预提费用 Accrued expenses预提负债 Provisions一年内到期的长期负债Long-term liabilities due within one year其他流动负债 Other current liabilities流动负债合计 Total current liabilities长期负债: LONG-TERM LIABILITIES:长期借款 Long-term loans应付债券 Bonds payable长期应付款 Long-term accounts payable专项应付款 Specific accounts payable其他长期负债 Other long-term liabilities长期负债合计 Total long-term liabilities递延税项: Deferred tax递延税款贷项 Deferred tax credit负债合计 Total other liabilities所有者权益:(或股东权益) OWNER`S EQUITY实收资本(或股本) Paid-in capital减:已归还投资 Less:Investments returned实收资本(或股本)净额 Paid-in capital-net资本公积 Capital surplus盈余公积 Surplus from profits其中:法定公益金 Including:statutory public welfare fund 未分配利润 Undistributed profit所有者权益(或股东权益)合计 T otal owner`s equity负债及所有者权益(或股东权益)合计 TOTAL LIABILITIES AND OWNER`S EQUITY损益表 Profit and Loss Statement项目 ITEMS一、营业收入 Income from main减:营业成本 Less:Cost of main operation营业税金及附加 Tax and additional expense二、经营利润 Income from main operation加:其他业务利润 Add:Income from other operation减:营业费用 Less:Operating expense管理费用 General and administrative expense财务费用 Financial expense三、营业利润 Operating Income加:投资收益 Add:Investment income补贴收入 Income from subsidies营业外收入 Non-operating income减:营业外支出 Less:Non-operating expense四、利润总额 Income before tax减:所得税 Less:Income tax五、净利润 NET INCOME回答者:sxtdc - 助理三级 3-8 13:57--------------------------------------------------------------------------------1 资产 assets11~ 12 流动资产 current assets111 现金及约当现金 cash and cash equivalents1111 库存现金 cash on hand1112 零用金/周转金 petty cash/revolving funds1113 银行存款 cash in banks1116 在途现金 cash in transit1117 约当现金 cash equivalents1118 其它现金及约当现金 other cash and cash equivalents 112 短期投资 short-term investment1121 短期投资 -股票 short-term investments - stock1122 短期投资 -短期票券 short-term investments - short-term notes and bills1123 短期投资-政府债券short-term investments - government bonds1124 短期投资 -受益凭证 short-term investments - beneficiary certificates1125 短期投资-公司债short-term investments - corporate bonds1128 短期投资 -其它 short-term investments - other1129 备抵短期投资跌价损失 allowance for reduction of short-term investment to market113 应收票据 notes receivable1131 应收票据 notes receivable1132 应收票据贴现 discounted notes receivable1137 应收票据 -关系人 notes receivable - related parties1138 其它应收票据 other notes receivable1139 备抵呆帐-应收票据allowance for uncollec- tible accounts- notes receivable114 应收帐款 accounts receivable1141 应收帐款 accounts receivable1142 应收分期帐款 installment accounts receivable1147 应收帐款 -关系人 accounts receivable - related parties 1149 备抵呆帐-应收帐款allowance for uncollec- tible accounts - accounts receivable118 其它应收款 other receivables1181 应收出售远汇款 forward exchange contract receivable 1182 应收远汇款 -外币 forward exchange contract receivable - foreign currencies1183 买卖远汇折价 discount on forward ex-change contract 1184 应收收益 earned revenue receivable1185 应收退税款 income tax refund receivable1187 其它应收款 - 关系人 other receivables - related parties 1188 其它应收款 - 其它 other receivables - other1189 备抵呆帐- 其它应收款allowance for uncollec- tible accounts - other receivables121~122 存货 inventories1211 商品存货 merchandise inventory1212 寄销商品 consigned goods1213 在途商品 goods in transit1219 备抵存货跌价损失 allowance for reduction of inventory to market1221 制成品 finished goods1222 寄销制成品 consigned finished goods1223 副产品 by-products1224 在制品 work in process1225 委外加工 work in process - outsourced1226 原料 raw materials1227 物料 supplies1228 在途原物料 materials and supplies in transit1229 备抵存货跌价损失 allowance for reduction of inventory to market125 预付费用 prepaid expenses1251 预付薪资 prepaid payroll1252 预付租金 prepaid rents1253 预付保险费 prepaid insurance1254 用品盘存 office supplies1255 预付所得税 prepaid income tax1258 其它预付费用 other prepaid expenses126 预付款项 prepayments1261 预付货款 prepayment for purchases1268 其它预付款项 other prepayments128~129 其它流动资产 other current assets1281 进项税额 VAT paid ( or input tax)1282 留抵税额 excess VAT paid (or overpaid VAT)1283 暂付款 temporary payments1284 代付款 payment on behalf of others1285 员工借支 advances to employees1286 存出保证金 refundable deposits1287 受限制存款 certificate of deposit-restricted1291 递延所得税资产 deferred income tax assets1292 递延兑换损失 deferred foreign exchange losses1293 业主(股东)往来 owners(stockholders) current account 1294 同业往来 current account with others1298 其它流动资产-其它 other current assets - other13 基金及长期投资 funds and long-term investments131 基金 funds1311 偿债基金 redemption fund (or sinking fund)1312 改良及扩充基金 fund for improvement and expansion 1313 意外损失准备基金 contingency fund1314 退休基金 pension fund1318 其它基金 other funds132 长期投资 long-term investments1321 长期股权投资 long-term equity investments1322 长期债券投资 long-term bond investments1323 长期不动产投资 long-term real estate in-vestments1324 人寿保险现金解约价值cash surrender value of life insurance1328 其它长期投资 other long-term investments1329 备抵长期投资跌价损失 allowance for excess of cost over market value of long-term investments14~ 15 固定资产 property , plant, and equipment141 土地 land1411 土地 land1418 土地-重估增值 land - revaluation increments142 土地改良物 land improvements1421 土地改良物 land improvements1428 土地改良物 -重估增值 land improvements - revaluation increments1429 累积折旧 -土地改良物 accumulated depreciation - land improvements143 房屋及建物 buildings1431 房屋及建物 buildings1438 房屋及建物 -重估增值 buildings -revaluation increments 1439 累积折旧-房屋及建物accumulated depreciation -buildings144~146 机(器)具及设备 machinery and equipment1441 机(器)具 machinery1448 机(器)具 -重估增值 machinery - revaluation increments 1449 累积折旧-机(器)具accumulated depreciation - machinery151 租赁资产 leased assets1511 租赁资产 leased assets1519 累积折旧 -租赁资产 accumulated depreciation - leased assets152 租赁权益改良 leasehold improvements1521 租赁权益改良 leasehold improvements1529 累积折旧- 租赁权益改良accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments for equipment1561 未完工程 construction in progress1562 预付购置设备款 prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation - miscellaneous property, plant, and equipment16 递耗资产 depletable assets161 递耗资产 depletable assets1611 天然资源 natural resources1618 天然资源-重估增值natural resources -revaluationincrements1619 累积折耗-天然资源accumulated depletion - natural resources17 无形资产 intangible assets171 商标权 trademarks1711 商标权 trademarks172 专利权 patents1721 专利权 patents173 特许权 franchise1731 特许权 franchise174 著作权 copyright1741 著作权 copyright175 计算机软件 computer software1751 计算机软件 computer software cost176 商誉 goodwill1761 商誉 goodwill177 开办费 organization costs1771 开办费 organization costs178 其它无形资产 other intangibles1781 递延退休金成本 deferred pension costs1782 租赁权益改良 leasehold improvements1788 其它无形资产-其它 other intangible assets - other18 其它资产 other assets181 递延资产 deferred assets1811 债券发行成本 deferred bond issuance costs1812 长期预付租金 long-term prepaid rent1813 长期预付保险费 long-term prepaid insurance1814 递延所得税资产 deferred income tax assets1815 预付退休金 prepaid pension cost1818 其它递延资产 other deferred assets182 闲置资产 idle assets1821 闲置资产 idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables1841 长期应收票据 long-term notes receivable1842 长期应收帐款 long-term accounts receivable1843 催收帐款 overdue receivables1847 长期应收票据及款项与催收帐款-关系人 long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项 other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产 assets leased to others1851 出租资产 assets leased to others1858 出租资产 -重估增值 assets leased to others - incremental value from revaluation1859 累积折旧-出租资产accumulated depreciation - assets leased to others186 存出保证金 refundable deposit1861 存出保证金 refundable deposits188 杂项资产 miscellaneous assets1881 受限制存款 certificate of deposit - restricted1888 杂项资产 -其它 miscellaneous assets - other2 负债 liabilities21~ 22 流动负债 current liabilities211 短期借款 short-term borrowings(debt)2111 银行透支 bank overdraft2112 银行借款 bank loan2114 短期借款 -业主 short-term borrowings - owners2115 短期借款 -员工 short-term borrowings - employees2117 短期借款 -关系人 short-term borrowings- related parties 2118 短期借款 -其它 short-term borrowings - other212 应付短期票券 short-term notes and bills payable2121 应付商业本票 commercial paper payable2122 银行承兑汇票 bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价 discount on short-term notes and bills payable213 应付票据 notes payable2131 应付票据 notes payable2137 应付票据 -关系人 notes payable - related parties2138 其它应付票据 other notes payable214 应付帐款 accounts pay able2141 应付帐款 accounts payable2147 应付帐款 -关系人 accounts payable - related parties216 应付所得税 income taxes payable2161 应付所得税 income tax payable217 应付费用 accrued expenses2171 应付薪工 accrued payroll2172 应付租金 accrued rent payable2173 应付利息 accrued interest payable2174 应付营业税 accrued VAT payable2175 应付税捐 -其它 accrued taxes payable- other2178 其它应付费用 other accrued expenses payable218~219 其它应付款 other payables2181 应付购入远汇款 forward exchange contract payable2182 应付远汇款 -外币 forward exchange contract payable - foreign currencies2183 买卖远汇溢价 premium on forward exchange contract 2184 应付土地房屋款payables on land and building purchased2185 应付设备款 Payables on equipment2187 其它应付款 -关系人 other payables - related parties2191 应付股利 dividend payable2192 应付红利 bonus payable2193 应付董监事酬劳 compensation payable to directors and supervisors2198 其它应付款 -其它 other payables - other226 预收款项advance receipts2261 预收货款 sales revenue received in advance2262 预收收入 revenue received in advance2268 其它预收款 other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债 corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-termlia- bilities - current portion228~229 其它流动负债 other current liabilities2281 销项税额 VAT received(or output tax)2283 暂收款 temporary receipts2284 代收款 receipts under custody2285 估计售后服务/保固负债 estimated warranty liabilities2291 递延所得税负债 deferred income tax liabilities2292 递延兑换利益 deferred foreign exchange gain2293 业主(股东)往来 owners current account2294 同业往来 current account with others2298 其它流动负债-其它 other current liabilities - others23 长期负债 long-term liabilities231 应付公司债 corporate bonds payable2311 应付公司债 corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款 long-term loans payable2321 长期银行借款 long-term loans payable - bank2324 长期借款 -业主 long-term loans payable - owners2325 长期借款 -员工 long-term loans payable - employees 2327 长期借款-关系人long-term loans payable - related parties2328 长期借款 -其它 long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据 long-term notes payable2332 长期应付帐款 long-term accounts pay-able2333 长期应付租赁负债 long-term capital lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties。

新会计准则下中英文对照财务报表

1. 出售、处置部门或被投资单位所得收益 2. 自然灾害发生的损失 3. 会计政策变更增加(或减少)利润总额 4. 会计估计变更增加(或减少)利润总额 5. 债务重组损失 6. 其他

ITEMS Income from sale of invst. units Less from natural disaster Profit from changes in policy Profit from accounting budget Less from liablities rebuilt Others 复核: 制表:

利 润 表 (INCOME STATEMENT)

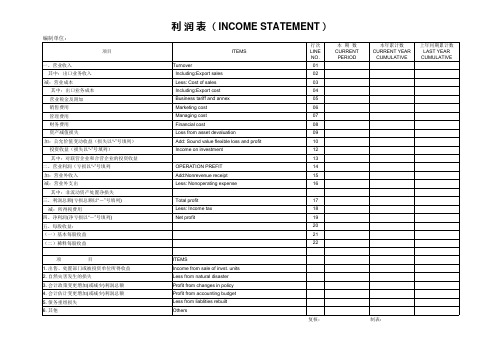

编制单位:

项目 一、营业收入 其中:出口业务收入 减:营业成本 其中:出口业务成本 营业税金及附加 销售费用 管理费用 财务费用 资产减值损失 加:公允价值变动收益(损失以“-”号填列) 投资收益(损失以“-”号填列) 其中:对联营企业和合营企业的投资收益 二、营业利润(亏损以“-”号填列 加:营业外收入 减:营业外支出 其中:非流动资产处置净损失 三、利润总额(亏损总额以“-”号填列) 减:所得税费用 四、净利润(净亏损以“-”号填列) 五、每股收益: (一)基本每股收益 (二)稀释每股收益 项 目 Total profit Less: Income tax Net profit 17 18 19 20 21 22 OPERATION PREFIT Add:Nonrevenue receipt Less: Nonoperating expense Turnover Including:Export sales Less: Cost of sales Including:Export cost Business tariff and annex Marketing cost Managing cost Financial cost Loss from asset devaluation Add: Sound value flexible loss and profit Income on investment ITEMS 行次 LINE NO. 01 02 03 04 05 06 07 08 09 10 12 13 14 15 16 本 期 数 CURRENT PERIOD 本年累计数E 上年同期累计数 LAST YEAR CUMULATIVE

会计报表附注中英文对照

最新会计报表附注中英文对照.简式) 最新会计报表附注中英文对照(字号:1 2008-12-27 14:00:46 阅读2069 评论审计报告中英对照大中小**铸造有限公司会计报表附注2006年度**foundry Co., Ltd.Notes to Financial Statements for the Year Ended December 31, 2006一、公司概况I. Profile of Company**铸造有限公司(以下简称“本公司”),成立于2005年12月14日,为有限责任公司。

经营地址为**玛钢工业园区。

企业法人营业执照注册号为**,注册资本为人民币壹佰万元。

经营范围:铸造、加工、销售;管道连接件、铝合金铸件、塑料制品;机加工、热镀各种铸件;经销各种炉料、生铁、机械设备;运输(国家有限制运输的除外)**foundry Co., Ltd. (hereinafter referred to as “the company”), a limited liability company with the registered capital of1,000,000 RMB, was set up on Dec. 14, 2005. The company islocated at ** industry zone. Its business license No. is **. The company is mainly engaged in foundry, processing, vendition, pipeline connector, Aluminum alloy casting, Plastic products,Machining, Hot plating various castings, selling variousfurnace charge, pig iron and machine equipment, Transport (except the limitative things in state law.) ***]二、重要会计政策和会计估计II. Significant Accounting Policy and Accounting Estimate本会计报表所载财务信息根据下列重要会计政策和会计估计编制,它们是根据国际会计准则拟定的,且对于本公司的实际情况而言,运用国际会计准则与运用中国企业会计制度所编制出的报表并无重大差异。

大会计报表中英文对照

资产负债表 Balance Sheet项目 ITEM货币资金 Cash短期投资 Short term investments应收票据 Notes receivable应收股利 Dividend receivable应收利息 Interest receivable应收帐款 Accounts receivable其他应收款 Other receivables预付帐款 Accounts prepaid期货保证金 Future guarantee应收补贴款 Allowance receivable应收出口退税 Export drawback receivable存货 Inventories其中:原材料 Including:Raw materials产成品(库存商品) Finished goods待摊费用 Prepaid and deferred expenses待处理流动资产净损失 Unsettled G/L on current assets一年内到期的长期债权投资 Long-term debenture investment falling due in a yaear 其他流动资产 Other current assets流动资产合计 Total current assets长期投资: Long-term investment:其中:长期股权投资 Including long term equity investment长期债权投资 Long term securities investment*合并价差 Incorporating price difference长期投资合计 Total long-term investment固定资产原价 Fixed assets-cost减:累计折旧 Less:Accumulated Dpreciation固定资产净值 Fixed assets-net value减:固定资产减值准备 Less:Impairment of fixed assets固定资产净额 Net value of fixed assets固定资产清理 Disposal of fixed assets工程物资 Project material在建工程 Construction in Progress待处理固定资产净损失 Unsettled G/L on fixed assets固定资产合计 Total tangible assets无形资产 Intangible assets其中:土地使用权 Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理 Including:Fixed assets repair固定资产改良支出 Improvement expenditure of fixed assets其他长期资产 Other long term assets其中:特准储备物资 Among it:Specially approved reserving materials无形及其他资产合计 Total intangible assets and other assets递延税款借项 Deferred assets debits资产总计 Total Assets资产负债表(续表) Balance Sheet项目 ITEM短期借款 Short-term loans应付票款 Notes payable应付帐款 Accounts payab1e预收帐款 Advances from customers应付工资 Accrued payro1l应付福利费 Welfare payable应付利润(股利) Profits payab1e应交税金 Taxes payable其他应交款 Other payable to government其他应付款 Other creditors预提费用 Provision for expenses预计负债 Accrued liabilities一年内到期的长期负债 Long term liabilities due within one year 其他流动负债 Other current liabilities流动负债合计 Total current liabilities长期借款 Long-term loans payable应付债券 Bonds payable长期应付款 long-term accounts payable专项应付款 Special accounts payable其他长期负债 Other long-term liabilities其中:特准储备资金 Including:Special reserve fund长期负债合计 Total long term liabilities递延税款贷项 Deferred taxation credit负债合计 Total liabilities* 少数股东权益 Minority interests实收资本(股本) Subscribed Capital国家资本 National capital集体资本 Collective capital法人资本 Legal person"s capital其中:国有法人资本 Including:State-owned legal person"s capital 集体法人资本 Collective legal person"s capital个人资本 Personal capital外商资本 Foreign businessmen"s capital资本公积 Capital surplus盈余公积 surplus reserve其中:法定盈余公积 Including:statutory surplus reserve公益金 public welfare fund补充流动资本 Supplermentary current capital* 未确认的投资损失(以“-”号填列) Unaffirmed investment loss未分配利润 Retained earnings外币报表折算差额 Converted difference in Foreign Currency Statements所有者权益合计 Total shareholder"s equity负债及所有者权益总计 Total Liabilities & Equity利润表 INCOME STATEMENT项目 ITEMS产品销售收入Sales of products其中:出口产品销售收入 Including:Export sales减:销售折扣与折让 Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本 Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利 Gross profit on sales减:销售费用 Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益) Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额 Total profit减:所得税 Less:Income tax净利润 Net profit现金流量表Cash Flows StatementPrepared by: Period: Unit:ItemsFlows from Operating Activities:01)Cash received from sales of goods or rendering of services02)Rental receivedValue added tax on sales received and refunds of value03)added tax paid04)Refund of other taxes and levy other than value added tax07)Other cash received relating to operating activities08)Sub-total of cash inflows09)Cash paid for goods and services10)Cash paid for operating leases11)Cash paid to and on behalf of employees12)Value added tax on purchases paid13)Income tax paid14)Taxes paid other than value added tax and income tax17)Other cash paid relating to operating activities18)Sub-total of cash outflows19)Net cash flows from operating activitiesFlows from Investing Activities:20)Cash received from return of investments21)Cash received from distribution of dividends or profits22)Cash received from bond interest incomeNet cash received from disposal of fixed assets,intangible 23)assets and other long-term assets26)Other cash received relating to investing activities27)Sub-total of cash inflowsCash paid to acquire fixed assets,intangible assets28)and other long-term assets29)Cash paid to acquire equity investments30)Cash paid to acquire debt investments33)Other cash paid relating to investing activities34)Sub-total of cash outflows35)Net cash flows from investing activitiesFlows from Financing Activities:36)Proceeds from issuing shares37)Proceeds from issuing bonds38)Proceeds from borrowings41)Other proceeds relating to financing activities42)Sub-total of cash inflows43)Cash repayments of amounts borrowed44)Cash payments of expenses on any financing activities45)Cash payments for distribution of dividends or profits46)Cash payments of interest expenses47)Cash payments for finance leases48)Cash payments for reduction of registered capital51)Other cash payments relating to financing activities52)Sub-total of cash outflows53)Net cash flows from financing activitiesof Foreign Exchange Rate Changes on CashIncrease in Cash and Cash EquivalentsSupplemental Informationand Financing Activities that do not Involve inCash Receipts and Payments56)Repayment of debts by the transfer of fixed assets57)Repayment of debts by the transfer of investments58)Investments in the form of fixed assets59)Repayments of debts by the transfer of investoriesof Net Profit to Cash Flows from OperatingActivities62)Net profit63)Add provision for bad debt or bad debt written off64)Depreciation of fixed assets65)Amortization of intangible assetsLosses on disposal of fixed assets,intangible assets66)and other long-term assets (or deduct:gains)67)Losses on scrapping of fixed assets68)Financial expenses69)Losses arising from investments (or deduct:gains)70)Defered tax credit (or deduct:debit)71)Decrease in inventories (or deduct:increase)72)Decrease in operating receivables (or deduct:increase)73)Increase in operating payables (or deduct:decrease)74)Net payment on value added tax (or deduct:net receipts75)Net cash flows from operating activitiesIncrease in Cash and Cash Equivalents76)cash at the end of the period77)Less:cash at the beginning of the period78)Plus:cash equivalents at the end of the period79)Less:cash equivalents at the beginning of the period80)Net increase in cash and cash equivalents现金流量表的现金流量声明拟制人:时间:单位:项目流量从经营活动:01 )所收到的现金从销售货物或提供劳务02 )收到的租金增值税销售额收到退款的价值03 )增值税缴纳04 )退回的其他税收和征费以外的增值税07 )其他现金收到有关经营活动08 )分,总现金流入量09 )用现金支付的商品和服务10 )用现金支付经营租赁11 )用现金支付,并代表员工12 )增值税购货支付13 )所得税的缴纳14 )支付的税款以外的增值税和所得税17 )其他现金支付有关的经营活动18 )分,总的现金流出19 )净经营活动的现金流量流向与投资活动:20 )所收到的现金收回投资21 )所收到的现金从分配股利,利润22 )所收到的现金从国债利息收入现金净额收到的处置固定资产,无形资产23 )资产和其他长期资产26 )其他收到的现金与投资活动27 )小计的现金流入量用现金支付购建固定资产,无形资产28 )和其他长期资产29 )用现金支付,以获取股权投资30 )用现金支付收购债权投资33 )其他现金支付的有关投资活动34 )分,总的现金流出35 )的净现金流量,投资活动产生流量筹资活动:36 )的收益,从发行股票37 )的收益,由发行债券38 )的收益,由借款41 )其他收益有关的融资活动42 ),小计的现金流入量43 )的现金偿还债务所支付的44 )现金支付的费用,对任何融资活动45 )支付现金,分配股利或利润46 )以现金支付的利息费用47 )以现金支付,融资租赁48 )以现金支付,减少注册资本51 )其他现金收支有关的融资活动52 )分,总的现金流出53 )的净现金流量从融资活动的外汇汇率变动对现金增加现金和现金等价物补充资料活动和筹资活动,不参与现金收款和付款56 )偿还债务的转让固定资产57 )偿还债务的转移投资58 )投资在形成固定资产59 )偿还债务的转移库存量净利润现金流量从经营活动62 )净利润63 )补充规定的坏帐或不良债务注销64 )固定资产折旧65 )无形资产摊销损失处置固定资产,无形资产66 )和其他长期资产(或减:收益)67 )损失固定资产报废68 )财务费用69 )引起的损失由投资管理(或减:收益)70 ) defered税收抵免(或减:借记卡)71 )减少存货(或减:增加)72 )减少经营性应收(或减:增加)73 )增加的经营应付账款(或减:减少)74 )净支付的增值税(或减:收益净额75 )净经营活动的现金流量增加现金和现金等价物76 )的现金,在此期限结束77 )减:现金期开始78 )加:现金等价物在此期限结束79 )减:现金等价物期开始80 ),净增加现金和现金等价物。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

最新会计报表附注中英文对照(简式)审计报告中英对照2008-12-27 14:00:46 阅读2069 评论1 字号:大中小**铸造有限公司会计报表附注2006年度**foundry Co., Ltd.Notes to Financial Statements for the Year Ended December 31, 2006一、公司概况I. Profile of Company**铸造有限公司(以下简称“本公司”),成立于2005年12月14日,为有限责任公司。

经营地址为**玛钢工业园区。

企业法人营业执照注册号为**,注册资本为人民币壹佰万元。