公众责任险扩展条款(英)

保险附加条款中英文对照

Indemnity to Principal Clause Independent Contractors Liability Clause

赔偿委托人条款 独立承包人责任条款

Landlord’s Furniture, Fixtures & Fittings under Care Custody & Control of Insured Landlord’s Liability Clause Leased Staff Residence Clause

and Retaining Wall Works

Testing Of Machinery and Installations Clause 机器设备试车考核条款

Time Adjustment Clause

时间调整特别条款

Time Schedule Clause Tunnels and Galleries Clause

承包人及分包人连带责任条款 契约责任条款

Cross Liability Defective Sanitary Installation

交叉责任条款 缺陷卫生设施条款

Delivery Risk Clause Displayed Merchandise Extension

运送货物扩展条款 商品展示条款

Defective Sanitation Liability Clause

Unarmoured Seawall Clause

Vibration, Removal or Weakening of Support 震动、移动或减弱支撑扩展条款 Clause

Waiver of Subrogation Clause against Subsidiary or Parent Company

公众责任险树枝折断折断扩展条款

公众责任险树枝折断扩展条款一、引言公众责任险是一种重要的商业保险,它主要针对企业在经营活动中可能对第三方造成的人身伤害或财产损失进行保障。

其中,树枝折断扩展条款是公众责任保险中的一项重要内容,它在特定情况下对树木折断所造成的损失进行保险赔偿。

本文将对公众责任险树枝折断扩展条款进行深入探讨,为您详细解读这一保险条款的意义和适用范围。

二、树枝折断扩展条款的意义树枝折断扩展条款是公众责任险中的一项重要保障内容,其意义主要在于对树木折断所造成的损失进行保险赔偿。

树木因年久失修、天灾等原因可能存在折断损坏的风险,在这种情况下,如果树木在公众场所折断并导致第三方人员受伤或财产损失,公众责任险的树枝折断扩展条款将承担相应的赔偿责任。

这一条款的设立有助于保障企业在经营活动中可能发生的树木折断事故所引发的第三方索赔事件,为企业提供了一定的风险保障。

三、树枝折断扩展条款的适用范围树枝折断扩展条款在公众责任险中的适用范围主要包括以下几个方面:1. 公共场所树木折断:公众责任险的树枝折断扩展条款通常适用于公共场所的树木折断事故。

公共场所的树木折断,可能导致行人、车辆或附近建筑物受到损害,树枝折断扩展条款将对此类情况提供保险赔偿。

2. 公共设施周围树木折断:除了公共场所,树枝折断扩展条款还适用于公共设施周围的树木折断情况。

一棵老树的枝条折断,恰好砸到了公交站亭顶上,导致亭顶损坏,这种情况也可以在树枝折断扩展条款中进行赔偿。

3. 树木折断导致的人身伤害:树木折断可能导致行人受伤或财产损失,公众责任险的树枝折断扩展条款还包括对此类人身伤害和财产损失的保险赔偿。

四、个人观点和理解公众责任险的树枝折断扩展条款在保险领域中起着非常重要的作用。

树木折断事故可能会给第三方带来不可预测的损失,而公众责任险的树枝折断扩展条款则可以有效地对此类损失进行保障和赔偿。

作为企业经营者,选择适用树枝折断扩展条款的公众责任险,不仅能够降低企业可能面临的风险,也能提升企业的公众形象和社会责任感。

公众责任险扩展条款

公众责任险扩展条款1. xx 天保单取消条款本保单可在任何时候由被保险人申请取消,但被保险人必须书面通知本公司,保险费将根据短期费率标准或最低保费予以调整。

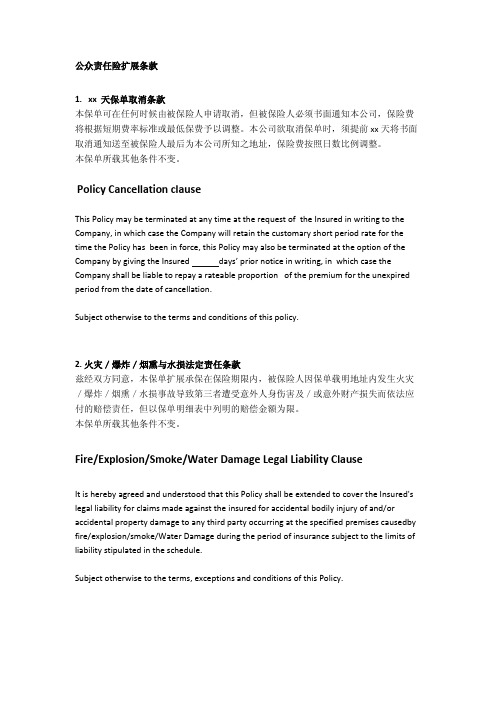

本公司欲取消保单时,须提前xx天将书面取消通知送至被保险人最后为本公司所知之地址,保险费按照日数比例调整。

本保单所载其他条件不变。

Policy Cancellation clauseThis Policy may be terminated at any time at the request of the Insured in writing to the Company, in which case the Company will retain the customary short period rate for the time the Policy has been in force, this Policy may also be terminated at the option of the Company by giving the Insured da ys’ prior notice in writing, in which case the Company shall be liable to repay a rateable proportion of the premium for the unexpired period from the date of cancellation.Subject otherwise to the terms and conditions of this policy.2. 火灾/爆炸/烟熏与水损法定责任条款兹经双方同意,本保单扩展承保在保险期限内,被保险人因保单载明地址内发生火灾/爆炸/烟熏/水损事故导致第三者遭受意外人身伤害及/或意外财产损失而依法应付的赔偿责任,但以保单明细表中列明的赔偿金额为限。

公众责任险 中英文对照

公众责任险中英文对照公众责任险,也被称为公众责任保险,是一种特殊的保险,它涵盖了因公共场所、公共设施或建筑物内的意外事故所导致的法律责任风险。

公众责任险的作用1. 风险转移:公众责任险能够将企业可能面临的法律责任风险转移给保险公司,降低企业的经营压力。

2. 保护企业声誉:在意外事故发生后,保险公司能够为企业在公众中提供积极的形象,有助于维护企业的声誉。

3. 减轻财务压力:如果发生意外事故,公众责任险能够为企业在事故处理、赔偿等方面提供财务支持,减轻企业的财务压力。

对于任何企业来说,公众责任险都是一个重要的保障工具,它能够为企业在面临法律纠纷时提供强大的支持。

适用范围公众责任险适用于各种类型的商业企业,如商场、酒店、餐饮、娱乐场所、学校、医院等。

这些场所可能因为意外事故引发法律纠纷,而公众责任险能够为这些场所提供全面的保障。

对于各种类型的商业企业来说,公众责任险都是一个不可或缺的保障工具。

Public liability insurance, also known as public liability insurance, is a special type of insurance that covers the risk of legal liability arising from accidents in public places,public facilities or buildings.Role of Public Liability Insurance1. Risk transfer: public liability insurance can transfer the risk of legal liability that the enterprise may face to the insurance company and reduce the operating pressure of the enterprise.2. Protection of corporate reputation: After an accident, the insurance company is able to provide a positive image of the company to the public, which helps to maintain the reputation of the company.3. Reduce financial pressure: If an accident occurs, public liability insurance can provide financial support to the enterprise in terms of accident handling, compensation, etc. and reduce the financial pressure of the enterprise.Public liability insurance is an important protection tool for any business, which can provide strong support when facing legal disputes.Scope of ApplicationPublic Liability Insurance is applicable to all types of business enterprises, such as shopping malls, hotels, restaurants, entertainment venues, schools and hospitals. These establishments can be subject to legal disputes due toaccidents and public liability insurance can provide comprehensive coverage for these establishments. Public liability insurance is an indispensable protection tool for all types of commercial enterprises.。

公众责任险附加条款

公众责任险附带条款1、广告招牌及装饰物责任条款兹经两方赞同并商定,本附带险扩展承保被保险人因在本保险单明细表中列明的营业场所范围内或四周地域部署的广告、霓虹灯、装饰物和相像物发买卖外事故造成第三者人身伤亡或财富损失机依照中华人民共和国〔不含香港、澳门、台湾地域〕法律应负的赔偿责任。

被保险人应保证指派合格人员对上述装置按期进行检查和保护。

主险条款与本附带险条款相反抗之处,以本附带险条款为准;本附带险条款未商定事项,以主险条款为准。

每次事故赔偿限额:RMB50万累计赔偿限额:RMB100万2、电梯、机器及自动装置条款〔包含无过失责任〕兹经两方赞同,只管存在相反规定,本保险扩展承保被保险人因有关客货电梯、自动装置、设备及机器设备发买卖外事故致使第三者人身伤亡和财富损失后惹起的经济赔偿责任。

包含被保险方无过失造成第三者不测伤害依法应担当的赔偿责任。

被保险人应保证:(一) 由受权承包商进行按期检查与维修;(二) 除非制造商或发证机构介绍其投入运转,否那么本保险不合用。

本保单所载其余条件不变。

3、装卸责任条款〔含叉车装卸〕兹经两方赞同,本保险扩展承保被保险人因其拥有的车辆〔含叉车、手推车等流动机械设备〕在营业场所内进行与经营有关的装卸过程中发买卖外事故造成第三者人身伤亡或财富损失机应负的赔偿责任。

本保单所载其余条件不变。

4、烟熏责任条款兹经两方赞同,本保险扩展承保因烟熏造成第三者人身伤亡或财富损失机被保险人应负的赔偿责任,但不得超出本保险限期内保险单明细表中列明的责任限额。

本保单所载其余条件不变。

5、火灾、水灾和爆炸责任条款兹经两方赞同,本保险扩展承保因火灾或爆炸。

水灾造成第三者人身伤亡或财富损失机被保险人应负的赔偿责任,但不得超出本保险限期内保险单明细表中列明的责任限额。

本保单所载其余条件不变。

6、自动承保新地址条款兹经两方赞同,本保险的赔偿将自被保险人新置财富建成或获取,或其转移至被保险人名下,或被保险人开始对其负责〔除非有其余保险存在〕时起,自动合用于和〔或〕包含其所引致的被保险人的法律赔偿责任。

公众责任险条款

公众责任险条款公民在公共场所发⽣意外伤害时,该公共场所的拥有者应该对此事负责,这就是公共责任。

那么公共责任险条款⾥包含了保险责任、责任免除、责任限额与免赔额(率)、保险期间、保险费等内容,关于公众责任险条款的更多内容,下⾯由店铺⼩编为你解答。

公众责任险条款⼀、总则第⼀条公众责任保险合同(以下简称本保险合同)由保险条款、投保单、保险单、保险凭证以及批单等组成。

凡涉及本保险合同的约定,均应采⽤书⾯形式。

第⼆条凡依法设⽴的企事业单位、社会团体、个体⼯商户、其他经济组织及⾃然⼈,均可作为本保险合同的被保险⼈。

⼆、保险责任第三条在保险期间内,被保险⼈在本保险合同载明的场所内依法从事⽣产、经营等业务时,因该场所内发⽣的意外事故造成第三者⼈⾝伤亡或财产损失,依照中华⼈民共和国法律(不包括港澳台地区法律)应由被保险⼈承担的经济赔偿责任,保险⼈按照本保险合同约定负责赔偿。

第四条被保险⼈的下列费⽤,保险⼈按照本保险合同约定也负责赔偿:(⼀)发⽣保险责任事故后,被保险⼈因保险事故⽽被提起仲裁或者诉讼的,对应由被保险⼈⽀付的仲裁或者诉讼费⽤以及事先经保险⼈书⾯同意⽀付的其他必要的、合理的费⽤(以下简称“法律费⽤”);(⼆)发⽣保险责任事故后,被保险⼈为缩⼩或减少对第三者⼈⾝伤亡或财产损失的赔偿责任所⽀付的必要的、合理的费⽤(以下简称“施救费⽤”)。

三、责任免除第五条下列原因造成的损失、费⽤和责任,保险⼈不负责赔偿:(⼀)投保⼈、被保险⼈及其代表的重⼤过失或故意⾏为;(⼆)战争、敌对⾏动、军事⾏为、武装冲突、罢⼯、骚乱、暴动、恐怖活动、盗窃、抢劫;(三)⾏政⾏为或司法⾏为;(四)核辐射、核爆炸、核污染及其他放射性污染;(五)地震及其次⽣灾害、海啸及其次⽣灾害、雷击、暴⾬、洪⽔、⽕⼭爆发、地下⽕、龙卷风、台风、暴风等⾃然灾害;(六)烟熏、⼤⽓污染、⼟地污染、⽔污染及其他各种污染;(七)锅炉爆炸、空中运⾏物体坠落。

第六条出现下列任⼀情形时,保险⼈不负责赔偿:(⼀)被保险⼈因在本保险合同载明的场所范围内所拥有、使⽤或经营的游泳池发⽣意外事故造成的第三者⼈⾝伤亡或财产损失;(⼆)被保险⼈因在本保险合同载明的固定场所内布置的⼴告、霓虹灯、灯饰物发⽣意外事故造成的第三者⼈⾝伤亡或财产损失;(三)被保险⼈因在本保险合同载明的场所范围内所拥有、使⽤或经营的停车场发⽣意外事故造成的第三者⼈⾝伤亡或财产损失;(四)被保险⼈因出租房屋或建筑物发⽣⽕灾造成第三者⼈⾝伤亡或财产损失的赔偿责任;(五)使⽤未经有关监督管理部门验收或经验收不合格的固定场所或设备。

公众责任险特约条款(英文)

01Cross Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this insurance shall apply to each insured party as if a separate policy had been issued to each party.Provided always that the aggregate liability of the Company for any one accident shall not exceed the limit of indemnity stipulated in the schedule.This clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional premium:02Contractual Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium,the Company shall indemnify the Insured against any claim made in respect of liability assumed by the Insured under any contract or agreement for bodily injury of and/or property damage to any third party subject to the limit of liability stipulated in this policy provided that such contract or agreement has been declared to and approved by the Company.This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:03Strike,Riot,Civil Commotion orMalicious Damage Extension ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the insurer's liability for accidental bodily injury of and/or accidental property damage to any third party occurring at the specified premises directly caused by strike, riot,civil commotion or malicious damage.This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:04Act of Terrorism Extension ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claim made against the Insured for the bodily injury of and/or property damage to any third party at the specified premises directly caused by any terrorist or terrorism organization.This clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:05Elevator and Escalator ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidental bodily injury of and/or accidental property damage to any third party in the normal operational use of the elevators or escalators at the premises specified in the Policy subject to the limit of liability stipulated in this Policy.It is warranted that the Insured shall see to it that regular inspection and maintenance of the elevators and escalators shall be carried out by qualified engineers.The amount of indemnity shall not exceed the following limit of liability.Limit of Indemnity(a.o.a.):Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:06Explosion of Boilers clauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for accidental bodily injury of and/or accidental property damage to any third party occurring at the specified premises resulting from boiler explosion due to its internal steam pressure subject to the limits of liability stipulated in this policy that the Insured has complied with all operating regulations laid down specifically for such boiler.It is warranted that the Insured shall see to it that regular inspection and maintenance of the boiler shall be carried out by qualified engineers.This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:07Fire&/or Explosion legal liability clauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this policy shall be extended to cover the Insured’s liability for claims made against the insured for accidents bodily injury of and/or accidental property damage to any third party occurring at the specified premises caused by fire or explosion subject to the following limits of liability during the period of insurance.Limit of Indemnity(a.o.a.):Aggregate Limit of Indemnity:This clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:08Food and Drinks Poisoning ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidental bodily injury of and/or accidental property damage to any third party which occurs during the period of insurance and arises out of poisoning by or foreign or deleterious matter in food or drink consumed in or about the premises specified in the Policy provided always that the Insured shall at all times take every possible precaution to prevent the sale or supply of any condition or free from contamination or for human consumption subject to the following limits of liability during the period of insurance.Limit of Indemnity(a.o.a.):Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:09Goods and Services ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured foraccidental bodily injury or accidental property damage which occurs during the period of insurance and arises out of goods and/or services sold or supplied including transportation provided by the Insured in the normal course of the business as hold proprietor,subject to the following limits of liability during the period of insurance:Limit of Indemnity(a.o.a.):Aggregate Limit of Indemnity:This clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:10Guest's Property ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for loss of or damage to the property belonging to guests or customers of the Insured whilst such property is under the custody or control of the Insured subject to a limit of Liability of_______any one guest,with the exception of losses of guests'property from safe deposit boxes contained at the premises where the maximum liability of any one guest is agreed to be_____.For the purpose of this extension the guests' property shall include clothing of such guests'sent for laundry,dry cleaning or pressing at the premises, subject always to the following limits during the period of insurance:Limit of Indemnity(a.o.a.):Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:11Tenants'Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured’s legal liability for the claims made against the Insured for accidental bodily injury of and/or accidental property damage to any third party caused by fire to the buildings leased.This Clause is subject otherwise to the terms,conditions and exceptions of this Policy.Additional Premium:12Building Alterations ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for the claims made against the Insured for accidental bodily injury of and/or property damage to any third party occurring at the premises resulting from the alterations,structural repairs,decorations and the like operations of the insured building。

公众责任险英文版

公众责任险英⽂版The public liability insurancefor the operation of the enterprise to support the umbrellaIn our daily life, we often go to public places such as hotels, supermarkets, shopping malls, movie theaters and office buildings to enjoy the convenience of life and fun.But often seemingly safe places, there are many unexpected accidents that we can't predict.Such as ground water slip fall, elevator parts, downhill, falling objects such as "outrageous fortune" the biggest security hidden danger, has become a public place and business managers will directly facing a lawsuit or claim.Another high-risk place that we often overlook is education training school. Due to the concentration of people and the relative isolation of the environment, it is more likely to cause widespread damage if accidents occur.Training object training schools for children, because children lack of self-protection ability, the school must have a comprehensive and effective safety protection measures, and after the accident will also unavoidable legal and ethical responsibility.But accidents are often unpredictable, and whether there is a better option for the site operator before an accident or casualty. It is particularly important to insure public liability insurance for the place in advance, which can be an effective way to pass on risks and make up for losses in the face of highcompensation or great loss.What is public liability insurance?Public Liability Insurance is also called general liability insurance or comprehensive liability insurance. It takes the public liability of the insured as the object of the insurance, and is the most independent and applicable insurance category in the liability insurance.Public responsibility refers to the damage of the person's property or personal property caused by the fault behavior of the victim in the public place of action, and the economic compensation responsibility of the victim should be borne by the victim according to law.The constitution of public responsibility is based on the legal responsibility of economic compensation, and its legal basis is the civil law and all kinds of relevant laws and regulations. In addition, in some places which are not public activities, if the public is injured by the responsible person in the place, it can also be attributed to the public responsibility.Therefore, public facilities, places, factories, office buildings, schools, hospitals, shops, exhibition halls, zoos, hotels, hotels, theaters, sports venues, and construction sites are all responsible for the risks of public liability accidents. The owners and managers of these places need to transfer their responsibility through public liability insurance.The responsibility of insurance companies in public liability insurance:1. the liability for economic compensation should be taken according to law when the insured person has made personal casualty or property loss;2. in the event of a responsible accident, if the legal proceedings arise, the insured shall bear the responsibility for the relevant litigation costs.However, the highest liability of the insurance company shall not exceed the limit of compensation for each accident or the limit of cumulative compensation stipulated in the policy.Characteristics of public liability insurance:The object of insurance is invisible: the public liability insurance guarantees the insured's economic compensation liability due to the accident caused by personal injury and property loss due to accident in the scope of his operation.A wide range of applications:this type of insurance can be applied to factories, office buildings, hotels, houses, shops, hospitals, schools, theaters, exhibition halls and other public places of activity.There are rich forms of expression: common responsibility, comprehensive responsibility, place responsibility, elevator responsibility, contractor's responsibility, etc., while China mainly displays public responsibility of the placeWhy should public liability insurance be covered?The public responsibility risk in life is everywhere. With the enhancement of people's awareness of rights protection, the general business places are facing the risk of responsibility disputes. After all, business units have the obligation to protect the basic personal safety of consumers.For example, some schools, educational institutions and other places of public gathering, often occur students during class accidental falls, participation in school activities,accidents, students trouble, fight, traffic accident on the way to school, food poisoning, fire and explosion accidents and other security risks.Once an accident occurs, causing casualties, the school should bear the responsibility for the accident. If the public liability insurance is applied, the commercial means can effectively avoid the economic compensation loss of the operator.The risk of public responsibility in life1. Shift risks for enterprise managementPublic liability insurance coverage so that enterprises can effectively transfer the risks in the process of operation, the relief may face high compensation responsibility and the contradiction between small payment ability, avoid due to inability to compensate thebankruptcy and production disruptions, and maintain the stability of production.In October 8th, Guangxi province Lingshan county junior middle school girl Huang in the classroom lectures, ceiling fans fall suddenly, rotating fan blade scraping to its left cheek, face and corner of the blood DC, constitute disfigurement. Lingshan County People's court sentenced the school to full responsibility, to compensate students for subsequent treatment costs and mental damage solatium. The school seeks compensation insurance with the public liability insurance policy signed by an insurance company in March of that year. After providing the claim data, the insurance company has successfully obtained the claim.By insuring public liability insurance, the school can effectively avoid the responsibility risk disputes and maintain the stability of the normal development of the school.2.Effectively protect the vital interests of the publicManagers in every public place are responsible for the customers and the public who visit your place. Although accidents can be reduced, but can not be completely avoided, operators should protect the public interest as the starting point, so that every public access to adequate security.In March this year, Maria Tung in an education institutions in class, because of the ground water caused Maria Tung slipped and fell, then rushed to hospital for treatment, treatmentcosts 5800 yuan. Maria Tung's parents immediately launched a claim to the educational institution. After contacting the educational institution and the insurance company, Maria Tung finally got the compensation.Public liability insurance through the market risk transfer mechanism, using commercial means to solve legal disputes, such as compensation liability, protect the legitimate rights and interests of the public, and maintain social harmony and stability.3.A number of national laws and regulations to encourageThe country has passed many laws and regulations many times, encouraging some public gathering public places to insure public liability insurance, ensuring the public safety, and adopting effective ways to prevent and control the risks actively. For example:"Notice of the general office of the State Council forwarded the Ministry of public security fire control reform and development program" (issued [1995]11) thirtieth:Fire insurance and public liability insurance should be taken in places such as important enterprises, inflammable and explosive dangerous chemicals places, large shopping malls, hotels, restaurants, theaters, dance halls and other public places. The insurance company can give preferential treatment and reward to the fire prevention work and the purchase of fire engines by the fire brigade".Article thirty-third of fire protection law:The State encourages and guides the public to gather places and enterprises that produce, store, transport or sell inflammable and explosive dangerous goods to insure public liability for fire risks.The thirty-seventh article of tort liability law:The organizers or the organizers of mass activities in public places such as hotels, shopping malls, banks, stations, entertainment places, etc., fail to fulfill the obligation of safety protection and cause damage to others, they shall bear the tort liability.How to insure public liability insurance?People in the business of insurance public liability insurance, general insurance business that unlike other fixed premium table, but usually each of the insured risk individually negotiated rates, in order to ensure that the insurer undertakes the responsibility and the risk premium to adapt.Therefore, insuring public liability insurance requires the insurance company to customize the insurance scheme according to the assessment of the enterprise's own risk. As a senior insurance brokerage company, Wachovia has rich experience in planning insurance schemes and claims, and can help enterprises to plan appropriate insurance programs according to the actual needs of enterprises.Public liability insurance coverage, the insurance industry in accordance with international practice, the insurance of public liability insurance according to each accident basic compensation limit and deductible respectively for personal injury and property damage insurance rate two, if the basic compensation limit and deductible or when the insurance premium should be appropriate, but and non proportionally.The calculation methods of public liability insurance premium include the following two situations:1.The compensation limit (accumulated or every accident compensation limit) as the basis of calculation,That is the insurance premium receivable = total amount of compensation * applicable rates2. To calculate the premium according to the size of the place,The insurance premium receivable insurance underwriter = place occupied area (squaremeters) * per square metre of insurance.LastShen zhen myonline insurance brokers reminded everyone ,even if the insured public liability insurance, still need to improve the sense of risk prevention. Business operators shall employ qualified staff, and maintain the use of buildings, roads, factories, machinery, apparatus and equipment for a long time in good condition, immediately to repair the defects have been found, or take temporary measures to prevent the occurrence of accidents.Once the policy insurance accident, insurance companies should contact immediately after, and the extent of the loss occurred in the accident report; without the examination and consent of insurance firms, can not change and repair of the accident related buildings, roads, factories, machinery, apparatus and equipment.For insurance, please contact myonline insurance brokers:400-6007-005。

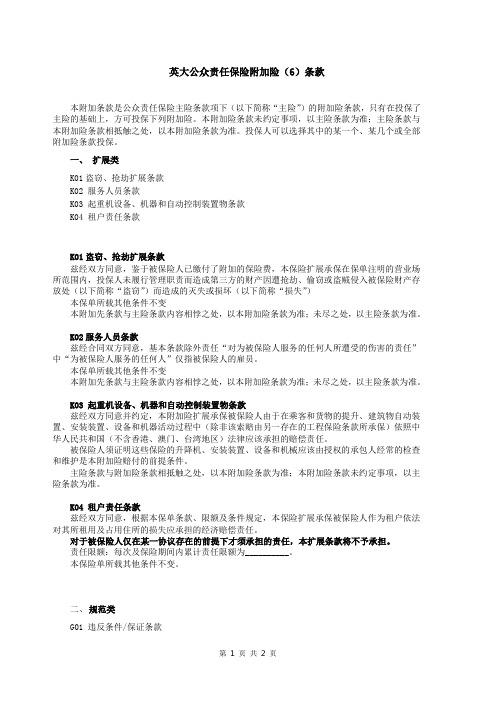

1-2英大公众责任保险附加险(6)条款

英大公众责任保险附加险(6)条款本附加条款是公众责任保险主险条款项下(以下简称“主险”)的附加险条款,只有在投保了主险的基础上,方可投保下列附加险。

本附加险条款未约定事项,以主险条款为准;主险条款与本附加险条款相抵触之处,以本附加险条款为准。

投保人可以选择其中的某一个、某几个或全部附加险条款投保。

一、扩展类K01盗窃、抢劫扩展条款K02 服务人员条款K03 起重机设备、机器和自动控制装置物条款K04 租户责任条款K01盗窃、抢劫扩展条款兹经双方同意,鉴于被保险人已缴付了附加的保险费,本保险扩展承保在保单注明的营业场所范围内,投保人未履行管理职责而造成第三方的财产因遭抢劫、偷窃或盗贼侵入被保险财产存放处(以下简称“盗窃”)而造成的灭失或损坏(以下简称“损失”)本保单所载其他条件不变本附加先条款与主险条款内容相悖之处,以本附加险条款为准;未尽之处,以主险条款为准。

K02服务人员条款兹经合同双方同意,基本条款除外责任“对为被保险人服务的任何人所遭受的伤害的责任”中“为被保险人服务的任何人”仅指被保险人的雇员。

本保单所载其他条件不变本附加先条款与主险条款内容相悖之处,以本附加险条款为准;未尽之处,以主险条款为准。

K03 起重机设备、机器和自动控制装置物条款兹经双方同意并约定,本附加险扩展承保被保险人由于在乘客和货物的提升、建筑物自动装置、安装装置、设备和机器活动过程中(除非该索赔由另一存在的工程保险条款所承保)依照中华人民共和国(不含香港、澳门、台湾地区)法律应该承担的赔偿责任。

被保险人须证明这些保险的升降机、安装装置、设备和机械应该由授权的承包人经常的检查和维护是本附加险赔付的前提条件。

主险条款与附加险条款相抵触之处,以本附加险条款为准;本附加险条款未约定事项,以主险条款为准。

K04 租户责任条款兹经双方同意,根据本保单条款、限额及条件规定,本保险扩展承保被保险人作为租户依法对其所租用及占用住所的损失应承担的经济赔偿责任。

公众责任险条款

公众责任险条款The document was prepared on January 2, 2021公众责任险条款一、责任范围根据本保险单所列范围,在本保险期内发生意外事故引起的,被保险人在法律上应承担的赔偿金额,本公司负责赔偿.二、除外责任除非另行特别规定,本保险单所列责任,不适用也不包括下列各项.1.被保险人根据协议应承担的责任,但即使没有该项协议,仍应承担的责任除外.2.对正为被保险人服务的任何人所遭受的伤害的责任.3.对财产损失的责任:a.被保险人,其雇佣人员或其代理人所有的财产或由其照管或由其控制的财产.b.被保险人或其雇佣人员或其代理人正在从事或一直从事工作的任何物品、土地、房屋或建筑.4.由于下列原因或与下列有关而引起的损失或伤害责任a.对于未载入本保险单表列而属于被保险人的或其所占有的或以其名义使用的任何牲口、脚踏车、车辆、火车头、各类船只、飞机、电梯、升降机、自动梯、起重机、吊车或其它升降装置.b.火灾、地震、爆炸、洪水、烟熏和水污.c.有缺陷的卫生装置或任何类型的中毒或任何不涪或有害的食物或饮料.5.由于震动,移动或减弱支撑引起任何土地或财产或房屋的损坏责任.6.由于战争、入侵、外敌行动、敌对行为不论宣战与否,内战、叛乱、革命、起义、军事行动或篡权行为的直接或间接引起的任何后果所致的责任.三、其他事项⒈一旦发生保险责任内的事故或索赔或诉讼时,被保险人或其代表应立即以书面通知本公司.2.未经本公司书面同意,在发生任何事故或索赔时,被保险人不应拒绝责任,谈判或做出任何承诺出价、议定或赔款.在必要时,本公司有权以被保险人的名义接办对任何索赔的抗辩,或以被保险人的名义,由本公司支付费用,为其自己的利益向任何人提出赔偿请求的诉讼.本公司有权对任何诉讼程序自行处理和解决任何索赔案伴.本公司如有需要时,被保险人应提供一切有关情况和协助.3.在发生本保险单项下的索赔时,如同时尚有其他保险承保同样责任或其中任何一部分的责任,本公司对有关赔偿将按比例负责赔付.4.无论何时,如发生与投保时申报的情况有重大变化,被保险人应在七天内通知本公司.本公司如认为有需要,被保险人应加付保险费.5.本公司可以在7天前以挂号信通知被保险人注销本保险单.对未到期的保险费按比例退给被保险人.6.被保险人应努力做到雇用可靠的、认真的、合格的工作人员并且使所有的建筑物、道路、工厂、机器、装修和设备处于坚实、良好可供使用的状态.被保险人应遵照当局所颁布的任何法律及规定的要求.被保险人对已经发现的缺陷如有需要应予立即修复,并视情况需要采取临时性的预防措施,以防止发生事故.但是发生本保险单项下承保的任何事故后,在未经本公司检查和同意之前,被保险人不得予以改变和修理.本公司在合理的时间内可以检查任何财物.本公司的检查人员如发现任何缺陷或危险时,将以书面通知被保险人.在该项缺陷或危险未被排除并使本公司认为满意之前,对其有关的或因而引起的一切责任本公司概不负责.7.被保险人与本公司之间的一切有关保险的争议应通过友好协商解决.如经协商达不成协议,可申请伸裁机构或向法院提出诉讼.除事先另有协议外,仲裁或诉讼应在被告方所在地.说明公众责任保险条款是公众责任保险合同的最重要的法律文件,一般由保险公司印制在公众责任险保单背后.这是保险公司投保人提出的有关订立公众责任保险合同的要约,一经投保人投保并订立保险合同,则该标准条款即成为公众责任保险合同中的主要条款.公众责任保险奈款的内容主要包括公众责任险的保险责任范围、除外责任以及有关索赔和赔付等其他事项.投保人在签订公众责任保险合同时,应当认真阅读和深入研究这些标准条款,以弄清双方的权利、义务.发生责任事故后,要依据有关规定及时索赔.公众责任险投保单兹拟向以下称承保人投保公众责任险,投保内容如下:说明公众责任险投保单是投保人填写的为被保险人申请投保公众责任险的要式文书,是投保人向保险人发出的正式要约.由于在投保单中没有保险公司的签章位置,因此该投保单虽经投保方填写完毕,但由于未经承保人签章作为承诺的意思表示,因而只有在保险公司签发了公众责任保险单后,公众责任保险合同始才成立.由于保险合同遵守最大诚信原则,投保人在填写投保单时,应该如实地完整地加以填写,以避免影响公众责任保险合同的法律效力.公众责任险保险单保险单号次本公司按照背面所载条款的规定,在本保险单期内,承保下列公众责任险,特立本保险单.一览表××××保险公司日期:___________________________说明公众责任险保单是保险公司承诺公众责任险承保的证明文件,保险公司制单并签章后,证明保险合同成立.在发生保险事故后,被保险人根据保单向保险公司索赔,保险公司也凭以理赔.保险人接到公众责任险投保单后,须注意下列事项.明确投保人与被保险人;弄清被保险人的业务性质,这是厘定保险费率的重要环节;掌握保险区域范围,如果超过规定区域范围的责任事故,未经特约,保险人不予承保;要通过各种渠道获得有关承保的信息资料并做好实地调查.保险人要视每一被保险人的风险情况逐笔议定费率,以保证费率与保险人所承担的风险相适应.保险费率视保险期限的不同可分为1年期费率标准费率和短期费率.保险人在厘定费率时还要考虑不同职业或工种的危险程度.保险费率制定后按保险期限、赔偿限额选择适用费率计算保险费.。

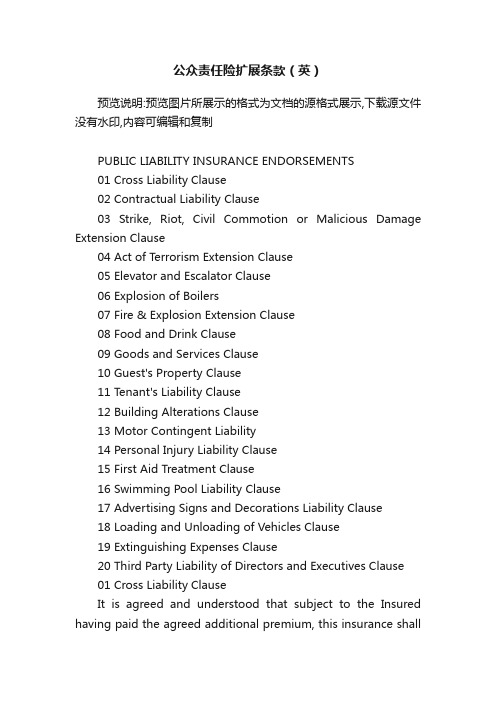

公众责任险扩展条款(英)

公众责任险扩展条款(英)预览说明:预览图片所展示的格式为文档的源格式展示,下载源文件没有水印,内容可编辑和复制PUBLIC LIABILITY INSURANCE ENDORSEMENTS01 Cross Liability Clause02 Contractual Liability Clause03 Strike, Riot, Civil Commotion or Malicious Damage Extension Clause04 Act of Terrorism Extension Clause05 Elevator and Escalator Clause06 Explosion of Boilers07 Fire & Explosion Extension Clause08 Food and Drink Clause09 Goods and Services Clause10 Guest's Property Clause11 Tenant's Liability Clause12 Building Alterations Clause13 Motor Contingent Liability14 Personal Injury Liability Clause15 First Aid Treatment Clause16 Swimming Pool Liability Clause17 Advertising Signs and Decorations Liability Clause18 Loading and Unloading of Vehicles Clause19 Extinguishing Expenses Clause20 Third Party Liability of Directors and Executives Clause01 Cross Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this insurance shallapply to each insured party as if a separate policy had been issued to each party.The Insurers' total liability in respect of the insured parties shall not however exceed in the aggregate for any one accident or series of accidents arising out of one event the limit of indemnity stated in the Schedule.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:02 Contractual Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, the Company shall indemnify the Insured against any claim made in respect of liability assumed by the Insuredunder any contract or agreement for bodily injury of and/or property damage to any third party subject to the limits of liability stipulated in this policy provided that such contract or agreement has been declared to and approved by the Company.This Clause is subject otherwise to the terms , conditions and exceptions of this Policy.Additional Premium:03 Strike, Riot, Civil Commotion or Malicious Damage Extension ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Polity shall be extended to cover the Insider's liability for accidental bodily injury of and/or accidental property damage to any third party occurring at the specified premises directly caused by strike, riot, civil commotion or malicious damage.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:04 Act of Terrorism Extension ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for the bodily injury of and/or property damage to any third party at the specified premises directly caused by any terrorist or terrorism organization.This clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:05 Elevator and Escalator ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidental bodily injury of and/or accidental property damage to any third party in the normal operational use of the elevators or escalators at the premises specified in the Policy subject to the limits of liability stipulated in this Policy.It is warranted that the Insured shall see to it that regular inspection and maintenance of the elevators andescalators shall be carried out by qualified engineers.The amount of indemnity shall not exceed the following limits of liability.Limit of Indemnity a.o.a.:Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms, conditions andexceptions of this Policy.Additional Premium:06 Explosion of BoilersIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insider's liability for accidental bodily injury of and/or accidental property damage to any third party occurring at the specified premises resulting from boiler explosion due to its internal steam pressure subject to the limits of liability stipulated in this policy that the Insured has complied with all operating regulations laid down specifically for such boiler.It is warranted that the Insured shall see to it that regular inspection and maintenance of the boiler shall be carried out by qualified engineers.This clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional premium:07 Fire & Explosion Extension ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the insured for accidents bodily injury of and/or accidental property damage to any third party occurring at the specified premises caused by fire or explosion subject to the following limits of liability during the period of insurance:Limit of Indemnity a.o.a.:Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:08 Food and Drink ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium , this Policy shall be extended to cover the Insured's legal liability for claims made against the Insured for accidental bodily injury of and/or accidental property damage to any third party which occurs during the period of insurance and arises out of poisoning by or foreign or deleterious matter in food or drink consumed in or about the premises specified in the Policy provided always that the Insured shall at all times take every possible precaution to prevent the sale or supply of any condition or free from contamination or for human consumption, subject to the following limits of liability during the period of insurance.Limit of Indemnity a.o.a.:Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:09 Goods and Services ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidental bodily injury or accidental property damage which occurs during the period of insurance and arises out of goods and/or services sold or supplied including transportation provided by the Insured in the normal course of the business as hold proprietor, subject to the following limits of liability during the period of insurance:Limit of Indemnity a.o.a.:Aggregate Limity of Indemnity:This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:10 Guest's Property ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for loss of or damage to the property belonging to guests or customers of the Insured whilst such property is under the custody orcontrol of the Insured subject to a limit of liability of ______any one guest, with the exception of losses of guests' property from safe deposit boxes contained at the premises where the maximum liability of any one guest is agreed to be__________. For the purpose of this extension the guests. property shall include clothing of such guests' sent for laundry, dry cleaning or pressing at the premises , subject always to the following limits during the period of insurance:Limit of Indemnity a.o.a.:Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional premium:11 Tenant's Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's legal liability for the claims made against the Insured for accidental bodily injury of and/oraccidental property damage to any third party caused by fire to the buildings leased.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:12 Building Alterations ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidental bodily injury of and/or property damage to any third party occurring at the premises resulting from the alterations, structural repairs, decorations and the like operations of the insured building provided that the Insured shall give provided that the Insured shall give previous notice to the Company to that effect and the Company may charge an additional premium if the risk exposure is increased.The Insured shall take all practicable safety measures to prevent accidents from happening while the insured building is undergoing the aforesaid process.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:13 Motor Contingent LiabilityIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for the claims made against the Insured for third party liability including passenger risk in respect of any motor car neither owned nor provided by the others while being used in connection with the business.This Clause is subject otherwise to the terms, conditions andexceptions of this Policy.Additional Premium:14 Personal Injury Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for the claims made in respect of personal injury to third parties arising out of the following offenses:1. false arrest, detention or imprisonment, or malicious prosecution2. libel, slander, defamation or violation of rights of privacy3. wrongful entry or eviction or other invasion of rights of private occupancy.The observance of the regulations and laws of the People's Republic of China shall be a condition precedent to any liability of the Company.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:15 First Aid Treatment ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured for reasonable costs or expenses of first aid treatment given or administered by the Insured to a third party injured at the premises upon an occurrence falling within the scope of this Policy.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:16 Swimming Pool Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidents happening in or around or arising out of the ownership, use or operation of the Insured's swimming pool.It is warranted that life-guards are on duty whenever the swimming pool is open for use.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:17 Advertising Signs and Decorations Liability ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for claims made against the Insured for accidental bodily injury or property damage to any third party resulting from the Insured's advertising signs, neon signs, decorations and the like in or about the premises.It is Warranted that the Insured shall see to it that regular inspection and maintenance of such property shall be carried out by qualified persons.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:18 Loading and Unloading of Vehicles ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured's liability for the claims arising from the loading and unloading of the Insured's vehicles in connection with the business at the specified premises.This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:19 Extinguishing Expenses ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the Insured for extinguishing expenses which should be necessarily andreasonably incurred in extinguishing fires at the premises, subject to the following limits of liability during the period of insurance.Limit of Indemnity a.o.a.:Aggregate Limit of Indemnity:This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:20 Third Party Liability of Directors and Executives ClauseIt is agreed and understood that subject to the Insured having paid the agreed additional premium, this Policy shall be extended to cover the third party liability of the Insured's directors and executives for accidents happening in their business travelling or business trips, subject to the following limits of liability during the period of insurance.Limit of Liability a.o.a.:Aggregate Limit of Liability:This Clause is subject otherwise to the terms, conditions and exceptions of this Policy.Additional Premium:PUBLIC LIABILITY INSURANCE ENDORSEMENTS。

公众责任保险(94版) - 英文条款

公众责任保险(1994版)条款Public Liability Insurance (1994 Version) Clause1. Scope of coverWithin the period of insurance and the scope set forth in the schedule of this insurance policy, if any third party is suffered from bodily injury or death or property loss due to accidents happened during operation of the business of the insured within its business scope, and according to law the insured shall bear the liability for economic indemnity, the insurer shall be liable for such indemnity in accordance with the following clauses.The insurer shall compensate for any legal cost paid by the insured due to the reasons mentioned above, as well as any other expenses of the insured agreed by the insurer in advance in written form.The amount of indemnity for each insured event shall be subject to the amount ought to be compensated by the insured as determined by local court or relevant governmental department according to current laws. However, in no case such amount shall exceed the indemnity limit for each insured event set forth in the schedule of this insurance policy. Within the insurance period, under the clauses of this insurance policy, the maximum indemnity liability for the abovementioned economic indemnity shall not exceed the aggregate limit of indemnity set forth in the schedule of this insurance policy.Definitions:Accident:refers to any sudden event that is unexpected and out of control of the insurer, causing property losses or bodily injury or death.2. ExclusionsThe insurer shall not bear the following liabilities for indemnity:Contractual liabilities that shall be borne by the insured, except for the liability of economic indemnity that shall still be borne by the insured without the contract;Any liabilities for the bodily injury or death or property loss suffered by any person serving the insured;Any liabilities for the loss of the following properties:Properties owned by, under the custody of or controlled by the insured or its representative or employee;Any articles, lands, houses or buildings used and occupied by the insured or its representative or employee for business purpose.Any liabilities for losses or injuries caused by:Livestock, bicycle, vehicle, locomotive, vessel, airplane, elevator, lift, moving staircase, crane, hoister or other lifting devices that is owned by, occupied by the insured or used in the insured’s name but not set forth in the schedule of this insurance policy;Fire, earthquake, explosion, flood and smoke;Air, land, water pollution and other pollutions;Defective sanitary installation, poisoning of any kind, or any unclean or harmful food or drink; Medical measures or suggestions made or accepted by the insured.Any liabilities for damages of land, properties, buildings due to quake, movement or weakening of support;Any liabilities due to direct or indirect results of war, act similar to war, act of hostility, armedconflict, terrorist activity, rebellion or coup;Any liabilities due to direct or indirect results of strike, riot, civil turbulence or malicious act; Intentional act or gross negligence of the insured or its representative;Any directly or indirect liabilities due to nuclear fission, nuclear fusion, nuclear weapon, nuclear material, nuclear radiation and radioactive pollution;Penalty, fine or punitive indemnity;The deductible that shall be borne by the insured as agreed in the schedule of the insurance policy and relevant clauses.3. Claims settlementIn case of occurrence of any event or litigation covered under this insurance policy:Unless agreed by the insurer in writing, the insurer shall not be bound by any commitments, offers, agreements, payments or indemnities made by the insured or its representative. If necessary, the insurer shall have the right to take over the debates or claims of any litigation in the name of the insured;The insurer shall have the right to, in the name of the insured, make claims to any liable party for the benefits of the insurer at its own account. Unless agreed by the insurer in writing, the insured shall not accept any payment or indemnity arrangements made by the reliable party for the relevant losses, or waive any right of claim towards such reliable party, otherwise, the so-caused consequence shall be borne by the insured;In the process of the litigation or claim settlement, the insurer shall have the right to handle any litigation or resolve any claims on its own discretion, and the insured shall have the obligation to provide the insurer with all and any necessary materials and assistance;The limitation period of actions of claiming for indemnity by the insured against the insurer is two years since the date when the insured know or should have known the occurrence of the insured event.4. The obligation of the insuredThe insured and its representative shall strictly fulfill the following obligations:If the insurer, prior to the conclusion of an insurance contract, inquire about the subject matter of the insurance or person to be insured, the insurance applicant should make a full and accurate disclosure. The insurer shall have the right to terminate the insurance contract, in the case that the insurance applicant intentionally or gross negligently fails to perform such obligation of making a full and accurate disclosure specified in the preceding paragraph to the extent that it would materially affect the insurer's decision whether or not to underwrite the insurance or whether or not to increase the premium rate.The contractual cancellation right under the preceding paragraph shall be extinguished if not exercised for thirty (30) days, commencing on date when the insurer knows the grounds of termination. And the insurer can not cancel the contract, if the contract has been established for more than two years; in case of occurrence of insured event, the insurer shall bear obligation for payment of insurance benefits.If any applicant intentionally fails to perform its obligation of making a full and accurate disclosure, the insurer shall bear no obligation for making any payment of the insurance benefits, or for returning the premiums paid, for the occurrence of the insured event which occurred prior to the termination of the contract.If an applicant gross negligently fails to perform its obligation of making a full and accurate disclosure and this materially affects the occurrence of an insured event, the insurer shall bear no obligation for making any payment of the insurance benefits for any insured event occurring before the termination of the contract, but may return the premiums paid.If the insurer has known the information that the insured fails to make a full and accurate disclosure, theinsurer can not terminate the contract; in case of occurrence of the insured event, the insurer shall bear the obligation for payment of the insurance benefits.The insured or its representative should pay the premium on time in accordance with the agreement specified in the schedule of the insurance policy and the endorsement;The insured shall engage reliable, serious and qualified staff and make shall all its buildings, roads, plants, machines, fitments and other devices are in good condition and available for use. Moreover, the insured shall be subject to any laws and regulations issued by local government, immediately repair any found defects, and take provisional preventive measures to avoid happening of the insured event;In case of occurrence of any event covered under this insurance policy, the insured or its representative shall:Inform the insurer in time and report the course, cause and degree of damage in written form within seven days or within a term prolonged agreed by the insurer in writing;Not change or repair its buildings, roads, plants, machines, fitments and other devices unless inspected and agreed by the insurer;Inform the insurer in writing when any litigation is expected and delivery the court summons or other legal documents to the insurer immediately upon receipt of the same;Provide all evidences, materials and bills as the basis for claims.5. General provisions(1) Policy cancellationThis policy may be canceled at any time at the request of the insurance applicant in writing or at the option of the insurer by giving a fifteen (15) days prior notice to the insured. In the former case the insurer shall retain a premium calculated on short term rate basis for the time the policy has been in force, while in the latter case such premium shall be calculated on pro rata daily basis.(2) Claim fraudThe insurer shall have the right to cancel the insurance contract and refuse to return the premiums paid, if the insured claims that an insured event that doesn’t exist has occurred and submits a claim for payment of the insurance benefits.If the insurance applicant or the insured intentionally causes the occurrence of an insured event, the insurer shall have the right to cancel the insurance contract, bear no obligation for indemnity or payment of the insurance benefits and decline to return the premiums paid.If the insurance applicant or the insured, following the occurrence of an insured event, provides forged and altered relevant evidence, information or other proofs, falsifies the cause of the occurrence of the insured event or overstates the extent of the loss, the insurer shall bear no obligation for indemnity or payment of the insurance benefits for the portion which is falsified or overstated.The insurance applicant or the insured shall refund or indemnify the insurer for any payments or expenses which were made or incurred by the insurer due to the commission of any act stipulated in the foregoing three paragraphs of this Article by the insurance applicant or the insured.(3) Reasonable inspectionThe insured shall observe all the laws, rules and regulations prescribed by the public security and fire departments of the State with respect to fire prevention, safety, production, operations, labor protection, and use of the special equipment, enhance the management, and take reasonable predictive measures to avoid or reduce the occurrence of the insured event.The representative of the insurer shall at any suitable time be entitled to attend the site and inspect orexamine the risk exposure of the property insured. For this purpose, the insured shall provide full assistance and all details and information required by the insurer as may be necessary for the assessment of the risk. The above mentioned inspection or examination shall in no circumstances be held as any admission to the insured by the insurer. The insurance applicant and the insured shall seriously implement any written suggestions provided by the insurer to eliminate risks and latent problems.In the event that the insurance applicant or the insured fails to abide by the foregoing agreements and due to which the insured event has occurred, the insurer shall bear no obligation for indemnity; the insurer is not liable for indemnity for any expanding losses due to the insurance applicant or the insured’s breach of the foregoing agreeme nts.(4) Duplicated insuranceShould any loss, damage, expenses or liability recoverable under the policy be also covered by any other insurance, the insurer shall only be liable to pay or contribute its proportion of the claim irrespective as to whether the other insurance is arranged by the Insured or others on his behalf, or whether any indemnification is obtainable under such other insurance.(5) SubrogationIn the event that the losses within the insurance liability shall be indemnified by related responsible party, the insurer may from the date when the insurer pay indemnity of insurance compensation to the insured, within the scope of indemnity, subrogate the insured’s right against related responsible party for compensation, and the insured should provide the insurer with necessary documents and knowing information.If the insured has already obtained insurance compensation from the responsible party, the insurer shall pay the amount after deducting such obtained amount.If the insured waives the right of claiming for indemnity against the responsible party after the occurrence of the insured event and before the insurer making the indemnity, the insurer is not liable for indemnity; If the insured, without the insurer's consent, waives the right of claiming for indemnity against the responsible party after indemnity is made by the insurer, the waiver of the insured shall be regarded as invalid; The insurer may deduct or request the insured to refund the corresponding amount if the insurer is not able to exercise the right of claiming for indemnity by subrogation due to the insured’s intentional misconduct or gross negligence.(6) Disputes settlementDisputes arising from the execution and performance of the policy shall be settled through negotiation between the parties hereto. Should no settlement be reached, the case in dispute shall be submitted to the arbitration institution specified in the policy. Where no arbitration institution is specified in the policy or no arbitration agreement is reached after disputes, either party hereinto may bring litigation to the People’s Court with jurisdiction.Any dispute with regard to the policy should apply the law of P.R.China (excluding Hongkong, Macao and Taiwan).。

公众责任保险条款(doc 8页)

公众责任保险条款(doc 8页)公众责任险条款一、责任范围根据本保险单所列范围,在本保险期内发生意外事故引起的,被保险人在法律上应承担的赔偿金额,本公司负责赔偿。

二、除外责任除非另行特别规定,本保险单所列责任,不适用也不包括下列各项。

1.被保险人根据协议应承担的责任,但即使没有该项协议,仍应承担的责任除外。

2.对正为被保险人服务的任何人所遭受的伤害的责任。

3.对财产损失的责任:a.被保险人,其雇佣人员或其代理人所有的财产或由其照管或由其控制的财产。

b.被保险人或其雇佣人员或其代理人正在从事或一直从事工作的任何物品、土地、房屋或建筑。

4.由于下列原因或与下列有关而引起的损失或伤害责任赔案伴。

本公司如有需要时,被保险人应提供一切有关情况和协助。

3.在发生本保险单项下的索赔时,如同时尚有其他保险承保同样责任或其中任何一部分的责任,本公司对有关赔偿将按比例负责赔付。

4.无论何时,如发生与投保时申报的情况有重大变化,被保险人应在七天内通知本公司。

本公司如认为有需要,被保险人应加付保险费。

5.本公司可以在7天前以挂号信通知被保险人注销本保险单。

对未到期的保险费按比例退给被保险人。

6.被保险人应努力做到雇用可靠的、认真的、合格的工作人员并且使所有的建筑物、道路、工厂、机器、装修和设备处于坚实、良好可供使用的状态。

被保险人应遵照当局所颁布的任何法律及规定的要求。

被保险人对已经发现的缺陷如有需要应予立即修复,并视情况需要采取临时性的预防措施,以防止发生事故。

但是发生本保险单项下承保的任何事故后,在未经本公司检查和同意之前,被保险人不得予以改变和修理。

本公司在合理的时间内可以检查任何财物。

本公司的检查人员如发现任何缺陷或危险时,将以书面通知被保险人。

在该项缺陷或危险未被排除并使本公司认为满意之前,对其有关的或因而引起的一切责任本公司概不负责。

7.被保险人与本公司之间的一切有关保险的争议应通过友好协商解决。

如经协商达不成协议,可申请伸裁机构或向法院提出诉讼。

公众责任保险条款英文