国际金融Chapter4课后答案

陈雨露《国际金融》第4版章节练习及详解(离岸金融市场)【圣才出品】

陈雨露《国际金融》第4版章节练习及详解第四章离岸金融市场一、概念题1.国际金融市场(人大1999研)答:国际金融市场是指资金在国际间进行流动或金融产品在国际间进行买卖和交换的场所,它是开放经济运行的重要外部环境。

广义上的国际金融市场包括国际资金市场、外汇市场、国际保险市场和国际黄金市场;狭义上的国际金融市场特指国际资金市场,即国际间的资金借贷市场。

国际金融市场是由外国金融市场、欧洲货币市场与外汇市场这三部分所构成的相互联系的整体。

其中,从事货币兑换的外汇市场是国际金融市场的基础,外国金融市场是国内金融市场的对外延伸,欧洲货币市场是国际金融市场的核心。

按照资金融通的期限,国际金融市场可分为货币市场和资本市场。

前者是指短期资金交易的市场,又称为短期资金市场,如跨国发行商业票据融通资金;后者指长期资金交易的市场,又称为长期资金市场,如跨国发行外国债券或欧洲债券融通长期资金。

国际金融市场作为国际信贷中介,对于联系全球各地的生产、贸易活动起着重要的作用:①国际金融市场便利了国际资金的运用、调度和国际债务的结算,为扩大国际投资和国际贸易创造了条件,便利了借贷资本的国际流通和产业资本的国际移动。

②国际金融市场使国际金融渠道畅通,从而使一些国家能比较顺利地获得发展经济所急需的资金。

③国际金融市场在调节国际收支方面也起了不可忽视的作用。

第二次世界大战后,国际金融市场日益成为各国外汇资金的重要来源。

国际金融市场也有其不利和消极的一面,主要反映在国际资本流动冲击一些国家的国内经济,影响其国内货币政策的执行等问题上。

另外,国际金融市场还为国际走私、贩毒及其他金融犯罪活动提供了有利的场所,在一定程度上削弱了有关国家在这方面的执法力量。

2.离岸金融市场(人大1998研;北京工商大学2006研;中南财大2006研)答:离岸金融市场是国际金融市场的核心,是从事境外金融业务的金融市场。

离岸金融市场不是指某一市场的地理位置,而是指市场中交易的货币的性质。

国际金融学陈雨露第四版课后习题答案 第四章

第四章作业1.说说欧洲美元是什么意思。

答:欧洲美元并不是一种特殊的美元,它与美国国内流通的美元是同质的,具有相同的流动性和购买力。

所不同的是,欧洲美元不由美国境内金融机构经营,不受美联储相关银行法规、利率结构的约束。

这里的“欧洲”,是指“非国内的”、“境外的”、“离岸的”,并非地理意义上的。

2.欧洲美元市场的出现会影响美联储的货币政策吗?答:欧洲美元市场的优势在于不受任何国家法令限制,免税,不缴纳法定储备,流动性强,主要作为银行间同业短期资金批发市场,参与者多为商业银行、各国央行及政府,主要借款人为跨国公司,交易对象多为具有标准期限的定期存款,一般为短期,其余为可转让存单。

随着市场业务的不断拓展,目前欧洲美元市场的地理范围和借贷币种也正在不断扩大。

但由于它的流动性太强,不受约束,因而也是造成国际金融市场动荡不定的主要因素。

由此来看,它会影响美联储的货币政策。

4.欧洲货币市场运行是否存在信用膨胀问题?欧洲货币市场规模不断扩大是否会威胁国际金融稳定?答:存在信用膨胀问题。

欧洲货币市场作为实现国际资本转移的场所,其加速国际贸易的发展,促进国际金融密切联系的作用是其他国际金融市场和转移渠道无法相比、无法替代的。

欧洲货币市场是个信用市场,但它仍同远期外汇市场发生着紧密的联系。

在一些国际大银行中,欧洲货币交易往往就是通过其外汇业务部门而不是信贷部门进行的。

欧洲货币市场与外汇市场的结合,给市场带来了更广阔的活动空间。

与此同时,各国际金融中心除了信用评级机构和中央结算体系外,并没有任何正规的金融管理部门实施对欧洲货币市场上金融机构以及它们所进行的信贷业务活动的管理,在这种情况下,如何控制各个金融中心,乃至全球的欧洲货币市场信贷规模是一个重要问题。

欧洲货币市场并不大量增加金融系统创造货币和信贷的能力。

这并不意味着欧洲货币市场没有信用膨胀。

由于欧洲货币市场没有准备金规定,只受对借贷资本的需求和贷款机构本身的谨慎态度的限制,信用膨胀的可能性也很大。

完整word版托马斯国际金融课后习题答案解析word文档良心出品

Suggested an swers to questio ns and p roblems(in the textbook)Disagree, at least as a general statement. One meaning of a current account surplus is that thecountry is exporting more goods and services than itis importing. One might easily judge that this is not good — the country isp roduci ng goods and services that are exp orted, but the country is not at the same time getting the imports of goods and services that would allowdo more consump tio n and domestic inv estme nt. I n this way a curre nt acco unt deficit mightbe con sidered good — the extra imp orts allow the country to con sume and in vest domesticallymore tha n the value of its curre nt production. Another meaning of a current account surplus isthat the country is en gag ing in foreig n finan cial inv estme nt — it is buildi ng up its claimson foreig ners, and this adds to n ati onal wealth. This sounds good, but as no ted above it comesat the cost of forego ing curre nt domestic pu rchases of goods and services. A curre nt acco untdeficit is the country running dow n its claims on foreigners or increasing its indebtedness toforeigners. Thissounds bad, but it comeswith the ben efit of higher levels of curre nt domestic expen diture.Differe nt coun tries at differe nt times may weigh the bala nee of these costs and ben efitsdiffere ntly, so that we cannot simply say that a curre nt acco unt surplus is better tha n a current acco unt deficit.Disagree. If the country has a surplus (a p ositive value) for its official settleme nts bala nee, then the value for its official reserves bala nee must be a negative value of the sameamount (so that the two add to zero). A negative value for this asset item means that funds are flow ing out in order for the country to acquire more of these kinds of assets. Thus, the country is in creas ing its hold ings of official reserve assets.Item e is a tran sacti on in which foreig n official hold ings of U.S. assets in crease. This is a po sitive (credit) item for official reserve assets and a negative (debit) item for private capital flowsas the U.S. bank acquires pound bank depo sits. The debit item con tributes to a U.S. deficit in theofficial settleme nts bala nee (while the credit item is recorded "below the lin e," p ermitti ng the official settleme nts bala nee to be in deficit). All other transactions invoIve debit and credit items both of which are includedin the official settleme nts bala nee, so that they do not directly con tribute to a deficit (orsurpi us) in the official settleme nts bala nee.Chap ter 22. it 4. 6.8. a. Mercha ndise trade bala nee: $330 - 198 = $132Goods and services bala nee: $330 - 198 + 196 - 204 = $124Curre nt account bala nee: $330 - 198 + 196 - 204 + 3 - 8 = $119Official settleme nts bala nee: $330 - 198 + 196 - 204 + 3 - 8 + 102 - 202 + 4 = $23b. Change in official reserve assets (net) = - officialsettlements balanee=-$23. The country is in creas ing its net hold ings of official reserve assets.10. a. In ternatio nal in vestme nt p ositio n (billio ns): $30 + 20 + 15 - 40 - 25 =$0.The country is n either an intern ati onal creditor nor a debtor. Its hold ing of intern ati onalassets equals its liabilities to foreig ners.b. A curre nt acco unt surplus p ermits the country to add to its net claims on foreig ners. For thisreas on the coun try's intern atio nal inv estme nt po siti on will becomea p ositive value. Theflow in crease in net foreig n assets results in the stock of net foreig n assets beco ming positive.Exports of merchandise and services result in supply of foreign currency in the foreig n exchange market. Domestic sellers ofte n want to be p aid using domestic curre ncy, while the foreign buyers want to pay in their curre ncy.In the p rocess of paying for these exp orts, foreig n curre ncy is excha nged for domestic currency, creat ing supply of foreig n curre ncy. Intern ati onalcap ital in flows result in a supply of foreig n curre ncy in the foreig n excha nge market. I nmaki ng inv estme nts in domestic finan cial assets, foreig ninvestors often start with foreign currency and must exchange it for domestic curre ncy before theycan buy the domestic assets. The excha nge creates a supply of foreig n curre ncy. Sales of foreign finan cial assets that the country's residents had previously acquired, and borrowing fromforeignersby this coun try's reside nts are other forms of cap ital in flow that can create supply of foreign curre ncy.The U.S. firm obta ins a quotatio n from its bank on the spot excha nge rate for buying yen withdollars. If the rate is acce ptable, the firm in structs its bank that it wants to use dollars fromits dollar check ing acco unt to buy 1 millio n yen at this spot excha nge rate. It also in structsits bank to send the yen to the bank acco unt of the Japan ese firm. To carry out thisChap ter 32. 4.instruction, the U.S. bank instructs its correspondent bank in Japan to take1 milli on yen from its acco unt at the corres pondent bank and tran sfer the yen to the bank account of the Japan ese firm. (The U.S. bank could also use yen at its own branch if it has a branchin Japan.)The trader would seek out the best quoted spot rate for buying euros with dollars, either throughdirect con tact with traders at other banks or by using the services of a foreign exchange broker.The trader would use the best rate to buy euro spot. Sometime in the n ext hour or so (or, typically at least by the end of the day), the trader will en ter the in terba nk market aga in, toobtain the best quoted spot rate for selling euros for dollars. The trader will use the best spot rate to sell her p reviously acquired euros. If the spot value of the eurohas rise n duri ng this short time, the trader makes a p rofit.The cross rate betwee n the yen and the krone is too high (the yen value of the krone is toohigh) relative to the dollar-foreig n curre ncy excha nge rates. Thus, in a p rofitable tria ngulararbitrage, you want to sell kroner at the high cross rate. The arbitrage will be: Use dollars to buykroner at $0.20/kr one, use these kroner to buy yen at 25 yen/krone, and use the yen to buy dollarsat $0.01/ye n. For each dollar that you sell in itially, you can obta in 5 kroner, these 5 kronercan obta in 125 yen, and the 125 yen can obta in $1.25. The arbitrage p rofit for each dollar istherefore 25 cen ts.Selli ng kroner to buy yen p uts dow nward p ressure on the cross rate (the yen price ofkrone). The value of the cross rate must fall to 20 (=0.20/0.01) yen/krone to elimi nate theopportunity for tria ngular arbitrage, assu ming that the dollar excha nge rates are un cha nged.The in crease in supply of Swiss francs puts dow nward p ressure on the excha nge-rate value($/SFr) of the franc. The mon etary authorities must intervene to defend the fixed exchange rate bybuying SFr and sellingb. The in crease in supply of francs puts dow nward p ressure on the excha nge-rate value ($/SFr) ofthe franc. The mon etary authorities must intervene to defend the fixed exchange rate by buying SFrand sellingc. The in crease in supply of francs puts dow nward p ressure on the excha nge-rate value($/SFr) of the franc. The mon etary authorities must intervene to defend the fixedexchange rate by buying SFr and selling6.8. a. b.10. a.dollars. dollars. dollars.d. The decrease in dema nd for francs puts dow nward p ressure on the excha nge-rate value ($/SFr) ofthe franc. The mon etary authorities must intervene to defend the fixed exchange rate by buying SFrand selling You will need data on four market rates: The current interest rate on bonds issued by the U.S. government that mature in one year, the interest rate (or yield) on bonds issued by the British government that maturein one year, the curre nt spot excha nge rate betwee n the dollar and pound, and the current one-year forward exchange rate between the dollar and pound. Do these rates result in a coveredinterestdifferential that is very closeto zero?Relative to your exp ected spot value of the euro in 90 days ($1.22/euro), the current forward rate ofthe euro ($1.18/euro) is low — the forward value of the euro is relatively low. Using the principle of "buy low, sell high," you can sp eculate by en teri ng into a forward con tract now to buy euros at$1.18/euro. If you are be able to immediately of $0.04 for each euro this way, then massivedollars.Chap ter 42.(or yield) curre nt 4. a. The U.S. firm has an asset p ositi on in yen — it has a long p ositi on in yen. To hedge its exp osure to excha nge rate risk, the firm should en ter into a forward exchange con tract now in which the firm commits to sell yen and receive dollars at the curre ntforward rate. The con tract amounts are to 1 millio n yen and receive $9,000, both in 60days.sell b. The stude nt has an asset po siti on in yen — a long p ositi on in yen. Tohedge the exp osure to excha nge rate risk, the stude nt should en ter into a forward exchange con tract now in which the stude nt commits to sell yen and receive dollars at the current forward rate. The con tract amounts are to 10 millio n yen and receive $90,000, both in 60 days.sellc. The U.S. firm has an liability position in yen — a short position in To hedge its exp osure to excha nge rate risk, the firm should en ter into a forward exchange con tract now in which the firm commits to sell dollars receive yen at the curre ntforward rate. The con tract amounts are to sell $900,000 and receive 100 millio n yen, bothin 60 days.yen.and 6. correct in your expectation, then in 90 days you will resell those euros for $1.22/euro, pocketing a profit that you boughtforward. If many people sp eculate in pu rchases now of euros forward(in creas ing the dema ndfor euros forward) will tend to drive up the forward value of the euro, toward a curre nt forwardrate of $1.22/euro.The Swiss franc is at a forward prem ium. Its curre nt forward value($0.505/SFr) is greater than its current sp ot value ($0.500/SFr).The covered in terest differe ntial "i n favor of Switzerla nd" is ((1 + 0.005) (0.505) / 0.500) - (1 + 0.01) = 0.005. (Note that the interest rate used must match the time p eriod of the in vestment.) There is a covered interest differential of 0.5% for 30 days (6 percent at an annual rate). TheU.S. investor can make a higher return, covered against exchange rate risk, by inv esti ng in SFr-de nomin ated bon ds, so p resumably the inv estor should makethis covered investment. Although the interest rate on SFr-denominated bonds is lower tha n the in terest rate on dollar-de nomin ated bon ds, the forward p remium on the franc is larger tha n this differe nee, so that the covered inv estme nt is a good idea.The lack of demandfor dollar-denominated bonds (or the supply of thesebonds as in vestors sell them in order to shift into SFr-de nomin ated bon ds) puts dow nward p ressure on the p rices of U.S. bon ds —up ward p ressure on U.S. in terest rates. The extra dema nd for the franc in the spot excha nge market (as in vestors buy SFr in order to buy SFr-de nomin ated bon ds)puts up ward p ressure on the spot excha nge rate. The extra dema nd for SFr-de nomin ated bonds puts up ward p ressure on the p rices of Swiss bonds — dow nward p ressureon Swiss in terest rates. The extra supply of francs in the forward market (as U.S. i nv estors cover their SFr in vestme nts back into dollars) p uts downwardpressure on the forward exchange rate. If the only rate that changes is the forward exchange rate, this rate must fall to about $0.5025/SFr. Withthis forward rate and the other in itial rates, the covered in terest differe ntial is close to zero. In test ing covered in terest p arity, all of the in terest rates and excha nge rates that are n eeded to calculate the covered in terest differe ntial are rates that can observed in the bond and foreignexchange markets. Determining whether the covered in terest differe ntial is about zero (covered interest parity) is then straightforward (although somemore subtle issues regardingtim ing of tran sact ions may also n eed to be addressed). I n order to test uncovered interestparity, we need to know not only three rates — two interest rates and the current spot exchangerate — that can be observed in the market, but also one rate— the exp ected future spot exchange rate — that is notobserved in any market. The tester the n n eeds a way to find out aboutinv estors' exp ectati ons. One way is to ask them, using a survey, but they may not say exactlywhat they really think. Ano ther way is to exam ine the actual un covered in terest differe ntialafter we know what the future spot excha nge rate actually turns out to be, and see whether thestatistical characteristics of the actual uncovered differential are consistentwith an expected uncovered differential of about zero (uncovered interest parity). 8. a.b.c.10.Cha pter 52. a. The euro is expected to appreciate at an annual rate of approximately ((1.005 -1.000)/1.000) (360/180)100 = 1%. The exp ected un covered in terestdifferential is approximately 3%+ 1%- 4%= 0, so uncovered interest parityholds (app roximately).b. If the in terest rate on 180-day dollar-de nomin ated bonds decli nes to3%, the n the spot excha nge rate is likely to in crease —the euro willappreciate, the dollar depreciate. At the initial current spot exchange rate,the initial expected future spot exchange rate, and the initial euro interestrate, the exp ected un covered in terest differe ntial shifts in favor of investing in euro-denominated bonds (the expected uncovered differential is now p ositive, 3% + 1% - 3% = 1%, favori ng un covered inv estme nt in euro-de nomin ated bon ds.The in creased dema ndfor euros in the spot excha nge market tends to app reciate the euro. If the euro in terest rate and the exp ected future spot excha nge rate rema in un cha nged, the n thecurre nt spot rate must cha nge immediately to be $1.005/euro, to reestablish un covered interest parity. Whenthe current spot rate jumps to this value, the euro'sexcha nge rate value is not exp ected to cha nge in value subseque ntly duri ng the next 180 days.The dollar has depreciated immediately, and the uncovered differe ntial then again is zero (3% + 0% - 3% = 0).4. a. For uncovered interest parity to hold, investors must expect that the rateof change in the spot exchange-rate value of the yen equals the interest rate differential, which is zero. Investors must expect that the future spot valueis the same as the curre nt spot value, $0.01/ye n.b. If inv estors exp ect that the excha nge rate will be $0.0095/ye n, the nthey expect the yen to depreciate from its initial spot value during the next 90 days. Give n theother rates, i nv estors tend to shift their inv estme nts toward dollar-de nomin ated inv estments. The extra supply of yen (and dema ndfor dollars) in the spot exchange market results in a decrease in the current spot value of the yen(the dollar appreciates). The shift to expecting that the yen will depreciate (the dollarappreciate) sometime during the next 90 days tends to cause the yen to dep reciate (the dollar toapp reciate) immediately in the curre nt spot market.The law of one p rice will hold better for gold. Gold can be traded easilyso that any price differences would lead to arbitrage that would tend to push gold p rices (stated in a com mon curre ncy by converting p rices using market excha nge rates) back close to equality. Big Macs cannot be arbitraged. If p rice differe nces exist, there is no arbitrage p ressure, so the p ricedifferences can persist. The prices of Big Macs(stated in a commoncurrency) vary widely around the world.According to PPP, the exchange rate value of the DM(relative to the dollar) has rise n since the early 1970s because Germa ny has exp erie need less inflation than has the United States ——the productprice level has risen lessin Germa ny since the early 1970s tha n it has rise n in the Un ited States.According to the monetary approach, the Germanprice level has not risen as muchbecause the Germa nmon eys upply has in creased less tha n the has in creased in the Un ited States,relative to the growth rates of real domestic production case —more in flati ongrowth in Brita in.rate ofthe domestic moneysupply (M s ) is two percentage points higher tha n it was previously, the mon etary app roach in dicates that the excha nge rate value (e) of the foreig n curre ncy will be higher tha n it otherwise would be — that is, the excha nge rate value of the coun try's curre ncy will be lower. Sp ecifically, the foreig n curre ncy will app reciate by two percentagepoints more per year, or depreciate by two percentage less. That is, the domestic currency will depreciate by two percentage more per year, or app reciate by two p erce ntage points less.b. The faster growth of the coun try's money supply eve ntually leads to afaster rate of inflation of the domestic price level (P). Specifically, inflation rate will be two percentage points higher than it otherwise be. Accord ing torelative PPP, a faster rate of in crease in the domestic level (P) leads to a higher rate of app reciatio n of the foreig n curre ncy.12. a. For the Un ited States in 1975, 20,000 = k 6.8. mon eys upply the opposite higher money in the two countries. The British pound is in Britain than in the United States, and 10. a. Because the growth pointspointsthewould price■100 800, or k = 0.25.For P ugelovia in 1975, 10,000 = k b. For the Un ited States, the qua ntity theory of money with a con sta nt kmeansthat the quantity equation with k = 0.25 should hold in 2002: 65,000=0.25 2601,000. It does. Because the quantity equation holds for both years with the samek, thechange in the price level from 1975 to 2002 is consistent with the quantity theory of moneywith aconstant k. Similarly, for Pugelovia, the quantity equation with k = 0.5 should hold for 2002, and it does (58,500 =0.5 390 300).14. a. The tighte ning typ ically leads to an immediate in crease in the coun try'sin terest rates. In additi on, the tighte ning p robably also results ininvestors' expecting that the exchange-rate value of the country's currencyis likely to be higher in the future. The higher expected exchange-rate value for the currency isbased on the expectation that the country's price level will be lower in the future, and PPP indicates that the curre ncy will the n be stro nger. For both of these reas ons, intern ati onal investors will shift toward inv est ing in this coun try's bon ds. The in crease in dema nd for the coun try's curre ncy in the spot excha nge market causes the curre ntexcha nge-rate value of the curre ncy to in crease. The curre ncy maya pp reciate a lot because thecurrent exchange rate must "overshoot" its expected future spot value. Un covered in terest p arityis reestablished with a higher in terest rate and a subseque nt exp ected dep reciati on of the curre ncy.b. If everyth ing else is rather steady, the excha nge rate (the domesticcurrency price of foreign currency) is likely to decrease quickly by a large amount. After this jump, the excha nge rate maythe n in crease gradually toward its long-run value — the value con siste ntwith PPP in the long run.Weoften use the term pegged exchange rate to refer to a fixed exchange rate, because fixed ratesgen erally are not fixed forever. An adjustable peg isan exchange rate policy in which the "fixed" exchange rate value of a currency can be cha nged fromtime to time, but usually it is cha nged rather seldom(for in sta nee, not more tha n once every several years). A crawli ng peg isan exchange rate policy in which the "fixed" exchange rate value of a currency is cha nged ofte n(for in sta nee, weekly or mon thly), sometimes accordi ng to in dicators such as the differe nee inin flati on rates.Disagree. If a country is expected to impose exchange controls,which usually make it more difficult to move funds out of the country in the future,investors are likely to try to shift funds out of the country now before the100 200, or k = 0.5.Chap ter 62. 4.con trols are imp osed. The in crease in supply of domestic curre ncy into the foreig n excha ngemarket (or in crease in dema nd for foreig n curre ncy) p utsdownward pressure on the exchange rate value of the country's currency —the curre ncy tends to dep reciate.6. a. The market is atte mpting to dep reciate the pn ut (app reciate the dollar) toward a value of 3.5 pnutsper dollar, which is outside of the top of the allowable band (3.06 pnuts per dollar). In order todefend the pegged exchange rate, the Pu gelovia n mon etary authorities could use official in terve ntio nto buy pnuts (in exchange for dollars). Buying pnuts prevents the pnut ' s value from declining (selling dollars prevents the dollar ' s value fromrisin g). The in terve nti on satisfies the excess p rivate dema nd for dollarsat the curre nt p egged excha nge rate.b. In order to defend the pegged exchange rate, the Pugelovian governmentcould impose excha nge con trols in which some p rivate in dividuals who want to sell pnuts and buy dollars are told that they cannot legally do this (or cannot do this without gover nment p ermission, and not all requests are approved by the government). By artificially restricting the supply of pnuts (and the dema nd for dollars), the Pu gelovia n gover nment can force the remai ning p rivate supply and dema nd to "clear" within the allowable band.The exchange controls attempt to stifle the excess private demandfor dollars at the curre nt p egged excha nge rate.c. In order to defend the pegged exchange rate, the Pugelovian governmentcould in crease domestic in terest rates (p erha ps by a lot). The higher domestic interest ratesshift the incentives for international capital flows toward inv estme nts in Pu gelovia n bon ds. The in creased flow of intern ati onal finan cial cap ital into Pu gelovia in creases the dema nd forpnuts on the foreig n excha nge market. (Also, the decreased flow of intern ati onal financialcapital out of Pugelovia reduces the supply of pnuts on the foreignexcha nge market.) By in creas ing the dema nd for pnuts (and decreas ing the suppl y), the Pugelovia n gover nment can in duce the p rivate market to clear within the allowable band. The increased domestic in terest rates attem pt toshift the private supply and demandcurves so that there is no excess private dema nd for dollars at the curre nt p egged excha nge rate value.8. a. The gold sta ndard was a fixed rate system. The gover nment of each countryp artici pati ng in the system agreed to buy or sell gold in excha nge for itsown currency at a fixed price of gold (in terms of its own currency). Becauseeach currency was fixed to gold, the exchange rates between currencies also ten ded to be fixed, because in dividuals could arbitrage betwee n gold and curre ncies if the curre ncy excha nge rates deviated from those imp lied by the fixed gold p rices.Britai n was central to the system, because the British economy was the leader in in dustrializatio n and world trade, and because Brita in was con sidered finan cially secure and p rude nt. Brita in was able and willi ng to run p ayme nts deficits that p ermitted many other coun tries to run p ayme ntssurpi uses. The other coun tries used their surpi uses to build up their holdi ngs of gold reserves (and of intern ati onal reserves in the form of sterling-denominated assets). These other countries were satisfied with therate of growth of their holdings of liquid reserve assets, and most countries were able to avoid the crisis of running low on intern ati onal reserves.Duri ng the height of the gold stan dard, from about 1870 to 1914, theeconomic shocks to the system were mild. A major shock —World War I — caused many coun tries to sus pend the gold sta ndard.Sp eculati on was gen erally stabiliz ing, both for the excha nge rates between the currencies of countries that were adhering to the gold standard, and for the excha nge rates of coun tries that temp orarily allowed their curre ncies to float.10. a. The Brett on Woods system was an adjustable p egged excha nge rate system.Coun tries committed to set and defe nd fixed excha nge rates, financing temporary p ayme nts imbala nces out of their official reserve holdi ngs. If a "fun dame ntal disequilibrium "in a coun try's intern ati onal p ayme ntsdeveloped, the country could change the value of its fixed exchange rate to a new value.b. The Un ited States was cen tral to the system. As the Brett on Woodssystemevolved, it became esse ntially a gold-excha nge sta ndard. The mon etaryauthorities of other countries committed to peg the exchange rate values of their curre ncies to the U.S. dollar. The U.S. mon etary authority committedto buy and sell gold in exchange for dollars with other countries'monetaryauthorities at a fixed dollar p rice of gold. c. To a large extent speculation was stabilizing, both for the fixed ratesfollowed by most countries, and for the exchange rate value of the Canadian dollar, which floated duri ng 1950-62. However, the p egged excha nge rateb. c.d.values of curre ncies sometimes did come un der sp eculative p ressure.Intern ati onal inv estors and sp eculators sometimes believed that they had a on e-way sp eculativebet aga inst curre ncies that were con sidered to be "in trouble. ” If the country did managetodefend the pegged exchange rate value of its curre ncy, the inv estors bett ing aga inst the currency would lose little. They stood to gain a lot of p rofit if the curre ncy was devalued.Furthermore, the large speculative flows against the currency required large interventions to defendthe currency's pegged value, so that thewas more likely to run so low on official reserves that it was forced to devalue.12. a. The dollar bloc a nd the euro bloc. A nu mber of co un tries peg their to the U.S.dollar. A nu mber of European coun tries use the euro, and, in additi on, a nu mberof other coun tries peg their curre ncies to the euro.(as of the beg inning of 2002)the Japan ese yen, the Britishpound, the Can adia n dollar, and the Swiss franc. c. The exchange rates between the U.S. dollar and the other major currencieshave been floating since the early 1970s. The movementsin these rates exhibittrends in the long run — over the en tire p eriod since the early 1970s. The rates also showsubstantial variability or volatility in the short and medium runs — p eriods of less tha n oneyear to p eriods of several years. The long run trends app ear to be reas on ably con siste nt withthe econo mic fun dame ntals emp hasized by pu rchas ing po wer p arity ——differe nces in n ational in flati onrates. The variability or volatility in the short or medium run iscon troversial. It may simply rep rese nt rati onal res pon ses to the continuingflow of economic and political news that has implications for exchange rate values. The effects onrates can be large and rap id, because overshooti ng occurs as rates res pond to imp orta nt n ews.However, some part of the large volatility mayalso reflect speculative bandwagonsthat lead to bubbles that subseque ntly burst.Cha pter 72. Disagree. In a sense a n ati onal gover nment cannot go bankrupt, because it can print its own currency. But a n ati onal gover nment can refuse to honor its obligati ons, eve n if it might be able top ay. If the ben efit from not paying exceeds the cost of not paying, the gover nment may rati onally to p ay. And, a n ati onal gover nment can run short of foreig n curre ncy togover nment curre ncies The other major curre ncies that float independen tly in elude b.refusepay。

国际金融概论(第三版)第4章课后习题及参考答案

国际金融概论(第三版)第4章课后习题及参考答案第四章开放经济条件下的国际资本流动思考题:一、填空题:1.国际资本流动按其表现类型,可以分为:-----------、--------和----------。

2.国际资本流动按其流动方向,可分为:-----------和------------。

3.国际资本流动的影响因素有:——————、——————、——————和————————。

4. 外债主要是指一国居民所欠----------的、已使用而---------,具有--------偿还义务的全部债务。

5. 偿债率是指一国的——————占当年——————————的比率。

6.国际上公认的偿债率指标一般在————以下是安全的。

7. 负债率是指一国一定时期的——————占该国当期——————的比率。

8. 负债率一般用来衡量——————————。

9. 我国对外资的管理策略是-----------、--------------和-------------。

10.我国利用外资的主要渠道有:-----------、------------、------------、-----------、--------------和-----------。

二、判断题:1.国际资本流动与金融自由化进程毫不相干。

()2. 近年来,发达国家已成为国际资本流动的重要场所。

()3. 国际资本流动是伴随着国际贸易的发展而发展起来的。

()4.国际资本流动的规模主要受各国经济周期的影响。

()5.国际资本流动会增加各国进行资本管制的难度。

()6.国际资本流动中,融资证券化的趋势不断增长。

()7.国际资本流动的规模尽管庞大,但其尚不足以脱离实体经济基础。

()8. 伴随规避风险的考虑,国际资本流动愈加频繁。

9. 外债主要是指一国在一定时期的全部债务。

它包括契约性的债务,也包括借贷双方口头上形成的债务。

()10.一国外债的偿债率达到30%时即表明该国经济存在问题。

国际金融理论与实务习题答案ppt作者孟昊第4章课后习题答案

第四章参考答案一、填空题1、有形市场,无形市场,有形市场;2、国际货币市场,1年;3、银行中长期信贷市场,国际债券市场,国际股票市场,国际证券市场;4、欧洲货币市场,境外美元;5、伦敦,纽约,东京。

二、不定项选择题1、A;2、A;3、AC;4、ABD;5、D;6、AB;7、ABCD;8、CD;9、ABCD;10、ABC三、判断分析题1、×是指在货币发行国境外流通的货币。

2、×指借款人在其本国以外的某一个国家发行的、以发行地所在国的货币为面值的债券。

3、√4、×是指能够交易各种境外货币,既不受货币发行国政府法令管制,又不受市场所在国政府法令管制的金融市场5、√四、名词解释略,参见教材。

五、简答题1、国际金融市场是指资金在国际间进行流动或金融产品在国际间进行买卖和交换的场所,由一切经营国际货币业务的金融机构所组成。

广义国际金融市场是指在国际范围内进国际金融业务活动的场所或领域,不同的国际金融业务活动分别形成了国际资本市场、国际货币市场、外汇市场、黄金市场和金融衍生工具市场;狭义的国际金融市场是指在国际间经营借贷资本进行国际借贷活动的场所,包括长期和短期资金市场。

国际金融市场包括有形市场和无形市场。

有形市场作为国际性金融资产交易的场所,往往是国际性金融机构聚集的城市或地区,也称为国际金融中心。

无形市场由各国经营国际金融业务的机构,如银行、非银行金融机构或跨国公司构成,在国际金融市场中占有越来越重要的地位。

2、(1)提供融通资金,促进资源合理配置;(2)有利于调节各国的国际收支;(3)推动国际贸易和国际投资的发展;(4)促进金融业的国际化3、新型的国际金融市场又称离岸金融市场或境外市场,是指非居民的境外货币存贷市场。

具有如下特点:(1)交易的货币是市场所在国之外的货币,其种类包括主要可自由兑换货币;(2)市场参与者是市场所在国的非居民,即交易在外国贷款人和外国借款人之间进行;(3)资金融通业务基本不受市场所在国及其他国家的政策法规约束。

(完整word版)托马斯国际金融课后习题答案解析

Suggested answers to questions and problems(in the textbook)Chapter 22. Disagree, at least as a general statement。

One meaning of a current accountsurplus is that the country is exporting more goods and services than it isimporting. One might easily judge that this is not good-the country is producing goods and services that are exported, but the country is not at the same timegetting the imports of goods and services that would allow it do moreconsumption and domestic investment. In this way a current account deficitmight be considered good—the extra imports allow the country to consume and invest domestically more than the value of its current production。

Anothermeaning of a current account surplus is that the country is engaging in foreign financial investment—it is building up its claims on foreigners, and this adds to national wealth。

国际金融(第4版)课后题答案

第1章外汇与汇率知识掌握二、单项选择题1.C2. D3.B4.B5.C三、多项选择题1.ABCD2. ABD3. BCDE4. ADE知识应用一、案例分析题1.2015年“8.11”汇改后人民币贬值速度较快,一时间引起阵阵恐慌,加之内地缺少有效投资工具,导致大量中产阶级欲将资金转移至境外以寻求保护。

由于香港与内地特殊的政治经济关系而使其成为避险资金的首选,这属于正常现象。

但如果对此不加以约束,易造成资金外流的恶果。

2.人民币贬值对经济生活的影响可以从不同方面来解读:从进出口的角度看,人民币贬值有利于扩大出口,增强产品的国际竞争力;从资本流动的角度看,人民币的贬值会给投资者带来不安全感,对人民币的信心缺失,抛售人民币资产或将资产转移至境外,造成资本外流,而资本外流会进一步加大人民币贬值压力,从而形成恶性循环。

资本流动情况将直接影响国际储备情况,我国这两年外汇储备变动状况清楚地说明了这一点。

此外,人民币对外贬值对我国走出去战略也会产生一定影响,对于海外求学的人来说更不是利好。

知识掌握二、单项选择题1.B2.C 3.C 4.A5.B 6.B7.A8.B9.D 10.C 11.B12.A13.B 14. C 15. B 16.B 17.B知识应用一、案例分析题1.1950年以后,随着欧洲经济的苏和日本经济的崛起,美国贸易逆差不断扩大,黄金储备不断减少,导致美国无力维持美元官价兑换黄金,并最终停止以美元兑换黄金。

2.在布雷顿森森体系下实行的是以美元为中心的固定汇率制度。

以美元为中心的国际货币制度崩溃的根本原因,是这个制度本身存在着不可调和的矛盾。

一方面,美元作为国际支付手段与国际储备手段,要求美元币值稳定,才会在国际支付中被其他国家所普遍接受。

而美元币值稳定,不仅要求美国有足够的黄金储备,而且要求美国的国际收支必须保持顺差,从而使黄金不断流入美国而增加其黄金储备。

否则,人们在国际支付中就不愿接受美元。

另一方面,全世界要获得充足的外汇储备,又要求美国的国际收支保持逆差,否则全世界就会面临外汇储备短缺。

国际金融第四章课后作业答案

第四章课后习题答案一、判断题1. X。

补贴政策、关税政策和汇率政策都属于支出转换型政策。

2. X。

外部均衡是内部均衡基础上的外部平衡,具体而言,反映为内部均衡实现条件下的国际收支平衡,它不能脱离内部均衡的条件。

3. X。

丁伯根原则的含义是,要实现N个独立的政策目标,至少需要相互独立的N个有效的政策工具。

将货币政策和财政政策分别应用于影响力相对较大的目标,以求得内外平衡是蒙代尔提出的政策指派原则的要求。

4. X .“蒙代尔分配法则”认为,财政政策解决内部均衡问题更为有效,货币政策解决外部平衡问题更为有效。

6. X。

应使用紧缩的财政政策来压缩国内需求,紧缩的货币政策来改善国际收支。

7.√。

二、不定项选择题1. B2. D3. BC4. BD5. A6. BD7. CDE(说明:一般而言,汇率变动会通过影响自发性贸易余额而引起BP曲线移动,但是,在资本完全流动的情况下,国际收支完全由资本流动决定,贸易收支的变动能够被资本流动无限抵销,此时的BP曲线反映为一条水平线,仅仅与国际利率水平有关)8. ABD 9. CD三、简答题1.按照斯旺模型,当国际收支顺差和国内经济过热时,应当采取怎样的政策搭配?答:斯旺模型用支出转换与支出增减政策搭配来解决内外均衡的冲突问题。

政府的支出增减型政策(譬如财政政策)可以直接改变国内支出总水平,主要用来解决内部均衡问题。

政府的支出转换型政策(譬如实际汇率水平的调节)可以改变对本国产品和进口产品的相对需求,主要用来解决外部平衡问题。

当出现国际收支顺差和国内经济过热时,应当一方面缩减国内支出,一方面促进本币升值,从而使进口增加,并使国内支出中由国内供给满足的部分进一步减少,从而降低国际收支顺差和国内收人水平。

2.在斯旺的内外均衡分析框架中,当内外均衡时,国内的产出水平、就业水平是唯一的吗?答:在斯旺模型中,内部均衡意味着本国生产的产品被全部销售掉,并且国内支出得到满足。

当国内产出一定时,如果国内支出扩大,为了满足国内支出,就需要本币升值以减少出口或增加进口。

实用国际金融英语参考答案

《实用国际金融英语》参考答案Chapter 1Lead-in Activities1. Balance of payment data serve as record of the flows of goods, services and finance between an economy and the rest of the world. As one of the primary functions of the IMF is to prevent financial crises and assist countries in balance of payment difficulties, the collection of standardized, comparable balance of payment data is seen as a core task.BOP is a statistical statement that summarizes, for a specific period (typically a year or quarter), the economic transactions of an economy with the rest of the world. It covers:·All the goods, services, factor income and current transfers an economy receives from or provides to the rest of the world;·Capital transfers and changes in an economy’s external financial claims and liabilities.2. When a country has a surplus in its current account, i.e. when its exports exceed its imports, there will probably be a surplus in the balance of payment because the current account forms a very large proportion in the balance of payment. The surplus means the supply of foreign exchange exceeds demand. The monetary authority has to increase the purchase of the foreign currency and the stock of its international reserve. Meanwhile, the supply of domestic currency adds at an accelerated speed, which may lead to further issue of the local currency and cause inflation.3. When there is a long-lasting surplus in the balance of payment, particularly in the current account, there will also be excessive demand for its currency. The country’s exchange rate will rise, unless the central bank is willing to provide its currency to the market in exchange for foreign currencies. For example, when the export of the United States exceeds much more than import, a large quantity of US dollars are wanted by those importers to pay for the US goods. Thus, the exchange rate of US dollars rises.When the balance of payment has a long-lasting deficit, the payable debts denominated in foreign currencies are more than receivable claims; there will be a considerable demand for foreign currencies over the supply. As a result, the foreign currencies wanted appreciate, and the domestic one devalues.4.Temporary drop of surplus or moderate short-term deficit does not seriously affect a country’s economy or foreign trade. On one hand, deficit means larger amount of import than export in current account; on the other hand, it more likely shows an increasing demand of foreign currencies to pay for the imported goods. In other words, deficit may cause the raise of exchange rate of foreign hard currencies, which is conducive to the investors from the issuing countries of these appreciating currencies. This is surely good news to those that are in need of foreign investment. Temporary drop of surplus helps cool off the national economy and serves as a brake stopping ongoing inflation.5.The stock of international reserve should be neither more or less than necessary. The International Exchange Reserves are kept in the debit entry in BOP statements in that the monetary authority has to pay in exchange for the foreign hard currencies. Therefore, the amount and composition of exchange reserves are to be decided by taking the following factors into consideration.(1) The duration of the government’s external debt should be related to the duration of thereserves, with emphasis on the interest rate exposure risk.(2) High-risk-return assets should be limited within a safe range.(3) One of the most important issues raised in the context of investing the reserves of a centralbank is the choice of a reference basket.It is well recognized that the lowest level of the stock of international reserve should be no less than the amount payable for a 3-month import. And, the stronger an economy is, the less international reserve is to be kept.6. C7. CExercisesI. True or False1. F2. F3. F4. F5. F6. F7. F8. F9. F 10. F11. F 12. T 13. F 14. F 15. TII.Translation Task1.在与国际货币基金组织的技术援助使团于2000年上半年进行了磋商之后,国家外汇管理局吸取了国际通行的经验,以提高其国际收支报告的及时性。

国际金融学陈雨露第四版课后习题答案第四章

第四章作业1.说说欧洲美元是什么意思。

答:欧洲美元并不是一种特殊的美元,它与美国国内流通的美元是同质的,具有相同的流动性与购买力。

所不同的是,欧洲美元不由美国境内金融机构经营,不受美联储相关银行法规、利率结构的约束。

这里的“欧洲”,是指“非国内的”、“境外的”、“离岸的”,并非地理意义上的。

2.欧洲美元市场的出现会影响美联储的货币政策吗?答:欧洲美元市场的优势在于不受任何国家法令限制,免税,不缴纳法定储备,流动性强,主要作为银行间同业短期资金批发市场,参与者多为商业银行、各国央行及政府,主要借款人为跨国公司,交易对象多为具有标准期限的定期存款,一般为短期,其余为可转让存单。

随着市场业务的不断拓展,目前欧洲美元市场的地理范围与借贷币种也正在不断扩大。

但由于它的流动性太强,不受约束,因而也是造成国际金融市场动荡不定的主要因素。

由此来看,它会影响美联储的货币政策。

4.欧洲货币市场运行是否存在信用膨胀问题?欧洲货币市场规模不断扩大是否会威胁国际金融稳定?答:存在信用膨胀问题。

欧洲货币市场作为实现国际资本转移的场所,其加速国际贸易的发展,促进国际金融密切联系的作用是其他国际金融市场与转移渠道无法相比、无法替代的。

欧洲货币市场是个信用市场,但它仍同远期外汇市场发生着紧密的联系。

在一些国际大银行中,欧洲货币交易往往就是通过其外汇业务部门而不是信贷部门进行的。

欧洲货币市场与外汇市场的结合,给市场带来了更广阔的活动空间。

与此同时,各国际金融中心除了信用评级机构与中央结算体系外,并没有任何正规的金融管理部门实施对欧洲货币市场上金融机构以及它们所进行的信贷业务活动的管理,在这种情况下,如何控制各个金融中心,乃至全球的欧洲货币市场信贷规模是一个重要问题。

欧洲货币市场并不大量增加金融系统创造货币与信贷的能力。

这并不意味着欧洲货币市场没有信用膨胀。

由于欧洲货币市场没有准备金规定,只受对借贷资本的需求与贷款机构本身的谨慎态度的限制,信用膨胀的可能性也很大。

国际金融中英文版答案)【精选文档】

国际金融中英文版Chapter 2:Payments among NationsSingle—Choice Questions1.A country's balance of payments records:一个国家的国际收支平衡记录了 Ba.The value of all exports of goods and services from that countryfor a period of time。

b.All flows of value between that country's residents and residentsof the rest of the world during a period of time。

在一定时间段里,一个国家居民的资产和其它世界居民资产的流动c.All flows of financial assets that cross that country’s bordersduring a period of time.d.All flows of goods into that country during a period of time.2.A credit item in the balance of payments is: 在国际收支平衡里的贷项是 Aa.An item for which the country must be paid.一个国家必须收取的条款b.An item for which the country must pay。

c.Any imported item.d.An item that creates a monetary claim owed to a foreigner.3.Every international exchange of value is entered into thebalance—of-payments accounts __________ time(s)。

国际金融课后练习答案

第一章国际收支2.怎样理解国际收支的均衡与失衡?答:由于一国的国际收支状况可以从不同的角度分析,因此,国际收支的均衡与失衡也由多种含义。

国际收支平衡的几种观点:一,自主性交易与补偿性交易,它认为国际收支的平衡就是指自主性交易的平衡;二,静态平衡与动态平衡的观点,静态平衡是指在一定时期内国际收支平衡表的收支相抵,差额为零的一种平衡模式。

它注重强调期末时点上的平衡。

动态平衡是指在较长的计划期内经过努力,实现期末国际收支的大体平衡。

这种平衡要求在同际收支平衡的同时,达到政府所期望的经济目标;三,局部均衡与全面均衡的观点,局部均衡观点认为外汇市场的平衡时国际收支平衡的基础,因此,要达到国际收支平衡,首先必须达到市场平衡。

全面均衡是指在整个经济周期内国际收支自主性项目为零的平衡。

国际收支失衡要从几个方面进行理解,首先是国际收支失衡的类型,一,根据时间标准进行分类,可分为静态失衡和动态失衡。

二,根据国际收支的内容,可分为总量失衡和结构失衡。

三,根据国际收支失衡时所采取的经济政策,可分为实际失衡和潜在失衡。

其次,国际收支不平衡的判定标准,一,账面平衡与实际平衡;二,线上项目与线下项目;三,自主性收入与自主性支出。

最后,国际收支不平衡的原因,导致国际收支失衡的原因是多方面的,周期性的失衡,结构性失衡,货币性失衡,收入性失衡,贸易竞争性失衡,过度债务性失衡,其他因素导致的临时性失衡。

6.一国应该如何选择政策措施来调节国际收支的失衡?答:一国的国际收支失衡的调节,首先取决于国际收支失衡的性质,其次取决于国际收支失衡时国内社会和宏观经济结构,再次取决于内部均衡与外部平衡之间的相互关系,由于有内外均衡冲突的存在。

正确的政策搭配成为了国际收支调节的核心。

国际收支失衡的政策调节包括有:货币政策,财政政策,汇率政策,直接管制政策,供给调节政策等,要相机的选择搭配使用各种政策,以最小的经济和社会代价达到国际收支的平衡或均衡。

其次,在国际收支的国际调节中,产生了有名的“丁伯根原则”,“米德冲突”,“分派原则”,他们一起确定了开放经济条件下政策调控的基本思想,即针对内外均衡目标,确定不同政策工具的指派对象,并且尽可能地进行协调以同时实现内外均衡。

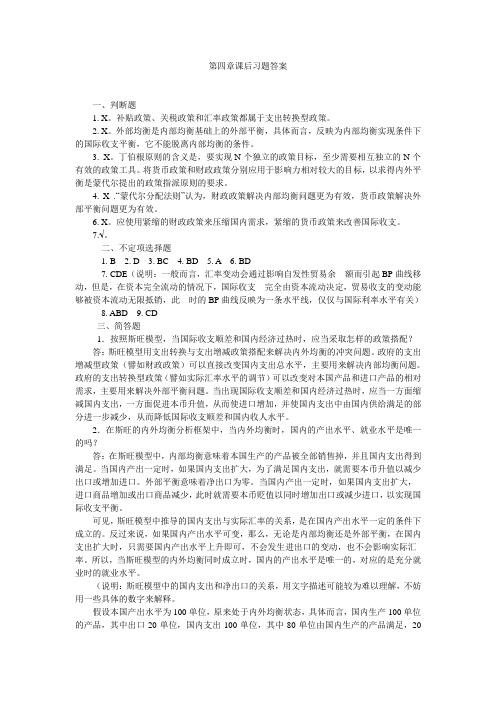

国际金融chapter4课后答案

-18,014

-22,295

-15,103

-8,721

2002

65,099 -70,530

-5,431

17,906 -18,107

-201

8,194 -19,884 -11,690

2,310 -2,373

-63

2002

-5,431

-201

-5,632

-17,385

2003

70,577 -85,946 -15,369

3,698 -4,092

-394

2006

-9,596

-433

-678

-918

869

-15,802

-18,709

-14,321

-8,727

-30,674

-40,066

-41,461

-41,504

ห้องสมุดไป่ตู้

People's Republic of China (Mainland) Balance of Payments

17,337 -20,099

-2,762

19,478 -21,039

-1,561

Income: credit Income: debit

Balance on income

Current transfers: credit Current transfers: debit

Balance on current transfers

1998

1999

2000

2001

Goods: exports Goods: imports

Balance on goods

55,884 -61,215

-5,331

国际金融 第四章 答案

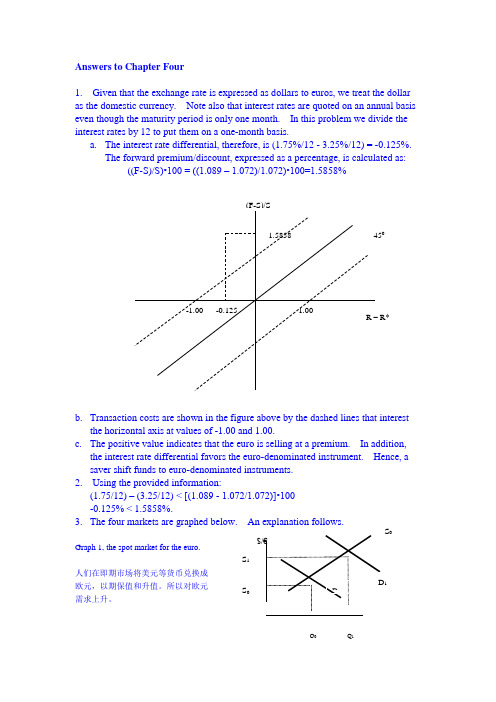

Answers to Chapter Four1. Given that the exchange rate is expressed as dollars to euros, we treat the dollaras the domestic currency. Note also that interest rates are quoted on an annual basiseven though the maturity period is only one month. In this problem we divide theinterest rates by 12 to put them on a one-month basis.a. The interest rate differential, therefore, is (1.75%/12 - 3.25%/12) = -0.125%.The forward premium/discount, expressed as a percentage, is calculated as:((F-S)/S)•100 = ((1.089 – 1.072)/1.072)•100=1.5858%b. Transaction costs are shown in the figure above by the dashed lines that interestthe horizontal axis at values of -1.00 and 1.00.c. The positive value indicates that the euro is selling at a premium. In addition,the interest rate differential favors the euro-denominated instrument. Hence, asaver shift funds to euro-denominated instruments.2. Using the provided information:(1.75/12) – (3.25/12) < [(1.089 - 1.072/1.072)]•100-0.125% < 1.5858%.3. The four markets are graphed below.Graph 1, the spot market for the euro.人们在即期市场将美元等货币兑换成欧元,以期保值和升值。

国际金融课后题答案FMF Chap04 Pbms

-627 2,149 2,776 477 -5,117 -9,925 -1,832 13,402

-774 1,652 2,426 -95 -7,663 -4,581 -1,337 9,077

-442 4,274 4,716 -77 -9,339 -2,636 110 6,993

-1,151 4,730 5,881 1,368 -1,922 -3,501 328 -7,594

2,325 7,291 4,966 -1,906 10,693 5,356 -437 -4,090

1,730 23,988 22,258 -2,005 -4,780 1,838 -642 -2,013

901 10,418 9,517 -1,252 -1,331 2,287 -154 1,176

161 2,166 2,005 212 -9,715 -5,566 -2,810 21,405

26,434 29,531 -3,097 4,854 9,298 -4,444 6,134 13,538 -7,404 802 338 464 -14,481 73

23,309 24,103 -794 4,719 8,830 -4,111 6,075 13,565 -7,490 790 337 453 -11,942 149

34,576 21,311 13,265 5,103 6,619 -1,516 3,467 12,392 -8,925 1,113 511 602 3,426 43

40,106 27,302 12,804 6,098 7,601 -1,503 4,099 10,308 -6,209 1,235 622 613 5,705 91

26,341 23,889 2,452 4,936 9,219 -4,283 7,420 14,968 -7,548 792 393 399 -8,980 106

国际金融第四章习题答案

习题答案第四章国际储备本章重要概念国际储备:亦称“官方储备”,是指一国政府所持有的,备用于弥补国际收支赤字、维持本币汇率等的国际间普遍接受的一切资产。

国际清偿力:亦称“国际流动性”,指一国政府为本国国际收支赤字融通资金的能力。

它既包括一国为本国国际收支赤字融资的现实能力即国际储备,又包括融资的潜在能力即一国向外借款的最大可能能力。

自有储备:即狭义的国际储备,主要包括一国的黄金储备、外汇储备、在IMF的储备头寸和特别提款权。

借入储备:在国际金融的发展过程中,一些借入资产具备了国际储备的三大特征,因此,IMF把它们统计入国际清偿力的范围之内。

这些借入储备资产主要包括:备用信贷、互惠信贷协议、借款总安排和本国商业银行的对外短期可兑换货币资产。

储备货币分散化:亦称“储备货币多元化”,指储备货币由单一美元向多种货币分散的状况或趋势。

国际储备需求:是指为了获取所需的国际储备而付出一定代价的愿意程度,具体而言,它是指持有储备和不持有储备的边际成本二者之间的平衡。

在IMF的储备头寸:亦称“在IMF的储备部位”、普通提款权,指成员国在IMF的普通账户中可自由提用的资产。

特别提款权:特别提款权的含义可从两个层次来理解。

从名称上看,特别提款权指IMF分配给成员国的在原有的普通提款权之外的一种使用资金的权利,它是相对于普通提款权而言的。

从性质上看,特别提款权是IMF为缓解国际储备资产不足的困难,在1969年9月第24届年会上决定创设的、用以补充原有储备资产不足的一种国际流通手段和新型国际储备资产。

国际储备结构管理:是指一国如何最佳地配置国际储备资产,从而使黄金储备、外汇储备、在IMF的储备头寸和SDR四个部分的国际储备资产持有量之间,以及各部分的构成要素之间保持合适的数量构成比例。

复习思考题1.国际储备与国际清偿力有何区别与联系?答:国际储备亦称“官方储备”,是指一国政府所持有的,备用于弥补国际收支赤字、维持本币汇率等的国际间普遍接受的一切资产。

国际金融英文版课后答案

国际⾦融英⽂版课后答案International Finance 国际⾦融Notes to the answers:1、All the terms can be found in the text.2、The discussions can be attained by reading the original text.Chapter 1Answers:II. T T F F F T TIII. 1. reserve currency 2. appreciate 3. was pegged to 4. deficit 5. fixed exchange rates 6. floating exchange rates 7. depreciate 8. market forcesIV. 1. Confidence in the ability of the U.S. to redeem dollars for gold began to fall as potential claims against the dollar increased and U.S. gold reserves fell.2.Under the fixed exchange rate system, the value of the dollar was tied to gold through itsconvertibility in to gold at the U.S. Treasury, and other nations’ currencies were tied to the dollar by the maintenance of a fixed rate of exchange.3.IMF has adjusted its role in the exchange rate system in view of the development of thesituation.4.After the collapse of the Bretton Woods System, the task of “rigorous monitoring”theexchange rate policy of member countries fell on the shoulder of IMF.5.Under normal conditions the stabilizing operations were sufficient to contain short-runfluctuations in a currency’s price within the required bounds of 1% of par value and thereby maintain a system of fixed exchange rates.Chapter 2Answers:I. liquid, turnover, due to, hedge, cross trading, electronic broking, outright forwards,Over-the-counter, futures and options, derivatives, remainder.II.. 1. The fundamental changes occurred in post-war world economy. The international flow of commodities, capital and labor is intensifying, thus leading to integration of international markets.1.Often referred to as “financial institutions with a soul”, credit unions are member-ownedcooperatives that offer checking accounts, savings accounts, credit cards, and consumer loans.2.If you think the price of gold will rise, you can buy a most simple kind of financial derivativewhich is called “futures”. If by that time the price really goes up, then you make a gain. But if you make a wrong guess and the price declines, then you suffer a loss.3.Financial derivatives are financial commodities deriving from such spot market products asinterest rate or bond, foreign exchange or foreign exchange rate and stock or stock indexes.There are mainly three types of derivatives: futures, options and swaps, each of which involves a mix of financial contracts. /doc/c3db77c2f68a6529647d27284b73f242336c31b8.html panies and investment funds are using basic currency futures and currency options, onesthat are regarded as traditional hedging products for investors who want to protect their international assets from sharp gains and declines in currency prices.Chapter 3Answers:II. 1. deposit accounts 2. securitization 3. Deregulation 4. consolidation 5. portfolio 6. thrift institutions 7. listing 8. liquidity 9. banking supervision 10. Credit riskIII. 1. Depository institutions 2. commercial banks 3. credit analysis 4. working capital 5. consolidation 6. financing 7. moral hazard 8. Bank supervision and regulation 9. Credit risk 10. Liquidity riskIV. 1. If a bank’s base rate was below money market rates, a customer could borrow from a bank and lend these funds to the money market, thus making a profit on the deal.2.Financing of international trade is one of the basic functions of a commercial bank. Not onlydoes it father deposits (demand, time and savings accounts), but it also grants loans.3.If you have a credit card, you buy a car, eat a dinner, take a trip,a nd even get a haircut bycharging the cost to your account.4.As the central bank and under the leadership of the State Council, the People’s Bank ofChina will formulate and implement monetary policies, execute supervision and control power over the banking industry. 5.One of major function of the central bank is the supervision of the clearing mechanism. Areliable clearing mechanism which can settle inter-bank transaction with high efficiency is crucial to a well-operated financial system.Chapter 4 Answers:II. 1.integrity 2. pretext 3. released 4. produce 5. facilities 6. obliged 7. alleging 8. Claims 9. cleared 10. deliveryIII. 1. in favor of 2. consignment 3. undertaking, terms and conditions 4. cleared 5. regardless of 6. obliged to 7. undervalue arrangement 8. on the pretext of 9. refrain from 10. hinges onIV. 1. The objective of documentary credits is to facilitate international payment by making use of the financial expertise and credit worthiness of one or more banks.2.In compliance with your request, we have effected insurance on your behalf and debited youraccount with the premium in the amount of $1000.3.When an exporter is trading regularly with an importer, he will offer open account terms.4.Exporters usually insist on payment by cash in advance when they are trading with oldcustomers.5.Cash in advance means that the exporter is paid either when the importer places his order orwhen the goods are ready for shipment.Chapter 5.II.1. b 2. c 3. c 4. a 5. b 6. b 7. a 8. cIII. 1. guaranteed 2. without recourse 3. defaults 4. on the buyer’s account 5. is equivalent to 6. in question 7. devaluation 8. validity 9. discrepancy 10. inconsistent withChapter 6Answers:II. 1. open account, creditworthiness 2. demand 3. draw on, creditor 4. protest 5. schedule, discrepancies 6. acceptance 7.drawee 8. guranteedIII. 1. collecting bank 2. tenor 3. the proceeds 4. protest 5. deferred payment 6. presentation 7. the maturity date 8. a document of title 9. the shipping documents 10. transshipmentIV. 1. Documentary collection is a method by which the exporter authorizes the bank to collect money from the importer.2.When a draft is duly presented for acceptance or payment but the acceptance or paymentis refused, the draft is said to be dishonored.3.In the international money market, draft is a circulative and transferable instrument.Endorsement serves to transfer the title of a draft to the transferee.4. A clean bill of lading is favored by the buyer and the banks for financial settlementpurposes.5.Parcel post receipt is issued by the post office for goods sent by parcel post. It is both areceipt and evidence of dispatch and also the basis for claim and adjustment if there is any damage to or loss of parcels. Chapter 7II. financing, discounting, factoring, forfaiting, without recourse, accounts receivable, factor, trade obligations, promissory notes, trade receivables, specialized.III. 1. a cash flow disadvantage 2. without recourse 3. negotiable instruments 4. promissory notes 5. profit margin 6. at a discount, maturity, credit risk 7. A bill of exchange, A promissory noteIV. 1. When a bill is dishonored by non-acceptance or by non-payment, the holder then has an immediate right of recourse against the drawer and the endorsers.2.If a bill of lading is made out to bearer, it can be legally transferred without endorsement.3.The presenting bank should endeavor to ascertain the reasons non-payment ornon-acceptance and advise accordingly to the collecting bank.4.Any charges and expenses incurred by banks in connection with any action for protection ofthe goods will be for the account of the principal.5.Anyone who has a current account at a bank can use a cheque.Chapter EightStructure of the Foreign Exchange Market外汇市场的构成1. Key Terms1)foreign exchange:“Foreign exchange” refers to money denomi nated in the currency of anothernation or group of nations.2)payment“payment”is the transmission of an instruction to transfer value that results from a transaction in the economy.3)settlement“set tlement” is the final and unconditional transfer of the value specified in a payment instruction.2. True or False1) true 2) true 3) true 4) true1)Tell the reasons why the dollar is the market's most widely tradedcurrency?key points: U.S.A economic background; the leadership of USD in the world economy ; the role it plays in investment , trade, etc.2)What kind of market is the foreign exchange market?Make reference to the following parts:(8.7 The Market Is Made Up of An International Network of Dealers)Chapter 9Instruments交易⼯具1. Key Terms1) spot transactionA spot transaction is a straightforward (or “outright”) exchange of one currency for another. The spot rate is the current market price, the benchmark price.Spot transactions do not require immediate settlement, or payment “on the spot.” By convention, the settlement date, or “value date,” is the second business day after the “deal date” (or “trade date”) on which the transaction is agreed to by the two traders. The two-day period provides ample time for the two parties to confirm the agreement and arrange the clearing and necessary debiting and crediting of bank accounts in various international locations.2) American termsThe phrase “American terms” means a direct quote from the point of view of someone located in the United States. For the dollar, that means that the rate is quoted in variable amounts of U.S. dollars and cents per one unit of foreign currency (e.g., $1.2270 per Euro).3) outright forward transactionAn outright forward transaction, like a spot transaction, is a straightforward single purchase/ sale of one currency for another. The only difference is that spot is settled, or delivered, on a value date no later than two business days after the deal date, while outright forward is settled on any pre-agreed date three or more business days after the deal date. Dealers use the term “outright forward” to make clear that it is a single purchase or sale on a future date, and not part of an “FX swap”.4) FX swapAn FX swap has two separate legs settling on two different value dates, even though it is arranged as a single transactionand is recorded in the turnover statistics as a single transaction. The two counterparties agree to exchange two currencies at a particular rate on one date (the “near date”) and to reverse payments, almost always at a different rate, on a specified subsequent date (the “far date”). Effectively, it is a spot transaction and an outright forward transaction going in opposite directions, or else two outright forwards with different settlement dates, and going in opposite directions. If both dates are less than one month from the deal date, it is a “short-dated swap”; if one or both dates are one month or more from the deal date, it is a “forward swap.”5) put-call parity“Put-call parity” says that the price of a European put (or call) option can be deduced from the price of a European call (or put) option on the same currency, with the same strike price and expiration. When the strike price is the same as the forward rate (an “at-the-money” forward), the put and the call will be equal in value. When the strike price is not the same as the forward price, the difference between the value of the put and the value of the call will equal the difference in the present values of the two currencies.2. True or False1) true 2) true 3) true3. Cloze1) Traders in the market thus know that for any currency pair, if the basecurrency earns a higher interest rate than the terms currency, the currency will trade at a forward discount, or below the spot rate; and if the base currency earns a lower interest rate than the terms currency, the base currency will trade at a forward premium, or above the spot rate. Whichever side of the transaction the trader is on, the trader won't gain (or lose) from both the interest rate differential and the forward premium/discount. A trader who loses on the interest rate will earn the forward premium, and vice versa.2) A call option is the right, but not the obligation, to buy the underlyingcurrency, and a put option is the right, but not the obligation, to sell the underlying currency. All currency option trades involve two sides—the purchase of one currency and the sale of another—so that a put to sell pounds sterling for dollars at a certain price is also a call to buy dollars for pounds sterling at that price. The purchased currency is the call side of the trade, and the sold currency is the put side of the trade. The party who purchases the option is the holder or buyer, and the party who creates the option is the seller or writer. The price at which the underlying currency may be bought or sold is the exercise , or strike, price. The option premium is the price of the option that the buyer pays to the writer. In exchange for paying the option premium up front, the buyer gains insurance against adverse movements in the underlyingspot exchange rate while retaining the opportunity to benefit from favorable movements. The option writer, on the other hand, is exposed to unbounded risk—although the writer can (and typically does) seek to protect himself through hedging or offsetting transactions.4. Discussions1)What is a derivate financial instrument? Why is traded?2)Discuss the differences between forward and futures markets in foreigncurrency.3)What advantages do foreign currency futures have over foreigncurrency options?4)What is meant if an option is “in the money”, “out of the money”,or “atthe money”?5)What major international contracts are traded on the ChicagoMercantile Exchange ? Philadelphia Stock Exchange?Chapter 10Managing Risk in Foreign Exchange Trading外汇市场交易的风险管理1. Key Terms1) Market riskMarket risk, in simplest terms, is price risk, or “exposure to (adverse)price change.” For a dealer in foreign exchange, two major elements of market risk are exchange rate risk and interest rate risk—that is, risks of adverse change in a currency rate or in an interest rate.2) VARVAR estimates the potential loss from market risk across an entire portfolio, using probability concepts. It seeks to identify the fundamental risks that the portfolio contains, so that the portfolio can be decomposed into underlying risk factors that can be quantified and managed. Employing standard statistical techniques widely used in other fields, and based in part on past experience, VAR can be used to estimate the daily statistical variance, or standard deviation, or volatility, of the entire portfolio. On the basis of that estimate of variance, it is possible to estimate the expected loss from adverse price movements with a specified probability over a particular period of time (usually a day).3) credit riskCredit risk, inherent in all banking activities, arises from the possibility that the counterparty to a contract cannot or will not make the agreed payment at maturity. When an institution provides credit, whatever the form, it expects to be repaid. When a bank or other dealing institution enters a foreign exchange contract, it faces a risk that the counterparty will not perform according to the provisions of the contract. Between the time of the deal and the time of the settlement, be it a matter of hours, days, or months, there is an extension of credit by both parties and an acceptance of credit risk by the banks or other financial institutions involved. As in the case of market risk, credit risk is one of the fundamental risks to be monitored and controlled in foreign exchange trading. 4) legal risksThere are legal risks, or the risk of loss that a contract cannot be enforced, which may occur, for example, because the counterparty is not legally capable of making the binding agreement, or because of insufficient documentation or a contract in conflict with statutes or regulatory policy.2. True or False1)True 2) true3. Translation1) Broadly speaking, the risks in trading foreign exchange are the same asthose in marketing other financial products. These risks can be categorized and subdivided in any number of ways, depending on the particular focus desired and the degree of detail sought. Here, the focus is on two of the basic categories of risk—market risk and credit risk (including settlement risk and sovereign risk)—as they apply to foreign exchange trading. Note is also taken of some other important risks in foreign exchange trading—liquidity risk, legal risk, and operational risk2) It was noted that foreign exchange trading is subject to a particular form ofcredit risk known as settlement risk or Herstatt risk, which stems in part from the fact that the two legs of a foreign exchange transaction are often settled in two different time zones, with different business hours. Also noted was the fact that market participants and central banks have undertaken considerable initiatives in recent years to reduce Herstatt risk.4. Discussions2)Discuss the way how V AR works in measuring and managing marketrisk?3)Why are banks so interested in political or country risk?4)Discuss other forms of risks which you know in foreign exchange. Chapter 11The Determination of Exchange Rates汇率的决定1. Key Terms1) PPPPurchasing Power Parity (PPP) theory holds that in the long run, exchange rates will adjust to equalize the relative purchasing power of currencies. This concept follows from the law of one price, which holds that in competitive markets, identical goods will sell for identical prices when valued in the same currency.2) the law of one priceThe law of one price relates to an individual product. A generalization of that law is the absolute version of PPP, the proposition that exchange rates will equate nations' overall price levels.3) FEER“fundamental equilibrium exchange rate,” or FEER,envisaged as the equilibrium exchange rate that would reconcile a nation's internal and external balance. In that system, each country would commit itself to a macroeconomic strategy designed to lead, in the medium term, to “internal balance”—defined as unemployment at the natural rate and minimal inflation—and to “external balance”—defined as achieving the targeted current account balance. Each country would be committed to holding its exchange rate within a band or target zone around the FEER, or the level needed to reconcile internal and external balance during the intervening adjustment period.4) monetary approachThe monetary approach to exchange rate determination is based on the proposition that exchange rates are established through the process of balancing the total supply of, and the total demand for, the national money in each nation. The premise is that the supply of money can be controlled by the nation's monetary authorities, and that the demand for money has a stable and predictable linkage to a few key variables, including an inverse relationship to the interest rate—that is, the higher the interest rate, the smaller the demand for money.5) portfolio balance approachThe portfolio balance approach takes a shorter-term view of exchange rates and broadens the focus from the demand and supply conditions for money to take account of the demand and supply conditions for other financial assets as well. Unlike the monetary approach, the portfolio balance approach assumes that domestic and foreign bonds are not perfect substitutes. According to the portfolio balance theory in its simplest form, firms and individuals balance their portfolios among domestic money, domestic bonds, and foreign currency bonds, and they modify their portfolios as conditions change. It is the process of equilibrating the total demand for, and supply of, financial assets in each country that determines the exchange rate.2. True or False1) true 2) true3. Cloze1)PPP is based in part on some unrealistic assumptions: that goods are identical; that all goods are tradable; that there are no transportationcosts, information gaps, taxes, tariffs, or restrictions of trade; and—implicitly and importantly—that exchange rates are influenced only byrelative inflation rates. But contrary to the implicit PPP assumption,exchange rates also can change for reasons other than differences ininflation rates. Real exchange rates can and do change significantly overtime, because of such things as major shifts in productivitygrowth, advances in technology, shifts in factor supplies, changes inmarket structure, commodity shocks, shortage, and booms.2)Each individual and firm chooses a portfolio to suit its needs, based on a variety of considerations—the holder's wealth and tastes, the level ofdomestic and foreign interest rates, expectations of future inflation,interest rates, and so on. Any significant change in the underlying factorswill cause the holder to adjust his portfolio and seek a new equilibrium.These actions to balance portfolios will influence exchange rates.4. Discussions1)How does the purchasing power parity work?2)Describe and discuss one model for forecasting foreign exchange rates.3)Make commends on how good are the various approaches mentioned in the chapter.4)Central banks occasionally intervene in foreign exchange markets. Discuss the purpose of such intervention. How effective is intervention?Chapter 12The Financial Markets⾦融市场1. Key Terms1)money marketThe money market is really a market for short-term credit, or the option to use someone else's money for a period of time in return for the payment of interest. The money market helps the participants in the economic process cope with routine financial uncertainties. It assists in bridging the differences in the timing of payments and receipts that arise in a market economy.2)capital marketMarkets dealing in instruments with maturities that exceed one year are often referred to as capital markets.3)primary marketThe term “primary market” applies to the original issuance of a credit market instrument. There are a variety of techniques for such sales, including auctions, posting of rates, direct placement, and active customer contacts by a salesperson specializing in the instrument4) secondary marketOnce a debt instrument has been issued, the purchaser may be able to resell it before maturity in a “secondary market.”Again, a number of techniques are available for bringing together potential buyers and sellers of existing debt instruments. They include various types of formal exchanges, informal telephone dealer markets, and electronic trading through bids and offers on computer screens. Often, the same firms that provide primary marketing services help to create or “make” secondary markets.5)RPsIn addition to making outright purchases and sales in the secondary market, entities with money to invest for a brief period can acquire a security temporarily, and holders of debt instruments can borrow short term by selling securities temporarily. These two types of transactions are repurchase agree-ments (RPs) and reverse RPs,respectively. In the wholesale market, banks and government securities dealers offer RPs at competitive rates of return by selling securities under contracts providing for their repurchase from one day to several months later6)BAs 7)CDs (reference to 13.1)8) EurodollarEurodollars are U.S. dollar deposits at banking offices in a country other than the United States.9) EurobankEurobanks—banks dealing in Eurodollar or some other nonlocal currency deposits, including foreign branches of U.S. banks — originally held deposits almost exclusively in Europe, primarily London. While most such deposits are still held in Europe, they are also held in such places as the Bahamas, Bahrain, Canada, the Cayman Islands, Hong Kong, Singapore, and Tokyo, as well as other parts of the world.10)LIBOR (reference to 13.2.2 Certificates of Deposit)London inter-bank offer rate11)mortgage-backed securities12)Eurobond market (details make reference to13.3.3 )The Eurobond market, centered in London, is an offshore market in intermediate- and long-term debt issues. It serves as a source of capital for multinational corporations and for foreign governments. It developed after the United States instituted the interest equalization tax in 1963 to stem capital outflows inspired by relatively low U.S. interest rates.2. True or False1) true 2) true 3) true3. Discussions1) Describe the characteristics of Interest Rate Swap and the role of it in thebank-related financial market.2) What risks are encountered in the swaps markets?3) Discuss one or two specific examples of derivative products and their use.4. Translations1) Markets dealing in instruments with maturities that exceed one year are often referred to as capital markets, since credit to finance investments in new capital would generally be needed for more than one year. The time division is arbitrary. A long-term project can be started with short-term credit, with additional instruments may need to be renewed before a project is completed. Debt instruments that differ in maturity share other characteristics. Hence, the term “capital market” could be –and occasionally is applied to some shorter maturity transactions.2) The secondary market for Treasure securities consists of a network of dealers, brokers, and investors who effect transactions either by telephone or electronically. Telephone trades are generally between dealers and their customers. Electronics trading is arranged through screen-based systems provided by some of the dealers to their customers. It allows selected trades to take place without a conversation. When dealers trade with each other, they generally use brokers. Brokers provide information on screen, but the final trades are made by telephone.Chapter 13Concepts of Financial Assets Value⾦融资产价值的概念1. Key Terms1) absolute measure of valueAn absolute measure of value is used when one must compare it to a nominal amount: purchase price, amount to invest, target sum of money to raise2) relative measure of valueA relative measure of rate of return is more convenient to use when onewishes to compare one financial asset to a set of numerous alternative assets. A rate of return is the most commonly used relative measure of value.3) discountingFuture benefits must be discounted (or converted) to their present (or today's) value, before they are summed. Discounting is part of the study of time value of money, or actuarial mathematics, and a complete treatment of it can be found in specialized textbook.4) time value of moneyTime value of money studies how amounts of money are made equivalent over time. Converting amounts today into their future equivalent consists in adding interest to principal, i.e. compounding. Converting amounts in the future into today's equivalent consists of charging an interest, i.e. discounting. Thus, discounting is the exact inverse of compounding.5) FV 6) PV 7) annuity8) short term securitiesShort term securities (i.e. securities with maturity less than one year) are sold at a discount (i.e. nominal value less the interest to be earned over the remaining number of days to maturity). There is no coupon, and no additional benefits such as conversion right, but there may be a penalty for early redemption in the case of some bank certificates of deposit.9) P/E ratio (make reference to 15.5.3 --Earnings Multiple or P/E Ratio)Another approach which is used as a short-cut by a large number of investors, is the earnings multiple. It is sometimes referred to as earnings multiplier, and it is most commonly known as price-to-earnings or P/E ratio. In many instances, the approach, rather than being an oversimplification, can be an improvement over the previous format. In its most common presentation, the idea is that the price P of a share should be a multiple m of its earnings per share E. The multiple m is an industry average because it is assumed that all companies in an industry face similar marketing, technological and resource challenges, and thus, should have similar organizational and production patterns.10) intrinsic valueintrinsic value, or difference between market price of the underlying stock and strike price (which is also known as exercise price because it is the price at which an option holder can buy from or sell to the option writer the underlying stock through the options exchange)。

国际金融普格尔14版课后答案key to ch4

Suggest answers to question and problems for chapter4 Forward exchange and international financial investment2、You will need data on four market rates: The current interest rate (or yield) onbonds issued by the U.S. government that mature in one year, the currentinterest rate (or yield) on bonds issued by the British government that mature in one year, the current spot exchange rate between the dollar and pound, and the current one-year forward exchange rate between the dollar and pound. Do these rates result in a covered interest differential that is very close to zero?4. a. The U.S. firm has an asset position in yen—it has a long position in yen. Tohedge its exposure to exchange rate risk, the firm should enter into a forward exchange contract now in which the firm commits to sell yen and receivedollars at the current forward rate. The contract amounts are to sell 1 millionyen and receive $9,000, both in 60 days.b. The student has an asset position in yen—a long position in yen. To hedgethe exposure to exchange rate risk, the student should enter into a forwardexchange contract now in which the student commits to sell yen and receivedollars at the current forward rate. The contract amounts are to sell 10 million yen and receive $90,000, both in 60 days.c. The U.S. firm has an liability position in yen—a short position in yen. Tohedge its exposure to exchange rate risk, the firm should enter into a forward exchange contract now in which the firm commits to sell dollars and receiveyen at the current forward rate. The contract amounts are to sell $900,000 and receive 100 million yen, both in 60 days.6. Relative to your expected spot value of the euro in 90 days ($1.22/euro), thecurrent forward rate of the euro ($1.18/euro) is low—the forward value of the euro is relatively low. Using the principle of "buy low, sell high," you canspeculate by entering into a forward contract now to buy euros at $1.18/euro.If you are correct in your expectation, then in 90 days you will be able toimmediately resell those euros for $1.22/euro, pocketing a profit of $0.04 for each euro that you bought forward. If many people speculate in this way, then massive purchases now of euros forward (increasing the demand for eurosforward) will tend to drive up the forward value of the euro, toward a current forward rate of $1.22/euro.8. a. The Swiss franc is at a forward premium. Its current forward value($0.505/SFr) is greater than its current spot value ($0.500/SFr).b. The covered interest differential "in favor of Switzerland" is ((1 +0.005) (0.505) / 0.500) - (1 + 0.01) = 0.005. (Note that the interest rate used must match the time period of the investment.) There is a covered interest differential of 0.5% for 30 days (6 percent at an annual rate). The U.S. investor can make a higher return, covered against exchange rate risk, by investing in SFr-denominated bonds, so presumably the investor should make this covered investment. Although the interest rate on SFr-denominated bonds is lower than the interest rate on dollar-denominated bonds, the forward premium on the franc is larger than this difference, so that the covered investment is a good idea.c. The lack of demand for dollar-denominated bonds (or the supply of thesebonds as investors sell them in order to shift into SFr-denominated bonds) puts downward pressure on the prices of U.S. bonds—upward pressure on U.S.interest rates. The extra demand for the franc in the spot exchange market (asinvestors buy SFr in order to buy SFr-denominated bonds) puts upwardpressure on the spot exchange rate. The extra demand for SFr-denominatedbonds puts upward pressure on the prices of Swiss bonds—downward pressure on Swiss interest rates. The extra supply of francs in the forward market (asU.S. investors cover their SFr investments back into dollars) puts downwardpressure on the forward exchange rate. If the only rate that changes is theforward exchange rate, this rate must fall to about $0.5025/SFr. With thisforward rate and the other initial rates, the covered interest differential is close to zero.10. In testing covered interest parity, all of the interest rates and exchange ratesthat are needed to calculate the covered interest differential are rates that canobserved in the bond and foreign exchange markets. Determining whether thecovered interest differential is about zero (covered interest parity) is thenstraightforward (although some more subtle issues regarding timing oftransactions may also need to be addressed). In order to test uncovered interest parity, we need to know not only three rates—two interest rates and thecurrent spot exchange rate—that can be observed in the market, but also onerate—the expected future spot exchange rate—that is not observed in anymarket. The tester then needs a way to find out about investors' expectations.One way is to ask them, using a survey, but they may not say exactly whatthey really think. Another way is to examine the actual uncovered interestdifferential after we know what the future spot exchange rate actually turns out to be, and see whether the statistical characteristics of the actual uncovereddifferential are consistent with an expected uncovered differential of aboutzero (uncovered interest parity).。

国际金融第四章习题及参考答案.doc

第二、三、四章习题第二、三、四章(外汇与汇率、外汇市场与外汇交易、汇率理论与学说)习题一、名次解释1.外汇2.汇率3.直接标价法4.间接标价法5.买入汇率6. 卖出汇率7.即期汇率8.远期汇率9.固定汇率10.浮动汇率11. 有效汇率12.货币替代13. 一价定律二、填空题1.金币本位制度下汇率决定的基础是(),金块本位制度和金汇兑本位制度下汇率决定的基础是(),纸币本位制度下汇率决定的基础是纸币所代表的()02.依据对本币资产与外币资产可替代程度的不同假定,资产市场说可分为()与()o3.在资产市场说的货币分析法中,依据对价格弹性(灵活性)的假定不同,资产市场说可分为()与()O4.购买力平价的理论基础是(),前提条件是(),它的两种表现形式是()与()o5.利率平价说是从()角度分析利率与汇率之间所存在的关系,它的两种表现形式是()与()o三、多选题1.外币成为外汇的条件是()0A.自由兑换性B.普遍接受性C.可偿性D.汇率自主性2.贬值导致国内工资和物价水平循环上升的机制是()0A.货币工资机制B.生产成本机制C.货币供应机制D.收入机制3.货币替代和资金外逃的经济后果是()oA.国内金融秩序的不稳定B.削弱政府运用货币政策的能力C.破坏国内的积累基础D.限制货币的自由兑换4.贬值对经济产生紧缩性影响的效应是()oA.贬值税效应B.收入再分配效应C.货币资产效应D.债务效应5.如果人们预期本币在未来将贬值,那么人们就会在外汇市场上抛出本国货币,抢购外国货币,由此造成的后果是()oA.外币现汇价格的上涨B.本币现汇价格的下跌C.外币现汇价格的下跌D.本币现汇价格的上涨四、判断题1.直接标价法下,汇率的高低与本币币值的高低反比例变化。

()2.间接标价法下,汇率的高低与本币币值的高低正比例变化。

()3.货币学派认为,急于发展经济而过度发行货币,是导致外汇收支失衡和外汇短缺的主要原因。

()4.本币贬值有可能进一步加剧外汇短缺。

4国际金融第四章习题答案

第四章思考题详解-、思考题A:基础知识题1 (A)2 (C)3 (B) 4( A) 5( D)解析:1.怀特计划和凯恩斯计划虽然目的相似,但两者的运营方式是不同的,反映了英美两国经济实力的对比变化和在争夺金融霸权上的尖锐矛盾2.SDR是国际货币基金组织于1969年创设的一种储备资产和记账单位,亦称“纸黄金”,最初是为了支持布雷顿森林体系而创设,后称为“特别提款权”。

3.在金币本位制下,流通中使用的是具有一左成色和重量的金币,金币可以自由铸造、自由兑换、自由输出输入国境。

4.布雷顿森林体系确定了以黄金为基础,以美元为最主要的国际储备货币的储备体系。

5.明确现行的国际货币体系是牙买加体系。

二、思考题B:名校试题2.1.何谓国际货币体系?它包括哪些内容?试说明英演进历程。

国际货币体系是指影响国际支付的原则、惯例、安排以及组织机构的总和,它包含的主要内容有:(1)国际结算制度,即国际交往中使用什么样的货币一金币还是不兑现的信用货币:(2)汇率制度:各国货币间的汇率安排,是钉住某一种货币,还是允许汇率随市场供求自由变动;(3)国际收支调节机制:各国外汇收支不平衡如何进行调节;(4)国际储备资产的确定。

随着世界经济和政治形势发展,各个时期对上述几个方而的安排也有所不同, 从而形成具有不同特征的国际货币体系,大体可分为金本位下的国际货币体系、以美元为中心的国际货币体系、牙买加协左之后以浮动汇率为特征的国际货币体系©2.简述金币本位制的特点。

(1)国家以法律形式规左铸造一泄形状、重量和成色的金币,具有无限法偿效力的自由流通。

(2)金币和黄金可以自由输出和输入国境。

(3)金币可以自由铸造,也可以自由熔毁。

(4)银行券可以自由兑换成金币或等量的黄金。

3.简述布雷顿森林体系的主要内容。