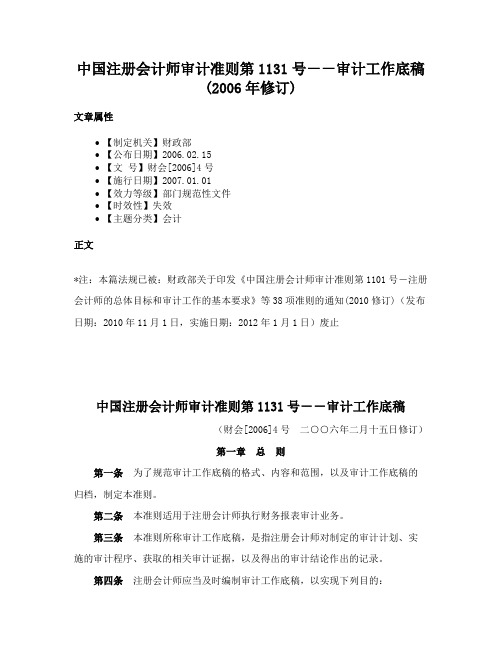

英文标准审计工作底稿

工作底稿-应付帐款

SHU LUN PAN CERTIFIED PUBLIC ACCOUNTANTS CO., LTD被审计单位: A公司审核员: 刘民日期: 2006.02.11 索引号: F3-1审查项目:应付帐款会计期间: 2005.12.31 复核员: 王一日期: 2006.02.11 页次:调整事项说明及调整分录1、(底稿见索引F3-5-1,F3-5-2),经查验,“恒贸实业公司”是A公司虚设的帐户,余额是以前年度虚列费用,隐匿的利润。

公司同意提供书面情况说明(索引号F3-5-4),并作以下审计调整。

ADJ:#1 调整本期费用借:管理费用998,918.00营业费用860,000.00贷:应付帐款—恒贸公司1,858,918,00ADJ:#2 将虚列的应付帐款转出.借:应付帐款-恒贸公司3,547,006.00贷:年初未分配利润2,376,494.02应交税金—所得税1,170,511.002、(底稿见索引F3-7),期末仓库收到“华文实业公司”200吨螺纹钢,因未收到有关单证,尚办理入帐手续,审计调整作暂估入帐处理。

螺纹钢@3250元/吨,总计金额650,000.00元。

(@3,,250元/吨* 200 吨=650,000.00元)ADJ:#3 螺纹钢料到单未到,暂估入帐借:存货-原料650,000.00贷:应付帐款—华文公司650,000.003、(底稿见索引F3-9)“三汇材料厂”期末借方余额511,192.00元是预付钢材款,应作重分类调整。

ADJ:#4 期末借方余额重分类调整。

借:预付帐款—三汇材料511,192.00贷:应付帐款—三汇材料511,192.004、(底稿见索引F3-8)”上海佳明贸易公司”同一笔采购设备款,在预收帐款和应付帐款两个科目同时挂帐。

ADJ:#5 冲销预付帐款借:应付帐款—佳明公司962,785.00贷:预付帐款—佳明公司962,785.00审计结论:期末余额审定数为9,419,623.00元,予以确认。

审计英语审计工作底稿

审计英语审计工作底稿一、考情分析从历年考试情况来看,本章在2013年考查了一道简答题。

往往和具体审计程序相联系,要注意工作底稿与监盘、函证等具体程序相联系的简答题,如分析工作底稿并纠错。

同时需要关注识别特征、审计工作底稿归档前后的变动、归档期限与保存期限等内容。

二、专业词汇审计工作底稿:Audit documentation/Audit working paper审计工作底稿的存在形式(纸质、电子介质、其他介质):The forms of audit documentation (paper, electronic, other forms)识别特征:Identification characteristics /Recognition features审计档案:Audit file归档:Filing审计工作底稿归档的期限:Filing Deadline of Audit Documentation审计工作底稿归档后的变动:The Change of Audit Documentation after Filing审计工作底稿的保存期限:Storage Life of Audit Documentation函证:Confirmation监盘:Supervision of inventory count三、重点、难点讲解Ⅰ.审计工作底稿的性质Ⅰ.The nature of audit documentation(一)审计工作底稿的存在形式存在形式:纸质电子介质其他介质电子或其他介质形式的应可以通过打印等方式,转换成纸质形式的审计工作底稿,并与其他纸质形式的审计工作底稿一并归档,同时,单独保存这些以电子或其他介质形式存在的审计工作底稿。

(一)The forms of audit documentationExistence form: paper, electronic, other formsElectronic and other forms can be converted into paper audit documentation by printing, and filed with other paper documentation, meanwhile, save those electronic and other forms of documentation separately.事务所对底稿的控制的目的:1.使审计工作底稿清晰地显示其生成、修改及复核的时间和人员;2.在审计业务的所有阶段,尤其是在项目组成员共享信息或通过互联网将信息传递给其他人员时,保护信息的完整性和安全性;3.防止未经授权改动审计工作底稿;4.允许项目组和其他经授权的人员为适当履行职责而接触审计工作底稿。

审计报告材料英文版(全).docx

AUDITOR ’ S REPORTYue Hua Shen / Yan Zi (2014)No.0002ICPA filing number: 020201401000420To all shareholders of ****** Co., Ltd:We have audited the accompanying financial statements of ****** Co.,Ltd (“ Your Company ” ), which comprise the balance sheet as of31 December 2013, the income statement,statement of changes in owner'sequity and cash flow statement for the year then ended, and notes to thefinancial statements.I. Management’ s responsibility for the financial statementsManagement of your Company is responsible for the preparation and fair presentation of financial statements. This responsibility includes: (1)in accordance with the Accounting Standards for Business Enterprises and its relevant provisions, preparing the financial statements andreflecting fair presentation; (2) designing, implementing and maintainingthe necessary internal control in order to free financial statements frommaterial misstatement, whether due to fraud or error.II. Auditors' responsibilityOur responsibility is to express an opinion on these financialstatements based on our audit. We conducted our audit in accordancewith Chinese Certified Public Accountants Auditing Standards.Those standards require that we comply with ethical requirements and plan andperform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements.The procedures selected depend on the auditors'judgment, including the assessment of the risks of material misstatement of the financial statements,whether due to fraud or error.In making those risk assessments, we consider the internal control relevant to the preparationand fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances,but not for the purpose of expressing an opinion on the effectiveness of the internal control.An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management,as well as evaluating the overall presentation of the financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.III.OpinionIn our opinion, the financial statements of your Company have beenprepared in accordance with the Accounting Standards for BusinessEnterprise and its relevant provisions in all material respect, and presentfairly the financial position of your Company as of 31 December 2013,and the results of its operations and cash flows for the year then ended.Guangdong Huaxin Accounting Firm (general partner)Guangdong, ChinaChinese Certified Public Accountant:Chinese Certified Public Accountant:January 3, 2014BALANCE SHEETAS OF 31 DECEMBER 2013Unit: RMB YuanCompany: ****** Co., LtdAsset Ending Beginnin Liabilities and all Ending Beginninbalance g parties ’equity (or balance gBalance shareholders' equity)Balance Current Assets:Current liabilities:Monetary funds Short-termborrowingsTransaction financial Transaction financialasset liabilitiesNotes receivable Notes payableAccount receivable Account payableAccount paid in Account received inadvance advanceInterest receivable Employee’scompensationpayableDividend receivable Tax payableOther account Interest payablereceivableInventories Dividend payableNon-current assets Other accountdue within 1 year payableOther current assets--Non-currentliabilities due within 1yearTotal current assets-Other currentliabilitiesNon-current assets:Total current-liabilitiesAvailable for sale Non-currentfinancial assets liabilities:Maturity investments Long-termborrowingsLong-term account Bonds payablereceivablesLong-term equity Long-term accountinvestment payableInvesting property Special payablesFixed asset Accrued liabilitiesProject in Deferred tax liabilitiesconstructionEngineering material Other non-currentliabilitiesFixed asset disposal Total non-current--liabilitiesProduction biological Total liabilities-assetsOil and gas assets Owner ’s equity( orshareholders’equity)Intangible assets Paid-in capital(orshare capital)Development Capital surplus-expenseGoodwill Less: Treasury StockLong-term expense Earned surplusto be apportionedDeferred tax assets Retained earnings-Other non-current Total owner’s equity-assets(or shareholders’equity)Total non-current-assetsTotal assets-Total liabilities and-owner’ s equity(orshareholders’equity)Prepared by:Audited by:Finance Manager:CompanyLeader:INCOME STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2013Unit: RMBYuanCompany: ****** Co., LtdItems Cumulative Amount inamount in this last yearyearI. Operating incomeMinus: Operating costTaxes and associate chargesSelling and distribution expensesAdministrative expenses-Financial expense-Asset impairment lossPlus: gain from change in fair value( losswith ‘- ‘ )Gain from investment ( loss with‘-‘)Including:income form investment onaffiliated enterprise and joint enterpriseII. Operating profit (loss with‘-‘)-Plus: non-business income--Less: non-business expenseIncluding:loss from non-current assetdisposalIII. Total profit (loss with‘-‘)-Less: Income taxIV. Net profit (loss with‘-‘)-V. Earnings per share(I) basic earnings per share(II) diluted earnings per shareVI. Other comprehensive earningsVII. Total comprehensive earnings-Prepared by:Audited by:Finance Manager:Company Leader:CASH FLOW STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2013Unit: RMBYuanCompany: ****** Co., LtdItems Times Amount in Cumulative this year amount in lastyear1.Cash flows arising from operating 0 activities:Cash received from sales of goods or 1 rending ofservicesRefund of tax and fare received2 Other cash received relating to3 operating activitiesSub-total of cash inflows4 Cash paid for goods and services5 Cash paid to and on behalf of employees6 Tax and fare paid7 Other cash paid relating to operating8 activitiesSub-total of cash outflows9 Net cash flow from operating activities10 2. Cash flows arising from investment0 activitiesCash received from return of11 investmentsCash received from investment income12 Net cash received from disposal of fixed13 assets, intangible assets and otherlong-term assetsNet cash received from disposal of14 subsidiaries and other business unitsOther cash received relating to15investment activitiesSub-total of cash inflows16 Cash paid for acquiring fixed assets,17 intangible assets and other long-term assetsCash paid for acquiring investments18 Net cash received from subsidiaries and19 other business unitsOther cash paid relating to investment20 activitiesSub-total of cash outflows21 Net cash flow from investing activities22 3.Cash flows arising from financing 0 activities:Cash received from absorbing 23 investmentCash received from borrowings24 Other cash relating to financing25 activitiesSub-total of cash inflows26 Cash paid for settling debt27 Cash paid for distribution of dividends28or profit or reimbursing interestOther cash payments relating to 29 financing activitiesSub-total of cash outflows30 Net cash flow from financing activities31 4. Influence on cash due to fluctuation in34 exchange rate increase in cash and cash 35 equivalentsAdd : Balance of cash and cash 36 equivalents at the beginning of the year6. Balance of cash and cash equivalents37 at the end of the yearSupplementary information:0 Attached project of cash flow statement0 1. Net profit is adjusted to cash flow of0 operating activitiesNet profit38 Impairment of assets39 Fixed asset depreciation, depletion of oil40 and gas assets and depreciation of productive biological assetsAmortization of intangible assets41 Amortization of long-term prepaid42 expensesTreatment of losses of fixed assets,43 intangible assets and other long-term assetsLoss on retirement of fixed assets44 Loss of changes in fair value45 Finance costs46 Investment losses47 Decrease in deferred income tax assets48 Increase in deferred income tax liabilities49 Decrease in inventories50 Decrease in operating receivables51 Increase in operating payables52 Others53 Net cash flow from operating activities54 2.Investing and financing activities not 0 relating to cashDebt into capital55 Convertible debt due within one year56 Finance leased fixed assets57 increase in cash and cash 0 equivalentsBalance of cash at the end of this period58Less: balance of cash at the beginning of59this periodAdd: balance of cash equivalents at the60end of this periodLess: balance of cash equivalents at the61beginning of this periodNet increase in cash and cash62equivalentsPrepared by:Audited by:Finance Manager:CompanyLeader:STATEMENT OF CHANGES IN OWNERS’ EQUITYFOR THE YEAR ENDED 31 DECEMBER 2013Company: ****** Co., LtdItems Amount in this year Amount in last yearPaid-Capit Earne Retai Total Paid Cap Earn Ret Totaup al d ned owne-up ital ed aine lcapit surpl surpl earni rs'capi surp surp d ownal us us ngs equit tal lus lus ear ers'实用标准文案I. balance at the end of last yearAdd:change of accounting policy Correction of errorsinprevious periodII.Balance at the beginning of this year III. Increase/ decrease ofy nin equigs ty -------------------------------------amount in this year “(-”means decrease)(I) Net profit(II)Gains and losses directly included in the owners ’ equity change amount in fair value ------------------实用标准文案of financial assets available for sale2.Influence of changes in other owners'equity of investors under the equity method3.Influence of income tax relating to the owners’equity project --------------------4. OthersSubtotal of (I) and (II) (III)Input an reduced capital of owners1. Input capital of owners2.Amount of shares included in the-----------------------------------owners ’ equity3. Others--------实用标准文案(IV) Profit distribution1.Withdrawing earned surplus2.Distribution to all owners (or shareholders)3.Others(V)Internal carrying forward of owners ’equity1.Capital surplus transfers to paid-in capital(or share capital)2.Earned surplus transfers to paid-in capital(or share capital)3.Earned surplus makes up losses ------------------------------------------------------------------------------4. Others--------IV. Balance at the end------of this periodLegal representative:Person in charge of accounting:Leader ofaccounting department:****** CO., LTDNOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31, 2013(All amounts in RMB Yuan)I. Company Profile******* Co., Ltd. (hereinafter referred to as the "Company") is a limitedliability company (Sino-foreign joint venture) jointly invested andestablished by **** Co., Ltd. and ******* Limited on 24 June 2013. OnDecember 26, 2013, the shareholders have been changed to***** CO., LTD and ******* LIMITED.Business License of Enterprise Legal Person License No.:Legal Representative:Registered Capital: RMB(Paid-in Capital: RMB)Address:Business Scope: Financing and leasing business; leasing business; purchase of leased property from home and abroad; residue value treatment and maintenance of leased property;c onsulting andguarantees of lease transaction (articles involved in the industry licensemanagement would be dealt in terms of national relevant stipulations)II. Declaration on following Accounting Standard for BusinessEnterprisesThe financial statements made by the Company are in accordance withthe requirements of Accounting Standard for Business Enterprises, whichreflects the financial position, financial performance and cash flow of theCompany truly and completely.III. Basic of preparation of financial statementsThe Company implements the Accounting Standards for BusinessEnterprises(‘ Finance and Accounting[2006]No.3” ) issued by theMinistry of Finance on February 15, 2006 and the successive regulations.The Company prepares its financial statements on a going concern basis,and recognizes and measures its accounting items in compliance withthe Accounting Standards for Business Enterprises–Basic Standardsand other relevant accounting standards,application guidelines and criteria for interpretation of provisions as well as the significantaccounting policies and accounting estimates on the basis of actual transactions and events.IV. The main accounting policies, accounting estimates and changesFiscal yearThe Company adopts the calendar year as its fiscal year from January 1to December 31.Functional currencyRMB was the functional currency of the Company.Accounting measurement attributeThe Company adopts the accrual basis for accounting treatments and double-entry bookkeeping of borrowing for financial accounting.Thehistorical c ost is generally as the measurement attribute, and whenaccounting elements determined are in line with the requirements of Accounting Standards for Enterprises and can be reliably measured, the replacement cost, net realizable value and fair value can be used for measurement.Accounting method of foreign currency transactionsThe Company’s foreign currency transactions adopt approximate spotexchange rate of the transaction date to convert into RMB in accordancewith systematic and rational method; on the balance sheet date,theforeign currency monetary items use the spot exchange rate of the balance sheet date. All balances of exchange arising from differencesbetween the balance sheet date spot exchange rate and the initialrecognition or the former balance sheet date spot exchange rate, exceptthat the exchange gains and losses arising by borrowing foreign currencyfor the construction or production of assets eligible for capitalization aretransacted in accordance with capitalization principles,are included inprofit or loss in this period;the foreign currency non-monetary items measured at historical cost will still be converted with the spot exchangerate of the transaction date.The standard for recognizing cash equivalentWhen making the cash flow statement, cash on hand and depositsreadily to be paid will be recognized as cash, and short-term (usually nomore than three months), highly liquid and readily convertible to knownamounts of cash with insignificant risk of changes in value arerecognized as cash equivalent.Financial InstrumentsClassification, recognition and measurement of financial assets- The company at the time of initial recognition of financial assets dividesit into the following four categories: financial assets measured at fairvalue with changes included in the profit or loss of this period, loans andreceivables, financial assets available for sale and held-to-maturityinvestments. Financial assets are measured at fair value when initially recognized. Relevant t ransaction costs of financial assets measured atfair value with changes included in the profit or loss of this period arerecognized in profit or loss of this period, and relevant transaction costsof other categories of financial assets are recognized in the amount initially recognized.--Financial assets measured at fair value with changes included in theprofit or loss of this period refer to the short-term sales financial assets, including financial assets held for trading or financial assets measured atfair value with changes included in the profit or loss of this period designated upon initial recognition by the management. Financial assets measured at fair value with changes included in the profit or loss of thisperiod are subsequently measured at fair value, and the interest or cash dividends obtained during the holding period will be recognized as investment income, and the gains or losses of the change in fair value atthe end of this period are recognized in the profit or loss in this period. When it is disposed, the difference between the fair value and the initial recorded amount is recognized as investment income, while adjusting gains from changes in the fair value.--Loans and receivables: the non-derivative financial assets without theprice in an active market and with fixed and determinable recovery costare classified as loans and receivables. Loans and receivables adopt theeffective interest method and take amortized cost for subsequent measurement,and gains or losses arising from derecognition,impairment or amortization are included in the profit or loss of this period.-- Financial assets available for sale: including non-derivative financial assets available for sale recognized initially and other non-derivative financial assets except for loans and receivables, held-to-maturity investments and trading financial assets.Financial assets available for sale are subsequently measured at fair value,and interest or cash dividends obtained during the holding period will be recognized as investment income, and gains or losses arising from the changes in fairvalue at the end of this period are recognized directly in owners' equityuntil the financial asset is derecognized or impaired and then is recognized as the profit or loss in this period.--Held-to-maturity investments: the non-derivative financial assets withclear intention and ability to hold to maturity by the management of the company, a fixed maturity date and fixed or determinable payments areclassified as held-to-maturity investments. Held-to-maturity investmentsadopt the effective interest method and take amortized cost for subsequentmeasurement,and gains or losses arisingfromderecognition, impairment or amortization are included in the profit orloss of this period.Classification, recognition and measurement of financial liabilities- The company at the time of initial recognition of financial liabilitiesdivides it into the following two categories: financial liabilities measuredat fair value with changes included in the profit or loss of this period andother financial liabilities. Financial liabilities are measured at fair value when initially recognized. Relevant transaction costs of financial liabilitiesmeasured at fair value with changes included in the profit or loss of thisperiod are recognized in profit or loss of this period, and relevant transaction costs of other financial liabilities are recognized in the amount initially recognized.-- Financial liabilities measured at fair value with changes included in theprofit or loss of this period include the trading financial liabilities andfinancial liabilities measured at fair value with changes included in theprofit or loss of this period designated upon initial recognition. Financialliabilities are subsequently measured at fair value, and the gains or lossesof the change in fair value are recognized in the profit or loss in this period.--Other financial liabilities: adopting the effective interest method andtaking amortized cost for subsequent measurement. The gains or lossesarising from derecognition or amortization is included in the profit or loss of this period.Requirements for derecognition of financial liabilitiesFinancial liabilities shall be entirely or partially derecognized if the present obligations derived from them are entirely or partiallydischarged.Where the Company enters into an agreement with a creditor so as to substitute the current financial liabilities with new ones,and the contract clauses of which are substantially different from thoseof the current ones, it shall recognize the new financial liabilities in placeof the current ones. Where substantial revisions are made to some or allof the contract clauses of the current financial liabilities,the Company shall recognize the new financial liabilities after revision of the contractclauses in place of the current ones entirely or partially.Upon entire or partial derecognition of financial liabilities,differences between the carrying amounts of the derecognized financial liabilities and the consideration paid (including non-monetary assets surrenderedor new financial liabilities assumed) are charged to profit or loss for thecurrent period.Where the Company redeems part of its financial liabilities,it shall allocate the carrying amounts of the entire financial liabilities betweenthe relative fair values of the parts that continue to be recognized andthe derecognized parts on the redemption date. Differences between thecarrying amounts allocated to the derecognized parts and the consideration paid (including non-monetary assets surrendered and thenew financial liabilities assumed)are charged to profit or loss for the current period.Recognition and measurement for transfer of financial assetsIf the Company has transferred nearly all of the risks and rewards relatingto the ownership of the financial assets to the transferee, they shall bederecognized. If it retains nearly all of the risks and rewards relating tothe ownership of the financial assets, they shall not be derecognized andwill be recognized as a financial liability. If the Company has not transferred nor retained nearly all of the risks and rewards relating to the ownership of the financial assets: (1) to give up the control of thefinancial assets to be derecognized; (2) not giving up control of the financial asset to be recognized based on the extent of its continuing involvement in the transferred financial assets and liabilities arerecognized accordingly.If the transfer of entire financial assets satisfy the criteria for derecognition,differences between the amounts of the following twoitems shall be recognized in profit or loss for the current period: (1) thecarrying amount of the transferred financial asset; (2) the aggregateconsideration received from the transfer plus the cumulative amounts ofthe changes in the fair values originally recognized in the owners’ equity.If the partial transfer of financial assets satisfy the criteria for derecognition,the carrying amounts of the entire financial assets transferred shall be split into the derecognized and recognized parts according to their respective fair values and differences between the amounts of the following two items are charged to profit or loss for thecurrent period: (1) the carrying amounts of the derecognized parts;(2) The aggregate consideration for the derecognized parts plus the portionof the accumulative amounts of the changes in the fair values of the derecognized parts which are originally recognized in the owners’equity.Determination of the fair value of financial instruments-If financial instruments trade in an active market, the quoted price in anactive market determines its fair value; if financial instrument trade not inan active market, the valuation techniques determine the fair value.Valuation techniques include recent market transaction price reference to the familiar situation and volunteer transaction, current fair valuereference to other substantially similar financial instruments, discountedcash flow method and option pricing model and so on.Test and Provisions for impairment loss on financial assets--Except trading financial assets, the Company makes assessment on thecarrying values of financial assets at the balance sheet date. If there isevidence that the fair value of specific financial asset has been impaired,provisions for impairment loss is made accordingly.--Measurement of impairment of financial assets measured atamortized costIf there is objective evidence that the financial asset measured at amortized costhas been impaired, the carrying amount of the financialasset is written down to the present value of estimated future cash flows (excluding future credit losses that have not yet occurred), and the amount of reduction is recognized as impairment loss and is recognizedin the profit or loss of this period. The Company carries out the impairment test of significant single financial asset separately, carries outthe impairment test on insignificant single financial asset from a single or combination of angles, and carries out the impairment test on single asset without objective evidence of impairment along with the financialassets with similar credit risk characteristics to constitute a combination, but does not carry out the impairment test on the provision for impairment of financial assets based on the single in the portfolio. In the subsequent period, if there is objective evidence that the value of financial asset has been restored and recognized relevant to the objective matters occurring after the impairment, previously recognizedimpairment loss shall be reversed and charged into the profit or loss ofthis period. But the book value after the reversal should not exceed theamortized cost at the reversal date of the financial assets supposed no provision for impairment.When the financial assets measured at amortized cost actually occur loss, offset against the related provision forimpairment.-- Available for sale financial assetsIf there is objective evidence that an impairment of available for salefinancial assets occurs,even though the financial asset has not been derecognised, the cumulative loss of decrease of the faire value originally recorded in the owner's equity should be transferred out and charged into the current profit and loss.The cumulative loss is the initial acquisition cost of available for sale financial assets, deducting the fairvalue of the withdrawing principal and amortization amount and impairment loss as well as net impairment amount originally charged into the profit or loss.Recognition and provision for bad debts of accounts receivableIf there is objective evidence that receivables are impaired at the end ofthis period, the carrying value will be written down to its present value of estimated future cash flows, and the amount of reduction is recognizedas impairment loss and is recognized in the current profit or loss. Presentvalue of estimated future cash flows is determined through future cashflows (excluding credit losses that have not been incurred) discounted atthe original effective interest rate,taking into account the value of related collateral(less estimated disposal costs, etc.).Original effective interest rate is the actual interest rate when the receivables are recognized initially.The estimated future cash flows of short-term receivables have small difference from the present value,and the estimated future cash flows are not discounted in determining the related impairment loss.The significant single receivables are separately carried out impairmenttest at the end of this period, and if there is objective evidence that theimpairment has occurred, based on the difference of the present value offuture cash flows less than the book value, the impairment loss is recognized and the provision of bad debts is done. The significant singleamount refers to top five receivable balances or the sum of payments accounting for more than 10% of receivable balances.If there is objective evidence that the individual non-significant receivables impairment has occurred, separate impairment test is done,the impairment loss is recognized and the provision for bad debts is done;other individual non-significant receivables and receivables not impaired after separate test are together divided into several combinations for impairment testing with aging as the similar credit risk characteristics,to determine the impairment loss and do provision for bad debts.In addition to separate provision for impairment of receivables,the company is based on the actual loss rate of receivable portfolio with thesame or similar to the previous year and aging as the similar credit risk characteristics, and combines the current situation to determine the ratioof provision for bad debts as follows:Aging Ratio of provisionWithin one year5%。

CH04Audit Objectives, Procedures, and Working Papers(审计学,英文版)

21

5.sufficient appropriate evidence in auditing

• The purpose of gathering and analysing evidence is to support the decision on whether the FS conform to GAAP. • (1)APPROPRIATENESS 品质 • (2)SUFFICIENCY 数量 • P123, Reliability

8

Client selection

• • • • C. predecessor auditor D. special attention or unusual risks E. independence F. special skills

9

RETENTION

• Major Changes • management, directors, ownership, legal counsel, financial condition, litigation status, nature of the business, scope of the audit engagement.

10

(2)Communication between predecessor and successor auditors

• Rules of Professional Conduct • A. successor obtain inf. From predecessor; • B. predecessor respond to successor; • C. client consent. • If the consent is refused, the successor should be wary.

审计底稿(英文版)

Audit Program31 December 2000Prepared byDate Reviewed byDate Approved byDateCLIENTYEAR ENDAUDIT PROGRAM FOR Cash & BankRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Compare the listing of cash and bank accounts with those of priorperiods and investigate any unexpected changes (e.g., creditbalances, unusual large balances, new accounts, closed accounts) orthe absence of expected changes._____ 2. Review interest received in relation to the average cash and bankbalances.Cash balances_____ 3. (a) Obtain a copy of the list of balances of cash as at 31/12/1999 and31/12/2000.(b) Check casting and agree total with general ledger controlaccount._____ 4. Scan cash entries noting any unusual items and make furtherinvestigation where considered necessary.Bank Balances_____ 5. (a) Obtain a copy of the list of balances of bank as at the period enddate; and(b) Check casting and agree total with general ledger control account.6. Bank Confirmation request (Note 2)(a) Get a standard bank confirmation request form from thestationery cupboard.(b) Fill in the client name, our reference number and the period oryear end date (please specify) for the bank to confirm.(c) Give the partial completed form to the relevant client staff .(d) Request the client to perform the following tasks:·Stamp the form with the company chop;·Have the form signed by an authorized signatory;·Fill in the balances in the appropriate boxes;·For items which are not applicable for the company, fill in“N/A” in the corresponding boxes; and·Confirm to us whether the form can be sent to the bank by mailor if the client is required to take the confirmation to the bank.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Cash & Bank (Continued)Ref Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by Bank Balances (Continued)(e) Check the completed confirmation form to ensure thefollowing:·the balances agreed to the bank statements as at theconfirmation date;·the form is properly signed;·the client has filled in all security and guarantee related matterson the bank confirmation; and·Send the bank confirmation form to the bank by post.OrIf the client staff has to take the confirmation to the bank, arrange astaff to go with him/her. (Note 3)(f) Keep copies of the confirmation in the file until replies areobtained from the banks.(g) When replies are received, check the confirmations received toensure that:·the forms were stamped and signed by the bank on the lastpage; and·the individual balances and information are endorsed by thebank staff personal chop. (Note 4)_____ 7. Examine the client’s bank reconciliation as at 31/12/2000 asfollows:a) agree book balance to Cash Book and General Ledger;b)agree balance per bank statement to bank statement at theyear end and bank confirmation received;c) check casting of the bank reconciliation;d)vouch all lodgments / lodgments with amount greater thanRMB _____ * not clear to the cash book and bank statementin the following month ensuring all lodgments are cleared;(Note 5)e) vouch all outstanding cheques / outstanding cheques withamount greater than RMB _____ * to the cash book and to thebank statement in the following month & note down the datewhen they are cleared; (Note 5)f) obtain explanations from the client of all outstanding lodgments/ lodgment with amounts greater than RMB_____ *;g) investigate all stale cheques / stale cheques with amountgreater than RMB_____ * issued for more than five / ten days*, and make appropriate adjustments thereof in the cash bookand ledger; (Note 6)CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Cash & Bank (Continued)Ref Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by Bank Balances (Continued)h) investigate all payments / payments with amount greater thanRMB_____ * recorded by the bank but not recorded by theclient, and make appropriate adjustments thereof in the cashbook and ledger; (Note 6) andi) investigate all receipts / receipts with amount greater thanRMB_____ * recorded by the bank but not recorded by theclient, and make appropriate adjustments thereof in the cashbook and ledger. (Note 6)_____ 8. Review the bank book for any unusual items (greater than RMB_____) such as: a) non-trading receipts or payments andb) transfers in and out of the bank accounts._____ 9. Select receipts larger than RMB ______ and payments larger thanRMB ______ within ____weeks before and after the year end toensure that they have been properly accounted for.General_____ 10. Review the cash and bank accounts in the general ledger for unusualitems._____ 11. Review the cash disbursements and cash receipts registers forunusual items; investigate any such items observed._____ 12. Review bank confirmations, minutes, loan agreements and otherdocuments for evidence of restrictions on the use of cash, or ofliens, or security interests in, cash._____ 13. Consider the covenants and other narratives given in loan and othermaterial agreements and determine compliance with the agreementsand whether necessary disclosure have been made._____ 14. Consider the implications of client management practices that resultin recurring short term loan to finance working capital. Considerinquiry of client management and alert your senior / executiveshould such short term loans be encountered in the audit.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Cash & Bank (Continued)Ref Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by* Delete as appropriateNote 1i. The cash count should be performed by cashier with the presence of a staff that normally is not involved in the cashier function.ii. Cash certificate is acceptable only if the petty cash balance is considered as immaterial and / or the risk associated is low/ minimal.Note 2i. Bank confirmations are sent on an individual branch basis, i.e. one confirmation per branch.ii. Confirmation should also be sent to accounts closed during the year.iii. If either the bank or the client refuses to reply/send the confirmation, consider if there is a significantlimitation of our audit scope and its implications.Note 3When it is not feasible for an EYHM staff to go with the client, we must reconsider if the confirmation obtained provides sufficient and reliable audit evidence due to the lack of independence.Note 4Alternatively, the bank may issue its own bank certificate to confirm the deposits and loans balances and confirm that no other business transactions exiting.Note 5The extent of vouching work depends on our assessment of the likelihood of errors occurring.Note 6We have to consider the effect in aggregate regarding the unadjusted items which are below the amount stipulated in this procedure whenever one is set.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Accounts ReceivableRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by1. Obtain or prepare a listing of accounts receivable and investigateunusual balances. Credit balances, and accounts that may not beaccounts receivable, or may not be properly classified as accountsreceivable trade (e.g. consignment accounts, related-party oremployee accounts ).2. Trace the total in the customers’ ledger to the general ledger controlaccount: investigate reconciling items greater than ¥________ andunusual items.3. Compare current period’s receivables as a percentage of net sales withprior periods’ percentages. Compare discounts, returns, andallowances with prior periods (e.g. as 5 - 10% of sales).4. As of 31/12/2000, perform confirmation procedures for accounts asfollows:a. Select key items (accounts greater than ¥________ and accountswith the following characteristics: long aging, or involved in legalcase) for positive confirmation procedures.b. Using a MUS or Random technique, select a representative sampleor account (as determined through use of Audit Risk Table__________) for positive / negative confirmation procedures.c. Trace information (i.e.. balance and addresses) from individualrequests to the subsidiary records. Send requests and prepareconfirmation statistics.d. Trace confirmation replies to the trial balance and request theclient to reconcile differences. Investigate explanations for differencesgreater than ¥_______ and any unusual explanations.e. Send second requests for all unanswered positive confirmationrequests.f. Examine subsequent cash receipts, shipping records, salescontracts, and other evidence to substantiate the validity of accountsfor which no reply or an unsatisfactory reply was received.g. Summarize the results of the confirmation procedures.5. Test sales cut-off for service rendering greater than ¥ for theLast days before year end and the first ___days after year end.Determine that the sales were recorded in the proper period throughreview of shipping documents, billings, sales register and othersupporting documents.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Accounts Receivable (Continued)Ref Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by6. Test for out-of-period credit memos by examining those greater than¥_____ issued for the period from the balance sheet dated to/ /2001. Inquire as to whether there are any unissued credits thatrelate to the period under audit.7. Test the aging of accounts receivable and unbilled contracts foramounts greater than ¥and accounts with the followingcharacteristics: opening receivable balance brought forward from // , to support the accuracy of the aged trial balance. Trace thedetails to and from the customer’s ledger accounts or supportingdocumentation.8. Compare aging, bad debt expanse, and write-offs with prior periods.Compar e the current period’s accounts receivable turnover and/ornumber of day’s sales outstanding with prior periods’ amounts.9. Evaluate the adequacy of the allowance for doubtful accounts and therelated provision as follows:a. From the aged trial balance as of 31/12/2000, select accounts withbalances greater than ¥ , accounts greater than ¥ thatare more than 180 days past due, and accounts with legalcontingencies.b. In addition to those accounts selected in a above, select anyadditional accounts that have a higher likelihood of error (e.g.. prioryear experience, industry concentration).c. For those accounts selected, discuss collectibles concerns with thecredit manager or other responsible individual and reviewcorrespondence files or other relevant data in support of the client’srepresentations.d. Review subsequent collections for those accounts selected forevaluation.e. Determine if any product related problems (e.g.. quality right ofreturn) are affecting collectibles and should be considered indetermining the adequacy of the allowance. These problems shouldalso be considered in determining the adequacy of the allowance forinventory obsolescence.f. Perform appropriate analytical review procedures.g. Conclude on the adequacy of the allowance.10. Review the accounts receivable and sales accounts in the generalledger and the sales and cash receipts registers for unusual items:investigate any such items observed.11. Determine whether any receivables are pledged as collateral orSubject to any liens; coordinate with work on debt payable.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR Prepayment & Construction in ProcessRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Obtain or prepare an analysis for each significant classification ofprepaid expenses, deferred charges, other assets or intangibles.Include adequate descriptions of significant components and thefollowing:a. Balance at the beginning of the periodb. Additions at costc. Deductions charged to expense, and to other accountd. Balance at the end of the period._____ 2. Foot the analyses and trace totals to the general ledger: trace thebeginning balances to the prior period audit working papers._____ 3. Compare the account balances with those of prior periods andinvestigate any unexpected changes (or the absence of expectedchanges). For accounts greater than ¥and accounts that havechanged by the greater of ¥ or 5~10% from the prior period.Recomputed the ending balance (and examine supporting documentsfor significant charges as appropriate) and determine that thecarrying amount does not exceed amounts properly allocable tofuture periods._____ 4. Trace amounts amortized to expense during the period to the relatedgeneral ledger accounts._____ 5. Confirm deposits and assets held by others for those items greaterthan ¥and items related to construction of shelters andunipoles, or items related to operating expenses for sales centers._____ 6. Review the accounts under this classification and the related incomeand expense accounts in the general ledger for unusual items:investigate any such items noted._____ 7. Determine that there has been no permanent impairment of value fordeferred charges, intangible assets, etc._____ 8. Determine that balances are properly classified in the balance sheet(current versus non-current, etc.).____ 9. Identify any exceptional item (i.e. prepaid legal fee). Investigate itsnature and consider the recoverability of these items and whether anyprovision is needs.10. Perform reasonableness test on amortisation of deferred expenses._____ 11. Send and obtain confirmations from staff and sales centers to verifyexistence of assets._____ 12. Perform overall analytical review on total prepayment andconstruction in progress._____ 13. Obtain and review a movement of construction in progress, examinesupporting documents for material additions.14. Test the calculation of capitalised interest if appropriate.____ 15. Check Completion Verification to ensure that CIP is transferred tofixed assets at proper time.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR AffiliatesRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by ______ 1. Review other receivable and payables, and reclassify currentaccounts with ultimate holding company, subsidiaries, fellowsubsidiaries and associate company to the proper accounts.______ 2. Agree or reconcile all current accounts balance with relatedparty by sending confirmation. Agree the current accountbalance with subsidiaries’ books and records.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR Fixed Assets and Concession RightsRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by ______ 1. Obtain or prepare a summary of property, plant and equipment andrelated depreciation (by major classification) including thefollowing:a. Beginning and ending balances at cost.b. Asset additions at cost.c. Asset retirements and dispositions.d. Other changes (e.g. transfers).e. Beginning and ending balances of the allowances fordepreciation.f. Additions to the allowance for depreciation accompanied by ananalysis of amounts charged to expense, absorbed in inventory,and capitalized.g. Reductions of the allowance for depreciation for retirements anddispositions.______ 2. Obtain or prepare a schedule of asset additions during the period,including description, date acquired, estimated useful life, and cost,for all additions of ¥ or more, with those under that amountcombined so the total additions ties to the summary schedule byclassification. Compare the level of property acquisitions for theperiod with the prior period.______ 3. Obtain or prepare a schedule of retirements and dispositionincluding description, date of acquisition, date of retirement ordisposition, cost, accumulated depreciation, net carrying value,proceeds of disposition, and gain or loss on disposition.______ 4. Trace the beginning balances per the summary schedule to endingbalances per the prior p eriod’s audit working papers.______ 5. Trace amounts per the summary schedule to the general ledger, thedetailed asset records, and to the schedules of additions, andretirements and dispositions; test the footings and crossfootings ofthe schedules.______ 6. For asset additions greater than ¥and additions with thefollowing characteristics: capitalised interests, or capitalised legalfees, examine supporting documents (purchase contracts, paidchecks, vendors’ invoices) to verify record ed cost. Challenge theestimated useful lives assigned.______ 7. For asset retirements and dispositions with net carrying valuesgreater than ¥ , examine supporting documents (bills of sale,contracts, copies of checks) to verify proceeds and determine thatthe appropriate cost and accumulated depreciation were removedfrom the accounting records. Recomputed gain or loss.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR Fixed Assets and Concession Rights (Cont’d)Ref Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 8. Examine support for charges greater than ¥to repair andmaintenance expense accounts for potential items that should havebeen capitalized. Compare repair and maintenance expense accountbalances with the prior period and investigate any unexpectedchanges (or the absence of expected changes)._____ 9. Perform physical inspection of selected shelters in 3 major citiesand determine asset recoverability / realization._____ 10. Note down the depreciation policy under the Group’s instruction.Perform reasonableness test or detail recalculations to assessdepreciation / amortization expense and tie the total expense perthe property summary to the general ledger accounts._____ 11. Obtain or prepare schedules of lease and rental expense detail.Examine support for charges greater than ¥________ to determineproper classification. Determine that any new leases have beenproperly accounted for._____ 12. Test the calculation of capitalized interest, if appropriate._____ 13. Review the property, plant and equipment and related accounts inthe general ledger for unusual items; investigate such items noted._____ 14. Review minutes, agreements, UCC filings, and other documents(e.g., bank and loan confirmations) for evidence of liens, pledges,security interests, and restrictions on property, plant andequipment._____ 15. Determine the tax basis of accounting for property, plant andequipment transactions, and verify that any book-tax differenceshave been accounted for property.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR Accounts Payable, Accruals and Other LiabilitiesRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by ______ 1. Obtain or prepare a schedule of accounts payable details as of thebalance sheet date: foot the schedule and trace the total to theaccounts payable balance in the general ledger.______ 2. Compare the list of accounts payable with those of prior periodsand investigate any unexpected changes (e.g. changes in majorvendors, in the proportion of debit balances, in the aging of theaccounts, etc.) or the absence of expected changes.______ 3. Review the accounts payable account in the general ledger andsupporting detail for unusual items. Investigate debit balancesand , if significant, consider requesting positive confirmations andpropose reclassification of amounts.______ 4. Obtain or prepare a schedule of accrued liabilities and deferredincome. Examine the composition and the computation of thoseaccounts considered significant or whether the change / lack ofchange in lance from the prior period is unexpected.______ 5. Compare the account balances with those of prior periods andinvestigate any unexpected changes (or the absence of expectedchanges).______ 6. Ensure the provision of welfare fund and staff welfare expensesare properly accrued and accounted for.______ 7. Review construction contracts and related documents for anyunrecorded liabilities and make adjustments if necessary.______ 8. Circularise the payable accounts with material balances.______ 9. Agree payable accounts with material balance to suppliers’statements or vouch to customer receipts, if available.______ 10. Perform a search for unrecorded liabilities at the year end byreviewing disbursements voucher and unpaid invoices overRMB after year end.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Tax payableRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by ______ 1. For detailed procedures, please see PRC TAX PROVISIONAUDIT PROGRAMME.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR Short Term Bank LoansRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Obtain or prepare a schedule and a movement of bank loan andrelated interest accounts by issue showing the following:Description (date of origin, type of debt, maturity, face amount,interest rate, timing and amount of payments): Activity in theprincipal and related interest accounts (beginning balance,additions, payments, ending balance)._____ 2. Test the clerical accuracy of the schedule in #1 above, and tracetotals to the general ledger. Compare the account balances withthose of prior periods and investigate any unexpected changes (orthe absence of expected changes)._____ 3. Confirm all debt account, including those paid off during theperiod, as of 31/12/2000. Information to be confirmed shouldinclude: principal and related interest due at end of period, terms,liens, security interests or assets pledged as collateral, andcompliance with covenants._____ 4. Test interest paid and accrued and tie expense to the trial balance.Perform an overall test of the reasonableness of interest expense bymultiplying the average interest rate by the average amount of debtoutstanding._____ 5. Vouch to supporting documents (bank-in slip etc.) to ensure thatrepayments have been made as expected and the year end balance iscorrect and correctly disclosed._____ 6. Obtain and review copies of all new debt agreements and anyexisting debt agreements for which we do not have a copy in ourfiles. Review to determine the terms, restrictions, and otherpertinent provisions of long-term debt._____ 7. Determine whether receivables, inventory, and / or property, plant,and equipment are pledged as collateral or subject to any liens._____ 8. Review short-term / long-term classification of debt for propriety.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR Share capitalRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Obtain or prepare an analysis of all equity accounts progressingform the beginning of the period to the end of the period. Test theclerical accuracy of the analysis. Trace the beginning balances toprior period audit working papers and trace ending balances to thegeneral ledger._____ 2. Examine support for and determine the propriety of accounting forany changes in the equity accounts from the prior period._____ 3. Review minutes or other supporting documents for theauthorization for and the details of transactions that affected theequity accounts during the period._____ 4. If the company does not keep itsown stock record books:a.Obtain confirmation of shares outstanding from the registrarand transfer agent.b. Reconcile the schedule to the general ledger._____ 5. Analysis activity in the retained earnings account during the period;trace the beginning balance to the prior period audit wordingpapers; trace the ending balance to the general ledger; trace incometo the financial statements and support other changes asappropriate._____ 6. Obtain the calculation sheets of minority interests (MI) and reviewit. Ensure that all proposed adjustment related to retained earningsare also affect the results of MI.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Commitments and contingenciesRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Review all contracts and agreements to determine the capitalcommitment._____ 2. Inquire management and check board minutes, bank confirmations,contracts, loan agreements, leases and correspondence withsolicitors for indications of other guarantees, commitments orcontingencies.CLIENT .YEAR END 31 December 2000AUDIT PROGRAM FOR RevenueRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Obtain or prepare a comparative analysis of sales (by product line,division, etc.) and other income accounts for the current andpreceding period and investigate acoounts that changed by thegreater of ¥ or 10%._____ 2. Select 20-25 sales transactions from throughout the period andsupport proper recording by comparing sales invoice information toshipping documents and tracing the invoice through the accountingsystem to recording the general ledger._____ 3. See Accounts Receivable step #10._____ 4. Review the other non-current credit accounts in the general ledgerfor unusual items._____ 5. Perform additional analytical review procedures as follows:See Accounts Receivable step #3._____ 6. Refer to Accounts Receivable for the procedures relating to tests ofcut-off of sales invoices and credit memos._____ 7. Examine support for the charges to the other non-current creditaccounts during the period._____ 8. Account for and test the numerical sequence of sales invoice and /or photos that is for completeness.CLIENTYEAR END 31 December 2000AUDIT PROGRAM FOR Cost and ExpensesRef Audit Procedures - Nature, Timing and Extent W.P. Ref. Performed by _____ 1. Obtain or prepare a comparative analysis of expense accounts(grouped by income statement classification ) and investigateaccounts that fluctuated by the greater of ¥ or 10~20%. Alsocompare each classification of expenses as a percentage of net saleswith prior period percentages and investigate unexpected changes(or the absence of expected changes)._____ 2. Review the expense accounts in the general ledger and thepurchases journal for unusual items; investigate any such itemsobserved._____ 3. Perform monthly analysis of salries, and identify any sales bonus orcommission to assess reasonableness._____ 4. Perform reasonableness test on the following items:a.shelters’ rental, electricity and subcontractors expensesbased on the fluctuation of shelters quantity.b.rental expenses for head office and sales centres.c.interest income._____ 5. Test any irregular items in “others” obtain adequate supportingdocuments and perform analysis._____ 6. Consider any commitment arisen from those rental contracts forshelters in each city and from those lease contracts for premises.。

2019年新版标准审计报告英文版

REPORT OF AUDITORS~~~~(2019)Audit No.000To the shareholders of~~~~Co.,Ltd.:Ⅰ.Audit opinionWe have audited the accompanying financial statements of~~~~Co.,Ltd. (hereinafter referred to as"the Company"),which comprise the balance sheet as at December31,2018,the income statement for the year then ended,cash flow statement,Statement of changes in owner’s equity and other relevant foot-notes to financial statements.In our opinion,the attached financial statements are prepared,in all material respects,in accordance with the Accounting Standards for Enterprises and present fairly the financial position of the Company as of December31,2018,and operating results and cash flow for the year then ended.Ⅱ.Basis for audit opinionWe conducted our audit in accordance with the Auditing Standards for Certified Public Accountants in China.Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report.According to the Code of Ethics for Chinese CPA,we are independent of the Company in accordance with the Code of Ethics for Chinese CPA and we have fulfilled our other ethical responsibilities in accordance with these requirements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.Ⅲ.Responsibilities of Management and Those Charged with Governance for the Financial StatementsThe Company's management is responsible for preparing the financial statements in accordance with the requirements of Accounting Standards for Small Business Enterprises to achieve a fair presentation,and for designing,implementing and maintaining internal control that is necessary to ensure that the financial statements are free from material misstatements,whether due to frauds or errors.In preparing the financial statements,management of the Company is responsible for assessing the Company's ability to continue as a going concern,disclosing matters related to going concern,if applicable,and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations,or has no realistic alternative but to do so.Those charged with governance are responsible for overseeing the Company's financial reporting process.Ⅳ.Auditor's Responsibilities for the Audit of the Financial StatementsOur objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement,whether due to fraud or error,and to issue an auditor's report that includes our opinion.Reasonable assurance is a high level of assurance,but is not a guarantee that an audit conducted in accordance with the audit standards will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material,if individually or in the aggregate,they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.As part of an audit in accordance with the audit standards,we exercise professional judgment and maintain professional scepticism throughout the audit.We also:(1)Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error,design and perform audit procedures responsive to those risks,and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error,as fraud may involve collusion,forgery,omissions,misrepresentations,or the override of internal control.(2)Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances,but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.(3)Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management of the Company.(4)Conclude on the appropriateness of using the going concern assumption by the management of the Company,and conclude,based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company's ability to continue as a going concern.If we conclude that a material uncertainty exists,we are required to draw attention in our auditor's report to the related disclosures in the financial statements,or if such disclosures are inadequate,to not express clean opinion.Our conclusions are based on the audit evidence obtained up to the date of our auditor's report.However, future events or conditions may cause the Company to cease to continue as a going concern.(5)Evaluate the overall presentation,structure and content of the financialstatements,including the disclosures,and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation. We communicate with those charged with governance regarding,among other matters, the planned scope and timing of the audit and significant audit matters,including any significant deficiencies in internal control that we identify during our audit.~~~~~CPAs Co.,Ltd.Certified Public Accountant:Tianjin,P.R.China Certified Public Accountant:April9,2019。

英文标准审计工作底稿

Systems notes & Background information

3

Control Objectives

Key Control Questions

Scheduleof findings

4

Quality Forms: File review checklist

Audit Remit

Clients Property removed/returned

Item No.

Y

N

Test and/or Findings

Ref.

Distribution

Original

Retain on Audit File

Client’s Property Removed/Returned

Audit Number

Client

Item No.

Description

Date Rec’vd

Key Control Questions

4

5

Working File Index

Audit Number

Client

Description

1

Final report or latest working draft

Action plan

Follow-up papers

Client questionnaire

Permanent File Index

Client

Description

Updated on

1

Audit report

Action plan

Follow-up papers

Client questionnaire

2

内部控制程序审计工作底稿

Procurement Internal Controls Work PRogram内部控制程序审计工作底稿Project Team (list members):项目组(列示成员)Project Phase Date Comments项目阶段日期备注 Planning Fieldwork工作范围 Report Issuance报告发布Time Audit Step ByYes/NoW/P Ref.时间审计步骤是/否,参考底稿由确认1. Are purchase orders based on authorized requisitions?1、采购订单是基于被批准的采购申请单?2. Are purchase orders properly coded to identify the cost objective (direct, indirect or inventory)?2、采购订单是否被适当编码以区分成本项目归属?(直接、间接或存货)3. Are purchase orders serially controlled and accounted for?3、采购订单是否连续编号控制?4. Is the use of standardized purchase orders required?4、需要采用标准化的采购订单吗?5. Are effective numerical document controls or status reports maintained to record the receipt of purchase requisitions?5、是否存在有效的连续编号控制文件或统计报告以记录收到的采购申请?6. Does the purchasing department maintain specifications for all materials and services used by the contractor?6、采购部门是否保存有合同商提供的所有原材料与劳务服务的说明书?7. Are requirements combined where appropriate?7、需求是否被适当的合并?8. Are make-or-buy decisions adequately documented?8、自制或采购决策是否被充分记录在案?9. Does the purchasing department have adequate controls to prevent unauthorized use of canceled or voided purchase requisitions?9、采购部门对无效或取消的采购申请的滥用有无充分的预防措施?10. is the purchasing department independent of other departments and responsible for procuring all materials, supplies, and equipment?10、采购部门是否与其他部门相互独立,并负责采购所有的原材料、供应品及设备?11. Are the receiving and inspection functions separate from the purchasing function?11、收货与检查工作是否与采购工作相互分离?12. Are copies of purchase orders furnished at the time of issuance to the receiving, accounts payable, and when appropriate, to the expediting departments?12、在采购订单发出时,是否同时将复印件送至收货部、应付款会计与支出部门?13. Do procedures require complete history files for items purchased frequently and for all major procurements?13、对经常采购货物、所有的重要采购项目是否保存有完整的历史记录?14. Are prices established at the time the order is placed for goods manufactured to order, rather than on an "advise price" or not-to-exceed basis?14、价格是否基于采购时货物的制造价格,而非“建议价格”或“不超过…价格”?15. Is purchasing required to develop and maintain lists of potential bidders or offerors for particular types of materials?15、特定货物的采购是否需要建立与维持“潜在的供应商报价体系”或竞价体系?16. Are periodic independent checks made to verify existence of suppliers on the bidder list?16、针对竞价单上的供应商是否进行定期的独立核查以确定其存在性?17. Is documentation required from engineering, quality or the requesting source to support the purchase from a single or directed source?17、需要从工程、质检或货物需求部门获取文件以确认商品只能从单一或直接来源采购吗?18. Do procedures require maintenance of adequate documentation in purchase order files?18、采购程序需要保留充分的采购订单相关文件吗?19. Is there a formal bid control system in place?19、是否存在正式的竞价控制系统?20. Do procedures require appropriate justification when the low bidder in a competitive solicitation is not selected?20、在竞标过程中,低价的竞标者没有被选中时,是否需要陈述适当的理由?21. Are there clearly defined responsibilities for negotiating price and terms and conditions?21、在价格、条款协商过程中,是否有明确的责任分工?22. Are practices in place to assure procurement at competitive prices including development of purchase requirements to achieve maximum competition?22、实际操作程序中,能否保证最大的竞争性以取得最优惠的价格?23. do non-competitive procurements require documented justification?23、非竞争性的采购是否有合理的解释文件?24. Is certified cost and pricing data obtained from subcontractors when required and is appropriate price analysis or cost analysis performed?24、在合同分包时,是否能从分包商处取得确认的成本与价格数据并对其进行分析?25. Is a listing of debarred suppliers maintained and checked against potential and existing suppliers?25、是否有排斥的供应商名单记录在案并与潜在的、现存的供应商名单想核对?26. Is there a supplier performance rating system that evaluates price, quality, and delivery performance?26、是否存在供应商业绩评价体系以评估其价格、质量、送货时间等业绩?27. Does a system exist to "flow down" required clauses?27、将所要求的条款顺利传达下去吗?28. are subcontractors reviewed for clauses which conflict with provisions of the prime contract(i.e., pricing and payment, patent rights, warranty, quality technical data, quality assurance requirements, etc.)?28、分包商是否复合与初包合同相冲突的条款(例如价格与付款、专利权、授权、质量技术数据、质量保证要求等?)29. Are processes in place to monitor subcontractors with progress payments?29、针对分包商是否存在进度监督机制以检查按进度付款情况?30. Is approval of subcontracts obtained or notice and consent obtained when required?30、在需要时能获得分包商的批准或同意文件吗?31. Do procedures require that prompt payment discounts be obtained and utilized?31、采购程序要求快速付款折扣的取得与利用吗?32. Do procedures prohibit splitting orders to avoid dollar thresholds for approval, cost analysis, cost accounting standards and submission of cost or pricing data?32、采购程序是否禁止订单拆分以避免授权金额门槛、成本分析、成本核算标准或成本与价格数据提供?33. Are delivery dates required on purchase requisitions?33、在采购申请上标明货物需要日期吗?34. Is the purchasing department required to follow-up on orders to assure timely delivery?34、采购部门被要求执行跟踪程序以保证及时到货吗?35. Do procedures require final purchasing packages to be reviewed by appropriate personnel?35、采购程序要求最后的采购单据包由适当的人员进行复核吗?36. are approval levels defined for purchase orders and supplements to purchase orders?36、是否针对采购订单与备品采购订单设置授权权限?37. Do competitive pricing policies exist for inter-entity orders?37、对公司内部采购是否存在竞争价格机制?38. Are inter-entity transactions handled in accordance with company policy?38、公司内部交易是按照公司政策执行的吗?39. Is there a system of reports and controls that reflects performance and provides the means through which the purchasing organization reports its performance to management?39、是否存在向管理层反映采购部门业绩的报告与控制程序40. Is receiving or giving gratuities, favors, or kickbacks prohibited?40、收取任何回扣、赠品、招待等是被禁止的吗?41. Are there awareness programs to advise purchasing personnel of the consequences of accepting or soliciting kickbacks?41、存在针对采购人员接受或要求回扣的处罚后果的提醒程序吗?42. Are there requirements for purchasing personnel to certify annually that they have not engaged in any prohibited activities, such as kickbacks and gratuities?42、采购人员是否被要求提报年度说明证实其没有从事任何被禁止的活动,例如取得回扣或赠品?43. are procurement personnel required to complete an annual conflict of interest certification, including disclosure of financial or ownership interest in suppliers?43、采购中间人是否被要求提报年度利益冲突说明,其中揭示其在供应商方的利益与所有权?44. Is a standard of conduct policy for suppliers disseminated to suppliersannually?44、是否每年均给供应商提送标准行为指导方针?45. Are suppliers required to provide representation that no kickbacks are provided, solicited or offered?45、供应商是否被要求提供关于没有回扣支付的说明?46. Is provision made for periodic rotation of procurement personnel?46、是否有定期轮换采购中间人的机制存在?47. Does the purchasing department conduct self-audits on a regularly scheduled basis?47、采购部门是否定期进行自我检查?48. Is there a program for education and training of purchasing personnel?48、对采购人员有培训程序吗?。

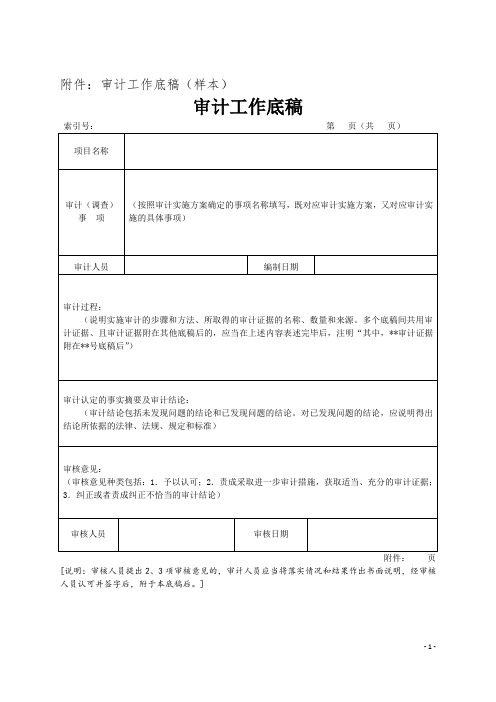

审计工作底稿(样本)

(审计结论包括未发现问题的结论和已发现问题的结论。对已发现问题的结论,应说明得出结论所依据的法律、法规、规定和标准)

审核意见:

(审核意见种类包括:1.予以认可;2.责成采取进一步审计措施,获取适当、充分的审计证据;3.纠正或者责成纠正不恰当的审底稿(样本)

审计工作底稿

索引号:第 页(共 页)

项目名称

审计(调查)

事项

(按照审计实施方案确定的事项名称填写,既对应审计实施方案,又对应审计实施的具体事项)

审计人员

编制日期

审计过程:

(说明实施审计的步骤和方法、所取得的审计证据的名称、数量和来源。多个底稿间共用审计证据、且审计证据附在其他底稿后的,应当在上述内容表述完毕后,注明“其中,**审计证据附在**号底稿后”)

[说明:审核人员提出2、3项审核意见的,审计人员应当将落实情况和结果作出书面说明,经审核人员认可并签字后,附于本底稿后。]

标准的审计工作底稿(模版)

编制日期

审计组长审核

海关意见

复核意见

复核人员

复核日期

注:“审计发现问题摘要及其依据”栏、“海关意见”栏不够用时,可另附页,但须注明对应《审计工作底稿》编号。

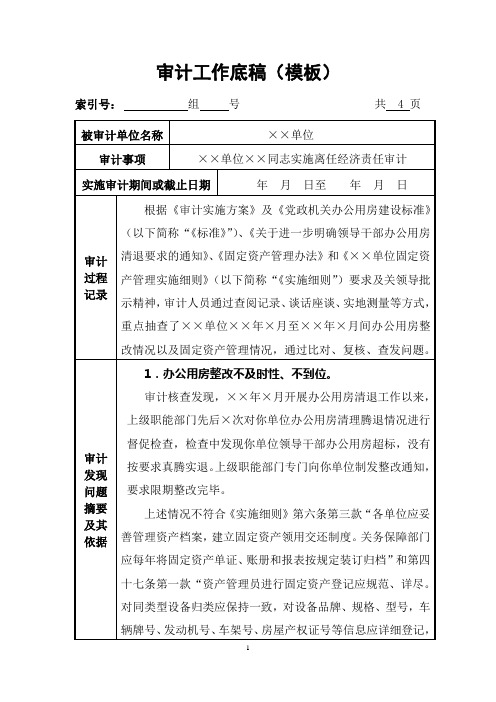

3.办理固定资产登记入帐不及时。

审计核查发现,你单位在固定资产登记不及时。××年×月至××年×月间,你单位共购建固定资产××件,有××件没有及时入关产,占比××%,有的采购时间与入关产时间隔半年之久。

上述情况不符合《实施细则》第四十七条“对于新购固定资产各单位应遵循规范的工作流程,严格审核,及时入账,把好入口关。”“三级预算单位购置的固定资产,在通过验收后由经办人员将申请购置设备的批复文件、发票、设备清单、《固定资产增加单》等相关单据提交本单位资产管理员,由其通过《固定资产管理信息系统》填制并打印《固定资产增加单》,经经办人员签字确认后,随购置费用报账凭证送交财务人员办理固定资产费用报账和新增固定资产财务记账;《固定资产增加单》一式三联,由资产(设备)管理员、财务人员及经办人员(使用部门)各执一联,凭以登记本部门资产实物使用保管账册”的规定。

审计工作底稿(模板)

索引号:组号 共4页

被审计单位名称

××单位

审计事项

××单位××同志实施离任经济责任审计

实施审计期间或截止日期

年月日至年月日

审计过程记录

根据《审计实施方案》及《党政机关办公用房建设标准》(以下简称“《标准》”)、《关于进一步明确领导干部办公用房清退要求的通知》、《固定资产管理办法》和《××单位固定资产管理实施细则》(以下简称“《实施细则”)要求及关领导批示精神,审计人员通过查阅记录、谈话座谈、实地测量等方式,重点抽查了××单位××年×月至××年×月间办公用房整改情况以及固定资产管理情况,通过比对、复核、查发问题。

how to prepare good audit working paper审计工作底稿