国际会计课后题答案版

国际会计第七版英文版课后答案(第七章)

国际会计第七版英文版课后答案(第七章)预览说明:预览图片所展示的格式为文档的源格式展示,下载源文件没有水印,内容可编辑和复制Chapter 7Financial Reporting and Changing PricesDiscussion Questions Solutions1.Historical-based financial statements may be misleading during periods of significant inflation.Many resources may have been acquired in periods when the purchasing power of the monetary unit was much higher. These expenses then typically are deducted from revenues that reflect current purchasing power. The resulting income number is unintelligible. Another problem for statement readers is that the value of assets recorded at their historical acquisition cost is typically understated as a result of inflation. Understated asset values produce understated expenses and overstated earnings.Financial trends are also difficult to interpret, as trend statistics generally include monetary units of different purchasing power. A positive trend in sales may be due to price changes, not real increases in sales.2. A price index is a cost ratio, that is, the ratio of a representative “basket” of goods and servicesconsumed by an average family, compared to the price of that same basket in a benchmark (“base”) year. The price index is invaluable in enabling a statement reader to translate sums of money paid in the past to their current purchasing power equivalents.3.This statement is partly true and shows the confusion thatsurrounds inflation accounting. Inaccounting for changing prices, users must distinguish between general price changes and specific price changes. General prices refer to the prices of all goods and services in the economy. The object of accounting for general price level changes is to preserve the general purchasing power of a company’s money capital. Specific price changes refer to changes in the prices of specific commodities. The object of accounting for specific price changes is to preserve a company’s productive capacity or operating capability.4.The congressman is wrong. The object of inflation accounting is to clarify the distinction betweencapital and income, not to minimize corporate taxes. Inflation accounting shows how much money the company can pay in expenses, taxes, and dividends, while keeping enough resources to maintain its capital.5.Although it is generally conceded in principle that price level-adjusted financial statements are moreuseful than conventional accounting statements during periods of significant inflation, it is a judgment call to identify exactly when price level-adjusted statements become more meaningful. Asa rule of thumb, executives in Brazil use an inflation rate greater than 10 % per month. Investors inGermany or Switzerland may believe that 5 % inflation per year is alarming. Unfortunately, no one has yet developed a formal, rigorous, easy-to-apply definition of meaningfulness.How does one determine whether the benefits of price level-adjusted accounting information exceed the costs? While the costs to generate such information can be measured, it is muchharder to quantify the benefits. Financial accounting deals with information produced by business enterprises for use by external decision makers. Consequently, measurement of the benefits of price level-adjusted information must cover all user groups in an economy. Multiple user groups, uneven distributions of benefits (both within and between groups), and favorable economy-wide spillover effects of price level information complicate the task. Adding international dimensions makes the problem even worse.6.The U.S. approach resembles the price-level adjusted current cost model, whereas the U.K.approach embraces the current cost model. While both require disclosure of the impact ofchanging prices on monetary items, the U.S. approach basically uses the general price level index to compute monetary gains and losses, whereas the U.K. employs specific prices changes by way of its gearing adjustment.1.The International Accounting Standards Board sanctions use of the general price level model orthe current cost framework. Whichever method is employed, these inflation adjustments must be expressed in terms of constant purchasing power as of the balance sheet date. Purchasing powergains or losses are to be included in current income. Firms adjusting their accounts for changingprices must disclose, at a minimum: a) the fact that end-of-period purchasing power adjustmentshave been made, b) the asset valuation framework employed in the primary financial statements,c) the type of inflation index or indexes employed and theirlevel at the end of the period as wellas their movements during the period, and d) the net purchasing power gain or loss on netmonetary items held during the period. Given the options that are available, analysts mustunderstand the differences between the approved inflation accounting methods to be able tocompare companies choosing one option over the other and to assure proper interpretation ofinflation adjusted amounts.2.The historical cost-constant dollar model measures the impact of general price level changes on afirm's reported performance and financial position. The current cost model examines the impact of specific price changes on enterprise income and wealth.The two measurement frameworks are similar in that both attempt to clarify the distinction between capital and income. They differ in reporting objectives. Whereas the historical cost/constant dollar model attempts to preserve the general purchasing power of a firm's original money capital, the current cost model attempts to preserve an entity's physical capital or productive capacity.3.Your authors think that restating foreign and domestic accounts to their current cost equivalentsproduces information that is far more helpful to investor decisions than historical cost methods, whether or not adjusted for changes in general price levels. Such information provides a performance measure that signals the maximum amount of resources that enterprises can distribute without reducing their productive capacity. It also facilitates comparisons ofconsolidated data.10. The gearing adjustment is an inflation adjustment that partially offsets the additional charges toincome associated with assets whose values are restated for inflation (e.g., higher depreciation and cost of sales). This adjustment recognizes that borrowers generally gain from inflation because they can repay their debts with currency of reduced purchasing power. Hence, it is unnecessary to recognize the higher replacement cost of inventory and plant and equipment in the income statement so far as they are financed by debt.11. Accounting for foreign inflation differs from accounting for domestic inflation in two major ways.First, foreign rates of inflation often are higher than domestic rates, which increases potential distortions in an entity's reported results from changing prices. Second, as foreign exchange rates and differential national rates of inflation are seldom perfectly negatively correlated, care must be taken to avoid double-dipping when consolidating the results of foreign operations.12.Double-dipping refers to methods that count the effects of foreign inflation twice in reportedearnings. Earnings are reduced once when cost of sales is adjusted upwards for inflation, andagain when inventories are translated to domestic currency using a current exchange rate, whichyields a translation loss. Since the change in the exchange rate itself was caused by inflation, the result is a double charge for inflation.Exercise Solutions1.This exercise is a good way to test students’ understanding of the various approaches toaccounting for changin g prices. Vestel’s earnings numbers are based on the general price levelmodel whereas Infosys is measuring its performance based on a current cost framework. Modello goes a step further and adjusts its current cost statements for changes in the general price level.Some may feel that current cost data, which is based on the notion of replacement costs, is toosubjective a notion to be reliable. Since general price level data are based on general price level indices, the numbers appearing in Vestel’s income statement are much more objective andfacilitates comparisons among companies using a similar methodology. Moreover, Vestel’sstatements do not violate the historical cost doctrine. Others will argue that the value of stockinvestments are based on discounted future cash flows. Accordingly, the current cost framework provided by Infosys is more germane to investor decisions as it measures the amount of earnings that could be distributed as dividends without reducing the firm’s future dividend gen eratingpotential. Moreover, current cost earnings, including the gearing adjustment , reflects how thefirm is impacted by prices that are more germane to the firm, as opposed to the general public.Some will argue that Modello’s income statement combin es the best of both worlds. However,there is merit to the argument that the income statementshould measure the performance of thefirm and that this is best accomplished with the current cost framework. Since individualinvestors are affected by the g eneral price level, they should adjust their share of a firm’s current cost earnings distributions for general inflation.2. a.Income Statement Historical Price Level Historical Cost-Cost Adjustment Constant Dollar Revenue MXP 144,000,000 420/340 MXP 177,882,353 Operating expenses (86,400,000) 420/340 (106,729,412) Depreciation (36,000,000) 420/263 (57,490,494)Operating income MXP 21,600,000 MXP 13,662,447a Monetary gains(losses) - (73,248,759)Net income MXP 53,280,000 MXP(59,586,312)Balance SheetCash MX(P 157,600,000 420/420 MXP 157,600,000Land 180,000,000 420/263 287,452,471Building 720,000,000 420/263 1,149,809,885Acc. Depreciation (36,000,000) 420/263 (57,490,494)Total MXP 1,021,600,000 MXP 1,537,371,862Owners' equity(beg.) MXP1,000,000,000 rolled forward b MXP 1,596,958,174Net income (loss) 21,600,000 (59,586,312)Owner's equity MXP 1,021,600,000 MXP 1,537,371,862(end)a Monetary loss:CashBeginning balance 1,000,000,000 420/263 1,596,958,174 Purchase ofreal estate ( 900,000,000) 420/263 (1,437,262,356)Rental revenues 144,000,000 420/340 177,882,353Operating expenses (86,400,000) 420/340 106,729,412)157,600,000 230,848,759-157,600,000 Monetary loss (73,248,759)b Beginning equity x price level adjustment = adjusted amount= P 1,000,000,000 x 420/263 = P 1,596,958,1742.b.Cost HC/Constant DollarReturn on Assets 21,600,000 (59,586,312)1,021,600,000 1,537,371,862= 2.1% = -3.9%Cost-based profitability ratios tend to provide a distorted (overstated) picture of a company's operating performance during a period of inflation.3.20X7 20X8Cash MJR 2,500 MJR 5,100Current liabilities (1,000) (1,200)LT-Debt (3,000) (4,000)Net monetary liabilities MJR (1,500) MJR (100)Zonolia Enterprise’s net monetary liability position changed by MJR1,400 during the year (MJR100) –(MJR1,500).4.Nominal Restate for ConstantMJR’s Majikstan GPL MJR’sNet monetary liab.'s MJR 1,500 x 32,900/30,000 = MJR1,645 12/31/X7Decrease during year (1,400) = (1,400)Net monetary liab.'s MJR 100 x 32,900/36,000 = MJR 9112/31/X8Monetary (general purchasing power) gain MJR 1545. Historical Current Cost Current Income Statement Cost Adjustment Cost Revenues MXP 144,000,000 - MXP 144,000,000 Operating expenses 86,400,000 - 86,400,000 Depreciation (36,000.000) 1.8 64,800,000 Net Income (loss) MXP 21,600,000 MXP (7,200,000)Balance SheetCash MXP 157,600,000 - P 157,600,000 Land 180,000,000 1.9 342,000,000 Building 720,000,000 1.8 1,296,000,000 Acc. Depreciation (36,000,000) 1.8 (64,800,000) Total MXP1,021,600,000 MXP 1,730,800,000 Owners' Equity Beg. Balance MXP1,000,000,000 MXP 1,000,000,000 OE revaluation a - 738,000,000Net income (loss) 21,600,000 (7,200,000) Total MXP1,021,600,000 MXP 1,730,800,000a Revaluation of land MXP 162,000,000Revaluation of building 576,000,000MXP 738,000,0006. Solution in 000,000's:MJR8,000 X 137.5/100.0 = MJR11,00020X7 20X8Current cost MJR8,000 MJR11,000Acc. depreciation (1,600) (3,300)aNet current cost MJR6,400 MJR7,700a Current cost depreciation = MJR800 X 137.5/100.0 = 1,100per year for 3 years.7. As no new assets were acquired during the year, we must determine to what extent the MJR3,000 increase in the current cost of Zonolia's equipment exceeded the change in the general price level during the year. The appropriate calculation follows: MJR11,000 - [MJR8,000 X 36,000/30,000]= MJR11,000 - MJR9,600= MJR1,400Alternatively, if we follow the FASB’s sug gested methodology, where calculations are expressed in average (20X8) dollars, current cost depreciation would be computed by reference to the average current cost of the related assets. Thus, Current cost, 12/31/X7 MJR8,000,000Current cost, 12/31/X8 11,000,000MJR19,000,000Average current cost MJR19,000,000/2 = MJR9,500,000Current cost depreciation at 10% = MJR950,000Increase in current cost of equipment, net of inflation (000's): Current Restate for Current cost/Cost Inflation Constant Zonos Current cost, net12/31/X7 MJR6,400 X 32,900/30,000 MJR7,019Depreciation (950) (950)Current cost, net12/31/X8 7,700 X 32,900/36,000 7,037MJR 2,250 MJR968The increase in the current cost of equipment, net of inflation is MJR968. The difference between the nominal renge amount (MJR2,250) and constant renges (MJR968) is the inflation component of the equipment's current cost increase.8. Restate-translate method:Constant Translate $ Equivalentsrenges of constantrengesIncrease in currentcost of equip., netof inflation MJR968,000 X 1/4,800 = $202Translate-restate method:CC (MJR) Translate CC ($) Restate CC/ Constant $U.S. GPLCC, net MJR 6,400,000 x 1/4,800 = $1,333 x 292.5/281.5 = $1,38512/31/X7Dep. (950,000) x 1/4,800 = (198) = (198)CC, net 7,700,000 x 1/4,800 = 1,604 x 292.5/303.5 = 1,54612/31/X8MJR 2,250,000 $ 469 $ 3599.20X7 20X8£m £mTrade receivables 242 270-Trade payables (170) (160)Net monetary working capital 72 110Change in monetary working capital = £38 (£110 - £72) Nominal Restate for Constant£British PPI £Net monetary W/C 72 X 110/100 = 79.212/31/20X7Increase during year 38 = 38.0Net monetary W/C 110 X 110/120 = 100.812/31/20X8Monetary working capital adjustment = (16.4)aa This amount is added to the current cost adjustments for depreciation and cost of sales because trade receivables exceeded trade payables, thus tying up working capital in an asset that lost purchasing power.Gearing adjustment:[(TL – CA)/(FA + I + MWC)] [CC Dep. Adj. + CC Sales Adj. + MWCA]where TL = total liabilities other than trade payablesCA = current assets other than trade receivables and inventoryFA = fixed assets including investmentsI = inventoryMWC = monetary working capitalCC Dep. Adj. = current cost depreciation adjustmentCC Sales adj. = current cost of sales adjustmentMWCA = monetary working capital adjustment= [(128 – 75)/(479 + 220 + 110] [£m 216]= [.066 ] [216]= £14.3The only number I could readily identify in problem 9 is inventory of 220. The next number I could come close on is fixed assets. Looks like the solution above says 479, the text for 08 indicates 473. I could not see where the 110 (MWC) came from. Neither is it clear where the other 3 items in brackets came from. The solution needs to be clearer before I can check the numbers.This gearing adjustment of £14.3 million is subtracted from the current cost of sales and depreciation adjustments. It represents the purchasing power gain from using debt to finance part of the firm's operating assets.a.Nominal Thai Historical Translation U.S.baht inflation c ost/constant rate dollaradjustment baht equivalentInven-tory BHT500,000 x 100/200 = BHT250,000 x .02 = $5,000b.Nominal Translation U.S. U.S. Historicalbaht rate dollar inflation c ost/constantequivalent adjustment dollarsInven-tory BHT500,000 x .02 = 10,000 x 180/198 = $9,090Sorry this seems confusing compared to number 2 where the year end index was in the numerator and either the beginning or average index was in the denominator (e.g. 420/340 or 420/263). It is not clear why we do the opposite here where the Thai price level doubles and we put the 200 in the denominator and 100 in the numerator.c. Most students will prefer the restate-translate method. This approach has merit if general and specific pricelevels move in tandem. If not, neither approach is satisfactory as both are based on a historical cost valuation framework that is generally irrelevant for investment decisions.d. For reasons enumerated in this chapter, we favor restating local currency assets for specific price changesand then translating these current cost equivalents to dollars using the current exchange rate.11. We assume that Doosan Enterprises translates its inventory at the current rate and adjusts its cost ofsales for inflation by simulating what it would have been ona LIFO basis. Two adjustments are necessarybecause local inflation impacts exchange rates used to translate foreign currency inventory balances to dollars.With FIFO inventories, a translation loss is recorded in "as reported" earnings when it is originally translatedto U.S. dollars by a current exchange rate that changed (devalued) during the period. This translation loss isan indirect charge for local inflation. The inflation adjustment (simulated LIFO charge) to increase "as reported" cost of sales to a current cost basis is an additional charge for inflation. Absent some offsettingentry, consolidated results would be charged twice for inflation. To avoid this double charge, the translation loss embodied in reported earnings is deducted from the simulated LIFO charge to arrive at a net U.S. dollarcurrent cost of sales adjustment. Steps in the adjustment process are as follows:1. FIFO inventory subject to simulated LIFO charge KRW10,920,0002. Restate line 1 to January 1 currency units(KRW10,920,000 x 100/120). The result is anapproximation of December 31 LIFO inventory KRW9,100,0003. Difference between FIFO and LIFO inventorybalances (line 1 minus line 2) is the additionallira LIFO expense (current cost adjustment)for the current year. KRW1,820,0004. Translate line 3 to dollars at the January 1exchange rate (KRW1,820,000 ÷ 900). The resultis the additional dollar LIFO expense for thecurrent year $ 2,0225. Calculate the translation loss on FIFO inventory(line 1) that has already been reflected in "asreported" results:a. Translate line 1 at Januaryexchange rate (KRW10,920,000 ÷ KRW900) $ 12,133b. Translate line 1 at December 31exchange rate (L 10,920,000 ÷ KRW1,170) $ 9,333c. The difference is the translationloss in “as reported” results $ (2,800)6. The difference between lines 4 and 5c isthe cost of sales adjustment in dollars:a. Additional dollar LIFO expense fromline 4. $ 2,022b. Less: Inventory translation loss alreadyreflected in "as reported” results (fromline 5c) $ (2,800)c. The difference is the net dollar currentcost of sales adjustment $ (778)Here, the current cost of sales adjustment is negative (i.e., reduces the dollar cost of sales adjustment). This is because the won devalued by more than the differential inflation rate (assuming a U.S. inflation rate close to zero). If the lira devalued by less than the differential inflation rate, the cost of sales adjustment would have been positive.12.1. Cost of fixed assets at 12/31 EUR20,0002. FIFO inventory at 12/31 EUR 8,0003. Total EUR28,0004. Less: Owners' equity at 12/31 EUR 2,0005. Liabilities used to financefixed assets and inventory EUR26,0006. Restate liabilities to beginningof period markka (EUR26,000 X300/390) EUR20,0007. Purchasing power gain EUR 6,0008. Purchasing power gain inpounds (EUR 6,000/EUR 1.5) £4,0009. Translation gain on appliedliabilities(EUR 26,000/EUR 1.5 -EUR26,000/EUR1.95) £4,00010. Net purchasing power gain £ -0-In this case the translation gain on liabilities used to finance nonmonetary assets equals the purchasing power gain because the currency devaluation matched the differential inflation of 30%. Hence, no purchasing power gains would be recognized.Case 7-1 SolutionCase 7.1 Kashmir Enterprises1.a–cHistorical Price Level HistoricalCost Adjustment Cost ConstantIncome Statement RupeesRevenues INR6,000,000 160/144 I NR6,666,667Cost of Sales 2,560,000 160/128 3,200,000Selling & Admin. 1,200,000 160/144 1,333,333Depreciation 160,000 160/128 200,000Interest 240,000 160/160 240,000Monetary gains (losses)a - 741,666Net Income INR1,840,000 INR2,435,000Balance SheetCash INR2,480,000 160/160 I NR2,480,000 Inventory 480,000 160/128 600,000Building 3,200,000 160/128 4,000,000Accu. depreciation (160,000) 160/128 (200,000) Total INR6,000,000 INR6,880,000Accounts payable INR 620,000 160/160 I NR 620,000 Notes payable 2,400,000 160/160 2,400,000 Owners' equity 2,980,000 3,860,000INR 6,000,000 INR6,880,000a Monetary gains/(losses):CashBeg. balance INR 720,000 160/128 INR1,150,000 Down payment (800,000) 160/128 (1,000,000) Sales 6,000,000 160/144 6,666,667Selling & Adm. exp. (1,200,000) 160/144 (1,333,333) Payment on account (2,200,000) 160/144 (2,444,444) Interest (240,000) 160/160 (240,000)INR 2,480,000 INR2,798,890-2,480,000Monetary loss INR (318,890)a Monetary gains and losses:Accounts PayableBeg. balance INR 420,000 160/128 INR525,000 Purchases 2,400,000 160/128 3,000,000Payments on account (2,200,000) 160/144 (2,444,444) INR 620,000 INR1,080,556- 620,000Monetary gain INR 460,556a Monetary gains/(losses):Notes PayablePurchase warehouse INR 2,400,000 160/128 INR 3,000,000 - 2,400,000Monetary gain INR 600,000Net monetary loss: INR(318,890) + INR460,556 + INR600,000 = INR741,666.Current Cost Financial StatementsHistorical Adjustment Current Cost Income Statement Cost F actor EquivalentsRevenues INR6,000,000 - INR 6,000,000Cost of Sales 2,560,000 1.3 3,328,000Selling and adm. 1,200,000 - 1,200,000Depreciation 160,000 1.4 224,000Interest 240,000 - 240,000Net Income INR 1,840,000 INR1,008,000Balance SheetCash INR 2,480,000 - INR 2,480,000Inventory 480,000 1.3 624,000Building 3,200,000 1.4 4,480,000Acc. depreciation 160,000 1.4 224,000Total INR 6,000,000 INR 7,360,000Accounts payable INR 620,000 - INR 620,000Notes payable 2,400,000 - 2,400,000Owners' equity 2,980,000 4,340,000INR 6,000,000 INR 7,360,0002. Your authors favor current cost over historical or historical cost/constant dollar financial statements. Finance theory states that investors are interested in a firm's dividend-generating potential, as the value of their investment depends on future cash flows. A firm's dividend-generating potential, in turn, is directly related to its productive capacity. Unless a firm preserves itsproductive capacity or physical capital(e.g.,plant, equipment, inventories), dividends can’t be sustained over time. Under these circumstances, current cost financial statements give investors information important to their decisions. They show the maximum resources that a firm can distribute to investors without impairing its operating capability.3.Translate-Restate MethodBalance Sheet, Jan. 1Local Currency Trans. Dollar Inflation Historical costRate Equivalents Adjustment Constant $Cash INR 920,000 .025 $23,000 - $23,000Inventory 640,000 .025 16,000 - 16,000 Total INR1,560,000 $39,000 $39,000A/P INR 420,000 .025 $10,500 - $10,500 Owners' equity 1,140,000 .025 28,500 - 28,500 Total INR 1,560,000 $39,000 $ 39,000Income StatementDec. 31Revenues INR 6,000,000 .022 $ 132,000 108/104 $ 137,077 Cost of sales 2,560,000 .022 56,320 108/100 60,825Selling & Adm. 1,200,000 .022 26,400 108/104 27,415 Depreciation 160,000 .022 3,520 108/100 3,802 Interest 240,000 .022 5,280 108/108 5,280Net Income INR 1,840,000 $ 40,480 $ 39,755 Monetary gains (losses)a - - 4,468$44,223a Monetary gains/(losses):CashBeg. Bal INR 920,000 .02 $ 18,400 108/100 $ 19,872Downpayment (800,000) .02 (16,000) 108/100 (17,280) Sales 6,000,000 .02 120,000 108/104 124,615Selling & Adm. (1,200,000) .02 (24,000) 108/104 (24,923)Payments on Acc. (2,200,000) .02 (44,000) 108/104 (45,692) Interest (240,000) .02 (4,800) 108/108 (4,800)INR 2,480,000 $ 49,600 51,792-49,600Monetary loss $ (2,192) Accounts PayableBeg. Bal. INR 420,000 .02 $ 8,400 108/100 $ 9,072Purchases 2,400,000 .02 48,000 108/100 51,840Pmt. on acc. (2,200,000) .02 (44,000) 108/104 45,692INR 620,000 $ 12,400 $ 15,592- 12,400Monetary gain $ 2,820Notes payablePur. W/house Rpe 2,400,000 .02 $ 48,000 108/100 $ 51,840 48,000Monetary gain $ 3,840Netmonetary gain: $(2,192) + $2,820 + $3,840 = $4,468.Balance Sheet Local Trans. Dollar Inflation Historical cost- Dec. 31 Currency Rate Equiv. Adjustment Constant $Cash INR 2,480,000 .02 48,600 108/108 $ 48,600 Inventory 480,000 .02 9,600 108/100 10,368 Building 3,200,000 .02 64,000 108/100 69,120Acc. Dep. 160,000 .02 3,200 108/100 3,456Total INR 6,000,000 $120,000 $ 124,632Acc. payable 620,000 .02 12,400 108/108 $ 12,400Notes payable 2,400,000 .02 48,000 108/108 48,000Trans. adj.b - (9,380) (9,978)Owners' equity c 2,980,000 68,980 74,210Total INR 6,000,000 $120,000 $124,632________________________________________________________________ __b Translation adjustment:Beginning net assets Rpe 1,140,000 (.02 - .025) = $ (5,700) X 108/100 = $(6,156)Increase in net assets Rpe 1,840,000 (.02 - .022) = (3,680) X 108/104 = $(3,822)$(9,380) $(9,978) c Balancing residualRestate - Translate MethodBalance Sheet Local Inflation Historical Cost- Trans. D ollar Jan 1. Currency Adjustment Constant rupee Rate equivalents Cash INR 920,000 128/128 INR 920,000 .025 $ 23,000 Inventory d 640,000 128/128 640,000 .025 16,000Total INR1,560,000 INR1,560,000 $ 39,000Acct. payable INR 420,000 128/128 INR 420,000 .025 $ 10,500Owner's equity 1,140,000 1,140,000 28,500Total INR 1,560,000 INR 1,560,000 $ 39,000d Assumes inventory acquired near year-end.Income StatementYear ended Dec. 31Revenues INR 6,000,000 160/144 INR 6,666,666 .022 $ 146,667Cost of Sales 2,560,000 160/128 3,200,000 .022 70,400 Selling & Adm. 1,200,000 160/144 1,333,333 .022 29,333 Depreciation 160,000 160/128 200,000 .022 4,400Interest 240,000 160/160 240,000 .022 5,280Net Income INR1,840,000 INR1,693,334 $ 37,254 Monetary gains(losses)a- 741,666 .022 16,317INR2,435,000 $ 53,571Balance SheetDec. 31Cash INR 2,480,000 160/160 INR 2,480,000 .02 $ 49,600Inventory 480,000 160/128 600,000 .02 12,000Building 3,200,000 160/128 4,000,000 .02 80,000Acc. deprec. 160,000 160/128 200,000 .02 4,000Total INR 6,000,000 INR 6,880,000 $137,600Acc. payable INR620,000 160/160 INR 620,000 .02 $ 12,400 Notes payable 2,400,000 160/160 2,400,000 .02 48,000Owner's equity 2,980,000 3,860,000 87,770 Translation adj.b - (10,570)Total INR 6,000,000 INR 6,880,000 $137,600________________________________________b Beginning net assets INR1,140,000 (.02 - .025) = $ (5,700)Change in net assets 2,435,000 ).02 - .022) = $(4,870)$(10,570)Both methods are inadequate for American investors because they are based on the historical cost valuation framework. A better reporting procedure is to restate local accounts to their current cost equivalents, then translate these amounts to the reporting currency using the year-end (current) foreign exchange rate. This is illustrated here.Restate (current cost)/Translate (current rate)Cash INR 920,000 - INR 920,000 .025 $ 23,000Inventory 640,000 - 640,000 .025 16,000Total INR 1,560,000 INR1,560,000 $ 39,000Acc. payable INR 420,000 - INR 420,000 .025 $ 10,500Owner's equity 1,140,000 - 1,140,000 28,500。

国际会计练习册答案 (上海财经大学出版社)

第十一章习题解答一、名词解释1国际税收:国际税收通常指两个或两个以上的主权国家或地区,由于对参与国际经济活动的纳税人行使税收管辖权而引起的一系列国家之间税收活动。

其实质是国家与国家之间的税收关系。

这种税收关系主要表现在两个方面。

第一,国家与国家之间的税收分配关系。

第二,国家与国家之间的税收竞争和税收协调关系。

2国家税收:国家税收是以国家政治权利为依托的强制性课征形式,国家税收涉及的是国家在征税过程中形成的国家与纳税人之间的利益分配关系,国家税收按课税对象不同存在不同的独立税种。

3国际重复征税:当两个或两个以上的国家对同一跨国纳税人的同一跨国所得(或财产)征收两次或两次以上性质相同的税收时,就出现了国际重复征税的结果。

国际重复征税是不同国家税收管辖权交叉重叠的结果,因此要了解国际重复征税问题,首先要弄清税收管辖权问题。

4税收管辖权:税收管辖权是一个主权国家在税收管理方面所行使的在一定范围内的征税权力,属于国家主权在税收领域中的体现。

5领土原则:领土原则指一个国家对其所属领土内的人、物和发生的事件,都有权按照本国的法律实施管辖。

这是由属地最高权原则引伸出来的管辖权,所以又称为属地原则。

6国籍原则:国籍原则指一个国家有权对一切有本国国籍的人实行管理,而不管这个人是居住在国内还是国外。

这是由属人最高权原则引伸出来的管辖权,所以又称为属人原则。

税收管辖权就是基于属地原则和属人原则而产生的。

7地域税收管辖权:地域税收管辖权,又称收入来源地管辖权。

即一个主权国家有权对来源于本国境内的所得征税,不管它是本国人的所得还是外国人的所得。

这里的所得包括经营所得(营业利润)、劳务所得、投资所得和财产所得。

8居民税收管辖权:居民税收管辖权,即一个主权国家有权对符合本国税法中规定条件的居民(自然人或法人)的所得征税。

这里的居民概念不同于行政管理法中居民的概念,它是税法上根据住所、注册地、居住意愿等因素确定的。

9公民税收管辖权:公民税收管辖权,即一个主权国家有权对拥有本国国籍的公民的所得征税。

国际会计练习册答案 (上海财经大学出版社)

第一章练习题解答习题1.名词解释1.1国际会计的概念: 国际会计(International Accounting)。

国际会计内容广阔但研究时间较短,因此,较难有一个确切的定义。

美国加州理工大学教授M.Zafar Iqbal等认为,国际会计是针对国际间经济业务的会计,是对不同国家会计准则的比较,以及世界范围内的会计准则的协调。

而美国会计学家Weirch 和Anderson则进一步将国际会计细化为三个概念,即跨国公司会计(Multinational Corporation Accounting)、比较会计(Comparative accounting)和世界会计(World Accounting)。

1.2跨国公司会计: 从跨国公司会计视角认为国际会计主要是为了处理跨国公司母公司与子公司之间的会计问题,其研究领域较为狭窄,应用范围较为单一,只是停留在国际会计产生的直接动因——国际贸易与跨国公司这一点上,而未将其理论全面化和高度化。

因此,代表的只是国际会计发展的初级对各个国家不同的会计模式进行研究和比较。

包括各国的会计理论、会计准则、会计实务、会计环境等。

1.3比较会计: 相对跨国公司会计而言,比较会计上升到了一定的高度和深度,是由点及面、从具体到抽象的质的飞跃,同时,又是承上启下的关键性转折。

因为它不仅是对跨国公司会计的扩充与深化;更主要的是为世界会计奠定了坚实的基础。

1.4世界会计: 世界会计是从全球的角度出发,致力于建设一套世界各国普遍接受的统一和标准的会计模式,这是国际会计的理想和终极奋斗目标,其意义是显而易见的。

它能使会计更好地为世界经济一体化而服务。

但由于会计受社会环境和经济环境的制约与影响,各个国家的政治、法律、经济及文化背景的巨大差异,使得这一工程必将是艰巨而困难的而只有经历了比较会计这一阶段,通过对各个国家会计情况的分析与对比,才能综合制定出全球统一的会计模式。

因此,世界会计是建立在比较会计基础之上的,目前及未来国际会计研究的重点。

国际会计第9版课后答案pdf

国际会计第9版课后答案pdf1、某公司为一般纳税人,2019年6月购入商品并取得增值税专用发票,价款100万元,增值税率13%;支付运费取得增值税专用发票,运费不含税价款为30万元,增值税率9%,则该批商品的入账成本为()。

[单选题] *A.130万元(正确答案)B.7万元C.3万元D.113万元2、下列项目中,不属于非流动负债的是()[单选题] *A.长期借款B.应付债券C.专项应付款D.预收的货款(正确答案)3、.(年嘉兴三模考)()就是会计在经济管理中固有的、内在的客观功能。

[单选题] * A会计的含义B会计的特点C会计的任务D会计的职能(正确答案)4、.(年浙江省第二次联考)会计人员的职业道德规范不包括()[单选题] *A操守为重、不做假账(正确答案)B爱岗敬业、诚实守信C、廉洁自律、客观公正D坚持准则、提高技能5、企业出售固定资产应交的增值税,应借记的会计科目是()。

[单选题] *A.税金及附加B.固定资产清理(正确答案)C.营业外支出D.其他业务成本6、.(年嘉兴二模考)企业对固定资产计提折旧以()假设为基本前提。

[单选题] *A会计主体B持续经营(正确答案)C会计分期D货币计量7、某企业自创一项专利,并经过有关部门审核注册获得其专利权。

该项专利权的研究开发费为15万元,其中开发阶段符合资本化条件的支出8万元;发生的注册登记费2万元,律师费1万元。

该项专利权的入账价值为()。

[单选题] *A.15万元B.21万元C.11万元(正确答案)D.18万元8、.(年浙江省高职考)下列项目中,不属于企业会计核算对象的经济活动是()[单选题] *A购买设备B请购原材料(正确答案)C接受捐赠D利润分配9、企业生产车间使用的固定资产发生的下列支出中,直接计入当期损益的是( )。

[单选题] *A.购入时发生的安装费用B.发生的装修费用C.购入时发生的运杂费D.发生的修理费(正确答案)10、已达到预定可使用状态但未办理竣工决算的固定资产,应根据()作暂估价值转入固定资产,待竣工决算后再作调整。

国际会计课后题答案第七章,第八章整理版

一、讨论题7.1对比本章引述的金融工具的3个定义,说明各自的特点。

经济学家和金融界所举的定义都把金融工具界定为金融领域运用的单证:史密斯的定义把金融工具表述为“对其他经济单位的债权凭证和所有权凭证”,而《银行与金融百科全书》的定义中列举了金融领域运用的各种单证。

FASB和IASC所下的定义基础是一致的,都把金融工具界定为现金、合同权利或义务及权益工具。

IASC 的定义较清晰,在指明金融工具是“形成个企业的金融资产并形成另一企业的金融负债或权益工具的合同”后,又分别就金融资产、金融负债和权益工具下了定义。

7.2对比本章引述的衍生金融工具的4个定义,说叫各自的特点。

OECD的定义指叫衍生金融工具是“一份双边合约或支付交换协议”,ISDA定义中的表述是“有关互换现金流量和旨存为交易名转移风险的双边合同”。

后名的表述更清晰。

两个定义都着币指明衍生金融工具价值的“衍生性”,并指明可作为衍生价值的基础的标的。

两者都列举了各种不同的标的。

FASB和IASC所下的定义基本上是致的,更便于作为衍生金融工具交易的会计处理所依据的概念。

讨论时可参照教本中归纳的6项最基本的特征展开(本章教学要点(二)第3点中的(2)也有简括的表述)。

7.3区分金融资产和负债与非金融资产和负债项日是否等同于区分货币性资产和负债与非货币性资产和负债项日?请予以说明。

不等同。

形成收取或支付现金或另金融资产的合同权利或义务,是金融资产和负债的最摹本的特征,以此(合同权利或义务)区别于非金融资产和负债(参阅教术7 2 1),而货币性资产和负债与非货币性资产和负债的区分则是根据这些项目对通货膨胀影响或汇率变动的不同反应而作出的。

二者是完全不相下的两种分类法。

更为币要的是,不要把“货币性金融资产和负债”与“货币性资产和负债”这两个概念相混淆。

前名是指“将按固定或可确定的金额收取或支付的金融资产和金融负债”,只是金融资产和金融负债的特定类别。

7.4衍生金融工具品目繁多,但其基本形式不外乎:(1)远期合同;(2)期货合同:(3)期权合同:(4)互换(掉期)合同。

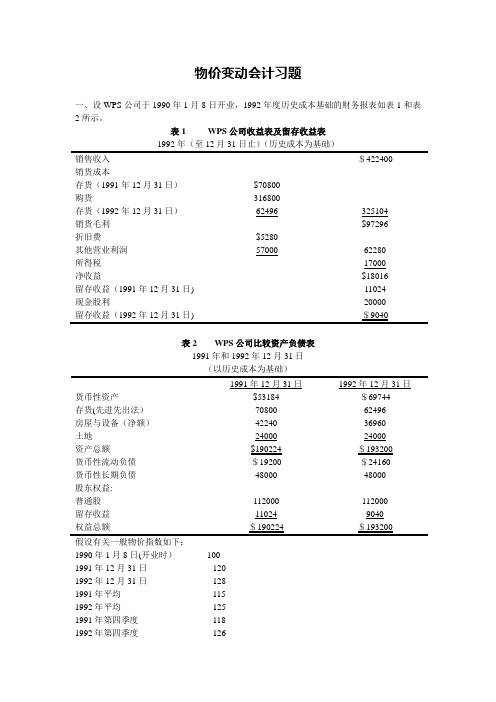

复旦大学-国际会计--习题及答案

物价变动会计习题一、设WPS公司于1990年1月8日开业,1992年度历史成本基础的财务报表如表1和表2所示。

表1 WPS公司收益表及留存收益表1992年(至12月31日止)(历史成本为基础)销售收入$422400销货成本存货(1991年12月31日)$70800购货316800存货(1992年12月31日)62496 325104销货毛利$97296折旧费$5280其他营业利润57000 62280所得税17000净收益$18016留存收益(1991年12月31日) 11024现金股利20000留存收益(1992年12月31日) $9040表2 WPS公司比较资产负债表1991年和1992年12月31日(以历史成本为基础)1991年12月31日1992年12月31日货币性资产$53184 $69744存货(先进先出法)70800 62496房屋与设备(净额)42240 36960土地24000 24000资产总额$190224 $193200货币性流动负债$19200 $24160货币性长期负债48000 48000股东权益:普通股112000 112000留存收益11024 90401990年1月8日(开业时)1001991年12月31日1201992年12月31日1281991年平均1151992年平均1251991年第四季度1181992年第四季度126再假设其他有关重要资料如下:(1)每年均按先进先出法计量存货,每年末的库存存货均为当年第四季度均匀购入。

(2)房屋与设备、土地均于开业时一次性购置,按10年、直线法提房屋与设备的折旧,不考虑预计净残值。

(3)普通股均于开业时对外发行。

(4)当年的销货收入、购货成本、其他营业费用与所得税在当年内均匀发生.(5)现金股利的分派在1992年12月31日完成。

(6)一般购买力为年末美元。

1、要求:按照一般购买力会计模式重编资产负债表、收益和留存收益表以及购买力损益计算表以上题中的表1与表2为基础,另补充有关资料如下:2、以现行成本为基础的销货成本为$345600。

国际会计练习册答案 (上海财经大学出版社)

第四章练习题解答1.名词解释1.1国际会计协调:国际会计协调是指对各国会计规范和会计信息的差异程度加以限制,从而增加会计信息在国际范围内的可比性的过程。

对国际会计协调的范畴完整、正确的认识,必须把握和理解以下几个方面。

(1)国际会计协调不是国际会计标准化,而是指各国会计规范和会计信息向接近的或一致的方向努力。

国际会计标准化,即全球共用一个统一的会计与报告标准,这是不可能实现的。

(2)国际会计协调的目的是追求会计信息在国际范围内的可比性和可理解性。

会计信息最终体现在财务报告上,而财务报告提供的主要是财务会计的信息,因此,对国际会计协调的对象主要是财务会计而不是管理会计。

财务会计的目的是为了向信息使用者提供决策有用的会计信息,为了满足多方面信息需求者的需要,各国大都建立了一套会计准则和会计制度来约束企业的财务会计和报告。

要使各国企业间的财务会计信息有可比性和可以理解性,就必须对各国会计准则和制度进行协调。

因此,国际会计协调的直接对象和内容是协调各国的会计规范。

(3)国际会计协调是建议性的,而不是强制性的,它是参与协调的各国共同协商的结果,它的最终方向是使先进的会计理论和方法在世界范围内得到推广和应用。

1.2会计国际化:会计国际化是指会计随着经济全球化的发展而客观发展起来的不可逆转的超越一国国界的趋向。

1.3会计国际协调化:会计国际协调化是以使不同国家间的财务报告变得更具有可比性、对制定决策更有用为目标的,一种降低国家间财务报告差异的过程。

它着眼于主观的推动和促进,是一个调节国别会计差异的过程。

随着协调化的进展,国别差异将不断缩小甚至在某些方面消失,协调化富有弹性和开放性,在不同时期的不同国际经济环境条件下,协调化可以有不同的含义。

1.4形式性协调:形式协调,是指会计准则的协调。

形式协调是会计协调的基本条件,通过准则协调一致,限制企业在会计实务上的多样化,减少财务报告的差异,进一步提高财务报告实质上的协调程度。

国际会计课后答案 重点

第一章导论2.会计可以被看做是包括三个部分:计量、披露和审计。

这种分类的优点和缺点是什么?你能提出其他有效的分类吗?Advantage: Some might argue that measurement, disclosure, and external auditing are three distinct (although related) processes, involving different members of the company. For example, corporate attorneys often are involved in disclosure issues, but seldom intervene in measurement ssues. The Board of Directors works with the external auditors but not necessarily with the comptroller s office. Thus, discussion of accounting requirements and voluntary accounting choices in different jurisdictions is simplified by focusing on the three components of accounting. Disadvantage: measurement, disclosure and auditing are interdependent, and should not be viewed in isolation of one another. A company choosing to disclose as little as possible, for example, may use accounting measurement approaches that reduce the information content of financial statements, and select an external auditor who will be relatively lenient in enforcing accounting requirements. One alternative classification might include accounting (measurement and disclosure), and auditing. A second classification might include financial reporting (annual and interim reporting, regulatory filings) and ad hoc disclosure (press releases, analyst meetings, etc). Any classification is arbitrary, and potentially useful depending on its purpose.优势:一些人可能认为测量,披露和外部审计是三个不同的(虽然相关)流程,涉及公司的不同成员。

国际会计练习册答案 (上海财经大学出版社)

第六章练习解答(第六章物价变动的国际会计)第一节通货膨胀对公司的影响第二节物价变动的会计处理方法第三节国际财务报告准则与国家规则和实践的比较习题解答1.名词解释1.1通货膨胀。

通货膨胀是指所有社会商品和劳务的一般价格水平或平均价格水平的持续上升。

在通货膨胀时期, 单位货币能买到的商品和劳务的量呈持续下降局面。

因此,通货膨胀也就是货币购买力的下降。

换句话说通货膨胀是指由于流通中纸币数量超过需要所引起的货币购买力下降和物价普通上涨的一种社会经济现象。

根据通货膨胀的程度不同,人们把通货膨胀划分为三类:第一类是指温和的通货膨胀;第二类是指急剧的通货膨胀;第三类是指恶性通货膨胀。

1.2一般购买力法。

一般购买力法是指在考虑总体物价水平的前提下,达到维持资产的实际购买力和所有者权益的会计计量方法。

一般购买力法用价格指数来调整国家货币单位购买力的一般变化。

其目的在于将不同时期的历史成本法下的名义数字转换成同一时期的数字,一般选取资产负债表日,这样使得财务报告中的所有数字都用同一购买力的货币单位来表示。

一般购买力法关注货币价值的上下波动,在财务报表中运用此方法调整会计科目时,必须识别哪些科目该调整、调整的依据(如消费者价格指数)以及在财务报表的哪些地方反映这些调整。

1.3 现值法。

现值法是指基于考虑现值或具体物价变化的会计处理方法。

现值法下更关注公司具体资产的成本或价值的变化,公司只有保持了其资产的原有价值,才会考虑公司的盈利是多少。

其目的是计量公司的有形资产、生产能力或营运资产。

因此,在现值法下,是从有形资产的角度来衡量营运和公司的财务状况。

那末,在现值法下强调公司所拥有的、或使用或出售的有形资产的特定价格变化。

1.4消费者价格指数(CPI):消费者价格指数(Consumer Price Index),是对一个固定的消费品一篮子价格的衡量,主要反映消费者支付商品和劳务的价格变化情况,也是一种度量通货膨胀水平的工具,以百分比变化为表达形式。

国际会计学课后作业

国际会计学》课后作业一(红色字为答案)姓名:学号:成绩:A. Explain to the concepts below1. International accountingInternational accounting is an area of accounting which study on how to treat specific accounting practice of a multinational company or how to provide information of an entity to non-domestic readers 国际会计是一种研究如何处理跨国公司具体的会计实务以及如何向非国内读者提供主体信息的会计领域。

2. goodwillGoodwill is capitalized as the difference between fair value of the consideration given in the exchange and the fair values of the underlying net assets acquired.商誉是在交易中得到的对价的公允价值与潜在净资产的公允价值之间的差额的资本化价值。

4.direct quoteThe exchange rate specifies the number of domestic currency units needed to acquire a unit of foreign currency. 汇率指定一定数量的国内货币单位获得一个单位的外国货币所需要的数量。

5.indirect quoteThe exchange rate specifies the price of a unit of the domestic currency in terms of the foreign currency. 汇率指定的以外国货币为单位的国内货币单位的价格。

国际会计(第七版)课后习题答案作者常勋国际会计教师手册(5-7章)(常勋等)

第5章国际会计协调化■教学目的与要求一、教学目的通过本章和第6章的学习,既要求学生能深刻领会国际会计协调化的含义和当前的强劲趋势,也要求学生了解各种国际性政府间机构(如联合国会计和报告国际准则政府间专家工作组、经济合作与发展组织常设会计准则工作组)、区域性国家联盟(如欧洲联盟)、官方机构国际组织(如证券委员会国际组织)以及民间国际组织(特别是会计职业界的国际组织,如国际会计师联合会和国际会计准则委员会以及区域性会计师联合会)对国际会计协调化所作的努力和成果。

本章介绍除国际会计准则委员会(将在第6章介绍)以外的各主要国际组织的作用和成果。

二、学习要求1.深刻理解国际会计协调化的含义。

2.了解推动国际会计协调化的6个主要国际组织的性质。

3.在推动国际会计协调化的其他国际组织中,关注欧洲会计师联合会和亚太会计师联合会。

4.了解有助于国际会计协调化的其他国际组织。

5.理解联合国会计和报告国际准则政府间专家工作组现今的作用只是推动国际会计协调化的权威性国际论坛。

6.着重理解欧洲联盟是推动国际会计协调化最具成效的区域性国家联盟。

7.了解经济合作与发展组织国际投资和跨国企业委员会及其常设会计准则工作组的活动。

8.了解证券交易委员会国际组织(IOSCO)作为官方机构的国际组织在国际协调中的重要作用。

9.着重理解国际会计师联合会的活动及国际审计准则。

■教学要点、重点与难点一、教学要点(一)国际会计协调化的含义较深入的阐明:1.对国际会计协调化(即会计的国际协调化),至今尚无公认的严谨的定义。

综合各家之说(参见教本),可以把国际会计协调化理解为:(1)国际会计协调化是一个限制和缩小会计差异,形成一套可接受的准则(标准)和惯例的过程;(2)其目的在于促进各国(和地区)的会计实务和财务信息的可比性;(3)国际会计协调化的意图在于归纳不同的会计制度,把多样化的实务组合成能产生共同协作结果的有序结构。

2.国际会计协调化的作用在于:(1)有助于进行国际商贸和经济合作活动;(2)促进了外国企业在国际货币市场融资(特别是在国际资本市场发行证券)时需提供的财务报表的可比性;(3)有利于跨国投资,便于跨国公司合并其分布在世界各地的子公司的财务报表。

国际会计第七版英文版课后答案(第十一章)

Chapter 11Financial Risk ManagementDiscussion Questions1.Enterprise risk management assesses individual risks in the context of a firm’s business strategy. Risksare viewed from a portfolio perspective with risks of various business functions, e.g., FX risk, interest rate risk, political risk and the like, being coordinated by a senior financial manager responsible for keeping top management apprised of critical risks that could interfere with the accomplishment of a firm’sstrategic objectives and devising risk optimization strategies. The variables that management accountants must track include factors both external and internal to the firm and varies from company to company.2.Market risk refers to the risk of loss due to unexpected changes in the prices of currencies, interest rates,commodities, and equities. It is not confined to price changes. Market risk also includes liquidity risk, market discontinuities, credit risk, regulatory risk, tax risk, and accounting risk. An example of a foreign exchange risk is a situation where an exporter invoices a credit sale to a foreign importer in foreign currency and foreign currency devalues prior to payment.3.An FX risk management program includes the following processes:a.Forecasting the expected movement in the relation between the yuan and your domesticcurrency.b.Measuring on a periodic basis your firm’s exposure to fluctuations in the value of the yuan.c.Designing protection strategies that will minimize losses should the yuan revalue.d.Establishing internal controls to measure your performance in hedging the risk of loss fromchanges in the value of the yuan.4.Translation exposure measures the impact of exchange rate changes on the domestic currency equivalentsof a firm s foreign currency assets and liabilities. It is primarily concerned with currency restatement.Transaction exposure measures the cash flow impact of fluctuating currency values on the settlement of commercial transactions denominated in foreign currencies. Transaction exposure is concerned with acurrency conversion (exchange) process. Economic exposure attempts to measure the impact of changing exchange rates on the future revenues, costs, and sales volume of a multinational entity. It is concerned with the temporal effects of exchange rate changes.Although FAS No. 52 attempts to mitigate concern with translation gains and losses (accounting exposure), it does not totally eliminate it. Companies choosing the U.S. dollar as their functional currency will still use the temporal translation method and report translation gains and losses in period income. Companies designating the local currency as the functional currency will find their asset exposures increased as inventories and fixed assets are translated using current exchange rates. While such translation gains and losses bypass income, the adverse effects of currency fluctuations on a company’s consolidated equity will still exist. This is especially likely where loan covenant and other contractual provisions specify minimum debt-to-equity ratios. This suggests that the issue of accounting versus economic exposure is far from settled.5.The chapter lists 10 specific methods to reduce a firm’s exposure to foreign exchange risk in adevaluation-prone country. These techniques, and possible cost-benefit trade-offs, are summarized in the following table.Methods Trade-Offsa. Minimize cash balances in a. Reduced exposure versusdevaluation-prone country higher business andfinancial risk due to possible "cash-outs."b. Remitting excess cash back b. Same as item a.to the parent company.c. Accelerate the collection c. Reduced exposure versusof local currency receivables possible reduction in salesd. Defer payment of local d. Reduced exposure versuscurrency payables impaired local credit ratinge. Speed up payment of e. Reduced exposure versusforeign currency payables foregone earnings on arelatively cheap creditsourcef. Invest local currency cash f. Reduced exposure versusbalances in inventories and higher transaction costsother assets less prone to and possible mis-devaluation loss allocation of corporateresourcesg. Invest in strong currency g. Reduced exposure versusforeign assets higher transaction costsand possible governmentinterference (e.g.exchange controls)h. Raise selling prices h. Reduced exposure versuspotential erosion ofmarket sharei. Invoice exports in hard i. Reduced exposure versuscurrencies possible reduction insales abroadj. Currency swaps j. Reduced translationexposure versus increasedtransaction exposure ifparent assesses theexposed affiliate aninterest charge in hardcurrency6. A multicurrency transactions exposure report differs from a multicurrency translation exposure report in anumber of ways. First, the transactions exposure report has a cash flow orientation instead of a static balance sheet orientation. It includes off balance sheet items that are executory in nature. Finally, a multicurrency transaction exposure report has a local currency orientation, whereas a multicurrency translation exposure report has a parent currency orientation.7.Derivative instruments are formal agreements that transfer financial risk from one party to another. Thevalue of a derivative is derived from its reference to a basic underlying instrument or variable such as a foreign currency receivable or a quantum of foreign exchange. Thus the value of a forward exchange contract is related to the change in the foreign exchange rate times the notional amount being hedged. An important accounting issue is whether derivatives should receive the same accounting treatment as the basic instruments to which they relate. Specifically, should a derivative instrument hedging a foreign currency asset appear in the financial statements as a foreign currency liability? If so, should its valuation base be identical to basic instruments? Do cash flows associated with derivative instruments have thesame economic meaning as those associated with basic instruments? How should gains and losses associated with derivative instruments be reflected in the income statement? Can and should risks attaching to these financial instruments be recognized and measured?8.Student responses should proceed along the following lines. Pele Corporation, a Brazilian firm, hasborrowed a certain sum of British pounds at 9 percent and is worried that the pound will appreciate relative to the real prior to maturity. To hedge this currency risk, it arranges with a bank to swap the pounds borrowed for an equivalent amount of reals for 3 years bearing the same rate of interest. During the 3-year period, it will make periodic interest payments to the bank in reals, and in return, receive periodic interest payments in pounds. At the end of the 3-year period, it will re-exchange the real principal for pounds at the original exchange rate.9. A futures contract is a commitment to purchase or deliver a specified quantity of a financial instrument orforeign currency at a future date at a price set when the contract is made. It differs from a forward contract in several respects. A futures contract is standardized in terms of size and delivery date whereas a forward contract is tailored to a customer’s needs. Futures contracts are freely traded on organized exchanges. In contrast, there is no secondary market for forward contracts as they are private agreements between two parties. Futures contracts are carried at market values with gains or losses taken immediately to income, whereas profits on a forward contract are realized only at the delivery date. Finally, a party to a futures contract must meet periodic margin requirements. In a forward contract, margins are set once, on the date of the initial transaction.10.Fair value hedges are hedges of a firm’s foreign currency assets and liabilities and firm fore ign currencycommitments. Cash flow hedges are hedges of forecasted transactions such as a future sale or purchase.Net investment hedges are hedges of an exposed balance sheet asset or liability position. For qualifying fair value hedges, all changes in the fair value of the derivative and the underlying item that is being hedged are recognized in earnings. For qualifying cash flow hedges, the change in the fair value of the derivative is recognized in Other Comprehensive Income and recognized in earnings when the hedged cash flows affect earnings. For qualifying hedges of a net investment, changes in the fair value of the derivative are recorded in comprehensive income11.In theory, the term highly effective means that gains or losses on hedging instruments should be shouldexactly offset gains or losses on the item being hedged. In practice, it means that gains or losses on the derivative substantially offset the changes in the value or cash flow of the hedged item. Measurement of this attribute is important. If a hedging instrument does not meet the highly effective test, the hedge is terminated and deferred gains or losses on the derivative are recognized immediately in current earnings.This, in turn, introduces volatility into a firm’s reporte d earnings.12.The notion of an opportunity cost refers to the return associated with your next best opportunity. In thearea of FX risk management, it entails comparing a given risk management strategy with an appropriate standard of comparison. This provides an objective means of assessing the effectiveness of a given risk reduction program. For example, when FX risk management programs are centralized at corporate headquarters, appropriate benchmarks against which to compare the success of corporate risk protection would be programs that local managers could have implemented on their own.Exercises1.Students usually gloss over diagrams without thinking them through. This exercise forces them to thinkthrough each step of the diagram and allows them to better internalize the risk management cycle.Responses might follow the following pattern: Step 1 involves operationalizing a firms strategies intoquantifiable objectives and then identifying developments both external and internal risks that could affect the achievement of these objectives. These risks are measured by the firm’s accountants and quantified in terms of their potential impact on the firm. For example, the firm may have as its strategic objective an increase of 5% of market share in a given country per year given assumptions about the rate of economic growth in that country. The chance that this growth rate may fall short of 5% and the impact of this shortfall for projected sales in that country would be quantified. Response formulation would involve identifying protection strategies to minimize the hit to sales of projected GNP shortfalls such as promotion campaigns to maintain sales or use of alternative sourcing venues to lower sales prices. This strategy would be implemented if projected GNP started to slow beyond a certain cutoff point. The impact of this protection strategy would then be quantified in terms of actual sales relative to forecast sales taking into account the costs of protection. The information contained in risk management performance reports would then be communicated to top management who would be in a position to reaffirm or alter strategic objectives and/or risk identification processes.2.Foreign exchange risk a devaluation of the foreign currency in which an account receivable wasdenominated would cause the domestic currency cash flows to decrease. This would cause current assets to decrease. Alternatively, a revaluation of the foreign currency would cause the account receivable and current assets to increase. Interest rate risk an increase in market rates of interest would cause the price ofa short-term fixed-rate debt instrument being held as a marketable security to decrease. This, in turn,would cause current assets to decrease. A decrease in interest rates would have the opposite effect.Commodity price risk an increase in the price of copper would cause the cost of copper purchases and the resultant unexpired cost of inventories in the current asset section of the balance sheet to increase. A fall in copper prices would have the opposite effect. Equity price risk a fall in stock prices would depress the carrying value of marketable securities (current assets), and conversely.3.The purpose of this exercise is to force students to look at manager ial accounting issues from the user’sperspective. Students may suggest additional information sources with respect to inflation differentials, balance of trade and balance of payments statistics, international monetary reserves, forward exchange quotations, the behavior of related currencies, and interest rate differentials. We recommend that this exercise be assigned to small groups to encourage teamwork. At the time this exercise was prepared, professional forecasters were predicting a rate of 10.5 ecrus to theU.S. dollar.Some groups may contend that exchange markets are efficient and that exchange rate changes are simply random events. Again, they must be prepared to convince management of their case, or at a minimum, identify the consequences of not attempting exchange rate forecasts.4. Current rate Current/Noncurrent Monetary/nonmonetaryExposed assets(PHP):Cash 500,000 500,000 500,000Accounts receivable 1,000,000 1,000,000 1,000,000 Inventories(LCM) 900,000 900,000Fixed assets 1,100,000 -- --Total 3,500,000 2,400,000 1,500,000 Exposed liabilities:Short-term payables 400,000 400,000 400,000Long-term debt 800,000 --- 800,000Total 1,200,000 400,000 1,200,000Positive/(negative) exposure 2,300,000 2,000,000 300,000 Positive exposure X $0.03 $69,000 $60,000 $9,000Positive exposure X $0.02 46,000 40,000 6,000 FX gain/(loss) $(23,000) $(20,000) $(3,000)5.ILS $ £$ EquivalentExposed Assets:Cash & due from banks 100,000 50,000 (40,000) 20,000Loans 200,000 ---- ---- 100,000Fixed assets ---- 30,000 ---- 30,000Exposed Liabilities:Deposits 40,000 ---- 15,000 50,000Owners equity ---- 100,000 ---- 100,000Net exposed assets 260,000 (20,000) (55,000) NIL(liabilities)ILS $ £$ EquivalentExposed Assets:Cash & due from banks 100,000 50,000 (40,000) 20,000Loans 200,000 ---- ---- 100,000Fixed assets ---- 30,000 ---- 30,000Exposed Liabilities:Deposits 40,000 ---- 15,000 50,000Owners equity ---- 100,000 ---- 100,000Net exposed assets 260,000 (20,000) (55,000) NIL(liabilities)6.Trial Balance BeforeILS $ £$ EquivalentCash & due from banks 100,000 50,000 (40,000) 20,000Loans 200,000 ---- ---- 100,000Fixed assets ---- 30,000 ---- 30,000Deposits 40,000 ---- 15,000 50,000 Owners equity ---- 100,000 ---- 100,000Trial Balance After(£/$/ILS = 1/2/8)ILS $ £$ EquivalentCash & due from banks 100,000 50,000 (40,000) (5,000)Loans 200,000 ---- ---- 50,000Fixed assets ---- 30,000 ---- 30,000Deposits 40,000 ---- 15,000 40,000 Owners equity ---- 100,000 ---- 100,000Translation loss $(65,000)7. One recommendation might be to reduce positive exposures by engaging in balance sheet hedging, that is, by remitting excess cash back to the corporate parent, reducing the affiliate bank’s outstanding loans, or increasing its deposits in Israeli shekels.. The trade-offs here are potentially negative effects on operations, such as not satisfying loan demand against hedging translation gains and losses. Another option is to increase the pricing of bank services in Israel to provide a profit margin that can offset any FX losses. Again, the effects of such actions on competitive positioning could far exceed the benefits of hedging. A third option is to buy a forward or currency swap to hedge the exposure. Trade-offs include the out-of-pocket cost of the exchange contract versus the reported losses avoided.1.If the U.S. dollar is the functional currency, the translation gain upon consolidation is aggregated with thetransaction loss on the foreign currency borrowing and disclosed as one line item in the consolidated income statement. This figure is determined as follows:Translation gain = Positive exposure X change in exchange rate= NZD3,000,000 x $.10= $300,000Transaction loss =NZD loan balance X change in exchange rate= NZD1,000,000 x $.10= $ (100,000)Aggregate exchange adjustment = $300,000 + $ (100,000)= $200,000If the New Zealand dollar is the functional currency, the translation gain upon consolidation bypasses income and appears as a separate component in consolidated equity. It is offset by the translation loss on the New Zealand dollar borrowing.9.4/1 CD (¥32,500,000 ÷ ¥120) $250,000Cash $250,000(Purchase of CD)Chips (¥32,500,000 ÷ ¥120) $270,833Cash (¥3,250,000 ÷ ¥120) $ 27,083A/P (¥29,250,000 ÷ ¥120) 243,750(To record credit purchase)7/1 CD (¥30,000,000 ÷ [¥120 - ¥110]) $ 22,727FX gain $ 22,727(To record gain on CD investment)Purchases (¥29,250,000 ÷ [¥120 - ¥110]) 22,159Accts. Payable 22,159(To record increase in purchases and related liability accounts owing to yen appreciation) 7/1 Cash (¥30,000,000 ÷ ¥110) $278,182Interest income (¥30,000,000 X .08 X ¼) ÷ ¥110] $ 5,455CD 272,727(To record maturation of CD)Interest expense [(¥29,250,000 x.08 x 3/12) ÷ ¥110) 5,318Accts. payable (¥29,250,000 ÷ ¥110) 265,909Cash 271,227(To record settlement of purchase transaction)10. Journal entries:6/1 CHF Contract receivable $133,333Deferred premium 3,334$ Contract payable $136,667(To record contract with the foreign currency dealer to exchange $136,667 for CHF 166,667)6/30 CHF Contract receivable 1,667Transaction gain 1,667(To record transaction gain from increased dollar equivalent of forward contract receivable; $.81 - $.80 x SWF 166,667)6/30 Premium expense 1,111Deferred premium 1,111(To amortize deferred premium for 1 month)9/1 SWCHF Contract receivable 3,333Transaction gain 3,333(To record additional transaction gain by adjusting forward contract to the new current rate; $.83 - $.81 x CHF 166,667)9/1 Premium expense 2,223Deferred premium 2,223(Amortization of deferred premium balance)9/1 $ Contract payable 136,667Cash 136,667 Foreign currency 138,333CHF Contract receivable 138,333(To record delivery of $136,667 to foreign currency dealer in exchange for CHF166,667 with a dollar equivalent of $138,334 (=CHF166,667 x $.83). The Swiss francs will, in turn be used to pay for the chocolate supplies).11. Calculations:If the premium on the forward contract is considered an operating expense, and the conditions for hedge treatment are met, i.e., management designates the forward contract as a hedge, documents its risk management objective and strategy, identifies the hedging instrument, the item being hedged and the risk exposure, and that the forward is effective both prospectively and retrospectively in hedging the risk, the gain on the forward can be offset against the loss on the payable as follows:Amount paid to settle the account payable on the purchase $138,333Less Transaction gain on forward contract (5,000)Cost of purchase $133,333The $133,000 is what was originally anticipated, CHF166.667 X $0.80 = $133,333.12. Journal entries:The call option is intended to hedge an uncertain cash flow. Accordingly, gains or losses on the hedging instrument would bedisclosed in comprehensive income and reclassified into earnings in the period the sale actually takes place.June 1 Premium expense $28,125Cash $28,125($.018 X CHF 62,500 X 25)August 31 Cash $40,625Comprehensive income $40,625[($.416 - $.39) X CHF 62,500 X 25]Case 11-1Exposure Identification1. Infosys appears to have several exposures as enumerated below.Foreign Exchange RiskPage Value-Drivers88 Revenues/Selling and administrative expenses89 Cash flows from interest/dividend income96 Revenue recognition/LT leases97 Operating income/foreign currency transactions/FA98 Marketing/Overseas staff expenses99 Derivative values100 Lease obligations101 Investment returns102 Segment revenues/expenses103 Dividends to ADS holders142 Penalties on export obligations149 Valuing intangibles150 Export revenuesCommodity Price RiskPage Value-Drivers98 Power and fuel expenses145 Brand valuation147/48 Current cost disclosures149 Value of intangiblesEquity Price RiskPage Value Drivers87 Share capital98 Diluted eps100 Stock option compensation expense103 Convertible preferreds145 Cost of capital151 Economic value-addedInterest Rate RiskPage Value Drivers88 Interest expense89 Cash flows from security investments/interest income97 Gratuity/Superannuation/Provident obligations143 Employee compensation145 Cost of capital149 Value of intangibles.151 Economic value-addedInformation on the company’s risk management policies are contained on pages 108-109 of their annual report which were not reproduced in Chapter 1. We include the relevant information here. Infosys derives its revenues from 51 countries of which 78 percent were denominated in US dollars. To minimize both transaction and translation risk the company:1.Tries to match expenses in local currency with receipts in the same currency.es forward exchange contracts to cover apportion of outstanding receivables.3.Denominates contracts in non-US and non-EU regions in internationally tradable currencies to minimizeexposures to local currencies that may have non-tradability risks.Case 11-2Value At Risk: What Are Our Options?Students should be asked to play the role of the consultant, and will find it to be a contentious issue. Suggested remedies that have merit are:1. The FASB should permit deferral accounting for rolling options which would take the derivative gain or loss on each option to equity until the anticipated event occurs, as opposed to taking it immediately to income. This, however, might encourage companies to game the system, so students should also suggest ways to keep this from happening.2. Another tack would be to adhere to generally accepted accounting principles and record the gain or loss on the derivative in current income as it is marked to market, but to disclose which transactions were undertaken for hedge purposes. Management could also game the system here as speculative activities could be disclosed as hedge activities.3. Another option that students might suggest is to revert back to the earlier U.S. practice of keeping the option off balance sheet and providing supplementary disclosure of mark-to-market accounting. This might be confusing to lay readers, but it would enable analysts to better understand the components of reported earnings.It is clear from the annual report clipping that management will ignore accounting pronouncements when it is in their interest to do so. Analysts must be alert to situations where management departs from GAAP to better reflect the economics of what transpired as opposed to doing so to manage earnings.精品文档,知识共享!!!。

国际会计练习册答案 (上海财经大学出版社)

第三章习题解答一、名词解释1 演绎法:在演绎法下先确定出相关的环境因素,然后把这些因素与不同国家的会计实务结合起来,从而提出不同的国家组别或者会计发展模式。

2归纳法:在归纳法下,先从单个国家的会计实务分析开始,然后确定出发展模式或者组别,最后对不同的经济、社会、政治和文化做出解释。

3 宏观经济模式:会计实务是从国家的经济目标中派生出来的并为其服务。

由于企业协调其活动以符合国家的政策,因此企业的目标通常遵循而不是引导国家的经济政策。

例如,国家为了避免商业周期的波动需要采取稳定就业的政策,可能采用导致利润被平均化的会计。

为刺激某个行业的发展,可能允许某行业快速冲销资本性支出。

代表国家有瑞典。

4微观经济模式:会计按照微观经济原则发展,单个的企业是关注的中心,它们的主要目的是生存。

为了保全实体资本,需要清楚区分资本与收益,以便评价和控制经营活动。

基于重置成本的会计计量适合此模式。

5独立学科方法:会计被看作一项经营职能,它的概念和原则来源于所服务的经营过程,企业借助于经验、实践和直觉来应对现实世界中的复杂性和不确定性。

会计在特殊的、零散的判断和试错中发展起来。

例如强调收益信息的披露。

在英国和美国,会计是作为独立学科发展的。

6统一方法:会计标准化并作为中央政府管理控制的工具。

计量、披露和列报上的统一性,使得会计信息更易于被政府计划部门、税务当局以及企业经理人员用来控制各种类型的经营活动。

这种模式常见于政府强烈干预经济的国家,会计被用来计量业绩、分配资源、征收税款和控制价格等。

前苏联和曾经实行计划经济的其他社会主义国家是典型的代表。

另外拥有统一的会计科目表的法国也是典型代表。

二、单项选择题1.国际会计在全球范围内面临的主要挑战包括( ):A.全球会计的协调 B. 新兴资本市场的财务报告确 C.社会和环境报告D.高科技时代的财务报告E.包括以上各项.【选E】2.按照国家将全球会计模式进行分类的好处在于( )A.通过考察属于同一群体的其他国家的经验,各国可以借鉴其会计经验。

国际会计课后题答案 版

第1章国际会计的形成与发展一、讨论题为什么说市场国际化,特别是货币市场和资本市场的国际化是会计国际化的主要推动力国际贸易和国际经济技术合作,促使会计成为一种国际商业语言。

特别是国际货币市场和资本市场的兴起向进入市场的贷款人或筹资者提出了应提供在国际间可比且可靠的财务信息的要求(即国际财务报告趋同化的要求),更成为会计国际化的主要推动力。

跨国公司是否在百分之百地推动会计国际化说明你的观点。

不是。

跨国公司对推动会计国际化有其两面性:一方面,基于其跨国经营和国际筹资的需要,他们希望通过会计国际化来缩小和协调国别差异;另一方面,他们又十分重视利用各国现存的会计差异来谋取财务利益。

后者也推动了各国会计模式和重要会计方法的国际比较研究。

(注意:“会计国际化”大体上与“会计的国际协调化”概念一致,而与国际会计研究中的“国别会计”观点对立)会计随商业活动的扩展而传播,你同意这种说法吗从历史发展的进程谈谈你的看法。

同意。

可主要就前殖民帝国的会计向其原殖民地传播、工业革命后西方会计的发展及在世界范围内的广泛传播以及第二次世界大战以后美国会计的影响在一定程度上主宰着世界各地的会计发展等历史事实,加以讨论。

哪些特定会计方法具有国际性质把外币交易和外币报表的折算引入会计领域,是会计国际化带来的独特问题。

它与由此引发的跨国企业合并和国际合并财务报表与外币折算相互关联和制约的问题,以及各国的物价变动影响在国际合并财务报表中如何处理和调整的问题,从20世纪70年代以来,就成为国际会计研究中既需协调一致但又矛盾重重的“三大难题”。

在世纪之交,金融工具(特别是衍生工具)的创新引发的会计处理问题,给传统的会计概念和实务带来了巨大的冲击,成为各国会计准则机构联合攻关、仍未妥善解决的难题。

此外,国际税务会计也是值得关注的课题。

你对会计国际化和国家化之间的矛盾及其消长有何看法会计国际化和国家化的矛盾实际上反映了经济全球化与各国的国家利益之间的矛盾及其消长过程。

国际会计学课后答案

国际会计学课后答案【篇一:国际会计第七版英文版课后答案(第六章)】foreign currency translationdiscussion questions solutions1. foreign currency translation is the process of restating a foreign account balance from one currency to another. foreign currency conversion is the process of physically exchanging one currency for another.2. in the foreign exchange spot market, currencies bought and sold must be delivered immediately,normally within 2 business days. thus a singaporean tourist buying u.s. dollars at the airportbefore boarding a plane for new york would hand over singapore dollars and immediatelyreceive the equivalent amount in u.s. dollars. the forward market handles agreements toexchange a fixed amount of one currency for another on an agreed date in the future. forexample, a french manufacturer exporting goods invoiced in euros to a japanese importer on 60- day credit terms would buy a forward contract to sell yen for euros 2 months in the future.transactions in the swap market involve the simultaneous purchase (or sale) of one currency inthe spot market and the sale (or purchase) of the same currency in the forward market. thus, acanadian investor wishing to take advantage of higher interest rates on 6-month treasury bills inthe united states would buy u.s. dollars with canadian dollars in the spot market and invest inthe united states. to guard against a fall in the value of the u.s. dollar before maturity (whenthe u.s. dollar proceeds are converted back to canadian dollars), the canadian investor wouldsimultaneously enter into a forward contract to sell u.s. dollars for canadian dollars 6 months inthe future at today s forward exchange rate.3. the question refers to alternative exchange rates that are used to translate foreign financialstatements. the current rate is the exchange rate at the financial statement date. it issometimes called the year-end or closing rate. the historical rate is the exchange rate at the timeof the underlying transaction. the average rate is the average of various exchange rates during afiscal period. since the average ratenormally is used to translate income statement items, it isoften weighted to reflect any seasonal changes in the volume of transactions during the period.translation gains and losses do not occur if exchange rates do not change. however, ifexchange rates change, the use of current and average rates causes translation gains and losses.these do not occur when the historical rate is used because the same (constant) rate is used eachperiod.4. in this example, the mexican affiliate s canadian dollar loan is denominated in canadian dollars.however, because the mexican affiliate’s functional currency is u.s. dollars, the peso equivalentof the canadian dollar borrowing would be remeasured in u.s. dollars prior to consolidation. ifthe mexican affiliate’s functional currency were the peso, the canadian dollar loan would beremeasured in pesos before being translated to u.s. dollars.5. a transaction gain or loss occurs when a foreign currency transaction, e.g., a foreign currencyborrowing, is settled at a different exchange rate than that which prevailed when the transactionwas originally incurred. in this case there is an exchange of one currency for another. atranslation gain or loss, on the other hand, is simply the result of a restatement process. there isno physical exchange of currencies involved.6. it is not possible to combine, add, or subtract accounting measurements expressed in differentcurrencies; thus, it is necessary to translate those accounts that are measured or denominated in aforeign currency into a single reporting currency. foreign currency translation can involverestatement or remeasurement. in restatement, the local (functional) currency is kept as the unitof measure; that is, the translation process multiplies the financial results and relationships in thelocal currency accounts by a constant, the current rate. in contrast, remeasurement translateslocal currency results as if the underlying transactions had taken place in the reporting(functional) currency of the parent company; for example, it changes the unit of measure of aforeign subsidiary from its local (foreign) currency to the u.s. dollar.7. major advantages and limitations of each of the major translation methods follow.current rate methodadvantages:a. retains the initial relationships in the foreign currency statements.b. simple to apply.limitations:a. violates the basic purpose of consolidation, which is to present the results of a parent and its subsidiaries as if they were a single entity.b. inconsistent with historical cost.c. presumes that all local assets and liabilities are subject to exchange risk.d. while stockholders equity adjustments shield an mnc s bottom line from translation gains and losses, such adjustments could distort certain financial ratios and be confusing.current-noncurrent methodadvantages:a. distortions in translated gross margins are reduced as inventories and translated at the current rate.b. reported earnings are shielded from the distorting effects of currency fluctuations as excess translation gains are deferred and used to offset future translation losses.limitations:a. uses balance sheet classification as basis for translation.b. assumes all current assets are exposed to exchange risk regardless of their form.c. assumes long-term debt is sheltered from exchange rate risk.monetary-nonmonetary methodadvantages:a. reflects changes in domestic currency equivalent of long-term debt on a timely basis.limitations:a. assumes that only monetary assets and liabilities are subject to exchange rate risk.b. exchange rate changes distort profit margins as sales transacted at current prices are matched against cost of sales measured at historical prices.c. uses balance sheet classification as basis for translation.d. nonmonetary items stated at current market values are translated at historical rates.temporal methodadvantages:a. theoretically valid: compatible with any accounting measurement method.b. has the effect of translating foreign subsidiaries operations as if they were originally transacted in the home currency, which is desirable for foreign operations that are extensions of the parent’s activities. limitation:a. a company increases its earnings volatility by recognizing translation gains and losses currently. in arguing for one translation method over another, your students should eventually realize that, in the present state of the art, there is probably no one translation method that is appropriate for all circumstances in which translations occur and for all purposes thattranslation serves. it is probably more fruitful to have students identify circumstances in which they think one translation method is more appropriate than another.8. the current rate method is appropriate when the foreign entity being consolidated is largely independent of the parent company. conditions which would justify this methodology is when the foreign affiliate tends to generate and expend cash flows in the local currency, sells a product locally so that its selling price is largely insulated from exchange rate changes, incurs expenses locally, finances its self locally and does not have very many transactions with the parentcompany. in contrast, the temporal method seems appropriate in those instances when theforeign affiliate’s operatio ns are integrally related to the parent company. conditions which would justify use of the temporal method are when the foreign affiliate transacts business in the parent currency and remits such cash flows to the parent company, sells a product largely in the parent country and whose selling price is sensitive to exchange rate changes,sources its factor inputs from the parent company, receives most of its financing from the parent and has a large two way flow of transactions with it.9. the history of foreign currency translation in the united states suggests that the development of accounting principles does not depend on theoretical considerations so much as on political, institutional, and economic influences that affect accounting standard setting. it may be morerealistic to recognize that theoretically sound solutions are impossible as long as policyprescriptions are evaluated on practical grounds. without specific choice criteria derived frominvestor decision models, it is fruitless to argue the conceptual merits of competing accountingtreatments. it is far more productive to admit that foreign currency translation choices are simplyarbitrary.readers of consolidated financial statements should know that the foreign currency translationmethod used is one of several alternatives, and this should be disclosed. this approach is moreopen and reduces the chance that readers will draw misleading inferences.10. foreign inflation, in particular, the differential rate of inflation between the country in which a subsidiary is located and the country of its parent determines foreign exchange rates.these rates, in turn, are used to translate foreign currency balances to parent currency.11. in the united kingdom, financial statements of affiliates domiciled in hyperinflationaryenvironments must first be adjusted to current price levels and then translated using the current rate; in the united states, the temporal method would be employed. the second part of this question is designed to get students from abroad to find out what companies in their homecountries are doing and thereby be in a position to share their new found knowledge with their classmates. they need simply get on the internet and read the footnotes of a major multinational company in their home country.12. under fas no. 52, the parent currency is designated as the functional currency for an affiliate, whose operations are considered to be an integral part of the parent company’s operations.accordingly, anything that affects consolidated earnings, including foreign currency translationgains and losses, is relevant to parent company shareholders and is included in reported earnings.in contrast, when a foreign affiliate s operations are independent of the parent s, the localcurrency is designated as its functional currency. since the focus is on the affiliate s localperformance, translation gains and losses that arise solely from consolidation are irrelevant and,therefore, are not included in consolidated income.exercises solutions1. ¥250,000,000 x .008557 = $2,139,250.the difference is due to rounding.。

国际会计课后习题部分答案

IASC是由来自澳大利亚、加拿大、法国、德国、日本、墨西哥、荷兰、英国和爱尔兰以及美国的会计职业团体于1973年发起成立的,其目标是制定和发布国际会计准则,促进国际会计的协调。

从1983年起,作为国际会计师联合会(IFAC)成员的所有会计职业团体均已成为IASC的成员。

中国于1998年5月正式加入IASC和国际会计师联合会。

到2000年,IASC已经拥有来自104个国家的143个成员。

1ASC的目标是,制定和发布国际会计准则,促进国际会计的协调。

截至2000年底,IASC已颁布41项国际会计准则(其中仍然有效的有36项)和24项解释公告。

国际会计准则委员会(IASC)承诺制定的核心准则(core standard)于2000年5月经证券委员会国际组织(I0SC0)认可并向各国资本市场推荐在跨境融资使用后,IASC的声誉空前提高,不仅伦敦证券交易所公开采用国际会计准则(IAS),欧盟还公告至2005年全体企业实施IAS.但是,美国SEC发表声明认为IAS 不是质量最好的准则,言下之意,美国是经济最发达的国家,因而美国FASB的准则是质量最高的。

在此情况下,IASC理事会(IASC Board)于1999年12月决议采纳战略工作组(Strategy Working Party)的未来规划建议,同意重组并投票选出7人组成的托管会提名委员会(Nominating Committee),提名委员会主席为时任美国SEC主席Arthur Levitt.提名委员会在2000年1月7日召开了第一次会议,决定设立由19人组成的托管会(Trustees),其主要职责是筹集资金、任命人员和日常监督。

2000年5月22日宣布选出的托管会成员,其主席为美国联邦储备局前主席Paul A.Volcker.2000年5月24日,IASC成员组织通过了重组决定和新章程(Constitution)。

2000年6月28日托管会任命英国ASB主席David Tweedie为重组后IASC 理事会(IASB)主席,于2001年1月1日起任职。

国际会计第七版课后答案第四章作者弗雷德里克

第四章比较会计:美洲和亚洲讨论问题1。

公共和私营部门机构参与调节和执行财务报告在美国。

财务会计准则委员会是一个私人的身体决定美国公认会计原则。

美国证券交易委员会有权决定美国公认会计准则对上市公司来说,但FASB推迟。

FASB和秒有一个密切的工作关系,确保FASB SEC标准是可以接受的。

美国证券交易委员会对上市公司实施财务报告规则。

公司积极审查申请。

审计师的执法者非公有制企业举行。

发布的会计准则在墨西哥是财务信息标准的研究和发展委员会(CINIF),一个独立的美国FASB公私部门的身体后图案。

墨西哥的权威发布会计准则是国家银行和证券委员会认可的政府机构,调节墨西哥证券交易所。

欧盟委员会负责执行上市公司财务报告准则。

然而,目前尚不清楚如何主动的委员会在调查其接收到的文件。

执行财务报告为非上市公司有效取决于审计师。

日本会计准则由私营部门机构设置,日本的会计准则委员会。

ASBJ的建立是最近在日本发展。

以前,会计准则制定是政府活动。

财务报告的执行有效取决于审计师。

证券交易所监管的金融服务机构,政府机构。

然而,目前尚不清楚如何主动FSA在监测由日本公司财务报告。

在中国会计准则制定是政府的活动。

中国会计准则委员会权威机构在财政部负责制定会计准则。

中国证券监督管理委员会是中国的政府机构监管的两个股票交易所。

中国证监会还负责执行上市公司财务报告。

许多中国执行机制的有效性问题。

印度特许会计师协会,一个私营部门的专业机构,在印度发展会计准则。

印度证券交易委员会财政部的一个机构,调节印度22证券交易所和负责执行财务报告规则。

然而,目前尚不清楚如何主动的董事会是由印度公司在监督财务报告。

总的来说,五个国家不同的私人和公共部门负责管理和执行财务报告。

在若干国家执法是可疑的。

美国最强大的机制来调节和执行五个国家的财务报告。

2。

美国和印度是普通法国家,面向公允表达的财务报告。

墨西哥也有面向公允表达的财务报告,因为美国的影响力。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

国际会计课后题答案版 Pleasure Group Office【T985AB-B866SYT-B182C-BS682T-STT18】第1章国际会计的形成与发展一、讨论题为什么说市场国际化,特别是货币市场和资本市场的国际化是会计国际化的主要推动力国际贸易和国际经济技术合作,促使会计成为一种国际商业语言。

特别是国际货币市场和资本市场的兴起向进入市场的贷款人或筹资者提出了应提供在国际间可比且可靠的财务信息的要求(即国际财务报告趋同化的要求),更成为会计国际化的主要推动力。

跨国公司是否在百分之百地推动会计国际化说明你的观点。

不是。

跨国公司对推动会计国际化有其两面性:一方面,基于其跨国经营和国际筹资的需要,他们希望通过会计国际化来缩小和协调国别差异;另一方面,他们又十分重视利用各国现存的会计差异来谋取财务利益。

后者也推动了各国会计模式和重要会计方法的国际比较研究。

(注意:“会计国际化”大体上与“会计的国际协调化”概念一致,而与国际会计研究中的“国别会计”观点对立)会计随商业活动的扩展而传播,你同意这种说法吗从历史发展的进程谈谈你的看法。

同意。

可主要就前殖民帝国的会计向其原殖民地传播、工业革命后西方会计的发展及在世界范围内的广泛传播以及第二次世界大战以后美国会计的影响在一定程度上主宰着世界各地的会计发展等历史事实,加以讨论。

哪些特定会计方法具有国际性质把外币交易和外币报表的折算引入会计领域,是会计国际化带来的独特问题。

它与由此引发的跨国企业合并和国际合并财务报表与外币折算相互关联和制约的问题,以及各国的物价变动影响在国际合并财务报表中如何处理和调整的问题,从20世纪70年代以来,就成为国际会计研究中既需协调一致但又矛盾重重的“三大难题”。

在世纪之交,金融工具(特别是衍生工具)的创新引发的会计处理问题,给传统的会计概念和实务带来了巨大的冲击,成为各国会计准则机构联合攻关、仍未妥善解决的难题。

此外,国际税务会计也是值得关注的课题。

你对会计国际化和国家化之间的矛盾及其消长有何看法会计国际化和国家化的矛盾实际上反映了经济全球化与各国的国家利益之间的矛盾及其消长过程。

可以认为,会计扎根于各国的政治、经济、思想、文化等社会因素之中,会计的国家特色是无法完全磨灭的。

会计国际化只能是一个缩小和协调国别差异的过程,并将随着经济全球化的步伐逐步前进,最终也只能是“求大同、存小异”。

绝对意义上的“世界会计”始终只能是一个目标。

这与国际货币市场和资本市场对会计国际化的要求——国际财务报告的趋同化,最终达到来自世界各地的财务报告的信息完全可比——也许属于不同的命题。

不同学者对会计国际化与国家化的看法各有偏好,是完全可以理解的。

在组织讨论中,可以鼓励学生发表有差别乃至相反的观点。

为什么说会计国际化是促使会计职业国际化的主要推动力后者的进展又为什么落后于前者的发展或者,你也可以就不同意“落后”的说法谈谈看法。

这只是一般的习惯说法。

实际上是:国际融资、投资活动和跨国公司的经营活动一方面推动了会计国际化,另一方面也必然要求会计职业界提供国际性服务,从而推动了会计职业国际化。

会计职业国际化所以落后于会计国际化的发展,其主要阻力来自各国对会计师职业资格的认可存在着多方面(如学历要求、考试要求、后续教育要求、颁发执业证书要求等等)的较大差异。

关于“不同意”的说法,主要有:(1)会计职业界已建立了强有力的国际组织;(2)从技术的角度上说,国际审计准则的制定及与各国审计准则的协调,其进展超越了国际会计准则。

值得探讨的问题是:(1)国际性会计师事务所在业务经营中的垄断趋势及实力悬殊,对会计职业国际化形成的影响。

(2)各国会计市场的准入对会计职业国际化的影响问题。

为什么说会计学家们对国际会计所下的定义反映了会计国际化和会计职业国际化进程的影响在20世纪60年代,国际会计协调化的趋向尚不明朗,以致有些会计学者(如科拉里奇和马霍)明确地把国际会计定义为对各国会计理论和实务的分析、对比和研究,而有些有远见的会计学家(如齐默曼教授等)则把国际会计定义为应该打破国界,发展为世界性的会计理论和实务研究,但也只是抽象地表达了他们对开拓国际会计研究的抱负、热忱和期望。

20世纪70年代初,会计学家韦里奇、艾弗里和安德森曾把国际会计的定义概括为三种观点:(1)一个全球体系;(2)一个描述各国现行准则和惯例并提供与此相关信息的方法;(3)母公司和国外子公司之间的会计实务。

在20世纪70年代至80年代,国际会计的发展,正是处在会计的国别差异显着而协调化工作卓有成效的趋势下,会计职业界国际组织的活动也日益彰显,特别是国际会计准则的制定和影响;另一方面,跨国公司的兴起和壮大,也对解决国际经营活动中的会计实务问题提出了较为迫切的要求。

20世纪80年代至90年代,随着国际会计协调化的强劲发展,在国别会计的研究中,不少学者也从静态的观点改持动态的观点,为存异趋同探索国际会计协调化的有效途径。

这才出现了如会计学家崔和缪勒的把国际会计的研究内容进行全面概括的定义,以至伊克彼、麦尔科和伊利马拉夫的十分简洁、直截了当的定义,而两者都明确地突出了会计的国际协调化。

你倾向于把国际会计定义为全球会计,还是国别会计鼓励学生各抒己见,而后基本上肯定:(1)全球会计应该是最终目标;(2)国际财务报告趋同化已是国际货币市场和资本市场发展的现实需求;(3)会计的国别差异可能是难以完全磨灭的,但“求大同,存小异”则是必然的发展趋势;(4)为此,应该变以静态的观点研究国别会计为以动态的观点研究国别会计。

你赞成把国际会计等同于跨国公司与国外子公司之间的会计实务吗不能完全等同。

虽然国际会计研究的课题几乎都与跨国公司经营活动的要求有关,但即使是跨国公司要求的国别会计的研究也发展成为世界会计模式的研究,而且带有宏观会计的性质,远远突破了跨国公司与国外子公司之间的会计实务研究的范畴。

此外,这种实务主义的观点也有损国际会计领域的理论研究。

二、练习题你对21世纪初跨国并购的前景有何看法自1997年至2000年,跨国并购的浪潮迭起。

其规模之大,遍布的行业之广,跨国公司行动之积极,在历史上都是空前的。

这种浪潮至世纪之交,开始回落。

从一般的规律来看,在并购高潮后出现回落,并非罕见,但这次回落幅度之大,则属罕见。

进入21世纪后,2001年上半年的并购交易就锐减了53%;至2002年,重大的并购交易,几乎从因特网上消失。

论者认为,2001年下半年全球证券市场和上市公司中暴露出来的通过并购制造经济泡沫和进行财务欺诈的事件,是这次跨国并购高潮急剧回落的独特原因。

2003年开始,跨国并购基本上趋于平稳,但时有因反国际垄断迫使巨大的跨国并购的事例发生。

第2章会计模式通论一、讨论题对于第1题中八项要素,按照它们对会计发展产生影响的重要性从高到低排序,然后论证你所排列的最高项目和最低项目。

其重要性排序大体如教本中所列,即:法律制度、企业资金来源、税制、政治和经济联系、通货膨胀、经济发展水平、教育水平、地理条件。

允许学生对序次相近的要素的排序有所变更。

之所以将法律制度列为影响最大的项目,是着眼于在成文法国家和不成文法国家中,在会计规程(包括会计准则、会计制度、各项单行法规)的制定、修订或废止的机制、会计信息应首先遵循合法性还是公允性、会计信息披露的透明度与信息使用者的需求、对财务案件的司法介入与行政介入的程序及法院判例的效用、政府对会计市场和会计职业界的监管体制等方面,其差别和影响都是最深刻和广泛的。

之所以将地理条件列为最后,是因为它只是指地理条件的邻近或地区差别,会因交往促进会计实务的协调或因差别导致会计观念和会计要求上的差异。

事实上,这种影响要透过其他因素才起作用。

各国之间会计实务的区别用文化、经济和法律制度中哪一个解释更好为什么不一定是哪一个解释得更好的问题。

用经济和法律制度的差异来解释各国之间会计实务的区别可能比较直接、生动、具体且联系紧密,但要作出深层次的解释,则只有从文化的差异切入。

可以鼓励学生就某些会计方法的国际差别,从有关国家的经济和法律制度的差异及文化差异两个方面进行解释。

本章中所讨论的四种会计发展模式在1967年最先被提出,这四种模式现在仍然适用吗为什么仍适用。

因为对会计发展模式进行的这种概括性的分类成为20世纪70年代以来不同会计学家对全球会计模式进行分类的概念依据,而国际会计协调化至今仍未能达到完全消除不同会计模式的基本差异的阶段。

假设荷兰是会计发展的微观经济模式的最佳代表,而美国则代表着独立范畴趋向。

这两种发展模式中存在一种比另一种更成功的情形吗如何衡量这两种不同模式的成功之处应该说,这两种发展模式各有成功之处。

(1)微观经济基础的会计发展模式从企业经济学中派生出会计概念与原则,把企业视为经营活动的中心,提出了“真实意义上的企业资本保全”的核心会计概念。

这对有效地区分资本与收益,乃至在物价持续上涨的20世纪70年代对“物价变动会计”的发展和财务报告的变革,都具有奠基意义。

荷兰会计学者早在20世纪20年代就提出了现行重置价值的计价理论。

(2)独立范畴趋向的会计发展模式的成功之处,在于把会计视为在企业经营管理实践中发展而成的独立学科,从而不应从经济学等其他学科中派生其概念和原则,而应从它服务的企业经营过程中派生出自己的概念和原则。

这就在极大程度上扩展了会计研究的范畴。

可以说,现代会计的概念架构和公认会计原则的发展,是这一模式的成功之处。

美国(和英国)会计模式在会计发展的领先地位(不仅领先于微观经济模式,更领先于宏观经济模式和统一会计趋向模式)雄辩地说明了这个事实。

根据(1)、(2)两点的剖析,着者倾向于认定独立范畴趋向模式的成功之处超过微观经济基础模式。

为什么计量实务相对稳健的国家同时在披露上倾向于保密,而计量方法不太稳健的国家则在披露上倾向于透明这主要取决于财务报告使用者群体对信息的需求。

在资本市场(证券市场)不够发达、企业的资金来源主要依靠所有者投资和银行信贷的情况下,无论是国家、私人投资者,还是作为债权人的银行,都倾向于采用相对稳健的计量方法,以保护企业和债权人的利益。

作为债权人的银行,也可以从企业直接取得所需的任何信息,而在公开发布的对外财务报告中倾向于限制披露,进行“必要”的保密。

在资本市场发达的国家,企业管理层倾向于采用比较激进的计量方法,展示其对公众投资者具有吸引力的经营业绩和财务状况,而众多的分散的公众所有者则要求从公开发布的对外财务报告中获取尽可能广泛的信息,证券监管部门为保护公众投资者的利益,也倾向于要求信息披露上的充分和透明。

对现存会计实务体系的判断性分类应归功于缪勒、诺比斯和盖瑞。

如何区分这三种分类(1)缪勒在1968年的分类开创了对全球会计模式的判断性分类。