投资学第9章习题及答案

投资学第9章习题及答案

本章习题1.简述利率敏感性的六个特征。

2.简述久期的法则。

3.凸性和价格波动之间有着怎样的关系?4.简述可赎回债券与不可赎回债券的凸性之间的区别。

5.简述负债管理策略中免疫策略的局限性。

6.简述积极的债券投资组合管理中互换策略的主要类型。

7.一种收益率为10%的9年期债券,久期为7.194年。

如果市场收益率改变50个基点,则债券价格变化的百分比是多少?8.某种半年付息的债券,其利率为8%,收益率为8%,期限为15年,麦考利久期为10年。

(1)利用上述信息,计算修正久期。

(2)解释为什么修正久期是计算债券利率敏感性的较好方法。

(3)确定修正久期变动的方向,如果:a.息票率为4%,而不是8%b.到期期限为7年而不是15年。

(4)说明在给定利率变化的情况下,修正久期与凸性是怎样用来估计债券价格变动的?第九章本章习题答案1. 在市场利率中,债券价格的敏感性变化对投资者而言显然十分重要。

为了了解利率风险的决定因素,可以参见图9-1。

该图表示四种债券价格相对于到期收益变化的变化百分比,它们有不同的息票率、初始到期收益率以及到期时间。

这四种债券的情况表明,当收益增加时,债券价格下降;价格曲线是凸的,这意味着收益下降对价格的影响远远大于等规模的收益增加。

通过观察,可以得出以下两个特征:(1)债券价格与收益呈反比,即:当收益升高时,债券价格下降;当收益上升时,债券价格上升。

(2)债券的到期收益升高会导致其价格变化幅度小于等规模的收益下降。

比较债券A和B的利率敏感性,除到期时间外,其他情况均基本相同。

图9-1表明债券B比债券A期限更长,对利率更敏感。

这体现出其另一特征:(3)长期债券价格对利率变化的敏感性比短期债券更高。

这不足为奇,例如,如果利率上涨,则当前贴现率较高,债券的价值下降。

由于利率适用于更多种类的远期现金流,则较高的贴现率的影响会更大。

值得注意的是,当债券B的期限是债券A的期限的6倍的时候,它的利率敏感性低于6倍。

投资学课后练习答案(贺显南版)

投资学练习答案导论2.A3.ABCDE4.正确第一至第四章习题1.公司剩余盈利2.固定、累积3.C4.D5.C6.C7.正确8.错误9.A 11.C 12.C 13.D14.AD 15.B 16A 17.B 18.D 20.C 21.B22.A 23.D 24.B 26.A 29.C 30.C 31.A32.C 33.错误 34.正确 35.正确 36.错误 37.C38.A 39.B 40.B第五章习题1.D2.AC3.AB4.BCD5.正确6.正确7.ABCD8.正确9.E 10.D 11.B 12.E13.D 14.C 17.C第六章练习8.D 10.B 12.B 13.A 14.C第七章练习1.B2.C3.C4.C5.D 8.C 9.B12.B 13.D 14.C 15.B 17.E 18.B 19.B 22.C 23.B 24.B 25E26.A 27.B 28.A 33错误 34.A 35.A第八章练习2.B3.A4.B5.D6.D7.C8.A9.B12.C 13.C 14.D 16.C 17.C 18.D19.B 23.B 25.D 27.C投资学第九章习题答案1.不做2.不做3.C4.不做5.不做6.3%7.不做8.B9. C 10.D 11. D 12.C 13.D 14.C 15.A 16.C 17.(答案为0.75) 18.D 19.C 20.B21.不做投资学第十章至第十一章习题答案1.相关系数为02. B3. B4. C5.错6.错7. B8. E9. A10.对11.D投资学第十二章至第十三章习题答案1.不做2.高于票面值因为10%大于8%3.具体看课本公式(老师只是讲公式没有给出确切得答案)4.贴现贴现率5.反方向6.C7.C8.对9.对10.不做11.折价平价溢价12.不做13.不做14.不做15.A16.C17.C18.具体看书本323页19.具体看课本325页20.看课本319至32021.不做22.不做第十四章至十五章习题答案1.先行同步滞后2.不做3.开拓拓展成熟衰落4.资产负责表损益表现金流量表5. C6.宏观分析行业分析公司分析7. A8. B9. A10.D11.D12.A13.A14.对15.对十七章注意事项: 注意技术分析得三大假设假设1. 市场行为涵盖一切信息假设2.价格沿趋势运动假设3.历史会重演。

投资学习题答案完整版机工版

习题(1章)1.根据你自身的情况,计算你自己的理想收益率与必要收益率。

这些收益率是有可能实现的吗?你觉得选择本章中讲到的哪些金融工具有可能帮助你实现这些收益率?参考解答:(1)理想收益率和必要收益率的计算请见Excel文件,可以在课堂上根据同学自身情况进行模拟计算或调整数值。

2.试讨论你对自己风险态度的认识,并询问一下你的家庭成员或者你身边的朋友的风险态度。

尝试对这些人(包括你自己)做一个风险排序。

参考解答:可以根据教材中第一章提供的专栏1-1进行打分,提供风险态度依据。

3.本章分析了积极配置资产类别并积极选择证券品种的投资者以及消极配置资产类别并消极选择证券品种的投资者,他们分别对应表1-9中的A组合和D组合。

试问选择B组合和C组合的投资者会怎样具体地选择资产配置方案和证券投资品种?参考解答:表1-9 资产类别配置与证券品种选择组合示意A组合是积极的资产类别配置与积极的证券品种选择,这一类组合的投资者通常根据对不同资产类别的预期收益率的判断而选择不同时机改变固定收益类和股权类资产的配置比重,并且根据对不同证券品种的预期收益率的判断而开展积极的证券交易。

D组合则是消极的资产类别配置与消极的证券品种选择,这一类组合的投资者将长期坚持其既定的在不同类别资产上的配置比重,并将长期持有具体资产类别的指数基金。

B组合根据对不同资产类别的预期收益率的判断而选择不同时机改变固定收益类和股权类资产的配置比重,但是对于具体资产品种的选择则倾向于消极持有。

C组合消极开展资产类别配置选择,但是在具体的资产品种选择上将根据对不同证券品种的预期收益率的判断而开展积极的证券交易。

4.从长期来看,投资的风险和回报是正相关的,为什么短期而言并不一定如此?参考解答:从长期来看,投资的风险和回报之间的正相关关系是金融市场在长期处于相对均衡状态时的结果,我们将在第七章和第八章进一步讨论背后的理论机制。

另一方面,由于金融资产的收益具有波动性,比如股票投资收益的波动性较高,有可能在某一个特定短期获得较高的收益,也有可能在某一个特点短期招致较大亏损,但是投资该股票承担的风险并没有发生大的变化,因此风险和回报之间的正相关关系在短期内未必成立。

投资学题库及答案

《投资学》(第四版)练习题第1章投资概述习题一、单项选择题1、下列行为不属于投资的是()。

CA. 购买汽车作为出租车使用B. 农民购买化肥C. 购买商品房自己居住D. 政府出资修筑高速公路2、投资的收益和风险往往()。

AA. 同方向变化B. 反方向变化C. 先同方向变化,后反方向变化D. 先反方向变化,后同方向变化二、判断题1、资本可以有各种表现形态,但必须有价值。

()√2、证券投资是以实物投资为基础的,是实物投资活动的延伸。

()√3、从银行贷款从事房地产投机的人不是投资主体。

()×三、多项选择题1、以下是投资主体必备条件的有()ABDA.拥有一定量的货币资金 B.对其拥有的货币资金具有支配权C.必须能控制其所投资企业的经营决策 D.能够承担投资的风险2、下列属于真实资本有()ABCA.机器设备 B.房地产 C.黄金 D.股票3、下列属于直接投资的有()ABA.企业设立新工厂 B.某公司收购另一家公司60%的股权C.居民个人购买1000股某公司股票 D.发放长期贷款而不参与被贷款企业的经营活动四、简答题1、直接投资与间接投资第2章市场经济与投资决定习题一、单项选择题1、市场经济制度与计划经济制度的最大区别在于()。

BA. 两种经济制度所属社会制度不一样B. 两种经济制度的基础性资源配置方式不一样C. 两种经济制度的生产方式不一样D. 两种经济制度的生产资料所有制不一样2、市场经济配置资源的主要手段是()。

DA. 分配机制B. 再分配机制C. 生产机制D. 价格机制二、判断题1、在市场经济体制下,自利性是经济活动主体从事经济活动的内在动力。

()√2、产权不明晰或产权缺乏严格的法律保护是造成市场失灵的重要原因之一。

()×3、按现代产权理论,完整意义上的产权主要是指对一种物品或资源的支配使用权、自由转让权以及剩余产品的收益权。

()×四、简答题1、市场失灵、缺陷第3章证券投资概述习题一、单项选择题1、在下列证券中,投资风险最低的是()AA、国库券B、金融债券C、国际机构债券D、公司债券2、中国某公司在美国发行的以欧元为面值货币的债券称之为()BA.外国债券 B.欧洲债券 C.武士债券 D.扬基债券3、中央银行在证券市场市场买卖证券的目的是()DA、赚取利润B、控制股份C、分散风险D、宏观调控4、资本证券主要包括()。

博迪《投资学》(第10版)章节题库-第九章至第十章【圣才出品】

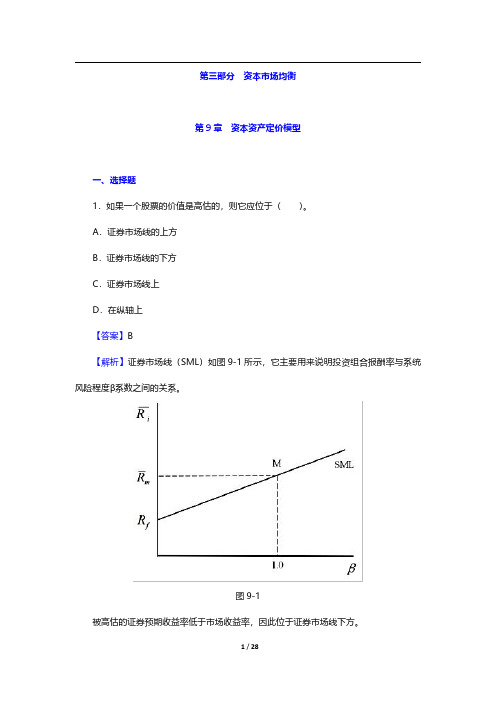

第三部分资本市场均衡第9章资本资产定价模型一、选择题1.如果一个股票的价值是高估的,则它应位于()。

A.证券市场线的上方B.证券市场线的下方C.证券市场线上D.在纵轴上【答案】B【解析】证券市场线(SML)如图9-1所示,它主要用来说明投资组合报酬率与系统风险程度β系数之间的关系。

图9-1被高估的证券预期收益率低于市场收益率,因此位于证券市场线下方。

2.无风险利率和市场预期收益率分别是3.5%和10.5%。

根据资本资产定价模型,一只β值是1.63的证券的预期收益是()。

A.10.12%B.14.91%C.16.56%D.18.79%【答案】B【解析】根据资本资产定价模型:E(r i)=r f+β[E(r M)-r f]=3.5%+1.63×(10.5%-3.5%)=14.91%。

3.资本资产定价模型给出了精确预测()的方法。

A.有效投资组合B.单一资产与风险资产组合期望收益率C.不同风险收益偏好下最优风险投资组合D.资产风险及其期望收益率之间的关系【答案】D【解析】根据资本资产定价模型,每一证券的期望收益率应等于无风险利率加上该证券由β系数测定的风险溢价。

4.假定一只股票定价合理,预期收益是15%,市场预期收益是10.5%,无风险利率是3.5%,这只股票的β值是()。

A.1.36B.1.52C.1.64D.1.75【答案】C【解析】既然α值假定为零,证券的收益就等于CAPM设定的收益。

因此,将已知的数值代入CAPM,即15%=[3.5%+(10.5%-3.5%)β],解得:β=1.64。

5.根据CAPM模型,市场期望收益率和无风险收益率分别是0.12和0.06,β值为1.2的证券A的期望收益率是()。

A.0.068B.0.12C.0.132D.0.142【答案】C【解析】根据资本资产定价模型,E(r i)=r f+[E(r M)-r f]βi=0.06+(0.12-0.06)×1.2=0.132。

威廉夏普投资学课后习题答案解析第九章

1. There are ten key assumptions underlying the CAPM:1. Investors evaluate portfolios by analyzing expected returns and standarddeviations over a one-period time horizon.2. Everything else equal, investors prefer portfolios with greater expectedreturns.3. Everything else equal, investors prefer portfolios with lower standarddeviations.4. Assets are infinitely divisible.5. Investors may borrow or lend at a single riskfree interest rate.6. Taxes and transaction costs are immaterial.7. All investors have the same one-period time horizon.8. All investors borrow and lend at the same riskfree rate.9. All investors have immediate and costless access to all relevant information.10. Investors possess homogeneous expectations regarding the expected returnsand risks of securities.3. The separation theorem states that an investor's optimal risky portfolio can bedetermined without reference to the investor's risk-return preferences.Assuming that every investor has the same expectations regarding expected returns and risks for available securities, and assuming that everyone faces the same riskfree rate, then the efficient set must be the same for all investors. This implies that every investor will hold the same risky portfolio. (That risky portfolio is represented by the point of tangency between a ray emanating from the riskfree asset and extending into risk-return space and tangent to the curved Markowitz efficient set.) The only difference in portfolios held by investors will be with respect to the amount of riskfree lending or borrowing undertaken, which will depend on the investors' individual risk-return preferences.6. If investors wish to hold more units of a security than are available, then they willbid up the price of the security, thereby reducing its expected return. The lower expected return will cause investors to reduce their desired holdings of the security.Conversely, if investors wish to hold fewer units of a security than are available, then they will bid down the security's price, thereby increasing its expected return.The higher expected return will cause investors to wish to hold more units of the security.This process will drive the price of the security toward its equilibrium value at which point the number of units investors wish to hold will equal the number of units outstanding. This equilibrating process will produce market clearing prices for all securities. Further, the riskfree rate will move to a level where the total amount of money borrowed will equal the supply of money available for lending.7. Investor does not require any adjustments by an investor in the market portfolio.Every security in the market portfolio is represented in proportion to its marketvalue relative to the market value of all securities. The market value of a secu rity is the units of the security outstanding times the market price of the security. Thus as relative prices of securities change, their relative market values and therefore their proportions of the market portfolio change concomitantly. No adjustment is required on the part of the investor.10. The equation of the Capital Market Line (CML) is:r p = r f + [(r M - r f )/ M ]* pIn this case, the market portfolio is composed of two securities, A and B . Thu s the expected return of the market portfolio is:r M = (X A ⨯ r A ) + (X B ⨯ r B )= (.40 ⨯ 10%) + (.60 ⨯ 15%)= 13.0%The standard deviation of the market portfolio is:[]2/122222B A AB B A B B A A M X X X X σσρσσσ++== {[(.40)² ⨯ (20)²] + [(.60)² ⨯ (28)²]+ [2 ⨯ (.40) ⨯ (.60) ⨯ (.30) ⨯ (20) ⨯ (28)]}½= [64 + 282.2 + 80.6]½ = 20.7%Therefore the equation for the CML is:r p = 5.0% + [(13.0% - 5.0%)/20.7%] ⨯ p= 5.0% + .39p12. The standard deviation of the market portfolio can be shown to equal the squareroot of the weighted average of the covariances of all its component securities with it. In the case of the this four security portfolio: M = [.20 ⨯ 242 + .30 ⨯ 360 + .20 ⨯ 155 + .30 ⨯ 210]½= (250.4)½ = 15.8%14. According to the CAPM, all investors will hold the market portfolio combinedwith riskfree borrowing or lending. Therefore all investors will be concerned with the risk (or standard deviation) of the market portfolio. The standard deviation of the market portfolio can be shown to be a function of the covariances with it of each of the securities that make up the market portfolio. Therefore th e contribution that each security makes to the market portfolio's risk will be directly related to its covariance with the market portfolio. Risk averse investors will demand higher returns from securities exhibiting higher covariances with the market portfolio.15. With respect to risk, the investor ultimately is concerned with the standarddeviation of his or her portfolio. Therefore, in evaluating a well-diversified portfolio, the relevant measure of risk is standard deviation. However, the contribution of an individual security to a portfolio's standard deviation is not the standard deviation of the security. That is, a portfolio's standard deviation is n ot simply the weighted average of the standard deviations of the component securities. The appropriate measure of a security's risk is the contribution that it makes to the standard deviation of a well-diversified portfolio. That contribution is reflected in the security's covariance with the portfolio.18. Oil is incorrect. The CAPM implies that it is possible for a security to have apositive standard deviation and an expected return less than the riskfree rate. Th e CAPM relationship specifies that:r p = r f + (r M - r f ) iM Thus a security with a negative covariance with the market portfolio would havean expected return less than the riskfree rate. In practice, however, few, if any , securities have a negative covariances with surrogates for the market portfolio.19. The beta of a security is calculated as:βσσi iM M =2Therefore:βA ==292151302.βB ==180150802. βC ==225151002.20. The beta of a portfolio is given by:ββp i i i n X ==∑1In Kitty's case:ßp = (.30 ⨯ .90) + (.10 ⨯ 1.30) + (.60 ⨯ 1.05)= 1.0322. a.b. r i = r f + (r M - r f )βi= 6% + (10% - 6%)ßi= 6% + (4%)ßi c. r A = 6% + (4%)(.85)= 9.4% r B= 6% + (4%)(1.20) = 10.8%24. A security that plots above the SML would be considered an attractive investment.The expected return offered by such a security is greater than that required given its risk. Investors should wish to add such a security to their portfolios.26. Market (or systematic) risk is the portion of a security's total risk that is related tomovements in the market portfolio and hence to the beta of the security. By definition, because the market portfolio is perfectly diversified, market risk in a portfolio cannot be reduced through diversification.Nonmarket (or unique or unsystematic) risk is the portion of a security's total riskthat is not related to moves in the market portfolio. Rather, it is related to even ts specific to the security. As a result, unique risk in a portfolio can be reduced through diversification.28. Two relationships are necessary to identify the missing data in the table:(1) r i = r f + (r M - r f )βi61218240.000.50 1.00 1.50 2.00E x p e c t e d R e t u r n (%)BetaR f =(2) ()2222i M p i εσσβσ+= Using these equations, consider security D first: 7.0 = r f + (r M - r f ) ⨯ 0 r f = 7.0% Next consider security B : 19.0 = 7.0 + (r M - 7.0) ⨯ 1.5 r M = 15.0% Next consider security C : 15.0 = 7.0 + (15.0 - 7.0) ßC ßC = 1.0 Further: (12)² = (1.0)² ⨯ σM 2 + 0 σM 2 = 12% Next consider security A : r A = 7.0 + (15.0 - 7.0)(.8) r A = 13.4% Further: A = [(.8)² ⨯ (12)² + 81]½= 13.2% Returning to security B : B = [(1.5)² ⨯ (12)² + 36]½ = 19.0% Finally, consider security E : 16.6 = 7.0 + (15.0 - 7.0) ßE ßE = 1.2 Further: (15)² = (1.2)² ⨯ (12)² + 2i εσ 2i εσ = 17.6。

博迪《投资学》(第9版)课后习题-资本资产定价模型(圣才出品)

第9章 资本资产定价模型一、习题1.如果()()1814P f M E r r E r =%, =6%, =%,那么该资产组合的β值等于多少?答:()()P f P M f E r r E r r β⎡⎤=+⨯−⎣⎦0.18=0.06+p β×(0.14-0.06)解得p β=0.12/0.08=1.5。

2.某证券的市场价格是50美元,期望收益率是14%,无风险利率为6%,市场风险溢价为8.5%。

如果该证券与市场投资组合的相关系数加倍(其他保持不变),该证券的市场价格是多少?假设该股票永远支付固定数额的股利。

答:如果该证券与市场投资组合的相关系数加倍(其他所有变量如方差保持不变),那么β和风险溢价也将加倍。

当前风险溢价为:14%-6%=8%。

因此新的风险溢价将变为16%,新的证券贴现率将变为:16%+6%=22%。

如果股票支付某一水平的永久红利,那么,从原始的数据中可以知道,红利必须满足永续年金的现值公式:价格=股利/贴现率即:50=D/0.14,解得,D =50×0.14=7(美元)。

在新的贴现率22%的情况下,股票价格为:7/0.22=31.82(美元)。

股票风险的增加使它的价值降低了36.36%。

3.下列选项是否正确?并给出解释。

a .β为零的股票提供的期望收益率为零。

b .资本资产定价模型认为投资者对持有高波动性证券要求更高的收益率。

c .你可以通过将75%的资金投资于短期国债,其余的资金投资于市场投资组合的方式来构建一个β为0.75的资产组合。

答:a .错误。

β=0意味着E (r )=r f ,不等于零。

b .错误。

只有承担了较高的系统风险(不可分散的风险或市场风险),投资者才要求较高期望收益;如果高风险债券的β较小,即使总风险较大,投资者要求的收益率也不会太高。

c .错误。

投资组合应当是75%的市场组合和25%的短期国债,此时β为:()()0.7510.2500.75p β=⨯+⨯=4.下表给出两个公司的数据。

《证券投资学》课后练习题9

第九章证券投资技术分析主要理论与方法一、选择题1.哪一种技术分析理论认为收盘价是最重要的价格?()A.道氏理论B.波浪理论C.切线理论D.形态理论2.K线理论起源于()A.美国B.日本C.印度D.英国3.在K线理论的四个价格中,()是最重要的。

A.开盘价B.收盘价C.最高价D.最低价4.在下列K线图中,开盘价等于最高价的有()A.光头光脚的阴线B.光头光脚的阳线C.十字星K线图D.带有上影线的光脚阳线5.在下列K线图中,收盘价等于最高价的有()A.光头光脚的阴线B.光头光脚的阳线C.十字星K线图D.带有上影线的光脚阳线6.K线图中的十字线的出现表明()A.多方力量还是略微比空方力量大点B.空方力量还是略微比多方力量大点C.多空双方的力量不分上下D.行情将继续维持以前的趋势,不存在大势变盘的意义7.黄昏之星通常出现在()A.上升趋势中B.下降趋势中C.横盘整理中D.顶部8.射击之星,一般出现在()A.顶部B.中部C.底部D.任意处9.下列不正确的说法是()A.锤形线出现在下降趋势的末端,而上吊线出现在上升趋势末端B.无论是锤形线还是上吊线其下影线都比实体长的多C.锤形线是熊尽牛来的信号,而上吊线是牛尽熊来的信号D.实体的颜色非常重要10.三白兵走势是:()A.两阴夹一阳B.两阳夹一阴C.三根阳线D.两阳一阴11.三乌鸦是指()A.一段下降趋势后的三根阳线B.一段下降趋势后的三根阴线C.一段上升趋势后的三根阳线D.一段上升趋势后的三根阴线12.光头光脚的长阳线表示当日()A.空方占优B.多方占优C.多、空平衡D.无法判断13.以下说法不正确的是()A.价格低开高收产生阳K线B.价格高开低收产生阴K线C.光头阳K线说明以当日最高价收盘D.今日价格高于前日价格必定是阳K线14.就单枝K线而言,反映多方占据绝对优势的K线形状是( )A.大十字星B.带有较长上影线的阳线C.光头光脚大阴线D.光头光脚大阳线15.不适合短线买进的股票是()A.买卖量都较小,股价轻度下跌B.遇个股利空但放量不跌C.无量大幅急跌D.分红除权后上涨16.下面一般不宜作为趋势分析对象的是()A.长期趋势B.中期趋势C.短期趋势D.中长期趋势17.在上升趋势中,将()连成一条直线,就得到上升趋势线A.两个低点B.两个高点C.一个低点、一个高点D.任意两点18.连接连续下降的高点得到()A.轨道线B.上升趋势线C.支撑线D.下降趋势线19.一般说来,可以根据下列()因素判断趋势线的有效性A.趋势线的斜率越大,有效性越强B.趋势线的斜率越小,有效性越强C.趋势线被触及的次数越少,有效性越被得到确认D.趋势线被触及的次数越多,有效性越被得到确认20.在上升趋势中,如果下一次未创新高,即未突破压力线,往后股价反而向下突破了这个上升趋势的支撑线,通常这意味着()A.上升趋势开始B.上升趋势保持C.上升趋势已经结束D.没有含义21.支撑线和压力线之所以能起支撑和压力作用,两者之间之所以能够相互转化,很大程度是由于()方面的原因A.机构主力争斗的结果B.心理因素C.筹码发布D.持有成本22.趋势线被突破后,这说明()A.股价会上升B.股价走势将反转C.股价会下跌D.股价走势将加速23.在技术分析理论中,不能单独存在的切线是()A.支撑线B.压力线C.轨道线D.趋势线24.下列说法正确的是()A.证券市场里的人分为多头和空头两种B.压力线只存在于上升行情中C.一旦市场趋势确立,市场变动就朝一个方向运动直到趋势改变D.支撑线和压力线是短暂的,可以相互转换25.费波纳奇数列正确的排列是()A.1,3,5,7...B.2,4,6,8...C.2,3,5,8...D.1,2,3,6...26.和黄金分割线有关的一些数字中,有一组最为重要,股价极容易在由这组数字产生的黄金分割线处产生支撑和压力,请找出这一组()A. 0.618、1.618、2.618 B. 0.382、06.18、1.191C. 0.618、1.618、4.236 D. 0.382、0.809、4.23627.依据三次突破原则的方法是()A.速度线B.扇形线C.甘氏线D.百分比线28.在百分比线中,()线最为重要A.1/4B.1/3C.1/2D.2/329.根据技术分析理论,不能独立存在的切线是()A.扇形线B.百分比线C.轨(通)道线D.速度线30.如果希望预测未来较长时期的走势,应当使用()A.K线B.K线组合C.形态理论D.黄金分割线31.下面四个图形中,唯一只被当作中继形态的是()A.旗形B.楔形C.菱形D.直角三角型32.()是最著名和最可靠的反转突破形态A.头肩形态B.双重顶(底)C.圆弧形态D.喇叭形33.头肩顶形态的高度是指()A.头的高度B.左、右肩连线的高度C.头到颈线的距离D.颈线的高度34.属于持续整理形态的有()A.菱形B.钻石形C.旗形D.W形态35.属于持续整理形态的有()A.菱形B.钻石形C.圆弧形D.三角形36.如果股价原有的趋势是向上,进入整理状态时形成上升三角形,那么可以初步判断今后的走势会()A.继续整理B.向下突破C.向上突破D.不能判断37.出现在顶部的看跌的形态是()A.菱形B.旗形C.楔形D.三角形38.下列对圆形底特征描述不正确的是()A.底部成交量极小B.从反转过程来看,不论股价或成交量都呈圆形C.上升行情属于爆发性的,涨得急,结束也快D.上涨初期成交量急速放大39.下列不属于持续形态的是()A.喇叭形B.矩形C.旗形D.三角形40.与头肩顶形态相比,三重形态更容易演变为()A.反转突破形态B.圆弧顶形态C.持续整理形态D.其他各种形态41.下列不正确说法的是()A.V形反转一般事先无征兆B.大都因市场外突发信息引起的C.可以结合支撑线、压力线以及技术指标通过消息面加以研判D.经过多次顶和底的试探42.下面不属于波浪理论主要考虑因素的是()A.成交量B.时间C.比例D.形态43.艾略特波浪理论的数学基础来自()A.周期理论B.黄金分割理论C.时间数列D.斐波那奇数列44.波浪理论认为一个完整的周期分为()A.推动5浪,调整3浪B.推动5浪,调整2浪C.推动3浪,调整3浪D.推动4浪,调整2浪45.下列不正确说法的是()A.每个推动浪又可细分为5浪B.每个调整浪又可细分为3浪C.波浪理论的数浪很容易D.推动第5浪通常有延伸浪46.波浪理论的最核心的内容是以()为基础的A.K线理论B.指标C.切线D.周期二、名词解释1、K线:一根K线记录了证券在一个交易时间段内的价格变动情况,将它们按照时间顺序连接起来就成为了K线图。

投资学:现代金融理财技术理论(后附:答案)

投资学:现代⾦融理财技术理论(后附:答案)第九章现代⾦融理财技术理论练习题:⼀、名词解释:1、预期收益2、期望收益率3、⽅差4、投资者共同偏好规则5、协⽅差6、相关系数7、结合线8、有效组合9、有效边缘10、资产组合效⽤11、效⽤⽆差异曲线12、最优资产组合13、市场组合14、资本市场线15、阿尔法系数 16、证券市场线17、证券特征线18、套利19、单指数模型20、多指数模型⼆、判断题:1、组合资产的收益率是各种资产收益率的加权平均。

2、离散程度是指各种收益可能性偏离预期风险的⼤⼩。

3、⽅差(标准差)越⼤,说明实际收益偏离预期收益的离散程度越⼤,风险就越⾼。

4、从正态分布离散程度的⼀般规律来看,实际收益率围绕期望收益左右两个标准差这⼀区域内波动的概率接近99.74%。

5、如果协⽅差是负值,表明资产A和资产B的收益有相互⼀致的变动趋向,即⼀种资产的收益⾼于预期收益,另⼀种资产的收益也⾼于预期收益。

6、市场组合中风险证券所占权重完全⼀致,在收益率上完全不相关。

7、所有有效组合都是由风险资产与市场组合再组合的结果。

8、⽆效组合位于资本市场线的下⽅。

9、市场组合中每⼀只风险证券⽐重均⾮零。

10、市场组合是充分分散的组合,因此没有系统风险。

11、协⽅差较⼩的证券,即使其⽅差较⼤,也会被认为是风险较⼩的证券。

12、资产的阿尔法系数为正,表明它位于证券市场线的下⽅,其价格被低估。

13、任何资产和资产组合的收益与系统风险⽆关,只决定于⾮系统风险的⾼低。

14、套利定价理论是要说明市场均衡时合理价位是如何形成的。

15、资本资产定价模型可以看着是套利定价理论的⼀种特殊情形。

16、套利模型为均衡模型,⽽特征线模型为⾮均衡模型。

17、单个证券因为随机误差项的⼲扰,收益率同共同因⼦间不存在完全线性关系,但充分分散的投资组合收益率则与共同因⼦间存在着明显的线性关系。

18、在市场均衡时,所有证券或证券组合的期望收益率都取决于风险因⼦的价值。

投资学第9章习题及答案

投资学第9章习题及答案篇一:投资学第九版课后习题答案--第10、11章第10章5、因为投资组合F的β=0,所以其预期收益等于无风险利率对于投资组合A,风险溢价与β的比率为(12-6)/1.2=5 对于投资组合E,风险溢价与β的比率为(8-6)/0.6=3.33对比表明,这里有套现机会存在。

例如,我们能创建一个投资组合G,其包含投资组合A和投资组合F,并且两者有相等的权重,使它满足β等于0.6;这样投资组合F的期望收益和β为:E(rG ) = (0.5 × 12%) + (0.5 × 6%) = 9%βG = (0.5 × 1.2) + (0.5 × 0%) = 0.6对比投资组合G和投资组合E,投资组合G跟E具有相同的β值,但具有更高的期望收益。

因此通过买入投资组合G,并卖出相同数量投资组合E资产就可以实现套现机会。

这种套现利润:rG �C rE =[9% + (0.6 × F)] ? [8% + (0.6 × F)] = 1%6、设无风险利率为rf,风险溢价因素RP,则:12% = rf + (1.2 × RP)9% = rf + (0.8 × RP)解之得: rf=3%,RP=7.5%7、a、由题目知,买进100万美元等权重的正α值的股票并同时卖出100万美元的等权重的负α值的股票;假定市场风险为0;则预期收益为:$1,000,000*0.02-$1,000,000*(-0.02)=$40,000b、对于分析师分析的20只股票,每只股票持有时都分别为$100,000,市场风险为0,公司持有的收益标准差为30%,所以20只股票的方差为20 × [($100,000 × 0.30)* ($100,000 × 0.30)] = $18,000,000,000故标准差为$134,164a、如果分析师分析的是50只股票,那么每只股票持有时都分别为$40,000,计算收益方差:50 × [(40,000 × 0.30)* (40,000 × 0.30)] = 7,200,000,000故标准差为$84,853;由于总投入资金不变,α值不变,故其期望收益也不变,为$40,0008、2a、?2??2?2M??(e)2?A?(0.82?202)?252?881222?2B?(1.0?20)?10?5002?C?(1.22?202)?202?976b、如果资产种类很多,并且具有相同的收益特征,每一个种类的充分分散投资组合将存在唯一的系统风险,因为非系统性风险随着n的无穷大会趋近于0,因此充分分散的投资组合的超额收益方差的均值为:2 ?A?2562?B?400?C2?576C、市场中不存在套现机会第11章9、答案:C。

《证券投资学》课后练习题9 大题答案

第九章证券投资技术分析主要理论与方法二、名词解释K线、开盘价、收盘价、最高价、最低价、阳线、阴线、影线、跳空、空头、多头、支撑线、压力线、趋势线、轨道线、黄金分割线、百分比线、速度线、甘氏线、反转形态、整理形态、头肩顶、头肩底、双重底、双重顶、三重底、三重顶、圆形底、圆形顶、三角形、矩形、楔形、旗形、喇叭形、菱形、V形、突破、随机漫步理论、循环周期理论、相反理论。

1. K线:K线图最早是日本德川幕府时代大阪的米商用来记录当时一天、一周或一月中米价涨跌行情的图示法,后被引入股市。

K线图有直观、立体感强、携带信息量大的特点,蕴涵着丰富的东方哲学思想,能充分显示股价趋势的强弱、买卖双方力量平衡的变化,预测后市走向较准确,是应用较多的技术分析手段。

2. 开盘价:目前我国股票市场采用集合竞价的方式产生开盘价。

3. 收盘价:是多空双方经过一段时间的争斗后最终达到的共识,是供需双方最后的暂时平衡点,具有指明价格的功能。

4. 最高价:是交易过程中出现的最高的价格。

5. 最低价:是交易过程中出现的最低的价格。

6. 阳线:收盘价高于开盘价时用空(或红)实体表示,称为阳线。

7. 阴线:开盘价高于收盘价时用黑(或蓝)实体表示,称为阴线。

8. 影线:影线表示高价和低价。

9.跳空:股价受利多或利空影响后,出现较大幅度上下跳动的现象。

大小所决定.10、空头:空头是投资者和股票商认为现时股价虽然较高,但对股市前景看坏,预计股价将会下跌,于是把借来的股票及时卖出,待股价跌至某一价位时再买进,以获取差额收益。

空头指的是变为股价已上涨到了最高点,很快便会下跌,或当股票已开始下跌时,认为还会继续下跌,趁高价时卖出的投资者。

采用这种先卖出后买进、从中赚取差价的交易方式称为空头。

人们通常把股价长期呈下跌趋势的股票市场称为空头市场,空头市场股价变化的特征是一连串的大跌小涨。

11、多头:多头是指投资者对股市看好,预计股价将会看涨,于是趁低价时买进股票,待股票上涨至某一价位时再卖出,以获取差额收益。

投资学第九章

元。该股票预计来年派发红利3美元。投资者预期 可以以41美元卖出。股票风险的=-0.5,该股票是 高估还是低估了?

• a. 因为市场组合的β定义为1,它的预期收益率为 12%。

• 如果股票支付某一水平的永久红利,则我们可以从红利D的原始数据 知道必须满足永久债券的等式:价格=红利/折现率

•

5 0 =D/ 0 . 1 4

•

D= 5 0×0 . 1 4 = 7 . 0 0美元

• 在新的折现率2 2%的条件下,股票价值为7美元/ 0 . 2 2 = 3 1 . 8 2美 元。股票风险的增加使得它的价值降低了3 6 . 3 6%。

• 为股票的β 等于1,它的预期收益率应该等 于市场收益率,即6 + 1 . 2 ( 1 6-6) =18%。

•

E(r) = (D1+P1-P0) /P0

•

0. 1 8 = ( 6 +P1-5 0 ) / 5 0

•

= 5 3美元

• 4、投资者购入一企业,其预期的永久现金 流为1 000美元,但因有风险而不确定。如 果投资者认为企业的贝塔值是0 . 5,当贝塔 值实际为1时,投资者愿意支付的金额比该 企业实际价值高多少?

散的或市场风险)的风险溢价。全部波动包 括不可分散的风险。

• c. 错。你的资产组合的75%应投资于市场, 25%投资于国库券。因此,

• β=0.75×1+ 0.25×0=0.75

如果简单的C A P M模型是有效的,下列各题中哪 些情形是有可能的,试说明之。每种情况单独考虑。

投资学第七版ch09课后答案

CHAPTER 9AN INTRODUCTION TO ASSET PRICING MODELSTRUE/FALSE QUESTIONS(t) 1 One of the assumptions of Capital Market Theory is that investors can borrow or lend at the risk-free rate.(f) 2 An assumption of Capital Market Theory is that buying or selling of assets entailsno taxes, but entails significant transaction costs.(t) 3 A risky asset is an asset with uncertain future returns, and uncertainty (or risk) is measured by the variance or standard deviation of returns.(t) 4 The standard deviation of a portfolio that combines the risk-free asset with risky assets is the linear proportion of the standard deviation of the risky asset portfolio.(t) 5 The Capital Market Line (CML) is the line from the intercept point that represents the risk-free rate tangent to the original efficient frontier.(t) 6 The market portfolio consists of all risky assets.(f) 7 All portfolios on the CML are perfectly negatively correlated, which means thatall portfolios on the CML are perfectly negatively correlated with thecompletely diversified market portfolio since it lies on the CML.(t) 8 Diversification reduces the unsystematic risk in a portfolio.(f) 9 The Capital Asset Pricing Model (CAPM) is a technique for determining theexpected risk on an asset.(t) 10 Beta is a standardized measure of systematic risk.(t) 11 Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.(f) 12 Arbitrage Pricing Theory (APT) specifies the exact number of risk factors andtheir identity388MULTIPLE CHOICE QUESTIONS(d) 1 Which of the following is not an assumption of the Capital Market Theory?a)All investors are Markowitz efficient investors.b)All investors have homogeneous expectations.c)There are no taxes or transaction costs in buying or selling assets.d)There are no risk-free assets.e)All investors have the same one period time horizon.(e) 2 The market portfolio consists of alla)New York Stock Exchange stocks.b)International stocks and bonds.c)Stocks and bonds.d)U.S. and non-U.S. stocks and bonds.e)Risky assets.(c) 3 The separation theorems divides decisions on from decisions on .a)Lending, borrowingb)Risk, returnc)Investing, financingd)Risky assets, risk free assetse)Buying stocks, buying bonds(d) 4 When identifying undervalued and overvalued assets, which of the followingstatements is false?a)An asset is properly valued if its estimated rate of return is equal to itsrequired rate of return.b)An asset is considered overvalued if its estimated rate of return is below itsrequired rate of return.c)An asset is considered undervalued if its estimated rate of return is above itsrequired rate of return.d)An asset is considered overvalued if its required rate of return is below itsestimated rate of return.e)None of the above (that is, all are true statements)(b) 5 Utilizing the security market line an investor o wning a stock with a beta of (-2)would expect the stock's return to in a market thata)Rise or fall an indeterminate amountb)Rise by 20.0%389c)Fall by 20.0%d)Rise by 10.2%e)Fall by 10.2%(d) 6 The Capital Market Line (CML) refers to the efficient formed by creatingportfolios thata)Invest solely in the market portfolio M.b)Lend at the risk free asset and invest in the market portfolio.c)Borrow at the risk free asset and invest in the market portfolio.d)Lend and borrow at the risk free rate and invest in the market portfolio.e)Short sell the market portfolio.(e) 7 As the number of stocks in a portfolio increasesa)The expected return of the portfolio increases because systematic riskdecreases.b)The expected return of the portfolio increases because unsystematic riskdecreases.c)The standard deviation of the portfolio increases because systematic riskincreases.d)The standard deviation of the portfolio decreases because systematic riskincreases.e)The standard deviation of the portfolio decreases because unsystematic riskdecreases.(a) 8 The Security Market Line (SML) represents the relation betweena)Risk and required return on an asset.b)Systematic risk and required return on an asset.c)Risk and return on a diversified portfolio of assets.d)Unsystematic risk and required return on an assete)Systematic risk and required return on a diversified portfolio of assets.(a) 9 In a macro-economic based risk factor model the following factor would be oneof many appropriate factorsa)Confidence risk.b)Maturity risk.c)Expected inflation risk.d)Call risk.e)Return difference between small capitalization and large capitalization stocks.(d) 10 In a multifactor model, confidence risk representsa)Unanticipated changes in the level of overall business activity.390b)Unanticipated changes in investors’ desired time to receive payouts.c)Unanticipated changes in short term and long term inflation rates.d)Unanticipated changes in the willingness of investors to take on investmentrisk.e)None of the above.(b) 11 In a multifactor model, time horizon risk representsa)Unanticipated changes in the level of overall business activity.b)Unanticipated changes in investors’ desired time to receive payouts.c)Unanticipated changes in short term and long term inflation rates.d)Unanticipated changes in the willingness of investors to take on investmentrisk.e)None of the above.(e) 12 In a micro-economic based risk factor model the following factor would be oneof many appropriate factorsa)Confidence risk.b)Maturity risk.c)Expected inflation risk.d)Call risk.e)Return difference between small capitalization and large capitalization stocks.391MULTIPLE CHOICE PROBLEMS(b) 1 Consider an asset that has a beta of 1.5. The return on the risk-free asset is 6.5%and the expected return on the stock index is 15%. The estimated return on theasset is 20%. Calculate the alpha for the asset.a)19.25%b)0.75%c)–0.75%d)9.75%e)9.0%(b) 2 The table below provides factor risk sensitivities and factor risk premia for a threefactor model for a particular asset where factor 1 is MP the growth rate in U.S.industrial production, factor 2 is UI the difference between actual and expectedinflation, and factor 3 is UPR the unanticipated change in bond credit spread.Risk FactorFactorSensitivity(β)RiskPremium(λ)MP 1.760.0259UI -0.8-0.0432UPR 0.87 0.0149Calculate the expected excess return for the asset.a)12.32%b)9.32%c) 4.56%d) 6.32%e)8.02%(b) 3 The variance of returns for a risky asset is 25%. The variance of the error term,Var(e) is 8%. What portion of the total risk of the asset, as measured by variance,is unsystematic?a)32%b)8%c)68%d)25%e)75%(c) 4 An investor wishes to construct a portfolio consisting of a 40% allocation to astock index and a 60% allocation to a risk free asset. The return on the risk-free392asset is 2% and the expected return on the stock index is 10%. The standarddeviation of returns on the stock index 8%. Calculate the expected standarddeviation of the portfolio.a) 5.2%b)8.0%c) 3.2%d) 4.0%e) 1.2%(b) 5 An investor wishes to construct a portfolio by borrowing 35% of his originalwealth and investing all the money in a stock index. The return on the risk-freeasset is 4.0% and the expected return on the stock index is 15%. Calculate theexpected return on the portfolio.a)18.25%b)18.85%c)9.50%d)15.00%e)11.15%(d) 6 An investor wishes to construct a portfolio consisting of a 70% allocation to astock index and a 30% allocation to a risk free asset. The return on the risk-freeasset is 4.5% and the expected return on the stock index is 12%. Calculate theexpected return on the portfolio.a)8.25%b)16.50%c)17.50%d)9.75%e)14.38%(d) 7 A stock has a beta of the stock is 1.1. The risk free rate is 2.5% and the return onthe market is 12%. The estimated return for the stock is 14%. According to theCAPM you shoulda)Sell because required return is 9.95%.b)Sell because required return is 16.5%.c)Buy because required return 11.5%.d)Buy because required return is 12.95%.e)Short because it is undervalued.(b) 8 Consider a risky asset that has a standard deviation of returns of 15. Calculate thecorrelation between the risky asset and a risk free asset.a) 1.0b)0.0393c)-1.0d)0.5e)-0.5(a) 9 The expected return for a stock, calculated using the CAPM, is 10.5%. Themarket return is 9.5% and the beta of the stock is 1.50. Calculate the implied risk-free rate.a)7.50%b)13.91%c)17.50%d)21.88%e)14.38%(d) 10 The expected return for a stock, calculated using the CAPM, is 25%. The risk freerate is 7.5% and the beta of the stock is 0.80. Calculate the implied return on themarket.a)7.50%b)13.91%c)17.50%d)21.88%e)14.38%(c) 11 The expected return for Zbrite stock calculated using the CAPM is 15.5%. Therisk free rate is 3.5% and the beta of the stock is 1.2. Calculate the implied marketrisk premium.a) 5.5%b) 6.5%c)10.0%d)15.5%e)12.0%(d) 12 Calculate the expected return for Express Inc. which has a beta of .69 when therisk free rate is.09 and you expect the market return to be .14.a)0.05%b)13.91%c)10.92%d)12.45%e)14.25%USE THE FOLLOWING INFORMATION FOR THE NEXT THREE PROBLEMS394You expect the risk-free rate (RFR) to be 5 percent and the market return to be 9 percent. You also have the following information about three stocks.CURRENT E XPECTED EXPECTEDSTOCK BETA PRICE PRICE DIVIDENDY 0.50 $ 40 $ 43 $ 1.50Z 2.00 $ 45 $ 49 $ 1.00(b) 13 What are the expected (required) rates of return for the three stocks (in the orderX, Y, Z)?a)16.50%, 5.50%, 22.00%b)11.00%, 7.00%, 13.00%c)7.95%, 11.25%, 11.11%d) 6.20%, 2.20%, 8.20%e)15.00%, 3.50%, 7.30%(a) 14 What are the estimated rates of return for the three stocks (in the order X, Y, Z)?a)7.95%, 11.25%, 11.11%b) 6.20%, 2.20%, 8.20%c)16.50%, 5.50%, 22.00%d)11.00%, 7.00%, 13.00%e)15.00%, 3.50%, 7.30%(e) 15 What is your investment strategy concerning the three stocks?a)Buy stock Y, it is undervalued.b)Buy stock X and Z, they are undervalued.c)Sell stocks X and Z, they are overvalued.d)Sell stock Y, it is overvalued.e)Choices a and cUSE THE FOLLOWING INFORMATION FOR THE NEXT FOUR PROBLEMSYear Return forGBCReturn forMarket1 25 122 10 133 5 174 -13 -155 11 -86 -20 9395(a) 16 Compute the beta for GBC Company using the historic returns presented above.a)0.4255b)0.5929c) 5.6825d)9.4163e)0.3333(e) 17 Compute the correlation coefficient between GBC and the Market Index.a)0.4255b)0.5929c) 5.6825d)9.4163e)0.3333(b) 18 Compute the intercept of the characteristic linea)0.4255b) 1.013c) 1.4385d)0.5875e)0.5219(d) 19 The equation of the characteristic line isa)R GBC + 1.013 = 0.4255(R Market)b)R GBC = 1.013 - 0.4255(R Market)c)R Market = 1.013 + 0.4255(R GBC)d)R GBC = 1.013 + 0.4255(R Market)e)R Market = 1.013 - 0.4255(R Market)396CHAPTER 9ANSWERS TO PROBLEMS1 6.5 + 1.5(15 – 6.5) = 19.25%alpha = 20 –19.25 = 0.75%2 The table below shows the relevant calculationsRisk FactorFactorSensitivity(β)RiskPremium(λ)(β)x(λ)MP 1.760.02590.0456UI -0.8-0.04320.0346UPR 0.870.01490.013Expected return 0.12323 8%/25% = 0.32. = 32% unsystematic.4 0.4(0.08) = 0.032 or 3.2%5 -0.35(4) + 1.35(15) = 18.85%6 E(R)= 0.3(4.5) + 0.7(12) = 9.75%7 E(R)= 2.5 + 1.1(12 – 2.5) = 12.95%. Buy the stock is undervalued.8 The correlation between a risky asset and a risk-freeasset is always zero.9 10.5 = X + 1.5(9.5 – X). X = 7.5%.10 25 = 7.5 + 0.8(X). X = 14.38%. Return on market = 14.38 + 7.5 = 21.88%11 15.5 = 3.5 + 1.2(X). X = 10%.12 k = .09 + .69 (.14 - .09) = .1245 = 12.45%For problems 13 - 15STOCK REQUIRED ESTIMATED EVALUATIONX .05 + 1.50(.09 - .05) = 11% (23 - 22 + 0.75)/22 = 7.95% OvervaluedY .05 + 0.50(.09 -.05) = 7% (43 - 40 + 1.50)/40 = 11.25% UndervaluedZ .05 + 2.00(.09 - .05) = 13% (49 - 45 + 1.00)/45 = 11.11% Overvalued397For problems 16 – 19The table below shows the relevant calculations.(1) (2) (3) (4) (5) (6) (7) (8)x(7)(6)GBCMarketMarketGBC))2(R-E(R ))2R-E(R )R-E(R )Year GBC Market(R-E(R7.33161.2622.0053.731 25 12484.008.337.0058.312 10 1369.3949.0024.6612.332.003 5 174.00152.03-19.67314.72-16.004 -13 -15386.91256.00-12.67-101.368.0064.005 11 -8160.534.33-99.59-23.0018.756 -20 9529.00841.33 358.00 Total 18 281386.003.00004.67Average168.27Variance 277.20Dev. 16.6512.97Std.Covariance 71.60 Correlation 0.33 Beta 0.425516 Beta for GBC Computer is computed as follows:Beta = Cov(GBC, Market)/ Variance MarketBeta = 18.40/82 = 0.224417 The correlation coefficient can be computed as follows:Correlation = Cov(GBC, Market)/(SD GBC x SD Market)= 71.6/(16.65 x 12.97) = 0.33Where:SD GBC = [1386/5]1/2 = 16.65SD Market = [841.33/5]1/2 = 12.97Cov(GBC, Market) = 358/5 = 71.6018 The alpha or intercept of the characteristic line is computed as follows:alpha = 3.0 - [(0.4255)(4.67)] = 1.013%R GBC = 1.013 + 0.4255(R Market)19398。

投资学第10版习题答案09

CHAPTER 9: THE CAPITAL ASSET PRICING MODELPROBLEM SETS1.2. If the security’s correlation coefficient with the market portfolio doubles (with all othervariables such as variances unchanged), then beta, and therefore the risk premium, will also double. The current risk premium is: 14% – 6% = 8%The new risk premium would be 16%, and the new discount rate for the security would be: 16% + 6% = 22%If the stock pays a constant perpetual dividend, then we know from the original data that the dividend (D) must satisfy the equation for the present value of a perpetuity:Price = Dividend/Discount rate50 = D /0.14 ⇒ D = 50 ⨯ 0.14 = $7.00At the new discount rate of 22%, the stock would be worth: $7/0.22 = $31.82The increase in stock risk has lowered its value by 36.36%.3. a.False. β = 0 implies E (r ) = r f , not zero.b. False. Investors require a risk premium only for bearing systematic (undiversifiable or market) risk. Total volatility, as measured by the standard deviation, includes diversifiable risk.c. False. Your portfolio should be invested 75% in the market portfolio and 25% in T-bills. Then:β(0.751)(0.250)0.75P =⨯+⨯=4. The expected return is the return predicted by the CAPM for a given level of systematicrisk.$1$5()β[()]().04 1.5(.10.04).13,or 13%().04 1.0(.10.04).10,or 10%i f i M f Discount Everything E r r E r r E r E r =+⨯-=+⨯-==+⨯-=()β[()].12.18.06β[.14.06]β 1.5.08P f P M f P P E r r E r r =+⨯-=+⨯-→==5. According to the CAPM, $1 Discount Stores requires a return of 13% based on itssystematic risk level of β = 1.5. However, the forecasted return is only 12%. Therefore, the security is currently overvalued.Everything $5 requires a return of 10% based on its systematic risk level of β = 1.0.However, the forecasted return is 11%. Therefore, the security is currently undervalued. 6. Correct answer is choice a. The expected return of a stock with a β = 1.0 must, onaverage, be the same as the expected return of the market which also has a β = 1.0.7. Correct answer is choice a. Beta is a measure of systematic risk. Since only systematic risk is rewarded, it is safe to conclude that the expected return will be higher for Kaskin’s stock than for Quinn’s stock.8.The appropriate discount rate for the project is:r f + β × [E (r M ) – r f ] = .08 + [1.8 ⨯ (.16 – .08)] = .224, or 22.4% Using this discount rate:101$15NPV $40$40[$151.224t t ==-+=-+⨯∑Annuity factor (22.4%, 10 years)] = $18.09 The internal rate of return (IRR) for the project is 35.73%. Recall from your introductory finance class that NPV is positive if IRR > discount rate (or, equivalently, hurdle rate). The highest value that beta can take before the hurdle rate exceeds the IRR is determined by:.3573 = .08 + β × (.16 – .08) ⇒ β = .2773/.08 = 3.479. a. Call the aggressive stock A and the defensive stock D. Beta is the sensitivity of thestock’s return to the market return, i.e., the change in the stock return per unitchange in the market return. Therefore, we compute each stock’s beta bycalculating the difference in its return across the two scenarios divided by the difference in the market return:.02.38.06.12β 2.00β0.30.05.25.05.25A D ---====--b.With the two scenarios equally likely, the expected return is an average of the twopossible outcomes:E(r A) = 0.5 ⨯ (–.02 + .38) = .18 = 18%E(r D) = 0.5 ⨯ (.06 + .12) = .09 = 9%c.The SML is determined by the market expected return of [0.5 × (.25 + .05)] =15%, with βM= 1, and r f = 6% (which has βf=0). See the following graph:The equation for the security market line is:E(r) = .06 + β × (.15 – .06)d. Based on its risk, the aggressive stock has a required expected return of:E(r A ) = .06 + 2.0 × (.15 – .06) = .24 = 24%The analyst’s forecast of expected return is only 18%. Thus the stock’s alpha is:αA = actually expected return – required return (given risk)= 18% – 24% = –6%Similarly, the required return for the defensive stock is:E(r D) = .06 + 0.3 × (.15 – .06) = 8.7%The analyst’s forecast of expected return for D is 9%, and hence, the stock has a positive alpha:αD = Actually expected return – Required return (given risk)= .09 – .087 = +0.003 = +0.3%The points for each stock plot on the graph as indicated above. e. The hurdle rate is determined by the project beta (0.3), not the firm’s beta . Thecorrect discount rate is 8.7%, the fair rate of return for stock D.10. Not possible. Portfolio A has a higher beta than Portfolio B, but the expected return forPortfolio A is lower than the expected return for Portfolio B. Thus, these two portfolios cannot exist in equilibrium.11. Possible. If the CAPM is valid, the expected rate of return compensates only forsystematic (market) risk, represented by beta, rather than for the standard deviation,which includes nonsystematic risk. Thus, Portfolio A’s lower rate of return can be paired with a higher standard deviation, as long as A’s beta is less than B’s.12. Not possible. The reward-to-variability ratio for Portfolio A is better than that of themarket. This scenario is impossible according to the CAPM because the CAPM predicts that the market is the most efficient portfolio. Using the numbers supplied:.16.10.18.100.50.33.12.24A M S S --==== Portfolio A provides a better risk-reward trade-off than the market portfolio.13. Not possible. Portfolio A clearly dominates the market portfolio. Portfolio A has both alower standard deviation and a higher expected return.14. Not possible. The SML for this scenario is: E(r ) = 10 + β × (18 – 10)Portfolios with beta equal to 1.5 have an expected return equal to:E (r ) = 10 + [1.5 × (18 – 10)] = 22%The expected return for Portfolio A is 16%; that is, Portfolio A plots below the SML (α A = –6%) and, hence, is an overpriced portfolio. This is inconsistent with the CAPM.15. Not possible. The SML is the same as in Problem 14. Here, Portfolio A’s required returnis: .10 + (.9 × .08) = 17.2%This is greater than 16%. Portfolio A is overpriced with a negative alpha:α A = –1.2%16. Possible. The CML is the same as in Problem 12. Portfolio A plots below the CML, asany asset is expected to. This scenario is not inconsistent with the CAPM.17. Since the stock’s beta is equal to 1.2, its expected rate of return is:.06 + [1.2 ⨯ (.16 – .06)] = 18%110110$50$6()0.18$53$50D P P PE r P P -+-+=→=→=18. The series of $1,000 payments is a perpetuity. If beta is 0.5, the cash flow should bediscounted at the rate:.06 + [0.5 × (.16 – .06)] = .11 = 11%PV = $1,000/0.11 = $9,090.91If, however, beta is equal to 1, then the investment should yield 16%, and the price paid for the firm should be:PV = $1,000/0.16 = $6,250The difference, $2,840.91, is the amount you will overpay if you erroneously assume that beta is 0.5 rather than 1.19. Using the SML: .04 = .06 + β × (.16 – .06) ⇒ β = –.02/.10 = –0.220. r 1 = 19%; r 2 = 16%; β1 = 1.5; β2 = 1a. To determine which investor was a better selector of individual stocks we look atabnormal return, which is the ex-post alpha; that is, the abnormal return is thedifference between the actual return and that predicted by the SML. Withoutinformation about the parameters of this equation (risk-free rate and market rate ofreturn) we cannot determine which investor was more accurate.b.If r f = 6% and r M = 14%, then (using the notation alpha for the abnormal return):α1 = .19 – [.06 + 1.5 × (.14 – .06)] = .19 – .18 = 1%α 2 = .16 – [.06 + 1 × (.14 – .06)] = .16 – .14 = 2%Here, the second investor has the larger abnormal return and thus appears to be the superior stock selector. By making better predictions, the secondinvestor appears to have tilted his portfolio toward underpriced stocks.c. If r f = 3% and r M = 15%, then:α1 = .19 – [.03 + 1.5 × (.15 – .03)] = .19 – .21 = –2%α2 = .16 – [.03+ 1 × (.15 – .03)] = .16 – .15 = 1%Here, not only does the second investor appear to be the superior stock selector,but the first investor’s predictions appear valueless (or worse).21. a. Since the market portfolio, by definition, has a beta of 1, its expected rate of returnis 12%.b. β = 0 means no systematic risk. Hence, the sto ck’s expected rate of return inmarket equilibrium is the risk-free rate, 5%.c.Using the SML, the fair expected rate of return for a stock with β = –0.5 is:()0.05[(0.5)(0.120.05)] 1.5%E r =+-⨯-= The actually expected rate of return, using the expected price and dividend for next year is:$41$3()10.1010%$40E r +=-== Because the actually expected return exceeds the fair return, the stock isunderpriced.22. In the zero-beta CAPM the zero-beta portfolio replaces the risk-free rate, and thus:E (r ) = 8 + 0.6(17 – 8) = 13.4%23. a. E (r P ) = r f + βP × [E (r M ) – r f ] = 5% + 0.8 (15% − 5%) = 13%α = 14% - 13% = 1%You should invest in this fund because alpha is positive.b. The passive portfolio with the same beta as the fund should be invested 80% in themarket-index portfolio and 20% in the money market account. For this portfolio:E (r P ) = (0.8 × 15%) + (0.2 × 5%) = 13%14% − 13% = 1% = α24. a. We would incorporate liquidity into the CCAPM in a manner analogous to the wayin which liquidity is incorporated into the conventional CAPM. In the latter case, inaddition to the market risk premium, expected return is also dependent on theexpected cost of illiquidity and three liquidity-related betas which measure thesensitivity of: (1) the security’s illiquidity to market illiquidity; (2) the security’sreturn to market illiquidity; and, (3) the security’s illiquidity to the market return. Asimilar approach can be used for the CCAPM, except that the liquidity betas wouldbe measured relative to consumption growth rather than the usual market index.b. As in part (a), nontraded assets would be incorporated into the CCAPM in afashion similar to part (a). Replace the market portfolio with consumption growth.The issue of liquidity is more acute with nontraded assets such as privately heldbusinesses and labor income.While ownership of a privately held business is analogous to ownership of an illiquidstock, expect a greater degree of illiquidity for the typical private business. If theowner of a privately held business is satisfied with the dividends paid out from thebusiness, then the lack of liquidity is not an issue. If the owner seeks to realizeincome greater than the business can pay out, then selling ownership, in full or part,typically entails a substantial liquidity discount. The illiquidity correction should betreated as suggested in part (a).The same general considerations apply to labor income, although it is probable thatthe lack of liquidity for labor income has an even greater impact on security marketequilibrium values. Labor income has a major impact on portfolio decisions. While itis possible to borrow against labor income to some degree, and some of the riskassociated with labor income can be ameliorated with insurance, it is plausible thatthe liquidity betas of consumption streams are quite significant, as the need toborrow against labor income is likely cyclical.CFA PROBLEMS1. a. Agree; Regan’s conclusion is correct. By definition, the market portfolio lies on thecapital market line (CML). Under the assumptions of capital market theory, allportfolios on the CML dominate, in a risk-return sense, portfolios that lie on theMarkowitz efficient frontier because, given that leverage is allowed, the CML creates aportfolio possibility line that is higher than all points on the efficient frontier except for themarket portfolio, which is Rainbow’s portfolio. Because Eagle’s portfolio lies on theMarkowitz efficient frontier at a point other than the market portfolio, Rainbow’sportfolio dominates Eagle’s portfolio.b. Nonsystematic risk is the unique risk of individual stocks in a portfolio that is diversifiedaway by holding a well-diversified portfolio. Total risk is composed of systematic(market) risk and nonsystematic (firm-specific) risk.Disagree; Wilson’s remark is incorrect. Because both portfolios lie on the Markowitzefficient frontier, neither Eagle nor Rainbow has any nonsystematic risk. Therefore,nonsystematic risk does not explain the different expected returns. The determiningfactor is that Rainbow lies on the (straight) line (the CML) connecting the risk-free assetand the market portfolio (Rainbow), at the point of tangency to the Markowitz efficientfrontier having the highest return per unit of risk. Wilson’s remark is also countered bythe fact that, since nonsystematic risk can be eliminated by diversification, the expectedreturn for bearing nonsystematic risk is zero. This is a result of the fact that well-diversified investors bid up the price of every asset to the point where only systematicrisk earns a positive return (nonsystematic risk earns no return).2. E(r) = r f + β × [E(r M) − r f]Furhman Labs: E(r) = .05 + 1.5 × [.115 − .05] = 14.75%Garten Testing: E(r) = .05 + 0.8 × [.115 − .05] = 10.20%If the forecast rate of return is less than (greater than) the required rate of return, then thesecurity is overvalued (undervalued).Furhman Labs: Forecast return –Required return = 13.25% − 14.75% = −1.50%Garten Testing: Forecast return –Required return = 11.25% − 10.20% = 1.05%Therefore, Furhman Labs is overvalued and Garten Testing is undervalued.3. a.4. d. From CAPM, the fair expected return = 8 + 1.25 × (15 - 8) = 16.75%Actually expected return = 17%α = 17 - 16.75 = 0.25%5. d.6. c.7. d.8. d. [You need to know the risk-free rate]9. d. [You need to know the risk-free rate]10.Under the CAPM, the only risk that investors are compensated for bearing is the risk thatcannot be diversified away (systematic risk). Because systematic risk (measured by beta) is equal to 1.0 for both portfolios, an investor would expect the same rate of return from both portfolios A and B. Moreover, since both portfolios are well diversified, it doesn’t matter if the specific risk of the individual securities is high or low. The firm-specific risk has been diversified away for both portfolios.11. a. McKay should borrow funds and invest those funds proportionately in Murray’sexisting portfolio (i.e., buy more risky assets on margin). In addition to increasedexpected return, the alternative portfolio on the capital market line will also haveincreased risk, which is caused by the higher proportion of risky assets in the totalportfolio.b. McKay should substitute low-beta stocks for high-beta stocks in order to reducethe overall beta of Y ork’s portfolio. By reducing the overall portfolio beta, McKaywill reduce the systematic risk of the portfolio and, therefore, reduce its volatilityrelative to the market. The security market line (SML) suggests such action (i.e.,moving down the SML), even though reducing beta may result in a slight loss ofportfolio efficiency unless full diversification is maintained. York’s primary objective,however, is not to maintain efficiency but to reduce risk exposure; reducing portfoliobeta meets that objective. Because York does not want to engage in borrowing orlending, McKay cannot reduce risk by selling equities and using the proceeds to buyrisk-free assets (i.e., lending part of the portfolio).12. a.Expected Return AlphaStock X 5% + 0.8 × (14% - 5%) = 12.2% 14.0% - 12.2% = 1.8%Stock Y 5% + 1.5 × (14% - 5%) = 18.5% 17.0% - 18.5% = -1.5%b.i. Kay should recommend Stock X because of its positive alpha, compared toStock Y, which has a negative alpha. In graphical terms, the expected return/riskprofile for Stock X plots above the security market line (SML), while the profile forStock Y plots below the SML. Also, depending on the individual risk preferencesof Kay’s clients, the lower beta for Stock X may have a beneficial effect on overallportfolio risk.ii. Kay should recommend Stock Y because it has higher forecasted return andlower standard deviation than Stock X. The respective Sharpe ratios for Stocks Xand Y and the market index are:Stock X: (14% - 5%)/36% = 0.25Stock Y: (17% - 5%)/25% = 0.48Market index: (14% - 5%)/15% = 0.60The market index has an even more attractive Sharpe ratio than either of the individual stocks, but, given the choice between Stock X and Stock Y, Stock Y is the superior alternative.When a stock is held as a single stock portfolio, standard deviation is the relevant risk measure. For such a portfolio, beta as a risk measure is irrelevant. Although holding a single asset is not a typically recommended investment strategy, some investors may hold what is essentially a single-asset portfolio when they hold the stock of their employer company. For such investors, the relevance of standard deviation versus beta is an important issue.。

证券投资学课后习题答案总结

证券投资学课后习题答案总结第一章股票1、什么是股份制度?它的主要功能有哪些?答:股份制度亦称股份公司制度,它是指以集资入股、共享收益、共担风险为特点的企业组织制度。

股份公司一般以发行股票的方式筹集股本,股票投资者依据他们所提供的生产要素份额参与公司收益分配。

在股份公司中,各个股东享有的权利和义务与他们所提供的生产要素份额相对应。

功能:一、筹集社会资金;二、改善和强化企业的经营管理。

2、什么是股票?它的主要特性是什么?答:股票是股份有限公司发行的,表示其股东按其持有的股份享受权益和承担义务的可转让的书面凭证。

股票作为股份公司的股份证明,表示其持有者在公司的地位与权利,股票持有者为公司股东.特性:1、不可返还性2、决策性3、风险性4、流动性5、价格波动性6、投机性3、普通股和优先股的区别?答:普通股是构成股份有限公司资本基础股份,是股份公司最先发行、必须发行的股票,是公司最常见、最重要的股票,也是最常见的股票。

其权利为:1、投票表决权2、收益分配权3、资产分配权4、优先认股权。

对公司优先股在股份公司中对公司利润、公司清理剩余资产享有的优先分配权的股份。

第一是领取股息优先。

第二是分配剩余财产优先。

优先股不利一面:股息率事先确定;无选举权和被选举权,无对公司决策表决权;在发放新股时,无优先认股权。

有利一面:投资者角度:收益固定,风险小于普通股,股息高于债券收益;筹资公司发行角度:股息固定不影响公司利润分配,发行优先股可以广泛的吸收资金,不影响普通股东经营管理权。

4、我国现行的股票类型有哪些?答:我国现行的股票按投资主体不同有国有股、法人股、公众股和外资股。

国有股是有权代表国家投资的部门或机构以国有资产向公司投资形成的股份,包括公司现有的国有资产折算的股份。

法人股是指企业法人或具有法人资格的事业单位和社会团体以其依法可支配的资产向股份有限公司非上市流通股权部分投资所形成的股份。

公众股即个人股,指社会个人或股份公司内部职工以个人合法财产投入公司形成的股份。

(完整word版)投资学第7版Test Bank答案09

Multiple Choice Questions1. In the context of the Capital Asset Pricing Model (CAPM) the relevant measure of riskisA) unique risk.B) beta.C) standard deviation of returns.D) variance of returns.E) none of the above.Answer: B Difficulty: EasyRationale: Once, a portfolio is diversified, the only risk remaining is systematic risk,which is measured by beta.2. According to the Capital Asset Pricing Model (CAPM) a well diversified portfolio's rateof return is a function ofA) market riskB) unsystematic riskC) unique risk.D) reinvestment risk.E) none of the above.Answer: A Difficulty: EasyRationale: With a diversified portfolio, the only risk remaining is market, or systematic, risk. This is the only risk that influences return according to the CAPM.3. The market portfolio has a beta ofA) 0.B) 1.C) -1.D) 0.5.E) none of the aboveAnswer: B Difficulty: EasyRationale: By definition, the beta of the market portfolio is 1.4. The risk-free rate and the expected market rate of return are 0.06 and 0.12, respectively.According to the capital asset pricing model (CAPM), the expected rate of return on security X with a beta of 1.2 is equal toA) 0.06.B) 0.144.C) 0.12.D) 0.132E) 0.18Answer: D Difficulty: EasyRationale: E(R) = 6% + 1.2(12 - 6) = 13.2%.5. The risk-free rate and the expected market rate of return are 0.056 and 0.125,respectively. According to the capital asset pricing model (CAPM), the expected rate of return on a security with a beta of 1.25 is equal toA) 0.1225B) 0.144.C) 0.153.D) 0.134E) 0.117Answer: A Difficulty: EasyRationale: E(R) = 5.6% + 1.25(12.5 - 5.6) = 14.225%.6. Which statement is not true regarding the market portfolio?A) It includes all publicly traded financial assets.B) It lies on the efficient frontier.C) All securities in the market portfolio are held in proportion to their market values.D) It is the tangency point between the capital market line and the indifference curve.E) All of the above are true.Answer: D Difficulty: ModerateRationale: The tangency point between the capital market line and the indifference curve is the optimal portfolio for a particular investor.7. Which statement is not true regarding the Capital Market Line (CML)?A) The CML is the line from the risk-free rate through the market portfolio.B) The CML is the best attainable capital allocation line.C) The CML is also called the security market line.D) The CML always has a positive slope.E) The risk measure for the CML is standard deviation.Answer: C Difficulty: ModerateRationale: Both the Capital Market Line and the Security Market Line depict risk/return relationships. However, the risk measure for the CML is standard deviation and the risk measure for the SML is beta (thus C is not true; the other statements are true).8. The market risk, beta, of a security is equal toA) the covariance between the security's return and the market return divided by thevariance of the market's returns.B) the covariance between the security and market returns divided by the standarddeviation of the market's returns.C) the variance of the security's returns divided by the covariance between the securityand market returns.D) the variance of the security's returns divided by the variance of the market's returns.E) none of the above.Answer: A Difficulty: ModerateRationale: Beta is a measure of how a security's return covaries with the market returns, normalized by the market variance.9. According to the Capital Asset Pricing Model (CAPM), the expected rate of return onany security is equal toA) R f+ β [E(R M)].B) R f + β [E(R M) - R f].C) β [E(R M) - R f].D) E(R M) + R f.E) none of the above.Answer: B Difficulty: ModerateRationale: The expected rate of return on any security is equal to the risk free rate plus the systematic risk of the security (beta) times the market risk premium, E(R M - R f).10. The Security Market Line (SML) isA) the line that describes the expected return-beta relationship for well-diversifiedportfolios only.B) also called the Capital Allocation Line.C) the line that is tangent to the efficient frontier of all risky assets.D) the line that represents the expected return-beta relationship.E) the line that represents the relationship between an individual security's return andthe market's return.Answer: D Difficulty: ModerateRationale: The SML is a measure of expected return per unit of risk, where risk isdefined as beta (systematic risk).11. According to the Capital Asset Pricing Model (CAPM), fairly priced securitiesA) have positive betas.B) have zero alphas.C) have negative betas.D) have positive alphas.E) none of the above.Answer: B Difficulty: ModerateRationale: A zero alpha results when the security is in equilibrium (fairly priced for the level of risk).12. According to the Capital Asset Pricing Model (CAPM), under priced securitiesA) have positive betas.B) have zero alphas.C) have negative betas.D) have positive alphas.E) none of the above.Answer: D Difficulty: Moderate13. According to the Capital Asset Pricing Model (CAPM), over priced securitiesA) have positive betas.B) have zero alphas.C) have negative betas.D) have positive alphas.E) none of the above.Answer: C Difficulty: ModerateRationale: A zero alpha results when the security is in equilibrium (fairly priced for the level of risk).14. According to the Capital Asset Pricing Model (CAPM),A) a security with a positive alpha is considered overpriced.B) a security with a zero alpha is considered to be a good buy.C) a security with a negative alpha is considered to be a good buy.D) a security with a positive alpha is considered to be underpriced.E) none of the above.Answer: D Difficulty: ModerateRationale: A security with a positive alpha is one that is expected to yield an abnormal positive rate of return, based on the perceived risk of the security, and thus isunderpriced.15. According to the Capital Asset Pricing Model (CAPM), which one of the followingstatements is false?A) The expected rate of return on a security decreases in direct proportion to a decreasein the risk-free rate.B) The expected rate of return on a security increases as its beta increases.C) A fairly priced security has an alpha of zero.D) In equilibrium, all securities lie on the security market line.E) All of the above statements are true.Answer: A Difficulty: ModerateRationale: Statements B, C, and D are true, but statement A is false.16. In a well diversified portfolioA) market risk is negligible.B) systematic risk is negligible.C) unsystematic risk is negligible.D) nondiversifiable risk is negligible.E) none of the above.Answer: C Difficulty: ModerateRationale: Market, or systematic, or nondiversifiable, risk is present in a diversified portfolio; the unsystematic risk has been eliminated.17. Empirical results regarding betas estimated from historical data indicate thatA) betas are constant over time.B) betas of all securities are always greater than one.C) betas are always near zero.D) betas appear to regress toward one over time.E) betas are always positive.Answer: D Difficulty: ModerateRationale: Betas vary over time, betas may be negative or less than one, betas are not always near zero; however, betas do appear to regress toward one over time.18. Your personal opinion is that a security has an expected rate of return of 0.11. It has abeta of 1.5. The risk-free rate is 0.05 and the market expected rate of return is 0.09.According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: C Difficulty: ModerateRationale: 11% = 5% + 1.5(9% - 5%) = 11.0%; therefore, the security is fairly priced.19. The risk-free rate is 7 percent. The expected market rate of return is 15 percent. If youexpect a stock with a beta of 1.3 to offer a rate of return of 12 percent, you shouldA) buy the stock because it is overpriced.B) sell short the stock because it is overpriced.C) sell the stock short because it is underpriced.D) buy the stock because it is underpriced.E) none of the above, as the stock is fairly priced.Answer: B Difficulty: ModerateRationale: 12% < 7% + 1.3(15% - 7%) = 17.40%; therefore, stock is overpriced and should be shorted.20. You invest $600 in a security with a beta of 1.2 and $400 in another security with a betaof 0.90. The beta of the resulting portfolio isA) 1.40B) 1.00C) 0.36D) 1.08E) 0.80Answer: D Difficulty: ModerateRationale: 0.6(1.2) + 0.4(0.90) = 1.08.21. A security has an expected rate of return of 0.10 and a beta of 1.1. The market expectedrate of return is 0.08 and the risk-free rate is 0.05. The alpha of the stock isA) 1.7%.B) -1.7%.C) 8.3%.D) 5.5%.E) none of the above.Answer: A Difficulty: ModerateRationale: 10% - [5% +1.1(8% - 5%)] = 1.7%.22. Your opinion is that CSCO has an expected rate of return of 0.13. It has a beta of 1.3.The risk-free rate is 0.04 and the market expected rate of return is 0.115. According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: B Difficulty: ModerateRationale: 11.5% - 4% + 1.3(11.5% - 4%) = -2.25%; therefore, the security isoverpriced.23. Your opinion is that CSCO has an expected rate of return of 0.1375. It has a beta of 1.3.The risk-free rate is 0.04 and the market expected rate of return is 0.115. According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: C Difficulty: ModerateRationale: 13.75% - 4% + 1.3(11.5% - 4%) = 0.0%; therefore, the security is fairlypriced.24. Your opinion is that CSCO has an expected rate of return of 0.15. It has a beta of 1.3.The risk-free rate is 0.04 and the market expected rate of return is 0.115. According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: A Difficulty: ModerateRationale: 15% - 4% + 1.3(11.5% - 4%) = 1.25%; therefore, the security is under priced.25. Your opinion is that Boeing has an expected rate of return of 0.112. It has a beta of 0.92.The risk-free rate is 0.04 and the market expected rate of return is 0.10. According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: A Difficulty: ModerateRationale: 11.2% - 4% + 0.92(10% - 4%) = 1.68%; therefore, the security is underpriced.26. Your opinion is that Boeing has an expected rate of return of 0.0952. It has a beta of0.92. The risk-free rate is 0.04 and the market expected rate of return is 0.10.According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: C Difficulty: ModerateRationale: 9.52% - 4% + 0.92(10% - 4%) = 0.0%; therefore, the security is fairly priced.27. Your opinion is that Boeing has an expected rate of return of 0.08. It has a beta of 0.92.The risk-free rate is 0.04 and the market expected rate of return is 0.10. According to the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: C Difficulty: ModerateRationale: 8.0% - 4% + 0.92(10% - 4%) = -1.52%; therefore, the security is overpriced.28. The risk-free rate is 4 percent. The expected market rate of return is 11 percent. If youexpect CAT with a beta of 1.0 to offer a rate of return of 10 percent, you shouldA) buy stock X because it is overpriced.B) sell short stock X because it is overpriced.C) sell stock short X because it is underpriced.D) buy stock X because it is underpriced.E) none of the above, as the stock is fairly priced.Answer: B Difficulty: ModerateRationale: 10% < 4% + 1.0(11% - 4%) = 11.0%; therefore, stock is overpriced andshould be shorted.29. The risk-free rate is 4 percent. The expected market rate of return is 11 percent. If youexpect CAT with a beta of 1.0 to offer a rate of return of 11 percent, you shouldA) buy stock X because it is overpriced.B) sell short stock X because it is overpriced.C) sell stock short X because it is underpriced.D) buy stock X because it is underpriced.E) none of the above, as the stock is fairly priced.Answer: E Difficulty: ModerateRationale: 11% = 4% + 1.0(11% - 4%) = 11.0%; therefore, stock is fairly priced. 30. The risk-free rate is 4 percent. The expected market rate of return is 11 percent. If youexpect CAT with a beta of 1.0 to offer a rate of return of 13 percent, you shouldA) buy stock X because it is overpriced.B) sell short stock X because it is overpriced.C) sell stock short X because it is underpriced.D) buy stock X because it is underpriced.E) none of the above, as the stock is fairly priced.Answer: D Difficulty: ModerateRationale: 13% > 4% + 1.0(11% - 4%) = 11.0%; therefore, stock is under priced. 31. You invest 55% of your money in security A with a beta of 1.4 and the rest of yourmoney in security B with a beta of 0.9. The beta of the resulting portfolio isA) 1.466B) 1.157C) 0.968D) 1.082E) 1.175Answer: E Difficulty: ModerateRationale: 0.55(1.4) + 0.45(0.90) = 1.175.32. Given the following two stocks A and BIf the expected market rate of return is 0.09 and the risk-free rate is 0.05, which security would be considered the better buy and why?A) A because it offers an expected excess return of 1.2%.B) B because it offers an expected excess return of 1.8%.C) A because it offers an expected excess return of 2.2%.D) B because it offers an expected return of 14%.E) B because it has a higher beta.Answer: C Difficulty: ModerateRationale: A's excess return is expected to be 12% - [5% + 1.2(9% - 5%)] = 2.2%. B's excess return is expected to be 14% - [5% + 1.8(9% - 5%)] = 1.8%.33. Capital Asset Pricing Theory asserts that portfolio returns are best explained by:A) economic factors.B) specific risk.C) systematic risk.D) diversification.E) none of the above.Answer: C Difficulty: EasyRationale: The risk remaining in diversified portfolios is systematic risk; thus, portfolio returns are commensurate with systematic risk.34. According to the CAPM, the risk premium an investor expects to receive on any stockor portfolio increases:A) directly with alpha.B) inversely with alpha.C) directly with beta.D) inversely with beta.E) in proportion to its standard deviation.Answer: C Difficulty: EasyRationale: The market rewards systematic risk, which is measured by beta, and thus, the risk premium on a stock or portfolio varies directly with beta.35. What is the expected return of a zero-beta security?A) The market rate of return.B) Zero rate of return.C) A negative rate of return.D) The risk-free rate.E) None of the above.Answer: D Difficulty: ModerateRationale: E(R S) = r f + 0(R M - r f) = r f.36. Standard deviation and beta both measure risk, but they are different in thatA) beta measures both systematic and unsystematic risk.B) beta measures only systematic risk while standard deviation is a measure of totalrisk.C) beta measures only unsystematic risk while standard deviation is a measure of totalrisk.D) beta measures both systematic and unsystematic risk while standard deviationmeasures only systematic risk.E) beta measures total risk while standard deviation measures only nonsystematic risk.Answer: B Difficulty: EasyRationale: B is the only true statement.37. The expected return-beta relationshipA) is the most familiar expression of the CAPM to practitioners.B) refers to the way in which the covariance between the returns on a stock and returnson the market measures the contribution of the stock to the variance of the marketportfolio, which is beta.C) assumes that investors hold well-diversified portfolios.D) all of the above are true.E) none of the above is true.Answer: D Difficulty: ModerateRationale: Statements A, B and C all describe the expected return-beta relationship.38. The security market line (SML)A) can be portrayed graphically as the expected return-beta relationship.B) can be portrayed graphically as the expected return-standard deviation of marketreturns relationship.C) provides a benchmark for evaluation of investment performance.D) A and C.E) B and C.Answer: D Difficulty: ModerateRationale: The SML is a measure of expected return-beta (the CML is a measure of expected return-standard deviation of market returns). The SML provides the expected return-beta relationship for "fairly priced" securities; thus if a portfolio manager selects securities that are underpriced and produces a portfolio with a positive alpha, thisportfolio manager would receive a positive evaluation.39. Research by Jeremy Stein of MIT resolves the dispute over whether beta is a sufficientpricing factor by suggesting that managers should use beta to estimateA) long-term returns but not short-term returns.B) short-term returns but not long-term returns.C) both long- and short-term returns.D) book-to-market ratios.E) None of the above was suggested by Stein.Answer: A Difficulty: Difficult40. Studies of liquidity spreads in security markets have shown thatA) liquid stocks earn higher returns than illiquid stocks.B) illiquid stocks earn higher returns than liquid stocks.C) both liquid and illiquid stocks earn the same returns.D) illiquid stocks are good investments for frequent, short-term traders.E) None of the above is true.Answer: B Difficulty: Difficult41. An underpriced security will plotA) on the Security Market Line.B) below the Security Market Line.C) above the Security Market Line.D) either above or below the Security Market Line depending on its covariance withthe market.E) either above or below the Security Market Line depending on its standard deviation.Answer: C Difficulty: EasyRationale: An underpriced security will have a higher expected return than the SML would predict; therefore it will plot above the SML.42. The risk premium on the market portfolio will be proportional toA) the average degree of risk aversion of the investor population.B) the risk of the market portfolio as measured by its variance.C) the risk of the market portfolio as measured by its beta.D) both A and B are true.E) both A and C are true.Answer: D Difficulty: ModerateRationale: The risk premium on the market portfolio is proportional to the averagedegree of risk aversion of the investor population and the risk of the market portfolio measured by its variance.43. In equilibrium, the marginal price of risk for a risky security must beA) equal to the marginal price of risk for the market portfolio.B) greater than the marginal price of risk for the market portfolio.C) less than the marginal price of risk for the market portfolio.D) adjusted by its degree of nonsystematic risk.E) none of the above is true.Answer: A Difficulty: ModerateRationale: In equilibrium, the marginal price of risk for a risky security must be equal to the marginal price of risk for the market. If not, investors will buy or sell the security until they are equal.44. The capital asset pricing model assumesA) all investors are price takers.B) all investors have the same holding period.C) investors pay taxes on capital gains.D) both A and B are true.E) A, B and C are all true.Answer: D Difficulty: EasyRationale: The CAPM assumes that investors are price-takers with the same single holding period and that there are no taxes or transaction costs.45. If investors do not know their investment horizons for certainA) the CAPM is no longer valid.B) the CAPM underlying assumptions are not violated.C) the implications of the CAPM are not violated as long as investors' liquidity needsare not priced.D) the implications of the CAPM are no longer useful.E) none of the above is true.Answer: C Difficulty: ModerateRationale: This is discussed in the chapter's section about extensions to the CAPM. It examines what the consequences are when the assumptions are removed.46. The value of the market portfolio equalsA) the sum of the values of all equity securities.B) the sum of the values of all equity and fixed income securities.C) the sum the values of all equity, fixed income, and derivative securities.D) the sum of the values of all equity, fixed income, and derivative securities plus thevalue of all mutual funds.E) the entire wealth of the economy.Answer: E Difficulty: ModerateRationale: The market portfolio includes all assets in existence.47. The amount that an investor allocates to the market portfolio is negatively related toI)the expected return on the market portfolio.II)the investor's risk aversion coefficient.III)the risk-free rate of return.IV)the variance of the market portfolioA) I and IIB) II and IIIC) II and IVD) II, III, and IVE) I, III, and IVAnswer: D Difficulty: ModerateRationale: The optimal proportion is given by y = (E(R M)-r f)/(.01xAσ2M). This amount will decrease as r f, A, and σ2M decrease.48. One of the assumptions of the CAPM is that investors exhibit myopic behavior. Whatdoes this mean?A) They plan for one identical holding period.B) They are price-takers who can't affect market prices through their trades.C) They are mean-variance optimizers.D) They have the same economic view of the world.E) They pay no taxes or transactions costs.Answer: A Difficulty: ModerateRationale: Myopic behavior is shortsighted, with no concern for medium-term orlong-term implications.49. The CAPM applies toA) portfolios of securities only.B) individual securities only.C) efficient portfolios of securities only.D) efficient portfolios and efficient individual securities only.E) all portfolios and individual securities.Answer: E Difficulty: ModerateRationale: The CAPM is an equilibrium model for all assets. Each asset's risk premium is a function of its beta coefficient and the risk premium on the market portfolio.50. Which of the following statements about the mutual fund theorem is true?I)It is similar to the separation property.II)It implies that a passive investment strategy can be efficient.III)It implies that efficient portfolios can be formed only through active strategies.IV)It means that professional managers have superior security selection strategies.A) I and IVB) I, II, and IVC) I and IID) III and IVE) II and IVAnswer: C Difficulty: ModerateRationale: The mutual fund theorem is similar to the separation property. The technical task of creating mutual funds can be delegated to professional managers; thenindividuals combine the mutual funds with risk-free assets according to theirpreferences. The passive strategy of investing in a market index fund is efficient.51. The expected return -- beta relationship of the CAPM is graphically represented byA) the security market line.B) the capital market line.C) the capital allocation line.D) the efficient frontier with a risk-free asset.E) the efficient frontier without a risk-free asset.Answer: A Difficulty: EasyRationale: The security market line shows expected return on the vertical axis and beta on the horizontal axis. It has an intercept of r f and a slope of E(R M) - r f.52. A “fairly priced” asset liesA) above the security market line.B) on the security market line.C) on the capital market line.D) above the capital market line.E) below the security market line.Answer: B Difficulty: EasyRationale: Securities that lie on the SML earn exactly the expected return generated by the CAPM. Their prices are proportional to their beta coefficients and they have alphas equal to zero.53. For the CAPM that examines illiquidity premiums, if there is correlation among assetsdue to common systematic risk factors, the illiquidity premium on asset i is a function ofA) the market's volatility.B) asset i's volatility.C) the trading costs of security i.D) the risk-free rate.E) the money supply.Answer: C Difficulty: ModerateRationale: The formula for this extension to the CAPM relaxes the assumption thattrading is costless.54. Your opinion is that security A has an expected rate of return of 0.145. It has a beta of1.5. The risk-free rate is 0.04 and the market expected rate of return is 0.11. Accordingto the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: C Difficulty: ModerateRationale: 14.5% = 4% + 1.5(11% - 4%) = 14.5%; therefore, the security is fairlypriced.55. Your opinion is that security C has an expected rate of return of 0.106. It has a beta of1.1. The risk-free rate is 0.04 and the market expected rate of return is 0.10. Accordingto the Capital Asset Pricing Model, this security isA) underpriced.B) overpriced.C) fairly priced.D) cannot be determined from data provided.E) none of the above.Answer: A Difficulty: ModerateRationale: 4% + 1.1(10% - 4%) = 10.6%; therefore, the security is fairly priced.56. The risk-free rate is 4 percent. The expected market rate of return is 12 percent. If youexpect stock X with a beta of 1.0 to offer a rate of return of 10 percent, you shouldA) buy stock X because it is overpriced.B) sell short stock X because it is overpriced.C) sell stock short X because it is underpriced.D) buy stock X because it is underpriced.E) none of the above, as the stock is fairly priced.Answer: B Difficulty: ModerateRationale: 10% < 4% + 1.0(12% - 4%) = 12.0%; therefore, stock is overpriced and should be shorted.57. The risk-free rate is 5 percent. The expected market rate of return is 11 percent. If youexpect stock X with a beta of 2.1 to offer a rate of return of 15 percent, you shouldA) buy stock X because it is overpriced.B) sell short stock X because it is overpriced.C) sell stock short X because it is underpriced.D) buy stock X because it is underpriced.E) none of the above, as the stock is fairly priced.Answer: B Difficulty: ModerateRationale: 15% < 5% + 2.1(11% - 5%) = 17.6%; therefore, stock is overpriced and should be shorted.58. You invest 50% of your money in security A with a beta of 1.6 and the rest of yourmoney in security B with a beta of 0.7. The beta of the resulting portfolio isA) 1.40B) 1.15C) 0.36D) 1.08E) 0.80Answer: B Difficulty: ModerateRationale: 0.5(1.6) + 0.5(0.70) = 1.15.。

(NEW)博迪《投资学》(第10版)笔记和课后习题详解

目 录第一部分 绪论第1章 投资环境1.1 复习笔记1.2 课后习题详解第2章 资产类别与金融工具2.1 复习笔记2.2 课后习题详解第3章 证券是如何交易的3.1 复习笔记3.2 课后习题详解第4章 共同基金与其他投资公司4.1 复习笔记4.2 课后习题详解第二部分 资产组合理论与实践第5章 风险与收益入门及历史回顾5.1 复习笔记5.2 课后习题详解第6章 风险资产配置6.1 复习笔记6.2 课后习题详解第7章 最优风险资产组合7.1 复习笔记7.2 课后习题详解第8章 指数模型8.1 复习笔记8.2 课后习题详解第三部分 资本市场均衡第9章 资本资产定价模型9.1 复习笔记9.2 课后习题详解第10章 套利定价理论与风险收益多因素模型10.1 复习笔记10.2 课后习题详解第11章 有效市场假说11.1 复习笔记11.2 课后习题详解第12章 行为金融与技术分析12.1 复习笔记12.2 课后习题详解第13章 证券收益的实证证据13.1 复习笔记13.2 课后习题详解第四部分 固定收益证券第14章 债券的价格与收益14.1 复习笔记14.2 课后习题详解第15章 利率的期限结构15.1 复习笔记15.2 课后习题详解第16章 债券资产组合管理16.1 复习笔记16.2 课后习题详解第五部分 证券分析第17章 宏观经济分析与行业分析17.1 复习笔记17.2 课后习题详解第18章 权益估值模型18.1 复习笔记18.2 课后习题详解第19章 财务报表分析19.1 复习笔记19.2 课后习题详解第六部分 期权、期货与其他衍生证券第20章 期权市场介绍20.1 复习笔记20.2 课后习题详解第21章 期权定价21.1 复习笔记21.2 课后习题详解第22章 期货市场22.1 复习笔记22.2 课后习题详解第23章 期货、互换与风险管理23.1 复习笔记23.2 课后习题详解第七部分 应用投资组合管理第24章 投资组合业绩评价24.1 复习笔记24.2 课后习题详解第25章 投资的国际分散化25.1 复习笔记25.2 课后习题详解第26章 对冲基金26.1 复习笔记26.2 课后习题详解第27章 积极型投资组合管理理论27.1 复习笔记27.2 课后习题详解第28章 投资政策与特许金融分析师协会结构28.1 复习笔记28.2 课后习题详解第一部分 绪论第1章 投资环境1.1 复习笔记1实物资产与金融资产(1)概念实物资产指经济活动中所创造的用于生产商品和提供服务的资产。

(完整版)证券投资学(第三版)练习及答案9

一、判断题1.证券投资过程基本上经过以下五个步骤:确定投资目标、选择投资策略、制定投资政策、构建和修正投资组合、评估投资业绩。

答案:非2.投资政策将决定资产分配决策,即如何将投资资金在投资对象之间进行分配。

答案:是3.积极的股票投资策略包括对未来收益、股利或市盈率的预测。

答案:是4.资产配置是指证券组合中各种不同资产所占的比率。

答案:是5、评估投资业绩的依据是投资组合的收益。

答案:非6.采用积极的股票管理策略的投资者花大量精力构造投资组合,而奉行消极管理策略的投资者只是简单的模仿某一股价指数以构造投资组合。

答案:是7.有效市场假说是描述资本市场资产定价的理论。

答案:非8.如果认为市场是无效的,就能够以历史数据和公开与非公开的信息为基础获取超额盈利。

答案:是9.技术分析以道氏理论为依据,以价格变动和量价关系为重点。

答案:非10.如果股票的市场价格低于它的理论价值,以基本分析为基础策略的建议是买入该股票。

答案:是11.被忽略的公司效应是指以证券分析师对不同股票的关注程度为基础的投资策略可能获得超常收益。

答案:是12.依据市净率可以将股票分为增长型和价值型两类。

答案:非14.债券的一个基本特性是它的价格与它所要求的收益率呈反方向变动。

答案:是15.债券价格的波动性与其持续期成正比。

答案:是16.债券的凸性的含义是:当债券收益率下降时,债券的价格以更小的曲率增长;当债券收益率提高时,债券的价格以更小的曲率降低。

答案:非17.债券投资的收益来自于;利息收入、资本利得和再投资收益。

答案:非18.债券的收益率曲线体现的是债券价格和其收益率之间的关系。

答案:非19.收益利差策略是基于相同类型中的不同债券之间收益率差额的预期变化而建立组合头寸的方法。

答案:非20.单一债券选择策略是指资金管理人通过寻找价格被高估或低估的债券以获利的策略。

答案:非21.在债券投资中使用杠杆的基本原则是借入资金的投资收益大于借入成本。

(完整版)投资学第10版习题答案09