专业英语会计分录

会计专业英语复习资料.doc

会计专业英语复习资料.doc会计专业英语复习资料⼀、短语中英互译1、会计分录2、投资活动3、后进先出法4、客观性原则5、注册会计师6、权责发⽣制7、累计折旧8、资产负债表9、经营决策10、银⾏存款11、到期⽇12、历史成本13、source document14、nominal rate15、credit sale16、sum-of-years-digits method17、economic entity assumption18、financial position19、fixed assets20、public hearing21、income statement22、sales discount23、value added tax24、trade mark25、bank overdraft⼆、从下列选项中选出最佳答案1、Generally,revenue is recorded by a business enterprise at a point when :( )A、Management decides it is appropriate to do soB、The product is available for sale to consumersC、An exchange has taken place and the earning process is virtually completeD、An order for merchandise has been received2、Why are certain costs capitalized when incurred and then depreciated or amortized over subsequent accounting periods?( )A、To reduce the income tax liabilityB、To aid management in making business decisionsC、To match the costs of production with revenue as earnedD、To adhere to the accounting concept of conservatism3、What accounting principle or concept justifies the use of accruals and deferrals?( )A、Going concernB、MaterialityC、ConsistencyD、Stable monetary unit4、An accrued expense can best be described as an amount ( )A、Paid and currently matched with revenueB、Paid and not currently matched with revenueC、Not paid and not currently matched with revenueD、Not paid and currently matched with revenue5、Continuation of a business enterprise in the absence of contrary evidence is an example of the principle or concept of ( )A、Business entityB、ConsistencyC、Going concernD、Substance over form6、In preparing a bank reconciliation,the amount of checks outstanding would be:( )A、added to the bank balance according to the bank statement.B、deducted from the bank balance according to the bank statement.C、added to the cash balance according to the depositor’s records.D、deducted from the cash balance according to the depositor’s records.7、Journal entries based on the bank reconciliation are required for:( )A、additions to the cash balance according to the depositor’s records.B、deductions from the cash balance according to the depositor’srecords.C、Both A and BD、Neither A nor B8、A petty cash fund is :( )A、used to pay relatively small amounts。

会计英语分录知识点总结

会计英语分录知识点总结一、会计英语分录的基本要素会计是一门全球通用的语言,它涉及许多专业术语和字词。

在会计学中,分录是记录交易和经济事件的基本手段。

下面,我们将从会计英语分录的基本要素出发,总结一些相关知识点。

1. 记入账户在会计英语中,记录交易的基本单位是账户。

账户是用于记录特定资产、负债、权益、收入和费用的记录单元。

例如,现金账户,应收账款账户等。

2. 借贷方会计英语中,交易记录为每个账户分为借贷两栏。

借方(Debit)表示账户的增加,贷方(Credit)表示账户的减少。

借贷方向是根据交易的性质和会计方程式(Assets = Liabilities + Equity)来决定的。

3. 交易金额每个会计分录都有对应的交易金额。

金额可能是正值,也可能是负值。

正值表示增加,负值表示减少。

交易金额必须对应借贷方向,以确保会计方程式的平衡。

二、会计分录的类型会计分录可以分为多种类型,如收入分录、费用分录、资产分录和负债分录。

以下是这些类型的简要介绍:1. 收入分录收入分录用于记录企业的销售收入或其他经济利益的增加。

例如,当企业出售产品或提供服务时,相关的收入分录会以增加负债的方式进行。

2. 费用分录费用分录用于记录企业的成本或其他经济利益的减少。

例如,当企业支付员工工资或采购原材料时,相关的费用分录会以增加负债的方式进行。

3. 资产分录资产分录用于记录企业的资产增加。

例如,当企业购买设备或现金流入时,相关的资产分录会以增加资产的方式进行。

4. 负债分录负债分录用于记录企业的负债增加。

例如,当企业借款或向供应商付款时,相关的负债分录会以增加负债的方式进行。

三、常见的会计英语分录术语除了基本要素和类型外,会计英语中还涉及许多特定的术语。

以下是一些常见的会计术语:1. 现金收入(Cash Receipts)指通过现金或支票等形式收到的款项或收入。

2. 现金支出(Cash Disbursements)指以现金或支票等形式支付的款项或费用。

专业英语会计分录

专业英语会计分录 Prepared on 24 November 2020专业英语分录练习1. The owner of Johnson company, Mr. Deep and his friends, invested 75 000 in cash, Land valuing 50 000 and Equipment A valuing 73 000 into the company.Dr. CashLandEquipment ACr. Capital2. Johnson Company receive a long-term bank loan of 60 000. The bank agreed to lend the money to it for 3 years with the annual interest rate of 12% and the interest shall be paid annually at the year ends while the principal should be paid back at the end of the third year. How did the company make the entry on Dec. 31Jan 1 Dr. cash 60 000Cr. Loan 60 000Dec 31 Dr. interest expense 600Interest payable 6600Cr. Cash 72003. Jan 1 Buy the business insurance for one year costing 24 000, the bill has not paid yet. Dr. prepaid insurance/unexpired insurance 24 000payable 24 0004. Johnson Company purchased 10 000 raw materials on credit and the supplier agree to collect cash one month later.Dr. raw materials 10 000Cr. Account payable 10 0005 Jan6 The company bought a company car at 11 000 for cash and cost 1 000 for transportation.Dr. Car 12000Cr. Cash 120006. The company paid to the manufacturing workers 10 000(all direct) and administrative staffs 4 500 (nonmanufacturing).Dr. manufacturing payroll 10000Salary expenses 4500Cr. Cash 145007. Company moved all the finished goods, with the cost of 45 500, into warehouse ready for sale.Dr. finished goods 45500Cr. Work in process 455008. Jan 11 Sale the product for 125 000. Half of the sales were for cash, half on credit. Also, it reported the cost of 40 000.Dr. cash 62500Account receivable 62500Cr. Sales revenue 125000Dr. cost of goods sold 40 000Cr. Finished goods 40 0009. Jan 31 Company used bad debt allowance method to record bad debt expense. It recognized 6% of the ending balance of Accounts receivable as the bad debt expense of that accounting period.Dr. bad debt expense 62500*6%=3750Cr. Bad debt allowance 62500*6%=3750 10. Jan 31 Record the accrual expense. (Suppose the car is supposed to be used for 5 years.)Dr. insurance expense 2000Cr. Prepaid insurance 2000Dr. Depreciation expense 200Cr. Accumulated Depreciation 200Dr. Interest expense 600Cr. Interest payable 60011. Jan 31 Close all the revenue account and expense account.Dr. sales revenue 125000Cr. Income summary 125000Dr. Income summary 51 050Cr. Salary expense 4500COGS 40000Bad debt expense 3750Insurance expense 2000Depreciation expense 200Interest expense 60012. Jan 31 Close the income summary account.Dr. income summary 73 950Cr. Retained earnings 73 950。

(财务会计)英文会计分录最全版

(财务会计)英文会计分录accompanyingdocument附件account账户、科目accountpayable应付账款accounttitle/accountingitem会计科目accountingdocument/accountingvoucument 会计凭证accountingelement会计要素accountingentity会计主体accountingentries会计分录accountingequation/accountingidentity 会计恒等式accountingfunction会计职能accountingpostulate会计假设accountingprinciple会计原则accountingreport/accountingstatement 会计报表accountingstandard会计准则accountingtimeperiodconcept会计分期accountsreceivable/receivables应收账款accrual-basisaccounting权责发生制原则accumulateddepreciation累计折旧amortizationexpense/expensenotallocated 待摊费用annualstatement年报ArthurAndersenWorldwide安达信全球assets资产balance余额balancesheet资产负债表begainningbalance/openingbalance 期初余额capital资本capitalexpenditure资本性支出capitalshare股本capitalsurplus资本公积cash现金cashinbank银行存款cashjournal现金日记账cashonhand现金cashsystem(basis)ofaccounting/cash-basisprinci 收付实现制certifiedpracticingaccountant注册会计师comparabilityprinciple可比性原则compoundjournalentry复合分录conservatism(保守)principle/theprudence(稳健)prin谨慎性原则consistencyprinciple 壹贯性原则contingentassets或有资产contingentliabilities 或有负债costaccounting成本会计creditbalance贷方余额creditside贷方currentinvestment 短期投资debitbalance借方余额debitside借方deferredassets递延资产deferredliabilities递延负债DeloitteToucheTohmatsu 德勤depreciablelife折旧年限depreciationexpense折旧费用depreciationrate折旧率descriptions摘要doubleentry复式记账double-entrybook-keeping 复式簿记employeebenefitspayable 应付福利费endingbalance期末余额Ernst&YoungInternational 安永国际estimateldscrapvalue估计残值exchangegain汇兑收益exchangeloss汇兑损失expenses/charges费用factoryoverhead/manufacturingexpense 制造费用financialaccounting财务会计financialexpense财务费用fiscalyear/accountingperiods会计年度fixedassets固定资产floatingassets/currentassets流动资产floatingliabilities/currentliability 流动负债generalledger总分类账going-concernbasis持续运营goodwill商誉historicalcost历史成本historicalcostprinciple历史成本原则:incomestatement/profitandlossstatement 利润表损益表incometax所得税intangibleassets无形资产internationalaccounting国际会计KPMGInternational毕马威国际liabilities负债liabilitydividend/dividendpayable应付股利long-terminvestmentlong-termliabilities长期负债managementaccounting 管理会计managementexpense 管理费用matchingprinciple配比原则materialityprinciple重要性原则monthlystatement月报negativegoodwill负商誉净资产netcost净成本netincome净收益netincomeapportionment 利润分配netproceeds净收入netprofit净利润non-operatinggain营业外收入non-operatinglossnotespayable应付票据notesreceivable/receivables 应收票据objectivity(reliability)principle 客观性原则obligee/creditor债权人Obligor/invester债务人operatingexpense营业费用operatingrevenue营业收入owner'sequity所有者权益periodexpense期间费用perpetualinventorysystem永续盘存制personalproperty动产physicalinventorysystem实地盘存制postingdocument记账凭证prepayments/paymentinadvance 预付款项PriceWaterHouseCoopers普华永道productcost/outputcost生产成本product/finishedgoods产成品profit利润profitaftertax税后利润profitbeforetax税前利润purchase购货purchasereturnandallowances 购货退回和折让quarterlystatement季报rawmaterials原材料realestate不动产relevanceprinciple相关性原则reserveforbaddebts/baddebtsexpense/provisi 坏帐准备residual(salvage)value折余价值(残值)retainsearning留存收益revenueexpenditure收益性支出revenues收入salesallowances 销货折让salesdiscount 销货折扣salesinvoice销货发票salesonaccount 赊销salesreturn销售退回salesrevenue 销售收入sellingcost销售成本sellingexpense销售费用simpleournalentry简单分录sourcedocument原始凭证stable-monetaryconcept货币计量starting-loadcost/organizationcosts开办费statementofcashflow/cashflowstatement 现金流量表stockonhand/inventory存货stub存根subsidiaryaccounts 明细账户subsidiaryledger 明细分类账surplusreserve盈余公积T-account/transfer T字形账户tangibleassets有形资产taxespayable应交税金theunderstandabilityprinciple明晰性原则timeliness及时性原则transaction交易travelingexpense差旅费trialbalance试算平衡undistributedprofits/undividedprofits 未分配利润unearnedrevenue预收款项unrelatedbusinessincome营业外收益usefullife使用年限valueaddedtax增值税voucher付款凭证wagespayable/salariespayable 应付工资workinprocess/goodsinprocess在产品。

会计英语知识点

会计英语知识点1. 会计英语基础知识会计英语是会计专业学生必备的一门语言技能。

了解会计英语的基础知识对于理解财务报表和参与国际商务交流至关重要。

本文将介绍几个重要的会计英语知识点。

2. 财务报表的英文表达财务报表是会计的核心内容之一。

常见的财务报表有资产负债表(Balance Sheet)、利润表(Income Statement)和现金流量表(Cash Flow Statement)。

在财务报表中,资产(Assets)、负债(Liabilities)和所有者权益(Owner's Equity)是三个关键概念。

3. 会计核算方法的英文表达会计核算方法是记录和处理会计业务的规定和方法。

常见的会计核算方法有现金基础会计法(Cash Basis Accounting)和权责发生制会计法(Accrual Basis Accounting)。

4. 会计凭证的英文表达会计凭证是会计记录的依据,用于记录和核实会计业务。

常见的会计凭证有收据(Receipt)、发票(Invoice)、收入凭证(Revenue Voucher)和支出凭证(Expense Voucher)。

5. 会计分录的英文表达会计分录是会计凭证上记录会计业务的方法和格式。

常见的会计分录有借方(Debit)和贷方(Credit),用于记录会计账户的增减情况。

6. 会计报告的英文表达会计报告是对财务状况和经营成果进行汇报的文件。

常见的会计报告有年度报告(Annual Report)和财务分析报告(Financial Analysis Report)。

其中,年度报告包括财务报表和管理层讨论与分析(Management Discussion and Analysis)。

7. 会计伦理的英文表达会计伦理是指会计人员在从事职业活动时应遵循的道德规范。

常见的会计伦理原则有诚实(Honesty)、保密(Confidentiality)和独立性(Independence)。

会计分录英文版

资产类 Assets流动资产 Current assets货币资金 Cash and cash equivalents库存现金 Cash on hand银行存款 Cash in bank其他货币资金 Other cash and cash equivalents外埠存款 Other city Cash in bank银行本票 Cashier's cheque银行汇票 Bank draft信用卡 Credit card信用证保证金 L/C Guarantee deposits存出投资款 Refundable deposits交易性金融资产 Financial assets held for trading短期投资 Short-term investments股票 Short-term investments - stock债券 Short-term investments - corporate bonds基金 Short-term investments - corporate funds其他 Short-term investments - other短期投资跌价准备 Short-term investments falling price reserves应收款 Account receivable应收票据 Note receivable银行承兑汇票 Bank acceptance商业承兑汇票 Trade acceptance 、应收股利 Dividend receivable应收利息 Interest receivable应收账款 Account receivable其他应收款 Other notes receivable坏账准备 Bad debt reserves资产减值损失 Asset impairment loss预付账款 Advance payment应收补贴款 Cover deficit by state subsidies of receivable库存资产 Inventories物资采购 Supplies purchasing原材料 Raw materials包装物 Wrappage低值易耗品 Low-value consumption goods材料成本差异 Materials cost variance自制半成品 Semi-Finished goods在途物资Materials in transport库存商品 Finished goods 商品进销差价 Differences between purchasing and selling price委托加工物资 Work in process - outsourced委托代销商品 Trust to and sell the goods on a commission basis受托代销商品 Commissioned and sell the goods on a commission basis存货跌价准备 Inventory falling price reserves分期收款发出商品 Collect money and send out the goods by stages待摊费用 Deferred and prepaid expenses长期投资 Long-term investment长期股权投资 Long-term investment on stocks股票投资 Investment on stocks其他股权投资 Other investment on stocks长期债权投资 Long-term investment on bonds债券投资 Investment on bonds其他债权投资 Other investment on bonds长期投资减值准备 Long-term investments depreciation reserves股权投资减值准备 Stock rights investment depreciation reserves债权投资减值准备 Bcreditor's rights investment depreciation reserves委托贷款 Entrust loans本金 Principal利息 Interest减值准备 Depreciation reserves固定资产 Fixed assets房屋 Building建筑物 Structure机器设备 Machinery equipment运输设备 Transportation facilities工具器具 Instruments and implement累计折旧 Accumulated depreciation固定资产减值准备 Fixed assets depreciation reserves 房屋、建筑物减值准备 Building/structure depreciation reserves机器设备减值准备 Machinery equipment depreciation reserves工程物资 Project goods and material专用材料 Special-purpose material专用设备 Special-purpose equipment预付大型设备款 Prepayments for equipment为生产准备的工具及器具 Preparative instruments and implement for fabricate在建工程 Construction-in-process安装工程 Erection works在安装设备 Erecting equipment-in-process技术改造工程 Technical innovation project大修理工程 General overhaul project在建工程减值准备 Construction-in-process depreciation reserves固定资产清理 Liquidation of fixed assets无形资产 Intangible assets专利权 Patents非专利技术 Non-Patents商标权 Trademarks, Trade names著作权 Copyrights土地使用权 Tenure商誉 Goodwill无形资产减值准备 Intangible Assets depreciation reserves专利权减值准备 Patent rights depreciation reserves商标权减值准备 trademark rights depreciation reserves 未确认融资费用 Unacknowledged financial charges待处理财产损溢 Wait deal assets loss or income长期待摊费用 Long-term deferred and prepaid expenses待处理财产损溢 Wait deal assets loss or income待处理流动资产损溢 Wait deal intangible assets loss or income待处理固定资产损溢 Wait deal fixed assets loss or income二、负债类 Liability短期负债 Current liability短期借款 Short-term borrowing应付票据 Notes payable银行承兑汇票 Bank acceptance商业承兑汇票 Trade acceptance应付账款 Account payable预收账款 Deposit received代销商品款 Proxy sale goods revenue应付工资 Accrued wages 应付福利费 Accrued welfarism应付股利 Dividends payable应交税金 Tax payable应交增值税 value added tax payable进项税额 Withholdings on VAT已交税金 Paying tax转出未交增值税 Unpaid VAT changeover减免税款 Tax deduction销项税额 Substituted money on VAT出口退税 Tax reimbursement for export进项税额转出 Changeover withnoldings on VAT出口抵减内销产品应纳税额 Export deduct domestic sales goods tax转出多交增值税 Overpaid VAT changeover未交增值税 Unpaid VAT应交营业税 Business tax payable应交消费税 Consumption tax payable应交资源税 Resources tax payable应交所得税 Income tax payable应交土地增值税 Increment tax on land value payable 应交城市维护建设税 Tax for maintaining and building cities payable应交房产税 Housing property tax payable应交土地使用税 Tenure tax payable应交车船使用税 Vehicle and vessel usage license plate tax(VVULPT) payable应交个人所得税 Personal income tax payable其他应交款 Other fund in conformity with paying其他应付款 Other payables预提费用 Drawing expense in advance其他负债 Other liabilities待转资产价值 Pending changerover assets value预计负债 Anticipation liabilities长期负债 Long-term Liabilities长期借款 Long-term loans一年内到期的长期借款 Long-term loans due within one year一年后到期的长期借款 Long-term loans due over one year应付债券 Bonds payable债券面值 Face value, Par value债券溢价 Premium on bonds债券折价 Discount on bonds应收利息 Interest receivable应计利息 Accrued interest长期应付款 Long-term account payable应付融资租赁款 Accrued financial lease outlay一年内到期的长期应付 Long-term account payable due within one year一年后到期的长期应付 Long-term account payable over one year专项应付款 Special payable一年内到期的专项应付 Long-term special payable due within one year一年后到期的专项应付 Long-term special payable over one year递延税款 Deferral taxes三、所有者权益类 OWNERS'' EQUITY资本 Capita实收资本(或股本) Paid-up capital(or stock)实收资本 Paicl-up capital实收股本 Paid-up stock已归还投资 Investment Returned公积资本公积 Capital reserve资本(或股本)溢价 Cpital(or Stock) premium接受捐赠非现金资产准备 Receive non-cash donate reserve股权投资准备 Stock right investment reserves拨款转入 Allocate sums changeover in外币资本折算差额 Foreign currency capital其他资本公积 Other capital reserve盈余公积 Surplus reserves法定盈余公积 Legal surplus任意盈余公积 Free surplus reserves法定公益金 Legal public welfare fund储备基金 Reserve fund企业发展基金 Enterprise expension fund利润归还投资 Profits capitalizad on return of investment 润 Profits本年利润 Current year profits利润分配 Profit distribution其他转入 Other chengeover in提取法定盈余公积 Withdrawal legal surplus 提取法定公益金 Withdrawal legal public welfare funds 提取储备基金 Withdrawal reserve fund提取企业发展基金 Withdrawal reserve for business expansion提取职工奖励及福利基金 Withdrawal staff and workers'' bonus and welfare fund利润归还投资 Profits capitalizad on return of investment 应付优先股股利 Preferred Stock dividends payable提取任意盈余公积 Withdrawal other common accumulation fund应付普通股股利 Common Stock dividends payable转作资本(或股本)的普通股股利 Common Stock dividends change to assets(or stock)未分配利润 Undistributed profit四、成本类 Cost生产成本 Cost of manufacture基本生产成本 Base cost of manufacture辅助生产成本 Auxiliary cost of manufacture制造费用 Manufacturing overhead材料费 Materials管理人员工资 Executive Salaries奖金 Wages退职金 Retirement allowance补贴 Bonus外保劳务费 Outsourcing fee福利费 Employee benefits/welfare会议费 Coferemce加班餐费 Special duties市内交通费 Business traveling通讯费 Correspondence电话费 Correspondence水电取暖费 Water and Steam税费 Taxes and dues租赁费 Rent管理费 Maintenance车辆维护费 Vehicles maintenance油料费 Vehicles maintenance培训费 Education and training接待费 Entertainment图书、印刷费 Books and printing运费 Transpotation保险费 Insurance premium支付手续费 Commission杂费 Sundry charges折旧费 Depreciation expense机物料消耗 Article of consumption劳动保护费 Labor protection fees季节性停工损失 Loss on seasonality cessation劳务成本 Service costs五、损益类 Profit and loss收入 Income业务收入 OPERATING INCOME主营业务收入 Prime operating revenue产品销售收入 Sales revenue服务收入 Service revenue其他业务收入 Other operating revenue材料销售 Sales materials代购代售包装物出租 Wrappage lease出让资产使用权收入 Remise right of assets revenue返还所得税 Reimbursement of income tax其他收入 Other revenue公允价值变动损益 Profit and loss arising from fair value changes持有至到期投资 Held-to-maturity investment投资收益 Investment income摊余成本 Amortized cost短期投资收益 Current investment income长期投资收益 Long-term investment income计提的委托贷款减值准备 Withdrawal of entrust loans reserves补贴收入 Subsidize revenue国家扶持补贴收入 Subsidize revenue from country其他补贴收入 Other subsidize revenue营业外收入 NON-OPERATING INCOME非货币性交易收益 Non-cash deal income现金溢余 Cash overage处置固定资产净收益 Net income on disposal of fixed assets出售无形资产收益 Income on sales of intangible assets 固定资产盘盈 Fixed assets inventory profit 罚款净收入 Net amercement income支出 Outlay业务支出 Revenue charges主营业务成本 Operating costs产品销售成本 Cost of goods sold服务成本 Cost of service主营业务税金及附加 Tax and associate charge营业税 Sales tax消费税 Consumption tax城市维护建设税 Tax for maintaining and building cities 资源税 Resources tax土地增值税 Increment tax on land value其他业务支出 Other business expense销售其他材料成本 Other cost of material sale其他劳务成本 Other cost of service其他业务税金及附加费 Other tax and associate charge 费用 Expenses营业费用 Operating expenses代销手续费 Consignment commission charge运杂费 Transpotation保险费 Insurance premium展览费 Exhibition fees广告费 Advertising fees管理费用 Administrative expenses职工工资 Staff Salaries修理费 Repair charge低值易耗摊销 Article of consumption办公费 Office allowance差旅费 Travelling expense工会经费 Labour union expenditure研究与开发费 Research and development expense福利费 Employee benefits/welfare职工教育经费 Personnel education待业保险费 Unemployment insurance劳动保险费 Labour insurance医疗保险费 Medical insurance会议费 Coferemce聘请中介机构费 Intermediary organs咨询费 Consult fees诉讼费 Legal cost业务招待费 Business entertainment技术转让费 Technology transfer fees矿产资源补偿费 Mineral resources compensation fees排污费 Pollution discharge fees房产税 Housing property tax车船使用税 Vehicle and vessel usage license plate tax(VVULPT)土地使用税 Tenure tax印花税 Stamp tax财务费用 Finance charge利息支出 Interest exchange汇兑损失 Foreign exchange loss各项手续费 Charge for trouble各项专门借款费用 Special-borrowing cost营业外支出 Nonbusiness expenditure捐赠支出 Donation outlay减值准备金 Depreciation reserves非常损失 Extraordinary loss处理固定资产净损失 Net loss on disposal of fixed assets出售无形资产损失 Loss on sales of intangible assets固定资产盘亏 Fixed assets inventory loss债务重组损失 Loss on arrangement罚款支出 Amercement outlay所得税 Income tax以前年度损益调整 Prior year income adjust ment应交税费-应交所得税 Tax payable - income tax payable应交税费-应交增值税(进项税额) Tax payable - VAT(input VAT)应交税费-应交增值税(销项税额)Tax payable - VAT(output VAT)应交税费-应交增值税(出口退税)Tax payable - VAT(refund of export duty)应交税费-应交增值税(进项税额转出)Tax payable - VAT(transfer-out of input VAT)应交税费-应交增值税(已交税金)Tax payable - VAT(taxes paid)应交税费-应交增值税(转出未交增值税)Tax payable - VAT(transfer-out of unpaid VAT)应交税费-应交增值税(转出多交增值税)Tax payable - VAT(transfer-out of overpaid VAT)应交税费-应交增值税(减免税款)Tax payable - VAT(VAT deductions and exemptions)应交税费-应交增值税(出口抵减内销产品应纳税额) Tax payable -VAT(export duty deductible from taxes payable on domestic sales)应交税费-应交营业税 Tax payable - business tax payable 应交税费-应交消费税 Tax payable - excise tax payable。

会计分录英文版

会计分录英文版资产类 Assets流动资产 Current assets货币资金 Cash and cash equivalents1001 现金 Cash1002 银行存款Cash in bank 1009 其他货币资金Other cash and cash equivalents100901 外埠存款 Other city Cash in bank100902 银行本票 Cashier''s cheque100903 银行汇票Bank draft 100904 信用卡Credit card 100905 信用证保证金 L/C Guarantee deposits100906 存出投资款 Refundable deposits1101 短期投资 Short-term investments110101 股票 Short-term investments - stock110102 债券Short-term investments - corporate bonds 110103 基金 Short-term investments - corporate funds 110110 其他 Short-term investments - other1102 短期投资跌价准备 Short-term investments falling price reserves应收款 Account receivable 1111 应收票据 Note receivable 银行承兑汇票 Bank acceptance 商业承兑汇票 Trade acceptance 1121 应收股利 Dividend receivable 1122 应收利息 Interestreceivable1131 应收账款 Accountreceivable1133 其他应收款 Other notesreceivable1141 坏账准备 Bad debtreserves1151 预付账款 Advance money 1161 应收补贴款 Cover deficit by state subsidies of receivable 库存资产 Inventories1201 物资采购 Supplies purchasing1211 原材料 Raw materials 1221 包装物 Wrappage1231 低值易耗品 Low-value consumption goods1232 材料成本差异 Materials cost variance1241 自制半成品 Semi-Finished goods1243 库存商品 Finished goods 1244 商品进销差价 Differences between purchasing and selling price1251 委托加工物资 Work in process - outsourced1261 委托代销商品 Trust to and sell the goods on a commission basis1271 受托代销商品Commissioned and sell the goods on a commission basis 1281 存货跌价准备 Inventory falling price reserves1291 分期收款发出商品 Collect money and send out the goodsby stages1301 待摊费用 Deferred and prepaid expenses长期投资 Long-term investment 1401 长期股权投资 Long-term investment on stocks 140101 股票投资 Investment on stocks140102 其他股权投资 Other investment on stocks1402 长期债权投资 Long-term investment on bonds 140201 债券投资 Investment on bonds140202 其他债权投资 Other investment on bonds1421 长期投资减值准备 Long- term investments depreciation reserves股权投资减值准备 Stock rights investment depreciation reserves债权投资减值准备 Bcreditor''s rights investment depreciation reserves1431 委托贷款 Entrust loans 143101 本金 Principal 143102 利息 Interest143103 减值准备 Depreciation reserves1501 固定资产 Fixed assets房屋 Building建筑物 Structure机器设备 Machinery equipment运输设备 Transportationfacilities工具器具 Instruments andimplement1502 累计折旧 Accumulateddepreciation1505 固定资产减值准备 Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves1601 工程物资 Project goods and material160101 专用材料 Special-purpose material160102 专用设备 Special-purpose equipment160103 预付大型设备款Prepayments for equipment 160104 为生产准备的工具及器具 Preparative instruments and implement for fabricate1603 在建工程 Construction-in-process安装工程 Erection works在安装设备 Erecting equipment-in-process技术改造工程 Technical innovation project大修理工程 General overhaul project1605 在建工程减值准备Construction-in-process depreciation reserves1701 固定资产清理 Liquidation of fixed assets1801 无形资产 Intangible assets 专利权 Patents非专利技术 Non-Patents商标权 Trademarks, Trade names著作权 Copyrights 土地使用权 Tenure 商誉 Goodwill1805 无形资产减值准备Intangible Assets depreciation reserves专利权减值准备 Patent rights depreciation reserves商标权减值准备 trademarkrights depreciation reserves1815 未确认融资费用Unacknowledged financial charges待处理财产损溢 Wait dealassets loss or income1901 长期待摊费用 Long-term deferred and prepaid expenses 1911 待处理财产损溢 Wait deal assets loss or income191101待处理流动资产损溢Wait deal intangible assets lossor income191102待处理固定资产损溢Wait deal fixed assets loss or income二、负债类 Liability短期负债 Current liability2101 短期借款 Short-term borrowing2111 应付票据 Notes payable 银行承兑汇票 Bank acceptance 商业承兑汇票 Trade acceptance 2121 应付账款 Account payable 2131 预收账款 Deposit received 2141 代销商品款 Proxy sale goods revenue2151 应付工资 Accrued wages 2153 应付福利费 Accrued welfarism2161 应付股利 Dividends payable2171 应交税金 Tax payable 217101 应交增值税 value added tax payable21710101 进项税额Withholdings on VAT 21710102 已交税金 Paying tax 21710103 转出未交增值税Unpaid VAT changeover 21710104 减免税款 Tax deduction21710105 销项税额 Substituted money on VAT21710106 出口退税 Tax reimbursement for export 21710107 进项税额转出Changeover withnoldings on VAT21710108 出口抵减内销产品应纳税额 Export deduct domesticsales goods tax21710109 转出多交增值税Overpaid VAT changeover21710110 未交增值税 UnpaidVAT217102 应交营业税 Businesstax payable217103 应交消费税Consumption tax payable217104 应交资源税 Resourcestax payable217105 应交所得税 Income taxpayable217106 应交土地增值税Increment tax on land valuepayable217107 应交城市维护建设税Tax for maintaining and building cities payable217108 应交房产税 Housing property tax payable217109 应交土地使用税 Tenure tax payable217110 应交车船使用税 Vehicle and vessel usage license plate tax(VVULPT) payable217111 应交个人所得税Personal income tax payable 2176 其他应交款 Other fund in conformity with paying2181 其他应付款 Other payables2191 预提费用 Drawing expense in advance其他负债 Other liabilities2201 待转资产价值 Pending changerover assets value 2211 预计负债 Anticipation liabilities长期负债Long-term Liabilities 2301 长期借款Long-term loans 一年内到期的长期借款 Long-term loans due within one year 一年后到期的长期借款 Long-term loans due over one year 2311 应付债券 Bonds payable 231101 债券面值 Face value, Par value 231102 债券溢价 Premium on bonds231103 债券折价 Discount on bonds231104 应计利息Accrued interest 2321 长期应付款Long-termaccount payable应付融资租赁款 Accruedfinancial lease outlay一年内到期的长期应付 Long-term account payable due withinone year一年后到期的长期应付 Long-term account payable over oneyear2331 专项应付款 Specialpayable一年内到期的专项应付 Long-term special payable due withinone year一年后到期的专项应付 Long-term special payable over oneyear2341 递延税款 Deferral taxes三、所有者权益类 OWNERS''EQUITY资本 Capita3101 实收资本(或股本) Paid-upcapital(or stock)实收资本 Paicl-up capital实收股本 Paid-up stock3103 已归还投资 Investment Returned公积3111 资本公积 Capital reserve 311101 资本(或股本)溢价Cpital(or Stock) premium 311102 接受捐赠非现金资产准备 Receive non-cash donate reserve311103 股权投资准备 Stock right investment reserves 311105 拨款转入 Allocate sums changeover in311106 外币资本折算差额Foreign currency capital 311107 其他资本公积 Other capital reserve3121 盈余公积 Surplus reserves 312101 法定盈余公积 Legal surplus312102 任意盈余公积 Free surplus reserves312103 法定公益金 Legal public welfare fund312104 储备基金 Reserve fund 312105 企业发展基金Enterprise expension fund312106 利润归还投资 Profitscapitalizad on return ofinvestment利润 Profits3131 本年利润 Current yearprofits3141 利润分配 Profit distribution314101 其他转入 Otherchengeover in314102 提取法定盈余公积Withdrawal legal surplus314103 提取法定公益金Withdrawal legal public welfarefunds314104 提取储备基金Withdrawal reserve fund314105 提取企业发展基金Withdrawal reserve for businessexpansion314106 提取职工奖励及福利基金 Withdrawal staff andworkers'' bonus and welfarefund314107 利润归还投资Profits capitalizad on return of investment314108 应付优先股股利Preferred Stock dividends payable314109 提取任意盈余公积Withdrawal other common accumulation fund314110 应付普通股股利Common Stock dividends payable314111 转作资本(或股本)的普通股股利Common Stockdividends change to assets(or stock)314115 未分配利润Undistributed profit四、成本类 Cost4101 生产成本 Cost of manufacture410101 基本生产成本 Base cost of manufacture410102 辅助生产成本 Auxiliary cost of manufacture 4105 制造费用 Manufacturing overhead材料费 Materials管理人员工资 Executive Salaries奖金 Wages退职金 Retirement allowance 补贴 Bonus外保劳务费 Outsourcing fee福利费 Employeebenefits/welfare会议费 Coferemce 加班餐费 Special duties市内交通费 Business traveling通讯费 Correspondence电话费 Correspondence水电取暖费 Water and Steam税费 Taxes and dues租赁费 Rent管理费 Maintenance车辆维护费 Vehiclesmaintenance油料费 Vehicles maintenance培训费 Education and training接待费 Entertainment图书、印刷费 Books andprinting运费 Transpotation保险费 Insurance premium支付手续费 Commission杂费 Sundry charges折旧费 Depreciation expense 机物料消耗 Article of consumption劳动保护费 Labor protection fees季节性停工损失 Loss on seasonality cessation4107 劳务成本 Service costs 五、损益类 Profit and loss收入 Income业务收入 OPERATING INCOME5101 主营业务收入 Prime operating revenue产品销售收入 Sales revenue 服务收入 Service revenue 5102 其他业务收入 Other operating revenue材料销售 Sales materials代购代售包装物出租 Wrappage lease 出让资产使用权收入 Remise right of assets revenue返还所得税 Reimbursement of income tax其他收入 Other revenue 5201 投资收益 Investmentincome短期投资收益 Current investment income长期投资收益 Long-term investment income计提的委托贷款减值准备Withdrawal of entrust loans reserves5203 补贴收入 Subsidize revenue国家扶持补贴收入 Subsidize revenue from country其他补贴收入 Other subsidize revenue5301 营业外收入 NON- OPERATING INCOME非货币性交易收益 Non-cashdeal income现金溢余 Cash overage处置固定资产净收益 Net income on disposal of fixed assets出售无形资产收益 Income on sales of intangible assets固定资产盘盈 Fixed assets inventory profit罚款净收入 Net amercement income支出 Outlay业务支出 Revenue charges5401 主营业务成本 Operating costs产品销售成本 Cost of goods sold服务成本 Cost of service5402 主营业务税金及附加 Tax and associate charge营业税 Sales tax消费税 Consumption tax城市维护建设税 Tax for maintaining and building cities 资源税Resources tax土地增值税 Increment tax on land value5405 其他业务支出 Other business expense销售其他材料成本 Other cost of material sale其他劳务成本 Other cost of service其他业务税金及附加费 Other tax and associate charge费用 Expenses5501 营业费用 Operating expenses代销手续费 Consignment commission charge运杂费 Transpotation保险费 Insurance premium展览费 Exhibition fees广告费 Advertising fees5502 管理费用 Administrative expenses职工工资 Staff Salaries修理费 Repair charge低值易耗摊销 Article of consumption办公费 Office allowance差旅费 Travelling expense 工会经费 Labour unionexpenditure研究与开发费 Research anddevelopment expense福利费 Employeebenefits/welfare职工教育经费 Personnel education待业保险费 Unemployment insurance劳动保险费 Labour insurance医疗保险费 Medical insurance 会议费 Coferemce聘请中介机构费 Intermediary organs咨询费 Consult fees诉讼费 Legal cost业务招待费 Business entertainment技术转让费 Technology transfer fees矿产资源补偿费 Mineral resources compensation fees 排污费 Pollution discharge fees 房产税 Housing property tax车船使用税 Vehicle and vessel usage license plate tax(VVULPT) 土地使用税 Tenure tax印花税 Stamp tax5503 财务费用 Finance charge 利息支出 Interest exchange汇兑损失 Foreign exchange loss 各项手续费 Charge for trouble 各项专门借款费用 Special- borrowing cost5601 营业外支出 Nonbusinessexpenditure捐赠支出 Donation outlay减值准备金 Depreciation reserves非常损失 Extraordinary loss处理固定资产净损失 Net loss on disposal of fixed assets出售无形资产损失 Loss on sales of intangible assets固定资产盘亏 Fixed assets inventory loss债务重组损失 Loss on arrangement罚款支出 Amercement outlay 5701 所得税 Income tax以前年度损益调整 Prior year income adjustment。

英文会计分录

中文科目是老的叫法)现金Cash in hand银行存款Cash in bank其他货币资金-外埠存款Other monetary assets - cash in other cities其他货币资金-银行本票Other monetary assets - cashier‘s check其他货币资金-银行汇票Other monetary assets - bank draft其他货币资金-信用卡Other monetary assets - credit cards其他货币资金-信用证保证金Other monetary assets - L/C deposit其他货币资金-存出投资款Other monetary assets - cash for investment 短期投资-股票投资Investments - Short term - stocks短期投资-债券投资Investments - Short term - bonds短期投资-基金投资Investments - Short term - funds短期投资-其他投资Investments - Short term - others短期投资跌价准备Provision for short-term investment长期股权投资-股票投资Long term equity investment - stocks长期股权投资-其他股权投资Long term equity investment - others 长期债券投资-债券投资Long term securities investemnt - bonds长期债券投资-其他债权投资Long term securities investment - others 长期投资减值准备Provision for long-term investment应收票据Notes receivable应收股利Dividends receivable应收利息Interest receivable应收帐款Trade debtors坏帐准备- 应收帐款Provision for doubtful debts - trade debtors预付帐款Prepayment应收补贴款Allowance receivable其他应收款Other debtors坏帐准备- 其他应收款Provision for doubtful debts - other debtors其他流动资产Other current assets物资采购Purchase原材料Raw materials包装物Packing materials低值易耗品Low value consumbles材料成本差异Material cost difference自制半成品Self-manufactured goods库存商品Finished goods商品进销差价Difference between purchase & sales of commodities委托加工物资Consigned processiong material委托代销商品Consignment-out受托代销商品Consignment-in分期收款发出商品Goods on instalment sales存货跌价准备Provision for obsolete stocks待摊费用Prepaid expenses待处理流动资产损益Unsettled G/L on current assets待处理固定资产损益Unsettled G/L on fixed assets委托贷款-本金Consignment loan - principle委托贷款-利息Consignment loan - interest委托贷款-减值准备Consignment loan - provision固定资产-房屋建筑物Fixed assets - Buildings固定资产-机器设备Fixed assets - Plant and machinery固定资产-电子设备、器具及家具Fixed assets - Electronic Equipment, furniture and fixtures固定资产-运输设备Fixed assets - Automobiles累计折旧Accumulated depreciation固定资产减值准备Impairment of fixed assets工程物资-专用材料Project material - specific materials工程物资-专用设备Project material - specific equipment工程物资-预付大型设备款Project material - prepaid for equipment工程物资-为生产准备的工具及器具Project material - tools and facilities for production在建工程Construction in progress在建工程减值准备Impairment of construction in progress固定资产清理Disposal of fixed assets无形资产-专利权Intangible assets - patent无形资产-非专利技术Intangible assets - industrial property and know-how无形资产-商标权Intangible assets - trademark rights无形资产-土地使用权Intangible assets - land use rights无形资产-商誉Intangible assets - goodwill无形资产减值准备Impairment of intangible assets长期待摊费用Deferred assets未确认融资费用Unrecognized finance fees其他长期资产Other long term assets递延税款借项Deferred assets debits应付票据Notes payable应付帐款Trade creditors预收帐款Adanvances from customers代销商品款Consignment-in payables其他应交款Other payable to government其他应付款Other creditors应付股利Proposed dividends待转资产价值Donated assets预计负债Accrued liabilities应付短期债券Short-term debentures payable其他流动负债Other current liabilities预提费用Accrued expenses应付工资Payroll payable应付福利费Welfare payable短期借款-抵押借款Bank loans - Short term - pledged短期借款-信用借款Bank loans - Short term - credit短期借款-担保借款Bank loans - Short term - guaranteed一年内到期长期借款Long term loans due within one year一年内到期长期应付款Long term payable due within one year长期借款Bank loans - Long term应付债券-债券面值Bond payable - Par value应付债券-债券溢价Bond payable - Excess应付债券-债券折价Bond payable - Discount应付债券-应计利息Bond payable - Accrued interest长期应付款Long term payable专项应付款Specific payable其他长期负债Other long term liabilities应交税金-所得税Tax payable - income tax应交税金-增值税Tax payable - V AT应交税金-营业税Tax payable - business tax应交税金-消费税Tax payable - consumable tax应交税金-其他Tax payable - others递延税款贷项Deferred taxation credit股本Share capital已归还投资Investment returned利润分配-其他转入Profit appropriation - other transfer in利润分配-提取法定盈余公积Profit appropriation - statutory surplus reserve利润分配-提取法定公益金Profit appropriation - statutory welfare reserve利润分配-提取储备基金Profit appropriation - reserve fund利润分配-提取企业发展基金Profit appropriation - enterprise development fund利润分配-提取职工奖励及福利基金Profit appropriation - staff bonus and welfare fund利润分配-利润归还投资Profit appropriation - return investment by profit利润分配-应付优先股股利Profit appropriation - preference shares dividends利润分配-提取任意盈余公积Profit appropriation - other surplus reserve利润分配-应付普通股股利Profit appropriation - ordinary shares dividends利润分配-转作股本的普通股股利Profit appropriation - ordinary shares dividends converted to shares期初未分配利润Retained earnings, beginning of the year资本公积-股本溢价Capital surplus - share premium资本公积-接受捐赠非现金资产准备Capital surplus - donation reserve资本公积-接受现金捐赠Capital surplus - cash donation资本公积-股权投资准备Capital surplus - investment reserve资本公积-拨款转入Capital surplus - subsidiary资本公积-外币资本折算差额Capital surplus - foreign currency translation资本公积-其他Capital surplus - others盈余公积-法定盈余公积金Surplus reserve - statutory surplus reserve盈余公积-任意盈余公积金Surplus reserve - other surplus reserve盈余公积-法定公益金Surplus reserve - statutory welfare reserve盈余公积-储备基金Surplus reserve - reserve fund盈余公积-企业发展基金Surplus reserve - enterprise development fund盈余公积-利润归还投资Surplus reserve - reture investment by investment主营业务收入Sales主营业务成本Cost of sales主营业务税金及附加Sales tax营业费用Operating expenses管理费用General and administrative expenses财务费用Financial expenses投资收益Investment income其他业务收入Other operating income营业外收入Non-operating income补贴收入Subsidy income其他业务支出Other operating expenses营业外支出Non-operating expenses所得税Income tax一、资产类assets现金cash on hand银行存款cash in bank其他货币资金other cash and cash equivalent短期投资short-term investment短期投资跌价准备short-term investments falling price reserve应收票据notes receivable应收股利dividend receivable应收利息interest receivable应收帐款accounts receivable坏帐准备bad debt reserve预付帐款advance money应收补贴款cover deficit receivable from state subsidize其他应收款other notes receivable在途物资materials in transit原材料raw materials包装物wrappage低值易耗品low-value consumption goods库存商品finished goods委托加工物资work in process-outsourced委托代销商品trust to and sell the goods on a commission basis受托代销商品commissioned and sell the goods on a commission basis 存货跌价准备inventory falling price reserve分期收款发出商品collect money and send out the goods by stages待摊费用deferred and prepaid expenses长期股权投资long-term investment on stocks长期债权投资long-term investment on bonds长期投资减值准备long-term investment depreciation reserve固定资产fixed assets累计折旧accumulated depreciation工程物资project goods and material在建工程project under construction固定资产清理fixed assets disposal无形资产intangible assets开办费organization/preliminary expenses长期待摊费用long-term deferred and prepaid expenses待处理财产损溢wait deal assets loss or income二、负债类debts短期借款short-term loan应付票据notes payable应付帐款accounts payable预收帐款advance payment代销商品款consignor payable应付工资accrued payroll应付福利费accrued welfarism应付股利dividends payable应交税金tax payable其他应交款accrued other payments其他应付款other payable预提费用drawing expenses in advance长期借款long-term loan应付债券debenture payable长期应付款long-term payable递延税款deferred tax住房周转金revolving fund of house三、所有者权益owners equity股本paid-up stock资本公积capital reserve盈余公积surplus reserve本年利润current year profit利润分配profit distribution四、成本类cost生产成本cost of manufacture制造费用manufacturing overhead五、损益类profit and loss (p/l)主营业务收入prime operating revenue其他业务收入other operating revenue折扣与折让discount and allowance投资收益investment income补贴收入subsidize revenue营业外收入non-operating income主营业务成本operating cost主营业务税金及附加tax and associate charge 其他业务支出other operating expenses存货跌价损失inventory falling price loss营业费用operating expenses管理费用general and administrative expenses 财务费用financial expenses营业外支出non-operating expenditure所得税income tax以前年度损益调整adjusted p/l for prior year。

会计专业英语(五篇范例)

会计专业英语(五篇范例)第一篇:会计专业英语Accounting termsAccounting entity会计主体Accounting procedure会计核算Accounting process会计程序/过程Accounting practice会计核算Accounting element会计要素Accounting principle会计原则Accounting standard会计准则Accounting assumption会计假设Accounting equation会计等式Business=Enterpris企业Firm=Company公司Organization组织Performance业绩 Financial position 财务状况Operating result 业绩、经营成果Economic activity经济活动Corporation有限责任公司(股份公司)Assets资产Liability负债Owner’s eq uity 所有者权益 Capital 资本Revenue收入Income收益Expense费用 Cost费用、成本Profit 利润Net income净收益Loss损失Users of accounting informationManager管理者Shareholder股东Owner所有者Accountant会计师Casher出纳Bookkeeper记账员Investor投资者Creditor债权人Supplier供货商Government政府Public公众Accounting EntityOrganization:①Not-for-profit organization②business organization1.business organization①Sole Proprietorship Enterprises独资经营企业②General Partnership Enterprises普通合伙企业③Limited Liability Partnership Enterprises有限责任合伙企业④Corporation股份公司2.Corporation①Owned by one person②Simple to establish③Owner controlled④Tax advantages3.General Partnership①Owned by more than one person②Simple to establish③Shared control ④Tax advantages4.Limited Liability Partnership①Only for certain occupations ②Limited liability for p artnership debts and obligations③Also a limitation on participation in management5.Corporation①Organized as a separate legal entity and owned by stockholders②Easy to transfer ownership③Easier to raise funds④No personal liabilityAccounting PrinciplesConcept概念Standard准则Convention惯例Assumption假设Rule规则Accounting AssumptionsAccounting entity assumption会计主体Going concern assumption持续经营 Money measurement assumption货币计量Accounting period assumption会计期间The qualitative characteristics of financial informationRelevant相关性Reliable可靠性Comparable可比性Understandable可理解性Timeliness及时性Prudence谨慎性Materiality重要性Consistency一贯性Substance over legal form实质重于形式Accruals basis权责发生制Principles about Measurement and PresentationThe Accrual Basis Principle权责发生制原则The Matching Principle配比原则The Historical Cost Principle历史成本原则The Distinction Between Revenue Expenditures and Capital Expenditures Principle划分收益性支出和资本性支出原则Accounting termsDouble-entryBookkeepingDouble-entry systemAccount title会计科目Code /chart of account title会计科目表Accounting entry 会计主体Debit 借Credit 贷Increase增加Decrease减少Sum总额Balance余额a debit balance 借方余额a credit balance贷方余额Trial balance试算平衡Total amount of debits/credits借/贷方金额合计Accounting cycle会计循环Fiscal year会计年度System accountingAccount账户Types of accounts账户的种类Accounting record 会计档案Typesof accountsAccount book账本Ledger分类账Journal日记账General ledger总分类账Subsidiary Ledger明细分类账General Journal总日记账Special Journal特种日记账Accounting ElementsAssets资产Liabilities 负债Profit利润Owners' Equity所有者权益Expenses费用Revenue收入liabilitiesCurrent liabilities流动负债Non-current liabilities非流动负债Short-Term Note Payable短期应付票据Long-T erm Note Payable长期应付票据Accrued liabilities应记负债Wages Payable /Salaries Payable 应付职工薪酬Taxes Payable 应交税费Dividends Payable应付股利long-term liabilities长期负债Contingent liabilities或有负债Accrued expenses预提费用Current Ratio流动比率Long-term loans payable长期借款Long-term accounts payable长期应付款Bonds payable应付债券Capitallease融资性租赁Operating lease经营性租赁Notes payable应付票据Accounts payable应付账款Unearned Fees=Unearned Revenue预收账款Current maturities of long-term debt将于一年内到期的长期负债Owners equityDividend股利Corporation公司Stock股票/存货Board of directors董事会Capital stock股本Preferred stock优先股Owner’s Capital所有者权益Common Stock普通股Share股份Capital reserve资本公积Statutory Surplus reserve盈余公积Additional paid-in Capital资本溢价/资本公积Paid-in capital 投入资本/实收资本Shareholder=stockholder=director股东Retained earnings=retained capital留存收益Original voucher/source voucher原始凭证Recording voucher 记账凭证Sales invoice销售发票Receipt收据Make entries做会计分录Adjusting entries调整分录Posting过账Closing entries结账The Income Statement利润表The Balance Sheet资产负债表The Cash Flow Statement现金流量表Prepare financial statements财务报表A Statement of Changes in Equity所有者权益变动表Current AssetsCurrent assets流动资产Quick assets速冻资产Cash现金Short-term investment短期金融投资Cash equivalent现金等价物Cash receipt现金收入Cash disbursement现金支出Petty cash fund备用金Bank reconciliation statement银行存款余额调节表Dividends Receivable 应付股利Inventory存货Gross method总价法Net method净价法Bad debts坏账Accounts receivables应收账款Notes receivables应收票据Discount trade discount商业折扣Cash discount /sales discount现金折扣Direct write-off method直接冲销法allowance method备抵法Non-trade receivables非营业应收款Interest receivables应收利息Dividends receivables应收股利Other receivable其它应收款InventoriesRaw material原材料Finished goods成品Merchandise商品Goods in process在成品Partially finished goods /Semi-finished goods半成品Low-value and perishable articles低值易耗品Low-valued and easily-damaged implements价格低廉的易耗用品Perpetual inventory system永续盘存制Periodic inventory system定期盘存制Raw material to be used in the production用于生产的原材料All kinds of materials,fuels,containers各种材料,燃料,包装物Non-Current AssetsBond债券Land土地Depreciation折扣Bonds investment债券投资Non-Current assets非流动资Intangible assets无形资产Shares investments股票投资Revenue expenditure营业支出Capital expenditure资产支出Long-term investment长期投资Plant asset=Fixed assets固定资产Bonds investmentMarket value市场价Premium溢价Discount折扣Salvage value残值Amortized cost摊销成本Useful life使用年限Cost-----historical cost历史成本Accumulated Depreciation加速折旧法Types of Bonds PayableConvertible bonds可兑换债券Callable bonds可提前(可通知)偿还的债券Secured bonds担保债券Unsecured bonds无担保债券Term bonds定期债券Serial bonds分期还本债券Registered bonds记名债券Bearer bonds不记名债券Present value现值Face value/principal value面值Maturity value到期值Contractual interest rate合同利率Market interest rate市场利率Effective interest rate实际利率Common Stock dividendsCash dividends现金股利Stock dividends股票股利Property dividends财产股利Fixed dividends股利事先确定Limited voting rights有限的投票权Dividends set down in advance先于普通股发放Revenue, Expenses and ProfitRevenue收入sales revenue销售收入cost费用/成本Expense 费用Profit利润gross profit利润总额net profit净利润net income 净收益Prime operating revenue主营业务收入Other operatingrevenue其它业务收入services revenue服务/劳务收入Cost of goods sold销货成本Periodic expense期间费用Operating expense 营业费用sellingexpense销售费用Financial expense 财务费用investment profit投资收益Non-operating income营业外收入Non-operating expense营业外支出Fees Earned服务费收入Rent Earned租金收入Interest Revenue利息收入Office wages expense管理人员工资Rent expense租金费用Telephone expense电话费Advertising expense广告费Administrative expense管理费用Interest expense利息费用(财务费用)Operating profit营业利润Net investment profit投资净收益 Net non-operating income营业外收支额Income StatementIncome statement利润表Profitability盈利能力Gross Profit on Sales销售毛利Operating result业务成果/运营成果Sales returns and allowances销售折扣/销售折让Operating Income/profit营业收入/营业利润Earnings Before Interest and Tax息税前收益Operating profitOperating Revenue-Operating Cost-Operating Taxes and Surcharges-Selling Expenses-Administrative Expense-FinancingExpense-Impairment loss+Profit or loss of assets at fair value+Net Investment Profit=Operating profitNet investment profitgains from external investments-investment losses incurred-any provision for impairment losses on investments=net investment profitGross ProfitOperating profit+Non-operating Income-Non-operating Expenses=Gross ProfitNetProfitGross Profit-Income Tax=Net ProfitThe basis of Balance Sheettotal revenues – total expenses = net incometotal expenses – total revenues = net lossMultiple-step FormSales-Sales Returns and Allowances=Net Sales-Cost of Goods Sold=Gross Profit on Sales-Operating Expenses=Operating Income +Other Revenues and Gains-Other Expenses and Losses=Net IncomeAccounting EquationAssets = Liabilities + Owners' EquityBasis of double-entry bookkeepingBasis of balance sheetaccounting equation always stays in balanceAssets = Liabilities + Owners' Equitybeg +(Revenue −Expenses)Assets + Expenses = Liabilities + Owners' Equitybeg + Revenue第二篇:会计专业英语会计是什么会计是什么?多年来,流行的说法,会计是会计,成绩和会计。

会计英语分录

•1)purchases of inventory in cash for $3 000•Dr. Inventory 3000Cr. Cash 3000•2)sales on account of $10 000•Dr. Accounts receivable 10 000Cr. Sales revenue 10 0003)paid $50 000 in salaries & wagesDr. Salaries & wages expense 50 000Cr. Bank deposit 50 0004)cash sale of US$1 180Dr. Cash 1 180Cr. Sales revenue 1 1805)pre-paid insurance for $12 000Dr. Prepaid insurance 12 000Cr. Bank deposit 12 0006) Issued a one-month-term note $20 000 for the payment of accounts payable .Dr. Accounts payable 20 000Cr. Notes payable 20 0007) purchased a piece of land as long-term investment for cash $10 000.Dr. Land 10 000Cr. Cash 10 0008) purchased office equipment for cash $5 000.Dr. Office equipment 5000Cr. Cash 50009) purchased on account a lot of merchandise amounting $60 000.Dr. Inventory 60 000Cr. Accounts payable 60 00010) made a sale of merchandise on account for $81 000Dr. Accounts receivable 81 000Cr. Sales revenue 81 00011) paid cash in advance for two months’ rent $800.Dr. Prepaid rent 800Cr. Cash 80012) collection from customers $70 000: $60 000 cash, $10 000 note–a one-month term note bearing 10.8% interest.Dr. Cash 60 000Notes receivable 10 000Cr. Accounts receivable 70 00013) paid $40 000 cash for accounts payable–liability item.Dr. Accounts payable 40 000Cr. Cash 40 00014) paid other expenses $5 200 in cash.Dr. Other expenses 5 200Cr. Cash 5 20015) paid cash for employees’ salaries $16 000 for the first four weeks of the month.Dr. Salary expenses 16 000Cr. Cash 16 00016) payment of cash dividend $2 000.Dr. Dividend 2 000Cr. Cash 2 00017) paid a $1 200 premium(费用)in cash for one year’s insurance in advance.Dr. Prepaid Insurance 1 200Cr. Cash 1 20018) At the end of this month, $100 of prepaid insurance had expired(期满) or been used up.Dr. Insurance Expense 100Cr. Prepaid Insurance 10019) The owner Andy invest $20 000 cash into businessDr. Bank Deposit 20 000Cr. Capital 20 00020) Purchased a dental equipment(牙科设备) for $16,000 cash in bank(银行存款)Dr. Dental equipment 16 000Cr. Cash in bank 16 00021) Purchase an air conditioner(空调)on credit for $16,000Dr. Air conditioner 16 000Cr. Account payable 16 00022) Received Accounting service revenue $1500Dr. Bank deposit 1 500Cr. Service revenue 1 50023) Sold goods on credit for $1000 that originally cost $600Dr. Account receivable 1000Cr. Sales revenues 1000Dr. Cost of good sold(主营业务成本) 600Cr. Inventory 60024) Paid money owed to the transportation company $100Dr. Account payable 100Cr. Bank deposit 10025) Received $150 cash from customer.Dr. cash 150Cr. Account receivable 15026) Owner withdrew $100 cash for personal useDr. Drawings(资本退出)100Cr. Cash 10027) Customer- Janson owing $100 has gone bankrupt (破产)Dr. Bad debts (坏账)100Cr. Account receivable 100。

专业英语会计分录资料

专业英语分录练习1. Jan.1 The owner of Johnson company, Mr. Deep and his friends, invested 75 000 in cash, Land valuing 50 000 and Equipment A valuing 73 000 into the company.Dr. CashLandEquipment ACr. Capital2. Jan.1 Johnson Company receive a long-term bank loan of 60 000. The bank agreed to lend the money to it for 3 years with the annual interest rate of 12% and the interest shall be paid annually at the year ends while the principal should be paid back at the end of the third year. How did the company make the entry on Dec. 31?Jan 1 Dr. cash 60 000Cr. Loan 60 000Dec 31 Dr. interest expense 600Interest payable 6600Cr. Cash 72003. Jan 1 Buy the business insurance for one year costing 24 000, the bill has not paid yet. Dr. prepaid insurance/unexpired insurance 24 000Cr.Account payable 24 0004. Jan.2 Johnson Company purchased 10 000 raw materials on credit and the supplier agree to collect cash one month later.Dr. raw materials 10 000Cr. Account payable 10 0005 Jan6 The company bought a company car at 11 000 for cash and cost 1 000 for transportation.Dr. Car 12000Cr. Cash 120006. Jan.7 The company paid to the manufacturing workers 10 000(all direct) and administrative staffs 4 500 (nonmanufacturing).Dr. manufacturing payroll 10000Salary expenses 4500Cr. Cash 145007. Jan.8 Company moved all the finished goods, with the cost of 45 500, into warehouse ready for sale.Dr. finished goods 45500Cr. Work in process 455008. Jan 11 Sale the product for 125 000. Half of the sales were for cash, half on credit. Also, it reported the cost of 40 000.Dr. cash 62500Account receivable 62500Cr. Sales revenue 125000Dr. cost of goods sold 40 000Cr. Finished goods 40 0009. Jan 31 Company used bad debt allowance method to record bad debt expense. It recognized 6% of the ending balance of Accounts receivable as the bad debt expense of that accounting period.Dr. bad debt expense 62500*6%=3750 Cr. Bad debt allowance 62500*6%=375010. Jan 31 Record the accrual expense. (Suppose the car is supposed to be used for 5 years.)Dr. insurance expense 2000Cr. Prepaid insurance 2000Dr. Depreciation expense 200Cr. Accumulated Depreciation 200Dr. Interest expense 600Cr. Interest payable 60011. Jan 31 Close all the revenue account and expense account.Dr. sales revenue 125000Cr. Income summary 125000Dr. Income summary 51 050Cr. Salary expense 4500COGS 40000Bad debt expense 3750Insurance expense 2000Depreciation expense 200Interest expense 60012. Jan 31 Close the income summary account.Dr. income summary 73 950Cr. Retained earnings 73 950。

会计英语分录

1/1 Ba l.

6,000 5,500

Re nta l Re ve nue 1/31 500

Learning Objective

To prepare adjusting entries to accrue unpaid expenses.

LO5

Accruing Unpaid Expenses

End of Current Period

Transaction Paid cash in advance of incurring expense (creates an asset).

Adjusting Entry Recognizes portion of asset consumed as expense, and Reduces balance of asset account.

Converting Liabilities to Revenue

Examples Include: Airline Ticket Sales Sports Teams’ Sales of Season Tickets

Converting Liabilities to Revenue

$6,000 Rental Contract Coverage for 12 Months $500 Monthly Rental Revenue Jan. 1 Dec. 31

GENERAL JOURNAL

Da te Ja n. Account Title s a nd Ex pla na tion 1 Ca sh Une a rne d Re nta l Re ve nue Colle cte d $6,000 in a dva nce for re nt. De bit 6,000 6,000 Cre dit

常见的会计分录英文表达

常见的会计分录英文表达(清楚整理)一、资产类assets现金cash on hand银行存款cash in bank其他货币资金other cash and cash equivalent短期投资short-term investment短期投资跌价准备short-term investments falling price reserve 应收票据notes receivable应收股利dividend receivable应收利息interest receivable应收帐款accounts receivable坏帐准备bad debts reserve预付帐款prepayments / payment in advance应收补贴款cover deficit receivable from state subsidize其他应收款other notes receivable在途物资materials in transit原材料raw materials包装物wrappage低值易耗品low-value consumption goods库存商品finished goods委托加工物资work in process-outsourced委托代销商品trust to and sell the goods on a commission basis受托代销商品commissioned and sell the goods on a commission basis存货跌价准备inventory falling price reserve分期收款发出商品collect money and send out the goods by stages 待摊费用deferred and prepaid expenses长期股权投资long-term investment on stocks长期债权投资long-term investment on bonds长期投资减值准备long-term investment depreciation reserve固定资产fixed assets累计折旧accumulated depreciation工程物资project goods and material在建工程project under construction固定资产清理fixed assets disposal无形资产intangible assets开办费organization/preliminary expenses长期待摊费用long-term deferred and prepaid expenses待处理财产损溢wait deal assets loss or income二、负债类debts短期借款short-term loan应付票据notes payable应付帐款accounts payable预收帐款advance payment代销商品款consignor payable应付工资accrued payroll应付福利费accrued welfarism应付股利dividends payable应交税金tax payable其他应交款accrued other payments其他应付款other payable预提费用drawing expenses in advance 长期借款long-term loan应付债券debenture payable长期应付款long-term payable递延税款deferred tax住房周转金revolving fund of house三、所有者权益owners equity股本paid-up stock资本公积capital reserve盈余公积surplus reserve本年利润current year profit利润分配profit distribution四、成本类cost生产成本cost of manufacture制造费用manufacturing overhead,五、损益类profit and loss (p/l)主营业务收入prime operating revenue其他业务收入other operating revenue折扣与折让discount and allowance投资收益investment income补贴收入subsidize revenue营业外收入non-operating income主营业务成本operating cost主营业务税金及附加tax and associate charge其他业务支出other operating expenses存货跌价损失inventory falling price loss营业费用operating expenses管理费用general and administrative expenses 财务费用financial expenses营业外支出non-operating expenditure所得税income tax以前年度损益调整adjusted p/l for prior year资产+费用=负责+所有者权益+收入财务三大主表:资产负债表、利润表(权益表)、现金流量表Account 帐chart of account 会计科目表credit 借方debit 贷方journal 日记帐ledger 分类帐posting 过帐trial balance 试算平衡表Accounting system 会计系统Audit 审计accrual-basis accounting 权责发生制会计accrued expense 应计费用accrued revenue 应计收入accumulated depreciation 累计折旧Balance sheet 资产负债表Income statement 损益表Statement of cash flow 现金流量表感谢下载!欢迎您的下载,资料仅供参考。

会计分录中英文试题及答案

1,从银行提取现金8000元,以备发放本月工资。

From the bank to withdraw cash from a 8000$, for issuing this month salary.借:库存现金8000贷:银行存款8000借:应付职工薪酬8000贷:库存现金80002,从银行借入期限三月贷款100000元,存入银行From the bank loan period march a loan of 100000 RMB, the bank2、借:银行存款100000贷:短期贷款1000003,企业购入设备一台,买价24000元,包装费300元,运输费700元,不需安装,直接交付使用。

Enterprise purchase equipment one, purchase price is 24000 yuan, packing charge 300 yuan, shipping cost is 700 yuan, do not need to install, direct delivery and use.借:固定资产25000贷:银行存款250004,购入乙材料8000千克,每千克0.5元,运杂费40元,税款及运费以银行存款支付,材料尚未到。

Buy b material 8000 kg, 0.5 yuan per kg, carry forty yuan, tax and freight to bank deposit payment, material not to.借:材料采购—乙材料4040应交税金—应交增值税(进项税额) 680贷:银行存款47205,上述乙采购验收入库。

The above b procurement check incoming.借:原材料—乙材料4040贷:材料采购—乙材料40406,计提固定资产折旧,车间使用的固定资产折旧1400元,厂部使用设备折旧800元。

会计英语分录知识点汇总

会计英语分录知识点汇总会计英语分录(Accounting Entries)是财务会计中重要的内容,它是记录和传递经济交易信息的基础。

在日常的财务工作中,掌握会计英语分录知识点至关重要。

在本文中,我们将对会计英语分录的相关知识进行汇总和总结,帮助读者更好地理解和应用。

一、会计的基本原理会计的基本原理是财务会计工作的根本基础。

主要包括会计等式(Accounting Equation)和货币计量性原则(Monetary Measurement Principle)。

1. 会计等式会计等式是财务会计中一个基本原理,用于描述资产、负债和所有者权益之间的关系。

其公式为:资产 = 负债 + 所有者权益。

在会计分录中,会计等式的平衡意味着每个交易都必须对应两个或更多的账户。

2. 货币计量性原则货币计量性原则要求所有会计交易必须以货币的形式进行记录和报告。

这意味着会计分录中所有的金额都必须以货币单位来表示,方便比较和分类。

二、会计分录的基本要素会计分录通常包括四个基本要素,即账户(Account)、借方(Debit)、贷方(Credit)和金额(Amount)。

1. 账户账户是会计中用来记录交易和事项的基本单位。

例如,现金账户、应收账款账户等。

会计分录中的每个项都要与相应的账户进行关联。

2. 借方和贷方借方和贷方是会计分录中用来表示金额增减方向的基本要素。

借方表示资产和费用的增加,负债和所有者权益的减少;贷方表示资产和费用的减少,负债和所有者权益的增加。

3. 金额金额是会计分录中表示交易数值的要素。

它可以是正数或负数,分别表示借方金额和贷方金额。

借方金额和贷方金额的数值必须相等,以保持会计等式的平衡。

三、常见的会计分录类型1. 现金收入当企业收到现金时,会计分录为:借方现金账户,贷方收入账户。

2. 货物销售当企业销售货物时,会计分录为:借方应收账款账户,贷方销售收入账户。

3. 货物采购当企业采购货物时,会计分录为:借方库存账户,贷方应付账款账户。

英文版会计分录

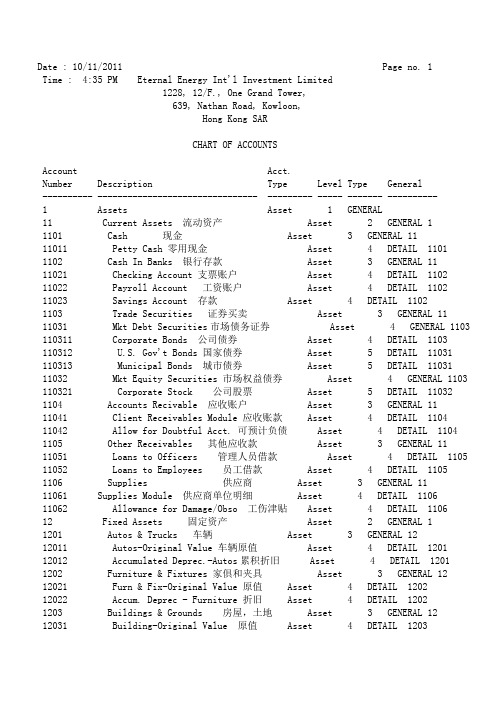

Date : 10/11/2011 Page no. 1Time : 4:35 PM Eternal Energy Int'l Investment Limited1228, 12/F., One Grand Tower,639, Nathan Road, Kowloon,Hong Kong SARCHART OF ACCOUNTSAccount Acct.Number Description Type Level Type General---------- -------------------------------- --------- ----- ------- ----------1 Assets Asset 1 GENERAL11 Current Assets 流动资产 Asset 2 GENERAL 11101 Cash 现金 Asset 3 GENERAL 1111011 Petty Cash 零用现金 Asset 4 DETAIL 11011102 Cash In Banks 银行存款 Asset 3 GENERAL 1111021 Checking Account 支票账户 Asset 4 DETAIL 110211022 Payroll Account 工资账户 Asset 4 DETAIL 110211023 Savings Account 存款 Asset 4 DETAIL 11021103 Trade Securities 证券买卖 Asset 3 GENERAL 11 11031 Mkt Debt Securities市场债务证券 Asset 4 GENERAL 1103 110311 Corporate Bonds 公司债券 Asset 4 DETAIL 1103110312 U.S. Gov't Bonds 国家债券 Asset 5 DETAIL 11031110313 Municipal Bonds 城市债券 Asset 5 DETAIL 1103111032 Mkt Equity Securities 市场权益债券 Asset 4 GENERAL 1103 110321 Corporate Stock 公司股票 Asset 5 DETAIL 110321104 Accounts Recivable 应收账户 Asset 3 GENERAL 1111041 Client Receivables Module 应收账款 Asset 4 DETAIL 110411042 Allow for Doubtful Acct. 可预计负债 Asset 4 DETAIL 1104 1105 Other Receivables 其他应收款 Asset 3 GENERAL 11 11051 Loans to Officers 管理人员借款 Asset 4 DETAIL 1105 11052 Loans to Employees 员工借款 Asset 4 DETAIL 11051106 Supplies 供应商 Asset 3 GENERAL 1111061 Supplies Module 供应商单位明细 Asset 4 DETAIL 110611062 Allowance for Damage/Obso 工伤津贴 Asset 4 DETAIL 110612 Fixed Assets 固定资产 Asset 2 GENERAL 11201 Autos & Trucks 车辆 Asset 3 GENERAL 1212011 Autos-Original Value 车辆原值 Asset 4 DETAIL 120112012 Accumulated Deprec.-Autos累积折旧 Asset 4 DETAIL 12011202 Furniture & Fixtures 家俱和夹具 Asset 3 GENERAL 12 12021 Furn & Fix-Original Value 原值 Asset 4 DETAIL 120212022 Accum. Deprec - Furniture 折旧 Asset 4 DETAIL 12021203 Buildings & Grounds 房屋,土地 Asset 3 GENERAL 1212031 Building-Original Value 原值 Asset 4 DETAIL 120312032 Accum. Deprec. - Building 折旧 Asset 4 DETAIL 12031204 Office Equipment 办公设备 Asset 3 GENERAL 1212041 Off. Equip-Original Value 办公设备原值 Asset 4 DETAIL 1204 12042 Accum Deprec-Office Equip 折旧 Asset 4 DETAIL 12041205 Other Assets 其他资产 Asset 3 GENERAL 1212051 Other Assets Org. Value 其他资产原值 Asset 4 DETAIL 1205 12052 Accum Deprec-Other Assets 折旧 Asset 4 DETAIL 120513 Deferred Assets 递延资产 Asset 2 GENERAL 11301 Leasehold Improvements 融资租赁设备 Asset 3 GENERAL 13 13011 Orig Value -Lease Improve 原值 Asset 4 DETAIL 130113012 Accum. Deprec. - Lease 折旧 Asset 4 DETAIL 13011302 Organization Expenses 开办费 Asset 3 GENERAL 1313021 Original Value - Org Exp. 开办费原值 Asset 4 DETAIL 1302 13022 Accum. Amort - Org Exp. 开办费摊销 Asset 4 DETAIL 1302 1303 Prepaid Expenses 预付费用 Asset 3 GENERAL 1313031 Prepaid Insurance 预付保险费 Asset 4 DETAIL 1303 13032 Prepaid Rent 预付租金 Asset 4 DETAIL 130313033 Prepaid Interest 预付利息 Asset 4 DETAIL 130313034 Prepaid Taxes 预付税费 Asset 4 DETAIL 130314 Other Assets 其他资金 Asset 2 GENERAL 11401 Deposits 存款 Asset 3 GENERAL 14Date : 10/11/2011 Page no. 2Time : 4:35 PM Eternal Energy Int'l Investment Limited1228, 12/F., One Grand Tower,639, Nathan Road, Kowloon,Hong Kong SARCHART OF ACCOUNTSAccount Acct.Number Description Type Level Type General---------- -------------------------------- --------- ----- ------- ----------14011 Rent Deposit 房租收入 Asset 4 DETAIL 140114012 Lease Deposit 租赁款 Asset 4 DETAIL 140114013 Utilities Deposit 国债 Asset 4 DETAIL 140114014 Security Deposit 证券收入 Asset 4 DETAIL 14011402 Invest. Held to Maturity 长期证券投资 Asset 3 GENERAL 14 14021 Certificate Of Deposit 信用证 Asset 4 DETAIL 140214022 Lng Term Debt Security 长期债权投资 Asset 4 DETAIL 1402 14023 Lng Term Equity Security 长期股权投资 Asset 4 DETAIL 1402 2 Liabilities 负债 Liability 1 GENERAL21 Short Term Liabilities 短期负债 Liability 2 GENERAL 22101 Accounts Payable 应付账款 Liability 3 GENERAL 2121011 Accounts Payable - Vendor 供应商 Liability 4 DETAIL 210121012 American Express 美国邮政 Liability 4 DETAIL 210121013 Master Card 信用卡 Liability 4 DETAIL 210121014 Shareholder Loan-Hareward 股东借款 Liability 4 DETAIL 21012102 Clients Escrow 预付账款 Liability 3 DETAIL 212103 Payroll Liabilities 应付职工薪酬 Liability 3 GENERAL 21 21031 Disability Insurance Liab 工伤保险 Liability 4 DETAIL 210321032 Health Insurance Liab. 健康保险 Liability 4 DETAIL 210321033 Dental Insurance Liab.牙科保险 Liability 4 DETAIL 210321034 Cafeteria Plan Liab. 失业保险 Liability 4 DETAIL 210321035 401 (K) Liab. Liability 4 DETAIL 210321036 Profit Sharing Liab. 应付职工利益 Liability 4 DETAIL 2103 21037 Pension Plan Liab. 应付福利费 Liability 4 DETAIL 2103 2104 Taxes Payable 应付税费 Liability 3 GENERAL 2121041 Payroll Taxes Payable 消费税 Liability 4 GENERAL 2104210411 Federal Payroll Taxes 个人所得税 Liability 5 DETAIL 21041 210412 State Payroll Tax W/Held 国家征收个人所得 Liability 5 DETAIL 21041210413 Local Payroll Tax W/Held 地方征收个人所得 Liability 5 DETAIL 21041 210414 FUTA 失业税 Liability 5 DETAIL 21041210415 SUI 水污染税 Liability 5 DETAIL 21041210416 SDI 土壤污染税 Liability 5 DETAIL 21041 21042 Sales Tax Payable 营业税 Liability 4 GENERAL 2104210421 State Sales Tax Payable 应交国家营业税 Liability 5 DETAIL 21042 210422 County Sales Tax Payable 应交州际营业税 Liability 5 DETAIL 21042210423 City Sales Tax Payable应交城市营业税 Liability 5 DETAIL 21042 210424 Other Sales Tax Payable 应交其他营业税 Liability 5 DETAIL 2104221043 Income/Property Tax 所得税 Liability 4 GENERAL 2104210431 Federal Income Tax 国家所得税 Liability 5 DETAIL 21043 210432 State Income Tax 州所得税 Liability 5 DETAIL 21043210433 Local Income Tax 应交所在地所得税 Liability 5 DETAIL 21043210434 Franchise Tax特许经营所得税 Liability 5 DETAIL 21043210435 Property Tax 财产所得税 Liability 5 DETAIL 210432105 Accrued Liabilities 应计负债 Liability 3 GENERAL 2121051 Accrued Rent 应付租金 Liability 4 DETAIL 210521052 Accrued Commissions应付佣金 Liability 4 DETAIL 210521053 Accrued Salaries 工资 Liability 4 DETAIL 210521054 Accrued Hourly 时薪 Liability 4 DETAIL 21052106 Other Current Liabilities 其他流动负债 Liability 3 GENERAL 2121061 Dividend Payable 股利支付 Liability 4 DETAIL 210622 Long Term Liabilities 长期负债 Liability 2 GENERAL 22201 Notes Payable 应付票据 Liability 3 DETAIL 222202 Mortgage Payable 按歇付款 Liability 3 DETAIL 2223 Deferred Liabilities 递延负债 Liability 2 GENERAL 2Date : 10/11/2011 Page no. 3Time : 4:35 PM Eternal Energy Int'l Investment Limited1228, 12/F., One Grand Tower,639, Nathan Road, Kowloon,Hong Kong SARCHART OF ACCOUNTSAccount Acct.Number Description Type Level Type General---------- -------------------------------- --------- ----- ------- ----------2301 Deferred Income 递延收入 Liability 3 DETAIL 232302 Reserve For Contingency 储备应急款 Liability 3 DETAIL 23 2303 Unearned Interest 预计利息 Liability 3 DETAIL 233 Stockholders Equity 股东股权 Capital 1 GENERAL31 Capital Stock 股本 Capital 2 GENERAL 33101 Preferred Stock 优先股 Capital 3 GENERAL 3131011 Par Value 原值 Capital 4 DETAIL 310131012 Paid In Excess Of Par 溢价 Capital 4 DETAIL 31013102 Common Stock 普通股 Capital 3 GENERAL 3131021 Par Value 原值 Capital 4 DETAIL 310231022 Paid In Excess Of Par 溢价 Capital 4 DETAIL 310232 Retained Earnings 留存收益 Capital 2 GENERAL 33200 2000 Profit/Loss 收益/损失 Capital 3 DETAIL 32 3201 2001 Profit/Loss 收益/损失 Capital 3 DETAIL 323202 2002 Profit/Loss 收益/损失 Capital 3 DETAIL 32 3203 2003 Profit/Loss收益/损失 Capital 3 DETAIL 3233 Current Earnings 本期盈余 Capital 2 DETAIL 34 Revenues 收入 Revenue 1 GENERAL41 Client Revenue 主营业务收入 Revenue 2 GENERAL 4 4101 Client Services 1客户1 Revenue 3 DETAIL 414102 Client Services 2客户2 Revenue 3 DETAIL 414103 Client Services 3客户3 Revenue 3 DETAIL 4142 Return: Client Services 劳务报酬 Revenue 2 GENERAL 44201 Return: Client Services 1 客户1 Revenue 3 DETAIL 424202 Return: Client Services 2客户2 Revenue 3 DETAIL 424203 Return: Client Services 3客户3 Revenue 3 DETAIL 4243 Financial Income 财务收入 Revenue 2 GENERAL 44301 Interest From Investments 投资利息 Revenue 3 DETAIL 434302 Dividends From Investment投资回报 Revenue 3 DETAIL 434303 Finance Charges 财务费用 Revenue 3 DETAIL 434304 Purchase Discounts 折扣 Revenue 3 DETAIL 434305 Sales Discount Taken 销售折扣 Revenue 3 DETAIL 4344 Other Income 其他收入 Revenue 2 GENERAL 44401 Recovery of Bad Debt 收回坏账 Revenue 3 DETAIL 444402 Gain on Sale of Asset 出售固定资产收入 Revenue 3 DETAIL 44 45 Shipping Revenues 运费收入 Revenue 2 GENERAL 44501 Freight Revenue 货运收入 Revenue 3 DETAIL 454502 Insurance Revenue 保险收入 Revenue 3 DETAIL 454503 Packaging Revenue 包装收入 Revenue 3 DETAIL 455 Total Expenses 总费用 Expense 1 GENERAL51 Special Client Expenses特殊客户费用 Expense 2 GENERAL 5 5101 Special Client 1 Expenses特殊客户 Expense 3 DETAIL 515102 Special Client 2 Expenses特殊客户 Expense 3 DETAIL 515103 Special Client 3 Expenses特殊客户 Expense 3 DETAIL 515150 Shipping Expenses 运费 Expense 3 GENERAL 5151501 Freight Expense 货运费 Expense 4 DETAIL 515051502 Insurance Expense保险费 Expense 4 DETAIL 515051503 Packaging Expense 包装费 Expense 4 DETAIL 515052 General & Admin. Expenses 一般管理费用 Expense 2 GENERAL 5 5201 Payroll Expense 工资费用 Expense 3 GENERAL 5252011 Wages 工资费用 Expense 4 GENERAL 5201520111 Salaries 年薪 Expense 5 DETAIL 52011520112 Hourly 时薪 Expense 5 DETAIL 52011520113 Overtime 加班费 Expense 5 DETAIL 52011Date : 10/11/2011 Page no. 4Time : 4:35 PM Eternal Energy Int'l Investment Limited1228, 12/F., One Grand Tower,639, Nathan Road, Kowloon,Hong Kong SARCHART OF ACCOUNTSAccount Acct.Number Description Type Level Type General---------- -------------------------------- --------- ----- ------- ----------520114 Bonuses 奖金 Expense 5 DETAIL 52011520115 Contract Labor 劳务承包费 Expense 5 DETAIL 52011 520116 Direct Labor 劳务工资 Expense 5 DETAIL 5201152012 Co. Sponsored Benifits 赞助支出 Expense 4 GENERAL 5201520121 Health Insurance 医疗保险 Expense 5 DETAIL 52012520122 Dental Insurance 牙科保险 Expense 5 DETAIL 52012520123 401(k) Plan Expense 5 DETAIL 5201252013 Payroll Taxes 个人所得税 Expense 4 GENERAL 5201 520131 FICA Employer 雇佣支出 Expense 5 DETAIL 52013520132 FUTA 失业税 Expense 5 DETAIL 52013520133 SUTA 失业保险 Expense 5 DETAIL 52013520134 Disability Insurance 工伤保险 Expense 5 DETAIL 520135202 Maintenance 维护费 Expense 3 GENERAL 5252021 Autos & Trucks Maint. 车辆 Expense 4 DETAIL 520252022 Furn. & Fixtures Maint.家俱与夹具 Expense 4 DETAIL 5202 52023 Buildings & Grounds Maint房屋与土地 Expense 4 DETAIL 5202 52025 Office Equipment Maint.办公设备 Expense 4 DETAIL 520252026 Other Maintenance 其他维护 Expense 4 DETAIL 52025203 Depreciation 折旧 Expense 3 GENERAL 5252031 Autos & Trucks Depr.车辆折旧 Expense 4 DETAIL 520352032 Furniture & Fixtures Depr 家俱与夹具折旧 Expense 4 DETAIL 5203 52033 Buildings & Grounds Depr. 房屋与土地折旧 Expense 4 DETAIL 5203 52035 Office Equipment Depr.办公设备折旧 Expense 4 DETAIL 5203 52036 Other Asset Depr.其他资产折旧 Expense 4 DETAIL 5203 5204 Amortization 摊销费用 Expense 3 GENERAL 52 52041 Leasehold Improvements 租赁改良费用 Expense 4 DETAIL 5204 52042 Organization Expense 开办费用 Expense 4 DETAIL 52045205 Rents & Leases 租金和租赁 Expense 3 GENERAL 52 52051 Vehicle Lease 车辆租赁 Expense 4 DETAIL 520552052 Furn.& Fixtures Lease 家俱与夹具租赁 Expense 4 DETAIL 5205 52053 Building Lease 房屋租赁 Expense 4 DETAIL 520552055 Office Equipment Lease 办公设备租赁 Expense 4 DETAIL 5205 52056 Other Equipment Lease其他设备租赁 Expense 4 DETAIL 5205 5206 Insurance 保险 Expense 3 GENERAL 5252061 Autos & Trucks Insurance 车辆保险 Expense 4 DETAIL 520652062 Gnrl Business Insurance 通用设备商业保险 Expense 4 DETAIL 5206 52063 Other Insurance 其他保险 Expense 4 DETAIL 52065207 Travel & Entertainment 旅差及招待费 Expense 3 GENERAL 52 52071 Lodging 住宿费 Expense 4 DETAIL 520752072 Transportation 车费 Expense 4 DETAIL 520752073 Meals 餐费 Expense 4 DETAIL 520752074 Entertainment 接待费 Expense 4 DETAIL 52075208 Shipping 航运费 Expense 3 GENERAL 5252081 Local Courier 国内快递 Expense 4 DETAIL 520852082 Federal Express 联邦快递 Expense 4 DETAIL 520852083 UPS UPS快递 Expense 4 DETAIL 52085210 Consulting Fees 顾问费 Expense 3 GENERAL 5252101 Accounting Consulting Fee 会计顾问费 Expense 4 DETAIL 5210 52103 Legal 律师费 Expense 4 DETAIL 521052104 Computer Consultant 电脑顾问费 Expense 4 DETAIL 5210 5211 Overhead Expenses 治安费 Expense 3 GENERAL 5252111 Office Supplies 办公用品 Expense 4 DETAIL 521152112 Telephone & Telegraph 电讯费 Expense 4 DETAIL 521152113 Mail/Postage 邮递费 Expense 4 DETAIL 5211Date : 10/11/2011 Page no. 5Time : 4:35 PM Eternal Energy Int'l Investment Limited1228, 12/F., One Grand Tower,639, Nathan Road, Kowloon,Hong Kong SARCHART OF ACCOUNTSAccount Acct.Number Description Type Level Type General---------- -------------------------------- --------- ----- ------- ----------52114 Utilities 公用事业费 Expense 4 DETAIL 5211 52115 Answering Service 服务费 Expense 4 DETAIL 521152116 Licenses / Permits牌照许可证费 Expense 4 DETAIL 5211 52117 Magazine Subcriptions 书报费 Expense 4 DETAIL 521152118 Cleaning Service 清洁费 Expense 4 DETAIL 52115212 Miscellaneous Expenses 杂费 Expense 3 DETAIL 525213 Other Taxes 其他税 Expense 3 GENERAL 5252131 Purchases Sales Tax 进项税 Expense 4 DETAIL 521352132 Property Tax 财产税 Expense 4 DETAIL 521352133 Franchise Tax 特许经营税 Expense 4 DETAIL 5213 5214 Continued Education继续教育费 Expense 3 GENERAL 52 52141 Continued Education 继续教育费 Expense 4 DETAIL 5214 5215 Advertising 广告费 Expense 3 GENERAL 5252151 Acct. Referal Service 证照审计费 Expense 4 DETAIL 5215 52152 Yellow Page Ad 黄页广告费 Expense 4 DETAIL 521552153 Other Advertising 其他广告费 Expense 4 DETAIL 5215 53 Financial Expenses 财务费用 Expense 2 GENERAL 55301 Credit Card Discount 信用卡折扣 Expense 3 DETAIL 53 5302 Interest 利息 Expense 3 DETAIL 535303 Bank Charges 银行费用 Expense 3 DETAIL 535305 Loss on Sale/Assets 销售白点 Expense 3 DETAIL 5354 Income Tax 所得税 Expense 2 GENERAL 55401 Federal Income Tax 应交国家 Expense 3 DETAIL 545402 State Income Tax 应交州 Expense 3 DETAIL 545403 City Income Tax 应交所在地 Expense 3 DETAIL 54 D Journal Difference 期间差异 Other Dr 1 DETAIL。

常见的会计分录英文表达

常见的会计分录英⽂表达常见的会计分录英⽂表达(清楚整理)⼀、资产类 assets现⾦ cash on hand银⾏存款 cash in bank其他货币资⾦ other cash and cash equivalent短期投资 short-term investment短期投资跌价准备 short-term investments falling price reserve 应收票据 notes receivable应收股利 dividend receivable应收利息 interest receivable应收帐款 accounts receivable坏帐准备 bad debts reserve预付帐款prepayments / payment in advance应收补贴款 cover deficit receivable from state subsidize其他应收款 other notes receivable在途物资 materials in transit原材料 raw materials包装物 wrappage低值易耗品 low-value consumption goods库存商品 finished goods委托加⼯物资 work in process-outsourced委托代销商品 trust to and sell the goods on a commission basis 受托代销商品 commissioned and sell the goods on a commission basis 存货跌价准备 inventory falling price reserve分期收款发出商品 collect money and send out the goods by stages 待摊费⽤ deferred and prepaid expenses长期股权投资 long-term investment on stocks长期债权投资 long-term investment on bonds长期投资减值准备 long-term investment depreciation reserve固定资产 fixed assets累计折旧 accumulated depreciation⼯程物资 project goods and material在建⼯程 project under construction固定资产清理 fixed assets disposal⽆形资产 intangible assets开办费 organization/preliminary expenses长期待摊费⽤ long-term deferred and prepaid expenses待处理财产损溢 wait deal assets loss or income ⼆、负债类 debts短期借款 short-term loan应付票据 notes payable应付帐款 accounts payable预收帐款 advance payment代销商品款 consignor payable应付⼯资 accrued payroll应付福利费 accrued welfarism应付股利 dividends payable应交税⾦ tax payable其他应交款 accrued other payments其他应付款 other payable预提费⽤ drawing expenses in advance长期借款 long-term loan应付债券 debenture payable长期应付款 long-term payable递延税款 deferred tax住房周转⾦ revolving fund of house三、所有者权益 owners equity股本 paid-up stock资本公积 capital reserve盈余公积 surplus reserve本年利润 current year profit利润分配 profit distribution四、成本类 cost⽣产成本 cost of manufacture制造费⽤manufacturing overhead,五、损益类 profit and loss (p/l)主营业务收⼊ prime operating revenue其他业务收⼊ other operating revenue折扣与折让 discount and allowance投资收益 investment income补贴收⼊ subsidize revenue营业外收⼊ non-operating income主营业务成本 operating cost主营业务税⾦及附加 tax and associate charge 其他业务⽀出 other operating expenses存货跌价损失 inventory falling price loss 营业费⽤ operating expenses管理费⽤ general and administrative expenses财务费⽤ financial expenses营业外⽀出 non-operating expenditure所得税 income tax以前年度损益调整 adjusted p/l for prior year资产+费⽤=负责+所有者权益+收⼊财务三⼤主表:资产负债表、利润表(权益表)、现⾦流量表Account 帐chart of account 会计科⽬表credit 借⽅ debit 贷⽅journal ⽇记帐 ledger 分类帐posting 过帐trial balance 试算平衡表Accounting system 会计系统Audit 审计accrual-basis accounting 权责发⽣制会计accrued expense 应计费⽤accrued revenue 应计收⼊accumulated depreciation 累计折旧Balance sheet 资产负债表Income statement 损益表Statement of cash flow 现⾦流量表(注:表格素材和资料部分来⾃⽹络,供参考。

财务英语会计分录

财务英语会计分录筹建阶段Get investmentProprietorship and PartnershipDr CashCr XXX’s capitalCompanyDr CashCr Common stock/Preferred stock (face value)Additional paid-in capitalBuy office furniture/equipment/office suppliesDr Furniture/Supplies/EquipmentCr cashFor merchandise business, purchase merchandiseDr PurchasesCr CashFor manufacturing business, purchase materialDr Material inventoryCr Cash运营阶段主要活动For service business, provide serviceDr CashCr Fees earned/Fees incomeFor merchandise business, send merchandise to customer Dr CashCr Sales/Sales revenueDr Cost of goods soldCr InventoryFor manufacturing business, from production to selling Dr Work in process inventoryCr Material inventoryDr Work in process inventoryCr Wages payableDr Work in process inventoryCr Overhead costDr Finished goods inventoryCr Work in process inventoryDr CashCr Sales/Sales revenueDr Cost of goods soldCr Finished goods inventory日常活动一、Receivables1. SalesSales on account/credit; receive from the client a promise of pay service/merchandise/product Dr Accounts receivable Cr fees income/sales revenueCustomer issue a note to replace the debtDr Notes receivableCr Accounts receivable2. Account for bad debtsAccountant recognize that there is XXX accounts receivable cannot be collected(direct write off ) Dr Bad debt expense Cr Accounts receivableAccountant estimate x% of accounts receivable cannot be collected every period(allowance method)Dr Bad debt expenseCr Allowance for bad debtAs the actual loss of XXX is recognizedDr Allowance for bad debtCr Accounts receivable3. On the maturity date of notesDr CashCr Notes receivableInterest income二、Fixed assets1. Accounting for depreciation(straight-line method, unit of production)Dr Depreciation expenseCr Accumulated depreciation2. Accounting for repairsOrdinary expenditureDr Repairs and Maintenance expenseCr CashCapital expenditureDr XXX(asset title)Cr Cash3. Accounting for impairmentDr Impairment lossDr Accumulated impairment loss4. Sale of used fixed assetBook value= Original cost-accumulated depreciation-accumulated impairment loss Selling price﹤book value, loss Dr CashAccumulated depreciationAccumulated impairment lossLoss on sale of XXXXCr XXXSelling price﹥book value, gain Dr CashAccumulated depreciation Accumulated impairment loss Cr XXXGain on sale of XXX三、Intangible asset AmortizationDr Amortization expenseCr XXX (asset title)四、Bonds payable1. Issue bondOn face valueDr CashCr bonds payableAt a discountDr CashDiscount on bondCr bonds payableAt a premiumDr CashCr bonds payablePremium on bond2. Account for interestOn face valueDr Bond interest expenseCr Cash/interest payableAt a discountDr Bond interest expenseCr cashDiscount on bondAt a premiumDr Bond interest expensePremium on bondCr Cash五、Equity ,disburse income1. Proprietorship and partnershipDr Income summaryCr XXX’s capital2. CompanyDr Income summaryCr retained earningsDr Dividends, Common stock/preferred stock Cr cash/dividend payable六、Other expense and payableDr Advertising expenseCr Advertising payableDr Wages expenseCr Wages payableDr Utilities expenseCr Utilities payableDr Income tax expenseCr Income tax payable七、Prepaid expenseDr Prepaid insurance/rentCr CashDr Insurance expense/rent expenseCr Prepaid insurance/rent沁园春·雪北国风光,千里冰封,万里雪飘。

(财务会计)英文会计分录最全版

(财务会计)英文会计分录accompanyingdocument附件account账户、科目accountpayable应付账款accounttitle/accountingitem会计科目accountingdocument/accountingvoucument 会计凭证accountingelement会计要素accountingentity会计主体accountingentries会计分录accountingequation/accountingidentity 会计恒等式accountingfunction会计职能accountingpostulate会计假设accountingprinciple会计原则accountingreport/accountingstatement 会计报表accountingstandard会计准则accountingtimeperiodconcept会计分期accountsreceivable/receivables应收账款accrual-basisaccounting权责发生制原则accumulateddepreciation累计折旧amortizationexpense/expensenotallocated 待摊费用annualstatement年报ArthurAndersenWorldwide安达信全球assets资产balance余额balancesheet资产负债表begainningbalance/openingbalance 期初余额capital资本capitalexpenditure资本性支出capitalshare股本capitalsurplus资本公积cash现金cashinbank银行存款cashjournal现金日记账cashonhand现金cashsystem(basis)ofaccounting/cash-basisprinci 收付实现制certifiedpracticingaccountant注册会计师comparabilityprinciple可比性原则compoundjournalentry复合分录conservatism(保守)principle/theprudence(稳健)prin谨慎性原则consistencyprinciple 壹贯性原则contingentassets或有资产contingentliabilities 或有负债costaccounting成本会计creditbalance贷方余额creditside贷方currentinvestment 短期投资debitbalance借方余额debitside借方deferredassets递延资产deferredliabilities递延负债DeloitteToucheTohmatsu 德勤depreciablelife折旧年限depreciationexpense折旧费用depreciationrate折旧率descriptions摘要doubleentry复式记账double-entrybook-keeping 复式簿记employeebenefitspayable 应付福利费endingbalance期末余额Ernst&YoungInternational 安永国际estimateldscrapvalue估计残值exchangegain汇兑收益exchangeloss汇兑损失expenses/charges费用factoryoverhead/manufacturingexpense 制造费用financialaccounting财务会计financialexpense财务费用fiscalyear/accountingperiods会计年度fixedassets固定资产floatingassets/currentassets流动资产floatingliabilities/currentliability 流动负债generalledger总分类账going-concernbasis持续运营goodwill商誉historicalcost历史成本historicalcostprinciple历史成本原则:incomestatement/profitandlossstatement 利润表损益表incometax所得税intangibleassets无形资产internationalaccounting国际会计KPMGInternational毕马威国际liabilities负债liabilitydividend/dividendpayable应付股利long-terminvestmentlong-termliabilities长期负债managementaccounting 管理会计managementexpense 管理费用matchingprinciple配比原则materialityprinciple重要性原则monthlystatement月报negativegoodwill负商誉净资产netcost净成本netincome净收益netincomeapportionment 利润分配netproceeds净收入netprofit净利润non-operatinggain营业外收入non-operatinglossnotespayable应付票据notesreceivable/receivables 应收票据objectivity(reliability)principle 客观性原则obligee/creditor债权人Obligor/invester债务人operatingexpense营业费用operatingrevenue营业收入owner'sequity所有者权益periodexpense期间费用perpetualinventorysystem永续盘存制personalproperty动产physicalinventorysystem实地盘存制postingdocument记账凭证prepayments/paymentinadvance 预付款项PriceWaterHouseCoopers普华永道productcost/outputcost生产成本product/finishedgoods产成品profit利润profitaftertax税后利润profitbeforetax税前利润purchase购货purchasereturnandallowances 购货退回和折让quarterlystatement季报rawmaterials原材料realestate不动产relevanceprinciple相关性原则reserveforbaddebts/baddebtsexpense/provisi 坏帐准备residual(salvage)value折余价值(残值)retainsearning留存收益revenueexpenditure收益性支出revenues收入salesallowances 销货折让salesdiscount 销货折扣salesinvoice销货发票salesonaccount 赊销salesreturn销售退回salesrevenue 销售收入sellingcost销售成本sellingexpense销售费用simpleournalentry简单分录sourcedocument原始凭证stable-monetaryconcept货币计量starting-loadcost/organizationcosts开办费statementofcashflow/cashflowstatement 现金流量表stockonhand/inventory存货stub存根subsidiaryaccounts 明细账户subsidiaryledger 明细分类账surplusreserve盈余公积T-account/transfer T字形账户tangibleassets有形资产taxespayable应交税金theunderstandabilityprinciple明晰性原则timeliness及时性原则transaction交易travelingexpense差旅费trialbalance试算平衡undistributedprofits/undividedprofits 未分配利润unearnedrevenue预收款项unrelatedbusinessincome营业外收益usefullife使用年限valueaddedtax增值税voucher付款凭证wagespayable/salariespayable 应付工资workinprocess/goodsinprocess在产品。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

专业英语会计分录

Company Document number:WTUT-WT88Y-W8BBGB-BWYTT-19998

专业英语分录练习

1. The owner of Johnson company, Mr. Deep and his friends, invested 75 000 in cash, Land valuing 50 000 and Equipment A valuing 73 000 into the company.

Dr. Cash

Land

Equipment A

Cr. Capital

2. Johnson Company receive a long-term bank loan of 60 000. The bank agreed to lend the money to it for 3 years with the annual interest rate of 12% and the interest shall be paid annually at the year ends while the principal should be paid back at the end of the third year. How did the company make the entry on Dec. 31

Jan 1 Dr. cash 60 000

Cr. Loan 60 000

Dec 31 Dr. interest expense 600

Interest payable 6600

Cr. Cash 7200

3. Jan 1 Buy the business insurance for one year costing 24 000, the bill has not paid yet. Dr. prepaid insurance/unexpired insurance 24 000

payable 24 000

4. Johnson Company purchased 10 000 raw materials on credit and the supplier agree to collect cash one month later.

Dr. raw materials 10 000

Cr. Account payable 10 000

5 Jan

6 The company bought a company car at 11 000 for cash and cost 1 000 for transportation.

Dr. Car 12000

Cr. Cash 12000