4还价核算表

还价核算表

还 价 核 算 表

填表日期:年月日填表人:编号:

核算规则:还价利润核算时保留2位小数。

还价成本核算时保留4位小数,小于1时保留5位小数,最终得出的单位采购成本保留2位小数。

核算信息:

进口商货物名称装运港

还价利润核算

货号客户还价(US$)计价单位贸易术语还价数量采购成本(¥)核算单位:

计算过程

销售收入总额(¥)

退税收入总额(¥)

采购成本总额(¥)

海洋运费总额(¥)

国内包干费总额(¥)

公司定额费总额(¥)

垫款利息总额(¥)

银行手续费总额(¥)

保险费总额(¥)

佣金总额(¥)

利润总额(¥)

销售利润率。

还 价 核 算 表Shanghai Twin City Trading Co., Ltd

计算 过55程*6. 63*1203* 232/(

采购 成海本洋 运国费内 包公干司 定垫额款 利银息行 手保续险 费佣总金 总额

310* 2138200 *161.060 *71192 07*109.20 08*402.10 68*402.10216 +49628290 .47/8

计算 过程

计算结果

货号

客户还价(US$)

计价单位

贸易术语

还价数量

销售利润率

核算 单

销售 收海入洋 国运内费 包银干行 手续

计算 过程

计算结果

保险 佣费金(¥)

(利¥)润 (采¥)购 成本

/

68777 .28+7 3812 .45/6

计算结果 68777.28 7200

56160 11880

1100 1684.8 865.47 171.94 302.62

3812.45 5.54%

货号

客户还价(US$)

还价采购成本核算

计价单位

贸易术语

还价数量

销售利润率

核算 单

销售 收海入洋 国运内费 包银干行 手保续险 佣费金(¥) (利¥)润 (采¥)购 成本

还价核算表

填表 日 核算 规

核算 信

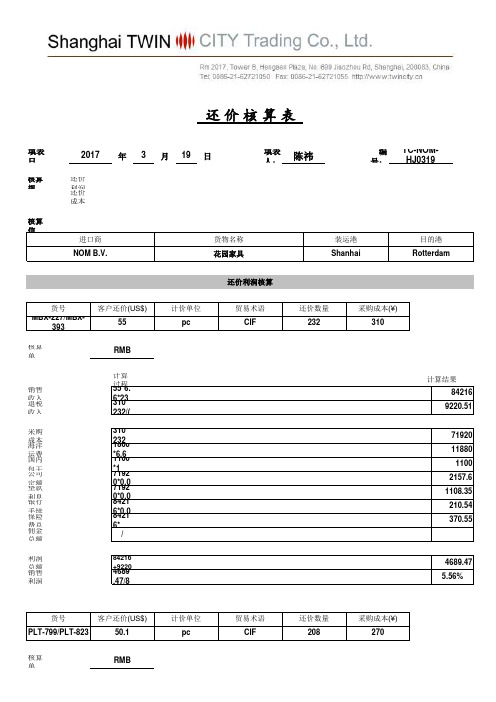

2017

还价 利还润价 成本

年 3 月 19 日

填表 人:

陈祎

编 TC-NOM号: HJ0319

进口商 NOM B.V.

货物名称 花园家具

装运港 Shanhai

目的港 Rotterdam

货号 MBX-227/MBX-

393

客户还价(US$) 55

核算 单

RMB

销售 收退入税 收入

成本核算方法参考表

成本核算方法参考表成本核算方法参考表一、包装类:(包含纸箱、标贴、说明书及胶袋)其标准公式为:材料单价/平方米X 用料面积= 包装产品单价;1、纸箱:是由面纸、坑纸、里纸粘合成纸板,再通过啤机成型出来的;A、纸箱:(长+ 宽+ 5 )X (宽+ 高+ 3 )X 2 /10000X 材料单价/平方米B、内盒(对扣)单价=(宽X 1.7~1.75+高+2)X [(长+宽)X2+2]/10000 X材料单价/平方米C、内盒(直扣)单价=[(宽+2)X 2+高)]X [(长+宽)X2+2]/10000 X材料单价/平方米2、胶袋:是由PE或其它材料薄膜通过封口机封口切割而成;其原始公式为:长X 宽X厚度X材料密度X 材料单价+加工费;3、标贴及说明书都可按其标准公式计算,只是每种材料的单价不一样。

二、五金塑料类:1、机加工类:在灯饰行业中最常用的材料为铁、铝、铜、不锈钢、锌合金及铝合金,因其物理特性不一样而造成其加工及表面处理也不一样,最终导致其成本的核算方法不一样,但成本的构成却是一样的:公式:产品单价=材料成本+ 加工费+表面处理费+工厂管理费、损耗及利润A、铁板及铝板的加工方法:冲压、车削、旋压、拉伸、翻沙、浇铸、压铸;表面处理方式为喷粉、喷漆、喷油、电镀、电泳及氧化;B、冲压、旋压、拉伸一般选用冲床、旋压机及液压机等,其做出的产品一般含有以下几个工序:裁板、落料、成型、整型及机加工详细公式:单价=落料材料费X 材料单价(元/KG)—废料回收费用+机加费用+表在处理费注: a 落料材料费为所实际所投入的材料费用;用公式表示为:(板材价格—落料后所剩废料费用)/ 板材实际落料个数d 废料回收费用为不能再利用的边角料所卖出所得的实际费用c 机加费用为产品通过冲压、旋压、冲孔、整形等工序完成后所产生的费用;e 铝旋压罩圆片的参考公式:落料直径=(上底+下底+斜长)X 2/3C、车削件:是将铝、铜或铁棒通过车床、铣床等设备车削出来的。

出口报价核算及还价核算

出口报价核算一、报价依据出口商品对外报价需根据出口成本、国际市场价格水平,结合企业的经营意图等多方面因素综合考虑,确定合理的价格。

国际市场商品价格千变万化,但通常受商品所固有的价值的影响,所以出口企业的成本,即出口成本就成为报价的基础。

(一)出口成本构成企业的出口成本包括两部分,即商品本身的成本和商品装运出口前的费用,即国内总费用。

商品本身的成本,即生产成本、加工成本和采购成本三种类型。

生产成本:制造商生产某一产品所需的投入。

加工成本:加工商对成品或半成品进行加工所需的成本。

采购成本:贸易商向供应商采购的价格,亦称进货成本。

•o国内总费用包括:国内运输费:出口货物在装运前所发生的境内运输费,通常有卡车运输费、内河运输费、路桥费、过境费及装卸费。

o包装费:包装费用通常包括在采购成本之中,但如果客户对货物的包装有特殊的要求,由此产生的费用就要作为包装费另加。

o仓储费:需要提前采购或另外存仓的货物往往会发生仓储费用。

o认证费:出口商办理出口许可、配额、产地证明其他证明所支付的费用。

o港区港杂费:出口货物在装运前在港区码头所需支付的各种费用。

o商检费:出口商品检验机构根据国家的有关规定或出口商的请求对货物进行检验所发生的费用。

o捐税:国家对出口商品征收、代收或退还的有关税费,通常有出口关税、增值税等。

o贷款利息:出口商由向国内供应商购进货物至从国外买方收到货款期间由于资金的占用而造成的利息损失,也包括出口商给予买方延期付款的利息损失。

o业务费用:出口商在经营中发生的有关费用,如:通讯费、交通费、交际费、广告费等等,又称为经营管理费。

银行费用:出口商委托银行向国外客户收取货款、进行资信调查等所支出的费用。

(二)出口盈亏核算换汇成本的核算。

换汇成本是指某出口商品换回一单位外汇所需的人民币成本。

换言之,即用多少元人民币的“出口成本”可换回单位外币的“净收入外汇”。

其计算公式为:出口换汇成本=出口商品总成本(人民币)÷出口销售外汇净收入(外币)其中,出口商品总成本(退税后)=出口商品购进价(含增值税)+定额费用••出口退税收入•出口外汇净收入为FOB净收入(扣除佣金、运、保费等劳务费用后的外汇净收入)。

还价核算一

1.MF1505:M:0.66*0.37*0.28=0.068立方米25/0.068=367.6 取367箱数量:367*8=2936件单位实际成本=260* ( 1+17%-9%) /( 1+17%) = 240 元/件销售收入= 30.25*2936*8.27=734491.78元实际成本=240*2936=704640元KT100:M:0.432*0.353*0.298=0.0454438立方米25/0.0454438=550.13005取550箱数量:550*3=1650件单位实际成本=180* ( 1+17%-9%) /( 1+17%) =166.1538462元/件销售收入=21.6*1650 *8.27 =294742.8元实际成本=166.1538462*1650=274153.8462元3269N :M:0.334*0.254*0.22=0.0186639立方米25/0.0186639=1339.4842取1339箱数量:1339*5=6695件单位实际成本=48* ( 1+17%-9%) /( 1+17%) =44.30769231元/件销售收入=5.8*6695*8.27=321132.37元实际成本=44.30769231*6695=296640元销售总收入=734491.78+294742.8+321132.37=1350366.95元实际总成本=704640+274153.8462+296640=1275433.846元国内运费:1800元包装费=1.5*(367+550+1339)=3384元出口商检费:200元报关费:250元港区港杂费:800元其它业务费用:1500元海运费=1250*8.27=10337.5元保险费=1350366.95*1.1*0.89%=13220.09244元总利润=销售总收入-实际总成本-费用=1350366.95-1275433.846-1800-3384-200-250-800-1500-10337.5-13220.09244=43 442元利润率=总利润/销售总收入=43442/1350366.95=0.032=3.2%2.M:0.71*0.3*0.38=0.08094立方米25/0.08094=308.8707685 取308箱数量:5*308=1540打单位实际成本=280*(1+17%-9%)/( 1+17%)=258.4615385元/打实际成本=258.4615385*1540=398030.77元销售收入=36.5*1540*8.27=464856.7元国内费用=398030.77*3%=11940.923元佣金=464856.7*4%=18594.268元海运费=2250*8.27=18607.5元利润=464856.7-398030.77-11940.923-18594.268-18607.5=17683.239元利润率=17683.239/464856.7=0.0380402=3.8%所以能达到1.实际成本=230*(1+17%-9%)/(1+17%)*1000=212300元销售收入=32*1000*8.27= 264640元拼箱费=120*8.27=992.4元运费=2800*8.27=23156元佣金=212300*2%=4246元利润=264640-212300-992.4-23156-4246=23945.6元利润率=23945.6/264640=0.09048=9%2.M:0.5*0.5*0.4=0.1立方米20英尺:25/0.1=250箱数量=250*2=500打销售收入=66.5*500*8.27=274978元运费=2800*8.27=23156元利润=销售收入*利润率=274978*5%=13748.9元实际成本=274978-23156-13748.9=238073元单位实际成本=238073/500=476.146元/打40英尺:55/0.1=550箱数量=550*2=1100打销售收入=66.5*1100*8.27=604951元实际成本=476.146*1100=523761元运费=5200*8.27=43004元佣金=604951*2%=12099元利润=604951-523761-43004-12099=26087元利润率=26087/604951=0.04312=4.3%还价核算三1. M:0.71*0.3*0.38=0.08立方米数量= 25/0.08=313箱数量= 313*5=1565打销售收入=36.5*1565*8.27=472403元国内费用=8*1565=12520元佣金=472403*4%=18896元运费=2250*8.27=18608元利润=销售收入*利润率=472403*5%=23620元应供货价=(472403-12520-18896-18608-23620)/1565*(1+17%)/(1+17%-9%)=276.03元降价=280-276.03=3.97元2. FOB价销售收入=303*100*8.27=250581元FOB价利润=250581*6%=15035元单位实际成本=(250581-15035)267948*5%/100=2355.46元/台CFR价销售收入=324*100*8.27=267948元CFR价利润=267948*5%=13397元实际成本=2355.46*100=235546元运费=(267948-13397-235546)/8.27=2290.0美元3.M:0.6*0.3*0.4=0.072立方米W:0.029MT25/0.072=347箱24.5/0.029=845箱所以取347箱数量=347*3=1041打运费=2250*8.27=18608元销售收入=80.6*1041*8.27=693891元利润=693891*4%=27756元购货成本=(销售收入-利润-运费-费用)*(1+增值税率)/(1+增值税率-退税率)=(693891-27756-18608-购货成本*4%)*(1+17%)/(1+17%-9%)所以购货成本=672353元每单位购货成本=672353/1041=645.872元降价=660-645.872=14.128元。

例题——出口价格核算

出口商品价格构成及核算实验的目的与要求:了解进出口业务中出口商进行成本核算的目的和意义,出口商品价格、成本核算的内容以及怎样填制出口商品成本核算单。

重点掌握出口商品价格的构成、成本及费用的计算方法,了解出口商品中税收的比重。

一、出口商品价格的构成出口商品价格的构成为生产成本、费用和利润三大要素。

其中:(一)出口商品的成本包括生产成本、加工成本和采购成本三种类型:1.生产成本:制造商生产某一产品所需的投入.2.加工成本:加工商对成品或半成品进行加工所需的成本。

3.采购成本:贸易商向供应商采购商品的价格,亦称购货成本。

对出口商来说,需要了解的主要是采购成本,成本占的比重最大,因而成为价格中的重要组成部分。

(二)出口商品费用1.直接费用:包装费、仓储费、国内运输费、认证费、港区港杂费、商检费、捐税(出口关税、增值税),出口运费、保险费、佣金2.间接费用:通讯费、交通费、经营管理费等3.银行费用:银行利息、通知费、寄单费、电汇费、改证费国内费用=(1+2+3)国外费用=出口运费、保险费、佣金(直接费用)(三)预期利润二、出口报价核算(顺算法)出口商品价格核算操作要点:出口报价核算有顺算法和逆算法之分,顺算法主要用于成本、费用和利润的叠加以产生正确的报价;而逆算法则是在进口商还价产生之后,用假定收入(进口商还价)减去实际支出(成本、费用)等于利润的原理来核对进口商还价或(出口报价)是否正确无误,出口商有无销售利润,并作出是否成交的最后决定。

(一)成本核算首先购货成本中包括了17%的增值税,而增值税的征收及退还均应根据货物本身的价格(即不含税的价格)而不是购货成本,因此:1。

购货成本购货成本(含税价)=货价(不含税价)+增值税额=货价(不含税价)×(1+ 增值税率)其中:增值税额=货价(不含税价)×增值税率2. 出口退税出口退税额=购货成本(含税价)×出口退税率(1+ 增值税率)=货价(不含税价)×出口退税率实际成本=购货成本-出口退税额(二)国内费用核算(参考国际贸易实务)1.直接费用:包装费、仓储费、国内运输费、认证费、港区港杂费、商检费、捐税(出口关税、增值税),2.间接费用:通讯费、交通费、经营管理费等3.银行费用:银行利息、通知费、寄单费、电汇费、改证费(三)国外费用核算(参考国际贸易实务)1.出口运费核算(1)杂件货物(散货)运费核算以海运为例,杂件货物(散货)海运运费由基本运费和附加运费组成。

还价核算表

2.0196

22.9500 226.22

335932.01

17852.01 4.90%

货号 7018V1&V4

客户还价(US$) 34

核算 单

20'FCL

计价单位 pc

贸易术语 CIF

还价数量 900pcs 1'20FCL

采购成本(¥) 220

销售 收退入税 收入

采购 成海本洋 运国费内 包公干司 定垫额款 利银息行 手保续险 费佣总金 总额

还价核算表

填表 日

核算 规

2010

还价 利还润价 成本

年 9 月 24 日

核算 信

进口商

Flish-man- Hillard Link Park CO.

货物名称 电子钟表

填表 人:

明霞

编 号:

FD-FSHHJ0924

装运港 SHANGHAI

目的港 KUWAIT

货号

7012F2&F3

核算 单

销售 收退入税 收入

10317.23 5.00%

货号 7012F2&F3

客户还价(US$) 21.1

核算 单

销售 收海入洋 国运内费 包银干行 手保续险 佣费金(¥) (利¥)润 (采¥)购 成本

pc

计算 过21程.1 09*060./7 21545060 /2215.15 02*10.1.2 0*11

21.1 0*10 (142. 4250-

36403 81.73805+ 2.01/

计价单位 pc

还价利润核算

贸易术语 CIF

还价数量 2556pcs 1'20FCL

还价核算表模板

5200*50 1500*6.27 900 5200*50*6% 5200*50*10%*(45/360) 948*6.27*50*0.3% 948*6.27*50*110%*0.8% /

297198+13333.33-260000-9405-900-15600-3250-891.59-2615.34 17869.4/297198

63360.00 13200.00

3518.30 10320.34

/

70216.09 5.99%

计算结果 297198.00 13333.33

260000.00 9405.00 900.00

15600.00 3250.00 891.59 2615.34 /

17869.40 6.01%

计算结果

294476.82 13210.26

7477

的港 apore

计算结果 1153441.74 53251.28 1038400.00 9405.00 900.00 62304.00 12980.00 3460.33 10150.29 / 69093.40 5.99%

计算结果 1172765.88 54153.85

1056000.00 9405.00 900.00

还价核算表

填表 日

核算 规

2018

还价 利还润价 成本

年9

核算 信

进口商

Bright Stationery Pte.

月 19 日

填表 人:

货物名称 Inkjet Plotter / Pen Plotter

***

编 号:

装运港 Shanghai

国际贸易实务操作十五个操作的练习答案飞达

国际贸易实务模拟实习学生作业班级学号13姓名吴尉实验一建立业务关系Dear sirs:We have come to know your company from the internet that you wish to buy clocks which made in China.We are very well connected with all the major dealers here of light industrial products, and feel sure we can sell large quantities of Chinese goods if we get your offers at competitive prices. We wish to express our desire to enter into business relationship with you.Please let us have all necessary information regarding your products for export. Located in Shanghai, we take the advantage to set up our solidified production basis in coastal and inland areas. We are a leading company with many years’experience in machinery export business We enjoy a good reputation internationally in the circle of text. A credible sales network has been set up and we have our regular clients from over 100 countries and regions worldwide. In order to acquaint you with the textiles we handle, we take pleasure in sending you by air our latest catalogue for yourHappy to give you a quotation upon receipt of your detailed requirements.We look forward to receiving your enquires soon..Yours faithfully,SHANGHAI FEIDA IMP. &MANAGER实验二出口报价核算由商品资料查询得商品包装方式均为:24只/纸箱运费等级为10 计费标准是M科威特属于波斯湾,查询得包箱费率FCL20'(USD)为2000 增值税为17% 进口关税为80% 所以每个货号的报价数量是169*24=4056只每个货号的国内费用是(1600+1200+100+1100+500+500)/(4056*4)=0.3082(元/只)每个货号的出口运费为:2000*8.25/(4*4056)=1.0170(元/只)货号8130G3含税采购成本:10(元/只)(1)实际成本=采购成本—退税收入=10-10*9%/(1+17%)=9.2308(元/只)(2)国内费用:0.3082(元/只)(3)出口运费:1.0170(元/只)(4)出口报价:CIFC3=(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)*保费率)=(9.2308+0.3082+1.0170)/(1-5%-110%*1%)/8.25=1.53(美元/只)货号7808J1含税采购成本:11(元/只)(1)实际成本=采购成本-退税收入= 11-11*9%/(1+17%)= 10.1538(元/只)(2)国内费用:0.31(元/只)(3)出口运费:1.0170(元/只)(4)出口报价:CIFC3=(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)*保费率)=(10.1538+0.3082+1.0170)/(1-5%-10%-110%*1%)/8.25=1.66(美元/只)货号7808P含税采购成本:8(元/只)(1)实际成本=采购成本-退税收入= 8-8*9%/(1+17%)=7.3846(元/只)(2)国内费用:0.3082(元/只)(3)出口运费:1.0170(元/只)(4)出口报价:CIFC3=(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)*保费率)=(7.3846+0.3082+1.0170)/(1-5%-10%-110%*1%)/8.25=1.26(美元/只)货号8130G2含税采购成本:8.5(元/只)(1)实际成本=采购成本-退税收入= 8.5-8.5*9%/(1+17%)= 7.8462(元/只)(2)国内费用:0.3082(元/只)(3)出口运费:1.0170(元/只)(4)出口报价:CIFC3=(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)*保费率)=(7.8462+0.3082+1.0170)/(1-5%-10%-110%*1%)/8.25=1.33(美元/只)实验三草拟发盘函Dear Sirs,Thank you for your fax of Mar. 7 from which we learn of your interest in our Chang jiang Brand Clock Art No.8130G3,7808J1, 7808P, 8130G2. We are sure that they arewell up to your high standards of quality and service. Hereby, we quote our favorable prices as follows:(1)COMMODITY: CHANG JIANG BRAND CLOCK(2)UNIT PRICE: CIFC5KUWAIT8130G3 US$ 1.53/PC.7808J1 US$ 1.66/PC.7808P US$ 1.26/PC.8130G2 US$ 1.33/PC(3)QUANTITY:169 CARTONS FOR EACH ART NO. TOTAL 676CARTONS IN ONE 20’ FCL CONTAINER(4)PACKING:EACH 24 PCS TO BE PACKED IN ONE CARTON(5)PAYMENT: TO BE PAYABLE BY AN IRREVOCABLE SIGHT LETTER OF CREDIT, FOR FULL CONTRACTVALUE THROUGH A BANK ACCEPTABLE TO THE SELLER.(6)SHIPMENT:FROM SHANGHAI TO KUWAIT TO BE EFFECTED WITHIN 30 DAYS AFTER THE RECEIPTOF THE RELEVANT L/C(7)INSURANCE: TO BE COVERED BY THE SELLER FOR 110% OF THE CONTRACT VALUE AGAINSTALL RISKS AND WAR RISK AS PER DATED 1/1/1981.(8) OTHER CONDITIONS: QUOTATION VALID UNTIL March 19, 2003.Yours faithfully,SHANGHAI FEIDA IMP.& EXP.CO.,LTD.MANAGER实验四出口还价核算1.客户还价后的利润额和利润率:8130G3还价后:1.53*(1-10%)=1.38(美元/只)7808J1还价后:1.66*(1-10%)=1.49(美元/只)7808P还价后:1.26*(1-10%)=1.13(美元/只)8130G2还价后:1.33*(1-10%)=1.20(美元/只)总货款收入=(1.38+1.49+1.13+1.20) *8.25*169*24=174,002.40(元)实际总成本=(10+11+8+8.5)*[1-1/(1+17%)*9%]*169*24=140,400.00(元)业务费用=1600+1200+100+1100+500+500=5,000(元)出口运费=2000*8.25=16,500.00(元)出口保费=174,002.40*110%*1%=1914.0264(元)客户佣金=174,002.40*5%=8700.12(元)总利润额=总货款收入-实际总成本-业务费用-出口运费-出口保费-客户佣金=174,002.40 - 140,400.00 - 5,000 - 16,500.00 1914.0264- 8700.12 =1488.25(元人民币)利润率=1488.25/174,002.40 = 0.86%2. 经客户还价后,出口商应掌握的国内供货价格(含税):=实际成本+退税收入=销售收入-利润-佣金-出口保费-出口运费-国内费用8130G3还价后实际成本1.38*(1-110%*1%-5%-5%)*8.25-0.3082-1.0170=8.796(1元/只)还价后购货成本8.7961/[1-9%/(1+17%)]=9.53(元/只)7808J1还价后实际成本1.49*(1-110%*1%-5%-5%)*8.25-0.3082-1.0170=9.6028(元/只)还价后购货成本9.6028/[1-9%/(1+17%)]=10.40(元/只)7808P还价后实际成本1.13*(1-110%*1%-5%-5%)*8.25-0.3082-1.0170=6.9625(元/只)还价后购货成本6.9625/[1-9%/(1+17%)]=7.54(元/只)8130G3还价后实际成本1.20*(1-110%*1%-5%-5%)*8.25-0.3082-1.0170=7.4759(元/只)还价后购货成本7.4759/[1-9%/(1+17%)]=8.10(元/只)3. 再次报价:8130G3 US$1.53*(1-3%)=US$1.487808J1 US$1.66*(1-3%)=US$1.617808P US$1.26*(1-3%)=US$1.228130G2 US$1.33*(1-3%)=US$1.29实验五拟写还盘函Dear Sirs,We have carefully read your fax dated March 17, 2001.After discussing the matter with our manufacturers, we would gladly inform you that you could get a 3% reduction. Please note that this is a big concession on our part which shows our goodwill and sincerity in establishing business relations between us. You can surely find later that the quality of our products is second to none, and that a 3% reduction is the best you can obtain.By the way, as we are new to each other, your suggestion of D/A at 30 days sight is unacceptable. Maybe after some transactions are successfully executed, you can obtain such favorable payment terms as D/P at sight.Meanwhile we would like to inform you that owing to a recent sharp increase in the cost of labor and materials we would be forced to adjust our price soon. So early reply would be in your interest.Yours faithfully,SHANGHAI FEIDA IMP. & EXP.CO, LTD.MANAGER实验六出口成交核算购货总成本4056*10+4056*11+4056*8+4056*8.5=152100(元)退税收入152100/1.17*0.09=11700(元)合同金额 4056*(1.48+1.61+1.22+1.29)=22713.60(美元)=187387.2(元)出口保险费 187387.2*1.1*0.01=2061.2592(元)客户佣金187387.2*5%=9369.36(元)国内费用 1600+1100+1000+1200+100=5000成交利润额187387.2+11700-152100-16500-2061.2592-9369.36-5000=14056.58(元)成交利润率14056.5808/8.25/22713.60=7.5%实验七出口合同签订Dear sirs,Many thanks for your order and we are sending you our signed Sales Confirmation No.FD-FLESC03 in duplicate. Please counter sign and return one for our file.We will do our best to execute your order and assure the goods’ quality, shipping date as well as the terms you asked for will receive our best attention.As the shipment date is approaching, please immediately instruct your banker to issue the relevant L/C at sight in our favor. The L/C has to reach here as quickly as possible or the shipment may be delayed.Best regards!Yours faithfully,SHANGHAI FEIDA IMP.&EXP.CO.,LTD.MANAGER实验八审核信用证上海飞达进出口有限公司SHANGHAI FEIDA IMP.&EXP. CO., LTD.上海沪闽路100号NO.100 HUMING ROAD SHANGHAI电话(PHONE): 电传(FAX): 审证意见:信用证存在的问题需要修改的理由①国外到期易产生逾期交单②合同号码错误与实际合同号码不符③付款期限不妥超出合同规定期限④商品名称错误与实际出运品名不符⑤一个品种货号有误与实际出运货号不符⑥信用证到期日有误与合同规定不符⑦没有受UCP500约束的文句信用证开立无依据审证人:XXX实验九修改信用证Dear Sirs,We are very glad to receive your L/C No. FLE-FDLC03, but we are quite sorry to find that it contains some discrepancies with the S/C. Please instruct your bank to amend the L/C as quickly as possible.The L/C is to be amended as follows:*The place of expiry: In China, instead of ‘In Kuwait’;*The Number of the S/C:FD-FLESC03, instead of FD-FLE03;*Please amend L/C at 30 days sight to be L/C at sight.*The name of the goods is CHANGJIANG BRAND CLOCK, in stead of ‘CANJIANG BRAND CLOCK’.*The Art NO. should be 8130G2 , instead of ‘8130G’.*The expiry date of the L/C should be JUNE 15TH 2001.*Please add the words “EXCEPT AS OTHERWISE STATED THIS CREDIT IS SUBJECT TO THE UNIFORM CUSTOMS AND PRACTICE FOR DOCUMENTARY CREDITS (1993 REVISION) INTERNATIONAL CHAMBER OF COMMERCE PUBLICATION NO.500.”With best regards!Yours faithfully,SHANGHAI FEIDA IMP.&EXP.CO.,LTD.x x xMANAGER实验十托运订舱相关单据(订舱委托书、商业发票、装箱单)见附件实验十一出口报关相关单据(出口货物报关单、商业发票及装箱单)见附件实验十二投保装船出口货物投保单见附件装船通知:Dear Sirs,We are grateful to inform you that the goods, Changjiang brand clock under S/C No.FD-FLESC03 and L/C No.FLE-FDLC03 have been shipped on S.S. Golden Star V.19 from Shanghai to Kuwait on May 20, 2001 B/L No.FD-FLEBL03.It will arrive at the destination in May 31, 2003.With best regards!Yours faithfully,SHANGHAI FEIDA IMP.&EXP.CO.,LTD.X X XMANAGER实验十三出口单据制作单据种类出单日期年份其他日期汇票 5月27日 2001商业发票 5月9日2001原产地证明 5月16日2001 5月14日(申请)商检证书 5月12日2001保险单据 5月18日2001海运提单 5月20日2001 5月20日(装船)单据见附件实验十四审单操作按照审核单据的要求,对各种单据进行审核;提交单据进行议付。

上海闵华进出口公司TMT作业

班级:国际商务1001 姓名:邢慧敏学号:100604020108 上海闵华- MINHUA IMP.&EXP. CO.LTD. Tea Set and Kitchenware01建交函上海闵华进出口有限公司SHANGHAI MINHUA IMPORT&EXPORT CO.LTDDATE: 02 MARCH, 2001 Dear Miss Suzuki:We know at The Geneva International Fair that you are interested in our 15PC TEA SET. It was a pity that we didn't have the chance to talk with you in detail at that time. Our company is professional in import and export porcelain, products include all kinds of tea, tableware, kitchen utensils, etc. The series can not only be put to daily use but also be kept as collection, and have already met with warm welcome in other Japanese cities .I think it is our mutual benefit to establish business relationship with us, and I am confident you will find a steady demand in Tokyo.We have sent you our catalogue by air-mail and wait for your early inquiry.Best Regards.Yours truly,Shanghai Minhua Imp. & Exp. Co. Ltd×××Sales Manager02出口报价核算⒈商品:15头茶具货号:NF911151)实际成本=采购成本-退税收入=100-100×9%/(1+17%)=92.3077(元/套)2)20英尺集装箱装箱量:25/(0.545×0.285×0.407)=395.4615,取整,395箱报价数量:4×395 =1580(套)3)国内费用:(1000+250+50+1200+1500+2000)/1580=3.7975(元/套)4)出口运费=820×8.25/1580=4.2816(元/套)5)出口报价:FOBC5 =(实际成本+国内费用)/(1-佣金率-预期利润率)=(92.3077+3.7975)/(1-5%-10%)/8.25=13.70(美元/套)CIFC5 =(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)×保费率)=(92.3077+3.7975+4.2816)/(1-5%-10%-110%×1%)/8.25=14.50(美元/套)2.商品:220CC咖啡杯碟货号:NC9041)实际成本=采购成本-退税收入=60-60×9%/(1+17%)=55.3846(元/盒)2)20英尺集装箱装箱量:25/(0.4×0.353×0.332)=533.2947箱,取整,395箱报价数量:8×533 =4264(盒)3)国内费用:(1000+250+50+1200+1500+2000)/4264=1.4071(元/盒) 4)出口运费=820×8.25/4264=1.5865(元/盒)5)出口报价FOBC5 =(实际成本+国内费用)/(1-佣金率-预期利润率)=(55.3846+1.4071)/(1-5%-10%)/8.25=8.10(美元/盒)CIFC5 =(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)×保费率)=(55.3846+1.4071+1.58650/(1-5%-10%-110%×1%)/8.25=8.43(美元/盒)3.商品:16件厨房杂件货号:NY10216/4081)实际成本=采购成本-退税收入=80-80×9%/(1+17%)=73.8462(元/套)2)20英尺集装箱装箱量:25/(0.565×0.35×0.24)=526.7594箱,取整,526箱报价数量:2×526 =1052(套)3)国内费用:(1000+250+50+1200+1500+2000)/4264=5.7034(元/套)4)出口运费=820×8.25/1052=6.4306(元/套)5)出口报价FOBC5=(实际成本+国内费用)/(1-佣金率-预期利润率)=(73.8462+5.7034)/(1-5%-10%)/8.25=11.34(美元/套)CIFC5=(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)×保费率)=(73.8462+5.7034+6.4306)/(1-5%-10%-110%×1%)/8.25 =12.42(美元/套)4.商品:20头餐具货号:NY911201)实际成本=采购成本-退税收入=90-90×9%/(1+17%)=83.0769(元/套)2)20英尺集装箱装箱量:25/(0.565×0.285×0.25)=621.0216箱,取整,621箱报价数量:2×261=1242(套)3)国内费用:(1000+250+50+1200+1500+2000)/1242 =4.8309(元/套)4)出口运费=820×8.25/1242=5.4469(元/套)5)出口报价:FOBC5=(实际成本+国内费用)/(1-佣金率-预期利润率)=(83.0769+4.8309)/(1-5%-10%)/8.25=12.54(美元/套)CIFC5=(实际成本+国内费用+出口运费)/(1-佣金率-预期利润率-(1+加成率)×保费率)=(83.0769+4.8309+5.4469)/(1-5%-10%-110%×1%)/8.25=13.49(美元)03 发盘函上海闵华进出口有限公司SHANGHAI MINHUA IMPORT&EXPORT CO.LTDDATE: 12 MARCH, 2001 Dear Miss Suzuki:Thanks for your prompt reply of March 7th, 2001. We are glad to learn that our commodities have met your need. At your request, we now offer our favorable quotation as follows:Commodity: 15 pc Tea Set 220cc Cup&Saucer,16pc Kitchenware and 20 pc Dinner SetART. NO. : NF91115 NC904 NY10216/408 NH91120 Packing: 1SET/BOX 4BOXES/CARTON 395CTNS/20'FCLHALF DOZ./BOX 8BOXES/CARTON 533CTNS/20'FCL1SET/COLAR BOX 2 BOXES/CARTON 526 CTNS/20'FCL1SET/COLAR BOX 2 BOXES/CARTON 621 CTNS/20'FCL MEASURE : 54.5x28.5x40.7 40x35.3x33.2 56.5x35x2456.5x28.5x25GROSS/NET:19/14.5 KGS 25/23.5 KGS 14/11 KGS20/16.5 KGSPRICE:(CIFC5YOKOHAMA): US$ 14.50/SET US$ 8.43/BOXUS$ 12.42/SET US$ 13.49/SET SHIPMENT: Within 40 days of the receipt of the relevant L/C. PAYMENT: Irrevocable sight L/C in our favor issued by a bank acceptable to the seller for full amount of contract value. Insurance: To be affected against W.P.A., Risk of Clash & Breakage and War Risk for 110% of total invoice value.We hope that you will find the price reasonable, in case you need further information, please contact us without any hesitation.By the way, please be noted that we can only hold this quotation valid for 8 days. Your early reply will be appreciated.Best regards,Yours truly,Shanghai Minhua Imp.&Exp. Co., Ltd.XXXSales manager04出口还价核算1) 利润核算货号NF91115成交金额:13×395×4×8.25=169455.00实际成本:100×395×4×1.08/1.17=145846.1538国内费用:1000+250+50+1200+1500+2000=6000.00海运运费:820×8.25=6765.00保险费用:169455×110%×1%=1864.005客户佣金:169455×5%=8472.75总利润额:169455.00 - 145846.16 - 6000.00 - 6765.00 - 1864.005- 8472.75 =507.09货号NC904成交金额:7.5×533×8×8.25=263835.00实际成本:60×533×8×1.08/1.17=236160.00国内费用:1000+250+50+1200+1500+2000=6000.00海运运费:820×8.25=6765.00保险费用:263835×110%×1%=2902.185客户佣金:263835×5%=13191.75总利润额:263835.00 - 236160.00 - 6000.00 - 6765.00 - 2902.185- 13191.75=-118394(此货号根据客户还价无利润,有亏损)货号NY10216/408成交金额:11.2×526×2×8.25=97204.80实际成本:80×526×2×1.08/1.17=77686.1538国内费用:1000+250+50+1200+1500+2000=6000.00海运运费:820×8.25=6765.00保险费用:97204.80×110%×1%=1069.2528客户佣金:97204.80×5%=4860.24总利润额:97204.80 - 77686.1538 - 6000.00 - 6765.00 - 1069.2528- 4860.24=824.15货号NH91120成交金额:12.2×621×2×8.25=125007.30实际成本:90×621×2×1.08/1.17=103181.5384国内费用:1000+250+50+1200+1500+2000=6000.00海运运费:820×8.25=6765.00保险费用:125007.30×110%×1%=1375.0803客户佣金:125007.30×5%=6250.365总利润额:125007.30 - 103181.53 - 6000.00 - 6765.00 - 1375.0803-6250.365=1435.322) 成本核算货号NF91115的实际成本:[13× (1-5%-8%-110%×1%)-820/1580] ×8.25-6000/1580 =84.0485采购成本:84.0485/1.08×1.17=91.05(元)/套货号NC904的实际成本:[7.5× (1-5%-8%-110%×1%)-820/4264] ×8.25-6000/4264 =50.1571采购成本:50.1571/1.08×1.17=54.34(元)/盒货号NY10216/408的实际成本:[11.2× (1-5%-8%-110%×1%)-820/1052] ×8.25-6000/1052 =67.2373采购成本:67.2373/1.08×1.17=72.84(元)/套货号NH91120的实际成本:[12.2 × (1-5%-8%-110%×1%)-820/1242] ×8.25-6000/1242 =76.1808采购成本:76.1808/1.08×1.17=82.53(元)/套3) 再次报价:在成本、运费和利润率改变的情况下,四个货号的报价如下:货号NF91115(CIFC5)[(95/1.17×1.08+6000/1580)/8.25+800/1580] / (1-5%-10%-110%×1%) =[11.0897+0.5063]/0.839=13.8(美元)/套货号NC904(CIFC5)[(55/1.17×1.08+6000/4264)/8.25+800/4264]/(1-5%-8%-110%×1%)=[6.3244+0.1876]/0.859=7.6(美元)/盒货号NY10216/408(CIFC5)[(75/1.17×1.08+6000/1052)/8.25+800/1052]/(1-5%-8%-110% ×1%) =[9.0829+0.7605]/0.859=11.5(美元)/套货号NH91120(CIFC5)[(85/1.17×1.08+6000/1242)/8.25+800/1242]/(1-5%-10%-110%×1%) =[10.0961+0.6441]/0.839=12.8(美元)/套05还盘函上海闵华进出口有限公司SHANGHAI MINHUA IMPORT&EXPORT CO.LTDDATE: 22 MARCH, 2001 Dear Miss Suzuki:We are sorry to hear that you do not consider our price competitive. Nowadays price is no more the dominant factor in promoting sales .quality guarantees the market. Our products enjoy a fame of excellent quality, graceful design, soft color and reasonable price, all of which will add to your marketing force.Your situation is well understood and in view of showing our sincerity in concluding the deal, we would like to give you a special quotation, which we think will help you get a successful start in the market and partly cover the cost of your sales promotion.COMMODITY ART. NO. CIFC5 YOKOHAMA15PC TEA SET NF91115 US$ 13.8/SET220CC CUP & SAUCER NC904 US$ 7.6/BOX16PC KITCHENW ARE NY10216/408 US$ 11.5/SET20PC DINNER SET NH91120 US$ 12.8/SETAccording to our usual practice, time D/P will be accepted only after we have established a satisfactory long-term business relationship. For this first transaction, L/C at 30 days' sight is the best we can do.The products are marketable, and we could keep the offer valid for another 8 days. Please take the opportunity and send us immediately your affirmative reply.With best regards!Yours truly,Shanghai Minhua Imp. & Exp. Co. Ltd.XXXSales Manager06出口成交核算1. 成交金额:(13.8×3160+7.6×4264+11.5×2104+12.8×1242)×8.25=116108×8.25 =957891.00(元)2. 实际成本:(95×3160+55×4264+75×2104+85×1242)×(1-1/1.17%×9%)=798090×1.08/1.17=736698.45(元)3. 国内费用:(1000+250+50+1200+1500+2000)×6=36000(元)4. 出口运费:800×6×8.25=39600(元)5. 出口保费:957891×110%×1%=10536.801(元)6. 客户佣金:957891×5%=47894.55(元)上缴利润=成交金额-实际成本-国内费用-出口运费-保费-佣金=957891-736698.45-36000-39600-10536.801-47894.55=87161.20(元)利润率=利润额/成交金额=87161.20/957891=9.10%07出口合同签订上海闵华进出口有限公司SHANGHAI MINHUA IMPORT&EXPORT CO.LTDDATE: 01APRIL, 2001 Dear Miss Suzuki:Thank you for your Order No.FJD-CN01.Attached is our signed S/C No.MH-FJDSC08 in duplicate. Please kindly countersign them and return one copy for our file.We assure you that we will try our best to execute the contract strictly conforming to the S/C stipulations. And we hope the goods will turn out to be satisfactory in your market. Please open the relative L/C in our favor immediately so that we can arrange shipment.Best regards!Yours truly,Shanghai Minhua Imp. & Exp. Co. Ltd.xxxxxSales Manager08审核信用证信用证存在的问题需要修改的理由1.国外到期 1. 易产生逾期交单2.投保险别有误 2.增加保费支出3.投保加成错误 3.增加保费支出4.信用证金额有误 4.无法全额出运货物5.两个品种货号有误 5.与实际出运货号不符6.三分之二正本提单议付不妥 6.受益人控制货权有风险7.三分之一正本提单直寄不妥7.受益人控制货权有风险8.受益人地址有误8.易出现单、证不符09修改信用证上海闵华进出口有限公司SHANGHAI MINHUA IMPORT&EXPORT CO.LTDDATE: 25APRIL, 2001 Dear Miss Suzuki:We are very glad to receive your L/C No. FJD-MHLC08, but we are quite sorry to find that it contains some discrepancies with the S/C. Please instruct your bank to amend the L/C as follows:1. The place of expiry is in China, instead of "in Japan";2. Insurance should cover "W.P.A. Risk and Clash & Breakage and War Risk for total invoice value plus 10%", instead of "All Risks and War Risk for total invoice value plus 110%'';3. The amount is US$116,108.00, instead of "US$112,467.00",and theamount in word have been amended accordingly;4. The covering goods are "Chinese Ceramic 15pc Tea set Art. No.NF91115, 220cc Cup & Saucer Art. No. NC904 , 16pc Kitchenware Art. No. NY10216/408, and 20pc Dinner Set Art. No. NH91120", instead of "Chinese Ceramic 15pc Tea set Art. No. 91115, 220cc Cup & Saucer Art. No. NC904, 16pc Kitchenware Art. No. NY10216, and 20pc Dinner Set Art. No. NH91120";5. 3/3 original clean on board ocean B/L made out to order and endorsed to our order marked "Freight Prepaid" and notify applicant is presented for negotiation.6. Delete Special Instructions 5) and insert the clause" Certificate stating that None-negotiable Shipping Documents must airmail to Fajitas Trading Co. Ltd.within 2 days after shipment is effected".7. The address of the beneficiary is 'RM.9012' instead of 'RM.9021'.Please amend the above accordingly.With best regards!Yours truly,Shanghai Minhua Imp. & Exp. Co. Ltd.XXXSales Manager14单据审核信用证0016100293496项下的结汇单据存在如下问题:所有单据均未显示出该批货物系分批装运的第一批。

成本核算 报价表

表单编号:JKSY/QP-KF-098 编制部门:

编制:

批准:

联系电话:

报价日期(公章):

产品名称 客户图号

原辅材料.外购外协件费用核算明细

主要费用核算明细 直接费用核算

直接生产工装模具费

产品净重 包装箱尺寸

原辅材料及外 材质及型 协外购名称 号规格

单位

消耗定 额

单价

金额

制造工 序名称

1.必须按表中内容逐项详细填写,如项目不全.不细.或

弄虚作假,一经发现,严肃处理。

报

企

价

2.对‘成本价格核算’栏中:制造费.期间费用的摊配比 业

主

例应在‘报价说明’栏注明。

报

要

3.各部门接到《报价表》15日内,务必及时迅速提供报 价

说

价及相关资料。

说

明

4.以上事项已列入客户《供方业绩评价标准》,并严格 明

考核。

合计

项目 销售收入(年) 工资总额(年)

燃动费总额 制造费总额 管理费总额 财务费总额 销售费总额

企业基本概况

上年

项目

利润总额(年)

固定资产原值

其中:厂房 设备

职工人数

生产工人数

企业年生产能力

上年

产品名称产品净重单位消耗定额单价金额工时单价工装模具名称造价模具寿命产品摊配额包装箱尺寸运输距离产品成本价格核算明细项目构成金额原辅材料费外购外协费燃料动力费直接工资费生产制造费工装模具费制造成本合计管理费财务费销售费期间费用合计企业报价含税合计合计项目上年项目上年销售收入年利润总额年工资总额年固定资产原值燃动费总额其中

定额工时 (小时)

工时单 价

工费 金额

还价核算表

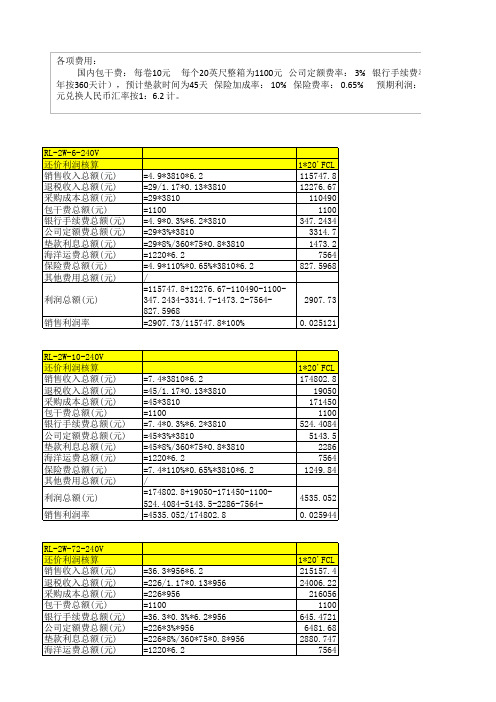

1*20'FCL 174802.8 19050 171450 1100 524.4084 5143.5 2286 7564 1249.84

RL-2W-72-240V 还价利润核算 销售收入总额(元) 退税收入总额(元) 采购成本总额(元) 包干费总额(元) 银行手续费总额(元) 公司定额费总额(元) 垫款利息总额(元) 海洋运费总额(元) 保险费总额(元) 其他费用总额(元) 利润总额(元)

roll =4.9*6.2 30.38 =1100/3810 0.288714 =4.9*0.3%*6.2 0.09114 =1220*6.2/3810 1.985302 =4.9*110%*0.65%*6.2 0.217217 =4.9*10%*6.2 3.038 =(30.38-0.288714-0.09114-1.985302-0.217217-3.038)/(1-13%/1.17+3%+8%/360*75*0. 26.55979

RL-2W-10-240V 还价成本核算 销售收入(元) 包干费(元) 银行手续费(元) 海洋运费(元) 保险费(元) 利润(元) 采购成本(元)

roll =7.4*6.2 45.88 =1100/3810 0.288714 =7.4*0.3%*6.2 0.13764 =1220*6.2/3810 1.985302 =7.4*110%*0.65%*6.2 0.328042 =7.4*10%*6.2 4.588 =(45.88-0.288714-0.13764-1.985302-0.328042-4.588)/(1-13%/1.17+3%+8%/360*75*0. 41.35527

1*20'FCL 215157.4 24006.22 216056 1100 645.4721 6481.68 2880.747 7564 1538.375

还价核算

还价核算:青岛北辰服装进出口公司收到加拿大ABC公司来电求购800套休闲服。

经了解,休闲服的国内购货成本为每套380元(含税);包装是每40套装1纸箱,毛重44公斤,纸箱尺码是60厘米×60厘米×50厘米,包装费用为每箱70元;国内运杂费共1800元;商检报关费600元;港区港杂费400元,北辰公司业务费1000元。

经查,休闲服出口海洋运费按照尺码吨计算,装运港至温哥华每立方米的运费为140美元;海运出口的保险费按照CIF成交价格加一成投保一切险,费率为2%,此外,休闲服的出口退税为11%,出口的银行费用为0.5%(按成交价格计算);预期利润率为出口报价的8%;温哥华公司要求3%的佣金,人民币对美元的汇率是7.18:1.(1)要求分别报出每套休闲服的FOBC3、CFRC3和CIFC3价格。

答:实际成本=380-380*11%/(1+17%)=344.27元国内费用=70/40+(1800+600+400+1000)800=6.5元/套包装箱数=800/40=20箱体积=0.6*0.6*0.5*20=3.6立方米海洋运费=140*7.18*3.6/800=4.52元银行费用=报价*0.5%保险费=CIF价*110%*2%FOB报价=实际成本+国内费用+银行手续费+利润=344.27+6.5+FOB价*0.5%+FOB价*8%=350.77+FOB价*8.5%=350.77/(1-8.5%)=383.36元/7.18=53.39美元FOBC3=FOB价/0.97=55.04美元CFR报价=实际成本+国内费用+海运费+银行手续费+利润=344.27+6.5+4.52+CFR价*0.5%+CFR价*8%=355.29+CFR价*8.5%=355.29/91.5%=388.3元/7.18=54.08美元CFRC3=CFR价/0.97=55.75美元CIF报价=实际成本+国内费用+海运费+保险费+银行手续费+利润=355.29/0.839=397.86元/7.18=55.41美元CIFC3=CIF价/0.97=57.12美元(2)如果客户提出如下还价:FOB净价:USD53/SETCFRC3:USD54/SETCIFC5:USD58/SET根据客户还盘计算三种不同交易条件,北辰公司出口800套休闲服能够获得的利润额分别为多少元?答: FOB价的利润额:FOBC3=FOB价/0.97=54.64美元还价金额=53*800*7.18=304432元实际总成本=344.27*800=275416元国内总费用=(6.5+53*0.5%*7.18)*800=6722.16元总利润额=304432-275416-6722.16=22293.84元CFR价的利润额:CFR价=CFRC3*(1-3%)=52.38美元=376.0884元还价金额=376.0884*800=300870.72元实际总成本=344.27*800=275416元国内总费用=(6.5+52.38*0.5%*7.18)*800+4.52*800=10320.35元总利润额=300870.72-275416-10320.35=15134.37元CIF价的利润额:CIF价=CIFC3*(1-3%)=56.26美元=403.9468元还价金额=403.9468*800=323157.44元实际总成本=344.27*800=275416元国内总费用=(6.5+52.38*0.5%*7.18)*800+4.52*800+403.9468*110%*2%=10329.24元总利润额=323157.44-275416-10329.24=37412.2元(3)如果北辰公司坚持报价中8%的利润率不变,那么按照客户提出的CFRC3还价,公司应掌握的国内购货成本(含税)应为每套多少元?答:CFR价=CFRC3*(1-3%)=52.38美元=376.0884元实际成本=376.09*(1-8%-0.5%)-6.5-4.52=333.10元实际成本=收购成本-出口退税=收购成本*(1-11%/117%)=收购成本*106/117收购成本=333.10*117/106=367.67元所以国内购货成本应该为每套367.67元。

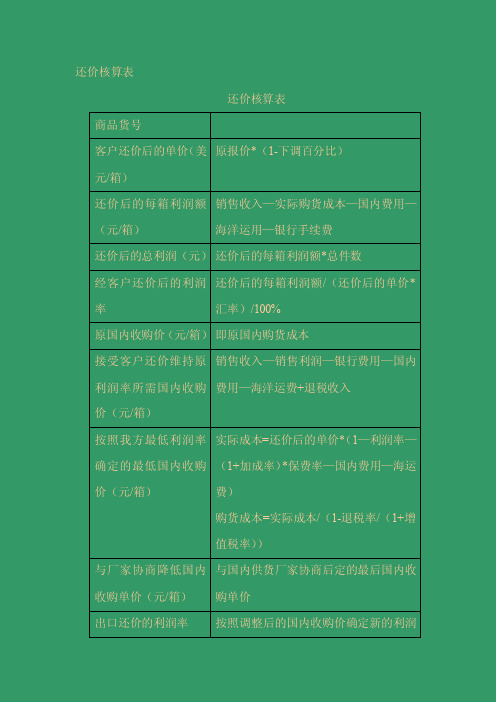

(国际贸易实务)还价核算表

还价核算表

还价核算表

商品货号

客户还价后的单价(美

元/箱)

原报价*(1-下调百分比)

还价后的每箱利润额(元/箱)销售收入—实际购货成本—国内费用—海洋运用—银行手续费

还价后的总利润(元)还价后的每箱利润额*总件数

经客户还价后的利润率还价后的每箱利润额/(还价后的单价*汇率)/100%

原国内收购价(元/箱)即原国内购货成本

接受客户还价维持原利润率所需国内收购价(元/箱)销售收入—销售利润—银行费用—国内费用—海洋运费+退税收入

按照我方最低利润率确定的最低国内收购价(元/箱)实际成本=还价后的单价*(1—利润率—(1+加成率)*保费率—国内费用—海运费)

购货成本=实际成本/(1-退税率/(1+增值税率))

与厂家协商降低国内收购单价(元/箱)与国内供货厂家协商后定的最后国内收购单价

出口还价的利润率按照调整后的国内收购价确定新的利润

率

出口还价(美元/箱)(购货成本—退税+银行费用—国内费

用—海洋运费+报价*利润率)/汇率。

04-还价核算

我公司拟出口全棉男式 衬衫1,000打至某港口,其中: 购货成本:650元/打; 增值税:17% ,退税率:9%; 国内费用:25元/打; 海运运费:10美元/打; 保险:加成10%,费率为1%; 预期利润率:10%; 汇率:8.25:1

(2)对方还盘USD 90.00/打,求我方的利润总额及总利润率。 解: 还价金额:90*1000*8.25 =742,500 元 实际总成本:600*1000 = 600,000元 国内总费用:25*1000 = 25,000元 总运费:10*1000*8.25 = 82,500元 总保费:742500*110%*1% = 8,167.50元 总利润额:742500-600000-25000-82500-8167.50 =26,832.50元 利润率:26832.50/742500 = 3.61%

我公司拟出口全棉男式 衬衫1,000打至某港口,其中: 购货成本:650元/打; 增值税:17% ,退税率:9%; 国内费用:25元/打; 海运运费:10美元/打; 保险:加成10%,费率为1%; 预期利润率:10%; 汇率:8.25:1

(4)请生产厂家协商,吃饭花去2000元,厂家初步同意降价至620 元/打, 但前提条件为数量加倍,求我方的利润总额及总利润率。 解:还价金额:90*2000*8.25 =1,485,000.00 元 实际总成本: [620-620*9%/(1+17%)] *2000=1,144,615.39元 国内总费用: 25*2000+2000= 52,000元 总运费:10*2000*8.25 =165,000元 总保费:1485000*110%*1% =16,335.00元 总利润额:1485000-1144615.39-52000-165000-16335 =107,049.62元 利润率:107049.62/1485000 = 7.21%

菜价调查表

1

冰鲜

2

冰鲜

3

冰鲜

4

冰鲜

5

冰鲜

6

冰鲜

7

冰鲜

8

冰鲜

9

冰鲜

10 冰鲜

11

菜

12

菜

13

菜

14

菜

15

菜

16

菜

17

菜

18

菜

19

菜

20

菜

21

菜

22

菜

23

菜

24

菜

25

菜

26

菜

27

菜

28

菜

29

菜

30

菜

31

菜

32

菜

33

菜

34

菜

35

菜

36

菜

37

菜

38

菜

39

菜

40

菜

41

菜

42

菜

名称 包心贡丸 香菇贡丸 冻鸡腿 冻鸡脚 冻鸡中翅 冻鸡全翅 冻鸡翅尖 冻鸡翅根 黑椒肠

单位 斤 斤 斤 斤 只 斤 只 瓶 瓶 斤 斤 斤 包 桶 包 瓶 瓶 斤 斤 斤 板 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 箱 斤 斤 箱 斤

单价

鱼蛋 包菜 菜花 菜心 大白菜 冬瓜 豆角 番茄 红萝卜 花菜 节瓜 金针菇 韭菜 苦瓜 辣椒 老南瓜 萝卜 木瓜 南瓜 茄瓜 青瓜 青椒 沙葛 生菜 蒜芯 土豆 娃娃菜 西芹 西生菜 香芹 芫茜 洋葱 油麦菜

单位 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤 斤

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

还 价 核 算 表

填表日期:年月日填表人:编号:

核算规则:还价利润核算时保留2位小数。

还价成本核算时保留4位小数,小于1时保留5位小数,最终得出的单位采购成本保留2位小数。

核算信息:

进口商货物名称装运港

还价利润核算

货号客户还价(US$)计价单位贸易术语还价数量采购成本(¥)核算单位:

计算过程

销售收入总额(¥)

退税收入总额(¥)

采购成本总额(¥)

海洋运费总额(¥)

国内包干费总额(¥)

公司定额费总额(¥)

垫款利息总额(¥)

银行手续费总额(¥)

保险费总额(¥)

佣金总额(¥)

利润总额(¥)

销售利润率。