摩根大通投资银行演示材料

JPmorgan ppt 摩根大通ppt课件

1824 The Chemical Bank is established.

1848 The Waterbury Bank opens, a predecessor of the Chase Manhattan Bank.

1871

J. Pierpont Morgan and Philadelphia banker Anthony Drexel form a private merchant banking

2019/6/4

recent company news

JPMorgan Chase Tower 270 Park Avenue

New York City, New York

In October 2014, JP Morgan sold its commodities trader unit to Mercuria for $800 million - a quarter of the initial valuation of $3.5 billion, as the transaction excluded some oil and metal stockpiles and other assets.

partnership in New York called Drexel, Morgan & Co. This is the earliest partnership that evolves into J.P.

Morgan.

1955 Chase National Bank merges with The Bank of the Manhattan Company to form Chase Manhattan Bank.

the world's sixth largest bank by total assets

《j.p.摩根大通》ppt课件

在19世纪末的美国,一旦一家财团被定义为托拉斯他就将遭到政府的针对和打击。但 摩根大通集团却因为其庞大的商业版图,让每一届想要拆分自己的美国政府都无从下手。

因为只要摩根大通集团发展得足够好,美国总统在竞选时就需要摩根大通为他们提供资 金。而当摩根大通拿出充足的资金支持总统之后,成为了政府幕后金主的摩根大通自然 也不会受到清算。

1

事实证明,皮尔庞特的直觉是正确的。在美国政府平稳地渡过了这次信任危机之后,摩根大通也 成为了共和党人颇为倚重的大财团。

2

借着这股胜利的东风,皮尔庞特一举让摩根银行收购了多家媒体和铁路公司。从此以后,摩根集 团就成为了横跨航运、制造、银行甚至是石油等多个领域的超级巨头。

3

1907年,美国再次爆发了严重的金融危机,无数的银行濒临破产。在这个时候,美国的财政部更 倾向于增发资金拯救这些银行,而摩根集团则抓紧时间收购那些运作良好的公司。

4

1893年,受到国际大宗货物交易价格波动的影响。美国国内也爆发了严重的经济危机。在这样的情况下,人们纷纷通过将手中的美元 兑换成黄金的方式来避险。

5

然而,在这个最为关键的时刻,美国联邦储蓄委员会却根本拿不出足够的黄金来应付市场上日益扩大的需求。而一旦民众对美国的银 行业彻底失去信心,美国的经济就将迎来总崩溃。

员都必须迎接一场更为凶险的博弈。

4

如果下一次他还能成功的话,摩根大通就 能够与美国的国家机器成功绑定。到时候, 营利对于摩根家族来说将不再是问题,他 们将会成立起一个令世人惊叹的商业帝国!

一落千丈的“商业巨头”

1933年,代表的富兰克林罗斯福走到了美国政治舞台的最中央。在认识到美国历次经济危机的根源之后, 罗斯福非常大胆地提出了一个要求:要想度过大萧条,美国政府就必须对美国国内的银行巨头开刀。 而当时美国社会当中影响力最大的银行业巨头就是由皮尔庞特一手创建的摩根大通集团了。 起初,摩根大通集团的掌门人对于美国政府的政令还不以为然。但由于前任总统吴服表现的实在太差,美 国的民众对摩根大通支持的共和党人普遍已经失去了信心。 罗斯福政府先是以清查税款的名义要求摩根大通集团向联邦政府递交相关的说明文件,而后罗斯福又直接 派人通知摩根大通集团的董事们: 为了确保未来市场上的公平秩序,摩根大通集团必须让手下的银行在普通商业业务与投资性业务之间选择 一项。因为一家银行同时从事两项业务是不被美国法律惊人的办法:摩根 银行可以和罗斯柴尔德家族合作,向美国社会中的 公众发售债券。而后摩根银行和罗斯柴尔德家族再

华尔街顶级投资银行——摩根大通面试经历_面试经历.doc

华尔街顶级投资银行——摩根大通面试经历_面试经历让我们先自我介绍一下。

在高年级和大学四年的成绩中,几所大学的概率统计系的毕业目标有点复杂:一定要在高年级寒假前出国,然后改变主意,在一周内去工作。

在工作面试之前,没有实习经验,也没有俱乐部活动经验。

从头到尾只有两次采访。

第一个被拒绝,第二个被提供。

鉴于我复杂的志向,我想先介绍出国工作的想法。

像所有其他出国的学生一样,我读了《新东方》,拿了两个G,经历了一个漫长而艰苦的申请过程.过去,包括我在内,没有人想找工作。

与他人的唯一不同是,当别人还在为申请感到困惑时,我仍然有闲暇去组织招聘会,比如在摩根士丹利和CICC的网页上张贴简历。

当时,我只是觉得有趣,想积累一些采访经验。

当摩根大通的出价到手时,我真的意识到了问题的严重性。

目前,有两种方法:出国攻读博士学位成为一名教师,或者工作攻读工商管理硕士学位成为一名行政人员。

尽管走另一条路而不走一条路是不可能的,但毕竟需要——年的博士学位。

当我曾经崇拜的师姐告诉我她对美国的失望时,我决定选择后者。

因为恐怕我没有成为教员的激情。

我喜欢美国,但我不喜欢它到我不得不去的地步。

此外,所有关于美国的梦可能只是我自己的一个例证。

当海外的资深兄弟姐妹告诉我们美国校园只是一些美丽的乡村时,这种幻觉就不复存在了。

尽管很难放弃之前的所有努力,但我们不能让沉没成本阻碍我们的决定。

第一次面试:言归正传,采访经历。

我遇到的第一家公司是CICC,招聘程序是:简历——团体面试——笔试——一对一面试。

简历无话可说,只需在网站上填写中英文表格。

它很长,你必须有耐心。

然后去清华集团面试。

这是我第一次去清华经济技术学院。

我迟到了。

当我到达时,我发现面试官比我晚。

看着周围人的衣服,我迫不及待地想把它们折回去:其他人都穿着乌鸦的衣服,而我穿着一件红色的毛衣和一件白色的外套,这让我很显眼。

不管怎样,我来这里是为了好玩,我想,所以我大摇大摆地走了过去。

群体面试意味着两个面试者向大约8名候选人介绍自己。

摩根大通复杂衍生品巨亏事件的案例分析_侯冰慧

摩根大通复杂衍生品巨亏事件的案例分析摘要:2012年5月,摩根大通在合成信贷资产组合仓位上出现20亿美元的巨额亏损,对冲基金以至整个华尔街都试图探究摩根大通巨亏的成因;另一方面,监管当局对摩根大通的交易也抱有怀疑态度,这一事件有可能加速“沃尔克规则”的推进实施。

基于此,本文首先描述导致摩根大通亏损的复杂衍生品及交易策略,然后对导致亏损的合成信贷资产组合进行风险分析,并依据事件和风险量化的结果总结了亏损原因。

本文试图通过已有资料及分析推理还原事件的真相,为我国未来衍生品交易风险管理提供案例借鉴。

关键词:摩根大通巨亏事件;复杂衍生品;交易策略;风险分析DOI :10.3773/j.issn.1006-4885.2013.05.073中图分类号:F 061.5文献标识码:A 文章编号:1002-9753(2013)05-0073-22侯冰慧基金项目:国家自然科学基金(70871023)。

作者简介:侯冰慧(1989—),河南三门峡人,对外经济贸易大学金融硕士,研究方向:金融工程。

1引言近年来全球金融衍生工具市场得到了快速的发展,衍生品的使用及其风险管理已经成为全球金融实践关注的焦点。

先不论这种关注是否来自金融市场更加严格的监管环境,但金融机构若想在如今这个相互关联相关影响的市场中长久生存下去,就必须要建立健全完备的风险管理体制架构。

然而由于不当交易及风险控制缺失而造成的亏损事件层出不穷,自著名的“巴林银行”亏损事件,至对冲基金界的神话“长期资本管理公司”由于风控失误损失40亿美元。

尤其是2008年全球金融危机以来,华尔街因衍生品而产生的亏损事件更是接连不断:摩根士丹利由于在次贷和相关敞口上的仓位亏损94亿美元,法兴银行因交易员越权交易欧洲股指期货造成71.6亿美元损失,瑞信参与未批准交易亏损23亿美元等等。

据美国货币监理署数据显示,截至2011年第四季度全球衍生品总敞口达到707亿美元,如此庞大的衍生品敞口如果得不到控制,很可能会对全球金融产生破坏性的影响。

投行并购的案例分析共20页文档

大通曼哈顿兼并J·P摩根案

➢ 大通以往的并购行为

1995年,化学银行,100亿美元 1999年,美国投资银行Hambrecht&Quist,

13.5亿美元 2000年,英国投资银行Robert Fleming集团,

77.5亿美元 2000年,Beacon集团,5亿美元 2000年9月,J.P.Morgan,360亿美元

大通曼哈顿兼并J·P摩根案

➢ 2000年12月31日,美国第三大银行大通曼哈顿公 司(the Chase Manhattan Corporation)兼并第 五大银行摩根公司(J·P·Morgan& Co.Incorporated)一案终于尘埃落定。由于两家 金融机构的显赫地位和交易金额的巨大,使得它 被视做银行业并购的又一典范案例。

➢ 2000年9月13日,大通曼哈顿公司正式宣布与摩 根公司达成了兼并协议。双方交易的条件是,大 通将按照9月12目的收盘价,以3.7股去交换摩 根的1股,交易价值高达360亿美元。12月11日, 美联储理事会以全票通过批准了这项兼并计划。

大通曼哈顿兼并J·P摩根案

➢ 12月22日,双方股东大会顺利通过了兼并计划。12月31 日,兼并正式完成。新组成的公司取名为JP.摩根大通公 司(J·P·Morgan Chase&Co),新公司的股票已于2001 年1月2日在纽约股票交易所开始交易。

大通曼哈顿兼并பைடு நூலகம்·P摩根案

➢ 从交易结果来看,这项交易导致摩根失去了独立性。在新 的董事会13个席位中,摩根只占了5席;从交易的过程看, 大通的计划是基于战略的考虑,而摩根只是被动地接受并 放弃了主权。为什么呢?

➢ 大通——摩根案例的真正特色和价值,首先反映在媒体鲜 为报道的大通的发展策略上。大通的历史可追溯到18世纪 末。1799年亚历山大·汉密尔顿(Alexander Hamilton) 和艾伦·伯福米德(Aaron Burrformed)在纽约成立曼哈 顿公司,当时的目的是为纽约提供自来水,后改为银行。 1877年,J·汤普森取林肯政府财政部长S·P·蔡斯(Chase: 汉译‘大通”)的姓创办了大通国民银行。1929年, J·D·洛克菲勒夺得控制权,次年,将其并入自家的公平信 托公司,名称仍沿用前者。1955年,大通国民银行与曼哈 顿银行合并组成大通曼哈顿银行,资产额达到70亿美元。 1965年参加联邦储备系统和联邦存款保险公司。1969年 成立银行持股公司——大通曼哈顿公司,大通曼哈顿银行 则为其主要子公司;截至1999年底,大通的资产总额达 4061亿美元,成为美国第三大银行,在1999年全球500强

InvestmentBank之JPMorganChase(JP摩根大通)

InvestmentBank之JPMorganChase(JP摩根大通)一、关于公司.简介Morgan Chase是一家领先性的国际金融公司,能够满足商业、企业、政府和个人的紧急金融需求。

它为公司策略提供咨询服务,集资,开拓金融市场工具,管理投资财产。

同时Morgan为抓住市场机遇,将自己的资产承诺于知名企业、好的投资和交易项目。

我们承诺将提供最高质量的咨询服务,规范地开展业务,保持在国际市场中的领先地位,以便提高股票持有者的回报率,最终令我们的客户满意。

为达到这个目标,我们将公司分成5个主要部门:金融与咨询市场拓展资产管理咨询股票投资资产权投资与经营.前沿变化在以前的美国,Glass-Steagall 法案中的结构缺陷充分的体现出来。

大公司开始寻找比从银行借钱更合算的方法。

于是银行被迫寻找新的生意机会。

Morgan 开始了它的前沿变化。

1989年,联邦储备给予Morgan 特权来承销公司债务证券。

一年后,特权扩大到承销股票。

随着在欧洲国家的经验的丰富,Morgan 已在美国积蓄了新的力量。

2000年美国大通银行宣布,将会收购JP摩根(JPMorgan)投资银行。

这项作价332亿美元的收购计划,将会产生出一家拥有6600亿美元资产的全球最大银行。

大通和JP摩根合并后将会名为“JP摩根大通”(JPMorganChase)。

JP Morgan Chase给全世界的客户提供强大的综合能力,其中包括:集资、战略咨询、市场拓展方法和资产管理等。

尽管公司目前的经营环境比它刚创立的时候更复杂、变化更迅速,但它的经营原则却始终保持不便,其3个宗旨是:正直、客观、正确。

.哲学与特点我们的哲学与特点--我们是如何经营的--与我们的能力和服务一样重要。

客观我们永远将客户的长期利益放在第一位。

公正的检验他们的情况并提出最好的战略选择建议。

团体合作由于团体合作,我们的客户可以受益于我们区域性与功能性综合能力以及最富有创造性的思维。

摩根大通

J·P·摩根公司是1968年12月20日建立的持有摩根银行全部股权的银行持股公司。 摩根大通

摩根银行原名纽约摩根担保信托公司,是1959年4月20日由两家商业银行合并而成的,一家也称为J·P·摩根公司,一家是纽约担保信托公司。 组成纽约摩根担保信托公司的J·P·摩根公司建于1860年,以J·皮尔庞特·摩根名字命名。创建之初,该公司只是一家个人经营的办事处,专门买卖外汇。尔后业务不断发展。1864年更名达布尼·摩根公司,1871年改称德雷克塞尔·摩根公司,1895年改为J·P·摩根公司。该公司从早期开始,就同美国金融界发生的历史事件有着密切关系。第一次世界大战期间,该公司包揽美国对西欧的金融业务,大发其财。根据1933年银行法,摩根公司改为商业银行,把原来经营的投资银行业务交付给摩根斯坦利。1940年以后,摩根公司由合伙公司改为股份有限公司,并开始经营信托业务。 纽约担保信托公司建于1864年,1896年改名为纽约担保信托公司。1910年合并莫顿信托公司和第五大道信托公司,1912年合并标准信托公司,1929年合并商业银行。 二战以后,美国银行界的竞争日趋剧烈。摩根公司同纽约担保信托公司合并为纽约摩根担保信托公司就加强了实力,能够更有效地进行竞争。60年代末期,作为纽约摩根担保信托公司即摩根银行的持股公司――J·P·摩根公司建立之后,经营范围进一步扩大。为了适应国内外金融市场的变化,该公司先后建立了一些新的附属机构,其中包括1971年建立的23――六公司(1976年更名为摩根社会发展公司)1981年建立的摩根期货公司,1986年建立的J·P·摩根证券公司等。 摩根大通银行

进入90年代以来,伴随着信息的浪潮,公司的业务范围进一步扩大,如推出网上银行、为用户提供更加方便的信用卡服务等等。银行的业务已遍布全球,公司的规模也进一步扩大,但公司仍始终本着真诚、公正与公平的原则,为全球千千万万个客户提供优质的服务。 摩根大通在香港有30年历史,多次被评为香港最优秀、最具影响力的投资银行,在执行香港复杂上市发行方面具有广泛的经验。1999年11月,摩根大通担任联席全球协调人,成功发行香港盈富基金。摩根大通在此次金额为43亿美元的交易中作用举足轻重,接获机构需求量为承销团之首,占机构投资者订单总量的32%,零售订单的6.4%。摩根大通自1987年起即开始在中国投资及开展投资银行业务,主承销过许多国企发行项目,包括多起H股重组上市项目:华能国际电力、安徽海螺、成渝高速等,B股有内蒙古伊泰煤矿等,以及N股:华能国际电力。今年5月,摩根大通在中国财政部10亿美元的10年期债券发行中担任联席牵头行及薄记行。此前,还为财政部1亿美元世纪债券和5亿美元7年期全球债券担任过主承销。摩根大通于2000年为华能国际收购山东华能担任财务顾问。 2004年6月14日,美联储发表声明,批准美国摩根大通银行与美国第一银行的兼并方案。合并后的新摩根大通银行资产总额达1.12万亿美元,一举超过美洲银行,与1.19万亿美元资产的第一大银行花旗仅一步之遥,而且业务也将从纽约扩展到整个中西部,成为了继花旗之后第二家真正跨地区的银行。

摩根大通发展历史

摩根大通发展历史一、摩根士丹利的发展历史摩根士丹利原是JP摩根大通公司中的投资部门,1933年美国经历了大萧条,国会通过《格拉斯-斯蒂格尔法》(Glass-Steagall Act),禁止公司同时提供商业银行与投资银行服务,摩根士丹利于是作为一家投资银行于1935年9月5日在纽约成立,而JP摩根则转为一家纯商业银行。

1941年摩根士丹利与纽约证券交易所合作,成为该证交所的合作伙伴。

公司在1970年代迅速扩张,雇员从250多人迅速增长到超过1,700人,并开始在全球范围内发展业务。

1986年摩根士丹利在纽约证券交易所挂牌交易。

进入1990年代,摩根士丹利进一步扩张,于1995年收购了一家资产管理公司,1997年则又兼并了西尔斯公司下设的投资银行迪安·威特公司(Dean Witter),并更名为摩根士丹利迪安·威特公司。

2001年公司改回原先的名字摩根士丹利。

1997年的合并使得美国金融界两位最具个性的银行家带到了一起:摩根士丹利的约翰·麦克(John Mack)与迪安·威特的裴熙亮(Philip Purcell),两人的冲突最终以2001年7月约翰·麦克的离职结束,从此之后裴熙亮就一直担任着摩根士丹利主席兼全球首席执行官的职务。

在他的带领下摩根士丹利逐渐发展成为全方位的金融服务公司,提供一站式的多种金融产品。

在2001年的911事件中,摩根士丹利丧失了在世界贸易中心中120万平方英尺的办公空间。

公司已经在曼哈顿附近新购置了75万平方英尺的办公大楼,目前是摩根士丹利的全球总部。

二、摩根大通银行的发展历程J.P.摩根大通公司是1968年12月20日建立的持有摩根银行全部股权的银行持股公司。

摩根银行原名纽约摩根担保信托公司,是1959年4月20日由两家商业银行合并而成的,一家也称为J.P.摩根公司,一家是纽约担保信托公司。

组成纽约摩根担保信托公司的J.P.摩根公司建于1860年,以J·皮尔庞特·摩根名字命名。

国际大型投资银行介绍PPT培训课件

摩根士丹利案例分析

成立时间与地点

摩根士丹利于1935年由摩根银行和士丹利公司合并而成,总部位于 美国纽约。

主要业务领域

摩根士丹利主要为客户提供全球化的投资银行服务,包括证券承销、 并购顾问、债券交易等。

创新与资本市场

摩根士丹利在资本市场和投资银行业务方面具有很强的创新能力和市 场影响力,不断推出新的金融产品和服务。

投资银行通过先进的电子交易平台和清算系统,确保交易的准确性和及时性。同 时,投资银行还会为客户提供证券托管和清算服务,以确保客户资产的安全和合 规性。

交易及直接投资业务

交易及直接投资业务是国际大型投资银行的重要业务之一,涉及固定收益、外汇、商品等交易以及直 接股权投资。这些交易和投资旨在帮助客户实现其财务目标和风险管理需求。

这些银行通常在全球范围内开展业 务,为客户提供跨境金融服务。

全方位服务

国际大型投资银行能够提供全方位 的金融服务,满足客户不同需求。

风险控制能力强

风险管理体系完善

灵活应对风险

国际大型投资银行通常拥有完善的风 险管理体系,通过严格的风险管理和 内部控制措施降低风险。

国际大型投资银行能够灵活应对各种 市场风险和挑战,通过合理的风险分 散和规避策略降低损失。

投资银行通过专业的交易团队和先进的交易技术,为客户提供定制化的交易和投资策略,以实现客户 的财务目标。同时,投资银行还会为客户提供市场分析和风险管理建议,以帮助客户降低风险并实现 稳健的回报。

03 国际大型投资银行的竞争 优势

资本实力雄厚

01

02

03

资本充足

国际大型投资银行通常拥 有雄厚的资本基础,能够 支持其开展大规模的业务 活动。

跨境金融服务

摩根财团并购总结与启示

摩根财团并购总结与启示回顾摩根整个发展历程,从传统的家族企业到当代的跨国公众公司,摩根经历了世界经济特别是美国经济的大风大浪,几经沉浮,依然保持着蓬勃的活力。

在摩根的成长过程中,兼并收购是经常采用的扩张手段。

前文在三个历史时期分别选取典型的摩根并购案例,勾画出了摩根的并购之路。

从这些并购案例中我们可以获得不少启示。

(一)顺应发展趋势,建立发展战略曾有人说过,摩根发展的历史就是美国金融发展的历史。

这既是再说摩根影响着美国经济,更是在说摩根的战略决策紧跟着美国经济的步伐。

摩根一并购发展壮大始于19世纪中后期。

当时的美国正处于工业化初期,包括铁路运输在内的基础设施建设是美国经济发展的发动机,也是美国的支柱产业之一。

掌握铁路运营权,就能够把握经济大动脉。

摩根公司敏锐的发现的其中的巨大商机,通过股票承销、二级市场认购、投票权代理等方式一步步渗透到铁路运输产业中,进而推动产业内部的企业整合和重组,提供按市场集中度,获得更多超额利润,并最终成为控制美国铁路2/3的金融寡头,赢得了美国经济运营的话语权。

南北战争就结束后,美国进入了工业化的新阶段。

钢铁工业作为这一时期的主要标志性产业,应经成为了经济舞台上的主角。

摩根公司并没有落后于历史的进步,积极参与到新一轮的产业革命中来。

这样,进入钢铁产业就成为摩根并购战略的下一个重点。

尽管当时的金融工具和并购手段不像今天这样多的令人眼花缭乱,但老摩根利用其个人的智慧和手腕实现了一个又一个商业梦想,建立了属于自己的商业王国。

摩根公司这一紧跟经济主流的战略原则始终没有改变。

在传统的资本主义时代,它是影响横亘金融界和产业界的金融寡头,染指诸如美国钢铁、通用电气、通用汽车、杜邦公司等声名显赫的跨国企业;在当今的新经济时代,它依然通过资本市场持有富有潜力的公司的股权,分享全球经济进步的成果。

(二)优化业务模块,注重协同效应每个时期社会经济的热点产业并非独一无二,选择哪个产业作为自己的并购目标对于并购来说是一个巨大的挑战。

世界十大投资银行简介汇总

世界十大投资银行简介1,高盛集团Goldman Sachs高盛集团成立于1869年,是全世界历史最悠久及规模最大的投资银行之一,总部设在纽约,并在东京、伦敦和香港设有分部,在23个国家拥有41个办事处。

其所有运作都建立于紧密一体的全球基础上,由优秀的专家为客户提供服务。

高盛集团同时拥有丰富的地区市场知识和国际运作能力。

随着全球经济的发展,公司亦持续不断地发展变化以帮助客户无论在世界何地都能敏锐地发现和抓住投资的机会。

2004年,高盛实现突破,在北京建立合资公司高盛高华证券有限公司,真正进入了正在快速发展的中国金融服务市场。

2,花旗集团Citigroup由花旗公司与旅行者集团于1998年合并而成。

换牌上市后,花旗集团运用增发新股集资于股市收购、或定向股权置换等方式进行大规模股权运作与扩张,并对收购的企业进行花旗式战略输出和全球化业务整合,成为美国第一家集商业银行、投资银行、保险、共同基金、证券交易等诸多金融服务业务于一身的金融集团。

合并后的花旗集团总资产达7000亿美元,净收入为500亿美元,在100个国家有1亿客户,拥有6000万张信用卡的消费客户。

从而成为世界上规模最大的全能金融集团之一。

3,摩根士丹利Morgan Stanley从1935年到1970年,大摩一统天下的威力令人侧目。

它的客户囊括了全球十大石油巨头中的6个,美国十大公司的7个。

当时惟一的广告词就是“如果上帝要融资,他也要找摩根士丹利。

” 大摩从20世纪80年代中期就积极开拓中国市场。

于1994年在北京和上海开设办事处。

1995年,摩根士丹利和中国建设银行共同创立了中国国际金融有限公司,这是到目前为止中国批准的唯一一家合资投资银行。

2000年,摩根士丹利协助完成了亚信、新浪网、中国石化和中国联通的境外上市发行。

4,摩根大通公司JP Morgan摩根大通(JP Morgan Chase Co)为全球历史最长、规模最大的金融服务集团之一,由大通银行、J.P.摩根公司及富林明集团在2000年完成合并。

证券发行与承销_案例

《证券发行与承销》案例目录案例1:最负盛名的投资银行家和中国的传奇故事 (2)案例2:世界十大投资银行之“大摩”“小摩” (3)案例3:股份制公司决议是否合规 (3)案例4:荒唐的发行,投资者拒绝买入 (4)案例5:证监会撤销两保荐人资格 (6)案例6:IPO的询价、定价环节可能存腐败 (6)案例7:摊薄市盈率和稀释每股收益 (7)案例8:精华制药低价增发派红包资本大鳄4天浮盈3亿 (8)案例9:新华保险A+H成功上市 (9)案例10:北汽集团广汇汽车先H后A或二季度赴港IPO (9)案例11:基金公司出昏招转债竟忘记转股百姓利润付水流 (11)案例12:首支外资法人银行金融债券成功发行 (13)案例13:吉利杠杆收购沃尔沃案例解析 (14)案例1:最负盛名的投资银行家和中国的传奇故事铃声响起时,约翰·麦克(JohnJ.Mack)感到诧异。

他所在的游艇上的应该只有为数极少人知道。

而且,这是美国殉难者纪念日的假期,谁会在这时找到自己呢?这个出人预料的来自中国。

对方自我介绍说,她是摩根士丹利某个IPO项目的负责人之一,受其客户之托并征得公司亚洲负责人的同意,她恳求麦克在两日之飞往。

“你是否知道我刚在十天前从返回?此事还是等我回公司后再说吧。

”麦克迅速放下了。

但这名中国员工并未放弃。

在这之后的数小时,她留下了多条留言,请求麦克听她述要他再次来华的原因及时间的紧迫。

最后,麦克拨回了,严厉表态:“好,我现在就听你说,希望你有充分的理由来解释你冒昧的要求。

否则,我就解雇你!”接下来,对方讲述了一家名为中国石油化工股份的困境。

这是2000年5月,中国的原油价格已经同国际接轨,但成品油价格还尚未市场化。

全球原油价格高涨下,严重的价格倒挂致使中石化筹备已久的海外上市无从进行。

因摩根士丹利是此次IPO项目的主承销商,中石化董事长毅中及总裁王基铭要求麦克到亲自拜见中国国家领导人,从中石化IPO的角度阐述上调成品油价格的必要性。

《投资银行学》课程笔记

《投资银行学》课程笔记第一章:导论一、投资银行概述1. 定义:投资银行是一种专业的金融服务机构,它主要在资本市场上为客户提供各种金融产品和服务,包括但不限于证券承销、并购咨询、资产管理、风险管理、市场研究等。

2. 功能:(1)融资功能:投资银行为企业、政府和其他金融机构提供融资服务,帮助它们通过发行股票、债券等证券来筹集资金。

(2)市场创造与流动性提供:投资银行通过参与证券的一级市场和二级市场,为市场提供流动性,促进证券交易的活跃。

(3)价值发现与定价:投资银行在证券发行和并购活动中,通过专业分析帮助发现资产的价值,并为其定价。

(4)风险管理:投资银行提供各种金融工具和服务,帮助客户管理和对冲市场风险。

3. 重要性:(1)资本市场引擎:投资银行是资本市场发展的引擎,它通过创新金融产品和提升服务质量,推动资本市场的繁荣。

(2)经济增长催化剂:投资银行通过为企业提供融资,促进技术创新和产业升级,从而加速经济增长。

(3)金融市场稳定器:投资银行在风险管理方面的作用有助于维护金融市场的稳定。

二、投资银行的发展历史和组织形式1. 发展历史:(1)早期阶段(19世纪末至20世纪初):投资银行主要以证券承销和交易为主,业务相对单一。

(2)成长阶段(20世纪中期):随着金融市场的发展,投资银行业务开始多元化,包括并购、资产管理等。

(3)全球化和金融创新阶段(20世纪末至21世纪初):投资银行国际化发展,金融创新产品不断涌现,如衍生品、结构性产品等。

(4)金融危机与监管改革(2008年后):金融危机暴露了投资银行的风险,随后全球范围内加强了金融监管。

2. 组织形式:(1)独立投资银行:专注于投资银行业务,如高盛、摩根士丹利等。

(2)全能银行:提供包括商业银行业务在内的全方位金融服务,如德意志银行、汇丰银行等。

(3)金融控股公司:通过控股多个子公司实现业务多元化,如摩根大通、花旗集团等。

三、投资银行的业务1. 证券发行与承销:(1)股票发行与承销:协助企业进行首次公开发行(IPO)和新股增发,包括尽职调查、估值、路演等。

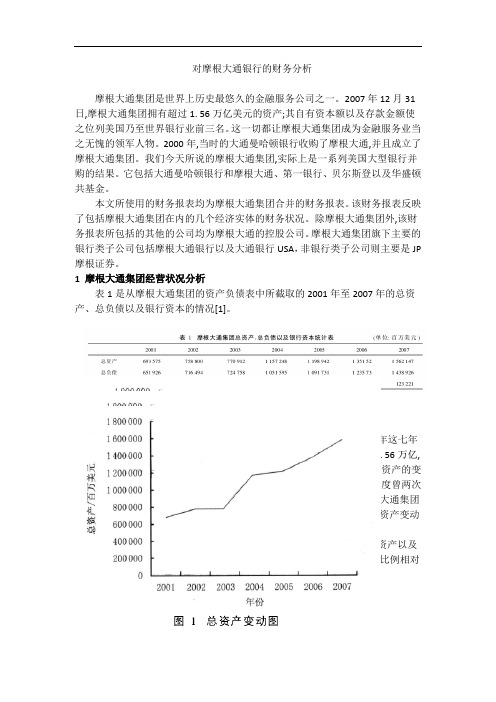

对摩根大通银行的财务分析

对摩根大通银行的财务分析摩根大通集团是世界上历史最悠久的金融服务公司之一。

2007年12月31日,摩根大通集团拥有超过1. 56万亿美元的资产;其自有资本额以及存款金额使之位列美国乃至世界银行业前三名。

这一切都让摩根大通集团成为金融服务业当之无愧的领军人物。

2000年,当时的大通曼哈顿银行收购了摩根大通,并且成立了摩根大通集团。

我们今天所说的摩根大通集团,实际上是一系列美国大型银行并购的结果。

它包括大通曼哈顿银行和摩根大通、第一银行、贝尔斯登以及华盛顿共基金。

本文所使用的财务报表均为摩根大通集团合并的财务报表。

该财务报表反映了包括摩根大通集团在内的几个经济实体的财务状况。

除摩根大通集团外,该财务报表所包括的其他的公司均为摩根大通的控股公司。

摩根大通集团旗下主要的银行类子公司包括摩根大通银行以及大通银行USA,非银行类子公司则主要是JP 摩根证券。

1 摩根大通集团经营状况分析表1是从摩根大通集团的资产负债表中所截取的2001年至2007年的总资产、总负债以及银行资本的情况[1]。

1. 1 资产状况分析从上表中我们不难看出,从2001年摩根大通集团正式成立到2007年这七年时间里,摩根大通集团的总资产从最初成立时的0. 69万亿增长超过了1. 56万亿,增长了125. 23%,年平均环比增长速度为14. 49%。

图1清楚地表明了总资产的变化走势。

摩根大通集团的资产在2003至2004年度以及2006至2007年度曾两次出现了快速增加。

这两次快速增长背后的原因是什么?究竟为什么摩根大通集团总资产会有这种高速的发展?通过表2可以分析摩根大通集团历年来的资产变动情况。

摩根大通集团的资产构成当中,最主要的三项分别是贷款、交易性资产以及无形资产。

其中,贷款和交易性资产的总量增长较快,但是在总资产中的比例相对稳定。

无形资产所占比重虽然只有10%左右,但是其增长速度非常惊人。

从两个数据表中可以看出,交易性资产的平均环比增长速度低于总资产增长速度,贷款总量的增长与总资产增长速度相近,无形资产的增长速度则大大高于总资产增长速度。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

JPM

7%

Rest of Top 10

(7%)

JPM

15%

2% Rest of Top Players

2014 CIB PERFORMANCE

2010

2011

2012

2013

2014

2010

2011

2012

2013

2014

JPM share 10.3%

11.2%

12.0%

11.0%

11.5%

JPM rank

Strategy by business

No significant change to 2014 strategy Good track record of optimizing business under multiple constraints

Now executing on plan for G-SIB optimization

from 3Q YTD run rate. 4 FY10 JPM/TS revenue is restated to exclude Commercial Card and Standby Letters of Credit.

5

We continue to have market-leading positions in most products

Consistently delivered market leading financial performance – over $34B in net revenue in 2014, largest in the industry #1 Global IB franchise, #1 Markets franchise, leading Research platform, and a top tier Transaction Services business

exchange rates across non-USD reporting peers. 3 TS: Market includes JPM, Citi, BAC, DB, HSBC, BNP and BoNY; JPM/BAC inclusive of firm-wide TS revenue; SS: Market includes JPM, Citi, HSBC, BoNY, STT, NTRS, Soc Gen and BNP; NTRS FY 2014 derived

measures which exclude the impact of FVA (effective 2013) and DVA on: revenues, net income, overhead ratio, comp/revenue ratio, non-comp/revenue ratio and return on equity. These measures are used by

2010

2011

2012

2013

Volatility4

JPM Top-10 Peers

2014

CIB 4% 6%

Markets 4% 11%

Fixed Income

6%

15%

1 CIB net revenue excludes FVA/DVA for 2013 and prior years; product splits additionally exclude the remaining impact of Credit Adjustments & Other.

4 Standard deviation divided by average over 2010-2014 period.

4

Equities 4% 7%

Strong share position and gains over multi-year period

2010 – 2014 Growth in Revenue Pools by Product (charts indexed to 2010)

Top 3 2nd Tier 3rd Tier

Competitive ranking in 16 product areas

Best-in-class returns with low revenue volatility Leading market share across all major business lines World-class franchise: unique scale, completeness, global reach Strong long-term prospects

CORPORATE & INVESTMENT BANK

Daniel Pinto, Chief Executive Officer Corporate & Investment Bank

February 24, 2015

Topics for discussion

Financial performance

JPM

(9%)

Rest of Top 10 (36%)

2012 7.5%

#1

2013 8.5%

#1

2014 8.1%

#1

2010 13.8%

#1

2011 17.8%

#1

2012 17.2%

#1

2013 19.7%

#1

2014 18.6%

#1

Treasury Services + Securities Services3,4

2014 CIB PERFORMANCE

1 Net revenues, net income, ROE, and overhead ratio excluding FVA (effective 2013) and DVA, are non-GAAP financial measures. Throughout this presentation, CIB provides several non-GAAP financial

management to assess the underlying performance of the business and for comparability with peers. For additional information on non-GAAP measures, please refer to the Notes section of the Firmwide

presentation.

2 All years are restated for preferred dividends. 3 All years are restated to exclude the impact of legal expense.

3

2014 CIB PERFORMANCE

Revenue diversification and scale drive stability

18%

$56.5

73

68

13%

63

$61.0

58

53

2010 2011 2012 2013 2014 Highlights

2010 2011 2012 2013 2014

$46.5

2010

$47.0

2011

$47.5

2012

+$13.5B 48 (up 28%)

43

2013 2014

Unparalleled client franchise with over 51,000 employees in 60 countries serving 7,200 of the world’s most significant corporates and financial institutions, governments and non-profit institutions

Net income1,2,3 ($B)

ROE1,3 (%) and capital ($B)

O/H ratio1,3

64% 66% 61% 58% 62% $33.4 $33.0 $35.7 $36.7 $34.6

$34.7

$10.4

$9.3

$8.5 $7.5

$8.9

$8.7

ቤተ መጻሕፍቲ ባይዱ

18%

19% 15% 17%

Page 2

11 23 27

CORPORATE & INVESTMENT BANK

2

CIB has a proven track record of strong and stable performance despite recent

headwinds

5 year average

Net revenues and O/H1,2 ($B)

#5

#4

#4

#4

#3

Treasury Services: Top 2; Sec. Services: Top 3

1 Industry revenue pool; revenue, wallet rank and share per Dealogic. 2 Revenues of 10 leading peers (JPM, GS, MS, C, BAC, CS, BARC, UBS, DB, HSBC), excluding FVA/DVA & one-time items and includes JPM preferred restatement; HSBC and BARC as of LTM3Q14; Based on 4Q

Global IB Fees – Dealogic1