债券市场及答案

债券市场分析与策略课后答案

债券市场分析与策略课后答案债券市场分析与策略课后答案第一部分:债券市场概述1. 什么是债券?答:债券是一种固定收益证券,指的是发行人向投资者发行债务证券,承诺在一定期间里按照约定的利率向投资者支付利息,并在到期日向投资者支付本金和最后一期利息。

投资者购买债券即为给发行人借款,债券的利率也称为债券收益率。

2. 债券市场的类型有哪些?答:债券市场的类型可以分为一级市场和二级市场。

一级市场也称为新股发行市场,是指债券发行时通过证券公司向广大投资者公开发行的场所。

二级市场也称为交易市场,是指投资者之间在证券交易所进行交易的场所。

3. 债券市场的功能有哪些?答:债券市场的主要功能包括为企业融资、为投资者提供固定收益投资机会、为政府调控经济提供手段等。

第二部分:债券风险与收益1. 债券风险可以分为哪些?答:债券风险可以分为违约风险、利率风险、市场风险和通胀风险。

2. 债券收益有哪些?答:债券收益可以分为票面利率收益和资本利得收益。

票面利率收益即为债券的利率收益,资本利得收益是指在债券购买时市场利率高于债券的票面利率,到期时债券价格上涨后所获得的溢价收益。

第三部分:债券分析与投资1. 什么是债券评级?答:债券评级是一种专业机构对债券信用风险的评估,并对债券进行等级标记,以提供投资者参考。

目前国内主要的债券评级机构有中诚信国际、联合信用评估等。

2. 债券分析的方法有哪些?答:常见的债券分析方法包括基本面分析、技术分析和宏观经济分析。

基本面分析着重考虑发行人的财务状况、经营状况和行业发展等情况。

技术分析主要从股票、期货市场的技术分析方法引入,对债券市场的交易趋势和价格进行分析。

宏观经济分析是从宏观环境中的经济因素对债券市场的影响进行分析。

3. 债券投资的策略有哪些?答:债券投资的策略可以从投资期限、风险偏好等方面进行考虑,包括买入看涨期权、减少风险并提高收益、购买高评级债券等策略。

常用的策略包括买入长期低风险债券、多元化配置固定收益投资品种等。

债券交易 练习题

天梯金融培训金融市场基础知识债券交易练习题一、单选题(43)1、下列选项中,不属于债券交易市场构成的是()。

A.中介服务机构B.发行者C.交易者D.市场监督者参考答案:B解析:债券交易市场是指已经发行的债券的流通交易场所,又称二级市场。

交易市场由各类交易者、中介服务机构以及市场监督者构成。

2、我国债券市场的主要交易场所是()。

A.由机构投资者参与的银行间市场B.由证券公司参与的交易所债券市场C.由个人投资者参与的银行柜台市场D.由证券公司参与的银行间市场参考答案:A解析:由机构投资者参与的银行间市场是我国债券市场的主天梯金融培训要交易场所,近年的债券托管量和交易量都占整个市场的90%左右。

3、仅面向中小企业和个人的债券交易市场是()。

A.银行间市场B.交易所债券市场C.网上债券市场D.柜台债券市场参考答案:D解析:柜台债券市场作为银行间市场的延伸,仅面向中小企业和个人,每个投资者以承办银行为交易对手,通过商业银行的营业网点进行记账式国债的买卖,属于零售市场。

4、在证券交易所进行债券交易时,遵循()原则,采用公开竞价方式进行。

A.价格优先、时间优先B.数量优先、时间优先C.时间优先、总额优先D.价格优先、数量优先参考答案:A解析:在三个证券交易所上市的债券有国债、企业债券、可转换债券等。

投资者实行会员制,市场参与者主要包括证券公司、天梯金融培训基金公司、保险公司、企业和个人等投资者,投资者将买卖指令输入交易所的电子系统,由电子系统集中撮合完成交易。

在进行交易时,遵循“价格优先、时间优先”的原则,采用公开竞价的方式进行。

5、银行间债券市场的清算平台是()。

A.中国证券登记结算有限公司B.银行柜台C.上海清算所D.中国人民银行参考答案:C解析:银行间债券市场的清算平台是上海清算所;交易所债券市场的清算平台是中国证券登记结算有限公司;银行柜台市场的清算平台是银行柜台。

6、债券市场最早出现和最基本的交易工具是()A.现券买卖B.回购交易C.远期交易D.期货交易参考答案:A解析:现券买卖是债券市场最早出现和最基本的交易工具。

证券金融基础知识(债券市场)习题及答案

1、(单选题)债券是一种有价证券,是社会各类经济主体为筹集资金而向债券投资者出具的、承诺按一定利率定期支付利息的并到期偿还本金的()凭证。

A.债权债务B.所有权、使用权C.权利义务D.转让权【答案】:A2、(多选题)以下关于债券基本性质描述正确的有()。

A.债券属于有价证券B.债券是一种虚拟资本C.债券是债权的体现D.债券是一种综合权利证券【答案】:ABC3、(多选题)下列关于政府债券的性质描述,正确的是()。

A.从形式上看,政府债券也是一种有价证券,它具有债券的一般性质B.政府债券本身无面额,但投资者投资于政府债券同样可以取得利息C.政府债券最初是政府弥补赤字的手段D.政府债券是政府筹集资金、扩大公共事业开支的重要手段【答案】:ACD4、(多选题)下列各项可转换债券的基本性质的说法中,正确的有()。

A.可转换债券一般都会有赎回条款B.公司股票价格在一段时期内连续高于转股价格并且达到某一幅度时赎回C.公司股票价格在一段时期内连续低于转股价格并且达到某一幅度时回售D.可转换债券转换成股票后,属于股权性质【答案】:ABCD5、(单选题)下面关于债券的叙述正确的是()。

A.债券尽管有面值,代表了一定的财产价值,但它也只是一种虚拟资本,而非真实资本B债权人除了按期取得本息外,对债务人也可以作其他干预C.由于债券期限越长,流动性越差,风险也就越大,所以长期债券的票面利率肯定高于短期债券的票面利率D.流通性是债券的特征之一,也是国债的基本特点,所有的国债都是可流通的【答案】:A6、(多选题)债券的票面要素有()。

A.发行单位的名称B.债券的票面金额C.债券的发行日期D.债券的票面利率【答案】:ABCD7、(单选题)下列关于债券的特征说法正确的是()。

A.债务人必须按期向债权人支付利息和偿还本金B.永续债的存在说明偿还性不是债券的一般特性C.债券的收益随发行者经营收益的变动而变动D.具有高度流动性的债券反而不安全【答案】:A8、(多选题)以下关于债券特征的表述中,正确的有()A.一般都可在流通市场上自由转让变现B.债券有规定的偿还期限,债务人必须按期向债权人偿还本金和支付利息C.债券期限越短时,债券的流动性就越强D.债券的收益主要来源于股息红利E.债券发行人的信用程度越高,债券的流动性就越强【答案】:ABCE9、(多选题)债券按发行主体可分为()。

债券市场与债券投资练习试卷1(题后含答案及解析)

债券市场与债券投资练习试卷1(题后含答案及解析) 题型有:1.1.与股票相比,债券所具有的最突出的特征是( )。

A.流动性B.风险性C.返还性D.收益性正确答案:C解析:债券具有返还性,而股票不具备。

知识模块:债券市场与债券投资2.同一时期发行的下列投资工具中,风险最低的是( )。

A.3个月期商业票据B.公司债券C.3个月期国库券D.长期国债正确答案:C解析:相对于公司债与商业票据,短期国债和中长期国债的发行主体是财政部,信用风险低;相对于长期国债,短期国债期限短,利率风险小。

知识模块:债券市场与债券投资3.某国库券还有半年到期,面值100元,现在价格96元,投资该国库券获得的等价收益率为( )。

A.8.00%B.8.16%C.8.33%D.8.51%正确答案:C解析:[(100-96)/96]×2=8.33% 知识模块:债券市场与债券投资4.某售价为96元,面值为100元的国库券,还有184天到期,下列说法正确的是( )。

A.该国库券的贴现收益率为7.13%B.该国库券的等价收益率为7.83%C.该国库券的有效年收益率为8.27%D.该国库券的有效年收益率为8.43%正确答案:D解析:贴现收益率RDY=(100-96)/100×360/184=7.83%,等价收益率REY=(100-96)/96×365/184=8.27%,有效年收益率REAR=[1+(100-96)/96]365/184-1=8.43% 知识模块:债券市场与债券投资5.期限为191天、票面价值100元的国库券,它的要价收益率为4.55%,那么投资者购买该国库券所需要支付的金额是( )。

A.93.93元B.96.70元C.97.67元D.98.15元正确答案:C解析:要价收益率实际上是与要价相对应的等价收益,4.55%=(100-P)/P×365/191,解得P=97.67元知识模块:债券市场与债券投资6.某国库券还有90天到期,面值100元,现价98元,则投资该国库券的等价收益率为( )。

第三章 债券 所有例题与答案

第三章债券第一节债券的特征与类型一、债券的定义与特征(一)债券的定义债券是一种有价证券,是社会各类经济主体为筹集资金而向债券投资者出具的、承诺按一定利率定期支付利息并到期偿还本金的债权债务凭证。

债券上规定资金借贷的权责关系主要有三点:第一,所借贷货币的数额;第二,借款时间;第三,在借贷时间内应有的补偿或代价是多少(即债券的利息)。

【例题1·单选题】债券是一种有价证券,是社会各类经济主体为筹集资金而向债券投资者出具的、承诺按一定利率定期支付利息的并到期偿还本金的()凭证。

A.设权B.所有权C.债权债务D.使用权[答疑编号1761030101]『正确答案』C【例题2·多选题】债券所规定的资金借贷双方的权责关系主要有()。

A.借贷的时间B.借贷货币资金的币种C.所借贷货币资金的数额D.在借贷时间内的资金成本或应有的补偿[答疑编号1761030102]『正确答案』ACD(二)债券的票面要素1.债券的票面价值。

2.债券的到期期限。

3.债券的票面利率4.债券发行者名称【例题·判断题】一般来说,当未来市场利率趋于下降时,应选择发行期限较长的债券。

()[答疑编号1761030103]『正确答案』错(三)债券的特征【例题1·多选题】债券的特征包括()。

A.偿还性B.收益性C.安全性D.永久性[答疑编号1761030104]『正确答案』ABC【例题2·判断题】在实际经济活动中,债券收益可以表现为三种形式:一是利息收入,二是资本损益,三是再投资收益。

()[答疑编号1761030105]『正确答案』对二、债券的分类(一)按发行主体分类1.政府债券。

2.金融债券。

3.公司债券。

【例题1·单选题】根据发行主体的不同,债券可以分为()。

A.国债和地方债券B.政府债券、金融债券和公司债券C.实物债券、凭证式债券和记账式债券D.零息债券、附息债券和息票累积债券[答疑编号1761030106]『正确答案』B【例题2·判断题】金融债券的发行主体是银行或非银行的金融机构。

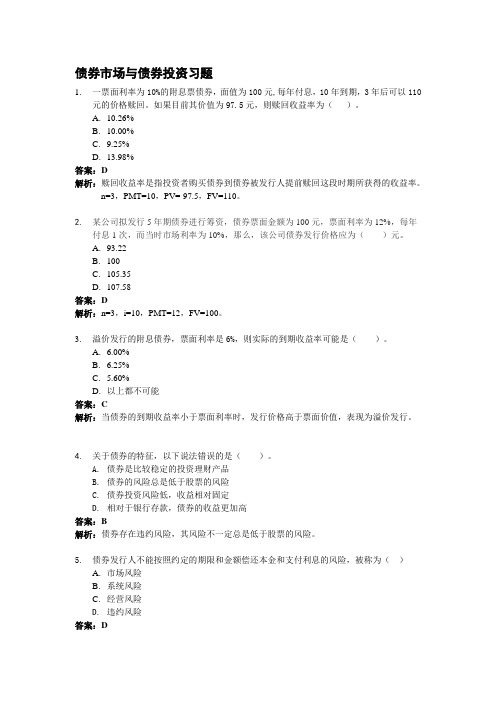

债券市场与债券投资习题

债券市场与债券投资习题1.一票面利率为10%的附息票债券,面值为100元,每年付息,10年到期,3年后可以110元的价格赎回。

如果目前其价值为97.5元,则赎回收益率为()。

A.10.26%B.10.00%C.9.25%D.13.98%答案:D解析:赎回收益率是指投资者购买债券到债券被发行人提前赎回这段时期所获得的收益率。

n=3,PMT=10,PV=-97.5,FV=110。

2.某公司拟发行5年期债券进行筹资,债券票面金额为100元,票面利率为12%,每年付息1次,而当时市场利率为10%,那么,该公司债券发行价格应为()元。

A.93.22B.100C.105.35D.107.58答案:D解析:n=3,i=10,PMT=12,FV=100。

3.溢价发行的附息债券,票面利率是6%,则实际的到期收益率可能是()。

A. 6.00%B. 6.25%C. 5.60%D.以上都不可能答案:C解析:当债券的到期收益率小于票面利率时,发行价格高于票面价值,表现为溢价发行。

4.关于债券的特征,以下说法错误的是()。

A.债券是比较稳定的投资理财产品B.债券的风险总是低于股票的风险C.债券投资风险低,收益相对固定D.相对于银行存款,债券的收益更加高答案:B解析:债券存在违约风险,其风险不一定总是低于股票的风险。

5.债券发行人不能按照约定的期限和金额偿还本金和支付利息的风险,被称为()A.市场风险B.系统风险C.经营风险D.违约风险答案:D解析:债券的违约风险是指发行者不能履行合约,无法按期还本付息,也叫信用风险。

6.考虑一债券,票面利率为10%,现在市场利率为8%,如果目前市场利率上升0.5%与下降0.5%,则()A.利率上升0.5%使债券价格下降幅度大于利率下降0.5%使债券上升幅度B.利率上升0.5%使债券价格下降幅度小于利率下降0.5%使债券上升幅度C.利率上升0.5%使债券价格下降幅度等于利率下降0.5%使债券上升幅度D.条件不足,无法判定答案:B解析:利率上升所引起价格的下降幅度小于因利率相同程度的下降而引起的价格的上升。

债券培训练习题(含答案)

固定收益培训课后练习卷1.以下关于债券说法正确的是()(单选)A.不同于股票,投资债券没有任何风险B.只有当持有到期时,投资债券没有任何风险C.赎回权是到期条款中投资者可以行使的权利D.回售权是到期条款中有利于投资者的条款答案:D2.以下债券全部属于信用债券的是()(单选)A.国债公司债B.央票企业债C.政策性金融债中期票据D.短融企业债答案:D3.债券按照交易场所可以分为()(单选)A.公募债券和私募债券B.银行间债券和交易所债券C.利率产品和信用产品D.以上说法均不正确答案:B4.以下关于债券收益率说法正确的为()(多选)A.市场中债券报价用的收益率是票面利率B.市场中债券报价用的收益率是到期收益率C.同一只债券,到期收益率越高,债券的价格越低D.同一只债券,到期收益率越高,债券的价格越高答案:B、C5.以下关于市场利率的期限结构说法错误的是()(单选)A.利率的期限结构是指债券收益率与到期日之间的关系B.预期理论认为长期收益率是由现在的和未来的短期利率预期决定的C.市场分割理论认为长期收益率是由整个债券市场的供需关系决定的D.风险溢价理论认为长期收益率是由投资者风险偏好决定的答案:C6.李先生买入一只剩余期限为3年的公司债,并打算持有到期,则该投资者面临以下风险中的哪种()(单选)A.信用风险B.利率风险C.流动性风险D.以上三者都有答案:A7.以下关于久期的说法正确的是()(单选)A.债券的剩余期限越长,其久期越短B.对于同期限的债券,债券的票面利率越高,其久期越短C.久期是用来衡量信用风险的指标D.久期越大,债券的风险越小8.债券投资组合中,所投资的债券的期限非常接近的投资策略为()(单选)A.杠铃策略B.子弹策略C.阶梯策略D.以上均不正确答案:B9.以下策略中不属于积极的投资策略的是()(单选)A.利率预期策略B.持有到期策略C.收益率价差策略D.资产分配策略答案:B10.以下衍生品中不能用来对冲利率产品风险的为()(单选)A.利率互换B.国债期货C.信用违约互换D.利率期权答案:C11.关于利率水平说法正确的为()(单选)A.通胀水平走高,市场预期利率水平会走高B.经济增长超预期,市场预期利率水平会走低C.央行采用宽松的货币政策,市场预期利率水平会走高D.以上说法均不正确答案:A12.假设投资者持有一只债券,当期市场价格为97,面值为100,久期为2.4,则当市场收益率上升1%时,该债券的价格变化约为()(单选)A.上涨100×2.4×1%B.上涨97×2.4×1%C.下跌100×2.4×1%D.下跌97×2.4×1%答案:D13.对于AA级5年期公司债A,其信用利差为()(单选)A.债券A的收益率—AA级1年期信用债收益率水平B.债券A的收益率—5年期国债收益率水平C.债券A的收益率—1年期国债收益率水平D.1年期国债收益率水平—债券A的收益率答案:B14.假设债券A目前的市场价格为102,面值为100,票面利率为4%,剩余期限为2.5年,该债券每年付息一次,则该债券的到期收益率r满足下列式子()(单选)答案:C15.投资者于2011年9月22日购买债券A,该债券的净价报价为97.5,债券票面利率为5%,付息日为8月6日,已知8月6日距9月22日有46天,则投资者买入该债券实际付出的价格为()(单选)B.97.5+100×5%C.97.5+100×5%×(46/360)D.97.5+100×5%×(365-46)/360答案:C16.按照发行量和托管量衡量,我国债券市场的主体市场是()(单选)A.银行间市场B.交易所市场C.商业银行柜台市场D.其他市场答案:A17、上海证券交易所独有的债券交易平台是()(单选)A.竞价交易平台B.固定收益平台C.大宗交易平台D.无答案:B18、银行间市场的主要结算和托管机构()(多选)A.中国证券登记结算公司B.中央国债登记结算有限责任公司C.上海清算所D.中国银行间市场交易商协会答案:BC19、按照银行间市场的托管账户体系,以下哪类账户可以作为直接结算成员()(多选)A.甲类账户B.乙类账户C.丙类账户D.丁类账户答案:AB20、按照银行间市场的托管账户体系,以下哪类账户可以作为结算代理人()(单选)A.甲类账户B.乙类账户C.丙类账户D.丁类账户答案:A21、下面选项哪个是银行间市场发行的企业债“10长高新债”的正确编码()(单选)A.122008B.1080008C.1081008D.1082008答案:B22、债券编码为“019110”的债券名称是()(单选)A.10传化CP01—银行间发行的传化集团有限公司2010年度第一期短期融资券B.11众和债—上交所发行的2011年新疆众和股份有限公司公司债券C.11国债10—银行间发行的2011年记账式附息(十期)国债D.11国债10—上交所发行的2011年记账式附息(十期)国债答案:D23、交易所和银行间市场的比较,错误的选项是()(单选)A.交易所市场是场外市场。

债券市场分析与策略第版答案完整版

债券市场分析与策略第版答案Document serial number【NL89WT-NY98YT-NC8CB-NNUUT-NUT108】CHAPTER 4BOND PRICE VOLATILITYCHAPTER SUMMARYTo use effective bond portfolio strategies, it is necessary to understand the price volatility of bonds resulting from changes in interest rates. The purpose of this chapter is to explain the price volatility characteristics of a bond and to present several measures to quantify price volatility.REVIEW OF THE PRICE-YIELD RELATIONSHIP FOR OPTION-FREE BONDSAn increase (decrease) in the required yield decreases (increases) the present value of its expected cash flows and therefore decreases (increases) the bond’s price. This relationship is not linear. The shape of the price-yield relationship for any option-free bond is referred to as a convex relationship.PRICE VOLATILITY CHARACTERISTICS OF OPTION-FREE BONDSThere are four properties concerning the price volatility of an option-free bond. (i) Although the prices of all option-free bonds move in the opposite direction from the change in yield required, the percentage price change is not the same for all bonds. (ii) For very small changes in the yield required, the percentage price change for a given bond is roughly the same, whether the yield required increases or decreases. (iii) For large changes in the required yield, the percentage price change is not the same for an increase in the required yield as it is for a decrease in the required yield. (iv) For a given large change in basis points, the percentage price increase is greater than the percentage price decrease.An explanation for these four properties of bond price volatility lies in the convex shape of the price-yield relationship.Characteristics of a Bond that Affect its Price VolatilityThere are two characteristics of an option-free bond that determine its price volatility: coupon and term to maturity.First, for a given term to maturity and initial yield, the price volatility of a bond is greater, the lower the coupon rate. This characteristic can be seen by comparing the 9%, 6%, and zero-coupon bonds with the same maturity. Second,for a given coupon rate and initial yield, the longer the term to maturity, the greater the price volatility.Effects of Yield to MaturityA bond trading at a higher yield to maturity will have lower price volatility. An implication of this is that for a given change in yields, price volatility is greater when yield levels in the market are low, and price volatility is lower when yield levels are high.MEASURES OF BOND PRICE VOLATILITYMoney managers, arbitrageurs, and traders need to have a way to measure a bond’s price volatility to implement hedging and trading strategies. Three measures that are commonly employed are price value of a basis point, yield value of a price change, and duration.Price Value of a Basis PointThe price value of a basis point, also referred to as the dollar value of an 01, is the change in the price of the bond if the required yield changes by 1 basis point. Note that this measure of price volatility indicates dollar price volatility as opposed to percentage price volatility (price change as a percent of the initial price). Typically, the price value of a basis point is expressed as the absolute value of the change in price. Price volatility is the same for an increase or a decrease of 1 basis point in required yield.Because this measure of price volatility is in terms of dollar price change, dividing the price value of a basis point by the initial price gives the percentage price change for a 1-basis-point change in yield.Yield Value of a Price ChangeAnother measure of the price volatility of a bond used by investors is the change in the yield for a specified price change. This is estimated by first calculating the bond’s yield to maturity if the bond’s price is decreased by, say, X dollars. Then the difference between the initial yield and the new yield is the yield value of an X dollar price change. The smaller this value, the greater the dollar price volatility, because it would take a smaller change in yield to produce a price change of X dollars.DurationThe Macaulay duration is one measure of the approximate change in price for a small change in yield.Macaulay duration = ()()()() 12121111n nC C nC nM+ +. . .+ +y y y yP++++where P = price of the bond, C = semiannual coupon interest (in dollars), y = one-half the yield to maturity or required yield, n = number of semiannual periods (number of years times 2), and M = maturity value (in dollars).Investors refer to the ratio of Macaulay duration to 1 + y as the modified duration. The equation is:modified duration = 1Macaulay duration y+.The modified duration is related to the approximate percentage change in price for a given change in yield as given by:Pdy dP 1= modified duration.Because for all option-free bonds modified duration is positive, the above equation states that there is an inverse relationship between modified duration and the approximate percentage change in price for a given yield change. This is to be expected from the fundamental principle that bond prices move in the opposite direction of the change in interest rates.In general, if the cash flows occur m times per year, the durations are adjusted by dividing by m , that is,duration in years = myear per periods m in duration .We can derive an alternative formula that does not have the extensive calculations of the Macaulay duration and the modified duration. This is done by rewriting the price of a bond in terms of its two components: (i) the present value of an annuity, where the annuity is the sum of the coupon payments, and (ii) the present value of the par value. By taking the first derivative and dividing by P, we obtain another formula for modified duration given by:modified duration = ()()()12100111n n n C /y C 1 y y y P+-⎡⎤-+⎢⎥++⎣⎦where the price is expressed as a percentage of par value.Properties of DurationThe modified duration and Macaulay duration of a coupon bond are less than the maturity. The Macaulay duration of a zero-coupon bond is equal to its maturity;a zero-coupon bond’s modified duration, however, is less than its maturity. Also, lower coupon rates generally have greater Macaulay and modified bond durations.There is a consistency between the properties of bond price volatility and the properties of modified duration. For example, a property of modified duration is that, ceteris paribus, bonds with longer the maturity will have greater modified durations. Also, generally the lower the coupon rate, the greater the modified duration. Thus, greater modified durations will have greater the price volatility. As we noted earlier, all other factors constant, the higher the yield level, the lower the price volatility. The same property holds for modified duration.Approximating the Percentage Price ChangeThe below equation can be used to approximate the percentage price change for a given change in required yield:PdP = (modified duration)(dy ).We can use this equation to provide an interpretation of modified duration. Suppose that the yield on any bond changes by 100 basis points. Then, substituting 100 basis points for dy into the above equation, we get:PdP = (modified duration) = (modified duration)(%).Thus, modified duration can be interpreted as the approximate percentage change in price for a 100-basis-point change in yield.Approximating the Dollar Price ChangeModified duration is a proxy for the percentage change in price. Investors also like to know the dollar price volatility of a bond. For small changes in the required yield, the below equation does a good job in estimating the change in price:dP = (dollar duration)(dy ).When there are large movements in the required yield, dollar duration or modified duration is not adequate to approximate the price reaction. Durationwill overestimate the price change when the required yield rises, thereby underestimating the new price. When the required yield falls, duration will underestimate the price change and thereby underestimate the new price.Spread DurationMarket participants compute a measure called spread duration. This measure is used in two ways: for fixed bonds and floating-rate bonds.A spread duration for a fixed-rate security is interpreted as the approximate change in the price of a fixed-rate bond for a 100-basis-point change in the spread.Portfolio DurationThus far we have looked at the duration of an individual bond. The duration of a portfolio is simply the weighted average duration of the bonds in the portfolios.Portfolio managers look at their interest rate exposure to a particular issue in terms of its contribution to portfolio duration. This measure is found by multiplying the weight of the issue in the portfolio by the duration of the individual issue given as:contribution to portfolio duration = weight of issue in portfolio x durationof issue.CONVEXITYBecause all the duration measures are only approximations for small changes in yield, they do not capture the effect of the convexity of a bond on its price performance when yields change by more than a small amount. The duration measure can be supplemented with an additional measure to capture the curvature or convexity of a bond.Measuring ConvexityDuration (modified or dollar) attempts to estimate a convex relationship with a straight line (the tangent line). We can use the first two terms of a Taylor series to approximate the price change. We get the dollar convexity measure of the bond:dollar convexity measure = 22dyP d .The approximate change in price due to convexity is:dP = (dollar convexity measure)(dy )2.The percentage change in the price of the bond due to convexity or the convexity measure is:convexity measure =221P d Pdy .The percentage price change due to convexity is:()()21convexity measure 2dP dy P =.In general, if the cash flows occur m times per year, convexity is adjusted to an annual figure as follows:convexity measure in year =yearperperiodminmeasureconvex ity2m.Approximating Percentage Price Change Using Duration and Convexity MeasuresUsing duration and convexity measures together gives a better approximation of the actual price change for a large movement in the required yield.Some Notes on ConvexityThere are three points that should be kept in mind regarding a bond’s convexity and convexity measure. First, it is important to understand the distinction between the use of the term convexity, which refers to the general shape of the price-yield relationship, and the term convexity measure, which is related to the quantification of how the price of the bond will change when interest rates change. The second point has to do with how to interpret the convexity measure. The final point is that in practice different vendors of analytical systems and different writers compute the convexity measure in different ways by scaling the measure in different ways.Value of ConvexityGenerally, the market will take the greater convexity bonds into account in pricing them. How much should the market want investors to pay up for convexity If investors expect that market yields will change by very little—that is, they expect low interest rate volatility—investors should not be willing to pay much for convexity. In fact, if the market prices convexity high, investors with expectations of low interest rate volatility will probably want to “sell convexity.”Properties of ConvexityAll option-free bonds have the following convexity properties. First, as the required yield increases (decreases), the convexity of a bond decreases (increases). This property is referred to as positive convexity. Second, for a given yield and maturity, lower coupon rates will have greater convexity. Third, for a given yield and modified duration, lower coupon rates will have smaller convexity.ADDITIONAL CONCERNS WHEN USING DURATIONRelying on duration as the sole measure of the price volatility of a bond may mislead investors. There are two other concerns about using duration that we should point out. First, in the derivation of the relationship between modified duration and bond price volatility, we assume that all cash flows for the bond are discounted at the same discount rate. Second, there is misapplication of duration to bonds with embedded options.DON’T THINK OF DURATION AS A MEASURE OF TIMEUnfortunately, market participants often confuse the main purpose of duration by constantly referring to it as some measure of the weighted average life of a bond. This is because of the original use of duration by Macaulay.APPROXIMATING A BOND’ S DURATION AND CONVEXITY MEASUREWhen we understand that duration is related to percentage price change, a simple formula can be used to calculate the approximate duration of a bond or any other more complex derivative securities or options described throughout this book. All we are interested in is the percentage price change of a bond when interest rates change by a small amount. The equation is:approximate duration = ()()02_P P P y +-∆where y is the change in yield used to calculate the new prices (in decimal form). What the formula is measuring is the average percentage price change (relative to the initial price) per 1-basis-point change in yield. It is important to emphasize here that duration is a by-product of a pricing model. If the pricing model is poor, the resulting duration estimate is poor.The convexity measure of any bond can be approximated using the following formula:approximate convexity measure = ()0202P P P P y +-+-∆.Duration of an Inverse FloaterThe duration of an inverse floater is a multiple of the duration of the collateral from which it is created. Assuming that the duration of the floateris close to zero, it can be shown that the duration of an inverse floater is as follows:duration of an inverse floater = (1 + L)(duration of collateral) Xcollateral pricesinverse priceswhere L is the ratio of the par value of the floater to the par value of the inverse floater.MEASURING A BOND PORTFOLIO’S RESPONSIVENESS TONONPARALLEL CHANGES IN INTEREST RATESThere have been several approaches to measuring yield curve risk. The two major ones are yield curve reshaping duration and key rate duration.Yield Curve Reshaping DurationThe yield curve reshaping duration approach focuses on the sensitivity of a portfolio to a change in the slope of the yield curve.Key Rate DurationThe most popular measure for estimating the sensitivity of a security or a portfolio to changes in the yield curve is key rate duration. The basic principle of key rate duration is to change the yield for a particular maturity of the yield curve and determine the sensitivity of a security or portfolio to that change holding all other yields constant.ANSWERS TO QUESTIONS FOR CHAPTER 4(Questions are in bold print followed by answers.)1. The price value of a basis point will be the same regardless if the yield is increased or decreased by 1 basis point. However, the price value of 100 basis points ., the change in price for a 100-basis-point change in interest rates) will not be the same if the yield is increased or decreased by 100 basis points. WhyThe convex relationship explains why the price value of a basis point ., the change in price for a 1-basis-point change in interest rates) will be roughly the same regardless if the yield is increased or decreased by 1 basis point, while the price value of 100 basis points will not be the same if the yield is increased or decreased by 100 basis points. More details are below.When the price-yield relationship for any option-free bond is graphed, it displays a convex shape. When the price of the option-free bond declines, we can observe that the required yield rises. However, this relationship is not linear. The convex shape of the price-yield relationship generates four properties concerning the price volatility of an option-free bond. First, although the prices of all option-free bonds move in the opposite direction from the change in yield required, the percentage price change is not the same for all bonds. Second, for very small changes in the yield required (like 1 basis point), the percentage price change for a given bond is roughly the same, whether the yield required increases or decreases. Third, for large changes in the required yield (like 100 basis points), the percentage price change is not the same for an increase in the required yield as it is for a decrease in the required yield. Fourth, for a given large change in basis points, the percentage price increase is greater than the percentage price decrease.2. Calculate the requested measures in parts (a) through (f) for bonds A andB (assume that each bond pays interest semiannually):Bond A Bond BCoupon8%9%8%8%Yield tomaturityMaturity (years)25Par$$Price$$(a) What is the price value of a basis point for bonds A and BFor bond A, we get a bond quote of $ for our initial price if we have a 2-year maturity, an 8% coupon rate and an 8% yield. If we change the yield one basis point so the yield is %, then we have the following variables and values:C = $40, y = / 2 = and n = 2(2) = 4.Inserting these values into the present value of the coupon payments formula, we get:()111n + r P = C r ⎡⎤-⎢⎥⎢⎥⎣⎦=()411 1 .04005$40 0.04005⎡⎤-⎢⎥⎢⎥⎣⎦= $.Computing the present value of the par or maturity value of $1,000 gives:()1n M r + = 4$1,000(1.04005)= $.If we add a basis point to the yield, we get the value of Bond A as: P = $ + $ = $ with a bond quote of $. For bond A the price value of a basis point is about $100 – $ = $ per $100.Using the bond valuation formulas as just completed above, the value of bondB with a yield of 8%, a coupon rate of 9%, and a maturity of 5 years is: P = $ + $ = $1, with a bond quote of $. If we add a basis point to the yield, we get the value of Bond B as: P = $ + $ = $1, with a bond quote of $. For bond B , the price value of a basis point is $ – $ = $ per $100.(b) Compute the Macaulay durations for the two bonds.For bond A with C = $40, n = 4, y = , P = $1,000 and M = $1,000, we have:Macaulay duration (half years) = ()()()()12121111n n C C nC nM + +. . .+ + y y y y P++++ =()()()()12441($40)2($40)4($40)4($1,000)1.04 1.04 1.04 1.04$1,000 + +. . .+ + = 000,1$09.775,3$ = .Macaulay duration (years) = Macaulay duration (half years) / 2 = / 2 = .For bond B with C = $45, n = 10, y = , P= $1, and M = $1,000, we have:Macaulay duration (half years) = ()()()()12121111n n C C nC nM + +. . .+ + y y y y P++++ =()()()()12441($45)2($45)10($45)10($1,000)1.04 1.04 1.04 1.04$1,040.55 + +. . .+ + = 55.040,1$2929.645,8$ = .Macaulay duration (years) = Macaulay duration (half years) / 2 = / 2 = .(c) Compute the modified duration for the two bonds.Taking our answer for the Macaulay duration in years in part (b), we can compute the modified duration for bond A by dividing by . We have:modified duration = Macaulay duration / (1+y) = / = .Taking our answer for the Macaulay duration in years in part (b), we can compute the modified duration for bond B by dividing by . We have:modified duration = Macaulay duration / (1+y) = / = .[NOTE. We could get the same answers for both bonds A and B by computing the modified duration using an alternative formula that does not require the extensive calculations required by the procedure in parts (a) and (b). This shortcut formula is:modified duration = ()()()12100111n n n C /y C 1 y y y P+-⎡⎤-+⎢⎥++⎣⎦.where C is the semiannual coupon payment, y is the semiannual yield, n is the number of semiannual periods, and P is the bond quote in 100’s.For bond A (expressing numbers in terms of a $100 bond quote), we have: C = $4, y = , n = 4, and P = $100. Inserting these values in our modified duration formula, we can solve as follows:()() ()12100111n nn C/yC1y y yP +-⎡⎤-+⎢⎥++⎣⎦ =()4524$100 $4/0.04 $411(1 .04(1 .04))0.04$100-⎡⎤-+⎢⎥⎣⎦ =($ + $0) / $100 = . Converting to annual number by dividing by two gives a modified duration for bond A of which is the same answer shown above.For bond B, we have C = $, n = 20, y = , and P = $. Inserting these values in our modified duration formula, we can solve as follows:()() ()12100111n nn C/yC1y y yP +-⎡⎤-+⎢⎥++⎣⎦ =()101124$100 $4.5/0.04 $4.511(1 .04(1 .04))0.04$104.055-⎡⎤-+⎢⎥⎣⎦ =($ –$ / $ = . Converting to annual number by dividing by two gives a modified duration for bond B of which is the same answer shown above.](d) Compute the approximate duration for bonds A and B using the shortcut formula by changing yields by 20 basis points and compare your answers with those calculated in part (c).To compute the approximate measure for bond A, which is a 2-year 8% coupon bond trading at 8% with an initial price (P0) of $1,000 (thus, it trades at its par value of $1,000), we proceed as follows.First, we increase the yield on the bond by 20 basis points from 8% to %. Thus, y is % or in decimal form. The new price (P+) can be computed using our bond valuation formula. Doing this we get $ with a bond price quote of $.Second, we decrease the yield on the bond by 20 basis points from 8% to %. The new price (P_) can be computed using our bond valuation formula. Doing this we get $1, with a bond price quote of $.Third, with the initial price, P0, equal to $100 (when expressed as a bond quote), the duration can be approximated as follows:approximate duration = ()()02_P P P y +-∆where y is the change in yield used to calculate the new prices (in decimal form). What the formula is measuring is the average percentage price change (relative to the initial price) per 20-basis-point change in yield. Inserting in our values, we have:approximate duration = )02.0)(100($26379.99$ 100.3638$ -= .This compares with computed in part (c). Thus, the approximate duration measure (to six decimal places for this problem) is the same as the modified duration computed in part (c).To compute the approximate measure for bond B , which is a 5-year 9% coupon bond trading at 8% with an initial price (P 0) of $, we proceed as follows.First, we increase the yield on the bond by 20 basis points from 8% to %. Thus, y is . The new price (P +) can be computed using our bond valuation formula. Doing this we get $1, with a bond price quote of $.Second, we decrease the yield on the bond by 20 basis points from 8% to %. The new price (P_) can be computed using our bond valuation formula. Doing this we get $1, with a bond price quote of $.Third, with the initial price, P 0, equal to $ (when expressed as a bond quote),the duration can be approximated as follows:approximate duration = ()()02_P P P y +-∆where y is the change in yield used to calculate the new prices (in decimal form). What the formula is measuring is the average percentage price change (relative to the initial price) per 20-basis-point change in yield. Inserting in our values, we have:approximate duration = )02.0)(104.0554($203.22831$ 8909.104$ -= .This compares with computed in part (c). Thus, the approximate duration measure is virtually the same as the modified duration computed in part (c).Besides the above approximate duration approach, there is another approach that is shorter than the Macaulay duration and modified duration approach. With this approach, we proceed as follows. For bond A, we add 20 basis points and get a yield of %. We now have C = $40, y = %, n = 4, and M = $1,000. Before we use this shortcut approach, we first compute P. As given above, we can use our bond valuation formula to get $.Now we can compute the modified duration for bond A using the below formula: modified duration = ()()()121001111n n n C /y C y y y P+-⎡⎤-+⎢⎥++⎣⎦.Putting in all applicable variables in terms of $100, we have: C = $4, n = 4, y = and P = $. Inserting these values in our modified duration formula, we can solve as follows:()4524$100 $4 / 0.041 $41 1 (1 .041(1 .041))0.041$99.6379-⎡⎤-+⎢⎥⎣⎦ = ($ + $ / $ =. Converting to annual number by dividing by two gives a modified duration for bond A of . This compares with computed in part (c). Since both round off to , the 20 point change in basis does not exercise any noticeable effect on our computation as the difference is only – = .For bond B , we add 20 basis points and get a yield of %. We now have C = $45, y = %, n = 10, and M = $1,000. Before we use the modified duration formula, we first compute P. Using our bond valuation formula, we get $1,.Now we can compute the modified duration for bond B as above for bond A. GivenC = $, n = 10, y = , and P =$, and inserting these values into the above formula for modified duration gives:modified duration = ($ – $ / $ = .Converting to annual number by dividing by two gives a modified duration for bond B of about . This compares with computed in part (c). Since both round off to , the 20-point change in basis does not exercise any noticeable effect on our computation. However, for the two year bond, we only had a difference of about , while for the five year bond, we have a difference of about . Thus, this shortcut approach gives a wider disagreement for the longer-term bond (bond B).(e) Compute the convexity measure for both bonds A and B.In half years, the convexity measure =Pdy P d 1 22. Noting that22dy P d = ()()()()3122(1)100 /2121 111n n n n n C y C Cn y y y y y ++⎡⎤⎡⎤+-⎢⎥--+⎢⎥⎢⎥++⎢⎥+⎣⎦⎣⎦,we can insert this quantity into our convexity measure (half year) formula to get:convexity measure = ()()()()3122(1)100 /2121 111n n n n n C y C Cn y y y y y ++⎡⎤⎡⎤+-⎢⎥--+⎢⎥⎢⎥++⎢⎥+⎣⎦⎣⎦1P ⎡⎤⎢⎥⎣⎦.For bond A , we have a 2-year 8% coupon bond trading at 8% with an initial price (P 0) of $1,000 with a bond quote of $100. Expressing numbers in terms of a $100 bond quote, we have: C = $4, y = , n = 4 and P = $100. Inserting these numbers into our convexity measure formula gives:convexity measure (half years) =()()()()345624(5)100 $4/0.042($4)12($4)41 (0.04) 1.04 1.041.04(0.04)⎡⎤⎡⎤-⎢⎥--+⎢⎥⎢⎥⎢⎥⎣⎦⎣⎦⎥⎦⎤⎢⎣⎡100$1 =[$125,000(0.) – $16, + $0]1$100⎡⎤⎢⎥⎣⎦= [$18, - $16, + 0]1$100⎡⎤⎢⎥⎣⎦=1,[] = . Convexity measure (years) = year per period m in measure convex ity 2m= / 2(2) = / 4 = . Dollar convexity measure = convexity measure (years) times P = ($100) equals about $.[NOTE. We can get the same convexity by proceeding as follows. First, we increase the yield on the bond by 10 basis points from 8% to %. Thus,y is . The new price (P +) can be computed using our bond valuation formula. Doing this we get $ with a bond quote of $. Second, we decrease the yield on the bond by 10 basis points from 8% to %. The new price (P _) can be computed using our bond valuation formula. Doing this we get $. Third, with the initial price, P 0, equal to $100, the convexity measure of any bond can beapproximated using the following formula:approximate convexity measure = ()0202P P P P y +-+-∆.Inserting in our values, the approximate convexity measure for bond A isapproximate convexity measure = )001.0(100$($100)2 9.81879$ 1817.100$ 2-+= .The approximate convexity measure of is almost identical to the convexity measure of computed above.]For bond B , we have a 5-year 9% coupon bond trading at 8% with an initial price (P 0) of $. Expressing numbers in terms of a $100 bond quote, we have: C= $, y = , n = 10, and P = $. Inserting these numbers into our convexity measure formula gives:convexity measure = ()()()()3122(1)100 /2121 111n n n n n C y C Cn y y y y y ++⎡⎤⎡⎤+-⎢⎥--+⎢⎥⎢⎥++⎢⎥+⎣⎦⎣⎦1P ⎡⎤⎢⎥⎣⎦.()()()()()3101112210(11)100 $4.5/0.0452($4.5)12($4.5)101 (0.04) 1.04 1.041.040.04⎡⎤⎡⎤-⎢⎥--+⎢⎥⎢⎥⎢⎥⎣⎦⎣⎦⎥⎦⎤⎢⎣⎡0554.104$1 =[$140,625[0.] – $36, + –$1,]⎥⎦⎤⎢⎣⎡0554.104$1 = [$45, – $36, + –$]⎥⎦⎤⎢⎣⎡0554.104$1 = 8,[] = . Convexity measure (years) = year per period m in measure convex ity 2m= / 2(2) = / 4 = . Dollar convexity measure = convexity measure (years) times P = ($1,。

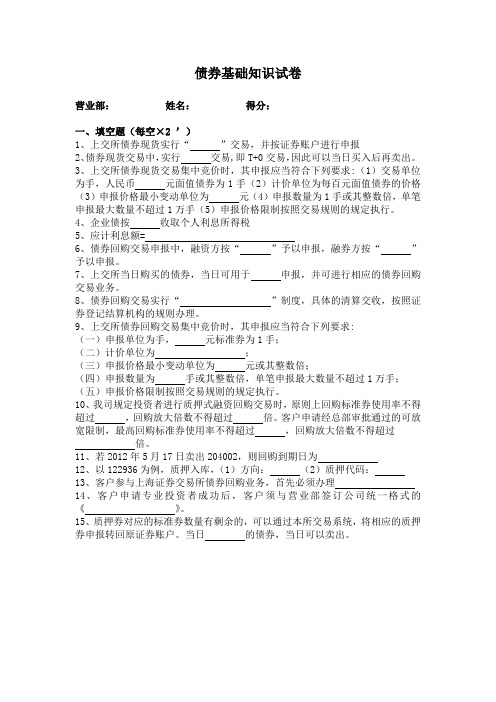

债券基础知识试卷(含参考答案)

债券基础知识试卷营业部:姓名:得分:一、填空题(每空×2 ’)1、上交所债券现货实行“”交易,并按证券账户进行申报2、债券现货交易中,实行交易,即T+0交易,因此可以当日买入后再卖出。

3、上交所债券现货交易集中竞价时,其申报应当符合下列要求:(1)交易单位为手,人民币元面值债券为1手(2)计价单位为每百元面值债券的价格(3)申报价格最小变动单位为元(4)申报数量为1手或其整数倍,单笔申报最大数量不超过1万手(5)申报价格限制按照交易规则的规定执行。

4、企业债按收取个人利息所得税5、应计利息额=6、债券回购交易申报中,融资方按“”予以申报,融券方按“”予以申报。

7、上交所当日购买的债券,当日可用于申报,并可进行相应的债券回购交易业务。

8、债券回购交易实行“”制度,具体的清算交收,按照证券登记结算机构的规则办理。

9、上交所债券回购交易集中竞价时,其申报应当符合下列要求:(一)申报单位为手,元标准券为1手;(二)计价单位为;(三)申报价格最小变动单位为元或其整数倍;(四)申报数量为手或其整数倍,单笔申报最大数量不超过1万手;(五)申报价格限制按照交易规则的规定执行。

10、我司规定投资者进行质押式融资回购交易时,原则上回购标准券使用率不得超过,回购放大倍数不得超过倍。

客户申请经总部审批通过的可放宽限制,最高回购标准券使用率不得超过,回购放大倍数不得超过倍。

11、若2012年5月17日卖出204002,则回购到期日为12、以122936为例,质押入库,(1)方向:(2)质押代码:13、客户参与上海证券交易所债券回购业务,首先必须办理14、客户申请专业投资者成功后,客户须与营业部签订公司统一格式的《》。

15、质押券对应的标准券数量有剩余的,可以通过本所交易系统,将相应的质押券申报转回原证券账户。

当日的债券,当日可以卖出。

二、简答题(每题×5 ’)1、如何计算应计利息额2、列举债券的相关风险3、列举上交所债券回购期限及代码4、购回价计算公式为5、如果在回购到期日(T日),客户不能支付到期应付款,属于违约行为(交收缺口部分下称“违约交收金额”)。

政府债券考试试题及答案解析

政府债券考试试题及答案解析一、单选题(本大题14小题.每题0.5分,共7.0分。

请从以下每一道考题下面备选答案中选择一个最佳答案,并在答题卡上将相应题号的相应字母所属的方框涂黑。

)第1题通常,被认为安全性最强的金融工具是( )。

A 商业票据B 企业债券C 国库券D 股票【正确答案】:C【本题分数】:0.5分【答案解析】[解析] ABCD四项金融工具的安全性由弱到强的顺序为:股票、商业票据、企业债券、国库券。

第2题我国为增加国有银行的资本金而发行的国债是( )。

A 特种国债B 保值国债C 财政国债D 特别国债【正确答案】:D【本题分数】:0.5分【答案解析】[解析] 特别国债是为了特定的政策目标而发行的国债。

国家为了增加国有银行的资本金而发行的国债属于特别国债。

第3题在名义收益率相等的情况下,如果考虑税收的因素,下列债券使投资者获得更多收益的是( )。

A 政府债券B 公司债券C 企业债券D 金融债券【正确答案】:A【本题分数】:0.5分【答案解析】[解析] 《中华人民共和国个人所得税法》规定,个人投资的公司债券利息、股息、红利所得应纳个人所得税,但国债和国家发行的金融债券的利息收入可免纳个人所得税。

因此,在政府债券与其他证券名义收益率相等的情况下,如果考虑税收因素,持有政府债券的投资者可以获得更多的实际投资收益。

第4题政府债券的最初功能是( )。

A 弥补财政赤字B 筹措建设资金C 便于调控宏观经济D 便于金融调控【正确答案】:A【本题分数】:0.5分【答案解析】[解析] 从功能上看,政府债券最初仅是政府弥补赤字的手段,但在现代商品经济条件下,政府债券已成为政府筹集资金、扩大公共开支的重要手段,并且随着金融市场的发展,逐渐具备了金融商品和信用工具的职能,成为国家实施宏观经济政策、进行宏观调控的工具。

第5题下列不属于记账式国债的特点的是( )。

A 安全性好B 流通性好C 适合长期国债的发行D 降低证券的发行成本【正确答案】:C【本题分数】:0.5分【答案解析】[解析] 记账式国债期限有长有短,但更适合短期国债的发行。

金融理财师(AFP)债券市场与债券投资章节练习试卷(题后含答案及解析)

金融理财师(AFP)债券市场与债券投资章节练习试卷(题后含答案及解析)题型有:1.1. 投资者在进行投资时,面临诸多投资产品的选择,但其收益与风险各不相同,即使在收益相当的情况下,风险也会有差别,下列对于债券风险的大小排序正确的是()。

A.国债<地方政府债券<企业债券<金融债券B.国债<企业债券<金融债券<地方政府债券C.金融债券<国债<地方政府债券<企业债券D.国债<地方政府债券<金融债券<企业债券正确答案:D 涉及知识点:债券市场与债券投资2. 关于凭证式债券的论述不正确的是()。

A.我国1994年开始发行凭证式国债B.我国的凭证式国债通过各银行储蓄网点和财政部门国债服务部面向社会发行C.券面上不印制票面金额,而是根据认购者的认购额填写实际的缴款金额 D.可记名、挂失,可以上市流通,从购买之日起计息正确答案:D解析:凭证式债券可记名、挂失,不能上市流通,从购买之日起计息。

知识模块:债券市场与债券投资3. 下面关于债券的叙述正确的是()。

A.债券尽管有面值,代表了一定的财产价值,但它也只是一种虚拟资本,而非真实资本B.债券代表债券投资者的权利,这种权利不是直接支配财产权而是资产所有权C.由于债券期限越长,流动性越差,风险也就较大,所以长期债券的票面利率肯定高于短期债券的票面利率D.流通性是债券的特征之一,也是国债的基本特点,所有的国债都是可流通的正确答案:A解析:债券代表债券投资者的权利,这种权利不是直接支配财产权,也不以资产所有权表现,而是一种债权。

债券票面利率与期限的关系较复杂,它们还受除时间以外其他因素的影响,所以有时也能见到短期债券票面利率高而长期债券票面利率低的现象。

流通性是债券的特征之一,也是国债的基本特点,但也有一些国债是不能流通的。

知识模块:债券市场与债券投资4. 关于债券的含义叙述错误的是()。

A.发行人是借入资金的经济主体B.投资者是出借资金的经济主体C.发行人需要在一定时期付息还本D.债券反映了发行者和投资者之间的委托、代理关系,而且是这一关系的法律凭证正确答案:D解析:债券反映了发行者和投资者之间的债权债务关系,而且是这一关系的法律凭证。

债券基础知识试卷(含参考答案)

营业部:姓名:得分:一、填空题(每空×’)、上交所债券现货实行(净价)交易,并按证券账户进行申报、债券现货交易中,实行(当日回转)交易,即交易,因此可以当日买入后再卖出.、上交所债券现货交易集中竞价时,其申报应当符合下列要求:()交易单位为手,人民币()元面值债券为手()计价单位为(每百元)面值债券地价格()申报价格最小变动单位为()元()申报数量为手或其整数倍,单笔申报最大数量不超过万手()申报价格限制按照交易规则地规定执行.个人收集整理勿做商业用途、企业债按()收取个人利息所得税、应计利息额(票面利率÷(天)×已计息天数)、债券回购交易申报中,融资方按(买入)予以申报,融券方按(卖出)予以申报.、上交所当日购买地债券,当日可用于(质押券)申报,并可进行相应地债券回购交易业务.、债券回购交易实行(一次成交、两次结算)制度,具体地清算交收,按照证券登记结算机构地规则办理.、上交所债券回购交易集中竞价时,其申报应当符合下列要求:(一)申报单位为手,()元标准券为手;(二)计价单位为(每百元资金到期年收益);(三)申报价格最小变动单位为()元或其整数倍;(四)申报数量为()手或其整数倍,单笔申报最大数量不超过万手;(五)申报价格限制按照交易规则地规定执行.、我司规定投资者进行质押式融资回购交易时,原则上回购标准券使用率不得超过(),回购放大倍数不得超过()倍.客户申请经总部审批通过地可放宽限制,最高回购标准券使用率不得超过(),回购放大倍数不得超过()倍.个人收集整理勿做商业用途、若年月日(周四)卖出,则回购到期日为(月日)、以为例,质押入库,()方向:(卖出)()质押代码:()、客户参与上海证券交易所债券回购业务,首先必须办理(证券帐户地指定交易手续).、客户申请专业投资者成功后,客户须与营业部签订公司统一格式地(债券质押式回购委托协议).、质押券对应地标准券数量有剩余地,可以通过本所交易系统,将相应地质押券申报转回原证券账户.当日(申报转回)地债券,当日可以卖出.个人收集整理勿做商业用途二、简答题(每题× ’)、如何计算应计利息额答:应计利息额票面利率÷(天)×已计息天数.应计利息额是指本付息期“起息日”至“成交日”所含利息金额.从“起息日”当天开始计算利息. 票面利率:固定利率债券是指发行票面利率;浮动利率债券是指本付息期计息利率.年度天数及已计息天数:年按天计算,闰年月日不计算利息;已计息天数是指“起息日”至“成交日”实际日历天数.当票面利率不能被天整除时,计算机系统按每百元利息额地精度(小数点后保留位)计算;交割单所列“应计利息额”按“舍入”原则,以元为单位保留位小数列示.交易日挂牌显示地“每百元应计利息额”是包括“交易日”当日在内地应计利息额;若债券持有到期,则应计利息额是自“起息日”至“到期日”(不包括到期日当日)地应计利息额.个人收集整理勿做商业用途、列举债券地相关风险答:(一)信用风险: 债券到期时,债务人是否能够还本付息. 这个风险只针对无担保债,可以参考债券地信用评级. 无担保债一般要比有担保债收益率高.个人收集整理勿做商业用途(二)利率风险: 央行基础利率上升则债券市场价格下降, 反之亦然. 理论上,债券地市场价格变化应该为久期*基础利率变化, 实际市场下中长期债券(久期年)受影响最大. 注意,这里地市场价格变化不影响债券持有到期地收益率.个人收集整理勿做商业用途(三)供求风险: 债券市场正在面临大发展,债券市场面临大扩容,短期可能出现资金面跟不上供应面地情况,此时债券价格会下跌以获取更高收益; 在牛市中,资金可能从债市转向股市,导致债券价格下跌; 经济下行周期时,政府一般会降息刺激经济发展,此时资金会涌入债券市场有可能出现泡沫.个人收集整理勿做商业用途(四)通货膨胀风险: 通货膨胀意味着市场要求更高地无风险收益率,央行也有可能加息,债券需要提高收益率才能吸引资金. 通货紧缩时,央行会降息以提高流动性和促进投资年时年期定存为略多.个人收集整理勿做商业用途(五)久期风险: 债券地久期风险是和上述风险联系在一起地,长久期实际上放大了利率波动风险和通货膨胀波动风险. 个人收集整理勿做商业用途、列举上交所债券回购期限及代码答:上海证券交易所可交易地质押式回购(括弧中为交易代码)分为日()、日()、日()、日()、日()、日()、日()、日()、日()共个品种.个人收集整理勿做商业用途、购回价计算公式为答:购回价元+年收益率×元×回购天数.、如果在回购到期日(日),客户不能支付到期应付款,属于违约行为(交收缺口部分下称“违约交收金额”).营业部须根据结算公司规定对客户进行处罚,具体按以下程序处理:个人收集整理勿做商业用途答:、按下列公式收取透支款项利息和违约金:每日透支款项利息违约交收金额×金融企业同业存款利率;每日违约金违约交收金额׉.(“每日”均含法定节假日).、在日收市前,要求客户自行处理部分证券或存入资金以偿付违约交收金额及利息、违约金.否则,营业部于日起卖出客户待处理地证券.变卖所得用于弥补违约交收款、利息及违约金.个人收集整理勿做商业用途、回购标准券占用率地计算公式、回购放大倍数地计算公式答:回购标准券占用率地计算公式为:回购标准券使用率融资回购交易未到期余额质押券对应地标准券总量回购放大倍数地计算公式为:回购放大倍数融资回购交易未到期余额投资者账户净资产、专业个人投资者应该符合条件答:证券账户净资产不低于人民币万元;具备债券投资基础知识,并通过相关测试;最近年内具有笔以上地债券交易成交记录;书面签署《债券市场专业投资者风险揭示书》,作出相关承诺;不存在严重不良诚信记录.个人收集整理勿做商业用途、在债券回购到期日,融资方可以获得哪些流动性便利答:回购到期日,交易系统根据结算公司提供地当日回购到期地数据,为相关账户增加相应可融资额度.融资方可以在可融资额度内进行新地融资回购,从而实现滚动融资;或者,融资方可以申报将相关质押券转回原证券账户,并可在当日卖出,卖出地资金可用于偿还到期购回款.个人收集整理勿做商业用途、说明在债券正回购交易中最大地风险答:是欠库和欠资.所谓欠库就是指当债券折算率降低后,没能及时补足债券,致使标准券可融资地资金量小于直接融入到资金量.所谓欠资就是指当质押债券到期,需要还款时,账户上可用资金不足以归还融资地资金及应付地利息.个人收集整理勿做商业用途、假设投资者有万闲置资金,比较其获得活期利息与做一天逆回购地收益情况,假设收益率为个人收集整理勿做商业用途答:以万为例,我们看看差别.如果不做回购,则一天地活期利息为万*元.如果做回购,一般利率为(周四可到),则回购利息为万*元,减去最高地佣金元,剩余元,比活期高元.个人收集整理勿做商业用途。

债券市场分析与策略第7版答案10

债券测试题及答案

债券测试题及答案一、单项选择题(每题2分,共10题)1. 债券的面值通常是多少?A. 100元B. 1000元C. 10000元D. 100000元答案:A2. 债券的票面利率是指?A. 发行人支付的利息与债券面值的比率B. 发行人支付的利息与债券市场价格的比率C. 发行人支付的利息与债券发行价格的比率D. 发行人支付的利息与债券购买价格的比率答案:A3. 以下哪个不是债券的基本特征?A. 偿还性B. 收益性C. 流通性D. 保险性答案:D4. 债券的发行价格高于其面值时,称为?A. 折价发行B. 溢价发行C. 等价发行D. 无价发行答案:B5. 债券的到期收益率是指?A. 债券的票面利率B. 债券的市场价格C. 债券的年利息收入与市场价格的比率D. 债券的年利息收入与面值的比率答案:C6. 债券的信用评级越高,其风险?A. 越高B. 越低C. 不变D. 无法确定答案:B7. 债券的期限是指?A. 债券的发行期限B. 债券的偿还期限C. 债券的交易期限D. 债券的持有期限答案:B8. 债券的发行人是?A. 投资者B. 借款人C. 发行人D. 承销商答案:C9. 债券的利息支付方式通常有?A. 一次性支付B. 每年支付C. 每半年支付D. 以上都是答案:D10. 债券的市场价格与市场利率的关系是?A. 正相关B. 负相关C. 无关D. 有时正相关,有时负相关答案:B二、多项选择题(每题3分,共5题)1. 债券的发行方式包括?A. 公开发行B. 私募发行C. 直接发行D. 间接发行答案:A|B|C|D2. 债券的分类依据包括?A. 发行主体B. 利息支付方式C. 债券期限D. 债券的偿还方式答案:A|B|C|D3. 债券的偿还方式包括?A. 到期一次性偿还B. 分期偿还C. 提前偿还D. 延期偿还答案:A|B|C|D4. 债券的流通方式包括?A. 场内交易B. 场外交易C. 电子交易D. 柜台交易答案:A|B|C|D5. 债券的风险包括?A. 利率风险B. 信用风险C. 流动性风险D. 通货膨胀风险答案:A|B|C|D三、判断题(每题1分,共5题)1. 债券的面值越大,其市场价格也越高。

金融市场第五章债券市场市场习题及答案

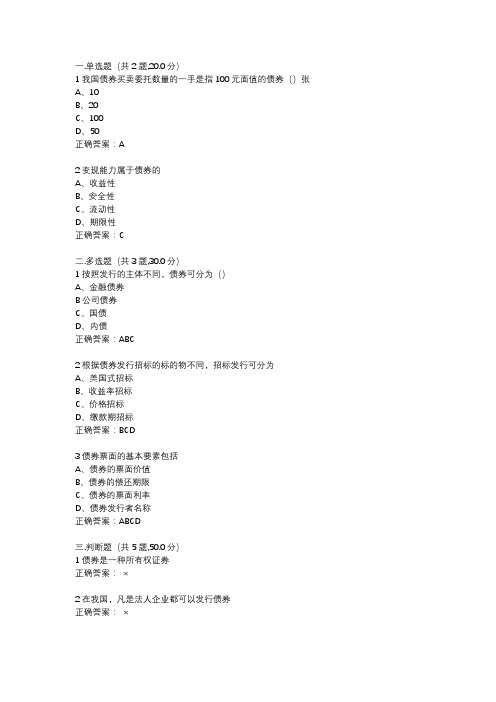

一.单选题(共2题,20.0分)

1我国债券买卖委托数量的一手是指100元面值的债券()张

A、10

B、20

C、100

D、50

正确答案:A

2变现能力属于债券的

A、收益性

B、安全性

C、流动性

D、期限性

正确答案:C

二.多选题(共3题,30.0分)

1按照发行的主体不同,债券可分为()

A、金融债券

B公司债券

C、国债

D、内债

正确答案:ABC

2根据债券发行招标的标的物不同,招标发行可分为

A、美国式招标

B、收益率招标

C、价格招标

D、缴款期招标

正确答案:BCD

3债券票面的基本要素包括

A、债券的票面价值

B、债券的偿还期限

C、债券的票面利率

D、债券发行者名称

正确答案:ABCD

三.判断题(共5题,50.0分)

1债券是一种所有权证券

正确答案:×

2在我国,凡是法人企业都可以发行债券

正确答案:×

3发行价格低于债券票面价格的发行称为折价发行正确答案:√

4国债资金主要用于生产,以赚取更多利润

正确答案:×

5债券的收益就是指债券的利息收入

正确答案:×。

债券市场分析与策略第7版答案2(最新整理)

CHAPTER 2PRICING OF BONDSCHAPTER SUMMARYThis chapter will focus on the time value of money and how to calculate the price of a bond. When pricing a bond it is necessary to estimate the expected cash flows and determine the appropriate yield at which to discount the expected cash flows. Among other aspects of a bond, we will look at the reasons why the price of a bond changesREVIEW OF TIME VALUE OF MONEYMoney has time value because of the opportunity to invest it at some interest rate.Future ValueThe future value of any sum of money invested today is:P n= P0(1+r)nwhere n = number of periods, P n= future value n periods from now (in dollars), P0= original principal (in dollars), r = interest rate per period (in decimal form), and the expression (1+r)n represents the future value of $1 invested today for n periods at a compounding rate of r.When interest is paid more than one time per year, both the interest rate and the number of periods used to compute the future value must be adjusted as follows:r = annual interest rate / number of times interest paid per year, andn = number of times interest paid per year times number of years.The higher future value when interest is paid semiannually, as opposed to annually, reflects the greater opportunity for reinvesting the interest paid.Future Value of an Ordinary AnnuityWhen the same amount of money is invested periodically, it is referred to as an annuity. When the first investment occurs one period from now, it is referred to as an ordinary annuity.The equation for the future value of an ordinary annuity is:P n =()11⎡⎤+-⎢⎥⎢⎥⎣⎦nrArwhere A is the amount of the annuity (in dollars).Example of Future Value of an Ordinary Annuity Using Annual Interest:If A = $2,000,000, r = 0.08, and n = 15, then P n = → P 15 = ()11n r A r ⎡⎤+-⎢⎥⎣⎦= $2,000,000[27.152125] = $54,304.250.08.0117217.3000,000,2$⎥⎦⎤⎢⎣⎡-Because 15($2,000,000) = $30,000,000 of this future value represents the total dollar amount of annual interest payments made by the issuer and invested by the portfolio manager, the balance of $54,304,250 – $30,000,000 = $24,304,250 is the interest earned by reinvesting these annual interest payments.Example of Future Value of an Ordinary Annuity Using Semiannual Interest:Consider the same example, but now we assume semiannual interest payments.If A = $2,000,000 / 2 = $1,000,000, r = 0.08 / 2 = 0.04, n = 2(15) = 30, thenP n = → P 30 = = =()11n r A r ⎡⎤+-⎢⎥⎢⎥⎣⎦04.01)04.(1000,000,1$30⎥⎦⎤⎢⎣⎡-04.012434.3000,000,1$⎥⎦⎤⎢⎣⎡-$1,000,000[56.085] = $56,085,000.The opportunity for more frequent reinvestment of interest payments received makes the interest earned of $26,085,000 from reinvesting the interest payments greater than the $24,304,250 interest earned when interest is paid only one time per year.Present ValueThe present value is the future value process in reverse. We have:.()11n PV r ⎡⎤=⎢⎥+⎣⎦For a given future value at a specified time in the future, the higher the interest rate (or discount rate), the lower the present value. For a given interest rate (discount rate), the further into the future that the future value will be received, then the lower its present value.Present Value of a Series of Future ValuesTo determine the present value of a series of future values, the present value of each future value must first be computed. Then these present values are added together to obtain the present value of the entire series of future values.Present Value of an Ordinary AnnuityWhen the same dollar amount of money is received each period or paid each year, the series is referred to as an annuity. When the first payment is received one period from now, the annuity is called an ordinary annuity. When the first payment is immediate, the annuity is called an annuity due.The present value of an ordinary annuity is:()111nr PV = A r ⎡⎤-⎢⎥+⎢⎥⎣⎦where A is the amount of the annuity (in dollars).The term in brackets is the present value of an ordinary annuity of $1 for n periods.Example of Present Value of an Ordinary Annuity Using Annual Interest:If A = $100, r = 0.09, and n = 8, then: = =()111nr PV = A r ⎡⎤-⎢⎥+⎢⎥⎣⎦()811 1.09$100 0.09⎡⎤-⎢⎥⎢⎥⎣⎦ = = $100[5.534811] = $553.48.11 1.99256$100 0.09⎡⎤-⎢⎥⎢⎥⎣⎦10.501867 $100 0.09-⎡⎤⎢⎥⎣⎦Present Value When Payments Occur More Than Once Per YearIf the future value to be received occurs more than once per year, then the present value formula is modified so that (i) the annual interest rate is divided by the frequency per year, and (ii) the number of periods when the future value will be received is adjusted by multiplying the number of years by the frequency per year.PRICING A BONDDetermining the price of any financial instrument requires an estimate of (i) the expected cash flows, and (ii) the appropriate required yield. The required yield reflects the yield for financial instruments with comparable risk, or alternative investments.The cash flows for a bond that the issuer cannot retire prior to its stated maturity date consist of periodic coupon interest payments to the maturity date, and the par (or maturity) value at maturity.In general, the price of a bond can be computed using the following formula:.()()111+∑nt t nt=M C P = + r + r where P = price (in dollars), n = number of periods (number of years times 2), C = semiannual coupon payment (in dollars), r = periodic interest rate (required annual yield divided by 2), M = maturity value, and t = time period when the payment is to be received.Computing the Value of a Bond: An Example:Consider a 20-year 10% coupon bond with a par value of $1,000 and a required yield of 11%. Given C = 0.1($1,000) / 2 = $50, n = 2(20) = 40 and r = 0.11 / 2 = 0.055, the present value of the coupon payments is:= = = =()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦()4011 1.055$50 0.055⎡⎤-⎢⎥⎢⎥⎣⎦11 8.51332$50 0.055⎡⎤-⎢⎥⎢⎥⎣⎦10.117463$50 0.055-⎡⎤⎢⎥⎣⎦ = $802.31.[]046131.1650$The present value of the par or maturity value of $1,000 is:= = = ()1n M r +()40$1,000.0551 51331.8000,1$$117.46.The price of the bond (P) = present value coupon payments + present value maturity value = $802.31 + $117.46 = $919.77.Pricing Zero-Coupon BondsFor zero-coupon bonds, the investor realizes interest as the difference between the maturity value and the purchase price. The equation is:()1nM P r =+where M is the maturity value. Thus, the price of a zero-coupon bond is simply the present value of the maturity value.Zero-Coupon Bond ExampleConsider the price of a zero-coupon bond that matures 15 years from now, if the maturity value is $1,000 and the required yield is 9.4%. Given M = $1,000, r = 0.094 / 2 = 0.047, and n = 2(15) = 30,we have: = = = $252.12.()1n M P r =+()30$1,0001.04799644.3000,1$Price-Yield RelationshipA fundamental property of a bond is that its price changes in the opposite direction from the change in the required yield. The reason is that the price of the bond is the present value of the cash flows.Relationship Between Coupon Rate, Required Yield, and PriceWhen yields in the marketplace rise above the coupon rate at a given point in time , the price of the bond falls so that an investor buying the bond can realizes capital appreciation. The appreciation represents a form of interest to a new investor to compensate for a coupon rate that is lower than the required yield. When a bond sells below its par value, it is said to be selling at a discount. A bond whose price is above its par value is said to be selling at a premium.Relationship Between Bond Price and Time if Interest Rates Are UnchangedFor a bond selling at par value, the coupon rate is equal to the required yield. As the bond moves closer to maturity, the bond will continue to sell at par value. Its price will remain constant as the bond moves toward the maturity date.The price of a bond will not remain constant for a bond selling at a premium or a discount. The discount bond increases in price as it approaches maturity, assuming that the required yield does not change. For a premium bond, the opposite occurs. For both bonds, the price will equal par value at the maturity date.Reasons for the Change in the Price of a BondThe price of a bond can change for three reasons: (i) there is a change in the required yield owing to changes in the credit quality of the issuer; (ii) there is a change in the price of the bond selling at a premium or a discount, without any change in the required yield, simply because the bond is moving toward maturity; or, (iii) there is a change in the required yield owing to a change in the yield on comparable bonds (i.e., a change in the yield required by the market).COMPLICATIONSThe framework for pricing a bond assumes the following: (i) the next coupon payment is exactly six months away; (ii) the cash flows are known; (iii) the appropriate required yield can be determined; and, (iv) one rate is used to discount all cash flows.Next Coupon Payment Due in Less than Six MonthsWhen an investor purchases a bond whose next coupon payment is due in less than six months, the accepted method for computing the price of the bond is as follows:n11t=1 = (1 + r )v t v n M C P + (1 + r (1 + r (1 + r )))--∑where v = (days between settlement and next coupon) / (days in six-month period).Cash Flows May Not Be KnownFor most bonds, the cash flows are not known with certainty. This is because an issuer may call a bond before the stated maturity date.Determining the Appropriate Required YieldAll required yields are benchmarked off yields offered by Treasury securities. From there, we must still decompose the required yield for a bond into its component parts.One Discount Rate Applicable to All Cash FlowsA bond can be viewed as a package of zero-coupon bonds, in which case a unique discount rate should be used to determine the present value of each cash flow.PRICING FLOATING-RATE AND INVERSE-FLOATING-RATE SECURITIESThe cash flow is not known for either a floating-rate or an inverse-floating-rate security; it will depend on the reference rate in the future.Price of a FloaterThe coupon rate of a floating-rate security (or floater) is equal to a reference rate plus some spread or margin. The price of a floater depends on (i) the spread over the reference rate and (ii) any restrictions that may be imposed on the resetting of the coupon rate.Price of an Inverse FloaterIn general, an inverse floater is created from a fixed-rate security. The security from which the inverse floater is created is called the collateral. From the collateral two bonds are created: a floater and an inverse floater.The price of a floater depends on (i) the spread over the reference rate and (ii) any restrictions that may be imposed on the resetting of the coupon rate. For example, a floater may have a maximum coupon rate called a cap or a minimum coupon rate called a floor. The price of a floater will trade close to its par value as long as the spread above the reference rate that the market requires is unchanged, and neither the cap nor the floor is reached.The price of an inverse floater equals the collateral’s price minus the floater’s price.PRICE QUOTES AND ACCRUED INTERESTPrice QuotesA bond selling at par is quoted as 100, meaning 100% of its par value. A bond selling at a discount will be selling for less than 100; a bond selling at a premium will be selling for more than 100. Accrued InterestWhen an investor purchases a bond between coupon payments, the investor must compensate the seller of the bond for the coupon interest earned from the time of the last coupon payment to the settlement date of the bond. This amount is called accrued interest. For corporate and municipal bonds, accrued interest is based on a 360-day year, with each month having 30 days.The amount that the buyer pays the seller is the agreed-upon price plus accrued interest. This is often referred to as the full price or dirty price. The price of a bond without accrued interest is called the clean price. The exceptions are bonds that are in default. Such bonds are said to be quoted flat, that is, without accrued interest.ANSWERS TO QUESTIONS FOR CHAPTER 2(Questions are in bold print followed by answers.)1. A pension fund manager invests $10 million in a debt obligation that promises to pay 7.3% per year for four years. What is the future value of the $10 million?To determine the future value of any sum of money invested today, we can use the future value equation, which is: P n= P0 (1 + r)n where n = number of periods, P n= future value n periods from now (in dollars), P0= original principal (in dollars) and r = interest rate per period (in decimal form). Inserting in our values, we have: P4 = $10,000,000(1.073)4 = $10,000,000(1.325558466) = $13,255,584.66.2. Suppose that a life insurance company has guaranteed a payment of $14 million to a pension fund 4.5 years from now. If the life insurance company receives a premium of $10.4 million from the pension fund and can invest the entire premium for 4.5 years at an annual interest rate of 6.25%, will it have sufficient funds from this investment to meet the $14 million obligation?To determine the future value of any sum of money invested today, we can use the future value equation, which is: P n= P0 (1 + r)n where n = number of periods, P n= future value n periods from now (in dollars), P0= original principal (in dollars)and r = interest rate per period (in decimal form). Inserting in our values, we have: P4.5= $10,400,000(1.0625)4.5= $10,400,000(1.313651676) = $13,661,977.43. Thus, it will be short $13,661,977.43 – $14,000,000 = $338,022.57.3. Answer the below questions.(a) The portfolio manager of a tax-exempt fund is considering investing $500,000 in a debt instrument that pays an annual interest rate of 5.7% for four years. At the end of four years, the portfolio manager plans to reinvest the proceeds for three more years and expects that for the three-year period, an annual interest rate of 7.2% can be earned. What is the future value of this investment?At the end of year four, the portfolio manager’s amount is given by: P n= P0 (1 + r)n. Inserting in our values, we have P4= $500,000(1.057)4 = $500,000(1.248245382) = $624,122.66. In three more years at the end of year seven, the manager amount is given by: P7= P4(1 + r)3. Inserting in our values, we have: P7= $624,122.66(1.072)3 = $624,122.66(1.231925248) = $768,872.47. (b) Suppose that the portfolio manager in Question 3, part a, has the opportunity to invest the $500,000 for seven years in a debt obligation that promises to pay an annual interest rate of 6.1% compounded semiannually. Is this investment alternative more attractive than the one in Question 3, part a?At the end of year seven, the portfolio manager’s amount is given by the following equation, which adjusts for semiannual compounding. We have: P n= P0(1 + r/2)2(n). Inserting in our values, wehave P 7 = $500,000(1 + 0.061/2)2(7) = $500,000(1.0305)14 = $500,000(1.522901960) = $761,450.98. Thus, this investment alternative is not more attractive. It is less by the amount of $761,450.98 – $768,872.47 = -$7,421.49.4. Suppose that a portfolio manager purchases $10 million of par value of an eight-year bond that has a coupon rate of 7% and pays interest once per year. The first annual coupon payment will be made one year from now. How much will the portfolio manager have if she(1) holds the bond until it matures eight years from now, and (2) can reinvest all the annual interest payments at an annual interest rate of 6.2%?At the end of year eight, the portfolio manager’s amount is given by the following equation, which adjusts for annual compounding.We have:()11+ Par Value n n + r P A r ⎡⎤-=⎢⎥⎢⎥⎣⎦where A = coupon rate times par value. Inserting in our values, we have:+ $10,000,000 = $700,000[9.9688005] + $10,000,000 = 88(1 + 0.062 1) = 0.07($10,000,000) 0.062P ⎡⎤-⎢⎥⎣⎦$6,978,160.38 + $10,000,000 = $16,978,160.38.5. Answer the below questions.(a) If the discount rate that is used to calculate the present value of a debt obligation’s cash flow is increased, what happens to the price of that debt obligation?A fundamental property of a bond is that its price changes in the opposite direction from the change in the required yield. The reason is that the price of the bond is the present value of the cash flows. As the required yield increases, the present value of the cash flow decreases; hence the price decreases. The opposite is true when the required yield decreases: The present value of the cash flows increases, and therefore the price of the bond increases.(b) Suppose that the discount rate used to calculate the present value of a debt obligation’s cash flow is x %. Suppose also that the only cash flows for this debt obligation are $200,000 four years from now and $200,000 five years from now. For which of these cash flows will the present value be greater?Cash flows that come earlier will have a greater value. As long as x% is positive and the amount is the same, the present value will be greater for the $200,000 four years from now compared to fiveyears from now. This can also be seen by noting that if x > 0 then . The ()()45111x 1x ⎡⎤⎡⎤>⎢⎥⎢⎥++⎣⎦⎣⎦latter inequality implies will hold.()()4511$2,000 $2,0001x 1x ⎡⎤⎡⎤>⎢⎥⎢⎥++⎣⎦⎣⎦6. The pension fund obligation of a corporation is calculated as the present value of the actuarially projected benefits that will have to be paid to beneficiaries. Why is the interest rate used to discount the projected benefits important?The present value increases as the discount rate decreases and decreases as the discount rate increases. Thus, in order to project the benefits accurately, we need an accurate estimate of the discount rate. If we underestimate the discount rate then we will be projecting more available pension funds than we will actually have.7. A pension fund manager knows that the following liabilities must be satisfied:Years from Now Liability (in millions)1 2.02 3.03 5.44 5.8Suppose that the pension fund manager wants to invest a sum of money that will satisfy this liability stream. Assuming that any amount that can be invested today can earn an annual interest rate of 7.6%, how much must be invested today to satisfy this liability stream?To satisfy year one’s liability (n = 1), the pension fund manager must invest an amount today that is equal to the future value of $2.0 million at 7.6%. We have: = = = $1,858,736.06.()1n n PV P 1 + r ⎡⎤=⎢⎥⎣⎦)076(1.1000,000,2$1⎥⎦⎤⎢⎣⎡[]929368030.0000,000,2$To satisfy year two’s liability (n = 2), the pension fund manager must invest an amount today that is equal to the future value of $3.0 million at 7.6%. We have:= = = $2,591,174.80.()1n n PV P 1 + r ⎡⎤=⎢⎥⎣⎦)076(1.1000,000,3$2⎥⎦⎤⎢⎣⎡[]50.86372493000,000,3$To satisfy year three’s liability (n = 3), the pension fund manager must invest an amount today that is equal to the future value of $5.4 million at 7.6%. We have:= = = $4,334,679.04.()1n n PV P 1 + r ⎡⎤=⎢⎥⎣⎦)076(1.1000,400,5$3⎥⎦⎤⎢⎣⎡[]10.80271834000,400,5$To satisfy year four’s liability (n = 4), the pension fund manager must invest an amount today that is equal to the future value of $5.8 million at 7.6%. We have:= = = $4,326,920.42.()1n n PV P 1 + r ⎡⎤=⎢⎥⎣⎦)076(1.1000,800,5$4⎥⎦⎤⎢⎣⎡[]30.74602076000,800,5$If we add the four present values, we get $1,858,736.06 + $2,591,174.80 + $4,334,679.04 + $4,326,920.42 = $13,111,510.32, which is the amount the pension fund manager needs to invest today to cover the liability stream for the next four years.8. Calculate for each of the following bonds the price per $1,000 of par value assuming semiannual coupon payments.BondCoupon Rate (%)Years to Maturity Required Yield (%)A8 9 7B920 9C61510D 014 8Consider a 9-year 8% coupon bond with a par value of $1,000 and a required yield of 7%. Given C = 0.08($1,000) / 2 = $40, n = 2(40) = 80 and r = 0.07 / 2 = 0.035, the present value of the coupon payments is:= = = ()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦()8011 1.035$40 0.035⎡⎤-⎢⎥⎢⎥⎣⎦11 15.6757375$400.035⎡⎤-⎢⎥⎢⎥⎣⎦[]035.020.06379285140$⎦⎤⎢⎣⎡-= = $1,069.951.[]26.748775740$The present value of the par or maturity value of $1,000 is: = = ()1n M+ r ()80$1,0001.035$1,00015.6757375= $63.793. Thus, the price of the bond (P) = present value of coupon payments + present value of par value = $1,069.951 + $63.793 = $1,133.74.Consider a 20-year 9% coupon bond with a par value of $1,000 and a required yield of 9%. GivenC = 0.09($1,000) / 2 = $45, n = 2(20) = 40 and r = 0.09 / 2 = 0.045, the present value of the coupon payments is:= = = =()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦()4011 1.045$45 0.045⎡⎤-⎢⎥⎢⎥⎣⎦11 5.81863645$45 0.045⎡⎤-⎢⎥⎢⎥⎣⎦1 0.1719287 $45 0.045-⎡⎤⎢⎥⎣⎦$45[18.401584] = $828.071.The present value of the par or maturity value of $1,000 is: = = ()1n M+ r ()40$1,0001.045$1,0005.81863645= $171.929. Thus, the price of the bond (P) = $828.071+ $171.929= $1,000.00. [NOTE. We already knew the answer would be $1,000 because the coupon rate equals the yield to maturity.]Consider a 15-year 6% coupon bond with a par value of $1,000 and a required yield of 10%. GivenC = 0.06($1,000) / 2 = $30, n = 2(15) = 30 and r = 0.10 / 2 = 0.05, the present value of the coupon payments is:= = = =()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦()3011 1.05$30 0.05⎡⎤-⎢⎥⎢⎥⎣⎦11 4.3219424$300.05⎡⎤-⎢⎥⎢⎥⎣⎦10.2313774 $30 0.05-⎡⎤⎢⎥⎣⎦$30[15.372451] = $461.174.The present value of the par or maturity value of $1,000 is: = = =()1n M+ r ()30$1,0001.053219424.4000,1$$231.377. Thus, the price of the bond (P) = $461.174 + $231.377= $692.55.Consider a 14-year 0% coupon bond with a par value of $1,000 and a required yield of 8%. GivenC = 0($1,000) / 2 = $0, n = 2(14) = 28 and r = 0.08 / 2 = 0.04, the present value of the coupon payments is:=== =()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦2811 (1.04)$0 0.04⎡⎤-⎢⎥⎢⎥⎣⎦11 2.998703319$0 0.055⎡⎤-⎢⎥⎢⎥⎣⎦055.00.3347747110$⎦⎤⎢⎣⎡-$0[16.66306322] = $0. [NOTE. We already knew the answer because the coupon rate is zero.]The present value of the par or maturity value of $1,000 is: = = = ()1nM+ r ()28$1,0001.04$1,0002.99870332$333.48. Thus, the price of the bond (P) = $0 + $333.48 = $333.48.9. Consider a bond selling at par ($100) with a coupon rate of 6% and 10 years to maturity.(a) What is the price of this bond if the required yield is 15%?We have a 10-year 6% coupon bond with a par value of $1,000 and a required yield of 15%. GivenC = 0.06($1,000) / 2 = $30, n = 2(10) = 20 and r = 0.15 / 2 = 0.075, the present value of the coupon payments is:= = = =()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦2011 (1.075)$30 0.075⎡⎤-⎢⎥⎢⎥⎣⎦11 4.2478511$30 0.075⎡⎤-⎢⎥⎢⎥⎣⎦1 0.2354131$30 0.075-⎡⎤⎢⎥⎣⎦$30[10.1944913] = $305.835.The present value of the par or maturity value of $1,000 is: = = =()1n M+ r ()20$1,0001.075$1,0004.2478511$235.413. Thus, the price of the bond (P) = $305.835 + $235.413 = $541.25.(b) What is the price of this bond if the required yield increases from 15% to 16%, and by what percentage did the price of this bond change?If the required yield increases from 15% to 16%, then we have:== = $294.544.()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦2011 (1.08)$30 0.08⎡⎤-⎢⎥⎢⎥⎣⎦[]9.818147430$The present value of the par or maturity value of $1,000 is: = = $214.548.()1n M + r ()20$1,0001.08Thus, the price of the bond (P) = $294.544 + $214.548= $509.09.The bond price falls with percentage fall is equivalent to= -0.059409 or about $509.09$541.25$541.25--5.94%.(c) What is the price of this bond if the required yield is 5%?If the required yield is 5%, then we have:= = = $467.675.()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦2011 (1.025)$30 0.025⎡⎤-⎢⎥⎢⎥⎣⎦[]15.589162330$The present value of the par or maturity value of $1,000 is: = = $610.271.()1n M + r ()20$1,0001.025Thus, the price of the bond (P) = $467.675 + $610.271 = $1,077.95.(d) What is the price of this bond if the required yield increases from 5% to 6%, and by what percentage did the price of this bond change?If the required yield increases from 5% to 6%, then we have:== = $446.324.()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦2011 (1.03)$30 0.03⎡⎤-⎢⎥⎢⎥⎣⎦[]614.877474830$The present value of the par or maturity value of $1,000 is: = = $553.676.()1n M + r )03.1(000,1$20The price of the bond (P) = $446.324 + $553.676 = $1,000.00. [NOTE. We already knew the answer would be $1,000 because the coupon rate equals the yield to maturity.]The bond price falls with the percentage fall equal to ($1,000.00 – $1,077.95) / $1,077.95 = -0.072310 or about -7.23%.(e) From your answers to Question 9, parts b and d, what can you say about the relative price volatility of a bond in a high-interest-rate environment compared to a low-interest-rate environment?We can say that there is more volatility in a low-interest-rate environment because there was a greater fall (-7.23% versus -5.94%).10. Suppose that you purchased a debt obligation three years ago at its par value of $100,000 and nine years remaining to maturity. The market price of this debt obligation today is $90,000. What are some reasons why the price of this debt obligation could have declined from time you purchased it three years ago?The price of a bond will change for one or more of the following three reasons:(i) There is a change in the required yield owing to changes in the credit quality of the issuer.(ii) There is a change in the price of the bond selling at a premium or a discount, without any change in the required yield, simply because the bond is moving toward maturity.(iii) There is a change in the required yield owing to a change in the yield on comparable bonds (i.e., a change in the yield required by the market).The first and third reasons are the likely reasons for the situation where the bond has plummeted from $100,000 to $90,000. The bond has plummeted in value because the credit quality of the issuer has fallen and/or the bond has plummeted because the yield on comparable bonds has increased.11. Suppose that you are reviewing a price sheet for bonds and see the following prices (per $100 par value) reported. You observe what seem to be several errors. Without calculating the price of each bond, indicate which bonds seem to be reported incorrectly, and explain why.BondPrice Coupon Rate (%)Required Yield (%)U9069V9698W11086X10505Y10779Z 10066If the required yield is the same as the coupon rate then the price of the bond should sell at its par value. This appears to be the case of bond Z since par values are typical at or near a $100 quote. If the required yield decreases below the coupon rate then the price of a bond should increase. This is the case for bond W. This is not the case for bond V so this bond is not reported correctly. If the required yield increases above the coupon rate then the price of a bond should decrease. This is the case for bond U. This is not the case for bonds X and Y so these bonds are not reported correctly. Thus, bonds V, X, and Y are incorrectly reported because the change in the bond price is not consistent with the difference between the coupon rate and the required yield.12. What is the maximum price of a bond?Consider an extreme case of a 100-year 20% coupon bond with a par value of $1,000 that after one year falls so that the required yield is 1%. Given C = 0.2 ($1,000) / 2 = $100, n = 2(99) = 198 and r = 0.01 / 2 = 0.005, the present value of the coupon payments is:= = =()111nr P = C r ⎡⎤-⎢⎥+⎢⎥⎣⎦19811 (1.005)$100 0.005⎡⎤-⎢⎥⎢⎥⎣⎦11 2.684604$100 0.005⎡⎤-⎢⎥⎢⎥⎣⎦= $1,000[1,125.51012] = $12,550.112.1 0.3724944 $100 0.005-⎡⎤⎢⎥⎣⎦The present value of the par value of $1,000 is: = = = $372.494.()1n M+ r ()198$1,0001.005$1,0002.684604Thus, the price of the bond (P) = $12,550.112 + $372.494 = $12,922.61.This is a percent increase of ($12,922.6 – $1,000) / $1,000 = 11.92606 or about 1,192.61%.If the required yield falls to 0.001%, then the bond price would increase to $20,778.33, which would be a percent increase of about 1,977.83%.。

债券试题及答案

债券试题及答案一、单选题(每题2分,共10分)1. 债券的面值是指:A. 债券的市场价格B. 债券的发行价格C. 债券的票面金额D. 债券的年利率答案:C2. 以下哪个不是债券的特点?A. 固定收益B. 可转让性C. 无风险D. 到期还本答案:C3. 债券的到期收益率是指:A. 债券的年利率B. 债券的发行利率C. 债券的票面利率D. 债券的年化收益率答案:D4. 债券的信用评级是由以下哪个机构提供的?A. 中央银行B. 证券交易所C. 信用评级机构D. 债券发行公司答案:C5. 债券的到期日是指:A. 债券发行的日期B. 债券的计息开始日期C. 债券的计息结束日期D. 债券的利息支付日期答案:C二、多选题(每题3分,共15分)1. 以下哪些因素会影响债券的价格?A. 利率水平B. 通货膨胀C. 投资者风险偏好D. 债券的信用评级答案:A, B, C, D2. 债券的发行方式包括:A. 公开发行B. 私募发行C. 直接发行D. 间接发行答案:A, B3. 以下哪些是债券发行的目的?A. 筹集资金B. 偿还债务C. 调整资产负债结构D. 增加公司知名度答案:A, B, C4. 债券的类型包括:A. 政府债券B. 企业债券C. 可转换债券D. 零息债券答案:A, B, C, D5. 债券投资的风险包括:A. 利率风险B. 信用风险C. 流动性风险D. 通货膨胀风险答案:A, B, C, D三、判断题(每题1分,共5分)1. 债券的面值和市场价格是相同的。

()答案:错误2. 债券的到期收益率高于票面利率时,债券价格会低于面值。

()答案:正确3. 债券的信用评级越高,其发行价格通常越低。

()答案:错误4. 债券的到期日越长,其价格波动性越大。

()答案:正确5. 债券的票面利率固定不变,因此其收益率也固定不变。

()答案:错误四、简答题(每题5分,共10分)1. 简述债券的到期收益率与市场价格之间的关系。

答案:债券的到期收益率与市场价格呈反向关系。

证券从业资格金融市场基础知识(债券市场)模拟试卷1(题后含答案及解析)

证券从业资格金融市场基础知识(债券市场)模拟试卷1(题后含答案及解析)题型有:1. 选择题 2. 综合型选择题选择题1.外国债券的发行一般由( )的金融机构、证券公司承销。

A.投资者所在国B.发行者所在国C.发行地所在国D.第三国正确答案:C解析:外国债券一般由发行地所在国的证券公司、金融机构承销,而欧洲债券则由一家或几家大银行牵头,组成十几家或几十家国际性银行在一个国家或几个国家同时承销。

知识模块:债券市场2.保险公司次级定期债务是指( )。

A.保险公司经批准定向募集的、期限在5年以上(含5年),本金和利息的清偿顺序列于保单责任和其他负债之后、先于保险公司股权资本的保险公司债务B.保险公司经批准定向募集的、期限在3年以上(含3年),本金和利息的清偿顺序列于保单责任和其他负债之后、先于保险公司股权资本的保险公司债务C.保险公司经批准定向募集的、期限在5年以上(含5年),本金和利息的清偿顺序列于保单责任和其他负债之前、先于保险公司股权资本的保险公司债务D.保险公司经批准定向募集的、期限在5年以上(不含5年),本金和利息的清偿顺序列于保单责任和其他负债之前、先于保险公司股权资本的保险公司债务正确答案:A解析:保险公司次级定期债务是指保险公司经批准定向募集的,期限在5年以上(含5年),本金和利息的清偿顺序列于保单责任和其他负债之后、先于保险公司股权资本的保险公司债务。

知识模块:债券市场3.根据发行主体的不同,债券可以分为( )。

A.零息债券、附息债券和息票累积债券B.实物债券、凭证式债券和记账式债券C.政府债券、金融债券和公司债券D.国债和地方债券正确答案:C解析:根据发行主体的不同,债券可以分为政府债券、金融债券和公司债券。

知识模块:债券市场4.在各类债券中,( )的信用等级是最高的。

A.金融债券B.政府债券C.公司债券D.国际债券正确答案:B解析:政府债券是政府发行的债券,由政府承担还本付息的责任,是国家信用的体现。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

债券市场及答案1、()负责受理短期融资券的发行注册。

A、中国银监会B、中国银行间市场交易商协会C、中国人民银行D、商务部正确答案:B【专家解析】根据《银行间债券市场非金融企业短期融资券业务指引》和《银行间债券市场非金融企业债务融资工具注册规则》的规定,中国银行间市场交易商协会负责受理短期融资券的发行注册。

2、下列中不属于债券基本性质的是()。

A、债券属于有价证券B、债券是一种虚拟资本C、债券是债权的表现D、发行人必须在约定的时间付息还本正确答案:D【专家解析】债券具有以下基本性质:(1)债券属于有价证券。

(2)债券是一种虚拟资本。

(3)债券是债权的表现。

3、下列关于债券与股票的说法中,错误的是()。

A、债券和股票都属于有价证券B、债券和股票的收益率是相互影响的C、债券通常有规定的票面利率,而股票的股息红利不固定D、债券和股票都是无期证券正确答案:D【专家解析】债券一般有规定的偿还期,期满时债务人必须按时归还本金,因此债券是一种有期证券。

股票通常是无须偿还的,一旦投资人股,股东便不能从股份公司抽回本金,因此股票是一种无期证券,或被称为“永久证券”。

但是,股票持有者可以通过市场转让收回投资资金。

故D项错误。

4、下列关于债券票面价值的说法中,正确的是()。

A、在债券的票面价值中,只需要规定债券的票面金额B、票面金额定得较小,发行成本也就较小C、票面金额定得较大,有利于小额投资者购买D、债券票面金额的确定要根据债券的发行对象、市场资金供给情况及债券发行费用等因素综合考虑正确答案:D【专家解析】A项,在债券的票面价值中,首先要规定票面价值的币种,币种确定后,则要规定债券的票面金额;B项,票面金额定得较小,债券本身的印刷及发行工作量大,费用可能较高;C项,票面金额定得较大,有利于少数大额投资者认购,但使小额投资者无法参与。

5、下列关于我国证券公司短期融资券的说法中,错误的是()。

A、约定在一定期限内还本付息B、在证券交易所发行C、在银行间债券市场发行D、以短期融资为目的正确答案:B【专家解析】证券公司短期融资券是指证券公司以短期融资为目的,在银行间债券市场发行的约定在一定期限内还本付息的金融债券。

6、回购交易通常在()交易中运用。

A、远期B、现货C、债券D、股票正确答案:C【专家解析】回购交易更多地具有短期融资的属性。

从运作方式看,它结合了现货交易和远期交易的特点,通常在债券交易中运用。

7、中小非金融企业集合票据流通转让的市场是()。

A、上海证券交易所B、深圳证券交易所C、银行间柜台市场D、银行间债券市场正确答案:D【专家解析】中小非金融企业集合票据在债权债务登记日的次一工作日即可在银行间债券市场流通转让。

8、()是指商业银行为补充附属资本发行的、清偿顺序位于股权资本之前但列在一般债务和次级债务之后、期限在15年以上、发行之日起10年内不可赎回的债券。

A、商业银行次级债券B、混合资本债券C、金融债券D、银行股票正确答案:B【专家解析】我国的混合资本债券是指商业银行为补充附属资本发行的、清偿顺序位于股权资本之前但列在一般债务和次级债务之后、期限在15年以上、发行之日起10年内不可赎回的债券。

9、下列关于中小非金融企业集合票据的说法中,错误的是()。

A、任一企业单只票据注册金额不超过10亿元人民币B、任一企业集合票据募集资金额不超过1亿元人民币C、中小非金融企业发行集合票据,应在中国银行间市场交易商协会注册,一次注册、一次发行D、中小非金融企业发行的集合票据在债权债务登记日的次一工作日即可在银行间债券市场流通转让正确答案:B【专家解析】任一企业集合票据募集资金额可以超过1亿元人民币10、银行间债券市场发行的记账式国债,主要面向()。

A、企业B、银行和非银行金融机构C、个人D、国外机构正确答案:B【专家解析】记账式国债的发行采用公开招标方式,可分为证券交易所市场发行、银行间债券市场发行以及同时在银行间债券市场和证券交易所市场发行(又称为“跨市场发行”)3种情况。

个人投资者可以购买证券交易所市场发行和跨市场发行的记账式国债,而银行间债券市场的发行主要面向银行和非银行金融机构等机构投资者。

11、下列不属于债券评级程序中前期准备阶段的是()。

A、评估客户向评估公司提出信用评级申请,双方签订《信用评级协议书》B、评估小组应向评估客户发出《评估调查资料清单》,要求评估客户在较短时间内把评估调查所需资料准备齐全C、根据需要,评估小组要向主管部门、工商行政部门、银行、税务部门及有关单位进行调查了解、进行核实D、评估公司指派项目评估小组,并制定项目评估方案正确答案:C【专家解析】选项A、B、D属于前期准备阶段,选项C属于信息收集阶段。

12、下列关于国际债券的说法中,正确的是()。

A、欧洲债券一般由发行地所在国的证券公司、金融机构承销B、欧洲债券在法律上所受的限制比外国债券宽松得多C、欧洲债券和外国债券在发行纳税方面不存在差异D、外国债券由,一家或几家大银行牵头,组织十几家或几十家国际性银行,在一个国家或几个国家同时承销正确答案:B【专家解析】外国债券一般由发行地所在国的证券公司、金融机构承销,而欧洲债券则由一家或几家大银行牵头,组织十几家或几十家国际性银行在一个国家或几个国家同时承销,故A、D项错误。

在发行纳税方面,外国债券受发行地所在国的税法管制,而欧洲债券的预扣税一般可以豁免,投资者的利息收入也免缴所得税,故C项错误。

13、依照不同的发行本位,国债可以分为()。

A、流通国债与非流通国债B、实物国债与货币国债C、短期国债与中长期国债D、实物债券与货币债券正确答案:B【专家解析】依照不同的发行本位,国债可以分为实物国债和货币国债。

14、一般来说,期限较长的债券票面利率定得较高,是由于债券()。

A、流动性差,风险相对较大B、流动性差,风险相对较小C、流动性强,风险相对较大D、流动性强,风险相对较小正确答案:A【专家解析】一般来说,期限较长的债券流动性差,风险相对较大,票面利率应该定得高一些;而期限较短的债券流动性强,风险相对较小,票面利率就可以定得低一些。

15、根据发行主体的不同,债券可以分为()。

A、零息债券、附息债券和息票累积债券B、实物债券、凭证式债券和记账式债券C、政府债券、金融债券和公司债券D、国债和地方债券正确答案:C【专家解析】根据发行主体的不同,债券可以分为政府债券、金融债券和公司债券。

16、下列关于债券成交原则的说法中,错误的是()。

A、价格优先就是证券公司按照交易最有利于投资委托人的利益的价格买进或卖出债券B、时间优先就是要求在相同的价格申报时,应该与最早提出该价格的一方成交C、价格优先就是要求在相同的价格申报时,应该与最早提出该价格的一方成交D、客户委托优先主要是要求证券公司在自营买卖和代理买卖之间,首先进行代理买卖正确答案:C【专家解析】时间优先就是要求在相同的价格申报时,应该与最早提出该价格的一方成交,选项C错误。

17、一国借款人在国际证券市场上以外国货币为面值、向外国投资者发行的债券是()。

A、国际债券B、亚洲债券C、外国债券D、欧洲债券正确答案:A【专家解析】国际债券是指一国借款人在国际证券市场上以外国货币为面值、向外国投资者发行的债券。

18、下列选项中,最早在中国内地发行过人民币债券的是()。

A、国际货币基金组织B、国际金融公司C、联合国D、世界贸易组织正确答案:B【专家解析】2005年10月9日,国际金融公司和亚洲开发银行这两家国际开发机构,在全国银行间债券市场分别发行人民币债券11.3亿元和10亿元,这是中国债券市场首次引入外资机构发行主体,中国的外国债券或熊猫债券市场便由此诞生。

19、可交换债券与可转换债券的相同之处是()。

A、发行主体和偿债主体一致B、适用的法规相似C、发行要素相似D、所换股份的来源一致正确答案:C【专家解析】可交换债券与可转换债券的相同之处是发行要素相似,都包括票面利率、期限、换股价格和换股比率、换股期限等。

20、下列关于地方政府债券的说法中,正确的是()。

A、地方政府债券通常可以分为一般债券和普通债券B、收入债券是指地方政府为缓解资金紧张或解决临时经费不足而发行的债券C、普通债券是指为筹集资金建设某项具体工程而发行的债券D、地方政府债券简称“地方债券”,也可以称为“地方公债”或“市政债券”正确答案:D【专家解析】地方政府债券按资金用途和偿还资金来源分类,通常可以分为一般债券(普通债券)和专项债券(收入债券)。

前者是指地方政府为缓解资金紧张或解决临时经费不足而发行的债券,后者是指为筹集资金建设某项具体工程而发行的债券。

故本题选D。

21、下列中不属于影响债券利率因素的是()。

A、筹资者的资信B、债券票面金额C、债券期限长短D、借贷资金市场利率水平正确答案:B【专家解析】影响债券利率的因素有:(1)借贷资金市场利率水平。

(2)筹资者的资信。

(3)债券期限长短。

22、下列关于凭证式国债的说法中,错误的是()。

A、采劝随买随卖”的方式进行交易B、采取向购买人开具凭证式国债收款凭证的方式进行发售C、利率按实际持有天数分档计付D、凭证式国债是一种可上市流通的储蓄型债券正确答案:D【专家解析】凭证式国债是一种不可上市流通的储蓄型债券,由具备凭证式国债承销团资格的机构承销。

23、次级债务是指由银行发行的,固定期限()的商业银行长期债务。

A、不低于5年(含5年)B、不低于3年(含3年)C、不低于5年(不含5年)D、不低于3年(不含3年)正确答案:A【专家解析】次级债务是指由银行发行的,固定期限不低于5年(含5年),除非银行倒闭或清算不用于弥补银行日常经营损失,且该项债务的索偿权排在存款和其他负债之后的商业银行长期债务。

24、深市投资者若要转托管需在买人成交的()日交收过后才能办理。

A、TB、T+1C、T+2D、T+3正确答案:D【专家解析】由于深市B股实行的是T+3交收,深市投资者若要转托管需在买人成交的T+3日交收过后才能办理。

25、回购交易通常情况下只有(),是一种超短期的金融工具。

A、6小时B、12小时C、18小时D、24小时正确答案:D【专家解析】回购交易长的有几个月,但通常情况下只有24小时,是一种超短期的金融工具。

26、企业发行的短期融资券待偿还余额不得超过企业净资产的()。

A、[15%]B、[25%]C、[30%]D、[40%]正确答案:D【专家解析】根据《银行间债券市场非金融企业短期融资券业务指引》的规定,企业发行短期融资券应遵守国家相关法律法规,短期融资券待偿还余额不得超过企业净资产的40%。

27、在公司债券有效存续期间,资信评级机构每年至少公告()跟踪评级报告。

A、1次B、2次C、3次D、5次正确答案:A【专家解析】《公司债券发行试点办法》规定,公司与资信评级机构应当约定,在债券有效存续期间,资信评级机构每年至少公告1次跟踪评级报告。