伯南克在华盛顿大学第一课 美联储的基本使命-课件

伯南克第一课英文讲义电子版本

伯南克第一课英文讲义伯南克第一课英文讲义北京时间3月21日凌晨,美联储主席伯南克稍早时在乔治-华盛顿大学商学院进行了针对该院学生系列讲座的第一讲,题目为:美联储的基本使命。

以下是伯南克本次讲座的英文讲义全文。

(资料来源于美联储网站)The Federal Reserve and the Financial CrisisOrigins and Mission of the Federal Reserve, Lecture 1George Washington University School of BusinessMarch 20, 2012, 12:45 p.m。

[Applause]President Steve Knapp: Well, good afternoon. I think the students here may know who I am but for those who are watching the broadcast, I'm Steve Knapp, President of George Washington University. And it's really a pleasure to welcome you to today's first class in the series entitled Reflections on the Federal Reserve and its place in today's economy, featuring the Chairman of the Federal Reserve, Dr. Ben Bernanke. I'm pleased to acknowledge that we have with us two of the university's trustees, Nelson Carbonell and Mark Shenkman, and also a number of faculty members are here in the audience and some of them will be teaching later in the series. Today is the first university lecture series delivered by a sitting Chairman of the Federal Reserve. I think it does provide an extraordinary opportunity for the students who are here in the classroom, but also for those watching online. They have an opportunity to gain insight into the nation's central banking system and a wide range of issues that affect this country and the world. I do want to say that there are microphones available for the students, and certainly encourage you when the Chairman's lecture is over to avail yourself of those and we hope there'll be a lively exchange of questions and answers at the end of the lecture. It's now a distinct honor to introduce the Chairman of the Board of Governors of the Federal Reserve System, Dr. Ben Bernanke. Dr. Bernanke took office in 2006, and is now serving a second term as Chairman. He also serves as Chairman of the Federal Reserve's Open Market Committee. Before his appointment as Chairman, Dr. Bernanke was involved with the Federal Reserve in several roles as a Member of the Board of Governors, as a visiting scholar, and as a member of the Academic Advisory Panel at the Federal Reserve Bank of New York. He also served as Chairman of the President's Council of Economic Advisers from June 2005 to January 2006.Now Chairman Bernanke is no stranger to academia. He's been a faculty member at Princeton, Stanford and New York University, as well as the Massachusetts Institute of Technology. He's held a Guggenheim and a Sloan Fellowship, and is a fellow of the Econometric Society and the American Academy of Arts and Sciences. Chairman Bernanke received aBachelor of Arts from Harvard University and a PhD from MIT. Ladies and gentlemen, please join me in welcoming Chairman of the Federal Reserve, Dr. Ben Bernanke.[ Applause ]Chairman Ben Bernanke: Thank you very much, President Knapp. Gee, this is great. This is what I used to do before I got in this line of work for 23 years and I've always enjoyed engaging with college students. So thank you for being here, and I hope we do have a good conversation. Let me particularly thank President Knapp and Professor Fort and George Washington University. As everybody here knows, these lectures are part of a real course and after I get off the scene there will be other professors talking about other aspects of the Fed and you'll hear different points of view which is great. And you'll have to do some papers and all those kinds of things and I'm going to read a few of the paper. So, I look forward to doing that.So, I'll be talking from slides, which is in part for the purpose of making this available to others who might be interested. These slides will be posted on the Federal Reserve's website, , as we go through. And so, if you need extra copies, by all means do that. And as President Knapp said, I'm going to be talking for a while from the presentation but at the end, I hope we can have some questions and answers.So, let me get started. So what I want to talk about in these four lectures is the Federal Reserve and the financial crisis. Now, my thinking about this is very much conditioned by my experience as an economic historian. I think when you talk about the issues that just occurred of the last few years, it makes the most sense to think about it in the broader context of central banking as its taking place over the centuries. So, even though we're going to be focusing a good bit of the lectures, particularly next week, on the financial crisis and how the Fed responded. I think we need to go back and look at the broader context. So, as we talk about the Fed we'll be talking about the origin and mission of central banks in general, and we're looking at previous financial crises, most notably the Great Depression, and see how that informed the Fed's actions and decisions in the recent crisis. So let me just give you a roadmap of the four lectures. Today, lecture one, we won't touch on the current crisis at all. Instead, we'll talk about what central banks are, what they do, how central banking got started in the United States and we'll do some history. We'll talk about how the Fed engaged with its first great challenge, the Great Depression of the 1930s. The second lecture on Thursday, we'll take up the history. We'll review developments in central banking and with the Federal Reserve after World War II talking about the conquest of inflation, the great moderation and other developments that occurred after World War II. But we'll spend a good bit of time lecture two, in lecture two, talking about the build-up to the crisis and some of the factors that led to the crisis of 2008, 2009.Then next week, we'll get into the more recent events. In lecture three, we'll talk about the intense phase of the financial crisis, its causes, its implications, and particularly, the response to the crisis by the Federal Reserve and by other policymakers. And then, in the final lecture, lecture four, we'll look at the aftermath. We'll talk about the recession that followed the crisis, the policy response of the Fed including monetary policy, the broader response in terms of the changes infinancial regulation, and a little bit of forward-looking discussion about how this experience will change how central banks operate and how the Federal Reserve will operate going forward. Sothis is our topic today is origins and missions of the Federal Reserve. So let's talk in general about what a central bank is. If you've had some background in economics you know that a central bank is not a regular bank, it's a government agency, and it stands at the center of the monetary and financial system of a country. Central banks are very important institutions, they have helped to guide the development of modern financial systems, modern monetary systems and they play a major role in economic policy. Now, we've had various arrangements over the years but today, virtually, all countries have central banks. The Federal Reserve in the United States, the Bank of Japan in Japan, Bank of Canada, and so on. The main exception is only cases where you have what's called a currency union where a number of countries collectively share a central bank. The most important example by far of that is the European Central Bank which is central bank to 17 European countries who share the common currency, the Euro. But even in that case, each of the participating countries does have its own central bank which is part of the overall system of the Euro. So central banks are now ubiquitous, even the smallest countries typically have central banks. Now, this is a very important theme here, what do Central Banks do? What is their mission? And as I'll discuss throughout the lectures, it's convenient to talk about two broad aspects of what central banks do. The first is to try to achieve macroeconomic stability. And by that, I generally mean stable growth in the economy, avoiding big swings, recessions and the like, and keeping inflation low and stable. So that's the economic function of a central bank. The other function of central banks, which is going to get a lot of attention, obviously, in these lectures, is the financial stability function. Central banks try to keep the financial system working normally and in particular, they either, they try to prevent or if unsuccessful in preventing they try to mitigate financial panics or financial crises. And I'll talk more about what those are. Now what are the tools that central banks use to achieve these two broad objectives? Very, in very simple terms, there are basically two broad sets of tools. On the economic stability side, the main tool as I'm sure everyone knows is monetary policy. In normal times, the Fed, for example, can raise or lower short-term interest rates. It does that by buying and selling securities in the open market. And again, in normal times, if the economy is growing too slowly or inflation is falling too low, the Fed can stimulate the economy by lowering interest rates. Lower interest rates feed through to a broad range of other interest rates that encourages spending, acquisition of homes for example, construction, investment by firms, borrowing. It just generates more demand, more spending and more investment in the economy, and that creates more thrust in growth so that to stimulate an economy, you lower interest rates. And similarly, if the economy is growing too hot, if inflation is becoming a problem, then the normal tool of central bank is to raise interest rates. So by raising the overnight interest rate, known in the United States as the federal funds rate, higher interest rates feed through the system and help to slow the economy by raising the cost of borrowing, of buying a house, of buying a car, or of investing in capital goods and that will slow the economy and reduce pressure of overheating. So, monetary policy is the basic tool that central banks have used for many, many years to try to keep the economy at a more or less even keel in terms of both growth and inflation.Now, a little less familiar is the main tool of central banks in dealing with financial panics or financial crises. And that tool is the provision of liquidity. So to address financial stabilityconcerns and for reasons I'll explain, one thing that central banks can do is make short-term loans to financial institutions. As I'll explain, providing short-term credit to financial institutions during a period of panic or crisis can help calm the market, can help stabilize those institutions and can help mitigate or bring to an end a financial crisis. So this activity which is an old one, as I'll discuss, is known as the lender of last resort tool. So again, if financial markets are disrupted, financial institutions don't have alternative sources of funding, then the central bank stands ready to service the lender of last resort providing liquidity to the system and thereby helping to stabilize the financial system.Now, there's a third tool which the Fed has had from the beginning and most central banks have which is financial regulation and supervision. Central banks usually play a role in supervising the banking system, assessing the extent of risk on their portfolios, making sure their practices are sound, and in that way, trying to keep the financial system healthy. To the extent that financial system can be kept healthy and its risk-taking within reasonable bounds, then the chance of a financial crisis occurring in the first place is reduced. However, this activity, and I will come back to it, this is something which is not unique to central banks. In the United States, for example, there are a number of different agencies, like the FDIC or the Office of the Comptroller of the Currency that work with the Fed in supervising the financial system. So this is not unique to central banks and so I'll be down playing this for the time being and focusing on the two principle tools, monetary policy and lender of last resort activities.Now, where do central banks come from? One thing people don't appreciate, I think, is that central banking is not a new development. It's been around for a very long time. The Swedes set up a central bank in 1668, three and a half centuries ago. The Bank of England was founded in 1694 and that of course for many decades or if not centuries was the most important and influential central bank in the world, and France in 1800. So, central bank theory and practice is, again, not a new thing. We have been thinking about these issues collectively as an economics profession and in other contexts for many, many years. Now, I've exaggerated slightly in a sense that, say, the Bank of England in 1694 wasn't set up from scratch, it's a full-fledged central bank, it was originally a private institution. And over time, it acquired some of the functions of a central bank such as issuing money or serving as lender of last resort. But over time, these central banks became essentially government agencies, government institutions as they all are today. Certainly, one important responsibility of central banks for much of the period that I'm talking about was to manage the gold standard to issue paper money that was backed by gold and I'll talk more about gold in a few moments.Now, the lender of last resort function, which I mentioned earlier, became important in the-- mostly in the 19th century. Early in the 19th century, the Bank of England was doing a lot of this type of activity and they became very good at it. And as we'll see, while the United States was suffering with banking panics in the latter part of the 19th century, banking panics in the United Kingdom were quite rare. So the Bank of England sort of set the pace in some sense. It was the most important central bank and it helped establish the practices and the approaches that we still use today. Now, I need to talk a little bit because it's less familiar about what a financial panic is. In general, a financial panic is sparked by a loss of confidence in an institution and I think the bestway to explain this is to give a familiar example. How many of you have ever seen the movie "It's a Wonderful Life"? No? Less people are watching Christmas movies than they used to be, I guess [laughter]. Well, one of the problems that Jimmy Stewart runs into as a banker in “It’s a Wonderful Life” is a threatened run on his institution. And what is a run? Well, let's imagine a situation like Jimmy Stewart's situation before there was any deposit insurance, no FDIC. And imagine you have a bank on the corner, just a regular commercial bank, the first bank of Washington, D.C., and this bank makes loans to businesses and the like, and it finances itself by taking deposits from the public and deposits are demand deposits, which means that anybody can pull out their money anytime they want which is important because people use deposits for ordinary activities, like shopping.Now imagine what would happen if for some reason, a rumor goes around that this bank has made some bad loans and is losing money. As a depositor, you say to yourself, "Well, I don't know if this rumor is true or not。

世界名校视频公开课列表

本课程涵盖了数据统计分析的基础内容,共四十二节课。Nicholas P. JEWELL教授主要采取ppt授课方式,让同学们更容易看到合记住知识点。并且复习起来非常方便。

8

《经济学》

斯坦福大学

网易、新浪

中英双字幕

课程简介

很多斯坦福商学院的人自豪地认为,哈佛商学院代表比较传统的经营管理培训,培养的是“西装革履式”的大企业管理人才;而斯坦福商学院则更强调开创新科技新企业的“小企业精神”,培养的是“穿T-恤衫”的新一代小企业家。这种说法有没有道理呢?

13

《美联储与金融危机》

乔治华盛顿大学

新浪

中英双字幕

课程简介

美联储主席本-伯南克将于今年3月份在乔治华盛顿大学商学院中担任四堂课的主讲,内容是阐述美联储在美国经济中所扮演的角色。

14

《银行业危机源起与后果》

英国公开

大学

新浪

中英双字幕

课程简介

2008年秋,全球金融危机,全世界的政府采取紧急措施以防止银行系统崩溃。这场自十九世纪三十年代以来最严重的金融危机造成了经济衰退。在英国,攀升的失业率、下降的房价和突增的政府债务,是银行系统临近崩溃造成的令人忧心的后果。本课深入观察了全球金融市场的衰败,解读银行业危机祸起之处。

耶鲁大学

网易、新浪

中英双字幕

课程简介

本课程通过分析在历史文献中最早的基督教运动提供了对基督教的起源历史研究,主要集中在新约集部分。虽然神学主题将占据我们主要的注意力,但是课程不只对新约的圣经神学部分进行研究。

2

《旧约全书导论》

耶鲁大学

网易、新浪

中英双字幕

课程简介

本课程探讨旧约(希伯来圣经)作为宗教生活的表达和古代以色列的思想,对西方文明的基础性文件。

美联储与中国央行PPT课件

美联储的组成

1)总统任命的联邦储备委员会理事会, 座落于华盛顿。 2)联邦公开市场委员会。 3)12个地方联邦储备银行,坐落在全 国的各大城市。 4)大量的私人银行成员,这些银行需持 有地方联储的不可转让股票 无忧PPT整理发布 5)各种咨询机构。

5

美联储的职责

1.制定并负责实施有关的货币政策。 2.对银行机构实行监管,并保护消费者 合法的信贷权利。 3.维持金融系统的稳定。 4.向美国政府,公众,金融机构,外国 机构等提供可靠的金融服务。 5.发行“美联储券”,即“美元”无忧PPT整理发布

• 美国将全国划分为12个储备区,每区设立一个联

邦储备银行。

8

• (2)联邦储备委员会。联邦储备系统的核心机构是联

邦储备委员会。该委员会由七名委员组成,主席和副主 席各一名,委员五名,由总统任命,并经参议院批准。 委员的任期长达14年,不得连任。

• (3)联邦公开市场委员会。他是联邦储备系统中另一 个重要机构。他有十二名成员组成,包括:联邦储备委 员会全部七名成员,纽约联邦储备银行行长,其他四个 名额由另外11个联邦储备银行行长轮流担任。该委员会 设一名主席,通常由联邦储备委员会主席担任;一名副 主席,通常由纽约联邦储备银行行长担任。另外,其他 所有联邦储备银行行长都可以参加联邦公开市场委员会 会议,但没有投票权。

16

单一银行制度

• 美国商业银行制度最大特 点是单一银行制度,即原则 上商业银行不得建立分支机 构,而银行设立分支机构是 提高效率和盈利水平,增强 安全性的有力措施。

17

实力雄厚的非银行金融机构

非银行金融机构包括:保险公司、储蓄 放款协会、互助储蓄银行、信贷协会、 私人养老金基金、退休金基金、金融 公司、投资 公司等。该类金融机构资 产总额大大地超过商业银行资产总额。 1985年,其资产总额为45622亿美元, 接近商业银行资产的2倍,美国非银行 金融机构如此发达,既是美国金融业 高度发展的结果,又是其金融深化的 标志。

伯南克授课讲义及要点

伯南克授课讲义及要点伯南克作为现任美联储主席走进华盛顿大学创造了美联储的历史,其授课内容完整讲授了央行的职责、美联储的历史、对两次历史性经济危机的应对方式、危机后的政策等内容,所讲授内容是了解美联储这个机构本身以及美国经济的一个很好的渠道,现略加整理,供大家学习交流。

美联储的基本使命:也就是央行的基本使命,一是保持宏观经济稳定。

所有央行都通过货币政策来实现低而稳定的通胀目标,促进稳定经济增长和就业。

二是维持金融稳定。

央行力求保持本国金融体系运转正常;重要的是避免或减轻金融混乱或危机。

金本位制度为什么会退出历史舞台:在金本位制度下,各国货币价值直接用来衡量,货币供给与需求保持一致,从而限制了中央银行对经济的干涉,保持了经济稳定。

然而,因为货币供给量完全受黄金输出入的限制,使其无法适应经济的快速变化与增长。

第二,世界各地黄金的占有量并不均匀,新金矿的发现必定会引起货币价值的巨大波动。

第三,由于各国间的汇率相对稳定,当一国出现赤字时,财政问题很容易大面积扩散到其他使用金本位制的国家。

二战后美联储货币政策的演变:1.美联储-财政部1951年协议。

在二战期间及之后,美联储在财政部压力下将长期利率压得很低,这便降低了美国政府在战争期间的融资成本。

但是,在经济强劲成长期间将利率维持在低水平容易导致经济过热及通货膨胀。

1951年为实现经济稳定,财政部同意终止此项协议,并让联储独立制定利率。

自1951年以来联储一直保持独立,主导货币政策以促进经济稳定,而无需应对短期内的政治压力。

2. 1950年代和60年代早期的联储。

1950年代多数时段和1960年代早期,美联储遵循“逆风而行”的货币政策,即谋求通胀和经济增长都保持合理的稳定水平。

3. 1960年代中期至1979年的货币政策。

1)自1960年代中期起,货币政策变得过于宽松。

2)导致通胀和通胀预期大幅上升。

3)通胀率最高时达到了13%。

4.沃尔克的去通胀化。

美联储主席沃尔克1979年宣称,两位数的通胀率已偏离货币政策的应当运行轨迹。

美联储主席伯南克公开课

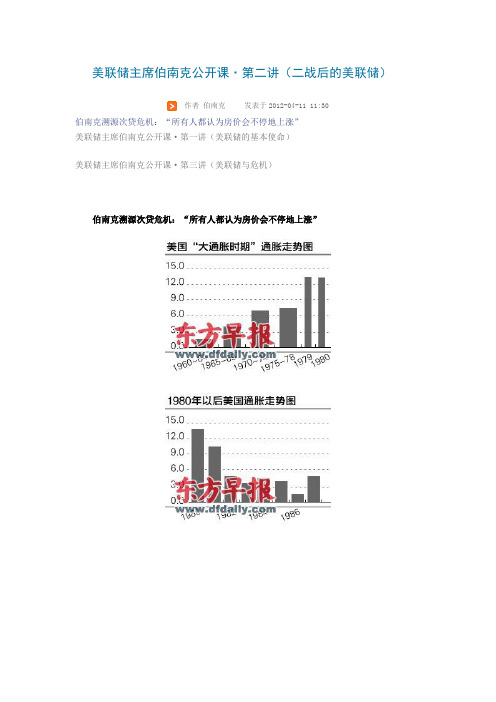

美联储主席伯南克公开课·第二讲(二战后的美联储)作者伯南克发表于2012-04-11 11:30伯南克溯源次贷危机:“所有人都认为房价会不停地上涨”美联储主席伯南克公开课·第一讲(美联储的基本使命)美联储主席伯南克公开课·第三讲(美联储与危机)伯南克溯源次贷危机:“所有人都认为房价会不停地上涨”本版制图郁斐伯南克(Ben S. Bernanke)上次课程(详见东方早报4月9日A24-A26版《伯南克开讲:央行须当最终贷款人,避免银行体系崩溃》)我们回顾了英格兰银行以及美联储的起源、美联储面临的第一个重大挑战、1930年代的大萧条等等。

今天,我将选取第二次世界大战(二战)以后的历史,讨论二战后某些重要的篇章。

我将从2008年次贷危机的起源讲起,本次讲座的后半部分及下一次的全部课程都将讨论危机本身。

危机伏笔:从“大通胀”到“大稳定”我们从二战开始讲起。

战争本身如何获得融资?通常情况下,战争的融资基本上靠借贷,二战期间,美国的国债迅速增长以支付战争所需。

美联储与美国财政部合作,利用其管理利率的能力使利率保持在低位,确保政府能更低廉地为二次大战融资。

战后国债依然存在,政府依然担心如何支付居高不下的国债利息。

因此,在战争真正结束后,美联储背负了将利率保持在低位的巨大压力。

但如果一直保持低利率,经济却持续增长和复苏,将面临经济过热和通胀风险。

1951年就出现了这样的情形,在一系列复杂的谈判后,美国财政部同意结束管制,允许美联储独立地确定必要的利率,以促进经济稳定,相关协议被称为“1951年美联储和财政部协定”,这也是政府首次明确承认美联储应被准许进行独立的运作。

在1950和1960年代,美联储的基本关注点是宏观经济的稳定。

在1951年至1970年担任美联储主席的是马丁(William McC. Martin),任期长达19年,格林斯潘的任期为18年半,他们两位在二战后领导美联储共计长达37年。

伯南克华盛顿大学第三课 美联储对金融危机的反应

17

The Crisisse prices fell, it became clear that the values of many mortgage‐related securities would fall sharply, imposing losses on financial firms, investment vehicles, and credit insurers (like AIG). • Because of complexity of many securities and poor risk monitoring, however, investors and even the firms themselves were unsure about where losses would fall.

4

Financial System Vulnerabilities Before the Crisis

• Private‐sector vulnerabilities

– excessive leverage (debt) – banks’ failure to adequately monitor and manage risks – excessive reliance on short‐term funding – increased use of exotic financial instruments that concentrated risk

– For financial stability: Central banks provide liquidity (short‐term loans) to financial institutions or markets to help calm financial panics.

伯南克公开课第三讲

伯南克公开课第三讲美联储与危机伯南克自辩危机应对:必须“注水”,没冒险使用纳税人的钱希望金融机构“大而不能倒”的困境不再出现2008年以前,美国金融机构极力怂恿居民通过抵押贷款购房伯南克(Ben S. Bernanke)在此前两课中我曾提到这一系列讲座的关键主题是央行的两大主要责任,即力求金融稳定和经济稳定。

为实现金融稳定,央行的主要工具是其作为最后贷款人的能力,央行通过向金融机构提供短期流动性来弥补匮乏的融资。

为实现经济稳定,央行的主要工具是货币政策,包括调整短期利率水平等。

今天我将主要讲讲金融危机发生的2008年和2009年,并关注央行作为最后贷款人的功能。

非优质贷款被“扮靓”并遍布所有金融机构上次我谈到了金融体系中存在的一些脆弱性使房价下跌的影响更加复杂,否则,仅仅房价下降给经济带去的冲击不过是像2000年科技股泡沫散去一样。

这里的脆弱性包括私人机构的脆弱性,包括过度举债等。

而更重要的是,银行无力监管自身风险,从19世纪一些银行的遭遇可以发现,如果短期资金撤出,那么银行面临挤兑状况时将无能为力。

此外,像信用违约掉期和其他有毒金融工具的过度使用等,都会导致风险在特定公司或特定市场中过度集中。

公共机构也存在脆弱性,包括监管结构上的缺陷、重要公司和市场未得到有效监管或至少法律方面的监管不充分等。

例如,监管机构在要求银行提高监管和管理其风险的能力上的努力是不够的。

危机开始后我们也关注到:不同的监管机构负责金融体系中的不同领域,而对整个金融体系的稳定则关注不够。

公共机构存在脆弱性的典型表现就是被称为政府资助企业的房利美和房地美。

房利美和房地美(下称“两房”)虽有股东和董事会,却并不仅仅是私人企业,它们是国会批准成立的,其使命是支持住房市场。

它们并不提供住房抵押贷款,相反,它们是作为中间人存在的,介于房屋抵押贷款最初提供方和抵押贷款的最终持有人之间。

所以,一家银行可以将抵押出售给房利美和房地美,后者会接受这些抵押品,并将其转变成抵押贷款支持债券。

伯南克在美联储的讲演

- 3 - of Iraq in March 2003, as well as a series of corporate scandals in 2002, further clouded the economic situation in the early part of the decade. Slide 1 shows the path, from the year 2000 to the present, of one key indicator of monetary policy, the target for the overnight federal funds rate set by the Federal Open Market Committee (FOMC). The Federal Reserve manages the federal funds rate, the interest rate at which banks lend to each other, to influence broader financial conditions and thus the course of the economy. As you can see, the target federal funds rate was lowered quickly in response to the 2001 recession, from 6.5 percent in late 2000 to 1.75 percent in December 2001 and to 1 percent in June 2003. After reaching the thenrecord low of 1 percent, the target rate remained at that level for a year. In June 2004, the FOMC began to raise the target rate, reaching 5.25 percent in June 2006 before pausing. (More recently, as you know, and as the rightward portion of the slide indicates, rates have been cut sharply once again.) The low policy rates during the 2002-06 period were accompanied at various times by “forward guidance” on policy from the Committee. For example, beginning in August 2003, the FOMC noted in four post-meeting statements that policy was likely to remain accommodative for a “considerable period.”2 The aggressive monetary policy response in 2002 and 2003 was motivated by two principal factors. First, although the recession technically ended in late 2001, the recovery remained quite weak and “jobless” into the latter part of 2003. Real gross domestic product (GDP), which normally grows above trend in the early stages of an economic expansion, rose at an average pace just above 2 percent in 2002 and the first

美联储的起源和使命--伯南克乔治华盛顿大学公开课

美联储的起源和使命--伯南克乔治华盛顿大学公开课广义央行:央行是政府机关,它处于一个国家货币和财政系统的中心地位,它帮助规范现代财政和货币系统的发展,在经济政策中起主要作用.央行的功能:1、(经济功能)促进宏观经济的稳定,即稳定经济增长,防止大的浮动和衰退,保持低而稳定的通胀率。

2、(财政稳定功能)央行尽力保持财政系统的正常运作,央行尤其尽力阻止,若未能阻止就尽力缓解金融恐慌或金融危机。

央行实现这两大目标所使用的工具:第一个工具--货币政策:在稳定经济方面,在常态下,央行主要的货币工具是提高或降低短期利率,通过在开放市场上买进或卖出证券.在常态下,如果经济增长缓慢,或是通胀降至过低,美联储将通过降低利率来刺激经济,低储蓄率将馈通(传导)其他各种利率,这将鼓励消费,例如购置房产,鼓励建设,公司投资,贷款,也就是将引发更多的需求,更多的消费,更多的在经济上的投资,也就拉动了经济增长。

因此要刺激经济,就降低利率;如果经济增长过快,如果通胀过高而成为问题,央行通常的应对是提高利率,通过提高隔夜利率(美国称为联邦基金利率),更高的利率馈通金融系统,这又助于减缓经济,通过提高买房的借贷成本、生产资料投资借贷成本,这将减缓经济过热的压力,因此,货币政策是基本工具,以将经济保持在一个增长和通胀都基本平稳的状态;第二个工具--最后贷款者行为:而我们更不熟悉的工具是央行应对金融恐慌和金融危机的主要工具,即流动性供给,为了解决对金融稳定笥的担忧,以及其他我将解释的原因,央行能做的就是向金融机构提供短期贷款,我将解释在恐慌或危机时期,向金融机构提供短期贷款能稳定市场,稳定金融机构,帮助缓解或结束金融危机,这并不是一个新方法,这种方法被称为“最后贷款者”。

如果金融市场崩溃,金融机构没有其他资金来源,这时央行将随时准备,作为最后贷款者来向系统提供流动性,从而帮助稳定金融系统。

第三个工具:美联储从最初就有的、大多数央行也有的是金融监管,央行通常起监管银行系统的作用,评估其证券投资组合风险程度,保障其行为的合理可靠,从而保持金融系统的健康。

美联储控制基础货币的能力PPT学习教案

第11页/共32页

其他影响基础货币的因素

浮款 财政部在美联储的存款 对外汇市场的干预

第12页/共32页

美联储控制基础货币的能力

公开市场操作由美联储控制 美联储无法决定银行向美联储借

款的金额 基础货币可以分解为两个部分:

MBn= MB - BR

货币供给与非借入基础货币 MBn 和向美联储借第1入3页/共的32页 准备金 BR的 数量成正向关系

第31页/共32页

第23页/共32页

推导货币乘数 II

准备金总额 (R)等于法定存款准备金 (RR) 和超额准备金 (ER)之和 R = RR + ER

法定存款准备金总额等于 法定存款准备金率乘以支票存款总额

RR = r D 用上式替换第一个公式中的 RR

R = (r D ) +ER 美联储制定的 r 小于 1

资产

负债

证券

-$100 流通中现金 -$100

减少了基础货币,减少额等于公开市场出售的金额 准备金保持不变

相比对准备金的影响,公开市场操作对基础货币的影响 更具确定性

第8页/共32页

存款向现金的转化

非银行公众

资产

负债

支票存款 -$100

现金

+$100

银行体系

资产

负债

准备金

-$100 支票存款 -$100

第30页/共32页

图 3 M1 和基础货币, 1929–1933

Source: Milton Friedman and Anna Jacobson Schwartz, A Monetary History of the United States, 1867–1960 (Princeton, NJ: Princeton University Press, 1963), p. 333.

1913年以来美联储政策目标、框架及责任演变

1913年以来美联储政策目标、框架及责任演变一、美联储最初成立目的是维护金融稳定美联储成立之时,人们普遍认为,市场恐慌是因流动资金需求得不到满足导致,成立美联储就是为缓解此种压力,通过贴现窗口为美联储的成员银行提供流动性需求。

美联储早期用于维护金融稳定的框架,很大程度上受到所谓真实票据理论和美国金本位制的影响。

在真实票据理论框架中,美联储通过调节银行系统流动性,满足市场流动性需求,最终实现维护金融和经济稳定目的。

在金本位制背景下,美联储经常采取措施,阻止黄金随国内货币供应变化而流入流出,此种做法,加上美国经济规模,让美联储在货币政策上拥有很大自主权。

最初,美联储主要政策工具是贷款数量和贷款利率,以及贴现率。

后为产生利润以满足其操作,美联储开始在公开市场购买政府证券。

20世纪20年代早期,美联储发现此种操作能影响银行储备和成本等。

此后,公开市场操作成为美联储主要货币政策工具。

二、大萧条时期,美联储放弃国际金本位制和真实票据理论20世纪30年代的大萧条时期,在经济衰退、政治发展等背景下,美联储不完善的政策体系崩溃,未能完成稳定金融的使命。

国际金本位制和真实票据理论也被遗弃。

大萧条使美联储在3个方面发生巨大变化:政策目标、框架、公众责任。

对于政策目标,大萧条期间失业率高企、物价大幅震荡,使得美联储增加了提高或维护充分就业、稳定物价的使命。

对于政策框架,开始关注货币政策对实际经济活动和就业的影响,以及帮助减少周期性波动。

同时,不再注重于维护金融稳定,部分原因是20世纪30年代成立了联邦存款保险公司和证券交易委员会,以及其他改革促使金融体系变得更稳定。

在治理和对公众责任上,1935年的银行法,从法律上加强了美联储独立性,为其提供了更强集中控制力。

尤其该法案创造了现代美国联邦公开市场委员会(FOMC)设置,董事会大多数委员拥有表决权。

但实践中,财政部继续对货币政策有很大影响,直到1951年美联储才开始恢复真正独立。

本 伯南克

在高中时代,他就是加州SAT考试年度最高分获得者,大学入学考试成绩达到1590分,离满分仅差10分。高 中毕业时,由于伯南克在各方面的优秀表现,他获得了美国高中毕业生的最高荣誉“美国优秀学生奖学金”。

1975年,伯南克在哈佛大学获得经济学最优等成绩,并于1979年在麻省理工学院(MIT)获得博士学位。在 麻省理工学院攻读博士学位时,伯南克最感兴趣的有两件事:美国20世纪30年代的经济大萧条和波士顿红袜棒球 队。“进入麻省理工后的第一个秋季,我逃了许多堂课,就为了看棒球联赛。”伯南克回忆说。那一年,波士顿 红袜队输掉了比赛,他至今仍为此伤心。同时,伯南克对美国经济大萧条的浓厚兴趣使他潜心思考和研究大萧条 的原因,并开始长期通货紧缩对经济所构成的威胁。

在离开学术界进入美联储以来的近三年里,伯南克更多的仍然是表现出了自己的学者风范,而不像是一个体 制内的政治决策者。凭借着自己脑子里的诸多新想法,他很快就为自己赢得了“个人创意工厂”的称号。他的自 由思想方式在那些早就习惯了美联储高度谨慎行事风格的银行家和投资者中很受欢迎。

不过令人惊奇的是,虽然伯南克的思维非常独立和活跃,但美联储此时表现出了更大的宽容。在2004年一次 采访中,伯南克表示:“我认为,我的很大一部分贡献,是我作为一名学术界人士、一名智囊人员所做出的。美 联储里没有人试图来协调我的观点,也没有人叫我闭嘴。”

伯南克讲话 伯南克美联储年会讲话全文 精品

伯南克讲话伯南克美联储年会讲话全文伯南克表示:美联储拥有一系列的工具,能利用这些工具提供额外的货币刺激性措施.他还表示,定于9月份召开的下次货币政策制定会议的会期将从一天增加至两天,目的是允许美联储理事对美国经济状况及美联储可能作出的回应进行更加完整的讨论.以下是伯南克此次讲话的全文内容:早上好.如往常一样,感谢堪萨斯城联储组织此次会议.今年的主题是美国的长期经济增长,把这作为主题是相当中肯的,正如过去几年时间里那样.尤其是,金融危机及接踵而至的缓慢的经济复苏进程已经促使某些人提出了一个问题,那就是虽然美国仍将拥有旺盛的长期增长,但是否有可能.不会面临更长的萧条时期.人们想知道的是,过去几年时间里非常缓慢的经济复苏进程——不仅在美国如此,在其他许多发达经济体中也是如此——是否会转变成某种更加持久的局面?我当然能够理解这些担忧情绪,而且完全认识到我们在恢复有益于健康增长的经济和财务状况方面所面临的挑战,并将在今天讨论其中一些话题.但就长期前景而言,我自己的观点更加乐观一些.就像我将讨论的那样,虽然重要的问题当然是存在的,但美国经济增长的基本面看起来并未因在过去四年中受到冲击而发生了永久性的变化.虽然可能需要花些时间,但我们有理由预期美国经济将重返与潜在基本面相一致的增长率和就业水平.但就过渡时期而言,美国经济政策制定者所面临的挑战是双倍的,也就是首先要帮助美国经济从危机和随后的衰退中进一步复苏;其次则是,在这样做的同时,还必须允许美国经济实现其长期增长潜力.经济政策应依据这两个目标来进行评估.今天早上,我将提供一些有关为何到目前为止美国经济复苏进程在很大程度上令人失望的想法,此外还将讨论美联储的政策回应.然后我将回到美国经济长期前景,以及美国经济政策需要在短期和长期前景两方面都必须行之有效的话题上来.经济和政策的近期前景讨论近期经济和政策前景的问题会让我想起,我们是如何落到今天这步田地的.在2019年和2019年中,全球市场被金融危机笼罩,这是大萧条时期以来最严重的一场危机.在2019年秋天,世界各地的经济政策制定者都看到,全球金融危机的风险正在上升,而且也明白这样的经济事件可能会带来十分黯淡的经济后果.正如我在这一论坛上曾经描述过的那样,各国政府和央行采取了强有力的行动,而且彼此间密切协调合作,试图避免即将来临的崩溃局面.无论是在美国还是海外,政策制定者都采取了行动来稳定金融体系,其方式是推出了重大的货币和财政刺激性措施.但是,尽管各国联手采取了这些强有力的措施,但全球经济仍无可避免地受到了严重损害.信贷冻结、资产价格急剧下跌、金融市场失灵以及由此而来的信心受挫导致全球生产和贸易在2019年底和2019年初进入自由落体的状态.我们今天在此召开会议,恰恰是在金融危机最强烈阶段的三年以后,同时也是国家经济研究局(NRER)判定经济开始复苏的两年多以后.那么,我们现在正站在什么位置上呢?过去几年时间里,经济状况发生了一些正面的发展,尤其鉴于我们在危机最深时所看到的经济前景这一方面来考虑就更是如此.从整体而言,全球经济已经实现了重大的增长,其中新兴市场经济体的增长速度最高.在美国,虽然按历史标准来看增长比较温和,但周期性的复苏进程已经进入第九个季度.在金融领域中,美国银行系统的整体健康性已大幅增强,银行持有的资本大幅增加.来自于银行的信贷可用性已有所改善,虽然在小企业贷款等类别中仍很紧缩.在这些贷款类别中,潜在借方的资产负债表仍旧受损.能进入公开债券市场融资的公司能够以有利的条款获得信贷.重要的是,金融部门中的结构性改革正在进行,国内外监管机构都已采取了雄心勃勃的计划,其目的是增强银行资本和流动性,尤其是具有系统重要性的银行;增强风险管理和提高透明度;增强市场基础设施;以及推出更加系统的或宏观谨慎的金融监管。

金融的本质

美联储为美国国际集团提供了紧急流动性援助,从而使其免于破产。

华盛顿互惠银行被摩根大通收购。

(2)应对举措

2008年10月10日,七国集团例行峰会在华盛顿举行,会议拟定了一份国 际申明,根据这些原则,各国将会共同采取措施来避免那些具有系统重 要性的金融机构破产。

美联储通过贴现窗口工具为银行提供短期融资。此次危机中,为了将 更多的流动性注入金融体系,延长了贴现窗口贷款到期时间。(通常是 隔夜到期),并且还对贴现窗口资金进行招标,让企业通过竞标决定其 贷款利率。

金融危机和恐慌往往发生在这样的情况下:各类金融机构资产负债表 的资产端往往都是低流动性资产(如长期贷款),而负债端都是高流动 性的短期负债(如储蓄存款)。在这种情形下,人们一旦对金融机构失 去信心,便会发生挤兑。这次金融危机带来的损失规模之所以这么大关 键在于这些住房抵押贷款分布于不同的证券中,并在不同的市场上进行 流动,没有人真正知道这些证券在哪儿,也没有人知道谁将会遭受损失。

(3)金融恐慌

金融系统都是建立在信念之上的。金融危机就是显而易见的银行挤 兑,是对整个金融系统的挤兑。人们对资金安全失去信心—无论是股东 还是债券持有者,无论是机构投资者还是鳏寡孤独—他们从金融系统中 暴走挤兑是体系的钱更加不安全,也是每一个人失去信心,而人类惯于 恐慌。

解决这一问题有个“白芝浩原则”。沃尔特•白芝浩是一名记者,他 认为在恐慌时期,中央银行应当大量放款,只要找上门来的人有抵押物。 这些抵押物必须是优质安全的,否则贷款就必须进行打折计算,同时央 行应征收惩罚性的利率,这样人们才不会利用恐慌局势占便宜。

2、“二战”后的美联储

(1)货币政策与通货膨胀

20世纪五六十年代,美联储主要关注的是维持宏观经济稳定。美联储 当时试图遵循所谓的“逆风向”货币政策。即经济过热时,采取紧缩性的 货币政策,经济增长缓慢时,采用扩张性的货币政策。

走进美联储(1)

决定公司主要是否从事财务活动

2

美联储的货币发行机制

美联储货币发行机制

美联储货 币发行机 制

美联储基 础货币投 放渠道

美联储三 大利率调 控机制

购买美 国国债

再贴现 贷款

购入黄 金等储备

资产

联邦基 准利率

贴现利 率

存款准 备金率

美联储货币发行机制,对于完善我 国货币发行制度的启示:

1.改革外汇管理制度,实现藏汇于民应该是完善我 国货币投放机制必然选择。 2.利率调控的市场化 3.美联储的货币体系也是造成通货膨胀的元凶,我 们不能盲目的学习,要根据国情作出相应的调整。

走进美联储

组长:吴虹 内容整合:陈珍真 银军霞 吴虹 徐海辉

PPT制作:傅珂愫 黄雨欣

录

目

02 03

04

01

美联储基本介绍

美联储的货币发行机制

美元如何成为世界货币霸主

பைடு நூலகம்

课题延伸

1

美联储基本介绍

美联储基本介绍

01 02 03 04

美联储产生的背景

美联储的结构

建立美联储的目的

美联储的基本职能

05

美联储近期的一些发展情况

1985年成立广场协议后,日元拉 开了不断升值的序幕, 但利率下降 和日元升值,却给日本出口企业带来 成本的上升、竞争力下降的困境,广 场协议后十年中日本汽车工业出口 下降了20%。为了应对这种局面,日 本企业开始纷纷向外转移, 1999年 海外生产比率增至14%。经济危机开 始爆发。

美联储主席百年首为本科生开课 中国女孩问房贷

美联储主席百年首为本科生开课 中国女孩问房贷2012年03月30日最近,毕业于金陵中学的南京女孩吴雨琪,忽然吸引了世界性的关注——3月27日(美国时间),美国乔治华盛顿大学,美联储主席本·伯南克开的选修课上,她作为唯一一名中国学生听课并发问伯南克。

这也是美联储成立100年来头一次由在任主席给本科生开课。

美联储主席为何“破天荒”给本科生上课?南京女孩是怎么获得这一机会的?“央行行长”上课有何与众不同?南京女孩的成长之路怎样?扬子晚报记者昨通过微博联系、并电话采访到吴雨琪及其老师父母。

开课美“央行行长”为何首度开课?“亲民公关”,被视为美联储成立百年“改形象”的信号3月20日,当笑容可掬的“白胡子爷爷”、59岁美联储主席本·伯南克走进教室。

来到她的面前,南京女孩吴雨琪依然感到难以置信——要知道,她只不过是一名大二学生。

而在乔治华盛顿大学,每个年级有2000人,全校有8000人。

经层层筛选上到这堂选修课的只有30人,她,是课上唯一一名中国人。

这也是近100年来,在任美联储主席首次给大学本科生开课,是围绕“反思美联储及其在当今经济环境中的地位”话题的选修课。

由伯南克授课的部分只有4节课,分别在美国时间20日、22日、27日和29日的12:45-14:00。

这之后则由其他老师授课,但学生们要在4月9日给伯南克交一篇论文才算课程结束。

别看这堂课只有1.5个学分,但在全球财经界乃至美国历史上,却有着信号性的转折意义:作为美国负责履行中央银行职责的机构,美联储成立于1913年。

但一直以来都非常神秘。

2008年前,美联储监管不力被视为金融危机起源的因素之一。

因此,这次“亲民公关”被视为美联储迎接成立百年“改形象”的一个信号,为全球财经界关注。

选课8千人进30人,南京女孩何以幸运?“汇率”文章打动伯南克,成课上唯一中国人回顾自己能入选的经历,吴雨琪认为既有努力,也有运气成分。

首先,建校于1821年的乔治华盛顿大学比邻白宫,与美联储同在华盛顿。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Fed–Treasury Accord of 1951

• In 1951, the Treasury agreed to end the arrangement and let the Fed set interest rates independently as needed to achieve economic stability. • The Fed has remained independent since 1951, conducting monetary policy to foster economic stability without responding to short-term political pressures.

Arthur Burns Chairman, 1970–1978

“In a rapidly changing world the opportunities for making mistakes are legion.”

10

The Volcker Disinflation

• To subdue double-digit inflation, Chairman Volcker announced, in October 1979, a dramatic break in the way that monetary policy would operate. • In practice, the new approach to monetary policy involved high interest rates (tight money) to slow the economy and fight inflation.

9

Central Banking in an Evolving Economy

• These experiences illustrate how central banks have to struggle with an evolving economy and imperfect knowledge.

12

The 1981–1982 Recession

• The high interest rates needed to bring down inflation were costly. • In the sharp recession during 1981 and 1982, unemployment peaked at nearly 11 percent.

18

Prelude to the Financial Crisis: The Housing Bubble

• From the late 1990s until early 2006, house prices soared 130 percent. • Meanwhile, mortgage lending standards deteriorated.

– One exception was a boom and bust in the stock

prices of “dot-com” companies that touched off a mild recession in 2001.

• Because of the relative tranquility during this period, monetary policy generally received greater emphasis than financial stability policies.

The Great Inflation: Monetary Policy from the Mid-1960s to 1979

• Starting in the mid1960s, monetary policy was too easy. • This stance led to a surge in inflation and inflation expectations. • Inflation peaked at about 13 percent.

13

The Great Moderation

• During the Great Inflation of the 1970s, both output and Alan Greenspan inflation were highly volatile. Chairman, 1987–2006 • Following the Volcker “… an environment of disinflation, from the mid- greater economic stability 1980s through 2007 has been key to (primarily Chairman impressive growth in the standards of living and Greenspan’s term), both economic welfare so output and inflation were evident in the United much less volatile. States.” • This was the period of “The 14 Great Moderation.”

17

Understanding the Great Moderation

• Financial stresses occurred (for example, the 1987 stock market crash), r economic damage.

Lecture 2: The Federal Reserve after World War II

Lecture 2: The Federal Reserve after World War II

1. Early Challenges 2. The Great Moderation 3. Origins of the Recent Crisis

3

Fed–Treasury Accord of 1951

• During World War II and subsequently, the Fed was pressed by the Treasury to keep longer-term interest rates low to allow the government debt accrued during the war to be financed more cheaply. • Keeping interest rates low even as the economy was growing strongly risked economic overheating and inflation.

• Financial stability

– Central banks try to ensure that the nation’s financial system functions properly; importantly, they try to prevent or mitigate financial panics or crises.

7

The Great Inflation: Why Was Monetary Policy Too Easy?

• Monetary policymakers were too optimistic about how “hot” the economy could run without generating inflation pressures. • When inflation began to rise, monetary policymakers responded too slowly.

Paul Volcker Chairman, 1979–1987

“To break the *inflation+ cycle, … we must have credible and disciplined monetary policy.”

11

Inflation in the 1980s

• In the years after the new disciplined monetary policy began, inflation fell markedly. • When Chairman Volcker left his post in 1987, the inflation rate was around 3 to 4 percent.

8

The Great Inflation: Why Was Monetary Policy Too Easy?

• Exacerbating factors included

– oil and food price shocks – fiscal policies (such as spending for the Vietnam War) that stretched economic capacity – Nixon’s wage-price controls that artificially held down inflation for a time

2

What Is the Mission of a Central Bank?

• Macroeconomic stability

– All central banks use monetary policy to strive for low and stable inflation; most also use monetary policy to try to promote stable growth in output and employment.