个人所得税缴纳说明(中英文版)

个人所得报税流程

个人所得报税流程【中英文实用版】**Personal Income Tax Filing Process****个人所得税申报流程**The personal income tax filing process is a yearly obligation for many individuals.It is important to accurately report your income and claim any allowable deductions or credits to ensure you pay the correct amount of tax.The process can vary depending on your country or region, but generally involves the following steps:对于许多人来说,个人所得税申报流程是一项年度义务。

准确报告您的收入并声称任何允许的扣除额或税收抵免,以确保您支付正确的税额至关重要。

该流程可能因国家或地区而异,但通常包括以下步骤:**Gather Income Information****收集收入信息**Collect all necessary documents that show your income for the tax year.This typically includes W-2 forms (or equivalent) from your employer, 1099 forms for any self-employment or freelance income, and any other relevant documents such as investment statements or interest paid on savings accounts.收集显示税务年度收入的所有必要文件。

税费计算中英文翻译

(INSTRUCTIONS FOR INDI计算公式(Formulas)税级(Tax Backet)一1st 二2nd 三3rd四4th 五5th 六6th 七7th一1st 二2nd 三3rd四4th 五5th 一1st 二2nd 三3rd 四4th 五5th六6th应纳税所得额×适用税率-速算扣除数(Taxable Income * Applicable tax rate - Quick Deduction)1.个人当月取得全年一次性奖金×适用税率-速算扣除数(Annual bonus* Applicable tax rate - Quick Deduction)1.应纳税额=应纳税所得额×适用税率—速算扣除数(Taxable Income * Applicable tax rate - Quick Deduction)2.(全年收入总额—成本、费用以及损失)×适用税率—速算扣除数(The total annual income-Costs, expenses and losses) * Applicable tax rate -Quick Deduction2.年终奖除以12低于2000也要纳税(Year-end awards/12 <2000 is also taxable)3.(个人当月取得年终奖-个人当月工资、薪金所得与费用扣除额的差额)×适用税率-速算扣除数 [Year-end awards- (individual monthly wage and salary -expenses deduction)]*Applicable tax rate - Quick Deduction七7th一1st 二2nd 三3rd 四4th 五5th 六6th 七7th每次收入≤4000元:应纳税额=(每次收入-800)×20%×(1-30%)Income≤4000=(Income-800)*20%*(1-30%)每次收入>4000元:应纳税额=每次收入×(1-20%)×20%×(1-30%)Income≥4000=Income*(1-20%)*20%*(1-30%)每次收入≤4000元:应纳税额=(每次收入-800)×20%Income≤4000 Yuan =(Income per time-800)*20%每次收入>4000元:应纳税额=每次收入×(1-20%)×20%>4000Yuan =Income per time *(1-20%)*20%应纳税额=应纳税所得额×适用税率=每次收入额×20%Tax payable=Income per time *20%对个人投资者从上市公司取得的股息红利所得,减按50%计入个人应纳税所得额Dividend income from listed companies should be reduced to 50%, andincluded in the individual taxable income ≤4000元,每次(月)收入额一准予扣除项目一修缮费用(800元为限)一800元]×20%(出租住房10%)≤4000Yuan=[Income-Deductible items-Repair costs(800 Yuan limit)-800]*20%(Rental housing10%)>4000元,应纳税额=[每次(月)收入额一准予扣除项目一修缮费用(800元为限)]×(1-20%)×20%(出租住房10%)>4000Yuan=[Income-Deductible items-Repair costs(800 Yuan limit)]*(1-20%)(Rental housing10%)应纳税额=(收入总额-财产原值-合理费用)×20%Tax payable=(Income-Original value of property- Reasonable expenses)*20%应纳税额=每次收入×20%Tax payable=Income per time *20%应纳税额=每次收入×20%Tax payable=Income per time *20%>=4000元,=应纳税所得额*适用税率=每次收入额*(1-20%)*20%>4000Yuan =Taxable Income * Applicable tax rate=Income per time *(1-20%)*20%>20000元,=应纳税所得额*适用税率-速算扣除数或=每次收入额*(1-20%)*适用税率-速算扣除数>20000Yuan=Taxable Income * Applicable tax rate-Quick Deduction =Income per time *(1-20%)*Applicable tax rate-Quick Deduction<4000元,=应纳税所得额*适用税率=(每次收入额-800)*20%<4000 Yuan =Taxable Income * Applicable tax rate=(Income per time-800)*20%速算扣除数 [Year-end awards- (individual monthly wage and salary -expenses deduction)]*Applicable tax rate - Quick Deduction。

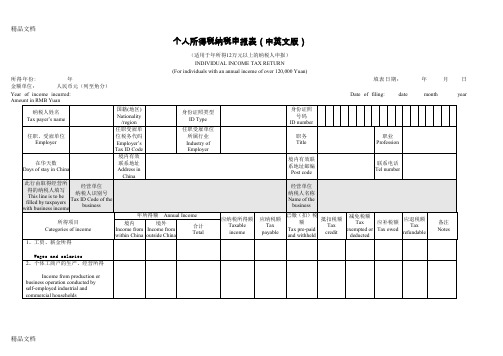

IIT-filing-return-个人所得税纳税申报表(中英文版)教学文稿

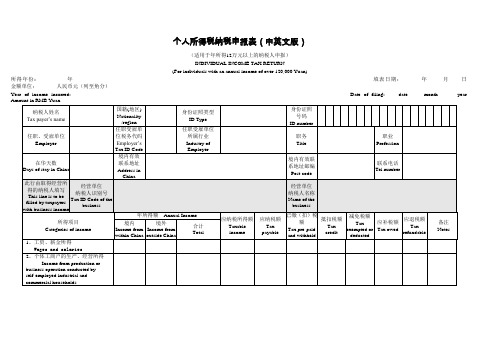

个人所得税纳税申报表(中英文版)(适用于年所得12万元以上的纳税人申报)INDIVIDUAL INCOME TAX RETURN(For individuals with an annual income of over 120,000 Yuan)所得年份: 年填表日期:年月日金额单位:人民币元(列至角分)Year of income incurred: Date of filing: date month year Amount in RMB Yuan章):Signature of responsible tax officer : Filing date: Time: Year/Month/Date Responsible tax offic填表须知一、本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二、负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三、填写本表应当使用中文,也可以同时用中、外两种文字填写。

四、本表各栏的填写说明如下:(一)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职、受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职、受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职、受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

个人所得税缴纳说明(中英文版)

关于缴纳所得税的说明**同志2011年的年薪总收入为*****元,月平均收入****.**元。

2011年住房公积金和社保共****元允许税前扣除。

按照《中华人民共和国个人所得税法》2007年第五次修正版之规定,人员月平均收入2000元以内的不缴纳个人所得税,月平均收入超过额度的按照累进税率计缴个人所得税。

因此2011年已缴个人所得税****元,年薪净总收入*******元左右。

其计算公式如下:应缴纳个人所得税=([(年薪总收入-个税起征点×12个月-全年缴纳社保及住房公积金)/12个月]×税率-速算扣除数)×12个月。

2011年应缴个税为:*******(元)******公司2011年1月1日Explanation of Individual Income Tax CalculationIn 2011, the annual income of **** is RMB*****; then his average income isRMB***** per month. Meanwhile, social insurance and house fund is RMB****. According to Regulations for the Implementation of the Individual Income Tax Law of the People's Republic of China in 2007, tax threshold is RMB2000 per month and those amounts exceeding this will be tax payable. In 2011, ****’s total amount of tax payment was RMB****, and annual net income was RMB****.The calculation formula is as following:annual tax payable = {[(annual income –tax threshold × 12 months – annual social insurance and house fund ) / 12 months] ×tax rate - quick calculation deduction } × 12 months.tax payable in 2010:RMB************* Co., Ltd.1st , Jan. 2011When you are old and grey and full of sleep,And nodding by the fire, take down this book,And slowly read, and dream of the soft lookYour eyes had once, and of their shadows deep;How many loved your moments of glad grace,And loved your beauty with love false or true,But one man loved the pilgrim soul in you,And loved the sorrows of your changing face; And bending down beside the glowing bars, Murmur, a little sadly, how love fledAnd paced upon the mountains overheadAnd hid his face amid a crowd of stars.The furthest distance in the worldIs not between life and deathBut when I stand in front of youYet you don't know thatI love you.The furthest distance in the worldIs not when I stand in front of youYet you can't see my loveBut when undoubtedly knowing the love from both Yet cannot be together.The furthest distance in the worldIs not being apart while being in loveBut when I plainly cannot resist the yearningYet pretending you have never been in my heart.The furthest distance in the worldIs not struggling against the tidesBut using one's indifferent heartTo dig an uncrossable riverFor the one who loves you.倚窗远眺,目光目光尽处必有一座山,那影影绰绰的黛绿色的影,是春天的颜色。

个人所得税法英文版

from their institutions Individual 第 15 章 个人所得税法Chapter 15 Individual Income TaxWho are the individuals liable to Individual Income Tax? What is the income from sources within China? What is the income from sources outside China?What income earned by an individual is subject to Individual Income Tax?How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?What does wage, salary income include specifically?How are salaries and wages assessed for Individual Income Tax payable?How is the “ additional deduction for expenses ” regulated for wages and salaries? How to compute the income tax payable on the bonus income on the year-end in one payment?How to compute the income tax payable on the income of welfare in kind?How to compute the income tax payable on the income stock options of employees of enterprises? How is severance pay taxed?How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?How to calculate the taxable income of individual Industrial and CommercialHouseholds?What are the rules concerning deductions for Individual Industrial and Commercial Households? How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?How do single proprietorship enterprises compute and pay income tax payable on their production and business income?How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return investment? How is income from contracted or leased operation of enterprises or assessed for Individual Income Tax?How is income from remuneration for personal service assessedfor Income Tax payable? How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?What expenses are not allowed for deductions for Individual Industrial and Commercial Households?What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?How to deduct the expenses concerning intangible assets used by IndividualIndustrial and Commercial Households?How do Individual Industrial and Commercial Households compute their income tax payable? How additional income tax is levied on remuneration income that is excessively high at onepayment?How is author ' s remuneration income assessed for Individual Income Tax payable?How is income from royalties assessed for Individual Income Tax payable?How is income from lease of property assessed for Individual Income Tax payable?How is income from transfer of property assessed for Individual Income Tax payable?How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?What do the interest, dividend, bonus, contingent income and/ or other income include specifically?How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?How to compute the income tax payable on income derived by two individuals or more together? How is donation income assessed for Individual Income Tax payable?How to compute the income tax payable in case that the employers bear theIndividual Income Tax for the taxpayers?How is income derived from sources outside China assessed for Individual IncomeTax payable?What are the main exemptions for Individual Income Tax?What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State?What are the main reductions for Individual Income Tax?What are the rules concerning the mode, time and places for Individual Income Tax payment? How to report and pay income tax on wages and salaries income?How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?How to report and pay income tax on income earned by taxpayers from sources outside China?税率 个丄八所得税法趙颔累进税率*九级、五级 比例税率;20^0(有加咸与減征)应纳税所得额规走Y J 纳税申报及缴纳代扣代缴L 两个判走标准厂纳税义筈兀1-居民纳税人与非居民纳税人划分应税所得项目’ 11个税目税收优惠境外所得已纳税额扣除’分国又分项计算扣除限额,差颔补税自行申扌艮 纳税义务人 判定标准 征税对象范围1.居民纳税人 (负无限纳税 义务) (1) 在中国境内有住所的个人(2) 在中国境内无住所,而在中国境内居住满一年的个 人。

中英文版扣缴个人所得税报告书反面 精品

根据《中华人民共和国个人所得税法》第九条的规定,制定本表,扣缴义务人应This return is designed in accordance with the provisions of Article 9 of INDIVIDUAL INCOM CHINA .The withholding agents should turn the tax withheld over to the State Treasury and authorities within seven days after the end of the taxable month.如果由扣缴义务人填写完税证,应在报送此表时附完税证副联______份General accountant(signature)填 表 须 知一、本表适用于扣缴义务人申报扣缴的所得税额。

二、扣缴义务人不能按规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准三、扣缴义务人未按规定期限向税务机关报送本表的,依照税收征管法第三十九条的规定四、填写本表要用中文,也可用中、外两种文字填写。

五、本表各栏的填写如下:1、扣缴义务人编码:填写办理税务登记时,由主管税务机关所确定的扣缴义务人的税务编码。

2、填写日期:填写办理扣缴申报时的实际日期。

3、扣缴义务人名称:填写实际支付个人工资、薪金等项所得的单位或个人的法定名称或姓名。

4、纳税人姓名:纳税义务人如在中国境内无住所,其姓名应当用中文和外文两种文字填写。

5、所得项目:按照税法规定项目填写。

同一纳税义务人有多项所得时,应分别填写。

6、所得期间:填写扣缴义务人支付所得的时间。

7、扣缴所得税额:适用超额累进税率的,按下列公式计算:速算扣除数=前一级的最高所得额×(本级税率-前一级税率)+前级速算扣除数扣缴所得税额=应纳税所得额×适用税率-速算扣除数适用比例税率计算的,按下列公式计算:扣缴所得税额=应纳税所得额×税率8、完税证字号与纳税日期:填写扣缴义务人在扣缴税款时填开的完税证(代缴款书)的字号及纳税日期Instructions1.This return is to be filled out by withholding agant as declaration on the withholding o2.In case of inability to file the return within the prescribed time limit,appliration sho tax authorities within the prescribed time limit and the filing time may be appropriatel3.In case of failure to submit the return within the prescribed time limit,punishment shal of Article 39 of THE OF PEOPLE'S REPLBLIC OF CHINA CONCERNING ADMINISRATION OF TAX COLLE4.The return should be filled out in Chinese language or both Chinese and foreign language5.Instructions for filling out items:a.withholding agent's file number:the file number given by the tax authorities in charge ab.Date of filling:the actual date of filling out the return. of withholding agent:the official name of unit or individual actually paying wages, to the tax payer.d.Tax payer's name:in case the tax payer have no domicile in china,the tax payer's name she.Categaries of income : the categaries of income stipulated in the tax law. In case the t state them separately.f.Income period : the date of the withholding agent making the paymentg.Amount of tax withheld:Where progressive rates are applicable,the formulas are:Quick the maximum income tax rate of tax rete of the quick calculationcalculation=of the preceding×(this income-the preceding)+deduction of thededuction range range range preceding rangeAmount of tax withheld=taxable income×applicable tax rate -quick calculation deduction Where flat rate is applicable,the formula is:Amount of tax to be withheld =taxable income tax rate.h.Tax certificate number and date of tax payment :the serial number and filling date of th payer by the withholding agnet when the tax is withheld.i.Declaration :to be signed by the payer , or by anthorized agent in case the tax payer is扣缴个人所得税报告表INDIVIDUAL INCOME TAX WITHHOLDING RETURN务人应将本月扣缴的税款在次月七日内缴入国库,并向当地机关报送本表。

个人纳税 英文作文

个人纳税英文作文英文:As a taxpayer, I believe it is important to understand the concept of personal taxation. Essentially, it is the amount of money an individual is required to pay to the government based on their income, assets, and other factors. This money is used to fund various government programs and services, such as healthcare, education, and infrastructure.There are different types of taxes that an individual may be required to pay, including income tax, property tax, and sales tax. Income tax is based on the amount of moneyan individual earns, and is usually calculated as a percentage of their income. Property tax is based on the value of the property an individual owns, such as a home or car. Sales tax is based on the amount of money anindividual spends on goods and services.It is important to understand the tax laws andregulations in your country, as they can vary depending on where you live. For example, in the United States, the tax code is very complex and can be difficult to navigate without the help of a professional. However, there are also many resources available to help individuals understand their tax obligations and file their taxes correctly.One of the benefits of paying taxes is that it helps to support the infrastructure and services that we rely on as a society. For example, taxes help to fund public schools, roads, and hospitals. Additionally, taxes can also be used to support social welfare programs, such as unemployment benefits and food assistance.Overall, while paying taxes may not be the most enjoyable task, it is an important civic duty that helps to support the common good.中文:作为一个纳税人,我认为了解个人纳税的概念非常重要。

个人异地纳税情况说明范文

个人异地纳税情况说明范文(中英文实用版)英文文档内容:Personal Out-of-town Tax Payment Explanation SampleIntroduction:This document aims to provide a detailed explanation of a personal out-of-town tax payment situation.It outlines the reasons for living and working in a different location from the taxpayer"s permanent residence and the implications for tax filing.Reasons for Out-of-town Residence:The taxpayer has relocated to another city for employment purposes.This relocation was necessary due to career advancements and better job opportunities in the new location.The taxpayer has been living and working in this city for the past two years.Tax Implications:As per the tax regulations, individuals are required to file their tax returns in the city where they have their permanent residence.However, in the taxpayer"s case, they are living and earning income in a different city.In order to comply with the tax laws, the taxpayer has been filing their tax returns in both the home city and the city of residence.Tax Filing Process:The taxpayer has been diligently fulfilling their tax obligations byfiling tax returns in both cities.They have been providing accurate and detailed information regarding their income, deductions, and credits in both jurisdictions.The taxpayer has also been keeping track of any tax credits or deductions applicable in each city to minimize their tax liability.Additional Documents:To support the tax filings, the taxpayer has maintained all necessary documents, such as payslips, employment contracts, rental agreements, and utility bills.These documents serve as evidence of the taxpayer"s residence and income in the new city.Conclusion:In conclusion, the taxpayer has been living and working in a different city from their permanent residence for the past two years.They have been filing tax returns in both cities to comply with the tax regulations.The taxpayer has diligently fulfilled their tax obligations by providing accurate information and maintaining necessary documents.This situation has been challenging, but the taxpayer has taken the necessary steps to ensure compliance with the tax laws.中文文档内容:个人异地纳税情况说明范文引言:本文旨在详细说明个人异地纳税情况。

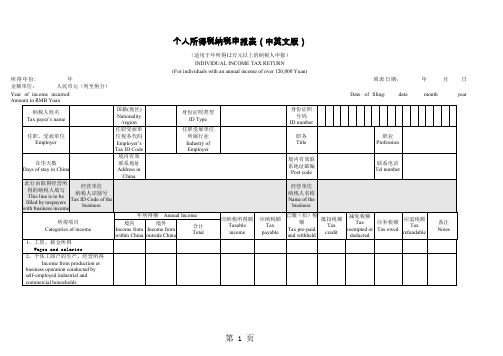

IIT-filing-return-个人所得税纳税申报表(中英文版)教学内容

个人所得税纳税申报表(中英文版)(适用于年所得12万元以上的纳税人申报)INDIVIDUAL INCOME TAX RETURN(For individuals with an annual income of over 120,000 Yuan)所得年份: 年填表日期:年月日金额单位:人民币元(列至角分)Year of income incurred: Date of filing: date month year Amount in RMB Yuan章):Signature of responsible tax officer : Filing date: Time: Year/Month/Date Responsible tax offic填表须知一、本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二、负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三、填写本表应当使用中文,也可以同时用中、外两种文字填写。

四、本表各栏的填写说明如下:(一)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职、受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职、受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职、受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

个人所得税缴纳清单 英文版

个人所得税缴纳清单英文版Here's a draft of an informal and conversational English version of a personal income tax payment statement:First off, let's get the numbers down. For the past year, I've paid quite a bit in taxes. Yeah, it's not fun, but it's a necessary evil, right? The total amount I've shelled out is quite substantial, but it's all for the greater good.You know, sometimes I wonder where all that money goes. But then I remember all the services and benefits we get in return. It's like a trade-off, really. We pay our taxes, and in return, we get a stable government, infrastructure, and social services.This year, I've made sure to keep track of my tax payments. It's important to be aware of what you're paying and why. After all, it's your hard-earned money. So, I've kept all the receipts and documentation organized just so Ican refer back to them anytime I want.Talking about taxes, have you ever tried using a tax calculator? It's super helpful! You can estimate how much you'll owe based on your income and deductions. It's a great way to stay on top of your finances and make sureyou're not paying too much or too little.Lastly, I've learned that it's always a good idea to consult a tax professional if you have any questions or concerns. They can guide you through the complex tax system and help you maximize your deductions and minimize your tax burden. So, don't hesitate to seek help if you need it!。

个人所得税纳税申报表中英文对照7页word

个人所得税纳税申报表(中英文版)(适用于年所得12万元以上的纳税人申报)INDIVIDUAL INCOME TAX RETURN(For individuals with an annual income of over 120,000 Yuan)所得年份: 年填表日期:年月日金额单位:人民币元(列至角分)Year of income incurred: Date of filing: date month year Amount in RMB Yuan章):Signature of responsible tax officer : Filing date: Time: Year/Month/Date Responsible tax offic填表须知一、本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二、负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三、填写本表应当使用中文,也可以同时用中、外两种文字填写。

四、本表各栏的填写说明如下:(一)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职、受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职、受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职、受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

外籍人员在中国缴纳个税的咨询解答 中英对照版本

外籍人员在中国缴纳个税的咨询解答(中英文对照)一、外籍人员在中国的纳税义务如何确定?外籍人员在中国的纳税义务,主要是考虑其是居民纳税人还是非居民纳税人。

居民负有全面纳税义务,非居民只负有部分纳税义务。

二、非居民纳税人纳税义务如何确定?在中国境内无住所又不居住或者无住所而在中国境内居住时间不满1年的个人,为非居民纳税人,具体纳税义务如下:1、无住所而在一个纳税年度在中国境内连续或累计居住时间不超过90日或税收协定规定的期限,属于境内短期停留人员,且不在境内常设机构担任固定职务的,就其实际在中国境内工作期间取得的由中国境内企业或个人支付或者由境内机构场所负担的部分征税。

2、无住所而在一个纳税年度在中国境内连续或累计居住时间超过90日或税收协定规定的期限的,就其实际在中国境内工作期间取得的来源于中国境内和境外的所得缴纳个人所得税。

三、居民纳税人纳税义务如何确定?在中国境内有住所,或者无住所而在中国境内居住满1年的个人,为居民纳税人,具体纳税义务如下:1、在中国境内有住所,应就其境内和境外一切所得一并缴纳个人所得税。

2、在中国境内无住所,但居住时间在1年以上不满5年的,就其在中国境内工作期间取得的来源于中国境内和境外的所得以及在中国境外工作期间取得的来源于中国境内的所得缴纳个人所得税。

3、在中国境内无住所,居住时间满5年的,从第6年起的以后年度,就其境内和境外的所得一并申报缴纳个人所得税。

四、外籍人员取得的哪些所得应视为来源于中国境内的所得,依法征收个人所得税?外籍人员取得的支付地在中国境内的所得,视为来源于中国境内的所得。

但下列所得不论支付地点是否在中国境内,也应视同为来源于中国境内的所得,照章征收个人所得税:(一)因任职、受雇、履约等在中国境内提供劳务而取得的所得;(二)将财产出租给承租人在中国境内使用而取得的所得;(三)转让中国境内的建筑物、土地使用权等财产或者在中国境内使用而取得的所得;(四)许可各种特许权在中国境内使用而取得的所得;(五)从中国境内的公司、企业以及其他经济组织或者个人取得的利息、股息和红利所得。

个人所得税纳税申报表中英文对照--资料

个人所得税纳税申报表(中英文版)税务乩关受理人{签税务机关受理时间, 受理申报税务机关名称(盖字),«):Signature of re^ponzible tax officer : Filing dace: Time: Year Mon± Date Rcuponzible tax offic填表须知本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二.负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三.填写本表应当使用中文,也可以同时用中.外两种文字填写。

四.本表各栏的填写说明如下:(—)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职.受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职.受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职.受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

其中,行业应按国民经济行业分类标准填写,一般填至大类。

(七)职务:填写纳税人在受理申报的任职.受雇单位所担任的职务。

(八)职业:填写纳税人的主要职业。

(九)在华天数:由中国境内无住所的纳税人填写在税款所属期内在华实际停留的总天数。

(十)中国境内有效联系地址:填写纳税人的住址或者有效联系地址。

其中,中国有住所的纳税人应填写其经常居住地址。

非居民个人所得税指南 英文版

非居民个人所得税指南英文版Here's a guide to non-resident individual income tax in a conversational and informal English style, following the requirements you've provided:Non-residents, you're probably wondering about taxes in this country. Don't worry, it's not that complicated. For income earned here, you'll usually need to pay taxes, but there are exemptions. Check the rules for your specific situation.Hey, non-resident friend! When it's time to file taxes, remember to include all your income sources. Even if you only worked here for a short time, you still need to report it. The tax office will appreciate your honesty.So, you're wondering about deductions? Non-residents can usually deduct expenses related to earning that income. Keep track of your receipts and invoices to make sure you get the most out of your tax return.Look, non-resident buddy, taxes can be confusing, but there's help available. The tax office has a website with lots of useful info. You can also hire a tax consultant to guide you through the process.Remember, non-residents, if you're not sure about something, ask! The tax office is there to help you understand your obligations and rights. Don't be afraid to reach out for clarification.And lastly, don't forget to file your taxes on time!。

个税汇算清缴英文指引

个税汇算清缴英文指引Understanding the personal income tax (PIT) annual settlement process is crucial for taxpayers. It's the time when you reconcile your tax payments for the year to ensure accuracy and compliance with tax laws.The process begins with reviewing your income and deductions for the year. This includes salary, bonuses, and any other forms of income, as well as deductions such as charitable donations or educational expenses.Next, you'll need to calculate your tax liability based on the tax brackets and rates applicable to your income. Remember, tax laws can change annually, so it's important to consult the latest tax regulations.Once you've determined your tax liability, compare it to the amount you've already paid throughout the year via withholdings or advance payments. If you've overpaid, you may be eligible for a refund.Conversely, if you owe additional tax, you'll need to make a payment to settle the difference. Failure to do so can result in penalties and interest.It's advisable to consult with a tax professional or use tax preparation software to assist with the calculation and filing process. They can provide personalized guidance basedon your specific financial situation.Finally, ensure you file your annual settlement by the deadline set by the tax authorities. Missing the deadline can lead to additional penalties, so it's in your best interest to stay organized and timely in your tax affairs.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

关于缴纳所得税的说明

**同志2011年的年薪总收入为*****元,月平均收入****.**元。

2011年住房公积金和社保共****元允许税前扣除。

按照《中华人民共和国个人所得税法》2007年第五次修正版之规定,人员月平均收入2000元以内的不缴纳个人所得税,月平均收入超过额度的按照累进税率计缴个人所得税。

因此2011年已缴个人所得税****元,年薪净总收入*******元左右。

其计算公式如下:

应缴纳个人所得税=([(年薪总收入-个税起征点×12个月-全年缴纳社保及住房公积金)/12个月]×税率-速算扣除数)×12个月。

2011年应缴个税为:*******(元)

******公司

2011年1月1日

Explanation of Individual Income T ax Calculation

In 2011, the annual income of **** is RMB*****; then his average income is RMB***** per month. Meanwhile, social insurance and house fund is RMB****.

According to Regulations for the Implementation of the Individual Income Tax Law of the People's Republic of China in 2007, tax threshold is RMB2000 per month and those amounts exceeding this will be tax payable. In 2011, ****’s total amount of tax payment was RMB****, and annual net income was RMB****.

The calculation formula is as following:

annual tax payable = {[(annual income –tax threshold ×12 months –annual social insurance and house fund ) / 12 months] ×tax rate - quick calculation deduction } × 12 months.

tax payable in 2010:

RMB*****

******** Co., Ltd.

1st , Jan. 2011。