Fundamental accounting principles 会计学原理1234689

Fundamental-accounting-principles-会计学原理1234689(汇编)

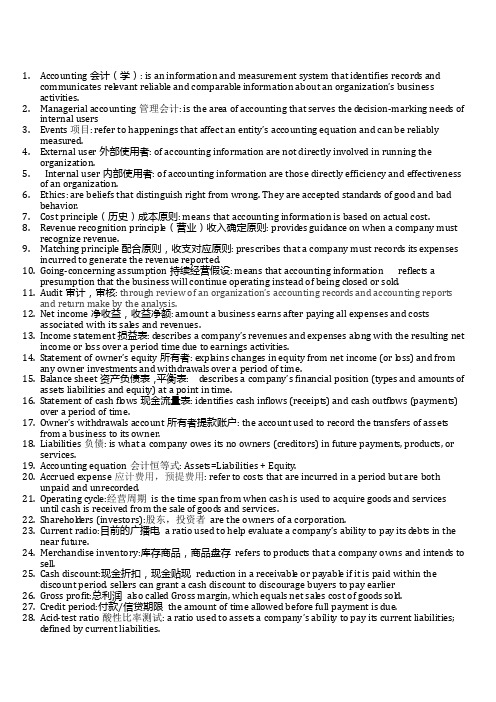

会计学原理概念整理C hapter 1 Accounting in Business第一章商业会计1. 会计信息使用者User of accounting information1. 外部信息使用者:External users of accounting information are not directly involved in running theExternal information user organization.银行 Banks储蓄贷款机构savings and loans 使用债权人消费合作社 co-opsLenders(creditors)抵押 mortgage金融机构 finance companies通用财务报表股东、董事会general-purpose financial statement shareholders(investors)、board of directors外部审计人员 external (independent) auditors员工employees工会 labor union美国国税局 the internal revenue service(IRS)政府管理机构 Regulators公用事业委员会Utility boards证券管理机构 securities regulators选举人 voters立法者 legislators政府官员 government officials捐赠人 contributors供应商 suppliers2. 内部信息使用者: Internal users of accounting information are those directly involved in managing andInternal information users operating an organizations研发经理 research and development managers使用采购经理 purchasing managers人力资源经理 human resource managers生产经理 production managers管理会计销售经理 distribution managersManagerial accounting 营销经理 marketing managers服务经理 service managers内部控制:Internal controls are procedures designed to protect company property and equipment, ensure Internal controls reliable accounting reports,promote efficiency , and encourage adherence to company policies.2. 会计领域的工作机会Opportunities in accounting1)四大领域财务 financial管理 managerial税收 taxation相关领域 accounting-related(见表 accounting opportunities Page4 )2)会计工作所占比例私用会计private accountingAccounting jobs by area公共会计public accounting政府、非营利机构及教育机构government,not-for-profit and education(见表accounting jobs by area Page4)3)会计证书CPA certified public accounting注册公共会计师Accounting certificate CMA certificate in management accounting注册管理会计证书CIA certified Internet auditor注册内部审计证书CB certified bookkeeper 注册簿记员CPP certified payroll professional注册薪金专家PFS personal financial specialist个人理财专家4)一些会计岗位的薪酬Salaries for several accounting position (Page 5)3. 会计基本原则Fundamentals of accounting1.概念accounting is guided by principles ,standards,concepts and assumptions。

Fundamental Accounting Principles (1)

7

01-C3: Ethics

8

1-9

Ethics – A Key Concept

The goal of accounting is to provide useful information for decisions. For information to be useful, it must be trusted. This demands ethics in accounting. Ethics are beliefs that distinguish right from wrong. They are accepted standards of good and bad behavior.

External users of accounting information are NOT directly involved in running the organization. Internal users of accounting information ARE directly involved in managing and operating an organization.

Differences between U.S. GAAP and IFRS are decreasing as the FASB and IASB pursue a convergence process aimed to achieve a single set of accounting standards for global use.

Accounting in Business

Chapter 1

PowerPoint Editor: Beth Kane, MBA, CPA

会计学原理名词解释

1.Accounting会计(学): is an information and measurement system that id entifies records andcommunicates relevant reliabl e and comparabl e information about an organization’s businessactivities.2.Managerial accounting管理会计: is the area of accounting that serves the d ecision-marking needs ofinternal users3.Events项目: refer to happenings that affect an entity’s accounting equation and can be reliablymeasured.4.External user外部使用者: of accounting information are not directly involved in running theorganization.5.Internal user内部使用者: of accounting information are those directly efficiency and effectivenessof an organization.6.Ethics: are beliefs that distinguish right from wrong. They are accepted standards of good and badbehavior.7.Cost principl e(历史)成本原则: means that accounting information is based on actual cost.8.Revenue recognition principl e(营业)收入确定原则: provid es guidance on when a company mustrecognize revenue.9.Matching principl e配合原则,收支对应原则: prescribes that a company must records its expensesincurred to generate the revenue reported.10.Going-concerning assumption持续经营假设: means that accounting information refl ects apresumption that the business will continue operating instead of being cl osed or sol d.11.Audit审计,审核: through review of an organization’s accounting records and accounting reportsand return make by the analysis. income净收益,收益净额: amount a business earns after paying all expenses and costsassociated with its sales and revenues.13.Income statement损益表: d escribes a company’s revenues and expenses al on g with the resulting netincome or l oss over a period time due to earnings activities.14.Statement of owner’s equity所有者: explains changes in equity from net income (or l oss) and fromany owner investments and withdrawals over a period of time.15.Balance sheet资产负债表,平衡表: d escribes a company’s financial position (types and amounts ofassets liabilities and equity) at a point in time.16.Statement of cash fl ows现金流量表: id entifies cash infl ows (receipts) and cash outfl ows (payments)over a period of time.17.Owner’s withdr awals account所有者提款账户: the account used to record the transfers of assetsfrom a business to its owner.18.Liabilities负债: is what a company owes its no owners (creditors) in future payments, products, orservices.19.Accounting equation会计恒等式: Assets=Liabilities + Equity.20.Accrued expense应计费用,预提费用: refer to costs that are incurred in a period but are bothunpaid and unrecord ed.21.Operating cycl e:经营周期is the time span from when cash is used to acquire goods and servicesuntil cash is received from the sale of goods and services.22.Sharehol d ers (investors):股东,投资者are the owners of a corporation.23.Current radio:目前的广播电a ratio used to help evaluate a company’s ability to pay its d ebts in thenear future.24.Merchandise inventory:库存商品,商品盘存refers to products that a company owns and intends tosell.25.Cash discount:现金折扣,现金贴现reduction in a receivabl e or payabl e if it is paid within thediscount period. sellers can grant a cash discount to discourage buyers to pay earlier26.Gross profit:总利润also call ed Gross margin, which equals net sales cost of goods sold.27.Credit period:付款/信贷期限the amount of time all owed before full payment is due.28.Acid-test ratio酸性比率测试: a ratio used to assets a company’s ability to pay its current liabilities;d efined by current liabilities.29.Selling expense:销售费用includ e the expenses of promoting sales by displaying and advertisingmerchandise, making sales, and d elivering goods to customers.(P124)30.General and administrative expense(一般)管理费用: support a company’s overall operatio ns andinclud e expenses related to accounting, human resource management, and financial management. 31.Time period assumption: 会计分期假设presumes that the life of a company can be divid ed intotime periods, such as months and years, and that useful reports can be prepared for those periods.32.Account receivabl e:应收账款are held by a sell er and d ecreased by customers to sell ers.33.Prepaid account (also call ed prepaid expenses): 预付费用/待摊费用are assets that representprepayments of future expenses (not current expenses).34.Purchase discount:购物折扣purchaser’s d escripti on of a cash discount received from a supplier ofgoods.35.Sales discount:销售折扣sell er’s d escription of a cash discount granted to buyers in return for earlypayment.36.Trad e discount:商业折扣reduction below list or catalog price hat is negotiated in setting the price ofgoods.37.FOB shipping point (FOB factory):寄发地交货means the buyer accepts ownership when the goodsd epart the s eller’s place of business.38.FOB d estination: 目的地交货,离岸交货means ownership of goods transfers to the buyer when thegoods arrive at the b uyer’s pl ace of business.39.Credit terms: 信贷条件,赊销付款条件for a purchase includ e the amounts and timing of paymentsfrom a buy to a seller.40.Current assets:流动资产are cash and other resources that are expected to be sol d, coll ect, or usedwithin one year or the company’s op erating cycle, whichever is l onger.41.Plant assets: 固定资产refers to l ong-term tangibl e assets used to produce and sell products andservices.42.Long-term investment:长期投资notes receivabl e and investments in stocks and bonds are long-termassets when they are expected to be hel d for more than the l onger of one year or the operating cycl e.43.Intangibl e assets:无形资产are long-term resources that benefit business operations, usually lackphysical form, and have uncertain benefits. (P98)44.Current liabilities: 流动负债are obligations due to be paid or settled within one year or theoperating cycl e, whichever is l onger.(P98)45.Long-term liabilities长期负债: are obligations not due within one year or the operating cycl e,whichever is l onger.46.Accounting cycl e:会计周期refers to the steps in preparing financial statements.(P95)47.Temporary (or nominal) accounts:临时账户,名义账户accumulate data related to one accountingperiod.48.Permanent (or real) accounts:永久账户,实际账户report on activities related to one or more futureaccounting periods.49.account reveivabl e(应收账款)are liquid assets,usually being converted into cash within a period of30 to 60 days. Therefore, accounts receivabl e from customers are classified as current assets,appearing in the balance sheet immediately after cash and marketabl e securities.50.d oubl e entry accounting(复式记账法)is a standard accounting method that involves each transactionbeing record ed in at l east two accounts, resulting in a d ebit to one or more accounts and a credit to one or more accounts.51.materiality(重要性原则)refers to the magnitud e of an omission or misstatement of accountinginformation that, consid ering the circumstances ,make it likely that the judgment of a reasonabl e person relying on the information would have been influenced by the omission or misstatement. 52.perpetual inventory system(定期盘存制)Und er the perpetual inventory system,the inventoryrecords are kept up-to-date.Virtually all large business organizations use perpetual inventorysystems.53.unearned revenue(预收账款/预收收入)A liability for unearned revenue arises when a customerpays in advance.54.financial statement(财务报表)Four related accounting reports that summarize the current financialposition of an entity and the results of its operations for the preceding year(or other thim period) 55.historical cost(历史成本)The historical cost of an asset is the exchange price in the transaction inwhich the asset was acquired56.d epreciation(折旧)The systematic allocation of the cost of an asset to expense over the years of itsestimated useful57.accrued liabilities(应计负债)The liabilities to pay an expense which has accrued during theperiod.Accrued liabilities are also call ed accrued expenses.58.income(收入)is d efined as increases in economic benefits during the reporting period,in the form ofinfl ows or enhancements of assets,or d ecreases of liabilities tha result in increases in equity,other than those relating to contributions from equity participants.Income encompasses both revenue and gains.59.asset(资产)is a resource controll ed by the enterprise as a result of past events and from whichfuture economic benefits are expected to fl ow to the enterprise.60.account payabl e(应付账款)often are subdivid ed into categories of trad e accounts payabl e and otheraccounts payabl e.Trad e accounts payabl e are short—term obligations to suppliers for purchases or merchandise.Other accounts payabl e includ e liabilities for any goods and services other thanmerchandise.61.FIFO(先进先出法)A method of computing the cost of inventory and the cost of goods sold based onthe assumption that the first merchandise acquired is the first merchandise sol d,and that the ending inventory consists of the most recently acquired goods.62.Goodwill(商誉)The present value of expected future earnings of a business in excess of the earningsnormally realized in the industry.63.cost principl e(历史成本原则)The cost principl e states that assets shoul d by record ed at theircost.Cost is the value exchanged at the time something is acquired.64.权责发生制accrual basis of accounting: Means that revenues, expenses and other changes in assets,liabilities, and owners’ equity are accounted for in the period in which the economic event takes place, not necessarily when the cash infl ows and outfl ows take place利润表income statement :An income statement is a financial statement showing the results of operations for a business by matching revenue and related expenses for a particular accountingperiod .It shows the net income or net loss.永续盘存制perpetual inventory system: Is a system of accounting for merchandise that provid es a continuous record showing the quantity and cost of all goods on hand.总账账户control accounts: Grouped according to the el ements of financial statement, the general l edger hol ds the individual control accounts.费用Expense: Generally speaking, expenses are costs that are charged against ,revenue and that are related to the entity’s basic business.二简答题1.State the steps of establishing internal control over cash(简述建立现金内部控制的程序) (1)Separate the function of handling cash from the maintenance of accounting records(将现金收付与记账职务分离)(2)Prepare an immediate control listing of cash receipts at the time and place that themoney is received(在收到现金的当时当地编制一份现金收入控制清单)(3)Require that all cash receipts be d eposited daily in the bank(每日都要将现金收入存入银行)(4)Make all payments by check(所有的付款都以支票形式通过银行支付)(5)Separate the function of approving expenditures from the function of signing checks(将核准支出职务与签发支票职务分离)2.What are the quality chatacteristics of accounting information(会计信息质量特征):Rel evance(相关性),reliability(可靠性),und erstandability(可理解性),comparability(可比性)3.Describe the steps(procedures) of accounting cycl e(描述会计循环的步骤)(1)id entify transactions or events to be record ed(确认需要记录的交易或事项)(2)journalize transactions and events(将交易或事项登记到日记账)(3)posting from journal to l edger(从日记账过入)(4)prepare unadjusted trial balance(编制调整前余额试算表)(5)journalize and post adjusting journal entries(将调整分录计入日记账并过入分类账)(6)prepare adjusted trial balance(编制调整后余额试算表)(7)prepare financial statements(编制财务报表)(8)journalize and post cl osing entries(将结账分录计入日记账并过账)(9)prepare post-cl osing trial balance(编制结账后余额试算表)4.Briefly state the four assumptions and explain(简述四个会计假设)Separate entity(会计主体假设),going concern(持续经营假设).,time-period(会计分期假设),monetary unit(货币计量假设)5.Briefly state the classification investment in securities(简述有价证券的列报)Trading securities(交易性证券),held-to-maturity securities(持有至到期投资),availabl e-for-sale securities(可供出售的金融资产),l ong-term investment in equity securities(长期股权投资)6.What are the accounting el ements(会计要素)Assets(资产),liabilities(负债),owners’ equity(所有者权益),revenues(收入),expenses(费用),income (利润)d oubl e-entrybookkeeping 复式记账financial statement财务报表accounting equation 会计恒等式owner’s equity所有者权益retained earning 留存收益source d ocument原始凭证computerized accounting system 电算化会计系统accumulated d epreciation累计折旧Proprietorship所有权post-cl osing trial balance调整后试算accrued expense应计费用real/permanent account 实账户nominal/temporary account虚账户notes to the financial statements会计报表附注balance sheet资产负债表Accounting Standards for Business Enterprise 企业会计准则cash fl ow statement 现金流量表l ong-term solvency长期偿债能力short-term liquidity 短期偿债能力provision for bad d ebts 坏账准备construction in progress在建工程d eferred tax on d ebit/credit 递延税款借贷项estimabl e liabilities 预计负债paid-in captical 实收资本accounting treatment 会计处理current period 当期inflation 通货膨胀purchasing power 购买力profit distribution 理论分配accounting information 会计信息IASC 国际会计准则委员会FASB 财务会计准则委员会Liquidity 流动性cash equivalent 现金等价物Financial instrument 金融工具semifinished goods 半成品Low-value and perishabl e articles 低值易耗品weighted average 加权平均法accelerated d epreciation method 加速折旧法moving average 移动平均法trad emark 商标权Copyrights 著作权par value 票面价值sales all owances 销售折让cost variance 成本差异periodic expense 期间费用turnover tax 流转税non-operating expense 营业外支出theoretical framework 理论框架financial distress 财务困境current ratio 流动比例P/E ratio 市盈率M/B 市值与账面价值比capitalization ratio 资本比率Horizontal analysis 横向分析fiscal period 会计期间Vertical analysis 纵向分析price ind ex 价格指数subsidiary 子公司parent company 母公司generally accepted accounting principl es 公认会计准则calendar year 日历年度historical rate 历史汇率Receivabl es 应收账款payabl es 应付账款TQM 全面质量管理TOC 约束理论direct material 直接材料Ord er-getting cost 订单获取成本ord er-filling cost 订单获取成本process costing system 分布成本计算法job-ord er costing system 分批成本计算法step-variabl e cost 阶梯式成本cost formula 成本公式profit margin 贡献边际the high-l ow method 高低点法the scattergraph method 散布图法the least-squares regression method 最小二乘回归法cost behavior 成本性态。

会计学原理约翰·J·怀尔德版上海交通大学

Information useful to help the enterprise achieve its goal, objectives and mission.

Types of Accounting Information

Financial Tax

Managerial

Integrity of Accounting Information

提供商品或服务所有者雇员和供应商顾顾客客债权人人目标和战略投资融资经营短期项目?现金?应收账款?存货长期项目?土地?建筑物?设备?专利?股票和债券短期项目?银行?供应商?员工?政府长期项目?长期债权人?股东采购销售生产管理企业活动概述importanceofaccounting

课程要求--教材与辅助资料

Financial Statements

Internal Users

• • • • • • • •

Board of Directors (董事会) Chief Executive Officer Chief Financial Officer Vice Presidents Business Unit Managers Plant Managers Store Managers Line Supervisors

• Conceptual Chapter Objectives • Analytical Chapter Objectives • Procedural Chapter Objectives

The Accounting Process

Economic Activities

Accounting links decision makers with economic activities and with the results of their decisions.

会计学原理Accounting Principle

3、唐宋时期:流水账和眷清账,“四 柱结算法”。 旧管+新收-开除 = 实 在

4、明清时期:“四柱清册” 进-缴 = 存-该

5、近代:引进复式记账方法

二、西方会计的产生

1、起源:中世纪地中海沿岸。 标志——复式记账 卢卡.巴其阿勒—— 《算术、几何与比例概要》

2、演变:佛罗伦萨式、热那亚式、威尼斯式。 3、发展:产业革命。

§1.5 会计假设 assumption

1、会计主体 accounting entity 2、持续经营 going concern 3、会计期间 accounting period 4、货币计量 measuring unit

§1.6 会计信息质量要求

1、客观性 企业应当以实际发生的交易或 事项为依据进行会计确认、计量和报告,如 实反映符合确认核计量要求的各项会计要素 及其他相关信息,保证会计信息真实可靠、 内容完整。

6、重要性 企业提供的会计信息应当反映与 企业财务状况、经营成果和现金流量等有关的 所有重要交易或者事项。

7、谨慎性 企业对交易或事项进行会计确、 计量和报告应当保持应有的谨慎,不应高估 资产或收益、低估负债或费用。

Fundamental Accounting Principles (2)

5

2-6

The Account and Its Analysis

An account is a record of increases and decreases in a specific asset, liability, equity, revenue, or expense item.

C2

For each transaction, (a) analyze the transaction using the accounting equation, (b) record the transaction in journal entry form, and c) post the entry using T-accounts to represent the general ledger accounts.

An account balance is the difference between the increases and decreases in an account. Notice the T-Account.

C4

19

NEED-TO-KNOW

Identify the normal balance (debit [Dr] or credit [Cr]) for each of the following accounts. 1) 2) 3) 4) 5) 6) 7) 8) 9) 10) Dr. Debit Cr. Credit Dr. Debit Cr. Credit Dr. Debit Dr. Debit Cr. Credit Cr. Credit Dr. Debit Dr. Debit = Prepaid Rent Owner, Capital Note Receivable Accounts Payable Accounts Receivable Equipment Interest Payable Unearned Revenue Land Prepaid Insurance Liabilities Decrease Increase Debits Credits Normal + Equity Decrease Increase Debits Credits

[精品]fundamentalaccountingprinciples第18版第二章资料讲解

![[精品]fundamentalaccountingprinciples第18版第二章资料讲解](https://img.taocdn.com/s3/m/89c3a89676eeaeaad1f33086.png)

Account Number 101 106 126 128 167

201

236 301

Account Name Cash Accounts receivable Supplies Prepaid insurance Equipment

role in double-entry accounting

Analytical Learning Objectives

A1: Analyze the impact of transactions on accounts and financial statements

A2: Compute the debt ratio and describe its use in analyzing financial position

*

*Analyzing and Recording Transactions

Conceptual Learning Objectives

C1: Explain the steps in processing transactions

C2: Describe source documents and their purpose

C1 Analyzing and Recording Process

Exchanges of economic consideration between two parties.

External Transactions occur between the organization and an outside party.

会计学原理23版 英文版课件WildFAP23eCh20PPT

EUP for Materials and Conversion Costs

11 Learning Objective C2: Define and compute equivalent units and explain their use in process costing.

Weighted Average versus FIFO Weighted Average versus FIFO

Learning Objective A1:

Compare process costing and job order costing.

5

Comparing Process and Job Order Costing Systems

Job Order Systems

Process Systems

Goods Sold.

2

Learning Objective C1:

Explain process operations and the way they differ from job order operations.

3

Process Operations

▪ Used for production of identical, low-cost items. ▪ Mass produced in automated continuous

12 Learning Objective C2: Define and compute equivalent units and explain their use in process costing.

Learning Objective

C3: Describe accounting for production activity and preparation of a process cost summary using weighted

Fundamental Accounting Principles

C5

Generally Accepted Accounting Principles

Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP).

Private accounting 60%

Government, not-for-profit, & education 15%

国际四大会计师事务所

PWC 普华永道 DTT 德勤

KPMG 毕马威 E&Y 安永

C4

Ethics—A Key Concept

Ethics

Beliefs that distinguish right from wrong Accepted standards of good and bad behavior

C5

Principles of Accounting

Objectivity Principle Accounting information is supported by independent, unbiased evidence.

Cost Principle Accounting information is based on actual cost.

C3

Opportunities in Accounting

Financial Managerial

•General accounting •Cost accounting •Budgeting •Internal auditing •Consulting •Controller •Treasurer •Strategy •Lenders •Consultants •Analysts •Traders •Directors •Underwriters •Planners •Appraisers

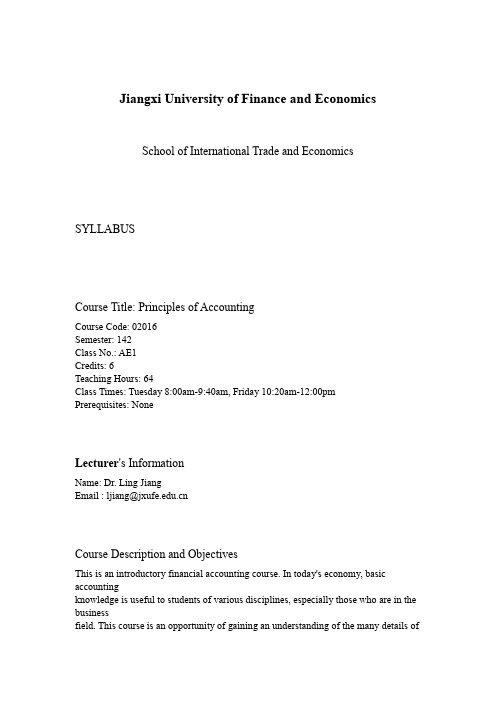

会计学原理双语142AccountingPrinciplesSYLLABUS

Jiangxi University of Finance and EconomicsSchool of International Trade and Economics SYLLABUSCourse Title: Principles of AccountingCourse Code: 02016Semester: 142Class No.: AE1Credits: 6Teaching Hours: 64Class Times: Tuesday 8:00am-9:40am, Friday 10:20am-12:00pm Prerequisites: NoneLecturer's InformationName: Dr. Ling JiangEmail : ljiang@Course Description and ObjectivesThis is an introductory financial accounting course. In today's economy, basic accountingknowledge is useful to students of various disciplines, especially those who are in the businessfield. This course is an opportunity of gaining an understanding of the many details ofoperation of a business entity from a financial information perspective. The focus is on thepreparation of corporate financial statements and interpreting the information by simple analyses.It is a prerequisite to more advanced accounting and business courses.Learning OutcomesUpon completion of the course, a student should achieve the following learning outcomes:Understand the operation of the accounting cycle.Understand how to account for business transactions.Understand how to prepare financial statements.Understand how to analyze a business entity's financial condition and operating results by usingfinancial statement information.Develop accounting-related critical thinking, problem solving, and ethical reasoning skills.1Teaching MethodsTeaching methods include formal lecture, group work, individual exercise, and class discussion.AssessmentFinal Examination 50%20% Mid-Term Examination10% Test 110% Test 210% Homework assignments, attendance, and class participation100%TotalTo obtain a passing grade, a student should achieve at least 60% in total.Tests and ExaminationsTests and Examinations will be held when the related learning content has been completed. Test1 covers chapters 1-4, Mid-Term Exam covers chapter 1-7, Test2 covers chapters 8-11, and theFinal Exam will focus on chapters 8-14, plus limited coverage on chapters 1-7. Homework, Attendance, and Class ParticipationIn-class exercises are opportunities to put chapter knowledge to practice. These can includegroup work, individual exercises, and case discussions. Homework problems are assigned toprovide additional exercises.Your InputYou will be expected to:Participate actively in group work, individual exercises, and class discussions. Complete homework assignments, and submit printed copies when they are due. Review textbook chapters, PowerPoint slides, and other study materials.Course outlineChapter 1 Accounting in BusinessChapter 2 Analyzing and Recording Transactions2Chapter 3 Adjusting Accounts and Preparing Financial StatementsChapter 4 Completing the Accounting CycleChapter 5 Accounting for Merchandising OperationsChapter 6 Inventories and Cost of SalesChapter 7 Accounting Information SystemChapter 8 Cash and Internal ControlsChapter 9 Accounting for ReceivablesChapter 10 Plant Assets, Natural Resources, and IntangiblesChapter 11 Current Liabilities and Payroll AccountingChapter 12 Long-Term LiabilitiesChapter 13 Investments and International OperationsChapter 14 Accounting for CorporationsTextbookJohn J. Wild, Ken W. Shaw, and Barbara Chiappetta, “Fundamental Accounting Principles,”21stedition, revised by Xuegang Cui and Qing Rao, English language reprint edition, McGraw-HillEducation (Asia) Co. and China Renmin University Press, 2013.Tentative Schedule34。

会计学原理 Fundamentals of Accounting

财政部颁发了新《企业会计准则》,并要求 自07年1月1日起在上市公司范围内施行,并

鼓励其他企业执行。新准则的出台标志着与

国际会计准则趋同的中国会计准则体系正式

建立,这在我国会计发展史上将成为新的里 程碑。

• 补充:我国会计法规体系可以从法律来源 上划分为三个层次:一是由全国人民代表 大会统一制定的会计法律如《会计法》; 二是由国务院或财政部制定的会计行政法 规如《企业会计准则》 ;三是由企业根据 《企业会计准则》的规定制定的会计核算 办法。

• 《企业会计制度》由国家财政部和地方财 政部统一制定的.

•

• 补充: 新准则大量借鉴了国际会计准 则的内容体系,包括公允价值的充分应用、 所得税会计、外币折算、职业判断的运用 等方面。

• 包括基本准则、38个具体准则

• 基本准则包括会计假设、会计信息质量要 求、会计要素、会计计量、财务会计报告

(2)国外

返回

• 五、会计对象

– 会计的对象是指会计核算和监督的内容。

• 只有能够以货币计量的经济活动才能纳入会计核算和监督的范 围。

• 能够以货币计量的经济活动通常被称为价值运动或资金运动。

– 因此,会计的对象可以高度概括为特定对象的资金运 动。

第二节 会计核算的基本前提

• 一、会计核算的基本前提: • 1、会计主体 • 2、持续经营 • 3、会计分期 • 4、货币计量

币计量。

三、会计的职能

• 1、反映职能

• 会计反映职能主要是 从价值量方面对会计 主体已经发生或已经 完成的各项经济活动 进行确认、计量、记 录和报告。它是会计 最基本的工作。

• 2、监督职能

• 会计监督职能主要是 利用会计资料和信息 对经济活动进行控制 和指导。监督的核心 是干预经济活动,使 之遵守国家有关法律 法规的规定。包括事 前监督、事中监督和 事后监督。

《财务管理学》课程中英文简介

《财务管理学》课程中英文简介Corporate Finance课程代码:040013A/040013B Course Code:040025A/040015A/040012B 040025A/040015A /040012B 040025A/040015A课程名称:财务管理学Course Name:Corporate Finance学时:48/32/80 Periods:48/32/80学分:3/2/5 Credits:3/2/5考核方式:考查/考试Assessment:Inspection/Examination先修课程:Preparatory Courses:成本管理会计学(上)MA1 Management AccountingⅠ本课程是国际会计专业方向的基础财务管理学课程,主要讲授的是财务经理在进行投资、筹资和日常营运管理过程中如何进行财务决策,才能实现股东财富最大化这一企业理财目标。

先修课程为管理会计基础(MA1)。

该课程主要包括以下内容:(1)财务管理学简介;(2)财务环境和其组成要素分析。

(3)证券估价。

(4)利息率和汇率的确定:利息率的影响因素和确定步骤、利率期限结构、风险溢价、汇率的影响因素、购买力平价理论和利率平价理论。

(5)战略决策——资本预算:主要讲授项目现金流的确定、资本预算方法和决策标准、内部报酬率法的优缺点分析、资本限额决策、资本预算决策中的风险分析。

(6)战略决策——资本成本:主要讲授资本结构、个别资本成本(包括债券、优先股、普通股)和综合资本成本的确定。

(7)经营决策——营运资本管理:主要讲授营运资本筹资决策、存货、应收帐款的管理。

(8)财务计划:主要讲授财务计划(或资金需求计划)的编制和分析。

Corporate Finance Fundamentals [FN1] is a fundamental course in managerial finance with an emphasis on the major decisions to be made by the financial executive of an organization. Topics introduced in FN1 include the following parts:Part 1 Introduction to the corporate finance; Part 2 The financial environment,including the financial system, the major intermediaries and the specialized markets; Part 3 Security valuation: Risk-free assets, including the interest rate as an opportunity cost, varying compound intervals and annuities; Part 4 The determinants of interest rates, including the determinants of interest rates, term structure effects; Part 5 Security valuation: Risk-adjusted discount rates, including the determinants of equity prices, the relationship between the price and the expected return; Part 6 Strategic decisions: Capital budgeting and cash flow estimation, including the capital budgeting process, estimating cash flows; Part 7 Strategic decisions: Capital budgeting evaluation criteria, including the NPV rule measures shareholder wealth, alternative capital budgeting criteria; Part 8 Financial planning, including Important elements in financial planning and the benefits of financial planning.《财务管理学》课程中英文简介Financial Management课程代码:040015A Course Code:040015A课程名称:财务管理学Course Name:Financial Management学时:80 Periods:80学分:5 Credits:5考核方式:考试Assessment:Examination先修课程:会计学基础Preparatory Courses:Accounting财务管理学是会计学和注册会计师专业的学科基础课,开设本课程的主要任务是加强学生对财务管理理论与实务的全面、深入了解,培养学生课堂讨论和课外阅读与写作的习惯,引导学生对有关现代企业财务管理问题进行思考,从而培养出适应市场经济需要的中级理财者。

会计学原理Accounting Principle

§1.7 会计要素确认和计量原则

规范了会计计量的5种计量属性 ➢ 历史成本 ➢ 重置成本 ➢ 可变现净值 ➢ 现值 ➢ 公允价值:适度引入,提高会计信息相关性

(一)历史成本

在历史成本计量下,资产按照购置时支付的现金或者现金等价物 的金额,或者按照购置资产时所付出的对价的公允价值计量。负债 按照因承担现时义务而实际收到的款项或者资产的金额,或者承担 现时义务的合同金,或者按照日常活动中为偿还负债预期需要支付 的现金或者现金等价物的金额计量。

配比原则是根据收入与费用的内在联系,要求将一 定时期内的收入与为取得收入所发生的费用在同一期 间进行确认和计量。在会计核算工作中坚持配比原则 有两层含义:一是因果配比,将收入与其对应的成本 相配比,比如,将主营业务收入与主营业务成本相配 比,将其他业务收入与其他业务成本相配比;二是期 间配比,将一定时期的收入与同时期的费用相配比, 比如,将当期的收入与管理费用、财务费用等期间费 用相配比等。

§1.5 会计假设 assumption

1、会计主体 accounting entity 2、持续经营 going concern 3、会计期间 accounting period 4、货币计量 measuring unit

§1.6 会计信息质量要求

1、客观性 企业应当以实际发生的交易或 事项为依据进行会计确认、计量和报告,如 实反映符合确认核计量要求的各项会计要素 及其他相关信息,保证会计信息真实可靠、 内容完整。

§1.2 会计的目标与会计职能

一、会计目标 1、满足政府宏观管理的需要 2、满足投资者决策的需要 3、满足企业自身管理经营的需要 二、会计的基本职能

反映、监督

§1.3 会计的内容和特点

一、会计的内容 会计核算、会计控制、会计分析、 会计检查、预测与决策

会计双语教程课件

3. Post

4. Prepare Unadjusted Trial Balance

5. Adjust

9. Prepare Post-Closing Trial balance

8. Close

7. Prepare Statements

6. Prepare Adjusted Trial Balance

说课内容

●教

材

● 教学对象 ● 教学内容

● 教学目标 ● 教学方法 ● 教学步骤 ● 板书框架

教材

Fundamental Accounting Principles(12th Canadian edition) Kermit rson,Tilly Jensen;

基础会计(第三版) 孙铮主编,上海财经大 学出版社。

Revenues

教学对象

充满朝气和活力的08级中加合作办学市场 营销专业(MAM)专科学生,初学会计 ,基础薄弱。

教学内容

第五章 结账 第二节 记账过程

重点:实账户与虚账户的概念; 结账过程与结账分录。

难点:结账的涵义; 本期损益账户的结构; 结账分录。

教学目标

知识方面:通过本课程教学,学生应能区 分实账户和虚账户,掌握结账的涵义和步 骤。

Learning Objectives

Describe and prepare a worksheet(工作 表) and explain its usefulness

Describe the closing process(结账过程 ) ,temporary accounts and permanent accounts(虚账户和实账户)

Temporary Account虚帐户

Fundamental Accounting Principles (13)

P1

14

NEED-TO-KNOW

Prepare journal entries to record the following four separate issuances of stock. 1) A corporation issued 80 shares of $5 par value common stock for $700 cash. 2) A corporation issued 40 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $800. The stock has a $1 per share stated value. 3) A corporation issued 40 shares of no-par common stock in exchange for land, estimated to be worth $800. The stock has no stated value. 4) A corporation issued 20 shares of $30 par value preferred stock for $900 cash. General Journal

Record liability for dividend.

June 5 Cash Common Stock, $10 par value Paid-in Capital in Excess of Par Value, Common

Issued 30,000 shares of common stock.

360,000 300,000 60,000

Fundamental Accounting Principles (9)

C1

8

9-9

Installment Accounts Receivable

Amounts owed by customers from credit sales for which payment is required in periodic amounts over an extended time period. The customer is usually charged interest.

09-C1: Accounts Receivable

2

9-3

Accounts Receivable

A receivable is an amount due from another party.

This graph shows recent dollar amounts of receivables and their percent of total assets for four well-known companies. A company must also maintain a separate account for each customer that tracks how much that customer purchases, has already paid, and by providing purchase options to the customer.

Cash collections are quicker.

6

9-7

Credit Card Sales

On July 15, TechCom has $100 of credit card sales with a 4% fee, and its $96 cash is received immediately on deposit.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

会计学原理概念整理C hapter 1 Accounting in Business第一章商业会计1. 会计信息使用者User of accounting information1. 外部信息使用者:External users of accounting information are not directly involved in running theExternal information user organization.银行 Banks储蓄贷款机构savings and loans 使用债权人消费合作社 co-opsLenders(creditors)抵押 mortgage金融机构 finance companies通用财务报表股东、董事会general-purpose financial statement shareholders(investors)、board of directors外部审计人员 external (independent) auditors员工employees工会 labor union美国国税局 the internal revenue service(IRS)政府管理机构 Regulators公用事业委员会Utility boards证券管理机构 securities regulators选举人 voters立法者 legislators政府官员 government officials捐赠人 contributors供应商 suppliers2. 内部信息使用者: Internal users of accounting information are those directly involved in managing andInternal information users operating an organizations研发经理 research and development managers使用采购经理 purchasing managers人力资源经理 human resource managers生产经理 production managers管理会计销售经理 distribution managersManagerial accounting 营销经理 marketing managers服务经理 service managers内部控制:Internal controls are procedures designed to protect company property and equipment, ensure Internal controls reliable accounting reports,promote efficiency , and encourage adherence to company policies.2. 会计领域的工作机会Opportunities in accounting1)四大领域财务 financial管理 managerial税收 taxation相关领域 accounting-related(见表 accounting opportunities Page4 )2)会计工作所占比例私用会计private accountingAccounting jobs by area公共会计public accounting政府、非营利机构及教育机构government,not-for-profit and education(见表accounting jobs by area Page4)3)会计证书CPA certified public accounting注册公共会计师Accounting certificate CMA certificate in management accounting注册管理会计证书CIA certified Internet auditor注册内部审计证书CB certified bookkeeper 注册簿记员CPP certified payroll professional注册薪金专家PFS personal financial specialist个人理财专家4)一些会计岗位的薪酬Salaries for several accounting position (Page 5)3. 会计基本原则Fundamentals of accounting1.概念accounting is guided by principles ,standards,concepts and assumptions。

2. 进行理论决策的指导方针Ethics---a key concept识别分析决策Identity ethical concerns analyze options make ethical decision3. Ethics of business and the social responsibility4. 公认会计原则Generally accepted accounting principles1.目的:make information in financial statements relevant,reliable,and comparable。

2.指定会计准则setting accounting principles两家机构美国财务会计准则委员会 FASB financial accounting standards board (private)Two main groupes 证券交易委员会 SEC securities and exchange commission (government)国际会计准则理事会 IASB Inernational accounting standards board国际财务报告准则 IFRS Inernational financial reporting standards3. 会计准则通则客观性 objectivity PrinciplePrinciples of accounting general principles成本 cost Principle持续经营 going concern Principle货币单位 monetary Principle收入确认原则取得 revenue is recognized when earnedRecognition principle 收入形式 proceeds from selling products andservices need not be in Cash现金+实物价值Cash+any other items会计主体原则独资企业 proprietaryBusiness entity principle 合伙企业 partnership公司 corporation 双重课税 S公司是例外具体准则 specific principles合伙企业 3种合伙人承担的有限责任1.LP 有限合伙企业普通合伙人承担无限责任Limited partnership 有限合伙人以投资额为限承担相应责任2.LLP 有限责任合伙企业对自己及其手下的行为负责Limited liability partnership3.LLC 有限责任公司税收与独资企业相同Limited liability company5. 财务报表损益表 income statement ---- revenue/expense所有者权益表 statement of owner’s equity----beginning capital /ending capitalIncrease investmentEvents IncomeDecrease withdrawalNet lossassets Cash资产负债表 balance sheet SuppliesEquipmentLiabilitiesoperating activities现金流量表 statement f Cash flows InvestingFinancingC hapter 2 Analyzing and Recording Transactions第二章交易分析和记录1.分析和记录过程Analyzing and recording process原始凭证记录过入总账试算平衡表Source document recording posting to Ledger trial balance1.原始凭证Source document2.账户及其分析the account and it’s analysis资产类账户 asset accounts账户概念及分类负责类账户 liability accounts所有者权益类账户 equity accounts总分类账概念: General Ledger (Ledger)is a recordcontaining all accounts used by a company.资产类账户现金 Cash accountasset accounts应收账款 accounts receivable(赊销 credit sales)应收票据 note receivable accounts /promissory note (期票)预付账款 prepaid accounts 保险 prepaid insurance(预付费用 prepaid expenses)费用账户预付租金 prepaid rentExpense accounts 预付服务费 prepaid services物料 supplies 费用账户办公用品(文具纸张笔)Expense accounts office supplies (stationary、paper、toner、pens)商店用品(包装材料、塑料袋、纸袋..)Store supplies (packaging materials、plastic、paper bags)●负债类账户 liability accounts负债人:creditors are individuals and organizations that own the right to receive payment from acompany.应付账款 accounts payable应付票据短期 short-time note payable accountnote payable 长期 long-time note payable account预收账款订阅费礼品券运动队记季票Unarthed revenue magazine subscription gift certificate season tickets sales by sports team订阅费商品销售收入票款收入Unarthed subscription Unarthed store sales Unarthed ticket revenue 应计负债应付工资 wages payableAccrued liabilities 应缴税收 taxes payable付利息 interest payable●所有者权益类账户 equity accounts权益所有者资本 owner’s capitalEquity 所有者提取 owner’s withdrawals所有者收入revenues所有者费用 expenses收入账户销售收入 salesRevenue accounts 佣金收入 commissions earned专业费用收入 professional fees earned租金收入 insurancerent earned利息收入 interest revenue费用账户广告费 advertising expenseexpense accounts 储藏费 store supplies expense办公室职员工资费 office salaries expense租金费 rent expense公共事业支出费 utilities expense保险费 insurance expense2.交易分析与会计处理Analyzing and recording transactions●分类账:Ledger :the collection of all accounts for an information system●会计科目表 chart of accounts 编号列表●T形账户是理解一项或多项交易所带来的影响的一个工具T-account represent a Ledger account and is a tool used to understand the effects of one more transactions.账户名称左:借方右:贷方Dr Cr账户余额:account balance借方余额:debit balance贷方余额:credit balance零余额:zero balance●复式记账法 : 每一笔交易至少会和对两个账户产生影响,要在这两个账户中分别记录。