CIA Part 1 - 2. Charter, Independence, and Objectivity

船运术语缩写

ABT about 大约ABV above 以上ACCT account 由...承担,租船人,租家ADV advise 通知ADD address 地址AFMT after fix main terms 主要条款定下之后AGT agent代理ARBI arbitration 仲裁BBB before breaking bulk 开舱卸货前B/DAYS banking days 银行工作日BENDS.BE both ends 指装卸两头(港)BGD bagged 袋装的BLK bulk 散装(货)BS/L bills of lading 提单BSS 1/1 bases 以一个装港一个卸港为基准BW AD brackish water arrival draft 船到卸港的吃水CHOPT charterers’ option 租家选择CHRTS charterers 租船人,租家CO charterers option 租家选择COMM commission 佣金COUNTER 还盘C/P charter party 租约C.Q.D customary quick dispatch 按港口习惯速度尽快装卸CVS consecutive voyageDFD demurrage/despatch 滞期/速遣DHD demurrage/free despatchDOP droppint outward pilotDRRK derrick 吊杆DWA T deadweight all toldDWCC deadweight cargo capacityEIU even if used 即使使用ETA expected time of arrival 预抵时间ETD expected time of departure 预离时间FHINC Fridays and holidays includedFIO free in & free out 船东不负责装/卸费FIOST free in,out, stowed(理舱)trimmed(平舱)FILO free in , liner out 船东不负责装,但负责卸FLT full liner term 全班轮条款,即船东负责装/卸费FLWS follows 下列FRT freight 运费FWAD fresh water arrival draftGENCON,GCN 金康合同GROSS TERMS liner termsIAC including Address Commission(租家佣金)IACS international association of classification societies 国际船级社LIFO liner in, free out 船东负责装,但不负责卸L YCN laycan laytime and cancel timeL/D loading/discharging 装/卸MIN 至少FLUSIT TWNMOLOO more or less at owners option 增减由船东选择NAABSA more or less at charterers option 增减由租家选择NOR notice of readiness船舶备安通知NOM nominated 指定的OAP over age premium 船的超龄保险OFFER 报盘OO owners option 船东选择OPTN option 选择OWRS owners 船东PART CGO part cargo 拼装P & I CLUB protection and indemnity associations 船东互保协会PPT prompt 即装,马上要装PMT per Metric Ton 每公吨PWWD per weather working day 每晴天工作日RCVRS receivers 收货人SBA safe berth anchor 安全锚地区性泊位SBP safe berth port 安全泊位安全港SDBC,SD single deck 一层舱统舱(船)S/F stowage Factor 积载因素SHEX Sunday holiday Except 星期天,节日不包括在内SHIPPER 发货人SPOT indicates that a ship or a cargo is immediately available. STEM refers to the readiness of cargo and is often a prerequisite to the fixing of a vessel, eg. Subject stem subject to the cargo availability on the required dates of shipment being confirmed. SURVEYORS 验船师SWL safe working load.SW AD salt water arrival draftSUB subject 以…为条件TD,TWN tweendeck 二层舱(船)TIP taking inward pilotTNNG tonnage 指船TTL totalUU unless used 除非使用WIBON whether in berth or not 不管靠泊与否WIFPON whether in free pratique or not 不管船舶检验与否WIJION whether in joint inspection or not 不管船舶联检与否WIPON whether in port or not 不管抵港与否W/M weight or neasureWOG without guarantee 不保证WP weather pernittingWTS working time saved 按节约的工作时间计算WWDSHINC weather working days Sundays and holidays included 晴天工作日,包括星期天及节假日W.W.W.W WIPON,WIBON,WIFPON,WIJIONYRS years 年BLT Built建造年份CALL SIGN: 呼号CBM: 立方米CLASS: 船级DRAFT 吃水DWT: Dead Weight 载重吨FLG: 船旗G/B: 散/包装舱容GRT/NRT: 总登记吨/净登记吨HH: hatch舱口hold舱APS arrival pilot station 到达引航站A TDNSHINE actual time of dispatchBOD bunker on deliveryBOR bunker on redeliveryBallast Water 压舱水Beaufort Scale 蒲福风级3级CONS consumption 消耗耗油Douglas state of sea 3 道式海浪3级DTLS detailsDLOSP 到达引航站DEL delivery 交船deratting certificate 恶意鼠证书ENT/VICT 给船长用于招待的费用FW fresh waterGMT 国际标准时H.cover hatch coverH+M value 船的价值ILOHC 还船时给船员的扫舱费NIL nothing 无IWL institute warranty limitsIFO industrial fuel oil 燃料油KTS knots节Laden 载满MDO 船用柴油marine diesel oil oilMGO marine gas oilNYPE 纽约土产期租船合同P/F prefer宁可,优先RDEL redelivery还船ROB remaining on boardSPD speed 航速—————————————以下可能有重复——————————————AA Always afloat 经常漂浮AA Always accessible 经常进入AA Average adjusters 海损理算师AAR Against all risks 承保一切险AB Able bodied seamen 一级水手AB Average bond 海损分担证书A/B AKtiebolaget (瑞典)股份公司A/B Abean 正横ABS American Bureau of Shipping 美国船级协会ABT About 大约ABB Abbreviation 缩略语A/C,ACCT Account 帐目AC Alter couse 改变航向AC Account current 活期存款,来往帐户AC Alernating current 交流电ACC Accepted; acceptance 接受,同意ACC.L Accommodation ladder 舷梯A.&C.P. Anchor & chains proved 锚及锚链试验合格ACV Air cushion vehicle 气垫船ACDGL Y Accordingly 遵照AD Anno Domini 公元后AD After draft 后吃水ADD Address 地址ADDCOM Address commission 租船佣金ADF Automatic direction finder 自动测向仪AD V AL Ad valorm 从价(运费)ADV Advise;advice; advance 告知;忠告;预支A/E Auxiliary engine 辅机AF Advanced freight 预付运费AFAC As fast as can 尽可能快地AF Agency fee 代理费AFP Agence France press 法新社AFS As follows 如下AFT After 在。

国际会计师资格的了解

国际会计师资格的了解关于国际会计师资格的了解导语:除了中国 CPA 之外,立志于从事会计工作的学子们还有更多选择,对于已经在职的会计从业者来说,也可以更多的了解国际会计师资格以便拓展职业发展之路。

由于国际会计师资格众多,让店铺带大家来迅速了解一下主要的国际会计师资格吧!一、日本1. CPA(Certified Public Accountant)由日本注册会计师(核数师)协会 JICPA 颁发认证,考试极为严苛,通过率仅有 10%不到,可以媲美中国注册会计师考试难度。

二、台湾呃,台湾同胞们都在考中国大陆的 CPA 资格,以前考 ACCA 的比较多。

三、新加坡1. CPA(Certified Public Accountant)由新加坡注册会计师协会(ICPAS)颁发认证,以前与 ACCA 有互认。

四、德国1. WP 和 VBP由德国注册会计师工会(WPK)颁发认证,WP 为法定审计师,VBP 为宣誓会计师,后者只能从事中小型企业的审计业务。

五、西班牙1. CPA(Certified Public Accountant)由西班牙注册会计师协会(以下简称 IACJCE)颁发认证。

六、香港1. CPA(Certified Public Accountant)由香港会计师工会(HKICPA)颁发认证,参加HKICPA 考试需要首先符合会计学专业学位认证或参加香港制定大学的'会计学专业课程,中国注册会计师协会与HKICPA 签署有相关协议,双方部分互认考试科目和成绩。

七、英国1. ACA英国皇家特许会计师 ACA 是在欧洲及全球最为承认的、声望最高的专业资格之一,由英格兰及威尔士特许会计师公会(ICAEW)颁发认证,ICAEW 的历史可以追溯至 1880 年之前。

ACA 在获取资格并工作十年后,通过一定测评还可获得 FCA(Fellow Chartered Accountant)的称号。

ICAEW 约有 138000 名会员,是欧洲人数最多也是影响力最大的会计师团体,这么说是有原因的,看了下面的信息,你就知道它的影响力如何了。

国际货运代理常用英语

国际货运代理相关英语表达(上)Unit 11. freight forwarder 货运代理人2. letter of credit 信用证3。

the mode of transport 运输模式4. freight cost 运费5。

the Forwarder’s Certificate of Receipt 货运代理人收货证明书6. the Forwarder’s Certificate of Transport 货运代理人运输证明书7。

container cargo 集装箱货物8。

foreign exchange trading 外汇交易9. exporting strategy 出口战略10。

cargo transportation 货物运输11。

customs clearance 清关12。

commission agent 委托代理人13. country of transshipment 转运国14。

movements of goods 货物运输15。

shipping space 舱位16。

a bill of lading 提单17. transit country 转口国18。

trade terms 贸易条款19. general cargo 杂货20. special cargoes 特殊货物21. a comprehensive package of service 全面的一揽子服务22. trade contract 贸易合同23。

relevant documents 相关单据24。

take delivery of the goods 提货Unit 2。

1。

FOB (FREE ON BOARD)船上交货2. CIP (COST INSURANCE AND FREIGHT) 运费,保费付至3. CFR (COST AND FREIGHT )成本加运费4. FCA (FREE CARRIER)货交承运人5. CPT (CARRIAGE PAID TO)运费付至6. CIF (COST INSURANCE AND FREIGHT) 成本,保费加运费7. insurance premium 保险费8. multi—modal transport 多式联运9. inland waterway transport 内河运输10. amendment 修改11. carrier 承运人12. ICC- International Chamber of Commerce 国际商会13。

船运常用英文缩写

ABT about 大约ABV above 以上ACCT account 由...承担,租船人,租家ADV advise 通知ADD address 地址AFMT after fix main terms 主要条款定下之后AGT agent代理ARBI arbitration 仲裁BBB before breaking bulk 开舱卸货前B/DAYS banking days 银行工作日BENDS.BE both ends 指装卸两头(港)BGD bagged 袋装的BLK bulk 散装(货)BS/L bills of lading 提单BSS 1/1 bases 以一个装港一个卸港为基准BWAD brackish water arrival draft 船到卸港的吃水CHOPT charterers’ option 租家选择CHRTS charterers 租船人,租家CO charterers option 租家选择COMM commission 佣金COUNTER 还盘C/P charter party 租约C.Q.D customary quick dispatch 按港口习惯速度尽快装卸CVS consecutive voyage,连续航程DFD demurrage/despatch 滞期/速遣DHD demurrage/free despatchDOP droppint outward pilotDRRK derrick 吊杆DWAT deadweight all toldDWCC deadweight cargo capacityEIU even if used 即使使用ETA expected time of arrival 预抵时间ETD expected time of departure 预离时间FHINC Fridays and holidays includedFIO free in & free out 船东不负责装/卸费FIOST free in,out, stowed(理舱) trimmed(平舱)FILO free in , liner out 船东不负责装,但负责卸FLT full liner term 全班轮条款,即船东负责装/卸费FLWS follows 下列FRT freight 运费FWAD fresh water arrival draftGENCON,GCN 金康合同GROSS TERMS liner termsIAC including Address Commission(租家佣金)IACS international association of classification societies 国际船级社 LIFO liner in, free out 船东负责装,但不负责卸LYCN laycan laytime and cancel timeL/D loading/discharging 装/卸MIN 至少FLUSIT TWNMOLOO more or less at owners option 增减由船东选择NAABSA more or less at charterers option 增减由租家选择NOR notice of readiness船舶备安通知NOM nominated 指定的OAP over age premium 船的超龄保险OFFER 报盘OO owners option 船东选择OPTN option 选择OWRS owners 船东PART CGO part cargo 拼装P & I CLUB protection and indemnity associations 船东互保协会 PPT prompt 即装,马上要装PMT per Metric Ton 每公吨PWWD per weather working day 每晴天工作日RCVRS receivers 收货人SBA safe berth anchor 安全锚地区性 泊位SBP safe berth port 安全 泊位 安全港SDBC,SD single deck 一层舱 统舱(船)S/F stowage Factor 积载因素SHEX Sunday holiday Except 星期天,节日不包括在内SHIPPER 发货人SPOT indicates that a ship or a cargo is immediately available. STEM refers to the readiness of cargo and is often a prerequisite to the fixing of a vessel, eg. Subject stem subject to the cargoavailability on the required dates of shipment being confirmed. SURVEYORS 验船师SWL safe working load.SWAD salt water arrival draftSUB subject 以…为条件TD,TWN tweendeck 二层舱(船)TIP taking inward pilotTNNG tonnage 指船TTL totalUU unless used 除非使用WIBON whether in berth or not 不管靠泊与否WIFPON whether in free pratique or not 不管船舶检验与否WIJION whether in joint inspection or not 不管船舶联检与否WIPON whether in port or not 不管抵港与否W/M weight or neasureWOG without guarantee 不保证WP weather pernittingWTS working time saved 按节约的工作时间计算WWDSHINC weather working days Sundays and holidays included晴天工作日,包括星期天及节假日W.W.W.W WIPON,WIBON,WIFPON,WIJIONYRS years 年BLT Built建造年份CALL SIGN: 呼号CBM: 立方米CLASS: 船级DRAFT 吃水DWT: Dead Weight 载重吨FLG: 船旗G/B: 散/包装舱容GRT/NRT: 总登记吨/净登记吨HH: hatch舱口 hold舱APS arrival pilot station 到达引航站 ATDNSHINE actual time of dispatch BOD bunker on deliveryBOR bunker on redeliveryBallast Water 压舱水Beaufort Scale 蒲福风级3级CONS consumption 消耗 耗油Douglas state of sea 3 道式海浪3级 DTLS detailsDLOSP 到达引航站DEL delivery 交船deratting certificate 恶意鼠证书 ENT/VICT 给船长用于招待的费用FW fresh waterGMT 国际标准时H.cover hatch coverH+M value 船的价值ILOHC 还船时给船员的扫舱费NIL nothing 无IWL institute warranty limitsIFO industrial fuel oil 燃料油KTS knots节Laden 载满MDO 船用柴油marine diesel oil oilMGO marine gas oilNYPE 纽约土产期租船合同P/F prefer宁可,优先RDEL redelivery还船ROB remaining on boardSPD speed 航速—————————————以下可能有重复——————————————AA Always afloat 经常漂浮AA Always accessible 经常进入AA Average adjusters 海损理算师AAR Against all risks 承保一切险AB Able bodied seamen 一级水手AB Average bond 海损分担证书A/B AKtiebolaget (瑞典)股份公司A/B Abean 正 横ABS American Bureau of Shipping 美国船级协会ABT About 大约ABB Abbreviation 缩略语A/C,ACCT Account 帐目AC Alter couse 改变航向AC Account current 活期存款,来往帐户AC Alernating current 交流电ACC Accepted; acceptance 接受,同意ACC.L Accommodation ladder 舷梯A.&C.P. Anchor & chains proved 锚及锚链试验合格ACV Air cushion vehicle 气垫船ACDGLY Accordingly 遵照AD Anno Domini 公元后AD After draft 后吃水ADD Address 地址ADDCOM Address commission 租船佣金ADF Automatic direction finder 自动测向仪AD VAL Ad valorm 从价(运费)ADV Advise;advice; advance 告知;忠告;预支A/E Auxiliary engine 辅机AF Advanced freight 预付运费AFAC As fast as can 尽可能快地AF Agency fee 代理费AFP Agence France press 法新社AFS As follows 如下AFT After 在。

航运英语

AFS As follows 如下

AFT After 在。。。之后

A/G Aktiengeselskabet (德)股份公司

AG Act of god 天灾

AGRIPROD Agricultural products 农产品

AS Annual survey 年检

ASA Always safely afloat 经常安全漂浮

ASAP As soon as possible 尽快

AT American terms(grain) 美国(谷物)条款

ATC All time to count 计入全部时间

ATL Actual total loss 实际全损

BS Bioler survey 锅炉检验

BS Balance sheet 决算表

BS Bill of sale 抵押证券

BS Bill of store 船上用品免税单

B/S Bags; bales 包;袋

B/ST Bill of sight 即期汇票

BST British Summer Time 英国夏季时间

AV Average 平均的;海损

AVR Automatic voltage regulator 自动电压调节器

AV Average speed 平均航速

AWB Air way bills 航空提单

ABS.STA Abstract statement 摘要

ADDEE,ADD'SEE Addressee 收信人,收报人

CF Cargo fall 吊货索

CUBF,C.F. Cubic feet 立方英尺

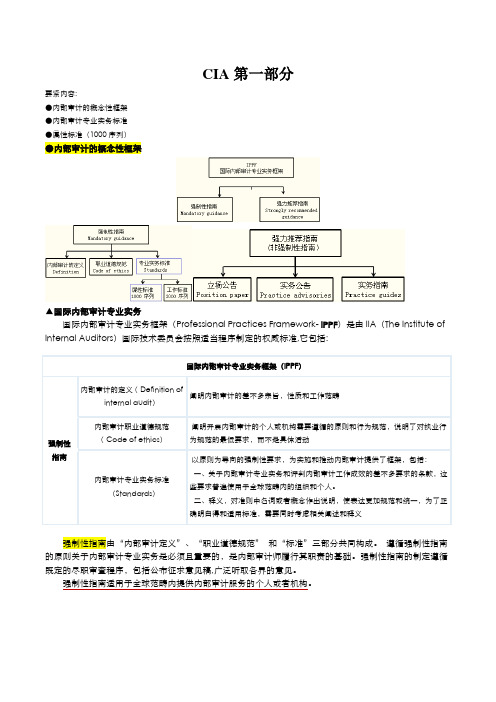

CIA第一部分

CIA第一部分要紧内容:●内部审计的概念性框架●内部审计专业实务标准●属性标准(1000序列)●内部审计的概念性框架▲国际内部审计专业实务国际内部审计专业实务框架(Professional Practices Framework- IPPF)是由IIA(The Institute of Internal Auditors)国际技术委员会按照适当程序制定的权威标准,它包括:国际内部审计专业实务框架(IPPF)强制性指南内部审计的定义( Definition ofinternal audit)阐明内部审计的差不多宗旨,性质和工作范畴内部审计职业道德规范( Code of ethics)阐明开展内部审计的个人或机构需要遵循的原则和行为规范,说明了对执业行为规范的最低要求,而不是具体活动内部审计专业实务标准(Standards)以原则为导向的强制性要求,为实施和推动内部审计提供了框架,包括:一、关于内部审计专业实务和评判内部审计工作成效的差不多要求的条款,这些要求普遍使用于全球范畴内的组织和个人。

二、释义,对准则中名词或者概念作出说明,使表达更加规范和统一,为了正确明白得和适用标准,需要同时考虑相关阐述和释义强制性指南由“内部审计定义”、“职业道德规范” 和“标准”三部分共同构成。

遵循强制性指南的原则关于内部审计专业实务是必须且重要的,是内部审计师履行其职责的基础。

强制性指南的制定遵循既定的尽职审查程序,包括公布征求意见稿,广泛听取各界的意见。

强制性指南适用于全球范畴内提供内部审计服务的个人或者机构。

强力举荐的指南是IIA通过正式批准程序认可的,阐述有效执行内部审计定义, 职业道德规范和标准的实务, 包括立场公告、实务公告和实务指南三部分。

强力举荐的指南尽管不具有强制性, 但它有助于对标准进行说明, 或将标准应用于特定内部审计环境中。

强力举荐的指南能够由胜任的内部审计师凭借其专业判定加以运用。

【典型试题】1、内部审计专业界使用的标准,不包括以下哪项内容?a.用于评估和衡量内部审计部门运行情形的标准。

考研英语真题单词-2016(英一)

2016(一)完形 - 柬埔寨的婚姻 Part1 单词1、recite v.背诵2、spouse n.配偶3、matchmaker n.媒⼈人4、negotiation n.协商5、investigate v.调查6、ritual a.仪式性的7、retain v.保持8、property n.财产9、gender n.性别Part2 短语1、in theory 理理论上2、show up 展现warm up 热身clear up 变得晴朗break up 分裂;离婚Text 1 - 挑战完美身材 Part1 单词1、preliminary a.初步的,预备的2、ultra- 极,超过某限度3、runway n.(延伸观众席的)延伸台道,T 型台4、incite v.煽动,⿎鼓动5、excessive a.过多的,极度的6、uplifting a.(在道德、⽂文化等⽅方⾯面)进⾏行行提升的7、impinge v.侵犯,侵害8、signal n.信号,暗号9、worth n.价值10、enforce v.执⾏行行,实施11、arbiter n.仲裁者,裁决⼈人12、hint v.暗示,示意13、intangible a.⽆无形的14、character n.个性,性格15、intellect n.智⼒力力,才智16、physique n.体格,体型17、severe a.严厉的,重的18、punishment n.惩罚,处罚19、mass n.质量量20、fine v.罚⾦金金,罚款21、inherent a.固有的,内在的22、adornment n.装饰23、index n.指数24、sanction n.制裁,处罚25、ethical a.道德的,伦理理的26、charter n.宪章27、persuasion n.说服28、compliance n.服从,遵从,顺从29、address v.对付,处理理,设法了了解并解决30、misuse v.误⽤用31、elevate v.提升Text 2 - 乡村保护的困境 Part1 单词1、poll n.⺠民意调查2、alongside prep.(与...)相⽐比3、enviable a.令⼈人羡慕的4、specifically ad.特意,专⻔门地5、dweller n.居⺠民6、refreshing a.清爽的,清新的7、pressure v.催促,迫使,呼吁8、concrete n.混凝⼟土9、consume v.消耗10、guardianship n.监护,保护11、endorse v.赞同,⽀支持12、sentiment n.观点,看法13、explicitly ad.明确地14、priority n.优先权15、conservation n.保护16、authorize v.批准,授权17、profitable a.有利利可图的18、likewise ad.同样地19、discontinue v.中⽌止,停⽌止20、council n.(英国地⽅方政府的)政务委员会,地⽅方议会21、plead v.请求22、sensible a.明智的,合理理的23、infrastructure n.基础设施24、identify v.(经考虑)确定25、intrusion n.侵犯26、meadow n.草地27、lobby n.游说团体28、renovation n.翻新29、renewal v.复兴30、out-of-town a.城外的,城郊的31、biased a.有偏⻅见的,偏袒⼀一⽅方的32、coherence a.⼀一致,协调33、corrupt a.破坏的,毁坏Part2 短语1、stick to 遵守Text 3 - 公司的光环效应 Part1 单词1、accept v.承认,同意2、premise n.前提3、clear-cut a.⼀一分为⼆二的、界限分明的4、monetary a.货币的、⾦金金融的5、prosecute v.起诉、告发6、corruption n.(尤指有权势者的)贪污、腐败、受贿7、donate v.捐赠、捐献8、diffuse v.发散、分散9、whereby prep.凭借,通过10、consideration n.体谅、考虑11、differentiate v.辨别、区别12、bribery n.(指⾏行行为)贿赂、⾏行行贿、受贿13、comprehensive a.全⾯面的14、lenient a.宽⼤大的、仁慈的15、penalty n.处罚、惩罚16、substantial a.重⼤大的、可观的17、demonstrate v.表明,证明18、whereas (正是⽤用法)尽管Part2 短语1、engage in 参与、从事2、take sth. as sth. 将...看作是3、good causes 慈善事业4、halo effect 光环效应5、have trouble doing sth. 做某事有困难的6、bank on 指望、依靠7、get into trouble with the law 陷⼊入法律律纠纷Text 4 - 纸媒转型Part1 单词1、cease v.中⽌止、停⽌止(做某事)2、newsprint n.(⽤用来印刷报纸的)新闻纸3、nostalgia n.怀旧之情4、incentive n.激励、刺刺激5、infrastructure n.基础设施、基础结构6、physical a.物质的、有形的7、press n.印刷机8、constraint n.限制、束缚9、migrate v.迁移10、dwarf v.(因⾃自身巨⼤大⽽而)使...显得矮⼩小,使相形⻅见绌11、counterpart n.对应的⼈人或物12、overhead n.企业惯常⽀支出、管理理费⽤用(租⾦金金、保险费、电费等)13、circulation n.(报纸或杂志的)发⾏行行量量、销售量量14、eliminate v.清除、消除15、foresighted a.有远⻅见的,有先⻅见之明的16、favor v.更更喜欢,喜爱,⽀支持17、obsess v.使着迷、使迷住18、subscription n.征订费19、aggressive a.有冲劲的,汲汲于成功的20、tremendous a.巨⼤大的,惊⼈人的Part2 短语1、make sense 有意义2、be obsessed with 沉溺于3、figure out 想出;解决新题型 - 提升职业形象Part1 单词1、context(事情发⽣生的)背景、环境2、present v.展示、展现3、assess v.评估,评定4、trustworthiness ( trustworthy 的变形) n.可信赖度,信⽤用5、solely ad.仅仅6、evolve v.逐渐形成、逐渐演变7、fragment v.(使)破裂、碎裂8、sneaker n.运动鞋9、magnify v.放⼤大,扩⼤大10、headshot n.⼤大头照,头像11、paradox v.⾃自相⽭矛盾12、conscious a.特别感兴趣的,关注的13、executive n.主管领导,⾏行行政领导14、transition n.过渡(期),转变15、perceive v.把...看做,认识16、pivot v.以...为中⼼心旋转17、refresh v.刷新,更更新18、approachable a.和蔼可亲的19、characterization n.(对⼈人或物的)特征描述20、anthropologist n.⼈人类学家21、enlist v.争取,谋取22、barber n.理理发师23、vain a.⾃自负的,虚荣的24、fatigue n.厌倦25、spouse n.配偶26、millennial n.千禧⼀一代27、efficient a.效率⾼高的Part2 短语1、step into 开始做,开始介⼊入2、take sb. seriously 认真对待某⼈人3、look up to 钦佩,尊敬4、fuss over 对某事过于关⼼心5、go-to option 可依赖的选择6、at once 同时,⼀一起翻译 - 放慢⽣生活节奏 Part1 单词1、birthright n.与⽣生俱来的权⼒力力2、mend v.愈合3、reawaken v.重新唤起;再次引发(感情、回忆等)4、nutrition n.营养(作⽤用);滋养5、access n.进⼊入权;使⽤用权;接触的机会6、temporarily ad.暂时地7、self-esteem n.⾃自尊(⼼心)8、perspective n.客观判断⼒力力,权衡轻重的能⼒力力9、innate a.天⽣生的,与⽣生俱来的10、unlearned a.不不学⽽而能的,不不学即会的;天然的11、surround v.环绕,围绕12、cure-all n.万灵药,灵丹丹妙药13、mundane a.平凡的,平淡的;乏味的14、foe n.敌⼈人,仇敌15、conscience n.良⼼心,良知16、instinct n.本能17、immune a.有免疫⼒力力的Part2 短语1、build into 使固定于;使成为...的⼀一部分2、take sb. / sth. seriously 认真对待某⼈人/某事3、work out (问题)逐渐解决;(复杂情况)逐渐化解4、slow down 放慢速度,减缓;松劲;放松5、in an instant ⽴立刻6、gain access to 接近7、common sense 常识⼩小作⽂文 - 通知范文NoticeDecember 20 It is exceedingly great to hear that you, as international students, have been enrolled by Peking University and will begin your study soon in China. Welcome! Today, this notice is for the purpose of providing relevant information about the library.Compared with other libraries, our library is the oldest in China and possesses more varieties of both classical and latest books, which will enable students to acquire diverse information they need. In addition, this library is characterized by its Information System, because you can search for any book merely by typing key words. Finally, it is advisable for you to take your Student Card, since without it, you cannot enter the gate, borrow books or read here. The opening time will be from 8: 00 to 21: 00 on both weekdays and weekends.Hope you enjoy the wholesome atmosphere of study in our library!The Library of Peking University译:通知12⽉月20⽇日听说你们作为国际学⽣生已经被北北京⼤大学录取,并将很快在中国开始学习,真是太棒了了。

CIA大纲2009年英文版本

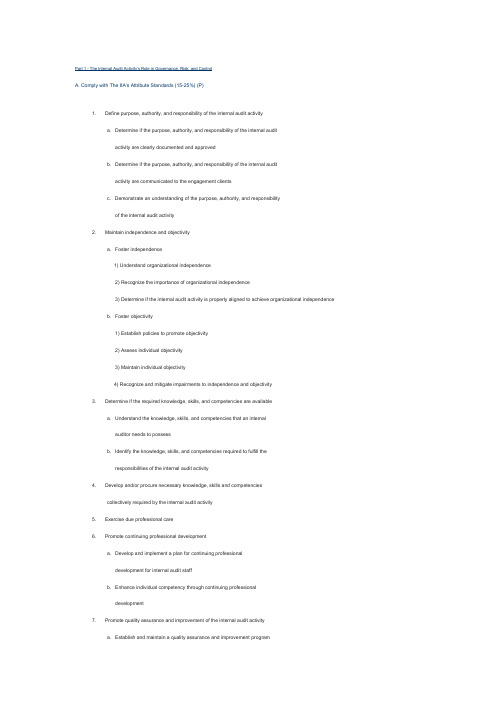

Part 1 - The Internal Audit Activity's Role in Governance, Risk, and ControlA. Comply with The IIA's Attribute Standards (15-25%) (P)1. Define purpose, authority, and responsibility of the internal audit activitya. Determine if the purpose, authority, and responsibility of the internal auditactivity are clearly documented and approvedb. Determine if the purpose, authority, and responsibility of the internal auditactivity are communicated to the engagement clientsc. Demonstrate an understanding of the purpose, authority, and responsibilityof the internal audit activity2. Maintain independence and objectivitya. Foster independence1) Understand organizational independence2) Recognize the importance of organizational independence3) Determine if the internal audit activity is properly aligned to achieve organizational independenceb. Foster objectivity1) Establish policies to promote objectivity2) Assess individual objectivity3) Maintain individual objectivity4) Recognize and mitigate impairments to independence and objectivity3. Determine if the required knowledge, skills, and competencies are availablea. Understand the knowledge, skills, and competencies that an internalauditor needs to possessb. Identify the knowledge, skills, and competencies required to fulfill theresponsibilities of the internal audit activity4. Develop and/or procure necessary knowledge, skills and competenciescollectively required by the internal audit activity5. Exercise due professional care6. Promote continuing professional developmenta. Develop and implement a plan for continuing professionaldevelopment for internal audit staffb. Enhance individual competency through continuing professionaldevelopment7. Promote quality assurance and improvement of the internal audit activitya. Establish and maintain a quality assurance and improvement programb. Monitor the effectiveness of the quality assurance and improvementprogramc. Report the results of the quality assurance and improvement programto the board or other governing bodyd. Conduct quality assurance procedures and recommend improvementsto the performance of the internal audit activity8. Abide by and promote compliance with The IIA Code of EthicsB. Establish a Risk-based Plan to Determine the Priorities of the Internal Audit Activity (15-25%) (P)1. Establish a framework for assessing risk2. Use the framework to:a. Identify sources of potential engagements (e.g., audit universe,management request, regulatory mandate)b. Assess organization-wide riskc. Solicit potential engagement topics from various sourcesd. Collect and analyze data on proposed engagementse. Rank and validate risk priorities3. Identify internal audit resource requirements4. Coordinate the internal audit activity's efforts with:a. External auditorb. Regulatory oversight bodiesc. Other internal assurance functions (e.g., health and safety department)5. Select engagements.a. Participate in the engagement selection processb. Select engagementsc. Communicate and obtain approval of the engagement plan from boardC. Understand the Internal Audit Activity's Role in Organizational Governance (10-20%) (P)1. Obtain board's approval of audit charter2. Communicate plan of engagements3. Report significant audit issues4. Communicate key performance indicators to board on a regular basis5. Discuss areas of significant risk6. Support board in enterprise-wide risk assessment7. Review positioning of the internal audit function within the risk management framework within the organization8. Monitor compliance with the corporate code of conduct/business practices9. Report on the effectiveness of the control framework10. Assist board in assessing the independence of the external auditor11. Assess ethical climate of the board12. Assess ethical climate of the organization13. Assess compliance with policies in specific areas (e.g., derivatives)14. Assess organization's reporting mechanism to the board15. Conduct follow-up and report on management response to regulatory body reviews16. Conduct follow-up and report on management response to external audit17. Assess the adequacy of the performance measurement system, achievement of corporate objective18. Support a culture of fraud awareness and encourage the reporting of improprietiesD. Perform Other Internal Audit Roles and Responsibilities (0-10%) (P)1. Ethics/Compliancea. Investigate and recommend resolution for ethics/compliance complaintsb. Determine disposition of ethics violationsc. Foster healthy ethical climated. Maintain and administer business conduct policy (e.g., conflict of interest)e. Report on compliance2. Risk Managementa. Develop and implement an organization-wide risk and control frameworkb. Coordinate enterprise-wide risk assessmentc. Report corporate risk assessment to boardd. Review business continuity planning process3. Privacya. Determine privacy vulnerabilitiesb. Report on compliance4. Information or physical securitya. Determine security vulnerabilitiesb. Determine disposition of security violationsc. Report on complianceE. Governance, Risk, and Control Knowledge Elements (15-25%)1. Corporate governance principles (A)2. Alternative control frameworks (A)3. Risk vocabulary and concepts (P)4. Risk management techniques (P)5. Risk/control implications of different organizational structures (P)6. Risk/control implications of different leadership styles (A)7. Change management (A)8. Conflict management (A)9. Management control techniques (P)10. Types of control (e.g., preventive, detective, input, output) (P)F. Plan Engagements (15-25%) (P)1. Initiate preliminary communication with engagement client2. Conduct a preliminary survey of the area of engagementa. Obtain input from engagement clientb. Perform analytical reviewsc. Perform benchmarkingd. Conduct interviewse. Review prior audit reports and other relevant documentationf. Map processesg. Develop checklists3. Complete a detailed risk assessment of the area (prioritize or evaluate risk/control factors)4. Coordinate audit engagement efforts witha. External auditorb. Regulatory oversight bodies5. Establish/refine engagement objectives and identify/finalize the scope of engagement6. Identify or develop criteria for assurance engagements (criteria against which to audit)7. Consider the potential for fraud when planning an engagementa. Be knowledgeable of the risk factors and red flags of fraudb. Identify common types of fraud associated with the engagement areac. Determine if risk of fraud requires special consideration whenconducting an engagement8. Determine engagement procedures9. Determine the level of staff and resources needed for the engagement10. Establish adequate planning and supervision of the engagement11. Prepare engagement work programPart 2 - Conducting the Internal Audit EngagementA. Conduct Engagements (25-35%) (P)1. Research and apply appropriate standards:a. IIA Professional Practices Framework (Code of Ethics, Standards,Practice Advisories)b. Other professional, legal, and regulatory standards2. Maintain an awareness of the potential for fraud when conducting an engagementa. Notice indicators or symptoms of fraudb. Design appropriate engagement steps to address significant riskof fraudc. Employ audit tests to detect fraudd. Determine if any suspected fraud merits investigation3. Collect data4. Evaluate the relevance, sufficiency, and competence of evidence5. Analyze and interpret data6. Develop work papers7. Review work papers8. Communicate interim progress9. Draw conclusions10. Develop recommendations when appropriate11. Report engagement resultsa. Conduct exit conferenceb. Prepare report or other communicationc. Approve engagement reportd. Determine distribution of reporte. Obtain management response to report12. Conduct client satisfaction survey13. Complete performance appraisals of engagement staffB. Conduct Specific Engagements (25-35%) (P)1. Conduct assurance engagementsa. Fraud investigation1) Determine appropriate parties to be involved with investigation2) Establish facts and extent of fraud (e.g., interviews, interrogationsand data analysis)3) Report outcomes to appropriate parties4) Complete a process review to improve controls to prevent fraudand recommend changesb. Risk and control self-assessment1) Facilitated approach(a) Client-facilitated(b) Audit-facilitated2) Questionnaire approach3) Self-certification approachc. Audits of third parties and contract auditingd. Quality audit engagementse. Due diligence audit engagementsf. Security audit engagementsg. Privacy audit engagementsh. Performance (key performance indicators) audit engagementsi. Operational (efficiency and effectiveness) audit engagementsj. Financial audit engagementsk. Information technology (IT) audit engagements1) Operating systems(a) Mainframe(b) Workstations(c) Server2) Application development(a) Application authentication(b) Systems development methodology(c) Change control(d) End user computing3) Data and network communications/connections (e.g., LAN, VAN,and WAN)4) Voice communications5) System security (e.g., firewalls, access control)6) Contingency planning7) Databases8) Functional areas of IT operations (e.g., data center operations)9) Web infrastructure10) Software licensing11) Electronic funds transfer (EFT)/Electronic data interchange (EDI)12) e-Commerce13) Information protection (e.g., viruses, privacy)14) Encryption15) Enterprise-wide resource planning (ERP) software (e.g., SAP R/3)l. Compliance audit engagements2. Conduct consulting engagementsa. Internal control trainingb. Business process reviewc. Benchmarkingd. Information technology (IT) and systems developmente. Design of performance measurement systemsC. Monitor Engagement Outcomes (5-15%) (P)1. Determine appropriate follow-up activity by the internal audit activity2. Identify appropriate method to monitor engagement outcomes3. Conduct follow-up activity4. Communicate monitoring plan and resultsD. Fraud Knowledge Elements (5-15%)1. Discovery sampling (A)2. Interrogation techniques (A)3. Forensic auditing (A)4. Use of computers in analyzing data (P)5. Red flag (P)6. Types of fraud (P)E. Engagement Tools (15-25%)1. Sampling (A)a. Nonstatistical (judgmental)b. Statistical2. Statistical analyses (process control techniques) (A)3. Data gathering tools (P)a. Interviewingb. Questionnairesc. Checklists4. Analytical review techniques (P)a. Ratio estimationb. Variance analysis (e.g., budget vs. actual)c. Other reasonableness tests5. Observation (P)6. Problem solving (P)7. Risk and control self-assessment (CSA) (A)8. Computerized audit tools and techniques (P)a. Embedded audit modulesb. Data extraction techniquesc. Generalized audit software (e.g., ACL, IDEA)d. Spreadsheet analysise. Automated work papers (e.g., Lotus Notes, Auditor Assistant)9. Process mapping including flowcharting (P)Part 3 - Business Analysis and Information TechnologyA. Business Processes (15-25%)1. Quality management (e.g., TQM) (A)2. The International Organization for Standardization (ISO) framework (A)3. Forecasting (A)4. Project management techniques (P)5. Business process analysis (e.g., workflow analysis and bottleneck management, theory of constraints) (P)6. Inventory management techniques and concepts (P)7. Marketing - pricing objectives and policies (A)8. Marketing - supply chain management (A)9. Human Resources (Individual performance management and measurement; supervision; environmental factors that affectperformance; facilitation techniques; personnel sourcing/staffing; training and development; safety) (P)10. Balanced scorecard (A)B. Financial Accounting and Finance (15-25%)1. Basic concepts and underlying principles of financial accounting (e.g., statements, terminology, relationships) (P)2. Intermediate concepts of financial accounting (e.g., bonds, leases, pensions, intangible assets, R&D) (A)3. Advanced concepts of financial accounting (e.g., consolidation, partnerships, foreign currency transactions) (A)4. Financial statement analysis (P)5. Cost of capital evaluation (A)6. Types of debt and equity (A)7. Financial instruments (e.g., derivatives) (A)8. Cash management (treasury functions) (A)9. Valuation models (A)a. Inventory valuationb. Business valuation10. Business development life cycles (A)C. Managerial Accounting (10-20%)1. Cost concepts (e.g., absorption, variable, fixed) (P)2. Capital budgeting (A)3. Operating budget (P)4. Transfer pricing (A)5. Cost-volume-profit analysis (A)6. Relevant cost (A)7. Costing systems (e.g., activity-based, standard) (A)8. Responsibility accounting (A)D. Regulatory, Legal, and Economics (5-15%) (A)1. Impact of government legislation and regulation on business2. Trade legislation and regulations3. Taxation schemes4. Contracts5. Nature and rules of legal evidence6. Key economic indicatorsE. Information Technology - IT (30-40%) (A)1. Control frameworks (e.g., COBIT)2. Data and network communications/connections (e.g., LAN, VAN, and WAN)3. Electronic funds transfer (EFT)4. e-Commerce5. Electronic data interchange (EDI)6. Functional areas of IT operations (e.g., data center operations)7. Encryption8. Information protection (e.g. viruses, privacy)9. Evaluate investment in IT (cost of ownership)10. Enterprise-wide resource planning (ERP) software (e.g., SAP R/3)11. Operating systems12. Application development13. Voice communications14. Contingency planning15. Systems security (e.g. firewalls, access control)16. Databases17. Software licensing18. Web infrastructureP=Candidates must exhibit proficiency (thorough understanding and ability to apply concepts) in these topic areas. A=Candidates must exhibit awareness (knowledge of terminology and fundamentals) in these topic areas.Part 4 - Business Management SkillsA. Strategic Management (20-30%) (A)1. Global analytical techniquesa. Structural analysis of industriesb. Competitive strategies (e.g., Porter's model)c. Competitive analysisd. Market signalse. Industry evolution2. Industry environmentsa. Competitive strategies related to:1) Fragmented industries2) Emerging industries3) Declining industriesb. Competition in global industries1) Sources/impediments2) Evolution of global markets3) Strategic alternatives4) Trends affecting competition3. Strategic decisionsa. Analysis of integration strategiesb. Capacity expansionc. Entry into new businesses4. Portfolio techniques of competitive analysis5. Product life cyclesB. Global Business Environments (15-25%) (A)1. Cultural/legal/political environmentsa. Balancing global requirements and local imperativesb. Global mindsets (personal characteristics/competencies)c. Sources and methods for managing complexities and contradictionsd. Managing multicultural teams2. Economic/financial environmentsa. Global, multinational, international, and multilocal compared and contrastedb. Requirements for entering the global market placec. Creating organizational adaptabilityd. Managing training and developmentC. Organizational Behavior (15-25%) (A)1. Motivationa. Relevance and implication of various theoriesb. Impact of job design, rewards, work schedules, etc.2. Communicationa. The processb. Organizational dynamicsc. Impact of computerization3. Performancea. Productivityb. Effectiveness4. Structurea. Centralized/decentralizedb. Departmentalizationc. New configurations (e.g., hourglass, cluster, network)D. Management Skills (20-30%) (A)1. Group dynamicsa. Traits (e.g., cohesiveness, roles, norms, groupthink)b. Stages of group developmentc. Organizational politicsd. Criteria and determinants of effectiveness2. Team buildinga. Methods used in team buildingb. Assessing team performance3. Leadership skillsa. Theories compared and contrastedb. Leadership grid (topology of leadership styles)c. Mentoring4. Personal time managementE. Negotiating (5-15%) (A)1. Conflict resolutiona. Competitive/cooperativeb. Compromise, forcing, smoothing, etc.2. Added-value negotiatinga. Descriptionb. Specific stepsP=Candidates must exhibit proficiency (thorough understanding and ability to apply concepts) in these topic areas. A=Candidates must exhibit awareness (knowledge of terminology and fundamentals) in these topic areas.。

中审网CIA考试一期一练(习题及解题思路

2005年CIA考试第1期1、《标准》规定,能实现内部审计机构独立性的途径是A.人员配置和监督。

B.持续的专业发展和应有的职业审慎。

C.人际关系和沟通。

D.组织状况和客观性。

2、内部审计主管对公司道德守则和决策环境实施审计,以下对这一审计的范围或建议的描述不恰当的是:(本题正确答案可能不止一个)a.审阅公司道德守则并与其他公司的守则进行比较。

b.对公司雇员进行调查,询问一些有关公司决策的道德质量方面的问题。

c.实施一次不记名的“道德测试”,确认是否雇员知道什么是不道德的行为或自己是否曾有过不道德的行为。

d,对董事会进行调查,确定他们支持公司道德守则的程度。

3、审计委员会具有许多服务功能,其中有些有益于内部审计。

那么审计委员会给内部审计师带来的最大益处是a.保护内部审计师的独立性免受管理层的不利影响。

b.审查年度审计计划并监督审计结果。

c.批准审计计划、日程表、人员配备以及必要时与内部审计师会面。

d.审查抽取到的公司经营活动的内部控制程序副本并与公司领导进行讨论。

4、根据准则规定,内部审计师在审计过程中应保持客观性。

假设某内部审计主管收到一笔年度奖金作为个人报酬的一部分,那么在什么情况下,这种奖金会损害审计主管的客观性?a.该奖金是由董事会或其所属的薪金管理委员会给予的。

b.该奖金是根据审计结果产生的美元补救金额或未来的节约额。

c.内部审计工作范围是审查内部控制而非帐户余额。

d.以上三项都选。

5、某政府机构希望了解向机动车颁发执照项目的执行情况,但其审计人员和人力资源都很短缺。

特别地,管理当局担心有可能●新执照申请被积压,●申请费的收取和处理方面的控制薄弱。

内部审计部门初步调查(Peliminary survey)以及有限的审计测试结果显示颁发执照程序运行正常,没有发现重大缺陷。

内部审计部门下一步应该:a.不再实施进一步审计工作,按调查结果发布正式审计报告并与管理当局讨论结果。

b.不再实施进一步审计工作,与管理当局及行政主管讨论有关问题并为以后审计工作编制方案,使得下一次不需再进行调查。

2014年国际注册内部审计师CIA考试科目考试大纲(Part 1 )

2014年国际注册内部审计师CIA考试科目考试大纲(Part 1 )Part 1 – Internal Audit Basics 内部审计基础知识I。

Mandatory Guidance (35-45%)强制性指南(35-45%)A. Definition of Internal Auditing内部审计定义1. Define purpose,authority, and responsibility of the internal audit activity明确内部审计的宗旨,权力和职责B。

Code of Ethics职业道德规范1. Abide by and promote compliance with The IIA Code of Ethics遵守和促进对国际内部审计师协会(IIA)《职业道德规范》的遵循C. International Standards国际标准1. Comply with The IIA's Attribute Standards遵守国际内部审计师协会的属性标准a。

Determine if the purpose, authority,and responsibility of the internal audit activity are documented in audit charter,approved by the Board and communicated to the engagement clients确定内部审计的宗旨、权力和职责是否在审计章程中加以说明,获得董事会批准并通报审计业务客户b。

Demonstrate an understanding of the purpose,authority, and responsibility of the internal audit activity阐明内部审计的宗旨、权力和职责2。

Maintain independence and objectivity保持独立性和客观性a。

2019ap美国历史知识点

2019ap美国历史知识点2019年AP美国历史考试涵盖了从大约公元1491年至今的美国历史。

以下是一些重要的知识点,它们可能在考试中出现:1. 早期接触与殖民时期(1491-1700):- 欧洲探险家对美洲的探索,如哥伦布的发现。

- 早期的殖民地建立,如詹姆斯敦和普利茅斯。

- 原住民与欧洲殖民者之间的互动,包括贸易和冲突。

2. 早期共和国(1700-1754):- 英国在北美的13个殖民地的建立。

- 法国与印第安战争的影响。

- 殖民地的社会结构和经济发展。

3. 帝国与独立(1754-1800):- 法国与印第安战争及其对美国独立的影响。

- 美国独立战争的起因、过程和结果。

- 美国宪法的制定和早期政府的建立。

4. 国家扩张与改革(1800-1848):- 路易斯安那购地和西部扩张。

- 工业革命对美国社会和经济的影响。

- 杰克逊时代的政治和经济改革。

5. 分裂、内战与重建(1844-1877):- 奴隶制争议和领土扩张。

- 美国内战的原因、过程和结果。

- 重建时期的政策和挑战。

6. 工业化与移民(1865-1898):- 工业化进程中的经济和社会变革。

- 大规模的欧洲移民及其对美国的影响。

- 美国对外扩张政策,如美西战争。

7. 进步时代与第一次世界大战(1890-1920):- 进步时代的社会和政治改革。

- 美国在第一次世界大战中的角色和影响。

8. 1920年代的繁荣与大萧条(1920-1939):- 1920年代的经济繁荣和文化变革。

- 大萧条的原因、影响和新政。

9. 第二次世界大战与冷战(1930-1960):- 第二次世界大战的原因、过程和结果。

- 冷战时期的政治、经济和军事对抗。

10. 民权运动与越南战争(1954-1980):- 民权运动的兴起和重要事件。

- 越南战争的原因、过程和影响。

11. 当代美国(1980至今):- 经济全球化和技术革命的影响。

- 政治和社会的变迁,包括恐怖主义、移民问题和环境问题。

2005年CIA考试大纲(四个部分)

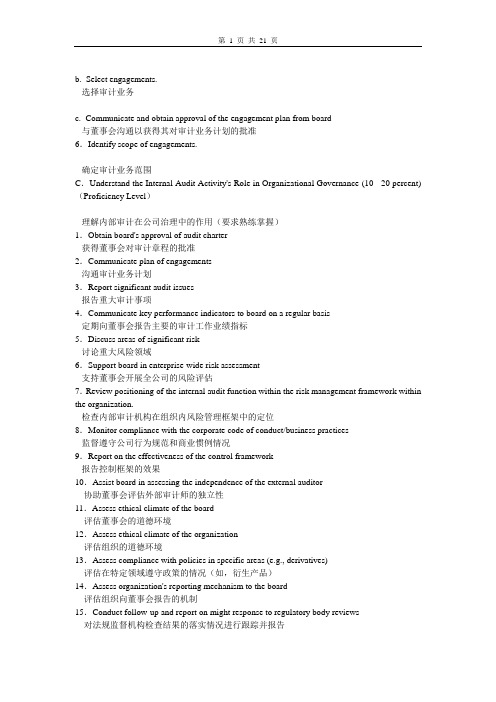

b. Select engagements.选择审计业务c. Communicate and obtain approval of the engagement plan from board与董事会沟通以获得其对审计业务计划的批准6.Identify scope of engagements.确定审计业务范围C.Understand the Internal Audit Activity's Role in Organizational Governance (10 - 20 percent) (Proficiency Level)理解内部审计在公司治理中的作用(要求熟练掌握)1.Obtain board's approval of audit charter获得董事会对审计章程的批准2.Communicate plan of engagements沟通审计业务计划3.Report significant audit issues报告重大审计事项4.Communicate key performance indicators to board on a regular basis定期向董事会报告主要的审计工作业绩指标5.Discuss areas of significant risk讨论重大风险领域6.Support board in enterprise-wide risk assessment支持董事会开展全公司的风险评估7.Review positioning of the internal audit function within the risk management framework within the organization.检查内部审计机构在组织内风险管理框架中的定位8.Monitor compliance with the corporate code of conduct/business practices监督遵守公司行为规范和商业惯例情况9.Report on the effectiveness of the control framework报告控制框架的效果10.Assist board in assessing the independence of the external auditor协助董事会评估外部审计师的独立性11.Assess ethical climate of the board评估董事会的道德环境12.Assess ethical climate of the organization评估组织的道德环境13.Assess compliance with policies in specific areas (e.g., derivatives)评估在特定领域遵守政策的情况(如,衍生产品)14.Assess organization's reporting mechanism to the board评估组织向董事会报告的机制15.Conduct follow-up and report on might response to regulatory body reviews对法规监督机构检查结果的落实情况进行跟踪并报告16.Conduct follow-up and report on might response to external audit对外部审计的结果进行跟踪并报告17.Assess the adequacy of the performance measurement system, achievement of corporate objective评估业绩测评系统的充分性和整体目标的实现情况18.Support a culture of fraud awareness and encourage the reporting of improprieties树立舞弊防范意识,鼓励报告不正当的行为D.Perform Other Internal Audit Roles and Responsibilities (0 - 10 percent) (Proficiency Level)执行其他内部审计任务和职责(0-10%)(要求熟练掌握)1.Ethics/compliance道德规范/合规情况a. Investigate and recommend resolution for ethics/compliance complaints对道德规范/合规情况的投诉进行调查并提出解决办法b. Determine disposition of ethics violations确定违反道德规范的处理c. Foster healthy ethical climate培养健康的道德氛围d. Maintain and administer business conduct policy (e.g., conflict of interest)维护和管理业务行为政策(如,利益冲突)e. Report on compliance报告合规情况2.Risk management风险管理a. Develop and implement an organization-wide risk and control framework建立和实施一个全组织的风险和控制框架b. Coordinate enterprise-wide risk assessment协调全公司的风险评估c. Report corporate risk assessment to broad向董事会报告公司的风险评估d. Review business continuity planning process检查经营持续性计划过程3.Privacy保密a. Determine privacy vulnerabilities确定保密的薄弱环节b. Report on compliance报告合规情况4.Information or physical security信息或物理安全a. Determine security vulnerabilities确定安全的薄弱环节b. Determine disposition of security violations确定对违反安全行为的处理c. Report on compliance报告合规情况E.Governance, Risk, and Control Knowledge Elements (15 - 25 percent)治理,风险,和控制知识要点(15-25%)1.Alternative models for corporate governance(Awareness Level)可选择的公司治理模型(要求了解)2.Alternative control frameworks(Awareness Level)可选择的控制框架(要求了解)3.Risk vocabulary and concepts(Proficiency Level)风险的词汇和概念(要求熟练掌握)4.Risk management techniques(Proficiency Level)风险管理技术(要求熟练掌握)5.Risk/control implications of different organizational structures(Proficiency Level)不同组织结构中的风险/控制内容(要求熟练掌握)6.Risk/control implications of different leadership styles(Awareness Level)不同领导风格下的风险/控制内容7.Change management(Awareness Level)变革管理8.Conflict management(Awareness Level)冲突管理9.Management control techniques(Proficiency Level)管理控制技术10.Types of control (preventive, detective, input, output) (Proficiency Level)控制类型(预防型、检查型、输入、输出)F.Plan Engagements (15 - 25 percent) (Proficiency Level)策划审计业务(15-25%)1.Initiate preliminary communication with engagement client开展与审计业务客户的初步沟通2.Conduct a preliminary survey of the area of engagement对审计业务范围实施初步调查a. Obtain input from engagement client从审计业务客户处获得信息b. Perform analytical reviews进行分析性复核c. Perform benchmarking进行基准比较d. Conduct interviews实施面谈e. Review prior audit reports and other relevant documentation查阅以前的审计报告和其他相关资料f. Map processes绘制流程图g. Develop Checklists编制检查清单3.Complete a detailed risk assessment of the area (prioritize or evaluate risk/control factors) 完成相关领域的详细风险评估(对风险/控制因素进行排序或评估)4.Coordinate audit engagement efforts with与以下方面协调审计业务工作:a. External auditor外部审计师b. Regulatory oversight bodies法规监督机构5.Establish/refine engagement objectives and finalize the scope of engagement.建立/完善审计业务的目标,确定审计业务的范围6.Identify or develop criteria for assurance engagements (criteria against which to audit)确认或开发保证业务的标准(审计所依照的标准)7.Consider the potential for fraud when planning an engagement在策划审计业务时考虑舞弊的潜在可能a. Be knowledgeable of the risk factors and red flags of fraud理解舞弊的风险因素和危险信号b. Identify common types of fraud associated with the engagement area.确认与审计业务范围相关的一般舞弊类型c. Determine if risk of fraud requires special consideration when conducting an engagement在实施审计业务时确定是否需要对舞弊的风险进行特殊考虑8.Determine engagement procedures.确定审计业务步骤9.Determine the level of staff and resources needed for the engagement确定审计业务所需的人员水平和资源10.Establish adequate planning and supervision of the engagement.建立对审计业务充分的计划和监督11.Prepare engagement work program.编制审计业务工作方案Part II - Conducting the Internal Audit Engagement第二部分–实施内部审计业务A. Conduct Engagements (25 - 35 percent) (Proficiency Level)实施审计业务(25 – 35%) (要求熟练掌握)1. Research and apply appropriate standards:研究和采用适当的标准:a. IIA Professional Practices Framework (e.g., Code of Ethics, Standards, Practice Advisories) IIA 职业实务框架(如,《道德规范》、《标准》、《实务公告》);b. Other professional., legal, and regulatory standards其他职业的、法律的和法规的标准;2. Maintain awareness of potential for fraud when conducting an engagement在实施审计业务时,要保持防范潜在舞弊的意识:a. Notice indicators or symptoms of fraud注意舞弊的迹象和征兆;b. Design appropriate engagement steps to address significant risk of fraud设计适当的审计业务步骤以应对重大的舞弊风险;c. Employ audit tests to detect fraud采用审计测试以发现舞弊;d. Determine if any suspected fraud merits investigation确定是否应对任何可疑的舞弊进行调查3. Collect data.收集数据。

国际法条约和其他法律渊源对於使用武力设立了很多限制

Article 51 of UN Charter allows self-defense if armed attack occurs 聯合國憲章第51條容許在面對武裝攻擊時自衛

15

Still unclear, however: 但是依然含糊不清:

In Renaissance, thinkers urged that negotiations precede resort to force 在文藝復興時期,思想家要求訴諸武力之前要進行談判

Vitoria argued that not every wrong is sufficient cause for war 維多利亞認為並不是每個錯誤都是發動戰爭的充分原因

1

Suarez held that wronged state must first demand reparatations Suarez說受e immune from attack 無辜者應該免受攻擊

Only proportionate force should be used 只可酌量使用武力

States were supposed to refrain from war for three months after arbitration, settlement or report 國家在仲裁、司法或調查報告之後三個月内應當克制戰爭

1928 General Treaty for the Renunciation of War (Kellogg-Briand Pact) 1928年《非戰公約》(《白裏安--凱洛哥公約》)

In Nalilaa Incident Arbitration (1928), German forces in Africa raided Portugese colony of Angola in retaliation for mistaken killing of Germans there. Portugal demanded compensation. 在Nalilaa事件仲裁案中(1928),為報復德人被誤殺,德國在 非洲的軍隊侵略在安高拉的葡國殖民地。葡國要求賠償

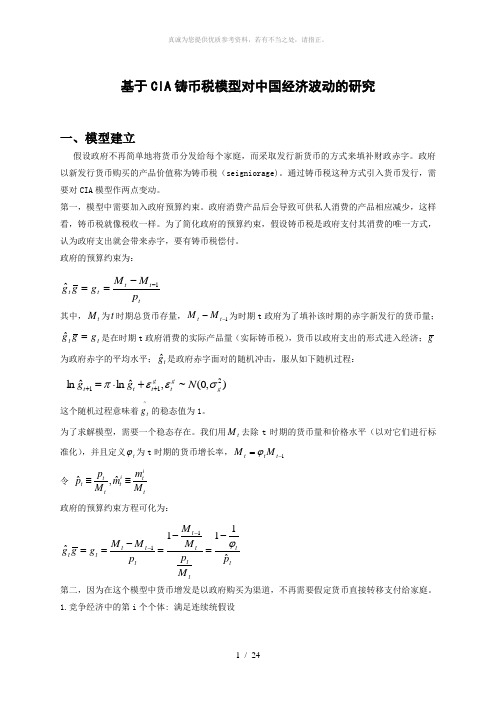

大作业CIA铸币税

基于CIA 铸币税模型对中国经济波动的研究一、模型建立假设政府不再简单地将货币分发给每个家庭,而采取发行新货币的方式来填补财政赤字。

政府以新发行货币购买的产品价值称为铸币税(seigniorage)。

通过铸币税这种方式引入货币发行,需要对CIA 模型作两点变动。

第一,模型中需要加入政府预算约束。

政府消费产品后会导致可供私人消费的产品相应减少,这样看,铸币税就像税收一样。

为了简化政府的预算约束,假设铸币税是政府支付其消费的唯一方式,认为政府支出就会带来赤字,要有铸币税偿付。

政府的预算约束为:tt t t t p M M g g g1ˆ--==其中,t M 为t 时期总货币存量,1--t t M M 为时期t 政府为了填补该时期的赤字新发行的货币量;t t g g g =ˆ是在时期t 政府消费的实际产品量(实际铸币税),货币以政府支出的形式进入经济;g为政府赤字的平均水平;t gˆ是政府赤字面对的随机冲击,服从如下随机过程: ),0(~,ˆln ˆln 211g g t g t t t N g gσεεπ+++⋅= 这个随机过程意味着^t g 的稳态值为1。

为了求解模型,需要一个稳态存在。

我们用t M 去除t 时期的货币量和价格水平(以对它们进行标准化),并且定义t ϕ为t 时期的货币增长率,1-=t t t M M ϕ令 ti t it t t t M m mM p p ≡≡ˆ,ˆ 政府的预算约束方程可化为:t ttt t t tt t t t p M p M M p M M g g gˆ111ˆ11ϕ-=-=-==-- 第二,因为在这个模型中货币增发是以政府购买为渠道,不再需要假定货币直接转移支付给家庭。

1.竞争经济中的第i 个个体: 满足连续统假设2.约束条件(1)、个体约束条件①.购买消费品要受到已有现金约束(CIA ):左右两边同除以t M1111----==⋅t t i t t i t t i t t M m M m M c p ϕ ,11011---==⎰t i t t m di m M令 ti t it t t t M m mM p p ≡≡ˆ,ˆ 。

第二章历史(提纲)

Part 3 The Consequences of the War 第三部分 战争的后果

gave birth to the first republic in the world. 促使世界上第一个共和国的诞生。

2.6 civil war 2.6 内战

That is the civil war start the civil war is the central in america's historical consciousness.

2-3The British Empire 大英帝国

Part 1 Origin 第1部分 起源

Part 2 "First" Bablishment of private companies to administer colonies and overseas trade Part 3 Rise of the "Second" British Empire

established himself as the Supreme Head of the Church of England亨利八世帮助英国国教从教皇权 威中分离出来,并确立了自己作为英国国教最高领袖的地位。 Queen Elizabeth keeping England in the ascendant through wars, and political and religious turmoil. perhaps England's most famous monarch伊丽莎白女王一世使英国在战争、政治和宗教动荡中 保持了优势也许是英国最著名的君主 William the Conqueror: the king who contributed the most on the English language.征服者威廉:对 英语贡献最大的国王

CIA考试精选题库----第三部分

CIA考试精选题库--------第三部分(经营分析与信息技术 )1某制造公司有几个相互独立的分公司,这些分公司不但与外部竞争,而且相互之间也展开竞争。

公司总裁希望各分公司经理努力使公司和其分公司的绩效达到最大。

在这种情况下,若进行部交易,交易价格为:A.全部生产成本。

B.全部生产成本+加成。

C.变动成本+加成。

D.产品的市场价格。

2某企业在X国和Y国都设有销售分公司。

该企业只销售一种产品,该产品的单位生产成本是$20。

上述三个国家之间不存在贸易壁垒或关税。

有关这三个国家的具体信息如下:国家企业所得税税前售价销售量其他成本本国 50% $30 1,500 $10,000X 国 60% $40 1,000 $12,500Y 国 40% $35 2,000 $11,000当该企业向(A列)销售分公司销售产品时,定价应该是(B列)的转移价格,才可以合法减免税款。

A.(A列)X和Y国(B列)最高。

B.(A列)X和Y国(B列)最低。

C.(A列)X国(B 列)最高。

D.(A列)Y国(B列)最高。

3质量控制小组现在已经被全世界所运用。

典型的质量控制小组是由5到10人组成的一个定期会面的小组。

质量控制小组的主要目是:A.改进组织中的领导质量。

B.发掘所有员工的创造性解决问题的潜能。

C.通过提供一个正式的沟通渠道,改善员工与管理层之间的沟通。

D.允许产生一个采取进一步的指挥行动的团队领导。

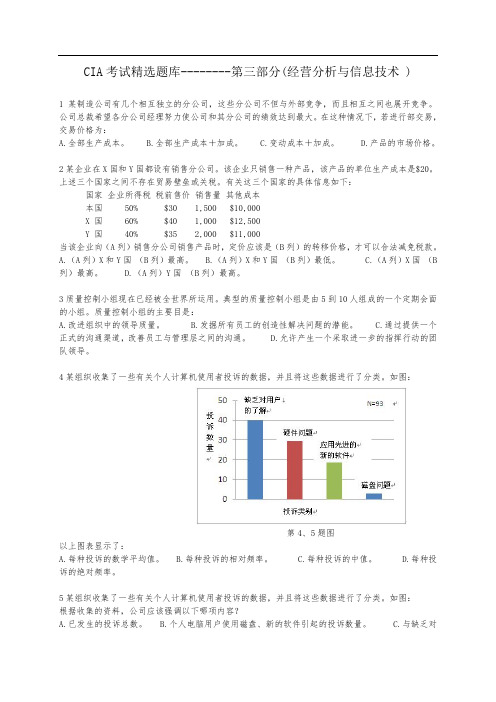

4某组织收集了一些有关个人计算机使用者投诉的数据,并且将这些数据进行了分类。

如图:第4、5题图以上图表显示了:A.每种投诉的数学平均值。

B.每种投诉的相对频率。

C.每种投诉的中值。

D.每种投诉的绝对频率。

5某组织收集了一些有关个人计算机使用者投诉的数据,并且将这些数据进行了分类。

如图:根据收集的资料,公司应该强调以下哪项内容?A.已发生的投诉总数。

B.个人电脑用户使用磁盘、新的软件引起的投诉数量。

C.与缺乏对用户的了解和硬件问题而发生的计算机投诉数量。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1STUDY UNIT TWOOBJECTIVITYCHARTER,INDEPENDENCE,ANDThe purpose,authority,and responsibility of internal auditing should be adequate to enable the internal audit activity to accomplish its objectives.For that reason,the purpose,authority,and responsibility should be stated in a written charter and periodically reassessed.Internal auditing is an independent,objective assurance and consulting activity designed to add value and improve an organization’s operations.Accordingly,the Standards require the internal audit activity to be independent and the internal auditors to be objective in performing their work.Thus, independence is an attribute of an organizational unit,and objectivity is an attribute of individuals.In this context,independence means that internal auditors can carry out their duties freely and objectively.Objectivity means independence in mental attitude.Core Conceptss The purpose,authority,and responsibility of the internal audit activity should be defined in a formal charter.s The nature of assurance and consulting services should be defined in the charter.s The internal audit activity should be independent,and the internal auditor should be objective.s The chief audit executive should report functionally to the audit committee.s Impairment of independence or objectivity should be disclosed.s Internal auditors should not assess operations for which they were previously responsible.2.1CHARTER1.This subunit concerns the content of the charter of the internal audit activity.One GeneralAttribute Standard,an Assurance Implementation Standard,a Consulting ImplementationStandard,and four Practice Advisories currently address this topic.2.1000Purpose,Authority,and Responsibility–The purpose,authority,andresponsibility of the internal audit activity should be formally defined in a charter,consistent with the Standards,and approved by the board.**The term“board”here and elsewhere in pronouncements of The IIA includes“anorganization’s governing body,such as a board of directors,supervisory board,head of an agency or legislative body,board of governors or trustees of a non-profit organization,or any other designated body of the organization,includingthe audit committee,to whom the chief audit executive may functionally report”(Glossary).2SU2:Charter,Independence,and Objectivitya.PRACTICE ADVISORY1000-1:INTERNAL AUDIT CHARTER1.The purpose,authority,and responsibility of the internal audit activity should bedefined in a charter.The chief audit executive should seek approval of thecharter by senior management as well as acceptance by the board,auditcommittee,or appropriate governing authority.The charter should(a)establishthe internal audit activity’s position within the organization;(b)authorizeaccess to records,personnel,and physical properties relevant to theperformance of engagements;and(c)define the scope of internal auditactivities.2.The internal audit activity’s charter should be in writing.A written statementprovides formal communication for review and approval by management and foracceptance by the board.It also facilitates a periodic assessment of theadequacy of the internal audit activity’s purpose,authority,and responsibility.Providing a formal,written document containing the charter of the internal auditactivity is critical in managing the auditing function within the organization.The purpose,authority,and responsibility should be defined and communicatedto establish the role of the internal audit activity and to provide a basis formanagement and the board to use in evaluating the operations of the function.If a question should arise,the charter also provides a formal,written agreementwith management and the board about the role and responsibilities of theinternal audit activity within the organization.3.The chief audit executive should periodically assess whether the purpose,authority,and responsibility,as defined in the charter,continue to be adequateto enable the internal audit activity to accomplish its objectives.The result ofthis periodic assessment should be communicated to senior management andboard.the3.1000.A1–The nature of assurance services provided to the organization should be definedin the audit charter.If assurances are to be provided to parties outside the organization,the nature of these assurances should also be defined in the charter.4.1000.C1–The nature of consulting services should be defined in the audit charter.a.PRACTICE ADVISORY1000.C1-1:PRINCIPLES GUIDING THE PERFORMANCEOF CONSULTING ACTIVITIES OF INTERNAL AUDITORS1.Value Proposition–The value proposition of the internal audit activity isrealized within every organization that employs internal auditors in a mannerthat suits the culture and resources of that organization.That value propositionis captured in the definition of internal auditing and includes assurance andconsulting activities designed to add value to the organization by bringing asystematic,disciplined approach to the areas of governance,risk,and control.SU2:Charter,Independence,and Objectivity32.Consistency with Internal Audit Definition–A disciplined,systematicevaluation methodology is incorporated in each internal audit activity.The list ofservices can generally be incorporated into the broad categories of assuranceand consulting.However,the services may also include evolving forms ofvalue-adding services that are consistent with the broad definition of internalauditing.3.Audit Activities Beyond Assurance and Consulting–There are multipleinternal auditing services.Assurance and consulting are not mutually exclusiveand do not preclude other auditing services,such as investigations andnonauditing roles.Many audit services will have both an assurance andconsultative(advising)role.4.Interrelationship between Assurance and Consulting–Internal auditconsulting enriches value-adding internal auditing.While consulting is often thedirect result of assurance services,it should also be recognized that assurancecould also be generated from consulting engagements.5.Empower Consulting Through the Internal Audit Charter–Internal auditorshave traditionally performed many types of consulting services,including theanalysis of controls built into developing systems,analysis of security products,serving on task forces to analyze operations and make recommendations,andso forth.The board(or audit committee)should empower the internal auditactivity to perform additional services if they do not represent a conflict ofinterest or detract from its obligations to the committee.That empowermentshould be reflected in the internal audit charter.6.Objectivity–Consulting services may enhance the auditor’s understanding ofbusiness processes or issues related to an assurance engagement and donot necessarily impair the auditor’s or the internal audit activity’s objectivity.Internal auditing is not a management decision-making function.Decisions toadopt or implement recommendations made as a result of an internal auditingadvisory service should be made by management.Therefore,internal auditingobjectivity should not be impaired by the decisions made by management.7.Internal Audit Foundation for Consulting Services–Much of consulting is anatural extension of assurance and investigative services and may representinformal or formal advice,analysis,or assessments.The internal audit activityis uniquely positioned to perform this type of consulting work based on(a)itsadherence to the highest standards of objectivity and(b)its breadth ofknowledge about organizational processes,risk,and strategies.munication of Fundamental Information–A primary internal auditingvalue is to provide assurance to senior management and audit committeedirectors.Consulting engagements cannot be performed in a manner thatmasks information that in the judgment of the chief audit executive(CAE)shouldbe presented to senior executives and board members.All consulting is to beunderstood in that context.9.Principles of Consulting Understood by the Organization–Organizationsmust have ground rules for the performance of consulting services that areunderstood by all members of an organization,and these rules should becodified in the audit charter approved by the audit committee and promulgatedin the organization.10.Formal Consulting Engagements –Management often engages outsideconsultants for formal consulting engagements that last a significant period oftime.However,an organization may find that the internal audit activity isuniquely qualified for some formal consulting tasks.If an internal audit activityundertakes to perform a formal consulting engagement,the internal audit groupshould bring a systematic,disciplined approach to the conduct of theengagement.11.CAE Responsibilities –Consulting services permit the CAE to enter intodialogue with management to address specific managerial issues.In thisdialogue,the breadth of the engagement and time frames are made responsiveto management needs.However,the CAE retains the prerogative of settingthe audit techniques and the right of reporting to senior executives and auditcommittee members when the nature and materiality of results pose significantrisks to the organization.12.Criteria for Resolving Conflicts or Evolving Issues –An internal auditor isfirst and foremost an internal auditor.Thus,in the performance of all services,the internal auditor is guided by The IIA Code of Ethics and the Attribute andPerformance Standards of the International Standards for the ProfessionalPractice of Internal Auditing.The resolution of any unforeseen conflicts oractivities should be consistent with the Code of Ethics andStandards.4SU 2:Charter,Independence,and ObjectivitySU2:Charter,Independence,and Objectivity5b.PRACTICE ADVISORY1000.C1-2:ADDITIONAL CONSIDERATIONS FORFORMAL CONSULTING ENGAGEMENTSThe following is the portion of this comprehensive Practice Advisory relevant toStandard1000.C1:Definition of Consulting Services1.The Glossary in the Standards defines“consulting services”as follows:“Advisory and related client service activities,the nature and scope of which areagreed with the client and which are intended to add value and improve anorganization’s governance,risk management,and control processes without theinternal auditor assuming management responsibility.Examples includecounsel,advice,facilitation,and training.”2.The chief audit executive should determine the methodology to use forclassifying engagements within the organization.In some circumstances,itmay be appropriate to conduct a“blended”engagement that incorporateselements of both consulting and assurance activities into one consolidatedapproach.In other cases,it may be appropriate to distinguish between theassurance and consulting components of the engagement.3.Internal auditors may conduct consulting services as part of their normal orroutine activities as well as in response to requests by management.Eachorganization should consider the type of consulting activities to be offered anddetermine if specific policies or procedures should be developed for each typeof activity.Possible categories could include:q Formal consulting engagements–planned and subject to writtenagreement.q Informal consulting engagements–routine activities,such asparticipation on standing committees,limited-life projects,ad-hocmeetings,and routine information exchange.q Special consulting engagements–participation on a merger andacquisition team or system conversion team.q Emergency consulting engagements–participation on a teamestablished for recovery or maintenance of operations after a disaster orother extraordinary business event or a team assembled to supplytemporary help to meet a special request or unusual deadline.4.Auditors generally should not agree to conduct a consulting engagement simplyto circumvent,or to allow others to circumvent,requirements that wouldnormally apply to an assurance engagement if the service in question is moreappropriately conducted as an assurance engagement.This does not precludeadjusting methodologies if services once conducted as assurance engagementsare deemed more suitable to being performed as a consulting engagement.6SU2:Charter,Independence,and Objectivityc.PRACTICE ADVISORY1000.C1-3:ADDITIONAL CONSIDERATIONS FORCONSULTING ENGAGEMENTS IN GOVERNMENT ORGANIZATIONALSETTINGS1.This Practice Advisory provides guidance for government audit organizationsconducting work in compliance with IIA Standards,but whose local governancerules,audit standards,policies,or legislation more strictly limit non-assurance(consulting)services.The parameters within which an organization plans toprovide non-assurance(consulting)services should be included in the internalaudit charter.They should be supported by the policies and procedures of theinternal audit activity.The guidance in this PA may assist organizations indeveloping relevant language and policies to manage the provision ofnon-assurance(consulting)services.2.Core Elements of the Role of Auditors.Through their assurance(audit)engagements,auditors help to ensure that management is accountable formeeting organizational objectives and complying with internal and externalrequirements for how operations and activities are carried out.Although theseengagements can include an“assistance”dimension through the inclusion ofrecommendations for improvement,the auditor does not bear ultimateresponsibility for making or authorizing the improvement.Should an auditortake responsibility for implementing or authorizing operationalimprovements,whether recommended in the course of an audit(assurance)engagement,or as a separate non-audit(consulting)engagement,the auditor isvery likely jeopardizing the independence and objectivity that are essential tothe role of audit.SU2:Charter,Independence,and Objectivity7 Even when assisting an organization through non-audit(consulting)activities,auditors should keep their activities within boundaries that define the coreelements of the audit function.These core elements include:q Auditors should be independent.They should avoid relationships andsituations that compromise their objectivity.q Auditors should not audit their own work.q Auditors should not perform management functions or makemanagement decisions.1The elements are“core”because they support the fundamental valueproposition of audit,namely,the principle that an objective third party isattesting to(or providing assurance to)the credibility of management’sassertions.Accordingly,to protect their ability to provide assurance,auditorsmust minimize potential threats to auditor independence that can arise when thesame audit function is also providing non-audit(consulting)services.In addition to the core elements above,other threats to auditor independencehave been identified,including the conduct of non-audit(consulting)work thatq Creates a mutuality of interest;or2q Places auditors in the role of advocate for the company.erning Rules.Specific jurisdictional rules that set restrictions on the workof auditors outside the audit(assurance)role may apply only to auditorsconducting the external(financial statement or statutory)audit,or they mayapply to auditors performing all types of audits.Moreover,the rules may havebeen established in the audit function’s enabling legislation,imposed byoversight or regulatory bodies,or included in codes of ethics or auditingstandards required for audits of specific organizations or jurisdictions.3It is theChief Audit Executive’s responsibility to ensure that the audit function’s charterand its policies and procedures comply with relevant governing rules.Moreover,even where the audit function is not subject to governing rules thatrestrict non-audit(consulting)services,CAEs will nevertheless need to ensurethat the quality assurance system is designed to manage or minimize threatsto auditor independence or objectivity.Otherwise,non-audit(consulting)assignments could have the long-term effect of compromising the auditfunction’s ability to carry out its audit(assurance)role.In addition,an auditfunction’s engagement in non-audit(consulting)work that compromises itsindependence could prevent other auditors from relying on the audit function’swork.1This principle has been articulated by numerous standard-setting bodies,including guidance publishedby IAASB/IFAC in its Code of Professional Ethics and the ernment Accountability Office in itsGenerally Accepted Government Auditing Standards.2This risk is raised in the January2003Smith Report on Audit Committees and Combined CodeGuidance,appointed by the Financial Reporting Council,and is addressed in guidance published byICAEW(Institute of Chartered Accountants in England and Wales),among others.3Examples of specific restrictions include U.K.’s Government Internal Audit Standard2.4.2,whichstates:“Objectivity is presumed to be impaired when individual auditors review any activity in which theyhave previously had executive responsibility,or in which they have provided consultancy advice.”Thisstandard is supplemented by Good Practice Guidance on Consultancy,which states:“In this role it isimportant that the internal auditor offers advice to management and does not undertake the task onbehalf of,or as a substitute for,management.Acceptance by management of the advice offered by theinternal auditor does not transfer or reduce management’s accountability for their own areas ofresponsibility.”(3.5.3)8SU2:Charter,Independence,and Objectivity4.Activities that Compromise Objectivity or Independence.Auditors’ability toengage in non-audit(consulting)work without compromising their independencedepends to some extent on where they“draw the line”between assisting orconsulting in the sense of advising,versus assisting by doing work that is theresponsibility of management.For example,providing advice on appropriatecontrols during system design with the clear understanding that managementhas responsibility for accepting or rejecting the advice would have a limitedimpact on the auditor’s objectivity toward that system in the future.By contrast,if the auditor led the system design team,decided which controls to select,oroversaw the implementation of the recommended controls,the auditor’s futureability to objectively evaluate that system would be significantly impaired.However,other non-audit assignments may not be as clear-cut.Accordingly,audit functions need to develop procedures for reviewing potential non-audit(consulting)assignments and determining whether they present a threat toindependence or objectivity.The review used to determine the effect onfuture independence and objectivity should be documented.Thisdocumentation should be provided to external quality control reviewers duringthe QAR engagement.5.Processes for Minimizing Threats to Objectivity or Independence.Theaudit function should implement controls that assist in reducing the potentialfor non-audit(consulting)projects to compromise objectivity of individualauditors,or the independence of the audit function as a whole.Techniques mayinclude:a.Charter language defining non-audit(consulting)service parameters.b.Policies and procedures limiting type,nature,or level of participation innon-audit(consulting)projects.e of a screening process for non-audit(consulting)projects,with limitson accepting engagements that might threaten objectivity.d.Segregation of non-audit(consulting)units from units conducting audits(assurance engagements)within the same audit function.e.Rotation of auditors on engagements.f.Employing outside providers for carrying out non-audit(consulting)engagements,or for conducting assurance engagements in activitieswhere the audit function’s prior involvement in non-audit(consulting)workhas been determined to impair objectivity/independence.g.Disclosure in audit reports where objectivity was impaired by participationin a prior non-audit(consulting)project.Attachment A provides examples of relevant language for some of these typesof control techniques.SU2:Charter,Independence,and Objectivity9Attachment AExample Language for Control Techniques Minimizing Threats to Auditor IndependenceCharter language defining non-audit(consulting)service parameters.Charter language will establish the boundaries within which the audit function will operate but is not expected to detail the specific services that would or would not be provided.Accordingly,if a baseline for independence has been described elsewhere in the Charter document,or is included in specifically applicable auditing standards that are referenced;the Charter may need only to include a reference to those other requirements to set parameters for services to be provided.Three examples below show language used in two cases where non-audit(consulting)services are limited to those where independence or objectivity should not be compromised,and for a case where the audit function may be called upon to do work that is normally management’s responsibility.s Where the audit function will be limiting non-audit(consulting)services to those that do not compromise objectivity or independence:“The auditor may also assist the mayor,the City Council,and management staff in carrying out their responsibilities by providing them with objective and timely information on the conduct of city operations or advising on appropriate management controls,in accordance with[title ofapplicable]Auditing Standards.”“The internal audit department may perform other non-audit functions,consistent with otherprovisions of this Charter,and prepare and submit such other reports as may be assigned by the Commission.”s Where the audit function will be providing a full range of non-audit services,even if certain such services may threaten objectivity or independence for audit work:“The auditor may from time to time be called upon to participate in non-audit activities of theAgency,to assist the Executive Director and managers in carrying out their responsibilities,as authorized by the Audit Committee.”Policies and procedures limiting type,nature,and/or level of participation in non-audit (consulting)projects;or establishing controls that minimize future threats to objectivity or independence from participation in non-audit engagements.If auditors do perform management functions for the organization,the audit unit should establish relevant policies and procedures. Specifically,policies should prohibit those individuals from planning,conducting,or reviewing future audits of the subject matter involving the non-audit(consulting)service.Moreover,if the audit function performs a non-audit(consulting)engagement that will impair the entire audit function’s independence or objectivity,the audit function’s oversight entity(e.g.,the audit committee)should be notified before the engagement begins that audit independence will be impaired on any future audit work performed within the area.Should the audit function proceed to conduct an audit in the activity where the impairment exists,this impairment should be identified in the audit report.These prohibitions can be relaxed if there are significant changes to the subject matter area after the assistance work was performed or if the assistance work involved some established de minimums standard,such as“under40hours.”The example policy and procedure below describes non-audit(consulting)services,and includes language(see underlined text)that limits the services to within parameters that minimize threats to objectivity and independence of the auditors.Policy:In addition to audit services,the Auditor’s Office provides three other types of services to managers in the jurisdiction,or at the request of the Commission—Quality Assurance for projects in process,Consulting and Training,and Control Self Assessment facilitated workshops.10SU2:Charter,Independence,and ObjectivityParameters for each type of service are detailed below.Quality Assurance Services:In providing quality assurance services,the Office of City Auditor will monitor and assist ongoing projects by assessing if:q project objectives will be achieved and are reasonable;q all options have been identified and thoroughly analyzed;q quantitative and qualitative analyses are complete and accurate;q a project plan has been established and project staff are adhering to the plan;andq best practices used by other jurisdictions to accomplish project objectives might be adopted in the City.Consulting Services and Training:Audit staff is available to provide assistance and training to City staff in designing management accountability systems and re-engineering operations.Audit staff is advisory only andmanagement must accept responsibility for implementing any suggestions.Control Self Assessment Facilitated Workshops:In this audit process,an employee team meets with auditors to hold structured discussions on how to achieve its objectives in the most efficient and effective way.Action plans,rather than a formal audit report,are developed to address any obstacles to the objective(s).Employee team members are responsible for implementing action plan steps.The example procedures on the next page contain language that clarifies actions to be taken by the audit function when non-audit(consulting)engagements are accepted that threaten independence and objectivity on future assurance(audit)engagements:When the audit function is requested by the Audit Committee to conduct non-audit engagements that are determined by the CAE to impair the audit function’s independence or an individualauditor’s objectivity for conducting subsequent audit work,the following procedures will be carried out:1.Prior to commencing the non-audit engagement,the CAE will communicate in writing withthe Audit Committee that the requested engagement will impair independence or objectivity;describe the nature of the impairment;and indicate the consequences of the impairment forfuture audit engagements(e.g.,that the audit function must decline future audits in the area,or the Audit Committee will need to contract with a third-party provider to conduct futureaudits).The CAE should request a response in writing from the Audit Committee,directingthe audit function either to proceed with the non-audit engagement,or to decline it.2.If the Audit Committee directs the audit function to proceed with the non-audit engagement,the CAE will document the impairment in:q The non-audit engagement’s documentation,with a copy to management responsible for the non-audit engagement;q The audit function’s annual project planning procedures;andq The audit function’s communications with external quality assurance providers at its next quality assurance review.If the Audit Committee directs the audit function to conduct an audit that includes in its scopeactivities or operations that were part of a prior non-audit engagement conducted by the audit function,about which the CAE previously determined that the non-audit engagement wouldcreate an impairment for future audit work,the following procedures should be carried out:1.Prior to commencing the audit engagement,the CAE will communicate in writing with theAudit Committee,provide notice and description of the impairment,and indicate options forcarrying out the work with a maximum of objectivity(e.g.,contracting with a third-partyprovider,or requesting the assistance of auditors from partner or regulatory entities).2.If the Audit Committee directs the audit function to proceed with the audit engagement,theCAE will document the impairment in:q The audit engagement’s planning documentation;andq The audit engagement’s final report.3.In addition,the CAE shall disclose the occurrence and provide full documentation to theaudit function’s external quality assurance providers at its next quality assurance review. Screening process for non-audit(consulting)projects.When accepting and performing consulting work,auditors should document their rationale for providing consulting services and demonstrate their judgment that the services do not violate the core elements of the audit role.This information should be disclosed to external quality assurance reviewers.One example policy for screening is below:1.Upon receipt of a request for non-audit(consulting)services,the Internal Audit Departmentwill consider whether providing such services would create a personal impairment either infact or appearance that would adversely affect either the assigned auditor’s objectivity or tothe department’s independence for conducting subsequent audits within the same area.Ifthe engagement is determined to constitute an impairment to independence or objectivity,the request should be declined.If declined,the factors and final conclusion will bedocumented in a memorandum addressed to the requestor of the services.2.Before performing non-audit(consulting)services,the auditor in charge will document anunderstanding with the requestor(s)that the requestor(s)are responsible for the outcome ofthe work;and,therefore,has a responsibility to be in a position in fact and appearance tomake an informed judgment on the results of the non-audit(consulting)work.The InternalAudit Department will establish an agreement with the requestor(s)concerning the objec-tive,scope,and limitations imposed on the non-audit(consulting)engagement services.。