管理会计第14版(charles 查尔斯)英文影印版课后答案

加里森第十四版管理会计课后题答案CH11

Chapter 11Performance Measurement in Decentralized OrganizationsSolutions to Questions11-1In a decentralized organization, decision-making authority isn’t confined to a few top executives; instead, decision-making authority is spread throughout the organization.11-2The benefits of decentralization include: (1) by delegating day-to-day problem solving to lower-level managers, top management can concentrate on bigger issues such as overall strategy; (2) empowering lower-level managers to make decisions puts decision-making authority in the hands of those who tend to have the most detailed and up-to-date information about day-to-day operations; (3) by eliminating layers of decision-making and approvals, organizations can respond more quickly to customers and to changes in the operating environment; (4) granting decision-making authority helps train lower-level managers for higher-level positions; and (5) empowering lower-level managers to make decisions can increase their motivation and job satisfaction.11-3The manager of a cost center has control over cost, but not revenue or the use of investment funds. A profit center manager has control over both cost and revenue. An investment center manager has control over cost and revenue and the use of investment funds.11-4Margin is the ratio of net operating income to total sales. Turnover is the ratio of total sales to average operating assets. The product of the two numbers is the ROI.11-5Residual income is the net operating income an investment center earns above the company’s minimum required rate of return on operating assets.11-6If ROI is used to evaluate performance, a manager of an investment center may reject a profitable investment opportunity whose rate of return exceeds the company’s required rate of return but whose rate of return is less than the investment center’s curren t ROI. The residual income approach overcomes this problem because any project whose rate of return exceeds the company’s minimum required rateof return will result in an increase in residual income.11-7The difference between delivery cycle time and throughput time is the waiting period between when an order is received and when production on the order is started. Throughput time is made up of process time, inspection time, move time, and queue time. Process time is value-added time and inspection time, move time, and queue time are non-value-added time. 11-8An MCE of less than 1 means that the production process includes non-value-added time. An MCE of 0.40, for example, means that 40% of throughput time consists of actual processing, and that the other 60% consists of moving, inspection, and other non-value-added activities.11-9 A company’s balanced scorecard should be derived from and support its strategy. Because different companies have different strategies, their balanced scorecards should be different.11-10The balanced scorecard is constructedto support the company’s strategy, which is atheory about what actions will further the company’s goals. Assuming that the company has financial goals, measures of financial performance must be included in the balanced scorecard as a check on the reality of the theory. If the internal business processes improve, but the financial outcomes do not improve, the theory may be flawed and the strategy should be changed.1. Net operating incomeMargin =Sales$5,400,000= = 30%$18,000,0002. SalesTurnover =Average operating assets$18,000,000= = 0.5$36,000,0003. ROI = Margin ?Turnover= 30% ?0.5 = 15%Average operating assets ...................... £2,200,000 Net operating income ............................Minimum required return:16% × £2,200,000 ............................. 352,000 Residual income.................................... £ 48,0001. Throughput time = Process time + Inspection time + Move time +Queue time= 2.8 days + 0.5 days + 0.7 days + 4.0 days= 8.0 days2. Only process time is value-added time; therefore the manufacturingcycle efficiency (MCE) is:Value-added time 2.8 daysMCE===0.35Throughput time8.0 days3. If the MCE is 35%, then 35% of throughput time was spent in value-added activities, the other 65% was spent in non-value-added activities.4. Delivery cycle time = Wait time + Throughput time= 16.0 days + 8.0 days= 24.0 days5. If all queue time is eliminated, then the throughput time drops to only 4days (0.5 + 2.8 + 0.7). The MCE becomes:Value-added time 2.8 daysMCE===0.70Throughput time 4.0 daysThus, the MCE increases to 70%. This exercise shows quite dramatically how lean production approach can improve operations and reducethroughput time.1. MPC’s previous manufacturing strategy was focused on high-volumeproduction of a limited range of paper grades. The goal of this strategy was to keep the machines running constantly to maximize the number of tons produced. Changeovers were avoided because they loweredequipment utilization. Maximizing tons produced and minimizingchangeovers helped spread the high fixed costs of paper manufacturing across more units of output. The new manufacturing strategy is focused on low-volume production of a wide range of products. The goals of this strategy are to increase the number of paper grades manufactured,decrease changeover times, and increase yields across non-standard grades. While MPC realizes that its new strategy will decrease itsequipment utilization, it will still strive to optimize the utilization of its high fixed cost resources within the confines of flexible production. In an economist’s terms, the old strategy focused on economies of scale while the new strategy focuses on economies of scope.2. Employees focus on improving those measures that are used to evaluatetheir performance. Therefore, strategically-aligned performancemeasures will channel employee effort towards improving those aspects of performance that are most important to obtaining strategic objectives.If a company changes its strategy but continues to evaluate employee performance using measures that do not support the new strategy, it will be motivating its employees to make decisions that promote the old strategy, not the new strategy. And if employees make decisions that promote the new strategy, their performance measures will suffer.Some performance measures that would be appropriate for MPC’s old strategy include: equipment utilization percentage, number of tons of paper produced, and cost per ton produced. These performancemeasures would not support MPC’s new strategy because they would discourage increasing the range of paper grades produced, increasing the number of changeovers performed, and decreasing the batch size produced per run.Exercise 11-4 (continued)3. Students’ answers may differ in some details from this solution.4. The hypotheses underlying the balanced scorecard are indicated by thearrows in the diagram. Reading from the bottom of the balancedscorecard, the hypotheses are:° If the number of employees trained to support the flexibility strategy increases, then the average changeover time will decrease and thenumber of different paper grades produced and the averagemanufacturing yield will increase.° If the average changeover time decreases, then the time to fill anorder will decrease.° If the number of different paper grades produced increases, then the customer satisfaction with breadth of product offerings will increase.° If the average manufacturing yield increases, then the contributionmargin per ton will increase.° If the time to fill an order decreases, then the number of newcustomers acquired, sales, and the contribution margin per ton willincrease.° If the customer satisfaction with breadth of product offeringsincreases, then the number of new customers acquired, sales, andthe contribution margin per ton will increase.° If the number of new customers acquired increases, then sales willincrease.Each of these hypotheses can be questioned. For example, the time to fill an order is a function of additional factors above and beyondchangeover times. Thus, MPC’s average changeover time could decrease while its time to fill an order increases if, for example, the shippingdepartment proves to be incapable of efficiently handling greaterproduct diversity, smaller batch sizes, and more frequent shipments.The fact that each of the hypotheses mentioned above can bequestioned does not invalidate the balanced scorecard. If the scorecard is used correctly, management will be able to identify which, if any, of the hypotheses are invalid and modify the balanced scorecardaccordingly.1. (b) (c)Net Average(a) Operating Operating ROISales Income* Assets (b) ÷ (c)$4,500,000 $290,000 $800,000 36.25%$4,600,000 $300,000 $800,000 37.50%$4,700,000 $310,000 $800,000 38.75%$4,800,000 $320,000 $800,000 40.00%$4,900,000 $330,000 $800,000 41.25%$5,000,000 $340,000 $800,000 42.50%*Sales × Contribution Margin Ratio – Fixed Expenses2. The ROI increases by 1.25% for each $100,000 increase in sales. Thishappens because each $100,000 increase in sales brings in an additional profit of $10,000. When this additional profit is divided by the average operating assets of $800,000, the result is an increase in the company’s ROI of 1.25%.Increase in sales ................................................... $100,000 (a)Contribution margin ratio ....................................... 10% (b)Increase in contribution margin and net operatingincome (a) × (b) ................................................ $10,000 (c)Average operating assets ....................................... $800,000 (d)Increase in return on investment (c) ÷ (d) ............. 1.25%1. Net operating incomeMargin =Sales$800,000= = 10%$8,000,000SalesTurnover =Average operating assets$8,000,000= = 2.5$3,200,000ROI = Margin ?Turnover= 10% ?2.5 = 25%2. Net operating incomeMargin =Sales$800,000(1.00 + 4.00)=$8,000,000(1.00 + 1.50)$4,000,000= = 20%$20,000,000SalesTurnover =Average operating assets$8,000,000 (1.00 + 1.50)=$3,200,000$20,000,000 =$ = 6.253,200,000ROI = Margin ?Turnover = 20% ?6.25 = 125%3. Net operating incomeMargin =Sales$800,000 + $250,000=$8,000,000 + $2,000,000$1,050,000= = 10.5%$10,000,000SalesTurnover =Average operating assets$8,000,000 + $2,000,000=$3,200,000 + $800,000$1 = 0,000,000= 2.5$4,000,000ROI = Margin ?Turnover= 10.5% ?2.5 = 26.25%1. ROI computations:Net operating income Sales ROI = ?Sales Average operating assetsPerth:$630,000$9,000,000? = 7% ?3 = 21% $9,000,000$3,000,000Darwin: $1,800,000$20,000,000? = 9% ?2 = 18% $20,000,000$10,000,0002. Perth DarwinAverage operating assets .................... $3,000,000 $10,000,000Net operating income .........................Minimum required return on averageoperating assets—16% × Averageoperating assets .............................. 480,000 1,600,000Residual income ................................. $150,000 $ 200,0003. No, the Darwin Division is simply larger than the Perth Division and forthis reason one would expect that it would have a greater amount of residual income. Residual income can’t be used to compare theperformance of divisions of different sizes. Larger divisions will almost always look better. In fact, in the case above, Darwin does not appear to be as well managed as Perth. Note from Part (1) that Darwin has only an 18% ROI as compared to 21% for Perth.Exercise 11-8 (15 minutes)Company A Company B Company C Sales ......................................... $400,000 * $750,000 * $600,000 * Net operating income ................. $32,000 $45,000 * $24,000 Average operating assets ........... $160,000 * $250,000 $150,000 * Return on investment (ROI) ....... 20% * 18% * 16% Minimum required rate of return:Percentage ............................. 15% * 20% 12% * Dollar amount ......................... $24,000 $50,000 * $18,000 Residual income ........................ $8,000 $(5,000) $6,000 * *Given.1. Computation of ROI.Division A:$300,000$6,000,000ROI = ? = 5% ?4 = 20% $6,000,000$1,500,000Division B:$900,000$10,000,000ROI = ? = 9% ?2 = 18% $10,000,000$5,000,000Division C:$180,000$8,000,000ROI = ? = 2.25% ?4 = 9% $8,000,000$2,000,0002. Division A Division B Division CAverage operating assets ..... $1,500,000 $5,000,000 $2,000,000 Required rate of return ........ × 15% × 18% × 12% Minimum required return ..... $ 225,000 $ 900,000 $ 240,000 Actual net operating income .Minimum required return(above) ............................ 225,000 900,000 240,000 Residual income .................. $ 75,000 $ 0 $ (60,000)3. a. and b. Division A Division B Division CReturn on investment (ROI) ... 20% 18% 9% Therefore, if the division ispresented with aninvestment opportunityyielding 17%, it probablywould................................. Reject Reject Accept Minimum required return forcomputing residual income .. 15% 18% 12% Therefore, if the division ispresented with aninvestment opportunityyielding 17%, it probablywould................................. Accept Reject Accept If performance is being measured by ROI, both Division A and Division B probably would reject the 17% investment opportunity. The reason is that these companies are presently earning a return greater than 17%;thus, the new investment would reduce the overall rate of return and place the divisional managers in a less favorable light. Division Cprobably would accept the 17% investment opportunity, because itsacceptance would i ncrease the Division’s overall rate of return.If performance is being measured by residual income, both Division A and Division C probably would accept the 17% investment opportunity.The 17% rate of return promised by the new investment is greater than their required rates of return of 15% and 12%, respectively, and would therefore add to the total amount of their residual income. Division B would reject the opportunity, because the 17% return on the newinvestment is less than B’s 18% required rate of return.Exercise 11-10 (15 minutes)1. ROI computations:Net operating income Sales ROI = ?Sales Average operating assetsEastern Division:$90,000$1,000,000? = 9% ?2 = 18% $1,000,000$500,000Western Division:$105,000$1,750,000? = 6% ?3.5 = 21% $1,750,000$500,0002. The manager of the Western Division seems to be doing the better job.Although her margin is three percentage points lower than the margin of the Eastern Division, her turnover is higher (a turnover of 3.5, ascompared to a turnover of two for the Eastern Division). The greater turnover more than offsets the lower margin, resulting in a 21% ROI, as compared to an 18% ROI for the other division.Notice that if you look at margin alone, then the Eastern Divisionappears to be the strongest division. This fact underscores theimportance of looking at turnover as well as at margin in evaluatingperformance in an investment center.Exercise 11-11 (45 minutes)1. Students’ answers may differ in some details from this solution.2. The hypotheses underlying the balanced scorecard are indicated by thearrows in the diagram. Reading from the bottom of the balancedscorecard, the hypotheses are:° If the amount of compensation paid above the industry averageincreases, then the percentage of job offers accepted and the level of employee morale will increase.° If the average number of years to be promoted decreases, then thepercentage of job offers accepted and the level of employee moralewill increase.° If the percentage of job offers accepted increases, then the ratio ofbillable hours to total hours should increase while the averagenumber of errors per tax return and the average time needed toprepare a return should decrease.° If employee morale increases, then the ratio of billable hours to total hours should increase while the average number of errors per taxreturn and the average time needed to prepare a return shoulddecrease.° If employee morale increases, then the customer satisfaction withservice quality should increase.° If the ratio of billable hours to total hours increases, then the revenue per employee should increase.° If the average number of errors per tax return decreases, then thecustomer satisfaction with effectiveness should increase.° If the average time needed to prepare a return decreases, then thecustomer satisfaction with efficiency should increase.° If the customer satisfaction with effectiveness, efficiency, and service quality increases, then the number of new customers acquired should increase.° If the number of new customers acquired increases, then salesshould increase.° If revenue per employee and sales increase, then the profit marginshould increase.Each of these hypotheses can be questioned. For example, Ariel’scustomers may define effectiveness as minimizing their tax liabilitywhich is not necessarily the same as minimizing the number of errors ina tax return. If some of Ariel’s customers became aware that Arieloverlooked legal tax minimizing opportunities, it is likely that the“customer satisfaction with effectiveness” measure would decline. This decline would probably puzzle Ariel because, although the firm prepared what it believed to be error-free returns, it overlooked opportunities to minimize customers’ taxes. In this example, Ariel’s internal businessprocess measure of the average number of errors per tax return does not fully capture the factors that drive the customer satisfaction. The fact that each of the hypotheses mentioned above can be questioned does not invalidate the balanced scorecard. If the scorecard is usedcorrectly, management will be able to identify which, if any, of thehypotheses are invalid and then modify the balanced scorecardaccordingly.3. The performance measure “total dollar amount of tax refundsgenerated” would motivate Ariel’s employees to aggressively search for tax minimization opportunities for its clients. However, employees may be too aggressive and recommend questionable or illegal tax practices to clients. This undesirable behavior could generate unfavorablepublicity and lead to major problems for the company as well as itscustomers. Overall, it would probably be unwise to use this performance measure in Ariel’s scorecard.However, if Ariel wanted to create a scorecard measure to capture this aspect of its client service responsibilities, it may make sense to focus the performance measure on its training process. Properly trainedemployees are more likely to recognize viable tax minimizationopportunities.4. E ach office’s individual per formance should be based on the scorecardmeasures only if the measures are controllable by those employed at the branch offices. In other words, it would not make sense to attempt to hold branch office managers responsible for measures such as the percent of job offers accepted or the amount of compensation paid above industry average. Recruiting and compensation decisions are not typically made at the branch offices. On the other hand, it would make sense to measure the branch offices with respect to internal business process, customer, and financial performance. Gathering this type of data would be useful for evaluating the performance of employees at each office.1. Net operating incomeMargin =Sales$16,000= = 2%$800,000SalesTurnover =Average operating assets$800,000= = 8$100,000ROI = Margin ?Turnover= 2% ?8 = 16%2. Net operating incomeMargin =Sales$16,000 + $6,000=$800,000 + $80,000$22,000= = 2.5%$880,000SalesTurnover =Average operating assets$800,000 + $80,000=$100,000$880,000= = 8.8$100,000ROI = Margin ?Turnover= 2.5% ?8.8 = 22%3. Net operating incomeMargin =Sales$16,000 + $3,200=$800,000$19,200= = 2.4%$800,000SalesTurnover =Average operating assets$800,000= = 8$100,000ROI = Margin ?Turnover= 2.4% ?8 = 19.2%4. Net operating incomeMargin =Sales$16,000= = 2%$800,000SalesTurnover =Average operating assets$800,000=$100,000 - $20,000$800,000= = 10$80,000ROI = Margin ?Turnover= 2% ?10 = 20%DivisionFab Consulting IT Sales ....................................... $800,000 * $650,000 $500,000 Net operating income ............... $72,000 * $26,000 $40,000 * Average operating assets ......... $400,000 $130,000 * $200,000 Margin .................................... 9% 4% * 8% * Turnover ................................. 2.0 5.0 * 2.5 Return on investment (ROI) ..... 18% * 20% 20% * *Given.Note that the Consulting and IT Divisions apparently have different strategies to obtain the same 20% return. The Consulting Division has a low margin and a high turnover, whereas the IT Division has just the opposite.Problem 11-14 (30 minutes)1. Present New Line Total(1) Sales ......................... $21,000,000 $9,000,000 $30,000,000(2) Net operating income . $1,680,000 $630,000 * $2,310,000(3) Operating assets ........ $5,250,000 $3,000,000 $8,250,000(4) Margin (2) ÷ (1) ......... 8.0% 7.0% 7.7%(5) Turnover (1) ÷ (3) ...... 4.00 3.00 3.64(6) ROI (4) × (5) ............. 32% 21% 28%* Sales ............................................................. $9,000,000Variable expenses (65% × $9,000,000) .......... 5,850,000Contribution margin ....................................... 3,150,000Fixed expenses .............................................. 2,520,000Net operating income ..................................... $ 630,0002. Fred Halloway will be inclined to reject the new product line becauseaccepting it would reduce his division’s overall rate of return.3. The new product line promises an ROI of 21%, whereas the company’soverall ROI last year was only 18%. Thus, adding the new line would increase the company’s overall ROI.4. a. Present New Line TotalOperating assets ..................... $5,250,000 $3,000,000 $8,250,000 Minimum required return ......... × 15% × 15% × 15% Minimum net operating income $787,500 $450,000 $1,237,500 Actual net operating income ....Minimum net operating income(above) ................................ 787,500 450,000 1,237,500 Residual income ...................... $ 892,500 $ 180,000 $1,072,500b. Under the residual income approach, Fred Halloway would be inclinedto accept the new product line because adding the product line would increase the total amount of his division’s residual income, as shown above.1. Breaking the ROI computation into two separate elements helps themanager to see important relationships that might remain hidden. First, the importance of turnover of assets as a key element to overallprofitability is emphasized. Prior to use of the ROI formula, managers tended to allow operating assets to swell to excessive levels. Second, the importance of sales volume in profit computations is stressed and explicitly recognized. Third, breaking the ROI computation into margin and turnover elements stresses the possibility of trading one off for the other in attempts to improve the overall profit picture. That is, acompany may shave its margins slightly hoping for a large enoughincrease in turnover to increase the overall rate of return. Fourth, itpermits a manager to reduce important profitability elements to ratio form, which enhances comparisons between units (divisions, etc.) of the organization.2. Companies in the Same IndustryA B CSales .................................. $4,000,000 * $1,500,000 * $6,000,000 Net operating income .......... $560,000 * $210,000 * $210,000 Average operating assets ..... $2,000,000 * $3,000,000 $3,000,000 * Margin ................................ 14% 14% 3.5% * Turnover ............................. 2.0 0.5 2.0 * Return on investment (ROI) . 28% 7% * 7% *Given.NAA Report No. 35 states (p. 35):“Introducing sales to measure level of operations helps to disclosespecific areas for more intensive investigation. Company B does as well as Company A in terms of profit margin, for both companies earn 14% on sales. But Company B has a much lower turnover of capital thandoes Company A. Whereas a dollar of investment in Company Asupports two dollars in sales each period, a dollar investment inCompany B supports only 50 cents in sales each period. This suggests that the analyst should look carefully at Company B’s investment. Is the company keeping an inventory larger than necessary for its salesvolume? Are receivables being collected promptly? Or did Company A acquire its fixed assets at a price level which was much lower than that at which Company B purchased its plant?”Thus, by including sales specifically in ROI computations the manager is able to discover possible problems, as well as reasons underlying a strong or a weak performance. Looking at Company A compared to Company C, notice that C’s turnover is the same as A’s, but C’s margin on sales is much lower. Why would C have such a low margin? Is it due to inefficiency, is it due to geographical location (thereby requiring higher salaries or transportation charges), is it due to excessive materials costs, or is it due to still other factors? ROI computations raise questions such as these, which form the basis for managerial action. To summarize, in order to bring B’s ROI into line with A’s, it seems obvious that B’s management will have to concentrate its efforts on increasing turnover, either by increasing sales or by reducing assets. It seems unlikely that B can appreciably increase its ROI by improving its margin on sales. On the other hand, C’s management should concentrate its efforts on the margin element by trying to pare down its operating expenses.Problem 11-16 (30 minutes)1. a., b., and c.Month1 2 3 4Throughput time in days:Process time .................................. 0.6 0.5 0.5 0.4Inspection time .............................. 0.7 0.7 0.4 0.3Move time ..................................... 0.5 0.5 0.4 0.5Queue time ................................... 3.6 3.6 2.6 1.7Total throughput time ..................... 5.4 5.3 3.9 2.9Manufacturing cycle efficiency (MCE):Process time ÷ Throughput time ..... 11.1% 9.4% 12.8% 13.8% Delivery cycle time in days:Wait time ...................................... 9.6 8.7 5.3 4.7Total throughput time ..................... 5.4 5.3 3.9 2.9Total delivery cycle time ................. 15.0 14.0 9.2 7.62. The general trend is favorable in all of the performance measures exceptfor total sales. On-time delivery is up, process time is down, inspection time is down, move time is basically unchanged, queue time is down, manufacturing cycle efficiency is up, and the delivery cycle time is down.Even though the company has improved its operations, it has not yet increased its sales. This may have happened because managementattention has been focused on the factory—working to improveoperations. However, it may be time now to exploit these improvements to go after more sales—perhaps by increased product promotion and better marketing strategies. It will ultimately be necessary to increase sales so as to translate the operational improvements into more profits.。

管理会计第14版(charles 查尔斯)英文影印版课后答案

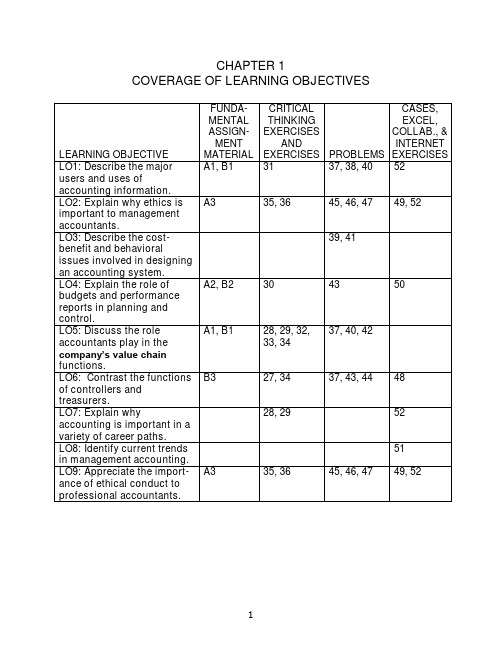

COVERAGE OF LEARNING OBJECTIVESManagerial Accounting and the Business Organization1-A1 (10-15 min.)Because the accountant's duties are often not sharply defined, some of these answers could be challenged:1. Attention directing and problem solving. Budgeting involves makingdecisions about planned activities -- hence, aiding problem solving.Budgets also direct attention to areas of opportunity or concern --hence, directing attention. Reporting against the budget also has ascorekeeping dimension.2. Problem solving. Helps a manager assess the impact of a decision.3. Scorekeeping. Reports on the results of an operation. Could also beattention direction if scrap is an area that might require management decisions.4. Attention directing. Focuses attention on areas that need attention.5. Attention directing. Helps managers learn about the informationcontained in a performance report.6. Scorekeeping. The statement merely reports what has happened.7. Problem solving. The cost comparison is apparently useful becausethe manager wishes to decide between two alternatives. Thus, it aids problem solving.8. Attention directing. Variances point out areas where results differfrom expectations. Interpreting them directs attention to possiblecauses of the differences.9. Problem solving. Aids a decision about where the parts should bemade.10. Scorekeeping. Determining a depreciation schedule is simply anexercise in preparing financial statements to report the results ofactivities.1. Budgeted Actual DeviationsAmounts Amounts or Variances Room rental $ 140 $ 140 $ 0Food 800 1,008 208UEntertainment 600 600 0Decorations 220 190 30FTotal $1,760 $1,938 $178U2. Because of the management by exception rule, room rental andentertainment require no explanation. The actual expenditure forfood exceeded the budget by $208. Of this $208, $150 is explained by attendance of 15 persons more than budgeted (at a budget of $10 per person) and $58 is explained by expenditures above $10 per person.Actual expenditures for decorations were $30 less than the budget. If all desired decorations were purchased, the decorations committee should be commended for their savings.1-A3 (10 min.)All of the situations raise possibilities for violation of the integrity standard. In addition, the manager in each situation must address an additional ethical standard:1. The General Mills manager must respect the confidentiality standard.He or she should not disclose any information about the new cereal.2. Roberto must address his level of competence for the assignment. Ifhis supervisor knows his level of expertise and wants an analysisfrom a “layperson” point of view, he should do it. However, if thesupervisor expects an expert analysis, Roberto must admit his lackof competence.3. The objectivity standard should cause Helen to decline to omit theinformation from her budget. It is relevant information, and itsomission may mislead readers of the budget.Because the accountant’s duties are often not sharply defined, some of these answers could be challenged:1. Scorekeeping. Records events.2. Scorekeeping. Simply recording of what has happened.3. Problem solving. Helps a manager decide between alternatives.4. Attention directing. Directs attention to the use of overtime labor.5. Problem solving. Provides information to managers for decidingbetween alternatives.6. Attention directing. Directs attention to why nursing costs increased.7. Attention directing. Directs attention to areas where actual resultsdiffered from the budget.8. Problem solving. Helps the vice-president to decide which course ofaction is best.9. Scorekeeping. Records costs in the department to which theybelong.10. Scorekeeping. Records actual overtime costs.11. Attention directing. Directs attention to stores with either high or lowratios of advertising expenses to sales.12. Attention directing. Directs attention to causes of returns of the drug.13. Attention directing or problem solving, depending on the use of theschedule. If it is to identify areas of high fuel usage it is attentiondirecting. If it is to plan for purchases of fuel, it is problem solving. 14. Problem solving. Provides information for deciding between twoalternative courses of action.15. Scorekeeping. Records items needed for financial statements.1 & 2. Budget Actual VarianceSales $75,000 $74,860 $ 140UCosts:Fireworks $35,000 $39,500 $4,500ULabor 15,000 13,000 2,000FOther 8,000 8,020 20UProfit $17,000 $14,340 $2,660U3. The cost of fireworks was $4,500 ÷ $35,000 = 13% over budget. Didfireworks suppliers raise their prices? Did competition cause retailprices to be lower than expected? There should be someexplanation for the extra cost of fireworks. Also, the labor cost was$2,000 ÷ $15,000 =13% below budget. It would be useful to discover why this cost was saved. Both sales and other costs were very close to budget.1-B3 (10 - 15 min.)1. Treasurer. Analysts affect the company's ability to raise capital,which is the responsibility of the treasurer.2. Controller. Advising managers aids operating decisions.3. Controller. Advice on cost analysis aids managers' operatingdecisions.4. Controller. Divisional financial statements report on operations.Financial statements are generally produced by the controller'sdepartment.5. Treasurer. Financing the business is the responsibility of thetreasurer.6. Controller. Tax returns are part of the accounting process overseenby the controller.7. Treasurer. Insurance, as with other risk management activities, isusually the responsibility of the treasurer.8. Treasurer. Allowing credit is a financial decision.1-1 Decision makers within and outside an organization use accounting information for three broad purposes:1. Internal reporting to managers for planning and controllingoperations.2. Internal reporting to managers for special decision-making and long-range planning.3. External reporting to stockholders, government, and other interestedparties.1-2 The emphasis of financial accounting has traditionally been on the historical data presented in the external reports. Management accounting emphasizes planning and control purposes.1-3 The branch of accounting described in the quotation is management accounting.1-4 Scorekeeping is the recording of data for a later evaluation of performance. Attention directing is the reporting and interpretation of information for the purpose of focusing on inefficiencies of operation or opportunities for improvement. Problem solving presents a concise analysis of alternative courses of action.1-5 GAAP applies to publicly issued annual financial reports. Internal accounting reports are not restricted by GAAP.1-6 Yes, but it covers more than that. The Foreign Corrupt Practices Act applies to all publicly-held companies and covers the quality of internal accounting control as well as bribes and other matters.1-7 Users cannot easily observe the quality of accounting information. Thus, they rely on the integrity of accountants to be sure the information is accurate. Information that is unreliable is worthless, so if accountants do not have a reputation for integrity, the information they produce will not have value.1-8 Three examples of service organizations are banks, insurance companies, and public accounting firms. Such organizations tend to be labor intensive, have outputs that are difficult to define and measure, and have both inputs and outputs that are difficult or impossible to store.1-9 Two considerations are cost-benefit balance and behavioral effects. Cost-benefit balance refers to how well an accounting system helps achieve management's goals in relation to the cost of the system. The behavioral consideration specifies that an accounting system should be judged by how it will affect the behavior (that is, decisions) of managers.1-10 Yes. The act of recording events has become as much a part of operating activities as the act of selling or buying. For example, cash receipts and disbursements must be traced, and receivables and payables must be recorded, or else gross confusion would ensue.1-11 A budget is a prediction and guide; a performance report is a tabulation of actual results compared with the budget; and a variance reconciles the differences between budget and actual.1-12 No. Management by exception means that management spends more effort on those areas that seem to be out of control and less on areas that are functioning as planned. This method is an efficient way for managers to decide where to put their time and effort.1-13 No. There is no perfect system of automatic control, nor does accounting control anything. Accounting is a tool used by managers in their control of operations.1-14 Information that is relevant for decisions about a product depends on the product's life-cycle stage. Therefore, to prepare and interpret information, accountants should be aware of the current stage of a product's life cycle.1-15 The six functions are: (1) research and development – generation and experimentation with new ideas; (2) product and service process design – detailed design and engineering of products; (3) production – use of resources to produce a product or service; (4) marketing - informing customers of the value and features of products or services; (5) distribution – delivering products or services to customers; and (6) customer service –support provided to customers.1-16 No. Not all of the functions are of equal importance to the success of a company. Measurement and reporting should focus on those functions that enable a company to gain and maintain a competitive edge.1-17 Line managers are directly responsible for the production and sale of goods or services. Staff managers have an advisory function – they support line managers.1-18 Management accountants are the information specialists, even in non-hierarchical companies. However, in such companies they are more directly involved with managers and are often parts of cross-functional teams.1- 19 A treasurer is concerned mainly with the company's financial matters, the controller with operating matters. In large organizations, there are sufficient activities associated with both financial and operating matters to justify two separate positions. In a small organization the same person might be both treasurer and controller.1-20 The four parts of the CMA examination are: (1) economics, finance, and management, (2) financial accounting and reporting, (3) management reporting, analysis, and behavioral issues, and (4) decision analysis and information systems.1-21 This is not true. About one-third of CEOs come from finance or accounting backgrounds. Accounting is excellent preparation for top management positions because accountants are often exposed to many parts of the company early in their careers.1-22 Changes in technology are affecting how accountants operate. They must be able to account for e-commerce transactions efficiently and safely, they often must integrate their accounting systems into ERP systems, and an increasing number are beginning to use XBRL to communicate information electronically.1-23 The essence of the just-in-time philosophy is the elimination of waste, accomplished by reducing the time products spend in the production process and trying to eliminate the time spent in processes that do not add value to the product.1-24 Moving tools and products that are in process from one location to another in a plant is an activity that does not add value to the product. So changing the plant layout to eliminate wasted movement and time improves production efficiency.1-25 The four major responsibilities are: (1) competence - develop knowledge; know and obey laws, regulations, and technical standards; and perform appropriate analyses, (2) confidentiality - refrain from disclosing or using confidential information, (3) integrity - avoid conflicts of interest, refuse gifts that might influence actions, recognize limitations, and avoid activities that might discredit the profession, and (4) objectivity - communicate information fairly, objectively, and completely, within confidentiality constraints.1-26 Standards do not always provide the needed guidance. Sometimes an action borders on being unethical, but it is not clearly an ethical violation. Other times two ethical standards conflict. In situations such as these, accountants must make ethical judgments.1-27 (5-10 min.)Typical activities associated with the treasurer function include:❑Provision of capital❑Investor relations❑Short-term financing❑Banking and custody❑Credits and collections❑Investments❑Risk managementTypical activities associated with the controller function include:❑Planning for control❑Reporting and interpreting❑Evaluating and consulting❑Tax administration❑Government reporting❑Protection of assets❑Economic appraisal1-28 (5-10 min.)Activities 2, 4, 5, and 6 are primarily associated with marketing decisions. The management accountant would assist in these decisions as follows: Boeing Company’s pricing decision requires cost data relevant to the new method of distributing spare parts. will need to know the costs of the advertising program as well as the additional costs of other value chain functions resulting from increased sales. TexMex Foods will need to know the incremental revenues and incremental costs associated with the special order. Target Stores needs to know the impact on both revenues and costs of closing one of its stores.Activities 1, 7, and 8 are primarily associated with production decisions. The management accountant would assist in these decisions as follows. Porsche Motor Company needs an analysis of the costs associated with purchasing the part compared to the costs of making the part. Dell will need to know the costs of the training program and the savings associated with increased efficiencies in the setup and changeover activities. General Motors needs to know the costs and salvage values of the replacement equipment, the proceeds of the sale of the old equipment, and the operating savings associated with the use of the new equipment.1-30 (5 min.)1. Management 4. Management 7. Financial2. Management 5. Management3. Financial 6. Financial1. Performance ReportBudget Actual Variance Explanation Revenues $220,000 $228,000 $8,000 F Additional salesfrom newproducts* Advertising cost 15,000 16,500 (1,500) U New advertisingCampaignNet $6,500 F* From the New Products Report, seven new products were added. This exceeded the plan to add six.2.Factors that may not have been considered include:a.The costs of new products may have exceeded their price.b.Customer satisfaction with new products may not have been partof the new products report.petitors’ reactions to the Starbucks store’s actions may nothave been anticipated.d.External uncontrollable factors such as increases in operatingcosts, adverse weather, changes in the overall economy, newcompetitors entering the market, or key employee turnover mayhave decreased efficiency.1-32 (5 min.)1. Line, support 3. Staff, marketing 5. Staff, support2. Staff, support 4. Line, marketing 6. Line, productionMicrosoft is a company that most students will know and have some understanding of what functions its managers perform. Nevertheless, this may not be an easy exercise for those who have little knowledge of how companies operate.Research & development – Because software companies must continually come out with new products and upgrades to their current products this is a critical function for Microsoft. More than one-fourth of Microsoft’s operating expenses are devoted to R&D.Design of products, services, or processes – For Microsoft the design and R&D process probably overlap considerably. Product design is critical; process design is probably not. One essential part of design is beta testing – that is, field testing of new software. This quality-control step is essential to prevent customer dissatisfaction with new products.Production – Microsoft produces disks and CD-ROMs and the manuals and packaging to go with them. However, they are increasingly delivering software over the Internet, which takes an initial process design and then few resources. It is not likely a major focus for Microsoft.Marketing – Microsoft spends more on sales and marketing than on any other operating expense. Increasing competition in software sales makes marketing essential to the company’s future. This function includes advertising and direct marketing activities, but it also includes activities of the company’s sales force. Distribution – This function is becoming simpler for Microsoft as it delivers more and more software over the Internet. Although the company must stay abreast of competitors in delivery methods, this is not likely to create a major competitive advantage or disadvantage for Microsoft.Customer service – Customer service is important, but Microsoft tries to minimize its costs in this area by product design – making things work right without needing deep computer expertise. Still, poor customer service can severely impact a company, so Microsoft must attend to it.Support functions – Most of the time these are not a major focus. There is one exception recently for Microsoft. Legal support has been front and center. The very future of the company was based on court judgments for which good legal support was essential.The management accountant's major purpose is to provide information that helps line managers in making decisions regarding the planning and controlling of operations. The accountant supplies information for scorekeeping, attention directing, and problem solving. In turn, managers use this and other information for routine and non-routine decisions and for evaluating subordinates and the performance of sub-parts of the organization. Management accountants must walk a delicate line between (1) making sure that managers are properly using the pertinent information and (2) making sure that the managers, not the accountants, are doing the actual managing.1-35(5 min.)Other costs of a poor ethical environment include legal costs and costs due to high employee turnover. Other benefits of a good ethical environment include low employee turnover, low loss from internal theft, and improved customer satisfaction resulting from better quality and service (that result from a more productive work environment).1-36(5 min.)There are numerous examples.“You understand how important it is to record this sale before year end, don’t you?”“Doing it this way is common for all companies in our business, so don’t worry!”“Trust me, the inventory is at the warehouse.”This problem can form the basis of an introductory discussion of the entire field of management accounting.1. The focus of management accounting is on helping internal users tomake better decisions, whereas the focus of financial accounting ison helping external users to make better decisions. Managementaccounting helps in making a host of decisions, including pricing,product choices, investments in equipment, making or buying goods and services, and manager rewards.2. Generally accepted accounting standards or principles affect bothinternal and external accounting. However, change in internalaccounting is not inhibited by generally accepted principles. Forexample, if an organization wants to account for assets on the basisof replacement costs for internal purposes, no outside agency canprohibit such accounting. Of course, this means that organizationsmay have to keep more than one set of records. There is nothingimmoral or unethical about having multiple sets of books, but theyareexpensive. Accounting data are commodities, just like butter or eggs.Innovations in internal accounting systems must meet the samecost-benefit tests that other commodities endure. That is, theirperceived increases in benefits must exceed their perceivedincreases in costs. Ultimately, benefits are measured by whetherbetter decisions are forthcoming in the form of increased net profitsor cost savings.3. Budgets, the formal expressions of management plans, are a majorfeature of management accounting, whereas they are not asprominent in financial accounting. Budgets are major devices forcompelling and disciplining management planning.4. An important use of management accounting information is theevaluation of performance, which often takes the form of comparisonof actual results against budgets, providing incentives and feedback to improve future decisions.5.Accounting systems have an enormous influence on the behavior ofindividuals affected by them. Management accounting is moreconcerned with the likely behavioral effects of various accountingalternatives that may be adopted than is financial accounting.1-38(10 min.)The main point of this question is that cost information is crucial for decisions regarding which products and services should be emphasized or de-emphasized. The incentives to measure costs precisely are far greater when flat fees are being received instead of reimbursements of costs.Note, too, that nonprofit organizations and profit-seeking organizations have similar desires regarding management accounting. Accountability is now in fashion for many purposes, including justification of prices, cost control, and response to criticisms by investors (whether they be donors, taxpayers, or others).When somebody's money is at stake, accounting systems get much love and attention. In a survey of 550 hospitals, hospital financial executives said that improved cost accounting systems "are crucial to responding to changes in hospital payment mechanisms and that better cost information is essential for more profitable and efficient operations." Hospitals will increasingly identify costs by product (type of case), not just by departments.1-39 (10 min.)Paperwork and systems often seem to become ends in themselves. However, the rationale that should underlie systems design is the cost-benefit philosophy or approach that is implied in the quotation. The aim is to get the managers and their subordinates collectively to make better decisions under one system versus another system -- for a given level of costs.Marks & Spencer should look at each of the management accounting reports it produces with an eye toward how it helps managers make better decisions. Does it provide needed scorekeeping? Does it direct attention to aspects of operations that might need altering? Does it provide information for specific management decisions? These types of questions will help identify the benefit of the information in the report.Then the company must consider the cost – not just the cost of collecting the data and preparing the reports, but the cost of educating managers to use the information and the cost of the time to read, digest, and act on the information. Too much information may be costly because it makes it time-consuming (and thus costly) to sift through the reams of information to find the few items that are important. And one cost may be the loss of important information because the total volume of information makes it too difficult to ferret out the important items.1-40(10 min.) Financial information is important in all companies. But how managers get and use financial information can differ depending on the culture and philosophies of the company.Top executives of a company often represent a functional area that is critical to the comparative economic advantage of the company. If technology is crucial, engineers generally hold important executive positions. If marketing differentiates the company from others, marketing executive s usually dominate. But regardless of the source of a company’s competitive advantage, its success will eventually be measured in economic terms. They must attend to financial aspects to thrive and often even to survive.Management accountants must work with the dominant managers in any organization. The modern trend toward use of cross-functional teams places management accountants at the center of the action regardless of what type of managers and executives dominate. Most companies realize that there is a financial dimension to almost every major decision, so they want the financial experts, management accountants, involved in the decisions. But to be accepted as an important part of these teams, the management accountants must know how to help managers in various functional areas. In General Mills, if accountants can’t talk the language of marketing, they will not have great influence. In ArvinMeritor, if they do not understand the information needs of engineers they will not provide value.1-41(10-15 min.)1. Boeing's competitive environment and manufacturing processeschanged greatly during the 1990s. An accounting system that served them well in their old environment would not necessarily be optimal in the 2000s. Boeing's management probably thought that changes in the accounting system were necessary to produce the kind of information necessary to remain competitive.2. A cost-benefit criterion was probably used. Boeing's management maynot have quantified the costs and the benefits, but they certainlyassessed whether the new system would help decisions enough towarrant the cost of the system.Many of the benefits of a better accounting system are hard to measure.They affect many strategic decisions of an organization. Withoutaccurate product costs, management will find it difficult to assess the consequences of their decisions. An accurate accounting system will help to price airplanes and other products competitively.3. More accurate product costs will usually result in better managementdecisions. But if the cost of the accounting system that produces the more accurate costs is too high, it may be best to forego the increased accuracy. The benefit of better decisions must exceed the added cost of the system for a change to be desirable.1-42(10 min.)1. There are many possible activities for each function of Nike's valuechain. Some possibilities are:Research and development -- Determining changes in customers'tastes and preferences for shoes and sportswear to come up withnew products (maybe the next "Air Jordans").Product and service process design -- Design a shoe to meet theincreasing demands of competitive athletes.Production -- Determine where to produce products and negotiatecontracts with the companies producing them.Marketing -- Signing prominent athletes to endorse Nike's products.Distribution -- Select the best locations for warehouses fordistribution to retail outlets.Customer service -- Formulate return policies for products thatcustomers perceive to be defective.2. Accounting information that aids managers' decisions includes:Research and development -- Trends in sales for various products, to determine which are becoming more and less popular.Product and service process design -- Production costs of variousshoe designs.Production -- Measure total costs, including both purchase cost and transportation costs, for production in various parts of the world.Marketing -- The added profits generated by the added sales due toproduct endorsements.Distribution -- Storage and shipping costs for different alternativewarehouse locations.Customer service -- The net cost of returned merchandise, to becompared with the benefits of better customer relations.。

管理会计课后练习参考答案.

第一章一、单选题1-5 BDBDB 6-9 DBBD二、多选题1-5 BCD ABC ABC ABCD ABCD 6-9 ABCD ABD ABC BCD三、简答题1. 狭义管理会计,又称微观管理会计,认为管理会计只为企业内部管理者提供计划,以控制所需信息的内部控制。

狭义管理会计的核心观点为:管理会计以企业为主体展开其管理活动;管理会计只为管理当局的管理目标服务;管理会计是一个信息系统,与财务会计并立,都是会计学的一个分支。

2. 20世纪70年代,管理会计的外延开始扩大,出现了广义管理会计概念。

广义管理会计的核心观点为:与狭义管理会计一样,管理会计以企业为主体展开其管理活动;但是管理会计不但为企业管理当局的管理目标服务,而且也为股东、债权人、税务当局等非管理集团服务;而从内容上看,管理会计包括了财务会计,同时还包括成本会计及财务管理。

3. 早期管理会计(20世纪初至50年代)。

19世纪末至20世纪早期,产业革命加速了资本主义经济的发展,促使企业生产规模迅速扩大,合伙经营和股份有限公司等企业组织形式相继出现,为会计的发展提供了广阔的天地。

20世纪,随着经济的发展,企业生产规模扩大,市场竞争也愈加激烈。

企业家意识到企业的经营效益不仅取决于产量的增长和外部市场的交易价格,更重要的是取决于成本的高低。

于是,从内部管理需要的角度出发,企业效益的衡量逐渐从由单纯的外部因素确定转向内部成本的计算和控制,产生了关于直接材料成本、人工成本、制造费用等成本项目的分类及具体的核算方法。

在该阶段,管理会计以成本控制为基本特征,以提高企业的生产效率和工作效率为主要目的。

其主要内容包括标准成本、预算控制和差异分析。

现代管理会计(20世纪50年代至80年代)。

20世纪50年代后,资本主义进入战后期。

现代科学技术的发展日新月异,并被大规模应用于生产,生产力获得迅速发展。

同时,资本主义企业进一步集中,跨国公司大量涌现,企业规模越来越大,市场情况瞬息万变,竞争愈加激烈。

管理会计(英文版)课后习题答案(高等教育出版社)chapter 16