SQAHND财政预算34

SQA-HND高等教育文凭项目全攻略

千里之行,始于足下。

SQA-HND高等教育文凭项目全攻略SQA-HND高等教育文凭项目是一种由苏格兰高等教育局(SQA)提供的国际学历认证项目。

该项目旨在为学生提供具有实践性、专业性和就业导向的教育经验,培养学生在特定领域的专业知识和技能。

在本文中,我们将为您介绍SQA-HND高等教育文凭项目的全攻略。

一、项目概述SQA-HND高等教育文凭项目是一种专业性较强的高等教育文凭项目,与学士学位相当。

该项目提供多个专业方向供学生选择,如商业管理、计算机科学、旅游管理等。

学生在完成一定的课程学习和实践实习后,可以获得SQA颁发的高等教育文凭。

二、申请条件1. 学历要求:申请人需具有高中毕业证书或同等学历。

2. 英语要求:申请人需达到评估组织要求的英语水平。

三、申请步骤1. 查询资料:在申请之前,学生需要查询相关资料,了解项目的课程设置、专业方向和就业前景。

2. 选择专业方向:根据个人兴趣和职业规划,选择适合自己的专业方向。

3. 提交申请:填写申请表并准备申请材料,如个人简历、学历证明、英语考试成绩等。

将这些材料递交给招生办公室。

4. 面试:根据学校要求,可能需要进行面试环节。

在面试中,申请人需要展示自己的学术能力、语言表达能力和专业兴趣。

5. 录取通知:根据申请成绩和面试表现,学校将会发放录取通知书给合适的申请人。

第1页/共2页锲而不舍,金石可镂。

四、课程设置SQA-HND高等教育文凭项目的课程设置根据不同的专业方向而有所不同。

一般包括专业课程、实践实习、学术研究等。

在专业课程中,学生将学习相关专业知识和技能,如市场营销、财务管理、软件开发等。

实践实习是为了让学生在实际工作环境中应用所学知识,提高职业能力。

学术研究是为了锻炼学生的学术能力和创新意识。

五、评估与考核在SQA-HND高等教育文凭项目中,学生的评估和考核方式多样化。

通常包括课程作业、实践实习报告、学术研究论文等。

学生需要按时完成各项作业,并在规定时间内提交。

HND项目有几种类型

HND项目有几种类型目前中国际有两种HND课程,一种是SQA HND,一种是BTEC HND。

以下是这两种课程的引见。

〔1〕SQA HNDSQA HND是由英国苏格兰学历管理委员会〔又称苏格兰资历监管局,简称SQ简称HND〕。

颁发的英国国度初等教育文凭〔Higher National Diploma,简称HND〕该文凭由英国文明委员会引荐,中英两国政府协作引进,经中国驻英国大使馆教育处认证,SQA HND文凭同等事于我国大专文凭。

Ø 国际项目院校是办学和实施教学管理的主体;Ø 英国苏格兰学历管理委员会〔SQA〕担任质量监管和文凭颁发;Ø 国外协作院校担任录取毕业生到国外继续学习;先生在国际完成三年的学习后,效果合格修满学分者可取得SQA颁发的HND文凭,同时取得中国休息和社会保证部职业技艺鉴定中心核发的国度三级职业资历证书。

取得SQA HND文凭的先生可以继续到英国、澳大利亚、新西兰、荷兰、美国、马来西亚等国度续本,取得本迷信位后效果优秀者继续攻读硕士学位。

〔2〕英国国度初等教育证书与文凭——HNDBTEC〔HND〕英国国度初等教育证书与文凭——其规范课程的要求适用于世界各个国度,先生在完成BTEC的课程后,失掉的将是具有国际化水准的、普遍供认的学历文凭。

在全世界范围内有110多个国度推行供认这些学历。

开发先生在任务中需求的实践技艺的初等职业教育文凭证书,也相当于英国大学前两年的课程,课程触及专业范围普遍,与实践任务环境联络严密。

关于先生而言,升学和失业是两件头号大事,BTEC HND职业学历证书教育在培育先生专业知识的同时为先生发明少量任务现场的实际时机。

因此BTEC HND既可以成为先生的职业资历,又可以协助先生进入海外大学攻读一年,取得学士学位,是先生海外升学与进入国际企业失业的最正确途径。

HND财政预算OUTCOME34报告

A financial analysis report for Tricol plcOutcome 3and4Class;10E6Name:Ma bodaSCN:125099297Candidate Num:22IntroductionTo operate better in financial aspect, the management of Tricol plc asked me to analyze their financial condition then make recommendations for them.FindingsPart A(ⅰ) Flex budget in line with actual activityTricol plc Flexed Budget for JuneOriginal budget FlexedbudgetActualresultsVariance2000 units 1600 units 1600unitsF/A££££Direct material 80,000 64,000 61,600 2,400 F Direct labor 36,000 28,800 35,200 6,400 A Variable productionoverhead4,000 3,200 3,200 0 Fixed costDepreciation 1,500 1,500 1,500 0 Rent and rates 2,500 2,500 2,500 0 Administration overhead 2,000 2,000 2,200 200 A Insurance costs 2,200 2,200 2,400 200 A Total 128,200 104,200 108,600 4,400 A(ⅱ) Variances calculationDirect material total variance(Standard units of actual production*standard price) -(actualquantity*actual price)(4 kg*1,600*£10) -£61,600 =£ 2,400 (F)Rate of significance: (3.75%)Direct material usage varianceStandard price*(standard units of actual production - actual quantity) £ 10*[ (4kgⅹ1,600) -5,600kg]= £8,000 (F)Rate of significance (12.5%)Direct material price varianceActual quantity * (standard price - actual price)5,600kg*[£ 10 -(£61,600/ 5,600kg) ]= £ (5,600) (A)Rate of significance: (8.75%)Direct labour total variance(Standard hours of actual production*standard rate ph) - (actual hours*actual rate ph)[ (2hrs*1,600) *£9]-£35,200=£(6,400) (A)Rate of significance: (22.22%)Direct labour efficiency varianceStandard rate ph* (standard hours of actual production - actual hours) £9*(2hrs*1,600-3,520hrs)=(2,880) (A)Rate of significance: (10%)Direct labour rate varianceActual hours*(standard rate ph – actual rate ph)3,520hrs*(£9*-£35,200/3,520hrs)= £(3,520) (A)Rate of significance: (12.22%)Total overhead varianceTotal standard overhead for actual production - total actual overheads (£18,000/12+£2,500+£2,200+£2,000)- (£1,500+£2,500+£2,200+£2,400)=£(400) (A)Rate of significance: (3.5%)(ⅲ) Report about variancesDirect material varianceThe direct material total variance can be analyzed in two aspects which are direct material volume and direct material price.For volume side, as calculated above, the budget volume is 6400kg; the actual volume is 5600kg. So there is 800kg variance which is favorable and each unit variance is 0.5kg. The likely reason causing the variance comes from three aspects. First of all, the company upgraded the production machinery recently, and new machine may use materials efficiently, so it reduced the waste of materials. Secondly, the company switched suppliers and using higher-grade materials can decrease wasteof materials too. Finally, the company has concluded ahigher-than-expected wage settlement for production operatives, which will maintain employees with higher skills as well as decrease turnoverof employees, and it also can increase efficiency in using materials.For price aspect, the budget price is £10 per kg, and the actual priceis £11per kg, it is adverse that one pound over the budget price. The company switching suppliers may cause the increase of negotiation cost. There may be a long-term relationship between Tricol plc and its old suppliers, so the suppliers may take lots of discounts to the firm. Afterchanging suppliers, the discount may disappear. Furthermore, higher grade materials increased unit price.Overall, the total material variance is favorable. £8,000 -£5,600=£2,400.Direct labour varianceThe direct labour total variance is composed of direct labour efficiency variance and direct labour rate variance.The budget direct labour hours are 3,200hrs and the actual labour hours are 3,520 hrs. There are more 320hrs needed than the budget, and each unit is 0.2hrs, which it is obviously adverse. The company upgrading the production machinery may need time for employees to adopt it. Also, employees need training time. The rebuild process of machinery consumed time too. In a word, the chargeable hours have increased.The budget direct laour hours rate is £9 per hour, the actual hours rate is £10 per hour. It is adverse that one pound higher than budgeted. It is possible caused by both internal and external factors.Higher-than-expected wage settlement may be internal reason for the variance, and new machinery may be needed to recruit new employees to operate the machinery, which also can increase the expense. For external factors, the changing of labour market may increase labour cost; the government legislation also can increase the labour cost, for example minimum pay.Both direct labour efficiency and direct labour rate variances are adverse, so the direct labour total variance is adverse.✧Overhead varianceAs calculated above, total overhead variance is caused by administration and insurance. Each factor has £200 variance, so the total overhead variance is £400 and it is adverse. During the process of changing supplier, the company needed more expense on public relationship or negotiation, in addition, in order to maintain the new machinery, administration cost will be increased too. For insurance aside, the improvement of machinery will need more insurance fees to cover, which also contributes to the increase of insurance fee of new employees.Part B◆Selection and application of two investment appraisal techniquesAs the company is keen to recoup the cost of the investment within five years, I will choose Payback period and Net Present Value to help me complete the appraisal.In order to fulfill the appraisal easily, there are some assumptions listed below should be considered before the appraisal.⑴ All revenue and inflow are assumed cash flow⑵ All investment cost incurred in year 0⑶ No uncertainty is considered⑷ Do not consider inflation and taxation⑸ Market rate of return is expected rate of return⑹ Rate of return is varying along with timeTricol plc Payback period for project distribution armYear Net cash flow Cumulative Cash Flow££Cash Flow Year 0 (1,000,000) (1,000,000) Cash Inflow Year 1 160,000 (840,000)Year 2 160,000 (680,000)Year 3 320,000 (360,000)Year 4 320,000 (40,000)Year 5 320,000 280,000 Net Cash Benefit Year 5 280.000 Note: req uire 40,000/320,000 in year 5= 1/8*year=1.5 mothsPayback=4 years 1.5 mothsTricol plc Net Present Value for project distribution armPresent Value Annual cash flow Present valuefactors at 10%£££Year 0 (1,000,000) 1.000 (1,000,000) Year 1 160,000 0.909 145,440Year 2 160,000 0.826 132,160Year 3 320,000 0.751 240,320Year 4 320,000 0.683 218,560Year 5 320,000 0.621 198,720 935,200 NPV (64,800)◆Recommendation about investmentAccording to Payback Period analysis, the investment cost can be recouped in year 4 and 1.5 moths. In other words, the period is under company’s expectation. The project can be executed. However, according to Net Present Value analysis, in terms of present value, within five years, what the NPV will bring net result is net cash loss but not net cash surplus. In general, the company should consider time value and other factors, so the project should not be executed.◆Factors impact on the investment should be consideredVarious factors will impact on result of investment. I will outline factors should be considered when the management reviewing my recommendation in financial and non-financial factors.✧Financial factorAs distribution arm is financial long-term beneficial project, it can be used inlong-term period and bring benefits continuous. The investment cost is £1,000,000, which can be considered a large investment. So it more likely needs long period payback period. The management should focus on longer cash flows for longer period of future. On the other hand, Net Present Value in year five is (28,000) only take 2.8% percents of the investment cost, it is more likely surplus in year six. Another financial factor is source of million pounds. If it is internal source, the management mainly concentrate on opportunities cost. If it is cost of capital or cost of capital taking much weight of the source, the management must pay costof the source firstly, the marketing rate of return likely low for the company, in addition, the management should use higher discounted cash flow.Non-financial factorThe investment must be consistence with company’s strategic plan. As Tricol is a plc, it must take social responsibility such as obeying government policy, minimizing impact on environment and minimizing impact on natives.ConclusionFor real competition is more complex and fierce, in order to make accurate decisions, management should consider more factors during the decision-making; furthermore, the management should use more tools to help them such as IRR, DCF.。

SQAHND财政预算34【实用资料】.doc

Contents1.0 Introduction ......................................................................................................... - 2 -2.0 The flexed budget ............................................................................................... - 2 -3.0 Calculate the Materials variances, Labour variances and the Total overhead. ... - 2 -3.1 Direct the materials variances , labour variances and the total overhead. .. - 2 -3.2 Variance analysis. ........................................................................................ - 3 -4.0 The recommendations for management (variances). .......................................... - 4 -5.0 Using four different methods to evaluate the financial. ...................................... - 5 -5.1 Identify the accounting rate of return........................................................... - 5 -5.2 Identify the payback. .................................................................................... - 5 -5.3 Identify the Net present value. ..................................................................... - 5 -5.4 Identify the Internal rate of return. ............................................................... - 6 -6.0 Recommendations for investment decision. ....................................................... - 6 -7.0 Conclusion .......................................................................................................... - 6 -8.0 Appendices .......................................................................................................... - 7 -1.0 IntroductionThis report will divided into two parts. Part A and Part B. In Part A,First of all, I will prepare a flexed budget in line with actual activity. Second, this will including the Materials variances, Labour variances and total overhead. At the same time, I will identify a minimum of one possible cause of the each variance. Finally, according to data analysis, there have been some recommendations to management of Matteck PLC. In Part B, It will have four different ways to evaluate financial performance and give recommendations for Matteck PLC. These ways are ARR ,Payback, NPV and IRR.Part A2.0 The flexed budgetFor Flex budged of Matteck PLC, we can see the Appendix 1.3.0 Calculate the Materials variances, Labour variances and the Total overhead.3.1 Direct the materials variances , labour variances and the total overhead.This section shows the Appendix 2.3.2 Variance analysis.Material price variance:The material price variance is ₤32,000(F). A ccording to the data analysis, it is ₤2/kg less expensive than planned. The possible reasons can be divided into three points: first, they could replace raw materials, using a lower - grade material. Second, the supplier to provide some discount for this batch of raw materials. Finally, learn from the case, the company has managed to locate new materials from an overseas. Due to the product from overseas, according to different exchange rate, the material will reduce the price.Material usage variance:The material usage variance is ₤30,000(A). The possible reasons include the effects of raw materials and the influence of the machine. If the company using poor quality raw materials, it may be more difficult to work. This will increase the waste materials. At the same time, the case shows that the company's new machinery can be fully used in the second week. The delay time may have caused the machine to use more materials than planned.Material total variance:The material total variance is 2,000(F). Case shows that the company's raw materials are from overseas suppliers. This will reduce some costs. Which leads to the material price variance is 32,000 (F). On the other hand, the company has introduced a new machine, the influence of machine installed time, caused some wasted of materials. This makes t he material usage variance is ₤30000 (A). Even if The company’s material total variance is 2000 (F). The company's management still should pay attention to The utilization of raw materials.Labour efficiency variance:The Labour efficiency variance is 10,000(F). The possible reasons could include the new machine to improve staff work efficiency. Using new machine can less labour hours. At the same time , the case shows that the company has had to employ more highly qualified staff. They can increase theworking efficiently through the higher skill.Labour Rate Variance:The Labour rate variance is 15,000(A). Through the calculation, the labour rate is ₤1.50 per hour higher than original. The possible reasons is ₤1.50 per hour higher than planned. The cost of direct labour is adverseness for this firm.Labour Total Variance:the Labour total variance is 5,000(A). The reasons of variance, the company has introduced the new machine, As the result the direct labor efficiency variance is favorable which is 10,000(F). On other hand, the labour rate is higher than standard labour rate. Finally, lead to the labour total variance is adverse,4.0 The recommendations for management (variances).1. The company should be had a variety of data investigation to set up complete data system. At the same time, through the different variance, the company can know more about the market information.2. The company should intensify the performance monitor for staff because the lower performance will accelerate waste of material and then lead to the material usage is increase, the performance monitor can help the company shrink the variance.3. Management: the company can provide some motivation policies to motivate the staff that is work hard and enhance the work enthusiastic of the staff. This can improve the staff work efficiency.Part B5.0 Using four different methods to evaluate the financial.5.1 Identify the accounting rate of return.ARRAverage profit=5000,300,3=660,000 Accounting rate of return=000,500,2000,660=26.4%The cases show that the company should have an accounting rate of return of at least 15%, through calculation, the ARR is 26.4%. Therefore, the data has meet company standards.5.2 Identify the payback.The company hopes to recover the cost of the investment within 4 four years. In fact, they just use 3 years 341days. (see Appendix 3.)5.3 Identify the Net present value.The NPV method calculates the present values of cash inflows and outflows and establishes whether. Basically, NPV provides an objective for evaluating and selecting investment projects. Moreover, it takes into account required rate of return of company and then takes into account time value of money. But there are substantialuncertainly factors in our world. For instance the inflation and deflation, the exchange rate.When the Matteck’s c ost of capital is 10%. The NPV is (46200). The NPV value less than 0. The company should not invest this project. ( see Appendix 4.)5.4 Identify the Internal rate of return.When the present value is 5%, the internal rate of return is 9.39%. Which less than 10% of company standard.therefore,the company should not invest this project.( see Appendix 5)6.0 Recommendations for investment decision.1.According the four method, The ARR and Payback are both implement for this project, but the NPV and IRR are not implemented for this Project. In this case ,the company should focus on the NPV and IRR.2.By calculates the net present values, it seems that the deficit, which means that the annual cash flows are not enough to allow more interest to be deducted and still repay the original investment. This investment is unworthy .3.Within five years. All the market factors are changeable. The information will have different change. And there are maybe some other situations occurred. So the Matteck PLC should not concern with the project.7.0 ConclusionThe report can help the company make the flex budget, and then by variances analysis and use thefour methods to evaluate the financial. Through the recommendations can help the company choose the best investment to gain the maximum profits.8.0 Appendices8.1 Appendix 18.2 Appendix 28.3 Appendix 3PaybackCapital cost ₤2,500,00 Year 1 ₤500,000 Year 2 ₤600,000 Year 3 ₤700,000 Year 4 ₤750,000 Year 5 ₤750,000 Total ₤3,300,000Payback=3 year+000,750000 ,800,1000,500,2×365days =3 year 341days8.4 Appendix 48.5 Appendix 5R=10% NPV=(46200) R=5% NPV=330256 IRR=5%+)200,46(256,330256,330 ×5%=9.39%。

sqahnd财政预算34.docx

Contents1.0 Introduction ...................................................................................................................... - 2 -2.0 The flexed budget ............................................................................................................. - 2 -3.0 Calculate the Materials variances, Labour variances and the Total overhead.....- 2 -3.1Direct the materials variances , labour variances and the total overhead....- 2 -3.2Variance analysis ................................................................................................... - 3 -4.0 The recommendations for management (variances) ........................................................ - 4 -5.0 Using four different methods to evaluate the financial .................................................... - 5 -5.1Identify the accounting rate of return ..................................................................... - 5 -5.2Identify the payback .............................................................................................. - 5 -5.3Identify the Net present value ................................................................................ - 5 -5.4Identify the Internal rate of return ......................................................................... - 6 -6.0 Recommendations for investment decision ...................................................................... - 6 -7.0 Conclusion ........................................................................................................................ - 7 -8.0 Appendices ....................................................................................................................... - 7 -1.0 IntroductionThis report will divided into two parts. Part A and Part B. In Part A,First of all, I will prepare a flexed budget in line with actual activity. Second, this will including the Materials variances, Labour variances and total overhead. At the same time, I will identify a minimum of one possible cause of the each variance. Finally, according to data analysis, there have been some recommendations to management of Matteck PLC. In Part B, It will have four different ways to evaluate financial performance and give recommendations for Matteck PLC. These ways are ARR ,Payback, NPV and IRR.Part A2.0 The flexed budgetFor Flex budged of Matteck PLC, we can see the Appendix 1.3.0 Calculate the Materials variances, Labour variances and the Total overhead.3.1Direct the materials variances , labour variances and the total overhead・This section shows the Appendix 2.3.2Variance analysis.Material price variance:The material price variance is £32,000(F). According to the data analysis, it is £2/kg less expensive-2-than planned. The possible reasons can be divided into three points: first, they could replace raw materials, using a lower - grade material. Second, the supplier to provide some discount for this batch of raw materials. Finally, learn from the case, the company has managed to locate new materials from an overseas. Due to the product from overseas, according to different exchange rate, the material will reduce the price.Material usage variance:The material usage variance is £30,000(A). The possible reasons include the effects of raw materials and the influence of the machine. If the company using poor quality raw materials, it may be more difficult to work. This will increase the waste materials. At the same time, the case shows that the company's new machinery can be fully used in the second week. The delay time may have caused the machine to use more materials than planned.Material total variance:The material total variance is 2,000(F). Case shows that the company's raw materials are from overseas suppliers. This will reduce some costs. Which leads to the material price variance is 32,000 (F). On the other hand, the company has introduced a new machine, the influence of machine installed time, caused some wasted of materials. This makes the material usage variance is €30000 (A). Even if The company's material total variance is 2000 (F). The company's management still should pay attention to The utilization of raw materials.Labour efficiency variance:The Labour efficiency variance is 10,000(F). The possible reasons could include the new machine to improve staff work cfYiciency. Using new machine can less labour hours. At the same lime , the case shows that the company has had to employ more highly qualified staff. They can increase theworking efficiently through the higher skill.Labour Rate Variance:The Labour rate variance is 15,000(A). Through the calculation, the labour rate is £1.50 per hour higher than original. The possible reasons is £1.50 per hour higher than planned. The cost of direct labour is adverseness for this firm.Labour Total Variance:the Labour total variance is 5,000(A). The reasons of variance, the company has introduced the newmachine, As the result the direct labor efficiency variance is favorable which is 10.000(F). On other hand, the labour rate is higher than standard labour rate. Finally, lead to the labour total variance is adverse,4.0 The recommendations for management (variances)・1.The company should be had a variety of data investigation to set up complete data system. At the same time, through the difierent variance, the company can know more about the market information.2.The company should intensify the performance monitor for statTbecause the lower performance will accelerate waste of material and then lead to the material usage is increase, the performance monitor can help the company shrink the variance.3.Management: the company can provide some motivation policies to motivate the staft' that is work hard and enhance the work enthusiastic of the staff. This can improve the staff work efficiency.Part B5.0 Using four different methods to evaluate the financial. 5.1 Identify the accounting rate of return ・ARRAverage profit= 3,300,0005=660,000Accounting rate of retum==26.4%The cases show that the company should have an accounting rate of return of at least 15%, through calculation, the ARR is 26.4%. Therefore, the data has meet company standards.5.2 Identify the payback.The company hopes to recover the cost of the investment within 4 four years. In fact, they just use 3 years 341 days, (see Appendix 3.)5.3 Identify the Net present value.The NPV method calculates the present values of cash inflows and outflows and establishes whether. Basically, NPV provides an objective for evaluating and selecting investment projects. Moreover, it takes into account required rate of return of company and then takes into account time value of money. But there are substantial660,000 2,500,000uncertainly factors in our world. For instance the inflation and deflation, the exchange rate. When the Matteck's cost of capital is 10%. The NPV is (46200). The NPV value less than 0. The company should not invest this project. ( see Appendix 4.)5.4Identify the Internal rate of return.When the present value is 5%, the internal rate of return is 9.39%. Which less than 10% of company slandard.thcrcfore,the company should not invest this project.(see Appendix 5)6.0 Recommendations for investment decision.1.According the four method, The ARR and Payback are both implement for this project, but the NPV and IRR are not implemented for this Project. In this case ,thc company should focus on the NPV and IRR.2.By calculates the net present values, it seems that the deficit, which means that the annual cash flows are not enough to allow more interest to be deducted and still repay the original investment. This investment is unworthy .3.Within five years. All the market factors are changeable. The information will have different change. And there are maybe some other situations occurred. So the Matteck PLC should not concern with the project.7.0 ConclusionThe report can help the company make the flex budget, and then by variances analysis and use the-6-four methods to evaluate the financial. Through the recommendations can help the company choose the best investment to gain the maximum profits.8.0 Appendices8.1Appendix 18.2Appendix 2-7-。

什么是HND项目什么是SQA 这些文凭能得到认证吗

【百度搜索,航程海归咨询】

什么是HND项目什么是SQA 这些文凭能得到认证吗

就读中外合作办学项目取得的国(境)外学历学位证书,都应该要申请国(境)外学历学位认证,只有通过了国(境)外学历学位认证的申请者,其学位证书才能够获得社会的承认。

如果是没有国(境)外学习经历或者学习时间不满6个月的应该申请中外合作办学学历学位认证。

要通过中外合作办学学历学位认证,首先最重要的一点即是该申请者所就读的中外合作办学项目是在教育部有备案的,如果中外合作办学认证系统没有找到所就读的中外合作办学项目,那么你注册的第一步就不能完成,也就不能提出认证申请。

遇到这种情况在认证系统注册没有找到就读的中外合作办学项目,即是所就读的办学项目是没有在教育部备案的,需要申请人自己联系办学项目的中方办学机构的相关负责人,需要中方办学机构负责人按照教育部留服中心的要求,在线注册进行项目确认手续。

这样在中方院校完成注册和项目确认程序之后,及备案成功之后,申请人就可以在合作办学系统中注册成功并提交认证申请。

按照实际情况了来说,如果是之前没有备案的中外合作办学项目,那么很可能在申请人联系该项目负责人之后,也不会在教育部留服中心进行注册和项目确认手续,或者说一些项目可能是在之前就在留服中心确认失败备案不成功的。

若是这样的情况,那申请者找项目负责人也是没有用的,可以与我们的海归顾问面对面交流这一问题,桑梵学历学位认证可以为你解决就读中外合作办学项目未备案的问题,帮助你成功通过学历学位认证。

SQA HND 疑难解答

1、SQA HND是什么?答:SQA HND是由英国苏格兰学历管理委员会(又称苏格兰资格监管局,简称SQA)颁发的英国国家高等教育文凭(Higher National Diploma,简称HND)。

该文凭由英国文化委员会推荐,中英两国政府合作引进,经中国驻英国大使馆教育处认证,SQA HND文凭等同于我国大专文凭。

2、SQA是什么性质的机构?答:SQA(Scottish Qualifications Authority)苏格兰学历管理委员会,又称苏格兰资格监管局,受苏格兰首相的直接领导,隶属苏格兰教育部。

是负责除学位和部分专业资格以外其它学历资格的开发、评估、颁证和资质鉴定的法定政府机构。

SQA是唯一得到中国驻英使馆认证的英国颁证机构。

SQA学历资格在世界上得到认可。

SQA的主要职能包括:设计与推广优质的国家资格证书、国家高等资格证书、职业资格证书;资格鉴定及授权发证;审批开设SQA证书项目的教育和培训机构;安排评估、评审及考试;体现质量保证职能;颁发学历资格证书。

3、国内学生完成SQA HND课程后可获得什么结果?答:学生在国内完成三年的学习后,成绩合格修满学分者可获得SQA颁发的HND 文凭,同时获得中国劳动和社会保障部职业技能鉴定中心核发的国家三级职业资格证书。

获得SQA HND文凭的学生可以继续到英国、澳大利亚、新西兰、荷兰、美国、马来西亚等国家续本,获得本科学位后成绩优异者可继续攻读硕士学位。

4、什么是“五年学业规划”?答:即前三年在国内完成HND课程,后两年到国外完成本科和硕士课程,整个过程为五年。

学生可根据自身情况选择分段学习。

第一年国内预科、第二、三年国内专业课程;获HND文凭并雅思成绩达到国外大学要求者第四年可国外续本,获得学士学位后,第五年可继续攻读硕士课程,实现“五年分段学习,国内外专本硕连读”。

5、SQA HND在国内的教学模式?答:国内课程教学模式有两种,分别为全英班和中文班,两者的特点有:6、SQA HND课程招生对象是谁?答:应、往届高中毕业生(或同等学历者)。

HND财政预算报告

1. IntroductionThis report is about a company Tricol plc, which makes a range of furniture and kitchenware, is now considering the development of its own distribution arm. It is provided assumptions, application of pay back period and NPV, evaluation and recommendation and other factors to be considered in this report. It could has important significance for assessing the rationalization of investment.2.0 Part AThe budget and calculation is showed on AppendixThere is a company policy to apply a rate of significance of 3% for any variance analysis. And the direct material variance can be analyzed in two aspects which are direct material volume and direct material price.The direct material price variance is adverse. The company has recently switched suppliers and it is now using high-grade materials. This may make the company lose the discount offered by original suppliersDirect labour variance is adverse. Reason may be that insurance is more than the budget insurance. The new machines use may result in this kind of situation, for the same reason overhead, including installation charges, staffing fees, maintenance increase and so on.There are two aspects what are weight of the direct materials and direct material price to analysis the total variance of direct material. From the weight of the direct materials, the budget for 6400 kg weight, the actual weight for 4600 kg, and the weight of each unit sent a 0.5 kg. The reasons are: the company changed suppliers,use the advanced materials to reduce the material waste; the production of equipment get upgrades, improve the production efficiency; Raised salary for employees to keep the higher technology and reduce the error, improve the efficiency in the use of materialsOverhead variance: total overhead variance is caused by administration and insurance. Each factor has £200 variance, so the total overhead variance is £400 and it is adverse. In addition, on side of insurance, Improving mechanical efficiency will need to pay more insurance cost, the employee of operate these equipment insurance costs also will be increasedRecommendationThere are some Suggestions can make the situation improved. The first, Ensure the quality, the price is cheap, but use the material. Secondly, The Company can establish policies to control administrative costs. They can try to use material price discount. The variance of labor, for enterprise is a must for the long-term cost of place, and wage increase, and may continue to increase, but Labour had reduced rate. Also has some advice. The company can provide the plan of the training, in order to improve production efficiency. Can also make employees responsible for the machine can be used a longer time.2.1 Part BAssumptionsThere are some views in the use of these data.The effects of the tax and inflation are neglected. Second, a given market returns will not change.●In the initial outflows of cash flow is satisfied, the time value of money beignored, not including interest is for the initial capital investment.●The expected return on the investment, here is to point to deduct the net cash flowfrom all the relevant costs.●Uncertainty does not exist●All the market factors are stableNet Present Value (NPV): The NPV method calculates the present values of cash inflows and outflows and establishes whether, in total, the present value of cash inflows is greater than the present value of cash outflows.Calculation of net present value, It is showed by Appendix.Payback: Those ways of in order to restore the original investment cost methods have to investment and project evaluation have many years, in order to received effect in shortest time. (1) year 0 means now (2) year 1 means at the end of 12 months from now (3) year 2 at the end of 2 years from now.Calculation of the payback period method, It is showed by Appendix.AnalyzeThe analysis of two investment appraisal techniquesDisadvantages of the payback method·It ignores cash flows after initial outflow has been met·It ignores risk·It ignores time value of money·It ignores the fact that benefits from different projects may accrue at an uneven rate ·No allowance is made for interest on the initial capital investment.Advantages of the NPV method·Provides an objective basis for evaluating and selecting investment projects ·Takes account of both magnitude and timing of expected cash flows in each period of a project’s lifeInvestors can not use a single formula to calculate the rate of return, they should consider the value of the time.In view of the data calculated above, payback will take four years and one-and-half month to complete, therefore, it seems to be reasonable to accept and invest this kind of project. However, in other method, it is impossible to fulfill a requirement of a 10% return. The actual rate of return must be less than 10%.Taking this two methods into consideration, firstly, net present value methods is more accurate than payback period method, secondly, although it cannot realize the expected return in 10% in the first 5 years, mainly basing on growing slowly and low return at beginning, it may bring a higher revenue and positive cash inflow in the future years.Personally, I think we can accept the new project for a period time. RecommendationThere are some Suggestions to continue to do investment company. We can from the financial factor analysis and the financial factors. The first. Form the economic factors. There are some Suggestions. The company must make sure that they have enough money to complete this investment. The company also need to consider budget control and the ability to solve problems. And then sure need to move on this investment. The company should consider whether to profit the most for the companylong-term interests. Then from non-financial aspects. Focus on the information about the change in the current social economic, political and legal. Whether can increase employment guidance. Clearly know people are willing to pay is suitable for this investment. Finally, the investment is in accordance with the company's strategy.3. ConclusionsThe company's consultants, this report can help the company bend of the budget and variance and use these two kinds of methods are analyzed, and help the company choose investment investment method. The company will make much profit.4. AppendixTricol Plc Flexed budgedBased on the all information about “Zupper” expendable table, I draw a table as following:The calculation of the variances and the variance rate1.Direct material total variance(standard units of actual production×standard price) –(actual quantity×actual price)[(4kg×1600)×£10] –£61600= £64000 –£61600=£2400 ( F )The rate for direct material total variances is £ 2,400/£ 64,000×100%=3.75%2.Direct material price varianceactual quantity×( standard price-actual price)=5600kg×( £10- £11)=5600kg×£1=5600 (A)The rate of direct material price variance is £ 5,600/£ 64,000×100%=8.75%3.Direct material usage variancestandard price×(standard units of actual production-actual units)=£10×(4kg×1600-5600kg)=£10×800kg=£8000 (F)The rate of direct material usage variance is £ 8,000/£ 64,000×100%=12.5%Note: When adding the price and usage variances the result must equal the total variance. Therefore, £5600(A) (price)+£8000(F) (usage) = £2400(F) (total).4.Direct labour total variance( standard hours of actual production×standard rate ph) -(actual hours×actual rate ph)[(2h×1600)×£9] -(3520h×£10)=(3200h×£9)-£35200=£28800 -£35200=£6400(A)The rate of diretc labour variance is 6400/28800×100%=22.2%5.Direct labour rate varianceactual hours×( standard rate ph-actual rate ph)3520h×(£9-£10)=3520h×£1=£3520(A)The rate of direct labour rate variance is £ 3,520/£ 28,800×100%=12.2%6.Direct labour efficiency variancestandard rate ph ×( standard hours of actual production-actual hours)£9×[2h×1600-3520h]=£9×(3200h-3520h)=£9×320h=£2880(A)The rate of direct labour efficiency variance is £ 2,880/£ 28,000×100%=10% Note: When adding rate and efficiency variances the result must equal the totalvariance. Therefore, £3520(A) (rate)+£2880(A) (efficiency) = £6400(A) (total).7.Overhead total variance(standard insurance cost-actual insurance cost)+(standard administration overheads-actual administration overheads)(£2200-£2400)+(£2000-£2200)=£200(A)+£200(A)=£400(A)The rate of overhead total variance is £ 400/£ 4,200×100%=9.52%Calculation of net present value at 10%Payback period method:In Year 5 the cash inflows for the full year are £320,000 but only £40,000 is required to recoup the initial investment. This is therefore reached in 1.5 months.Payback= 40000/320000*Year 5= 1/8 Year 5= 4 year 1.5monthsPayback will take 4 year 1.5months.。

SQA HND Preparing Financial Forecasts财政预算?题目及答案

题目:Outcome(s) covered1 and 2Assessment task instructionsQuestion 1Jamieson Tech Ltd is a manufacturing company. The following is an extract from their budgeted information for the year after overhead costs have been apportioned to the relevant production department:The following information relates to Overhead costs:(a) Within each department, Production Overheads are absorbed on the following basis:Department A—Labour Hour RateDepartment B—Machine Hour Rate(b) Administration Overheads are 10% of Prime Cost(c) Selling and Distribution Overheads are 10% of Production CostThe company has received an order for a job—referencenumber: 35/TGB. Specific details are as follows:(i) The job will require two types of Direct Materials–Material V and Material Z–as follows:100 kg of Material V @£8/kg 80 kg of Material Z @£12/kg(ii) The job will require the following Direct Labour:Department A— 100 hours @£6.00 per hour DepartmentB— 110 hours @£4.00 per hour(iii) In Department B, the order will require 80 hours’ mac hine time(iv) For this specific job, the company will have to hire a special machine—the cost of this hire is£400(v) The company requires a profit margin of 20% on this jobYou are required to: Prepare an Operating Statement for the job, using the above information, showing clearly Total Cost, Profit and Selling Price. Question 2Jamieson Tech Ltd also manufacture Product ref CPO. Again, the production process for this product utilises Departments A and B. The Operating Statement below outlines the expected costs, profit and selling price of one unit of this product.A large and important customer, Ceesay plc, has approached Jamieson Tech Ltd and offered them£304,000 for 100 units of product CPO.The management of Jamieson Tech Ltd is considering this special order, especially as tightening market conditions mean that the future selling price of CPO is expected to fall by 10%. However, in order to meet the tight deadlines for this special order they would need to reorganise their usual production processes, in particular to access the extra labour required in DepartmentA. They are therefore considering the following options:(a) Reject Ceesay’s offer assuming the expected fall in selling price.(b) Accept the special order, but make up the labour required by temporarily closing Department C (which makes product TUC) and transferring employees from Department C to Department A. This will result in a lost contribution of£10,000 from ceasing to make and sell product TUC. In addition, the temporary closure of Department C will result in its share of Fixed Overheads being re-allocated to theother departments. This will increase the Departmental Overhead Absorption Rates and will mean that, for this special order, Department A will incur additional Fixed Overheads of£2,000 and Department B will incur additional Fixed Overheads of£1,000.(c) Accept the special order, but utilise overtime in Department A in order to meet the requirements of this job (this would avoid the need to close Department C). This would mean that the direct labour for this order in Department A would be charged at time-and-a-half.In addition, if the company went ahead with options (b) or (c) above, and accepted the special order from Ceesay, their direct material suppliers would give them an additional trade discount of 20%.You are required to:(i) Produce a Marginal Cost Statement, using the above information, analysing the three alternative courses of action. The statement should show clearly the effect of changing costs/and or revenue levels on Contribution and Profit. Assume all Overhead Costs are Fixed Costs.(ii) Produce a short report to the management of Jamieson Tech Ltd, in which you recommend and justify an appropriate course of action.答案:Assessment task1Outcome(s) covered1 and 2Suggested solution and making an assessment decisionThe standard required for a pass should be based on the principal criteria: Does the candidate demonstrate an understanding of the preparation of this financial information?It is not intended that occasional arithmetical errors should be regarded as requiring a complete reassessment. Up to two errors of principle from each question could be reQuestion 2(a) Jamieson Tech Ltd Marginal Cost Operating Statement 100 units of Product CPO—offer by Ceesay plc(b) Short report to management:The report should briefly outline the three options under consideration and then recommend which option to adopt— this should be supported by a rational justification.For example, the second option (Accept offer— close C) should be accepted as it provides the greatest contribution towards fixed costs and also results in the highest projected profit. Consideration should also be given to the third option (Accept offer— retain C) as this option is still profitable and closing Department C (even on a temporary basis) may have a detrimental impact on staff and on future contribution and profits from this department.。

HND SQA 财政预算outcome3 答案

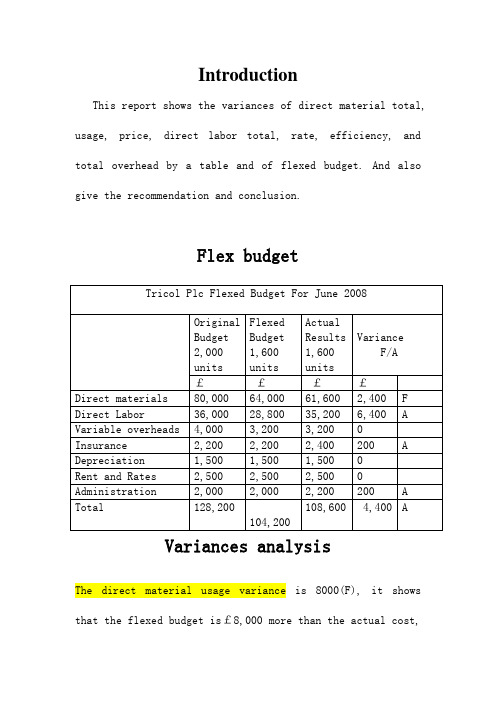

IntroductionThis report shows the variances of direct material total, usage, price, direct labor total, rate, efficiency, and total overhead by a table and of flexed budget. And also give the recommendation and conclusion.Flex budgetVariances analysisThe direct material usage variance is 8000(F), it shows that the flexed budget is£8,000 more than the actual cost,as a result of the using of higher-grade materials and changing of the way of production.The direct material price variance is 5600(A), which means that the actual price is£5600 more than the flexed budget price, because of the Tricol PLC had changed their supplier and purchase the higher-grade material lead to the price raised from £10 per/kg to£11 per/kg.The direct material total = direct material usage – direct material price.As calculated above, 8000-5600=2400, the direct material total variance is£2400.The direct labor rate variance is 3520(A), which means that the actual labor rate is£3520 more than the flexed budget, caused by the company supplied a higher-than-expected wage, the labor cost raised from£9 per hour to£10 per hour, and may because Some employees still apprentices, with poor efficiency.The direct labor efficiency variance is 2880(A), as to say, the actual labor efficiency is£2880 more than flexedbudget efficiency.It may be because the machine on the production line equipment getting old and it influence the efficiency of employees at the time of production, or maybe the culture of the company is not so well at current time, which result in reduced efficiency.The direct labor total variance is 6400(A) caused by the labor rate variance and efficiency variance. It shows that the actual total labor is £6400 more than the flexed budget total labor.The total overhead variance is 400(A) that means the actual total overhead is £400 more than flexed budget, which caused by the changing of administration overhead and insurance cost both. These two things may change by the company change the salary of the management, and they may add extra insurances for the employees or the machinery.ConclusionThere is a policy of the company in which the company applies a rate of significance of 3% for any Variance analysis. According to the data above, we can clearly seethat all the actual variances are higher than 3%, it may caused by the actual production for June was 80% of the target amount, and there are some respects had been changed in the factory.RecommendationI’d give some advices to Tricol Plc for improving their business.●To improve the efficiency not only by increase thesalary but also change the way of production.●The company may discuss with the new supplier to lowerraw material prices.●Training a group of experienced staff.Appendix1. Direct material total variance(Standard units of actual production *standard price) - (actual quantity* actual price)10*4*1600- 61600=2,400(F) 2400/64000=3.75%2. Direct material usage varianceStandard price*(standard units of actual production –actual units)10*(4*1600-5600) =8,000(F) 8000/64000=12.5%3. Direct material price varianceActual quantity *(standard price –actual price)5600*(10-11) =5,600(A) 5600/64000=8.75%4. Direct labor total variance(Standard hours of actual production*standard rate ph) –(actual hours*actual rate ph)2*1600*9-35,200=6400(A) 6400/28800=22.22%5. Direct labor efficiency varianceStandard rate ph*(standard hours of actual production- actual hours)9*(1,600*2-3,520) =2880(A) 2880/28800=10%6. Direct labor rate varianceActual hours*(standard rate ph-actual rate ph)3520*(9-10) =3,520(A) 3520/28800= 12.22%7. Total overhead varianceTotal standard overhead for actual production- total actual overheads(1600*2-3,200) - (8,200-8,600) =400(A) 400/ (3200+8200) =3.51 %。

SQA HND留学项目介绍

山东育路网SQA HND留学项目介绍近年来,越来越多的人喜欢出国留学,很多家长更倾向于让孩子选择SQA HND项目,但是SQA HND 项目到底是什么呢?下面山东育路小编就来为大家介绍一下:什么是HND?HND是英文Higher National Diploma的简称,中文解释为英国高等教育文凭,相当于英国大学二年级毕业的水平。

该课程凭借高质量的课程体系、先进的教学理念、灵活而又严格的教学管理体系,享誉全球。

学生在完成学业后,得到的将是具有国际水准的、普遍承认(不包括中国)的学历文凭,相当于完成了英国大学二年级的课程(英国大学本科学制为三年),学生可以申请进入英国大学攻读最后一年,完成课程后,学生可以获得其就读大学的学士学位,同时可以申请硕士学位相关课程。

关于SQA HNDSQA HND是由英国苏格兰学历管理委员会(又称苏格兰资格监管局,简称SQA)颁发的英国高等教育文凭(Higher National Diploma,简称HND)。

苏格兰政府拥有15所大学,其证书得到苏格兰政府的认可。

国内项目院校是办学和实施教学管理的主体;英国苏格兰学历管理委员会( SQA )负责质量监管和文凭颁发;中国劳动和社会保障部职业技能鉴定中心(OSTA)负责国家职业资格证书颁发;北京英伦育才教育培训中心作为SQA授权机构,主要为项目院校提供相关服务,包括引进项目,整合资源,协调运作等;国外合作院校负责录取毕业生到国外继续学习;用人单位负责毕业生的就业指导。

SQA HND项目引进情况为合理有效地引进国外优质教育资源,培养我国社会发展所需技能型应用型紧缺人才,在教育部有关司局和研究机构的指导和有关省、市教育厅密切配合下,教育部留学服务中心与英国苏格兰资格监管局( Scottish Qualifications Authority ,简称SQA )举行了多次磋商,于2003 年11 月25 日正式与其签定了合作备忘录,正式引进并推广该监管局开发的英国高等教育文凭课程( Higher National Diploma ,简称HND ),通称SQA HND 课程。

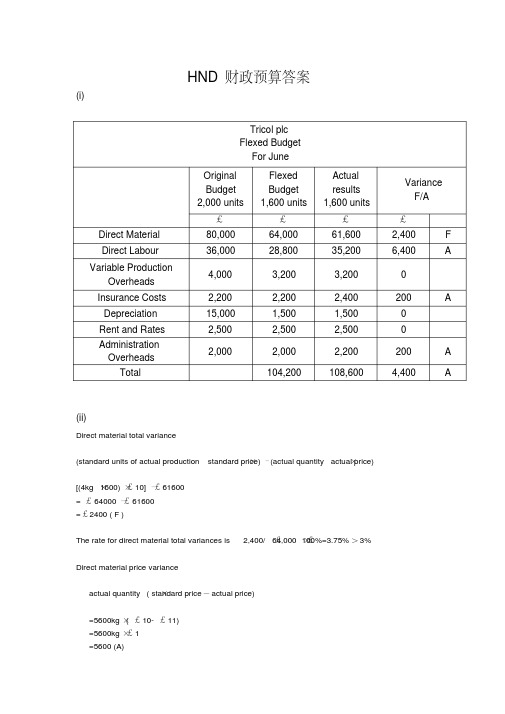

HND财政预算答案

HND 财政预算答案(i)(ii)Direct material total variance (standard units of actual production ×standard price) – (actual quantity ×actual price) [(4kg ×1600)×£10] –£61600 = £64000 –£61600 =£2400 ( F )The rate for direct material total variances is £ 2,400/£ 64,000×100%=3.75%>3%Direct material price varianceactual quantity ×( standard price -actual price) =5600kg ×( £10- £11) =5600kg ×£1 =5600 (A)Tricol plc Flexed Budget For JuneOriginal Budget 2,000 unitsFlexed Budget 1,600 unitsActual results 1,600 unitsVariance F/A ££££Direct Material 80,000 64,000 61,600 2,400 F Direct Labour 36,000 28,800 35,200 6,400 AVariable ProductionOverheads 4,000 3,200 3,200 0 Insurance Costs 2,200 2,200 2,400 200 A Depreciation 15,000 1,500 1,500 0 Rent and Rates 2,500 2,500 2,500 0 Administration Overheads2,0002,000 2,200 200 A Total104,200108,6004,400A100%=8.75%>3%64,000×5,600/£The rate of direct material price variance is £Direct material usage variancestandard price×(standard units of actual production-actual units)=£10×(4kg×1600-5600kg)=£10×800kg=£8000 (F)100%=12.5%>3%64,000×8,000/£The rate of direct material usage variance is £Note: When adding the price and usage variances the result must equal the total variance. Therefore, £5600(A) (price)+£8000(F) (usage) = £2400(F) (total).Direct labour total varianceactual ( standard hours of actual production×standard rate ph) -(actual hours×rate ph)[(2h×1600)×£9] -(3520h×£10)=(3200h×£9)-£35200=£28800 -£35200=£6400(A)100%=22.2%>3%The rate of diretc labour variance is 6400/28800×Direct labour rate variance( standard rate ph-actual rate ph)actual hours×3520h×(£9-£10)=3520h×£1=£3520(A)28,800×100%=12.2%>3%3,520/£The rate of direct labour rate variance is £Direct labour efficiency variance( standard hours of actual production-standard rate ph ×actual hours)£9×[2h×1600-3520h]=£9×(3200h-3520h)=£9×320h=£2880(A)28,000×100%=10%>3%2,880/£The rate of direct labour efficiency variance is £Note: When adding rate and efficiency variances the result must equal the total variance. Therefore, £3520(A) (rate)+£2880(A) (efficiency) = £6400(A) (total).Overhead total variance(standard insurance cost-actual insurance cost)+(standard administrationoverheads-actual administration overheads)(£2200-£2400)+(£2000-£2200)=£200(A)+£200(A)=£400(A)100%=9.52%>3%4,200×400/£The rate of overhead total variance is £(iii)AnalysisMaterial varianceFrom the actual budget, we can see that the direct material total variance is £2,400(F). The Direct material usage variance is £8,000 (F),the Direct material price variance is £(5,600)(A).The possible reasons for material usage variances are include:Use new machinery.Use higher qualityThe possible reasons for material price variance:Change suppliers.Use higher quality material.Loss of discountLabour varianceThe direct labour total variance is £(6,400) (A) ,the Direct labour efficiency variance is £(2,880) (A) and the Direct labour rate variance is£(6,400) (A).The possible reason for direct labour efficiency variance:Lower grade workforceShortage of skilled laborThe possible reason for direct labour rate varianceHigher grade workforcesShortage of skilled labourOverhead varianceThe total overhead variance is £(400)(A). The Insurance and Administration variances are £(200)(A). The total overhead variance is £(400)(A).The possible reasons for overhead variances:Using new machineryIncreased administration costTo conclude a higher-than-expected wage settlement for production operates.Difficult trading conditionsIntensely competitionRecommendationAccording to above analysis, we can easily understand the organization’s current situation. In order to achieve the lower costs and high profit here some recommendations divided in three sections which in clued material variances, labour variances as well as the overhead variances.The recommendation for material variances:Investigate the cheaper material.Hold a staff training program to increase their work efficiency.Negotiate with current supplier in order to achieve lower price.The recommendation for labour variances:Provide training program to staff for higher skill of operating the new material.Consider about the lower grade labourThe recommendation for overhead variances:try to decrease the administration costTeach the staffs scientifically use these overhead in order to make it longer-used.Part BPayback period method:Year Anuual cash flow Cumulative0 (1,000,000) (1,000,000)1 160,000 (840,000)2 160,000 (680,000)3 320,000 (360,000)4 320,000 (40,000)5(1/8 of 320,000) 40,000 NIL5(7/8 of 320,000) 280,000 240,000Payback will take 4 year 1.5months.Net present ValueAnnual Cash Flow Present ValueFactorsat 10%Present Value££££Year 0 (1,000,000) 1.000 (1,000,000)1 160,000 0.909 145,4402 160,000 0.826 132,1603 320,000 0.751 240,3204 320,000 0.683 218,5605 320,000 0.621 198,720 935,200Net PresentValue£(64,800)The premise of payback period methodsIdentify all of the costs of initial investment. Assume that they will be paid now. Find the cash inflow for each project. Add up cash flows each year until cost of project covered. Pick the project with the shortest payback period. If the payback period is only one year then it should be compared with an internal figureThe premise of discounted cash flow techniqueUncertainty does not exist. There is no inflation. The appropriate discount rate to use is known, to avoid unnecessary c alculations. When undertaking DCF questions, the discount rates have been computed for you, and are given in the discount tables .Unlimited funds can be raised at a competitive rate.Analyzing payback period methodAccording to the payback period method, the original capital that the company invest is £1,000,000 and there are 5 years for the company to get the return that is the budgeted payback period. According to the program, 4 years and 1.5 months that the company will get its all investments. At the last year, company will get the return about £280,000. As a result, based on the period method, the project will be profitable and is worth to invest.Analyzing discounted cash flow techniqueIf the company uses the discounted cash flow technique, according to the peogram,the investment is £1,000,000, and the net present value is 10%. The budgeted payback period is 5 years. After 5 years, the NPV for the project will be £-64,800. It shows that the return is less than the investment. It will be the loss of £64,800 to invest this project. So this project will not be profitable and is not worth to invest.RecommendationAccording to the two methods, it is not difficult to find that the company would betterto choose the payback period method. The company chooses payback period method could get the profit of £280,000 and less 5 years could get the all investment. And for the discounted cash flow technique, it will cost 5 years and loss £64,800 at lastof the project. So, based on the profit, the company would better to choose the payback period method.Consideration of other factorsFirst, the environment is one factor that the managers should to consider. Tricol makes a range of furniture and kitchenware. It may make pollute during the producing. If the company does not pay attention to the environment, it may get some fine.Technology is one factor that the managers should to consider about. If the company uses the new technology and equipment in the project, it could improve its productivity. And improve its profitability.The company should also think about the legal. The company should insure that the project is not against the legal. If not, company may be punished by the government and even be banded.At last, company should consider its customers. It should consider that its products, making by the project, will be attracted by the customers. If no customers like it, they may get little profit for the project.ConclusionAs an advisor for the company, this report can help the company make the flex budget and variances and use the two methods to analysis the investment and help the company choose the best method. This will help company make much profit.。

财政预算Outcome3 and 4

£8000 £52790

0 £255

F

Material Variance

• Three Variance (see P192 for formulas): 1. Direct Material TOTAL Variance 2. Direct Material USAGE Variance 3. Direct Material PRICE Variance

Direct material (£)

Direct labour (£) Variable Overheads Fixed Overheads

Production Cost

Variance

What does variance mean? • A variance is the difference between actual and budgeted cost. • Types of variance

Name

Favorable Variance (F) Adverse Variance (A)

Meaning

Result from actual activity is better than budgeted Result from actual activity is worse than budgeted

3. Direct Labour EFFICIENTY Variance 每小时人工工资率预算数×(实际产量需耗用 的预算小时数-实际生产耗用小时数)

Overheads Variances (P203)

Total Overhead Variance = Total Standard Overheads for actual production-Total Actual Overheads 实际生产发生制造费用的预算数-实际生产 发生制造费用的实际数

HND财政预算 preparing financial forecasts

Report aboutPreparing Financial ForecastsOutcome 3&4Unit code: DE3J 35Unit title: Preparing Financial Forecasts Candidate’s Name: Hu HanchangScottish Candidate Number: 115517880 Instructor:Zhang JiaDate: 23th12 2011contents1.0 Introduction (3)2.0 Main Bodies (3)Part A (3)2.1 Tricol Plc Flexed budged (3)2.2 The calculation of the variances (3)2.3 Variance analysis and recommendations (3)2.3.1 Direct material total variance and recommendations (3)2.3.2 Direct material usage variance (4)2.3.3 Direct material price variance (4)2.3.4 Direct labour total variance (5)2.3.5 Direct labour efficiency variance (5)2.3.6 Direct labour rate variance (6)2.3.7 Total Overhead variance (6)Part B (7)2.4 Analysis of two investment appraisal technique (7)2.4.1 Calculation of net present value and features of NPV (7)2.4.2 Calculation of the payback period method (8)2.4.3 Recommendations for investment decision (9)2.5 Other non-financial factors (9)3.0 Conclusion (10)4.0 Reference (10)5.0 Appendix (11)1.0 IntroductionThe report about Tricol plc which is main containing two parts: Part A and Part B.In Part A, this report will give the Flex the budget figures with actual activity and analysis variances, furthermore the report will give some recommendations to management. In Part B, the report will application of two investment appraisal techniques to evaluation the financial viability of Tricol plc and give recommendations.2.0 Main BodiesPart A2.1 Tricol Plc Flexed budgedFor Flex budged of Tricol plc, we can see the Appendix 12.2 The calculation of the variancesThis section shows the Appendix 2.2.3 Variance analysis and recommendationsIn this part, we need considerate that the company policy need to analyses the variance is more than a rate of significance of 3%, on the other hand, difficult trading conditions, actual production of June was 80% of the target amount.2.3.1 Direct material total variance and recommendationsDirect material total variance is favourable.The reasons of variance, recently, the company has introduced the production machinery, due to the employees who can not expertly operate the new machinery to produce which leads to the material usage variance is increase to 8000F. In addition,The Company has switched suppliers currently; it is using the higher-grade material now, as the result of issue, the material price must raise from original £10 per kg to £11 per kg, which leads to the material price variance is 5600A. Further direct material total variance is 2400F.Recommendations:The actual activity is over the Flex the budget, due to the company uses thehigher-grade material. We suggest that the company can use the lower grade quality materials to shrink the variance; in addition, the company can hire the higher grade workforce to expertly operation the new machine, and then shrink the variance.2.3.2 Direct material usage varianceDirect material usage variance is favourable.The reasons of it, the company has switched suppliers currently, the material is higher quality, which can produce substantial products than lower material, and then the average usage of direct material is low. Moreover, the company has updated machines; it can produce to the higher quality of products, and then reduce the amount of rejected products. Finally the material usage variance is 8000F.Recommendations: the rate of direct material usage variance is12.5%, it is more than 3%. So we should consideration that reduces the variance, if the company has decided to use the higher-grade material to production, we suggest that the company should intensify the performance monitor for staff because the lower performance will accelerate waste of material and then lead to the material usage is increase, the performance monitor can help the company shrink the variance.2.3.3 Direct material price varianceDirect material price variance is adverseThe reasons of variance, the company has switched suppliers currently, it is using thehigher-grade material now, as the result of issue, the material price must raise from original £10 per kg to £11 per kg. In addition, the loss of discount, also can effect the material price variance.Recommendations: The company can turn to others suppliers who can help you reduce the cost of material. On the other hand, the company can negotiation with suppliers to gain the lower discount also can shrink the variance.2.3.4 Direct labour total varianceDirect labour total variance is adverseThe reasons of variance, the company has introduced the new machine, however, the employees who inexpertly operate the new machinery to produce, as the result, the actual labor hours is over the budget, the hours changes from 3200 hours to 3520 hours. As the result the direct labor efficiency variance is adverse which is 2880 A. In addition, the company has recently concluded a higher-than-expected wage settlement for production operations. As the result of that, the labour rate is higher than standard labour rate from £9 per hour to £10 per hour. As the result of it, the direct labour rate variance is adverseness for this firm which is 3520A. Finally, lead to the labour total variance is adverse, which is 6400.Recommendations:The company can provide training to enhance the staff’s skill, in addition, it can hire the higher-grade employee to improve the efficiency.2.3.5 Direct labour efficiency varianceDirect labour efficiency variance is adverseReasons of it, maybe low incentive, the staff need continuously motivation who can improve the efficiency. In addition, the company maybe hire lower-grade workforce to produce, it has negative impact of efficiency.Recommendations:Because the company has upgraded the production machine, as the result the staff only gains the new skills, furthermore the company can provide some trainings of high quality to staff. In addition, the company can hire the higher-grade workforce to reduce the shrink variance.2.3.6 Direct labour rate varianceDirect labour rate variance is adverseReasons of it, the firm has recently concluded a higher-than-expected wage settlement for production operations. As the result of that, the labour rate is higher than standard labour rate from £9 per hour to £10 per hour. As the result of it, the cost of direct labour is adverseness for this firm.Recommendations:This company can hire some lower grade workforce, and then can pay a lower salary. Moreover, the company can provide some motivation policies to motivate the staff that is work hard and enhance the work enthusiastic of the staff.2.3.7 Total Overhead varianceTotal Overhead variance is adverseThe reasons of it, due to the company using the higher-grade material, it maybe lead to the administration overhead is increase such as the company needs hire the expensive transport charges to transport the higher-grade material, as the result the administration overhead is increase to 2200. In addition, the company has upgraded the machinery; it leads to the insurance cost is increase by 200; finally the total overhead variance is adverse which is 400A.Recommendations: we suggest that the company use the low-grade material and training staff to shrink the variance.Part B2.4 Analysis of two investment appraisal techniqueIn this part, the report will use net present value and the payback period method to describe, in addition, making some assumptions to analysis.The assumption as follows:Within five years. All the market factors are stably. There is no change in exchange rate. And the report is taking no account of the inflation and deflation. In addition, taxation can be excluded by government. Moreover, there is no other income or expenditure in the investment projects. Furthermore, unlimited funds can be provided during the developing.2.4.1 Calculation of net present value and features of NPVIt is showed by Appendix 3.Net Present ValueThe NPV method calculates the present values of cash inflows and outflows and establishes whether, in total, the present value of cash inflows is greater than the present value of cash outflows.Advantages of NPV as follows:Basically, NPV provides an objective for evaluating and selecting investment projects. Moreover, it takes into account required rate of return of company and then takes into account time value of money. In addition, it focuses on cash inflows and outflow rather on accounting profits. Also it takes account of both magnitude and timing of expected cash inflows in each period of a project's life.Disadvantages of NPV:Firstly, there are substantial uncertainly factors in our world. For instance the inflationand deflation, the exchange rate, if they have a little change then the cash flow is uncertainly. In addition, the concept is difficult for the layman to grasp. On the other hand, assumes that we can borrow as required and at a competitive rate of interest. Also, the cost of capital used to calculate the discount factor is usually hard to forecast.2.4.2 Calculation of the payback period methodIt is showed by Appendix 4.Payback periodGenerally speaking, It is mostly popular techniques. Further, the number of years is the measures method. And then it is expected to be taken to recover the cost of the original investment.Advantages of it as follows:It is known to all that Payback period was considered easy to operate and understand. Indeed, as a measure to compare the profitability of the project, and it is use of cash flow rather than accounting profit which is a more objective basis. In addition, it is believed that the investment recovery period is short, low-risk projects. Furthermore, in short-term, this way can reduce the risk of loss through the obsolescence. Beside these, it useful as a measure of liquidity, a more direct return of cash is preferred.Disadvantages of it:Initial, it ignored risk and time value of money, further it ignores cash flows after initial outflow has been met. In addition, it is ignoring the fact that benefit from different projects may accrue at uneven rate. There is no allowance for interest and the initial capital investment2.4.3 Recommendations for investment decisionSome recommendations for the company:As leader, the actual profit is indispensable for them who should consider the value of the time rather than they can use a single formula to calculate the rate of return.In my opinion, Payback period will take four years and one-and-half month to return the investment capital, It is slowly growing and can return, if the leader decisions long-term investment, I think that it is reasonable to accept this project.Nonetheless, by calculates the net present values, it seems that the deficit, which means that the annual cash flows are not enough to allow more interest to be deducted and still repay the original investment. This investment is unworthy while as it less than 10% return. This is because too much interest has been deducted to allow all the capital to be repaid. If consideration the method, I suggest that the company can reject this project.2.5 Other non-financial factorsAs the leaders, they need consideration the whole factors such as non-financial factors to make decision as follows:For Technological factors, it is mostly importance to company because it is changing rapidly; the company purchases these products whether they can meet the organization development in the future.For government, whether government supports are produced or use these products.For environment, and the products have effect for environment, such as carbon dioxide, it will lead to the global warming, as the company, it has responsibility for communities.In addition, the human resource factors, whether the company need hire the new staff to achievement the organization’s goals.3.0 ConclusionThe report can help the company make the flex budget, and then by variances analysis and use the two methods to analysis the investment, further it can help the company choose the best investment to gain the maximum profits.4.0 ReferenceBooks:SQA Unit Student Guide (2005): DG6M 34-International Marketing: An Introduction, China Modern Economic Publishing House.Appendix 1Tricol Plc Flexed budgedDue to difficult trading conditions, actual production of June was 80% of the target amount. We can get next chart:The calculation of the variances and the variance rateDirect material total variance(Standard units of actual production × standard price) – (actual quantity ×actual price) [(4kg×1600)×£10] –£61600= £64000 –£61600=£2400 ( F )The rate for direct material total variances is £ 2,400/£ 64,000×100%=3.75%Direct material usage varianceStandard price× (standard units of actual production-actual units)£10×(4kg×1600-5600kg)=£10×800kg=£8000 (F)The rate of direct material usage variance is £ 8,000/£ 64,000×100%=12.5%Direct material price varianceActual quantity×( standard price-actual price)5600kg×( £10 - £11)=5600kg×£1=5600 (A)The rate of direct material price variance is £ 5,600/£ 64,000×100%=8.75%Note: When adding the price and usage variances equal the total variance. Therefore, £5600(A) (price)+£8000(F) (usage) = £2400(F) (total).Direct labour total variance( Standard hours of actual production × standard rate ph) -(actual hours × actual rate ph)[(2h×1600)×£9] -(3520h×£10)=(3200h×£9)-£35200=£28800 -£35200=£6400(A)The rate of direct labor variance is 6400/28800×100%=22.2%Direct labour efficiency varianceStandard rate ph ×( standard hours of actual production-actual hours)£9×[2h×1600-3520h]=£9×(3200h-3520h)=£9×320h=£2880(A)The rate of direct labors efficiency variance is £ 2,880/£ 28,000×100%=10%Direct labour rate varianceActual hours×( standard rate ph-actual rate ph)3520h×(£9-£10)=3520h×£1=£3520(A)The rate of direct labors rate variance is £ 3,520/£ 28,800×100%=12.2%Note: When adding rate and efficiency variances equal the total variance. Therefore, £3520(A) (rate)+£2880(A) (efficiency) = £6400(A) (total).Total Overhead variance(Standard insurance cost-actual insurance cost)+(standard administration overheads -actual administration overheads)(£2200-£2400)+(£2000-£2200)=£200(A)+£200(A)=£400(A)The rate of overhead total variance is £ 400/£ 4,200×100%=9.52%Appendix 3Calculation of net present value at 10%Appendix 4Payback period method:In 5 Year, the cash inflows for the full year are £320,000 but only £40,000 is return the initial investment. Payback= 40000/320000*Year = 1/8 Year = 1.5months Payback will take 4 year 1.5months.。

HND-财政预算OUTCOME-34报告--你不过我从此消失!.doc

HND-财政预算OUTCOME-34报告--你不过我从此消失!A financial analysis report for Tricol plcOutcome 3and4Class;10E6Name:Ma bodaSCN:125099297Candidate Num:22IntroductionTo operate better in financial aspect, the management of Tricol plc asked me to analyze their financial condition then make recommendations for them.FindingsPart A(ⅰ) Flex budget in line with actual activityTricol plc Flexed Budget for JuneOriginal budget FlexedbudgetActualresultsVariance2000 units 1600 units 1600unitsF/A££££Direct material 80,000 64,000 61,600 2,400 F Direct labor 36,000 28,800 35,200 6,400 A Variable production overhead 4,000 3,200 3,200 0 Fixed costDepreciation 1,500 1,500 1,500 0 Rent and rates 2,500 2,500 2,500 0 Administration overhead 2,000 2,000 2,200 200 A Insurance costs 2,200 2,200 2,400 200 A Total 128,200 104,200 108,600 4,400 A (ⅱ) Variances calculationDirect material total variance(Standard units of actual production*standard price) -(actual quantity*actual price)(4 kg*1,600*£10) -£61,600 =£2,400 (F)Rate of significance: (3.75%)Direct material usage varianceStandard price*(standard units of actual production -actual quantity)£10*[ (4kgⅹ1,600) -5,600kg]= £8,000 (F)Rate of significance (12.5%)Direct material price varianceActual quantity * (standard price -actual price)5,600kg*[£10 -(£61,600/ 5,600kg) ]= £(5,600) (A)Rate of significance: (8.75%)Direct labour total variance(Standard hours of actual production*standard rate ph) - (actual hours*actual rate ph)[ (2hrs*1,600) *£9]-£35,200=£(6,400) (A)Rate of significance: (22.22%)Direct labour efficiency varianceStandard rate ph* (standard hours of actual production -actual hours)£9*(2hrs*1,600-3,520hrs)=(2,880) (A)Rate of significance: (10%)Direct labour rate varianceActual hours*(standard rate ph – actual rate ph)3,520hrs*(£9*-£35,200/3,520hrs)= £(3,520) (A)Rate of significance: (12.22%)Total overhead varianceTotal standard overhead for actual production -total actual overheads (£18,000/12+£2,500+£2,200+£2,000)- (£1,500+£2,500+£2,200+£2,400)=£(400) (A)Rate of significance: (3.5%)(ⅲ) Report about variances✧Direct material varianceThe direct material total variance can be analyzed in two aspects which are direct material volume and direct material price.For volume side, as calculated above, the budget volume is 6400kg; the actual volume is 5600kg. So there is 800kg variance which is favorable and each unit variance is 0.5kg. The likely reason causing the variance comes from three aspects. First of all, the company upgraded the production machinery recently, and new machine may use materials efficiently, so it reduced the waste of materials. Secondly, the company switched suppliers and using higher-grade materials can decrease waste of materials too. Finally, the company has concluded a higher-than-expected wage settlement for production operatives, which will maintain employees with higher skills as well as decrease turnover of employees, and it also can increase efficiency in using materials.For price aspect, the budget price is £10 per kg, and the actual price is £11per kg, it is adverse that one pound over the budget price. The company switching suppliers may cause the increase of negotiation cost. There may be a long-term relationship between Tricol plc and its old suppliers, so the suppliers may take lots of discounts to the firm. After changing suppliers, the discount may disappear. Furthermore, higher grade materials increased unit price.Overall, the total material variance is favorable. £8,000 -£5,600=£2,400.✧Direct labour varianceThe direct labour total variance is composed of direct labour efficiency variance and direct labour rate variance.The budget direct labour hours are 3,200hrs and the actual labour hours are3,520 hrs. There are more 320hrs needed than the budget, and each unit is 0.2hrs, which it is obviously adverse. The company upgrading the production machinery may need time for employees to adopt it. Also, employees need training time. The rebuild process of machinery consumed time too. In a word, the chargeable hours have increased.The budget direct laour hours rate is £9 per hour, the actual hours rate is £10 per hour. It is adverse that one pound higher than budgeted. It is possible caused by both internal and external factors. Higher-than-expected wage settlement may be internal reason for the variance, and new machinery may be needed to recruit new employees to operate the machinery, which also can increase the expense. For external factors, the changing of labour market may increase labour cost; the government legislation also can increase the labour cost, for example minimum pay.Both direct labour efficiency and direct labour rate variances are adverse, so the direct labour total variance is adverse.Overhead varianceAs calculated above, total overhead variance is caused by administration and insurance. Each factor has £200 variance, so the total overhead variance is £400 and it is adverse. During the process of changing supplier, the company needed more expense on public relationship or negotiation, in addition, in order to maintain the new machinery, administration cost will be increased too. For insurance aside, the improvement of machinery will need more insurance fees tocover, which also contributes to the increase of insurance fee of new employees.Part BSelection and application of two investment appraisal techniquesAs the company is keen to recoup the cost of the investment within five years, I will choose Payback period and Net Present Value to help me complete the appraisal.In order to fulfill the appraisal easily, there are some assumptions listed below should be considered before the appraisal.⑴ All revenue and inflow are assumed cash flow⑵ All investment cost incurred in year 0⑶ No uncertainty is considered⑷ Do not consider inflation and taxation⑸ Market rate of return is expected rate of return⑹ Rate of return is varying along with timeTricol plc Payback period for project distribution armYear Net cash flow Cumulative Cash Flow££Cash Flow Year 0 (1,000,000) (1,000,000) Cash Inflow Year 1 160,000 (840,000)Year 2 160,000 (680,000)Year 3 320,000 (360,000)Year 4 320,000 (40,000)Year 5 320,000 280,000 Net Cash Benefit Year 5 280.000 Note: req uire 40,000/320,000 in year 5= 1/8*year=1.5 mothsPayback=4 years 1.5 mothsTricol plc Net Present Value for project distribution armPresent Value Annual cash flow Present valuefactors at 10%£££Year 0 (1,000,000) 1.000 (1,000,000) Year 1 160,000 0.909 145,440Year 2 160,000 0.826 132,160Year 3 320,000 0.751 240,320Year 4 320,000 0.683 218,560Year 5 320,000 0.621 198,720 935,200 NPV (64,800)Recommendation about investmentAccording to Payback Period analysis, the investment cost can be recouped in year 4 and 1.5 moths. In other words, the period is under company’s expectation. The project can be executed. However, according to Net Present Value analysis, in terms of present value, within five years, what the NPV will bring net result is net cash loss but not net cash surplus. In general, the company should consider time value and other factors, so the project should not be executed.◆Factors impact on the investment should be consideredVarious factors will impact on result of investment. I will outline factors should be considered when the management reviewing my recommendation in financial and non-financial factors.✧Financial factorAs distribution arm is financial long-term beneficial project, it can be used inlong-term period and bring benefits continuous. The investment cost is£1,000,000, which can be considered a large investment. So it more likely needs long period payback period. The management should focus on longer cash flows for longer period of future. On the other hand, Net Present Value in year five is (28,000) only take 2.8% percents of the investment cost, it is more likely surplus in year six. Another financial factor is source of million pounds. If it is internal source, the management mainly concentrate on opportunities cost. If it is cost of capital or cost of capital taking much weight of the source, the management must pay cost of the source firstly, the marketing rate of return likely low for the company, in addition, the management should use higher discounted cash flow.✧Non-financial factorThe investment must be consistence with company’s strategic plan. As Tricol is a plc, it must take social responsibility such as obeying government policy, minimizing impact on environment and minimizing impact on natives.ConclusionFor real competition is more complex and fierce, in order to make accuratedecisions, management should consider more factors during the decision-making; furthermore, the management should use more tools to help them such as IRR, DCF.。

上海财大SQAHND项目:七成毕业生英国读硕士

上海财大SQAHND项目:七成毕业生英国读硕士近日,记者从上海财经大学国际教育学院获悉,开办英国高等教育文凭项目(SQA HND)至今,出国深造的本科毕业生中,七成以上已就读或申请英国的硕士研究生。

虽然这些学生当年高考成绩并不十分理想,但通过HND这条留学“绿色通道”,他们不仅比昔日的同窗提前两年取得硕士文凭,而且比直接店铺至少节省了40万元。

今年,“受益”于金融危机,既经济又稳妥的“国内留学”项目HND受到考生和家长的格外青睐,在上财大国际教育学院,甚至有考生高考刚结束就跑来“占座”。

现场:金融危机促“经济型”留学升温“HND项目在国内一年的学费才2万多元,仅相当于国外学费的十分之一,甚至不及国内民办高校的收费,而学生却可以拿到英国高等教育文凭,之后到英国几十所合作高校深造,一年就可以拿到本科学历,两年就可以拿到硕士学位。

即使不出国,凭借过硬的技能、纯正的外语和国家职业资格证书,也不用为找工作发愁。