国际会计复习资料中英结合版

《最新国际会计科目中英文对照》(2013.9)

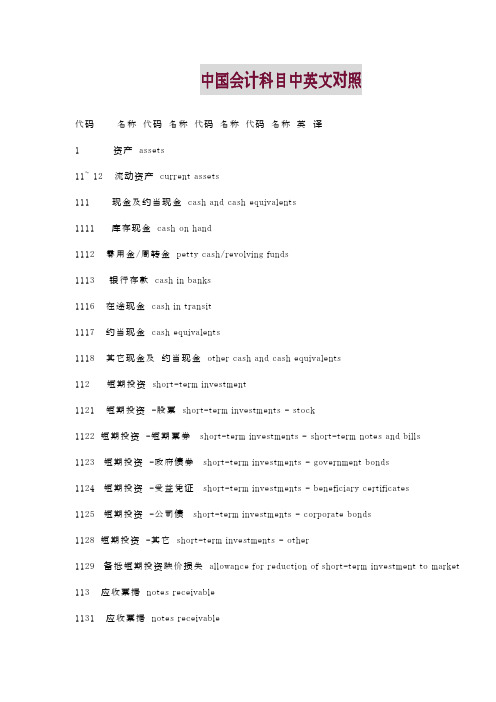

中国会计科目中英文对照代码名称代码名称代码名称代码名称英译1 资产assets11~ 12 流动资产current assets111 现金及约当现金cash and cash equivalents1111 库存现金cash on hand1112 零用金/周转金petty cash/revolving funds1113 银行存款cash in banks1116 在途现金cash in transit1117 约当现金cash equivalents1118 其它现金及约当现金other cash and cash equivalents112 短期投资short-term investment1121 短期投资-股票short-term investments - stock1122 短期投资-短期票券short-term investments - short-term notes and bills1123 短期投资-政府债券short-term investments - government bonds1124 短期投资-受益凭证short-term investments - beneficiary certificates1125 短期投资-公司债short-term investments - corporate bonds1128 短期投资-其它short-term investments - other1129 备抵短期投资跌价损失allowance for reduction of short-term investment to market 113 应收票据notes receivable1131 应收票据notes receivable1132 应收票据贴现discounted notes receivable1137 应收票据-关系人notes receivable - related parties1138 其它应收票据other notes receivable1139 备抵呆帐-应收票据allowance for uncollec- tible accounts- notes receivable114 应收帐款accounts receivable1141 应收帐款accounts receivable1142 应收分期帐款installment accounts receivable1147 应收帐款-关系人accounts receivable - related parties1149 备抵呆帐-应收帐款allowance for uncollec- tible accounts - accounts receivable 118 其它应收款other receivables1181 应收出售远汇款forward exchange contract receivable1182 应收远汇款-外币forward exchange contract receivable - foreign currencies1183 买卖远汇折价discount on forward ex-change contract1184 应收收益earned revenue receivable1185 应收退税款income tax refund receivable1187 其它应收款- 关系人other receivables - related parties1188 其它应收款- 其它other receivables - other1189 备抵呆帐- 其它应收款allowance for uncollec- tible accounts - other receivables 121~122 存货inventories1211 商品存货merchandise inventory1212 寄销商品consigned goods1213 在途商品goods in transit1219 备抵存货跌价损失allowance for reduction of inventory to market1221 制成品finished goods1222 寄销制成品consigned finished goods1223 副产品by-products1224 在制品work in process1225 委外加工work in process - outsourced1226 原料raw materials1227 物料supplies1228 在途原物料materials and supplies in transit1229 备抵存货跌价损失allowance for reduction of inventory to market 125 预付费用prepaid expenses1251 预付薪资prepaid payroll1252 预付租金prepaid rents1253 预付保险费prepaid insurance1254 用品盘存office supplies1255 预付所得税prepaid income tax1258 其它预付费用other prepaid expenses126 预付款项prepayments1261 预付货款prepayment for purchases1268 其它预付款项other prepayments128~129 其它流动资产other current assets1281 进项税额VAT paid ( or input tax)1282 留抵税额excess VAT paid (or overpaid VAT)1283 暂付款temporary payments1284 代付款payment on behalf of others1285 员工借支advances to employees1286 存出保证金refundable deposits1287 受限制存款certificate of deposit-restricted1291 递延所得税资产deferred income tax assets1292 递延兑换损失deferred foreign exchange losses1293 业主(股东)往来owners'(stockholders') current account1294 同业往来current account with others1298 其它流动资产-其它other current assets - other13 基金及长期投资funds and long-term investments131 基金funds1311 偿债基金redemption fund (or sinking fund)1312 改良及扩充基金fund for improvement and expansion1313 意外损失准备基金contingency fund1314 退休基金pension fund1318 其它基金other funds132 长期投资long-term investments1321 长期股权投资long-term equity investments1322 长期债券投资long-term bond investments1323 长期不动产投资long-term real estate in-vestments1324 人寿保险现金解约价值cash surrender value of life insurance1328 其它长期投资other long-term investments1329 备抵长期投资跌价损失allowance for excess of cost over market value of long-term investments14~ 15 固定资产property , plant, and equipment141 土地land1411 土地land1418 土地-重估增值land - revaluation increments142 土地改良物land improvements1421 土地改良物land improvements1428 土地改良物-重估增值land improvements - revaluation increments1429 累积折旧-土地改良物accumulated depreciation - land improvements143 房屋及建物buildings1431 房屋及建物buildings1438 房屋及建物-重估增值buildings -revaluation increments1439 累积折旧-房屋及建物accumulated depreciation - buildings144~146 机(器)具及设备machinery and equipment1441 机(器)具machinery1448 机(器)具-重估增值machinery - revaluation increments1449 累积折旧-机(器)具accumulated depreciation - machinery151 租赁资产leased assets1511 租赁资产leased assets1519 累积折旧-租赁资产accumulated depreciation - leased assets152 租赁权益改良leasehold improvements1521 租赁权益改良leasehold improvements1529 累积折旧- 租赁权益改良accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments for equipment 1561 未完工程construction in progress1562 预付购置设备款prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation - miscellaneous property, plant, andequipment16 递耗资产depletable assets161 递耗资产depletable assets1611 天然资源natural resources1618 天然资源-重估增值natural resources -revaluation increments 1619 累积折耗-天然资源accumulated depletion - natural resources 17 无形资产intangible assets171 商标权trademarks1711 商标权trademarks172 专利权patents1721 专利权patents173 特许权franchise1731 特许权franchise174 著作权copyright1741 著作权copyright175 计算机软件computer software1751 计算机软件computer software cost176 商誉goodwill1761 商誉goodwill177 开办费organization costs1771 开办费organization costs178 其它无形资产other intangibles1781 递延退休金成本deferred pension costs1782 租赁权益改良leasehold improvements1788 其它无形资产-其它other intangible assets - other18 其它资产other assets181 递延资产deferred assets1811 债券发行成本deferred bond issuance costs1812 长期预付租金long-term prepaid rent1813 长期预付保险费long-term prepaid insurance1814 递延所得税资产deferred income tax assets1815 预付退休金prepaid pension cost1818 其它递延资产other deferred assets182 闲置资产idle assets1821 闲置资产idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables 1841 长期应收票据long-term notes receivable1842 长期应收帐款long-term accounts receivable1843 催收帐款overdue receivables1847 长期应收票据及款项与催收帐款-关系人long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产assets leased to others1851 出租资产assets leased to others1858 出租资产-重估增值assets leased to others - incremental value from revaluation1859 累积折旧-出租资产accumulated depreciation - assets leased to others 186 存出保证金refundable deposit1861 存出保证金refundable deposits188 杂项资产miscellaneous assets1881 受限制存款certificate of deposit - restricted1888 杂项资产-其它miscellaneous assets - other2 负债liabilities21~ 22 流动负债current liabilities211 短期借款short-term borrowings(debt)2111 银行透支bank overdraft2112 银行借款bank loan2114 短期借款-业主short-term borrowings - owners2115 短期借款-员工short-term borrowings - employees2117 短期借款-关系人short-term borrowings- related parties2118 短期借款-其它short-term borrowings - other212 应付短期票券short-term notes and bills payable2121 应付商业本票commercial paper payable2122 银行承兑汇票bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价discount on short-term notes and bills payable213 应付票据notes payable2131 应付票据notes payable2137 应付票据-关系人notes payable - related parties2138 其它应付票据other notes payable214 应付帐款accounts pay able2141 应付帐款accounts payable2147 应付帐款-关系人accounts payable - related parties216 应付所得税income taxes payable2161 应付所得税income tax payable217 应付费用accrued expenses2171 应付薪工accrued payroll2172 应付租金accrued rent payable2173 应付利息accrued interest payable2174 应付营业税accrued VAT payable2175 应付税捐-其它accrued taxes payable- other2178 其它应付费用other accrued expenses payable218~219 其它应付款other payables2181 应付购入远汇款forward exchange contract payable2182 应付远汇款-外币forward exchange contract payable - foreign currencies 2183 买卖远汇溢价premium on forward exchange contract2184 应付土地房屋款payables on land and building purchased2185 应付设备款Payables on equipment2187 其它应付款-关系人other payables - related parties2191 应付股利dividend payable2192 应付红利bonus payable2193 应付董监事酬劳compensation payable to directors and supervisors2198 其它应付款-其它other payables - other226 预收款项advance receipts2261 预收货款sales revenue received in advance2262 预收收入revenue received in advance2268 其它预收款other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion 2271 一年或一营业周期内到期公司债corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion 228~229 其它流动负债other current liabilities2281 销项税额VAT received(or output tax)2283 暂收款temporary receipts2284 代收款receipts under custody2285 估计售后服务/保固负债estimated warranty liabilities2291 递延所得税负债deferred income tax liabilities2292 递延兑换利益deferred foreign exchange gain2293 业主(股东)往来owners' current account2294 同业往来current account with others2298 其它流动负债-其它other current liabilities - others23 长期负债long-term liabilities231 应付公司债corporate bonds payable2311 应付公司债corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款long-term loans payable2321 长期银行借款long-term loans payable - bank2324 长期借款-业主long-term loans payable - owners2325 长期借款-员工long-term loans payable - employees2327 长期借款-关系人long-term loans payable - related parties2328 长期借款-其它long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据long-term notes payable2332 长期应付帐款long-term accounts pay-able2333 长期应付租赁负债long-term capital lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties 2338 其它长期应付款项other long-term payables234 估计应付土地增值税accrued liabilities for land value increment tax2341 估计应付土地增值税estimated accrued land value incremental tax pay-able235 应计退休金负债accrued pension liabilities2351 应计退休金负债accrued pension liabilities238 其它长期负债other long-term liabilities2388 其它长期负债-其它other long-term liabilities - other28 其它负债other liabilities281 递延负债deferred liabilities2811 递延收入deferred revenue2814 递延所得税负债deferred income tax liabilities2818 其它递延负债other deferred liabilities286 存入保证金deposits received2861 存入保证金guarantee deposit received288 杂项负债miscellaneous liabilities2888 杂项负债-其它miscellaneous liabilities - other3 业主权益owners' equity31 资本capital311 资本(或股本)capital3111 普通股股本capital - common stock3112 特别股股本capital - preferred stock3113 预收股本capital collected in advance3114 待分配股票股利stock dividends to be distributed3115 资本capital32 资本公积additional paid-in capital321 股票溢价paid-in capital in excess of par3211 普通股股票溢价paid-in capital in excess of par- common stock 3212 特别股股票溢价paid-in capital in excess of par- preferred stock 323 资产重估增值准备capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积capital surplus from gain on disposal of assets。

国际会计科目中英文对照

国际会计科目中英文对照Account 帐户Accounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Book keeping 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室Income statement 损益表Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会Statement of cash flow 现金流量表Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系Assets 资产Business entity 企业个体Capital stock 股本Corporation 公司Cost principle 成本原则Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设Inflation 通货膨涨Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量Operating activities 经营活动Owners equity 所有者权益Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设Stockholders 股东Stockholders equity 股东权益Window dressing 门面粉饰财会名词汉英对照表(1)会计与会计理论会计accounting决策人Decision Maker投资人Investor股东Shareholder债权人Creditor财务会计Financial Accounting管理会计Management Accounting成本会计Cost Accounting私业会计Private Accounting公众会计Public Accounting注册会计师CPA Certified Public Accountant 国际会计准则委员会IASC美国注册会计师协会AICPA财务会计准则委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship合伙人企业Partnership公司Corporation会计目标Accounting Objectives会计假设Accounting Assumptions会计要素Accounting Elements会计原则Accounting Principles会计实务过程Accounting Procedures财务报表Financial Statements财务分析Financial Analysis会计主体假设Separate-entity Assumption货币计量假设Unit-of-measure Assumption持续经营假设Continuity(Going-concern)Assumption 会计分期假设Time-period Assumption资产Asset负债Liability业主权益Owners Equity收入Revenue费用Expense收益Income亏损Loss历史成本原则Cost Principle收入实现原则Revenue Principle配比原则Matching Principle全面披露原则Full-disclosure (Reporting)Principle 客观性原则Objective Principle一致性原则Consistent Principle可比性原则Comparability Principle重大性原则Materiality Principle稳健性原则Conservatism Principle权责发生制Accrual Basis现金收付制Cash Basis财务报告Financial Report流动资产Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益Retained Earning---------------------(2)会计循环会计循环Accounting Procedure/Cycle会计信息系统Accounting information System 帐户Ledger会计科目Account会计分录Journal entry原始凭证Source Document日记帐Journal总分类帐General Ledger明细分类帐Subsidiary Ledger试算平衡Trial Balance现金收款日记帐Cash receipt journal现金付款日记帐Cash disbursements journal 销售日记帐Sales Journal购货日记帐Purchase Journal普通日记帐General Journal工作底稿Worksheet调整分录Adjusting entries结帐Closing entries---------------------(3)现金与应收帐款现金Cash银行存款Cash in bank库存现金Cash in hand流动资产Current assets偿债基金Sinking fund定额备用金Imprest petty cash支票Check(cheque)银行对帐单Bank statement银行存款调节表Bank reconciliation statement 在途存款Outstanding deposit在途支票Outstanding check应付凭单Vouchers payable应收帐款Account receivable应收票据Note receivable起运点交货价 F.O.B shipping point目的地交货价 F.O.B destination point商业折扣Trade discount现金折扣Cash discount销售退回及折让Sales return and allowance坏帐费用Bad debt expense备抵法Allowance method备抵坏帐Bad debt allowance损益表法Income statement approach资产负债表法Balance sheet approach帐龄分析法Aging analysis method直接冲销法Direct write-off method带息票据Interest bearing note不带息票据Non-interest bearing note出票人Maker受款人Payee本金Principal利息率Interest rate到期日Maturity date本票Promissory note贴现Discount背书Endorse拒付费Protest fee---------------------(4)存货存货Inventory商品存货Merchandise inventory产成品存货Finished goods inventory在产品存货Work in process inventory原材料存货Raw materials inventory起运地离岸价格 F.O.B shipping point目的地抵岸价格 F.O.B destination寄销Consignment寄销人Consignor承销人Consignee定期盘存Periodic inventory永续盘存Perpetual inventory购货Purchase购货折让和折扣Purchase allowance and discounts 存货盈余或短缺Inventory overages and shortages 分批认定法Specific identification加权平均法Weighted average先进先出法First-in, first-out or FIFO后进先出法Lost-in, first-out or LIFO移动平均法Moving average成本或市价孰低法Lower of cost or market or LCM 市价Market value重置成本Replacement cost可变现净值Net realizable value上限Upper limit下限Lower limit毛利法Gross margin method零售价格法Retail method成本率Cost ratio---------------------(5)长期投资长期投资Long-term investment长期股票投资Investment on stocks长期债券投资Investment on bonds成本法Cost method权益法Equity method合并法Consolidation method股利宣布日Declaration date股权登记日Date of record除息日Ex-dividend date付息日Payment date债券面值Face value, Par value债券折价Discount on bonds债券溢价Premium on bonds票面利率Contract interest rate, stated rate市场利率Market interest ratio, Effective rate普通股Common Stock优先股Preferred Stock现金股利Cash dividends股票股利Stock dividends清算股利Liquidating dividends到期日Maturity date到期值Maturity value直线摊销法Straight-Line method of amortization实际利息摊销法Effective-interest method of amortization---------------------(6)固定资产固定资产Plant assets or Fixed assets原值Original value预计使用年限Expected useful life预计残?nbsp;Estimated residual value折旧费用Depreciation expense累计折旧Accumulated depreciation帐面价值Carrying value应提折旧成本Depreciation cost净值Net value在建工程Construction-in-process磨损Wear and tear过时Obsolescence直线法Straight-line method (SL)工作量法Units-of-production method (UOP)加速折旧法Accelerated depreciation method双倍余额递减法Double-declining balance method (DDB)年数总和法Sum-of-the-years-digits method (SYD)以旧换新Trade in经营租赁Operating lease融资租赁Capital lease廉价购买权Bargain purchase option (BPO)资产负债表外筹资Off-balance-sheet financing最低租赁付款额Minimum lease payments---------------------(7)无形资产无形资产Intangible assets专利权Patents商标权Trademarks, Trade names著作权Copyrights特许权或专营权Franchises商誉Goodwill开办费Organization cost租赁权Leasehold摊销Amortization---------------------(8)流动负债负债Liability流动负债Current liability应付帐款Account payable应付票据Notes payable贴现票据Discount notes长期负债一年内到期部分Current maturities of long-term liabilities 应付股利Dividends payable预收收益Prepayments by customers存入保证金Refundable deposits应付费用Accrual expense增值税value added tax营业税Business tax应付所得税Income tax payable应付奖金Bonuses payable产品质量担保负债Estimated liabilities under product warranties 赠品和兑换券Premiums, coupons and trading stamps或有事项Contingency或有负债Contingent或有损失Loss contingencies或有利得Gain contingencies永久性差异Permanent difference时间性差异Timing difference应付税款法Taxes payable method纳税影响会计法Tax effect accounting method递延所得税负债法Deferred income tax liability method---------------------(9)长期负债长期负债Long-term Liabilities应付公司债券Bonds payable有担保品的公司债券Secured Bonds抵押公司债券Mortgage Bonds保证公司债券Guaranteed Bonds信用公司债券Debenture Bonds一次还本公司债券Term Bonds分期还本公司债券Serial Bonds可转换公司债券Convertible Bonds可赎回公司债券Callable Bonds可要求公司债券Redeemable Bonds记名公司债券Registered Bonds无记名公司债券Coupon Bonds普通公司债券Ordinary Bonds收益公司债券Income Bonds名义利率,票面利率Nominal rate实际利率Actual rate有效利率Effective rate溢价Premium折价Discount面值Par value直线法Straight-line method实际利率法Effective interest method到期直接偿付Repayment at maturity提前偿付Repayment at advance偿债基金Sinking fund长期应付票据Long-term notes payable抵押借款Mortgage loan---------------------(10)业主权益权益Equity业主权益Owners equity股东权益Stockholders equity投入资本Contributed capital缴入资本Paid-in capital股本Capital stock资本公积Capital surplus留存收益Retained earnings核定股本Authorized capital stock实收资本Issued capital stock发行在外股本Outstanding capital stock库藏股Treasury stock普通股Common stock优先股Preferred stock累积优先股Cumulative preferred stock非累积优先股Noncumulative preferred stock完全参加优先股Fully participating preferred stock部分参加优先股Partially participating preferred stock非部分参加优先股Nonpartially participating preferred stock 现金发行Issuance for cash非现金发行Issuance for noncash consideration股票的合并发行Lump-sum sales of stock发行成本Issuance cost成本法Cost method面值法Par value method捐赠资本Donated capital盈余分配Distribution of earnings股利Dividend股利政策Dividend policy宣布日Date of declaration股权登记日Date of record除息日Ex-dividend date股利支付日Date of payment现金股利Cash dividend股票股利Stock dividend拨款appropriation---------------------(11)财务报表财务报表Financial Statement资产负债表Balance Sheet收益表Income Statement帐户式Account Form报告式Report Form编制(报表)Prepare工作底稿Worksheet多步式Multi-step单步式Single-step---------------------(12)财务状况变动表财务状况变动表中的现金基础SCFP.Cash Basis(现金流量表)财务状况变动表中的营运资金基础SCFP.Working Capital Basis (资金来源与运用表)营运资金Working Capital全部资源概念All-resources concept直接:)业务Direct exchanges正常营业活动Normal operating activities财务活动Financing activities投资活动Investing activities---------------------(13)财务报表分析财务报表分析Analysis of financial statements比较财务报表Comparative financial statements趋势百分比Trend percentage比率Ratios普通股每股收益Earnings per share of common stock股利收益率Dividend yield ratio价益比Price-earnings ratio普通股每股帐面价值Book value per share of common stock资本报酬率Return on investment总资产报酬率Return on total asset债券收益率Yield rate on bonds已获利息倍数Number of times interest earned债券比率Debt ratio优先股收益率Yield rate on preferred stock营运资本Working Capital周转Turnover存货周转率Inventory turnover应收帐款周转率Accounts receivable turnover流动比率Current ratio速动比率Quick ratio酸性试验比率Acid test ratio(14)合并财务报表合并财务报表Consolidated financial statements吸收合并Merger创立合并Consolidation控股公司Parent company附属公司Subsidiary company少数股权Minority interest权益联营合并Pooling of interest购买合并Combination by purchase权益法Equity method成本法Cost method---------------------(15)物价变动中的会计计量物价变动之会计Price-level changes accounting一般物价水平会计General price-level accounting货币购买力会计Purchasing-power accounting统一币值会计Constant dollar accounting历史成本Historical cost现行价值会计Current value accounting现行成本Current cost重置成本Replacement cost物价指数Price-level index国民生产总值物价指数Gross national product implicit price deflator (or GNP deflator)消费物价指数Consumer price index (or CPI)批发物价指数Wholesale price index货币性资产Monetary assets货币性负债Monetary liabilities货币购买力损益Purchasing-power gains or losses资产持有损益Holding gains or losses未实现的资产持有损益Unrealized holding gains or losses现行价值与统一币值会计Constant dollar and current cost accounting。

国际会计中英文对照

国际会计中英文对照第一篇:国际会计中英文对照国际会计科目中英文对照 Account 帐户Accounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Bookkeepking 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室Income statement 损益表Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会Statement of cash flow 现金流量表Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系Assets 资产Business entity 企业个体Capital stock 股本Corporation 公司Cost principle 成本原则Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设Inflation 通货膨涨Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量Operating activities 经营活动Owners equity 所有者权益Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设Stockholders 股东Stockholders equity 股东权益Window dressing 门面粉饰财会名词汉英对照表(1)会计与会计理论会计accounting决策人Decision Maker投资人Investor股东Shareholder债权人Creditor财务会计Financial Accounting管理会计Management Accounting成本会计Cost Accounting私业会计Private Accounting公众会计 Public Accounting注册会计师 CPA Certified Public Accountant 国际会计准则委员会IASC美国注册会计师协会AICPA财务会计准则委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship合伙人企业 Partnership公司 Corporation 会计目标Accounting Objectives会计假设Accounting Assumptions会计要素 Accounting Elements会计原则 Accounting Principles会计实务过程 Accounting Procedures财务报表 Financial Statements财务分析Financial Analysis会计主体假设 Separate-entity Assumption货币计量假设 Unit-of-measure Assumption持续经营假设Continuity(Going-concern)Assumption 会计分期假设 Time-period Assumption资产 Asset负债 Liability业主权益Owners Equity收入Revenue费用Expense收益Income亏损 Loss历史成本原则 Cost Principle收入实现原则 Revenue Principle配比原则 Matching Principle全面披露原则Full-disclosure(Reporting)Principle客观性原则 Objective Principle一致性原则 Consistent Principle可比性原则Comparability Principle重大性原则 Materiality Principle稳健性原则Conservatism Principle权责发生制Accrual Basis现金收付制Cash Basis财务报告 Financial Report流动资产 Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益 Retained Earning(2)会计循环会计循环Accounting Procedure/Cycle会计信息系统Accounting information System帐户 Ledger会计科目 Account会计分录 Journal entry原始凭证 Source Document日记帐 Journal 总分类帐 General Ledger明细分类帐 Subsidiary Ledger试算平衡 Trial Balance现金收款日记帐Cash receipt journal现金付款日记帐Cash disbursements journal销售日记帐Sales Journal购货日记帐Purchase Journal普通日记帐 General Journal工作底稿 Worksheet 调整分录 Adjusting entries结帐 Closing entries(3)现金与应收帐款现金 Cash银行存款 Cash in bank库存现金 Cash in hand流动资产 Current assets偿债基金Sinking fund定额备用金Imprest petty cash支票Check(cheque)银行对帐单 Bank statement银行存款调节表Bank reconciliation statement 在途存款Outstanding deposit在途支票Outstanding check应付凭单Vouchers payable应收帐款Account receivable应收票据Note receivable起运点交货价F.O.B shipping point目的地交货价F.O.B destination point商业折扣 Trade discount现金折扣 Cash discount 销售退回及折让 Sales return and allowance坏帐费用 Bad debtexpense备抵法 Allowance method备抵坏帐 Bad debt allowance 损益表法 Income statement approach资产负债表法 Balance sheet approach帐龄分析法Aging analysis method直接冲销法Direct write-off method带息票据 Interest bearing note不带息票据 Non-interest bearing note出票人 Maker受款人 Payee本金 Principal利息率 Interest rate到期日 Maturity date本票Promissory note贴现Discount背书Endorse拒付费Protest fee(4)存货存货 Inventory商品存货Merchandise inventory产成品存货Finished goods inventory在产品存货 Work in process inventory原材料存货 Raw materials inventory起运地离岸价格 F.O.B shipping point目的地抵岸价格 F.O.B destination寄销 Consignment寄销人 Consignor承销人 Consignee定期盘存Periodic inventory永续盘存Perpetual inventory购货 Purchase购货折让和折扣 Purchase allowance and discounts 存货盈余或短缺Inventory overages and shortages 分批认定法Specific identification加权平均法Weighted average先进先出法First-in, first-out or FIFO后进先出法Lost-in, first-out or LIFO移动平均法Moving average成本或市价孰低法 Lower of cost or market or LCM 市价 Market value重置成本 Replacement cost可变现净值 Net realizable value上限 Upper limit下限 Lower limit毛利法 Gross margin method零售价格法 Retail method成本率 Cost ratio(5)长期投资长期投资 Long-term investment长期股票投资 Investment on stocks长期债券投资 Investment on bonds成本法 Cost method权益法Equity method合并法Consolidation method股利宣布日Declaration date股权登记日Date of record除息日Ex-dividenddate付息日 Payment date债券面值 Face value, Par value债券折价 Discount on bonds债券溢价 Premium on bonds票面利率 Contract interest rate, stated rate市场利率 Market interest ratio, Effective rate普通股Common Stock优先股Preferred Stock现金股利 Cash dividends股票股利 Stock dividends 清算股利Liquidating dividends到期日Maturity date到期值Maturity value直线摊销法 Straight-Line method of amortization实际利息摊销法 Effective-interest method of amortization(6)固定资产固定资产 Plant assets or Fixed assets原值 Original value预计使用年限Expected useful life预计残?nbsp;Estimated residual value折旧费用Depreciation expense累计折旧Accumulated depreciation帐面价值Carrying value应提折旧成本Depreciation cost净值 Net value在建工程Construction-in-process磨损Wear and tear过时Obsolescence直线法 Straight-line method(SL)工作量法Units-of-production method(UOP)加速折旧法Accelerated depreciation method双倍余额递减法 Double-declining balance method(DDB)年数总和法 Sum-of-the-years-digits method(SYD)以旧换新 Trade in经营租赁 Operating lease融资租赁 Capital lease廉价购买权Bargain purchase option(BPO)资产负债表外筹资Off-balance-sheet financing最低租赁付款额Minimum lease payments(7)无形资产无形资产 Intangible assets专利权 Patents商标权 Trademarks, Trade names著作权 Copyrights特许权或专营权 Franchises商誉 Goodwill开办费 Organization cost租赁权 Leasehold摊销 Amortization (8)流动负债负债 Liability流动负债 Current liability应付帐款 Account payable应付票据Notes payable贴现票据 Discount notes长期负债一年内到期部分Current maturities of long-term liabilities应付股利Dividends payable预收收益Prepayments by customers存入保证金Refundable deposits应付费用Accrual expense增值税 value added tax营业税 Business tax应付所得税 Income tax payable应付奖金 Bonuses payable产品质量担保负债Estimated liabilities under product warranties赠品和兑换券 Premiums, coupons and trading stamps或有事项 Contingency或有负债 Contingent或有损失 Loss contingencies 或有利得 Gain contingencies永久性差异 Permanent difference时间性差异 Timing difference应付税款法 Taxes payable method 纳税影响会计法 Tax effect accounting method递延所得税负债法 Deferred income tax liability method(9)长期负债长期负债 Long-term Liabilities应付公司债券 Bonds payable有担保品的公司债券Secured Bonds抵押公司债券Mortgage Bonds 保证公司债券Guaranteed Bonds信用公司债券Debenture Bonds 一次还本公司债券 Term Bonds分期还本公司债券 Serial Bonds可转换公司债券 Convertible Bonds可赎回公司债券 Callable Bonds 可要求公司债券Redeemable Bonds记名公司债券Registered Bonds无记名公司债券Coupon Bonds普通公司债券Ordinary Bonds收益公司债券Income Bonds名义利率,票面利率Nominal rate实际利率 Actual rate有效利率 Effective rate溢价 Premium折价 Discount面值 Par value直线法 Straight-line method实际利率法Effective interest method到期直接偿付Repayment at maturity提前偿付 Repayment at advance偿债基金Sinking fund长期应付票据Long-term notes payable抵押借款Mortgage loan(10)业主权益权益 Equity业主权益 Owners equity股东权益 Stockholders equity投入资本 Contributed capital缴入资本 Paid-in capital股本 Capital stock 资本公积Capital surplus留存收益Retained earnings核定股本Authorized capital stock实收资本 Issued capital stock 发行在外股本 Outstanding capital stock库藏股 Treasury stock 普通股 Common stock优先股 Preferred stock累积优先股Cumulative preferred stock非累积优先股Noncumulative preferred stock完全参加优先股 Fully participating preferred stock部分参加优先股Partially participating preferred stock非部分参加优先股 Nonpartially participating preferred stock 现金发行 Issuance for cash非现金发行 Issuance for noncash consideration股票的合并发行Lump-sum sales of stock发行成本Issuance cost成本法Cost method面值法 Par value method捐赠资本 Donated capital盈余分配 Distribution of earnings股利 Dividend股利政策 Dividend policy宣布日 Date of declaration股权登记日Date of record除息日Ex-dividend date股利支付日Date of payment现金股利Cash dividend股票股利Stock dividend拨款appropriation(11)财务报表财务报表Financial Statement资产负债表Balance Sheet收益表 Income Statement帐户式 Account Form报告式 Report Form编制(报表)Prepare工作底稿Worksheet多步式Multi-step单步式Single-step(12)财务状况变动表财务状况变动表中的现金基础 SCFP.Cash Basis(现金流量表)财务状况变动表中的营运资金基础 SCFP.Working Capital Basis(资金来源与运用表)营运资金 Working Capital全部资源概念All-resources concept直接:)业务Direct exchanges正常营业活动 Normal operating activities财务活动 Financing activities投资活动 Investing activities(13)财务报表分析财务报表分析Analysis of financial statements比较财务报表Comparative financial statements趋势百分比 Trend percentage比率 Ratios普通股每股收益 Earnings per share of common stock股利收益率 Dividend yield ratio价益比 Price-earnings ratio普通股每股帐面价值 Book value per share of common stock 资本报酬率Return on investment总资产报酬率Return on total asset债券收益率 Yield rate on bonds已获利息倍数 Number of times interest earned债券比率 Debt ratio优先股收益率 Yield rate on preferred stock营运资本 Working Capital周转 Turnover存货周转率 Inventory turnover应收帐款周转率Accounts receivable turnover流动比率Current ratio速动比率 Quick ratio酸性试验比率 Acid test ratio(14)合并财务报表合并财务报表Consolidated financial statements吸收合并Merger创立合并Consolidation控股公司Parent company附属公司Subsidiary company少数股权Minority interest权益联营合并Pooling of interest购买合并Combination by purchase权益法Equity method成本法 Cost method(15)物价变动中的会计计量物价变动之会计Price-level changes accounting一般物价水平会计General price-level accounting货币购买力会计Purchasing-power accounting统一币值会计 Constant dollar accounting历史成本 Historical cost现行价值会计 Current value accounting现行成本 Current cost 重置成本 Replacement cost物价指数 Price-level index 国民生产总值物价指数Gross national product implicit price deflator(or GNP deflator)消费物价指数Consumer price index(or CPI)批发物价指数Wholesale price index货币性资产Monetary assets货币性负债Monetary liabilities货币购买力损益 Purchasing-power gains or losses资产持有损益 Holding gains or losses未实现的资产持有损益 Unrealized holding gains or losses现行价值与统一币值会计 Constant dollar and current cost accounting 第二篇:中英文对照A《美国口语惯用法例句集粹》AA(Page 1-4)1.about1)2)3)4)5)6)7)I'd like to know what this is all about.我想知道这到底是怎么回事。

国际会计复习资料中英结合版

国际会计复习资料中英结合版A.Basic Knowledge1.we view accounting as consisting of three broad areas: measuremen t、[‘meʒəmənt](计量)disclosure[dis’kləuʒə](披露) and auditin g[‘ɔ:ditiŋ](审计).2.The three international organization of accounting profession are(International Federation of Accountants;IFAC) (国际会计师联合会)(International Accounting Standards Committee; IASC) (国际会计准则委员会)(International Auditing practice Committee;IAPC) (国际审计实务委员会)3.Hofstede’s four cultural dimensions are(霍夫斯泰德的四个文化层面):(1)individualism(个人主义)(2)power distance(权力距离)(3)uncertainty avoidance(风险规避)(4)masculinity(阳刚之气)4. The four culture dimensions that affect a nation’s financial report ing practices by Gray refer to?阻碍一个国家的财务报告的做法的四个层面系指:(1)Professionalism (职业主义维度)(2)Uniformity (统一性维度)(3)conservatism (保守主义维度)(4)Secrecy (保密性维度)5.Accounting standard setting normally involves a combination of pri vate and public sector groups.(会计准则的制定通常涉及结合私营和公共部门的群体。

国际会计英文版 (翻译)

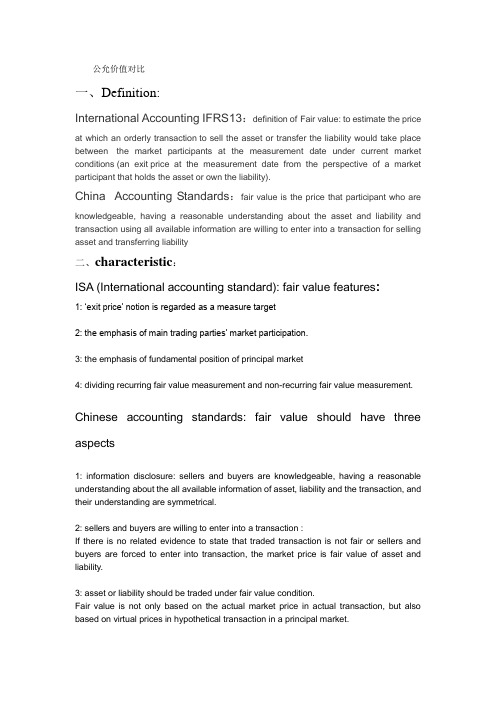

公允价值对比一、Definition:International Accounting IFRS13:definition of Fair value: to estimate the priceat which an orderly transaction to sell the asset or transfer the liability would take place between the market participants at the measurement date under current market conditions (an exit price at the measurement date from the perspective of a market participant that holds the asset or own the liability).China Accounting Standards:fair value is the price that participant who areknowledgeable, having a reasonable understanding about the asset and liability and transaction using all available information are willing to enter into a transaction for selling asset and transferring liability二、characteristic:ISA (International accounting standard): fair value features:1: ‘exit price’ notion is regarded as a measure target2: the emphasis of main trading parties’ market participation.3: the emphasis of fundamental position of principal market4: dividing recurring fair value measurement and non-recurring fair value measurement. Chinese accounting standards: fair value should have three aspects1: information disclosure: sellers and buyers are knowledgeable, having a reasonable understanding about the all available information of asset, liability and the transaction, and their understanding are symmetrical.2: sellers and buyers are willing to enter into a transaction :If there is no related evidence to state that traded transaction is not fair or sellers and buyers are forced to enter into transaction, the market price is fair value of asset and liability.3: asset or liability should be traded under fair value condition.Fair value is not only based on the actual market price in actual transaction, but also based on virtual prices in hypothetical transaction in a principal market.三、Field of applicationThe international accounting standards1.《SFAS159—The Fair value option for financial assets and financial liabilities》allow listing corporation to choose the financial assets fair value more .FASB set the policy objectives of fair value measurement consistent with IAS39.PS: SFAS, Statement of Financial Accounting StandardsIAS, International Accounting Standard2. The fair value measurement of non financial assets choice. 《IAS40—Investment property》allow enterprises to choose historical cost or fair value in the subsequent measurement of the investment real estate. If you select the historical cost also needs to disclosure fair value in the footnotes, unless that fair value cannot be reliably confirmed; Once you select the fair value are not allowed back to the historical cost measurement.3.《IAS16-Property, plant and equipment standards》and 《IAS38-intangible assets. For IAS16, allowing enterprises in the balance sheet date on the subsequent measurement of property, plant and equipment adopt the historical cost or fair value, and the same asset class requires consistent measurement attributes, all kinds of measurement attributes are required to be depreciated. Property, plant and equipment value should be recorded into the owner’s equity under the condition of using fair value measurement.China Accounting standards1.The new guidelines《No. 37 - presentation of financial instruments》prescribed in 16th guideline: The enterprise should disclose the financial assets and financial liabilities what are measured at fair value and whose fluctuations are recorded into the current profits and losses statement.2.Subsequent measurement of investment property and the application of fair value in the final estimation.3.The new guidelines《NO.24 hedging》prescribed in the second guideline:Hedging is that enterprises, in order to avoid foreign exchange risk, interest rate risk, commodity price risk, stock price risk, credit risk, etc., specify one or more than a hedging instrument, make the changes in fair value or cash flow of a hedging instrument, and are expected to offset the hedged item changes in fair value or cash flow in whole or in part.四.Environmental differencesThe international accounting standards1. The appearance of FRS13 has a profound theoretical basis2. The mature market environment3. The adequate assessment proceduresChina Accounting standards1. It is not mature from theory to practice, the use of fair value has no uniform standardcaliber, it is a leading factor that some industries cannot make comparison analysis simply.2. Stock market in China is not yet mature currently.3. Derivative financial instruments are relatively backward4. Immature market environment.。

《最新国际会计科目中英文对照》(2013.9)

1253 预付 保险费 prepaid insurance

1254 用品 盘存 office supplies

1255 预付 所得税 prepaid income tax

1258 其它 预付费用 other prepaid expenses

126 预付 款项 prepaymen ts

1129 113 1131 1132 1137 1138 1139 114 1141

备抵短期投资跌价损失 应收票据 应收票据 应收票据贴现 应收票据 -关系人 其它应收票据

备抵呆帐 -应收票据 应收帐款 应收帐款

1142 应收

分期帐款 installment accounts receivable

1147 应收

1283 暂付 款 temporary payments

1284 代付 款 payment on behalf of others

1285 员工 借支 advances to employees

1286 存出 保证金 refundable deposits

1287 受限 制存款 certificate of depositrestricted

中国会计科目中英文对照

代码

1

资产

名称

11~ 12 流动资产

111 1111 1112 1113 1116 1117 1118

现金及约当现金 库存现金 零用金/周转金 银行存款 在途现金 约当现金 其它现金及约当现金

112 1121 1122 1123 1124 1125 1128

短期投资 短期投资 -股票 短期投资 -短期票券 短期投资 -政府债券 短期投资 -受益凭证 短期投资 -公司债 短期投资 -其它

国际会计双语期末复习精品文档12页

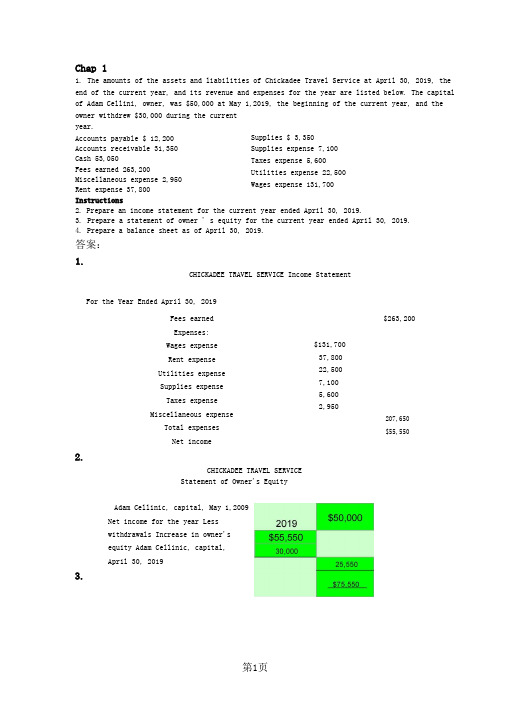

Chap 11. The amounts of the assets and liabilities of Chickadee Travel Service at April 30, 2019, the end of the current year, and its revenue and expenses for the year are listed below. The capital of Adam Cellini, owner, was $50,000 at May 1,2019, the beginning of the current year, and the owner withdrew $30,000 during the current year.Accounts payable $ 12,200Accounts receivable 31,350 Cash 53,050 Fees earned 263,200 Miscellaneous expense 2,950Rent expense 37,800 Instructions2. Prepare an income statement for the current year ended April 30, 2019.3. Prepare a statement of owner ' s equity for the current year ended April 30, 2019.4. Prepare a balance sheet as of April 30, 2019.答案: 1.CHICKADEE TRAVEL SERVICE Income StatementFor the Year Ended April 30, 20192.CHICKADEE TRAVEL SERVICEStatement of Owner's EquityAdam Cellinic, capital, May 1,2009 Net income for the year Less withdrawals Increase in owner's equity Adam Cellinic, capital, April 30, 20193.Supplies $ 3,350 Supplies expense 7,100 Taxes expense 5,600 Utilities expense 22,500 Wages expense 131,700Fees earned Expenses: Wages expense Rent expense Utilities expense Supplies expense Taxes expense Miscellaneous expenseTotal expensesNet income$263,200$131,700 37,800 22,500 7,100 5,600 2,950207,650 $55,550CHICKADEE TRAVEL SERVICEBalance SheetApril 30,2019Liabilities$87,750_Total liabilities and owner's equity$87,750Chap 21. The Zuni Co. has the following accounts in its ledger: Cash; Accounts Receivable; Supplies; Office Equipment; Accounts Payable; Gayle McCall, Capital; Gayle McCall, Drawing; Fees Earned; Rent Expense; Advertising Expense; Utilities Expense; Miscellaneous Expense.Journalize the following selected transactions for August 2019 in a two-column journal. Journal entry explanations may be omitted. August 1. Paid rent for the month, $1,500.2. Paid advertising expense, $700. 4. Paid cash for supplies, $1,050.6. Purchased office equipment on account, $7,500. 8. Received cash from customers on account, $3,600. 12. Paid creditor on account, $1,150. 20. Withdrew cash for personal use, $1,000.25. Paid cash for repairs to office equipment, $500. 30. Paid telephone bill for the month, $195.31. Fees earned and billed to customers for the month, $10,150. 32. Paid electricity bill for the month, $380.答案:2019August 1. Rent Expense (1500)Cash ........................................ 1500 2. Advertising Expense . (700)Cash ........................................ 700 4. Supplies . (1050)Cash ........................................ 1050 6. Office Equipment .. (7500)Accounts Payable ............................ 7500 8. Cash (3600)Accounts Receivable ........................ 3600 12. Accounts Payable (1150)Cash .......................................... 1150 20. Gayle McCall, Drawing .. (1000)Cash .............................................. 1000 25. Miscellaneous Expense (500)Cash (500)AssetsCash Accounts receivable SuppliesAccounts payable$53,050 3,1503,350 Owner's Equity$ 75,550$12,200Total assets30.Utilities Expense (195)Cash (195)31.Cash (10150)Fees Earned (10150)32.Utilities Expense (380)Cash (380)Chapter 3? The Matching Concept and the Adjusting ProcessPROBLEM 3-5AGreco Service Co., which specializes in appliance repair services, is owned and operated by Curtis Loomis. Greco Service Co. ' s accounting clerk prepared the followingtrial balance at December 31,2019:Greco Service Co.Trial BalanceDecember 31,2019Cash .................................................................. 4,200Accounts Receivable ................................................... 20,600Prepaid Insurance ...................................................... 6,000Supplies .............................................................. 1,450Land ................................................................. 100,000Building .............................................................. 161,500Accumulated Depreciation —Building ....................... ................................75,700 Equipment ...................................................... 80,100Accumulated Depreciation —Equipment ................................................ 35,300Accounts Payable ............................ ....................................................7,500 Unearned Rent ................... ..........................................................7,200 Curtis Loomis, Capital ....... ...........................................................157,100 Curtis Loomis, Drawing ............................................ 5,000Fees Earned ........................... ........................................................257,200 Salaries and Wages Expense ........................................ 101,800Utilities Expense ..................................................... 28,200Advertising Expense .................................................... 15,000Repairs Expense ........................................................ 12,100Miscellaneous Expense .................................................. 4,050540,000 540,000 The data needed to determine year-end adjustments are as follows: a. Depreciation of building for the year, $3,600. b. Depreciation of equipment for the year, $2,400. c. Accrued salaries and wages at December 31, $2,170. d. Unexpired insurance at December 31, $3,500. e. Fees earned but unbilled on December 31, $4,350. f. Supplies on hand at December 31, $375.g. Rent unearned at December 31, $2,800. Instructions 1. Journalize the adjusting entries. Add additional accounts as needed. 2. Determine the balances of the accounts affected by the adjusting entries and prepare an adjusted trial balance. 答案:1.2.Repairs ExpenseDepreciation Expense - Equipment Insurance ExpenseDepreciation Expense - Building Supplies Expense Miscellaneous ExpenseChapter 4 Completing the Accounting Cycle1. I thaca Services Co. offers cleaning services to business clients. Complete the following work sheet for Ithaca Services Co, and prepare an income statement, statement of owner s equity, balance she and the closing entries for Ithaca Services Co.Ithaca Services Co.Work Sheet For the Year Ended January 31,2019Account Title Adjusted Trial BalanceIncome StatementBalance SheetDr.Cr.Dr.Cr.Dr.Cr.Cash8Accounts Receivable 57Supplies3Prepaid Insurance 6Land r 501Equipment32Accumulated Depr. — Equip. 7Accounts Payable26Wages Payable1Terry Dagley, Capital 112Terry Dagley, Drawing 8Fees Earned 67Wages Expense 17Rent Expense 8Insurance Expense r 6 1Utilities Expense 6Depreciation Expense 5Supplies Expense 51Miscellaneous Expense 2Totals213213Net income (loss)答案:ITHACA SERVICES CO. Income Statement For the Year Ended January 31, 2019 Fees earned .................................................... $67 Expenses: Wages expense .............................. $17 Rent expense ....................................... 8 Insurance expense .................................. 6 Utilities expense .................................. 6 Supplies expense .. (5)12,100 2,400 2,500 3,600 1,075 4,050 552,520Depreciation expense ................................ 5 Miscellaneous expense ............................... 2 Total expenses ....................... Net income .................................... ITHACA SERVICES CO.Statement of Owner s EquityFor the Year Ended January 31,2019 Terry Dagley, capital, $112Net income for the year ................................ $18 Less withdrawals (8)Increase in owner equity ............................................... 10 Terry Dagley, capital, October 31, 2019 ............................... $122ITHACA SERVICES CO. Balance Sheet January 31, 2019 Assets LiabilitiesCurrent assets: Current liabilities: Cash .................... $ 8 Accounts payable ...... $26 Accounts receivable.... 57 Wages payable ........... 1 Supplies ............. 3 Total liabilities ......... $ 27 Prepaid insurance . (6)Total current assets.. $ 74 Property, plant, and equipment: Land $ 50 Equipment .......... $32Less accum. depr.... 7 ___ Owner' s Equity Total property, plant, Terry Dagley, capital... 122 and equipment... ...75 Total liabilities and Total assets ................. $149 owner' s equity. .$149 2019 Jan. 31 Fees Earned . (67)Income Summary (67)31 Income Summary (49)Wages Expense ............................... 17 Rent Expense ................................ 8 Insurance Expense ........................... 6 Utilities Expense ........................... 6 Supplies Expense ............................ 5 Depreciation Expense ...................... 5 Miscellaneous Expense (2)31 Income Summary (18)Terry Dagley, Capital (18)31 Gloria Millard, Capital (8)Terry Dagley, Drawing (8)Chapter 6 ? Accounting for Merchandising BusinessesPROBLEM 6-5AThe following were selected from among the transactions completed by Ingress Company during January of the current year:Jan. 3. Purchased merchandise on account from Pynn Co., list price $16,000, trade discount 35%, terms FOB shipping point, 2/10, n/30, with prepaid transportation costs of $320 added to the invoice.5. Purchased merchandise on account from Wilhelm Co., $8,000, terms FOB destination, 1/10,n/30.6. Sold merchandise on account to Sievert Co., list price $12,500, trade discount 40%, terms 2/10, n/30. The cost of the merchandise sold was $4,500.7. Returned $1,800 of merchandise purchased on January 5 from Wilhelm Co. 13. Paid Pynn Co. on account for purchase of January 3, less discount.15. Paid Wilhelm Co. on account for purchase of January 5, less return of January 7 and discount. 16. Received cash on account from sale of January 6 to Sievert Co., less discount.19. Sold merchandise on nonbank credit cards and reported accounts to the card company, American Express, $6,450. The cost of the merchandise sold was $3,950.22. Sold merchandise on account to Elk River Co., $3,480, terms 2/10, n/30. The cost of the merchandise sold was $1,400.23. Sold merchandise for cash, $9,350. The cost of the merchandise sold was $5,750.25. Received merchandise returned by Elk River Co. from sale on January 22, $1,480. The cost of the returned49_ ..$ 18merchandise was $600.31.Received cash from American Express for nonbank credit card sales of January 19, less $225 service fee. InstructionsJournalize the transactions.答案:1.Jan. 3 Merchandise Inventory ................... 10,720Accounts Payable —Pynn Co ................................ 10,720[$16,000 - ($16,000 35%)] = $10,400;$10,400 + $320 = $10,720.5 Merchandise Inventory ........................... 8,000Accounts Payable —Wilhelm Co .............................. 8,0006 Accounts Receivable —Sievert Co ..................... 7,500Sales ............................................. 7,500[$12,500 - ($12,500 *0%)] = $7,5006Cost of Merchandise Sold ....................... 4,500Merchandise Inventory ..................................... 4,5007Accounts Payable —Wilhelm Co ................. 1,800Merchandise Inventory .................................... 1,80013 Accounts Payable —Pynn Co .................... 10,720Cash ...................................................... 10,512Merchandise Inventory (208)15 Accounts Payable —Wilhelm Co ..................... 6,200Cash .............................. ...................... 6,138Merchandise Inventory (62)16 Cash ................................................ 7,350Sales Discount (150)Accounts Receivable —Sievert Co ......................... 7,50019 Accounts Receivable--American Express .............. 6,450Sales .................................................... 6,45019 Cost of Merchandise Sold .......................... 3,950Merchandise Inventory ........ ................ 3,95022 Accounts Receivable —Elk River Co ............. 3,480Sales .................................................... 3,48022 Cost of Merchandise Sold .......................... 1,400Merchandise Inventory .......... ............ 1,40023 Cash ................................................ 9,350Sales ................................................... 9,350Dec. 23 Cost of Merchandise Sold ..................... 5,750Merchandise Inventory ........ ............... 5,75025 Sales Returns and Allowances .................... 1,480Accounts Receivable —Elk River Co. ... …1,48025 Merchandise Inventory (600)Cost of Merchandise Sold ............ .. (600)31 Credit Card Expense (225)Cash (225)Cash ............................................... 6,450Accounts Receivable--American Express ............. 6,450Questions of chap 7 Inventories1.The units of an item available for sale during the year were as follows:Jan. 1 Inventory 42 units at $120Mar. 4 Purchase 58 units at $130Aug. 7 Purchase 20 units at $136Nov. 15 Purchase 30 units at $140There are 36 units of the item in the physical inventory at December 31. The periodic inventory system is used. Determine the inventory cost and the cost of merchandise sold by three methods, presenting your answers in the following form:Cost Inventory Method Merchandise InventoryMerchandise Solda.First-in, first-out $ $st-in, first-outc. Average cost 答案:CostMerchandise MerchandiseInventory Method Inventory Solda.FIFO .............. $5,016 $14,484b.LIFO .............. 4,320 15,180c.Average cost ...... 4,680 14,820Cost of merchandise available for sale: 42 units at $120 .$5,04058 units at $130 ...................................... 7,54020 units at $136 ...................................... 2,72030 units at $140 ...................................... 4,200150 units (at average cost of $130) ................... $19,500a.First-in, first-out: Merchandise inventory: 30 units at $140 $4,2006 units at $136 (816)36 units ............................................. $5,016Merchandise sold: $19,500 - $5,016 ......................... $14,484st-in, first-out: Merchandise inventory: 36 units at $120 $4,320Merchandise sold: $19,500 - $4,320 ...................... $15,180c.Average cost:Merchandise inventory:36 units at $130($19,500/150 units) ....................$4,680Merchandise sold:$19,750 - $4,680 ........................................ $14,820Chap 81. The following data were accumulated for use in reconciling the bank account ofKidstock Co. for March:a.Cash balance according to the depositor ' s records at March 31, $7,671.45.b.Cash balance according to the bank statement at March 31, $4,457.25.c.Checks outstanding, $2,276.20.d.Deposit in transit, not recorded by bank, $5,780.40.e. A check for $145 in payment of an account was erroneously recorded in thecheck register as $451.f.Bank debit memorandum for service charges, $16.00.Prepare a bank reconciliation, using the format shown in Exhibit 7.And journalize the entry or entries that should be made by the depositor.答案:Kidstock CO.Bank ReconciliationMarch 31, 20 — Cash balance according to bank statement .............................................................. $4457.25Add deposit in transit, not recorded by bank .................. 5780.4$17,850Deduct outstanding checks ..................................... 2276.2 _______Adjusted balance ................................................ $7961.45Cash balance according to company ' s records .......................... 7671.45Add error in recording check (306)$13,695 Deduct bank service charge (16)Adjusted balance ................................................ $7961.45EntriesCash (306)Accounts Payable (306)Miscellaneous Administrative Expense (16)Cash (16)Chap91、For a business that makes advance provision for uncollectible receivables(a)Journalize the entries to record the following:(1)Record the adjusting entry at December 31, the end of the fiscal year, to provide for doubtfulaccounts. The accounts receivable account has a balance of $800,000, and the contra asset accountbefore adjustment has a debit balance of $600. Analysis of the receivables indicates doubtfulaccounts of $18,000.(2)In March of the following fiscal year, the $350 owed by Fronk Co. on account is written off asuncollectible.(3)Eight months later, $200 of the Fronk Co. account is reinstated and payment of thatamount is received.(4)In October, $400 is received on the $600 owed by Dodger Co. and the remainder is written off asuncollectible.(b)Based on the data in (a)⑴ above, what is the net realizable value of the accounts receivable asreported on the balance sheet as of December 31?(c)Assuming that the business had been following the direct write-off procedure in accounting foruncollectible receivables, journalize the entries to record the following:(1)Recorded the write-off of account of Fronk Co. [(a) (2) above].(2)Reinstated account of Fronk Co. for $200 and recorded payment of that amount received [(a) (3)above].(3)Recorded the receipt of $400 from Dodger Co. in (a) (4) above and wrote off the remainder owedas uncollectible.2.Watson Company issued a 60-day, 8% note for $18,000, dated April 5, to Laker Company on account.(Assume a 360-day year when calculating interest.)(a)Determine the due date of the note.(b)Determine the maturity value of the note.(c)Journalize the entries to record the following:(1)receipt of the note by the payee, and(2)receipt by the payee of the amount due on the note at maturity. Round answers to the nearest$1.答案:1、(a)⑴Uncollectible Accounts Expense Allowance forDoubtful Accounts 18,60018,600(2) Allowance for Doubtful Accounts 350Accounts Receivable-Fronk Co 350 ⑶Accounts Receivable-Fronk Co 200Allowance for Doubtful Accounts 200Cash 200Accounts Receivable-Fronk Co 200 (4) Cash 400Allowance for Doubtful Accounts 200Accounts Receivable-Dodger Co 600(b) $782,000 ($800,000 - $18,000)(c)⑴Uncollectible Accounts ExpenseAccounts Receivable-Fronk Co 350350(2) Accounts Receivable-Fronk Co 200Uncollectible Accounts Expense 200Cash 200Accounts Receivable-Fronk Co 200 ⑶Cash 400Uncollectible Accounts Expense 200Accounts Receivable-Dodger Co 600 2、(a) June 4(b) $18,240(c) Note Receivable-Watson CoAccount Receivable-Watson Co Cash18,240Note Receivable-Watson Co 18,000Interest Revenue240Chap10Getco Co. has a sales representative who must travel a substantial amount. A car for this purpose was acquired January 2 four years ago at a cost of $20,000. It is estimated to have a total useful life of 4 years or 100,000 miles and no re-sidual value.Instructions:(1) Record the annual depreciation on Getco s car at the end of the first and third years of ownership using the straight-line method and a December 31 year end.(2) Record the annual depreciation on Getco s car at the end of the first and third years of ownership using the double-declining-balance method and a December 31 year end.(3) Record the annual depreciation on Getco s car at the end of the first and third years of ownership using the units-of-production method, assuming no residual value, and using a December 31 year end. The car was driven 35,000 miles in the first year and 28,000 miles in the third year.答案:(1) Dec. 31 Depreciation Expense —Automobile .............. 5,000* Accumulated Depreciation —Automobile ............ 5,000 *($20,000/4)Dec. 31 Depreciation Expense —Automobile ....................... 5,000 Accumulated Depreciation —Automobile ............ 5,000 (2) Dec. 31 Depreciation Expense —Automobile ..................... 10,000* Accumulated Depreciation —Automobile ............ 10,000 *($20,000 x 50%)Dec. 31 Depreciation Expense —Automobile ..................... 2,500* Accumulated Depreciation —Automobile ............ 2,500 *[($20,000 - $10,000 - $5,000) x 50%](3) Dec. 31 Depreciation Expense —Automobile .............. 7,000* Accumulated Depreciation —Automobile ...... 7,000 *(35,000 miles x $0.20) Dec. 31 Depreciation Expense —Automobile ..................... 5,600* Accumulated Depreciation —Automobile ...... 5,600 *(28,000 milesx $0.20)Chapter 11 —Current Liabilities and Payroll1.On January 2nd, Premier Sales borrows $13,500 cash on a note payable from Trusted Lenders with terms 90 days, 12%. Premier Sales and Trusted Lenders uses a 360-day year for interest calculations. Premier Sales makes adjusting entries at the end of each calendar quarter. Journalize the initiation of the loan, the recognition of interest expense for the quarter and the payment of the note on its due date.2.On August 1, Batson Company issued a 60-day note with a face amount of $120,000 to Jergens Company for merchandiseinventory. (Assume a 360-day year is used for interest calculations.)a. Determine the proceeds of the note assuming the note carries an interest rate of 6%.b.Determine the proceeds of the note assuming the note is discounted at 6%.答案:1. ANS:18,00018,000April 2 Calculations: $13,500x12%x (2/360 days) = $92. On August 1, Batson Company issued a 60-day note with a face amount of$120,000 to Jergens Company for merchandise inventory. (Assume a 360-day year is used for interest calculations.)Determine the proceeds ofthe note assuming the note carries an interest rate of6%. Determine the proceeds ofthe note assuming the note is discounted at 6%. $120,000$118,800$120,000-($120,000 6% 60/360)A company had stock outstanding as follows during each of its first three years of operations:2,500 shares of$10, $100 par, cumulative preferred stock and 50,000 shares of$10 par common stock.The amounts distributed as dividends are presented below. Determine the total and per share dividends for each class of stock for each year by completing the schedule.Preferred Common2. On May 1, 10,000 shares of$10 par common stock were issued at $30, and on May 7, 5,000 shares of$50 par preferred stock were issued at$111. Journalize the entries for May 1 and May 7.3. A corporation purchased for cash 5,000 shares of its own $10 par common stock at $26 a share. In thefollowing year, it sold 2,000 of the treasury shares at $29 a share for cash.(a) Journalize the entries to record the purchase (treasury stock is recorded at cost).Journalize the entries to record the sale of the stock.a. Ib. I2.ANS:a. b. Chap 121. .Year 1 2 3Dividends$10,000 25,00060,000Total Per Share Total Per Share (b)。

(完整word版)会计专业英语复习单词和句子翻译

(完整word版)会计专业英语复习单词和句子翻译Lession 1Information system 信息系统Modern business 现代企业Financinal position 财务状况Financial data 财务数据Financial strength 财务实力Financial report 财务报告Accounting process 会计过程,会计处理方法Financial accounting 财务会计Decision making 决策Managerial accounting 管理会计Financial executives 财务经理Performance report 业绩报告Cost-benefit data 成本—效益数据Cost accounting 成本会计Tax accounting 税务会计Budgetary accounting 预算会计Governmental and not-for—profit accounting 政府及非营利组织会计Human resources accounting 人力资源会计Environmental accounting 环境会计Social accounting 社会会计International accounting 国际会计Tax returns 纳税申报单Lesson 2Financial statement (report)财务报表(报告) Balance sheet 平衡表,资产负债表Income statement 收益表,损益表Statement of cash flows 现金流量表Owners' equity 业主权益At a glance 一瞥Accounting equation 会计等式,会计平衡式,会计方程式Current asset 流动资产Long—term asset 长期资产Normal operating cycle 正常经营周期Other than 除……外,处了Marketable securities 上市证券,有价证券Accounts receivable 应收帐款Prepaid insurance 预付保险费Supplies on hand 在用物料Fixed assets 固定资产Rather than 而不是Plant and equipment 厂场设备Depreciable asset 应折旧资产Original cost 原始成本Store fixtures 店面装置Accumulated depreciation 累计折旧,累积折旧Book value 账面价值Intangible asset 无形资产Lession3Current liability 流动负债Notes payable 应付票据Accrued salaries payable 应付账款Accured salaries payable 应计未付薪金Income tax payable 应付所得税Property tax payable 应付财产税Mortgage payable 应付抵押借款Bonds payable 应付债券,应付公司券Sole proprietorship 独资State corporation law 州公司法(美国)Capital stock 股本Retained earnings 留存收益,保留盈利Legal restrictions 法律约束Undistributed earnings 未分配收益,未分配盈利Engage in 参与Board of directors 董事会Divedend payable 应付股利Lesson4Merchandising company 商业公司Net income 净收益Net loss 净损失Operating results 经营成果Cost of goods sold 销售成本,商品销售成本Operating expenses 营业费用,经营费用Sales returns and allowances 销货退回及折让Sales discounts 销货(售)折让Gross sales 销货(售)总额Net sales 销货(售)净额Beginning inventory 期初存货Net purchases 购货净额Ending inventory 期末存货Purchases returns and allowances 购货退还及折让Purchases discounts 购货折扣Transportation in 购货运费Transportation out 销货运费Cost of goods available for sale 可供销售的商品成本Gross profit on sales 销货(售)毛利Selling expenses 销货(售)费用Administrative expenses 管理费用Sales salaries expense 销货(售)人员薪金Advertising expenses 广告费Depreciation expense 折旧费Insurance expense 保险费Rent expense 租赁费,租金Office salaries expense 办事人员薪金Utilities expense 公用事业(水、电、热)费Supplies expense 物料用品费Interest expense 利息收益Interest income 利息费用Relate to 与……有关Financial income and expense 财务收益和费用Extraordinary items 非常项目Lession5“two-column" account 两栏式账户Normal balance 正常余额Double—entry bookkeeping system 复式记账法,复式记账系统Source document 原始凭证Check stub 支票存根A set of 一组,一套Records of original entry 原始记录簿Chart of accounts 账户一览表,会计科目表Income summary 收益汇总,损益汇总Control account 控制账户,统驭账户,统制账户Subsidiary ledger 辅助分类账,明细分类账Perpetual inventory system 永续盘存制Lession 6Special journal 特种日记账General journal 普通日记账In consrast to 与此对比,与此相反In addition to 除。

国际会计复习资料

国际会计复习资料一、名词解释:1、国际会计P222、欧盟第4号指令P2653、IOSCO P2544、国际转让价格P5095、外汇市场P4086、汇兑损益P4117、外币交易P4128、现行汇率法P4229、信用风险P44910、金融期权P45911、货币互换P46112、战略经营单位P56913、交易风险P61714、合并财务报表P349二、填空:1、观点,是英国公司法提出的对公司财务会计和报告要求的指导思想。

P53真实和公允2、2002年7月,国会通过了《萨班斯-奥克斯莱法案》。

P97美国3、作为法国-西班牙-意大利会模式的基本特征。

P124服从税制需要4、法国财务会计和报告的核心是全国会计法典:。

P126会计总方案5、在法国,会计职业可分为和两种。

职业会计师、注册审计师P1336、对荷兰会计起着最主要、最直接影响的是荷兰的和。

P144公司法、会计职业团体7、三法体制是指在日本在会计领域主要有三部法律约束着企业的会计行为,这三部法律即为、和。

P153《商法》、《证券交易法》《法人税法》8、新加坡的会计准则由新加坡注册会计师协会下属的制定并对外公布。

P188会计准则委员会9、挪威和瑞典只允许使用资产负债表格式。

P195水平式10、是复式簿记的发源地。

P197意大利11、衡量实质性协调和协调化的统计方法最早是由提出的。

P251范塔斯12、致力于国际会计协调的国际组织主要分为和两大类:和。

P254政府类和职业类13、合并会计报表最早出现于。

P350美国14、在实务中,常用的财务报告分析方法有、、和。

P392比较分析、趋势分析、结构分析和比率分析15、是指将以某一外币表示的财务报表折算为另一种特定货币表示的财务报表的会计处理程序。

P418外币财务报表折算16、是指因交易的对方无法履行合同而造成己方财务上的损失。

P449信用风险17、跨国公司运用转移价格的一个重要作用是减轻或逃避各种税收。

主要包括、、三种。

国际会计(完整版)..

Chap 1Q1: Explain how international accounting differs from purely domestic.1.In the domestic case, accounting is an information service that provides financial informationabout a domestic entity to domestic users of that information.2.International accounting is distinctive in that the entity being reported on is either amultinational company (MNC跨国公司) with operations and transactions that transcend national boundaries or involved on entity with reporting obligations to readers who are located outside the reporting entity’s country.Q2: Indentify several internal and external reporting issues that arise when business and investment transcend national borders.External:1.Does translation from one set of measurement rules to another change the information contactof the origin message?(计量规则转换问题)2.Should accounts of foreign operations be translated to parent currency when consolidatedstatement ate prepared?(合并财务报表转换问题)3.Which exchange rates should be employed when translating from one currency to another?(汇率问题)Internal:1.Which exchange rates should be used for budgeting purpose?(编制预算汇率转换)2.Should foreign managers be evaluated in terms of parent currency or the manager operates?(子公司经理人业绩评价用哪种货币)3.Which prices should one use when transferring goods or services between the members of themultinational enterprise cost market, cost-plus, or other cost problem?(在跨国公司不同子公司进行物品或服务的转换的定价问题)Q3:Re-exam Q1.which describes the outsourcing process for HP’s production of the ProLiant Ml 150. For each leg of the production chain, indentify the various accounting and related issues that might arise For step 1 and 2: the idea for the ProLiant Ml 150 is spawned in Singapore and approved in Honstan. ①difference in legal practices regarding rights, and compensation schemes for intellectual properly development may vary between the U.S and Singapore as the latter’s legal system has been influenced by the U.K system. International tax issues also surface in terms of ②royalty payment(印税)arrangements and their tax consequences in both Singapore and the U.S.For step 4:①language communication between Singapore and Taiwan could cause some issues of interpretation. Production in Taiwan raises internal reporting issues such as should ②exchange rate fluctuation between the Taiwanese dollar and the U.S dollar be incorporated into the cost of production or accounted for separately as a non-operating foreign exchange gain or loss.(非主营汇兑利得或损失). In ③evaluating the creditworthiness (借贷信用)of the Taiwanese manufacturer, should the financial statements of the Taiwanese manufacturer be translated to U.S. GAAP or not. If a ratio analysis is performed, should ④Taiwanese liquidity(流动性)and solvency ratios(长期偿债能力)be interpreted based on U.S. financial norms or Taiwanese norms?Step 5: should clients in Southeast Asian countries be charged ①identical prices(均一价格)or should prices be flexed(弹性)for differences in charge rates, transportation arrangement(运输费用)ect. What ②legal issues(法律问题)are raised in the case of bribes (贿赂)expected or the part of commercial buyers(商业买家)and how would these payments be treated under the U.S Foreign Corrupt Practice Act(美国国外贿赂行为法).Q4: Revisit 1-6 (P10), calculate the 2005’s ROE(Return on Equity 股本回报率) for Electralux under IFRS and GAAP respectively.Chap 2Q1:This chapter identifies 7 economics, sociohistorical(社会历史),and institutional factors believed to influence accounting development.1. Explain how each one effect accounting practice.(Book Page 27-30, teacher underlined in class)2. What are effects if 7 factors?There are 2 combinations:①Common law legal system + Strong equity markets + Separation of financial and taxaccounting②Code law legal system + Credit-based financing (bank) + Accounting rules conform to tax lawQ2: Refer to previous Q1, rank them from the most to least important as far as accounting development is concerned, then justify both the top and bottom items in your ranking.1.Sources of finance2.Legal system3.Taxation4.Political and economic tiescation levels6.Inflation7.Level of economic developmentQ3:Are national differences in accounting practice better explained by culture or by economic and legal factors? Why?1.This question is controversial and there is no course of option at present.2.Economic and legal factors are more clearly linked to specific features pf accounting, whereascultural variables are linked to broader generalization(概念通则)about accounting.3.However, culture exerts a second-order effect on accounting(文化对会计的影响在第二位)。

国际会计复习资料 2