现金流量表英文课件

现金流量表中英文版

行次 本年累计 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64

现金流量表

单位名称:

项目

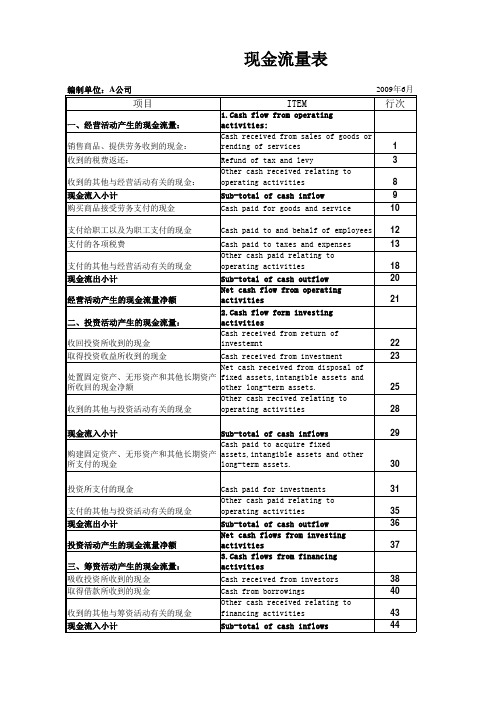

一、经营活动产生的现金流量 cash flow from operating activities 销售商品和提供劳务收到的现金 cash from selling commodities or offering labor 收到的税费返还 refund of tax and fee received 收到的其他与经营活动有关的现金 other cash received related to operating activities 现金流入小计 cash inflow subtotal 购买商品、接受务支付的现金 cash paid for commodities or labor 支付给职工以及为职工支付的现金 cash paid to and for employees 支付的各项税费 taxes and fees paid 支付的其他与经营活动有关的现金 other cash paid related to operating activities 现金流出小计 cash outflow subtotal 经营活动产生的现金流量净额 cash flow generated from operating activities net amount 二、投资活动产生的现金流量 cash flow from investing activities 收回投资所收到的现金 cash from investment with drawal 取得投资收益所收到的现金 cash from investment income 处置固定资产无形资产和其他长期资产所收回的现金净额 net cash from disposing fixed assets,intangible assets and other long-term assets 收到的其他与投资活动有关的现金 other cash received related to investing activities 现金流入小计 cash inflow subtotal 购建固定资产无形资产和其他长期资产所支付的现金 cash paid for buying fixed assets,intangible assets and other long-term investment 投资所支付的现金 cash paid for investment 支付的其他与投资活动有关的现金 other cash paid related to investing activities 现金流出小计 cash outflow subtotal 投资活动产生的现金流量净额 cash flow generated from investing activities net amount 三、筹资活动产生的现金流量 cash flow from financing activities 吸收投资所收到的现金 cash received from accepting investment 借款所收到的现金 Cash from borrowings 收到的其他与筹资活动有关的现金 Other cash received relating to financing activities 现金流入小计 cash inflow subtotal 偿还债务所支付的现金 Cash repayments of amount borrowed 分配股利、利润或偿付利息所支付的现金 Cash payments for distrbution of dividends or profits 支付的其他与筹资活动有关的现金 Other cash payment relating to financing activities 现金流出小计 cash outflow subtotal 筹资活动产生的现金流量净额 Net cash flows from financing activities 四、汇率变动对现金的影响 Effect of foreign exchang rate changes on cash Net increase in cash and cash equivalents 五、现金及现金等价物净增加额

现金流量表英语

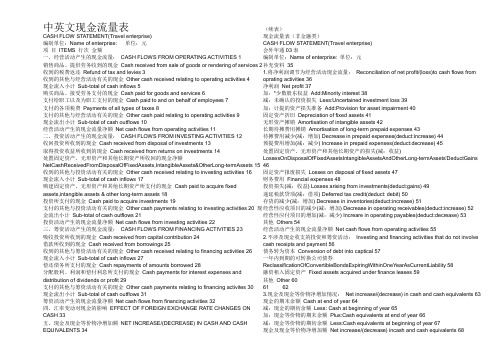

Project Row No_Amount 1. Cash Flow from Operating Activities00 Cash from selling commodities or offering labor10 Refund of tax and fee received20 Other cash received related to operating activities30 Cash InflowSubtotal40 Cash paid for commodities or labor50 Cash paid to and for employees60 Taxes and fees paid70 Other cash paid related to operating activities80 Cash OutflowSubtotal90 Cash flow generated from operating activitiesNet Amount100 2. Cash Flow from Investing Activities00 Cash from investment withdrawal110 Cash from investment income120 Net cash from disposing fixed assets, intangible assets an130 Other cash received related to investing activities140 Cash InflowSubtotal150 Cash paid for buying fixed assets, intangible assets and oth160 Cash paid for investment170 Other cash paid related to investing activities180 Cash OutflowSubtotal190 Cash flow generated from investing activitiesNet Amount200 3. Cash Flow from Financing Activities00 Cash received from accepting investment210 Borrowings220 Other cash received related to financing activities230 Cash InflowSubtotal240 Cash paid for debt250 Cash paid for dividend , profit or interest260 Other cash paid related to financing activities270 Cash OutflowSubtotal280 Cash flow from financing activitiesNet Amount2904. Foreign Currency Translation Gains(Losses)3205. Net Increase Of Cash and Cash Equivalents330 Supplementary Schedule:00 Indirect Method00 1. Convert net profit to cash flow from operating activities00 Net profit340 Provision for asset losses350 Depreciation for fixed assets360 Amortization of intangible assets370 Amortization of long-term deferred expenses380 Decrease of deferred expenses390 Increase of accrued expenses400 loss of disposing fixed assets, intangible assets and other l410 Scrap loss of fixed assets420 Financial expenses430 Investment losses440 Deferred tax liabilities450 Decrease of inventory460 Decrease of operation receivables470 Increase of operation payables480 Others490 Net cash from operating activities5002. Investing and financing activities not involved in cash00 Debt converted to capital510 Convertible bond maturity within one year520 Leasehold improvements5303. Net increase of cash and cash equivalents00 Cash ending bal.542789591 Less: cash beginning bal.552789591 Plus: cash equivalents' ending bal.560 Less: cash equivalents' beginning bal.570 Net increase of cash and cash equivalents580项目行次金额一、经营活动产生的现金流量00销售商品、提供劳务收到的现金10收到的税费返还20收到的其它与经营活动有关的现金30现金流入小计40购买商品、接受劳务支付的现金50支付给职工以及为职工支付的现金60支付的各项税费70支付的其它与经营活动有关的现金80现金流出小计90经营活动产生的现金流量净额100二、投资活动产生的现金流量00收回投资所收到的现金110取得投资收益所收到的现金120处置固定资产、无形资产和其他长期资产所收回的现金净额130收到的其它与投资活动有关的现金140现金流入小计150购建固定资产、无形资产和其他长期资产所支付的现金160投资所支付的现金170支付的其他与投资活动有关的现金180现金流出小计190投资活动产生的现金流量净额200三、筹资活动产生的现金流量00吸收投资所收到的现金210借款所收到的现金220收到的其它与筹资活动有关的现金230现金流入小计240偿还债务所支付的现金250分配股利、利润或偿付利息所支付的现金260支付的其它与筹资活动有关的现金270现金流出小计280筹资活动产生的现金流量净额290四、汇率变动对现金的影响320五、现金及现金等价物净增加额330补充资料:00现金流量附表项目00 1、将净利润调节为经营活动现金流量00净利润340计提的资产减值准备350固定资产折旧360无形资产摊销370长期待摊费用摊销380待摊费用减少390预提费用增加400处理固定资产、无形资产和其他长期资产的损失410固定资产报废损失420财务费用430投资损失440递延税款贷项450存货的减少460经营性应收项目的减少470经营性应付项目的增加480其他490经营活动产生的现金流量净额5002、不涉及现金收支的投资和筹资活动00债务转为资本510一年内到期的可转换公司债券520融资租入固定资产5303、现金及现金等价物净增加情况00现金的期末余额542789591减:现金的期初余额552789591加:现金等价物的期末余额560减:现金等价物的期初余额570现金及现金等价物的净增加额580。

会计英语第九章现金流量表第一组

LOGO

过渡页

TRANSITION PAGE

Chapter 9

— 17 —

9.3 Preeparing Cash Flow Statement -------Direct Method

LOGO

— *—

Chapter 9

Statement of

Cash

Flows

— 18 —

• Direct method is based on individual item in income statement. Major classes of revenues are shown as gross cash inflows from operations, and expenses are shown as gross cash outflows from operations. The information necessary to determine the operating cash flows is obtained by adjusting sales, LOGO

A statement of cash flows reports the cash

receipts and cash payments of an entity during period.It explains the causes for the changes in cash

by providing information about operating,financing

Cash is cash on hand and deposits that are

readily available for payment.

Cash equivalents are highly liquid short-term

现金流量表 CASH FLOW STATEMENT(中英文对照版)

第 2 页,共 2 页

line(行)

1 2 3 4 5 6 7 8 9 10 11 12 13 15 16 17 18 19 20 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46

第 1 页,共 2 页

ITEMS Increase in prepaid expenses(deduct:decrease) LossesOnDisposalOfFixedAssetsIntangibleAssetsAndOtherLong-termAssets'DeductGains Losses on disposal of fixed assets Financial expenses Losses arising from investments(deduct:gains) Deferred tax credit(deduct: debit) Decrease in inventories(deduct:increase) Decrease in operating receivables(deduct:increase) Increare in operating payables(deduct:decrease) Others Net cash flows from operating activities 2、 Investing and financing activities that do not involve cash receipts and payment: Conversion of debt into captical Re class ification Of Convertible Bonds Expiring Within One Year As Current Liability Fixed assets acquired under finance leases Other 3、 Net increase/(decrease) in cash and cash equivalents: Cash at end of year Less: Cash at beginning of year Plus:Cash equivalents at end of year Less:Cash equivalents at beginning of year Net increase/(decrease) incash and cash equivalents

英文会计现金流量表PPT课件

-

7

THANKS FOR YOUR COMING

-

8

Need for additional financing for the future period

Ability to pay dividends and meet obligations

Transactions involving cash and noncash investment and

Function of the Statement of Cash Flows

-

1

PART ONE

The function of the statement of cash flows acts a very important part.

There are three primary purposes of the statement.

Another purpose

It is useful to management and external users.

Cash Flows

-

3

PART ONE

Why we need the statement of cash flows? 现金净流量=现金流入-现金流出 利润=收入-费用 BUT 收入≠现金流入 费用≠现金流出

-

2

PART ONE

To provide information that couldn’t be provided in balance sheet and the income statement .

Secondary purpose

Primary purpose

现金流量表_模板(中英对照)

Cash Inflow Subtotal

现金流入小计

Depreciation for fixed assets

固定资产折旧

Cash paid for commodities or labor

购买商品、接受劳务支付的现金

Amortization of intangible assets

现金流出小计

Loss of disposing fixed assets,intangible assets and other long-term assets (Less: profit)

处置固定资产、无形资产和其他长期资产的损失(减:受益)

Cash flow generated from operating activities Net Amount

Cash received from accepting investment

吸收投资所收到的现金

increase of cash and cash equivalents

3.现金及现金等价物净增加情况

Cash Flows Statement

现金流量表

Tabulatedby编制单位:Date日期:Unit单位: RMB Yuan元

Items项目

Line No.行次

Amount金额

Items项目

Line No.行次

Amount

金额

I. Cash Flow from Operating Activities

投资活动产生的现金流量净额

Convertible bond maturity within one year

一年内到期的可转换公司债券

III. Cash Flow from Financing Activities

现金流量表中英文版

Cash Flow Statement(现金流量表 Period:(日期)

Item(项目) Ⅰ Cash flows from operating activities:(一、经营活动产生的现金流量)

Cash received from the sale of goods or rendering of services(销售商品、提供劳务收到的现金) Refunds of taxes(收到的税费返还) Other cash receipts relating to operating activities(收到的其他与经营活动有关的现金) Sub-total of cash inflows(现金流入小计) Cash paid for goods and services(购买商品、接受劳务支付的现金) Cash paid to and on behalf of employees(支付给职工以及为职工支付的现金) Payments of all types of taxes(支付的各项税费) Other cash payments relating to operating activities(支付的其他与经营活动有关的现金) Sub-total of cash outflows(现金流出小计) Net cash flows from operating activities(经营活动产生的现金流量净额) Ⅱ Cash flows from investing activities:(投资活动产生的现金流量) Cash received from return of the investments(收回投资所收到的现金) Cash received from return on investment(取得投资收益所收到的现金) Net cash received from the sale of fixed assets intangible assets and other long-term assets(处置固定资产、无形资产和其他长期资产所收回 Other cash receipts relating activities(收到的其他与投资活动有关的现金)

现金流量表中英文(cash flow statement)

22 23

Cash received from investment Net cash received from disposal of fixed assets,intangible assets and 处置固定资产、无形资产和其他长期资产所收回的现金净额 other long-term assets. Other cash recived relating to 收到的其他与投资活动有关的现金 operating activities 现金流入小计 Sub-total of cash inflows Cash paid to acquire fixed assets,intangible assets and other 购建固定资产、无形资产和其他长期资产所支付的现金 long-term assets. 投资所支付的现金 支付的其他与投资活动有关的现金 现金流出小计 投资活动产生的现金流量净额 三、筹资活动产生的现金流量: 吸收投资所收到的现金 取得借款所收到的现金 收到的其他与筹资活动有关的现金 现金流入小计 偿还债务所支付的现金 Cash paid for investments Other cash paid relating to operating activities Sub-total of cash outflow Net cash flows from investing activities 3.Cash flows from financing activities Cash received from investors Cash from borrowings Other cash received relating to financing activities Sub-total of cash inflows

现金流量表中英文版

现金流量表中英文版现金流量表(非金融类)CASH FLOW STATEMENT(Travel enterprise)会外年通03表编制单位:Name of enterprise: 单位:元项目 ITEMS 行次金额一、经营活动产生的现金流量: CASH FLOWS FROM OPERATING ACTIVITIES 1销售商品、提供劳务收到的现金 Cash received from sale of goods or rendering of services 2收到的税费返还 Refund of tax and levies 3收到的其他与经营活动有关的现金 Other cash received relating to operating activities 4现金流入小计 Sub-total of cash inflows 5购买商品、接受劳务支付的现金 Cash paid for goods and services 6支付给职工以及为职工支付的现金 Cash paid to and on behalf of employees 7支付的各项税费 Payments of all types of taxes 8支付的其他与经营活动有关的现金 Other cash paid relating to operating activities 9现金流出小计 Sub-total of cash outflows 10经营活动产生的现金流量净额 Net cash flows from operating activities 11二、投资活动产生的现金流量: CASH FLOWS FROM INVESTING ACTIVITIES 12收回投资所收到的现金 Cash received from disposal of investments 13取得投资收益所收到的现金 Cash received from returns on investments 14处置固定资产、无形资产和其他长期资产所收回的现金净额NetCashReceivedFromDisposalOfFixedAssets,IntangibleAssets&OtherLong-termAssets 15收到的其他与投资活动有关的现金 Other cash received relating to investing activities 16现金流入小计 Sub-total of cash inflows 17购建固定资产、无形资产和其他长期资产所支付的现金 Cash paid to acquire fixed assets,intangible assets & other long-term assets 18投资所支付的现金 Cash paid to acquire investments 19支付的其他与投资活动有关的现金 Other cash payments relating to investing activities 20现金流出小计 Sub-total of cash outflows 21投资活动产生的现金流量净额 Net cash flows from investing activities 22三、筹资活动产生的现金流量: CASH FLOWS FROM FINANCING ACTIVITIES 23吸收投资所收到的现金 Cash received from capital contribution 24借款所收到的现金 Cash received from borrowings 25收到的其他与筹资活动有关的现金 Other cash received relating to financing activities 26现金流入小计 Sub-total of cash inflows 27偿还债务所支付的现金 Cash repayments of amounts borrowed 28分配股利、利润和偿付利息所支付的现金 Cash payments for interest expenses and distribution of dividends or profit 29支付的其他与筹资活动有关的现金 Other cash payments relating to financing activites 30现金流出小计 Sub-total of cash outflows 31筹资活动产生的现金流量净额 Net cash flows from financing activities 32四、汇率变动对现金的影响 EFFECT OF FOREIGN EXCHANGE RATE CHANGES ON CASH 33五、现金及现金等价物净增加额 NET INCREASE/(DECREASE) IN CASH AND CASH EQUIVALENTS 34(续表)现金流量表(非金融类)CASH FLOW STATEMENT(Travel enterprise)会外年通03表编制单位:Name of enterprise: 单位:元补充资料 351.将净利润调节为经营活动现金流量: Reconciliation of net profit/(loss)to cash flows from oprating activities 36净利润 Net profit 37加:*少数股东权益 Add:Minority interest 38减:未确认的投资损失 Less:Uncertained investment loss 39加:计提的资产损失准备 Add:Provision for asset impairment 40固定资产折旧 Depreciation of fixed assets 41无形资产摊销 Amortisation of intangible assets 42长期待摊费用摊销 Amortisation of long-term prepaid expenses 43待摊费用减少(减:增加) Decrease in prepaid expenses(deduct:increase) 44预提费用增加(减:减少) Increase in prepaid expenses(deduct:decrease) 45处置固定资产、无形资产和其他长期资产的损失(减:收益) LossesOnDisposalOfFixedAssetsIntangibleAssetsAndOtherLong-termAssets'DeductGains 46固定资产报废损失 Losses on disposal of fixed assets 47财务费用 Financial expenses 48投资损失(减:收益) Losses arising from investments(deduct:gains) 49递延税款贷项(减:借项) Deferred tax credit(deduct: debit) 50存货的减少(减:增加) Decrease in inventories(deduct:increase) 51经营性应收项目的减少(减:增加) Decrease in operating receivables(deduct:increase) 52经营性应付项目的增加(减:减少) Increare in operating payables(deduct:decrease) 53其他 Others 54经营活动产生的现金流量净额 Net cash flows from operating activities 552.不涉及现金收支的投资和筹资活动: Investing and financing activities that do not involve cash receipts and payment 56 债务转为资本 Conversion of debt into captical 57一年内到期的可转换公司债券 ReclassificationOfConvertibleBondsExpiringWithinOneYearAsCurrentLiability 58融资租入固定资产 Fixed assets acquired under finance leases 59其他 Other 6061623.现金及现金等价物净增加情况: Net increase/(decrease) in cash and cash equivalents 63现金的期末余额 Cash at end of year 64减:现金的期初余额 Less: Cash at beginning of year 65加:现金等价物的期末余额 Plus:Cash equivalents at end of year 66减:现金等价物的期初余额 Less:Cash equivalents at beginning of year 67现金及现金等价物净增加额 Net increase/(decrease) incash and cash equivalents 68。

现金流量表-英文

现金流分析(英文)(ppt 66页)

• Operating profits • Decrease in

working capital

• Operating losses • Increase in working

capital

• Ability of a company’s

investment decisions to generate cash

Cash flow is the measure of a company’s strategic value.

• The market value of a company is equal to the present value of its

expected future cash flows

• Accounting methods can be used to “manage” earnings; CASH is

harder to manipulate

Cash is King!

bc

BOS CU7010598KRA 5 Copyright© 1998 Bain & Company, Inc.

bc

BOS CU7010598KRA 9 Copyright© 1998 Bain & Company, Inc.

Cash Flow

Investing Cash Flow

Investing cash flow measures the use of a business’s cash for the acquisition of non-current assets.

• Investments in ongoing operations - property, plant and equipment - are

现金流量表英文版ch07 statement of cash flows.ppt

13

The operating cash flows section of the statement of cash flows under the indirect method would appear something like this:

11

financing activities are:

(a) cash proceeds from issuing shares or other equity instruments;

(b) cash payments to owners to acquire or redeem the enterprise's shares;

Bank overdrafts which are repayable on demand and which form an integral part of an enterprise's cash management are also included as a component of cash and cash equivalents.

Guidance notes indicate that an investment normally meets the definition of a cash equivalent when it has a maturity of three months or less from the date of acquisition.

中英文现金流量表

中英文现金流量表 CASH FLOW STATEMENT(Travel enterprise) 编制单位:Name of enterprise: 单位:元 项 目 ITEMS 行次 金额 一、经营活动产生的现金流量: CASH FLOWS FROM OPERATING ACTIVITIES 1 销售商品、提供劳务收到的现金 Cash received from sale of goods or rendering of services 2 收到的税费返还 Refund of tax and levies 3 收到的其他与经营活动有关的现金 Other cash received relating to operating activities 4 现金流入小计 Sub-total of cash inflows 5 购买商品、接受劳务支付的现金 Cash paid for goods and services 6 支付给职工以及为职工支付的现金 Cash paid to and on behalf of employees 7 支付的各项税费 Payments of all types of taxes 8 支付的其他与经营活动有关的现金 Other cash paid relating to operating activities 9 现金流出小计 Sub-total of cash outflows 10 经营活动产生的现金流量净额 Net cash flows from operating activities 11 二、投资活动产生的现金流量: CASH FLOWS FROM INVESTING ACTIVITIES 12 收回投资所收到的现金 Cash received from disposal of investments 13 取得投资收益所收到的现金 Cash received from returns on investments 14 处置固定资产、无形资产和其他长期资产所收回的现金净额 NetCashReceivedFromDisposalOfFixedAssets,IntangibleAssets&OtherLong-termAssets 15 收到的其他与投资活动有关的现金 Other cash received relating to investing activities 16 现金流入小计 Sub-total of cash inflows 17 购建固定资产、无形资产和其他长期资产所支付的现金 Cash paid to acquire fixed assets,intangible assets & other long-term assets 18 投资所支付的现金 Cash paid to acquire investments 19 支付的其他与投资活动有关的现金 Other cash payments relating to investing activities 20 现金流出小计 Sub-total of cash outflows 21 投资活动产生的现金流量净额 Net cash flows from investing activities 22 三、筹资活动产生的现金流量: CASH FLOWS FROM FINANCING ACTIVITIES 23 吸收投资所收到的现金 Cash received from capital contribution 24 借款所收到的现金 Cash received from borrowings 25 收到的其他与筹资活动有关的现金 Other cash received relating to financing activities 26 现金流入小计 Sub-total of cash inflows 27 偿还债务所支付的现金 Cash repayments of amounts borrowed 28 分配股利、利润和偿付利息所支付的现金 Cash payments for interest expenses and distribution of dividends or profit 29 支付的其他与筹资活动有关的现金 Other cash payments relating to financing activites 30 现金流出小计 Sub-total of cash outflows 31 筹资活动产生的现金流量净额 Net cash flows from financing activities 32 四、汇率变动对现金的影响 EFFECT OF FOREIGN EXCHANGE RATE CHANGES ON CASH 33 五、现金及现金等价物净增加额 NET INCREASE/(DECREASE) IN CASH AND CASH EQUIVALENTS 34 (续表)现金流量表(非金融类)CASH FLOW STATEMENT(Travel enterprise)会外年通03表编制单位:Name of enterprise: 单位:元补充资料 351.将净利润调节为经营活动现金流量: Reconciliation of net profit/(loss)to cash flows from oprating activities 36净利润 Net profit 37加:*少数股东权益 Add:Minority interest 38减:未确认的投资损失 Less:Uncertained investment loss 39加:计提的资产损失准备 Add:Provision for asset impairment 40固定资产折旧 Depreciation of fixed assets 41无形资产摊销 Amortisation of intangible assets 42长期待摊费用摊销 Amortisation of long-term prepaid expenses 43待摊费用减少(减:增加) Decrease in prepaid expenses(deduct:increase) 44预提费用增加(减:减少) Increase in prepaid expenses(deduct:decrease) 45处置固定资产、无形资产和其他长期资产的损失(减:收益)LossesOnDisposalOfFixedAssetsIntangibleAssetsAndOtherLong-termAssets'DeductGains 46固定资产报废损失 Losses on disposal of fixed assets 47财务费用 Financial expenses 48投资损失(减:收益) Losses arising from investments(deduct:gains) 49递延税款贷项(减:借项) Deferred tax credit(deduct: debit) 50存货的减少(减:增加) Decrease in inventories(deduct:increase) 51经营性应收项目的减少(减:增加) Decrease in operating receivables(deduct:increase) 52 经营性应付项目的增加(减:减少) Increare in operating payables(deduct:decrease) 53 其他 Others 54经营活动产生的现金流量净额 Net cash flows from operating activities 552.不涉及现金收支的投资和筹资活动: Investing and financing activities that do not involve cash receipts and payment 56债务转为资本 Conversion of debt into captical 57一年内到期的可转换公司债券ReclassificationOfConvertibleBondsExpiringWithinOneYearAsCurrentLiability 58融资租入固定资产 Fixed assets acquired under finance leases 59其他 Other 6061 623.现金及现金等价物净增加情况: Net increase/(decrease) in cash and cash equivalents 63 现金的期末余额 Cash at end of year 64减:现金的期初余额 Less: Cash at beginning of year 65加:现金等价物的期末余额 Plus:Cash equivalents at end of year 66减:现金等价物的期初余额 Less:Cash equivalents at beginning of year 67现金及现金等价物净增加额 Net increase/(decrease) incash and cash equivalents 68。

现金流量表英文版ch07 statement of cash flows

(a) cash payments to acquire property, plant and equipment, intangibles and other long-term assets. These payments include those relating to capitalised development costs and self-constructed property, plant and equipment;

(c) cash payments to suppliers for goods and services;

(d) cash payments to and on behalf of employees;

5

Examples of cash flows arising from

11

investing activities are:

8

Taxes on Income

11

cash flows arising from taxes on income are normally classified as operating, unless they can be specifically identified with financing or investing activities

Cash receipts from customers

中英现金流量表

支付给职工以及 为职工支付的现金

支付的各项税费 经营活动产生的 现金流量净额

Cash paid to and on behalf of employees

Payments of all types of taxes Net cash flows from operating activities

01

Cash paid to acquire investments

Net cash flows from investing activities

02

PART 01

中英文现金流量表——正表 中英文现金流量表

三、筹资活劢产生的现金流量 CASH FLOWS FROM FINANCING ACTIVITIES 吸收投资所收到的现金 Cash received from capital contribution

PART 01

中英文现金流量表——正表 中英文现金流量表

二、投资活劢产生的现金流量 CASH FLOWS FROM INVESTING ACTIVITIES 收回投资所收到的现金 取得投资收益所收到的现金 处置固定资产、无形资产和 其他长期资产收回现金净额 购建固定资产、无形资产和 其他长期资产所支付的现金 投资所支付的现金 投资活动产生的 现金流量净额 Cash received from disposal of investments Cash received from returns on investments

销售商品、提供劳务 收到的现金

收到的税费返还 购买商品、接受劳务 支付的现金

Cash received from sale of goods or rendering of services

Refund of tax and levies Cash paid for goods and services

现金流量表中英文(cash flow statement)

22 23

Cash received from investment Net cash received from disposal of fixed assets,intangible assets and 处置固定资产、无形资产和其他长期资产所收回的现金净额 other long-term assets. Other cash recived relating to 收到的其他与投资活动有关的现金 operating activities 现金流入小计 Sub-total of cash inflows Cash paid to acquire fixed assets,intangible assets and other 购建固定资产、无形资产和其他长期资产所支付的现金 long-term assets. 投资所支付的现金 支付的其他与投资活动有关的现金 现金流出小计 投资活动产生的现金流量净额 三、筹资活动产生的现金流量: 吸收投资所收到的现金 取得借款所收到的现金 收到的其他与筹资活动有关的现金 现金流入小计 偿还债务所支付的现金 Cash paid for investments Other cash paid relating to operating activities Sub-total of cash outflow Net cash flows from investing activities 3.Cash flows from financing activities Cash received from investors Cash from borrowings Other cash received relating to financing activities Sub-total of cash inflows

现金流量-现金流量表英文版 精品

4

11 Examples of cash flows from operating activities are:

(a) cash receipts from the sale of goods and the rendering of services;

(b) cash receipts from royalties, fees, commissions and other revenue;

3

11 2. Presentation of the Statement

of Cash Flows

Cash flows must be analysed between operating, investing and financing activities.

Operating activities are the principal revenue-

disposal of long-term assets and other investments not included in cash equivalents.

Financing activities are activities that result in changes

in the size and composition of the equity capital and borrowings of the enterprise.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1. 2. 3.

4.

5. 6. 7.

Effect On profit on cash Repayment of a loan none decrease Making a sale on credit increase none Buying a non-current asset for cash none decrease Receiving cash from a debtor none increase Depreciating a non-current asset decrease none Buying some inventories for cash none decrease Making a share issue for cash none increase

②

投资现金流(CFI) 源于购置不动产、厂房和设备或是兼并子公司或机构部门、购买或出售 对其他公司的投资。

• • • • •

处置资产 处置固定资产、无形资产和其他长期资产 (购买投资) (购买固定资产、无形资产和其他长期资产) 投资活动产生的净现金流量

③

筹资现金流(CFF) 这个金额是以发行股票、债券的现金收入减去偿还债务和支付股东股利 等现金流出而计算出来的。

Cash flow statement

Cash flow statement The importance of cash

Topic

Features of cash flow statement

Comparison between Income statement and Cash flow statement Format Relationship between the three financial statements

In-class activity: income vs. cash

Biblioteka How profit and cash for a period may be affected differently by particular transactions or events. The following is a list of business/accounting events. In each case, state the effect (increase, decrease or no effect) on both profit and cash.

The relationship between the three financial statements

Owner’ s claim Balance sheet at the start of the accounting period Assets (Cash) Cash flow statement Income statement (profit and loss account) Owner’s claim Balance sheet at the end of the accounting period Assets (Cash)

No regulation Any financial information contained within these two statements

Can Income Statement answer the cash question?

钱 赚钱 赢利

“赚钱”,“赢利”

金融学角度: “赚钱”vs.“赢利”

真正的商业活动注重的是:

数字意义上的赢利 最终的真实收入 “赚钱”不等于“赢利” 是资金的流动。

“赚钱”和“赢利”一样吗?

“赢利”的一个麻烦 数学家、统计学家和会计师同时接受面试官的 提问。面试官的问题是“2+2等于几”。

“等于4。” “应该等于4,其误差无限趋近于零。” “能不能让他们先暂时回避一下”,“你想让2+2 等于几?”

The importance of cash

When compared with the balance sheet, income statement

Bone Muscle Blood

企业的底子 企业的面子 真正的居家过日子

Who is King today?

Product is King

“发现一个好公司的秘密——解读现金流量表”

/s/blog_5dcde5e70100qs6 9.html

如何解读“现金为王” /p-800815582904.html /view/d0ff1840a8956b ec0975e30c.html 现金为王:现金可随时调动,资产不能随时变 为现金。如有急需;古董、楼宇、厂房、地皮、 物业、金银手饰、钻石都不能马上变现金。

Take the example of a business making a sale

Standard layout of CFS

造血功能 每股经营活动现金流量 支付给职工以及为职工 支付的现金 Cash flows from operating activities plus or minus Cash flows from investing activities plus or minus Cash flows from financing activities equals

营业额=15 000日元×6 000台=9 000万日元 成本=10 000日元×6 000台=6 000万日元 赢利=9 000万日元-6 000万日元=3 000万 日元 会计学角度:

进货、销售额 进货:已经支付了1亿日元的现金 销售额却只有9 000万日元 资金环节:1000万日元的赤字

日本从美国进口BBQ烤炉进行销售。一台烤炉 的采购价格是10 000日元,计划以每台15 000 日元的价格出售。这样每售出一台烤炉就能得 到5 000日元的赢利。 假设4月份进货10 000台烤炉,到12月的时候 销售出去6 000台。那么在这种情况下,本年 度的销售情况(损益表)如何编制?

BBQ烤炉的损益表

Technology is King

壁炉如何赚钱?

Who is King today?

1. 2. 3. 4. … 管理 营销 渠道

沃尔玛、苏宁、国美

5. 终端

盛大收购Actoz公司,联想收购IBM全球PC业务

6. 资源:水、电、气、煤、油、矿、森林、土地、 粮食 7. 现金

After-class exercise

Depreciation derivation

For example: 10万日元购入的榨汁机,耐用期 为5年

定额法:产生2万日元的减价折旧费,最后卖出时 产生了1万日元的赢利。 定率法:减价折旧费按照投资额的一定折旧率[(1 /耐用年数)×250%=0.5]计算,是5万日元,产 生2万日元的赤字 会计学规则在不同国家有不同的计算方式。

“10年前的民营企业,现在还活着的不到20%。 主要问题其实不是管理不善,而是财务危机— —投资失误导致资金紧张,最后资金链断 裂。 ” “最怕现金流出问题 ”

The position of Cash Flow Statement

A recent addition to the set of financial statements

Conclusion

To gain an insight into cash movements over time

the income statement is not the answer. This may lead to an increase in wealth and will be reflected in the income statement If the sale is made on credit No cash changes hands The profit and the cash generated for a period will rarely go hand in hand.

Sample of cash flow statement

ABC公司现金流量表 2010年12月31日

经营活动中的现金流量

净利润 折旧 存货的增加 经营活动现金流量总计 23.4 30 (28) 25.4 (90) (10) 94.6 20

投资活动中的现金流量

房屋及设备投资

筹资活动中的现金流量

股利支付 短期负债的增加 现金的变动

Importance of cash

What are responsible for the success and failure of a business?

Case study

/society/201008/75016bea5b84-472e-a1c0-177b643a46db.shtml

Net increase (or decrease) in cash and cash equivalents over the period

放血功能

输血功能

现金流量表:格式

①

经营活动现金流(CFO) 包括了所有既不属于投资又不属于筹资的交易事项而产生的现金流 量。

• • • • •

销售产品或提供劳务所收到的现金 (购买支付的现金) (支付给员工的现金) (支付所得税等各种税收的现金) 经营活动产生的净现金流量

接受股东投资收到的现金 接受债权性投资收到的现金 (偿还债务支付的现金) (偿还利息支付的现金) (支付股利支付的现金) 筹资活动产生的净现金流量