JOURNAL OF REAL ESTATE RESEARCH Factors Affecting Foreign Investor Choice in Types of U.S.

五,外文原版期刊目录(2002年)

297B0009

Journal of Financial and Quantitative Analysis

金融与数量分析

季

95--2002

20.

297B0073

Financial Analysts Journal.

金融分析家杂志

季

97--2002

21

297B0094

297C0052

Financial Management #

国际管理与决策杂志(英)

4/y

图书馆

3424元

47

714 LB057

International Journal of Industrial organization

工业组织的国际学报

12/

9521元

48

715B0119

Journal of Environment Economics and Management

Financial Management

财务管理(网上)

财务管理

4/y

月

95--2002

22

297B0098

Strategic Finance.

财政策略

月

99--2002

23

297B0237

297B0237

297B0237

The Journal of Real Estate Research

The Journal of Real Estate Portfolio Management #

工程经济学家

(网上)

2/y

95--2002

34

714B0063-A

Management Science

大学英语试卷

Test ThreeI. WritingDirections: For this part, you are allowed 30 minutes to write a composition on the topic: A Letter to the President of the University about Improving the Sports Facilities on Campus. You should write no more than 120 words, and base your composition on the outline given below in Chinese:假设你是李明,请你写一封信给校长,建议改善本校体育设施状况,内容应涉及体育设施对大学生的重要性,对目前学校体育设施的状况可以表扬,可以提出批评建议,也可以兼而有之。

A Letter to the President of the University________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _________________________________________________________________________________ _____________________________________________________________________________Ⅱ. Multiple Choices1. _______ his earnings as a football coach, he also owns and runs a chain of sports shops.A. ExceptB. besideC. Apart fromD. Except for2. He felt that he_______ the coldness that had grown between them.A. was blamed toB. was to blame forC. was to be blamed forD. blamed3. The manager promised to keep us _____ of how our business was going on.A. informedB. informingC. knowingD. known4. Besides this, it also provides ___________ other choices for its readers.A. a bit ofB. a great deal ofC. a large amount ofD. a large number of5. You’d better not _______ these two sentences, otherwise the readers cannot fully understand you.A. move outB. leave outC. pick outD. take out.A迁出;B遗漏;iC挑选出;D取出;6. The UK ________ Great Britain and Northern Ireland, is a country famous _____ its history.A. consisted of , forB. consisting of, asC. consisting of , forD. consisted of, as7. Enough of it! Nobody here thinks what you are saying should make any ______.A. valueB. useC. funD. sense.8. After recovering from his illness, he was advised to ________ gardening as a hobby.A. take awayB. take offC. take onD. take up9. We’ll have a party tomorrow and all the decoratio ns are ________.A. in hand.B. in useC. in place.D. in time.10. The computer system ______ suddenly while he was searching for information on the Internet.A. broke downB. broke outC. broke upD. broke in11. Just go to the shop, show them the dress, and demand that they _______ the damage.A. will pay forB. are paying forC. must pay forD. should pay for12. __________ not to miss the flight at 15:20, the manager set out for the airport in a hurry.A. RemindingB. RemindedC. To remindD. Having reminded13. In the dream Peter saw himself _____ by a fierce wolf, and woke suddenly with a start.A. chasedB. to be chasedC. be chasedD. having been chased.14. He said he never heard this word _______ in spoken English.A. useB. to useC. usingD. used15. Though _____ money, his parents managed to send him to university.A. lackingB. lackC. lackedD. to lack16. From the ________ look on my teacher’s face, I know she was_______ with the results.A. satisfying; satisfyingB. satisfied; satisfiedC. satisfying; satisfiedD. satisfied; satisfying17. Most of the artists _______ to the party were from South Africa.A. invitedB. to inviteC. being invitedD. had been invited.18. Little ______ that the police are about to arrest him.A. he knowsB. does he knowC. he doesn’t knowD. did I feel19. On the ground ___________ a sick goat, whose life was in danger.A. layB. laysC. lyingD. laying20. Only when your identity has been checked ___________.A. you are allowed toB. you will be allowed inC. will you allow inD. will you be allowed inⅢ. Fast ReadingHigh Hopes for Low-income HousingJiachunyuan, a 2,780-unit affordable housing project in Tianjin financed by the country’s first low-income housing investment fund broke ground over the weekend. It has grabbed the attention of not only low-income Tianjin residents but also analysts all over the country because extending the financing channels for affordable housing is becoming increasingly important as urban populations throughout China continue to swell.The low-income housing investment fund that boosters say may go as high as 5 billion yuan ($732 million) was launched this June. An employee of the Tianjin Real Estate Development Management Group Co, the project's developer declined to say how much the fund has raised to date.Zhang Yong, the general manager of the State-owned developer attending 3th China International Private Equity Forum in Tianjin, described the fund as a kind of private equity fund that will increase financing channels for the low-income housing construction.At present, major portions of the fund come from central and local government fiscal revenue and local government land sales profits and from an unspent portion of the national Housing Fund.No less than 10 p ercent of the local governments’income from land sales must be spent on building affordable housing projects, according to the low-income housing fund management guidelines released by the Ministry of Finance at the end of 2007.“But most local governments do not follow the guidelines strictly and spend less of their land sales profits,” said Chen Guoqiang, director of the real estate research center of the Peking University.Central government pressureBut because the central government has announced several times last month that it plans to increase the supply of low-cost homes, expanding the financing channels has become a hot topic.“Extending the financing channels for building affordable houses is really necessary especially when the government plans to enlarge the scale of the low income houses,” Chen said.Increasing the number of affordable homes was highlighted on December 14 when new guidelines were released following an executive meeting of the State Council chaired by Premier Wen Jiabao. Zhang Ping, director of the National Development and Reform Commission, also confirmed that on December 9. On November 28, Wen said in Shanghai that China would enact fiscal, financial and land policies to support the construction of low-income housing.Consequently all eyes are on Tianjin's model and some other low-income housing financing ideas.Lower rates worrisomeChen Guoqiang of the Peking University said the Tianjin model is a good start, but the lower return rate of the affordable housing investment fund is still a major concern of analysts.Yi Xianrong, a researcher of the Chinese Academy of Social Sciences (CASS) said, who would prefer to invest the affordable housing investment fund remains a big question, especially.Under normal conditions, the return rate of a private equity fund is much higher than bank interest rates, and it is too difficult to judge the return rates of the Tianjin fund because it's still too new, said Yang Guohua, an analyst from Hong Yuan Securities.“It's expected the residents will m ove into the new units in 2012,” said an employee who asked to remain anonymous from the Tianjin development group. "The price will be much lower," he added, declining to specify how much lower. The average home sales price in Tianjin last week reached 8,478 yuan per square meter, up 5.88 percent over the previous week, according the report by China Index Academy, a real estate research institute.Yin Jianfeng, a researcher from CASS, said, “setting up the fund is not an effective way to solve the low income housing problem because the transactions are too complex. There are two ways for the government to subsidize low-income residents, one is increasing the supply of affordable houses, another is to give money directly to them. I prefer the latter one because that is the simplest and most effective way,” he added.But an employee in charge of investing management at the Tianjin development group said that while the return rate of the fund would not be high, its risks are also low because of strong government support.The REITs solution?And some analysts also said setting up Real Estate Investment Trusts (REITs), which have been popular in Hong Kong and in some countries including the US and UK for some low rental housing, would also be a possible choice.Analysts were quoted by China Real Estate Business as saying that, REITs may debut in China by the end of this year because planning for trial launches have begun in Beijing, Shanghai and Tianjin.Meng Xiaosu, president of China National Real Estate Development Group, also suggested at a real estate financial forum in Guangzhou over the weekend that setting up REITs for low-rent houses may be possible. “Using them to solve issues like lack of liquidity may be a possible choice, at least we can use the private capital e ffectively.”But Li Zhanjun, a researcher for E-house (China R&D institute), said that “both the REITs and Tianjin's affordable housing investing fund are fully market oriented, but the low-income housing projects are fully government oriented, so it is too difficulty to mix the two things togeth er.”Du Lihong, an expert who studies REITs for Beta Fact, a real estate and financial research consulting center in Beijing, was also skeptical. She said lower REIT yields for low-rental homes posed the biggest cha llenge. “Their rental prices are too low, and no one would like to invest in REITs because of this – only if the government would of fer some preferential policies.”But REITs for affordable housing projects have been set up in the US and UK, Du said, adding that “there are still some overseas models from which China could learn although we have different backgrounds and systems.”For questions 21~27, choose the best answer from the four choices marked A, B, C and D.21. The affordable housing project has drawn the attention of .A. low-income residentsB. analystsC. both A and BD. high-income residents22. At present, major portions of the fund come from .A. central governmentB.local government fiscal revenueC. an unspent portion of the national Housing FundD. all of the above23. According to Chen Guoqiang, most local governments do not follow the guidelines strictly and spend of their land sales profits.A. lessB. moreC. muchD. little24. percent of the local governments’ income from land sales must be spent on building affordable housing projects, according to the low-income housing fund management guidelines.A. 10 or moreB. 20 or moreC. less than 10D. more than 825. On November 28, Premier Wen said in Shanghai that China would enact policies to support the construction of low-income housing.A. fiscalB. economicC. financial and landD. both A and C26. Mentioning subsidizing low-income residents, which one does Yin Jianfeng prefer?A. Increasing the supply of affordable houses.B. Giving money directly to them.C. Not mentioned.D. Reducing tax.27. According to Li Zhanjun, a researcher for E-house (China R&D institute), the low income housing projects are .A. low-income residents orientedB. fully market orientedC. fully government orientedD. real estate company orientedFor questions 28~30, complete the sentences with the information given in the passage.28. Then central government plans to increase , expanding the financing channels.29. According to Chen, the lower return rate of the affordable housing investment fund is stillof analysts.30. for affordable housing projects have been set up in the US and UK.Ⅳ. Reading in DepthPassage ASri Lanka is known as the “Pearl of the Indian Ocean”, and it is easy to see why. This little country never fails to please visitors.ArriveThe national airline is Sri Lankan Airlines, which flies from Colombo to London and a couple of other European cities. The country’s main airport is Colombo Bandaranaike, located 29km north of the capital city.Why now?The best time to visit Sri La nka’s southern beaches is from November to April. So by going early in the season, you’ll get the best weather. Also in November, Deepavali, known as “Diwali” or the“Festival of Lights”, is Sri Lanka’s main religious festival, celebrated throughout the co untry.SeeThere is plenty to see in Sri Lanka. The ancient capital cities of Polonnaruwa and Anuradhapura are worth seeing, and so are many outstanding ruins. Other mustsees are the rock fortress (要塞) of Sigiriya, towering over the jungle as far as the eye can see, and Dambulla’s cave temple, the country’s largest and best preserved. Both are UNESCO World Heritage (遗产) Sites. Kandy is a picture-like town, which was the last stronghold of the Kandyan Kings. Today it is a cultural relic centre where age-old customs, arts, and crafts remain.DoSri Lanka owns about 1,600km of beautiful palm-shaded beaches as well as warm, pure seas and colourful coral reefs. You can explore the underwater world, and surfing and diving are available too. Away from the shore, wildlife is a big draw for Sri Lanka, and Yala National Park is one of the best places in the word to see wild animals including leopards (豹) and elephants.TasteSri Lanka is celebrated for its excellent food, with a particular emphasis on fresh fruit and vegetables on menus everywhere. Fish and seafood are a big part of the local diet.Did you know?Sri Lanka is known for its tea, but it is also the world’s largest producer and exporter of cinnamon(肉桂).31. Which of the following is a cultural relic centre of Sri Lanka?A. Kandy.B. Anuradhapura.C. Polonnaruwa.D. Colombo.32. If you want to know something about “Diwali”, you’d better go there in .A. September.B. October.C. November.D. May.33. We learn from the passage that Sri Lanka .A. is in the Pacific OceanB. is famous for its excellent foodC. is the world’s largest producer of teaD. has only flights to London34. The author wrote the article in order to .A. introduce the picturesque landscape of Sri LankaB. let readers know what is famous for in Sri LankaC. make Sri Lanka well known throughout the worldD. let people get more travel information about Sri LankaPassage BJoin the thousands of professionals and international travelers who depend on Chanps- Elysees Schau ins Land, Puerta del Sol, and Acquerello italiano to help them stay in touch with the languages and cultures they love. Designed to help you greatly improve your listening, vocabulary, and cultural IQ, these unique European audio-magazines (有声杂志) are guaranteed (保证) to give you enthusiasm and determination to study the language - or your money backEach audio-magazine consists of an hour-long programme on CD or DVD. You'll hear interviews with well-known Europeans, passages covering current events and issues as well as feature stories on the culture you love. A small book. which goes with CD or DVD, contains a complete set of printed materials, notes (background notes included) averaging 600 words and expression translated into English. The result you build fluency month in and month out.To help you put language study into your busy life, we've made each audio-magazine convenient.Work on language fluency while driving to work, exercising, or cooking--- anytime and anywhere you want.Best of all each programme is put together by professional broadcasters, journalists, and editors who have a strong interest in European languages and cultures. That enthusiasm comes through in every edition. From New York to London to Singapore? the users tell us no company produces a better product for language learners at all levels. Ring for more information, or order at WWW. audiomagazine. com. We guarantee that you have nothing to lose if it's not for you; let us know within 6 weeks and we will completely reimburse you.35. The audio-magazines in the passage are_____________.A. published in European languagesB. read on the computer screenC. designed in the form of small-sized booksD. broadcast on television and the radio36. The audio-magazines are mainly for_________.A. European journalistsB. professional travelersC. language learnersD. magazine collectors37. What is mentioned as a feature of the audio-magazines?A. They are translated into English.B. They are convenient for the users.C. They are very easy to readD. They are cheap and popular.38. What does the underlined part "reimburse you" probably mean?A. Return the money you paid.B. Change the product you bought.C. Offer you a free repair.D. Guarantee you the quality.Passage CTo the Editor,I have been reading your newspaper, the Hometown Gazette, for the past two years, ever since I moved to Smithville. We moved here from New York City, so I am accustomed to reading excellent newspapers such as The New York Times. In fact, we still have the Times delivered on Sundays. The entire family enjoys reading the recipes(食谱) in the newspaper, as well as the Styles section.The Times is great, but the Gazette is another sto ry. I’ ve never read an article that doesn't contain at least three or four spelling or grammatical err ors. For instance, in last week’s issue, you misspelled the word“secretary,”used a singular verb with a plural noun, and used “it's” as a possessive(所有格). And that was just in the lead story! In case you never went to elementary school, “it's” means “it is.”It's not a possessive adjective!It’s a pity that this tiny little hick (乡下) town has only one newspaper, because I’d like to have an alternative to the rag you publish. I find it hard to believe your news stories. If you can’t spell correctly, how can you get your facts right?I’ve been meaning to get this off my chest for some time. Please cancel my subscription(订阅). And buy yourself a dictionary.Sincerely,Jane Z. Jones39. Which phrase from the passage shows the writer’s prejudice(偏见)?A. get this off my chestB. tiny little hick townC. reading the recipes in the magazineD. three or four spelling or grammatical errors40. The author's tone in this passage can best be described as .A. happyB. humorousC.objective(客观的)D. angry41. Which statement from the passage is a fact ?A. We still have the Times delivered on Sundays.B. It’s a pity this town has only one newspaper.C. The Times is great, but the Gazette is another story.D. You never went to elementary school.42. Which statement of the following is not true according to the passage?A. The writer once lived in New York City, so he was used to reading newspapers like The New York Times.B. The entire family enjoys reading the Styles section in the local newspaper.C. The writer has long been planning to express his dissatisfaction with the local newspaper.D. It is obvious that the editors of the newspaper are not very careful about their work.Passage DNew York: when the first jet struck, World Trade Center at 8:48 am on Tuesday, the People in 2 World Trade Center with a view of the instant damage across the divide had the clearest sense of what they, too, must do: get out fast.Katherine Hachinski, who had been knocked off her chair by the blast of heat exploding from the neighboring tower, was one of those. Despite her 70 years of age, Ms Hachinski, an architect working on the 91st floor of 2 World Trade Centre, the south tower, went for the stairs. Twelve floors above her, Judy Wein, an executive (经理), screamed and set off too.But others up and down the 110 floors, many without clear views of the damage across the way and thus unclear about what was happening, were not so sure. And the 18 minutes before the next plane would hit were ticking off.Nobody were uncertain about what was the best thing to do, formal announcements inside the sound tower instructed people to stay put, telling them that the building was all right and the threat was limited to the other tower.Some left, others stayed. Some began to climb down and, when met with more announcements and other cautions to stop or return, went back up. The decisions made in those instants proved to be of great importance, because many who chose to stay were doomed(注定死亡) when the second jet crashed into the south tower, killing many and stranding(使某物留在) many more in the floors above where the jet hit.One of those caught in indecision was the executive at Fuji Bank UAS.Richard Jacobs of Fuji Bank left the 79th floor with the other office workers, but on the 48th floor they heard the announcement that the situation was under control. Several got in the lifts and went back up, two minutes or so before the plane crashed-into their floor.“I just don’t know what happened to them,” Mr. Jacobs said.43. From the passage, we know that the south tower was hit by the plane_______.A. at 8: 30B. 18 minutes earlier than the north towerC. at around 9:06D. at 8:4844. The underlined words “stay put” means_______.A. stay in the buildingB. leave at onceC. put everything back and then leaveD. keep silent45. Fewer people would have died if_______.A. more announcement had been madeB. people hadn’t used the liftsC. the incident had happened on a weekendⅤ. ClozeSome people cannot learn in ordinary schools. Physical or _____46_____ illness prevents a child from learning. Today new _____47_____ are being used in special schools to help the disabled __48____ . A school is being __49_____ in New Jersey, USA. It is called Bancroft. Here the disabled will be trained to __50____ themselves and to get along in the outside world. Bancroft is not surrounded by ___51__of any kind. Its director insists that it be ___52__ so that students may gradually develop __53____ relations with the rest of the world. Bancroft students will__54__ in apartments, cooking their own meals, and learning to perform other ____55_____. As they become ___56___, they will buy their own furniture, paying for it out of their own ___57___. They will pay for their food, too. They will learn to expect _____58___bills for the calls they make every month. As a step toward the goal of becoming __59____, each disabled person will decide what kind of work he wants to be __60___ to do. While some of the training will be ___61___ on within Bancroft itself, most of the students will receive __62___ training in nearby towns. They will be trained by town people. After the training has been ___63____ completed, the student will work _64__ an assistant and will begin to earn money. After that he will leave Bancroft, ___65___ the school will continue to give him help if he _66__ it. How long will it take a student to ____67___ his training under this new sys tem? The director says, “For some a year will be ___68___. For others it might take ten years.” For all, however, this method offers new___69___. Many will learn to be __70___and independent, supporting themselves in the world.46. A. spirit B. mental C. thought D. body47. A. plans B. decisions C. tools D. methods48. A. learn B. live C. earn D. play49. A. turned up B. set up C. searched for D. longed for50. A. enjoy B. teach C. help D. support51. A. trainers B. students C. trees D. walls52. A. free B. open C. quiet D. different53. A. special B. familiar C. normal D. close54. A. live B. study C. hide D. cook55. A. operations B. tasks C. plays D. acts56. A. strong B. healthy C. able D. happy57. A. hands B. wealth C. earnings D. abilities58. A. telephone B. education C. housing D. food59. A. brave B. clever C. learned D. independent60. A. asked B. sent C. trained D. made61. A. taken B. called C. tried D. carried62. A. life B. job C. body D. mind63. A. successfully B. gradually C. quickly D. hardly64. A. with B. for C. like D. as65. A. and B. but C. so D. or66. A. needs B. asks C. gets D. offers67. A. receive B. get C. complete D. stop68. A. short B. enough C. good D. long69. A. ideas B. abilities C. time D. work70. A. helpful B. careful C. useful D. cheerfulⅥ. Translation71.Only then________ (莫妮卡才意识到她有多爱她的丈夫).72.________ (这份工作吸引我的地方)is the salary and the possibility of foreign travel.73.It is time that________ (我们为期末考试做准备).74.If you had________(听了我的劝告,你就通过考试了).75.What do you think of his suggestion that________ (我们应该把家搬到离父母近点儿的地方)?。

国际经济学杂志排名及其影响因子1-100)

14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34

35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59

60 61 62 63 64 65 66

国际经济 学杂志排 名及其影 响因子 (1100)

(201104-17 18:42:27 ) 转载▼ 标签: 经济学

杂志

影响因子

杂谈 以下的排 名来自 IDEAS/Re PEc: 影 响因子应 该是累计 的而不是 当年的, 这里只列 出了前 100名:

Rank

1 2 3 4 5 6 7 8 9 10 11 12 13

Proceedings, Federal Reserve Bank of Philadelphia American Economic Journal: Macroeconomics, American Economic Association Journal of Law, Economics and Organization, Oxford University Press Journal of Law & Economics, University of Chicago Press Journal of Environmental Economics and Management, Elsevier Journal of International Money and Finance, Elsevier World Bank Research Observer, Oxford University Press Journal of Money, Credit and Banking, Blackwell Publishing Labour Economics, Elsevier Proceedings, Board of Governors of the Federal Reserve System (U.S.) Journal of Development Economics, Elsevier Oxford Bulletin of Economics and Statistics, Department of Economics, University Proceedings, Federal Reserve Bank of Dallas Economic Policy Review, Federal Reserve Bank of New York Games and Economic Behavior, Elsevier Econometrics Journal, Royal Economic Society Journal of Empirical Finance, Elsevier Experimental Economics, Springer Journal of Health Economics, Elsevier International Journal of Central Banking, International Journal of Central Journal of Economic Dynamics and Control, Elsevier Journal of Risk and Uncertainty, Springer Journal of Population Economics, Springer Journal of Industrial Economics, Blackwell Publishing International Finance, Blackwell Publishing International Journal of Industrial Organization, Elsevier

物业管理国外文献综述

物业管理国外文献综述1。

物业管理体系研究Alice Christudason对新加坡住宅区物业管理体系的选择进行研究,通过对内部管理组织和代理公司两种物业管理体系对比研究发现,如果考虑高效和实用,最好选择专业代理人,如果管理委员会由具有足够驱动力、忠诚度、知识水平且愿将时间付出给小区的成员构成,则可以选择内部管理组织,管理委员会就可以直接运行和控制小区的日常和长期工作[1]。

C Y Yiu等首次从制度经济学的角度对物业管理的制度安排提出了一个分析框架[2]。

Alice Christudason研究显示,虽然多层次的系统可以缓解单层管理公司系统一些现有的为题,但是可能会出现其他问题,包括运营成本的增加,为多层管理公司找到足够的志愿者和冲突可能性的增加[3]。

2. 物业管理与政府治理研究Steve R Doe研究并提出政府应当利用中介服务机构,充分发挥它们在社区管理中的作用[4];Altrichte从政府的角度上指出,政府应当采用潜在的社区管理措施,并且通过这些措施来改善对社区的管理[5]。

Beate Klingenberg经过建模研究认为租金管制不仅对业主,而且对资产管理者和承租人都具有预想不到的负面后果,从而提出应重新探讨和审查租金管制政策[6].3.物业管理的溢出效应研究物业管理与房地产价格间有一个重要的和积极的关系。

人们愿意分别为ISO9001认证和HKMAQA的物业管理公司管理的资产多支付4.92%和2.84%[7]。

Eddie Chi—man Hui通过研究物业管理对房地产价格的影响发现,ISO14001认证对资产价值的影响小于ISO9001和香港管理协会质量认证两个管理标准[8].Jinhuan Li 提出一种新的评价方法,以确定物业管理服务对香港私人住宅价值的重要性,结果表明,物业管理资产增加价值,尤其是年长和危房特性的资产[9]。

但是Roland Füss研究表明,超额收益的来源和资产特性有关,物业资产管理并不能成为主要驱动力,特别是资产的年限和规模可控的情况下,其作用更为有限[10].4. 物业管理转化路径研究Alan Phelps研究提出组织意志,战略重点,投资的智慧和创业文化是决定物业管理向资产管理转化的四个关键因素[11]。

JOURNAL OF REAL ESTATE RESEARCH Percentage Leases and the Advantages of

JOURNAL OF REAL ESTATE RESEARCHPercentage Leases and the Advantages of Regional MallsPeter F.Colwell* Henry J.Munneke**Abstract.The differences in the ownership structures of downtown retail districts and shopping centers may give rise to varying space allocations and rental contracts found in these markets.This article specifically examines the value-enhancing aspects of percentage leases and explores the mechanisms of tenant mix,risk sharing and rent discrimination through which this value is created.The use of percentage leases may lead to superior returns by allowing a rent structure that approaches perfect price discrimination.Risk sharing through the use of percentage leases may also create value for the property owner and lead to lower rents for tenants.IntroductionIn what important dimensions are shopping centers superior to downtown retail districts?It is fairly obvious that they are located differently and the shopping center location may be superior in providing access for shoppers using contemporary modes of transport.Access may relate to attributes such as proximity to circumferential highways or the adequacy or price of parking.What probably is less obvious,but arguably no less important,is that downtown retail shops have many owners(i.e.,are owned atomistically),whereas shopping centers are collections of stores owned by a single entity.This ownership difference gives rise to differences in space allocation and rental contracts.Shopping centers,especially regional malls,provide a context in which it is possible to use percentage lease contracts in which rent is a percentage of the tenant’s gross income.This article shows that percentage leases,in the jargon of real estate practice,create value.Three mechanisms by which percentage leases create value are diversification,risk sharing and rent discrimination.The methodology in this article is theoretical,based on a series of graphical presentations.The techniques are well established,for example using measures of expected utility and the analysis of the benefits of trade through Edgeworth boxes. These techniques have not before been applied in a systematic explanation of the value-enhancing aspects of percentage leases:tenant mix,risk sharing and rent discrimination.Recent work by Lee(1988),Vandell and Carter(1993)and Eppli and Benjamin(1994)provide extensive overviews of the general literature concerning retail research.1*University of Illinois,Urbana,IL61821or pcolwell@.**University of Georgia,Athens,GA30602-6255or hmunneke@.239240JOURNAL OF REAL ESTATE RESEARCH VOLUME 15,NUMBER 3,1998The theory presented provides insight into the practical use of percentage leases and their possible role in urban spatial organization.The inclusion of percentage rents within a property’s rent structure can lead to superior returns over a uniform rent structure and can also lead to possible benefits to the tenant via lower rents.Even though the use of percentage leases may create value ,the ownership structure of downtown retail districts is not conducive to the use of percentage leases.Thus,the benefit associated with percentage leases varies spatially,affecting the spatial organization of shopping.This article is divided into five parts,the first three are devoted to diversification,risk sharing and rent discrimination,respectively.In the final two sections,we offer practical applications and our conclusions.DiversificationA landlord acting in much the same way as an insurance company may add value to a portfolio of leases by bringing together tenants with different income prospects,if the incomes of the tenants are not perfectly positively correlated.The tenants are attracted by the risk reduction associated with percentage leases when compared to flat rent contracts.Consider the case of a landlord with a portfolio of two leases.Further,consider an extreme case in which the tenants have one of two gross incomes,low income or high income.Still further,assume that the incomes of these tenants are perfectly negatively correlated,when one experiences the low income the other experiences the high income.Under these conditions,the principles relating to diversification can be shown by the use of an Edgeworth box diagram (see Exhibit 1).The sides of the Edgeworth box represent a tenant’s income prospects net of all costs except rent.The longer horizontal sides represent high income net of non-rent costs and the shorter vertical sides represent low income net of non-rent costs.It is assumed that non-rent costs are proportional to income,so the slope of the diagonal line connecting the opposite corners of the box is the ratio of the two gross incomes.The tenant’s rents are measured from the upper right-hand corner,with the remaining portion of income net of non-rent cost referred to as net income is defined here as gross income minus the non-rent costs of operation (income net of non-rent cost)minus rent.Note that the tenant’s net income could be measured from the lower left-hand corner.Flat rent contracts,equal rent in either state of income,are found along a 45Њline from the upper right-hand corner of the box.This line will be referred to as the tenants’flat rent line.All contracts falling along a line perpendicular to the tenants flat rent line (45Њline)produce equal receipts for the landlord (recall the covariance of the two tenants’incomes).Thus,these lines will be denoted as equal-expected-rent (EER)lines.For example in Exhibit 1,contract a represents a particular flat rent contract and all contracts that produce receipts for the landlord equal to those of contact a are found along EER 1.Under a percentage rent contract,rents are proportional to income and therefore,the ratio of the rents is equal to the ratio of the gross incomes.Thus,PERCENTAGE LEASES AND THE ADV ANTAGES OF REGIONAL MALLS241Exhibit1Value Created through Tenant Diversificationpercentage rent contracts fall upon the diagonal connecting the upper right-hand corner with the opposite corner of the box.Contract b is the percentage rent contract that produces rent equivalent to theflat rent contract a.Contract c is a contract in which the percentage of rent for the high income exceeds the percentage for the low income.In contrast to the landlord,each tenant faces uncertain prospects,so it is not sufficient to focus on the tenant’s expected net income as an indicator of welfare.Rather,it is necessary to understand that tenants’expected utility is affected by lease contracts.In an Edgeworth box diagram,this is done by utilizing indifference curves that we will refer to as equal-expected-utility(EEU)curves.The slope of an EEU curve,often called the marginal rate of substitution,is the negative of the ratio of the marginal utility at high net income to the marginal utility at low net income(i.e.,probabilities are not involved because the probabilities of the two incomes are equal).If a tenant faces zero risk,net income in the high and low state are equal,and the marginal utilities must also be equal.Therefore,along a45Њline out of the lower left-hand corner,the slope of the EEU curve or marginal rate of substitution isϪ1,the same as the landlord’s equal expected rent line.Elsewhere,the tenant’s EEU curve is242JOURNAL OF REAL ESTATE RESEARCH VOLUME 15,NUMBER 3,1998convex,because the tenants are risk averse.As high net income increases and low net income decreases along an EEU curve,the marginal utility increases if income is low and the marginal utility decreases if income is high.Therefore,the ratio of marginal low net income to marginal high net income increases and the slope of the EEU curve becomes steeper.To focus on the benefits of diversification as distinct from the benefits of risk sharing,the advantage to the tenant of a percentage rent contract verses a flat rent contract will be examined holding the landlord’s aggregate revenue constant (i.e.,the landlord will assume no additional risk by using percentage rents in place of flat rents).Thus,risk is not introduced into the landlord’s portfolio.If the landlord’s position is to remain unchanged,then the resulting improvement in net income for the tenant with low income must equal the resulting decline in net income when income is high.The advantage to the tenant of a percentage rent contract in contrast to a flat rent contract can be found by comparing the flat rent contract a to the percentage contract b .Both contracts fall on the same EER line,thus providing the landlord with equivalent aggregate rent.The EEU curve that passes through contract a ,EEU 1,falls below contract b (i.e.,a EEU curve higher than EEU 1goes through point b ),thus the tenant prefers the percentage contract b to the flat rent contract a .This unequivocally demonstrates that the tenants are better off under the percentage lease than they were under the flat lease,holding the landlord at the same level of revenue.It cannot be argued that the percentage rent contract maximizes tenant welfare while holding aggregate rent constant,only that it offers an improvement over a flat rent contract.Actually,contract c maximizes tenant welfare in this context.The EEU curve associated with contract c would have a slope of Ϫ1at point c ,therefore the EEU curve would be tangent with EER 1at point c .Another way to look at the problem is to hold the tenants’welfare constant and identify the premium they would be willing to pay in return for the reduced risk they face as a result of the percentage lease.The landlord’s rent receipts will increase by the amount that the tenants’expected income declines.In Exhibit 1,the percentage contract d ,provides the tenant with an equivalent level of utility to that of the flat rent contract a .The premium paid to the landlord is the difference between the increase in rent under high income and the rent decline under low income.The premium associated with contract d when compared to contract a can be represented as the difference in the levels of rent associated with each contract’s EER line,as shown in Exhibit 1.The percentage rent does not represent the optimal contract in the sense of maximizing aggregate rent while holding tenant utility constant.The optimal contract would be at point e ,where the EER curve is tangent to the EEU 1curve.Although the percentage rent contract is not optimal in the sense of maximizing aggregate rent while holding tenant utility constant,it does provide a premium over a flat rent contract.While percentage rent contracts have been shown to be superior to flat rent contracts,it appears that even more extreme rent contracts are superior to percentage leases.PERCENTAGE LEASES AND THE ADV ANTAGES OF REGIONAL MALLS243 This appearance results from artificially constraining of the landlord to a riskless position.On the other hand,this constraint is useful in distinguishing the benefits of diversification from the benefits of risk sharing.Risk Sharing2To focus on the value creation associated with risk sharing alone,the gains associated with diversification from altering the rent contingencies in the lease must be removed. This can be accomplished by assuming a landlord with a single tenant(i.e.,atomistic ownership).As before,assume that the tenant has uncertain income in that income could be either high or low.The different levels of income are assumed to occur with equal probability.The question is whether moving away from a contract withflat rent could benefit one party(i.e.,the tenant or the landlord)without injuring the other.If so,it should be a simple matter to redistribute the gains so both would be made better off by the change. Of course,aflat rent contract produces a certain outcome for the landlord while requiring the tenant to bear all of the risk.We wouldfirst like to show that holding the tenant’s expected utility constant,but decreasing his risk,will cause the landlord to share risk and may cause the landlord’s expected utility to increase.The proposition that risk sharing necessarily creates value actually can be proven using an Edgeworth box diagram(see Exhibit2).When the landlord faces uncertain prospects,we must use indifference curves to judge landlord welfare.The landlord’s equal-expected-utility(eeu)curves have the same direction of curvature relative to the upper right-hand corner of the box as the tenant’s EEU curves do relative to the lower left-hand corner.Both the tenant and landlord are risk averse.The landlord’s eeu curves have a slope ofϪ1at their intersection with the tenant’sflat rent line.At points along the tenant’sflat rent line there is certainty for the landlord(i.e.,regardless of the state of income,rents are equal),thus the numerator and denominator of the marginal rate of substitution are equal.Beginning withflat rent contract a,and holding the tenant’s expected utility constant leads us to percentage rent contract d.The landlord is better off with contract d than with contract a;contract d is associated with a higher level of expected utility than contract a.This demonstrates conclusively that risk sharing via percentage rents is superior to aflat rent contract.Note however that the landlord’s utility would bemaximized at an even more extreme contract f,the tangency point of eeu2and EEU1.The landlord receives an increase in expected rent to overcome the increase in risk of moving from a certainflat rent to a contract in which rent is related to the tenant’s income.In Exhibit2,the increase in expected rent could be illustrated as the differencebetween the EER line which is tangent to eeu1at point a and the higher EER throughpoint g.The tenant,in order to maintain a constant level of satisfaction,must enjoy an offsetting decline in the variation of net income.The decline in variation of net income can be seen as the relatively large change in rents for high income when244JOURNAL OF REAL ESTATE RESEARCHVOLUME 15,NUMBER 3,1998Exhibit 2Value Created through Risk Sharingcompared to the change in rents for low income when moving from a flat rent contract a to the percentage contract g .The decline in the difference between the high and low outcomes is exactly equal to the new variation in rent received by the landlord.Another way of looking at the problem would be to hold landlord expected utility constant.Again,starting with contract a ,the percentage rent contract g makes the tenant better off but not as well off as contract h ,found at the tangency point of eeu 1and EEU 2.Once again,we see that risk sharing by the use of percentage rents is superior to a flat rent contract.The final percentage rent contract would be negotiated somewhere between contracts d and g depending on the bargaining power of the two parties.While the percentage lease may not be optimal,it approximates an optimal contract under the various conditions specified.Risk sharing always creates value if the parties to the contract are risk averse.Rent DiscriminationDoes a competent manager of a mall rent a vacant store to the highest bidder?This is the competitive result that should be found in downtown’s with atomistic ownership,PERCENTAGE LEASES AND THE ADV ANTAGES OF REGIONAL MALLS245246JOURNAL OF REAL ESTATE RESEARCHVOLUME15,NUMBER3,1998PERCENTAGE LEASES AND THE ADV ANTAGES OF REGIONAL MALLS 247equal to the area under the marginal revenue curve up to allocation x (i.e.,the area of ⌬adR x equals the area of ⌬bdf ).If the landlord requires a contract contingency where each type A tenant is charged a different rent per square foot,thereby extracting all surplus,then the marginal revenue from imposing perfect price discrimination would be higher at each allocation.The surplus at allocation x is shown by the darkly shaded triangle (⌬bR x c );the total revenue is the area of the shaded trapezoid.The area of the trapezoid is equal to the area under the curve labeled marginal revenue with perfect discrimination.A landlord may use percentage rent contracts to create a contingent contract that calls for a different rent from every tenant.For example,a landlord that charges type A tenants a base rent of R x per square foot with a contingency that if income rises above R x /r ,the tenants must pay 100r %of their income as rent;a contingent contract that potentially calls for a different rent from every tenant.If a tenant’s willingness to pay is based roughly on income,then percentage leases approximate perfect rent discrimination.Suppose that type B tenants are anchor tenants and get little or no positive externalities from type A tenants.The willingness to pay without externalities is then the same as that with externalities and the same as the marginal revenue with perfect price discrimination.Furthermore,anchor tenants are likely to have much flatter demand curves because their opportunities include many close substitutes (e.g.,freestanding stores outside of the mall’s ring road).Exhibit 5illustrates an extreme case in which type B tenants have a perfectly elastic demand curve.In this case,type B tenants have marginal curves that are identical to their average curve,the flat demand curve.If retail space is leased to the highest bidder (i.e.,if the landlord were playing a competitive/downtown game),then the landlord’s portfolio of leases would move toward the situation illustrated in Exhibit 5with all rents equal at the amount that the marginal tenants are willing to pay;R 1A and R 1B for type A and B tenants,respectively.Under this scenario,a majority of space,x 1,would be allocated to type A tenants and T Ϫx 1to type B tenants.The landlord’s revenue would equal the area of the rectangle with the darkest shading (rectangle 0R 1A R 1B T ).Suppose,on the other hand,that space is leased so as to maximize revenue and that it is possible to rent discriminate across tenant types.That is,it is not possible for a tenant to rent space as a shoe store and then switch merchandise to become a jewelry store.In this case of simple rent discrimination,the allocation of space would be at x 2with a majority of the space now being allocated to type B tenants,with much less allocated to type A tenants.Rent per square foot for type A tenants would be R 2A and R 1B for type B tenants.Under simple rent discrimination,the landlord’s revenue is greater than if leased to the highest bidder by the area the triangle with the lightest shading (⌬bjR 1A ).Finally,imagine that the landlord possesses contract attributes,perhaps percentage leases,that allow him to engage in perfect rent discrimination.Not only can different248JOURNAL OF REAL ESTATE RESEARCHVOLUME15,NUMBER3,1998discriminator would choose the allocation x2with no vacancy.This allocation is thatwhich equates the perfect price discriminating marginal revenue for each type of tenant.Recall that for tenant type C,the demand curve and the perfect rent discriminating marginal revenue curve are one and the same.The base rents chargedtype A and type C tenants are R2A and R2C,respectively.The relative rents reversewhen simple and perfect rent discrimination are compared.Type A tenants are charged more base rent than type C with perfect rent discrimination,but type A tenants are charged less rent than type C with simple rent discrimination.As a side issue,note that the relative allocations are very different in Exhibits5and 6.In Exhibit5,the perfect rent discrimination produces an allocation between those of simple rent discrimination and competition.In Exhibit6,the competitive allocation (i.e.,where the demand curves cross)is between the extremes of simple and perfect rent discrimination.ImplicationsThe practical applications of the theory in this article are to alert property managers, urban economists and urban planners to the source of a new view of urban spatial organization.First,property managers should take from this article a new appreciation of the importance of charging different rents to different tenants.They can achieve superior returns by traditional price discrimination(i.e.,charging higher rents to less rent sensitive tenants),but may push the envelope further by recognizing that percentage rents may move the rent structure toward perfect price discrimination. Property managers and tenants should begin to recognize the gains both sides of the lease contract may get from the risk sharing aspects of percentage leases.Tenants may share in any benefits that appear to accrue to landlords via lower rents.Tenants should be drawn to the insurance features of percentage leases.Of course,shoppers may be advantaged by lower prices emerging from the benefits of tenants.Finally, this article alerts urban economists and urban planners to an alternative view of the decline of downtown shopping associated with the rise of suburban malls.To some extent,this change in the spatial organization of shopping may be due to the fact that the downtown ownership structure does not facilitate the use of percentage leases and the benefits that accrue from these leases.In the most down-to-earth terms possible, property managers in some areas of real estate should not develop uniform rent policies,neither should they necessarily rent to the highest bidder.Planners,on the other hand,should not think that physical changes to the downtown,such as creating ‘‘malls’’by closing streets,will be sufficient to return downtowns to their previous dominance in shopping.Rather,the property-rights/ownership-structure may be an impediment to the return of downtown shopping as a result of limiting the nature of leases.ConclusionThree mechanisms are important in explaining the usefulness of percentage leases. These are diversification,risk sharing and rent discrimination.These mechanisms,viaVOLUME15,NUMBER3,1998percentage leases,provide a landlord with a portfolio of leases an opportunity for gains overflat rent contracts.Whether this opportunity exists or not depends on the diversity of the tenants’income prospects.In general,it pays to share risk if the parties to a contract are each risk averse.This is as true in the context of retail leases as any other.Rent discrimination influences the allocation of space and the aggregate rent that can be generated.Atomistic downtown storeowners do not have the ability to benefit from diversification and rent discrimination,but mall owners do.Either atomistic or mall landlords may benefit from risk sharing,but the confidence a landlord has in tenants’gross incomefigures and thus the opportunity to risk share, may be closely associated with national tenants and regional malls.While this article outlines three of the mechanisms that make percentage leases create value,it does not exhaust all of the possibilities.For example,as noted in Miceli and Sirmans(1992),percentage leases may resolve what would otherwise be an agency problem.If,for example,the levels of mall advertising,maintenance and security are influenced by manager effort and if these levels affect the incomes of the tenants,it may be desirable to involve the landlord in the businesses of the tenants via percentage leases.The presence of this incentive will induce the landlord to provide an appropriate level of effort.Note that underflat rent contracts,if the landlord’s effort has no influence on the level rent collected,then he maximizes profits by setting the level of effort to zero(see Miceli and Sirmans,1992).Of course,the use of net leases (i.e.,charging tenants for operating expenses)substantially diminishes the impact of this agency problem since the landlord can pass the costs on to the tenant.A percentage lease with a base can also be thought of as a call option.While this article is concerned with the advantages of percentage leases,there are contexts in which percentage leases are inappropriate.A landlord must have confidence in the gross incomefigures provided by the tenant before the use of a percentage lease can be justifindlords may take some comfort in the fact that the tenant must report the samefigures to the sales and income tax authorities so the landlord can free-ride on their monitoring programs.However,such comfort may be placing too much weight on a very thin reed(i.e.,governmental monitoring).There may be some incentives not to cheat beyond the sanctions imposed by the tax authorities and landlord.These incentives may include the desire to establish an accurate sales record that can be revealed for an anticipated sale of the business,as well as ethical and religious proscriptions against lying.Nevertheless,a retail establishment may have some tendency to skim(i.e.,close the cash register at some point during the day),thereby cheating both the tax authorities and the landlord who uses percentage lease contracts.If the landlord believes that some tenant attribute is associated with skimming but that the amounts skimmed are somewhat proportional to actual gross income,the landlord would tend to raise the percentage for tenants with that attribute.This is a‘‘lemons problem’’and would force all such tenants to skim.The opposite effect might be found for traditional money laundering stores(e.g., arcade games).These stores would tend to report more income than they produce possibly causing landlords to charge them lower percentages.There is an important exception to this propensity to lie.National tenants tend to provide honestfiguresbecause they must report to the home office,as well as to the tax authorities and the landlord.Thus regional malls,that exclusively,or nearly exclusively,lease to national tenants,are the prime candidates for the use of percentage leases.Notes1For readers interested in studies exploring the determinants of shopping center rents,see Benjamin,Boyle and Sirmans(1990),Gatzlaff,Sirmans and Guidry(1993)and Sirmans and Diskin(1994).2Inspired by Brueckner(1993)and by conversations with Jan K.Brueckner.ReferencesBenjamin,J.D.,G.W.Boyle and C.F.Sirmans,Retail Leasing:The Determinants of Shopping Center Rents,Journal of the American Real Estate and Urban Economics Association,1990, 18,302–12.——,Price Discrimination in Shopping Center Leases,Journal of Urban Economics,1992,32, 299–17.Brueckner,J.K.,Inter-Store Externalities and Space Allocation in Shopping Centers,Journal of Real Estate Finance and Economics,1993,7,5–16.Eppli,M.J.and J.D.Benjamin,The Evolution of Shopping Center Research:A Review and Analysis,Journal of Real Estate Research,1994,9,5–32.Gatzlaff,D,H.,G.S.Sirmans and B.A.Diskin,The Effect of Anchor Tenant Loss on Shopping Center Rents,Journal of Real Estate Research,1994,9,99–110.Lee,K.,The Economics of Shopping Centers:A Literature Survey,Working Paper,University of Illinois,1988.Miceli,T.J.and C.F.Sirmans,Contracting With Spatial Externalities and Agency Problems: The Case of Shopping Center Leases,Working Paper,The University of Connecticut,1992. Sirmans,C.F.and K.A.Guidry,The Determinants of Shopping Center Rents,Journal of Real Estate Research,1993,8,107–16.Vandell,K.D.and C.C.Carter,Retail Store Location and Market Analysis:A Review of the Research,Journal of Real Estate Literature,1993,1,13–45.VOLUME15,NUMBER3,1998。

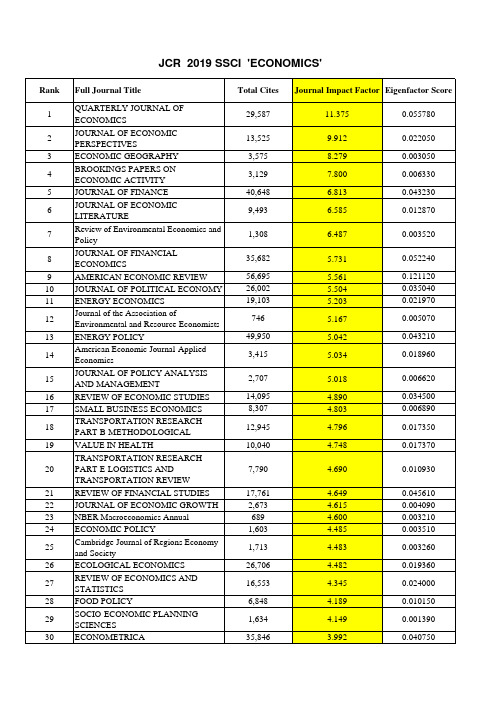

2019年JCR检索经济学类期刊影响因子

Journal Impact Factor Eigenfactor Score

11.375

0.055780

9.912 8.279 7.800 6.813 6.585

0.022050 0.003050 0.006330 0.043230 0.012870

6.487

0.003520

5.731 5.561 5.504 5.203

JOURNAL OF ECONOMIC GEOGRAPHY

52

Economics of Energy & Environmental Policy

53 Review of International Organizations

54

WORK EMPLOYMENT AND SOCIETY

55 NEW POLITICAL ECONOMY

106 Journal of Choice Modelling

857 3,998 13,839 818 3,603

6,573

9,238

2,402

3,607

2,111

860

1,899 1,234 587 2,879 2,239

79

Applied Health Economics and Health Policy

80 Education Finance and Policy

81 ENERGY JOURNAL

82 European Journal of Health Economics

83

EUROPEAN REVIEW OF AGRICULTURAL ECONOMICS

75

JCMS-Journal of Common Market Studies

不动产证券化参考文献

mBI¡B1.¨L B a s B M2002¡A u x W a H U Bs v A m x W g a u Z n A T Q E A157-171¡C2.«2002¡A u Taiwan – REITs o B i s v A m zP N Q n A26-42¡C3.«A2002¡A u p v A m z PN Q n A105-122¡C4.±i B w1992¡A u P a o s v A m F v jn A64A345-414¡C5.±i B B N2002¡A u i s-»D R v A m z P N Q n A1-25¡C6.³N2002¡A u s H U i a P vT v A m x W u Z n A T G A37-60¡C7.ÁB2002¡A u O W t M I v A m x Wu Z n A T G A1-21¡CII¡B s i1.§y2003¡A m-²z P-¡n A A O G Z Uq C2.ªL v(1995)¡A u O W g a J s v A O W g ae U C3.±i2003¡A m a P R n A A O¥G CH6A pp.155-261¡C4.±i B w1999¡A m n A T A O G M C5.±2002¡A m P g s P O W F qn A O G H C6.²s1998¡A u i s v A vP p C7.³F B A B w2002¡A m G z P n A A O GC8.»N j1999¡A m n A A O G C9.ÁB F (2003)¡A m G k P B n A A O GC10.Á2002¡A m P p n A A O G x WV CIII¡B h1.¤1990¡A u s v i R v A j v P p e s h C2.¤T H1998¡A u s v A j k s hC3.¥w1980¡A u P a o s v A j ps h C4.¦v q2002¡A u H U W g s v A jt h C5.§d d1996¡A u O W o i s v A O W j sh C6.§f g R1998¡A u k s - ¥H O v A O W j k s h C7.§1996¡A u P a o G K a ov A j s h C8.§v2002¡A u b v A z ks h C9.§2001¡A u I Q v A O W js h C10.©P A o2001¡A u g i R--²z Qv A H j D z h h C11.ªL C T2001¡A u x W s v A zz s h C12.ªL2000¡A u H U k s v A j k sh C13.ªL I a2002¡A u g a o s v A H jD z h h C14.ªL y2001¡A u x W U v s v A H jt h C15.ªL1997¡A u s v A F j z s h C16.ª2002¡A u e v(NPL)¤B z s v AO W j s h C17.«2001¡A u j J w s BOTi v A O W j s h C18.¬x q2001¡A u O H U P b i s v As j z t s h C19.-P2002¡A u p k D R v A x j kt h C20.®L w2002¡A u v T-¤k gB R v A O W j v P m s h C21.¯2003¡A u i s v A F v j a F sh C22.°s2001¡A u U V c P g Z s—¥H x W vv v A O W j s h C23.Òq1993¡A u H U s v A F d j k sh C24.±i q g2002¡A u H k v A F v jz s h C25.±t2003¡A u s G H u vv A F v j k t s h C26.³A2002¡A u P p B z s v A x j ps h C27.³D1999¡A u u v U e M v P O v A js h C28.³1997¡A u B s s v A jp e s h C29.³F2002¡A u k s---v Aj k s h C30.³1999¡A u g a H U P s H U v A O Wj s h C31.³L2002¡A u H v o i P i s v A H jT t h b M Z h C32.³1995¡A u D v A F v j F s hC33.³W2002¡A u x B p o i s v A H jD z h h C34.³2002¡A u s v A j k s h C35.³1991¡A u z F s v A jz s h C36.´L1998¡A u O W H U z s v A H j/°th C37.·M1999¡A u x W i s v A a z g zs h C38.·q1990¡A u H t U B P DA s v A j g a z s h C39.¸M1999¡A u s H U P H U v AO W j s h C40.¸a1997¡A u C O v(CMOs)--µc P I s v Aj t h C41.¾G f1997¡A u U v s v A j ks h C42.¾G a N2001¡A u s v A x jP z s h C43.ÃC m1997¡A u H U I n t g Q v A O Wj s h C44.ÃC s k2000¡A u z q(AMC)³i v Ts v A s j z t s h C45.Ä2001¡A u v I-¤v Aj t h CIV¡B1. Q A F g e D A91.3.14¡C2. 2002A j D A91.6.28¡C3. m z P N Q n A v D A91.9.28¡C4. H U o i Q A O W V D A92.8.7¡C5. k P A H U P D A92.9.15¡CV¡B l1.ÄT(2002,12)¡A w s H U- s Y CapitaMall Trust A C K.tw/market/20021203.phpG BI¡B Agency and management1.Ambrose, B., and Peter Linneman¡2001¡, “REIT organizational structure and operational characteristics,” The Journal of Real Estate Research, V ol. 21, No. 3,141-162.2.Campell, D. Robert (2002), “Shareholder Wealth Effects in Equity REIT Restructuring transactions: Sell-Offs, Mergers and Joint Ventures,” Journal of Real Estate Literature, V ol.10, No.2, 205-222.3.Campell, D. Robert, Milena Petrova and C. F. Sirmans (2003), “Wealth Effects of Diversification and Financial Deal Structuring: Evidence from REIT Property Portfolio Acquisitions,” Real Estate Economics, V ol. 31, No.3, 347-366.4.Cannon, Ethridge Susanne and Stephen C. V ogt (1995), “REITS and Their Management: An Analysis of Organizational Structure, Performance and management Compensation,” The Journal of Real Estate Research, V ol.10, No. 3, 297-317.5.Capozza, Dennis R. and Paul J.Seguin q2000¡r,¡Debt, Agency, and Management Contracts in REITs: The External Advisor Puzzle,¡ The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 91-6.Fu, Yuming and Lilian K Ng. (2001), “Market efficiency and return statistics: Evidence from real-estate and stock markets using a present-value approach,” Real Estate Economics, V ol. 29, Iss. 2, p. 227 (24 pages)7.Graff, A. Richard (2001), “Economic analysis suggests that REIT investment characteristics are not as advertised,” Journal of Real Estate Portfolio management, V ol.7, No.2, 99-124.8.Howton, D. Shawn and Shelly W Howton (2001),”The wealth effects of REIT straight debt offerings,“ Journal of Real Estate Portfolio Management ,V ol. 7,Iss. 2, p. 151 (7 pages)9.Mueller, R. Glenn (1998),”REIT size and earnings growth: Is bigger better, or a new challenge?” Journal of Real Estate Portfolio Management, V ol. 4, Iss.2, p. 149 (9 pages)10.Yang, S. 2001¡, “Is bigger better: a reexamination of the scale economies ofREITs,” Journal of Real Estate Portfolio Management, V ol. 7, No. 1, 67-77II¡B Risk and Return1.Anderson, I. Randy and Youguo Liang(2001), “Mature and yet imperfect: Real estate capital market arbitrage ,” Journal of Real Estate PortfolioManagement,V ol. 7, Iss. 3, p. 281 (8 pages)2.Benjamin, D. John, G Stacy Sirmans and Emily N Zietz(2001), ”Returns and risk on real estate and other investments: More evidence,” Journal of Real Estate Portfolio Management , V ol. 7, Iss. 3, p. 183 (32 pages)3.Bond, A. Shaun, G. Andrew Karolyi and Anthony B. Sanders (2003), “International Real Estate Returns: A Multifactor, Multicountry Approach,” Real Estate Economics, V ol.31, No.3, 481-.4.Capozza, Dennis R. and Paul J.Seguin (2003), “Inside Ownership, Risk Sharing and Tobin’s q-ratios: Evidence from REITs,” Real Estate Economics, V ol.31, No.3, 367-404.5.Chui, C. W. Andy, Sheridan Titman and K. C. John Wei (2003), “The Cross Sectionof Expected REIT Returns,” Real Estate Economics, V ol.31, No.3, 451-480.6.Cooper, Michael, David H. Downs, and Gary A. Patterson (2000), “Asymmetric information and the predictability of Real Estate returns,” The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 225-.7.Downs, H. David.q2000¡r,¡Assessing the Real Estate Pricing Puzzle: A Diagnostic Application of the Stochastic Discounting Factor to the Distribution of REIT Returns,¡The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 155- 8.Glasock, John L., Chiuling Lu, and Raymond W. So q2000¡r,¡Further Evidence on the Integration of REIT, Bond, and Stock Returns,¡ The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 177-9.Han, Jun and Youguo Liang (1995), “The Historical Performance of Real Estate Investment Trusts,” The Journal of Real Estate Research, V ol. 10, No.3, 235-262. 10.Li, Yuming and ko Wang (1995), “The Predictability of REIT Returns and MarketSegmentation,” The Journal of Real Estate Research, V ol 10.No.4, 471-482.11.Liang, Youguo , Willard Mcintosh and James R. Web (1995), “IntertemporalChanges in the Riskiness of REITS” The Journal of Real Estate Research, V ol10.No.4, 427-443.12.Ling, David C., Andy Naranjo, and Michael D. Ryngaert q2000r,ThePredictability of Equity REIT Returns: Time Variation and Economic Significance,¡The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 117-.13.Ling, David and Andy Naranjo (2003), “The Dynamics of REIT Capital Flows andReturns,” Real Estate Economics, V ol.31, No.3, 405-434.14.Liow, Kim-Hiang (2002), “Commercial Real Estate Analysis and Investment,”Journal of Property Investment & Finance, V ol. 20, Iss. 3, p. 304 (3 pages)15.Mueller, R. Glenn and Randy I Anderson (2002), “The growth and performance ofinternational public real estate markets,” Journal of Real Estate Portfolio Management, V ol.8, Iss. 4, p. 128 (12 pages)16.Sahin, F. Olgun(2003),” Investing in REITs: Real Estate InvestmentTrusts-Revised & Updated Edition,” Journal of Real Estate Literature, V ol. 11, Iss.2, p. 22117.Seiler, J. Michael, Arjun Chatrath, James R Webb (2001), “Real asset ownershipand the risk and return to stockholders,” The Journal of Real Estate Research, V ol.22, Iss. 1/2, p. 199 (14 pages)18.Stevenson, Simon (2002), “Momentum effects and mean reversion in real estatesecurities,” The Journal of Real Estate Research, V ol. 23, Iss. 1, p. 47 (18 pages)19.Yamazaki, Ritsuko (2001), “ Empirical testing of real option pricing models usingland price index in Japan,” Journal of Property Investment & Finance, V ol. 19, Iss.1, p. 53 (20 pages)III¡B Pricing ,valuation1.Anderson, I. Randy, Thomas M Springer (2003), “REIT selection and portfolio construction: Using operating efficiency as an indicator of performance”, Journal of Real Estate Portfolio Management, V ol. 9, Iss. 1, p. 17.2.Capozza, R. Dennis, and Sohan Lee (1995), “Property type, size and REIT value,” The Journal of Real Estate Research, V ol. 10, No. 4,363-380.3.Clayton, Jim, Greg MacKinnon (2001), ”The time-varying nature of the link between REIT, real estate and financial asset returns”, Journal of Real Estate Portfolio Management, V ol. 7, Iss. 1, p. 43. (12 pages)4.DeWeese, Gary S.¡1998¡, “The Role of the Professional Appraiser in REIT Valuations,” The Appraisal journal, July, 236-241.5.Falzon, Robert ¡2002¡, ”Stock Market Rotations and REIT Valuation,” Prudential Real Estate Investors, November.6.Graham, M. Carol and John R. Knight 2000¡, “Cash Flows vs. Earnings in the valuation of Equity REITs,” Journal of Real Estate Portfolio Management, V ol. 6, No. 1, 17-25.7.He, T. Ling (2000), “Causal Relationships Between Apartment REIT Stock Returns and Unsecuritized Residential Real Estate,” Journal of Real Estate Portfolio Management, V ol.6, No.4, 365-372.8.Kallberg, G. Jarl, Crocker H. Liu and Anand Srinivasan (2003), “Dividend Pricing Models and REITs,” Real Estate Economics, V ol.31, No.3, 435-450.9.Kuhle, L. James and Jaime R. Alvayay (2000), “The Efficiency of Equity REIT Prices,” Journal of Real Estate Portfolio management, V ol.6, No.4, 349-354.10.Liang, Youguo and James R. Web (1995), ”Pricing Interest-Rate Risk for MortgageREITs,” The Journal of Real Estate Research, V ol 10.No.4, 461-469.11.Ling, C. David,Andy Naranjo (1999), “The integration of commercial real estatemarkets and stock markets”, Real Estate Economics, V ol. 27, Iss. 3, p. 483 (33 pages)12.Pagliari, Jr. L. Joseph and James R. Webb (1995), “ A Fundamental Examination ofSecuritized and Unsecuritized Real Estate,” The Journal of Real Estate Research, V ol 10.No.4, 381-426.IV¡B law1. Campbell, D. Robert, C F Sirmans (2002), “Policy implications of structural options in the development of real estate investment trusts in Europe,” Journal of Property Investment & Finance, V ol. 20, Iss. 4, p. 388 (18 pages)2. Ott, L. Richard, Robert A Van Ness (2002), “An analysis of the impact of the Taxpayer Relief Act of 1997 on the valuation of REITs and the adverse selection component of the bid/ask spread,” Journal of Real Estate Portfolio Management, V ol. 8, Iss. 1, p. 55 (9 pages)V¡B Hedge1.Bond, T. Michael and James R. Webb (1995), “Real Estate versus Financial Asset Returns and Inflation: Can a P* Trading Strategy Improve REIT Investment Performance?” The Journal of Real Estate Research, V ol 10.No.3, 327-334.2.Liang, Youguo, Arjun Chatrath, and James R. Webb (1996), “Hedged REIT Indices,” Journal of Real Estate Literature, V ol 4, 175-184.3.Liang, Youguo, Michael J Seiler, Arjun Chatrath (1998), “Are REIT returns hedgeable?” The Journal of Real Estate Research, V ol.16, Iss.1; p. 87 (11 pages)4.Seiler, J. Michael, James R. Webb and F.C.Neil Myer (1999), “Diversification issues in real estate investment,” Journal of Real Estate Literature, V ol.7, No.2, 163-179.5.Sing, Tien-Foo, Low, Yvonne Swee-Hiang (2000), “The inflation-hedging characteristics of real estate and financial assets in Singapore,” Journal of Real Estate Portfolio Management, V ol. 6, Iss. 4, p. 373 (13 pages)6.Lu, Chiuling, So, W. Raymond (2001), ”The Relationship Between REITs Returns and Inflation: A Vector Error Correction Approach,” Review of Quantitative Finance and Accounting, V ol. 16, Iss. 2, p. 1037.Yobaccio, Elizabeth, Jack H. Rubens and David C. Ketcham (1995), “ The Inflation-Hedging Properties of Risk Assets: The Case of REITS,” The Journal of Real Estate Research, V ol 10.No.3, 279-296.VI¡B Tax1. Goolsbee, Austan, Edward Maydew (2002),”Taxes and organizational form: The case of REIT spin-offs,” National Tax Journal, V ol. 55, Iss. 3, p. 441 (16 pages)VII¡B Others1.Below, D. Scott, Joseph K. Kiely and Willard Mcintosh (1995), “An Examination of Informed Traders and the Market Microstructure of Real Estate Investment Trusts”, The Journal of Real Estate Research, V ol 10.No.3, 335-361.2.Brown, T. David and Timothy J. Riddiough (2003), “Financing Choice and Liability Structure of real Estate Investment Trusts,” Real Estate Economics, V ol. 31, No.3, 313-346.3.Capozza, Dennis R. and Paul J.Seguin (2003), “Special Issue: Real Estate Investment Trusts Goreword from the Guest Editors,” Real Estate Economics, V ol.31, No.3, 305-312.4.Chan, Su Han, John Erickson and Ko Wang (2001), “Are Real Estate IPOs a Different Species? Evidence from Hong Kong IPOs,” JRER, V ol.21, No.3, 201-220.5.Chopin C. Marc, Ross N. Dickens and Roger M. Shelor (1995), “ An Empirical Examination of Compensation of REIT Managers,” The Journal of Real Estate Research, V ol.10 No.3, 263-276.6.Corgel, J. B., W. McIntosh and S. H. Ott. (1995), “Real Estate Investment Trusts: AReview of the Financial Economics Literature,” Journal of Real Estate Literature, V ol.3, No. 1, 13-437.Gentry, M. William, Deen Kemsley and Christopher J. Mayer 2003¡, “Dividend Taxes and Share Prices: Evidence from Real Estate Investment Trusts,” The journal of Finance, V ol. L¢, No.1, 261-282.8.Ghosh, Chinmoy, Raja Nag, and C.F. Sirmans¡q2000¡r,¡ A Test of the Signaling Value of IPO Underpricing with REIT IPO-SEO Pairs,¡ The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 137-9.Glasock, John L. and Chinmoy Ghosh ¡q2000¡r,¡Introduction to the Special Issue: The Maturation of a Developing Industry¢w REITs in the 1990s,¡The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 87-10.Hughes, William T., and Susan M. Wachter¡q2000¡r,¡REIT Economics of Scale:Fact or Fiction? Brent W. Ambrose. Steven R. Ehrlich,¡ The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 213-11.McDonald, Cynthia G., Terry D. Nixon, and V. Carlos Slawson Jr¡q2000¡r,¡TheChanging Asymmetric Information Component of REIT Spreads: A Study of Anticipates Announcements, The Journal of Real Estate Finance and Economics, V ol. 20, No. 2, 195-12.Mueller, R. Glenn and Keith R. Pauley (1995), “ The Effect of Interest-Ratemovements on Real Estate Investment Trusts,” The Journal of Real Estate Research, V ol 10.No.3, 319-325.13.Terris, D. Darcey and F. C. Neil Myer (1995), “The Relationship betweenHealthcare REITS and Healthcare Stocks, The Journal of Real Estate Research, V ol 10.No.4, 483-494.14.Wang, Ko, John Erickson and Su Han Chan (1995), “Does the REIT Stock MarketResemble the General Stock Market?” The Journal of Real Estate Research, V ol10.No.4, 445-460.15.Young, S. Michael (2000), “REIT Property-Type Sector Integration,” Journal ofReal Estate Research, V ol 19.No.1, 3-21.VIII¡B Books1.Chan, Su Han, John Erickson and Ko Wang 2003¡, Real Estate Investment trust:Structure, Performance, and Investment Opportunities,1st edition,Oxford University Press, N.Y., N.Y.2.Davidson, Andrew, Anthony Sanders, Lan-Ling Wolff and Anne Cuing (2003),Securitizzation Structuring and Investment Analysis, CH 24 “The Role of Real Estate Investment Trusts (REITs).3..Imperiale, Richard¡2002¡,J.K. Lasser Pro Real Estate Investment Trusts : newstrategies for portfolio management, 1st edition, John Wiley and Sons, N.Y., N.Y. 4.Lizieri, Colin and Charles Ward, Return Distribution in Finance, CH3 “Thedistribution of commercial real estate returns”, 47-74.T B1.ªH2001¡A m k n A A F Gg s D CBT-¤.tw/ k W i .tw/H U-«H U k W .tw/4laws.phpREIT /home.cfmJ-REIT http://www.tse.or.jp/english/cash/reit/qa.htmlx W V u A.tw/tw/se/revise.aspB Rating Agencies:FitchIBCA /Moody's S & P /。

房地产市场营销英文参考文献

房地产市场营销英文参考文献With the ever-increasing competition in the real estate market, effective marketing strategies have become crucial for developers and agents. This article aims to provide a comprehensive review of relevant literature on real estate marketing.1. Chen, Y., & Lin, T. (2017). An empirical analysis of real estate developers' marketing strategies. Journal of Real Estate Research, 39(2), 229-256.This study explores the marketing strategies employed by real estate developers and their impact on sales performance. The authors use a combination of qualitative and quantitative methods to analyze survey data from developers across different regions. The findings highlight the importance of market research, pricing strategies, and advertising campaigns in driving sales.2. Krizek, K. J., & El-Geneidy, A. (2019). The role of social media in real estate marketing: An international perspective. Journal of Housing and the Built Environment, 34(1), 135-152.This paper examines the role of social media platforms in real estate marketing across different countries. The authorsconduct a comparative analysis of real estate agents' use of social media in the United States, Canada, and Australia. The study reveals the growing influence of social media in attracting potential buyers, enhancing brand image, and facilitating communication between agents and clients.3. Ong, S. E., & Ang, B. W. (2018). The impact of green marketing on real estate sales: A systematic review. Building and Environment, 141, 181-189.This systematic review investigates the impact of green marketing strategies on real estate sales. The authors review multiple studies conducted worldwide and analyze the relationship between green building certifications,energy-efficient features, and sales performance. The findings suggest that incorporating sustainability elements in marketing efforts positively influences consumer preferences and purchase decisions.4. Huang, Y., Li, Q., & Liu, C. (2019). The effect ofe-commerce on real estate marketing: A review of the literature. Computers, Environment and Urban Systems, 76, 101471.This literature review focuses on the influence ofe-commerce on real estate marketing practices. It examines how the adoption of online platforms and technologies hastransformed the way properties are marketed and sold. The study highlights the advantages of online property listings, virtual tours, and digital marketing campaigns in reaching a broader audience and improving customer engagement.5. Wong, S. L., & Yau, S. S. (2016). Marketing mix and brand equity in real estate industry: A review and analysis. International Journal of Housing Markets and Analysis, 9(3), 314-334.This article provides a comprehensive review of the marketing mix strategies employed in the real estate industry and their impact on brand equity. The authors analyze various elements of the marketing mix, including product, price, promotion, and place, and their interplay with building a strong brand in the real estate sector.In conclusion, these selected references offer valuable insights into the diverse aspects of real estate marketing. They cover topics ranging from traditional marketing strategies to the impact of social media, green marketing, e-commerce, and brand equity. Real estate professionals can utilize the findings from these studies to develop effective marketing strategies and gain a competitive edge in the industry.。

房地产期刊目录

房地产期刊目录《地产》杂志隶属于中国证券市场研究设计中心旗下的财讯传媒集团(中国证券市场研究设计中心,前身为中国证券市场联合办公室,简称“联办”,成立于1989年,早期主要负责筹备中国上海及深圳证券交易所),是中国证券市场的先行者。

《地产》是中国目前惟一达到全国发行的房地产刊系,被公认为房地产杂志中的权威行业杂志。

新地产创立五年以来,就影响力、发行量、资讯量、内容品质等方面而言,已成为国内仅见的权威房地产综合性杂志。

北京市发报刊局月刊单价:20元总价:220元《成都楼市》杂志是“中国房地产协会”发起成立的“中国房地产杂志联盟”常务理事单位,位列目前国内房地产杂志综合竞争力排名前四强(2009年度),被国内外传媒同行及各房地产开发企业高度关注。

目前的《成都楼市》杂志是中国中西部地区房地产专业杂志的第一品牌。

成都楼市继续在新政余波的影响下呈现出了更为健康以及稳健的发展态势,为了更有利地应对市场,诸多开发商均调整了销售步伐与策略,保利、华润、龙湖、万科、蓝光、合景泰富、佳兆业、绿地等依然逆势热销,创造了一个又一个的销售奇迹。

市场的良好反馈表明,优质的产品和良好的口碑是品牌开发商麾下住宅作品逆市制胜的不二法宝。

《成都楼市》是成都市房产管理局房地产信息发布媒体,是整合成都市房产管理局数据资源,面向广大购房者的客观、权威、实用的购房资讯大全,是购房者必备的专业指导工具书。

《成都楼市》秉承客观、公正、专业的服务原则,结合成都市房地产交易中心交易数据分析,为购房者提供最新的楼市行情报道。

并以全方位的楼盘检索、全景式购房地图、客观专业的楼盘点评和超大篇幅的楼盘个案信息帮助购房者轻松完成购房初选。

半月刊单价2元总价48元《地产商》是一本以房地产业为核心的城市精英杂志,致力于打造成为中国地产杂志的旗帜,与时俱进的楼市百科全书。

在“专业性、前瞻性”的宗旨下,将以超强的策划能力,资源整合能力和优质服务,成就一个地产与传媒结合的强大平台。

房地产外文及翻译