《会计专业英语》期末试题(A卷)答案(共五则)

《财会专业英语》期末试卷及答案

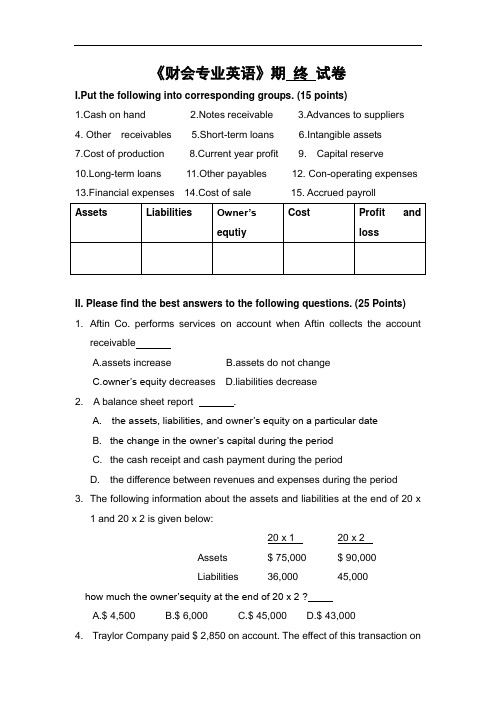

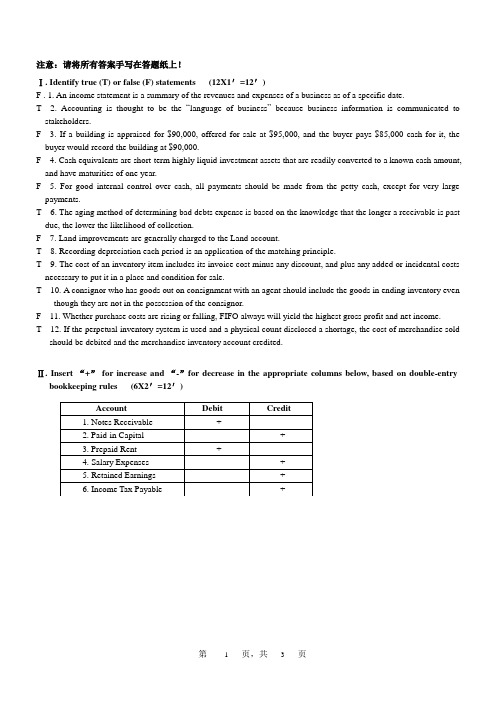

《财会专业英语》期终试卷I.Put the following into corresponding groups. (15 points)1.Cash on hand2.Notes receivable3.Advances to suppliers4. Other receivables5.Short-term loans6.Intangible assets7.Cost of production 8.Current year profit 9. Capital reserve10.Long-term loans 11.Other payables 12. Con-operating expenses 13.Financial expenses 14.Cost of sale 15. Accrued payrollAssets Liabilities Owner’sequtiy Cost Profit andlossII.Please find the best answers to the following questions. (25 Points) 1. Aftin Co. performs services on account when Aftin collects the accountreceivableA.assets increaseB.assets do not changeC.owner’s equity d ecreasesD.liabilities decrease2. A balance sheet report .A. the assets, liabilities, and owner’s equity on a particular dateB. the change in the owner’s capital during the periodC. the cash receipt and cash payment during the periodD. the difference between revenues and expenses during the period3. The following information about the assets and liabilities at the end of 20 x1 and 20 x2 is given below:20 x 1 20 x 2Assets $ 75,000 $ 90,000Liabilities 36,000 45,000how much the owner’sequity at the end of 20 x 2 ?A.$ 4,500B.$ 6,000C.$ 45,000D.$ 43,0004. Traylor Company paid $ 2,850 on account. The effect of this transaction onthe accounting equation is to .A. Decreas e assets and decrease owner’s equityB. Increase liabilities and decrease owner’s equityC. Have no effect on total assetsD. Decrease assets and decrease liabilities5. The entry to record the collection of $ 890 from a customer on account is .A. Dr.Accounts Payable 890Cr. Cash 890B. Dr.Cash 890Cr. Accounts Receivable 890C. Dr.Cash 890Cr. Account Payable 890D. Dr.Cash 890Cr. Service Revenue 8906. The ending Cash account balance is $ 57,600. During the period, cash receipts equal $ 124,300. If the cash payments during the period total $ 135,100, then the beginning Cash amount must haveA. $ 68,400B.$ 46,800C. $ 181,900D.annot be determined from theinformation given7. Use the following selected information for the Alecia Company to calculate the correct credit column total for a trial balance .Accounts receivable $ 7,200Accounts payable $ 6,900Building $ 179,400Cash $ 15,800Capital $ 64,000Insurance expense $ 6,500Salary expense $ 56,100Salary payable $ 3,600Service revenue $ 190,500A. $ 201,000B. $ 137,100C. $ 265,000D. $ 74,5008. ABC paid $500 for inventories in cash ,and purchased additional inventories on account for $700 in the month. At the end of the month,ABC paid $300 of the account payable.what is the balance in the inventoryies account?A $ 500B. $ 900C. $ 1,200D. $ 1,5009.The debit side of an account is used to recordA.increasesB.decreasesC. increases or decreases,depending on the type of accountD.decline10.ABC ,began the year with total assets of $120,000,liabilities of $70,000,and owner’s equit y of $50,000.during the year ABC earned revenue of $110,000 and paid espenses of $30,000.and also invensted an additional $20,000 in the business .how much is the owner’s equity at the end of the year?A. $150,000B.$180,000C.$190,000D.$220,00011.Which of the following is true? __________.A. Owners’ Equity - Assets = LiabilitiesB. Assets –Owners’ Equity = LiabilitiesC. Assets + Liabilities = Owners’ EquityD. Liabilities = Owners’ Equity + Assets12.Which of these is an example of an liability account? _____ ________.A. Service RevenueB. CashC. Accounts ReceivableD. Short-term loans13.Which of the following is a correct statement of the rules of debit and credit? ______.A. Debits increase assets and decrease liabilitiesB. Debits increase assets and increase owners’ equityC. Credits decrease assets and decrease liabilitiesD. Credits increase assets and increase owners’ equity14.If earnings haven’t been distributed as dividends, it should have been retained in the company. The name of this portion of number listed in the balance sheet is ____________.A. paid-in capitalB. retained earningsC. dividendD. cash15.Please select the components which should be deducted from the original value of plant assets when we compute their net value _______.A. Merchandise inventoryB. Income tax payableC. Accumulated depreciationD. Retained earnings16.Which of the following would not be included on a balance sheet?A. Accounts receivable.B. Accounts payable.C. Sales.D. Cash.17. Remington provided the following information about its balance sheet:Cash $ 100Accounts receivable 500Stockholders' equity 700Accounts payable 200Short-term loans 1,000Based on the information provided, how much are Remington's liabilities?A. $200.B. $900.C. $1,200.D. $1,700.18. Gerald had beginning total stockholders' equity of $160,000. During theyear, total assets increased by $240,000 and total liabilities increased by $120,000. Gerald's net income was $180,000. No additional investments were made; however, dividends did occur during the year. How much were the dividends?A. $20,000.B. $60,000.C. $140,000.D. $220,000.19.If the assets of a business are $162,600 and the liabilities are $86,000,howmuch is the owner’s equity?A..$76,600B. $248,600.C. $147,000.D. $250,000.20.Aftin Co. purchases on account when Aftin pay the account payableA.assets increaseB.assets do not changeC.owner’s equity decreasesD.liabilities decrease21.A income statement reports .A. the assets, liabilit ies, and owner’s equity on a particular dateB. the change in the owner’s capital during the periodC. the cash receipt and cash payment during the periodD. the difference between revenues and expenses during the period22.The following information about the assets and liabilities at the end of 20 x 1and 20 x 2 is given below: 20 x 1 20 x 2Assets $ 75,000 $ 90,000Liabilities 36,000 45,000 If net income in 20 x 2 was $ 1,500 and there were no withdrawals, how much did the owner invest?A.$ 4,500B.$ 6,000C.$ 45,000D.$ 43,00023.Traylor Company receive $ 2 850 on account. The effect of this transactionon the accounting equation is to .A. Decrease assets and decrease owner’s equityB. Increase liabilities and decrease owner’s equityC. Have no effect on total assetsD. Decrease assets and decrease liabilities24.The entry to record the collection of $ 8000 from a customer on accountis .A. Dr.Accounts Payable 8000Cr.Cash 8000B. Dr.Cash 8000Cr.Accounts Receivable 8000C. Dr.Cash 8000Cr.Account Payable 8000D. Dr.Cash 8000Cr.Service Revenue 800025.A list of a business entitys assests,liabilities,and owner’s equity on a givendate isA.a balance sheetB.an income statementC.a statement of cash flow C. A retained earnings statementIII. Translate the following sentences into Chinese.(10 points)1. The accounting profession today is changing rapidly.2. Assets are what you own.Liabilities are what you owe.Owner’s Equty iswhat’s left over .3. The original voucher is obtained or filled in what business transactions tookplace.4. Normally an asset account will have a debit balance.5. The term “debit” is often abbreviated to “Dr.”IV. Prepare a convenient bank reconciliation form according to the following bank statement and depositor’s book.(10 points)Bank StatementDate Description Money out Money In BalanceMay01 44 000May02 Salary 30 000May10 Check034 20 000May18 Interest Paid 5 000May23 Cash Withdrawal 15 000May31 Sales 38 000 72 000Depositor’s RecordDate Description Money out Money In Balance May01 44 000 May02 Salary 30 000May10 Check034 20 000May18 Check 035 46 000May23 Cash Withdrawal 15 000May31 Sales 50 000 43 000Bank ReconciliationDate MonthItems Amonut Items AmonutBalance per Bank Statement Balance per Depositor’sRecordAdd: Deposits not yetcredited by bankLess: Outstanding check Add: Items credited by the bank,bet not yetentered on books. Less: Items charged bythe bank,bet notyet entered onbooks.Adjusted Balance Adjusted BalanceV. Put the correct answer into the blanks.(6points)1.The basic Accouting equation is: .2.The rule of debits and credits is: ,.3. Using straight-line depreciation,Annual Dpreciation=( - )/VI. Translate The Following Terms Into Chinese . (10 points).1. surplus reserve2.manufacturing machine3. Construction in progress worth5. promissory note6. in other words7.profit distribution 8. storage room9.principal plus interest 10. accounting statementVII. The following is transactions of ABC company.please make entries.(24 poins)1. .ABC company was established on Jan.1,2010,when the owners,MrsSmiths and his friends,invested $30,000 in cash,patent X,valuing $24,000 and equipment A,valuing $40,000 into the company.2. ABC sells merchandise to another customer and send the customer a$2,500 bill for the products they provide. They allows the customer to pay these goods within 30 days.3. A customer buys $3,000 worth of goods from ABC ,and draws a promissorynote from a lacal bank.4. ABC buys a machine for $20,000,and pays the bill in cash.5. ABC paid the telephone bill for $700 in cash.6. ABC paid $3,800 on the accounts payable.7. ABC determine the month depreciation of the manufactory bulding for$5,000.8. ABC purchasese materials of $5,000 on account.9. ABC sells some goods to a client and receives a check from the customerfor $ 2,000 for the goods provided.10.ABC issues a 9%-5,$100,000 bond at its face amount. The bond is dated January 1, 2010 and requires interest payments until the bond principal at the end of 5 years.(1) Entry to bonds issued;(2) Entry to record the accrual interest for each year;(3) 2014 the company repays the principal plus interest.《财会专业英语》期末试卷答卷I.Put the following into corresponding groups. (15 points)Assets Liabilities Owner’sequtiy Cost Profit andlossII. Please find the best answers to the following questions. (25 Points) 1 2 3 4 5 6 7 8 9 1011 12 13 14 15 16 17 18 19 2021 22 23 24 25III. Translate the following sentences into Chinese.(10 points)1.2.3.4.5.IV. (10points)Bank ReconciliationDate MonthItems Amonut Items Amonut Balance per Bank Statement Balance per Depositor’s RecordAdd: Deposits not yetcredited by bank Less: Outstanding check Add: Items credited by the bank,bet not yet enteredon books.Less: Items charged by the bank,bet not yet enteredon books.Adjusted Balance Adjusted BalanceV. Put the correct answer into the blanks.(6points)1.The basic Accouting equation is: .2.The rule of debits and credits is: ,.3. Using straight-line depreciation,Annual Dpreciation=( - )/VI. Translate The Following Terms Into Chinese . (10 points).1. 2.3. 4.5. 6.7. 8.9. 10.VII. The following is transactions of ABC company.please make entries.(24 poins)《财会专业英语》答案I.Put the following into corresponding groups. (15 points)Assets Liabilities Owner’sequtiy Cost Profit andloss1、2、3、4、6、5、11、15 8、9、7、10、12、13、14II. Please find the best answers to the following questions. (25 Points)1 2 3 4 5 6 7 8 9 10B ACD B A C C C A11 12 13 14 15 16 17 18 19 20B D A BC C CD A D21 22 23 24 25D A C B AIII. Translate the following sentences into Chinese.(10 points)(略)IV. (10points)Bank ReconciliationDate 31 Month MayItems Amonut Items Amonut Balance per Bank Statement 72 000 Balance per Depositor’s Record43 000Add: Deposits not yetcredited by bank Less: Outstanding check 50 00046 000Add: Items credited by thebank,bet not yet enteredon books.Less: Items charged by thebank,bet not yet enteredon books.38 0005 000Adjusted Balance 76 000 Adjusted Balance 76 000 V. Put the correct answer into the blanks.(6points)1.Asse ts=Liabilities+Owner’s equity .2. Every debit must have a credit,all debits must equal all credits. ,3. Using straight-line depreciation,Annual Dpreciation=( Original Cost- Salvage Value) /Years of Service LifeVI. Translate The Following Terms Into Chinese . (10 points).(略)VII. The following is transactions of ABC company.please make entries.(24 poins)(略)Love is not a maybe thing. You know when you love someone.。

10级会计英语期末考试卷A答案卷(可编辑修改word版)

2010 级 XXXX 试卷 A 卷 第 1 页 共 2 页海丰县中等职业技术学校期末考试试卷 A 卷(2011-2012 学年度第一学期)考试年级: 10 级 考试科目:Accounting English 成绩:Ⅰ Single choice.(15%)1. Assets can be divided intoC .A. long-term assets and short-term assetsB. current assets and long-term assetsC. current assets and fixed assets2. General ledger account is generally set by Baccording to the current accounting policiesin our country.A. police stationB. ministry of financeC. politics3.A are the symbols of bookkeeping.A. Debit and creditB. DebitC. Credit4.A is one of the accounting methods used by accountants worldwide.A. Debit-credit bookkeepingB. Double entry bookkeepingC. Journal entry5. In order to ensure the correctness and reliability of the accounting material and protect the entirety ofproperty, we must doC .A. property calculationB. cost calculationC. property checking6.The fixes assets belong toB .A. current assetsB. tangible assetsC. intangible assets7. F or our country, which form of the income statement does we adoptC.A. single-step formB. two-step formC. multiple-step form8. T he original vouchers includeA, transfer check stub and receipt in the operation ofpurchasing material and storage of material in the warehouse after check.A. invoice for purchasesB. invoice for transport chargeC. payment 9.How many sources of fund procurement are there?B.A. OneB. TwoC. Three10. The value of raw material transfers into the product A .A. once onlyB. twiceC. gradually11.C assets need to be depreciated periodically in its service life in accounting .A. TangibleB. IntangibleC. Fixed12. Salary for salesperson is recorded underB.A. operating expenseB. administrative expenseC. operating cost13. There are two forms of the balance sheet. One is account form, the other is B.A. single-step form B report formC. multiple-step form14.Assets=C+ Owner’s equity.A. LiabilityB. RevenueC. Liabilities15.Revenue-Expenses= A.A. ProfitsB. LiabilitiesC. ExpensesⅡ Multiple choice.(20%)1. Posting documents include ABC .A. receipt voucherB. payment voucherC. transfer voucherD. accounting voucher 2.Filling in the original voucher BD .A. only in black inkB. in blue inkC. with ball penD. in black ink3.In the operation of purchasing fixed assets, the original voucher include ABCD.A. invoice for purchasesB. invoice for transport chargeC. receiptD. transfer check stub4.Which belongs to the fixed assets?BC. A. glasswareB. equipmentC. machineD. buckets5.The fixed assets AD.A .have high valueB. can be taken back after many yearsC. can be consumed easilyD. are called tangible assets.6.The fixed assets are held by ABCD.A. manufacture merchandiseB. offer laborC. rentingD. management班级:座号:姓名:装订线10.How many kinds of revenue are there? ABCD .A. The income for selling goodsB. The income for offering serviceC. The income for transferring assetsD. The income for selling fixed assets Ⅲ Gap filling.(15%)1.The three accounting elements which reflect the financial standing areliabilities , owner’s equity . assets ,2.A company got a six-month loan of RMB 20 000 from Industrial and Commercial Bank of China and athree-year loan of RMB 100 000 from Agricultural Bank of China. Both the amount has been deposited intothe bank. Please make the entry. (5% )The entry would be: Dr: Bank deposit 120 000Cr: Short-term loan 20 000Long-term loan 100 0002.Double Entry bookkeeping is divided into_debit-credit bookkeeping_,receipts-payment bookkeeping,increase-decrease bookkeeping.Debit-credit bookkeeping_is internationally used and compulsorily used in China as well.3.There are two sources of fund procurement ,one is _invested capital and the other is borrowedcapital .4.Investors can invest in many ways like _cash , equipment and material .Intangible assets can be used if the proportion stipulated is matched.5.The loan can be divided into _long-term loan and short-term loan according to the maturity.Ⅳ True ( T ) or False ( F ).(10%)1.T he income must be the increase in assets. ( F )2.T he enterprise should confirm the revenue when handing the ownership evidence or the stuff to theopposite party. ( T )3.T he short-term loan needs to be returned in one year and a half and the long-term loan can be returnedover one year and a half. ( F )4.I nterest is recorded under finance charge. ( T )5.The advertising expense is recorded in the administrative expenses.( F )Ⅴ Practice.(40%)1.A catering company bought equipment last month with the price of RMB 150 000.The expected service life is 5 years. The depreciation is calculated. ( 5% )The entry would be:Dr: Operating expenses 2 500Cr: Accumulative depreciation 2 500 3.I f the materials an ice-cream company used in a month include the ice-cream powder with 20 kilograms and RMB 50 each kilogram, seasoning of RMB 200, the salary for employees of RMB 5 000 per month, charge for electricity and water of RMB 1200, rent of RMB 4 000 and depreciation of the equipment of RMB 1000. Write down the concerned accounts. (10%)The entry would be:Dr: Operating cost 1 200 Dr: Operating expenses 1 000Cr: Material 1 200 Cr: accumulative depreciation 1 000Dr: Administrative expenses 5 000 Dr: Administrative expenses 5 200Cr: Wages payable 5 000 Cr: Account payable --- electricity and water 1 200--- rent 4 0004.C ompany A has purchased 1 000 skirts with cost of RMB 50 each one and unit sales price of RMB 100, but hasn’t received the payment. The accounting system for small-sized corporation is applied. Please make the accounting entry.( business tax rate takes 5% of the sales revenue, tax for maintaining and building cities and for extra charges of education funds takes 7% and 3% of business turnover(营业额).) (20% )The entry would be:Dr: Bank deposit 100 000 Dr: Operating cost 50 000Cr: Operating revenue 100 000 Cr: Merchandise inventory 50 000Dr: Tax and associate charge 5 000Cr: Tax payable---business tax payable 5 000Dr: Tax and associate charge 500Cr: Tax payable---Tax for maintaining and building cities payable 35---extra charges of education funds 152010 级XXXX 试卷A 卷第2 页共2 页。

《会计英语》期末试卷A

《会计英语》期末试卷A2011-2012学年第一学期期末考试试卷(A卷)级专业学生姓名学号成绩I.将下列科目正确分类,填入表格中. (16 points)1.Cash on hand2.Notes receivable3.Sales4.Paid-in capital5.Short-term loans6.Intangible assets7.Cost of production 8.Current year profit 9. Raw materials 10. General and administrative expenses 11.Accounts receivabl 12.Fixed assets 13.Financial expenses 14.Cost of sale15.Sales tax 16.Accrued payrollII. 将下列词汇字母填入适当的横线(7 points)A.dibitB.creditC.leftD.rightE. out of balanceF. in balance1.To ① means to record an amount on the right side.2.The word ② is used to refer to the left side of a liability account and the ③ side of a revenue account.3.When the sum of the amount on the left side is equal tothe sum of the amount on the right side,the account is said to be④ .4. When the sum of the amount on the left side is not equal to the sumof the amount on the right side,the account is said to be ⑤ .5.The word ⑥ is used to refer to the right si de of a Asset accountandthe ⑦ side of a cost account.III将下列词汇和他们的解释相匹配.(10 points)1.account2.balance3.asset account4.debit5.credit6.purchase7.taxation 8.accountant 9.budget10.financialA.a person whose profession is to keeping and examine business accountsB.buy somethingC.the system of charging taxesD.a tool used to illustrate business transactions,desreases or increasesin assetes,liabilitiesand other accounting elementsE.the left side of an accountF.an account recording properties used in the operation or investing.G.the right side of an accountH.the differnece between the debits and credits of anaccountI.an estimate of probable future income and expenditureJ.relating to money or the management of money.IV. 选择题。

会计专业英语试卷(推荐5篇)

A.withdrawalsB.accounts receivableC.interest payable 6.Which of the following is an assets account?

A.notes missionC.bonds payable 7.Which of the following is an owner’s equity account?

Passage 1

Many rule govern drivers on the streets and highways.The most common one is the speed limit.The speed limit controls how fast a car may go.On streets in the city, the speed limit is usually 25 or 35 miles per hour.On the highways between cities, the speed limit is usually 55 miles per hour.When people drive faster than the speed limit, a policeman can stop them.The policeman gives them pieces of paper which call traffic tickets.Traffic tickets tell the drivers how much they must pay.When drivers receive too many tickets, they probably cannot drive for a while.The rush hour is when people are going to or returning from work.At rush hour there are many cars on the streets and traffic moves very slowly.Nearly al big cities have rush hours and traffic jams.Drivers do not get tickets very often for speeding during the rush hour because they cannot drive fast.1.The most common rule to govern drivers on the streets and highways is _____.A.the traffic lightB.the traffic licenseC.the traffic jamD.th计专业英语试卷(推荐5篇)

会计英语(A)试题及答案

会计英语期末考试题(A卷)I. Multiple Choices (10%)1、Users of accounting information who have a direct interest in the business include().A. Present and Potential Investors;B. Present and Potential Creditors;C. Management;D. Tax Authorities;E. Customers and the general public2、In most cases, the management of a corporation consists of ( ).A、president;B、vice president;C、controller;D、treasurer;E、secretary3、Which of the following expressions are belonged to intangible assets? ( )A、cash in the safe; B. accounting system software; C. brand name; D. office building;E. customer and supplier relationship4、The source documents of the business transaction include ( ).A、cancelled checks;B、supplier invoices;C、cash receipts;D、purchase orders;E、notes for loan5、Which of the following businesses should draw up financial statements? ( ).A、private individuals;B、non-profit organizations;C、retailers;D、wholesalers;E、service Industries6、The closing entries consist of ( ) steps.A、2;B、3;C、4;D、5;E、67、Cash receipts of a company include ( ).A、bills;B、coins;C、promissory note signed by the customer;D、checks signed by the customer;E、goods paid by the credit cards8、Cash flow can be divided into three components which are ( ).A、Managing cash flow;B、Operating cash flow;C、Investing cash flow;D、Financing cash flow;E、Marketing cash flow9、Three generally accepted methods that may be used to estimate the allowance are ( ).A、Percentage of Credit Sales Method;B、Total Sales Method;C、Accounts Receivable Aging Method;D、Percentage of Receivables Method;E、Straight-line Method10、A promissory note is signed on October 3rd, due in 60 days, maturity date of the note is ( ).A、November 30th;B、December 1st;C、December 2nd;D、December 3rd;E、December 4thII. Write T (true) before the statements which are true and F (false) before the statements which are false. (5%)1、()Stockholders should take part in the daily management and the decision-making.2、()Purchasing assets by incurring a liability will increase both the assets and liabilities. However, owner’s equity will be unaffected.3、()The balance of debits and credits means that there is not any error during the recording and calculating.4、()At the end of an accounting period, the prepaid expenses should be adjusted. Otherwise, the assets will be understated and the expenses will be exaggerated.5、()More profit means more cash on hand.III. Words and T erms (16%)1、Notes Receivable ______________________2、Prepaid Insurance ___________________3、journal __________________4、Accumulated Depreciation ____________________5、accrual accounting __________________6、Sales returns and allowances ________________7、bad debts __________________8、maturity date ____________________9、存货_________________ 10、预收影印费_________________________ 11、复式记账________________________ 12、红利______________________13、会计循环_______________________ 14、试算平衡_________________________ 15、损益汇总账户______________________16、有价证券_______________________IV. Fill in the following blanks with proper words. (14%)1、Three basic forms of business organization are:____________________、________________ and corporations .2、The expanded accounting equation is: Assets = Liabilities + Owner’s equity + ________________ —_________________3、Basically, the T account has three parts: a _______________, the debit and the _____________.4、Promissory notes are classified as ______________________ notes and ____________________ notes.5、The _______________________ is a collection of the business’s accounts and often takes the form of simple ___________________________ account.6、At the beginning of accounting period, the investment cost of marketable securities includes ________________, taxes, and ________________________ .7、Net income equals _____________________________ less ____________________________.V. T ranslate the following sentences into Chinese. (15%)1、Accounting is defined as “an information system that measures, processes, and communicates financial information about an identifiable economic entity”.2、Cash consists of money or any medium of exchange that a bank will accept at face value for deposit, and money in a bank or banks.3、The accounting cycle refers to the accounting process that begins with the analysis of transactions to the closing of books.4、Analyzing how the balance sheet changes over time will reveal essential information about the company’s business trends.5、The estimate of the uncollectibles at the end of a fiscal period should be based on past experience and forecasts of future business activity.VI. Calculating based on the information given. (15%)1、At the beginning of 2011, the assets of Brian Smith Company were $250,000, and its owner’s equity was $135,000. During the year, assets increased $45,000, and liabilities decreased $8,000. What was the owner’s equity at the end of 2011?2、On June 5, 2011, Tracy Norwood Company sold customer $20,000 of merchandise, terms 2/10, 1/20, n/30, on which a sales return of $800 is granted on June 11. Tracy received payment in full from customer on June 17. Please calculate the amount the customer has to pay on June 17.3、In order to raise cash, George Ross Co. discounted a $4000, 90-day note 30 days before the maturity date. Interest rate of the note is 8% and the discount rate is 10%. Please compute the proceeds from discount.VII、Make entries and financial statements. (25%)On December 31st, 20XX, Mike Andrew got the following ledger accounts: Cash —$6,780 (dr.); Accounts Receivable —$1,600 (cr.); Prepaid Insurance —$480 (dr.); Supplies —$600 (dr.); Cutting Machine —$920 (dr.); Accounts Payable —$40 (cr.); Mike Andrew, Capital —$6,800 (cr.); Service Revenue —$580 (cr.); Wages Expense —$200 (dr.); Telephone Expense —$40 (dr.).Suppose $200 of supplies had been used up within this month. The estimated useful life of cutting machine is 2 years and salvage value is zero. The insurance policy is one year.Make the entries of adjustment and prepare work sheet, income statement, statement of owner’s equity and balance sheet according to these accounts.1、Entries of adjustment2、Work SheetMike Andrew CompanyWork SheetDec.31, 20XX3、Income StatementMike Andrew CompanyIncome Statement4、Statement of Owner’s EquityMike Andrew CompanyStatement of Owner’s Equity5、Balance SheetMike Andrew CompanyBalance Sheet会计英语A卷答案一、多选题:1、ABC2、ABCDE3、BCE4、ABCDE5、ABCDE6、C7、ABDE8、BCD9、ACD10、C评分标准:共计10分,每题1分,多选、少选、错选均不得分二、判断题:1、F2、T3、F4、F5、F评分标准:共计5分,每题1分三、词汇题:1、应收票据2、预付保险费3、日记账4、累计折旧5、权责发生制会计(应计会计)6、销售退回与折让7、坏账8、到期日9、inventory10、Unearned Photocopy Fees11、double-entry bookkeeping12、dividend 13、accounting cycle14、trial balance15、income summary account16、marketable securities评分标准:共计16分,每题1分。

《财会专业英语》期末考试卷及问题详解

《财会专业英语》期终试卷I.Put the following into corresponding groups. (15 points)1.Cash on hand2.Notes receivable3.Advances to suppliers4. Other receivables5.Short-term loans6.Intangible assets7.Cost of production 8.Current year profit 9. Capital reserve10.Long-term loans 11.Other payables 12. Con-operating expenses 13.Financial expenses 14.Cost of sale 15. Accrued payrollII.Please find the best answers to the following questions. (25 Points) 1. Aftin Co. performs services on account when Aftin collects the accountreceivableA.assets increaseB.assets do not changeC.owner’s equity d ecreasesD.liabilities decrease2. A balance sheet report .A. the assets, liabilities, and owner’s equity on a particular dateB. the change in the owner’s capital during the periodC. the cash receipt and cash payment during the periodD. the difference between revenues and expenses during the period3. The following information about the assets and liabilities at the end of 20 x1 and 20 x2 is given below:20 x 1 20 x 2Assets $ 75,000 $ 90,000Liabilities 36,000 45,000how much the owner’sequity at the end of 20 x 2 ?A.$ 4,500B.$ 6,000C.$ 45,000D.$ 43,0004. Traylor Company paid $ 2,850 on account. The effect of this transaction onthe accounting equation is to .A. Decreas e assets and decrease owner’s equityB. Increase liabilities and decrease owner’s equityC. Have no effect on total assetsD. Decrease assets and decrease liabilities5. The entry to record the collection of $ 890 from a customer on account is .A. Dr.Accounts Payable 890Cr. Cash 890B. Dr.Cash 890Cr. Accounts Receivable 890C. Dr.Cash 890Cr. Account Payable 890D. Dr.Cash 890Cr. Service Revenue 8906. The ending Cash account balance is $ 57,600. During the period, cash receipts equal $ 124,300. If the cash payments during the period total $ 135,100, then the beginning Cash amount must haveA. $ 68,400B.$ 46,800C. $ 181,900D.annot be determined from theinformation given7. Use the following selected information for the Alecia Company to calculate the correct credit column total for a trial balance .Accounts receivable $ 7,200Accounts payable $ 6,900Building $ 179,400Cash $ 15,800Capital $ 64,000Insurance expense $ 6,500Salary expense $ 56,100Salary payable $ 3,600Service revenue $ 190,500A. $ 201,000B. $ 137,100C. $ 265,000D. $ 74,5008. ABC paid $500 for inventories in cash ,and purchased additional inventories on account for $700 in the month. At the end of the month,ABC paid $300 of the account payable.what is the balance in the inventoryies account?A $ 500B. $ 900C. $ 1,200D. $ 1,5009.The debit side of an account is used to recordA.increasesB.decreasesC. increases or decreases,depending on the type of accountD.decline10.ABC ,began the year with total assets of $120,000,liabilities of $70,000,and owner’s equit y of $50,000.during the year ABC earned revenue of $110,000 and paid espenses of $30,000.and also invensted an additional $20,000 in the business .how much is the owner’s equity at the end of the year?A. $150,000B.$180,000C.$190,000D.$220,00011.Which of the following is true? __________.A. Owners’ Equity - Assets = LiabilitiesB. Assets –Owners’ Equity = LiabilitiesC. Assets + Liabilities = Owners’ EquityD. Liabilities = Owners’ Equity + Assets12.Which of these is an example of an liability account? _____ ________.A. Service RevenueB. CashC. Accounts ReceivableD. Short-term loans13.Which of the following is a correct statement of the rules of debit and credit? ______.A. Debits increase assets and decrease liabilitiesB. Debits increase assets and increase owners’ equityC. Credits decrease assets and decrease liabilitiesD. Credits increase assets and increase owners’ equity14.If earnings haven’t been distributed as dividends, it should have been retained in the company. The name of this portion of number listed in the balance sheet is ____________.A. paid-in capitalB. retained earningsC. dividendD. cash15.Please select the components which should be deducted from the original value of plant assets when we compute their net value _______.A. Merchandise inventoryB. Income tax payableC. Accumulated depreciationD. Retained earnings16.Which of the following would not be included on a balance sheet?A. Accounts receivable.B. Accounts payable.C. Sales.D. Cash.17. Remington provided the following information about its balance sheet:Cash $ 100Accounts receivable 500Stockholders' equity 700Accounts payable 200Short-term loans 1,000Based on the information provided, how much are Remington's liabilities?A. $200.B. $900.C. $1,200.D. $1,700.18. Gerald had beginning total stockholders' equity of $160,000. During theyear, total assets increased by $240,000 and total liabilities increased by $120,000. Gerald's net income was $180,000. No additional investments were made; however, dividends did occur during the year. How much were the dividends?A. $20,000.B. $60,000.C. $140,000.D. $220,000.19.If the assets of a business are $162,600 and the liabilities are $86,000,howmuch is the owner’s equity?A..$76,600B. $248,600.C. $147,000.D. $250,000.20.Aftin Co. purchases on account when Aftin pay the account payableA.assets increaseB.assets do not changeC.owner’s equity decreasesD.liabilities decrease21.A income statement reports .A. the assets, liabilities, and owner’s equity on a particular dateB. the change in the owner’s capital during the periodC. the cash receipt and cash payment during the periodD. the difference between revenues and expenses during the period22.The following information about the assets and liabilities at the end of 20 x 1and 20 x 2 is given below: 20 x 1 20 x 2Assets $ 75,000 $ 90,000Liabilities 36,000 45,000 If net income in 20 x 2 was $ 1,500 and there were no withdrawals, how much did the owner invest?A.$ 4,500B.$ 6,000C.$ 45,000D.$ 43,00023.Traylor Company receive $ 2 850 on account. The effect of this transactionon the accounting equation is to .A. Decrease assets and decreas e owner’s equityB. Increase liabilities and decrease owner’s equityC. Have no effect on total assetsD. Decrease assets and decrease liabilities24.The entry to record the collection of $ 8000 from a customer on accountis .A. Dr.Accounts Payable 8000Cr.Cash 8000B. Dr.Cash 8000Cr.Accounts Receivable 8000C. Dr.Cash 8000Cr.Account Payable 8000D. Dr.Cash 8000Cr.Service Revenue 800025.A list of a business entitys assests,liabilities,and owner’s equity on a givendate isA.a balance sheetB.an income statementC.a statement of cash flow C. A retained earnings statementIII. Translate the following sentences into Chinese.(10 points)1. The accounting profession today is changing rapidly.2. Assets are what you own.Liabilities are what you owe.Owner’s Equty iswhat’s left over .3. The original voucher is obtained or filled in what business transactions tookplace.4. Normally an asset account will have a debit balance.5. The term “debit” is often abbreviated to “Dr.”IV. Prepare a convenient bank reconciliation form according to the following bank statement and depositor’s book.(10 points)Bank StatementDepositor’s RecordBank ReconciliationDate MonthV. Put the correct answer into the blanks.(6points)1.The basic Accouting equation is: .2.The rule of debits and credits is: ,.3. Using straight-line depreciation,Annual Dpreciation=( - )/VI. Translate The Following Terms Into Chinese . (10 points).1. surplus reserve2.manufacturing machine3. Construction in progress worth5. promissory note6. in other words7.profit distribution 8. storage room9.principal plus interest 10. accounting statementVII. The following is transactions of ABC company.please make entries.(24 poins)1. .ABC company was established on Jan.1,2010,when the owners,MrsSmiths and his friends,invested $30,000 in cash,patent X,valuing $24,000 and equipment A,valuing $40,000 into the company.2. ABC sells merchandise to another customer and send the customer a$2,500 bill for the products they provide. They allows the customer to pay these goods within 30 days.3. A customer buys $3,000 worth of goods from ABC ,and draws a promissorynote from a lacal bank.4. ABC buys a machine for $20,000,and pays the bill in cash.5. ABC paid the telephone bill for $700 in cash.6. ABC paid $3,800 on the accounts payable.7. ABC determine the month depreciation of the manufactory bulding for$5,000.8. ABC purchasese materials of $5,000 on account.9. ABC sells some goods to a client and receives a check from the customerfor $ 2,000 for the goods provided.10.ABC issues a 9%-5,$100,000 bond at its face amount. The bond is dated January 1, 2010 and requires interest payments until the bond principal at the end of 5 years.(1) Entry to bonds issued;(2) Entry to record the accrual interest for each year;(3) 2014 the company repays the principal plus interest.《财会专业英语》期末试卷答卷I.Put the following into corresponding groups. (15 points)II. Please find the best answers to the following questions. (25 Points)III. Translate the following sentences into Chinese.(10 points)1.2.3.4.5.IV. (10points)Bank ReconciliationDate MonthV. Put the correct answer into the blanks.(6points)1.The basic Accouting equation is: .2.The rule of debits and credits is: ,.3. Using straight-line depreciation,Annual Dpreciation=( - )/VI. Translate The Following Terms Into Chinese . (10 points).1. 2.3. 4.5. 6.7. 8.9. 10.VII. The following is transactions of ABC company.please make entries.(24 poins)《财会专业英语》答案I.Put the following into corresponding groups. (15 points)II. Please find the best answers to the following questions. (25 Points)III. Translate the following sentences into Chinese.(10 points) (略)IV. (10points)Bank ReconciliationDate 31 Month MayV. Put the correct answer into the blanks.(6points)1.Assets=Liabilities+Owner’s equity .2. Every debit must have a credit,all debits must equal all credits. ,3. Using straight-line depreciation,Annual Dpreciation=( Original Cost- Salvage Value) /Years of Service LifeVI. Translate The Following Terms Into Chinese . (10 points).(略)VII. The following is transactions of ABC company.please make entries.(24 poins)(略)。

会计专业英语试题及答案

会计专业英语试题及答案一、选择题(每题2分,共20分)1. Which of the following is not an accounting principle?A. Accrual BasisB. Going ConcernC. ConsistencyD. Cash BasisAnswer: D2. The process of summarizing, analyzing, and reporting financial data is known as:A. BudgetingB. AccountingC. AuditingD. TaxationAnswer: B3. What is the term used to describe the systematic and periodic recording of financial transactions?A. BookkeepingB. PayrollC. TaxationD. AuditingAnswer: A4. Which of the following is not a component of the balance sheet?A. AssetsB. LiabilitiesC. EquityD. RevenueAnswer: D5. The matching principle requires that:A. Expenses are recognized when incurredB. Expenses are recognized when paidC. Expenses are recognized in the same period as the revenue they generateD. Expenses are recognized when the cash is received Answer: C6. The accounting equation is:A. Assets = Liabilities + EquityB. Assets - Liabilities = EquityC. Assets + Equity = LiabilitiesD. Assets = Equity - LiabilitiesAnswer: A7. The term "double-entry bookkeeping" refers to the practice of:A. Recording transactions twiceB. Recording transactions in two accountsC. Recording debits and credits for every transactionD. Recording transactions in two different booksAnswer: C8. Which of the following is not a type of intangible asset?A. PatentsB. TrademarksC. GoodwillD. InventoryAnswer: D9. The purpose of an income statement is to show:A. The financial position of a company at a point in timeB. The changes in equity over a period of timeC. The financial performance of a company over a period of timeD. The cash flows of a company over a period of time Answer: C10. The statement of cash flows is used to report:A. How cash is generated and used during a periodB. The net income of a company for a periodC. The changes in equity for a periodD. The changes in assets and liabilities for a period Answer: A二、填空题(每题2分,共20分)1. The accounting cycle includes the following steps:journalizing, posting, __________, adjusting entries, and closing entries.Answer: trial balance2. The __________ principle requires that all business transactions should be recorded at their fair value in the accounting records.Answer: Fair Value3. The __________ is a summary of all the journal entries fora period, listed in date order.Answer: General Journal4. __________ are expenses that have been incurred but not yet paid.Answer: Accrued Expenses5. The __________ is a report that shows the beginning cash balance, cash receipts, cash payments, and the ending cash balance for a period.Answer: Cash Flow Statement6. The __________ ratio is calculated by dividing current assets by current liabilities.Answer: Current Ratio7. __________ are assets that are expected to be converted into cash or used up within one year or one operating cycle. Answer: Current Assets8. __________ is the process of determining the cost of goodssold and the value of ending inventory.Answer: Costing9. __________ is the process of estimating the useful life of an asset and allocating its cost over that period.Answer: Depreciation10. __________ is the process of adjusting the accounts to reflect the proper revenue and expenses for the period. Answer: Accrual Accounting三、简答题(每题10分,共20分)1. Explain the difference between revenue and profit. Answer: Revenue is the income generated from the normal business activities of an entity during a specific period, before deducting expenses. Profit, on the other hand, is the excess of revenues and gains over expenses and losses for a period. It represents the net income or net earnings of a business.2. What are the main components of a balance sheet?Answer: The main components of a balance sheet are assets, liabilities, and equity. Assets represent what a company owns or controls with future economic benefit. Liabilities are obligations or debts that a company owes to others. Equity is the residual interest in the assets of the entity after deducting all its liabilities, representing the ownership interest of the shareholders.四、计算题(每题15分,共30分)1. Calculate the net income for the year if the revenue is$500,000, the cost of goods sold is $300,000, operating expenses are $80,000, and other expenses are $20,000. Answer: Net Income = Revenue - Cost of Goods Sold - Operating。

会计英语试卷含答案.doc

会计专业英语期末考试试卷1考试时间:2小时总分:100分一、判断:每题1分,共10分(正确的在题后括号内打钩,错误的打叉。

)1、R etained earning is not an asset; it is an element of stockholders'equity.( )2、在收付实现制下,收入是按照它在实际发生的期间,而不是实际收取现款的期间登记入账。

()3、The subsidiary accounts receivable ledger trial balance should agreewith the balance of the accounts receivable account in the general ledger.( )4、Cash budgets are not important to the management of cash flows.( )5、Profits decrease the owner's equity in the business. ( )6、All inventories shall be taken stock periodically. ( )7、In the periodic inventory system(实地盘存制),the business does not keep acontinuous record of the inventory on hand.( )8、Non-current liabilities are obligations that must be paid within one year or theoperating cycle (whichever is longer).( )9、Central to the definition of a contingent liability is the element ofuncertainty.( )10、T he owner, s equity in a business is increased by borrowing money froma bank.( )二、单项选择题:每题2分,共20分(每题只有1个正确答案,多选或选错不得分)1、W hen an amount is entered on the ( ) side of an account, it is a credit, and theaccount is said to be credited.A、leftB、rightC、left or rightD、others2、Which is not included in long-term assets?( )A、fixed assetsB、intangible assetsC、cashD、deferred assets3、If a delivery truck costs $ 10, 000 and has an estimated residual value (残值)of $ 2, 000 at the end of its estimated useful life of fiveyears, the annual depreciation would be ( ) under the straight-line method.A、$ 2, 400B、$2, 000C、$ 1, 800D、$ 1, 6004、Total assets will be ( ) by the act of borrowing money from a bank.A、decreasedB、increasedC、remained (保持不变)D、uncertain5、The owners of a corporation (股份公司)are termed (称为)( )A、stockholdersB、investorsC、creditorsD、none of above (都不是)6、()是指会计忽略通货膨胀影响,对货币价值变动不作调整。

会计英语 期末试题及答案

会计英语期末试题及答案第一部分:单项选择题(共20题,每题1分,共20分)1. The ________ principle states that expenses should be recorded and recognized in the accounting period in which they are incurred.a) Materialityb) Matchingc) Conservatismd) Historical cost答案:b) Matching2. In accounting, the term "debit" refers to:a) An increase in an asset or expense accountb) An increase in a liability or revenue accountc) A decrease in an asset or expense accountd) A decrease in a liability or revenue account答案:a) An increase in an asset or expense account3. The ________ principle states that all relevant information that could affect the decision-making of users should be included in the financial statements.a) Materialityb) Faithful representationc) Comparabilityd) Relevance答案:d) Relevance4. The balance sheet reports:a) Revenues, expenses, and net incomeb) Assets, liabilities, and equityc) Cash flows from operating, investing, and financing activitiesd) Changes in equity during the accounting period答案:b) Assets, liabilities, and equity5. Which of the following statements about the accrual basis of accounting is true?a) Revenues and expenses are recognized when cash is received or paidb) Transactions are recorded when they occur, regardless of when cash is received or paidc) Only cash transactions are recorded in the financial statementsd) Liabilities and expenses are recognized when they are incurred, and revenues are recognized when cash is received答案:b) Transactions are recorded when they occur, regardless of when cash is received or paid6. The financial statement that shows a company's revenues, expenses, and net income or loss for a specific period of time is the:a) Income statementb) Statement of cash flowsc) Balance sheetd) Statement of retained earnings答案:a) Income statement7. A decrease in an asset account is recorded as a ________.a) Debitb) Creditc) Liabilityd) Equity答案:b) Credit8. The accounting equation can be expressed as:a) Assets = Liabilities + Equityb) Assets + Liabilities = Equityc) Equity = Assets + Liabilitiesd) Liabilities + Equity = Assets答案:a) Assets = Liabilities + Equity9. The financial statement that shows the changes in equity during the accounting period is the:a) Income statementb) Statement of cash flowsc) Balance sheetd) Statement of retained earnings答案:d) Statement of retained earnings10. Which of the following is an example of an intangible asset?a) Landb) Buildingsc) Inventoryd) Goodwill答案:d) Goodwill11. The ________ principle states that assets should be recorded at their original cost.a) Objectivityb) Consistencyc) Historical costd) Materiality答案:c) Historical cost12. The statement of cash flows reports:a) Revenues, expenses, and net incomeb) Assets, liabilities, and equityc) Cash flows from operating, investing, and financing activitiesd) Changes in equity during the accounting period答案:c) Cash flows from operating, investing, and financing activities13. Which of the following is a current liability?a) Accounts payableb) Bond payable due in 10 yearsc) Mortgage payable due in 5 yearsd) Long-term note payable答案:a) Accounts payable14. The ________ principle states that the financial statements should be prepared assuming that the entity will continue to operate indefinitely.a) Going concernb) Revenue recognitionc) Materialityd) Consistency答案:a) Going concern15. Which financial statement reports the financial position of a company at a specific point in time?a) Income statementb) Statement of cash flowsc) Balance sheetd) Statement of retained earnings答案:c) Balance sheet16. The ________ states that an entity should use the same accounting methods and procedures from period to period.a) Materialityb) Going concernc) Consistencyd) Historical cost答案:c) Consistency17. What type of account is "Accounts Receivable"?a) Assetb) Liabilityc) Revenued) Expense答案:a) Asset18. The financial statement that shows the cash inflows and outflows from operating, investing, and financing activities is the:a) Income statementb) Statement of cash flowsc) Balance sheetd) Statement of retained earnings答案:b) Statement of cash flows19. If a company has a current ratio greater than 1, it means that:a) The company has more assets than liabilitiesb) The company has more liabilities than assetsc) The company is profitabled) The company can pay its current liabilities with its current assets答案:d) The company can pay its current liabilities with its current assets20. Which of the following is considered an external user of financial statements?a) Company managementb) Employeesc) Suppliersd) Creditors答案:d) Creditors第二部分:填空题(共10题,每题2分,共20分)1. The periodicity assumption assumes that a company's activities can be divided into ________ periods of equal length.答案:accounting2. The ________ principle states that an entity should recognize revenues when they are earned, regardless of when cash is received.答案:revenue recognition3. The adjusting entry to record the use of supplies during an accounting period would include a ________ to the Supplies Expense account.答案:debit4. The adjusting entry to recognize revenue that has been earned but not yet collected would include a ________ to the Accounts Receivable account.答案:credit5. The ________ principle requires that expenses be reported in the same period as the revenue that is earned as a result of those expenses.答案:matching6. The financial statement that reports the financial position of a company at a specific point in time is the ________.答案:balance sheet7. The accounting equa tion can be expressed as: ________ = Assets − Liabilities.答案:Equity8. The financial statement that shows the changes in equity during the accounting period is the ________.答案:statement of retained earnings9. The adjusting entry to record the portion of prepaid rent that has been used during an accounting period would include a ________ to the Rent Expense account.答案:debit10. The unearned revenue account is a ________ account.答案:liability第三部分:简答题(共4题,每题10分,共40分)1. What is the matching principle in accounting? Why is it important?答案:The matching principle in accounting states that expenses should be recorded and recognized in the accounting period in which they are incurred, regardless of when the cash is paid. This principle is important to ensure that the expenses are properly matched with the revenues that theyhelp generate. By matching expenses with revenues, the financial statements provide a more accurate representation of the company's financial performance during a specific period. This helps users of the financial statements make informed decisions based on reliable financial information.2. Explain the difference between an asset and a liability. Provide an example of each.答案:An asset is a resource owned by a company that has economic value and is expected to provide future benefits. Examples of assets include cash, accounts receivable, inventory, and property, plant, and equipment.A liability, on the other hand, is an obligation or debt owed by a company to external parties. It represents an economic sacrifice that the company is required to make in the future. Examples of liabilities include accounts payable, loans payable, and accrued expenses.3. What is the purpose of the statement of cash flows? How is it prepared?答案:The purpose of the statement of cash flows is to provide information about the cash inflows and outflows from operating, investing, and financing activities during a specific period. It helps users understand how a company generates and uses its cash resources.The statement of cash flows is prepared using the indirect method or the direct method. In the indirect method, the net income from the income statement is adjusted for non-cash items and changes in working capital to arrive at the net cash provided by operating activities. Cash flows from investing and financing activities are directly reported. In the direct method,the actual cash receipts and payments are directly reported in each category of cash flows.4. What is the purpose of the adjusting entries? Provide two examples of adjusting entries and explain their impact on the financial statements.答案:The purpose of adjusting entries is to ensure that the revenues and expenses are properly recognized in the accounting period in which they are incurred, and that the balance sheet accounts reflect the true financial position of the company at the end of the period.Two examples of adjusting entries are:- Accrued expenses: An adjusting entry is made to recognize expenses that have been incurred but not yet paid or recorded. For example, at the end of the accounting period, salaries for the last few days of the period may not have been paid. An adjusting entry is made to recognize the expense for the unpaid salaries, which increases the expenses on the income statement and decreases the retained earnings on the balance sheet.- Prepaid expenses: An adjusting entry is made to recognize expenses that have been paid in advance but have not yet been used. For example, if a company pays rent for the next three months in advance, an adjusting entry is made to allocate a portion of the prepaid rent to the current accounting period. This decreases the prepaid rent on the balance sheet and increases the rent expense on the income statement.。

会计专业英语期末试题及答案

会计专业英语期末试题及答案1、In many cities, a low-carbon lifestyle has become(). [单选题] *A. more popular and more popularB. more and more popular(正确答案)C. the most popularD. most and most popular2、We all wondered()Tom broke up with his girlfriend. [单选题] *A. thatB. whatC. whoD. why(正确答案)3、He went to America last Friday. Alice came to the airport to _______ him _______. [单选题] *A. take; offB. see; off(正确答案)C. send; upD. put; away4、The rain is very heavy _______ we have to stay at home. [单选题] *A. butB. becauseC. so(正确答案)D. and5、______! It’s not the end of the world. Let’s try it again.()[单选题] *A. Put upB. Set upC. Cheer up(正确答案)D. Pick up6、--_______ do you have to do after school?--Do my homework, of course. [单选题] *A. What(正确答案)B. WhenC. WhereD. How7、39.—What do you ________ my new dress?—Very beautiful. [单选题] * A.look atB.think aboutC.think of(正确答案)D.look through8、They may not be very exciting, but you can expect ______ a lot from them.()[单选题] *A. to learn(正确答案)B. learnC. learningD. learned9、The hall in our school is _____ to hold 500 people. [单选题] *A. big enough(正确答案)B. enough bigC. very smallD. very big10、What do you think of the idea that _____ honest man who married and brought up a large family did more service than he who continued single and only talked of _____ population. [单选题] *A. a, /B. an, /C. a, theD. an, the(正确答案)11、20.Jerry is hard-working. It’s not ______ that he can pass the exam easily. [单选题] * A.surpriseB.surprising (正确答案)C.surprisedD.surprises12、You wouldn't have seen her if it _____ not been for him . [单选题] *A. hasB. had(正确答案)C. haveD.is having13、My home is about _______ away from the school. [单选题] *A. three hundred metreB. three hundreds metresC. three hundred metres(正确答案)D. three hundreds metre14、30.I want to find ______ and make much money. [单选题] *A.worksB.jobC.a job(正确答案)D.a work15、Many people prefer the bowls made of steel to the _____ made of plastic. [单选题] *A. itB. ones(正确答案)C. oneD. them16、The red jacket is _______ than the green one. [单选题] *A. cheapB. cheapestC. cheaper(正确答案)D. more cheap17、Grandfather lives with us. We all _______ him when he gets ill. [单选题] *A. look after(正确答案)B. look atC. look forD. look like18、By the end of this month, all this _____. [单选题] *A. is changedB.will changeC. will have changed(正确答案)D. has changed19、Customers see location as the first factor when_____a decision about buying a house. [单选题] *A.makeB.to makeC.making(正确答案)D.made20、Can I _______ your order now? [单选题] *A. makeB. likeC. giveD. take(正确答案)21、Which animal do you like _______, a cat, a dog or a bird? [单选题] *A. very muchB. best(正确答案)C. betterD. well22、Now people can _______ with their friends far away by e-mail, cellphone or letter. [单选题] *A. keep onB. keep in touch(正确答案)C. keep upD. keep off23、If we want to keep fit, we should try to _______ bad habits. [单选题] *A. keepB. haveC. getD. get rid of(正确答案)24、Her ideas sound right, but _____ I'm not completely sure. [单选题] *A. somehow(正确答案)B. somewhatC. somewhereD. sometime25、The flowers _______ sweet. [单选题] *A. tasteB. smell(正确答案)C. soundD. feel26、( ) You had your birthday party the other day,_________ [单选题] *A. hadn't you?B. had you?C. did you?D. didn't you?(正确答案)27、The work will be finished _______ this month. [单选题] *A. at the endB. in the endC. by the endD. at the end of(正确答案)28、The students _____ outdoors when the visitors arrived. [单选题] *A. were playing(正确答案)B. have playedC. would playD. could play29、Why don’t you _______ the bad habit of smoking. [单选题] *A. apply forB. get rid of(正确答案)C. work asD. graduate from30、pencil - box is beautiful. But ____ is more beautiful than ____. [单选题] *A. Tom's; my; heB. Tom's; mine; his(正确答案)C. Tom's; mine; himD. Tom's; my; his。

会计专业英语试题含答案

注意:请将所有答案手写在答题纸上!Ⅰ. Identify true (T) or false (F) statements (12X1′=12′)F . 1. An income statement is a summary of the revenues and expenses of a business as of a specific date.T 2. Accounting is thought to be the “language of business”because business information is communicated to stakeholders.F 3. If a building is appraised for $90,000, offered for sale at $95,000, and the buyer pays $85,000 cash for it, the buyer would record the building at $90,000.F 4. Cash equivalents are short-term highly liquid investment assets that are readily converted to a known cash amount, and have maturities of one year.F 5. For good internal control over cash, all payments should be made from the petty cash, except for very large payments.T 6. The aging method of determining bad debts expense is based on the knowledge that the longer a receivable is past due, the lower the likelihood of collection.F 7. Land improvements are generally charged to the Land account.T 8. Recording depreciation each period is an application of the matching principle.T 9. The cost of an inventory item includes its invoice cost minus any discount, and plus any added or incidental costs necessary to put it in a place and condition for sale.T 10. A consignor who has goods out on consignment with an agent should include the goods in ending inventory even though they are not in the possession of the consignor.F 11. Whether purchase costs are rising or falling, FIFO always will yield the highest gross profit and net income.T 12. If the perpetual inventory system is used and a physical count disclosed a shortage, the cost of merchandise sold should be debited and the merchandise inventory account credited.Ⅱ. Insert “+” for increase and “-”for decrease in the appropriate columns below, based on double-entry bookkeeping rules (6X2′=12′)Ⅲ. Translate the accounting terms from English to Chinese (No. 1-6) and from Chinese to English (No. 7-10) (10X2′=20′)1. General journal (总分类账)2. Accounting elements (会计要素)3. Closing entries(结账分录)4. CICPA(中国注册会计师协会)5. Net realizable value(可变现净值)6. Accrual-basis accounting (应计制会计)7. 非流动负债(non-current liabilities)8. 历史成本(Historical cost)9. 分类账(ledger)10. 经营周期(Operating cycle)Ⅳ. Short answer questions (3X6′=18′)1.What is accounting?Accounting may be described as the process of identifying, measuring, recording,and communicating economic information to permit informed judgments anddecisions by users of that information2.What is depreciation of plant assets? What is the basic purpose of depreciation?Depreciation, as the term is used in accounting, is the allocation of the cost of atangible plant asset to expense in the periods in which services are received from theasset. In short, the basic purpose of depreciation is to achieve the matching principlethat is, to offset the revenue of an accounting period with the costs of the goodsand services being consumed in the effort to generate that revenue.3.Identify the tools of financial statement analysis.The analysis of financial data employs various techniques to emphasize thecomparative and relative significance of the data presented and to evaluate theposition of the firm. Three commonly used tools are as following.Horizontal analysisevaluates a series of financial statement data over a periodof time.Verticalanalysis evaluates financial statement data by expressing each item in afinancial statement as a percent of a base amount.Ratio analysisexpresses the relationship among selected items of financialstatement data.Ⅴ. Problem Solving (38′)1. Analyze the effects of business transactions on the Accounting Equation. (2X5′=10′)Transaction (1): paid a $6,500 premium on July 1 for one year’s insurance in advance.Transaction (2): bought office equipment from Brown Company on account $2,800.2. Prepare journal entries for the two transactions in No. 1 above-mentioned. (2X5′=10′)3. Samuel Co. Ltd issued a $15,000, 6%, 9-month note payable. How much is the interest payment at maturity?(Calculating process is required) (6′)4. Assume the financial position data of Sue Company consist of the following items: (2X6′=12′)Sue CompanyBalance Sheet (Partial)January 31, 2011Required: Calculate its current ratio and acid-test ratio. Calculating steps are needed.。

《会计专业英语》期末测试卷及答案2套

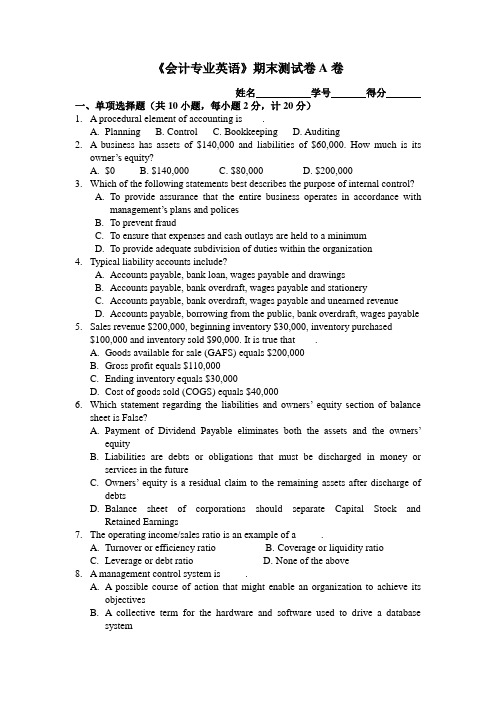

《会计专业英语》期末测试卷A卷姓名学号得分一、单项选择题(共10小题,每小题2分,计20分)1. A procedural element of accounting is____.A.PlanningB. ControlC. BookkeepingD. Auditing2. A business has assets of $140,000 and liabilities of $60,000. How much is itsowner’s equit y?A.$0B. $140,000C. $80,000D. $200,0003.Which of the following statements best describes the purpose of internal control?A.To provide assurance that the entire business operates in accordance withmanagement’s plans and policesB.To prevent fraudC.To ensure that expenses and cash outlays are held to a minimumD.To provide adequate subdivision of duties within the organization4.Typical liability accounts include?A.Accounts payable, bank loan, wages payable and drawingsB.Accounts payable, bank overdraft, wages payable and stationeryC.Accounts payable, bank overdraft, wages payable and unearned revenueD.Accounts payable, borrowing from the public, bank overdraft, wages payable5.Sales revenue $200,000, beginning inventory $30,000, inventory purchased$100,000 and inventory sold $90,000. It is true that____.A.Goods available for sale (GAFS) equals $200,000B.Gross profit equals $110,000C.Ending inventory equals $30,000D.Cost of goods sold (COGS) equals $40,0006.W hich statement regarding the liabilities and owners’ equity section of balancesheet is False?A.Payment of Dividend Payable eliminates both the assets and the owners’equityB.Liabilities are debts or obligations that must be discharged in money orservices in the futureC.Owners’ equity is a residual claim to the remaining assets after discharge ofdebtsD.Balance sheet of corporations should separate Capital Stock andRetained Earnings7.The operating income/sales ratio is an example of a_____.A.Turnover or efficiency ratioB. Coverage or liquidity ratioC.Leverage or debt ratioD. None of the above8. A management control system is_____.A.A possible course of action that might enable an organization to achieve itsobjectivesB. A collective term for the hardware and software used to drive a databasesystemC. A set up that measures and corrects the performance of activities ofsubordinates in order to make sure that the objectives of an organization are being met and their associated plans arebeing carried outD.A system that controls and maximizes the profits of an organizationpany A manufactures and sells only one product, the selling price per unit ofproducts is $20, and the variable cost per unit is $15, the total fixed cost for the year is $80,000. Then the break-even sales for Company A is_____.A. $400,000B.16, 000C.320, 000D. $240,00010.The total estimate sales for the coming year is 250,000 units. The estimatedinventory at the beginning of the year is 22,500 units, and the desired inventory at the end of the year is 30,000 units. The total production indicated in the production budget is_____.A. 242,500 unitsB. 280,000 unitsC. 257,000 unitsD. 302,500 units二、多项选择题(共5小题,每小题4分,计20分)1.Which of the following are fixed costs?A.Telephone billB.Annual salary of the chief accountantC.The management accountant's annual membership fee to ACCA (paid by thecompany)D.Wages of warehousemen2.For commercial bank, which two parts does the operating revenue mainlyinclude?A.Asset RevenueB. Rental RevenueC. Service RevenueD. Bond Revenue3.Which of these are the audit objectives?A.ValidityB. CompletenessC. TimingD. Valuation4.Which of the following statements regarding materiality and misstatements iscorrect?A.Materiality decisions are made relative to the size of the organization beingaudited.B. A lower materiality level would increase the extent of audit proceduresperformed.C.At the planning stage, the auditor should design specific procedures to detectmaterial qualitative misstatements.D.Likely aggregate misstatements include the net effect of uncorrectedmisstatements in opening equity.5.The audit report should include the following basic contents_____.A. The titleB. The introductory paragraphC. The scope paragraphD. The opinion paragraph三、判断题(正确写“T”,错误写“F”。

会计英语期末试题及答案

会计英语期末试题及答案一、选择题1. Which of the following statements best describes the purpose of financial accounting?a) Providing information for internal decision making.b) Reporting financial information to external parties.c) Assisting in tax planning and preparation.d) Analyzing operational performance.2. What is the primary goal of financial reporting?a) Providing relevant and reliable information.b) Minimizing taxes and maximizing profits.c) Meeting government regulations.d) Facilitating internal control.3. Which of the following is an example of an external user of financial information?a) Chief Financial Officer (CFO).b) Production Manager.c) Shareholders.d) Human Resources Manager.4. The accounting equation can be stated as:a) Assets = Liabilities + Equity.b) Equity = Assets - Liabilities.c) Liabilities = Assets - Equity.d) Assets = Equity - Liabilities.5. What is the purpose of the income statement?a) To report the company's financial position at a specific point in time.b) To disclose changes in the company's equity during a period of time.c) To report the company's revenues, expenses, and net income for a period of time.d) To provide information about the company's cash flows.二、填空题1. A company's assets are equal to its _______________ minus its liabilities.2. The _______________ principle states that expenses should be recorded in the same accounting period as the revenues they help to generate.3. The financial statements include the _______________, the balance sheet, the statement of cash flows, and the statement of stockholders' equity.4. _______________ involves analyzing and interpreting financial information to make informed business decisions.5. The _______________ is a financial ratio that measures a company's ability to pay its short-term debts.三、解答题1. Explain the difference between accrual accounting and cash accounting.2. Discuss the importance of the balance sheet in financial reporting.3. Describe the purpose and content of the statement of cash flows.4. What is the role of the Generally Accepted Accounting Principles (GAAP) in financial reporting?5. Explain the concept of depreciation and how it is recorded in the financial statements.答案:一、选择题1. b) Reporting financial information to external parties.2. a) Providing relevant and reliable information.3. c) Shareholders.4. a) Assets = Liabilities + Equity.5. c) To report the company's revenues, expenses, and net income for a period of time.二、填空题1. Equity2. Matching3. Income statement4. Financial analysis5. Current ratio三、解答题1. Accrual accounting recognizes revenue and expenses when they are earned or incurred, regardless of when the associated cash flows occur. Cash accounting, on the other hand, records revenue and expenses only when cash is received or paid out. Accrual accounting provides a more accurate picture of a company's financial health and performance.2. The balance sheet is a financial statement that provides a snapshot of a company's financial position at a specific point in time. It shows the company's assets, liabilities, and equity. The balance sheet is important for investors, creditors, and other stakeholders to assess the company's liquidity, solvency, and overall financial stability.3. The statement of cash flows reports the cash inflows and outflows from a company's operating activities, investing activities, and financing activities. Its purpose is to provide information about the cash generated and used by the company during a specific period of time. It helps users understand the company's cash flow patterns and assess its ability to generate cash for future operations and investments.4. Generally Accepted Accounting Principles (GAAP) are a set of accounting standards and guidelines that companies must follow when preparing their financial statements. GAAP ensures consistency, comparability, and transparency in financial reporting, allowing users of financial statements to make meaningful and informed decisions. It helps maintain public trust in the financial reporting process.5. Depreciation is the systematic allocation of the cost of a long-term asset over its useful life. It reflects the wearing out, consumption, or expiration of the asset's value over time. Depreciation is recorded as an expense on the income statement and as an accumulated depreciation contra-asset on the balance sheet. It helps match the cost of the asset with the revenue it helps to generate, providing a more accurate reflection of the company's profitability.。

会计专业英语 A卷-参考

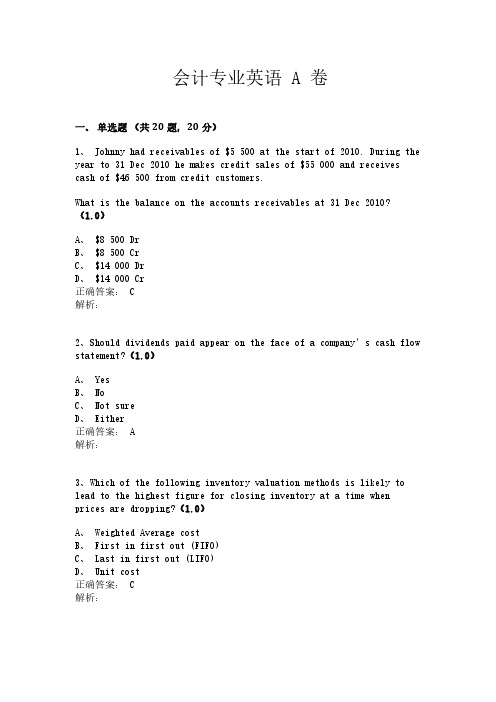

一、单选题(共20题,20分会计专业英语A 卷)1、Johnny had receivables of $5500at the start of 2010.During the year to 31Dec 2010he makes credit sales of $55000and receives cash of $46500from credit customers.What is the balance on the accounts receivables at 31Dec 2010?(1.0)A、$8500DrB、$8500CrC、$14000DrD、$14000Cr正确答案:C解析:2、Should dividends paid appear on the face of a company’s cash flow statement?(1.0)A、YesB、NoC、Not sureD、Either正确答案:A解析:3、Which of the following inventory valuation methods is likely to lead to the highest figure for closing inventory at a time when prices are dropping?(1.0)A、Weighted Average costB、First in first out (FIFO)C、Last in first out (LIFO)D、Unit cost正确答案:C解析:4、Which of following items may appear as non-current assets in a company’s the statement of financial position?(1)plant,equipment,and property(2)company car(3)€4000cash(4)€1000cheque(1.0)A、(1),(3)B、(1),(2)C、(2),(3)D、(2),(4)正确答案:B解析:5、Which of the following items may appear as current liabilities ina company’s balance sheet?(1)investment in subsidiary(2)Loan matured within one year.(3)income tax accrued untill year end.(4)Preference dividend accrued(1.0)A、(2),(3)and(4)B、(1),(3)and(4)C、(1),(2)and(4)D、(1),(2)and(3)正确答案:A解析:7、Beta purchased some plant and equipment on01/07/2010for$60,000. The estimated residual value of the plant in10years time is estimated to be$6,000.Beta’s policy is to charge depreciation on the straight line basis,with a proportionate charge in the period of acquisition.What should the depreciation charge for the plant be in Beta’s accounting period of18months to30/09/2010?(1.0)A、$5400B、$900C、$675D、$1350正确答案:B解析:8、A company’s income statement for the year ended31December2005 showed a net profit of$83,600.It was later found that$18,000paid for the purchase of a motor van had been debited to the motor expenses account.It is the company’s policy to depreciate motor vans at25per cent per year on the straight line basis,with a full year’s charge in the year of acquisition.What would the net profit be after adjusting for this error?(1.0)A、$97,100B、$70,100C、$106,100D、$101,600正确答案:A解析:9、Which of the following statements are correct?(1)to be prudent,company charge depreciation annually on the fixed asset(2)substance over form means that the commercial effect of a transaction must always be shown in the financial statements even if this differs from legal form(3)in order to achieve the comparable,items should be treated in the same way year on year(1.0)A、2and3onlyB、All of themC、1and2onlyD、3only正确答案:B解析:10、In preparing a company’s cash flow statement,which,if any,of the following items could form part of the calculation of cash flow from financing activities?(1)Proceeds of sale of premises(2)Dividends received(3)Issue of shares(1.0)A、1onlyB、2onlyC、3onlyD、None of them.正确答案:D解析:11、To understand and use accounting information in making economic decisions,you must understand:(1.0)A、Language of business.B、Is an end rather than a means to an end.C、Useful for decision making.D、Used by business,government,nonprofit organizations,and individuals.正确答案:B解析:13、External users of financial accounting information include all of the following except:(1.0)A、Investors.B、Labor unions.C、Line managers.D、General public.正确答案:C解析:14、Objectives of financial reporting to external investors and creditors include preparing information about all of the following except:(1.0)A、Information used to determine which products to produce.B、Information about economic resources,claims to those resources, and changes in both resources and claims.C、Information that is useful in assessing the amount,timing,and uncertainty of future cash flows.D、Information that is useful in making investment and credit decisions.正确答案:A解析:15、Which of the following are important factors in ensuring the integrity of accounting information?(1.0)A、Institutional factors,such as standards for preparing information.B、Professional organizations,such as the American Institute of CPAs.C、Competence,judgment,and ethical behavior of individual accountants.D、All of the above.正确答案:D解析:17、Listed below are some characteristics of financial information.(1)True(2)Prudence(3)Completeness(4)CorrectWhich of these characteristics contribute to reliability?(1.0)A、(1),(3)and(4)onlyB、(1),(2)and(4)onlyC、(1),(2)and(3)onlyD、(2),(3)and(4)only正确答案:A解析:18、In preparing its financial statements for the current year,a company’s closing inventory was understated by$300,000.What will be the effect of this error if it remains uncorrected?(1.0)A、The current year’s profit will be overstated and next year’s profit will be understatedB、The current year’s profit will be understated but there will be no effect on next year’s profitC、The current year’s profit will be understated and next year’s profit will be overstatedD、The current year’s profit will be overstated but there will be no effect on next year’s profit.正确答案:C解析:20、In times of inflation In times of rising prices,what effect does the use of the historical cost concept have on a company’s asset values and profit?(1.0)A、Asset values and profit both undervaluedB、Asset values and profit both overvaluedC、Asset values undervalued and profit overvaluedD、Asset values overvalued and profit undervalued正确答案:C解析:二、判断题(共10题,10分)2、An income statement is a summary of the revenues and expenses of a business as of a specific date.(1.0)正确答案:错误解析:3、If a building is appraised for$90,000,offered for sale at$95,000,and the buyer pays$85,000cash for it,the buyer would record the building at$90,000.(1.0)正确答案:错误解析:4、Cash equivalents are short-term highly liquid investment assets that are readily converted to a known cash amount,and have maturities of one year.(1.0)正确答案:错误解析:5、For good internal control over cash,all payments should be made from the petty cash,except for very large payments.(1.0)正确答案:错误解析:7、Land improvements are generally charged to the Land account.(1.0)正确答案:错误解析:8、Recording depreciation each period is an application of the matching principle.(1.0)正确答案:正确解析:9、The cost of an inventory item includes its invoice cost minus any discount,and plus any added or incidental costs necessary to put it in a place and condition for sale.(1.0)正确答案:正确解析:三、论述题(共2题,30分)1、J.Linda began a public accounting practice and completed these transactions during November of the current year:1Paid the premium on two insurance policies,$375.2Completed accounting work for Jack Hall and collected $15cash therefore.3Completed accounting work for Sun Bank on credit,$350.4Purchase additional office supplies on credit,$25.5Received $350from Sun Bank for the work completed on November 13.(10.0)正确答案:第1空:1Prepaid Insurance375Cash3752Cash 15Accounting Revenue 153Accounts Receivble 350Accounting Revenue 3504Office Supplies 25Accounts Payable 255Cash 350Accounts Receivable350解析:Most accounting methods are based on the assumption that thebusiness enterprise Will have a long life.Experience indicates that,in spite of numerous business failures ,companies have a fairly hig 2、what is Going Concern Assumption(20.0)正确答案:hcontinuance rate.Although accountants do not believe that business firms will last ,they do expect them to last long enough to fufill their objetives and commit-ments.A balance sheet is prepared under the assumption that the concern for which the Statement is made will continue ,so far "a going concern the assets used in carrying its operations are not for sale.Their current market values usually can not be established as is required bythe "objectivity principle解析:1、Research and development (R&D 四、阅读理解(共1题,40分))Accounting treatment of R&DUnder International Accounting Standards the accounting for R&D is dealt with under IAS 38,Intangible Assets.IAS 38states that an intangible asset is to be recognised if,and only if,the following criteria are met:it is probable that future economic benefits from the asset will flow to the entity,the cost of the asset can be reliably measured.The above recognition criteria look straightforward enough,but in reality it can prove to be very difficult to assess whether or not these have been met.In order to make this recognition of intangibles more clear,IAS 38separates an R&D project into a research phase and a development phase.Research phaseIt is impossible to demonstrate whether or not a product or service at the research stage will generate any probable future economic benefit.As a result,IAS 38states that all expenditure incurred at the research stage should be written off to the statement ofcomprehensive income as an expense when incurred,and will never be capitalised as an intangible asset.Development phaseUnder IAS38,an intangible asset arising from development must be capitalised if an entity can demonstrate all of the following criteria:the technical feasibility of completing the intangible asset(so that it will be available for use or sale);intention to complete and use or sell the asset;ability to use or sell the asset; existence of a market or,if to be used internally,the usefulness of the asset;availability of adequate technical,financial,and other resources to complete the asset;the cost of the asset can be measured reliably.If any of the recognition criteria are not met then the expenditure must be charged to the income statement as incurred.Note that if the recognition criteria have been met, capitalisation must take place.Once development costs have been capitalised,the asset should be amortised in accordance with the accruals concept over its finite life.Amortisation must only begin when commercial production has commenced.(40.0)(1)、[简答题](10分)Outline the criterias of recognition of intangible assets正确答案:IAS38states that an intangible asset is to be recognised if,and only if,the following criteria are met:it is probable that future economic benefits from the asset will flow to the entity.(2)、[简答题](10分)Criterias to recognised as development正确答案:the technical feasibility of completing the intangible asset(so that it will be available for use or sale);intention to complete and use or sell the asset;ability to use or sell the asset;existence of a market or,if to be used internally,the usefulness of the asset.(3)、[简答题](10分)Identify the accounting treatment of research phase正确答案:IAS38states that all expenditure incurred at the research stage should be written off to the statement of comprehensive income as an expense when incurred,and will never be capitalised as an intangible asset.(4)、[简答题](10分)Identify the accounting treatment of development phase正确答案:intangible asset arising from development must be capitalised Once development costs have been capitalised,the asset should be amortised in accordance with the accruals concept over its finite life.解析:。

最新会计专业英语期末考试试卷和答案