Optimal Investment in Derivative Securities

Optimal Positioning in Derivative Securities

Peter Carr Morgan Stanley 1585 Broadway, 6th Floor New York, NY 10036 (212) 761-7340 carrp@ Dilip Madan College of Business & Management University of Maryland College Park, MD 20742 (301) 405-2127 dbm@

1 For example, three recent comprehensive texts on asset allocation are Gibson 17], Vince 38], or Leibowitz et. al. 27], none of which cover derivatives. 2 See Evnine and Hendriksson 15] and Tilley and Latainer 37] for discussions on the use of options in an asset allocation framework.

Abstract

1

Optimal Positioning in Derivative Securities

1 Introduction

The portfolio selection problem pioneered by Merton 28] generally does not consider derivative securities as potential investment vehicles. Similarly, the asset allocation approach favored by practitioners does not1 consider derivatives as a distinct asset class. If derivatives (forwards, futures, swaps, options, and exotics) are considered at all, they are only viewed as tactical2 vehicles for e ciently re-allocating funds across broad asset classes, such as cash, xed-income, equity, and alternative investments. Thus, the question of how investors should optimally position themselves in derivatives has been largely left unanswered by both the academic and practitioner communities. The absence of a coherent framework for determining optimal derivatives positioning is likely due to the complexity of the problem and to the overwhelming success of the arbitrage-based models for pricing derivatives. Since these models are dynamically complete in the underlying assets, derivatives are redundant securities. In these models, the optimal position in derivatives is either indeterminate or in nite, depending on whether an investor agrees or disagrees with the derivative's market price. Clearly, these models are unsuited for the development of a normative theory, which is capable of providing guidance both for investors contemplating various investment alternatives, and for regulators assessing the e cacy of derivatives markets. The purpose of this paper is to delineate conditions under which investors nd it optimal to add derivatives to their portfolio mix. A second purpose is to nd the optimal position in both primary and secondary assets. We show that under reasonable market conditions, derivatives are not redundant, but instead comprise a separate asset class, imperfectly correlated with other broad asset classes. Under this view, the introduction of derivatives enhances the investment possibility frontier. In fact, this paper extends a line of investigation initiated by Ross 32] in which derivatives complete the market. Working in a single period setting, we show how investors can determine

格雷厄姆价值投资选股公式

格雷厄姆价值投资选股公式摘要:1.格雷厄姆简介2.价值投资理念3.格雷厄姆价值投资选股公式4.公式的应用和意义5.总结正文:1.格雷厄姆简介本杰明·格雷厄姆(Benjamin Graham)是一位著名的美国投资大师,被誉为“华尔街教父”。

他生于1894 年,逝世于1976 年。

格雷厄姆是价值投资的奠基人,他的投资理念在投资界产生了深远的影响。

他的经典之作《证券分析》和《聪明的投资者》为投资者提供了宝贵的投资经验和智慧。

2.价值投资理念价值投资是一种长期投资策略,旨在寻找市场上被低估的优质股票。

价值投资者相信,通过买入低估值的股票并长期持有,可以在市场回归合理估值时获得超额收益。

价值投资的核心理念是“安全边际”,即在购买股票时,要确保购买价格低于其内在价值,以降低投资风险。

3.格雷厄姆价值投资选股公式格雷厄姆提出了一个著名的选股公式,该公式可以帮助投资者筛选出具有投资价值的股票。

公式如下:价值= (EBITDA * 8.5 + 净资产* 2)/ 股票总数其中,EBITDA 表示息税前利润加折旧摊销;净资产表示公司的账面价值;股票总数表示公司发行的股票总数。

4.公式的应用和意义该公式的应用主要体现在以下几个方面:(1)评估公司的内在价值:通过计算价值,投资者可以了解公司的内在价值,从而判断股票是否被低估或高估。

(2)筛选优质股票:投资者可以使用该公式对多个股票进行评估,从而筛选出具有投资价值的优质股票。

(3)风险控制:该公式可以帮助投资者判断购买股票的价格是否合理,从而降低投资风险。

5.总结格雷厄姆的价值投资选股公式为投资者提供了一种评估股票价值的有效方法。

通过应用该公式,投资者可以更好地筛选优质股票,实现长期稳定的投资收益。

格雷厄姆价值投资选股公式

格雷厄姆价值投资选股公式摘要:1.价值投资的概念2.格雷厄姆的选股公式3.公式中的各个指标解释4.如何运用格雷厄姆价值投资选股公式进行选股5.实际案例分析6.总结正文:价值投资是一种长期投资策略,其核心理念是寻找那些被市场低估的优质股票。

这种投资策略的创始人之一是美国著名投资大师本杰明·格雷厄姆。

他提出了一套著名的选股公式,用以帮助投资者筛选出具有投资价值的股票。

格雷厄姆价值投资选股公式如下:市盈率(PE)< 15市净率(PB)< 1.5股息率(Dividend Yield)> 2%接下来我们将详细解释公式中的各个指标:1.市盈率(PE):市盈率是指股价与每股收益的比例。

它反映了投资者愿意为每单位净利润支付的价格。

通常,市盈率越低,投资者购买每股收益所需支付的价格越低,表示股票相对便宜。

格雷厄姆认为,市盈率应低于15 倍,以保证投资者购买到被低估的股票。

2.市净率(PB):市净率是指股价与每股净资产的比例。

它反映了投资者愿意为每单位净资产支付的价格。

通常,市净率越低,投资者购买每股净资产所需支付的价格越低,表示股票相对便宜。

格雷厄姆认为,市净率应低于1.5 倍,以保证投资者购买到被低估的股票。

3.股息率(Dividend Yield):股息率是指股息与股票价格的比例。

它反映了投资者持有股票每年可获得的现金分红。

通常,股息率越高,投资者持有的股票每年可获得的现金分红越多。

格雷厄姆认为,股息率应高于2%,以保证投资者在长期投资中获得稳定的收益。

运用格雷厄姆价值投资选股公式进行选股时,投资者需将上述三个指标同时满足。

通过筛选出满足条件的股票,投资者可以进一步对这些股票进行研究和分析,找出具有长期投资价值的股票。

以下是一个实际案例分析:某公司股票,当前市盈率为12 倍,市净率为1.2 倍,股息率为3%。

根据格雷厄姆价值投资选股公式,该股票满足所有条件,可以认为具有投资价值。

投资者可以进一步分析公司的基本面、行业前景等因素,决定是否进行投资。

法律意见书英文

法律意见书英文【篇一:英文法律意见书】haoway investments limited uegisteredsenior secured debt securities关于豪威投资有限公司未登记优先担保债券的attorney’s opinions法律意见书chongqing, p. r. chinamarch 17, 2007二零零七年三月十七日re: haoway investments limited uegistered senior secured debt securities关于豪威投资有限公司未登记优先担保债券的attorney opinion letter法律意见书dated on march 17, 2007二oo七年三月十七日gentleman or madam,敬启者:investment limited (haoway) and chongqing gaoshan real estate development co. ltd. (gaoshan) (our clients), deliver our opinion as follows:according to (a) the european parliament?s purvis report; (b) the post-fsap report on asset management; (c) cesr?s mandate for the asset management experts group; (d) the iosco report on “issues arising from the participation of retail investors in hedge funds” (e) article 2 of directive 2001/108/ec (amending the ucits [undertakings for collective investment in transferable securities” or “ucits investment fund”] directive 85/611 oninvestments), we delivered these opinions based on the accepted professional standards and regulations and on the principles of due diligence:根据(a) 欧洲议会的《purvis报告》,(b) 《关于资产管理的后fsap报告》,(c) 欧洲证券管理委员会对于资产管理专家小组的强制要求,(d) 国际证监会组织关于“零散投资人参与对冲基金有关问题”的报告,(e) 欧盟第2001/108/ec号指令第2条(关于修订ucits [可转让证券集合投资事业,也称证券投资基金]投资的第85/611号指令等有关法律法规的规定,本所按照律师行业公认的业务标准、道德规范和勤勉尽责的精神出具本法律意见书。

财务管理英文题库及答案

财务管理英文题库及答案1. Question: What is the primary goal of financial management in a business?Answer: The primary goal of financial management in a business is to maximize the value of the firm to its shareholders by making optimal investment and financing decisions.2. Question: What is the difference between a current asset and a non-current asset?Answer: A current asset is an asset that is expected to be converted to cash or used up within one year or one operating cycle of the business. A non-current asset, on the other hand, is an asset that is not expected to be converted to cash or used up within one year or one operating cycle.3. Question: Explain the concept of Time Value of Money (TVM).Answer: The Time Value of Money (TVM) is a financial concept that states that a sum of money received today isworth more than the same sum received in the future due toits potential earning capacity. This principle is fundamental to finance and is used to evaluate the relative worth of money at different points in time.4. Question: What is the formula for calculating the presentvalue of a future sum of money?Answer: The formula for calculating the present value (PV) of a future sum of money (FV) is: PV = FV / (1 + r)^n, where r is the discount rate and n is the number of periods.5. Question: Define the term 'Leverage' in the context of financial management.Answer: Leverage in financial management refers to the use of borrowed funds to increase the potential return of an investment. It is a strategy that can amplify gains but also increases the risk of losses if the investment does not perform as expected.6. Question: What is the DuPont Identity and how is it usedin financial analysis?Answer: The DuPont Identity is a formula used to break down the return on equity (ROE) into three parts: net profit margin, asset turnover, and financial leverage. It is used in financial analysis to understand the drivers of a company's profitability and to compare it with other companies.7. Question: How does inflation affect a company's financial statements?Answer: Inflation affects a company's financial statements by reducing the purchasing power of money. It can lead to higher costs for raw materials and labor, which can decrease profit margins. Additionally, inflation can cause assets andliabilities to be understated, and it may affect the real value of reported earnings.8. Question: Explain the concept of Capital Budgeting and its importance.Answer: Capital Budgeting is the process of evaluating the profitability of long-term investments or projects. It is important because it helps a company decide which projects to undertake based on their potential to generate returns over time, considering the time value of money and the risks involved.9. Question: What is the difference between a fixed cost anda variable cost?Answer: A fixed cost is a cost that does not change with the level of production or sales, such as rent or salaries. A variable cost, however, changes in direct proportion to the level of production or sales, such as raw materials or direct labor costs.10. Question: Define the term 'Liquidity Ratios' and provide examples.Answer: Liquidity Ratios are financial metrics used to measure a company's ability to pay off its short-term debts. Examples include the Current Ratio (current assets divided by current liabilities) and the Quick Ratio (current assets minus inventory divided by current liabilities). These ratios help assess the liquidity position of a business.。

安盛隽宇投资保险计划

2013年9月

本概要提供本產品的重要資料,是銷售說明書的一部份。 請勿單憑本概要作出投保決定。 本產品資料概要最後一頁附有 「詞彙」 部份。 請參閱 「詞彙」 部份,以查閱以斜體顯示的詞彙之解釋。

資料便覽

保險公司名稱: • 安盛保險 (百慕達) 有限公司 一筆過投資或定期保費供款: • 定期保費 定期保費繳費模式: • 每月/每半年/每年 最短供款年期: • 5至30年,由保單持有人於保單簽發時決定 ( 「目標供款年期」 ) 徵收退保費(提早贖回費)年期: • 您所選擇的目標供款年期內 保單貨幣: • 港元/美元/歐羅/英鎊/澳元/新加坡元 最低定期保費(每年度): • 19,200港元/2,400美元/2,400歐羅/ 1,600英鎊/2,880澳元/3,840新加坡元 最高定期保費: • 視乎核保要求的規定 保單的準據法律: • 香港特別行政區法律 身故賠償: 基本身故賠償選項:戶口價值 的101%。 特級身故賠償選項:以下兩項中較高者: (i) 戶口價值 的101%;或 (ii) 已繳付的定期保費總額,再扣除提取部份款項之總額。

5

雋宇投資保險計劃

本產品涉及哪些費用及收費? (續)

有關計劃的收費 收費率 買賣差價 現時豁免收取。惟保留收取不高於買入價之1%的買 賣差價之權利。 扣除方式 反映在投資選擇項的單位價格中

轉換費

現時豁免收取。惟保留日後收取不高於轉出金額1% 的轉換費之權利。

從轉出的金額中扣除

• 適用於目標供款年期完結前 (i) 退保,及 (ii) 終止 保單 (因被保人身故除外) • 提早贖回費為: (i) 百份比(如下所示)乘以 (ii) 最初供款戶口價值 • 該等百分比為: – 於首個保單年度:100% – 自第2個保單年度起,請根據由退保或終止保單 日期 起直至您所選的目 標供款 年期完結時之 年期參照下表: 年期^ 提早贖回費 29 28 27 26 25 24 23 22 21 20 19 18 17 16 提早贖回 費比率 99% 98% 97% 96% 95% 94% 93% 92% 91% 90% 89% 88% 86% 82% 年期^ 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 提早贖回 費比率 78% 74% 70% 65% 60% 56% 52% 49% 45% 40% 32% 26% 20% 14% 8%

基金对冲基金投资词汇_金融银行英语词汇

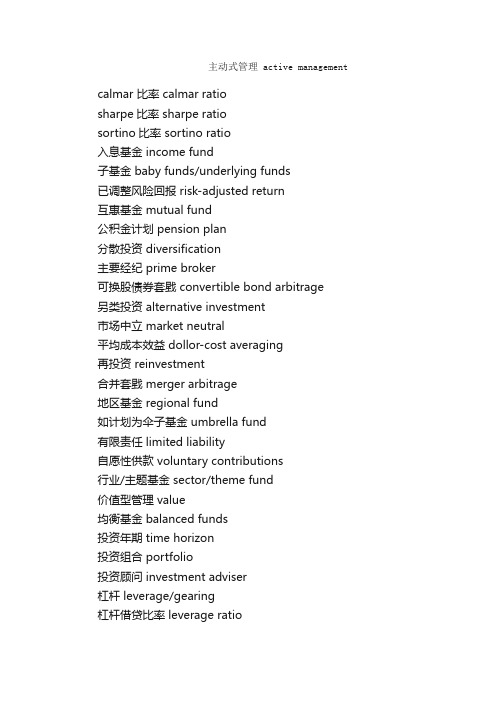

主动式管理 active managementcalmar 比率 calmar ratiosharpe比率 sharpe ratiosortino比率 sortino ratio入息基金 income fund子基金 baby funds/underlying funds已调整风险回报 risk-adjusted return互惠基金 mutual fund公积金计划 pension plan分散投资 diversification主要经纪 prime broker可换股债券套戥 convertible bond arbitrage另类投资 alternative investment市场中立 market neutral平均成本效益 dollor-cost averaging再投资 reinvestment合并套戥 merger arbitrage地区基金 regional fund如计划为伞子基金 umbrella fund有限责任 limited liability自愿性供款 voluntary contributions行业/主题基金 sector/theme fund价值型管理 value均衡基金 balanced funds投资年期 time horizon投资组合 portfolio投资顾问 investment adviser杠杆 leverage/gearing杠杆借贷比率 leverage ratio每日估值 daily valuation每年回报 annual return供款 contribution受压 / 濒临破产的证券 distressed securities定息工具套戥 fixed income arbitrage定息基金 fixed-income fund承受风险能力 risk tolerance注册地 domicile沽空 short selling波幅 volatility股份 share股息分派 dividened distributions股票基金 equity fund表现费 performance fees阿尔法系数 alpha非认可基金 unauthorised fund信托人 trustee保本对冲基金 capital guaranteed hedge funds封闭式基金 closed-end fund界定利益计划 defined benefit plan界定供款计划 defined contribution plan相关系数 correlation重大事件主导的投资 event driven/special situations 首次认购费 front-end fee套戥 arbitrage效率前缘 efficient frontier高收益 high yield基金公会 hkifa基金经理 fund manager基金销售文件 prospectus基准 benchmarks被动式管理 passive management离岸基金 offshore fund最大跌幅 maximum drawdown揣测最佳时机 market timing期货管理型基金 managed futures短仓 /淡仓 short position跌势差 downside deviation雇主供款 employer contribution雇员供款 employee contribution新高价 high-on-high basis新兴市场 emerging markets新兴市场基金 emerging markets fund管理费 managemantfee增长和收入基金 growthand income fund严格评估 due diligence买入价 bid price买卖差价 bid-offer spread传统基金 traditional fund债券基金 bond fund单一对冲基金 single strategy hedge fund 单位 unit单位信托基金 unit trust卖出价 offer price奖励费 incentive fees对冲 hedge对冲基金 hedge fund对冲基金的基金 fund of hedge funds (fohfs) 对冲基金指引 hedge funds guidelines开放式基金 open-end fund强制性供款 mandatory contributions强积金 mandatory provident fund scheme-mpf 总回报 total return标准差 standard deviation毕苏期权定价模式 black-scholes环球宏观 macro funds环球基金 global fund绝对回报 absolute return认可基金 authorised funds认沽期权 put option/put认股权证基金 warrant fund认购期权 call option/call证券借出 stock lending贝他系数 beta资产分配 asset allocation资产净值 netasset value-nav赎回 redemption赎回通知期 redemption notice period赎回费 redemption fee赎回费 / 买入费 redemption price / bid price进取型的投资管理 aggressive growth进取型增长基金 aggressive growth fund长 / 短仓持股 long/short equity长仓 / 好仓 / 持货 long position预设回报率 hurdle rate。

投资组合管理中有效前沿及最优比例计算方法探讨

投资组合管理中有效前沿及最优比例计算方法探讨投资组合管理是投资者在追求最大化收益的同时控制风险的关键任务之一。

有效前沿是一个重要的概念,指的是在给定风险水平下,能够实现最大化投资收益的投资组合集合。

本文将探讨有效前沿的构建方法以及最优比例计算的相关技术。

有效前沿是现代投资组合理论的重要组成部分。

这个概念最早由Markowitz提出,在他的研究中引入了资产的协方差矩阵来度量投资组合的风险和收益。

有效前沿通过评估不同资产配置方案的风险-收益比来确定最佳的投资组合。

投资组合中的每一种配置方案都可以看作是一个点,构成了一个由风险和收益构成的二维曲线。

尽管曲线上的每个点都是有效的投资组合,但只有在曲线上的点才是最有吸引力的选择,因为它们提供了最佳的风险-收益权衡。

有效前沿的构建通常使用优化算法来完成。

常见的方法包括均值-方差模型和Monte Carlo模拟。

均值-方差模型通过最小化投资组合的方差,同时最大化投资组合的收益来确定有效前沿。

这个模型的核心是有效边界,即在给定风险水平下可以实现的最大投资收益。

Monte Carlo模拟则通过随机生成大量的投资组合以覆盖整个投资空间,然后计算每个投资组合的收益和风险,以此来构建有效前沿。

在构建有效前沿之后,投资者需要选择最优的投资组合比例。

最优比例的计算方法可以有多种。

其中,一个常见的方法是最小方差法。

最小方差法通过最小化整个投资组合的方差来确定最优的资产比例。

这个方法在实践中比较简单易用,并且可以通过历史数据来估计资产的协方差矩阵。

另一个方法是马尔科维茨模型,它通过引入风险规避系数来实现收益和风险之间的权衡,从而确定最优比例。

除了以上方法外,还有一些其他的方法可以用来计算最优比例。

例如,基于风险平价的方法可以将不同资产配置的风险权重调整为相等,以实现更平衡的投资组合。

而基于收益平价的方法则将不同资产配置的收益权重调整为相等,以实现更平均的投资收益。

这些方法通常需要根据投资者的特定目标和约束条件来确定最优比例。

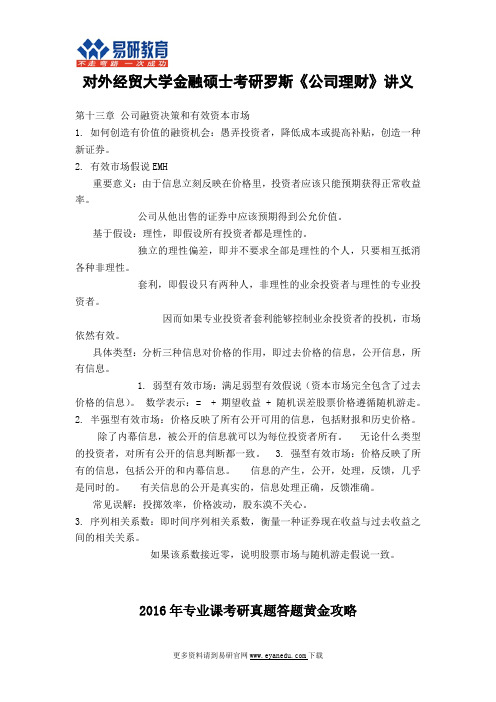

对外经贸大学金融硕士罗斯《公司理财》讲义13

对外经贸大学金融硕士考研罗斯《公司理财》讲义第十三章公司融资决策和有效资本市场1.如何创造有价值的融资机会:愚弄投资者,降低成本或提高补贴,创造一种新证券。

2.有效市场假说EMH重要意义:由于信息立刻反映在价格里,投资者应该只能预期获得正常收益率。

公司从他出售的证券中应该预期得到公允价值。

基于假设:理性,即假设所有投资者都是理性的。

独立的理性偏差,即并不要求全部是理性的个人,只要相互抵消各种非理性。

套利,即假设只有两种人,非理性的业余投资者与理性的专业投资者。

因而如果专业投资者套利能够控制业余投资者的投机,市场依然有效。

具体类型:分析三种信息对价格的作用,即过去价格的信息,公开信息,所有信息。

1.弱型有效市场:满足弱型有效假说(资本市场完全包含了过去价格的信息)。

数学表示:=+期望收益+随机误差股票价格遵循随机游走。

2.半强型有效市场:价格反映了所有公开可用的信息,包括财报和历史价格。

除了内幕信息,被公开的信息就可以为每位投资者所有。

无论什么类型的投资者,对所有公开的信息判断都一致。

3.强型有效市场:价格反映了所有的信息,包括公开的和内幕信息。

信息的产生,公开,处理,反馈,几乎是同时的。

有关信息的公开是真实的,信息处理正确,反馈准确。

常见误解:投掷效率,价格波动,股东漠不关心。

3.序列相关系数:即时间序列相关系数,衡量一种证券现在收益与过去收益之间的相关关系。

如果该系数接近零,说明股票市场与随机游走假说一致。

2016年专业课考研真题答题黄金攻略名师点评:认为只要专业课重点背会了,就能拿高分,是广大考生普遍存在的误区。

而学会答题方法才是专业课取得高分的关键。

下面易研老师以经常考察的名词解释、简答题、论述题、案例分析为例,来讲解标准的答题思路。

(一)名词解析答题方法【考研名师答题方法点拨】名词解释最简单,最容易得分。

在复习的时候要把参考书中的核心概念和重点概念夯实。

近5-10年的真题是复习名词解释的必备资料,通过研磨真题你可以知道哪些名词是出题老师经常考察的,并且每年很多高校的名词解释还有一定的重复。

证券投资学5证券投资组合理论

布的良好效果,请言简意赅地阐述您的观点。

三项资产组合的效率前沿 方差为:

ABCE(aRAbRBCRC) 0.334.6%+0.338.60%+0.3416%

=9.765%

若

将

,相关系数

Var(aRA bRB CRC)

的资产C引入组合 AB中,

0.332 0.05622+0.332 0.06332+0.342 0.0752

有无风险资产组合的效率前沿

(一)无风险资产的定义

第二节 证券资产组合的效率前沿

(二)允许无风险资产下的投资组合

一.投资于一种无风险资产和一种风险资产的情形

为了考察无风险贷款对有效集的影响,我们首先要分析由一种无风险资产和一种风险资产组 成的投资组合的预期收益率和风险。

假设风险资产和无风险资产在投资组合中的比例分别为X1和X2,它们的预期收益率分别

1

p

这样,我们可以算出该组合的预期收益率为: 我们可以算出改组合的标准差为: 由上式可得: 代入一式

第二节 证券资产组合的效率前沿

在图中,A点表示无风险资产,B点

表示风险资产,由这两种资产构成的投资组

合的预期收益率和风险一定落在A、B这个

RP

线段上,因此AB连线可以称为资产配置线。 B

由于A、B线段上的组合均是可行的,

率最高。

E(R)

C

比如,相对于区域中的L点,组合N与他的

F

期望收益率相同,但风险却低得多,组合F与L的风

NL

险大小相同,但期望收益率相同。

E

B

A

因此,现在投资者只会在NF之间选择,不

σ

必估计到L的存在

第二节 证 券资产组合 的效率前沿

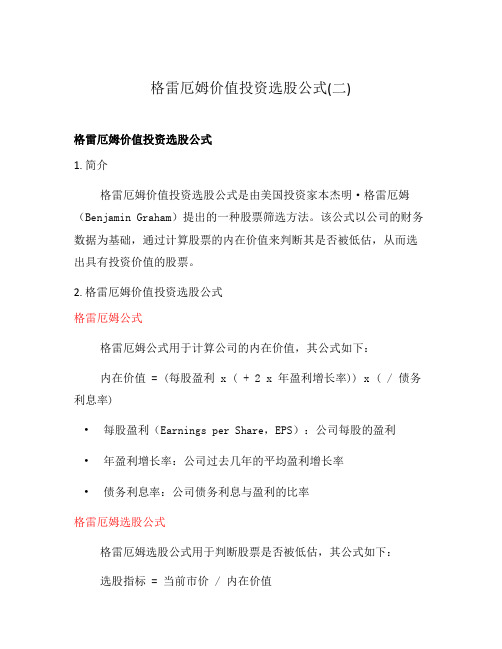

格雷厄姆价值投资选股公式(二)

格雷厄姆价值投资选股公式(二)格雷厄姆价值投资选股公式1. 简介格雷厄姆价值投资选股公式是由美国投资家本杰明·格雷厄姆(Benjamin Graham)提出的一种股票筛选方法。

该公式以公司的财务数据为基础,通过计算股票的内在价值来判断其是否被低估,从而选出具有投资价值的股票。

2. 格雷厄姆价值投资选股公式格雷厄姆公式格雷厄姆公式用于计算公司的内在价值,其公式如下:内在价值 = (每股盈利 x ( + 2 x 年盈利增长率)) x ( / 债务利息率)•每股盈利(Earnings per Share,EPS):公司每股的盈利•年盈利增长率:公司过去几年的平均盈利增长率•债务利息率:公司债务利息与盈利的比率格雷厄姆选股公式格雷厄姆选股公式用于判断股票是否被低估,其公式如下:选股指标 = 当前市价 / 内在价值根据格雷厄姆的理论,如果选股指标小于1,则认为该股票被低估,具有投资价值。

3. 举例说明假设某公司每股盈利为3元,年盈利增长率为6%,债务利息率为5%。

根据格雷厄姆公式计算,该公司的内在价值为:内在价值 = (3 x ( + 2 x 6%)) x ( / 5%) = 元假设该公司的当前市价为40元,根据格雷厄姆选股公式计算,该公司的选股指标为:选股指标 = 40 / =由于选股指标小于1,根据格雷厄姆的理论,可以认为该股票被低估,具有投资价值。

4. 总结格雷厄姆价值投资选股公式是一种基于财务数据计算股票内在价值的方法,通过对比股票当前市价和内在价值的比例来判断其是否被低估。

投资者可以使用该公式进行股票筛选,从而选择具有投资价值的股票。

但需要注意,该公式只是一种参考方法,投资者在实际操作中还需考虑其他因素,并综合判断股票的潜在风险和回报。

英语作文-金融资产管理公司创新投资策略,提高市场竞争力

英语作文-金融资产管理公司创新投资策略,提高市场竞争力Innovative Investment Strategies for Financial Asset Management Companies to Enhance Market Competitiveness。

The landscape of financial asset management is evolving rapidly, driven by dynamic market conditions, technological advancements, and shifting investor preferences. In this context, the adoption of innovative investment strategies becomes crucial for financial asset management companies aiming to bolster their market competitiveness.Effective utilization of data analytics stands at the forefront of modern investment strategies. By leveraging big data and machine learning algorithms, asset managers can extract actionable insights from vast datasets. These insights are pivotal in identifying emerging market trends, predicting asset price movements, and optimizing portfolio allocations in real-time. Moreover, the integration of artificial intelligence enhances decision-making processes, enabling quicker adjustments to market volatility and improving overall investment performance.Diversification remains a cornerstone of resilient investment strategies. Beyond traditional asset classes, such as equities and bonds, diversified portfolios now encompass alternative investments like private equity, venture capital, and real estate. These assets offer unique risk-return profiles and can provide essential diversification benefits, reducing portfolio volatility and enhancing long-term returns. Furthermore, strategic partnerships with niche investment firms or specialized asset managers facilitate access to exclusive investment opportunities, further enriching portfolio diversification.Risk management strategies have also evolved significantly, becoming more sophisticated and proactive. Modern asset management firms employ advanced risk assessment models that incorporate scenario analysis, stress testing, and Monte Carlo simulations. These methodologies allow firms to quantify and mitigate various riskseffectively, including market risk, credit risk, liquidity risk, and operational risk. By implementing robust risk management frameworks, companies can safeguard investor capital while maintaining competitive performance metrics.In response to growing environmental, social, and governance (ESG) considerations, sustainable investing has gained prominence across asset management sectors. Integrating ESG factors into investment strategies not only aligns with ethical principles but also mitigates risks associated with regulatory changes and reputational damage. Sustainable investments encompass a broad spectrum, ranging from renewable energy projects to socially responsible corporate bonds, thereby attracting a diverse investor base and enhancing overall portfolio resilience.Technological innovation continues to redefine client engagement and service delivery within asset management. The proliferation of digital platforms and fintech solutions enables firms to offer personalized investment advice, real-time portfolio monitoring, and seamless transaction capabilities. Additionally, leveraging blockchain technology enhances transparency, security, and efficiency in managing investment operations and fund distributions.Amidst the evolving landscape, agility emerges as a critical determinant of competitive advantage. Financial asset management companies must embrace a culture of innovation and adaptability, continually refining investment strategies to capitalize on emerging opportunities and navigate evolving market dynamics. Proactive monitoring of global macroeconomic trends, geopolitical developments, and regulatory changes is essential to anticipate market shifts and optimize investment outcomes.In conclusion, the pursuit of innovative investment strategies is imperative for financial asset management companies seeking to enhance market competitiveness. By harnessing data analytics, diversifying portfolios, strengthening risk management frameworks, embracing sustainable investing practices, leveraging technological advancements, and fostering organizational agility, firms can position themselves at the forefront of the industry. Ultimately, a commitment to innovation not only drives superiorinvestment performance but also cultivates long-term client trust and satisfaction in an increasingly competitive marketplace.。

投资学(双语)_课程大纲

《投资学(双语)》教学大纲课程编号:091333B课程类型:□通识教育必修课□通识教育选修课□专业必修课□√专业选修课□学科基础课总学时:48 讲课学时:48 实验(上机)学时:学分:3适用对象:资产评估先修课程:金融学1.教学目标(黑体,小四号字)投资学是随着我国金融市场的发展特别是资本证券市场的发展,高校为适应社会对从事金融证券投资业务活动的应用性专业人才不断扩大的需要而开设的一门课程。

本课程的教学目标是通过课堂教学,让学生系统地掌握投资领域的基本理论、熟悉金融工具的基本定价规律,在教学中立足开拓学生的国际视野,注重培养学生分析问题、解决问题的能力,为成为卓越评估师打下坚实的知识基础。

目标1:系统了解现代投资理论、原理和内在机制目标2:掌握各种金融工具的特点和定价规律。

目标3:在学习中注重培养学生分析问题、解决问题的能力。

2.教学内容及其与毕业要求的对应关系(黑体,小四号字)可包括但不限于:1.教学内容讲授上的要求精讲内容包括金融市场、基金、风险与收益、马克维茨投资组合理论、因素模型;粗讲投资过程、各种金融工具的特点。

2.教学方法、教学手段根据本课程的特点以及培养目标的要求,在教学中应遵循循序渐进、深入浅出的原则和理论与实践相结合的原则。

在课堂教学中以导读与释疑为主,教师以教学大纲为依据,以主要教材为蓝本,提要基本内容、识记基本概念、讲解基本原理、讲解重点难点,课下要求学生阅读大量投资领域相关文献以加深对课程所授知识的理解深度。

3.对课后作业以及学生自学的要求本课程在学习中将安排4-5次课外综合作业,重点考察学生所学知识的掌握程度。

对于一些容易理解的知识点放置课下学习,为学生提供探索与思考的空间。

4.该课程从哪些方面促进了毕业要求的实现(1)本课程学习可以帮助学生金融市场的运行规律,能够采用科学的方法从金融市场中搜集相关数据与信息并进行和分析处理,进而形成恰当投资决策;(2)本课程学习可以帮助学生逐渐形成团队协作意识,并在资产评估团队活动中发挥个人能力,同时与其他成员进行协调合作;(3)本课程学习可以帮助学生养成自主学习和终身学习意识,培养其创业创新能力及不断学习与适应发展的能力。

巴塞尔资本协议中英文完整版(05第一部分(英文))

Basel Committeeon Banking SupervisionConsultative Document The NewBasel Capital Accord Issued for comment by 31 July 2003 April 2003Table of ContentsPart 1: Scope of A pplication (1)A. Introduction (1)B. Banking, securities and other financial subsidiaries (1)C. Significant minority investments in banking, securities and other financial entities (2)D. Insurance entities (2)E. Significant investments in commercial entities (4)F. Deduction of investments pursuant to this part (4)Part 2: The First Pillar - Minimum Capital Requirements (6)I. Calculation of minimum capital requirements (6)II. Credit Risk - The Standardised Approach (6)A. The standardised approach - general rules (6)1. Individual claims (7)(i) Claims on sovereigns (7)(ii) Claims on non-central government public sector entities (PSEs) (8)(iii) Claims on multilateral development banks (MDBs) (8)(iv) Claims on banks (9)(v) Claims on securities firms (10)(vi) Claims on corporates (10)(vii) Claims included in the regulatory retail portfolios (11)(viii) Claims secured by residential property (11)(ix) Claims secured by commercial real estate (12)(x) Past due loans (12)(xi) Higher-risk categories (13)(xii) Other assets (13)(xiii) Off-balance sheet items (13)2. External credit assessments (14)(i) The recognition process (14)(ii) Eligibility criteria (14)3. Implementation considerations (15)(i) The mapping process (15)(ii) Multiple assessments (15)(iii) Issuer versus issues assessment (15)(iv) Domestic currency and foreign currency assessments (16)(v) Short term/long term assessments (16)(vi) Level of application of the assessment (17)(vii) Unsolicited ratings (17)B. The standardised approach - credit risk mitigation (17)1. Overarching issues (17)(i) Introduction (17)(ii) General remarks (18)(iii) Legal certainty (18)2. Overview of Credit Risk Mitigation Techniques (19)(i) Collateralised transactions (19)(ii) On-balance sheet netting (21)(iii) Guarantees and credit derivatives (21)(iv) Maturity mismatch (21)(v) Miscellaneous (22)3. Collateral (22)(i) Eligible financial collateral (22)(ii) The comprehensive approach (23)(iii) The simple approach (31)(iv) Collateralised OTC derivatives transactions (32)4. On-balance sheet netting (32)5. Guarantees and credit derivatives (33)(i) Operational requirements (33)(ii) Range of eligible guarantors/protection providers (35)(iii) Risk weights (35)(iv) Currency mismatches (36)(v) Sovereign guarantees (36)6. Maturity mismatches (37)(i) Definition of maturity (37)(ii) Risk weights for maturity mismatches (37)7. Other items related to the treatment of CRM techniques (37)(i) Treatment of pools of CRM techniques (37)(ii) First-to-default credit derivatives (38)(iii) Second-to-default credit derivatives (38)III. Credit Risk - The Internal Ratings-Based Approach (38)A. Overview (38)B. Mechanics of the IRB Approach (39)1. Categorisation of exposures (39)(i) Definition of corporate exposures (39)(ii) Definition of sovereign exposures (41)(iii) Definition of bank exposures (41)(iv) Definition of retail exposures (41)(v) Definition of qualifying revolving retail exposures (42)(vi) Definition of equity exposures (43)(vii) Definition of eligible purchased receivables (45)2. Foundation and advanced approaches (46)(i) Corporate, sovereign, and bank exposures (46)(ii) Retail exposures (47)(iii) Equity exposures (47)(iv) Eligible purchased receivables (47)3. Adoption of the IRB approach across asset classes (47)4. Transition arrangements (48)(i) Parallel calculation for banks adopting the advanced approach (48)(ii) Corporate, sovereign, bank, and retail exposures (48)(iii) Equity exposures (49)C. Rules for Corporate, Sovereign, and Bank Exposures (49)1. Risk-weighted assets for corporate, sovereign, and bank exposures (50)(i) Formula for derivation of risk weights (50)(ii) Firm-size adjustment for small and medium-sized entities (SME) (50)(iii) Risk weights for specialised lending (51)2. Risk components (52)(i) Probability of Default (PD) (52)(ii) Loss Given Default (LGD) (52)(iii) Exposure at Default (EAD) (56)(iv) Effective Maturity (M) (58)D. Rules for Retail Exposures (59)1. Risk-weighted assets for retail exposures (59)(i) Residential mortgage exposures (60)(ii) Qualifying revolving retail exposures (60)(iii) Other retail exposures (60)2. Risk components (61)(i) Probability of default (PD) and loss given default (LGD) (61)(ii) Recognition of guarantees and credit derivatives (61)(iii) Exposure at default (EAD) (61)E. Rules for Equity Exposures (62)1. Risk weighted assets for equity exposures (62)(i) Market-based approach (62)(ii) PD/LGD approach (63)(iii) Exclusions to the market-based and PD/LGD approaches (64)2. Risk components (64)F. Rules for Purchased Receivables (65)1. Risk-weighted assets for default risk (65)(i) Purchased retail receivables (65)(ii) Purchased corporate receivables (65)2. Risk-weighted assets for dilution risk (67)(i) Treatment of purchased discounts (67)(ii) Recognition of guarantees (67)G. Recognition of Provisions (68)H. Minimum Requirements for IRB Approach (69)1. Composition of minimum requirements (69)2. Compliance with minimum requirements (70)3. Rating system design (70)(i) Rating dimensions (70)(ii) Rating structure (71)(iii) Rating criteria (72)(iv) Assessment horizon (73)(v) Use of models (73)(vi) Documentation of rating system design (74)4. Risk rating system operations (75)(i) Coverage of ratings (75)(ii) Integrity of rating process (75)(iii) Overrides (76)(iv) Data maintenance (76)(v) Stress tests used in assessment of capital adequacy (77)5. Corporate governance and oversight (77)(i) Corporate governance (77)(ii) Credit risk control (78)(iii) Internal and external audit (78)6. Use of internal ratings (79)7. Risk quantification (79)(i) Overall requirements for estimation (79)(ii) Definition of default (80)(iii) Re-ageing (81)(iv) Treatment of overdrafts (82)(v) Definition of loss - all asset classes (82)(vi) Requirements specific to PD estimation (82)(vii) Requirements specific to own-LGD estimates (83)(viii) Requirements specific to own-EAD estimates (84)(ix) Minimum requirements for assessing effect of guarantees and credit derivatives (86)(x) Minimum requirements for estimating PD and LGD (EL) (87)8. Validation of internal estimates (89)9. Supervisory LGD and EAD estimates (90)(i) Definition of eligibility of CRE and RRE as collateral (90)(ii) Operational requirements for eligible CRE/RRE (91)(iii) Requirements for recognition of financial receivables (92)10. Requirements for recognition of leasing (94)11. Calculation of capital charges for equity exposures (94)(i) The internal models market-based approach (94)(ii) Capital charge and risk quantification (95)(iii) Risk management process and controls (96)(iv) Validation and documentation (97)12. Disclosure requirements (99)IV. C redit Risk - Securitisation Framework (99)A. Scope and definitions of transactions covered under the securitisation framework 99B. Definitions (100)1. Different roles played by banks (100)(i) Investing bank (100)(ii) Originating bank (100)2. General terminology (101)(i) Clean-up call (101)(ii) Credit enhancement (101)(iii) Early amortisation (101)(iv) Excess spread (101)(v) Implicit support (101)(vi) Special purpose entity (SPE) (102)C. Operational requirements for the recognition of risk transference (102)1. Operational requirements for traditional securitisations (102)2. Operational requirements for synthetic securitisations (103)3. Operational requirements and treatment of clean-up calls (103)D. Treatment of securitisation exposures (104)1. Minimum capital requirement (104)(i) Deduction (104)(ii) Implicit support (104)2. Operational requirements for use of external credit assessments (104)3. Standardised approach for securitisation exposures (105)(i) Scope (105)(ii) Risk weights (105)(iii) Exceptions to general treatment of unrated securitisation exposures (106)(iv) Credit conversion factors for off-balance sheet exposures (107)(v) Recognition of credit risk mitigants (108)(vi) Capital requirement for early amortisation provisions (109)(vii) Determination of CCFs for controlled early amortisation features (110)(viii) Determination of CCFs for non-controlled early amortisation features .. 1114. Internal ratings-based approach for securitisation exposures (112)(i) Scope (112)(ii) Definition of K IRB (113)(iii) Hierarchy of approaches (113)(iv) Maximum capital requirement (114)(v) Rating Based Approach (RBA) (114)(vi) Supervisory Formula (SF) (116)(vii) Liquidity facilities (119)(viii) Eligible servicer cash advance facilities (119)(ix) Recognition of credit risk mitigants (119)(x) Capital requirements for early amortisation provisions (120)V. Operational Risk (120)A. Definition of operational risk (120)B. The Measurement methodologies (120)1. The Basic Indicator Approach (121)2. The Standardised Approach (122)3. Advanced Measurement Approach (AMA) (123)C. Qualifying criteria (123)1. General criteria (123)2. Standardised approach (124)3. Advanced measurement approaches (125)(i) Qualitative standards (125)(ii) Quantitative standards (126)(iii) Risk mitigation (129)D. Partial use (130)VI. T rading book issues (131)A. Definition of the trading book (131)B. Prudent valuation guidance (132)1. Systems and controls (132)2. Valuation methodologies (132)(i) Marking to market (132)(ii) Marking to model (133)(iii) Independence price verification (133)3. Valuation adjustments or reserves (134)C. Treatment of counterparty credit risk in the trading book (134)D. Trading book capital treatment for specific risk under the standardisedmethodology (135)1. Specific risk capital charges for government paper (135)2. Specific risk rules for unrated debt securities (135)3. Specific risk capital charges for positions hedged by credit derivatives (136)4. Add-on factor for credit derivatives (137)Part 3: The Second Pillar - Supervisory Review Process (138)A. Importance of supervisory review (138)B. Four key principles for supervisory review (139)C. Specific issues to be addressed under the supervisory review process (145)D. Other aspects of the supervisory review process (151)Part 4: The Third Pillar - Market Discipline (154)A. General considerations (154)1. Disclosure requirements (154)2. Guiding principles (154)3. Achieving appropriate disclosure (154)4. Interaction with accounting disclosures (155)5. Materiality (155)6. Frequency (156)7. Proprietary and confidential information (156)B. The disclosure requirements (156)1. General disclosure principle (156)2. Scope of application (157)3. Capital (158)4. Risk exposure and assessment (159)(i) General qualitative disclosure requirement (160)(ii) Credit risk (160)(iii) Market risk (167)(iv) Operational risk (168)(v) Interest rate risk in the banking book (168)Annex 1 The 15% of Tier 1 Limit on Innovative Instruments (169)Annex 2 Standardised Approach - Implementing the Mapping Process (170)Annex 3 Illustrative IRB risk weights (174)Annex 4 Supervisory Slotting Criteria for Specialised Lending (176)Annex 5 Illustrative Examples : Calculating the Effect of Credit Risk Mitigationunder Supervisory Formula (195)Annex 6 Mapping of Business Lines (199)Annex 7 Detailed loss event type classification (202)Annex 8 Overview of Methodologies for the Capital Treatment of Transactions Secured by Financial Collateral under the Standardised and IRB Approaches (204)Annex 9 The Simplified Standardised Approach (206)AcronymsABCP Asset-backed commercial paperADC Acquisition, development and constructionAMA Advanced measurement approachesASA Alternative standardised approachCCF Credit conversion factorCDR Cumulative default rateCF Commodities financeCRM Credit risk mitigationEAD Exposure at defaultECA Export credit agencyECAI External credit assessment institutionEL Expected lossFMI Future margin incomeHVCRE High-volatility commercial real estateIPRE Income-producing real estateIRB approach Internal ratings-based approachLGD Loss given defaultM Effective maturityMDB Multilateral development bankNIF Note issuance facilityOF Object financePD Probability of defaultPF Project financePSE Public sector entityRBA Ratings-based approachRUF Revolving underwriting facilitySF Supervisory formulaSL Specialised lendingSME Small- and medium-sized enterpriseSPE Special purpose entityUCITS Undertakings for collective investments in transferable securities UL Unexpected lossPart 1: Scope of ApplicationA. Introduction1. The New Basel Capital Accord (the New Accord) will be applied on a consolidated basis to internationally active banks. This is the best means to preserve the integrity of capital in banks with subsidiaries by eliminating double gearing.2. The scope of application of the Accord will be extended to include, on a fully consolidated basis, any holding company that is the parent entity within a banking group to ensure that it captures the risk of the whole banking group.1 Banking groups are groups that engage predominantly in banking activities and, in some countries, a banking group may be registered as a bank.3. The Accord will also apply to all internationally active banks at every tier within a banking group, also on a fully consolidated basis (see illustrative chart at the end of this section).2 A three-year transitional period for applying full sub-consolidation will be provided for those countries where this is not currently a requirement.4. Further, as one of the principal objectives of supervision is the protection of depositors, it is essential to ensure that capital recognised in capital adequacy measures is readily available for those depositors. Accordingly, supervisors should test that individual banks are adequately capitalised on a stand-alone basis.B. Banking, securities and other financial subsidiaries5. To the greatest extent possible, all banking and other relevant financial activities3 (both regulated and unregulated) conducted within a group containing an internationally active bank will be captured through consolidation. Thus, majority-owned or-controlled banking entities, securities entities (where subject to broadly similar regulation or where securities activities are deemed banking activities) and other financial entities4 should generally be fully consolidated.6. Supervisors will assess the appropriateness of recognising in consolidated capital the minority interests that arise from the consolidation of less than wholly owned banking,1 A holding company that is a parent of a banking group may itself have a parent holding company. In somestructures, this parent holding company may not be subject to this Accord because it is not considered a parent of a banking group.2As an alternative to full sub-consolidation, the application of the Accord to the stand-alone bank (i.e. on a basis that does not consolidate assets and liabilities of subsidiaries) would achieve the same objective, providing the full book value of any investments in subsidiaries and significant minority-owned stakes is deducted from the bank's capital.3In Part 1, “financial activities” do not include insurance activities and “financial entities” do not include insurance entities.4Examples of the types of activities that financial entities might be involved in include financial leasing, issuing credit cards, portfolio management, investment advisory, custodial and safekeeping services and other similar activities that are ancillary to the business of banking.1securities or other financial entities. Supervisors will adjust the amount of such minority interests that may be included in capital in the event the capital from such minority interests is not readily available to other group entities.7. There may be instances where it is not feasible or desirable to consolidate certain securities or other regulated financial entities. This would be only in cases where such holdings are acquired through debt previously contracted and held on a temporary basis, are subject to different regulation, or where non-consolidation for regulatory capital purposes is otherwise required by law. In such cases, it is imperative for the bank supervisor to obtain sufficient information from supervisors responsible for such entities.8. If any majority-owned securities and other financial subsidiaries are not consolidated for capital purposes, all equity and other regulatory capital investments in those entities attributable to the group will be deducted, and the assets and liabilities, as well as third-party capital investments in the subsidiary will be removed from the bank’s balance sheet. Supervisors will ensure that the entity that is not consolidated and for which the capital investment is deducted meets regulatory capital requirements. Supervisors will monitor actions taken by the subsidiary to correct any capital shortfall and, if it is not corrected in a timely manner, the shortfall will also be deducted from the parent ba nk’s capital.C. Significant minority investments in banking, securities and otherfinancial entities9. Significant minority investments in banking, securities and other financial entities, where control does not exist, will be excluded from the banking g roup’s capital by deduction of the equity and other regulatory investments. Alternatively, such investments might be, under certain conditions, consolidated on a pro rata basis. For example, pro rata consolidation may be appropriate for joint ventures or where the supervisor is satisfied that the parent is legally or de facto expected to support the entity on a proportionate basis only and the other significant shareholders have the means and the willingness to proportionately support it. The threshold above which minority investments will be deemed significant and be thus either deducted or consolidated on a pro-rata basis is to be determined by national accounting and/or regulatory practices. As an example, the threshold for pro-rata inclusion in the European Union is defined as equity interests of between 20% and 50%.10. The Committee reaffirms the view set out in the 1988 Accord that reciprocal cross-holdings of bank capital artificially designed to inflate the capital position of banks will be deducted for capital adequacy purposes.D. Insurance entities11. A bank that owns an insurance subsidiary bears the full entrepreneurial risks of the subsidiary and should recognise on a group-wide basis the risks included in the whole group. When measuring regulatory capital for banks, the Committee believes that at this stage it is, in principle, appropriate to deduct banks’ equity and other regulatory capital investments in insurance subsidiaries and also significant minority investments in insurance entities. Under this approach the bank would remove from its balance sheet assets and liabilities, as well as third party capital investments in an insurance subsidiary. Alternative approaches that can be 2applied should, in any case, include a group-wide perspective for determining capital adequacy and avoid double counting of capital.12. Due to issues of competitive equality, some G10 countries will retain their existing risk weighting treatment5 as an exception to the approaches described above and introduce risk aggregation only on a consistent basis to that applied domestically by insurance supervisors for insurance firms with banking subsidiaries.6 The Committee invites insurance supervisors to develop further and adopt approaches that comply with the above standards.13. Banks should disclose the national regulatory approach used with respect to insurance entities in determining their reported capital positions.14. The capital invested in a majority-owned or controlled insurance entity may exceed the amount of regulatory capital required for such an entity (surplus capital). Supervisors may permit the recognition of such surplus capital in calculating a bank’s capital adequacy, under limited circumstances.7 National regulatory practices will determine the parameters and criteria, such as legal transferability, for assessing the amount and availability of surplus capital that could be recognised in bank capital. Other examples of availability criteria include: restrictions on transferability due to regulatory constraints, to tax implications and to adverse impacts on external credit assessment institutions’ ratings. Banks recognising surplus capital in insurance subsidiaries will publicly disclose the amount of such surplus capital recognised in their capital. Where a bank does not have a full ownership interest in an insurance entity (e.g. 50% or more but less than 100% interest), surplus capital recognised should be proportionate to the percentage interest held. Surplus capital in significant minority-owned insurance entities will not be recognised, as the bank would not be in a position to direct the transfer of the capital in an entity which it does not control.15. Supervisors will ensure that majority-owned or controlled insurance subsidiaries, which are not consolidated and for which capital investments are deducted or subject to an alternative group-wide approach, are themselves adequately capitalised to reduce the possibility of future potential losses to the bank. Supervisors will monitor actions taken by the subsidiary to correct any capital shortfall and, if it is not corrected in a timely manner, the shortfall will also be deducted from the parent bank’s capital.5For banks using the standardised approach this would mean applying no less than a 100% risk weight, while for banks on the IRB approach, the appropriate risk weight based on the IRB rules shall apply to such investments.6Where the existing treatment is retained, third party capital invested in the insurance subsidiary (i.e. minority interests) cannot be included in the bank’s capital adequacy measurement.7In a deduction approach, the amount deducted for all equity and other regulatory capital investments will be adjusted to reflect the amount of capital in those entities that is in surplus to regulatory requirements, i.e. the amount deducted would be the lesser of the investment or the regulatory capital requirement. The amount representing the surplus capital, i.e. the difference between the amount of the investment in those entities and their regulatory capital requirement, would be risk-weighted as an equity investment. If using an alternative group-wide approach, an equivalent treatment of surplus capital will be made.3E. Significant investments in commercial entities16. Significant minority and majority investments in commercial entities which exceed certain materiality levels will be deducted from banks’ capital. Materiality levels will be determined by national accounting and/or regulatory practices. Materiality levels of 15% of the bank’s capital for indiv idual significant investments in commercial entities and 60% of the bank’s capital for the aggregate of such investments, or stricter levels, will be applied. The amount to be deducted will be that portion of the investment that exceeds the materiality level.17. Investments in significant minority- and majority-owned and controlled commercial entities below the materiality levels noted above will be risk weighted at no lower than 100% for banks using the standardised approach. For banks using the IRB approach, the investment would be risk weighted in accordance with the methodology the Committee is developing for equities and would not be less than 100%.F. Deduction of investments pursuant to this part18. Where deductions of investments are made pursuant to this part on scope of application, the deductions will be 50% from Tier 1 and 50% from Tier 2.19. Goodwill relating to entities subject to a deduction approach pursuant to this part should be deducted from Tier 1 in the same manner as goodwill relating to consolidated subsidiaries, and the remainder of the investments should be deducted as provided for in this part. A similar treatment of goodwill should be applied, if using an alternative group-wide approach pursuant to paragraph 11.20. The issuance of the final Accord will clarify that the limits on Tier 2 and Tier 3 capital and on innovative Tier 1 instruments will be based on the amount of Tier 1 capital after deduction of goodwill but before the deductions of investments pursuant to this part on scope of application (see Annex 1 for an example how to calculate the 15% limit for innovative Tier 1 instruments).4IL L U ST R A T IO N O F N E W SC O PE O F A PPL IC A T IO N O F T H E A C C O R D(1) B oundary of predom inant banking group. T he A ccord is to be applied at this level on a consolidated basis, i.e. up(paragraph 2).to holding com pany level .(2), (3)and (4): the A ccord is also to be applied at low e r levels to all internationally active banks on a consolidatedbasis.5。

兹维博迪投资学知识点总结

兹维博迪投资学知识点总结兹维博迪(Benjamin Graham)是20世纪著名的投资理论家之一,他被誉为价值投资之父。

其所著《证券分析》和《智慧投资者》两部著作影响了无数的投资者和分析师,成为投资界的经典之作。

兹维博迪的投资理念主要包括价值投资、风险管理和长期投资。

下面将对兹维博迪投资学知识点进行总结,以便读者能够更深入地了解其投资理念。

一、价值投资1. 价值投资的概念价值投资是指根据公司实际价值来选择投资标的,即购买价格低于其内在价值的股票。

兹维博迪认为,股价的波动不代表公司价值的波动,因此投资者应该关注公司的真实价值而不是市场短期波动。

2. 安全边际兹维博迪强调安全边际的重要性,即购买股票时要求价格远低于其内在价值,以确保投资具有较高的安全性和回报潜力。

3. 长期投资兹维博迪提倡长期投资,他认为投资者应该把握好公司的长期价值增长,而不是被短期市场波动所左右。

通过长期持有股票,可以更好地享受公司价值的增长和分红回报。

二、风险管理1. 风险的认知兹维博迪认为,任何投资都存在一定的风险,投资者必须要认清并能够合理管理风险。

他主张了解投资标的的风险特征,以及如何避免和规避风险。

2. 多样化投资为了降低投资风险,兹维博迪建议投资者分散投资,即通过购买多种不相关股票来降低整体投资组合的风险。

3. 投资原则兹维博迪强调投资者要坚守交易原则,包括自律、冷静和理性,不被市场情绪所左右,以及坚持价值投资的原则,不盲从短期市场的热点。

三、投资技巧1. 企业分析兹维博迪鼓励投资者要对所投资的公司进行深入的分析,包括了解其经营模式、财务状况、行业竞争力等,并通过比较公司的内在价值和市场价格来寻找投资机会。

2. 市场心理兹维博迪提醒投资者注意市场心理的影响,警惕市场的短期情绪波动,并通过理性的思考和冷静的判断来进行投资决策。

3. 价值投资策略兹维博迪强调价值投资策略的重要性,包括寻找低估的优质公司、购买价格远低于其内在价值、长期持有等,这些策略符合他对长期投资和安全边际的观点。

18699221_瑞·达利欧

“在极度透明和极度求真的基础上,实现创意择优——确保最优的想法脱颖而出。

”桥水基金创始人瑞 · 达利欧(Ray Dalio)WISE MAN 大方之家正所谓“久病成良医”,我们应该了解债务危机发生的内在规律。

瑞·达利欧从一个投资者的角度建立了理解债务危机的债务大周期模型。

李珍 北京报道1975年,瑞•达利欧26岁时在自己的两居室寓所中创办了桥水基金,至今,管理资金超过1500亿美元,是全球最赚钱的对冲基金公司。

他凭借独到的投资准则改变了基金业,美国投资界重要刊物《CIO 》称瑞•达利欧为“投资界的史蒂夫•乔布斯”。

2007年达利欧成功预测到了美国的次贷危机,从而让桥水采取了相应的防范和应对策略。

3月22日,中信出版集团主办的2019经济展望与投资趋势暨《债务危机》新书发布会上,达利欧与中国投资者分享了债务危机的应对原则。

瑞•达利欧基于对过去100年间所有的大的债务危机分析,建立了债务大周期模型。

他认为每次债务危机的表现形式都不完全一样,但大致的周期差不多。

如果知道模型中因素相互之间如何运作,基本就能对经济形势做出预测。

瑞•达利欧的“原则”瑞•达利欧多年前养成的习惯,做决策时要把决策内容全部写下来,因为要进行反思。

每次进行交易时都会写下来,为什么要做这样一笔交易,然后再回过头来要看为什么当时做了这样一笔交易。

“每次都把交易的条件、标准或原则写下来时,我发现,相似的事情不断地重复发生,所以重要的是,要有自己的应对原则。

” 瑞•达利欧说。

他认为在处理当下事件的时候要有一个原则——了解现实情况,每次意想不到的情况发生时,说明有些事情是之前没有经历过,但实际上又发生过很多次。

“所以人们需要知道经济机器是如何运行的、市场机器是如何运行的,因为它们之间存在因果的联系,是不断重复发生的。

”2018年,瑞•达利欧发布的《原则》一书,畅销全球。

他多次表达过对看重持有原则的好奇。

在《原则》中他写道:“人们很少把自己的原则写下来与别人分享,这太令人遗憾了。

Lévy市场下保险公司的最优投资策略

一、引言 随着保险公司可以在资本市场进行投

资,越来越多的投资者关注保险公司的投 资组合问题,在现实生活中保险公司投资 决策者并不是完全理性的,最著名的就 是累积前景理论 (CPT) 来弥补 EUM 的缺 陷, 在 Guo(2014) 之 前 没 有 人 把 CPT 引 入保险公司的投资决策中,Guo(2014) 即 引入进来,并指出保险公司的盈余是服从 列维过程,然而在保险公司在资本市场进 行投资的时候,价格过程由于受到很多因 素的影响,不是一个连续的过程,而是存 在一个跳的的过程,至今还没有文章在 CPT 原理中加入保险公司的风险资产价 格服从列维过程。本文假设者是损失厌恶 的,满足 S- 型效用函数,为了使模型更 具有现实性,我们假定保险公司投资于一 种无风险资产和 n 种风险资产,风险资产 的价格过程服从列维过程,并且假定保险 公司的盈余过程也是服从列维过程的。再 运用鞅方法,得出最优投资策略和最优财 富过程。 二、模型

假设保险公司在时间 [0,T] 内在资 本市场投资 n+1 种资产,一种无风险资 产和 n 种风险资产,其中无风险资产的价 格满足

n 种风险资产的价格过程 满足

独 立 的,

是 瞬 时 扩 散 率,源自是列维过程。假定保险公司的盈余过程 U(t) 是复

合的泊松过程或 Cramér-Lundberg 模型。

[2] 米辉,张曙光 . 财富约束下损失厌 恶投资者的动态投资组合选择 [J]. 系统工 程理论与实践,2013,33(5):5-9.

( 作者单位:南京财经大学 )

Copyright©博看网 . All Rights Reserved.

229

下将求出 (2.12) 中的 ,由于

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Dilip B. Madan Robert H. Smith School of Business Van Munching Hall University of Maryland College Park, MD. 20742 (301) 405-2127 dbm@ May 24, 2000

Optimal Investment in Derivative Securities

Peter Carr Banc of America Securities 9 West 57th Street, 40th floor New York, N.Y. 10019 (212) 583-8529 carrp@ Xing Jin Robert H. Smith School of Business Van Munching Hall University of Maryland College Park, MD. 20742 (301) 405-7130 xjin@

Abstract We consider the problem of optimal investment in a risky asset, and in derivatives written on the price process of this asset, when the underlying asset price process is a pure jump L´ evy process. The duality approach of Karatzas and Shreve is used to derive the optimal consumption and investment plans. In our economy, the optimal derivative payoff can be constructed from dynamic trading in the risky asset and in European options of all strikes. Specific closed forms illustrate the optimal derivative contracts when the utility function is in the HARA class and when the statistical and risk-neutral price processes are in the variance gamma (VG) class. In this case, we observe that the optimal derivative contract pays a function of the price relatives continuously through time.

Hale Waihona Puke 11 Introduction

In a classic paper, Merton [23] derived the optimal consumption and investment rules for investors maximizing the expected utility of their consumption in an economy consisting of a riskless asset and risky assets whose prices follow geometric Brownian motion. He showed that when investors have HARA (hyperbolic absolute risk aversion) utility functions, then one can solve for the optimal consumption and investment rules in closed form. Merton’s analysis relied on Markov state processes and sought to obtain explicit solutions to the Hamilton-Jacobi-Bellman equation in this context. Subsequently, Pliska [26], Cox and Huang [5], and Karatzas, Lehoczky and Shreve [16] all showed how to solve these problems in a non-Markovian context by applying stochastic duality theory in the context of complete markets. Our interest here is in determining optimal strategies for investing in derivative assets such as options of various strikes. In Merton’s economy, the continuity of the underlying stock price process and the resulting completeness of markets renders options redundant. In contrast to Merton, we consider an economy in which dynamic trading in options is necessary and sufficient for market completeness. We accomplish this by assuming that both the statistical and risk-neutral processes for the underlying risky asset price are pure jump processes of finite variation which are infinitely divisible with independent increments. Our solution methods follow the duality approach as described in Karatzas and Shreve [17]. To generate explicit illustrative solutions, we focus on a particularly tractable subclass of processes called the variance gamma (VG) process, which is discussed in detail in [22], [21], and [20]. While the demand for options can arise from many sources, our focus on jumps stems from fundamental considerations regarding the nature of price processes in an arbitragefree economy. Recently, Madan [19] has argued that all arbitrage-free continuous time price processes must be both semi-martingales and time-changed Brownian motion. Furthermore, it is argued that if the time change is not locally deterministic, then the resulting price process is discontinuous. If the price is modelled as a pure jump L´ evy process with infinity activity, then the need for a continuous martingale component is obviated, since there will be an infinite number of small jumps in any time interval. Our focus on processes of finite variation is motivated by the observation in [19] that for such processes, the requirement of equivalence between the statistical and risk-neutral probabilities imposes no integrability or parametric restrictions. Thus, the resulting class of processes is quite rich in its ability to describe both the statistical and risk-neutral dynamics of market data, as is evidenced by the special VG model studied in [20]. For HARA investors in an economy for which the statistical and risk-neutral price processes are both VG processes, we show that the optimal derivative security is a contract written on the underlying asset’s instantaneous returns (as measured by log price relatives), rather than on its final price. The optimal contract pays a function of this return when prices change. We also show how such a payoff may be synthesized by dynamic trading in options of all strikes and a single maturity. For statistical volatilities below risk-neutral ones, we show that the optimal derivative contract for intermediate levels of risk aversion is a collar that finances downside protection against drops in the market by selling upside gain. We also note in passing that certain houses have recently started offering derivatives whose payoffs are tied to returns in response to investor demand1 . The outline of this paper is as follows. Section 2 presents the financial market model. Section 3 gives a brief description of the martingale representation theorem in our pure jump context, which is used to generate our completeness results later. Self-financing strategies and the budget constraint are described in detail in section 4. The finite