罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](风险、资本成本和资本预算)【圣才

罗斯《公司理财》(第9版)课后习题(第13~15章)【圣才出品】

罗斯《公司理财》(第9版)课后习题第13章风险、资本成本和资本预算一、概念题1.资产贝塔(asset beta)答:资产贝塔是指企业总资产的贝塔系数。

除非完全依靠权益融资,否则不能把资产贝塔看作普通股的贝塔系数。

其公式为:其中,β权益是杠杆企业权益的贝塔。

公式包括两部分,即负债的贝塔乘以负债在资本结构中的百分比;权益的贝塔乘以权益在资本结构中的百分比。

这个组合包括企业的负债和权益,所以组合贝塔就是资产贝塔。

在实际中,负债的贝塔很低,一般假设为零。

若假设负债的贝塔为零,则:对于杠杆企业,权益/(负债+权益)一定小于1,所以β资产<β权益,将上式变形,有:有财务杠杆的情况下,权益贝塔一定大于资产贝塔。

2.经营杠杆(operating leverage)答:经营杠杆是指由于固定成本的存在而导致息税前利润变动大于产销业务量变动的杠杆效应。

对经营杠杆的计量最常用的指标是经营杠杆系数或经营杠杆度。

经营杠杆系数,是指息税前利润变动率相当于销售量变动率的倍数。

用公式可以表示为:式中,EBIT为息税前利润;F为固定成本。

经营杠杆系数不是固定不变的。

当企业的固定成本总额、单位产品的变动成本、销售价格、销售数量等因素发生变动时,经营杠杆系数也会发生变动。

经营杠杆系数越高,对经营杠杆利益的影响就越强,经营杠杆风险也就越高。

经营杠杆越大,企业的贝塔系数就越大。

3.权益资本成本(cost of equity capital)答:权益资本成本就是投资股东要求的回报率,用CAPM模型表示股票的期望收益率为:其中,R F是无风险利率;是市场组合的期望收益率与无风险利率之差,也称为期望超额市场收益率或市场风险溢价。

所以要估计企业权益资本成本,需要知道以下三个变量:①无风险利率;②市场风险溢价;③公司权益的贝塔系数。

4.加权平均资本成本(weighted average cost of capital,r WACC)答:平均资本成本是权益资本成本和债务资本成本的加权平均,所以,通常称之为加权平均资本成本,r WACC,其计算公式如下:式中的权数分别是权益占总价值的比重,即和负债占总价值的比重,即。

罗斯《公司理财》(第9版)课后习题(第1~3章)【圣才出品】

罗斯《公司理财》(第9版)课后习题第1章公司理财导论一、概念题1.资本预算(capital budgeting)答:资本预算是指综合反映投资资金来源与运用的预算,是为了获得未来产生现金流量的长期资产而现在投资支出的预算。

资本预算决策也称为长期投资决策,它是公司创造价值的主要方法。

资本预算决策一般指固定资产投资决策,耗资大,周期长,长期影响公司的产销能力和财务状况,决策正确与否影响公司的生存与发展。

完整的资本预算过程包括:寻找增长机会,制定长期投资战略,预测投资项目的现金流,分析评估投资项目,控制投资项目的执行情况。

资本预算可通过不同的资本预算方法来解决,如回收期法、净现值法和内部收益率法等。

2.货币市场(money markets)答:货币市场指期限不超过一年的资金借贷和短期有价证券交易的金融市场,亦称“短期金融市场”或“短期资金市场”,包括同业拆借市场、银行短期存贷市场、票据市场、短期证券市场、大额可转让存单市场、回购协议市场等。

其参加者为各种政府机构、各种银行和非银行金融机构及公司等。

货币市场具有四个基本特征:①融资期限短,一般在一年以内,最短的只有半天,主要用于满足短期资金周转的需要;②流动性强,金融工具可以在市场上随时兑现,交易对象主要是期限短、流动性强、风险小的信用工具,如票据、存单等,这些工具变现能力强,近似于货币,可称为“准货币”,故称货币市场;③安全性高,由于货币市场上的交易大多采用即期交易,即成交后马上结清,通常不存在因成交与结算日之间时间相对过长而引起价格巨大波动的现象,对投资者来说,收益具有较大保障;④政策性明显,货币市场由货币当局直接参加,是中央银行同商业银行及其他金融机构的资金连接的主渠道,是国家利用货币政策工具调节全国金融活动的杠杆支点。

货币市场的交易主体是短期资金的供需者。

需求者是为了获得现实的支付手段,调节资金的流动性并保持必要的支付能力,供应者提供的资金也大多是短期临时闲置性的资金。

Cha07罗斯公司理财第九版原版书课后习题

Cha07罗斯公司理财第九版原版书课后习题to abandon, and timing options.4. Decision trees represent an approach for valuing projects with these hidden, or real, options.Concept Questions1. Forecasting Risk What is forecasting risk? In general, would the degree of forecasting risk begreater for a new product or a cost-cutting proposal? Why?2. Sensitivity Analysis and Scenario Analysis What is the essential difference betweensensitivity analysis and scenario analysis?3. Marginal Cash Flows A coworker claims that looking at all this marginal this and incrementalthat is just a bunch of nonsense, and states, “Listen, if our average revenue doesn’t exceed our average cost, then we will have a negative cash flow, and we will go broke!” How do you respond?4. Break-Even Point As a shareholder of a firm that is contemplating a new project, would yoube more concerned with the accounting break-even point, the cash break-even point (the point at which operating cash flow is zero), or the financial break-even point? Why?5. Break-Even Point Assume a firm is considering a new project that requires an initialinvestment and has equal sales and costs over its life. Will the project reach the accounting, cash, or financial break-even point first? Which will it reach next? Last? Will this order always apply?6. Real Options Why does traditional NPV analysis tend to underestimate the true value of acapital budgeting project?7. Real Options The Mango Republic has just liberalized its markets and is now permittingforeign investors. Tesla Manufacturing has analyzed starting a project in the country and has determined that the project hasa negative NPV. Why might the company go ahead with the project? What type of option is most likely to add value to this project?8. Sensitivity Analysis and Breakeven How does sensitivity analysis interact with break-evenanalysis?9. Option to Wait An option can often have more than one source of value. Consider a loggingcompany. The company can log the timber today or wait another year (or more) to log the timber.What advantages would waiting one year potentially have?10. Project Analysis You are discussing a project analysis witha coworker. The project involvesreal options, such as expanding the project if successful, or abandoning the project if it fails. Your coworker makes the following statement: “This analysis is ridiculous. We looked at expanding or abandoning the project in two years, but there are many other options we should consider. For example, we could expand in one year, and expand further in two years. Or we could expand in one year, and abandon the project in two years. There are too many options for us to examine.Because of this, anything this analysis would give us is worthless.” How would you evaluate this statement? Considering that with any capital budgeting project there are an infinite number of real options, when do you stop the option analysis on an individual project?Questions and Problems: connect?BASIC (Questions 1–10)1. Sensitivity Analysis and Break-Even Point We are evaluating a project that costs$724,000, has an eight-year life, and has no salvage value. Assume that depreciation is straight-line to zero over the life of the project. Sales are projected at 75,000 units per year. Price per unit is $39, variable cost per unit is $23, and fixed costs are $850,000 per year. The tax rate is 35 percent, and we require a 15 percent return on this project.1. Calculate the accounting break-even point.2. Calculate the base-case cash flow and NPV. What is the sensitivity of NPV to changes inthe sales figure? Explain what your answer tells you about a 500-unit decrease in projected sales.3. What is the sensitivity of OCF to changes in the variable cost figure? Explain what youranswer tells you about a $1 decrease in estimated variable costs.2. Scenario Analysis In the previous problem, suppose the projections given for price, quantity,variable costs, and fixed costs are all accurate to w ithin ±10 percent. Calculate the best-case and worst-case NPV figures.3. Calculating Breakeven In each of the following cases, find the unknown variable. Ignoretaxes.4. Financial Breakeven L.J.’s Toys Inc. just purchased a $250,000 machine to produce toy cars.The machine will be fully depreciated by the straight-line method over its five-year economic life.Each toy sells for $25. The variable cost per toy is $6, and the firm incurs fixed costs of $360,000 each year. The corporate tax rate for the company is 34 percent. The appropriate discount rate is12 percent. What is the financial break-even point for the project?5. Option to Wait Your company is deciding whether to invest in a new machine. The newmachine will increase cash flow by $340,000 per year. You believe the technology used in the machine has a 10-year life; in other words, no matter when you purchase the machine, it will be obsolete 10 years from today. The machine is currently priced at $1,800,000. The cost of the machine will decline by $130,000 per year until it reaches $1,150,000, where it will remain. If your required return is 12 percent, should you purchase the machine? If so, when should you purchase it?6. Decision Trees Ang Electronics, Inc., has developed a new DVDR. If the DVDR is successful,the present value of the payoff (when the product is brought to market) is $22 million. If the DVDR fails, the present value of the payoff is $9 million. If the product goes directly to market, there is a50 percent chance of success. Alternatively, Ang can delay the launch by one year and spend $1.5million to test market the DVDR. Test marketing would allow the firm to improve the product and increase the probability of success to 80 percent. The appropriate discount rate is 11 percent.Should the firm conduct test marketing?7. Decision Trees The manager for a growing firm is considering the launch of a new product. Ifthe product goes directly to market, there is a 50 percent chance of success. For $135,000 the manager can conduct a focus group that will increase the product’s chance of success to 65 percent. Alternatively, the manager has the option to pay a consulting firm $400,000 to research the market and refine the product. The consulting firm successfully launches new products 85 percent of the time. If the firm successfully launches the product, the payoff will be $1.5 million. If the product is a failure, the NPV is zero. Which action will result in the highest expected payoff to the firm?8. Decision Trees B&B has a new baby powder ready to market. If the firm goes directly to themarket with the product, there is only a 55 percent chance of success. However, the firm can conduct customer segment research, which will take a year and cost $1.8 million. By going through research, B&B will be able to better target potential customers and will increase the probability of success to 70 percent. If successful, the baby powder will bring a present value profit (at time of initial selling) of $28 million. If unsuccessful, the present value payoff is only $4 million. Should the firm conduct customer segment research or go directly to market? The appropriate discount rate is15 percent.9. Financial Break-Even Analysis You are considering investing in a company that cultivatesabalone for sale to local restaurants. Use the following information:The discount rate for the company is 15 percent, the initial investment in equipment is $360,000, and the project’s economic life is seven years. Assume the equipment is depreciated on a straight-line basis over the project’s life.1. What is the accounting break-even level for the project?2. What is the financial break-even level for the project?10. Financial Breakeven Niko has purchased a brand new machine to produce its High Flight lineof shoes. The machine has an economic life of five years. The depreciation schedule for the machine is straight-line with no salvage value. The machine costs $390,000. The sales price per pair of shoes is $60, while the variable cost is $14. $185,000 of fixed costs per year are attributed to the machine. Assume that the corporate tax rate is 34 percent and the appropriate discount rate is 8 percent. What is the financial break-even point?INTERMEDIATE (Questions 11–25)11. Break-Even Intuition Consider a project with a required return of R percent that costs $I andwill last for N years. The project uses straight-line depreciation to zero over the N-year life; there are neither salvage value nor net working capital requirements.1. At the accounting break-even level of output, what is the IRR of this project? The paybackperiod? The NPV?2. At the cash break-even level of output, what is the IRR of this project? The paybackperiod? The NPV?3. At the financial break-even level of output, what is the IRR of this project? The paybackperiod? The NPV?12. Sensitivity Analysis Consider a four-year project with the following information: Initial fixedasset investment = $380,000; straight-line depreciation to zero over the four-year life; zero salvage value; price = $54; variable costs = $42; fixed costs = $185,000; quantity sold = 90,000 units; tax rate = 34 percent. How sensitive is OCF to changes in quantity sold?13. Project Analysis You are considering a new product launch. The project will cost $960,000,have a four-year life, and have no salvage value; depreciation is straight-line to zero. Sales are projected at 240 units per year; price per unit will be $25,000; variable cost per unit will be $19,500; and fixed costs will be $830,000 per year. The required return on the project is 15 percent, and the relevant tax rate is 35 percent.1. Based on your experience, you think the unit sales, variable cost, and fixed costprojections given here are probably accurate to within ±10 percent. What are the upper and lower bounds for these projections? What is the base-case NPV? What are the best-case and worst-case scenarios?2. Evaluate the sensitivity of your base-case NPV to changes in fixed costs.3. What is the accounting break-even level of output for this project?14. Project Analysis McGilla Golf has decided to sell a newline of golf clubs. The clubs will sell for$750 per set and have a variable cost of $390 per set. The company has spent $150,000 for a marketing study that determined the company will sell 55,000 sets per year for seven years. The marketing study also determined that the company will lose sales of 12,000 sets of its high-priced clubs. The high-priced clubs sell at $1,100 and have variable costs of $620. The company will also increase sales of its cheap clubs by 15,000 sets. The cheap clubs sell for $400 and have variable costs of $210 per set. The fixed costs each year will be $8,100,000. The company has also spent $1,000,000 on research and development for the new clubs. The plant and equipment required will cost $18,900,000 and will be depreciated on a straight-line basis. The new clubs will also require an increase in net working capital of $1,400,000 that will be returned at the end of the project. The tax rate is 40 percent, and the cost of capital is 14 percent. Calculate the payback period, the NPV, and the IRR.15. Scenario Analysis In the previous problem, you feel that the values are accurate to withinonly ±10 percent. What are the best-case and worst-case NPVs? (Hint: The price and variable costs for the two existing sets of clubs are known with certainty; only the sales gained or lost are uncertain.)16. Sensitivity Analysis McGilla Golf would like to know the sensitivity of NPV to changes in theprice of the new clubs and the quantity of new clubs sold. What is the sensitivity of the NPV to each of these variables?17. Abandonment Value We are examining a new project. We expect to sell 9,000 units per yearat $50 net cash flow apiece for the next 10 years. In otherwords, the annual operating cash flow is projected to be $50 × 9,000 = $450,000. The relevant discount rate is 16 percent, and the initial investment required is $1,900,000.1. What is the base-case NPV?2. After the first year, the project can be dismantled and sold for $1,300,000. If expectedsales are revised based on the first year’s performance, when would it make sense to abandon the investment? In other words, at what level of expected sales would it make sense to abandon the project?3. Explain how the $1,300,000 abandonment value can be viewed as the opportunity cost ofkeeping the project in one year.18. Abandonment In the previous problem, suppose you think it is likely that expected sales willbe revised upward to 11,000 units if the first year is a success and revised downward to 4,000 units if the first year is not a success.1. If success and failure are equally likely, what is the NPV of the project? Consider thepossibility of abandonment in answering.2. What is the value of the option to abandon?19. Abandonment and Expansion In the previous problem, suppose the scale of the project canbe doubled in one year in the sense that twice as many units can be produced and sold. Naturally, expansion would be desirable only if the project were a success. This implies that if the project is a success, projected sales after expansion will be 22,000. Again assuming that success and failure are equally likely,what is the NPV of the project? Note that abandonment is still an option if the project is a failure. What is the value of the option to expand?20. Break-Even Analysis Your buddy comes to you with a sure-fire way to make some quickmoney and help pay off your student loans. His idea is to sell T-shirts with the words “I get” on them. “You get it?” He says, “You see all those bumper stickers and T-shirts that say ‘got milk’ or ‘got surf.’ So this says, ‘I get.’ It’s funn y! All we have to do is buy a used silk screen press for $3,200 and we are in business!” Assume there are no fixed costs, and you depreciate the $3,200 in the first period. Taxes are 30 percent.1. What is the accounting break-even point if each shirt costs $7 to make and you can sellthem for $10 apiece?Now assume one year has passed and you have sold 5,000 shirts! You find out that the Dairy Farmers of America have copyrighted the “got milk” slogan and are requiring you to pay $12,000 to continue operations. You expect this craze will last for another three years and that your discount rate is 12 percent.2. What is the financial break-even point for your enterprise now?21. Decision Trees Young screenwriter Carl Draper has just finished his first script. It has action,drama, and humor, and he thinks it will be a blockbuster. He takes the script to every motion picture studio in town and tries to sell it but to no avail. Finally, ACME studios offers to buy the script for either (a) $12,000 or (b) 1 pe rcent of the movie’s profits. There are two decisions the studio will have to make. First is to decide if the script is good or bad, and second if the movieis good or bad. First, there is a 90 percent chance that the script is bad. If it is bad, the studio does nothing more and throws the script out. If the script is good, they will shoot the movie. After the movie is shot, the studio will review it, and there is a 70 percent chance that the movie is bad. If the movie is bad, the movie will not be promoted and will not turn a profit. If the movie is good, the studio will promote heavily; the average profit for this type of movie is $20 million. Carl rejects the $12,000 and says he wants the 1 percent of profits. Was this a good decision by Carl?22. Option to Wait Hickock Mining is evaluating when to open a gold mine. The mine has 60,000ounces of gold left that can be mined, and mining operations will produce 7,500 ounces per year.The required return on the gold mine is 12 percent, and it will cost $14 million to open the mine.When the mine is opened, the company will sign a contract that will guarantee the price of gold for the remaining life of the mine. If the mine is opened today, each ounce of gold will generate an aftertax cash flow of $450 per ounce. If the company waits one year, there is a 60 percent probability that the contract price will generate an aftertax cash flow of $500 per ounce and a 40 percent probability that the aftertax cash flow will be $410 per ounce. What is the value of the option to wait?23. Abandonment Decisions Allied Products, Inc., is considering a new product launch. The firmexpects to have an annual operating cash flow of $22 million for the next 10 years. Allied Products uses a discount rate of 19 percent for new product launches. The initial investment is $84 million.Assume that the project has no salvage value at the end of its economic life.1. What is the NPV of the new product?2. After the first year, the project can be dismantled and sold for $30 million. If theestimates of remaining cash flows are revised based on the first year’s experience, at what level of expected cash flows does it make sense to abandon the project?24. Expansion Decisions Applied Nanotech is thinking about introducing a new surface cleaningmachine. The marketing department has come up with the estimate that Applied Nanotech can sell15 units per year at $410,000 net cash flow per unit for the next five years. The engineeringdepartment has come up with the estimate that developing the machine will take a $17 million initial investment. The finance department has estimated that a 25 percent discount rate should beused.1. What is the base-case NPV?2. If unsuccessful, after the first year the project can be dismantled and will have an aftertaxsalvage value of $11 million. Also, after the first year, expected cash flows will be revised up to 20 units per year or to 0 units, with equal probability. What is the revised NPV?25. Scenario Analysis You are the financial analyst for a tennis racket manufacturer. Thecompany is considering using a graphitelike material in its tennis rackets. The company has estimated the information in the following table about the market for a racket with the newmaterial. The company expects to sell the racket for six years. The equipment required for the project has no salvage value. The required return for projects of this type is 13 percent, and the company has a 40 percent tax rate. Should you recommend the project?CHALLENGE (Questions 26–30)26. Scenario Analysis Consider a project to supply Detroit with 55,000 tons of machine screwsannually for automobile production. You will need an initial $1,700,000 investment in threading equipment to get the project started; the project will last for five years. The accounting department estimates that annual fixed costs will be $520,000 and that variable costs should be $220 per ton;accounting will depreciate the initial fixed asset investment straight-line to zero over the five-year project life. It also estimates a salvage value of $300,000 after dismantling costs. The marketing department estimates that the automakers will let the contract at a selling price of $245 per ton.The engineering department estimates you will need an initial net working capital investment of $600,000. You require a 13 percent return and face a marginal tax rate of 38 percent on this project.1. What is the estimated OCF for this project? The NPV? Should you pursue this project?2. Suppose you believe that the accounting department’sinitial cost and salvage valueprojections are accurate only to within ±15 percent; the marketing department’s price estimate is accurate only to within ±10 percent; and the engineering department’s net working capital estimate is accurate only to within ±5 p ercent. What is your worst-case scenario for this project? Your best-case scenario? Do you still want to pursue the project? 27. Sensitivity Analysis In Problem 26, suppose you’re confident about your own projections, butyou’re a little unsure about Detroit’s actual machine screw requirements. What is the sensitivity of the project OCF to changes in the quantity supplied? What about the sensitivity of NPV to changes in quantity supplied? Given the sensitivity number you calculated, is there some minimum level of output below which you wouldn’t want to operate? Why?28. Abandonment Decisions Consider the following project for Hand Clapper, Inc. The companyis considering a four-year project to manufacture clap-command garage door openers. This project requires an initial investment of $10 million that will be depreciated straight-line to zero over the project’s life. An initial investment in net working capital of $1.3 million is required to support spare parts inventory; this cost is fully recoverable whenever the project ends. The company believes it can generate $7.35 million in pretax revenues with $2.4 million in total pretax operating costs. The tax rate is 38 percent, and the discount rate is 16 percent. The market value of the equipment over the life of the project is as follows:Lumber is sold by the company for its “pond value.” Pond value is the amount a mill will pay for a log delivered to the mill location. The price paid for logs delivered to a mill is quoted in dollars per thousands of board feet (MBF), and the price depends on the grade of the logs. The forest Bunyan Lumber is evaluatingwas planted by the company 20 years ago and is made up entirely of Douglas fir trees. The table here shows the current price per MBF for the three grades of timber the company feels will come from the stand:Steve believes that the pond value of lumber will increase at the inflation rate. The company is planning to thin the forest today, and it expects to realize a positive cash flow of $1,000 per acre from thinning. The thinning is done to increase the growth rate of the remaining trees, and it is always done 20 years following a planting.The major decision the company faces is when to log the forest. When the company logs the forest, it will immediately replant saplings, which will allow for a future harvest. The longer the forest is allowed to grow, the larger the harvest becomes per acre. Additionally, an older forest has a higher grade of timber. Steve has compiled the following table with the expected harvest per acre in thousands of board feet, along with the breakdown of the timber grades:The company expects to lose 5 percent of the timber it cuts due to defects and breakage.The forest will be clear-cut when the company harvests the timber. This method of harvesting allows for faster growth of replanted trees. All of the harvesting, processing, replanting, andtransportation are to be handled by subcontractors hired by Bunyan Lumber. The cost of the logging is expected to be $140 per MBF. A road system has to be constructed and is expected to cost $50 per MBF on average. Sales preparation and administrative costs, excluding office overhead costs, are expected to be $18 per MBF.As soon as the harvesting is complete, the company will reforest the land. Reforesting costs include the following:All costs are expected to increase at the inflation rate.Assume all cash flows occur at the year of harvest. For example, if the company begins harvesting the timber 20 years from today, the cash flow from the harvest will be received 20 years from today. When the company logs the land, it will immediately replant the land with new saplings. The harvest period chosen will be repeated for the foreseeable future. The company’s nominal required return is 10 percent, and the inflation rate is expected to be 3.7 percent per year. Bunyan Lumber has a 35 percent tax rate.Clear-cutting is a controversial method of forest management. To obtain the necessary permits, Bunyan Lumber has agreed to contribute to a conservation fund every time it harvests the lumber. If the company harvested the forest today, the required contribution would be $250,000. The company has agreed that the required contribution will grow by 3.2 percent per year. When should the company harvest the forest?。

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](租赁)【圣才出品】

【圣才出品】](https://img.taocdn.com/s3/m/8bebf6679ec3d5bbfc0a748a.png)

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解]第21章租赁21.1复习笔记租赁是承租人和出租人之间的一项契约性协议。

协议中规定承租人拥有使用租赁资产的权利,同时必须定期向资产的所有者——出租人支付租金。

租赁既有短期租赁,也有长期租赁,本章主要是关于租赁期限长于5年的长期租赁。

1.租赁租赁是指出租人以收取租金为条件,在契约或合同规定的期限内,将资产租借给承租人使用的一种经济行为。

租赁行为在实质上具有借贷属性,不过它直接涉及的是实物而不是钱。

在租赁业务中,出租人主要是各种专业租赁公司,承租人主要是其他各类企业,租赁物大多为设备等固定资产。

2.租赁的分类(1)融资租赁。

融资租赁是指由租赁公司按照承租企业的要求购买设备,并在契约或合同规定的较长期限内提供给承租企业使用的信用性业务,也称为资本租赁、财务租赁。

它是现代租赁的主要类型。

承租企业采用融资租赁的主要目的是为了融通资金。

一般融资的对象是资金,而融资租赁集融资与租赁于一身,具有借贷性质,是承租企业筹集长期资金的一种特殊方式。

融资租赁要有三方当事人(出租人、承租人和出卖人)参与,通常由两个合同(融资租赁合同、买卖合同)或者两个以上合同构成,其内容是融资,表现形式是融物。

融资租赁的形式包括直接租赁、售后租回和杠杆租赁三种。

固定资产租赁业务如具有下列情况之一,通常确认为融资租赁:①在租赁期满时,资产的所有权由出租人转让给承租人;②承租人有廉价购买选择权;③租赁期为资产使用年限的大部分(如75%以上);④租赁开始日租赁应付款的现值之和不小于租赁资产的公允价值。

(2)经营租赁。

经营租赁是指由出租人向承租企业提供租赁设备,并提供设备维修保养和人员培训等服务性业务,也称为营运租赁、服务租赁。

经营租赁通常为短期租赁。

承租企业采用经营租赁的目的,主要不在于融通资本,而是获得设备的短期使用和出租人提供的专门技术服务。

从承租企业无须先筹资再购买设备即可享有设备使用权的角度来看,经营租赁也有短期筹资的作用。

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解-第8篇理财专题【圣才出品】

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解-第8篇理财专题【圣才出品】第8篇理财专题第29章收购、兼并与剥离29.1 复习笔记企业间的并购是一项充满不确定性的投资活动。

在并购决策中必须运用的基本法则是:当一家企业能够为并购企业的股东带来正的净现值时才会被并购。

因此确定目标企业的净现值显得尤为重要。

并购具有以下几个特点:并购活动产生的收益被称作协同效应;并购活动涉及复杂的会计、税收和法律因素;并购是股东可行使的一种重要控制机制;并购分析通常以计算并购双方的总价值为中心;并购有时涉及非善意交易。

1.收购的基本形式收购是指一个公司(收购方)用现金、债券或股票购买另一家公司的部分或全部资产或股权,从而获得对该公司的控制权的经济活动。

收购的对象一般有两种:股权和资产。

企业可以运用以下三种基本法律程序进行收购,即:①吸收合并或新设合并;②收购股票;③收购资产。

吸收合并是指一家企业被另一家企业吸收,兼并企业保持其名称和身份,并且收购被兼并企业的全部资产和负债的收购形式。

吸收合并的目标企业不再作为一个独立经营实体而存在。

新设合并是指兼并企业和被兼并企业终止各自的法人形式,共同组成一家新的企业。

收购股票是指用现金、股票或其他证券购买目标企业具有表决权的股票。

2.并购的分类兼并通常是指一个公司以现金、证券或其他形式购买取得其他公司的产权,使其他公司丧失法人资格或改变法人实体,并取得对这些企业决策控制权的经济行为。

兼并和收购虽然有很多不同,但也存在不少相似之处:①兼并与收购的基本动因相似。

要么为扩大企业的市场占有率;要么为扩大企业生产规模,实现规模经营;要么为拓宽企业经营范围,实现分散经营或综合化经营。

总之,企业兼并或收购都是增强企业实力的外部扩张策略或途径。

②企业兼并与收购都以企业产权交易为对象,都是企业资本营运的基本方式。

正是由于两者有很多相似之处,现实中,两者通常统称为“并购”。

按照并购双方的业务性质可以分为:(1)横向并购。

罗斯《公司理财》(第9版)配套题库【课后习题-会计报表与现金流量】

第2章会计报表与现金流量一、概念题1.资产负债表(balance sheet)答:资产负债表指反映企业某一特定日期财务状况的会计报表。

它是根据资产、负债和所有者权益之间的相互关系,按照一定的分类标准和一定的顺序,把企业一定日期的资产、负债和所有者权益各项目予以适当排列,并对日常会计核算工作中形成的大量数据进行高度浓缩整理后编制而成的。

资产负债表是企业最重要的对外报表之一,它能为投资者和企业管理当局提供有关企业的资源分布状况、债权人和股东对资产的要求权、企业的偿债能力和未来财务状况趋势等信息。

资产负债表的格式主要有账户式和垂直式两种,当前会计实务中采用较多的是账户式资产负债表。

账户式资产负债表分左右两方列示,左边列示企业的资产,右边列示负债和所有者权益,左右两方的合计数相等。

通常,资产负债表还提供期初数和期末数的比较资料。

2.损益表(income statement)答:损益表是指反映一个企业某一会计期间经营成果的会计报表,亦称“利润表”或“收益表”。

它把一定期间的收入与相关的费用进行配比,从而计算出企业一定期间的净利润(或净亏损)。

它反映企业生产经营的收入实现和成本耗费情况,表明企业的生产经营成果。

同时,通过该表提供不同时期的比较数字(如本月数、本年累计数、上年数),可以分析企业今后利润的发展趋势和获利能力。

损益表的结果可以分为多步式和单步式两种。

多步式损益表中的损益是通过多步配比而来的。

单步式损益表则是将本期所有的收入加在一起,然后将所有的费用加总在一起,通过一次配比求出本期损益。

3.现金流量(cash flow)答:现金流量是指某一段时期内企业现金流入和流出的数量。

如企业销售商品、提供劳务、出售固定资产、向银行借款等取得现金,形成企业的现金流入;购买原材料、接受劳务、购建固定资产、对外投资、偿还债务等而支付现金,形成企业的现金流出。

现金流量信息能够表明企业经营状况是否良好、资金是否紧缺、企业偿付能力大小,从而为投资者、债权人、企业管理者提供非常有用的信息。

罗斯公司理财第九版课后习题答案中文版

第一章1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢?”5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。

7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。

较少的私人投资者能减少不同的企业目标。

高比重的机构所有权导致高学历的股东和管理层讨论决策风险项目。

此外,机构投资者比私人投资者可以根据自己的资源和经验更好地对管理层实施有效的监督机制。

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](股票估值)【圣才出品】

【圣才出品】](https://img.taocdn.com/s3/m/e1dcbc711fb91a37f111f18583d049649b660eea.png)

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](股票估值)【圣才出品】罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解]第9章股票估值9.1复习笔记1.不同类型股票的估值(1)零增长股利股利不变时,一股股票的价格由下式给出:在这里假定Div1=Div2=…=Div。

(2)固定增长率股利如果股利以恒定的速率增长,那么一股股票的价格就为:式中,g是增长率;Div是第一期期末的股利。

(3)变动增长率股利2.股利折现模型中的参数估计(1)对增长率g的估计有效估计增长率的方法是:g=留存收益比率×留存收益收益率(ROE)只要公司保持其股利支付率不变,g就可以表示公司的股利增长率以及盈利增长率。

(2)对折现率R的估计对于折现率R的估计为:R=Div/P0+g该式表明总收益率R由两部分组成。

其中,第一部分被称为股利收益率,是预期的现金股利与当前的价格之比。

3.增长机会每股股价可以写做:该式表明,每股股价可以看做两部分的加和。

第一部分(EPS/R)是当公司满足于现状,而将其盈利全部发放给投资者时的价值;第二部分是当公司将盈利留存并用于投资新项目时的新增价值。

当公司投资于正NPVGO的增长机会时,公司价值增加。

反之,当公司选择负NPVGO 的投资机会时,公司价值降低。

但是,不管项目的NPV是正的还是负的,盈利和股利都是增长的。

不应该折现利润来获得每股价格,因为有部分盈利被用于再投资了。

只有股利被分到股东手中,也只有股利可以加以折现以获得股票价格。

4.市盈率即股票的市盈率是三个因素的函数:(1)增长机会。

拥有强劲增长机会的公司具有高市盈率。

(2)风险。

低风险股票具有高市盈率。

(3)会计方法。

采用保守会计方法的公司具有高市盈率。

5.股票市场交易商:持有一项存货,然后准备在任何时点进行买卖。

经纪人:将买者和卖者撮合在一起,但并不持有存货。

9.2课后习题详解一、概念题1.股利支付率(payout ratio)答:股利支付率一般指公司发放给普通股股东的现金股利占总利润的比例。

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](跨国公司财务)【圣才出品】

【圣才出品】](https://img.taocdn.com/s3/m/3a7d4c63eefdc8d376ee32ab.png)

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解]第31章跨国公司财务31.1复习笔记随着经济全球化的发展,跨国公司越来越多。

跨国公司经营必须考虑各种因素,其中包括外币汇率、各国不同的利率、国外经营所用的复杂会计方法、外国税率和外国政府的干涉等等。

公司财务的基本原理仍然适用于跨国公司。

外汇问题是跨国财务中最重要、最复杂的难题。

当跨国公司进行资本预算决策或融资决策时,外汇市场能为其提供信息和机会。

外汇、利率和通货膨胀三者的相互关系构成了汇率基本理论。

即:购买力平价理论、利率平价理论和预期理论。

跨国公司融资决策通常有以下三种基本途径:将本国货币用于国外经营业务、向投资所在国借贷和向第三国借贷。

三种途径各有优缺点。

1.有关专业术语(1)美国存托凭证(ADR)。

美国存托凭证是指在美国发行的一种代表外国股权的证券。

外国公司运用以美元发行的ADR实现外国股票在美国上市交易,来吸引更多的潜在的美国投资者群体。

这些ADR通常由投资银行持有并为其做市,它以两种形式存在:一是在交易所挂牌交易的ADR,称为公司保荐形式;另一种是非保荐形式。

这两种形式的ADR均可由个人投资和买卖。

ADR解决了美国与国外证券交易制度、惯例、语言、外汇管理等不尽相同所造成的交易上的困难,是外国公司在美国市场上筹资的重要金融工具,同时也是美国投资者最广泛接受的外国证券形式。

(2)交叉汇率。

交叉汇率是指两种货币之间(通常都不是美元)通过第三种货币联系起来的汇率。

美元是决定交叉汇率的中介货币。

例如,如果投资者想卖出日元买进瑞士法郎,他可能先卖出日元买入美元,随后又卖出美元买入瑞士法郎。

所以,虽然该交易只涉及日元与瑞士法郎,但是美元汇率起到了基准作用。

(3)欧洲货币单位。

欧洲货币单位是指1979年设计的由10种欧洲货币组成的一揽子货币,它是欧洲货币体系(EMS)的货币单位。

根据章程,EMS成员国每五年或者当出现某种货币权重发生25%或以上的变动时,都要重新估算一次ECU的组成。

罗斯《公司理财》(第9版)课后习题(第16~18章)【圣才出品】

罗斯《公司理财》(第9版)课后习题第16章资本结构:基本概念一、概念题1.馅饼模型(pie model)答:馅饼模型是一种分析公司资本结构的模型,用来讨论公司应如何选择负债权益比的问题。

该理论将公司的筹资要求权之和比作一个馅饼,并且将公司的价值定义为负债和所有者权益之和。

该理论认为,债权人和股东将分别得到不同大小的馅饼块,但是整个馅饼的大小,也就是公司的实际价值,却完全不会受到馅饼分割方式的影响。

也就是说,公司的融资结构只影响公司利润的分配方式,即这个利润馅饼如何被分割以及由谁承担公司的风险,不会对公司的价值造成任何影响。

2.MM命题Ⅰ(MM Proposition I)答:不考虑公司所得税情况下的MM命题Ⅰ指的是,公司的价值取决于未来经营活动净收益的资本化程度,资本化率与公司的风险相一致。

这一命题有两个直接推论:a.公司的平均资本成本与公司资本结构无关;b.公司的平均资本成本等于与之风险相同的零举债公司的资本化率。

3.MM命题Ⅱ(MM Proposition II)答:不考虑公司所得税情况下的MM命题Ⅱ指的是,举债经营公司的权益资本成本等于零举债经营公司的权益资本成本加上风险报酬率。

风险报酬率的多少取决于公司举债经营的程度。

命题二表明,随着公司负债的增加,公司的权益资本成本也将提高。

4.MM命题Ⅰ(公司税)[MM Proposition I(corporate taxes)]答:MM命题一,零举债经营公司的价值是公司税后经营收益除以公司权益资本成本所得的结果,而举债经营公司的价值等于同类风险的零举债经营公司的价值加上税款节余额。

根据这一结论,当公司负债增加时,举债经营公司价值增加较快。

特别地,当公司负债筹资的比重为100%时,公司的价值最大。

5.MM命题Ⅱ(公司税)[MM Proposition II(corporate taxes)]答:MM命题二,举债公司的权益资本成本等于同类风险零举债经营公司的权益资本成本加上风险报酬率,而风险报酬率又取决于公司资本结构和公司所得税税率。

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](公司理财导论)【圣才出品】

【圣才出品】](https://img.taocdn.com/s3/m/b63331b352d380eb62946dff.png)

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解]第1章公司理财导论[视频讲解]1.1复习笔记公司的首要目标——股东财富最大化决定了公司理财的目标。

公司理财研究的是稀缺资金如何在企业和市场内进行有效配置,它是在股份有限公司已成为现代企业制度最主要组织形式的时代背景下,就公司经营过程中的资金运动进行预测、组织、协调、分析和控制的一种决策与管理活动。

从决策角度来讲,公司理财的决策内容包括投资决策、筹资决策、股利决策和净流动资金决策;从管理角度来讲,公司理财的管理职能主要是指对资金筹集和资金投放的管理。

公司理财的基本内容包括:投资决策(资本预算)、融资决策(资本结构)、短期财务管理(营运资本)。

1.资产负债表资产负债表是总括反映企业某一特定日期财务状况的会计报表,它是根据资产、负债和所有者权益之间的相互关系,按照一定的分类标准和一定的顺序,把企业一定日期的资产、负债和所有者权益各项目予以适当排列,并对日常工作中形成的大量数据进行高度浓缩整理后编制而成的。

资产负债表可以反映资本预算、资本支出、资本结构以及经营中的现金流量管理等方面的内容。

2.资本结构资本结构是指企业各种资本的构成及其比例关系,它有广义和狭义之分。

广义资本结构,亦称财务结构,指企业全部资本的构成,既包括长期资本,也包括短期资本(主要指短期债务资本)。

狭义资本结构,主要指企业长期资本的构成,而不包括短期资本。

通常人们将资本结构表示为债务资本与权益资本的比例关系(D/E)或债务资本在总资本的构成(D/A)。

准确地讲,企业的资本结构应定义为有偿负债与所有者权益的比例。

资本结构是由企业采用各种筹资方式筹集资本形成的。

筹资方式的选择及组合决定着企业资本结构及其变化。

资本结构是企业筹资决策的核心问题。

企业应综合考虑影响资本结构的因素,运用适当方法优化资本结构,从而实现最佳资本结构。

资本结构优化有利于降低资本成本,获取财务杠杆利益。

3.财务经理财务经理是公司管理团队中的重要成员,其主要职责是通过资本预算、融资和资产流动性管理为公司创造价值。

罗斯《公司理财》(第9版)课后习题(第22~24章)【圣才出品】

罗斯《公司理财》(第9版)课后习题第22章期权与公司理财一、概念题1.期权(option)答:期权是指在预先约定的日期,以事先确定的价格买卖某种特定商品、金融工具或相关期货合约的权利。

期权实质上是一种选择权,其交易是一种权利的买卖。

期权对于买方来说,只是一种权利,即拥有在一定时间内以一定价格出售或购买一定数量的商品、金融工具或相关期货合约的权利,不承担必须买进或卖出的义务,其损失为购买期权的费用。

对于期权的卖方来说,由于收取了期权费,则须承担到期时或到期前由买方所选择的交割履约义务和责任。

其固定收益为期权费,而损失则是不确定的。

期权价格的变动是以其基础商品、金融工具或相关期货价格的变动为基础的。

其变动规律是:基础期货价格上涨时,买进期权的价格上涨,而卖出期权的价格下跌;反之,当基础期货价格下跌时,买进期权的价格下跌,而卖出期权的价格上涨。

期权按照交易性质可分为看涨期权(买入期权)、看跌期权(卖出期权)和双重期权三种类型;按照履约期限可分为美式期权和欧式期权。

2.美式期权(American options)答:美式期权是指买入期权的一方在合约到期日前的任何工作日包括到期日当天都可以行使的期权,其结算日在履约日之后的一天或两天。

大多数的美式期权允许持有者在交易日到履约日之间随时履约,但也有一些合同规定一段比较短的时间可以履约,如“到期日前两周”。

3.买入期权(call option)答:买入期权又称“买方期权”、“看涨期权”、“多头期权”、“敲进”。

它是期权买方在合约到期日或有效期内按照预先敲定的交割价格从期权卖方手中买入某种金融资产或商品的权利,是期权交易的种类之一。

购买这种期权以人们预测市场价格将有上涨趋势为前提。

投资者在支付一定的期权费取得该种期权后,在合约到期日或到期日之前的有效期限内,若市场价格超过协定价格与期权费之和的水平,则可通过行使期权以协定价格买入合约规定的一定数量的金融资产或商品,再以市场价格卖出,从而获利。

《公司理财》罗斯中文第九版南大笔记

《公司理财》罗斯中文第九版南大笔记第一篇综述企业经营活动中三类不同的重要问题:1、资本预算问题(长期投资项目)2、融资:如何筹集资金?3、短期融资和净营运资本管理第一章公司理财导论1.1什么是公司理财?1.1.1资产负债表()流动资产固定资产有形无形流动负债长期负债+所有者权益++=+ 流动资产-流动负债净营运资本=短期负债:那些必须在一年之内必须偿还的代款和债务;长期负债:不必再一年之内偿还的贷款和债务。

资本结构:公司短期债务、长期债务和股东权益的比例。

1.1.2资本结构债权人和股东V(公司的价值)=B(负债的价值)+S(所有者权益的价值)如何确定资本结构将影响公司的价值。

1.1.3财务经理财务经理的大部分工作在于通过资本预算、融资和资产流动性管理为公司创造价值。

两个问题:1.现金流量的确认:财务分析的大量工作就是从会计报表中获得现金流量的信息(注意会计角度与财务角度的区别)2.现金流量的时点3.现金流量的风险1.2公司证券对公司价值的或有索取权负债的基本特征是借债的公司承诺在某一确定的时间支付给债权人一笔固定的金额。

债券和股票时伴随或依附于公司总价值的收益索取权。

1.3公司制企业1.3.1个体业主制 1.3.2合伙制 1.3.3公司制有限责任、产权易于转让和永续经营是其主要优点。

1.4公司制企业的目标公司制企业力图通过采取行动提高现有公司股票的价值以使股东财富最大化。

1.4.1代理成本和系列契约理论的观点代理成本:股东的监督成本和实施控制的成本 1.4.2管理者的目标管理者的目标可能不同于股东的目标。

Donaldson 提出的管理者的两大动机:① (组织的)生存;② 独立性和自我满足。

1.4.3所有权和控制权的分离——谁在经营企业?1.4.4股东应控制管理者行为吗?促使股东可以控制管理者的因素:① 股东通过股东大会选举董事;② 报酬计划和业绩激励计划;③被接管的危险;④ 经理市场的激烈竞争。

罗斯《公司理财》第9版精要版英文原书课后部分章节答案

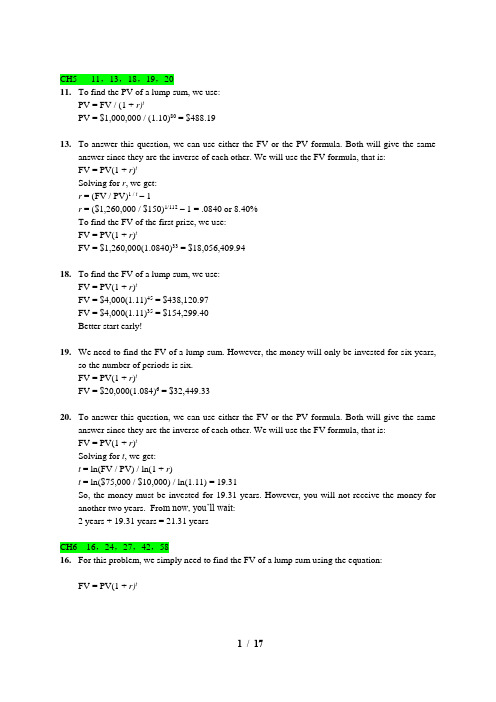

CH5 11,13,18,19,2011.To find the PV of a lump sum, we use:PV = FV / (1 + r)tPV = $1,000,000 / (1.10)80 = $488.1913.To answer this question, we can use either the FV or the PV formula. Both will give the sameanswer since they are the inverse of each other. We will use the FV formula, that is:FV = PV(1 + r)tSolving for r, we get:r = (FV / PV)1 / t– 1r = ($1,260,000 / $150)1/112– 1 = .0840 or 8.40%To find the FV of the first prize, we use:FV = PV(1 + r)tFV = $1,260,000(1.0840)33 = $18,056,409.9418.To find the FV of a lump sum, we use:FV = PV(1 + r)tFV = $4,000(1.11)45 = $438,120.97FV = $4,000(1.11)35 = $154,299.40Better start early!19. We need to find the FV of a lump sum. However, the money will only be invested for six years,so the number of periods is six.FV = PV(1 + r)tFV = $20,000(1.084)6 = $32,449.3320.To answer this question, we can use either the FV or the PV formula. Both will give the sameanswer since they are the inverse of each other. We will use the FV formula, that is:FV = PV(1 + r)tSolving for t, we get:t = ln(FV / PV) / ln(1 + r)t = ln($75,000 / $10,000) / ln(1.11) = 19.31So, the money must be invested for 19.31 years. However, you will not receive the money for another two years. Fro m now, you’ll wait:2 years + 19.31 years = 21.31 yearsCH6 16,24,27,42,5816.For this problem, we simply need to find the FV of a lump sum using the equation:FV = PV(1 + r)tIt is important to note that compounding occurs semiannually. To account for this, we will divide the interest rate by two (the number of compounding periods in a year), and multiply the number of periods by two. Doing so, we get:FV = $2,100[1 + (.084/2)]34 = $8,505.9324.This problem requires us to find the FVA. The equation to find the FVA is:FVA = C{[(1 + r)t– 1] / r}FVA = $300[{[1 + (.10/12) ]360 – 1} / (.10/12)] = $678,146.3827.The cash flows are annual and the compounding period is quarterly, so we need to calculate theEAR to make the interest rate comparable with the timing of the cash flows. Using the equation for the EAR, we get:EAR = [1 + (APR / m)]m– 1EAR = [1 + (.11/4)]4– 1 = .1146 or 11.46%And now we use the EAR to find the PV of each cash flow as a lump sum and add them together: PV = $725 / 1.1146 + $980 / 1.11462 + $1,360 / 1.11464 = $2,320.3642.The amount of principal paid on the loan is the PV of the monthly payments you make. So, thepresent value of the $1,150 monthly payments is:PVA = $1,150[(1 – {1 / [1 + (.0635/12)]}360) / (.0635/12)] = $184,817.42The monthly payments of $1,150 will amount to a principal payment of $184,817.42. The amount of principal you will still owe is:$240,000 – 184,817.42 = $55,182.58This remaining principal amount will increase at the interest rate on the loan until the end of the loan period. So the balloon payment in 30 years, which is the FV of the remaining principal will be:Balloon payment = $55,182.58[1 + (.0635/12)]360 = $368,936.5458.To answer this question, we should find the PV of both options, and compare them. Since we arepurchasing the car, the lowest PV is the best option. The PV of the leasing is simply the PV of the lease payments, plus the $99. The interest rate we would use for the leasing option is thesame as the interest rate of the loan. The PV of leasing is:PV = $99 + $450{1 – [1 / (1 + .07/12)12(3)]} / (.07/12) = $14,672.91The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV of the resale price is:PV = $23,000 / [1 + (.07/12)]12(3) = $18,654.82The PV of the decision to purchase is:$32,000 – 18,654.82 = $13,345.18In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is lower. To find the breakeven resale price, we need to find the resale price that makes the PV of the two options the same. In other words, the PV of the decision to buy should be:$32,000 – PV of resale price = $14,672.91PV of resale price = $17,327.09The resale price that would make the PV of the lease versus buy decision is the FV of this value, so:Breakeven resale price = $17,327.09[1 + (.07/12)]12(3) = $21,363.01CH7 3,18,21,22,313.The price of any bond is the PV of the interest payment, plus the PV of the par value. Notice thisproblem assumes an annual coupon. The price of the bond will be:P = $75({1 – [1/(1 + .0875)]10 } / .0875) + $1,000[1 / (1 + .0875)10] = $918.89We would like to introduce shorthand notation here. Rather than write (or type, as the case may be) the entire equation for the PV of a lump sum, or the PVA equation, it is common to abbreviate the equations as:PVIF R,t = 1 / (1 + r)twhich stands for Present Value Interest FactorPVIFA R,t= ({1 – [1/(1 + r)]t } / r )which stands for Present Value Interest Factor of an AnnuityThese abbreviations are short hand notation for the equations in which the interest rate and the number of periods are substituted into the equation and solved. We will use this shorthand notation in remainder of the solutions key.18.The bond price equation for this bond is:P0 = $1,068 = $46(PVIFA R%,18) + $1,000(PVIF R%,18)Using a spreadsheet, financial calculator, or trial and error we find:R = 4.06%This is the semiannual interest rate, so the YTM is:YTM = 2 4.06% = 8.12%The current yield is:Current yield = Annual coupon payment / Price = $92 / $1,068 = .0861 or 8.61%The effective annual yield is the same as the EAR, so using the EAR equation from the previous chapter:Effective annual yield = (1 + 0.0406)2– 1 = .0829 or 8.29%20. Accrued interest is the coupon payment for the period times the fraction of the period that haspassed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are four months until the next coupon payment, so two months have passed since the last coupon payment. The accrued interest for the bond is:Accrued interest = $74/2 × 2/6 = $12.33And we calculate the clean price as:Clean price = Dirty price – Accrued interest = $968 – 12.33 = $955.6721. Accrued interest is the coupon payment for the period times the fraction of the period that haspassed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are two months until the next coupon payment, so four months have passed since the last coupon payment. The accrued interest for the bond is:Accrued interest = $68/2 × 4/6 = $22.67And we calculate the dirty price as:Dirty price = Clean price + Accrued interest = $1,073 + 22.67 = $1,095.6722.To find the number of years to maturity for the bond, we need to find the price of the bond. Sincewe already have the coupon rate, we can use the bond price equation, and solve for the number of years to maturity. We are given the current yield of the bond, so we can calculate the price as: Current yield = .0755 = $80/P0P0 = $80/.0755 = $1,059.60Now that we have the price of the bond, the bond price equation is:P = $1,059.60 = $80[(1 – (1/1.072)t ) / .072 ] + $1,000/1.072tWe can solve this equation for t as follows:$1,059.60(1.072)t = $1,111.11(1.072)t– 1,111.11 + 1,000111.11 = 51.51(1.072)t2.1570 = 1.072tt = log 2.1570 / log 1.072 = 11.06 11 yearsThe bond has 11 years to maturity.31.The price of any bond (or financial instrument) is the PV of the future cash flows. Even thoughBond M makes different coupons payments, to find the price of the bond, we just find the PV of the cash flows. The PV of the cash flows for Bond M is:P M= $1,100(PVIFA3.5%,16)(PVIF3.5%,12) + $1,400(PVIFA3.5%,12)(PVIF3.5%,28) + $20,000(PVIF3.5%,40)P M= $19,018.78Notice that for the coupon payments of $1,400, we found the PVA for the coupon payments, and then discounted the lump sum back to today.Bond N is a zero coupon bond with a $20,000 par value, therefore, the price of the bond is the PV of the par, or:P N= $20,000(PVIF3.5%,40) = $5,051.45CH8 4,18,20,22,24ing the constant growth model, we find the price of the stock today is:P0 = D1 / (R– g) = $3.04 / (.11 – .038) = $42.2218.The price of a share of preferred stock is the dividend payment divided by the required return.We know the dividend payment in Year 20, so we can find the price of the stock in Year 19, one year before the first dividend payment. Doing so, we get:P19 = $20.00 / .064P19 = $312.50The price of the stock today is the PV of the stock price in the future, so the price today will be: P0 = $312.50 / (1.064)19P0 = $96.1520.We can use the two-stage dividend growth model for this problem, which is:P0 = [D0(1 + g1)/(R –g1)]{1 – [(1 + g1)/(1 + R)]T}+ [(1 + g1)/(1 + R)]T[D0(1 + g2)/(R –g2)]P0= [$1.25(1.28)/(.13 – .28)][1 – (1.28/1.13)8] + [(1.28)/(1.13)]8[$1.25(1.06)/(.13 – .06)]P0= $69.5522.We are asked to find the dividend yield and capital gains yield for each of the stocks. All of thestocks have a 15 percent required return, which is the sum of the dividend yield and the capital gains yield. To find the components of the total return, we need to find the stock price for each stock. Using this stock price and the dividend, we can calculate the dividend yield. The capital gains yield for the stock will be the total return (required return) minus the dividend yield.W: P0 = D0(1 + g) / (R–g) = $4.50(1.10)/(.19 – .10) = $55.00Dividend yield = D1/P0 = $4.50(1.10)/$55.00 = .09 or 9%Capital gains yield = .19 – .09 = .10 or 10%X: P0 = D0(1 + g) / (R–g) = $4.50/(.19 – 0) = $23.68Dividend yield = D1/P0 = $4.50/$23.68 = .19 or 19%Capital gains yield = .19 – .19 = 0%Y: P0 = D0(1 + g) / (R–g) = $4.50(1 – .05)/(.19 + .05) = $17.81Dividend yield = D1/P0 = $4.50(0.95)/$17.81 = .24 or 24%Capital gains yield = .19 – .24 = –.05 or –5%Z: P2 = D2(1 + g) / (R–g) = D0(1 + g1)2(1 + g2)/(R–g2) = $4.50(1.20)2(1.12)/(.19 – .12) = $103.68P0 = $4.50 (1.20) / (1.19) + $4.50 (1.20)2/ (1.19)2 + $103.68 / (1.19)2 = $82.33Dividend yield = D1/P0 = $4.50(1.20)/$82.33 = .066 or 6.6%Capital gains yield = .19 – .066 = .124 or 12.4%In all cases, the required return is 19%, but the return is distributed differently between current income and capital gains. High growth stocks have an appreciable capital gains component but a relatively small current income yield; conversely, mature, negative-growth stocks provide a high current income but also price depreciation over time.24.Here we have a stock with supernormal growth, but the dividend growth changes every year forthe first four years. We can find the price of the stock in Year 3 since the dividend growth rate is constant after the third dividend. The price of the stock in Year 3 will be the dividend in Year 4, divided by the required return minus the constant dividend growth rate. So, the price in Year 3 will be:P3 = $2.45(1.20)(1.15)(1.10)(1.05) / (.11 – .05) = $65.08The price of the stock today will be the PV of the first three dividends, plus the PV of the stock price in Year 3, so:P0 = $2.45(1.20)/(1.11) + $2.45(1.20)(1.15)/1.112 + $2.45(1.20)(1.15)(1.10)/1.113 + $65.08/1.113 P0 = $55.70CH9 3,4,6,9,153.Project A has cash flows of $19,000 in Year 1, so the cash flows are short by $21,000 ofrecapturing the initial investment, so the payback for Project A is:Payback = 1 + ($21,000 / $25,000) = 1.84 yearsProject B has cash flows of:Cash flows = $14,000 + 17,000 + 24,000 = $55,000during this first three years. The cash flows are still short by $5,000 of recapturing the initial investment, so the payback for Project B is:B: Payback = 3 + ($5,000 / $270,000) = 3.019 yearsUsing the payback criterion and a cutoff of 3 years, accept project A and reject project B.4.When we use discounted payback, we need to find the value of all cash flows today. The valuetoday of the project cash flows for the first four years is:Value today of Year 1 cash flow = $4,200/1.14 = $3,684.21Value today of Year 2 cash flow = $5,300/1.142 = $4,078.18Value today of Year 3 cash flow = $6,100/1.143 = $4,117.33Value today of Year 4 cash flow = $7,400/1.144 = $4,381.39To find the discounted payback, we use these values to find the payback period. The discounted first year cash flow is $3,684.21, so the discounted payback for a $7,000 initial cost is:Discounted payback = 1 + ($7,000 – 3,684.21)/$4,078.18 = 1.81 yearsFor an initial cost of $10,000, the discounted payback is:Discounted payback = 2 + ($10,000 – 3,684.21 – 4,078.18)/$4,117.33 = 2.54 yearsNotice the calculation of discounted payback. We know the payback period is between two and three years, so we subtract the discounted values of the Year 1 and Year 2 cash flows from the initial cost. This is the numerator, which is the discounted amount we still need to make to recover our initial investment. We divide this amount by the discounted amount we will earn in Year 3 to get the fractional portion of the discounted payback.If the initial cost is $13,000, the discounted payback is:Discounted payback = 3 + ($13,000 – 3,684.21 – 4,078.18 – 4,117.33) / $4,381.39 = 3.26 years6.Our definition of AAR is the average net income divided by the average book value. The averagenet income for this project is:Average net income = ($1,938,200 + 2,201,600 + 1,876,000 + 1,329,500) / 4 = $1,836,325And the average book value is:Average book value = ($15,000,000 + 0) / 2 = $7,500,000So, the AAR for this project is:AAR = Average net income / Average book value = $1,836,325 / $7,500,000 = .2448 or 24.48%9.The NPV of a project is the PV of the outflows minus the PV of the inflows. Since the cashinflows are an annuity, the equation for the NPV of this project at an 8 percent required return is: NPV = –$138,000 + $28,500(PVIFA8%, 9) = $40,036.31At an 8 percent required return, the NPV is positive, so we would accept the project.The equation for the NPV of the project at a 20 percent required return is:NPV = –$138,000 + $28,500(PVIFA20%, 9) = –$23,117.45At a 20 percent required return, the NPV is negative, so we would reject the project.We would be indifferent to the project if the required return was equal to the IRR of the project, since at that required return the NPV is zero. The IRR of the project is:0 = –$138,000 + $28,500(PVIFA IRR, 9)IRR = 14.59%15.The profitability index is defined as the PV of the cash inflows divided by the PV of the cashoutflows. The equation for the profitability index at a required return of 10 percent is:PI = [$7,300/1.1 + $6,900/1.12 + $5,700/1.13] / $14,000 = 1.187The equation for the profitability index at a required return of 15 percent is:PI = [$7,300/1.15 + $6,900/1.152 + $5,700/1.153] / $14,000 = 1.094The equation for the profitability index at a required return of 22 percent is:PI = [$7,300/1.22 + $6,900/1.222 + $5,700/1.223] / $14,000 = 0.983We would accept the project if the required return were 10 percent or 15 percent since the PI is greater than one. We would reject the project if the required return were 22 percent since the PI is less than one.CH10 9,13,14,17,18ing the tax shield approach to calculating OCF (Remember the approach is irrelevant; the finalanswer will be the same no matter which of the four methods you use.), we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = ($2,650,000 – 840,000)(1 – 0.35) + 0.35($3,900,000/3)OCF = $1,631,50013.First we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation = $560,000/5Annual depreciation = $112,000Now, we calculate the aftertax salvage value. The aftertax salvage value is the market price minus (or plus) the taxes on the sale of the equipment, so:Aftertax salvage value = MV + (BV – MV)t cVery often the book value of the equipment is zero as it is in this case. If the book value is zero, the equation for the aftertax salvage value becomes:Aftertax salvage value = MV + (0 – MV)t cAftertax salvage value = MV(1 – t c)We will use this equation to find the aftertax salvage value since we know the book value is zero.So, the aftertax salvage value is:Aftertax salvage value = $85,000(1 – 0.34)Aftertax salvage value = $56,100Using the tax shield approach, we find the OCF for the project is:OCF = $165,000(1 – 0.34) + 0.34($112,000)OCF = $146,980Now we can find the project NPV. Notice we include the NWC in the initial cash outlay. The recovery of the NWC occurs in Year 5, along with the aftertax salvage value.NPV = –$560,000 – 29,000 + $146,980(PVIFA10%,5) + [($56,100 + 29,000) / 1.105]NPV = $21,010.2414.First we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation charge = $720,000/5Annual depreciation charge = $144,000The aftertax salvage value of the equipment is:Aftertax salvage value = $75,000(1 – 0.35)Aftertax salvage value = $48,750Using the tax shield approach, the OCF is:OCF = $260,000(1 – 0.35) + 0.35($144,000)OCF = $219,400Now we can find the project IRR. There is an unusual feature that is a part of this project.Accepting this project means that we will reduce NWC. This reduction in NWC is a cash inflow at Year 0. This reduction in NWC implies that when the project ends, we will have to increase NWC. So, at the end of the project, we will have a cash outflow to restore the NWC to its level before the project. We also must include the aftertax salvage value at the end of the project. The IRR of the project is:NPV = 0 = –$720,000 + 110,000 + $219,400(PVIFA IRR%,5) + [($48,750 – 110,000) / (1+IRR)5]IRR = 21.65%17.We will need the aftertax salvage value of the equipment to compute the EAC. Even though theequipment for each product has a different initial cost, both have the same salvage value. The aftertax salvage value for both is:Both cases: aftertax salvage value = $40,000(1 – 0.35) = $26,000To calculate the EAC, we first need the OCF and NPV of each option. The OCF and NPV for Techron I is:OCF = –$67,000(1 – 0.35) + 0.35($290,000/3) = –9,716.67NPV = –$290,000 – $9,716.67(PVIFA10%,3) + ($26,000/1.103) = –$294,629.73EAC = –$294,629.73 / (PVIFA10%,3) = –$118,474.97And the OCF and NPV for Techron II is:OCF = –$35,000(1 – 0.35) + 0.35($510,000/5) = $12,950NPV = –$510,000 + $12,950(PVIFA10%,5) + ($26,000/1.105) = –$444,765.36EAC = –$444,765.36 / (PVIFA10%,5) = –$117,327.98The two milling machines have unequal lives, so they can only be compared by expressing both on an equivalent annual basis, which is what the EAC method does. Thus, you prefer the Techron II because it has the lower (less negative) annual cost.18.To find the bid price, we need to calculate all other cash flows for the project, and then solve forthe bid price. The aftertax salvage value of the equipment is:Aftertax salvage value = $70,000(1 – 0.35) = $45,500Now we can solve for the necessary OCF that will give the project a zero NPV. The equation for the NPV of the project is:NPV = 0 = –$940,000 – 75,000 + OCF(PVIFA12%,5) + [($75,000 + 45,500) / 1.125]Solving for the OCF, we find the OCF that makes the project NPV equal to zero is:OCF = $946,625.06 / PVIFA12%,5 = $262,603.01The easiest way to calculate the bid price is the tax shield approach, so:OCF = $262,603.01 = [(P – v)Q – FC ](1 – t c) + t c D$262,603.01 = [(P – $9.25)(185,000) – $305,000 ](1 – 0.35) + 0.35($940,000/5)P = $12.54CH14 6、9、20、23、246. The pretax cost of debt is the YTM of the company’s bonds, so:P0 = $1,070 = $35(PVIFA R%,30) + $1,000(PVIF R%,30)R = 3.137%YTM = 2 × 3.137% = 6.27%And the aftertax cost of debt is:R D = .0627(1 – .35) = .0408 or 4.08%9. ing the equation to calculate the WACC, we find:WACC = .60(.14) + .05(.06) + .35(.08)(1 – .35) = .1052 or 10.52%b.Since interest is tax deductible and dividends are not, we must look at the after-tax cost ofdebt, which is:.08(1 – .35) = .0520 or 5.20%Hence, on an after-tax basis, debt is cheaper than the preferred stock.ing the debt-equity ratio to calculate the WACC, we find:WACC = (.90/1.90)(.048) + (1/1.90)(.13) = .0912 or 9.12%Since the project is riskier than the company, we need to adjust the project discount rate for the additional risk. Using the subjective risk factor given, we find:Project discount rate = 9.12% + 2.00% = 11.12%We would accept the project if the NPV is positive. The NPV is the PV of the cash outflows plus the PV of the cash inflows. Since we have the costs, we just need to find the PV of inflows. The cash inflows are a growing perpetuity. If you remember, the equation for the PV of a growing perpetuity is the same as the dividend growth equation, so:PV of future CF = $2,700,000/(.1112 – .04) = $37,943,787The project should only be undertaken if its cost is less than $37,943,787 since costs less than this amount will result in a positive NPV.23. ing the dividend discount model, the cost of equity is:R E = [(0.80)(1.05)/$61] + .05R E = .0638 or 6.38%ing the CAPM, the cost of equity is:R E = .055 + 1.50(.1200 – .0550)R E = .1525 or 15.25%c.When using the dividend growth model or the CAPM, you must remember that both areestimates for the cost of equity. Additionally, and perhaps more importantly, each methodof estimating the cost of equity depends upon different assumptions.Challenge24.We can use the debt-equity ratio to calculate the weights of equity and debt. The debt of thecompany has a weight for long-term debt and a weight for accounts payable. We can use the weight given for accounts payable to calculate the weight of accounts payable and the weight of long-term debt. The weight of each will be:Accounts payable weight = .20/1.20 = .17Long-term debt weight = 1/1.20 = .83Since the accounts payable has the same cost as the overall WACC, we can write the equation for the WACC as:WACC = (1/1.7)(.14) + (0.7/1.7)[(.20/1.2)WACC + (1/1.2)(.08)(1 – .35)]Solving for WACC, we find:WACC = .0824 + .4118[(.20/1.2)WACC + .0433]WACC = .0824 + (.0686)WACC + .0178(.9314)WACC = .1002WACC = .1076 or 10.76%We will use basically the same equation to calculate the weighted average flotation cost, except we will use the flotation cost for each form of financing. Doing so, we get:Flotation costs = (1/1.7)(.08) + (0.7/1.7)[(.20/1.2)(0) + (1/1.2)(.04)] = .0608 or 6.08%The total amount we need to raise to fund the new equipment will be:Amount raised cost = $45,000,000/(1 – .0608)Amount raised = $47,912,317Since the cash flows go to perpetuity, we can calculate the present value using the equation for the PV of a perpetuity. The NPV is:NPV = –$47,912,317 + ($6,200,000/.1076)NPV = $9,719,777CH16 1,4,12,14,171. a. A table outlining the income statement for the three possible states of the economy isshown below. The EPS is the net income divided by the 5,000 shares outstanding. The lastrow shows the percentage change in EPS the company will experience in a recession or anexpansion economy.Recession Normal ExpansionEBIT $14,000 $28,000 $36,400Interest 0 0 0NI $14,000 $28,000 $36,400EPS $ 2.80 $ 5.60 $ 7.28%∆EPS –50 –––+30b.If the company undergoes the proposed recapitalization, it will repurchase:Share price = Equity / Shares outstandingShare price = $250,000/5,000Share price = $50Shares repurchased = Debt issued / Share priceShares repurchased =$90,000/$50Shares repurchased = 1,800The interest payment each year under all three scenarios will be:Interest payment = $90,000(.07) = $6,300The last row shows the percentage change in EPS the company will experience in arecession or an expansion economy under the proposed recapitalization.Recession Normal ExpansionEBIT $14,000 $28,000 $36,400Interest 6,300 6,300 6,300NI $7,700 $21,700 $30,100EPS $2.41 $ 6.78 $9.41%∆EPS –64.52 –––+38.714. a.Under Plan I, the unlevered company, net income is the same as EBIT with no corporate tax.The EPS under this capitalization will be:EPS = $350,000/160,000 sharesEPS = $2.19Under Plan II, the levered company, EBIT will be reduced by the interest payment. The interest payment is the amount of debt times the interest rate, so:NI = $500,000 – .08($2,800,000)NI = $126,000And the EPS will be:EPS = $126,000/80,000 sharesEPS = $1.58Plan I has the higher EPS when EBIT is $350,000.b.Under Plan I, the net income is $500,000 and the EPS is:EPS = $500,000/160,000 sharesEPS = $3.13Under Plan II, the net income is:NI = $500,000 – .08($2,800,000)NI = $276,000And the EPS is:EPS = $276,000/80,000 sharesEPS = $3.45Plan II has the higher EPS when EBIT is $500,000.c.To find the breakeven EBIT for two different capital structures, we simply set the equationsfor EPS equal to each other and solve for EBIT. The breakeven EBIT is:EBIT/160,000 = [EBIT – .08($2,800,000)]/80,000EBIT = $448,00012. a.With the information provided, we can use the equation for calculating WACC to find thecost of equity. The equation for WACC is:WACC = (E/V)R E + (D/V)R D(1 – t C)The company has a debt-equity ratio of 1.5, which implies the weight of debt is 1.5/2.5, and the weight of equity is 1/2.5, soWACC = .10 = (1/2.5)R E + (1.5/2.5)(.07)(1 – .35)R E = .1818 or 18.18%b.To find the unlevered cost of equity we need to use M&M Proposition II with taxes, so:R E = R U + (R U– R D)(D/E)(1 – t C).1818 = R U + (R U– .07)(1.5)(1 – .35)R U = .1266 or 12.66%c.To find the cost of equity under different capital structures, we can again use M&MProposition II with taxes. With a debt-equity ratio of 2, the cost of equity is:R E = R U + (R U– R D)(D/E)(1 – t C)R E = .1266 + (.1266 – .07)(2)(1 – .35)R E = .2001 or 20.01%With a debt-equity ratio of 1.0, the cost of equity is:R E = .1266 + (.1266 – .07)(1)(1 – .35)R E = .1634 or 16.34%And with a debt-equity ratio of 0, the cost of equity is:R E = .1266 + (.1266 – .07)(0)(1 – .35)R E = R U = .1266 or 12.66%14. a.The value of the unlevered firm is:V U = EBIT(1 – t C)/R UV U = $92,000(1 – .35)/.15V U = $398,666.67b.The value of the levered firm is:V U = V U + t C DV U = $398,666.67 + .35($60,000)V U = $419,666.6717.With no debt, we are finding the value of an unlevered firm, so:V U = EBIT(1 – t C)/R UV U = $14,000(1 – .35)/.16V U = $56,875With debt, we simply need to use the equation for the value of a levered firm. With 50 percent debt, one-half of the firm value is debt, so the value of the levered firm is:V L = V U + t C(D/V)V UV L = $56,875 + .35(.50)($56,875)V L = $66,828.13And with 100 percent debt, the value of the firm is:V L = V U + t C(D/V)V UV L = $56,875 + .35(1.0)($56,875)V L = $76,781.25c.The net cash flows is the present value of the average daily collections times the daily interest rate, minus the transaction cost per day, so:Net cash flow per day = $1,276,275(.0002) – $0.50(385)Net cash flow per day = $62.76The net cash flow per check is the net cash flow per day divided by the number of checksreceived per day, or:Net cash flow per check = $62.76/385Net cash flow per check = $0.16Alternatively, we could find the net cash flow per check as the number of days the system reduces collection time times the average check amount times the daily interest rate, minusthe transaction cost per check. Doing so, we confirm our previous answer as:Net cash flow per check = 3($1,105)(.0002) – $0.50Net cash flow per check = $0.16 per checkThis makes the total costs:Total costs = $18,900,000 + 56,320,000 = $75,220,000The flotation costs as a percentage of the amount raised is the total cost divided by the amount raised, so:Flotation cost percentage = $75,220,000/$180,780,000 = .4161 or 41.61%8.The number of rights needed per new share is:Number of rights needed = 120,000 old shares/25,000 new shares = 4.8 rights per new share.Using P RO as the rights-on price, and P S as the subscription price, we can express the price per share of the stock ex-rights as:P X = [NP RO + P S]/(N + 1)a.P X = [4.8($94) + $94]/(4.80 + 1) = $94.00; No change.b. P X = [4.8($94) + $90]/(4.80 + 1) = $93.31; Price drops by $0.69 per share.。

罗斯公司理财(第9版)题库(视频讲解)+课后习题+模拟试题】

B.C+D,剩下的钱投资于证券市场 C.D+E,剩下的钱投资于证券市场 D.D+F

【答案】D 查看答案 【解析】所谓现值指数法又称盈利指数法,是指未来收益的现值总额和初始投资 现值总额之比,其实质是每一元初始投资所能获取的未来收益的现值额,盈利指 数可以表示为:

当资金不足以支付所有净现值为正的项目时,就需要进行资本配置。在资本配置 时就应该优先考虑盈利指数大的项目。D 项,现值指数为:

,为最大。

13 下面对资本资产定价模型的描述中错误的是( )。[中央财经大学 2012 金融硕士] A.单个证券的期望收益率由两部分组成,无风险利率以及风险溢价 B.风险溢价的大小取决于β值的大小 C.β越大,单个证券的风险越高,得到的风险补偿也越高

D.β度量的是单个证券的全部风险,包括系统性风险和非系统性风险 【答案】D 查看答案 【解析】根据 CAPM 模型,股票的期望收益率为: RS=RF+β×(RM-RF) 上式表明:单个证券的期望收益率由两部分组成,一是资金的时间价值,即无风 险利率;二是投资者因承担系统风险而得到的风险报酬,即风险溢价。其中风险 溢价的大小取决于β值的大小,是用来度量系统风险的,β越大,单个证券的风 险越高,得到的风险补偿也越高。

Байду номын сангаас

第 8 篇 理财专题 第 29 章 收购、兼并与剥离 第 30 章 财务困境 第 31 章 跨国公司财务

第四部分 模拟试题 罗斯《公司理财》配套模拟试题及详解(一) 罗斯《公司理财》配套模拟试题及详解(二)

内容简介

本书是罗斯《公司理财》(第 9 版)教材的配套题库,主要包括以下内容:

第一部分为名校考研真题【视频讲解】。本部分按选择题、判断题、概念题、简答题、 计算题、论述题等题型,对近年来众多名校考研涉及到罗斯《公司理财》的真题进行详细解 析。方便考生熟悉考点,掌握答题方法。部分考研真题提供高清视频讲解,圣才名师从考查 知识点、试题难度、相关考点等方面进行全方位的讲解。

罗斯《公司理财》(第9版)笔记和课后习题(含考研真题)详解[视频讲解]

![罗斯《公司理财》(第9版)笔记和课后习题(含考研真题)详解[视频讲解]](https://img.taocdn.com/s3/m/11fc1368998fcc22bdd10d65.png)

罗斯《公司理财》(第9版)笔记和课后习题详解第1章公司理财导论1.1复习笔记公司的首要目标——股东财富最大化决定了公司理财的目标。

公司理财研究的是稀缺资金如何在企业和市场内进行有效配置,它是在股份有限公司已成为现代企业制度最主要组织形式的时代背景下,就公司经营过程中的资金运动进行预测、组织、协调、分析和控制的一种决策与管理活动。

从决策角度来讲,公司理财的决策内容包括投资决策、筹资决策、股利决策和净流动资金决策;从管理角度来讲,公司理财的管理职能主要是指对资金筹集和资金投放的管理。

公司理财的基本内容包括:投资决策(资本预算)、融资决策(资本结构)、短期财务管理(营运资本)。

1.资产负债表资产负债表是总括反映企业某一特定日期财务状况的会计报表,它是根据资产、负债和所有者权益之间的相互关系,按照一定的分类标准和一定的顺序,把企业一定日期的资产、负债和所有者权益各项目予以适当排列,并对日常工作中形成的大量数据进行高度浓缩整理后编制而成的。

资产负债表可以反映资本预算、资本支出、资本结构以及经营中的现金流量管理等方面的内容。

2.资本结构资本结构是指企业各种资本的构成及其比例关系,它有广义和狭义之分。

广义资本结构,亦称财务结构,指企业全部资本的构成,既包括长期资本,也包括短期资本(主要指短期债务资本)。

狭义资本结构,主要指企业长期资本的构成,而不包括短期资本。

通常人们将资本结构表示为债务资本与权益资本的比例关系(D/E)或债务资本在总资本的构成(D/A)。

准确地讲,企业的资本结构应定义为有偿负债与所有者权益的比例。

资本结构是由企业采用各种筹资方式筹集资本形成的。

筹资方式的选择及组合决定着企业资本结构及其变化。

资本结构是企业筹资决策的核心问题。

企业应综合考虑影响资本结构的因素,运用适当方法优化资本结构,从而实现最佳资本结构。

资本结构优化有利于降低资本成本,获取财务杠杆利益。

3.财务经理财务经理是公司管理团队中的重要成员,其主要职责是通过资本预算、融资和资产流动性管理为公司创造价值。

罗斯《公司理财》(第9版)配套题库【课后习题-资本结构:债务运用的制约因素】

罗斯《公司理财》(第9版)配套题库【课后习题-资本结构:债务运用的制约因素】第17章资本结构:债务运用的制约因素一、概念题1.代理成本(agency costs)答:代理成本指委托人基于委托代理关系所产生的,因代理人(经营者、雇员等)怠工、不负责任、偏离股东目标和以种种手段从公司获取财富等而发生的各种成本的总称。

在本章中,代理成本是指债权人为保护自身利益,防止公司股东财富最大化的利己策略,对企业经营做出种种限制或提高利率,由此使企业增加的费用或机会成本。

所有权和控制权的分离是产生代理问题和代理成本的根本原因。

实证分析表明,代理关系产生的经济基础是公司股东向经营者(代理人)授予经营管理权,虽然这样做可降低公司的经营成本,因为由众多的股东直接参与公司决策、经营管理、生产控制的成本是惊人的。

但是代理关系的确立又必然招致代理成本。

代理成本的存在会影响公司经营效率,甚至可能威胁公司的生存。

代理成本可划分为三部分:委托人的监督成本、代理人的担保成本和剩余损失。

2.转换发行(exchange offers)答:转换发行是资本结构变更的一种形式,指以债券或优先股交换普通股,或相反,以普通股交换比优先股更高的要求权,从而达到调整杠杆率、调整资本风险的目的的资本结构变更形式。

如果公司认为其财务杠杆率过高,那么公司可以增发部分普通股,用以换回部分债券或优先股,以降低公司的财务负担。

但这种做法容易造成股权分散。

反之,若公司认为有必要通过提高财务杠杆率来提高股东权益的收益率水平,则可以增发债券或优先股,以换回部分流通在外的普通股。

3.市场索取权(marketed claims)答:市场索取权指可以在金融市场上买卖交易的财产索取权利,包括股东和债权人对公司财产的索取权。

谈到公司价值时,一般仅指市场性索取权的价值V M,而不包括非市场性索取权的价值V N。

市场性索取权的价值V M,通常会随资本结构的变化而变化,尤其是随负债权益比的变化而变化。

罗斯《公司理财》(第9版)课后习题(第19~21章)【圣才出品】

罗斯《公司理财》(第9版)课后习题第19章股利政策和其他支付政策一、概念题1.追随者(clienteles)答:追随者是由早期著名的财务学家Miller和Modigliani(1961)、Elton和Gruber (1970)以及Black和Scholes(1974)等人所提出的一种经典理论假说,该假说认为处于不同税收等级(具有不同交易成本或不同投资约束条件)的投资者对股利支付水平具有不同的需求,具体体现在公司股利支付率与投资者的税收等级(交易成本或投资约束条件)之间存在显著的相关关系。

如果股东在乎税收,股票将吸引重视股利收益率的税收追随者。

追随者的形成过程如下表所示:2.自制股利(homemade dividends)答:自制股利是指投资者抵销公司股利政策的一种做法:当股利水平低于投资者期望的水平时,投资者可以通过出售部分股票以获取期望的现金收入;若股利水平高于投资者期望的水平,投资者可以用股利收入购买一些该公司的股票。

通过自制股利,投资者可以使公司的股利政策的变化失效,因此股利政策是无关的。

3.股利发放日(date of payment)答:股利发放日:也称为付息日,指将股利正式支付给登记在册股东的日期。

在这一天,企业应将股利通过邮寄等方式支付给股东,计算机交易系统可以通过中央结算登记系统将股利直接打入股东资金账户,由股东向其证券代理商领取股利。

4.信息内涵效应(information-content effect)答:信息内涵效应是指股利政策的宣告导致股价随之变化的现象。

信息内涵效应是根据信号传播论提出的概念,主要内容是:公司管理者与外部投资者之间存在着信息不对称,管理者占有更多的有关企业前景方面的内部信息。

当管理者预计公司的发展前景良好,未来业绩有大幅度增长时,就会通过增加股利的方式将这一信息及时告诉股东和潜在的投资者;相反,如果预计到公司的发展前景不太好,未来盈利将呈持续性不理想时,那么他们往往维持甚至降低现有股利水平,这等于向股东和潜在投资者发出了利差信号。

Cha08 罗斯公司理财第九版原版书课后习题

Earlier in the chapter, we saw how bonds were rated based on their credit risk. What you will find if you start looking at bonds of different ratings is that lower-rated bonds have higher yields.We stated earlier in this chapter that a bond’s yield is calculated assuming that all the promised payments will be made. As a result, it is really a promised yield, and it may or may not be what you will earn. In particular, if the issuer defaults, your actual yield will be lower, probably much lower. This fact is particularly important when it comes to junk bonds. Thanks to a clever bit of marketing, such bonds are now commonly called high-yield bonds, which has a much nicer ring to it; but now you recognize that these are really high promised yield bonds.Next, recall that we discussed earlier how municipal bonds are free from most taxes and, as a result, have much lower yields than taxable bonds. Investors demand the extra yield on a taxable bond as compensation for the unfavorable tax treatment. This extra compensation is the taxability premium.Finally, bonds have varying degrees of liquidity. As we discussed earlier, there are an enormous number of bond issues, most of which do not trade on a regular basis. As a result, if you wanted to sell quickly, you would probably not get as good a price as you could otherwise. Investors prefer liquid assets to illiquid ones, so they demand a liquidity premium on top of all the other premiums we have discussed. As a result, all else being the same, less liquid bonds will have higher yields than more liquid bonds.ConclusionIf we combine everything we have discussed, we find that bond yields represent the combined effect of no fewer than six factors. The first is the real rate of interest. On top of the real rate are five premiums representing compensation for (1) expected future inflation, (2) interest rate risk, (3) default risk, (4) taxability, and (5) lack of liquidity. As a result, determining the appropriate yield on a bond requires careful analysis of each of these factors.Summary and ConclusionsThis chapter has explored bonds, bond yields, and interest rates. We saw that:1. Determining bond prices and yields is an application of basic discounted cash flow principles.2. Bond values move in the direction opposite that of interest rates, leading to potential gains orlosses for bond investors.3. Bonds are rated based on their default risk. Some bonds, such as Treasury bonds, have no riskof default, whereas so-called junk bonds have substantial default risk.4. Almost all bond trading is OTC, with little or no market transparency in many cases. As a result,bond price and volume information can be difficult to find for some types of bonds.5. Bond yields and interest rates reflect six different factors: the real interest rate and fivepremiums that investors demand as compensation for inflation, interest rate risk, default risk, taxability, and lack of liquidity.In closing, we note that bonds are a vital source of financing to governments and corporations of all types. Bond prices and yields are a rich subject, and our one chapter, necessarily, touches on only the most important concepts and ideas. There is a great deal more we could say, but, instead, we will move on to stocks in our next chapter.Concept Questions1. Treasury Bonds Is it true that a U.S. Treasury security is risk-free?2. Interest Rate Risk Which has greater interest rate risk, a 30-year Treasury bond or a 30-year21. Using Bond Quotes Suppose the following bond quote for IOU Corporation appears in thefinancial page of today’s newspaper. Assume the bond has a face value of $1,000 and the current date is April 15, 2010. What is the yield to maturity of the bond? What is the current yield?22. Finding the Maturity You’ve just found a 10 percent coupon bond on the market that sells forpar value. What is the maturity on this bond?CHALLENGE (Questions 23–30)23. Components of Bond Returns Bond P is a premium bond with a 9 percent coupon. Bond D isa 5 percent coupon bond currently selling at a discount. Both bonds make annual payments, havea YTM of 7 percent, and have five years to maturity. What is the current yield for Bond P? For BondD? If interest rates remain unchanged, what is the expected capital gains yield over the next year for Bond P? For Bond D? Explain your answers and the interrelationship among the various types of yields.24. Holding Period Yield The YTM on a bond is the interest rate you earn on your investment ifinterest rates don’t change. If you actually sell the bond before it matures, your realized return is known as the holding period yield (HPY).1. Suppose that today you buy a 9 percent annual coupon bond for $1,140. The bond has 10years to maturity. What rate of return do you expect to earn on your investment?2. Two years from now, the YTM on your bond has declined by 1 percent, and you decide tosell. What price will your bond sell for? What is the HPY on your investment? Compare this yield to the YTM when you first bought the bond. Why are they different?25. Valuing Bonds The Morgan Corporation has two different bonds currently outstanding. Bond Mhas a face value of $20,000 and matures in 20 years. The bond makes no payments for the first six years, then pays $800 every six months over the subsequent eight years, and finally pays $1,000 every six months over the last six years. Bond N also has a face value of $20,000 and a maturity of20 years; it makes no coupon payments over the life of the bond. If the required return on boththese bonds is 8 percent compounded semiannually, what is the current price of Bond M? Of Bond N?26. R eal Cash Flows When Marilyn Monroe died, ex-husband Joe DiMaggio vowed to place freshflowers on her grave every Sunday as long as he lived. The week after she died in 1962, a bunch of fresh flowers that the former baseball player thought appropriate for the star cost about $8.Based on actuarial tables, “Joltin’ Joe” could expect to live for 30 years after the actress died.Assume that the EAR is 10.7 percent. Also, assume that the price of the flowers will increase at 3.5 percent per year, when expressed as an EAR. Assuming that each year has exactly 52 weeks, what is the present value of this commitment? Joe began purchasing flowers the week after Marilyn died.27. Real Cash Flows You are planning to save for retirement over the next 30 years. To save forretirement, you will invest $800 a month in a stock account in real dollars and $400 a month in a bond account in real dollars. The effective annual return of the stock account is expected to be 12 percent, and the bond account will earn 7 percent. When you retire, you will combine your money into an account with an 8 percent effective return. The inflation rate over this period is expected to be 4 percent. How much can you withdraw each month from your account in real terms assuminga 25-year withdrawal period? What is the nominal dollar amount of your last withdrawal?28. Real Cash Flows Paul Adams owns a health club in downtown Los Angeles. He charges hiscustomers an annual fee of $500 and has an existing customer base of 500. Paul plans to raise the annual fee by 6 percent every year and expects the club membership to grow at a constant rate of3 percent for the next five years. The overall expenses of running the health club are $75,000 ayear and are expected to grow at the inflation rate of 2 percent annually. After five years, Paul2. How many of the coupon bonds must East Coast Yachts issue to raise the $40 million? Howmany of the zeroes must it issue?3. In 20 years, what will be the principal repayment due if East Coast Yachts issues the couponbonds? What if it issues the zeroes?4. What are the company’s considerations in issuing a coupon bond compared to a zero couponbond?5. Suppose East Coast Yachts issues the coupon bonds with a make-whole call provision. Themake-whole call rate is the Treasury rate plus .40 percent. If East Coast calls the bonds in 7 years when the Treasury rate is 5.6 percent, what is the call price of the bond? What if it is 9.1 percent?6. Are investors really made whole with a make-whole call provision?7. After considering all the relevant factors, would you recommend a zero coupon issue or aregular coupon issue? Why? Would you recommend an ordinary call feature or a make-whole call feature? Why?。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解]

第13章风险、资本成本和资本预算[视频讲解]

13.1复习笔记

运用净现值法,按无风险利率对现金流量折现,可以准确评价无风险现金流量。

然而,现实中的绝大多数未来现金流是有风险的,这就要求有一种能对有风险现金流进行折现的方法。

确定风险项目净现值所用的折现率可根据资本资产定价模型CAPM(或套利模型APT)来计算。

如果某无负债企业要评价一个有风险项目,可以运用证券市场线SML来确定项目所要求的收益率r s,r s也称为权益资本成本。

当企业既有债务融资又有权益融资时,所用的折现率应是项目的综合资本成本,即债务资本成本和权益资本成本的加权平均。

联系企业的风险贴现率与资本市场要求的收益率的原理在于如下一个简单资本预算原则:企业多余的现金,可以立即派发股利,投资者收到股利自己进行投资,也可以用于投资项目产生未来的现金流发放股利。

从股东利益出发,股东会在自己投资和企业投资中选择期望收益率较高的一个。

只有当项目的期望收益率大于风险水平相当的金融资产的期望收益率时,项目才可行。

因此项目的折现率应该等于同样风险水平的金融资产的期望收益率。

这也说明了资本市场价格信号作用。

1.权益资本成本

从企业的角度来看,权益资本成本就是其期望收益率,若用CAPM模型,股票的期望收益率为:

其中,R F是无风险利率,是市场组合的期望收益率与无风险利率之差,也称为期望超额市场收益率或市场风险溢价。

要估计企业权益资本成本,需要知道以下三个变量:①无风险利率;②市场风险溢价;

③公司的贝塔系数。

根据权益资本成本计算企业项目的贴现率需要有两个重要假设:①新项目的贝塔风险与企业风险相同;②企业无债务融资。

2.贝塔的估计

估算公司贝塔值的基本方法是利用T个观测值按照如下公式估计:

估算贝塔值可能存在以下问题:①贝塔可能随时间的推移而发生变化;②样本容量可能太小;③贝塔受财务杠杆和经营风险变化的影响。

可以通过如下途径解决上述问题:①第1个和第2个问题可通过采用更加复杂的统计技术加以解决;②根据财务风险和经营风险的变化对贝塔作相应的调整,有助于解决第3个问题;③注意同行业类似企业的平均β估计值。

根据企业自身历史数据来估算企业贝塔系数是一种常用方法,也有人认为运用整个行业的贝塔系数可以更好地估算企业的贝塔系数。

有时两者计算的结果差异很大。

总的来说,可以遵循下列原则:如果认为企业的经营与所在行业其他企业的经营十分类似,用行业贝塔降低估计误差。

如果认为企业的经营与行业内其他企业的经营有着根本性差别,则应选择企业的贝塔。

3.贝塔的确定

前面介绍的回归分析方法估算贝塔并未阐明贝塔是由哪些因素决定的。

主要存在以下三个因素:收入的周期性、经营杠杆和财务杠杆。

(1)收入的周期性。

有些企业的收入具有明显的周期性,也就是说,这些企业在经济周期的扩张阶段经营得很好,而在经济周期的紧缩阶段则经营得很差。

由于贝塔是股票收益率与市场收益率的标准协方差,所以周期性强的股票有较高的贝塔值。

需要注意的是,周期性不等于变动性,正如股票的标准差大并不一定贝塔就高。

(2)经营杠杆。

企业固定成本的比重越大,经营杠杆越大。

经营杠杆大的企业在商业周期的扩张阶段,边际销量的增加对应的边际EBIT更大,因为变动成本较小。

在商业周期的紧缩阶段也如此。

所以在企业收入的周期性对贝塔起决定性的作用同时,经营杠杆将这种作用放大了。

企业如果收入的周期性强且经营杠杆高,则贝塔值也高;反之,如果收入的周期性不明显且经营杠杆低,则贝塔值也低。

(3)财务杠杆。

假定某人拥有企业全部的资产和负债,即拥有整个企业,那么,这个由资产和负债共同构成的企业的组合贝塔系数等于组合中每个单项的贝塔的加权平均,所以有:

在全权益公司,权益贝塔就等于资产贝塔。

在有负债的情况下,由于在实际中,负债的

贝塔很低,一般假设为零。

则有:所以有财务杠杆的情况下,权益贝塔一定大于资产贝塔。

4.有负债情况下的资本成本

假定某企业运用债务和权益融资来进行投资,企业按r B借入债务资本,按r S取得权益资本。

即权益资本成本是r S,债务资本成本是借款利率r B,平均资本成本是权益资本成本和债务资本成本的加权平均,所以,通常称之为加权平均资本成本,r WACC,其计算如下:

式中的权数分别是权益占总价值的比重,即;和负债占总价值的比重,即。

显然,若企业无负债,即是一个100%权益企业,其平均资本成本就等于权益资本成本r S。

若企业负债特别多而权益几乎为0,即是一个100%负债的企业,其平均资本成本就等于债务资本成本r B。

需要注意的是,无论是负债还是权益,公司理财关心的是市场价值而不是账面价值。

此外由于对公司来说利息是可以抵税的,综上所述,可以得到公司的平均资本成本:

在企业有负债时,项目的折现率应为r WACC。

5.流动性与期望报酬

流动性较差的股票的交易费用会降低投资者获得的总报酬。

投资者投资于高风险股票时会要求比较高的期望回报率。

由于投资者的期望报酬率对公司而言就是资本成本,因此,资本成本与公司的贝塔成正相关。

投资者对投资于具有较高交易费用的股票会要求一个比较高的期望报酬率。

这种比较高的期望报酬率意味着公司必须承担比较高的资本成本。

公司有动机降低交易成本以降低资本成本。

公司可以通过降低交易成本来降低他们的资本成本,实际可行的建议包括股票拆细、更完整的信息披露和与证券分析师更有效的协作。

13.2课后习题详解

一、概念题

1.资产贝塔(asset beta)

答:资产贝塔是指企业总资产的贝塔系数。

除非完全依靠权益融资,否则不能把资产贝塔看作普通股的贝塔系数。

其公式为:

其中,β权益是杠杆企业权益的贝塔。

公式包括两部分,即负债的贝塔乘以负债在资本结构中的百分比;权益的贝塔乘以权益在资本结构中的百分比。

这个组合包括企业的负债和权益,所以组合贝塔就是资产贝塔。

在实际中,负债的贝塔很低,一般假设为零。

若假设负债的贝塔为零,则:

对于杠杆企业,权益/(负债+权益)一定小于1,所以β资产<β权益,将上式变形,有:

有财务杠杆的情况下,权益贝塔一定大于资产贝塔。

2.经营杠杆(operating leverage)

答:经营杠杆是指由于固定成本的存在而导致息税前利润变动大于产销业务量变动的杠杆效应。

对经营杠杆的计量最常用的指标是经营杠杆系数或经营杠杆度。

经营杠杆系数,是指息税前利润变动率相当于销售量变动率的倍数。

用公式可以表示为:

式中,EBIT为息税前利润;F为固定成本。

经营杠杆系数不是固定不变的。

当企业的固定成本总额、单位产品的变动成本、销售价格、销售数量等因素发生变动时,经营杠杆系数也会发生变动。

经营杠杆系数越高,对经营杠杆利益的影响就越强,经营杠杆风险也就越高。

经营杠杆越大,企业的贝塔系数就越大。

3.权益资本成本(cost of equity capital)

答:权益资本成本就是投资股东要求的回报率,用CAPM模型表示股票的期望收益率为:

其中,R F是无风险利率;是市场组合的期望收益率与无风险利率之差,也称为期望超额市场收益率或市场风险溢价。

所以要估计企业权益资本成本,需要知道以下三个变量:①无风险利率;②市场风险溢价;③公司权益的贝塔系数。

4.加权平均资本成本(weighted average cost of capital,r WACC)