Fixed assets Apr 2013

香港会计准则13-投资性固定资产

SSAP 13STATEMENT OF STANDARD ACCOUNTING PRACTICE 13ACCOUNTING FOR INVESTMENT PROPERTIES(Issued October 1987, revised July 1990, September 1994,and December 2000 in red text and underlined type)The standards, which have been set in bold italic type, should be read in the context of the background material and implementation guidance and in the context of the Foreword to Statements of Standard Accounting Practice and Accounting Guidelines. Statements of Standard Accounting Practice are not intended to apply to immaterial items (see paragraph 8 of the Foreword).IntroductionUnder the accounting requirements of SSAP 6 "Deprecitation accounting" SSAP 17 "Property, plant and equipment", in order to match revenues with costs and charges period by period the depreciable amounts of depreciable assets are allocated over their estimated useful lives on a systematic basis. Under those requirements it is also accepted that an increase in the value of a depreciable asset does not generally remove the necessity to charge depreciation to reflect on a systematic basis the consumption of the asset.A different treatment is, however, required where the fixed assets of a company are held not for consumption in the business operations but as investments, the disposal of which would not materially affect any manufacturing or trading operations of a company. In such a case the current value of these investments, and changes in that current value, are of prime importance rather than a calculation of systematic periodic depreciation. Consequently, for the proper appreciation of the financial position, a different accounting treatment is considered appropriate for fixed assets held as investments (called in this Statement "investment properties").Scopepanies Insurance companies which avail themselves of the exemptions under Part III ofthe Tenth Schedule to the Companies Ordinance (banking, insurance and shippingcompanies)and charitable, Government subvented and not-for-profit organisations whoselong-term financial objective is other than to achieve operating profits (eg. tradeassociations, clubs and pension funds) are exempted from compliance with this Statementprovided that full disclosure of their accounting policies is made.Definitions2.Subject to the exceptions in paragraph 4 below, an "investment property" is an interest inland and/or buildings:a.in respect of which construction work and development have been completed; andb.which is held for its investment potential, any rental income being negotiated at arm'slength.3. Investment properties may be held by a company which holds investments as part of itsbusiness such as a property investment company. Investment properties may also be held by a company whose main business is not the holding of investments.4.The following are exceptions from the definition of an investment property in paragraph 2above:a. A property, or that part of a property, which is owned and occupied by a companyfor its own purposes is not an investment property.b. A property, or that part of a property, let to and occupied by another company inthe group is not an investment property for the purposes of its own financialstatement or the consolidated financial statements.5. A property of which only 15 per cent or less by area or value is occupied by the company oranother company in the group ("owner-occupied") should normally be regarded as an investment property even though part of it is not held for investment purposes. The standards in thisStatement will therefore apply to the whole property.6. If a property is partially owner-occupied and partially held for investment purposes then the partoccupied by the owner (which is more than 15 per cent by area or value) should be treated as a depreciable asset and SSAP 6 "Deprecitation accounting"SSAP 17 "Property, plant andequipment" should be applied; the part held as an investment property should be identifiedseparately in the financial statements and stated at their carrying amount in accordance with the standards in this Statement.Open market value7."Open market value", as defined by the Hong Kong Institute of Surveyors, means the bestprice at which an interest in a property might reasonably be expected to be sold at the date of valuation assuming:a. a willing seller;b. a reasonable period in which to negotiate the sale taking into account the nature ofthe property and the state of the market;c.that values will remain static during that period;d.that the property will be freely exposed to the open market; ande.that no account will be taken of any additional bid by a purchaser with a specialinterest.8.Subject to paragraphs 9, 12 and 13 below, investment properties should be included in thebalance sheet at their open market value, based on a period end valuation carried out:a.annually by persons holding a recognised professional qualification in valuingproperties and having recent post-qualification experience in valuing properties inthe location and in the category of the properties concerned; andb.at least every three years by an external valuer with similar qualifications to those ina. above.9.Investment properties should not be subject to periodic charges for depreciation on the basis ofSSAP 6 "Deprecitation accounting" except where the unexpired term of the lease is 20 years or less, in which case depreciation must be provided on the then carrying amount over theremaining term of the lease.10. Investment properties are excluded from the definition of depreciable assets (SSAP 6) and areconsequently not subject to an annual depreciation charge on the ground that such properties are not held for consumption in the business operations but as investments.11. Where an investment property is held on a lease with an unexpired term of 20 years or less it isnecessary to recognise the annual depreciation in the profit and loss account to avoid the situation whereby a short lease is amortised against the investment property revaluation reserve while the rentals are taken to the profit and loss account.Exemption from open market value12.For the purpose of their own financial statements, unlisted companies with investmentproperties the estimated open market value of which in aggregate is less than HK$50 million or less than 15 per cent of the carrying amount of total assets of the company may carry those investment properties at cost or, if they have been measured previously at estimated openmarket value, at the most recently determined estimated open market value. In either case, and, subject to paragraph 9 above they should not be depreciated, but any impairment should result in a reduction of the carrying amount.13.For the purpose of the consolidated financial statements, investment properties may be statedat cost or, if they have been measured previously at estimated open market value, at the most recently determined estimated open market value, if the parent company is unlisted and the aggregate estimated open market value of investment properties at group level is less thanHK$50 million or less than 15 per cent of the carrying amount of total group assets. In either case, and, subject to paragraph 9 above they should not be depreciated, but any impairment should result in a reduction of the carrying amount.14. This Statement requires investment properties of enterprises falling within the scope of thisStatement to be included in the balance sheet at open market value at the period end. Enterprises which satisfy the exemption criteria set out in paragraphs 12 and 13 are exempted from therequirement and may state investment properties at cost or at estimated open market value.15. The exemptions are allowed because the costs of complying with the valuation requirement inparagraph 8 may be disproportionate to the benefits.16. "Estimated open market value" means open market value estimated by the directors for thepurpose of establishing the exemption criteria and, in respect of an eligible enterprise whichchooses to take advantage of the exemptions in paragraphs 12 and 13 above, for determining the carrying amount of investment properties. Estimated open market value may be determined by the directors, by reference to recent transactions in similar properties or where such market value is not available, other estimation techniques, for example, depreciated replacement cost or income capitalisation techniques.Changes in value17.Subject to paragraph 19 below, changes in the value of investment properties should not betaken to the profit and loss account but should be treated as movements in an investmentproperty revaluation reserve, unless the total of this reserve is insufficient to cover a deficit ona portfolio basis, in which case the amount by which the deficit exceeds the total amount in theinvestment property revaluation reserve should be charged to the profit and loss account.Where a deficit has previously been charged to the profit and loss account and a revaluation surplus subsequently arises, this surplus should be credited to the profit and loss account to the extent of the deficit previously charged.18. Paragraph 17 requires that when the deficits on the revaluation of investment properties exceedthe balance of the investment property revaluation reserve the resulting debit balance should be charged to the profit and loss account. Where a revaluation deficit arises in an individualcompany which is part of a group and there is a net surplus on revaluations of investmentproperties in the group, the deficit can be charged against the revaluation reserve in theconsolidated financial statements.19.Paragraph 17 does not apply to the long-term business of insurance companies where changesin value are dealt with in the relevant fund account.Disclosure in financial statements20.Investment properties should be included under the classification of fixed assets in the balancesheet. Investment properties with an unexpired term of 20 years or less which are depreciated should continue to be classified as investment properties within fixed assets.21.Where the company's assets include investment properties the following information should bedisclosed:a.the accounting policies for:i.the determination of the carrying amount of investment properties,ii.the treatment of changes in value of investment properties carried atrevalued amounts, andiii.the treatment of any revaluation surplus on the sale of a revalued investment property;b.the carrying amount of investment properties;c.the balance on the investment property revaluation reserve together with details ofmovements during the accounting period;d.any surplus or deficit on revaluation taken to the profit and loss account during theaccounting period;e.the profit or loss on disposal of any investment properties;f.the gross rental income from investment properties;g.significant restrictions on the realisability of investment properties, or the remittanceof income and proceeds of disposal; andh.for investment properties stated at revalued amounts:i.the policy for the frequency of revaluation,ii.the date of the latest revaluation, andiii.the names of the persons making the valuation, or particulars of theirqualifications, together with the bases of valuation used by them. If a personmaking a valuation is an employee or officer of the company or group whichowns the asset, this fact.Effective date22.Except for paragraph 1, the accounting practices set out in this Statement should be adopted assoon as possible and regarded as standard in respect of financial statements relating to periods ending on or after 31 October 1994. Paragraph 1 should be regarded as Standard in respect of financial statements relating to periods beginning on or after 1 July 2000.Transitional arrangements23. Enterprises which state their investment properties at carrying value, as permitted under SSAP 13before the September 1994 amendment, may continue to do so provided that they meet theexemption criteria of paragraphs 12 and 13 and the investment properties have not beensubsequently restated at open market values or estimated open market values. Subject toparagraph 9, the investment properties should not be depreciated but any impairment should be provided for.Notes on legal requirements in Hong Kong24. The reference to "the Schedule" below are to the Tenth Schedule to the Companies Ordinance.25. Paragraph 5 of the Schedule requires disclosure of the aggregate amount of the cost or valuationof fixed assets under appropriate headings and of the aggregate amount provided or written off since the date of acquisition or valuation for depreciation or diminution in value.26. Paragraph 12(7) of the Schedule requires disclosure of the years in which fixed assets wereseverally valued and their respective values, and in the case of assets valued during the financial period:a. the name of the persons who valued them or particulars of their qualifications for doingso; andb. the bases of valuation used by such persons.27. Paragraph 12(8) of the Schedule requires disclosure of the amounts of fixed assets acquired ordisposed of during the year under each heading. Where fixed assets include land, paragraph 12(9) requires separate disclosure of the amounts ascribable to:a. land in Hong Kong held on long lease, medium-term lease and short lease respectively;andb. land outside Hong Kong held freehold, on long lease, medium-term lease and short leaserespectively.28. Under paragraph 13 of the Schedule disclosure must be made of the amount charged to revenueby way of provision for depreciation, renewals or diminution in value of fixed assets.29. Paragraph 13(1)(h) of the Schedule requires disclosure of rental income from land and buildings(after deduction of ground rents, rates and other out-goings).30. The above provisions apply to all companies other than banking, insurance and shippingcompanies which are entitled to certain disclosure exemptions under the provisions of Part III of the Schedule.。

第六章 固定资产(Plant assets or Fixed assets)

第六章固定资产(Plant assets or Fixed assets)本章主要内容固定资产的分类与计价固定资产的取得固定资产的折旧固定资产的后续支出固定资产的处置固定资产的清查第一节固定资产的性质、分类和计价一、固定资产的性质:有形;供企业生产经营使用;使用期限大于1年;价值标准:生产经营用未作规定,非生产经营用的固定资产单位价值在2000元以上;具有盈利能力;资本性支出。

二、固定资产的分类(一)按经济用途进行分类:经营用和非经营(二)按使用情况分类:在用、未用和不需用(三)按所有权分类:自有和融资租入注意:固定资产和存货的区别。

三、固定资产的计价(一)计价基础:1、原始价值(Original value)或历史成本:(一般采用)购建固定资产的一切合理支出;2、重置成本:(盘盈、接受捐赠等情况)重新购置的支出;3、折余价值或净值(Net value):原始成本或重置成本扣除折旧后的余额。

第二节固定资产的取得一、固定资产的购置不需安装借:固定资产贷:银行存款、应付账款等科目需要安装:购入时:借:在建工程(Construction-in-process)贷:银行存款等安装时:借:在建工程贷:银行存款等安装结束:借:固定资产贷:在建工程二、固定资产增加的自行建造1、自营工程:购入工程所需物资时:借:工程物资贷:银行存款建造过程:借:在建工程贷:工程物资(领用工程所需物资)原材料(领用生产原料,注意增值税的处理)生产成本(生产车间)应付工资(支付工程人员工资)工程完工:借:固定资产贷:在建工程2、出包工程:出包并预付工程款:借:在建工程贷:银行存款补付工程款:借:在建工程贷:银行存款工程验收交付使用:借:固定资产贷:在建工程举例:CJ公司2002年1月2日与SF公司签订一项建筑合同,SF公司为CJ公司建造一栋办公楼,合同规定,该大楼的总造价800万元,工期2年(连带装修),为建造此楼,CJ公司2002年1月2日向银行取得长期借款400万元、期限3年、年利率8%。

微软官方教材_财务_ Fixed Assets

Basic Setup of Fixed Assets

Simplify setup of Assets

Inquiries

Uses of Fixed Asset Groups

Reporting

Setting up Posting Profiles

19 of 8

Parameters

Parameters are the last step in setting up Fixed Assets.

15 of 8

Five Methods for Depreciation Calculation – Manual

• Manual depreciation is always calculated as the percentage of the Acquisition price – Scrap value • Most flexible … more setup! • Depreciate base on schedule specified by user • (Example of Manual schedule setup): • - Year 1 = 10 % (10,000*10%) • - Year 2 = 50 % (10,000*50%) • - Year 3 = 8 % (10,000*8%) • - Year 4 = 12 % (10,000*12%) • - Year 5 = 20 % (10,000*20%)

Test Your Skills – General Setup of Fixed Assets Test Your Skills – Basic Setup of Fixed Assets

Microsoft® Business Solutions –Axapta ® Fixed Assets Module

固定资产采购程序

Definition of fixed assets固定资产的定义_Value more than RMB2000 per unit._单位价值超过人民币2000元的资产;_Working duration/useful life more than 1 year_使用期限超过1年的资产一.Capital expenditure application固定资产购置申请_Request department applies fixed assets acquisition by filling the Part I of Capital Expenditure Application (please refer to the attachment FIN415A). The application form should be approved by the request department head and reviewed by the financial department before finally approved by the General Manager or the Board or the higher Group Management._任何部门需要采购增添固定资产的,须填写固定资产审购表第一部分(请参阅附件FN0121A),由部门经理批准,交财务部根据预算计划审核,最后由总经理或董事会或更高管理层批准。

二.Fixed assets acquisition and receipt procedure固定资产购置验收程序_At least two suppliers should be considered by the purchase department for comparison._固定资产的采购部门必须选择不少于两个供应商以作比较。

_Related technical standards or requirements of acquiring fixed assets should be confirmed by relevant technical department of the Company or the Group._固定资产的技术标准及要求须经公司或集团相关专业部门的确认。

会计常用英语词汇——资产类Assets

房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate 在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or incom e 待处理固定资产损溢Wait deal fixed assets loss or income流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents外埠存款Other city Cash in bank银行本票Cashier''s cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments-stock债券Short-term investments-corporate bonds基金Short-term investments-corporate funds其他Short-term investments-other短期投资跌价准备Short-term investments falling price reserves 应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrap page低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process-outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis 存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investm ent长期股权投资Long-term investm ent on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investm ent on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investm ents depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备B creditor''s rights investment depreciation reserves 委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets。

财务会计固定资产

Financial Analysis

and Interpretation

会本四 六组制作

• Ratio of fixed assets to long-term liabilities =Fixed assets/Long-term liabilities To illustrate,the following data were taken from the 2002 and 2001 fianacial statements of Procter & Gamble 2002 2001 • Property,Plant, And equipment $13,349 $13095 • Long-term debt 11,201 9,792

• Sum-of-the-years-digits is an accelerated depreciation method ,meaning it assums the asset will lose the majority of its value in the first few years of its useful life. • AS with other depreciation methods,Sum-of-theYears-Digits is based on the purchase prise,salvage value,and years of usefulness.

Accum Book • Mineral deposits: Cost Depl. Value Alaska deposit….$1200,000 $800,000 $400,000 Wyoming deposit….750,000 200,000 550,000 • $1950,000 $1000,000 950,000 • Total property,plant, and equipment……………………………………………………..1,629,000 • Intangible assets: Patents……………………………………………………………$75,000 Goodwill……………………………………………………………50,000 Total intangible assets…………………………………………..125,000

2013年注会综合常见英语词汇一览

2013年注会综合常见英语词汇一览递延税款贷项 Deferred taxation credit股本 Share capital已归还投资 Investment returned利润分配-其他转入 Profit appropriation - other transfer in利润分配-提取法定盈余公积 Profit appropriation - statutory surplus reserve 利润分配-提取法定公益金 Profit appropriation - statutory welfare reserve 利润分配-提取储备基金 Profit appropriation - reserve fund利润分配-提取企业发展基金 Profit appropriation - enterprise development fund利润分配-提取职工奖励及福利基金 Profit appropriation - staff bonus and welfare fund利润分配-利润归还投资 Profit appropriation - return investment by profit 利润分配-应付优先股股利 Profit appropriation - preference shares dividends 利润分配-提取任意盈余公积 Profit appropriation - other surplus reserve利润分配-应付普通股股利 Profit appropriation - ordinary shares dividends利润分配-转作股本的普通股股利 Profit appropriation - ordinary shares dividends converted to shares期初未分配利润 Retained earnings, beginning of the year资本公积-股本溢价 Capital surplus - share premium资本公积-接受捐赠非现金资产准备 Capital surplus - donation reserve资本公积-接受现金捐赠 Capital surplus - cash donation资本公积-股权投资准备 Capital surplus - investment reserve资本公积-拨款转入 Capital surplus - subsidiary资本公积-外币资本折算差额 Capital surplus - foreign currency translation 资本公积-其他 Capital surplus - others盈余公积-法定盈余公积金 Surplus reserve - statutory surplus reserve盈余公积-任意盈余公积金 Surplus reserve - other surplus reserve盈余公积-法定公益金 Surplus reserve - statutory welfare reserve盈余公积-储备基金 Surplus reserve - reserve fund盈余公积-企业发展基金 Surplus reserve - enterprise development fund盈余公积-利润归还投资 Surplus reserve - reture investment by investment 主营业务收入 Sales主营业务成本 Cost of sales主营业务税金及附加 Sales tax营业费用 Operating expenses管理费用 General and ad-ministrative expenses财务费用 Financial expenses投资收益 Investment income其他业务收入 Other operating income营业外收入 Non-operating income补贴收入 Subsidy income其他业务支出 Other operating expenses营业外支出 Non-operating expenses所得税 Income tax一、资产类 assets现金 cash on hand银行存款 cash in bank其他货币资金 other cash and cash equivalent短期投资 short-term investment短期投资跌价准备 short-term investments falling price reserve应收票据 notes receivable应收股利 dividend receivable应收利息 interest receivable应收帐款 accounts receivable坏帐准备 bad debt reserve预付帐款 advance money应收补贴款 cover deficit receivable from state subsidize其他应收款 other notes receivable在途物资 materials in transit原材料 raw materials包装物 wrappage低值易耗品 low-value consumption goods库存商品 finished goods委托加工物资 work in process-outsourced委托代销商品 trust to and sell the goods on a commission basis受托代销商品 commissioned and sell the goods on a commission basis 存货跌价准备 inventory falling price reserve分期收款发出商品 collect money and send out the goods by stages待摊费用 deferred and prepaid expenses长期股权投资 long-term investment on stocks长期债权投资 long-term investment on bonds长期投资减值准备 long-term investment depreciation reserve 固定资产 fixed assets累计折旧 accumulated depreciation工程物资 project goods and material在建工程 project under construction固定资产清理 fixed assets disposal无形资产 intangible assets开办费 organization/preliminary expenses长期待摊费用 long-term deferred and prepaid expenses待处理财产损溢 wait deal assets loss or income负债类 debts短期借款 short-term loan应付票据 notes payable应付帐款 accounts payable预收帐款 advance payment代销商品款 consignor payable应付工资 accrued payroll应付福利费 accrued welfarism应付股利 dividends payable应交税金 tax payable其他应交款 accrued other payments其他应付款 other payable预提费用 drawing expenses in advance 长期借款 long-term loan应付债券 debenture payable长期应付款 long-term payable递延税款 deferred tax住房周转金 revolving fund of house 三、所有者权益 owners equity股本 paid-up stock资本公积 capital reserve盈余公积 surplus reserve本年利润 current year profit利润分配 profit distribution四、成本类 cost生产成本 cost of manufacture制造费用 manufacturing overhead五、损益类 profit and loss (p/l)主营业务收入 prime operating revenue 其他业务收入 other operating revenue 折扣与折让 discount and allowance投资收益 investment income补贴收入 subsidize revenue营业外收入 non-operating income主营业务成本 operating cost主营业务税金及附加 tax and associate charge 其他业务支出 other operating expenses存货跌价损失 inventory falling price loss营业费用 operating expenses管理费用 general and ad-ministrative expenses 财务费用 financial expenses营业外支出 non-operating expenditure所得税 income tax以前年度损益调整 adjusted p/l for prior year。

CHAPTER 5 Fixed assets and depreciation

Expensing fixed assets

Fixed assets generally have a finite life – as

they age (technically, commercially), their

1. How do we determine tha appropriate value of an asset at the point of acquisition?

2. How do we systematically recognise the expensing of the asset over time?

Source: IAS 16 - Property, Plant and Equipment

Use with Global Financial Accounting and Reporting ISBN 1-84480-265-5 © 2005 Peter Walton and Walter Aerts

Introduction Section 1 - General principles of asset

valuation Section 2 – Specific asset valuation

problems

Use with Global Financial Accounting and Reporting ISBN 1-84480-265-5 © 2005 Peter Walton and Walter Aerts

❖ Can include internal costs

Subsequent expenditure is added to the cost only if it will produce economic benefits beyond its originally assessed performance

无形资产+固定资产作价合同模板

无形资产+固定资产作价合同模板英文回答:Intangible Asset + Fixed Asset Valuation Contract Template.Introduction:This contract template is designed for the valuation of both intangible assets and fixed assets. It provides a framework for parties involved in a transaction to determine the value of these assets and establish the terms and conditions of the agreement. The template can be customized to suit the specific needs of the parties involved.1. Parties to the Contract:The contract should clearly identify the parties involved in the transaction. This includes the buyer andthe seller, along with any other relevant entities or individuals.2. Description of Assets:The contract should provide a detailed description of the intangible assets and fixed assets that are being valued. This includes information such as the nature of the assets, their condition, and any relevant documentation or records.3. Valuation Methodology:The contract should outline the methodology to be used for valuing the assets. This may include methods such as market-based valuation, income-based valuation, or cost-based valuation. The parties should agree on the specific approach to be used.4. Valuation Date:The contract should specify the date on which thevaluation will be conducted. This is important as asset values may fluctuate over time, and it ensures that both parties are working with the same set of information.5. Consideration:The contract should state the consideration to be paid for the assets. This may be a fixed amount, a percentage of the total asset value, or any other agreed-upon form of consideration.6. Terms and Conditions:The contract should include any additional terms and conditions that are relevant to the transaction. This may include provisions regarding payment terms, warranties, dispute resolution, or any other important aspects of the agreement.7. Confidentiality:The contract should include provisions to protect theconfidentiality of any sensitive information that may be shared during the valuation process. This ensures that both parties maintain the privacy and security of their respective assets.Conclusion:This template provides a comprehensive framework for valuing both intangible assets and fixed assets. By clearly outlining the parties involved, the assets being valued, the valuation methodology, and the terms and conditions of the agreement, this contract template helps facilitate a smooth and transparent transaction.中文回答:无形资产+固定资产作价合同模板。

固定资产处理审批手续流程

固定资产处理审批手续流程英文回答:Fixed Asset Disposal Approval Process.1. Initiation of Disposal Request.The department or individual responsible for the fixed asset initiates a disposal request.The request typically includes information such as the asset's description, condition, and reason for disposal.2. Review and Approval by Department Manager.The department manager reviews the disposal request and approves or rejects it.If approved, the manager signs the request and forwards it to the appropriate authority.3. Finance Department Review.The finance department reviews the request to ensure that the asset is properly accounted for and that its disposal proceeds are recorded accurately.The finance department may also verify the asset's condition and consult with the department requesting disposal.4. Approval by Senior Management.Senior management, typically represented by the CFO or CEO, reviews the request and makes a final approval decision.Senior management considers factors such as theasset's value, disposal method, and potential impact on the company.5. Disposal Execution.Once approved, the disposal plan is executed as per the chosen disposal method, such as sale, scrap, or donation.The proceeds from the disposal are recorded accordingly and used for designated purposes.6. Asset Removal and Documentation.The asset is physically removed from the company's premises.Relevant documentation, such as disposal receipts or transfer agreements, is maintained for record-keeping purposes.中文回答:固定资产处理审批手续流程。

Focus-ERP Fixed Assets

ContentsFixed Assets (2)Fixed Assets Tree (3)Asset Details (4)Depreciation Details (6)Depreciation Query (9)Accounting Links (10)Asset Usage (11)Asset Transfer (12)Asset Maintenance (13)Asset Repairs (14)Change Asset Value (15)Asset Disposal (16)Fixed Assets Report (17)Fixed Assets Report (18)Depreciation Schedule (19)Post Depreciation Entries (20)Fixed AssetsFocus now brings you a fully integrated Fixed Assets Module, capable of managing the Fixed Assets inventory in any Organization. The Module comprises a List of all the Fixed Assets in a Tree Format, similar to the Accounts Tree or Products Tree. You have complete flexibility in defining Asset Groups, to classify your Fixed Assets as per your requirements. Besides this, you have options to record full details of each Asset, right from the time of purchase until disposal of the same. Focus makes it simple for you to maintain records of each Asset by incorporating separate Screens for an Asset‟s Usage, Maintenance, Repairs, Transfer and Disposal.The Fixed Assets Menu is displayed when selected from the Fixed Assets option of the Main Menu, as shown below.The various options in the Fixed Assets Module are shown below.∙Fixed Assets Tree∙Assets Usage∙Transfer of Assets∙Asset Maintenance∙Asset Repairs∙Change Asset Value∙Disposal of Assets∙Fixed Assets Report∙Depreciation Schedule∙Post Depreciation EntriesLet‟s look at each of these options in detail on the following pages.Fixed Assets TreeThe Fixed Assets window is displayed when selected under the Fixed Assets Tree option of the Fixed Assets Menu.The Fixed Assets Tree is similar to the Accounts or Products Tree, wherein you can create and arrange all your Fixed Asset items under separate groups and classify them at different levels as required.Apart from this, you can create/add Asset records, edit or delete them as required. The Procedure to be followed for all operations in the Tree is exactly similar to that described earlier in the Accounts or Products Tree. Kindly refer to the Chapter entitled “Getting Started-Create Masters” for more information on this topic.Asset DetailsTo create a new Fixed Assets Record, click Add in the Fixed Assets Tree window displayed on the previous page. The Fixed Assets Master window is displayed as shown above. It consists of four Panels, each containing details about the Fixed Asset. Here in the Asset Details Panel shown, we enter the Description of the Asset, the Asset Code, Alias, the Asset Type, the Location, Value, Date of Purchase, the Vendor or Supplier, Purchase Date, Price, Quantity, Cumulative Depreciation, Insured Value, Scrap Value, Purchase Limit and Quantity Limit.computer in .jpg format. Click the button beside the Photo field and the Browse window is displayed to help you jpg file of the asset, as shown on the next page.Select the file and click Open to attach the photo to the Asset record.One more option is available in Fixed Assets master creation screen wherein you can opt for creating multiple Asset codes for as much quantity as you are mentioning in the quantity field.This option will create e.g. if quantity is given as “10” then 10 different assets with running sequence of codes and asset names.This will reduce the burden of creating multiple asset codes for bulk purchases of assets.You can now move to the next Panel – Depreciation Details.Depreciation DetailsIn the Depreciation Details Panel, you have to select the parameters based on which the Depreciation will be calculated for the Asset. These parameters are explained below.Depreciation MethodsDepreciation calculations vary from one Asset Type to another, depending on the Method of Depreciation selected. Focus provides for the following methods explained below.∙Based on Usage:This method is usually applied to Plant and Machinery, where the wear and tear of the Machines is proportionate to the usage of the machines. Hence, the Starting Unit of the Machine at the beginning of the accounting period is required for Depreciation calculations.∙Charge Off: A fixed amount is written off as Depreciation every year, until the Total Asset Value is fully written off.∙Straight Line Method:In this method, the Original Cost of the Asset is written off in equal instalments over the expected useful life of the Asset. Hence, if the Original Cost of the Asset is 10,000/- and the expected useful life of the Asset is 5 years, the Depreciation Amount for the Asset would be 2,000/- per year, calculated pro-rata for the number of days of any given period.∙WDV Diminishing Value: Here, the Depreciation for the year is calculated ata fixed rate on the Written Down Value (WDV) of the Asset i.e. the Cost of theAsset minus the Depreciation calculated upto the previous year. Thus, if the Cost of an Asset is 10,000/- and the Rate of Depreciation is 10%, the Depreciation calculations would be done as shown below.Year 1: Cost = 10,000 Depreciation = 1,000Year 2: WDV = 9,000 Depreciation = 900Year 3: WDV = 8,100 Depreciation = 810Depreciation would continue until the value of the Asset is fully diminished.∙WDV Diminishing Value Calculated Half Yearly: This method is similar to the previous method (WDV Diminishing Value). The only difference is that the calculations are done pro-rata for the number of days of any given period.Select the Method of Depreciation from the selection box as required.Select the Unit of Usage. The Unit of Usage would not be applicable to all types of Assets; it would mainly apply to those Assets where the Method of Depreciation selected is …Based on Usage‟. The default units are KM, Hour, Production Quantity or Production Runs.Enter the Rate of Depreciation applicable to the Asset. Rates of Depreciation may be different for different types of Fixed Assets.Select the Date of Commencement starting from which the Asset is to be depreciated.Enter the Starting Unit applicable, if …Based on Usage‟ is selected as Method of Depreciation.The Depreciation for the Asset will be calculated based on the parameters entered above.In Straight Line method normally Focus asks for the number of years in which the asset will be written off.If required we can even maintain Depreciation in Straight Line method and have the depreciation rate mentioned.If this option is required we have you tick on the option of “Always define Depreciation R ate as %age” in Preferences under Masters tab as shown in the figure below.If this option is checked on, then Focus will ask for the “Rate of depreciation” for such assets where the method of depreciation is selected as “Straight Line”.Depreciation QueryThe Depreciation Query Panel allows you to find out the Accumulated Depreciation for an Asset on any given date. Select the Date from the Date combo box. The Year-to-Date Depreciation and the Prior Year C/F Depreciation figures are shown, together with the Meter Reading, if applicable.Accounting LinksAccounting Links are necessary for the generation and posting of Depreciation and Asset Disposal entries. You have to nominate the Accounts, which will be updated, when the Depreciation or Asset Transfer/Disposal entries are generated.Select the Asset Account Code, the Accumulated Depreciation Account Code, the Depreciation P/L Account Code and the Sales Account.Once you have completed entering the details on all four Panels of the Fixed Assets Master window, click OK to create the record or click Cancel to close the Fixed Assets Master window and return to the Main Menu without adding the record to the Master.If you wish to add more fields to the Fixed Assets Master record, click the Customize button. The Customization of Fields window is displayed, wherein you can add extra fields to the record. The procedure for this is similar to that of the Accounts Master or Products Master. (Refer the chapter entitled Getting Started-Create Masters).Asset UsageThe Usage or Consumption of certain Assets can be recorded either through consumption of units which is determined by their meter readings or by recording the quantum of production it is used for, based on the Batch Numbers.The Asset Usage entry screen displayed above provides for the recording of the usage or consumption of the same at user-selected intervals.The Usage Entry window is displayed when selected under the Assets Usage option of the Fixed Assets Menu.The Usage No. is similar to the Document or Voucher No. in Financial Accounting. Enter or select the Usage No., Date, Unit and Asset Code of the Asset.If usage of the Asset is determined by the Meter Readings, in the Meter Reading box, enter the Last Reading and New Units consumed. The New Reading is automatically calculated and displayed.If usage is based on the Production Quantity, in the Usage based on Production box, enter the Batch Number, Product and Quantity produced.Click Update to save the Usage record or click Cancel to close the Usage Entry window and return to the Main Menu.Asset TransferIt is inevitable that movable Assets like machinery, furniture, computer equipment, etc. are transferred from one location or branch to another to meet requirements for the same.When Assets are moved from one place to another, it becomes necessary to record the change of location of the asset and also account for the depreciation of the same in the new location from the date of transfer.The Transfer window is displayed when selected under the Transfer of Assets option of the Fixed Assets Menu.The Transfer No. is like a Document No. reference. Enter the Transfer No. Select the Date, Asset Code and the Location to which the Asset is being transferred. Enter the current value of the Asset. In the Commencement Date box, select the date from which Depreciation of the Asset should commence at the new location. Usually, depreciation continues from the Original date of purchase. Optionally, you can choose the New radio button and select a new date, from which Depreciation calculations at the new location should commence.Click Update to save the Asset Transfer record or click Cancel to close the Transfer window and return to the Main Menu.Asset MaintenanceSome Fixed Assets like machinery usually have a Maintenance Contract or Agreement setup to ensure that they are maintained in good running condition at all times.The Asset Maintenance screen allows the user to keep track of the Maintenance Contracts for the Assets, thereby fulfilling an important requirement in Fixed Asset management.The Maintenance window is displayed when selected under the Maintenance option of the Fixed Assets Menu.Enter the Contract No. Select the Asset Code, Commencement Date and Expiry Date of the Contract, and the Vendor from the respective combo boxes. Enter the No. of Units, the Rate and the Value of the Contract.Click OK to save the Contract Details or click Cancel to close the Maintenance window and return to the Main Menu.Asset RepairsDuring the life of an Asset, it is necessary to keep track of the performance of the machine, the number of times it has undergone repairs, the spares or parts added/replaced, the value of such repairs, etc.The above Asset Repair screen helps the user to keep track of repairs and servicing for all equipments and machines whenever they are carried out.The Repair window is displayed when selected under the Repairs option of the Fixed Assets Menu.Enter the Repair No. Select the Date of Repair and the Asset Code. Enter the Quantity, Rate and Value of the Asset. Next select the Warranty Date. Enter the details of the Parts Added or Replaced and finally enter the Remarks, if any.Click OK to save the Asset Repair details or click Cancel to close the Repair window and return to the Main Menu.Change Asset ValueSometimes, the value of an Asset may need to be enhanced or increased, whenever modifications are made to the Asset. For this purpose, Focus provides the Change Value option, wherein the User can add to the value of the Asset and specify the Commence-ment Date for Depreciation to be calculated on the additional value.The Change Value window is displayed when selected under the Change Assets Value option of the Fixed Assets Menu.Enter the Document No. Select the Asset Code and Date from the respective combo boxes. Enter the Additional Value by which the Asset Value is to be increased. Select the Commencement Date for Depreciation to be calculated and enter details of the Additional Value in the Remarks text box.Click Save to update the changes or click Cancel to close the Change Value window and return to the Main Menu.Asset DisposalAssets are generally disposed of when they have served their useful life and purpose or if they become obsolete. If the Asset is disposed, the details of the transaction need to be recorded, since Depreciation should not be calculated on an Asset from the date of disposal.The Asset Disposal screen above helps the user to record the details of such Asset disposal transactions, as and when they take place.The Disposal window is displayed when selected under the Disposal of Assets option of the Fixed Assets Menu.The Disposal No. is like a Document reference. Enter the Disposal No. Select the Date and Asset Code from the respective combo boxes. Enter the Accumulated Depreciation amount for the Asset to be disposed. Select the Sale Account and enter the Quantity and Value of the Sale.Click OK to update the database or click Cancel to close the Disposal window and return to the Main Menu.Fixed Assets ReportThe Fixed Assets Report in Focus allows you to view the Master information for all Fixed Assets in a customized format.The Report Parameters are displayed in the Tree window shown above. You can select individual Assets, whose details are to be displayed in the report, by clicking them in the Tree window. Click Select All Items if you wish to view the Report for all Assets. Click Unselect All to reset the selection at any time and make a fresh selection. Select the period for which you wish to see the report by selecting the From and To Dates in the Report Dates box. Select the Report Layout from the Report combo box. Lastly, select the report Output Destination from the Output box. Click OK to process the report or click Cancel to close the Tree window and return to the Main Menu.Note that you can customize any existing Report Layout by selecting the Layout from the Layout combo and then clicking the Customize Report button. You can also filter the Fixed Assets Report as per your requirements. Click Set Report Filters to enter the criteria for filtering the Report. For more information on how to customize or filter the report, please refer to the chapter entitled Reporting Basics.A sample Fixed Assets Report is displayed on the next page.Fixed Assets ReportDepreciation ScheduleThe Depreciation Schedule Report gives you the complete details of the Assets during the selected period. Full details are available and the report can be customized to suit the user‟s requirements. The Report is entitled …Fixed Assets Schedule‟ and printed in columnar format. A sample report is displayed below.Post Depreciation EntriesBased on the information defined in the Fixed Assets Master, the Depreciation on Fixed Assets can be auto-calculated and entries for the same generated/posted to the respective Accounts, nominated in the Accounting Links Panel for each Asset.The Depreciation Posting window is displayed when you select this option from the Fixed Assets Menu.Enter the Depreciation Posting Date. If you wish to have a single entry posted after consolidating the Depreciation for the Asset Groups, select the Consolidated Posting checkbox.Click OK to process and post the Depreciation entries or click Cancel to close the Depreciation Posting window and return to the Main Menu.。

会计翻译

Fixed Assets-固定资产Assets that are relatively permanent, such as land and buildings, andequipment.土地、房屋以及设备等相对固定的资产Certified Management Accountant (CMA)-注册管理会计师A professional accountant who has met certain educational and experience requirements, passed a qualifying exam in the field and been certified by the institute of Certified Management Accountants.是指达到一定的教育和经验要求,且在该领域通过了由注册管理会计师协会的认证考试的一种专业会计师。

Certified Public Accountant (CPA)-注册会计师An accountant who passes a series of examinations established by the American Institute of certified Public accountants.Cost of Goods Sold (or Cost of Goods Manufactured)-商品销售成本A measure of the cost of merchandise sold or cost of new materials and supplies used for producing items for resale.-是指一种商品销售成本或用于生产转售的新材料和补给成本Currrent Assets-流动资产Assets that will be converted into cash within one year.一年内兑现的资产Depreciation-折旧、贬值The systematic write-off of the cost of a tangible asses over its estimateduseful life.是指某种超过预计使用寿命的有形资产成本折旧DoubleEntry Bookkeeping-复式薄记The concept of writing every business transacion in two places. 是指在两个地方记录每一笔业务。

固定资产管理流程

PwC175

3

Fixed Assets - Measures/Cost Drivers

No of Business Unit FTEs per Fixed Assets FTE

5,200

1,400 350

90 percentile

Median

10 percentile

Fixed Assets cost per Business Unit FTE (in £s) £31

Accounts Payable

Purchasing PwC175

Circuit Provisioning

Project accounting

Audit

7

Fixed Assets - Level 1 Overview

Notification procedures

System validation controls

Maintain Asset

Register FA 1.4

Reports

types or categories

Requester FA accountant Finance

AP system FA accounting staff Cost centre managers

FA accounting staff Cost centre manager Management accountant

Verified FA

reports

Register

Reconciled GL A/ c’s

Verify Physical Assets FA 1.6

Authorised GL adjustments

FA accounting staff Inventory staff

中国会计科目的中英文对照一、资产类Assets

⼀、资产类 Assets流动资产 Current assets货币资⾦ Cash and cash equivalents1001 现⾦ Cash1002 银⾏存款 Cash in bank1009 其他货币资⾦ Other cash and cash equivalents'100901 外埠存款 Other city Cash in bank'100902 银⾏本票 Cashier's cheque'100903 银⾏汇票 Bank draft'100904 信⽤卡 Credit card'100905 信⽤证保证⾦ L/C Guarantee deposits'100906 存出投资款 Refundable deposits1101 短期投资 Short-term investments'110101 股票 Short-term investments - stock'110102 债券 Short-term investments - corporate bonds'110103 基⾦ Short-term investments - corporate funds'110110 其他 Short-term investments - other1102 短期投资跌价准备 Short-term investments falling price reserves应收款 Account receivable1111 应收票据 Note receivable银⾏承兑汇票 Bank acceptance商业承兑汇票 Trade acceptance1121 应收股利 Dividend receivable1122 应收利息 Interest receivable1131 应收账款 Account receivable1133 其他应收款 Other notes receivable1141 坏账准备 Bad debt reserves1151 预付账款 Advance money1161 应收补贴款 Cover deficit by state subsidies of receivable库存资产 Inventories1201 物资采购 Supplies purchasing1211 原材料 Raw materials1221 包装物 Wrappage1231 低值易耗品 Low-value consumption goods1232 材料成本差异 Materials cost variance1241 ⾃制半成品 Semi-Finished goods1243 库存商品 Finished goods1244 商品进销差价 Differences between purchasing and selling price1251 委托加⼯物资 Work in process - outsourced1261 委托代销商品 Trust to and sell the goods on a commission basis1271 受托代销商品 Commissioned and sell the goods on a commission basis 1281 存货跌价准备 Inventory falling price reserves1291 分期收款发出商品 Collect money and send out the goods by stages 1301 待摊费⽤ Deferred and prepaid expenses长期投资 Long-term investment1401 长期股权投资 Long-term investment on stocks'140101 股票投资 Investment on stocks'140102 其他股权投资 Other investment on stocks1402 长期债权投资 Long-term investment on bonds'140201 债券投资 Investment on bonds'140202 其他债权投资 Other investment on bonds1421 长期投资减值准备 Long-term investments depreciation reserves股权投资减值准备 Stock rights investment depreciation reserves债权投资减值准备 Bcreditor's rights investment depreciation reserves1431 委托贷款 Entrust loans'143101 本⾦ Principal'143102 利息 Interest'143103 减值准备 Depreciation reserves1501 固定资产 Fixed assets房屋 Building建筑物 Structure机器设备 Machinery equipment运输设备 Transportation facilities⼯具器具 Instruments and implement1502 累计折旧 Accumulated depreciation1505 固定资产减值准备 Fixed assets depreciation reserves房屋、建筑物减值准备 Building/structure depreciation reserves机器设备减值准备 Machinery equipment depreciation reserves1601 ⼯程物资 Project goods and material'160101 专⽤材料 Special-purpose material'160102 专⽤设备 Special-purpose equipment'160103 预付⼤型设备款 Prepayments for equipment'160104 为⽣产准备的⼯具及器具 Preparative instruments and implement for fabricate 1603 在建⼯程 Construction-in-process安装⼯程 Erection works在安装设备 Erecting equipment-in-process技术改造⼯程 Technical innovation project⼤修理⼯程 General overhaul project1605 在建⼯程减值准备 Construction-in-process depreciation reserves1701 固定资产清理 Liquidation of fixed assets1801 ⽆形资产 Intangible assets专利权 Patents⾮专利技术 Non-Patents商标权 Trademarks, Trade names著作权 Copyrights⼟地使⽤权 Tenure商誉 Goodwill1805 ⽆形资产减值准备 Intangible Assets depreciation reserves专利权减值准备 Patent rights depreciation reserves商标权减值准备 trademark rights depreciation reserves1815 未确认融资费⽤ Unacknowledged financial charges待处理财产损溢 Wait deal assets loss or income1901 长期待摊费⽤ Long-term deferred and prepaid expenses1911 待处理财产损溢 Wait deal assets loss or income'191101待处理流动资产损溢 Wait deal intangible assets loss or income'191102待处理固定资产损溢 Wait deal fixed assets loss or income。

51固定资产

【例】:某企业购入不需安装的机器设备一台,

用银行存款支付买价20 000元,增值税3 400 元,包装费100元,运输费200元(其中7%可作 为增值税进项税额抵扣),机器设备投入使用。

根据以上资料,编制会计分录如下: 固定资产原始价值 =20 000+100+200×(1-7%)=20 286

重置价值

重置价值是指企业在当前的条件下,重新购置

同样的固定资产所需的全部耗费的货币表现。

折余价值

折余价值也称为净值,是指固定资产原值减去 已提折旧后的余额。

现值

现值是指固定资产在使用期间以及处置时产生

的未来净现金流量的折现值。

固定资产的确认条件

(1)该固定资产包含的经济利益很可能流入

第五章 固定资产及无形资产

第一节 固定资产 第二节 无形资产

第一节 固定资产(fixed assets)

一、概述 二、固定资产的初始计量 三、固定资产折旧

四、固定资产的后续支出

五、固定资产的期末计价 六、固定资产的处置

固定资产的性质

固定资产(fixed assets)是企业生产经营过程中

例5-1:甲机械公司以生产销售W1型号的机床

为主业,2000年12月31日,甲公司有W1型号 机床10台待售,单价15 000元,估计使用寿命 为10年。甲公司有厂房一座,价值800万元, 估计使用年限为20年,已使用5年。W1型号机 床主要由A材料加工而成,A材料的单价为 5000元,公司现有库存10件。另外,在公司管 理人员办公室内有电话两部,单价300元,估 计可使用年限为5年;空调一部,单价5000元, 估计可使用年限为5年。

的实际成本计入工程成本,借记“在建工程” 科目,贷记“工程物资”科目。盘盈的工程物 资,作相反的处理,即借记“工程物资”,贷 记“在建工程”。 企业自营建造的固定资产在交付使用时,应根 据自营工程的实际成本,借记“固定资产”科 目,贷记“在建工程”科目。

新加坡企业所得税申报表

@ 2014 IRAS Singapore

Updated as at 21 Apr 2014

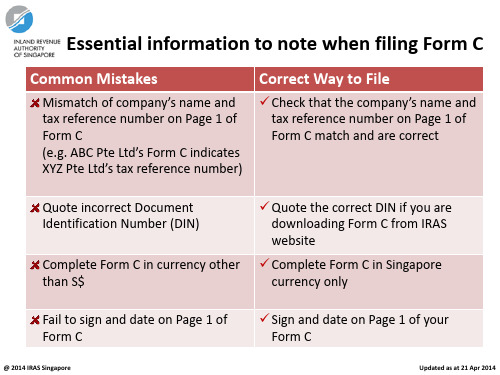

Essential information to note when filing Form C

Page 3: Box 11 (Chargeable Income to be taxed at rates other than 17%) • Include all chargeable income taxable at concessionary rates. • Use the incentive type codes in Appendix 1B on Page 7 of Explanatory Notes to Form C. • Do not enter any exempt income.

Page 2: Box 1d • If net rent after deducting rental expenses (before Industrial Building Allowances/Land Intensification Allowances) is negative, enter $0 in Box 1d. • Claim for Industrial Building Allowances (IBA)/Land Intensification Allowances (LIA) against rental income should be entered in Box 1a. E.g. If IBA/LIA claim is computed to be $150,000 for YA 2014, enter $150,000 in Box 1a and indicate “X” on the left.

ACCAF3知识点:Revaluationoffixedassets

ACCA F3 知识点:Revaluation of fixed assets今天浦江财经给大家说说ACCA F次口识点中的Revaluation of fixed assets,也就是关于固定资产的重新评估。

During a period of inflation, the current monetary value of fixed assets such as land and buildings may be much in excess of their net book value. A business may wish to reflect the current worth of such assets on its balance sheets.The difference (usually a surplus) between the revalued amount and the amount net book value needs to be credited to an account separate from the profit and loss account as the gain is not realized (i.e. there is no intention of turning the asset into cash by selling it). This account is known as a revaluation reserve.The journal entry for an upward revaluation is:Dr Land and building XXCr Revaluation reserve XX这里还有三点注意的地方,大家需要记住:(a) When a non -current asset has been revalued, the charged for depreciation should be based on the revalued amount and the remaining useful life of the asset.(b) This charge will be higher than depreciation prior to the revaluation.(c) The excess of the new depreciation charge over the old depreciation charge should be transfer from the revaluation reserve to accumulated profits. (within the capital section of the balance sheet)。

汽车固定资产处置税务处理会计科目

汽车固定资产处置税务处理会计科目- 借:累计折旧(汽车固定资产) Debit: Accumulated Depreciation (Automobile Fixed Assets)- 借:汽车固定资产减值准备 Debit: Impairment Provision for Automobile Fixed Assets- 贷:汽车固定资产 Credit: Automobile Fixed Assets- 贷:固定资产处置损失 Credit: Loss on Disposal of Fixed Assets- 贷:固定资产处置款 Credit: Proceeds from Disposal of Fixed Assets- 借:租赁过渡费用 Debit: Lease Transition Expenses- 贷:应付租赁费用 Credit: Accounts Payable- Lease Expenses- 借:资产报废成本 Debit: Asset Scrapping Cost- 贷:累计折旧(资产报废) Credit: Accumulated Depreciation (Scrapped Asset)- 借:处置应收款 Debit: Accounts Receivable - Disposal Proceeds- 贷:应收款项 Credit: Accounts Receivable- 借:应交增值税 Debit: VAT Payable- 贷:应交税金费用 Credit: Tax Expense Payable- 借:一般所得税费用 Debit: General Income Tax Expense- 贷:应交税金费用 Credit: Tax Expense Payable- 借:其他相关费用 Debit: Other Related Expenses- 贷:应付相关费用 Credit: Accounts Payable- Related Expenses请注意,这仅是一个假设的科目列表,实际的会计科目结构可能因所在国家/地区的规定和企业的具体情况而有所不同。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

明细表FIXED ASSETS 固定资产明细表FIXED ASSETS日期:2013-04-30AssetsNo设 备 名 称购买日期使用地点原值(RMB)购买原值折旧年数折旧年限月折旧额已折旧额剩余折旧额预留残值(5%)净值EquipmentPurchase Date LocationPurchase Price Actual PriceDepreci ation years Depreciable life Monthdepreciation Already depreciationResidual depreciation Reserve salvage value Net value AD001打印机(Printer )2005/11/17Office 2099.00AD002传真机(Electrograph)2005/11/17Office 789.00AD003空调(Air-condition)2006/2/5Office 2240.005年AD004空调(Air-condition)2006/2/5Office 2240.005年AD005空调(Air-condition)2006/2/5QC 2240.005年AD006-015空调10台(Air-condition)2011/8/10Toolroom 26500.003年2011.9.1-2014.8.31736.1114722.2011777.800.0011777.8AD016金税卡2010/3/23Office 1210.261416.001年2010.5.1-2011.4.300.001210.260.000.000.00AD017-023购7台电脑2009.11-37#Office 33600.003年2009.12.1-2012.11.300.0033600.000.000.000.00AD024购1台电脑(pengping PC)2010/8/9office 1965.812300.001年2010.9.1-2011.8.310.001965.810.000.000.00AD025购1台电脑(Jennifer PC)2011/11/19office 2905.983400.001年2013.1.31-2013.12.31242.17968.681937.300.001937.30QC002万能测长仪(Universal Length 2006/2/9QC 85470.08100000.0010年2006.5.1-2016.4.30702.8355894.7125301.874273.5029575.37QC003投影仪(Projection Machine)2007/4/12QC 23000.0010年2007.7.1-2017.6.30185.7912560.469475.331150.0010625.33QC004加密狗软件2011/9/19QC 4273.505000.002年2012.1.1-2013.12.31237.423561.30712.200.00712.20TR003CNC车床(CNC Lathe)2006/3/30Toolroom 64957.2776000.0010年2006.5.1-2016.4.30533.9542487.0319222.383247.8622470.24TR004普通车床(Conventional Lathe)2006/4/19Toolroom 19230.7722500.0010年2006.5.1-2016.4.30152.8112768.125501.11961.546462.65TR005金属代锯(Metal Saw)2006/5/22Toolroom 1840.005年2006.6.1-2011.5.310.001656.000.00184.00184.00TR0013相交流电机2006/6/22Toolroom 4721.13TR0023相交流电机2006/6/22Toolroom TR006研磨机(Lapping m/c)2006/6/22Toolroom 4000.0010年TR007研磨机(Lapping m/c)2006/6/22Toolroom 4000.0010年TR008研磨机(Lapping m/c)2006/6/22Toolroom 4000.0010年TR009研磨机(Lapping m/c)2006/6/22Toolroom 4000.0010年TR010螺纹磨床M-16(Thread Grinder 2006/10/19Toolroom 400000.0010年2006.11.1-2016.10.313254.89243294.40136705.6020000.00156705.60TR011平面磨床(Surface Grinder)2006/10/24Toolroom 24500.0010年2006.11.1-2016.10.31199.3614901.878373.131225.009598.13TR012外圆磨床(Cyl Grinder) 2006/10/24Toolroom 21800.0010年2006.11.1-2016.10.31177.3913259.557450.451090.008540.45TR013数控车床(CNC Lathe)2007/7/11Toolroom 62000.0010年2007.10.1-2017.9.30499.6232420.3426479.663100.0029579.66TR014立式加工中心(VMC)2007/7/12Toolroom 240303.50217000.0010年2007.9.1-2017.8.311937.98127513.63100774.6912015.18112789.87TR016锯床(Hack Saw)2007/9/2Toolroom 18000.0010年2007.10.1-2017.9.30145.059412.357687.65900.008587.65TR017空压机(Compressor Air)2007/9/30Toolroom 34500.0010年2007.11.1-2017.10.31277.8017773.9415001.061725.0016726.06TR018铣床(Millinh m/c)2007/9/2Toolroom 7000.0010年2007.10.1-2017.9.3056.413660.372989.63350.003339.63TR019螺纹磨床M-33(Thread Grinder 2008/11/3Toolroom 46114.6930600.0010年2009.1.1-2019.12.31367.8718793.3925015.562305.7427321.30TR020螺纹磨床M-16(Thread Grinder 2008/11/3Toolroom 59714.6844200.0010年2009.1.1-2019.12.31476.3724336.0932392.852985.7435378.59TR021干燥箱(Tempering Furnace) 2010/10/19Toolroom 7521.378800.0010年2010.12.1-2020.11.3059.541726.665418.64376.075794.71TR022柜式深冷箱(Sub-Zero M/C)2010/9/17Toolroom 38581.6530253.0010年2010.12.1-2020.11.30305.448857.7621494.811929.0823423.89TR023万能工具磨(universal tool g 2011/7/26Toolroom 24000.008年2011.08.1-2019.07.31237.504987.5017812.501200.0019012.50TR024无心磨床(旧)(Centreless Gr 2011/11/24Toolroom 64360.9958670.008年2012.1.1-2019.12.31636.9110407.1050735.843218.0553953.89TR025外圆磨床(旧)(Cyl Grinder) 2011/11/24Toolroom 44736.1538901.008年2012.1.1-2019.12.31442.707233.7235265.622236.8137502.43TR026立式车床(旧)(Stand Lathe)2011/11/24Toolroom 7700.707334.008年2012.1.1-2019.12.3176.201245.126070.54385.046455.58TR027铣床(旧)(Millinh m/c)2011/11/24Toolroom 6160.355867.008年2012.1.1-2019.12.3160.96996.104856.23308.025164.25TR028螺纹磨床M-33(旧)(Thread Gr 2011/11/24Toolroom 36031.1831886.008年2012.1.1-2019.12.31356.565826.1828403.531801.5630205.09TR029螺纹磨床M-16(旧)(Thread Gr 2011/11/24Toolroom 57650.3451018.008年2012.1.1-2019.12.31570.509321.9645445.862882.5248328.38TR030QC 硬度计(sclerometer)2012/2/8Toolroom 3333.333900.0010年2012.3.1-2022.2.2826.39369.462797.20166.672963.87TR031喷砂机(sand blasting machin 2012/2/14Toolroom 4487.185250.0010年2012.3.1-2022.2.2835.52497.283765.54224.363989.90TR032内圆磨床(internal grinder)2012/2/24Toolroom 93162.39109000.0010年2012.4.1-2022.3.31737.549588.0278916.254658.1283574.37TR033切割机(cutting machine)2012/4/25Toolroom 1260.005年2012.5.1-2017.4.3020.00240.00957.0063.001020.00AD026财务软件(software)2013/3/14Office 2380.003年2013.4.1-2016.3.3162.8162.812198.19119.002317.19AD027打印机(Printer )2013/3/21Office3119.665年2013.4.1-2018.3.3149.4049.402914.28155.983070.26合 计 (RMB)1598201.3014031.37770761.80750070.7476754.30826825.04336.002006.5.1-2016.4.31131.0438.54236.0610482.374717.63800.005517.632982.261502.81144.40144.402743.600.006384.000.001738.87336.005年10年2006.4.1-2011.3.310.002006.3.1-2011.2.280.002006.8.1-2016.7.31。