The influence of accounting information on the financial management of enterprises and the

新视野大学英语(第三版)U校园读写教程4第二单元答案

Answer the following questions briefly based on the given pictures.1) Lipstick is used to apply color to the lips. 2)2) 第一篇阅读Nail polish is applied to fingernails or toenails to decorate and / or protect the nails. 3) Eye shadow is applied to areas around the eyes, usually on the eyelids and under the eyebrows, to make the eyes stand out or look more attractive. 4) Mascara is used to enhance the eyes. It may help make the eyelashes darker, thicker and longer. 5) Eyeliner is used to draw lines around the eyes so as to createa more beautiful contour. 6) Powder foundation is used to tone the face and give it an even, uniform color. It can cover flaws, and some can also protect the face from damage caused by sunlight. Facial masks, sunscreen, facial cream, eye cream, etc. Reference: 1. • Yes, I do use some of these products once in a while. For example, when I go to parties, I often apply lipstick and eyeliner. On such occasions, putting on some makeup gives me a good mood. • No, I don't use any of them because I'm a male and these products are all for women. However, I do apply sunscreen when I stay outdoors for a lo ng time in summer. 2. • Yes, they are generally used by women. What men usually do may be just shaving and having a haircut. • No, I don't think only women use cosmetics. Although men in general do not use such products in daily life, it is possible that male actors and singers wear some makeup when they perform.1. The sentence means that it is very difficult, or even impossible, for a man to give a right answer when a woman asks him how she looks, no matter how hard he thinks about it and how many different answers he tries.2. Men are satisfied with being average-looking, paying little attention to their looks. In contrast, women pay great attention to their body and image, considering their appearance as not good enough even if they are in fact attractive.3. The interaction of many psychological and societal factors, for example, their childhood experiences with toys, and the influence of the media.4. Girls' toys are proportioned to have extreme measures of the body (e.g. in terms of height, weight and waist size), whereas boys' toys can look weird rather than handsome.5. It implies that men pay little attention to the details of their appearance.6.Cindy Crawford is mentioned as an example to show that the beauty industry and the media have great influence on women's devotion to physical beauty and the use of beauty products.27. The author thinks that the claim is not right since men in fact pay little attention to the details of women's appearance. 8. Women think so because men do not even care about their own appearance. For instance, a man often does not bother to clean the cream in his hair or ears after shaving.1. I think there are three main factors accounting for women's greater attention to appearance. The first are cultural traditions. It is common in many cultures that people put high value on beauty when they look at women. The second is the requirement of certain jobs. For example, in China airline companies set certain criteria for appearance (e.g. in terms of height and weight) when they recruit stewards and stewardesses. Finally, the influence of the media is another strong factor which shapes women's pursuit of physical beauty. There are a lot of advertisements of cosmetics and skincare products in various media such as TV, magazines and newspapers. They often have celebrities as the spokesperson for the advertised products, which makes women have an illusion that they could look as good as those famous stars if they use the products. In short, these three factors exert immense influence on how women value appearance.2. • Yes. On certain formal occasions, a person, either female or male, has to pay attention to his attire. Sample cases are job interviews, business meetings, weddings, and banquets. This is because to dress properly is an important element of successful completion of these events. • No. People do not have to care what others think of them as long as they feel comfortable and satisfied with their looks themselves. After all, this is the most important source of happiness to people.3. In my opinion, the important traits of human beauty include two types, one for appearance and one for inner qualities. Features that characterize a beautiful appearance are a good-looking body, proper clothes and accessories, as well as use of makeup that matches the occasion or event one is attending. Inner qualities that make a person beautiful mainly include good manners and positive personality traits such as honesty, bravery or friendliness.4. • Yes.Women should pay great attention to their appearance and hence need to wear makeup. This is because beauty is, believe it or not, usually an important quality for women to succeed, for example, when they want to look for a job or an ideal husband. • No. What really makes a person beautiful is inner beauty rather than physical appearance. A beautiful look can't last long, but inner beauty, for example, intelligence and honesty, may make a person successful and happy throughout his life. 5. I would market a new product by three means. First, I can ask a celebrity, for example a famous movie star or a supermodel, to be the brand spokesperson on TV. This is a common practice in the advertising industry, and I think it is very effective. Second, I will hire people to distribute flyers and give away free samples of the product on the streets, so the product can reach potential customers directly. Inaddition, I may post advertisements on public transportation vehicles such as buses and subways. In this way, the commercials can be seen by a large number of people.人们普遍认为,威廉・莎士比亚是最伟大的英语作家和世界杰出的戏剧家。

新视野大学英语(第三版)U校园读写教程4第二单元secionA答案

Answer the following questions briefly based on the given pictures.1) Lipstick is used to apply color to the lips.2) Nail polish is applied to fingernails or toenails to decorate and / or protect the nails.3) Eye shadow is applied to areas around the eyes, usually on the eyelids and under the eyebrows, to make the eyes stand out or look more attractive.4) Mascara is used to enhance the eyes. It may help make the eyelashes darker, thicker and longer.5) Eyeliner is used to draw lines around the eyes so as to create a more beautiful contour.6) Powder foundation is used to tone the face and give it an even, uniform color. It can cover flaws, and some can also protect the face from damage caused by sunlight. Facial masks, sunscreen, facial cream, eye cream, etc.Reference:1.• Yes, I do use some of these products once in a while. For example, when I go to parties, I often apply lipstick and eyeliner. On such occasions, putting on some makeup gives me a good mood.• No, I don't use any of them because I'm a male and these products are all for women. However, I do apply sunscreen when I stay outdoors for a long time in summer. 2.• Yes, they are generally used by women. What men usually do may be just shaving and having a haircut.• No, I don't think only women use cosmetics. Although men in general do not use such products in daily life, it is possible that male actors and singers wear some makeup when they perform.1. The sentence means that it is very difficult, or even impossible, for a man to give a right answer when a woman asks him how she looks, no matter how hard he thinks about it and how many different answers he tries.2. Men are satisfied with being average-looking, paying little attention to their looks. In contrast, women pay great attention to their body and image, considering their appearance as not good enough even if they are in fact attractive.3. The interaction of many psychological and societal factors, for example, their childhood experiences with toys, and the influence of the media.4. Girls' toys are proportioned to have extreme measures of the body (e.g. in terms of height, weight and waist size), whereas boys' toys can look weird rather than handsome.5. It implies that men pay little attention to the details of their appearance.6. Cindy Crawford is mentioned as an example to show that the beauty industry and the media have great influence on women's devotion to physical beauty and the use of beauty products.7. The author thinks that the claim is not right since men in fact pay little attention to the details of women's appearance.8. Women think so because men do not even care about their own appearance. For instance, a man often does not bother to clean the cream in his hair or ears after shaving.1.I think there are three main factors accounting for women's greater attention to appearance. The first are cultural traditions. It is common in many cultures that people put high value on beauty when they look at women. The second is the requirement of certain jobs. For example, in China airline companies set certain criteria for appearance (e.g. in terms of height and weight) when they recruit stewards and stewardesses. Finally, the influence of the media is another strong factor which shapes women's pursuit of physical beauty. There are a lot of advertisements of cosmetics and skincare products in various media such as TV, magazines and newspapers. They often have celebrities as the spokesperson for the advertised products, which makes women have an illusion that they could look as good as those famous stars if they use the products. In short, these three factors exert immense influence on how women value appearance.2.• Yes. On certain f ormal occasions, a person, either female or male, has to pay attention to his attire. Sample cases are job interviews, business meetings, weddings, and banquets. This is because to dress properly is an important element of successful completion of these events.• No. People do not have to care what others think of them as long as they feel comfortable and satisfied with their looks themselves. After all, this is the most important source of happiness to people.3.In my opinion, the important traits of human beauty include two types, one for appearance and one for inner qualities. Features that characterize a beautiful appearance are a good-looking body, proper clothes and accessories, as well as use of makeup that matches the occasion or event one is attending. Inner qualities that make a person beautiful mainly include good manners and positive personality traits such as honesty, bravery or friendliness.4.• Yes. Women should pay great attention to their appearance and hence need to wear makeup. This is because beauty is, believe it or not, usually an important quality for women to succeed, for example, when they want to look for a job or an ideal husband.• No. What really makes a person beautiful is inner beauty rather than physical appearance. A beautiful look can't last long, but inner beauty, for example, intelligence and honesty, may make a person successful and happy throughout his life.5.I would market a new product by three means. First, I can ask a celebrity, for example a famous movie star or a supermodel, to be the brand spokesperson on TV. This is a common practice in the advertising industry, and I think it is very effective. Second, I will hire people to distribute flyers and give away free samples of the product on the streets, so the product can reach potential customers directly. Inaddition, I may post advertisements on public transportation vehicles such as buses and subways. In this way, the commercials can be seen by a large number of people.1.deficient2.prosecution3.outragestrand4.appeased5.conformity6.strandplement8.transient9.appliances10.o utfitdeficient, orientation, confrontation, composer, binder, scanner, manufacturer, erase, imperialist, leftist, terrorist, humanistdomination scanners humanist confrontation leftists orientation erased terrorists manufacturers binder imperialists composersachieving gorgeous considered context accessories appreciated complexion handsome comment admirationin hopes of came up with excused herself was obsessed with reaching out to voice an opinion on live up to in terms ofWhen you get yourself ready to go to school or work in the morning, or attend a party in the evening, you may have to do various preparations. What you consider as essential to prepare largely depends on whether you are a female or a male. Women and men take care of their appearance in different ways, which are mainly shown in three areas.One difference lies in the variety of beauty products that women and men use. Women have a great variety of tools and skincare products; for example, combs and clips for hair, brushes for powder foundation, and eyeliners for eyebrows, creams for face, to name just a few. Men, however, do not use so many things. They may comb their hair, but they seldom use cosmetics.Another difference involves the amount of clothes women and men have. Females usually have many more clothes than men do. You may well be familiar with movie scenes in which a woman tries on the outfits in her wardrobe one after another and still hesitates about which one to wear. Unlike females, males do not buy themselves piles of clothes as long as they still have something at home.人们普遍认为,威廉・莎士比亚是最伟大的英语作家和世界杰出的戏剧家。

会计英语作文

会计英语作文Title: The Importance of Accounting in Business Management。

Accounting plays a pivotal role in the successful management of businesses worldwide. It serves as the language of business, providing crucial information for decision-making, financial reporting, and performance evaluation. In this essay, we will delve into the significance of accounting in business management.First and foremost, accounting serves as a tool for financial reporting. Through various financial statements such as the balance sheet, income statement, and cash flow statement, businesses communicate their financial health and performance to stakeholders, including investors, creditors, and regulators. These reports provide insights into the company's profitability, liquidity, and solvency, enabling stakeholders to make informed decisions.Furthermore, accounting facilitates effective decision-making by providing timely and accurate financial information. Managers rely on accounting data to assess the profitability of different projects, allocate resources efficiently, and formulate strategic plans. For instance, cost accounting helps managers determine the cost of producing goods or services, enabling them to set competitive prices and maximize profitability.Moreover, accounting plays a crucial role in compliance and regulatory requirements. Businesses must adhere to various accounting standards and regulations imposed by regulatory bodies such as the Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission (SEC). Compliance with these standards ensures transparency, consistency, and credibility in financial reporting, fostering trust among stakeholders.In addition to external reporting, accounting also aids in internal control and decision support. Internal controls help safeguard assets, prevent fraud, and ensure the accuracy of financial records. By implementing internalcontrol measures such as segregation of duties, authorization procedures, and regular audits, businesses mitigate risks and enhance operational efficiency.Furthermore, managerial accounting provides valuable insights for internal decision-making. Through techniques such as budgeting, variance analysis, and performance measurement, managers can evaluate the financial performance of different departments, identify areas for improvement, and make informed decisions to achieve organizational goals.Moreover, accounting serves as a basis for performance evaluation and incentive systems. By measuring key performance indicators (KPIs) such as return on investment (ROI), profitability ratios, and efficiency metrics, businesses can assess the effectiveness of their operations and reward employees based on their contributions to the company's success. Performance-based incentives motivate employees to perform better and align their efforts with organizational objectives.Additionally, accounting facilitates financial planning and forecasting, allowing businesses to anticipate future trends, risks, and opportunities. Through budgeting, forecasting, and financial modeling, managers can develop strategic plans, allocate resources effectively, and mitigate potential risks. Accurate financial forecasts enable businesses to adapt to changing market conditions, capitalize on emerging opportunities, and maintain long-term sustainability.In conclusion, accounting plays a multifaceted role in business management, encompassing financial reporting, decision support, compliance, internal control, performance evaluation, and strategic planning. By providing timely and accurate financial information, accounting enables businesses to make informed decisions, comply with regulatory requirements, optimize performance, and achieve their strategic objectives. Therefore, accounting is indispensable for the successful management and operation of businesses in today's competitive marketplace.。

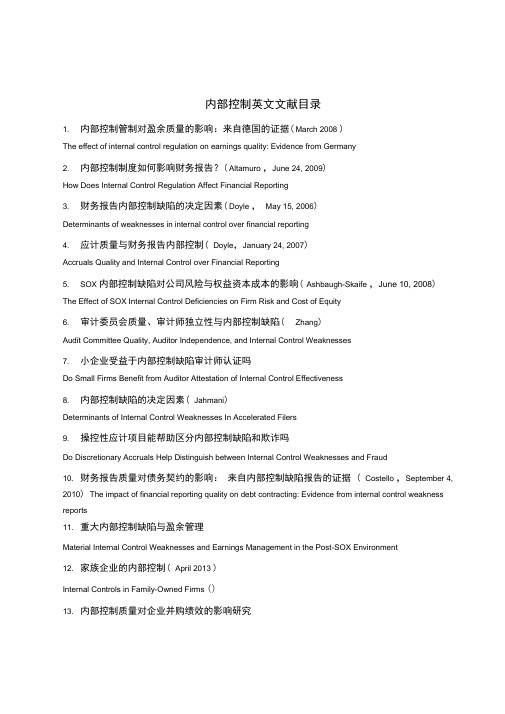

(完整版)内部控制英文文献目录

内部控制英文文献目录1. 内部控制管制对盈余质量的影响:来自德国的证据( March 2008 )The effect of internal control regulation on earnings quality: Evidence from Germany2. 内部控制制度如何影响财务报告?( Altamuro ,June 24, 2009)How Does Internal Control Regulation Affect Financial Reporting3. 财务报告内部控制缺陷的决定因素( Doyle ,May 15, 2006)Determinants of weaknesses in internal control over financial reporting4. 应计质量与财务报告内部控制( Doyle,January 24, 2007)Accruals Quality and Internal Control over Financial Reporting5. SOX 内部控制缺陷对公司风险与权益资本成本的影响( Ashbaugh-Skaife ,June 10, 2008) The Effect of SOX Internal Control Deficiencies on Firm Risk and Cost of Equity6. 审计委员会质量、审计师独立性与内部控制缺陷( Zhang)Audit Committee Quality, Auditor Independence, and Internal Control Weaknesses7. 小企业受益于内部控制缺陷审计师认证吗Do Small Firms Benefit from Auditor Attestation of Internal Control Effectiveness8. 内部控制缺陷的决定因素( Jahmani)Determinants of Internal Control Weaknesses In Accelerated Filers9. 操控性应计项目能帮助区分内部控制缺陷和欺诈吗Do Discretionary Accruals Help Distinguish between Internal Control Weaknesses and Fraud10. 财务报告质量对债务契约的影响:来自内部控制缺陷报告的证据 ( Costello ,September 4, 2010) The impact of financial reporting quality on debt contracting: Evidence from internal control weakness reports11. 重大内部控制缺陷与盈余管理Material Internal Control Weaknesses and Earnings Management in the Post-SOX Environment12. 家族企业的内部控制( April 2013 )Internal Controls in Family-Owned Firms ()13. 内部控制质量对企业并购绩效的影响研究Study on the Impact of the Quality of Internal Control on the Performance of M&A14. 内部控制质量与信用违约互换利差( January 2014)Internal Control Quality and Credit Default Swap Spreads15. 家族企业内部控制:特征和后果Internal Control in Family Firms: Characteristics and Consequences16. 内部控制报告与会计信息质量:洞察”遵守或解释的“内部控制制度Internal control reporting and accounting quality :Insight "comply-or-explain" internal control regime17. 内部控制报告与会计稳健性Internal Control Reporting and Accounting Conservatism18. 会计信息质量影响产品市场契约吗?来自政府合同授予的证据( March 2014 )Does Accounting Quality Influence Product Market Contracting? Evidence from Government Contract Awards19. 公司特征与财务报告质量:尼日利亚制造业上市公司的证据20. 内部控制情况与专家审计师选择The Association between Internal Control Situations and Specialist Auditor Choices21. 审计费用反应了控制风险的风险溢价吗( 2013-07 )Do Audit Fees Reflect Risk Premiums for Control Risk?22. 内部控制质量与审计定价Internal Control Quality and Audit Pricing under the Sarbanes-Oxley Act23. 内部控制缺陷与权益资本成本:来自萨班斯法案404 节披露的证据Internal Control Weakness and Cost of Equity: Evidence from SOX Section 404 Disclosures24. 内部控制缺陷与信息不确定性Internal Control Weaknesses and Information Uncertainty25. 重大内部控制缺陷与股票价格崩溃危险:来自404 条款披露的证据( May 2013 )Material Weaknessin Internal Control and Stock Price Crash Risk: Evidence from SOX Section 404 Disclosure 26. SOX 内部控制缺陷对公司风险与权益资本成本的影响The Effect of SOX Internal Control Deficiencies on Firm Risk and Cost of Equity27. 信用评级、债务成本与内部控制信息披露:SOX302 和SOX404 法的比较28. 萨班斯-奥克斯利法案对会计信息债务契约价值的影响The Effect of Sarbanes-Oxley on the Debt Contracting Value of Accounting Information29. 财务报告内部控制的不利意见与审计师解聘/辞职Adverse Internal Control over Financial Reporting Opinions and Auditor Dismissals/Resignations30. 新管理人员任命与随后的SOX 法案404 的意见Appointment of New Executives and Subsequent SOX 404 Opinion31. 萨班斯奥克斯利:有关萨班斯法案404 影响的证据Sarbanes-Oxley: The Evidence Regarding the Impact of Sox 40432. 内部控制有效性自愿披露的经济决定因素及后果:从首次公开发行的证据( March 2013 ) Economic Determinants and Consequences of Voluntary Disclosure of Internal Control Effectiveness: Evidence from Initial Public Offerings33. 非营利组织中内部控制问题的原因和后果The Causes and Consequences of Internal Control Problems in Nonprofit Organizations34. SOX 内部控制披露在公司控制权市场中的价值The Value of SOX Internal Control Disclosures in the Market for Corporate Control35. 内部控制缺陷与销售、一般的及行政费用的非对称性行为Internal Control Weakness and the Asymmetrical Behavior of Selling, General, and Administrative Costs36. 内部控制缺陷及补救措施披露对投资者感知的盈余质量的影响The Impact of Disclosures of Internal Control Weaknesses and Remediation on Investor-Perceived Earnings Quality37. 内部控制缺陷与美国上市的中国公司与美国公司的审计师SOX Internal Control Deficiencies and Auditors of U.S.-Listed Chinese versus U.S. Firms38. 内部控制信息披露与代理成本—来自瑞士的非金融类上市公司的证据( January 2013) Internal Control Disclosure and Agency Costs Evidence from Swiss listed non-financial Companies39. 萨班斯奥克斯利法案与公司投资:来自自然实验的新证据The Sarbanes-Oxley Act and Corporate Investment: New Evidence from a Natural Experiment40. 国内投资者保护、所有权结构与交叉上市公司遵守SOX 要求披露内部控制缺陷Home Country Investor Protection, Ownership Structure and Cross-Listed Firms 'Compliance with SOX-Mandated Internal Control Deficiency Disclosure41. 审计师对披露重大缺陷相关风险的看法Auditors ' Percenpsti o f the Risks Associated with Disclosing Material Weaknesses42. 交叉上市公司提供与美国公司相同质量的披露?来自萨班斯-奥克斯利法案302 条款下的内部控制缺陷信息披露的证据Do cross-listed firms provide the same quality disclosure as U.S. firms? Evidence from the internal control deficiency disclosure under Section 302 of the Sarbanes-Oxley Act43. 内部控制缺陷与并购绩效Internal Control Weaknesses and Acquisition Performance44. 萨班斯-奥克斯利法案302 条款下的内部控制缺陷对审计费用的影响The Effect of Internal Control Weakness under Section 404 of the Sarbanes-Oxley Act on Audit Fees45. 审计师对财务报告内部控制的评价对审计费用、债务成本及净遵从收益The Effect of Auditors ' Assessment of Internal Control of over Financial Reporting on Audit Fees, Cost of Debt and Net Compliance Benefit46. 上市公司披露的信息含量与萨班斯-奥克斯利法案Information Content of Public Firm Disclosures and the Sarbanes-Oxley Act47. 财务错报与股票市场的契约:从增发的证据Financial Misstatements and Contracting in the Equity Market: Evidence from Seasoned Equity Offerings48. 公司治理质量与SOX 302 条款下内部控制报告Corporate Governance Quality and Internal Control Reporting Under Sox Section 30249. 审计委员会质量、审计师独立性与内部控制缺陷Audit Committee Quality, Auditor Independence, and Internal Control Weaknesses50. SOX404 条款的影响:成本,盈余质量与股票价格The Effect of SOX Section 404: Costs, Earnings Quality, and Stock Prices51. 内部控制缺陷与银行贷款契约:来自SOX404 条款披露的证据Internal Control Weakness and Bank Loan Contracting: Evidence from SOX Section 404 Disclosures52. 审计师对财务报告内部控制的决策:分析、综合和研究方向Auditors I'nternal Control Over Financial Reporting Decisions: Analysis, Synthesis, and Research Directions 53. 应计质量与财务报告内部控制( Doyle ,The Accounting Review, forthcoming )Accruals Quality and Internal Control over Financial Reporting54. 业绩基础CEO 和CFO 薪酬对内部控制质量的影响The impact of performance-based CEO and CFO compensation on internal control quality55. 内部控制重大缺陷与CFO 薪酬Internal Control Material Weaknesses and CFO Compensation56. 财务报告内部控制缺陷的决定因素Determinants of weaknesses in internal control over financial reporting57. 内部控制与管理指南Internal Control and Management Guidance58. 2002 萨班斯-奥克斯利法案302 条款下内部控制缺陷的市场反应以及这些缺陷的特征Market Reactions to the Disclosure of Internal Control Weaknesses and to the Characteristics of thoseWeaknesses under Section 302 of the Sarbanes Oxley Act of 200259. 自愿报告内部风险管理和控制系统的经济激励Economic Incentives for Voluntary Reporting on Internal Risk Management and Control Systems60. 后萨班斯法案时代审计意见的信息含量The information content of audit opinions in the post-sox era61. 上市公司披露的信息含量与萨班斯-奥克斯利法案( April, 2010 )Information Content of Public Firm Disclosures and the Sarbanes-Oxley Act62. 信息摩擦如何影响公司资产流动性的选择?萨班斯法案404 条款的影响How do Informational Frictions Affect the Firm s Choice of A'sset Liquidity? The Effect of SOX Section 404 63. 已审计的信息披露给资本市场参与者带来利益是什么( December 19, 2013)What are the benefits of audited disclosures to equity market participants64. 诉讼风险与审计定价:公众股权的作用( January 7, 2013)Litigation Risk and Audit Pricing: The Role of Public Equity65. 萨班斯-奥克斯利法案对IPO 和高收益债券发行人的影响The Impact of Sarbanes-Oxley on IPOs and High Yield Debt Issuers66. 来自金融危机的公司治理的经验教训The Corporate Governance Lessons from the Financial Crisis67. 谁对企业欺诈吹口哨Who Blows the Whistle on Corporate Fraud68. 内部控制缺陷与现金持有价值Internal Control Weakness and Value of Cash Holdings69. 民族文化和制度环境对内部控制信息披露的影响The impact of national culture and institutional Environment on internal control disclosures70. 财务报告质量与权益资本成本之间联系的讨论:一些个人的意见( June 6, 2013)Some Personal Observations on the Debate on the Link between Financial Reporting Quality and the Cost of Equity Capital71. 使用盈利预测同时估计企业层面的权益资本成本和长期增长Using Earnings Forecasts to Simultaneously Estimate Firm-Specific Cost of Equity and Long-Term Growth72. 高管薪酬差距与权益资本成本Executive Pay Disparity and the Cost of Equity Capital73. 财务报告质量与公司债券市场(博士论文,Mingzhi Liu, 2011 )Financial Reporting Quality and Corporate Bond MarketsReferencesAboody, D., J. Hughes, and J. Liu. (2005) Earnings quality, insider trading, and cost of capital. Journalof Acco un ti ng Research 43: 651 -673.Akins, B., J. Ng and R. Verdi (2012) Investor competition over information and the pricing of information asymmetry. The Accounting Review 87(1): 35-58.Ali, A., A. Klein and J. Rosenfeld. (1992) Analysts ' use of information abouttrpaenrsmitaonryent andearnings components in forecasting annual EPS. The Accounting Review 67: 183-198.Amihud, Y., and H. Mendelson. (1986) Asset pricing and the bid-ask spread. Journal of Financial Econo mics 17: 223 —49.Artiach, T. and P. Clarkson. (2011) Disclosure, conservatism and the cost of equity capital: A review of the foundation literature. Accounting and Finance 51(1): 2-49.Ashbaugh-Skaiffe, H., D. Collins, W. Kinney, Jr., and R. LaFond (2009) The effect of SOX internal control deficiencies on firm risk and cost of equity. Journal of Accounting Research 47(1): 1-43.Armstrong, C., J. Core, D. Taylor and R. Verrecchia (2011) When does information asymmetry affect the cost of capital? Journal of Accounting Research 49(1): 1-40.Balakrishnan, K., R. Vashishtha and R. Verrecchia (2012) Aggregate competition, information asymmetry and cost of capital: Evidence from equity market liberalization. Working paper, University of Pennsylvania.Barron, O., O. Kim, S. Lim and D. Stevens (1998) Using analysts forecasts to measure properties on analysts ' information environmeTnth.e Accounting Review 73: 421-433.Barry, C., and S. Brown. (1985) Differential information and security market equilibrium. Journal of Financial and Quantitative Analysis 20: 407 T22.Barth, M., W. Beaver, and W. Landsman (2001) The relevance of value-relevance literature for financial accounting standard setting: Another view, Journal of A”ccounting and Economics (Sept): 77-104.Barth, M., Y. Konchitchki and W. Landsman (2013) Cost of capital and earnings transparency. Journal of Accounting and Economics , forthcoming.Beyer A., D. Cohen, T. Lys and B. Walther (2010) The financial reporting environment: Review of the recent literature. Journal of Accounting and Economics 50: 296-343.Bhattacharya, N., F. Ecker, P. Olsson, and K. Schipper (2012) Direct and mediated association among earnings quality, information asymmetry, and the cost of capital, The Accounting Review 87(2): 449-482. Botosan, C. (1997) Disclosure level and the cost of equity capital. The Accounting Review 72: 323 -350. Botosan, C., and M. Plumlee. (2002) A re-examination of disclosure level and the expected cost of equity capital. Journal of Accounting Research 40: 21 ZO.Botosan, C., M. Plumlee and Y. Xie (2004) The role of information precision in determining the cost of equity capital. Review of Accounting Studies 9 (2-3): 233-259.Botosan, C., and M. Plumlee. (2005) Assessing alternative proxies for the expected risk premium. The Accounting Review 80: 21-53.Botosan, C., M. Plumlee and H. Wen. (2011) The relation between expected returns, realized returns, and firm risk characteristics. Contemporary Accounting Research 28(4): 1085-1122.Brown, P. and T. Walter (2012) The CAPM: Theoretical validity, empirical intractability and practical applications. Abacus 1-7.Callahan, C., R. Smith and A. Spencer (2012) An examination of the cost of capital implications of FIN 46. The Accounting Review 87(4): 1105-1134.Chava, S., and A. Purnanandam (2010) Is default risk negatively related to stock returns? Review of Financial Studies 23: 2523-2559.Chen, S., B. Miao and T. Shevlin (2013) A new measure of disclosure quality: The level of disaggregation of accounting data in annual reports. Working paper, The University of Texas at Austin. Christensen, P., L. de la Rosa and G. Feltham (2010) Information and the cost of capital: An ex ante perspective. The Accounting Review 85(3): 817-848.Clarkson, P., J. Guedes and R. Thompson (1996) On the diversifiability, observability, and measurement of estimation risk. Journal of Financial and Quantitative Analysis 31: 69084.Claus, J., and J. Thomas (2001) Equity premia as low as three percent? Evidence from analysts earnings forecasts for domestic and international stock markets. The Journal of Finance 56(5): 1629-1666.Clinch G., and B. Lombardi (2011) Information and the cost of capital: the Easley- O' Hara(2004) modelwith endogeneous information acquisition. Australian Journal of Management 36(5): 5-14.Coles, J., U. Loewenstein, and J. Suay. (1995) On equilibrium pricing under parameter uncertainty. The Journal of Financial and Quantitative Analysis 30: 347 -374.Core, J., (2001) A review of the empirical disclosure literature: Discussion. Journal of Accounting and Economics 31: 441-456.Core, J., W. Guay and R. Verdi, (2008) Is accruals quality a priced risk factor? Journal of Accountingand Economics 46: 2-22.Daniel, K. and S. Titman, 1997, Evidence on the characteristics of cross-sectional variation in common stock returns. Journal of Finance 52, 1-33.Daske, H., L Hail, C. Leuz and R. Verdi (2008) Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research 46: 1085-1142.Daske, H., L Hail, C. Leuz and R. Verdi, (2013) Adopting a label: Heterogeneity in the economic consequences around IAS/IFRS adoptions. Journal of Accounting Research 51(3):495-548.Dechow, P. and I. Dichev. (2002) The quality of accruals and earnings: the role of accrual estimation errors. The Accounting Review 77 (Supplement): 35-59.Dechow, P., W. Ge and C. Schrand (2010) Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics 50: 344-401.Dhaliwal, D., L. Krull and W. Moser (2005) Dividend taxes and implied cost of equity capital. Journal of Accounting Research 43(5): 675-708.Dhaliwal, D., L. Krull and O. Li (2007) Did the 2003 Tax Act reduce the cost of equity capital? Journal of Accounting and Economics 43(1): 121-150.Diamond, D., and R. Verrecchia. (1991) Disclosure, liquidity, and cost of capital. Journal of Finance 46: 1325 -59. Dye, R., (2001) An evaluation of “ essayson disclosure a”nd the disclosure literature in accounting. Journal of Accounting and Economics 32: 181-235.Easley, D., S. Hvidkjaer and M. O'Hara.(2002) Is information risk a determinant of asset returns. Journal of Finance 57: 2185-2221.Easley, D., and M. O' Hara. (2004) Information and the cost of capital. Journal of Fi nance 59: 1553-1583. Easton, P. (2004) PE ratios, PEG ratios, and estimating the implied expected rate of return on equity capital. The Accounting Review 79(1): 73-96.Easton, P., and S. Monahan. (2005) An evaluation of accounting based measures of expected returns. The Accounting Review 80: 501 -538.Easton, P., and S. Monahan. (2010) Evaluating accounting-based measures of expected returns: Easton and Monahan and Botosan and Plumlee redux. Working paper, University of Notre Dame.Ecker, F., J. Francis, I. Kim, P. Olsson, and K. Schipper (2006). A returns-based representation of earnings quality. The Accounting Review 81: 749 -780.Fama, E., and J. MacBeth. 1973. Risk, return, and equilibrium: Empirical tests. Journal of Political Economy 81: 607-636.Fama, E., and K. French. (1992) The cross-section of expected stock returns. Journal of Finance 47(2): 427-465. Fama, E., and K. French. (1993) Common risk factors in the returns on bonds and stocks. Journal of Financial Economics 33: 3-56.Francis, J., LaFond, R., Olsson, P., and K. Schipper. (2004) Costs of equity and earnings attributes. The Accounting Review 79: 967-1010.Francis, J., LaFond, R., Olsson, P., and K. Schipper. (2005) The market pricing of accruals quality. Journal of Accounting & Economics 39: 295-327.Francis, J., Nanda, D., and P. Olsson. (2008) Voluntary disclosure, information quality, and costs of capital. Journal of Accounting Research 46 (1): 53-99.Gebhardt,W., C. Lee and B. Swaminathan (2001) Towards an ex ante cost of capital. Journal of Accounting Research 39(1): 135-176.Goh, B-W., J. Lee, C-Y. Lim and T. Shevlin (2013) The effect of corporate tax avoidance on the cost of equity. Working paper, Singapore Management University.Gow, I., G. Ormazabal and D. Taylor (2010) Correcting for cross-sectional and time-series dependence in accounting research The Accounting Review 85(2): 483-512.Gray, P., P. Koh and Y. Tong (2009) Accruals quality, information risk and cost of capital: Evidence from Australia. Journal of Business Finance and Accounting 36(1-2): 51-72.Guay, W., S.P. Kothari and S. Shu (2011) Properties of implied cost of capital using analysts forecasts. Australian Journal of Management 36(2): 125-149.Hail, L. (2002) The impact of voluntary corporate disclosure on the ex-ante cost of capital for Swiss firms European Accounting Review 11: 741-773.Hail, L., and C. Leuz. (2006) International differences in the cost of equity capital: Do legal institutions and securities regulation matter? Journal of Accounting Research 44(3): 485-531.Healy, P., and K. Palepu (2001) Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405-440. Hirshleifer, D., K. Hou, and S.H. Teoh (2012) The accrual anomaly: Risk or mispricing? ManagementScienee (58-2); 320 -335.Holthausen, R., and R. Watts (2001) The relevance of value-relevance literature for financial accounting standard setting. Journal of Accounting and Economics (Sept): 3-75.Hribar, P. and T, Jenkins. (2004) The effect of accounting restatements on earnings revisions and the estimated cost of capital. Review of Accounting Studies 9(2-3): 337-356.Hughes, J. S., J. Liu, and J. Liu. (2007) Information asymmetry, diversification, and cost of capital. The Accounting Review 82: 705-729.Hughes, J. S., J. Liu, and J. Liu. (2009) On the association between expected returns and implied cost of capital R”eview of Accounting Studies 14: 246-259.Hutchens, M. and S. Rego (2013) Tax risk and the cost of equity capital. Working paper, Indiana University. Hwang, L-S., W-J. Lee, S-Y. Lim and K-H. Park, (2013) Does information risk affect the implied cost of equity capital? An analysis of PIN and adjusted PIN. Journal of Accounting and Economics 55(2-3): 148-167.Kim, D., and Y. Qi (2010) Accruals quality, stock returns, and macroeconomic conditions. The Accounting Review 85(3): 937-978.Klein, R., and V. Bawa. (1977) The effect of estimation risk on optimal portfolio choice. Journal of Financial Economics 3: 215-231.Kothari, S.P., X. Li and J. Short. (2009) The effect of disclosures by management, analysts, and financial press oncost of capital, return volatility, and analyst forecasts: A study using content analysis. The Accounting Review82(5): 1255-1297.Kravet, T. and T. Shevlin. (2010) Accounting restatements and information risk. Review of Accounting Studies 15: 264-294.Kyle, A. (1985) Continuous auctions and insider trade. Econometrica 53(6): 1315-1335.Lambert, R., C. Leuz, and R. Verrecchia. (2007) Accounting information, disclosure, and the cost of capital. Journal of Accounting Research 45(2): 385-420.Lambert, R., C. Leuz, and R. Verrecchia. (2012) Information asymmetry, information precision, and the cost of capital. Review of Finance 16: 1-29.Lambert, R., (2009) Discussion of “onthe association between expected returns and implied cost of capital R”eview of Accounting Studies 14: 260-268.Leuz, C., and R. Verrecchia (2004) Firms ' capital allocatio n choices, in formati on qhuaCys tandcapital. Work ing paper, Uni versity of Penn sylva nia.Li, V., T. Shevli n and D. Shores (2013) Revisit ing the AQ measure of accrual quality. Work ing paper, Uni versityof Wash ington.Lys, T., and S. Sohn. (1990) The associati on betwee n revisi ons of finan cial an alyst forecastsearning and security price cha nges. Jour nal of Acco un ti ng and Econo mics 13: 341-363.Mashruwala, C. and S. Mashruwala (2011) The pric ing of accrual quality: January versus the rest of the year. TheAccou nting Review 86(4): 1349-1381.McInnis, J. (2010) Earnings smoothness, average returns and implied cost of equity capital. The Accou ntingReview 85(1): 315-341.Mohanram, P., and D. Gode (2013) Removing predictable analyst forecast errors to improve implied cost of equity estimates. Review of Acco un ti ng Studies 18: 443-478.Ogneva, M., K.R. Subramanyam, and K. Raghunandan (2007) Internal control weakness and cost of equity: Evidenee from SOX Section 404 disclosures. The Accou nti ng Review 82(5) :1255-1297.Ogneva, M., (2012) Accrual quality, realized returns, and expected returns: The importanee of con trolli ng forcash flow shocks, The Accou nting Review 87(4): 1415-1444.Peterse n, M., (2009) Estimati ng sta ndard errors in finance data pan els: Compari ng approaches. Reviewof Financial Studies 22(1): 435-480.Petkova, R. (2006) Do the Fama-Fre nch factors proxy for inno vati on in predictive variables? Journal of Finance61: 581-612.Reidl, E., and G. Serafeim (2011) In formati on risk and fair values: An exam in ati on of equity betas. Journal ofAccounting Research 49(4): 1083-1122.Strobl, G., (2013) Earnings manipulation and the cost of capital. Journal of Accounting Research, forthco ming. Verrecchia, R. (2001) Essays on disclosure. Journal of Accounting and Economics 32: 97-180.Vuolteenaho, T. (2002) What drives firm-level stock returns? The Journal of Finance 57: 233 -264.How Do Various Forms of Auditor Rotation Affect Audit Quality? Evidence from China内部控制质量、企业风险与权益资本成本一一理论分析与实证检验1. Accruals Quality and In ternal Con trol over Finan cial Report in g.Acco un ti ng Review, Oct2007, V ol.82 Issue52. Audit Committee Quality and Internal Control An Empirical Analysis.FullAccounting Review, Apr2005, Vol.80 Issue 23. Bala ncing the Dual Resp on sibilities of Busin ess Un it Con trollers Field and Survey Evide nee. Accounting Review, Jul2009, Vol. 84 Issue44. Corporate Governance and Internal Control over Financial Reporting A Comparison ofRegulatory Regimes Accou nting Review, May2009, Vol. 84 Issue 35. Ear nings Man ageme nt of Firms Report ing Material In ternal Con trol Weak nesses un der Sect ion 404of the Sarbanes-Oxley Act. Auditing, Nov2008, Vol. 27 Issue 26. Economic Incentives for V oluntary Reporting on Internal Risk Management and Control Systems.Auditing, May2008, V ol. 27 Issue 67. Firm Characteristics and Volu ntary Man ageme nt Reports on In ternal Con trol. Audit ing, Nov2006,Vol. 25 Issue28. Former Audit Partners on the Audit Committee and Internal Control Deficiencies. Accounting Review,Mar2009, Vol. 849.Internal Control Quality and Audit Pricing under the Sarbanes-Oxley Act . Auditing, May2008, Vol.2710.Internal Control Weakness and Cost of Equity Evidenee from SOX Section 404 Disclosures Accou nti ngReview, Oct2007, Vol. 8211.I nternal Control Weak nesses and In formatio n Un certai nty. Accou nting Review, May2008, Vol. 8312.lnternal Controls and the Detection of Management Fraud. Journal of Accounting Research, Sprin g99,Vol. 3713.Reduci ng Man ageme nt's In flue nee on Auditors Judgme nts An Experime ntal In vestigati on of SOX404 Assessme nts Acco un ti ng Review, Nov2008, V)l. 8314.SOX Section 404 Material WeaknessDisclosures and Audit Fees.Full Auditing, May2006, Vol. 2515.The Effect of SOX Internal Control Deficiencies and Their Remediation on Accrual Quality. AccountingReview, Jan2008, Vol. 8316.The Impact of SOX Section 404 Internal Control Quality Assessment on Audit Delay in the SOX Era.Auditing, Nov2006, Vol. 25Ashbaugh-Skaife, H., Collins, D. W., & Kinney Jr., W. R. (2007). The discovery and reporting of internal con trol deficie ncies prior to SOX-ma ndated audits. Jour nal of Acco unting and Economics, 44(1 —2), 166 -92.Ashbaugh-Skaife, H., Collins, D. W., Kinney Jr, W. R., & Lafond, R. (2009). The Effect of SOX Internal Control Deficiencies on Firm Risk and Cost of Equity. Journal of Accounting Research, 47(1),1 -43.Bahramian, A. (2011), Evaluation of the effectiveness of internal controls in an Investment Company, Master Thesis in Imam Hossein University, Iran.Daraby, M, (2006), analyzing the effect of strengthening internal controls, audit reports of companies listed on the Stock Audit, Master Thesis in Azan Islamic university.Doyle, J., Ge, W., & McVay, S. (2007). Determinants of weaknesses in internal control over financial reporting. Journal of Accounting and Economics, 44(1 -2), 193 -223.Feng, M., Li, C., & McVay, S. (2009). Internal control and management guidance. Journal of Accounting and Economics, 48(2 -3), 190 -209.Maham K., Poriya Nasab, A. (2000), Internal control) Integrated Framework( , Report of the Committee of the Commission Tardy, azman Hesabresy, Pages 118, 135.Ogneva, M., Subramanyam, K. R., & Raghunandan, K. (2007). Internal control weakness and cost of equity: evidence from SOX Section 404 disclosures. The Accounting Review, 82(5), 1255-1297.Rezaie Jahangoshaee, H, (1996). A analytical study of the degree of reliance of independent auditors on firms internal controls, Master Thesis, shahid Beheshti University, Iran.。

我对会计的了解英语作文

我对会计的了解英语作文Accounting is a critical field that plays a vital role in the success of businesses and organizations of all sizes. It involves the systematic recording, analyzing, and reporting of financial transactions and information to provide a clear picture of a company's financial health and performance. As an individual with a keen interest in finance and business, I have developed a deep understanding of the importance of accounting and its various aspects.At its core, accounting serves as the language of business, enabling stakeholders such as investors, creditors, and management to make informed decisions. It provides a structured framework for tracking and reporting on a company's assets, liabilities, revenues, and expenses, which are essential for monitoring financial performance, identifying areas for improvement, and ensuring compliance with relevant laws and regulations.One of the key functions of accounting is financial reporting. Accountants are responsible for preparing financial statements, including the balance sheet, income statement, and cash flowstatement, which offer a comprehensive view of a company's financial position and performance. These reports are not only crucial for internal decision-making but also serve as a means of communication with external stakeholders, such as investors and regulatory bodies.Accurate and timely financial reporting is crucial for maintaining transparency and building trust in the business community. Accountants must adhere to strict accounting standards and principles, such as the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS), to ensure the reliability and comparability of financial information. This attention to detail and adherence to professional standards is what sets accounting apart as a highly specialized and respected field.Beyond financial reporting, accounting encompasses a wide range of functions, including budgeting, cost analysis, tax preparation, and internal auditing. Budgeting, for instance, involves the allocation of financial resources to different areas of the business, allowing management to plan and control expenditures effectively. Cost analysis, on the other hand, helps organizations identify and manage their costs, ultimately improving profitability and operational efficiency.Tax preparation is another critical aspect of accounting, asbusinesses must comply with complex tax laws and regulations to avoid penalties and ensure they are paying the appropriate amount of taxes. Accountants play a crucial role in this process, helping organizations navigate the tax landscape and maximize their tax savings through legitimate means.Internal auditing, meanwhile, is a crucial function that ensures the accuracy and reliability of a company's financial records and internal controls. Accountants who specialize in internal auditing work to identify potential risks, detect fraudulent activities, and recommend improvements to the organization's financial management practices.The importance of accounting extends beyond the boundaries of individual businesses. At a broader level, accounting information is essential for the proper functioning of the financial system and the overall economy. Accurate and transparent financial reporting helps investors make informed decisions, facilitates the efficient allocation of capital, and contributes to the stability of the financial markets.Moreover, the field of accounting is constantly evolving, with new technologies and methodologies being introduced to improve the efficiency and accuracy of financial management. The rise of data analytics, for example, has enabled accountants to leverage large datasets and sophisticated algorithms to gain deeper insights into a company's financial performance, identify trends, and make moreinformed decisions.As the business landscape becomes increasingly complex and globalized, the role of accountants is becoming more multifaceted and strategic. In addition to their traditional financial reporting responsibilities, accountants are now expected to provide advisory services, offer insights on business strategy, and collaborate with cross-functional teams to drive organizational success.In conclusion, my understanding of accounting has deepened through my studies and exposure to the field. I recognize accounting as a vital discipline that underpins the success of businesses and the broader economy. The attention to detail, adherence to professional standards, and strategic decision-making capabilities required of accountants make it a highly respected and in-demand profession. As I continue to explore the field, I am excited to see how accounting will evolve and contribute to the ever-changing business landscape.。

会计政策与会计估计变更对企业财务状况的影响

1会计政策变更1.1含义会计政策是指企业在会计核算时所遵循的具体原则以及企业所采用的具体会计处理方法。

会计政策变更即企业对同一经济业务所允许采用的会计处理方法采用其他选择的行为。

为了对比不同时期的会计信息,使财报阅读者在比较企业不同时期的财报时,可以有效认识企业的财务状况、经营成果和现金流量的趋势,通常应该在不同时期选择一致的会计政策,不应也不能随意变更会计政策,不然就会降低会计信息的可比性,使财报阅读者对企业经营绩效比较时发生困难。

1.2条件企业出现下列情况时,应改变之前使用的会计政策:①相关法律法规或行业标准会计制度变更;②会计政策变更可以呈现更有效、更相关的会计信息。

1.3对企业财务状况质量分析的影响上述情况中第一种会计政策变更属外在因素,企业按行业有关规定执行即可。

该情况不是企业会计政策变更的一般性原因。

为企业财务状况、经营成果和现金流量呈现的会计信息更有效、更相关而变更会计政策,是企业选择会计政策的内在因素。

如果企业认为之前所选的会计政策提供的有关信息不如新会计政策所能呈现的信息有效与相关,那么企业可以考虑变更会计政策。

但必须注意的是,这种变更其必要性主要根据企业主观意愿。

通常,企业变更会计政策可能参考另外的情况。

企业财报阅读者理应考虑此情形。

2耐威科技会计政策变更分析2017年4月24日,北京天圆全会计师事务所发布了《关于北京耐威科技股份有限公司2016年会计政策变更的专项说明》。

公告中关于耐威科技会计政策变更的内容如下。

2.1会计政策变更的原因根据《增值税会计处理规定》(下称《规定》),2016年5月1日之后发生的与增值税相关的交易,影响资产、负债等金额的,予以调整。

利润表中的“税金及附加”项目代替原“营业税金及附加”项目,并包括了土地使用税、房产税、印花税、车船税等原计入“管理费用”的相关税费。

2.2具体的会计处理根据《规定》,2016年1~4月份,印花税及其他有关税费仍在“管理费用”项目中进行核算;5~12月在“税金及附加”核算。

财务会计英文版课后习题答案Ch12

CHAPTER 12 DISCUSSION QUESTIONS1.There are several reasons for a firm to makeinvestments in assets not directly related to the primary operations of its business (that is, investments in assets other than property, plant, equipment, and inventory). Companies usually make short-term investments be-cause of a temporary surplus of cash. They make long-term investments either because they believe that purchased investments provide a good return on money invested or because they want to gain influ-ence or control over investee companies.2.The risk and return trade-off of investmentsis that investors must usually decide whether they want a potentially higher return with more risk or a lower return with less risk.Most investments fall somewhere along a risk-return continuum. Investments that pro-vide high returns but have low risk are desir-able, but rare.3.The FASB has defined four different classifi-cations for debt and equity securities: trading securities, available-for-sale securities, held-to-maturity securities, and equity method se-curities.4. A security will be classified as trading if theinvestor is making the investment with the intent of selling the security should the need for cash arise, or to realize short-term profits should the price of the security increase.5. A security will be classified as held-to-maturity if the investor intends to hold the security until it matures. This criterion means that only debt securities can be classified as held-to-maturity, as equity securities typically do not mature. If a debt security is classified as held-to-maturity, any premium or discount associated with the security must be amor-tized over the life of the debt security.6.To be classified as an equity method securi-ty, an investor must typically own between20 and 50% of the outstanding commonstock of the investee. Ownership of between20 and 50% generally indicates the ability ofthe investor to significantly influence the operations and decisions of the investee.7.When an investor purchases debt and equitysecurities, two types of returns may be rea-lized. The first type of return is the receipt ofinterest (in the case of debt) or dividends (inthe case of equity). The second type of re-turn is from an increase in the price of thesecurity. To realize this type of return, the in-vestor must sell the security.8.When a security is sold, the seller must haveseveral pieces of information to properly ac-count for the transaction. The seller mustknow the selling price as well as the histori-cal cost of the security. The differencebetween these two amounts results in a rea-lized gain or loss on the sale.9.The difference between a realized gain orloss and an unrealized gain or loss relates tothe account ing concept of arm’s-lengthtransactions. The term ―realized‖ indicatesthat an arm’s-length transaction has takenplace and a security has been sold. A rea-lized gain indicates that the security was soldfor more than its historical cost, while a rea-lized loss means that the security was soldfor less than its original purchase price. Anunrealized gain means that the price of thesecurity being held has increased above itshistorical cost, but the security has not beensold. If the security is still being held and theprice falls below its historical cost, an unrea-lized loss has occurred.10.The account ―Market Adjustment‖ is used tovalue both trading and available-for-sale se-curities at their market value. Trading andavailable-for-sale securities are initiallyrecorded at their historical cost, and as theirvalue changes, the historical cost remainsthe same on the books. To reflect marketvalues on the books, the market adjustmentaccount is used to record both increasesand decreases in value. A separate marketadjustment account is used for both tradingand available-for-sale securities.11.Changes in the value of trading securities,both increases and decreases, are recordedon the books of the investor. Prior to 1994,only declines below historical cost wererecorded on the books. In 1994, however,434Chapter 12the rules were changed to allow companiesto record both increases and decreases invalue. At the end of each accounting period,the market value of the portfolio of tradingsecurities is compared to its historical cost,and the difference is recorded in the marketadjustment account. The offsetting credit (inthe case of increases in value) or debit (inthe case of decreases in value) is recordedin an income statement account as an un-realized gain or loss.12.Accounting for changes in the value ofavailable-for-sale securities is similar to theprocedures applied when accounting fortrading securities with one important differ-ence. Instead of recording any unrealizedincreases or decreases in value on theincome statement, unrealized increasesand decreases in value are recorded in astockholders’ equity account, UnrealizedIncrease/Decrease in Value of Available-for-Sale Securities—Equity. Thus, the journalentry to record unrealized changes in valuealways contains the stockholders’ equity a c-count and the market adjustment—available-for-sale securities account.13.The market adjustment account can befurther adjusted; however, the adjustmentaccount should always report the total netchange in the value of the security. For ex-ample, if a security that cost $200 rose invalue to $300 during the first period and thento $350 during the second period, the mar-ket adjustment account would show a bal-ance of $150 at the end of the second period. 14.Premiums and discounts on available-for-sale securities are not amortized because itis assumed that trading and available-for-sale securities will not be held long enoughto warrant the need to amortize a premiumor discount.15.Changes in the value of held-to-maturity andequity method securities are not accountedfor on the books of the investor. For held-to-maturity securities, the investor intends tohold the debt security until it matures, and asa result, changes in value will not affectthe eventual maturity value of the security.For equity method securities, the investoris holding the security for the purpose ofbeing able to influence the operating deci-sions of the investee on a long-term basis.Thus, temporary changes in value of equitymethod securities are ignored for accountingpurposes.16.The only difference between the accountingfor trading securities and available-for-salesecurities lies in unrealized changes in valueof those securities. For trading securities,the changes in value are recorded on the in-come statement. For available-for-sale se-curities, the unrealized changes in value arerecorded in a stockholders’ equity a ccount. 17.*When buying a held-to-maturity security, aninvestor purchases the right to receive twodifferent types of future cash receipts. First,the investor receives periodic interest pay-ments over the life of the security; second,the investor receives the face amount (prin-cipal) of the security at maturity.18.* A company would usually be willing to paymore than the face amount (a premium) fora held-to-maturity security when the interestrate on the security is higher than the marketrate of interest for similar investments. Thepaying of a higher price reduces the statedrate of interest to a point where it approx-imates the market rate of interest.19.*The amortization of a discount increases theamount earned on a held-to-maturity securitybecause at maturity investors receive theface value, which is higher than the amountoriginally paid. These increased proceedsmust be recognized over the life of the secu-rity through amortization. The amortization ofa discount increases interest from a statedrate to a higher effective rate.20.*An investor purchasing held-to-maturitysecurities (typically bonds) between interestdates must pay for accrued interest becauseat the next interest payment date a fullpe riod’s interest will be received, eventhough the securities have been held for onlya portion of the period. Because the securi-ties are sold in relatively small denomina-tions and are usually owned by numerousindividuals, it is almost impossible for acompany to know who bought how manybonds on which dates. Therefore, with manyheld-to-maturity securities, whoever ownsthe securities on the interest payment datereceives the full period’s i nterest.*Relates to expanded material.Chapter 12 43521.*The effective-interest amortization method istheoretically superior to the straight-lineamortization method because it takes intoconsideration the time value of money. Withthe effective-interest method, the amount ofinterest recognized is the effective interestrate times the amount of money actuallybeing borrowed at any period of time. Thestraight-line method is only an approximationof the true rate of interest.22.*The key criterion for using the equity methodis the ability of the investor to influence theoperations or decisions of the investee.23.*The accounting profession has providedguidelines to determine if the ability tosignificantly influence the operating deci-sions of an investee exists. The primaryguideline is degree of ownership. If the in-vestor owns between 20 and 50% of a cor-poration’s outstanding common stock, it isassumed that the investor is able to signifi-cantly influence the investee. Thus, unlessevidence exists to the contrary, ownership ofbetween 20 and 50% would require the useof the equity method.24.* When an investor purchases a trading secu-rity, revenue is recognized when interest ordividends are received. A gain or loss (un-re alized) is recorded when the security’sprice changes in value. For an investmentaccounted for under the equity method, rev-enue is recognized when the investee re-ports income for the period. This recognitionserves to increase the investment ac-count. The investment account is decreasedwhen dividends are received from the inves-tee. Unlike trading securities, temporarychanges in the value of equity method secur-ities are not recorded on the investor’sbooks.25.* Consolidated financial statements are pre-pared when a corporation owns more than50% of the stock of another company (acontrolling interest).26.* In the consolidated balance sheet, minorityinterest is the amount of equity investmentmade by outside shareholders to consolidat-ed subsidiaries that are not 100% owned bythe parent. In the consolidated incomestatement, minority interest income (shownas a subtraction) reflects the amount ofincome belonging to outside shareholders ofconsolidated subsidiaries that are not 100%owned.*Relates to expanded material.436Chapter 12PRACTICE EXERCISESPE 12–1 (LO1) Why Companies Invest in Other CompaniesThe correct answer is B.a. True. Most cases of companies investing in other companies are to investexcess cash.b. False. Investing in other companies will not necessarily eliminate risk in oth-er investments.c. True. By investing in other companies, the investing company can gain in-fluence over the operations of another company.d. True. When one company owns a significant portion of another company,the owner company can essentially control the operations of the owned company.PE 12–2 (LO2) Classifying a SecurityThe correct answer is C. Held-to-maturity securities are always considered debt securities. Trading and available-for-sale securities can sometimes be consi-dered debt securities. True to their name, equity method securities are always considered equity securities.PE 12–3 (LO2) Equity Method SecuritiesThe correct answer is A. An entity is presumed to have significant influence upon the operations of another company when it owns 20 to 50% of the outstanding voting stock.PE 12–4 (LO2) Disclosure of SecuritiesThe correct answers are A and C. Equity method securities are valued at cost ad-justed for changes in the net assets of the investee. Held-to-maturity securities are valued at amortized cost.PE 12–5 (LO3) Accounting for the Purchase of Trading and Available-for-Sale SecuritiesInvestment in Trading Securities ................................................... 65,400 Investment in Available-for-Sale Securities .................................. 79,600 Cash ............................................................................................ 145,000 Purchased various securities.Chapter 12 437 PE 12–6 (LO3) Accounting for the Return Earned on an InvestmentCash ................................................................................................. 1,359 Interest Revenue (459)Dividend Revenue (900)To record interest and dividends earned on securities.PE 12–7 (LO3) Accounting for the Sale of SecuritiesCash ................................................................................................. 25,200 Realized Loss on Sale of Trading Securities ................................ 2,800 Investment in Trading Securities ............................................. 28,000 To record the sale of Security 1 with original cost of$28,000 for $25,200.PE 12–8 (LO4) Changes in Value of Trading SecuritiesMarket Adjustment—Trading Securities (750)Unrealized Gain on Trading Securities—Income (750)To recognize the increase in value of the trading security($24,250 – $23,500 = $750).PE 12–9 (LO4) Changes in Value of Available-for-Sale SecuritiesUnrealized Increase/Decrease in Value of Available-for-SaleSecurities—Equity (400)Market Adjustment—Available-for-Sale Securities (400)To record net change in value of available-for-sale securities(Security 1 increased in value by $400, and Security 2 de-clined in value by $800).PE 12–10 (LO4) Subsequent Changes in Value of Trading Securities Unrealized Loss on Trading Securities—Income ......................... 1,900 Market Adjustment—Trading Securities .................................. 1,900 To adjust the market adjustment account to requiredending balance.Once this entry is posted, Market Adjustment—Trading Securities will have the required $800 credit balance as follows:438Chapter 12 PE 12–11 (LO5) Computing the Value of Held-to-Maturity Securities*First, we must compute the present value of the bonds as follows:Quarterly interest payment ($30,000 ⨯ 0.08 ⨯ ¼) ............... $ 600Present value of an annuity of 16 payments of $1 at 3%(Table II) ........................................................................... ⨯ 12.5611Present value of interest payments .................................... $ 7,537 Principal (face value) of bonds ........................................... $ 30,000Present value of $1 received 16 periods in the futurediscounted at 3% (Table I) .............................................. ⨯ 0.6232Present value of principal .................................................... 18,696 Total present value of investment ...................................... $26,233The value of the bonds can also be computed using a business calculator as follows:a. CLEAR ALL.b. Set P/YR to 1.1. 30,000 Press FV.2. 600 Press PMT.3. 16 Press N.4. 3 Press I/YR.5. Press PV for the answer of $26,231.67.PE 12–12 (LO5) Accounting for the Initial Purchase of Held-to-MaturitySecurities*The journal entry to record the purchase of this security is as follows:Investment in Held-to-Maturity Securities .......................... 26,233 Cash .............................................................................. 26,233 PE 12–13 (LO5) Straight-Line Amortization of Bond Discounts*The company will record a bond discount amortization of $676.83 ($40,000 –$35,939 = $4,061; $4,061/3 years ⨯ ½ = $676.83) on each date. Every six months, the company will make the following entry:Cash ...................................................................................... 2,000.00Investment in Held-to-Maturity Securities .......................... 676.83 Bond Interest Revenue ................................................ 2,676.83 Received semiannual bond interest and amortizedbond discount.*Relates to expanded material.Chapter 12 439 PE 12–14 (LO5) Straight-Line Amortization of Bond Premiums*The company will record a bond premium amortization of $567.90 ($68,407.39 –$65,000.00 = $3,407.39; $3,407.39/3 years ⨯ ½ = $567.90) on each date. Every six months, the company will make the following entry:Cash ...................................................................................... 3,250.00 Investment in Held-to-Maturity Securities .................. 567.90 Bond Interest Revenue ................................................ 2,682.10 PE 12–15 (LO5) Effective-Interest Amortization of Bond Premiums*The first step is to compute the market rate on bonds of similar risk as follows:a. CLEAR ALL.b. Set P/YR to 1.1. 65,000 Press FV.2. -68,407.39 Press PV.3. 3,250 Press PMT.4. 6 Press N.5. Press I/YR for the answer of 4%.The market interest rate of 4% is the semiannual rate, so the annual rate is 8%. The following amortization table shows the amount of interest earned and the amount of amortization for each period.InterestActually Earned(0.08 ⨯ ½ ⨯Cash Investment Amount of Investment Time Period Received Balance) Amortization Balance Acquisition date $68,407.39 Year 1, first six months $3,250 $2,736.30 $513.70 67,893.69 Year 1, second six months 3,250 2,715.75 534.25 67,359.44 Year 2, first six months 3,250 2,694.38 555.62 66,803.82 Year 2, second six months 3,250 2,672.15 577.85 66,225.97 Year 3, first six months 3,250 2,649.04 600.96 65,625.01 Year 3, second six months 3,250 2,624.99 625.01 65,000.00 Using the above amortization schedule, the journal entry for the first interest payment received is as follows:Cash ...................................................................................... 3,250.00 Investment in Held-to-Maturity Securities .................. 513.70 Bond Interest Revenue ................................................ 2,736.30 *Relates to expanded material.440Chapter 12 PE 12–15* (LO5) (Concluded)Using the above amortization schedule, the journal entry for the second interest payment received is as follows:Cash ...................................................................................... 3,250.00 Investment in Held-to-Maturity Securities .................. 534.25 Bond Interest Revenue ................................................ 2,715.75 PE 12–16 (LO5) Accounting for the Sale of Bond Investments*Cash ...................................................................................... 67,000.00Loss on Sale of Bonds......................................................... 359.44 Investment in Held-to-Maturity Bonds ........................ 67,359.44 Sold held-to-maturity bonds for $67,359.44.The following table shows the book value of the investment at the end of the first year (after the second interest payment) is $67,359.44.InterestActually Earned(0.08 ⨯ ½ ⨯Cash Investment Amount of Investment Time Period Received Balance) Amortization Balance Acquisition date $68,407.39 Year 1, first six months $3,250 $2,736.30 $513.70 67,893.69 Year 1, second six months 3,250 2,715.75 534.25 67,359.44 Year 2, first six months 3,250 2,694.38 555.62 66,803.82 Year 2, second six months 3,250 2,672.15 577.85 66,225.97 Year 3, first six months 3,250 2,649.04 600.96 65,625.01 Year 3, second six months 3,250 2,624.99 625.01 65,000.00 *Relates to expanded material.Chapter 12 441 PE 12–17 (LO6) Accounting for Investments Using the Equity Method* Investment in Hall Company .......................................................... 32,000 Revenue from Investments ....................................................... 32,000 To recognize Manwill’s portion of Hall’s net income ($80,000 ⨯0.40 = $32,000).Cash ................................................................................................. 8,000 Investment in Hall Company ..................................................... 8,000 To recognize Manwill’s portion of Hall’s dividends paid ($20,000⨯ 0.40 = $8,000).No entry is made for market value adjustments under the equity method of ac-counting for investments.PE 12–18 (LO7) Consolidated Financial Statements*Parent Company will report $135 ($150 ⨯ 0.90) as Income from Sub on its own in-come statement. On the consolidated financial statements, all of Sub’s revenue and expenses will be reported. Also reported will be Minority Interest in the amount of $15.*Relates to expanded material.442Chapter 12EXERCISESE 12–19 (LO3, LO4) Investment in Trading Securities—Journal Entries2008July 1 Investment in Trading Securities ................................... 8,300Cash ............................................................................ 8,300 Purchased 350 shares of Bateman Companystock at $22 per share plus $600 commission.Oct. 31 Cash (700)Dividend Revenue (700)Received a $2.00 per share dividend on350 shares of Bateman Company stock.Dec. 31 Unrealized Loss on Trading Securities—Income ......... 1,650Market Adjustment—Trading Securities .................. 1,650 To reduce trading securities to market($8,300 – $6,650).2009Feb. 20 Cash ................................................................................. 4,550Realized Gain on Sale of Trading Securities (400)Investment in Trading Securities ............................. 4,150 Sold 175 shares of Bateman Company stock[(175 shares ⨯ $26 = $4,550); one-half oforiginal cost of $8,300 is $4,150].Oct. 31 Cash (385)Dividend Revenue (385)Received a $2.20 per share dividend on175 shares of Bateman Company stock.Dec. 31 Market Adjustment—Trading Securities ....................... 2,575Unrealized Gain on Trading Securities—Income .... 2,575 To increase trading securities to market givena credit balance in the market adjustment of$1,650. Cost = $8,300 – $4,150 = $4,150;market = $29 ⨯ 175 shares = $5,075.Chapter 12 443 E 12–20 (LO3, LO4) Investment in Trading Securities—Journal EntriesJuly 16 Investment in Trading Securities ................................... 41,880Cash ............................................................................ 41,880 Purchased 4,000 shares of Eli Corporation stock.Sept. 23 Cash ................................................................................. 3,600Dividend Revenue ...................................................... 3,600 Received a cash dividend of $0.90 per share on4,000 shares of Eli Corporation stock.28 Cash ................................................................................. 21,840Investment in Trading Securities ............................. 20,940Realized Gain on Sale of Trading Securities (900)Sold 2,000 shares of Eli Corporation stock at $11per share—paid a commission of $160. [Cash =($11 ⨯ 2,000) – $160; short-term investment =$41,880 ⨯ 1/2; gain = $21,840 – $20,940].Dec. 31 Market Adjustment—Trading Securities ....................... 1,560Unrealized Gain on Trading Securities—Income .... 1,560 To increase value of securities to market [$11.25⨯ 2,000 shares – ($41,880 – $20,940) = $1,560].E 12–21 (LO3, LO4) Investment in Available-for-Sale Securities—JournalEntriesJan. 14 Investment in Available-for-Sale Securities .................. 83,200Cash ............................................................................ 83,200 Purchased 4,000 shares of Pinegar Corporationstock at $20.80 per share.Mar. 31 Cash ................................................................................. 1,000Dividend Revenue ...................................................... 1,000 Received a cash dividend of $0.25 per share on4,000 shares of Pinegar Corporation stock.Aug. 28 Cash ................................................................................. 36,160Investment in Available-for-Sale Securities ............ 33,280Realized Gain on Sale of Available-for-SaleSecurities ................................................................. 2,880Sold 1,600 shares of Pinegar Corporation stock at$22.60 per share [gain = 1,600 shares ⨯ ($22.60 –$20.80) = $2,880].444Chapter 12 E 12–21 (LO3, LO4) (Concluded)Dec. 31 Market Adjustment—Available-for-Sale Securities ...... 7,680Unrealized Increase/Decrease in Value ofAvailable-for-Sale Securities—Equity ................... 7,680To increase value of securities to marketvalue using market adjustment account[2,400 shares ⨯ ($24.00 – $20.80) = $7,680].E 12–22 (LO3, LO4) Investment in Securities2007Jan. 17 Investment in Available-for-Sale Securities .................. 89,500Cash ............................................................................ 89,500 Purchased 2,750 shares of Horner Companystock for $89,500.May 10 Cash ................................................................................. 3,575Dividend Revenue ...................................................... 3,575 Received a cash dividend of $1.30 per share on2,750 shares of Horner Company stock.Dec. 31 Unrealized Increase/Decrease in Value of Available-for-Sale Securities—Equity ......................................... 7,000Market Adjustment—Available-for-Sale Securities .7,000 To decrease value of securities to market valueusing market adjustment account (2,750 shares⨯ $30.00 = $82,500; $89,500 – $82,500 = $7,000).2008May 22 Investment in Available-for-Sale Securities .................. 30,000Cash ............................................................................ 30,000 Purchased an additional 750 shares of HornerCompany stock for $40 per share.July 18 Cash ................................................................................. 3,150Dividend Revenue ...................................................... 3,150 Received a cash dividend of $0.90 per share on3,500 shares of Horner Company stock.Chapter 12 445 E 12–22 (LO3, LO4) (Concluded)Dec. 31 Market Adjustment—Available-for-Sale Securities ...... 34,500Unrealized Increase/Decrease in Value ofAvailable-for-Sale Securities—Equity ................... 34,500To adjust portfolio of available-for-sale securitiesto market given a credit balance in the marketadjustment account from the prior period of$7,000. Market = $147,000 (3,500 shares ⨯ $42);Historical cost = $119,500 ($89,500 + $30,000);$147,000 – $119,500 = $27,500 + $7,000 = $34,500.2009June 7 Cash ................................................................................. 3,500Dividend Revenue ...................................................... 3,500 Received a cash dividend of $1.00 per share on3,500 shares of Horner Company stock.Oct. 5 Cash ................................................................................. 94,500 Realized Loss on Sale of Available-for-Sale Securities 25,000Investment in Available-for-Sale Securities ............ 119,500 To record sale of all Horner Company stock for$27 per share. Loss on sale = [$119,500 – ($27 ⨯3,500 shares)].Dec. 31 Unrealized Increase/Decrease in Value ofAvailable-for-Sale Securities—Equity ......................... 27,500Market Adjustment—Available-for-Sale Securities .27,500 Eliminate market adjustment account as allavailable-for-sale securities have been sold.Balance prior to adjustment is $27,500 ($34,500debit – $7,000 credit).E 12–23 (LO4) Investment in Equity Securities1. Market ValueSecurity Cost (December 31, 2009)A $250,000 $130,000B 160,000 169,000C 315,000 350,000Total $725,000 $649,000An unrealized loss of $76,000 ($725,000 –$649,000) would be recognized, reducing net income to $554,000 ($630,000 – $76,000).。

account information

management

5

1 Introduction

Basic Back knowledge

1、The definition : accounting information is refers to the information that the accounting units reveal to investors, creditors, or other users of the information through the form of financial statements, financial reports or note about unit’s financial position and operating results.

Tianjin university of commerce-Graduate department

11

2 Literature Review

Foreign literatures

Paper : Competition, Efficiency, and Cost Allocation in Government Agencies: Evidences on the Federal Reserve System. Author : (Cavaalluzo,Ittner and Larcker(1998)) Purpose: Highlighted the importance of external competition to governmental efficiency and accounting system design and use. Method:The empirical research

会计专业 英语作文

会计专业英语作文## The Role of Accounting in Modern Business: ACritical Analysis。

Accounting, often referred to as the "language of business," is a vital component of modern business operations. It involves the systematic recording, analyzing, and reporting of financial transactions, providing stakeholders with the information needed to make informed decisions. This essay explores the significance of accounting in contemporary business, highlighting its key functions, the ethical considerations it entails, and its evolving role in the digital age.### Key Functions of Accounting。

At its core, accounting serves several critical functions. Firstly, it facilitates financial record-keeping, ensuring that businesses maintain accurate and reliable financial data. This data is essential for tracking revenue,expenses, assets, and liabilities, providing a clearpicture of a company's financial health.Secondly, accounting plays a pivotal role in financial analysis. By analyzing financial statements such as the balance sheet, income statement, and cash flow statement, accountants can assess a company's profitability, liquidity, solvency, and efficiency. This analysis informs strategic decision-making, helping businesses identify areas for improvement and growth opportunities.Another key function is compliance with legal and regulatory requirements. Accountants ensure that businesses adhere to financial reporting standards and tax regulations, reducing the risk of legal issues and penalties. This compliance function also promotes transparency and accountability, fostering trust among stakeholders.### Ethical Considerations in Accounting。

英语作文 e-commerce change the wor

英语作文e-commerce change the wore-commerce change the worIntroduction: in the 21st century, with the rapid development of computer technology and network technology, e-commerce has become a very powerful way of life and commerce. Under the environment of e-commerce, manufacturers will produce according to their needs, and their sales will be completed with the help of computers and networks. It will completely change the business process of traditional business model, and revolutionary changes will inevitably lead to the connotation and significance of accounting management The extension of information technology has a revolutionary impact, and fundamentally challenges the basic theory of traditional accounting system and accounting model.This paper analyzes the impact of e-commerce on accounting, and puts forward improvement measures. Any accounting theory is based on a certain accounting environment and practice. E-commerce has greatly changed the traditional accounting environment and inevitably produces accounting theory The influence of e-commerce is a virtual enterprise both in organization and geography.The traditional accounting principle and the corresponding development need, on the basis of modern information technology, e-commerce has an impact on the traditional accounting mode. In the new social and economic environment, e-commerce is facing unprecedented opportunities and challenges in the development of China.。

人工智能对于会计行业的影响和对策研究-毕业论文

本科毕业设计(论文)题目人工智能对于会计行业的影响和对策研究人工智能对于会计行业的影响和对策研究摘要随着会计信息化的发展,人丄智能给会讣带来了重大革新,极大地提升了会讣工作的效率,但也给会计机构和会计人员带来了一些负面影响。

本文通过介绍人工智能在会计行业的应用现状,对会计行业和会计人员的积极影响和消极影响两个角度进行分析,层层深入,最后提出会计人员应对人工智能冲击的对策,以求促进会计人员的更好职业发展。