特许公认会计师ACCA最新考试形式2015

我成功通过了ACCA考试的经验分享

我成功通过了ACCA考试的经验分享ACCA是Association of Chartered Certified Accountants的缩写,即特许公认会计师学会。

作为一名职业会计师,拥有ACCA证书,可以在全球范围内开展不同的会计工作,甚至可以成为高管层的成员。

不过,ACCA考试并不是一项易事,它对考生的知识、技能和经验都有着非常高的要求。

但是,只要坚持,相信你也能像我一样,成功通过ACCA考试。

在这里,我将分享我通过ACCA考试的经验,希望能够帮助到准备参加ACCA考试的考生。

这里的经验和建议不一定是绝对的,但是是适合我个人的,你可以借鉴一下。

一、学习计划的制定ACCA考试内容比较庞杂,需要学习、掌握很多知识。

因此,制定一个合理的学习计划是非常重要的。

在制定学习计划时,要充分考虑自己的实际情况,例如时间、英语水平、工作负担等因素。

可以根据每个知识点的难易程度,制定相应的学习计划,然后根据计划进行复习和练习。

还需要注意的是,不要把所有的时间都放在学习上,适当休息和娱乐能够缓解压力,让你更有精神去学习。

二、重视语言能力ACCA考试主要以英文进行,因此,语言能力是ACCA考试成功与否的关键。

如果你不擅长英语,需要花费更多的时间和精力去提升语言能力。

我自己在考试初期就比较弱,因此我选择了英语培训班进行学习和提高。

通过课上的听说练习、写作指导和听力训练,使我在英语方面有了很好的提高。

在进行考试的时候,可以根据英语能力的水平,选择适合自己的考试时间段,充分准备。

三、专业书籍的选择专业知识是ACCA考试的重点,相应的教材和专业书籍是非常有必要的。

在选择书籍时,可以先去了解一下不同的书籍,找到适合自己的。

这些书籍能够帮助你深入理解ACCA考试的知识点,提供实用的例子和练习情景。

如果你在ACCA考试中遇到一些难点或者不理解的地方,可以通过书中提供的联系方式寻求帮助。

记得不要盲目的购买教材,更多的时候考试内容可能是在讲座中或其他的学习资源中展现。

会计证书怎么考试

会计证书怎么考试会计证书是证明个人在会计领域具备专业知识和技能的证书。

在职场上,拥有会计证书可以为职业发展提供有力的支持。

而且在某些行业中,必须拥有会计证书才能从事某些职业,比如会计师、审计师等。

会计证书考试的难度相对较高,需要考生具有扎实的会计知识和相关实践经验。

本文将从专业会计师的角度分析会计证书怎么考试。

一、会计证书的分类及考试根据认证机构的不同,会计证书主要可以分为CMA(管理会计师)、CPA(注册会计师)、ACCA(特许公认会计师)、CFA(特许金融分析师)等。

每种会计证书都有不同的证书要求和考试科目。

比较常见的是国内的注册会计师(CPA)和管理会计师(CMA)证书。

1、CPA考试注册会计师是指符合国家注册会计师制度要求,取得注册会计师资格的会计师。

取得CPA证书需要经过考试和实习两个环节。

考试分为四门科目,分别为《会计、审计》、《财务、财税法律》、《经济法、信息技术》和《管理、审计实务》。

在考试合格后,还需要完成相关的工作经验和实习,然后提交相应的申请,通过审批后获得CPA证书。

2、CMA考试管理会计师是指符合国际管理会计师协会要求,通过CMA考试、并具有大量工作经验的会计师。

取得CMA证书需要经过两个环节,分别是CMA考试和工作经验。

CMA考试分为两个部分,第一部分为《财务规划、绩效管理、成本管理、内部控制》;第二部分为《财务决策、风险管理、投资组合、外部财务报告与决策》。

CMA考试一年有两个考试时间,考试通过后,还需要拥有两年的财务管理经验,通过国际管理会计师协会的审批后才可以取得CMA证书。

二、考试前的准备1、了解考试内容和形式在准备考试前,要充分了解考试的内容、形式和考试时间等信息。

可以通过认证机构的官方网站或者所在学校进行查询和咨询,也可以向曾经考过证的前辈寻求有效建议和经验。

2、简历和申请在准备考试之前,必须事先准备好简历、推荐信和申请等相关材料,并在考试之前提交给认证机构,以便实现顺利报名和考试。

特许公认会计师 F6考试常用计算公式与答题方法介绍

特许公认会计师 F6考试常用计算公式与答题方法介绍ACCA F6的标准格式的确很复杂,所以有很多同学就会自己创造一种新的格式,或者是直接使用恒等式得出计算结果。

确实最后那个数字是正确的,但是在F6的考试中那个数字恰巧不是很重要。

那么临考前有什么办法能够帮助自己多拿几分呢?浦江财经为你介绍特许公认会计师F6考试常用计算公式与答题方法。

大家在做题的时候发现考官给的标准答案后面附带了很多的“NOTE”。

这些“NOTE”其实并不是ACCA考试答案的一部分,而只是考官关于题目考点的解释。

那么我们应该在什么时候写“NOTE”呢?通常情况下在计算中遇到“exempt income”, “exempt benefit”以及capital gain计算的“exempt asset”的时候才需要写“NOTE”。

NOTE不需要写的长篇大论,通常推荐用一句话把事情表达清楚就可以了,毕竟通常这些条目只有half Mark。

Adjustment of trading profit Trading profit 的调整是考试当中的重要考点,但是考生的得分率通常都不尽人意,为什么会这样呢?1、格式书写不符合规范如下是案列trading profit 调整的固定提问方式:Where a question requires the adjustment of profits, candidates will be told in there quire ments what figure to start their computation with (normally the net profit figure for an unincorporated business, or the profit before taxation figure for a limited company). They will also be told that they should list all of the items referred to in the notes to the question, indicating by the use of zero (0) any items, which do not require adjustment. Please see the end of this article for different wording used in variant papers.考生会被要求从一个固定的数字开始调整。

acca科目设置

acca科目设置

ACCA(特许公认会计师)是英国特许公认会计师协会(Association of Chartered Certified Accountants)的缩写,是全球公认的会计师资质之一。

ACCA考试科目设置如下:

1. 基础知识模块(Fundamentals Level):

- F1:会计师在商业环境中的角色

- F2:管理会计

- F3:财务会计

2. 专业水平模块(Professional Level):

- P1:战略领导者

- P2:企业管理者

- P3:项目管理者

3. 核心专业水平模块(Core Professional Level):

- P4:高级财务报告

- P5:高级绩效管理

- P6:高级税务

- P7:高级审计与认证

4. 选修专业水平模块(Options Professional Level):考生从以下四门课程中选择两门进行考试

- P4:高级财务管理

- P5:高级税务管理

- P6:高级外部风险评估

- P7:高级财务咨询

ACCA考试科目设置灵活多样,而且考生可以根据自己的实际情况进行选择和安排。

ACCA考试案例讲解与分析

ACCA考试案例讲解与分析ACCA(特许公认会计师)考试是全球范围内广泛认可的专业会计资格考试。

本文将对ACCA考试案例进行讲解与分析,以帮助考生更好地理解和应对考试。

1. 案例背景介绍ACCA考试案例通常基于真实的商业环境,包含一个或多个企业的具体情形。

在讨论具体案例之前,我们先简要介绍一下案例的背景,确保读者对所讨论的企业有所了解。

2. 分析主题一接下来,我们将深入分析第一个主题。

在这个主题中,我们将讨论企业面临的挑战、机会以及可能的解决方案。

我们将通过分析相关数据和信息,探讨企业在当前环境下的战略和经营问题。

3. 分析主题二在这一部分,我们将转向第二个主题。

这个主题可能与企业的财务管理、风险管理或战略决策等有关。

我们将提供必要的背景信息和数据,对该主题进行深入的分析和讨论。

4. 分析主题三在此部分,我们将探讨第三个主题,该主题可能涉及市场营销、人力资源管理、信息技术等方面。

我们将着重分析企业在这些领域面临的问题以及运用何种方法进行改进的可行性。

5. 关键分析点总结在这一部分,我们将概述前面所讨论的主要分析点,并强调其中最重要的问题和解决方案。

读者可以从中得出结论,并理解到这些问题在ACCA考试中的重要性。

6. 案例结论在本节中,我们将总结整个案例的分析过程,并提出综合的结论。

我们将回顾所讨论的主题,强调每个主题的关键点,并根据这些分析得出最终的结论。

7. 总结与建议在最后一部分,我们将总结全文,并提出一些建议,以帮助考生在ACCA考试中取得优异成绩。

我们将强调重要的复习和备考策略,以及在考场中应对案例题的方法和技巧。

通过对ACCA考试案例的讲解与分析,希望本文能够帮助考生更好地理解考试内容,提供有效的解题思路和方法。

考生们可以通过阅读本文更好地应对ACCA考试中的具体案例,充分发挥自己的分析和解决问题的能力,以取得优异的成绩。

(注意:本文内容仅为虚构案例,不涉及真实企业)。

acca p4公式

acca p4公式【1.ACCA P4考试简介】ACCA(Association of Chartered Certified Accountants,特许公认会计师公会)是全球知名的财务和会计专业资格认证。

P4是ACCA专业阶段考试中的一门,全称为“Applied Knowledge in Financial Management”(财务管理应用知识)。

该课程主要考察考生对财务管理领域各种工具、方法和实务的理解和应用能力。

【2.ACCA P4公式概述】在ACCA P4考试中,涉及众多财务管理相关的公式。

这些公式既包括基本的财务比率、现金流量和利润分配等,也包括复杂的估值、风险管理和企业战略等领域。

掌握这些公式对于考生在考试中取得优异成绩至关重要。

【3.重要公式及其应用】以下是ACCA P4考试中一些重要公式及其应用:1.财务比率:包括流动比率、速动比率、负债比率、权益比率、利润率、毛利率、净利润率等。

2.现金流量:包括经营现金流、投资现金流、筹资现金流等。

3.估值模型:包括市盈率(P/E)估值、市净率(P/B)估值、企业价值(EV)估值等。

4.风险管理:包括风险价值(VaR)、预期损失(ES)等。

5.企业战略:包括市占率、竞争力分析等。

【4.公式记忆与实践技巧】1.制定学习计划:合理安排时间,逐步掌握各个公式及其应用。

2.制作公式手册:将常用公式整理成手册,便于随时查阅。

3.做练习题:通过大量练习题巩固公式,提高实际应用能力。

4.参加模拟考试:模拟真实考试环境,检验自己的学习成果。

【5.结论与建议】ACCA P4考试对考生的财务管理知识体系提出了较高要求。

要想在考试中取得好成绩,熟练掌握相关公式是关键。

通过制定学习计划、制作公式手册、做练习题和参加模拟考试等方法,相信大家一定能掌握这些公式,并在考试中发挥出色。

祝各位考试顺利!请注意,以上内容仅供参考,实际考试要求可能会有所不同。

五大国际会计师资格证书人气最旺

五大国际会计师资格证书人气最旺经济全球化致使会计标准也趋于全球一体化。

从起,全球所有国家全部采用了国际财务报告准则(IFRS)编制会计报表。

我国是在2 月,由财政部发布了39项企业会计准则和48项注册会计师审计准则,这套准则体系自1月1日起在上市公司起正式施行。

为要达到国际执业水平,取得一个或多个国外会计师资格证书变成了众多从业人员的孜孜追求。

目前已进入中国的国外认证的会计师资格证书有五种:ACCA(英国特许公认会计师认证),AIA(国际会计师专业资格证书),CGA(加拿大注册会计师),CMA(美国管理会计师考试),CTA(澳大利亚公证会计师考试)和IFM(国际财务管理师)。

每张证书适应的国家和教学、考试内容都有一定区别,用来适应不同国家的会计制度。

ACCA特许公认会计师ACCA实际上是特许公认会计师公会(The Association of Chartered Certified Accountants)的缩写,它是英国具有特许头衔的4家注册会计师协会之一,也是当今最知名的国际性会计师组织之一。

ACCA的国际地位举足轻重,联合国于确定其环球课程时,就是以ACCA的课程作为蓝本。

ACCA会员资格得到欧盟立法以及许多国家公司法的承认,因此说具备ACCA 资格就拥有了打开这一职业发展之门的金钥匙毫不为过,因此又被称为“国际财会界的通行证”。

尽管ACCA以其全球公认而令人神往,但又以全英文考试难度大、综合能力要求高而令人生畏。

它共分为三个阶段14门课程,每次考试最多只能报考4门,学员只要在注册后内完成所有考卷并积累相关工作经验,可申请成为ACCA 会员,并授予“特许公认会计师”称衔,可使用ACCA作为头衔。

由于是全英语教材,加上ACCA苛刻的考试方式,能在十年中“磨成一剑”的人并不多。

有资料显示,自ACCA在国内启动以来,到目前国内注册的学员尚不到万人,会员不足千人。

而据有关人士估计,我国大约需要35万名注册会计师。

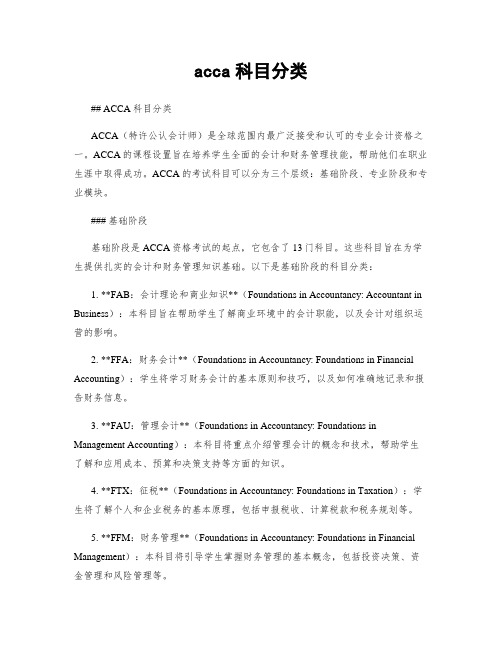

acca科目分类

acca科目分类## ACCA科目分类ACCA(特许公认会计师)是全球范围内最广泛接受和认可的专业会计资格之一。

ACCA的课程设置旨在培养学生全面的会计和财务管理技能,帮助他们在职业生涯中取得成功。

ACCA的考试科目可以分为三个层级:基础阶段、专业阶段和专业模块。

### 基础阶段基础阶段是ACCA资格考试的起点,它包含了13门科目。

这些科目旨在为学生提供扎实的会计和财务管理知识基础。

以下是基础阶段的科目分类:1. **FAB:会计理论和商业知识**(Foundations in Accountancy: Accountant in Business):本科目旨在帮助学生了解商业环境中的会计职能,以及会计对组织运营的影响。

2. **FFA:财务会计**(Foundations in Accountancy: Foundations in Financial Accounting):学生将学习财务会计的基本原则和技巧,以及如何准确地记录和报告财务信息。

3. **FAU:管理会计**(Foundations in Accountancy: Foundations in Management Accounting):本科目将重点介绍管理会计的概念和技术,帮助学生了解和应用成本、预算和决策支持等方面的知识。

4. **FTX:征税**(Foundations in Accountancy: Foundations in Taxation):学生将了解个人和企业税务的基本原理,包括申报税收、计算税款和税务规划等。

5. **FFM:财务管理**(Foundations in Accountancy: Foundations in Financial Management):本科目将引导学生掌握财务管理的基本概念,包括投资决策、资金管理和风险管理等。

6. **FAF:审计与保证**(Foundations in Accountancy: Foundations in Audit and Assurance):学生将学习审计和保证的基本原理和程序,以及如何评估和报告审计结果。

国际注册内部审计师考试攻略

国际注册内部审计师考试攻略一、ACCA+CIA 双重持证ACCA (特许公认会计师公会)与IIA(国际注册内部审计师协会)达成协议,自2015年11月起,ACCA会员可参加为其特别设计的CIA(国际注册内部审计师)测试。

一旦ACCA会员通过此项测试,则可获得国际注册内部审计师称号。

该测试包含了CIA资格考试的核心考纲以及学习目标。

ACCA与IIA都对此次携手合作表达了良好的祝愿。

ACCA战略与发展执行董事Alan Hatfield表示,虽然ACCA会员在其学习过程中已经学习了相当的有关风险、内部控制以及公司治理的知识,但连篇累赘的有关低质量内审以及由此造成的投资者信心下降的报道,还是提醒我们应该加强有关内部审计的学习。

此次为ACCA会员提供CIA挑战测试不但可以帮助他们获得CIA称号,也是一个提升他们内审专业知识的良机。

而IIA主席兼CEO Richard F. Chambers也表示与ACCA的协议达成创造了双方合作的'先河。

此外,ACCA还在其官方的网站上开辟了专门的版块为IIA及ACCA会员提供有关内审的相关资料。

这些资料包括了一些专业的指导以及有关内审的文章,为管理层以及审计委员会提供了有益的帮助。

ACCA and IIA joinforces to boost internal audit industry with new exam and specialised resources,Internal auditexam offered to ACCA members alongside membership of the IIA。

This deal willprovide an opportunity for ACCA members to become CIA certified through acustomised exam, which will include key syllabus and learning outcomes of theCIA exam.“This is an excellent opportunity to allowexisting ACCA members to further develop their expertise in this specialisedfield in which, being qualified clearly matters. Offering the CIA ChallengeExam to our members is a value-add, where our members working in internalaudit, or those who are looking to develop a career in internal audit, canobtain the CIA designation and clearly demonstrate their expertise in thisarea.“ACCA has alsolaunched a new resource for IIA and ACCA members working in internal audit witha section on the ACCA website. Thisincludes useful guides and articlesincluding internal audit for managers and also for the audit committee.二、CIA考试指南信息一.时间:每年举行一次,时间为11月第3周的周六、周日。

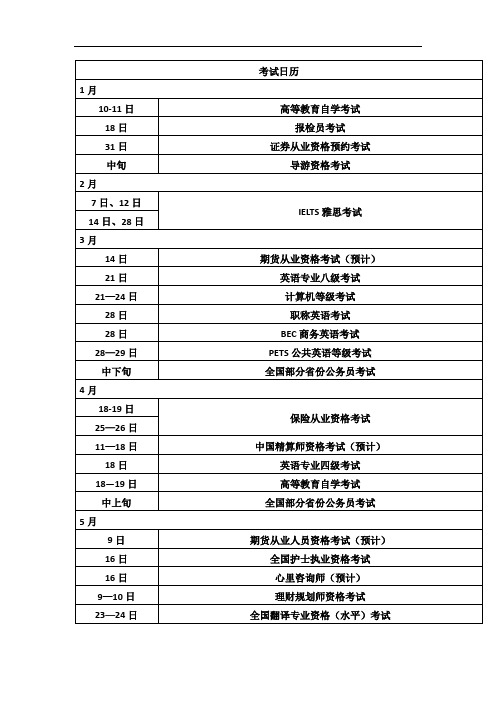

2015年资格考试时间安排表

全国翻译专业资格(水平)考试

23—24日

监理工程师考试

23—24日

全国计算机软件水平考试

16、23、30日

BEC商务英语考试(预计)

6月

1—10日

ACCA考试(预计)

7-9日

全国高考

20日左右

全国英语4、6级

1Байду номын сангаас—14日

质量工程师(预计)

6月底

中考

7月

4日

期货从业资格考试(预计)

4—5日

考试日历

1月

10-11日

高等教育自学考试

18日

报检员考试

31日

证券从业资格预约考试

中旬

导游资格考试

2月

7日、12日

IELTS雅思考试

14日、28日

3月

14日

期货从业资格考试(预计)

21日

英语专业八级考试

21—24日

计算机等级考试

28日

职称英语考试

28日

BEC商务英语考试

28—29日

PETS公共英语等级考试

19—20日

一级建造师

19—20日

国家司法考试

20日

统计从业资格考试

11月

7日

经济师考试

7—8日

全国翻译专业资格(水平)考试、计算机软件水平考试

7—8日

理财规划师考试(预计)

21日

期货从业资格考试(预计)

14、21、28日

BEC商务英语考试(预计)

12月

1—10日

ACCA考试(预计)

6日

日语等级考试(预计)

高等教育自学考试

5日

日语等级考试(预计)

英国特许公认会计师ACCA简介

ACCA,全称英国特许公认会计师公会,成⽴于1904年,是⽬前世界上的国际性专业会计师组织,⽬前,ACCA在全球170多个国家和地区拥有37多万名会员和学员,认可雇主超过7,500家,在我国ACCA学员和会员总数已达1.5万⼈,认可雇主249家。

ACCA是国际上各国学⽣最多、学员规模发展最快的国际专业会计组织。

ACCA是国际会计准则理事会(IASB)的创始成员,也是国际会计师联合会(IFAC)的成员。

1999年2⽉联合国通过了以ACCA课程⼤纲为蓝本的《职业会计师专业教育国际⼤纲》,该⼤纲成为世界各地职业会计师考试课程设置的⼀个衡量基准。

ACCA会员资格在国际上得到了⼴泛认可,尤其得到了欧盟⽴法以及许多国家公司法的承认。

所以,拥有ACCA会员资格,就有了在世界各地就业的通⾏证。

ACCA会员可在国际⼯商企业财务部门、审计/会计师事务所、⾦融机构和财政、税务部门从事财务和财务管理⼯作,许多会员在世界各地⼤公司担任⾼级职位(财务经理、财务总监CFO甚⾄公司总裁CEO)。

ACCA的宗旨是: 为有能⼒之⼠在职业⽣涯的全程提供⾼质量的专业机会 推⼴的道德和管理标准 为公众利益服务 在21世纪知识经济中,在国内、国际及全球各个层⾯上做领跑先锋 拥有“特许公认会计师”职业资格的ACCA会员,分布在⼯业、商业、公共机构和会计师事务所。

ACCA得到英国和爱尔兰⽴法的许可,可以向会员颁发注册审计师执照;在英国,ACCA还可以授权其会员办理破产执⾏事务。

在英国之外,按“欧盟职业资格互认指导原则”,ACCA会员资格得到欧盟各国的认可。

此外,ACCA资格也得到全球许多国家的会计法和公司法的认可。

拥有ACCA职业资格的会计师以其拥有诚信的品德、专业的精神和融会贯通的专业知识和技能所著称。

ACCA的声誉植根于近百年来为社会提供⾼质量的会计和财务资格。

ACCA不但是⼀个拥有悠久传统的组织,⽽且是⼀个极具前瞻性思维的组织,同时,也由于拥有⼤量年轻的会员⽽充满活⼒。

特许公认会计师—ACCA

ACCA考试ACCA是"英国特许公认会计师公会"(The Association of Chartered Certified Accountants)的简称,是目前世界上领先的专业会计师团体,也是国际学员最多、学员规模发展最快的专业会计师组织。

ACCA 会员资格得到欧盟立法以及许多国家公司法的承认。

介绍特许公认会计师ACCA是什么?英国特许公认会计师公会(The Association of Chartered Certified Accountants)简称ACCA,成立于1904年,是目前世界上领先的专业会计师团体,也是国际学员最多、学员规模发展最快的专业会计师组织。

ACCA总部设在伦敦,在美国洛杉矶、加拿大多伦多、澳大利亚悉尼建有分会,在世界上70多个城市均设有办事处。

ACCA自1988年进入中国以来,经历20余年快速发展,目前在中国拥有超过20,000名会员及34,000名学员,并在北京、上海、成都、广州、深圳以及香港设有共6个办事处,在澳门设有一个联络中心。

ACCA为全世界有志投身于财务、会计以及管理领域的专才提供首选的资格认证,一贯坚持最高的标准,提高财会人员的专业素质,职业操守以及监管能力,并秉承为公众利益服务的原则。

在英国,英国立法许可ACCA会员从事审计、投资顾问和破产执行的工作。

ACCA会员资格得到欧盟立法以及许多国家公司法的承认。

ACCA在欧洲会计专家协会(FEE)、亚太会计师联合会(CAPA)和加勒比特许会计师协会(ICAC)等会计组织中起着非常重要的作用。

在国际上,ACCA是国际会计准则理事会(IASB)的创始成员,也是国际会计师联合会(IFAC)的成员。

为何要成为ACCA职业资格证持有人?ACCA是国际认可范围最高的财务人员资格证书!ACCA专业资格考试是最具权威性的国际认证资格考试,目前在170个国家和地区拥有近32.5万学员和12.2万会员,设有250多个考点,操作上具有真正的国际性。

会计考的8个证书的含金量

会计考的8个证书的含金量作为一个专业会计师,我们都知道,会计考试是非常严谨的考试,而考取会计证书的过程总是需要经过长期的学习和实践。

在全球范围内,有多种不同的专业会计师证书,每个证书都代表着不同的加权和含金量。

在本文中,我们将会以会计专业的角度来分析和评价其中的八个不同的会计证书,并帮助您更好地了解并选择最适合自己的证书。

一、注册会计师(CPA)这是最常被提及的一种会计证书,在美国,注册会计师证书是最有价值的证书之一,同时也是美国公认最优秀的专业会计师证书之一。

证书持有人经过了对会计、审计、税收和商法等多个领域的深度学习和考试。

得到该证书者在领域内通常被认为是精英人士。

同时,得到这样的证书还意味着持有人要经过很严格的监管和持续的职业学习。

在中国内地,由于当地法规的限制,注册会计师证书在国内得到了一定的限制。

但是,持有这样的证书依然是顶尖职业人士和精英群体。

二、公认会计师(CMA)这是美国国际管理会计师协会(IMA)颁发的证书之一。

这个证书侧重于财务规划、内部控制、预算管理、投资分析等方面的学习,同时也注重认证持有人对商业战略以及成本风险研究等方面的才能。

在不同国家和地区中,CMA的含金量也不同。

而在国内,CMA这个证书相对较为减值,但它还是意味着你具有了国际化的视野,同时证明了您的职业选择很有策略性。

三、特许公认会计师(ACCA)ACCA 注重于会计专业的深度研究,包括财务报告、审计、税收、商业法和银行等领域。

ACCA和CMA相似,在国外特别是英国,都是非常具有含金量的证书,而在国内尤其是在新加坡,ACCA证书则有较高的含金量。

ACCA认证持有者通常具有严谨的专业精神,掌握着会计专业的实践,这对于那些想要在金融领域深耕的人来说是非常有利的。

四、注册财务策划师(CFP)这个证书专注于个人财务规划、风险管理、投资策略和保险财务等方面的研究。

CFP在国际上普遍被认为是会计业的重要证书之一,被用作评估财务计划师的能力。

acca ma公式

acca ma公式ACCA MA是ACCA(全球特许公认会计师协会)资格考试中的一门核心科目,全称为Management Accounting,即管理会计。

在ACCA考试中,MA是第二门考试科目,也是考生需要掌握的重要知识点之一。

本文将围绕ACCA MA公式展开讨论,介绍其背景、重要性以及一些常用的公式。

ACCA MA公式是ACCA MA考试中的重要内容之一。

在准备ACCA MA考试时,掌握这些公式是至关重要的。

这些公式可以帮助考生在实际工作中解决管理会计方面的问题,提高决策能力和管理水平。

让我们来了解一下ACCA MA的背景。

ACCA MA旨在为考生提供在管理会计领域进行决策和规划所需的知识和技能。

管理会计是一种应用会计和财务概念和技术来支持管理决策制定的方法。

它主要关注与企业内部的管理活动相关的会计信息。

管理会计通过提供支持管理决策所需的信息,帮助企业实现其战略目标。

ACCA MA考试涵盖了多个主题,包括成本和收益管理、预算和预测、绩效评估和控制、资本投资决策等。

在这些主题中,公式是解决问题和做出决策的关键工具之一。

下面我们来介绍一些常用的ACCA MA公式。

首先是成本和收益管理方面的公式。

其中一种常用的公式是成本-收益比(Cost-Volume-Profit Ratio)。

成本-收益比可以帮助企业计算出达到盈亏平衡点所需的销售额。

公式为:成本-收益比= 固定成本/ (销售价格 - 变动成本)。

其次是预算和预测方面的公式。

预算和预测是管理会计中非常重要的主题,企业通过制定预算和预测来规划和控制经营活动。

一种常用的公式是静态预算方差(Static Budget Variance)。

静态预算方差是实际结果与预算结果之间的差异。

公式为:静态预算方差= 实际结果 - 预算结果。

绩效评估和控制也是ACCA MA考试的重要内容之一。

在绩效评估和控制方面,考生需要掌握一些重要的公式,如投资回报率(Return on Investment)和剩余收益(Residual Income)。

境外会计职业资格ACCA,AICPA介绍

目前, 在我国的境外会计职业资格主要有来自英国、美国、加拿大、澳大利亚等发达国家、国际会计机构香港等地, 如特许公认会计师、英国特许会计师、美国注册会计师、澳大利亚注册会计师、国际注册内部审计师等16 种。

本文将调查所得各类考试概况、考试科目设置、考试或培训收费标准等简要介绍。

一、英国特许会计师( ACA)英国特许会计师( The Associate Chartered Accountant, ACA) ,又名英格兰皇家特许会计师, 是由英格兰及威尔士特许会计师协会( ICAEW) 组织的资格考试。

ICAEW是英国和欧洲重要的会计行业组织, 有126 年的历史, 拥有12.8 万名会员, 分布在142 个国家的商业和公共部门中, ACA 资格在世界范围内获得公认并享有很高的声誉。

2006 年中国注册会计师协会与ICAEW签订合作备忘, 启动了“英国特许会计师合作培训项目”。

ACA 资格考试目前分两个阶段: 专业课阶段有 6 科考试( 会计、审计与保全、企业财务、商务管理、财务报告、税法) , 高级阶段有3 科考试。

对于参加到本项目中的中国学员, ICAEW将予以免试专业课阶段的5 科, 另外增加一门财务报告小考,因此完成全部考试只需要通过以下课程: 商务管理、财务报告小考、高级阶段考试以及高级案例研究。

截止2007 年8 月, 国内第一批75 名ACA学员中, 已有半数以上的学员通过了专业阶段的全部考试。

二、特许公认会计师( ACCA)特许公认会计师( Association of Chartered Certified Accountants, ACCA) 是特许公认会计师公会颁发的职业资格。

特许公认会计师公会成立于1904 年, 是目前全球最大的国际会计师组织,总部设在英国伦敦, 目前在160 多个国家和地区拥有32 万会员和学员, 设有250 多个考点。

ACCA 考试是比较早进入中国的资格考试之一, 其培训项目1988 年进入大陆, 主体证书考试1990 年进入国内。

2015年6月ACCA考试《高级财务管理》真题及答案

2015年6月ACCA考试《高级财务管理》真题及答案2015年6月ACCA考试《高级财务管理》真题(总分:100,做题时间:180分钟)一、Section A – This ONE question is compulsory and MUST be attempted(总题数:1,分数:50.00)1.Yilandwe Yilandwe, whose currency is the Yilandwe Rand (YR), has faced extremely difficult economic challenges in the past 25 years because of some questionable economic policies and political decisions made by its previous governments.Although Yilandwe’s population is generally p oor, its people are nevertheless well-educated and ambitious. Just over three years ago, a new government took office and since then it has imposed a number of strict monetary and fiscal controls, including an annual corporation tax rate of 40%, in an attempt to bring Yilandwe out of its difficulties. As a result, the annual rate of inflation has fallen rapidly from a high of 65% to its current level of 33%. These strict monetary and fiscal controls have made Yilandwe’s government popular in the larger citi es and towns, but less popular in the rural areas which seem to have suffered disproportionately from the strict monetary and fiscal controls. It is expected that Yilandwe’s annual inflation rate will continue to fall in the coming few years as follows: Yi landwe’s government has decided to continue the progress made so far, by encouraging foreign direct investment into the country. Recently, government representatives held trade shows internationally and offered businesses a number of concessions, including: (i) zero corporation tax payable in the first two years of operation; and (ii) an opportunity to carry forward tax losses and write them off against future profits made after the first twoyears. The government representatives also promised international companies investing in Yilandwe prime locations in towns and cities with good transport links. Imoni Co Imoni Co, a large listed company based in the USA with the US dollar ($) as its currency, manufactures high tech diagnostic components for machinery, which it exports worldwide. After attending one of the trade shows, Imoni Co is considering setting up an assembly plant in Yilandwe where parts would be sent and assembled into a specific type of component, which is currently being assembled in the USA. Once assembled, the component will be exported directly to companies based in the European Union (EU). These exports will be invoiced in Euro (€). Assembly plant in Yilandwe: financial and other data projections It is initially assumed that the project will last for four years. The four-year project will require investments of YR21,000 million for land and buildings, YR18,000 million for machinery and YR9,600 million for working capital to be made immediately. The working capital will need to be increased annually at the start of each of the next three years by Yilandwe’s inflation rate and it is assumed t hat this will be released at the end of the project’s life. It can be assumed that the assembly plant can be built very quickly and production started almost immediately. This is because the basic facilities and infrastructure are already in place as the plant will be built on the premises and grounds of a school. The school is ideally located, near the main highway and railway lines. As a result, the school will close and the children currently studying there will be relocated to other schools in the city. The government has kindly agreed to provide free buses to take the children to these schools for a period of six months to give parents time to arrange appropriate transport in the future for their children. The currentselling price of each component is €700 and this price is likely to increase by the average EU rate of inflation from year 1 onwards. The number of components expectedto be sold every year are as follows: The parts needed to assemble into the components in Yilandwe will be sent from the USA by Imoni Co at a cost of $200 per component unit, from which Imoni Co would currently earn a pre-tax contribution of $40 for each component unit. However, Imoni Co feels that it can negotiate with Yilandwe’s government and increase the transfer price to $280 per component unit. The variable costs related to assembling the components in Yilandwe are currently YR15,960 per component unit. The current annual fixed costs of the assembly plant are YR4,600 million. All these costs, wherever incurred, are expec ted to increase by that country’s annual inflation every year from year 1 onwards. Imoni Co pays corporation tax on profits at an annual rate of 20% in the USA. The tax in both the USA and Yilandwe is payable in the year that the tax liability arises. A bilateral tax treaty exists between Yilandwe and the USA. Tax allowable depreciation is available at 25% per year on the machinery on a straight-line basis. Imoni Co will expect annual royalties from the assembly plant to be made every year. The normal annual royalty fee is currently $20 million, but Imoni Co feels that it can negotiate this with Yilandwe’s government and increase the royalty fee by 80%. Once agreed, this fee will not be subject to any inflationary increase in the project’s four-year period. If Imoni Co does decide to invest in an assembly plant in Yilandwe, its exports from the USA to the EU will fall and it will incur redundancy costs. As a result, Imoni Co’s after-tax cash flows will reduce by the following amounts: Imoni Co normally uses its cost of capital of 9% to assess newprojects. However, the finance director suggests that Imoni Co should use a project specific discount rate of 12% instead. Required:(分数:50.00)(1).(a) Discuss the possible benefits and drawbacks to Imoni Co of setting up its own assembly plant in Yilandwe,compared to licensing a company based in Yilandwe to undertake the assembly on its behalf. (5 marks)(分数:25.00)________________________________________________________________ _________________ _________正确答案:(Benefits of own investment as opposed to licensing Imoni Co may be able to benefit from setting up its own plant as opposed to licensing in a number of ways. Yilandwe wants to attract foreign investment and is willing to offer a number of financial concessions to foreign investors which may not be available to local companies. The company may be able to control the quality of the components more easily, and offer better and targeted training facilities if it has direct control of the labour resources. The company may also be able to maintain the confidentiality of its products, whereas assigning the assembly rights to another company may allow that company to imitate the products more easily. Investing internationally may provide opportunities for risk diversification, especially if Imoni Co’s shareholders are not well-diversified internationally themselves. Finally, direct investment may provide Imoni Co with new opportunities in the future, such as follow-on options. Drawbacks of own investment as opposed to licensing Direct investment in a new plant will probably require higher, upfront costs from Imoni Co compared to licensing the assembly rights to a local manufacturer. It may be able to utilise these saved costs on other projects. Imoni Co will most likely be exposed to higher risksinvolved with international investment such as political risks, cultural risks and legal risks. With licensing these risks may be reduced somewhat. The licensee, because it would be a local company, may understand the operational systems of doing business in Yilandwe better. It will therefore be able to get off-the-ground quicker. Imoni Co, on the other hand, will need to become familiar with the local systems and culture, which may take time and make it less efficient initially. Similarly, investing directly inYilandwe may mean that it costs Imoni Co more to train the staff and possibly require a steeper learning curve from them. However, the scenario does say that the country has a motivated and well-educated labour force and this may mitigate this issue somewhat. (Note: Credit will be given for alternative, relevant suggestions))解析:(2).(b) Prepare a report which: (i) Evaluates the financial acceptability of the investment in the assembly plant in Yilandwe;(21 marks) (ii) Discusses the assumptions made in producing the estimates, and the other risks and issues which Imoni Co should consider before making the final decision; (17 marks) (iii) Provides a reasoned recommendation on whether or not Imoni Co should invest in the assembly plant in Yilandwe.(3 marks) Professional marks will be awarded in part (b) for the format, structure and presentation of the report.(4 marks) (分数:25.00)________________________________________________________________ _________________ _________正确答案:(Report on the proposed assembly plant in Yilandwe This report considers whether or not it would bebeneficial for Imoni Co to set up a parts assembly plant in Yilandwe. It takes account of the financial projections, presented in detail in appendices 1 and 2, discusses the assumptions made in arriving at the projections and discusses other non-financial issues which should be considered. The report concludes by giving a reasoned recommendation on the acceptability of the project. Assumptions made in producing the financial projections It is assumed that all the estimates such as sales revenue, costs, royalties, initial investment costs, working capital, and costs of capital and inflation figures are accurate. There is considerable uncertainty surrounding the accuracy of these and a small change in them could change the forecasts of the project quite considerably.A number of projections using sensitivity and scenario analysis may aid in the decision making process. It is assumed that no additional tax is payable in the USA for the profits made during the first two years of the project’s life when the company will not pay tax in Yilandwe either. This is especially relevant to year 2 of the project. No details are provided on whether or not the project ends after four years. This is an assumption which is made, but the project may last beyond four years and therefore may yield a positive net present value. Additionally, even if the project ceases after four years, no details are given about the sale of the land, buildings and machinery. The residual value of these non-current assets could have a considerable bearing on the outcome of the project. It is assumed that the increase in the transfer price of the parts sent from the USA directly increases the contribution which Imoni Co earns from the transfer. This is probably not an unreasonable assumption. However, it is also assumed that the negotiations with Yilandwe’s gover nment willbe successful with respect to increasing the transfer price and the royalty fee.Imoni Co needs to assess whether or not this assumption is realistic. The basis for using a cost of capital of 12% is not clear and an explanation is not provided about whether or not this is an accurate or reasonable figure. The underpinning basis for how it is determined may need further investigation. Although the scenario states that the project can start almost immediately, in reality this may not be possible and Imoni Co may need to factor in possible delays. It is assumed that future exchange rates will reflect the differential in inflation rates between the respective countries. However,it is unlikely that the exchange rates will move fully in line with the inflation rate differentials. Other risks and issues Investing in Yilandwe may result in significant political risks. The scenario states that the current political party is not very popular。

ACCA P5-finanl mock

ACCAPaper P5Advanced Performance ManagementFinal Mock – September 2015Instructions:Take a few moments to review the notes on the inside of this page titled, 'Get into good exam habits now!' before attempting this exam.DO NOT OPEN THIS PAPER UNTIL YOU ARE READY TO START UNDER EXAMINATION CONDITIONSGet into good exam habits now!Take a moment to focus on the right approach for this exam.Effective time managementWatch the clock, allow 1.8 minutes per mark. Work out how long you can spend on each question and do not exceed that time.Take a few moments to think what the requirements are asking for and how you are going to answer them.Effective planningThis paper is in exactly the same format as the real exam. You should read through the paper and plan the order in which you will tackle the questions. Always start with the one you feel mostconfident about and take time to choose the questions you will answer in sections with a choice.Read the requirements carefully: focus on mark allocation, question words and potential overlap between requirements.Identify and make sure you pick up the easy marks available in each question.Effective layoutPresent your numerical solutions using the standard layouts you have seen. Show and reference your workings clearly.With written elements try and make a number of distinct points using headings and short paragraphs. You should aim to make a separate point for each mark.Ensure that you explain the points you are making ie why is the point a strength, criticism or opportunity?Give yourself plenty of space to add extra lines as necessary, it will also make it easier for the examiner to mark.SECTION AThis question is compulsory and must be attemptedQuestion 1Crown Oak Construction (Crown Oak) is a well-established, quoted company, based in a western European country. It specialises in the construction of timber framed buildings such as barns, garages, car ports etc, which are built to order.Traditionally, Crown Oak has used timber sourced from its own country, and it prides itself on using only timber from sustainable sources.Historically, Crown Oak and Henderson have been the two main companies in the market, but recently a new competitor has joined the market. The new competitor is based in another European country, and it makes pre-packaged timber framed buildings which are much quicker to construct than Crown Oak's designs have historically been. Not all of the timber used in the new competitor's buildings comes from sustainable sources though.In response to the threat from the new competitor, Crown Oak's directors have decided to move into the building of pre-assembled wooden structure houses imported from Scandinavia. Pre-assembled buildings are relatively cheaper than Crown Oak's current 'build to order' units, and the directors believe there is a need for cheaper products as interest rates have recently started rising again – a move which some analysts believe could threaten the fragile economic recovery in Crown Oak's country. The move into this new market (for pre-assembled buildings) will involve considerable investment in new non-current assets and will lead to additional direct labour being employed. Crown Oak has already begun to purchase the new equipment required. However, as this is a growing market, the directors believe that in the longer term this will be a profitable new area of market share for the company.By contrast, the directors of Henderson Construction have decided to concentrate on maintaining current market share, and they have no plans to grow by developing new products or entering new markets. However, the company continues to monitor its costs constantly, and reduces these wherever possible, in a bid to increase profitability by improving operating efficiency.Crown Oak's CSFs and KPIsCustomer satisfaction and service have always been key elements of Crown Oak's business model, and the board have identified the following critical success factors (CSFs) for the business:To improve productivity by using leading edge construction techniquesTo maximise profits within acceptable levels of riskTo maintain customer satisfaction by providing excellent customer serviceThe following key performance indicators (KPIs) are currently reported in the monthly reports produced for the Board: units sold, gross profit (%), average sales price per unit, contribution per unit, quality costs per unit, operational gearing (represented by fixed costs/variable costs), return on capital employed (ROCE), and average customer satisfaction score.The current KPIs were selected by Crown Oak's previous finance director, who had worked for the company for a number of years before he retired last year. His replacement, recruited from another construction company, is concerned that Crown Oak is not paying sufficient attention to market share and cost control. He has suggested that the Crown Oak's KPIs should be updated, although there was little enthusiasm for this from the other board members, who say that the current measures have allowed them to run the business successfully for a number of years.The Operations Director has also raised concerns about the validity of the budgeted figures for the last year. Heis aware that Crown Oak's performance has been worse than budgeted, but he has pointed out that the budget had not anticipated the new market entrant, and also did not accurately reflect the mix of products Crown Oakhad sold during the year (see Appendix 2). In particular, the number of customers undertaking barn conversions has fallen significantly, as a result of the recent increase in interest rates making customers more reluctant totake out the loans needed to fund the projects.The Operations Director is also concerned about an increase in the number of jobs where Crown Oak has had to carry out remedial work after the initial construction has been completed. He thinks the cost of remedial work could be excessive, but the current performance reporting system does not provide any information about this. The Finance Director is preparing a summary report looking at Crown Oak's performance for the last year and asked you, as the management accountant, to help draft this for him. The data in Appendix 1 has already been prepared by the assistant management accountant, and has been calculated correctly.Appendix 1Summary financial information for the most recent financial year: to 31 March 20X5 (annual figures)Crown Oak Crown Oak HendersonActual $m Budget$mActual$mRevenue 439 452 550 Variable costsMaterials and labour 275 272 331Sub-contractor costs 52 34 39 Quality costs 10 8 5Fixed costsStaff costs 23 23 27 General expenses 28 22 23 Depreciation 27 26 23Profit before interest and tax 24 67 102Other data $m $m $m Shareholders' funds 413 424 444Long term loans 120 80 20Notes:1. Total market size for 20X5 was $1,670m. The total market size in 20X4 was $1,585m, and Crown Oak'stotal revenue in 20X4 was $434m.2. The total number of units sold by Crown Oak in 20X5 was 40,360 compared to budget of 41,000. (seeAppendix 2).3. Crown Oak's actual average number of employees for 20X5 was 2,200 compared to a budget of 2,000.Henderson's average number of employees for the year was 2,500.Fixed staff costs, and other fixed costs, are treated as central costs, and are not included in the cost of producing units.4. At the end of every completed job, Crown Oak asks customers to complete a short questionnaire abouthow satisfied they are with their new buildings. This includes a satisfaction rating from '5' (very satisfied) to '1' (very unsatisfied). Crown Oak's target average customer satisfaction score is 4.0, but across 20X5, the average score was 3.7.5. Crown Oak has 200 million ordinary shares issued. Total dividends of $30 million have been proposed for20X5; which is the same amount as had originally been budgeted for the year.Appendix 2 – Crown Oak's units sold and pricesUnits sold Actual Units soldBudgetPri c e ($)Barns 5,437 6,970 18,000 Garages 18,155 16,810 12,000Car ports 11,193 10,660 8,000Other 5,575 6,560 6,000Note: Actual prices for each product type remained in line with budget across the year.RequiredDraft a report for the Board of Crown Oak which:(i) Calculates the key performance indicators (KPIs) the Board uses to assess the company's performance.(9 marks)[You should include actual and budget KPI figures for Crown Oak, and actual benchmark figures forHenderson where possible.](ii) Takes each critical success factor (CSF) in turn, and evaluates how the suggested KPIs fit to the CSF.(11 marks) (iii) Evaluates the extent to which the CSFs reflect the competitive pressures which Crown Oak is facing.(10 marks) (iv) Evaluates the extent to which Crown Oak and Henderson's product market strategies explain the relative performance of the two companies. (6 marks) (v) Explains the potential conflicts that the management of Crown Oak could face in relation to short- and long-run performance. (6 marks) (vi) Discusses the likely reaction of the shareholders and market to the results of Crown Oak for the year ended 31 March 20X5. (4 marks) Professional marks will be awarded for the format, style and structure of the discussion of your answer.(4 marks)(Total: 50 marks)SECTION BTWO questions ONLY to be attemptedQuestion 2Glenn Associates (GA) is a security firm which provides installation and service contracts for security systems for private and business clients. In the last few years the amount of business generated has started to slow and the directors realise that, in order to maintain their success, the business must grow. The strategy of the business is to increase their customer base. This is particularly important for installations as, once a system is installed by GA, the service business should follow automatically. A further strategic concern of the directors is that business will only be retained if the quality of the service provided by GA is of the highest standard. A further aspect of the strategy of the business is that costs must be controlled in order to encourage sales without increasing prices. In the past the Managing Director of GA has only assessed performance of the company on the basis of financial performance indicators. However, having recently attended a course which touched on the subject of the importance of non-financial performance indicators, he is now considering whether to incorporate relevant indicators into the management accounting reporting system.You are the accountant for Glenn Associates, and the Managing Director has provided you with the following data about the company's performance for the year ended 31 March 20X5.Selected statistics for the year ended 31 March 20X5Revenue $11,840,000Net profit $947,600Total client enquiriesNew business 4,230Repeat business 1,840Enquiries turned into contractsNew business 3,005Repeat business 1,510Number of service call outs 14,320Number of engineers employedInstallations 34Service 95Total engineer hoursInstallations 68,300Service 213,750Numbers of customer complaintsInstallation 934Service 1,250Time to reach client when called out 3.2 hours (average)Chargeable time of engineersInstallations 62,830 hrsService 166,790 hrsTime between initial enquiryand installation 5 days (average)Number of service contracts20X4 15,89020X5 18,890Number of installations20X4 8,12020X5 9,635Required(a) Explain the growing emphasis on non-financial performance indicators for a business such as GA.(4 marks)(b) Using only the information provided produce a range of non-financial performance indicators under eachof the following headings:(i) Competitiveness(ii) Resource utilisation(iii) QualityExplain the importance to GA of each indicator of performance you produce and assess GA'sperformance as a result.(16 marks)(c) Comment critically on the value of using non-financial performance measures (such as competitiveness,resource utilisation and quality) within an integrated system of performance measurement, such as Lynch and Cross's performance pyramid or Fitzgerald and Moon's building blocks model.(5 marks)(Total: 25 marks)Question 3Edwards Incorporated (EI) is a multi-national diversified business which operates on a divisionalised basis. The manager of each division of EI is responsible for capital investment choices within a capital budget set by the Board of EI and is paid an annual bonus related to the return on investment of the division for each accounting year. EI has a weighted average cost of capital of 10%.TT is a division of EI, which provides equipment to the building trade. The manager of TT is currently assessing a project to open a new superstore to sell equipment. The project has an initial cost of $1 million, will last for four years, has no residual value and has a positive net present value of $0.35 million.The profitability of the project in the first year will be:$'000 Revenue800Cost of sales(380)Gross profit420Expenses:Wages 120Advertising costs40Depreciation140Profit before tax120Tax30Net profit90 TT currently has a return on investment of 15.8% based on average investment. It is estimated that, at the end of the first year of trading, the replacement cost of the net assets of the investment will be $1 million.The managing director of TT Division is looking for investments to stabilise the financial performance of the division, which has been variable in recent years due to changing economic conditions and fluctuating sales demand.Required:(a) (i) Calculate both the return on investment and residual income for the first year of trading of thisinvestment. Explain whether the manager of TT is likely to invest in this project and whether theboard of EI would agree with this decision.(ii) Calculate the economic value added (EVA ®) of this investment for the first year of trading and comment on the investment opportunity from the viewpoint of both the group and the managerconcerned. Assume that economic depreciation is the same as accounting depreciation chargedagainst income. (12 marks) (b) Discuss four reasons why a division's performance should be measured separately from that of adivisional manager's performance. (4 marks) (c) EI has divisions operating in several different countries. Explain the problems that may be encountered incomparing the performance of divisions in different countries. (4 marks) (d) Discuss the view that divisional measures such as residual income and economic value added fail to takeaccount of liquidity and gearing as key aspects of performance, and suggest how liquidity and gearingcould be monitored at divisional level within a company such as EI.(5 marks)(Total: 25 marks)Question 4Gibson & Chew (G&C) is a certified accountancy practice specialising in medium-sized company audits, venture finance and taxation planning. G&C comprises six partners, eight managers, three other qualified staff, 15 accounting technicians and trainees and 20 office support staff. The senior and founding partners are David Gibson and Charles Chew. Gibson manages the audit part of the practice while Chew manages the special finance and taxation part. The workloads in the two areas are broadly equal.G&C has a good professional reputation and the practice has, over the 10 years since its formation, grown steadily. G&C prides itself on being a good employer. It pays staff market salary rates or above, provides a pleasant office working environment and supports its junior staff by paying their fees for professional training. Two years ago the two senior partners designed and implemented a staff appraisal scheme to assist in the process of staff development and staff performance reviews. The system has been based around an annual appraisal interview conducted by either David Gibson or Charles Chew. All staff have since been appraised once, the last few employees having just been appraised by the partners. The time delay in seeing all staff has posed some problems as the senior partners had also intended to use the appraisal interview as the basis to agree the annual bonus.Partners, managers and support staff views on the appraisal scheme have been very mixed. Some informal comments have been so negative as to cause the two senior partners to question whether the scheme should be abandoned altogether. Charles Chew and David Gibson have decided to list their feelings about the scheme and its operation.'The appraisal scheme has taken up far more of our time than we first thought.''Appraisal interviews have been very difficult to fit into our busy schedule.''We have had to see staff at random, as and when the appraisal interview could be organised.''Some staff seem to see the interview as an opportunity to complain or ask for things. If we make criticisms, some individuals get upset and ask us what more we expect them to do.''Some staff just sit there and do not contribute anything to the interview.''It is difficult to think of having to start again with the second round of interviews so soon after finishing the first.' 'We know for a fact that some of the problems in performance that we pointed out to staff during their appraisal interview have been totally ignored.''We have doubts whether the scheme has improved partnership performance in terms of client service, productivity and overall fee income.'Required(a) Explain the function, operation and potential benefits of staff appraisal schemes. (8 marks)(b) Comment on the apparent appraisal problems experienced at Gibson & Chew and suggest how asuccessful appraisal scheme could be organised and operated so as to address these problems.(12 marks)(c) Recommend performance measures that may help the senior partners to assess client service,productivity and overall fee income, and comment on the merits and limitations of each of the measures you have recommended.(5 marks)(Total: 25 marks)Maths tablesBPP House, Aldine Place, London W12 8AA Tel: 0845 0751 100 (for orders within the UK) Tel: +44 (0)20 8740 2211Fax: +44 (0)20 8740 1184/learningmedia。

accaf阶段考试顺序

ACCA(特许公认会计师)考试的阶段包括三个主要的考试级别:基础阶段、应用阶段和专业阶段。

以下是一般情况下ACCA 考试阶段的顺序:1. 基础阶段(Fundamentals Level):- AB(F1)- Accountant in Business- MA(F2)- Management Accounting- FA(F3)- Financial Accounting- LW(F4)- Corporate and Business Law- PM(F5)- Performance Management- TX(F6)- Taxation- FR(F7)- Financial Reporting- AA(F8)- Audit and Assurance- FM(F9)- Financial Management2. 应用阶段(Applied Knowledge and Applied Skills):在完成基础阶段的所有九门考试后,您将获得ACCA 的知识模块证书(Knowledge Module Certificate)和技能模块证书(Skills Module Certificate)。

接下来,您可以选择应用阶段的考试顺序,选择适合自己的顺序考试。

- SBL(P1)- Strategic Business Leader- SBR(P2)- Strategic Business Reporting- APM(P3)- Advanced Performance Management- ATX(P6)- Advanced Taxation- AAA(P7)- Advanced Audit and Assurance3. 专业阶段(Strategic Professional):在完成应用阶段的所有考试后,您将获得ACCA 的技能模块证书(Skills Module Certificate)。

接下来是专业阶段的考试,其中包含两门必修考试和两门选修考试:- SBR(P2)- Strategic Business Reporting(如果在应用阶段未选择考试)- SBL(P4)- Strategic Business Leader(如果在应用阶段未选择考试)- Options Modules(从以下选项中选择两门考试):- AFM(P4)- Advanced Financial Management- APM(P5)- Advanced Performance Management- ATX(P6)- Advanced Taxation- AAA(P7)- Advanced Audit and Assurance请注意,考试的顺序并非固定的,您可以根据自己的需求和兴趣选择适合自己的考试顺序。

acca sbl 12月 pre seen 材料解读 -回复

acca sbl 12月pre seen 材料解读-回复关于ACCA SBL 12月Pre-seen材料的解读ACCA(特许公认会计师协会)SBL(战略商务领导)考试是ACCA职业资格中的重要科目之一。

在12月的备考中,学员们将开始研究和分析Pre-seen材料,以便更好地应对考试。

在本文中,我们将一步一步地解读这些材料,并提供一些建议,以帮助学员们在考试中取得成功。

第一步:阅读材料并建立框架首先,学员们应该仔细阅读Pre-seen材料,并理解其中所提供的信息。

这包括公司的背景、组织结构、战略目标、财务状况等。

学员们可以将这些信息整理成一个框架,以便更好地组织和理解材料。

例如,可以将公司的组织结构制作成一个组织图,标示出不同的部门和职能,并将战略目标和财务状况与各部门相关联。

第二步:分析问题并制定解决方案在理解了Pre-seen材料的基础上,学员们应该开始分析材料中提出的问题,并制定相应的解决方案。

这些问题可能涉及到公司的战略问题、业务流程改进、财务管理等方面。

为了更好地回答这些问题,学员们可以根据材料中提供的信息,运用SWOT分析、PESTEL分析等工具和框架,深入分析公司的内部和外部环境,并找出解决问题的途径和方法。

第三步:与实际经验和理论知识结合在进行材料分析和解决方案制定的过程中,学员们应该运用自己的实际经验和理论知识,来进一步丰富和支持自己的分析和建议。

比如,学员们可以结合自己在实际工作中的经验,提供实际操作性的解决方案;同时,也可以结合自己学习ACCA课程中的知识,为自己的分析提供专业性的支持。

第四步:考虑利益相关方和可持续发展在解决问题和制定解决方案的过程中,学员们应该考虑到不同利益相关方的需求和期望,以及公司的可持续发展。

这包括股东、员工、客户、社会和环境等方面。

学员们可以通过分析材料,了解公司目前面临的挑战和机遇,制定可持续发展的战略,并考虑各利益相关方的需求,以实现公司的长期发展目标。

ACCA国际财会基础资格(简称FLQ)考试大纲

ACCA 国际财会基础资格(简称FLQ)考试大纲ACCA(特许公认会计师公会)2011 年推出了国际财会基础资格(Foundation-level Qalifications,简称FLQ)这一全新的资格认证项目包括一系列初级资格考试,学员可灵活选择,全面照顾学员和企业双方的实际需求。

该资格涵盖全面的财务和管理会计知识,并将专业素质和职业操守纳入考核范围。

该资格将包括:财务和管理会计入门证书财务和管理会计中级证书商业会计证书公认会计技师资格证书(CAT)无ACCA 学员注册资格的学生,可以无条件注册成为FLQ 学员,在获得商业会计证书后转换成为ACCA 学员。

FLQ-Financial Accounting (FFA)考试大纲To develop knowledge and understanding of the underlying principles and concepts relating to financial accounting and to demonstrate technical proficiency in the use of double entry techniques, including the preparation and interpretation of basic financial statements for sole traders, companies and simple groups of companies.温馨提醒:FLQ 中FFA 课程的考试大纲与ACCA F3 科目的考试大纲是完全一致的,学生可以用F3 的教材,并参加F3 的考试辅导来通过FFA 的考试。

FLQ-Accountant in Business (FAB)考试大纲To understand business in the context of its environment, including economic, legal, and regulatory influences on such aspects as governance,。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

特许公认会计师ACCA最新考试形式2015

本文由高顿ACCA整理发布,转载请注明出处

2014年8月,推出一系列F4考试资源;2014年12月,F4考试实行机考/笔试两种形式;2014年12月,F5,7,8,9考试改题型;2015年1月,部分地区取消F1,2,3笔试;2015年6月,F6考试改题型;2016年9月(预计),F5-9添加CBE(机考);2017年起,全球范围F1,2,3将取消笔试。

2014年8月,推出一系列F4考试资源

为支持F4考试变化(2014年12月),ACCA将于2014年8月提供更多资源供学员备考,资源包括:

技术文章TechnicalArticles(with special focus on CBE)

考试介绍Examiner ApproachInterviews(updated to reflect new structure)

视频Short Video(overview ofnew format andquestion types)

2014年12月,F4考试实行机考/笔试两种形式

F4考试在2014年12月将有较大的变化,包括考试将引入Objective Tests and MTQ(客观题和多任务题),考试时间将缩短为2小时。

学生可以在机考和笔试两种考试形式中选择一种。

改变只限F4 Global卷和UK卷,所有其他variant paper维持笔试。

F4的机考考试时间可以做到非常灵活,模式参照现在F1-3机考。

至此,F4将不能成为申请牛津布鲁克斯本科文凭的英文条件。

ALP有望成为F4机考中心。

相关的考官文章及样卷链接:

/gb/en/student/acca-qual-student-journey/qual-resource/acca -qualification/f4.html

2014年12月,F5,7,8,9考试改题型

ACCA将于2014年12月改变F5,F7,F8,F9的笔试题型。

届时相关考试都会分为两部分,A部分将包括选择题(以更广泛地测试大纲内容)。

B部分是传统题型。

相关的样卷都可以通过ACCA官网下载。

路径为ACCA官网->studentpage-> access resources ->选中相关科目,左手边栏目中有“December 2014 Specimen Exams”。

2015年1月,部分地区取消F1,2,3笔试

ACCA为了在2017年完全实现F1,2,3机考,将于2015年1月起,逐步按区域取消笔试。

第一批将取消笔试的区域有:阿曼,香港,斯里兰卡,柬埔寨,捷克共和国。

2015年6月,F6考试改题型

ACCA将于2016年6月改变F6笔试题型,也将引入客观题和多任务题。

(样卷请见注释图片2)

2015年9月或2016年3月(预计),增加F5-9考试次数(机考和笔试)

ACCA预计在2015年9月或者2016年3月时,将原有的2个考季改为4个,即每年的3月、6月、9月、12月四个考季。

改成4个考季后,每个考季13周,时间安排如下:

学习6周

考试2周

等成绩5周

最早可在等成绩的第1周报考下两季的考试。

改成4个考季之后,每个考季最多能考4门,但是一年最多能考8门新的(不含重考)科目。

目前的是每年考8门,不论重考否。

2016年9月(预计),F5-9添加CBE(机考)

ACCA计划在2016年9月在F5-9添加机考,但这一定是在改成4个考季之后才会实行。

从此,所有添加机考的科目,将不再提供PastExam Paper(历年真题)和Examiner’s Answer(考官答案),并且机考题目来自强大的Question Bank(题库)。

ACCA会定期向其中添加新题。

2017年起,全球范围F1,2,3将取消笔试

针对考试形式的变化,权威的三家机构将会相继推出新教材。

例如,针对12月的考试,BPP,Becker和Kaplan将分别会在5月,6月和10月出版新教材。

最后,对于机考,ACCA承诺会尽量优化考试界面,争取所有笔试能做的,机考都能做到。

(例如在题目上highlight, add, delete, draft)。

更多ACCA资讯请关注高顿ACCA官网:。