Selfsimilar additive processes and financial modelling

similar_text运行原理

similar_text运行原理Similar_text是一种用于比较两个字符串相似度的函数,它可以判断两个字符串之间的相似程度,从而可以应用于文本匹配、信息检索以及自然语言处理等领域中。

在本篇文章中,我将详细解释similar_text函数的原理和运行过程,并提供一步一步的说明。

1. 什么是similar_text函数?在PHP编程语言中,similar_text是一个内置函数,用于比较两个字符串的相似度。

它返回两个字符串之间的相似字符数。

相似字符数越多,表示两个字符串的相似度越高。

2. 函数声明和参数similar_text函数的声明如下:int similar_text ( string first , string second [, float &percent ])该函数有三个参数:- first:要比较的第一个字符串。

- second:要比较的第二个字符串。

- &percent(可选):一个引用变量,用于存储相似度的百分比值。

3. 运行过程(1) 计算两个字符串的长度similar_text函数首先会计算两个字符串的长度,分别存储在first_len和second_len变量中。

(2) 创建字符映射表使用一个二维数组matrix来存储两个字符串中每个字符的匹配状况。

matrix[i][j]表示第一个字符串中的第i个字符和第二个字符串中的第j个字符的匹配状态。

(3) 初始化矩阵接下来,similar_text函数会初始化矩阵matrix的第一行和第一列。

假设第一个字符串长度为first_len,第二个字符串长度为second_len,则将matrix[0][j]设为j(j=0至second_len),将matrix[i][0]设为i(i=0至first_len)。

(4) 计算相似字符数通过遍历两个字符串的所有字符,计算它们的匹配状态,从而得到相似字符数。

similar_text函数使用了一个嵌套循环遍历字符串,迭代i变量从1至first_len,迭代j变量从1至second_len。

深度优先局部聚合哈希

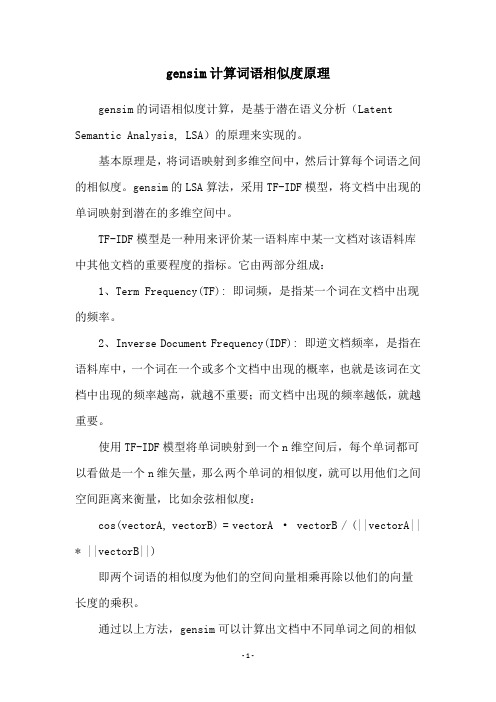

Vol.48,No.6Jun. 202 1第48卷第6期2 0 2 1年6月湖南大学学报)自然科学版)Journal of Hunan University (Natural Sciences )文章编号:1674-2974(2021 )06-0058-09 DOI : 10.16339/ki.hdxbzkb.2021.06.009深度优先局艺B 聚合哈希龙显忠g,程成李云12(1.南京邮电大学计算机学院,江苏南京210023;2.江苏省大数据安全与智能处理重点实验室,江苏南京210023)摘 要:已有的深度监督哈希方法不能有效地利用提取到的卷积特征,同时,也忽视了数据对之间相似性信息分布对于哈希网络的作用,最终导致学到的哈希编码之间的区分性不足.为了解决该问题,提出了一种新颖的深度监督哈希方法,称之为深度优先局部聚合哈希(DeepPriority Local Aggregated Hashing , DPLAH ). DPLAH 将局部聚合描述子向量嵌入到哈希网络 中,提高网络对同类数据的表达能力,并且通过在数据对之间施加不同权重,从而减少相似性 信息分布倾斜对哈希网络的影响.利用Pytorch 深度框架进行DPLAH 实验,使用NetVLAD 层 对Resnet18网络模型输出的卷积特征进行聚合,将聚合得到的特征进行哈希编码学习.在CI-FAR-10和NUS-WIDE 数据集上的图像检索实验表明,与使用手工特征和卷积神经网络特征的非深度哈希学习算法的最好结果相比,DPLAH 的平均准确率均值要高出11%,同时,DPLAH 的平均准确率均值比非对称深度监督哈希方法高出2%.关键词:深度哈希学习;卷积神经网络;图像检索;局部聚合描述子向量中图分类号:TP391.4文献标志码:ADeep Priority Local Aggregated HashingLONG Xianzhong 1,覮,CHENG Cheng1,2,LI Yun 1,2(1. School of Computer Science & Technology ,Nanjing University of Posts and Telecommunications ,Nanjing 210023, China ;2. Key Laboratory of Jiangsu Big Data Security and Intelligent Processing ,Nanjing 210023, China )Abstract : The existing deep supervised hashing methods cannot effectively utilize the extracted convolution fea tures, but also ignore the role of the similarity information distribution between data pairs on the hash network, result ing in insufficient discrimination between the learned hash codes. In order to solve this problem, a novel deep super vised hashing method called deep priority locally aggregated hashing (DPLAH) is proposed in this paper, which em beds the vector of locally aggregated descriptors (VLAD) into the hash network, so as to improve the ability of the hashnetwork to express the similar data, and reduce the impact of similarity distribution skew on the hash network by im posing different weights on the data pairs. DPLAH experiment is carried out by using the Pytorch deep framework. Theconvolution features of the Resnet18 network model output are aggregated by using the NetVLAD layer, and the hashcoding is learned by using the aggregated features. The image retrieval experiments on the CIFAR-10 and NUS - WIDE datasets show that the mean average precision (MAP) of DPLAH is11 percentage points higher than that of* 收稿日期:2020-04-26基金项目:国家自然科学基金资助项目(61906098,61772284),National Natural Science Foundation of China(61906098, 61772284);国家重 点研发计划项目(2018YFB 1003702) , National Key Research and Development Program of China (2018YFB1003702)作者简介:龙显忠(1985—),男,河南信阳人,南京邮电大学讲师,工学博士,硕士生导师覮 通信联系人,E-mail : *************.cn第6期龙显忠等:深度优先局部聚合哈希59non-deep hash learning algorithms using manual features and convolution neural network features,and the MAP of DPLAH is2percentage points higher than that of asymmetric deep supervised hashing method.Key words:deep Hash learning;convolutional neural network;image retrieval;vector of locally aggregated de-scriptors(VLAD)随着信息检索技术的不断发展和完善,如今人们可以利用互联网轻易获取感兴趣的数据内容,然而,信息技术的发展同时导致了数据规模的迅猛增长.面对海量的数据以及超大规模的数据集,利用最近邻搜索[1(Nearest Neighbor Search,NN)的检索技术已经无法获得理想的检索效果与可接受的检索时间.因此,近年来,近似最近邻搜索[2(Approximate Nearest Neighbor Search,ANN)变得越来越流行,它通过搜索可能相似的几个数据而不再局限于返回最相似的数据,在牺牲可接受范围的精度下提高了检索效率.作为一种广泛使用的ANN搜索技术,哈希方法(Hashing)[3]将数据转换为紧凑的二进制编码(哈希编码)表示,同时保证相似的数据对生成相似的二进制编码.利用哈希编码来表示原始数据,显著减少了数据的存储和查询开销,从而可以应对大规模数据中的检索问题.因此,哈希方法吸引了越来越多学者的关注.当前哈希方法主要分为两类:数据独立的哈希方法和数据依赖的哈希方法,这两类哈希方法的区别在于哈希函数是否需要训练数据来定义.局部敏感哈希(Locality Sensitive Hashing,LSH)[4]作为数据独立的哈希代表,它利用独立于训练数据的随机投影作为哈希函数•相反,数据依赖哈希的哈希函数需要通过训练数据学习出来,因此,数据依赖的哈希也被称为哈希学习,数据依赖的哈希通常具有更好的性能.近年来,哈希方法的研究主要侧重于哈希学习方面.根据哈希学习过程中是否使用标签,哈希学习方法可以进一步分为:监督哈希学习和无监督哈希学习.典型的无监督哈希学习包括:谱哈希[5(Spectral Hashing,SH);迭代量化哈希[6](Iterative Quantization, ITQ);离散图哈希[7(Discrete Graph Hashing,DGH);有序嵌入哈希[8](Ordinal Embedding Hashing,OEH)等.无监督哈希学习方法仅使用无标签的数据来学习哈希函数,将输入的数据映射为哈希编码的形式.相反,监督哈希学习方法通过利用监督信息来学习哈希函数,由于利用了带有标签的数据,监督哈希方法往往比无监督哈希方法具有更好的准确性,本文的研究主要针对监督哈希学习方法.传统的监督哈希方法包括:核监督哈希[9](Supervised Hashing with Kernels,KSH);潜在因子哈希[10](Latent Factor Hashing,LFH);快速监督哈希[11](Fast Supervised Hashing,FastH);监督离散哈希[1(Super-vised Discrete Hashing,SDH)等.随着深度学习技术的发展[13],利用神经网络提取的特征已经逐渐替代手工特征,推动了深度监督哈希的进步.具有代表性的深度监督哈希方法包括:卷积神经网络哈希[1(Convolutional Neural Networks Hashing,CNNH);深度语义排序哈希[15](Deep Semantic Ranking Based Hash-ing,DSRH);深度成对监督哈希[16](Deep Pairwise-Supervised Hashing,DPSH);深度监督离散哈希[17](Deep Supervised Discrete Hashing,DSDH);深度优先哈希[18](Deep Priority Hashing,DPH)等.通过将特征学习和哈希编码学习(或哈希函数学习)集成到一个端到端网络中,深度监督哈希方法可以显著优于非深度监督哈希方法.到目前为止,大多数现有的深度哈希方法都采用对称策略来学习查询数据和数据集的哈希编码以及深度哈希函数.相反,非对称深度监督哈希[19](Asymmetric Deep Supervised Hashing,ADSH)以非对称的方式处理查询数据和整个数据库数据,解决了对称方式中训练开销较大的问题,仅仅通过查询数据就可以对神经网络进行训练来学习哈希函数,整个数据库的哈希编码可以通过优化直接得到.本文的模型同样利用了ADSH的非对称训练策略.然而,现有的非对称深度监督哈希方法并没有考虑到数据之间的相似性分布对于哈希网络的影响,可能导致结果是:容易在汉明空间中保持相似关系的数据对,往往会被训练得越来越好;相反,那些难以在汉明空间中保持相似关系的数据对,往往在训练后得到的提升并不显著.同时大部分现有的深度监督哈希方法在哈希网络中没有充分有效利用提60湖南大学学报(自然科学版)2021年取到的卷积特征.本文提出了一种新的深度监督哈希方法,称为深度优先局部聚合哈希(Deep Priority Local Aggregated Hashing,DPLAH).DPLAH的贡献主要有三个方面:1)DPLAH采用非对称的方式处理查询数据和数据库数据,同时DPLAH网络会优先学习查询数据和数据库数据之间困难的数据对,从而减轻相似性分布倾斜对哈希网络的影响.2)DPLAH设计了全新的深度哈希网络,具体来说,DPLAH将局部聚合表示融入到哈希网络中,提高了哈希网络对同类数据的表达能力.同时考虑到数据的局部聚合表示对于分类任务的有效性.3)在两个大型数据集上的实验结果表明,DPLAH在实际应用中性能优越.1相关工作本节分别对哈希学习[3]、NetVLAD[20]和Focal Loss[21]进行介绍.DPLAH分别利用NetVLAD和Focal Loss提高哈希网络对同类数据的表达能力及减轻数据之间相似性分布倾斜对于哈希网络的影响. 1.1哈希学习哈希学习[3]的任务是学习查询数据和数据库数据的哈希编码表示,同时要满足原始数据之间的近邻关系与数据哈希编码之间的近邻关系相一致的条件.具体来说,利用机器学习方法将所有数据映射成{0,1}r形式的二进制编码(r表示哈希编码长度),在原空间中不相似的数据点将被映射成不相似)即汉明距离较大)的两个二进制编码,而原空间中相似的两个数据点将被映射成相似(即汉明距离较小)的两个二进制编码.为了便于计算,大部分哈希方法学习{-1,1}r形式的哈希编码,这是因为{-1,1}r形式的哈希编码对之间的内积等于哈希编码的长度减去汉明距离的两倍,同时{-1,1}r形式的哈希编码可以容易转化为{0,1}r形式的二进制编码.图1是哈希学习的示意图.经过特征提取后的高维向量被用来表示原始图像,哈希函数h将每张图像映射成8bits的哈希编码,使原来相似的数据对(图中老虎1和老虎2)之间的哈希编码汉明距离尽可能小,原来不相似的数据对(图中大象和老虎1)之间的哈希编码汉明距离尽可能大.h(大象)=10001010h(老虎1)=01100001h(老虎2)=01100101相似度尽可能小相似度尽可能大图1哈希学习示意图Fig.1Hashing learning diagram1.2NetVLADNetVLAD的提出是用于解决端到端的场景识别问题[20(场景识别被当作一个实例检索任务),它将传统的局部聚合描述子向量(Vector of Locally Aggregated Descriptors,VLAD[22])结构嵌入到CNN网络中,得到了一个新的VLAD层.可以容易地将NetVLAD 使用在任意CNN结构中,利用反向传播算法进行优化,它能够有效地提高对同类别图像的表达能力,并提高分类的性能.NetVLAD的编码步骤为:利用卷积神经网络提取图像的卷积特征;利用NetVLAD层对卷积特征进行聚合操作.图2为NetVLAD层的示意图.在特征提取阶段,NetVLAD会在最后一个卷积层上裁剪卷积特征,并将其视为密集的描述符提取器,最后一个卷积层的输出是H伊W伊D映射,可以将其视为在H伊W空间位置提取的一组D维特征,该方法在实例检索和纹理识别任务[23別中都表现出了很好的效果.NetVLAD layer(KxD)x lVLADvectorh------->图2NetVLAD层示意图⑷Fig.2NetVLAD layer diagram1201NetVLAD在特征聚合阶段,利用一个新的池化层对裁剪的CNN特征进行聚合,这个新的池化层被称为NetVLAD层.NetVLAD的聚合操作公式如下:NV((,k)二移a(x)(血⑺-C((j))(1)i=1式中:血(j)和C)(j)分别表示第i个特征的第j维和第k个聚类中心的第j维;恣&)表示特征您与第k个视觉单词之间的权.NetVLAD特征聚合的输入为:NetVLAD裁剪得到的N个D维的卷积特征,K个聚第6期龙显忠等:深度优先局部聚合哈希61类中心.VLAD的特征分配方式是硬分配,即每个特征只和对应的最近邻聚类中心相关联,这种分配方式会造成较大的量化误差,并且,这种分配方式嵌入到卷积神经网络中无法进行反向传播更新参数.因此,NetVLAD采用软分配的方式进行特征分配,软分配对应的公式如下:-琢II Xi-C*II 2=—e(2)-琢II X-Ck,II2k,如果琢寅+肄,那么对于最接近的聚类中心,龟&)的值为1,其他为0.aS)可以进一步重写为:w j X i+b ka(x i)=—e-)3)w J'X i+b kk,式中:W k=2琢C k;b k=-琢||C k||2.最终的NetVLAD的聚合表示可以写为:N w;x+b kv(j,k)=移—----(x(j)-Ck(j))(4)i=1w j.X i+b k移ek,1.3Focal Loss对于目标检测方法,一般可以分为两种类型:单阶段目标检测和两阶段目标检测,通常情况下,两阶段的目标检测效果要优于单阶段的目标检测.Lin等人[21]揭示了前景和背景的极度不平衡导致了单阶段目标检测的效果无法令人满意,具体而言,容易被分类的背景虽然对应的损失很低,但由于图像中背景的比重很大,对于损失依旧有很大的贡献,从而导致收敛到不够好的一个结果.Lin等人[21]提出了Focal Loss应对这一问题,图3是对应的示意图.使用交叉爛作为目标检测中的分类损失,对于易分类的样本,它的损失虽然很低,但数据的不平衡导致大量易分类的损失之和压倒了难分类的样本损失,最终难分类的样本不能在神经网络中得到有效的训练.Focal Loss的本质是一种加权思想,权重可根据分类正确的概率p得到,利用酌可以对该权重的强度进行调整.针对非对称深度哈希方法,希望难以在汉明空间中保持相似关系的数据对优先训练,具体来说,对于DPLAH的整体训练损失,通过施加权重的方式,相对提高难以在汉明空间中保持相似关系的数据对之间的训练损失.然而深度哈希学习并不是一个分类任务,因此无法像Focal Loss一样根据分类正确的概率设计权重,哈希学习的目的是学到保相似性的哈希编码,本文最终利用数据对哈希编码的相似度作为权重的设计依据具体的权重形式将在模型部分详细介绍.正确分类的概率图3Focal Loss示意图[21】Fig.3Focal Loss diagram12112深度优先局部聚合哈希2.1基本定义DPLAH模型采用非对称的网络设计.Q={0},=1表示n张查询图像,X={X i}m1表示数据库有m张图像;查询图像和数据库图像的标签分别用Z={Z i},=1和Y ={川1表示;i=[Z i1,…,zj1,i=1,…,n;c表示类另数;如果查询图像0属于类别j,j=1,…,c;那么z”=1,否则=0.利用标签信息,可以构造图像对的相似性矩阵S沂{-1,1}"伊”,s”=1表示查询图像q,和数据库中的图像X j语义相似,S j=-1表示查询图像和数据库中的图像X j语义不相似.深度哈希方法的目标是学习查询图像和数据库中图像的哈希编码,查询图像的哈希编码用U沂{-1,1}"",表示,数据库中图像的哈希编码用B沂{-1,1}m伊r表示,其中r表示哈希编码的长度.对于DPLAH模型,它在特征提取部分采用预训练好的Resnet18网络[25].图4为DPLAH网络的结构示意图,利用NetVLAD层聚合Resnet18网络提取到的卷积特征,哈希编码通过VLAD编码得到,由于VLAD编码在分类任务中被广泛使用,于是本文将NetVLAD层的输出作为分类任务的输入,利用图像的标签信息监督NetVLAD层对卷积特征的利用.事实上,任何一种CNN模型都能实现图像特征提取的功能,所以对于选用哪种网络进行特征学习并不是本文的重点.62湖南大学学报(自然科学版)2021年conv1图4DPLAH结构Fig.4DPLAH structure图像标签soft-max1,0,1,1,0□1,0,0,0,11,1,0,1,0---------*----------VLADVLAD core)c)l・>:i>数据库图像的哈希编码2.2DPLAH模型的目标函数为了学习可以保留查询图像与数据库图像之间相似性的哈希编码,一种常见的方法是利用相似性的监督信息S e{-1,1}n伊"、生成的哈希编码长度r,以及查询图像的哈希编码仏和数据库中图像的哈希编码b三者之间的关系[9],即最小化相似性的监督信息与哈希编码对内积之间的L损失.考虑到相似性分布的倾斜问题,本文通过施加权重来调节查询图像和数据库图像之间的损失,其公式可以表示为:min J=移移(1-w)(u T b j-rs)专,B i=1j=1s.t.U沂{-1,1}n伊r,B沂{-1,1}m伊r,W沂R n伊m(5)受FocalLoss启发,希望深度哈希网络优先训练相似性不容易保留图像对,然而Focal Loss利用图像的分类结果对损失进行调整,因此,需要重新进行设计,由于哈希学习的目的是为了保留图像在汉明空间中的相似性关系,本文利用哈希编码的余弦相似度来设计权重,其表达式为:1+。

gensim计算词语相似度原理

gensim计算词语相似度原理

gensim的词语相似度计算,是基于潜在语义分析(Latent Semantic Analysis, LSA)的原理来实现的。

基本原理是,将词语映射到多维空间中,然后计算每个词语之间的相似度。

gensim的LSA算法,采用TF-IDF模型,将文档中出现的单词映射到潜在的多维空间中。

TF-IDF模型是一种用来评价某一语料库中某一文档对该语料库中其他文档的重要程度的指标。

它由两部分组成:

1、Term Frequency(TF): 即词频,是指某一个词在文档中出现的频率。

2、Inverse Document Frequency(IDF): 即逆文档频率,是指在语料库中,一个词在一个或多个文档中出现的概率,也就是该词在文档中出现的频率越高,就越不重要;而文档中出现的频率越低,就越重要。

使用TF-IDF模型将单词映射到一个n维空间后,每个单词都可以看做是一个n维矢量,那么两个单词的相似度,就可以用他们之间空间距离来衡量,比如余弦相似度:

cos(vectorA, vectorB) = vectorA · vectorB / (||vectorA|| * ||vectorB||)

即两个词语的相似度为他们的空间向量相乘再除以他们的向量

长度的乘积。

通过以上方法,gensim可以计算出文档中不同单词之间的相似

度,从而推断出文档等同语句的内容。

selfattention的结构

self-attention的结构包括以下几个部分:

1. 输入:self-attention的输入是一个序列,可以是文本、图像等,每个元素都会被转换为一个向量。

2. 线性变换:将输入序列中的每个向量分别进行线性变换,得到三个新的向量序列,分别表示查询

(Query)、键(Key)和值(Value)。

3. 缩放点积:将查询向量和键向量进行点积运算,并除以一个缩放因子,以避免梯度消失或爆炸的问

题。

缩放因子通常是键向量的维度的平方根。

4. 归一化:将缩放点积的结果输入到一个softmax函数中,进行归一化处理,得到每个元素对应的权

重。

5. 加权和:将归一化后的权重与值向量进行加权和,得到self-attention的输出序列。

通过self-attention的结构,模型可以学习到输入序列中不同元素之间的关系,从而提取出更加丰富的特征信息。

同时,self-attention还可以并行计算,提高了模型的计算效率。

Ellis-Corrective-Feedback

T tries to elicit correct pronunciation and the corrects

S: alib[ai]

S fails again

T: okay, listen, listen, alb[ay] T models correct pronunciation

SS: alib(ay)

Theoretical perspectives

1. The Interaction Hypothesis (Long 1996) 2. The Output Hypothesis (Swain 1985;

1995) 3. The Noticing Hypothesis (Schmidt

1994; 2001) 4. Focus on form (Long 1991)

2. In the course of this, they produce errors. 3. They receive feedback that they recognize as

corrective. 4. The feedback causes them to notice the errors they

first row. (uptake)

The complexity of corrective feedback

Corrective feedback (CF) occurs frequently in instructional settings (but much less frequently in naturalistic settings)

Commentary

Initial focus on meaning Student perceives the feedback as corrective

python 语义相似度计算

python 语义相似度计算标题:Python语义相似度计算的应用与发展引言:Python语义相似度计算是一项重要的自然语言处理技术,通过对文本的语义进行建模和比较,可以实现词句之间的相似度度量。

该技术在信息检索、文本分类、机器翻译等领域有广泛的应用。

本文将介绍Python语义相似度计算的原理、方法以及其在实际应用中的发展。

一、Python语义相似度计算原理语义相似度计算是基于自然语言处理和机器学习的技术,其主要原理包括词向量表示、语义匹配和相似度度量。

首先,将文本表示为向量形式,常用的方法有词袋模型和词嵌入模型。

然后,通过计算向量之间的相似度,确定文本的相似程度。

二、Python语义相似度计算方法1. 基于词袋模型的相似度计算:将文本表示为词频向量,利用余弦相似度或欧氏距离等方法计算相似度。

2. 基于Word2Vec的相似度计算:通过训练词向量模型,将文本表示为词向量,然后计算词向量之间的相似度。

3. 基于BERT的相似度计算:使用预训练的BERT模型,将文本编码为向量表示,然后计算向量之间的相似度。

三、Python语义相似度计算的应用1. 信息检索:通过计算查询和文档之间的相似度,实现精确的文本匹配和检索。

2. 文本分类:利用语义相似度计算,可以将文本进行分类和归类,提高文本分类的准确性。

3. 机器翻译:通过计算原文和目标文之间的相似度,改善机器翻译的质量。

4. 智能问答:通过计算问题和答案之间的相似度,实现智能问答系统的快速响应。

四、Python语义相似度计算的发展前景随着自然语言处理技术的不断发展,Python语义相似度计算也在不断进步。

未来的发展方向包括更精确的词向量表示、更高效的相似度计算方法以及更广泛的应用领域。

此外,与深度学习、知识图谱等技术的结合也将推动语义相似度计算的发展。

结论:Python语义相似度计算是一项重要的自然语言处理技术,具有广泛的应用前景。

通过不断改进算法和方法,可以提高计算的准确性和效率,使得语义相似度计算在各个领域发挥更大的作用。

李宏毅-B站机器学习视频课件BP全

Gradient Descent

Network parameters

Starting

0

Parameters

L

L w1

L w

2

L b1

L b2

w1 , w2 ,, b1 , b2 ,

b

4

2

=

′

’’

′ ′′

(Chain rule)

=

+

′ ′′

Assumed

?

?

3

4

it’s known

Backpropagation – Backward pass

Compute Τ for all activation function inputs z

Chain Rule

y g x

Case 1

z h y

x y z

Case 2

x g s

y hs

x

s

z

y

dz dz dy

dx dy dx

z k x, y

dz z dx z dy

ds x ds y ds

Backpropagation

2

Compute Τ for all parameters

Backward pass:

Compute Τ for all activation

function inputs z

Backpropagation – Forward pass

数据挖掘算法原理与实现第2版第三章课后答案

数据挖掘算法原理与实现第2版第三章课后答案

1.密度聚类分析:

原理:密度聚类分析是指通过测量数据对象之间的密度(density)

来将其聚成几个聚类的一种聚类分析方法。

它把距离邻近的数据归入同一

类簇,并把不相连的数据分成不同的类簇。

实现:通过划分空间中每一点的邻域来衡量数据点之间的聚类密度。

它将每个数据点周围与它最近的K个数据点用一个空间圆包围起来,以定

义该数据点处的聚类密度。

然后,可以使用距离函数将所有点分配到最邻

近的类中。

2.引擎树:

原理:引擎树(Search Engine Tree,SET)是一种非常有效的数据

挖掘方法,它能够快速挖掘关系数据库中指定的有价值的知识。

实现:SET是一种基于决策树的技术,通过从关系数据库的历史数据

中提取出有价值的信息,来建立一种易于理解的引擎树,以及一些有益的

信息发现知识,以便用户快速找到想要的信息。

SET对原始数据进行一系

列数据挖掘处理后,能够提取出其中模式分析的信息,从而实现快速、高

效的引擎。

3.最大期望聚类:

原理:最大期望聚类(Maximization Expectation Clustering,MEC)是一种有效的数据挖掘算法,它可以自动识别出潜在的类簇结构,提取出

类簇内部的模式,帮助用户快速完成类簇分析任务。

qdrant 相似度查询算法

qdrant 相似度查询算法一、qdrant相似度查询算法的原理qdrant相似度查询算法是一种基于向量空间模型的相似度计算方法。

该算法通过将待查询的向量与已有的向量集合进行相似度比较,从而找到与之最相似的向量。

在qdrant相似度查询算法中,首先需要将待查询的向量和已有的向量进行向量化,通常使用词袋模型或者词向量模型进行表示。

然后,通过计算两个向量之间的余弦相似度来衡量它们之间的相似程度。

余弦相似度是通过计算两个向量的内积除以它们的模长得到的,值域在[-1, 1]之间,值越接近1表示两个向量越相似。

二、qdrant相似度查询算法的应用场景1. 文本相似度查询:qdrant相似度查询算法可以用于文本相似度查询,通过将文本向量化,并计算文本之间的相似度,可以实现文本的快速检索和推荐。

2. 图像相似度查询:qdrant相似度查询算法也可以用于图像相似度查询,通过将图像向量化,并计算图像之间的相似度,可以实现图像的快速搜索和匹配。

3. 推荐系统:qdrant相似度查询算法可以用于推荐系统中的用户相似度计算和物品相似度计算,通过计算用户之间或物品之间的相似度,可以为用户提供个性化的推荐结果。

三、qdrant相似度查询算法的优势1. 高效性:qdrant相似度查询算法利用向量空间模型进行相似度计算,避免了传统的遍历搜索方法,因此具有较高的查询效率。

2. 精确性:qdrant相似度查询算法使用余弦相似度作为相似度度量,可以较准确地衡量向量之间的相似程度。

3. 可扩展性:qdrant相似度查询算法可以处理大规模的向量集合,支持高并发的查询请求,具有良好的可扩展性。

4. 应用广泛:qdrant相似度查询算法可以应用于文本、图像等多种类型的数据,适用于各种不同的应用场景。

qdrant相似度查询算法是一种基于向量空间模型的相似度计算方法,可以用于文本相似度查询、图像相似度查询以及推荐系统等应用中。

该算法具有高效性、精确性、可扩展性和广泛的应用范围,对于提高数据检索和推荐的效率和准确性具有重要意义。

python实现贝叶斯知识追踪模型代码

Python实现贝叶斯知识追踪模型代码1. 简介贝叶斯知识追踪模型是一种基于贝叶斯统计原理的机器学习模型,用于追踪知识的演化过程。

它能够根据已有的知识数据和新的观测数据,通过贝叶斯推断方法更新知识模型的概率分布,从而实现对知识的追踪和更新。

在本文中,我们将使用Python语言实现贝叶斯知识追踪模型的代码,并详细介绍算法的原理和实现细节。

2. 贝叶斯知识追踪模型原理2.1 贝叶斯统计原理贝叶斯统计原理是一种基于条件概率的统计推断方法。

在贝叶斯统计中,我们将待推断的未知量称为参数,将已观测到的数据称为观测量。

贝叶斯统计的核心思想是通过已观测数据更新对参数的先验概率分布,得到参数的后验概率分布。

具体地,假设我们有一个参数θ和一组观测数据D,我们希望推断参数θ的概率分布。

根据贝叶斯统计原理,我们可以通过以下公式计算参数θ的后验概率分布:P(θ|D)=P(D|θ)⋅P(θ)P(D)其中,$ P(θ|D) $ 表示参数θ在给定观测数据D下的后验概率,$ P(D|θ)$ 表示观测数据D在给定参数θ下的概率,$ P(θ) $ 表示参数θ的先验概率,$ P(D) $ 表示观测数据D的边缘概率。

2.2 贝叶斯知识追踪模型贝叶斯知识追踪模型是基于贝叶斯统计原理的推断模型,用于追踪知识的演化过程。

在贝叶斯知识追踪模型中,我们将知识的状态变化看作是参数的变化,将观测数据看作是对知识状态的观测。

具体地,假设我们有一个知识模型,其中每个知识点对应一个参数θ,表示该知识点的概率。

我们还有一组观测数据D,表示新的知识点观测结果。

根据贝叶斯统计原理,我们可以通过观测数据D更新知识模型的概率分布。

具体步骤如下:1.初始化知识模型的先验概率分布P(θ);2.根据观测数据D计算每个知识点的似然概率P(D|θ);3.根据贝叶斯统计原理计算每个知识点的后验概率分布P(θ|D)。

在实际应用中,我们可以使用迭代的方式,每次观测到新的数据时更新知识模型的概率分布。

refiner 参数

refiner 参数Refiner 参数是指在机器学习或数据预处理过程中用于优化模型或数据集的参数。

这些参数通常用于调整模型或数据集的复杂度、精度、过拟合或欠拟合等问题。

Refiner 参数的具体值取决于所使用的模型和数据集,但以下是一些常见的Refiner 参数及其作用:1. 正则化参数(Regularization Parameters):用于控制模型复杂度的参数,例如 L1 和 L2 正则化。

这些参数可以防止模型过拟合,并提高模型的泛化能力。

2. 学习率(Learning Rate):用于控制模型权重更新的步长。

较大的学习率可能导致模型收敛更快,但也可能导致模型不稳定;较小的学习率可能导致模型收敛更稳定,但也可能导致训练时间过长。

3. 动量(Momentum):用于加速模型收敛并减少训练过程中的震荡。

它通过在梯度方向上增加一维项来加速权重更新。

4. 批归一化(Batch Normalization):用于加速模型收敛并提高模型的泛化能力。

它通过在每一层神经网络中归一化输入特征来加速训练过程。

5. Dropout(丢弃):用于防止模型过拟合。

在训练过程中,Dropout 随机将一部分输入神经元设置为零,以防止模型对训练数据中的噪声或特定特征的依赖。

6. 早停(Early Stopping):用于防止模型过拟合。

当验证损失在连续几个批次中不再改善时,训练过程可以提前停止,以避免过拟合。

7. 剪枝(Pruning):用于减小模型的大小和计算复杂度。

它通过去除神经网络中的一部分连接或神经元来简化模型结构,以提高推理速度和减少过拟合。

这些参数通常需要通过实验来调整,以找到最优的值,以便在训练过程中获得最佳的性能和泛化能力。

自相似性 下

4得到两幅图像的整体描述符,在两幅图像中找到相对几何位置和描述符值相同的部分具体步骤如下首先要过滤掉欠描述符,即中心块突出(和周围的任何块都不相似的)和一大片同类的区域(颜色纹理等相同)。

前者的突出部分可以发现其描述符值在归一化前都低于某一阈值,后者可以通过稀疏度测量的方式找到。

接着使用“概率星状图”模型局部描述符的相对几何关系,Sigmoid functionSigmoid函数是一个S型函数. Sigmoid函数的数学公式为5 图像中对象的检测Figure 4. 对象检测. (a) 模板(b)相关性检测. 被灰色覆盖的彩色部分是连续相关性值大于某一阈值的图像部分。

具体步骤如下:1、给定一个感兴趣的模板,通过计算它的局部图像的描述符(运用公式1)来生成其整体描述符。

2、运用第四部分的算法在一对图像中查找模板整体描述Figure 5. Detection using a sketch. (a) A hand-sketched template. (b) Detected locations in other images.Sec.4.Figure 6. Detection using a sketch. (a) A hand-sketched template.(b) The images against which it was compared with the corresponding detectionsFigure 7. Comparison to other descriptors and match measures. We compared our method with several other state-of-the-art localdescriptors and matching methods on more than 60 challenging image pairs. All these methods failed to find thetemplate in Image 2 in themajority of the pairs, whereas our method found the objects in the correct location in 86% of them. Each method was used to generate alikelihood surface, and peaks above 90% of its highest value are displayed. Displayed are a few such examples (these are representativeresults, each template was compared against multiple images not shown in the figure) – see text for more details. The object in each pairof images was of similar size (up to +/- 20% in scale), but is often displayed larger, for visibility purposes.。

levenshtein 相似度算法实现 -回复

levenshtein 相似度算法实现-回复什么是Levenshtein相似度算法?Levenshtein相似度算法,也称为编辑距离算法,是用于衡量两个字符串之间差异程度的一种方法。

它通过计算将一个字符串转换为另一个字符串所需的最少操作次数来确定相似度。

这种算法最早由俄罗斯科学家Vladimir Levenshtein于1965年提出,因此得名。

它对于自然语言处理、拼写检查、语音识别等领域,具有广泛的应用价值。

Levenshtein 相似度算法主要包括三种基本操作,分别是插入、删除和替换。

插入操作指的是在一个字符串中插入一个字符,使其与另一个字符串匹配;删除操作指的是从一个字符串中删除一个字符,使其与另一个字符串匹配;替换操作指的是将一个字符串中的字符替换为另一个字符,使其与另一个字符串匹配。

接下来,我们将一步一步地回答如何实现这种算法。

第一步是确定两个字符串,我们假设这两个字符串分别是A和B。

第二步是创建一个二维数组DP,大小为(A的长度+1)乘以(B的长度+1)。

这个数组将用于存储每个子问题的解,并且有助于计算整体问题的解。

第三步是初始化DP数组。

我们需要将DP数组的第一行和第一列填充为从0到A的长度和从0到B的长度的整数。

第四步是开始填充DP数组。

我们可以使用一个两层嵌套的循环来遍历数组的每个元素,并计算编辑距离。

对于数组中的每个元素,我们可以使用以下公式来计算编辑距离:if A[i-1] == B[j-1]:DP[i][j] = DP[i-1][j-1]else:DP[i][j] = min(DP[i-1][j] + 1, DP[i][j-1] + 1, DP[i-1][j-1] + 1)其中,A[i-1]表示A字符串的第i个字符,B[j-1]表示B字符串的第j个字符。

在这个公式中,如果A的第i个字符和B的第j个字符相同,则编辑距离与上一个子问题的编辑距离相等。

如果它们不相同,则编辑距离等于上一个子问题的编辑距离加上1,或者等于上一个子问题的插入、删除或替换操作的编辑距离。

Recurrent extensions of self–similar Markov processes and Cramer’s condition

Universit´e s de Paris6&Paris7-CNRS(UMR7599)PR´EPUBLICATIONS DU LABORATOIRE DE PROBABILIT´ES&MOD`ELES AL´EATOIRES4,place Jussieu-Case188-75252Paris cedex05http://www.proba.jussieu.frRecurrent extensions of self-similarMarkov processes and Cramer’s conditionV.RIVEROJUILLET2003Pr´e publication n o838Laboratoire de Probabilit´e s et Mod`e les Al´e atoires,CNRS-UMR7599, Universit´e Paris VI&Universit´e Paris VII,4,place Jussieu,Case188,F-75252Paris Cedex05.Recurrent extensions of self–similar Markov processes and Cramer’s conditionV´ıctor RIVERO∗†July4,2003AbstractLetξbe a real valued L´e vy process that drifts to−∞and satisfies Cramer’s condition,and X a self–similar Markov process associated toξvia Lamperti’s[22]transformation.In this case,X has0as a trap and fulfills the assumptions of Vuolle-Apiala[34].We deduce from[34]thatthere exists a unique excursion measure n,compatible with the semigroup of X and such thatn(X0+>0)=0.Here,we give a precise description of n via its associated entrance law.To thatend,we construct a self–similar process X ,which can be viewed as X conditioned to never hit0,and then we construct n in a similar way like the Brownian excursion measure is constructedvia the law of a Bessel(3)process.An alternative description of n is given by specifying the lawof the excursion process conditioned to have a given length.We establish some duality relationsfrom which we determine the image under time reversal of n.Key words.Self–similar Markov process,description of excursion measures,weak dual-ity,L´e vy processes.A.M.S.Classification.60J25(60G18).1IntroductionLet X=(X t,t≥0)be a strong Markov process with values in[0,∞[and for x≥0,denote by P x its law starting from x.Assume that X fulfills the scaling property:thereexists someα>0such thatthe law of(cX tc−1/α,t≥0)under P x is P cx,(1) for any x≥0and c>0.Such processes were introduced by Lamperti[22]under the nameof semi–stable processes,nowadays they are calledα–self–similar Markov processes.Werefer to Embrechts and Maejima[14]for a recent account on self–similar processes.Lamperti established that for eachfixedα>0,there exists a one to one correspondence betweenα–self–similar Markov processes on]0,∞[and L´e vy processes that we next sketch.Let(D,D)be the space of c`a dl`a g pathsω:[0,∞[→]−∞,∞[endowed with theσ–algebra ∗Research supported by a grant from CONACYT(National Council of science and technology Mexico).†Laboratoire de Probabilit´e s et Mod`e les Al´e atoires,Universit´e Pierre et Marie Curie;175,rue du Chevaleret, F-75013Paris,France.mail:rivero@ccr.jussieu.fr121INTRODUCTION generated by the coordinate maps and the naturalfiltration(D t,t≥0).Let P be aprobability measure on D such that under P the coordinate processξis a L´e vy processthat drifts to−∞,i.e.lim s→∞ξs=−∞.Set for t≥0τ(t)=inf{s>0, s0eξr/αdr>t},with the usual convention that inf{∅}=∞.For an arbitrary x>0,let P x be thedistribution on D+={ω:[0,∞[→[0,∞[c`a dl`a g},of the time–changed processx exp ξτ(tx−1/α) ,t≥0,where the above quantity is assumed to be0whenτ(tx−1/α)=∞.We agree that P0isthe law of the process identical to0.Classical results on time change yields that under(P x,x≥0)the process X is Markovian with respect to thefiltration(G t=Dτ(t),t≥0).Furthermore,X has the scaling property(1).Thus,X is a self–similar Markov process on[0,∞[having0as trap or absorbing point.Conversely,any self–similar Markov processthat has0as a trap can be constructed in this way,cf.[22].Let T0be thefirst hitting time of0for X,i.e.T0=inf{t>0:X t=0}.It should be clear that the distribution of T0under P x is the same as that of x1/αI underP,with I the so–called L´e vy exponential functional associated toξandα,that isI= ∞0exp{ξs/α}ds.(2)Sinceξdrifts to−∞we have that I<∞,P–a.s.and as a consequence P x(T0<∞)=1for all x>0.Denote P t and V q the semigroup and resolvent for the process X killed attime T0,say(X,T0),P t f(x)=E x(f(X t),t<T0),x>0,V q f(x)= ∞0e−qt P t f(x)dt,x>0,for measurable functions f non–negative or bounded.It is customary to refer to(X,T0)as the minimal process.Given that the former construction enables to describe the behavior of the self–similar Markov process X until itsfirst hitting time of0,Lamperti[22]raised the following ques-tion:What are the self–similar Markov processes X on[0,∞[which behave like(X,T0) up to the time T0?Lamperti solved this problem in the case when the minimal processis a Brownian motion killed at0.Then Vuolle-Apiala[34]tackled this problem using theexcursion theory for Markov processes and assuming that the following hypotheses hold.There existsκ>0such that(H1-a)the limitlim x→0E x(1−e−T0)xκ,exists and is strictly positive;3(H1-b)the limitlimx→0V q f(x) x,exists for all f∈C K]0,∞[and is strictly positive for some such functions,with C K]0,∞[={f:R→R,continuous and with compact support on]0,∞[}.The main result in[34]is the existence of an unique entrance law(n s,s>0)such thatlims→0n s B c=0,for every neighborhood B of0and∞0e−s n s1ds=1.This entrance law is determined by its q–potential by the formula∞0e−qs n s fds=lim x→0V q f(x)E x(1−e−T0),q>0,(3) for f∈C K]0,∞[.Then,using the results of Blumenthal[7],Vuolle-Apiala proved that associated to the entrance law(n s,s>0)there exists a unique recurrent Markov process X having the scaling property(1)which is an extension of the minimal process(X,T0), that is X killed at time T0is equivalent to(X,T0)and0is a recurrent regular state for X,i.e. P x(T0<∞)=1,∀x>0, P0(T0=0)=1,with P the law on D+of X.Furthermore,we know from[7]that there exists a unique excursion measure say n,on(D+,G∞)compatible with the semigroup P t such that its associated entrance law is(n s,s>0);the property lim s→0n s B c=0,for any B neigh-borhood of0is equivalent to n(X0+>0)=0,that is the process leaves0continuously under n.Then the excursion measure n is the unique excursion measure having the prop-erties n(X0+>0)=0and n(1−e−T0)=1.See subsection2.1for the definitions.Thefirst aim of this paper is provide a more explicit description of the excursion measure n and its associated entrance law(n s,s>0).To that purpose,we shall mimic a well known construction of the Brownian excursion measure via the Bessel(3)process that we next sketch for ease of reference.Let P(respectively R)be a probability measure on (D+,G∞)under which the coordinate process is a Brownian motion killed at0(respectively a Bessel(3)process).The probability measure R appears as the law of the Brownian motion conditioned to never hit0.More precisely,for u>0,x>0limt→∞P x(A|T0>t)=R x(A),for any A∈G u,see e.g.McKean[23].Moreover,the function h(x)=x−1,x>0is excessive for the semigroup of the Bessel(3)process and its h–transform is the semigroup of the Brownian motion killed at0.Let n be the h–transform of R0via the function h(x)=x−1,i.e.n is the unique measure on(D+,G∞)with support on{T0>0}such that under n the coordinate process is Markovian with semigroup that of the Brownian motion killed at0,and for every stopping time T in G t and any G T–measurable variableF T,n(F T,T<T0)=R0(F T1X T).41INTRODUCTION Then the measure n is a multiple of the Itˆo’s excursion measure for Brownian motion,seee.g.Imhof[20]§4.In order to carry out this program we will make the following hypotheses on the L´e vy processξ.(H2-a)ξis not arithmetic,i.e.the state space is not a subgroup of k Z for any real number k;(H2-b)There existsθ>0such that E(eθξ1)=1;(H2-c)E(ξ+1eθξ1)<∞,with a+=a∨0.The condition(H2-c)can be stated in terms of the L´e vy measure ofξas(H2-c’) {x>1}xeθxΠ(dx)<∞;cf.Sato[32]Theorem25.3.Such hypotheses are satisfied by a wide class of L´e vy processes,in particular by those associated with self–similar diffusions and stable processes.In thesequel we will refer to these hypotheses as the(H2)hypotheses,unless otherwise stated.The condition(H2-b)is the so–called Cramer’s condition for the L´e vy processξand forcesξto drifts to−∞or equivalently E(ξ1)<0.Cramer’s condition enable us toconstruct a law P on D,such that under P the coordinate processξ ,is a L´e vy processthat drifts to∞and P |D t=eθξt P|D t.Then,we will show that the self–similar Markovprocess X associated to the L´e vy processξ plays the rˆo le of a Bessel(3)process in ourconstruction of the excursion measure n.The rest of this paper is organized as follows.In Subsection2.1we recall the Itˆo’s program as settled by Blumenthal[7].The excursion measure n that interests us is theonly excursion measure having the property n(X0+>0)=0.Nevertheless,this is notthe only excursion measure compatible with the semigroup of the minimal process,that iswhy in Subsection2.2we review some properties that should be satisfied by any excursionmeasure corresponding to a self–similar extension of the minimal process.There we alsoobtain necessary and sufficient conditions for the existence of an excursion measure n jsuch that n j(X0=0)=0,which are valid for any self–similar Markov process having0asa trap.In Subsection2.3we construct a self–similar Markov process X which is related to(X,T0)in an analogue way like the Bessel(3)process does to Brownian motion killed at0,prove that the conditions(H1)are satisfied under the hypothesis(H2),give a more explicitexpression for the limit in equation(3)and that the hypothesis(H1)imply the conditions(H2-b,c).Next,in Section3we give our main description of the excursion measure n andgive an answer to the question raised by Lamperti that can be sketched as follows:givena L´e vy processξsatisfying the hypotheses(H2),then anα–self–similar Markov processX associated toξ,admits a recurrent extension that leaves0continuously a.s.if andonly if0<αθ<1.The purpose of Section4is to give an alternative description of themeasure n by determining the law of the excursion process conditioned by its length,forBrownian motion this corresponds to the description of the Itˆo excursion measure via thelaw of a Bessel(3)bridge.In Section5we study some duality relations for the minimalprocess and in particular we determine the image under time reversal of n.Finally,in theAppendix A we establish that the extensions of any two minimal processes which are inweak duality still are in weak duality as could be expected.Last,the development of this work is largely based on the theory of h–transforms of Doob,cf.Sharpe[33]or Walsh[35],which will be used without further reference.5 2Preliminaries andfirst resultsThis section contains several parts.In thefirst one,we recall the Itˆo’s program and the results in Blumenthal[7].The purpose of Subsection2.2is study the excursion measures compatible with the semigroup of the minimal process(X,T0).Finally,in Subsection2.3we establish the existence of a self–similar Markov process X which bears the same relation to the minimal process(X,T0)as the Bessel(3)process does to Brownian motion killed at0.The results in Subsections2.1and2.2do not require hypotheses(H2).2.1Some general facts on recurrent extensions of Markov processesA measure n on(D+,G∞)having infinite mass is called a pseudo excursion measure com-patible with the semigroup P t if the following are satisfied:(i)n is carried by{ω∈D+|T0(ω)>0and X t(ω)=0,∀t≥T0};(ii)for every bounded G∞–measurable H and each t>0andΛ∈G tn(H◦θt,Λ∩{t<T0})=n(E X t(H),Λ∩{t<T0}),whereθt denotes the shift operator.If moreover(iii)n(1−e−T0)<∞;we will say that n is an excursion measure.A normalized excursion measure n is an excursion measure n such that n(1−e−T0)=1.The rˆo le played by condition(iii)will be explained below.The entrance law associated to a pseudo excursion measure n is defined byn s(dy):=n(X s∈dy,s<T0),s>0.A partial converse holds:given an entrance law(n s,s>0)such that∞0(1−e−s)dn s1<∞,there exists a unique excursion measure n such that its associated entrance law is(n s,s> 0),see e.g.[7].It is well known in the theory of Markov process that a way to construct recurrent extensions of a Markov process is the Itˆo’s program or pathwise approach that can be described as follows.Assume that there exists an excursion measure n compatible withthe semigroup of the minimal process P t.Realize a Poisson point process∆=(∆s,s>0)on D+with characteristic measure n.Thus each atom∆s is a path and T0(∆s)denotesits lifetime,i.e.T0(∆s)=inf{t>0:∆s(t)=0}.Setσt= s≤t T0(∆s),t≥0.62PRELIMINARIES AND FIRST RESULTS Since n(1−e−T0)<∞,σt<∞a.s.for every t>0.It follows that the processσ=(σt,t≥0)is an increasing c`a dl`a g process with stationary and independent increments,i.e.a subordinator.Its law is characterized by its Laplace exponentφ,defined byE(e−λσ1)=e−φ(λ),λ>0,andφ(λ)can be expressed thanks to the L´e vy–Kintchine’s formula asφ(λ)= ]0,∞[(1−e−λs)ν(ds),withνa measure such that s∧1ν(ds)<∞,called the L´e vy measure ofσ;see e.g.Bertoin[1]§3for background.An application of the exponential formula for Poissonpoint process givesE(e−λσ1)=e−n(1−e−λT0),λ>0,i.e.φ(λ)=n(1−e−λT0)and the tail of the L´e vy measure is given byν[s,∞[=n(s<T0)=n s1,s>0.Observe that if we assumeφ(1)=n(1−e−T0)=1thenφis uniquely determined.Sincen has infinite mass,σt is strictly increasing in t.Let L t be the local time at0,i.e.thecontinuous inverse ofσL t=inf{r>0:σr>t}=inf{r>0:σr≥t}.Define a process( X t,t≥0)as follows.For t≥0,let L t=s,thenσs−≤t≤σs,setX t= ∆s(t−σs−)ifσs−<σs0ifσs−=σs or s=0.(4)That the process so constructed is a Markov process has been established in all its gene-rality by Salisbury[30,31]and under some regularity hypotheses on the semigroup of theminimal process by Blumenthal[7].See also Rogers[29]for its analytical counterpart.Inour setting the hypotheses in[7]are satisfied as it is stated in the following lemma.Lemma1.Let C0]0,∞[,be the space of continuous functions on]0,∞[vanishing at0and∞.(i)if f∈C0]0,∞[,then P t f∈C0]0,∞[and P t f→f uniformly as t→0.(ii)E x(e−qT0)is continuous in x for each q>0andlim x→0E x(e−T0)=1and limx→∞E x(e−T0)=0.A proof to this Lemma can be found in[34]pp.549–550.Then we have from[7]that X is a Markov process with Feller semigroup and its resolvent{U q,q>0}satisfiesU q f(x)=V q f(x)+E x(e−qT0)U q f(0),x>0,for f∈C b(R+)={f:R+→R,continuous and bounded}.That is X is an extension of the minimal process.Furthermore,if{X t,t≥0}is a Markov process extending the minimal one with Itˆo excursion measure n and local time at0,say{L t,t≥0},such thatE ( ∞0e−s dL s)=1,2.2Some properties of excursion measures for self–similar Markov process7 where E is the law for X .Then the process X and X are equivalent and the Itˆo’s excursion measure for X is n.Thus,the results in[7]establish a one to one relation between excursion measures and recurrent extensions of Markov process.Given an excursion measure n we will say that theassociated extension of the minimal process leaves0continuously a.s.if n(X0+>0)=0or equivalently,in terms of its entrance law,lim s→0n s(B c)=0for every neighborhood Bof0,see e.g.[7];if n is such that n(X0+=0)=0,we will say that the extension leaves0by jumps a.s.The latter condition on n is equivalent to the existence of a jumping–inmeasureη,that isηis aσ–finite measure on]0,∞[such that the entrance law associatedto n can be expressed asn s f=n(f(X s),s<T0)= ]0,∞[η(dx)P s f(x),s>0,for every f∈C b(R+),cf.Meyer[25].Finally,observe that if n is a pseudo excursion measure that does not satisfies the condition(iii),one can still realize a Poisson point process of excursions on(D+,G∞)withcharacteristic measure n but we can not form a process extending the minimal one by sticking together the excursions because the sum of lengths s≤t T0(Y s),is infinite P-a.s.for every t>0.2.2Some properties of excursion measures for self–similarMarkov processNext,we deduce necessary and sufficient conditions that must be satisfied by an excursionmeasure in order that the associated recurrent extension of the minimal process to be self–similar.For c∈R,let H c be the dilatation H c f(x)=f(cx).Lemma2.Let n be an excursion measure and X the associated recurrent extension ofthe minimal process.The following are equivalent(i)The process X has the scaling property(ii)there existsγ∈]0,1[such that for any c>0,n( T00e−qs f(X s)ds)=c(1−γ)/αn( T00e−(qc1/αs)H c f(X s)ds),for f∈C b(R+).(iii)there existsγ∈]0,1[such that for any c>0,n s f=c−γ/αn s/c1/αH c f for all s>0,for f∈C b(R+).Remark If one of the conditions(i–iii)in the previous Lemma holds,then the subordi-natorσwhich is the inverse local time of X,is a stable subordinator of parameterγ,withγdetermined in the condition(ii)or(iii).Proof.(ii)⇐⇒(iii)is straightforward.82PRELIMINARIES AND FIRST RESULTS(i)⇒(ii).Suppose that there exists an excursion measure n such that the associated recurrent extension X has the scaling property(1).Let M be the random set of zeros for the process X,i.e.M={t≥0| X(t)=0}.By construction M is the closed range of the subordinatorσ=(σt,t≥0),that is M is a regenerative set.The recurrence of X implies that M is unbounded a.s.By the scaling property for X we have thatM=d c M,for each c>0,that is M is self–similar.Thus the subordinator should have the scaling property andsince the only L´e vy processes that have the scaling property are the stable processes itfollows thatσis a subordinator stable of parameterγfor someγ∈]0,1[or in terms of itsLaplace exponentφ(λ)=n(1−e−λT0)=λγ,λ>0.Recall that the scaling property forthe extension can be stated in terms of its resolvent by saying that for any c>0,U q f(x)=c1/αU qc1/αH c f(x/c),for all x≥0,(5) for f∈C b(R+).Using the compensation formula for Poisson point processes we get thatU q f(0)=n( T00e−qs f(X s)ds)n(1−e0),(6)From equation(5)we have that the measure n should be such thatn( T00e−qs f(X s)ds) n(1−e0)=c1/αn( T00e−qc1/αs H c f(X s)ds)n(1−e−qc1/αT0),and therefore we conclude thatn( T00e−qs f(X s)ds)=c(1−γ)/αn( T00e−(qc1/αs)H c f(X s)ds).(ii)⇒(i).The scaling property of X is obtained by means of(5).In fact,the only thing that should be verified is that equation(5)holds for x=0,since we have the identity U q f(x)=V q f(x)+E x(e−qT0)U q f(0),x>0,and the scaling property of the minimal process stated in terms of its resolvent V q,i.e.V q f(x)=c1/αV qc1/αH c f(x/c),x>0,c>0,q>0.Indeed,by construction it follows that the formula(6)holds and the hypothesis(ii)implies that n(1−e−qT0)=qγ,q>0;the conclusion is immediate.In the following proposition we give a description of the sojourn measure of X and a necessary condition for the existence of a excursion measure n such that one of the conditions in the Lemma2holds.Lemma3.Let n be a normalized excursion measure and X the associated extension of the minimal process(X,T0).Assume that one of the conditions(i–iii)in Lemma2holds. Thenn( T001{X s∈dy}ds)=Cα,γy(1−α−γ)/αdy,y>0,withγdetermined in(ii)of Lemma2and Cα,γ∈]0,∞[a constant.As a consequence, E(I−(1−γ))<∞and Cα,γ=(αE(I−(1−γ))Γ(1−γ))−1,where I denote the exponential functional(2).2.2Some properties of excursion measures for self–similar Markov process9Proof.Recall that the sojourn measuren( T001X s∈dy ds)= ∞0n s(dy)ds,is aσ–finite measure on]0,∞[and is the unique excessive measure for the semigroup of the process X,see e.g.Dellacherie et al.[12]XIX.46.Next,using the result(iii)inLemma2and the Fubini’s Theorem we obtain the following representation of the sojournmeasure,for f≥0measurable∞0n s fds= ∞0s−γn1(H sαf)ds= n1(dz) ∞0s−γf(sαz)ds=Cα,γ ∞0u(1−α−γ)/αf(u)du,with0<Cα,γ=α−1 n1(dz)z−(1−γ)/α<∞.This proves thefirst part of the claimedresult.We now prove that E(I−(1−γ))<∞.On the one hand,the functionϕ(x)=E x(e−T0)is integrable with respect to the sojourn measure.To see this,use the Markovproperty under n,to obtainn( T00ϕ(X s)ds)= ∞0n(ϕ(X s),s<T0)ds= ∞0n(e−T0◦θs,s<T0)ds= ∞0n(e−(T0−s),s<T0)ds=n(1−e−T0)=1.On the other hand,using the representation of the sojourn measure,Fubini’s Theoremand the scaling property we have thatCα,γ ∞0E y(e−T0)y(1−α−γ)/αdy=Cα,γ ∞0E(e−y1/αI)y(1−α−γ)/αdy=Cα,γαE(I−(1−γ))Γ(1−γ).Therefore,E(I−(1−γ))<∞and Cα,γ=(αE(I−(1−γ))Γ(1−γ))−1.We next study the extensions X that leave0a.s.by ing only the scaling property(1)it can be verified that the only possible jumping–in measures such that theassociated excursion measure satisfies(ii)in Lemma2should be of the typeη(dx)=bα,βx−(1+β)dx,x>0,0<αβ<1,with a constant bα,β>0,depending onαandβ,cf.[34].This being said we can state anelementary but satisfactory result on the existence of extensions of the minimal processthat leaves0by jumps a.s.102PRELIMINARIES AND FIRST RESULTSProposition 1.Let β∈]0,1/α[.The following are equivalent(i)E (I αβ)<∞,(ii)The pseudo excursion measure n j =P η,based on the jumping–in measure η(dx )=x −(1+β)dx,x >0,is an excursion measure,(iii)the minimal process (X,T 0)admits an extension X,that is a self–similar recurrent Markov process and leaves 0by jumps a.s.according to the jumping–in measureη(dx )=b α,βx −(1+β)dx,with b α,β=β/E (I αβ)Γ(1−αβ).If one of these conditions holds then γin (ii)in Lemma 2is equal to αβ.The condition (i)in Proposition 1is easily verified under weak technical assumptions.Namely,if we assume the hypothesis (H2)the aforementioned condition is verified for every β∈]0,(1/α)∧θ[;this will we deduced from Lemma 4below.On the other hand,that condition is verified in other settings as can be viewed in the following example.Example 1(Generalized self–similar saw tooth processes).Let α>0,ζa sub-ordinator such that E (ζ1)<∞,and X the α–self–similar process associated to the L´e vy process ξ=−ζ.Then ξdrifts to −∞,X has a finite lifetime T 0and X decreases from its starting point until the time T 0,when it is absorbed at 0.Furthermore,it was proved by Carmona et al.[10]that the L´e vy exponential functional I = ∞0exp {−ζs /α}ds,has finite integral moments of all orders.It follows that the condition (i)in Proposition 1is satisfied by every β∈]0,1/α[.Thus for each β∈]0,1/α[the α–self–similar extension X that leaves 0by jumps according to the jumping–in measure in (iii)of Proposition 1,is a process having sample paths that looks like a saw with “rough”tooths.These are all the possible extensions of X,that is,it is impossible to construct an excursion measure such that its associated extension of (X,T 0)leaves 0continuously a.s.since we know that the process X decreases to 0.Proof of Proposition 1.Let η(dx )=x −(1+β)dx,x >0and n j be the pseudo excursion measure n j =P η.By definition the entrance law associated to n j is n j s f =∞0dx x −(1+β)P s f (x ),s >0.Thus the only thing that should be verified by n j to be an excursion measure is that n j (1−e −T 0)<∞.This follows from the elementary calculation ∞0dx x −(1+β)E x (1−e −T 0)= ∞0dx x −(1+β)E (1−e −x 1/αI )=αEdy y −αβ−1(1−e −yI ) =E (I αβ)Γ(1−αβ)β.That is,n j (1−e −T 0)<∞if and only if E (I αβ)<∞,which proves the equivalence between the assertions in (i)and (ii).If (ii)holds it follows from the results in [7]and the Lemma 2that associated to the normalized excursion measure n j =b α,βP ηthere exists a unique extension of the minimal process (X,T 0)that is a self–similar Markov process and that leaves 0by jumps according to the jumping–in measure b α,βx −(1+β)dx,x >0,whichestablish (iii).Conversely,if (iii)holds the Itˆo ’s excursion measure of X,is n j =b α,βP ηand the statement in (ii)follows.2.3The process X analogue to the Bessel(3)process112.3The process X analogue to the Bessel(3)processHere we shall establish the existence of a self–similar Markov process X that can beviewed as the self–similar Markov process(X,T0)conditioned to never hit0.In the case(X,T0)is a Brownian motion killed at0,X corresponds to the Bessel(3)process.Tothat end,we next recall some facts on L´e vy processes and density transformations anddeduce some consequence for self–similar Markov processes.We assume henceforth(H2).The law of a L´e vy processξ,is characterized by a functionΨ:R→C,defined by the relationE(e iuξ1)=exp{−Ψ(u)},u∈R.The functionΨis called the characteristic exponent of the L´e vy processξand can beexpressed thank to the L´e vy–Khintchine’s formula asΨ(u)=iau+σ2u22+ R(1−e iux+iux1{|x|<1})Π(dx),whereΠis a measure on R\{0}such that (|x|2∧1)Π(dx)<∞.The measureΠis called the L´e vy measure,a the drift andσ2the Gaussian coefficient ofξ.Conditions(H2-b,c) imply that the L´e vy exponent ofξadmits an analytic extension to the complex strip I(z)∈[−θ,0].Thus we can define a functionψ:[0,θ]→R byE(eλξ1)=eψ(λ)andψ(λ)=−Ψ(−iλ),0≤λ≤θ.Holder’s inequality implies thatψis a convex function and thatθis the unique solution to the equationψ(λ)=0forλ>0.Furthermore,the function h(x)=eθx is invariant for the semigroup ofξ.Let P be the h–transform of P via the invariant function h(x)=eθx.That is,the measure P is the unique measure on(D,D)such that for everyfinite D t-stopping time T and each A∈D TP (A)=P(eθξT A).Under P the process(ξt,t≥0)still is a L´e vy process,with characteristic exponentΨ (u)=Ψ(u−iθ),u∈R,and drifts to∞,more precisely,0<m :=E (ξ1)=ψ (θ−)<∞.See e.g.Sato[32]§33,for a proof of these facts and more about this change of measure.Let P x denote the law on D+of the self–similar Markov process started at x>0 associated to the L´e vy processξ via Lamperti’s transformation.In the sequel it will be implicit that the superscript refers to the measures P or P .We now establish a relation between the probability measures P and P analogue to that between the law of a Brownian motion killed at0and the law of a Bessel(3)process,see e.g.McKean[23]. Informally,the law P x can be interpreted as the law under P x of X conditioned to never hit0.Proposition2.(i)Let x>0arbitrary,we have that P x is the unique measure such that for every T stopping time in G t we haveP x(A)=x−θP x(A XθT,T<T0),for any A∈G T.In particular,the function h∗:[0,∞[→[0,∞[defined by h∗(x)=xθis invariant for the semigroup P t.122PRELIMINARIES AND FIRST RESULTS(ii)For every x>0and t>0we haveP x(A)=lims→∞P x(A|T0>s),for any A∈G t.The proof of(i)in Proposition2is a straightforward consequence of the fact that P is the h–transform of P and that for every T stopping time in G t we have thatτ(T)isan stopping time in F t.To prove(ii)in Proposition2we need the following lemma thatprovides us a tail estimation for the law of the L´e vy exponential functional I associatedtoξas defined in(2).Lemma4.Under the conditions(H2)we have thatlimt→∞tαθP(I>t)=C,where0<C=αm tαθ−1(P(I>t)−P(eξ 1I>t))dt<∞,withξ 1=dξ1and independent of I.If0<αθ<1,thenC=αmE(I−(1−αθ)).Two proofs of this result have been given in a slight restrictive setting by Mejane[24]. However,one of its proofs can be extended to our case and in fact it is an easy consequence of a result on random equations originally due to Kesten[21]who in turn uses a difficult result on random matrices.A simpler proof of Kesten’s result was given in Goldie[19]. Sketch of proof of Lemma4.It is straightforward that the L´e vy exponential functional I satisfies the equation in lawI=d 10eξs/αds+eξ1/αI =Q+MI ,with I the L´e vy exponential functional associated toξ ={ξ t=ξ1+t−ξ1,t≥0},a L´e vy process independent of F1and with the same distribution asξ.Thus,according to[21] if the conditions(i–iv)below are satisfied then there exists a strictly positive constant C such thatlimt→∞tαθP(I>t)=C.The hypotheses of Kesten’s Theorem are(i)M is not arithmetic(ii)E(Mαθ)=1,(iii)E(Mαθln+(M))<∞,(iv)E(Qαθ)<∞.。

我准备好去写作业的英语

Im ready to start my homework in English.Heres a detailed plan for the tasks I need to complete:1.Reading Comprehension:I will begin by reading the assigned English literature or textbook chapter.Ill make sure to understand the main ideas,themes,and any new vocabulary introduced.2.Vocabulary List:After reading,Ill compile a list of new words and phrases Ive encountered.Ill define them,note their usage in sentences,and try to use them in my own sentences to reinforce my understanding.3.Grammar Practice:Ill review the grammar points covered in class or in the textbook, focusing on any areas where I feel less confident.Ill complete any grammar exercises provided to practice these rules.4.Writing Assignment:If theres a writing task,Ill brainstorm ideas,create an outline,and then draft my essay or story.Ill pay attention to the structure,coherence,and use of appropriate language.5.Editing and Proofreading:Once Ive written my first draft,Ill take a break and then return to it with fresh eyes.Ill check for grammatical errors,spelling mistakes,and ensure that the writing flows well.6.Peer Review:If possible,Ill ask a classmate or friend to review my work and provide feedback.This can help me catch any errors I might have missed and gain new perspectives on my writing.7.Final Revisions:Based on the feedback,Ill make the necessary revisions to polish my work.8.Submission:Finally,Ill ensure that my assignment is formatted correctly according to the teachers guidelines and submit it on time.9.SelfReflection:After submitting,Ill reflect on what I learned from the assignment and identify areas for improvement for future tasks.By following this plan,I aim to complete my English homework effectively and enhance my language skills.。

flink 中 similar用法

flink 中 similar用法Flink 中 Similar 的用法1. 概述在 Flink 中,similar 是一个用于查找相似项的函数。

它可以帮助我们在大规模数据集中快速找到与给定项相似的其他项。

这对于推荐系统、搜索引擎等具有相似性需求的场景非常有用。

2. 安装在使用 similar 函数之前,需要确保已经安装了 Flink。

你可以按照官方文档提供的步骤进行安装。

3. 基本语法similar 函数通常使用 SQL 或 DataStream API 调用。

下面是其基本语法:SELECT item_id, similar(item_id, threshold) FROM ta ble_name•item_id: 需要查找相似项的项的ID•threshold: 相似度的阈值,只返回相似度大于等于阈值的项4. 示例一:基于 SQL 的调用方式假设我们有一个用户电影评分的数据集,包含用户ID、电影ID 和评分。

我们想找出与给定电影ID相似度大于等于的其他电影。

SELECT item_id, similar(item_id, ) FROM ratings WHE RE item_id = 'movie_123'执行以上 SQL 查询后,将返回与电影ID为“movie_123” 相似度大于等于的其他电影。

5. 示例二:基于 DataStream API 的调用方式如果我们使用 DataStream API,代码如下所示:// 创建 ExecutionEnvironment 或 StreamExecutionEnvir onmentStreamExecutionEnvironment env = ();// 创建 DataStream,读取评分数据流DataStream<Tuple3<String, String, Double>> ratings = ("l ocalhost", 9999).map(new RatingParser());// 定义 similar 函数SimilarFunction similarFunction = new SimilarFunction(); // 调用 similar 函数,并打印结果DataStream<Tuple2<String, Double>> similarItems = rating s.keyBy(tuple -> ) // 根据电影ID进行分组.flatMap(new SimilarItemsFlatMap(similarFunction)); ();// 执行任务("Find Similar Items");在以上代码中,我们首先创建一个 DataStream 读取评分数据流。

自注意力机制的计算,例题

自注意力机制的计算,例题自注意力机制是一种用于文本、图像等序列数据的注意力机制。

它可以捕捉序列中任意两个元素之间的关系,从而更好地理解序列的语义。

自注意力机制的计算步骤如下:1.首先,将序列中的每个元素表示为一个向量。

2.然后,计算每个元素与其他元素之间的注意力权重。

3.最后,根据注意力权重对每个元素进行加权求和,得到序列的新表示。

例题假设我们有一个序列"I love you",其中每个单词表示为一个向量。

✧import torch✧x=torch.tensor([✧[1,2,3],✧[4,5,6],✧[7,8,9],])首先,我们计算每个元素与其他元素之间的注意力权重。

✧计算查询向量✧q=x✧计算键向量✧k=x✧计算值向量✧v=x✧计算注意力权重✧attention=torch.matmul(q,k.t())/torch.sqrt(x.size(-1))✧使用softmax函数归一化注意力权重✧attention=torch.softmax(attention,dim=-1)得到的注意力权重如下:✧tensor([[0.375,0.25,0.375],✧[0.25,0.5,0.25],✧[0.375,0.25,0.375]])最后,根据注意力权重对每个元素进行加权求和,得到序列的新表示。

✧计算加权求和✧output=attention.matmul(v)✧输出结果✧print(output)得到的输出结果如下:✧tensor([5.25,6.75,5.25])可以看到,输出结果中,第一个元素的值最高,这表明"I"与其他两个元素的关系最为紧密。

IBM Cognos Transformer V11.0 用户指南说明书

风格相似度计算

风格相似度计算是一种用于衡量两个事物之间风格相似程度的方法。

在自然语言处理

领域,风格相似度计算经常应用于文本比较、风格迁移和风格分类等任务中。

下面介绍几种常见的风格相似度计算方法:

1. 文本特征提取:通过提取文本的特征向量,可以表示文本的风格特征。

常见的特征

包括词频、TF-IDF、词向量(如Word2Vec、GloVe)、句法结构、情感倾向等。

然后,根据两个文本的特征向量进行相似度计算,如余弦相似度、欧氏距离、曼哈顿距离等。

2. 风格迁移模型:风格迁移模型可以将一个文本的风格转换为另一个文本的风格。

通

过比较迁移后的文本与原始文本的相似性,可以得到风格相似度。

常见的风格迁移模

型包括CycleGAN、StarGAN等。

3. 语言模型:通过训练语言模型,可以获得文本的语言规律和风格特点。

通过比较两

个文本的生成概率或条件概率,可以计算它们之间的风格相似度。

常见的语言模型包

括n-gram模型、RNN(循环神经网络)和Transformer模型。

4. 相似度度量方法:除了上述方法外,还有一些专门用于测量文本相似度的方法,如

编辑距离、Jaccard相似度等。

这些方法通过比较文本之间的相同元素或操作次数来计

算相似度。

需要注意的是,风格相似度计算是一个复杂的问题,不同的任务和领域可能适用不同

的方法。

此外,风格的定义和理解也是主观的,因此在进行风格相似度计算时,需要

根据具体情况选择合适的方法,并结合实际应用需求进行调整和评估。

贝叶斯超参数优化 多层感知器

贝叶斯超参数优化是一种用于自动调整机器学习模型超参数的优化技术。

它使用贝叶斯概率理论来估计超参数的最佳值,以优化模型的性能。

多层感知器(MLP)是一种常用的神经网络模型,由多个隐藏层组成,每个层包含多个神经元。

MLP可以用于分类、回归等多种任务。

当使用贝叶斯超参数优化来调整MLP的超参数时,通常会选择一些常见的超参数,如学习率、批量大小、迭代次数等。

贝叶斯优化器会根据这些超参数的性能,选择下一个可能的最佳值。

它通过在每个步骤中随机选择少量的超参数组合,而不是搜索每个可能的组合,来提高效率。

在实践中,贝叶斯超参数优化通常使用一种称为高斯过程回归(Gaussian Process Regression)的方法,该方法可以估计每个超参数的可能值以及它们的概率分布。

然后,根据这些信息选择下一个超参数的值,以最大化模型性能的预期改善。

使用贝叶斯超参数优化可以自动调整超参数,避免了手动调整的困难和耗时。

此外,它还可以帮助找到更好的超参数组合,从而提高模型的性能和准确性。

这对于机器学习任务的实验和开发非常重要,因为它可以帮助快速找到最佳的模型配置。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

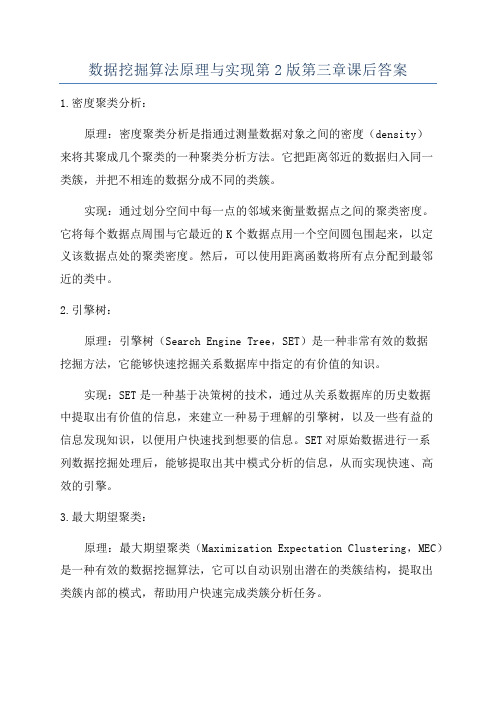

Selfsimilar Additive Processes and Financial ModelingCraig A.NolderDepartment of MathematicsFlorida State UniversityTallahassee,FL32306-4510,USAnolder@ABSTRACT.We present here theoretical reasons to use selfsimilar additive processes to model asset prices and a program for calibrations and implementations.L´e vy processes are stationary additive processes and are selfsimilar only in the stable case.In contrast any selfdecomposable distribution will generate selfsimilar additive processes with any positive exponent of selfsimilarity.Selfsimilar additive processes due to nonstationarity need not adhere to a Central Limit Theorem.It is hoped that because of this these models will exhibit implied volitility smirks at high maturities.KEY WORDS:selfsimilar additive processes,option pricing1IntroductionFinancial time series often exhibit selfsimilar scaling properties[11],[2],[5].As such this is a desirable feature of a mathematical model of these phenomena.Indeed the Brownian motion process in the Black-Scholes model is2-stable and hence12-selfsimilar.Mandelbrot proposed the use of more general stableprocesses infinance[11].Except in the Gaussian case however,these processes have infinite variance. As a result a stock price process modeled as an exponential stable process may not possess an equivalent martingale measure and option prices can be infinite.However P.Carr and L.Wu[6]have shown that in the extreme case of maximum negative skewness these stable exponential L´e vy processes result infinite valued price processes.At the same time the stock process retains infinite variance.As such even though the increments are independent and stationary,the conditions for a central limit are violated.Moreover the scaled distributions are similar over all time horizons due to the selfsimilarity of the processes.The combination of these properties allow a calibratedfit to a volatility smirk of S and P index data in[6]over a two year maturity span.Recently other distributions have been proposed as the basis of exponential L´e vy stock price models.Notably are the normal inverse Gaussian[3],truncated stable[5]and the generalized hyperbolic[7].Many authors have proposed the use of the L´e vy processes that these distributions generate. However,except in the stable case,these processes do not have selfsimilar scaling properties.Moreover these processes havefinite moments and,as a result of the central limit theorem,will not produce the volatility smirk which will insteadflatten with increasing maturity.On the other hand all of the above distributions are in fact selfdecomposable.Because of this one can construct selfsimilar additive processes with any exponent H>0.As such the distributions of these additive processes agree with those of the corresponding L´e vy processes at time1,but have different time evolutions.We investigate here these additive processes as models for asset pricing.Although the increments are no longer stationary,we still have spatially homogeneous Markov processes.Because ofthis the option pricing formulas are similar to the L´e vy case.As such selfsimilar additive processes offer great promise as versatile modeling tools infinance:1.Any selfdecomposable distribution defines selfsimilar processes.2.There is an entire family of these processes for each initial distribution,one for each selfsimilarexponent H>0.3.Except in the stable(when the variance is infinite)the increments are nonstationary and a normalcentral limit theorem need not apply.4.The selfsimilar property will allow fat negative tails to persist over all time horizons.A calibratedmodel shouldfit volatility smirks of implied volatilities over a wide range of maturities.We remark that many authors justify stationarity by claiming it in fact defines the temporal index. Moreover time deformations of market activity are required to attain stationarity(e.g.,[4]).Selfsimilar processes may be another way to accommodate nonstationarity.Although the distributions of time incre-ments are not the same they are related through(1)and(5).Moreover additive processes of different types can be pasted together using(3).2Additive ProcessesDefinition2.1.A real valued stochastic process{X t|t≥0}on a probability space(Ω,F,P)is an additive process if(i)for allfinite partitions0≤t0<t1...<t k,the increments X tk −X tk−1,...,X tare independent.(ii)X0=0a.s.(iii){X t}is stochastically continuous(iv)the sample paths have c`a dl`a g modifications a.s.As such an additive process with stationary increments is a L´e vy process.Given an additive process{X t}we writeµs,t for the distribution of X t−X s,0≤s≤t<∞.It follows thatµs,t is infinitely divisible andµs,t⋆µt,u=µs,u(1) for0≤s≤t≤u<∞,µs,s=δ0,0≤δ<∞,µs,t→δ0as s↑t,µs,t→δ0as t↓s.Moreover,conversely,given a system of probability measures satisfying(1)it follows from Kolmogorov’s Existence Theorem that an additive process exists with these distributions.Since the distributionµ0,t=µt=P X t is infinitely divisible for each t≥0,its characteristic exponent has characteristics(a t,νt,γt),log E(e izX t)=−a t2z2+izγt(2)+ R e izx−1−izxI[−1,1] νt(dx).The system of triplets satisfies the conditions(i)a0=0,ν0=0,γ0=0,(ii)if0≤s≤t<∞,then a s≤a tandνs(B)→νt(B)for Borel sets B,(iii)as s→t in[0,∞),a s→a t,νs(B)→νt(B)for B⊂ x |x|>ε ,ε>0andγs→γt.See[9].Conversely,given a system of infinitely divisible distributions that satisfy the conditions(3),thenthere exists an additive process such that P Xt=µt,t≥0.In this case the infinitely divisible distributionµs,t has generating triple(a t−a s,νt−νs,γt−γs).Also if{X t}is an additive process,thenP s.t(x,B)=P(X t−X s∈B−x),0≤s≤t,is a spatially homogeneous transition function and{X t}is a Markov process with this transition function and starting at zero.3Asset Process and Option PricingWe write{S t}for an asset price process that we model using an additive process{X t}:dS t=S t(r dt+σdX t).(3) here r is a riskless interest rate.The volitility parameterσcan be used both to calculate implied volitilities from market data and as a second source of randomness in(3).Under usual assumptions of an absence of arbitrage there exists an equivalent martingale measure under which the discounted stock process is a (sigma)-martingale.Let P be the market measure and Q the equivalent martingale measure.Given a European option with payoff g(S T)at expiry T,we write the fair option price at time t, 0≤t≤T,V t=e−r(T−t)E Q(g(S T)|F t).(4) 4Selfsimilar Processes and Selfdecomposable DistributionsSeveral important distributions that have recently been used infinancial modelling are selfdecompos-able.Among these are stable,truncated stable,normal inverse Gaussian and generalized hyperbolic dis-tributions.The L´e vy processes that these distributions determine appear as asset price processes in theliterature.We examine here an infinite class of additive processes canonically determined by a selfdecom-posable distribution,one for each exponent H>0.Only in the stable case with H≥12do these processesagree in law with the canonical L´e vy processes.Definition4.1.A probability measureµon R is selfdecomposable if,for any b>1,there is a probability measureρb on R such thatµ(z)= µ z b ρb(z).(5) Definition4.2.A stochastic process{X t|t≥0}on R is H-sellfsimilar,H>0,if for any a>0{X at|t≥0}d={a H X t|t≥0}.A(non-trivial)selfdecomposable distribution determines an H-selfsimilar additive process.In factlet H>0,0<s<t,and b=(ts )H in(5).Then defineµt andµs,t by µt(z)= µ(t H z)and µs,t(z)=ρ(t s)H(t H z)so that µt(z)= µs(z) µs,t(z).Withµ0=δ0,µ0,t=µt andµt,t=δ0,the corresponding measures determined above satisfy(1)and so determine an additive process{X t}.Notice it follows that for any a>0,X at d=a H X t and so{X t}is an H-selfsimilar process.For details see p.100[9].5Work in ProgressThe following programs are underway.1.Analyze market data for evidence of selfsimilarities.Obtain estimates for the exponent(s)of self-similarity.Some techiques are in[8].2.Calculate densities for selfsimilar processes whose distributions at time1are models of observeddistributions of market data.These include the normal inverse Gaussian,Generalized hyperbolic, Truncated stable and stable distributions.We remark that“stable”processes are L´e vy processes only when the exponent of selfsimilarity is larger than or equal to1.23.Calibrate the parameters in the model(volitility,selfsimilar exponent and the parameters of theinitial distributions)with market data.Calculate theoretical market prices using the model.4.Recalculate implied volitilities using market data and calibrated models.5.Calibrate a stochastic volitility model to add volitility clustering.Thefigures1–4compare a Gaussian process with a Levy process and three additive selfsimilar processes at four different times.The designations of these processes appear in the keys in this order. The graphs are at times1,1.5,3and6.The variance of the Gaussian at time1matches that of the other processes whose distributions are indentical at time1and all means are zero.The time is thefirst parameter in the key.The initial distributions of the nonGaussian processes are a truncated stable distribution with characteristic function proportional to50ln25−(25−ix)ln(25−ix)−(25+ix)ln(25+ix)as a function of x.The second parameter in the key is the exponent H in the selfsimilar processes and the third is a label: 0Gaussian,1Levy,2additive selfsimilar.We acknowledge Mack Galloway for his help in developing the software.Results of the above investigations will be published elsewhere.References[1]Boyarchenko,S.I.and Levendorskii,S.Z.,Non-Gaussian Merton-Black-Scholes Theory,World Sci-entific,2002.[2]Barndorff-Nielsen,O.E.and Prause,K.,Apparent scaling,Finance and Stochastics,5,2001,103–113.[3]Barndorff-Nielsen,O.E.and Shephard,N.,Modelling by L´e vy processes forfinancial econometrics,L´e vy Processes Theory and Applications,Birkhauser Boston,2001.[4]Cont,R.,Empirical properties of asset returns:stylized facts and statistical issues,Quantitative Fi-nance,1,2001,223–236.[5]Carr,Peter,P.,Geman,H.,Madan,D.B.and Yor,M.,Thefine structure of asset returns:An empiricalinvestigation,Journal of Business,75,2002,305–332.[6]Carr,P.and Wu,L.,Thefinite moment log stable process and option pricing,The Journal of Finance,28(2),2003,753–777.[7]Eberlein,E.,Application of generalized hyperbolic L´e vy motions tofinance,L´e vy Processes Theoryand Applications,Birkhauser Boston,2001.[8]Embrechts,P.and Maejima,M.Selfsimilar Processes,Princeton University Press,Princeton,N.J.,2992.[9]Sato,K.,L´e vy Processes and Infinitely Divisible Distributions,Cambridge University Press,1999.[10]Jacod,J.and Shiryaev,A.N.,Limit Theorems for Stochastic Processes,Springer-Verlag,1987.[11]Mandelbrot,Benoit B.,The variation of certain speculative prices,Journal of Business,36,1963,394–419.[12]Maejima,M.and Naito,Y.,Semi-selfdecomposable distributions and a new class of limit theorems,Prob.Theory and Rel.Fields,112(1),1998,13–21.[13]Maejima,M.,Sato,K.and Watanabe,T.,Remarks on semi-selfsimilar processes,preprint.。