Financing Current Assets(英文版)(ppt 32页)

FinancingCurrentAssets(英文版)

Firms have little control over the level of accruals. Levels are influenced more by industry custom, economic factors, and tax laws.

Copyright © 2001 by Harcourt, Inc.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

17 - 17

Why must we use EAR to evaluate the alternative loans?

Nominal (quoted) rate = 8% in all cases.

Advantages of short-term credit:

Low cost--visualize yield curve. Can get funds relatively quickly. Can repay without penalty.

Copyright © 2001 by Harcourt, Inc.

$

Temp. C.A.

} S-T Loans

Perm C.A. Fixed Assets

L-T Fin: Stock, Bonds, Spon. C.L.

Years

Lower dashed line, more aggressive.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

17 - 13

Nominal Cost Formula, 1/10, net 40

k Nom

资产负债表英文课件

Deferred Tax LiabilityAmounts that report the future tax sequences of events that have occurred in prior years but have not yet been taxed

02

Asset category

Current assets

Cash and cash equivalents - Sum of cash, coins, and checks that are immediately available

Inventory - Stock of raw materials, work in progress, and finished goods

Components

Equity companies paid in capital, retained earnings, and other comprehensive income

Importance

Equity provides a measure of the financial well being of a company and serves as a basis for evaluating its performance and making investment decisions

03

Copyright - Protects original works of authorship

04

Technology licenses - Give the company the right to use someone else's technology or intellectual property

英文版中级财务会计第3章PPT

Periodic Inventory System

Beginning inventory + Purchases (net)-Ending Inventory = cost of goods sold

example

Periodic System

Apr. 1 Apr. 10 Apr. 20

100 units 80 units 70 units 250 units

Balance Sheet ($ in millions) 2009 2008 Current assets: Inventories Finished goods $ 660 $ 775 Work in process 38 43 Materials and supplies 330 402 Total $1,028 $1,220

Alternative inventory systems

A company using a perpetual system maintains a continuous record of the physical quantities in its inventory.

Comparison of system

Classification of inventory in different types of company

Merchandising company Merchandise inventory

Manufacturing company Raw materials inventory Work in process Finished goods inventory

2011 Inventory Accounts payable

金融市场学英文版ppt

1

Chapter 1

The Financial System

Copyright 2003 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Accounting by Willis Slides prepared by Kaye Watson

2

Learning Objectives

financial markets • Categorise the main types of financial institutions • Understand the impact of a financial crisis on a financial system and a real economy

Copyright 2003 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Accounting by Willis Slides prepared by Kaye Watson

13

1.2 Functions of the Financial System (cont.)

• An efficient financial system – Encourages savings – Savings flow to the most efficient users – Implements the monetary policy of governments by influencing interest rates – The combination of assets and liabilities comprising the desired attributes of return, risk, liquidity and timing of cash flows

chapter 12 financing current assets

The cost of trade credit

某企业按照“2/10,N/30”的条件购买一批 商品,价值100 000元。如果企业在10天付 款,则可获得最长为10天的免费信用,并 可取得折扣2000元(100000×2%),免费 信用额为98000元(1000000-2000)。

如果企业放弃这笔折扣,在第30天付款, 付款总额为100 000元,其中包括:供应商 提供的10天免费信用而应支付的款项98000 元;供应商提供的20天有代价信用而应支 付的利息2000元。

Chapter 12

Financing current Assets

LEARNING OBJECTIVES

区分三种流动资产管理策略 简要说明流动负债融资的优点和缺点 列举出四类主要的短期融资类别 区分商业信用的免费信用和有代价信用,学会计

算不利用现金折扣时的成本,能够说明展期信用 为什么会降低商业信用的成本,以及不利之处 学会计算应付票据贴现利息和贴现额 学会计算各种短期银行贷款条件下的实际利率 解释什么是担保贷款,以及哪些种类的担保品可 用来作为短期银行贷款的担保

(1)应付账款

应付账款按其是否支付代价,分为:

免费信用(free trade credit)指买方在规定的 折扣期限内享受折扣而获得的信用

有代价信用(costly trade credit)指买方企业 放弃折扣而获得的信用

展期信用(stretching accounts payable)指买 方企业在规定的信用期限届满后推迟付款而强 制获得的信用

Years Lower dashed line would be more aggressive.

Moderate financing policy

财务报表英文版

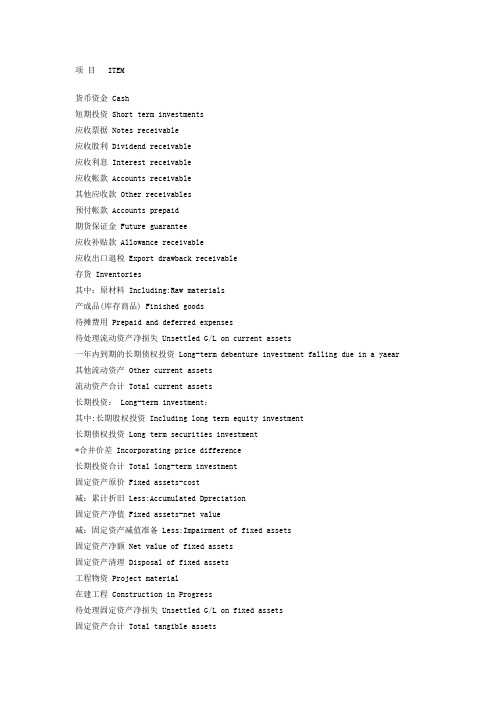

项目 ITEM货币资金Cash短期投资Short term investments应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收帐款Accounts receivable其他应收款 Other receivables预付帐款 Accounts prepaid期货保证金 Future guarantee应收补贴款 Allowance receivable应收出口退税 Export drawback receivable存货Inventories其中:原材料 Including:Raw materials产成品(库存商品) Finished goods待摊费用Prepaid and deferred expenses待处理流动资产净损失Unsettled G/L on current assets一年内到期的长期债权投资 Long-term debenture investment falling due in a yaear 其他流动资产Other current assets流动资产合计Total current assets长期投资: Long-term investment:其中:长期股权投资 Including long term equity investment长期债权投资 Long term securities investment*合并价差 Incorporating price difference长期投资合计Total long-term investment固定资产原价 Fixed assets-cost减:累计折旧 Less:Accumulated Dpreciation固定资产净值 Fixed assets-net value减:固定资产减值准备Less:Impairment of fixed assets固定资产净额Net value of fixed assets固定资产清理Disposal of fixed assets工程物资Project material在建工程Construction in Progress待处理固定资产净损失Unsettled G/L on fixed assets固定资产合计 Total tangible assets无形资产Intangible assets其中:土地使用权Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理Including:Fixed assets repair固定资产改良支出 Improvement expenditure of fixed assets其他长期资产 Other long term assets其中:特准储备物资Among it:Specially approved reserving materials 无形及其他资产合计Total intangible assets and other assets递延税款借项 Deferred assets debits资产总计Total Assets资产负债表(续表) Balance Sheet项目 ITEM短期借款Short-term loans应付票款Notes payable应付帐款Accounts payab1e预收帐款Advances from customers应付工资Accrued payro1l应付福利费 Welfare payable应付利润(股利) Profits payab1e应交税金Taxes payable其他应交款 Other payable to government其他应付款 Other creditors预提费用Provision for expenses预计负债Accrued liabilities一年内到期的长期负债Long term liabilities due within one year其他流动负债Other current liabilities流动负债合计 Total current liabilities长期借款Long-term loans payable应付债券Bonds payable长期应付款 long-term accounts payable专项应付款 Special accounts payable其他长期负债Other long-term liabilities其中:特准储备资金 Including:Special reserve fund长期负债合计Total long term liabilities递延税款贷项Deferred taxation credit负债合计Total liabilities* 少数股东权益Minority interests实收资本(股本) Subscribed Capital国家资本National capital集体资本Collective capital法人资本Legal person"s capital其中:国有法人资本Including:State-owned legal person"s capital集体法人资本Collective legal person"s capital个人资本Personal capital外商资本Foreign businessmen"s capital资本公积Capital surplus盈余公积surplus reserve其中:法定盈余公积Including:statutory surplus reserve公益金 public welfare fund补充流动资本Supplermentary current capital* 未确认的投资损失(以“-”号填列) Unaffirmed investment loss未分配利润 Retained earnings外币报表折算差额 Converted difference in Foreign Currency Statements 所有者权益合计 Total shareholder"s equity负债及所有者权益总计Total Liabilities & Equity利润表 INCOME STATEMENT项目 ITEMS产品销售收入Sales of products其中:出口产品销售收入 Including:Export sales减:销售折扣与折让 Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本 Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利 Gross profit on sales减:销售费用 Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益) Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额 Total profit减:所得税 Less:Income tax净利润 Net profit现金流量表Cash Flows StatementPrepared by: Period: Unit:Items1.Cash Flows from Operating Activities:01)Cash received from sales of goods or rendering of services02)Rental receivedValue added tax on sales received and refunds of value03)added tax paid04)Refund of other taxes and levy other than value added tax07)Other cash received relating to operating activities08)Sub-total of cash inflows09)Cash paid for goods and services10)Cash paid for operating leases11)Cash paid to and on behalf of employees12)Value added tax on purchases paid13)Income tax paid14)Taxes paid other than value added tax and income tax17)Other cash paid relating to operating activities18)Sub-total of cash outflows19)Net cash flows from operating activities2.Cash Flows from Investing Activities:20)Cash received from return of investments21)Cash received from distribution of dividends or profits22)Cash received from bond interest incomeNet cash received from disposal of fixed assets,intangible23)assets and other long-term assets26)Other cash received relating to investing activities27)Sub-total of cash inflowsCash paid to acquire fixed assets,intangible assets28)and other long-term assets29)Cash paid to acquire equity investments30)Cash paid to acquire debt investments33)Other cash paid relating to investing activities34)Sub-total of cash outflows35)Net cash flows from investing activities3.Cash Flows from Financing Activities:36)Proceeds from issuing shares37)Proceeds from issuing bonds38)Proceeds from borrowings41)Other proceeds relating to financing activities42)Sub-total of cash inflows43)Cash repayments of amounts borrowed44)Cash payments of expenses on any financing activities45)Cash payments for distribution of dividends or profits46)Cash payments of interest expenses47)Cash payments for finance leases48)Cash payments for reduction of registered capital51)Other cash payments relating to financing activities52)Sub-total of cash outflows53)Net cash flows from financing activities4.Effect of Foreign Exchange Rate Changes on Cash Increase in Cash and Cash EquivalentsSupplemental Information1.Investing and Financing Activities that do not Involve inCash Receipts and Payments56)Repayment of debts by the transfer of fixed assets57)Repayment of debts by the transfer of investments58)Investments in the form of fixed assets59)Repayments of debts by the transfer of investories2.Reconciliation of Net Profit to Cash Flows from Operating Activities62)Net profit63)Add provision for bad debt or bad debt written off64)Depreciation of fixed assets65)Amortization of intangible assetsLosses on disposal of fixed assets,intangible assets66)and other long-term assets (or deduct:gains)67)Losses on scrapping of fixed assets68)Financial expenses69)Losses arising from investments (or deduct:gains)70)Defered tax credit (or deduct:debit)71)Decrease in inventories (or deduct:increase)72)Decrease in operating receivables (or deduct:increase)73)Increase in operating payables (or deduct:decrease)74)Net payment on value added tax (or deduct:net receipts75)Net cash flows from operating activities Increase in Cash and Cash Equivalents76)cash at the end of the period77)Less:cash at the beginning of the period78)Plus:cash equivalents at the end of the period79)Less:cash equivalents at the beginning of the period80)Net increase in cash and cash equivalents。

会计英语课件:Current Assets

$9 000 + $3 000 = $9 000 +

$3 000

▪ Now consider the following transactions that happened in 2020: ▪ (1) Two purchases of electric motor were made; ▪ (2) One sale of the goods took place.

Specific Identification

Includes in cost of goods sold the costs of the specific items sold.

Used when handling a relatively small number of costly, easily distinguishable items.

revenues.

Average-Cost

Prices items in the inventory on the basis of the average cost of all similar goods available during the period.

Not as subject to income manipulation. Measuring a specific physical flow of

▪ Cash is money in the form of bills or coins, which can prompt payment for goods or services in currency or by check.

▪ Cash is listed first in the balance sheet, because it is the most liquid of all current assets.

CH17FinancingCurrentAssets(财务管理,英文版)

Conservative: Use permanent capital for permanent assets and temporary assets.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

17 - 3

Moderate Financing Policy

All rights reserved.

17 - 7

Is there a cost to accruals? Do firms have much control over amount of accruals?

Accruals are free in that no explicit interest is charged.

All rights reserved.

17 - 2

Working Capital Financing Policies

Moderate: Match the maturity of the assets with the maturity of the financing.

Aggressive: Use short-term financing to finance permanent assets.

17 - 10

Company buys goods worth $3,000,000. That’s the cash price.

They must pay $30,303 more if they don’t take discounts.

Think of the extra $30,303 as a financing cost similar to the interest on a loan.

CURRENTASSETS

CURRENTASSETSIntroductionIn financial accounting, current assets are assets that are expected to be converted into cash or used up within a year or an operating cycle, whichever is longer. These assets are an essential component of a company’s balance sheet as they provide liquidity and help meet day-to-day operational expenses. This document aims to provide an overview of current assets, their classification, and significance in financial reporting.Classification of Current AssetsCurrent assets can be classified into the following categories:1. Cash and Cash EquivalentsThis category includes cash on hand, cash held in bank accounts, and investments that are highly liquid and have a short-term maturity (usually within three months). Cash and cash equivalents provide immediate access to funds and are crucial for meeting short-term obligations, such as paying salaries, purchasing inventory, or settling short-term debts.2. Marketable SecuritiesMarketable securities are financial instruments, such as stocks, bonds, or treasury bills, that can be easily bought or sold in the financial markets. These securities are classified as current assets if they are expected to be liquidated within oneyear. While providing some level of flexibility, investing in marketable securities also carries a degree of risk.3. Accounts ReceivableAccounts receivable represent the amounts owed to a company by its customers for goods or services rendered on credit. It is an important component of working capital, and its management is crucial for maintaining a healthy cash flow. However, companies need to be vigilant about timely collection of accounts receivable to avoid potential bad debts and financial difficulties.4. InventoryInventory includes raw materials, work-in-progress, and finished goods held by a company for sale, production, or distribution. Managing inventory efficiently is essential to meet customer demand, minimize holding costs, and prevent obsolescence. Any excess inventory can tie up funds unnecessarily and impact cash flow.5. Prepaid ExpensesPrepaid expenses are future expenses paid in advance, such as insurance premiums, rent, or subscriptions. These expenses are initially recorded as assets but gradually recognized as expenses over time, depending on the benefits received. Prepaid expenses help companies spread out the cost of significant expenses and improve financial planning.Significance of Current AssetsCurrent assets play a vital role in evaluating a company’s financial health, liquidity, and management efficiency. Some of the key significance of current assets are:1. Liquidity AssessmentCurrent assets provide insight into the company’s ability to meet short-term obligations and its overall liquidity. A higher ratio of current assets to current liabilities indicates a healthier liquidity position and the ability to cover immediate financial obligations.2. Working Capital ManagementEffective management of current assets, especially accounts receivable and inventory, is crucial for maintaining optimal levels of working capital. Companies need to strike a balance between cash flow, liquidity, and maintaining sufficient inventory levels to meet customer demand.3. Financial StabilityA strong current asset base enhances the company’s financial stability and resilience against unexpected cash flow disruptions. It provides a buffer to withstand unforeseen expenses or external economic uncertainties.4. Decision MakingFinancial analysis of current assets helps stakeholders, such as investors, creditors, and management, make informeddecisions about the company’s financial position, profitability, and risk profile. It provides insights into the company’s operational efficiency, sales cycle, and cash management practices.ConclusionIn conclusion, current assets are an essential component of a company’s balance sheet, providing liquidity, assessing financial health, and aiding in decision-making. It is crucial for companies to manage their current assets effectively to ensure optimal cash flow, working capital management, and overall financial stability. By carefully analyzing and monitoring current assets, companies can enhance their financial performance and navigate challenges in an increasingly competitive business environment.Note: Markdown is a lightweight markup language, conveniently used for formatting plain text, and it can be easily converted to HTML and other formats.。

Financial Management PPT (17)

Is there a cost to accruals? Do firms have much control over amount of accruals? Accruals are free in that no explicit interest is charged.

Firms have little control over the level of accruals. Levels are influenced more by industry custom, economic factors, and tax laws.

17 - 14

Effective Annual Rate, 1/10, net 40

Periodic rate = 0.01/0.99 = 1.01%. Periods/year = 360/(40 – 10) = 12. EAR = (1 + Periodic rate)n – 1.0 = (1.0101)12 – 1.0 = 12.82%.

17 - 2

Working Capital Financing Policies Moderate: Match the maturity of the assets with the maturity of the financing. Aggressive: Use short-term financing to finance permanent assets. Conservative: Use permanent capital for permanent assets and temporary assets.

CH16ManagingCurrentAssets财务管理,英文版.ppt

All rights reserved.

16 - 4

How does SKI’s working capital policy compare with the industry?

Working capital policy is reflected in current ratio, quick ratio, turnover of cash and securities, inventory turnover, and DSO.

These ratios indicate SKI has large amounts of working capital relative to its level of sales. SKI is either very conservative or inefficient.

Copyright © 2001 by Harcourt, Inc.

Copyright © 2001 by Harcourt, Inc.

All rights reserved.

16 - 8

What’s the goal of cash management?

To meet above objectives, especially to have cash for transactions, yet not have any excess cash.

16 - 9

Ways to Minimize Cash Holdings

Use a lockbox.

Insist on wire transfers from customers.

Synchronize inflows and outflows.

Use a remote disbursement account.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

= $8,333.

Gross/Net Breakdown

Company buys goods worth $3,000,000. That’s the cash price.

They must pay $30,303 more if they don’t take discounts.

$ Marketable Securities

Zero S-T debt

Perm C.A. Fixed Assets

L-T Fin: Stock, Bonds, Spon. C.L.

Years

What is short-term credit, and what are the major sources?

Payables level if don’t take

discount:

Payables = $8,333(40) = $333,333.

Credit Breakdown:

Total trade credit

= $333,333

Free trade credit

= 83,333

Costly trade credit = $250,000

=

0.1212

=

12.12%.

But the $30,303 is paid all during the year, not at year-end, so EAR rate is higher.

Moderate: Match the maturity of the assets with the maturity of the financing.

Aggressive: Use short-term financing to finance permanent assets.

Conservative: Use permanent capital பைடு நூலகம்or permanent assets and temporary assets.

Is there a cost to accruals? Do firms have much control over amount of accruals?

Accruals are free in that no explicit interest is charged.

Firms have little control over the level of accruals. Levels are influenced more by industry custom, economic factors, and tax laws.

To company, yes. Required repayment always looms. May have trouble rolling over loans.

Advantages of short-term credit:

Low cost--visualize yield curve. Can get funds relatively quickly. Can repay without penalty.

What is trade credit?

Trade credit is credit furnished by a firm’s suppliers.

Trade credit is often the largest source of short-term credit, especially for small firms.

Think of the extra $30,303 as a financing cost similar to the interest on a loan.

Want to compare that cost with the cost of a bank loan.

Payables level if take discount: Payables = $8,333(10) = $83,333.

S-T credit: Any debt scheduled for repayment within one year.

Major sources: Accounts payable (trade credit) Bank loans Commercial paper Accruals

Is S-T credit riskier than L-T?

Moderate Financing Policy

$

Temp. C.A.

} S-T Loans

Perm C.A. Fixed Assets

L-T Fin: Stock, Bonds, Spon. C.L.

Years

Lower dashed line, more aggressive.

Conservative Financing Policy

CHAPTER 17

Financing Current Assets

Working capital financing policies A/P (trade credit) Commercial paper S-T bank loans

Working Capital Financing Policies

Spontaneous, easy to get, but cost can be high.

B&B buys $3,030,303 gross, or $3,000,000 net, on terms of 1/10, net 30, and pays on Day 40. How much

free and costly trade credit, and what’s the cost of costly trade credit?

Nominal Cost of Costly Trade Credit

Firm loses 0.01($3,030,303) = $30,303 of discounts to obtain $250,000 in extra trade credit, so

kNom

=

$30,303 $250,000