金蝶资产负债表公式

1金蝶资产负债表公式知识讲解

其中:公益金 未分配利润

所有者权益合计

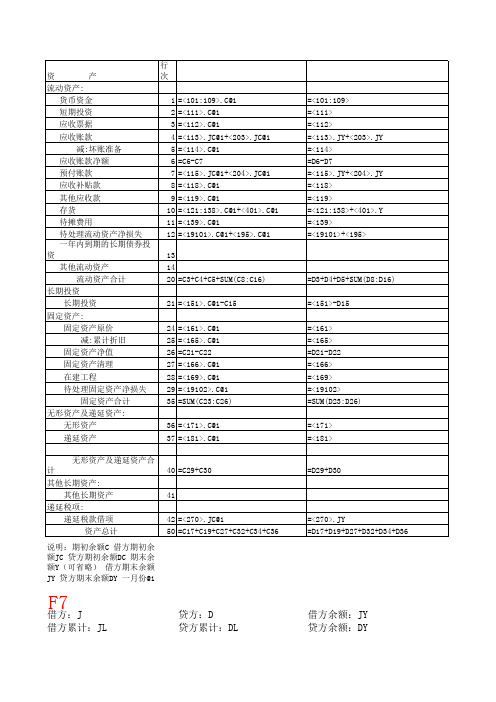

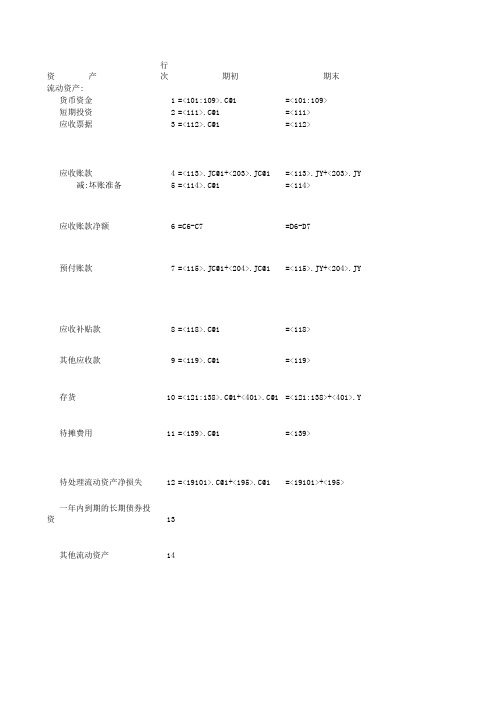

行 次

51 =<201>.C@1 52 =<202>.C@1 53 =<203>.DC@1+<113>.DC@1 54 =<204>.DC@1+<115>.DC@1 55 =<209>.C@1 56 =<211>.C@1 57 =<214>.C@1 58 =<221>.C@1 59 =<223>.C@1 60 =<229>.C@1 61 =<231>.C@1 62

资

产

流动资产:

货币资金

短期投资

应收票据

应收账款

减:坏账准备

应收账款净额

预付账款

应收补贴款

其他应收款

存货

待摊费用

待处理流动资产净损失 一年内到期的长期债券投 资

其他流动资产

流动资产合计

长期投资

长期投资

固定资产:

固定资产原价

减:累计折旧

固定资产净值

固定资产清理

在建工程

待处理固定资产净损失

固定资产合计

无形资产及递延资产:

=D3+D4+D5+SUM(D8:D16 =<165> =D21-D22 =<166> =<169> =<19102> =SUM(D23:D26)

=<171> =<181>

=D29+D30

=<270>.JY =D17+D19+D27+D32+D34+D36

金蝶软件报表公式定义

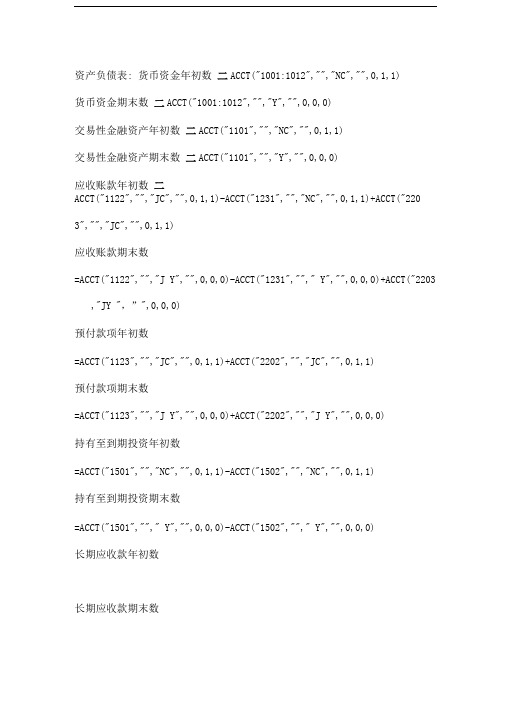

资产负债表: 货币资金年初数二ACCT("1001:1012","","NC","",0,1,1)货币资金期末数二ACCT("1001:1012","","Y","",0,0,0)交易性金融资产年初数二ACCT("1101","","NC","",0,1,1)交易性金融资产期末数二ACCT("1101","","Y","",0,0,0)应收账款年初数二ACCT("1122","","JC","",0,1,1)-ACCT("1231","","NC","",0,1,1)+ACCT("220 3","","JC","",0,1,1)应收账款期末数=ACCT("1122","","J Y","",0,0,0)-ACCT("1231",""," Y","",0,0,0)+ACCT("2203 ,"JY ",”",0,0,0)预付款项年初数=ACCT("1123","","JC","",0,1,1)+ACCT("2202","","JC","",0,1,1)预付款项期末数=ACCT("1123","","J Y","",0,0,0)+ACCT("2202","","J Y","",0,0,0)持有至到期投资年初数=ACCT("1501","","NC","",0,1,1)-ACCT("1502","","NC","",0,1,1)持有至到期投资期末数=ACCT("1501",""," Y","",0,0,0)-ACCT("1502",""," Y","",0,0,0)长期应收款年初数长期应收款期末数长期股权投资年初数二ACCT("1511","","NC","",0,1,1)-ACCT("1512","","NC","",0,1,1)长期股权投资期末数==ACCT("1511",""," Y","",0,0,0)-ACCT("1512",""," Y","",0,0,0)固定资产年初据二ACCT("1601","","NC","",0,1,1)-ACCT("1602","","NC","",0,1,1)-ACCT("16 03","","NC","",0,1,1)固定资产期末据=ACCT("1601",""," Y","",0,0,0)-ACCT("1602",""," Y","",0,0,0)-ACCT("1603", ""," Y","",0,0,0)无形资产年初数二ACCT("1701","","NC","",0,1,1)-ACCT("1702","","NC","",0,1,1)-ACCT("1703","","NC","",0,1,1)无形资产期末数=ACCT("1701",""," Y","",0,0,0)-ACCT("1702",""," Y","",0,0,0)-ACCT("1703", ""," Y","",0,0,0)应付账款年初数二ACCT("2202","","DC","",0,1,1)+ACCT("1123","","DC","",0,1,1)应付账款期末数预收款项年初预收款项期末=ACCT("2203","","D Y","",0,0,0)+ACCT("1122","","D Y","",0,0,0)长期应付款年初数二ACCT("2701","","NC","",0,1,1)-ACCT("2702","","NC","",0,1,1)长期应付款期末数=ACCT("2701",""," Y","",0,0,0)-ACCT("2702",""," Y","",0,0,0)所有者权益年初数二SUM(I3O:I31)-I32+I33+I34所有者权益期末数二SUM(H30:H31)-H32+H33+H34未分配利润二ACCT("4104","","NC","",0,1,1)+ACCT("4103","","NC","",0,1,1)未分配利润期末数二ACCT("4104","","y","",0,0,0)+ACCT("4103","","y","",0,0,0)+ACCT("6001","","y","",0,0,0)+ACCT("6051","","y","",0,0,0)-ACCT("6401","","y","",0,0 ,0)-ACCT("6402","","y","",0,0,0)-ACCT("6403","","y","",0,0,0)-ACCT("6601","”,"y","",0,0,0)-ACCT("6602","","y","",0,0,0)-ACCT("6603","","y","",0,0 ,0)-ACCT("6701","","y","",0,0,0)+ACCT("6101","","y","",0,0,0)+ACCT("6111","","y","",0,0,0)+ACCT("6301","","y","",0,0,0)-ACCT("6711","","y","",0,0 ,0)-ACCT("6801","","y","",0,0,0)存货年初数二ACCT("1401:1406","","NC","",0,1,1)-ACCT("1471","","NC","",0,1,1)+ACC",”NC","",0,1,1)-ACCT("1407","","NC","",0,1,1)存货期末数=二ACCT("1401:1406",""," Y","",0,0,0)-ACCT("1471","","Y","",O,O,O)+ACCT(”5001",""," Y","",0,0,0)+ACCT("1408",""," Y","",0,0,0)+ACCT("1411","","Y ",”",0,0,0)-ACCT("1407","","Y ","",0,0,0)利润表营业收入上期数=二ACCT("6001","","SL","",-1.0,0,0)+ACCT("6051","","SL","",-1.0,0,0)营业收入本期数=ACCT("6001","","SL","",0,0,0)+ACCT("6051","","SL","",0,0,0)营业成本上期数=ACCT("6401","","SL","",-1.0,0,0)+ACCT("6402","","SL","",-1.0,0,0)营业成本本期数=ACCT("6401","","SL","",0,0,0)+ACCT("6402","","SL","",0,0,0)营业税金及附加上期数二ACCT("6403","","SL","",-1.0,0,0)营业税金及附加本期数二=ACCT("6403","","SL","",0,0,0)销售费用上期=ACCT("6601","","SL","",-1.0,0,0)销售费用本期=ACCT("6601","","SL","",0,0,0)管理费用上期数=ACCT("6602","","SL","",-1.0,0,0)管理费用本期数=ACCT("6602","","SL","",0,0,0)财务费用上期=ACCT("6603","","SL","",-1.0,0,0)财务费用本期二ACCT("6603","","SL","",0,0,0)资产减值损失二ACCT("6701","","SL","",-1.0,0,0)资产减值损失=二ACCT("6701","","SL","",0,0,0)公允价值变动收益二ACCT("6101","","SL","",-1.0,0,0) 公允价值变动收益二ACCT("6101","","SL","",0,0,0) 投资收益二ACCT("6111","","SL","",-1.0,0,0)投资收益二ACCT("6111","","SL","",0,0,0)营业利润二E4-E5-E6-E7-E8-E9-E10+E11+E12营业利润二D4-D5-D6-D7-D8-D9-D10+D11+D12营业外收入二ACCT("6301","","SL","",-1.0,0,0)营业外收入=ACCT("6301","","SL","",0,0,0)营业外支出二ACCT("6711","","SL","",-1.0,0,0)营业外支出二ACCT("6711","","SL","",0,0,0)利润总额二E14+E15-E16利润总额二D14+D15-D16所得税费用二ACCT("6801","","SL","",-1.0,0,0)所得税费用二ACCT("6801","","SL","",0,0,0)。

金蝶资产负债表利润表取数详细说明

(一)科目取数公式=<科目代码1:科目代码2>[$币别][.SS][@n]或=<科目代码1:科目代码2>[$币别][.SS][@(y,p)]参数说明:科目代码1:科目代码2:会计科目代码范围。

“:科目代码2”可以省略。

币别:币别代码,如RMB。

省略为综合本位币。

SS:取数标志,省略为本期期末余额。

C 期初余额JC 借方期初余额DC 贷方期初余额AC 期初绝对余额Y 期末余额JY 借方期末余额DY 贷方期末余额AY 期末绝对余额JF 借方发生额DF 贷方发生额JL 借方本年累计发生额DL 贷方本年累计发生额SY 损益表本期实际发生额SL 损益表本年实际发生额B 取科目预算数据TC 折合本位币期初余额TJC 折合本位币借方期初余额TDC 折合本位币贷方期初余额TAC 折合本位币期初绝对余额TY 折合本位币期末余额TJY 折合本位币借方期末余额TDY 折合本位币贷方期末余额TAY 折合本位币期初绝对余额TJF 折合本位币借方发生额TDF 折合本位币贷方发生额TJL 折合本位币借方本年累计发生额TDL 折合本位币贷方本年累计发生额TSY 折合本位币损益表本期实际发生额TSL 折合本位币损益表本年实际发生额n:会计期间。

(若0:本期,-1:上一期,-2:上两期,...),省略为本期。

y:会计年份。

(若0:本年,-1:前一年,-2:前两年,...)p:指定年份的会计期间。

(二)核算项目取数核算项目取数,与科目取数公式兼容。

公式描述如下:=<科目代码1:科目代码2|项目类别|项目代码1:项目代码2>$币别.ss@n或=<科目代码1:科目代码2|项目类别|项目代码1:项目代码2>$币别.ss@(y,p)取数公式中除“<>”内有所区别,其余与科目取数中的描述完全相同。

下面只针对“<>”中的内容进行补充说明:“<>”中内容用于选择科目和核算项目,公式中的科目代码,项目类别和项目代码,在字符“|”和“:”的分隔下可以进行20种组合,得到不同范围的科目和核算项目。

金碟财务软件资产负债表考试公式注解

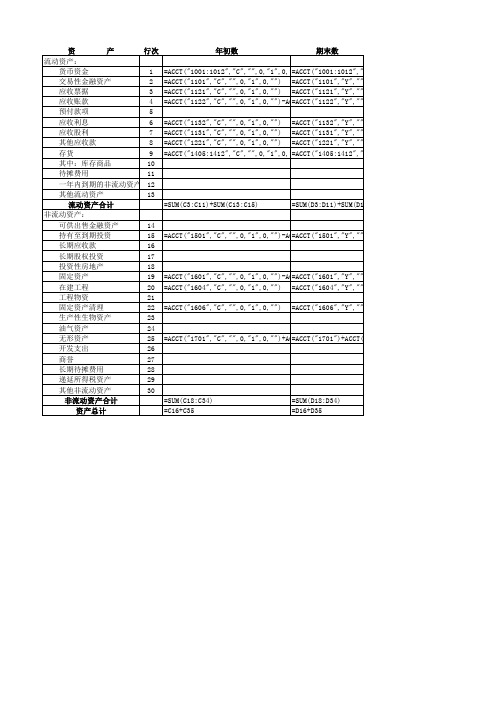

资 产行次期初期末流动资产:货币资金1=<101:109>.C@1=<101:109>短期投资2=<111>.C@1=<111>应收票据3=<112>.C@1=<112>应收账款4=<113>.JC@1+<203>.JC@1=<113>.JY+<203>.JY减:坏账准备5=<114>.C@1=<114>应收账款净额6=C6-C7=D6-D7预付账款7=<115>.JC@1+<204>.JC@1=<115>.JY+<204>.JY应收补贴款8=<118>.C@1=<118>其他应收款9=<119>.C@1=<119>存货10=<121:138>.C@1+<401>.C@1=<121:138>+<401>.Y待摊费用11=<139>.C@1=<139>待处理流动资产净损失12=<19101>.C@1+<195>.C@1=<19101>+<195>一年内到期的长期债券投资13其他流动资产14流动资产合计20=C3+C4+C5+SUM(C8:C16)=D3+D4+D5+SUM(D8:D16)长期投资长期投资21=<151>.C@1-C15=<151>-D15固定资产:固定资产原价24=<161>.C@1=<161>减:累计折旧25=<165>.C@1=<165>固定资产净值26=C21-C22=D21-D22固定资产清理27=<166>.C@1=<166>在建工程28=<169>.C@1=<169>待处理固定资产净损失29=<19102>.C@1=<19102>固定资产合计35=SUM(C23:C26)=SUM(D23:D26)无形资产及递延资产:无形资产36=<171>.C@1=<171>递延资产37=<181>.C@1=<181>无形资产及递延资产合计40=C29+C30=D29+D30其他长期资产:其他长期资产41递延税项:递延税款借项42=<270>.JC@1=<270>.JY资产总计50=C17+C19+C27+C32+C34+C36=D17+D19+D27+D32+D34+D36负债及所有者权益行次流动负债:短期借款51=<201>.C@1=<201>应付票据52=<202>.C@1=<202>应付账款53=<203>.DC@1+<113>.DC@1=<203>.DY+<113>.DY预收账款54=<204>.DC@1+<115>.DC@1=<204>.DY+<115>.DY@用以说明科目所属的会计期间其他应付款55=<209>.C@1=<209>应付工资56=<211>.C@1=<211>如:@(2001,1)表示2001年第一个会计期间 应付福利费57=<214>.C@1=<214>如:@(2001,-1)表示2001年上一个会计期间 未交税金58=<221>.C@1=<221>没有下一个会计期间的说法,因为下一个会 未付利润59=<223>.C@1=<223>如:@1表示本年的第一个会计期间其他未交款60=<229>.C@1=<229>@-1表示本年上一期预提费用61=<231>.C@1=<231>@-2表示本年倒数第二期一年内到期的长期负债62@(-3,-3)表示倒数第三年倒数第三 其他流动负债63@(-1,0)表示去年本期流动负债合计70=SUM(G3:G15)=SUM(H3:H15)[1:3]表示求1-3行的和长期负债:<111>表示"短期投资"这个科目111 长期借款71=<241>.C@1=<241>.JC表示借方期初余额应付债券72=<251>.C@1=<251>.JY表示借方期末余额长期应付款73=<261>.C@1=<261>.C期初余额其他长期负债80=<272>.C@1+<275>.C@1=<272>+<275>.DY贷方期末余额其中:住房周转金81=<275>.C@1=<275><>科目后面什么没有表示期末余额长期负债合计83=SUM(G18:G21)-G14=SUM(H18:H21)-H14递延税项:递延税款贷项85=<270>.DC@1=<270>.JY负债合计90=G26+G24+G16=H26+H24+H16所有者权益:实收资本91=<301>.C@1=<301>资本公积92=<311>.C@1=<311>盈余公积93=<313>.C@1=<313>其中:公益金94=<31302>.C@1=<31302>未分配利润95=<321>.C@1+<322>.C@1=<321>+<322>所有者权益合计96=G33+SUM(G29:G31)=H33+SUM(H29:H31)100=G34+G27=H34+H27负债及所有者权益总计属的会计期间1)表示2001年第一个会计期间-1)表示2001年上一个会计期间会计期间的说法,因为下一个会计期间尚未发生本年的第一个会计期间本年倒数第二期表示倒数第三年倒数第三期表示去年本期示求1-3行的和示"短期投资"这个科目111是它的科目代码借方期初余额借方期末余额面什么没有表示期末余额。

金蝶软件资产负债表

资产负债表:货币资金年初数=ACCT("1001:1012","","NC","",0,1,1)货币资金期末数=ACCT("1001:1012","","Y","",0,0,0)交易性金融资产年初数=ACCT("1101","","NC","",0,1,1)交易性金融资产期末数=ACCT("1101","","Y","",0,0,0)应收账款年初数=ACCT("1122","","JC","",0,1,1)-ACCT("1231","","NC","",0,1,1)+ACCT("2203","","JC","",0,1,1)应收账款期末数=ACCT("1122","","JY","",0,0,0)-ACCT("1231","","Y","",0,0,0)+ACCT("2203","","JY","",0,0,0)预付款项年初数=ACCT("1123","","JC","",0,1,1)+ACCT("2202","","JC","",0,1,1)预付款项期末数=ACCT("1123","","JY","",0,0,0)+ACCT("2202","","JY","",0,0,0)持有至到期投资年初数=ACCT("1501","","NC","",0,1,1)-ACCT("1502","","NC","",0,1,1)持有至到期投资期末数=ACCT("1501","","Y","",0,0,0)-ACCT("1502","","Y","",0,0,0)长期应收款年初数=ACCT("1531","","NC","",0,1,1)-ACCT("1532","","NC","",0,1,1)长期应收款期末数=ACCT("1531","","Y","",0,0,0)-ACCT("1532","","Y","",0,0,0)长期股权投资年初数=ACCT("1511","","NC","",0,1,1)-ACCT("1512","","NC","",0,1,1)长期股权投资期末数==ACCT("1511","","Y","",0,0,0)-ACCT("1512","","Y","",0,0,0)固定资产年初据=ACCT("1601","","NC","",0,1,1)-ACCT("1602","","NC","",0,1,1)-ACCT("1603","","NC","",0,1,1)固定资产期末据=ACCT("1601","","Y","",0,0,0)-ACCT("1602","","Y","",0,0,0)-ACCT("1603","","Y","",0,0,0)无形资产年初数=ACCT("1701","","NC","",0,1,1)-ACCT("1702","","NC","",0,1,1)-ACCT("1703","","NC","",0,1,1) 无形资产期末数=ACCT("1701","","Y","",0,0,0)-ACCT("1702","","Y","",0,0,0)-ACCT("1703","","Y","",0,0,0)应付账款年初数=ACCT("2202","","DC","",0,1,1)+ACCT("1123","","DC","",0,1,1)应付账款期末数=ACCT("2202","","DY","",0,0,0)+ACCT("1123","","DY","",0,0,0)预收款项年初=ACCT("2203","","DC","",0,1,1)+ACCT("1122","","DC","",0,1,1)预收款项期末=ACCT("2203","","DY","",0,0,0)+ACCT("1122","","DY","",0,0,0)长期应付款年初数=ACCT("2701","","NC","",0,1,1)-ACCT("2702","","NC","",0,1,1)长期应付款期末数=ACCT("2701","","Y","",0,0,0)-ACCT("2702","","Y","",0,0,0)所有者权益年初数=SUM(I30:I31)-I32+I33+I34所有者权益期末数=SUM(H30:H31)-H32+H33+H34未分配利润=ACCT("4104","","NC","",0,1,1)+ACCT("4103","","NC","",0,1,1)未分配利润期末数=ACCT("4104","","y","",0,0,0)+ACCT("4103","","y","",0,0,0)+ACCT("6001","","y","",0,0,0)+ACCT("6051","","y","",0 ,0,0)-ACCT("6401","","y","",0,0,0)-ACCT("6402","","y","",0,0,0)-ACCT("6403","","y","",0,0,0)-ACCT("6601","","y"," ",0,0,0)-ACCT("6602","","y","",0,0,0)-ACCT("6603","","y","",0,0,0)-ACCT("6701","","y","",0,0,0)+ACCT("6101","","y ","",0,0,0)+ACCT("6111","","y","",0,0,0)+ACCT("6301","","y","",0,0,0)-ACCT("6711","","y","",0,0,0)-ACCT("6801"," ","y","",0,0,0)存货年初数=ACCT("1401:1406","","NC","",0,1,1)-ACCT("1471","","NC","",0,1,1)+ACCT("5001","","NC","",0,1, 1)+ACCT("1408","","NC","",0,1,1)+ACCT("1411","","NC","",0,1,1)-ACCT("1407","","NC","",0,1,1) 存货期末数==ACCT("1401:1406","","Y","",0,0,0)-ACCT("1471","","Y","",0,0,0)+ACCT("5001","","Y","",0,0,0)+A CCT("1408","","Y","",0,0,0)+ACCT("1411","","Y","",0,0,0)-ACCT("1407","","Y","",0,0,0)。

金蝶报表公式

JC 借方期初余额

DC 贷方期初余额

AC 期初绝对余额

Y 期末余额

JY 借方期末余额

DY 贷方期末余额

AY 期末绝对余额

JF 借方发生额 DF 贷方发生额

JL 借方本年累计发生额

DL 贷方本年累计发生额

SY 损益表本期实际发生额

SL 损益表本年实际发生额

B 取科目预算数据

处理方法:

1、打开报表与分析中的资产负债表,选择菜单中的属性→报表属性;

2、打开“报表属性”→“页眉页脚”→选择需要编辑的栏目→点击“编辑页眉页脚”,如下图;

3、在“单位名称:”后输入“长沙某软件有限公司”,在分段符“|”后输入取数公式:“&[会计年度]年&[报表期间]月&[最大日期]日”,完成后点击“确定”即可保存。

如下图所示:

日期取数公式:

年:&[会计年度]

月:&[报表期间]

日:&[最大日期]

在对应的公式后加入对应的单位即可。

完整的公式为:“&[[会计年度]年&[报表期间]月&[最大日期]日”。

“|”为分段符,可以将一行分成N段。

4、最后,退出报表时记得点击保存。

1金蝶资产负债表公式知识讲解

F7

借方:J 借方累计:JL

贷方:D 贷方累计:DL

=<101:109> =<111> =<112> =<113>.JY+<203>.JY =<114> =D6-D7 =<115>.JY+<204>.JY =<118> =<119> =<121:138>+<401>.Y =<139> =<19101>+<195>

63 70 =SUM(G3:G15)

=<201> =<202> =<203>.DY+<113>.DY =<204>.DY+<115>.DY =<209> =<211> =<214> =<221> =<223> =<229> =<231>

=SUM(H3:H15)

71 =<241>.C@1 72 =<251>.C@1 73 =<261>.C@1 80 =<272>.C@1+<275>.C@1 81 =<275>.C@1

13 14 20 =C3+C4+C5+SUM(C8:C16)

21 =<151>.C@1-C15

24 =<161>.C@1 25 =<165>.C@1 26 =C21-C22 27 =<166>.C@1 28 =<169>.C@1 29 =<19102>.C@1 35 =SUM(C23:C26)

金蝶资产负债表公式设置

金蝶资产负债表公式设置金蝶资产负债表公式设置金蝶是一家全球化的企业管理软件解决方案提供商,其涉及的业务范围包括财务会计、采购管理、销售管理、人力资源管理等多个方面。

在财务会计方面,金蝶的资产负债表公式设置非常精细。

下面就来详细解析一下。

一、资产负债表的概念资产负债表是一张反映企业某一时点上的资产、负债和所有者权益状况的财务报表。

它包括两个部分:资产部分和负债及所有者权益部分。

资产部分反映的是企业拥有的资源和对外应收款项,主要包括现金、存款、应收账款、存货、固定资产等。

负债及所有者权益部分反映的是企业担负的债务和归属于所有者的权益,主要包括应付账款、长期负债、营业收入、所有者权益等。

二、金蝶资产负债表公式设置金蝶资产负债表公式设置非常完善和灵活,可以根据企业的实际情况进行设置。

在设置资产负债表时,需要分别设置资产部分和负债及所有者权益部分。

1. 资产部分的公式设置金蝶资产负债表的资产部分主要由流动资产和非流动资产两个部分组成。

在设置流动资产时,需要分别设置现金、银行存款、应收账款、存货、其他应收款的公式,具体如下:(1)现金公式现金=现金流入-现金流出(2)银行存款公式银行存款=人民币存款+外币存款(3)应收账款公式应收账款=销售收入-收回的账款(4)存货公式存货=进入的货物-出售的货物(5)其他应收款公式其他应收款=其他资产-其他应收账款-预付款项在设置非流动资产时,需要分别设置固定资产、长期投资、无形资产和其他资产的公式,具体如下:(1)固定资产公式固定资产=累计折旧-固定资产减值准备(2)长期投资公式长期投资=长期应收款+长期股权投资(3)无形资产公式无形资产=研发支出+专利、商标、著作权+商誉(4)其他资产公式其他资产=其他非流动资产2. 负债及所有者权益部分的公式设置在设置负债及所有者权益部分时,需要分别设置流动负债、非流动负债和所有者权益三个部分,具体如下:(1)流动负债公式流动负债=短期借款+应付账款+预收款项+其他应付款(2)非流动负债公式非流动负债=长期负债+长期应付款+递延所得税负债(3)所有者权益公式所有者权益=实收资本+资本公积+盈余公积+未分配利润三、总结金蝶资产负债表公式的设置非常精细,能够满足不同企业的财务会计需求。

金蝶软件报表公式定义

资产负债表:货币资金年初数=ACCT(”1001:1012”,"",”NC”,"”,0,1,1)货币资金期末数=ACCT("1001:1012”,"",”Y","”,0,0,0)交易性金融资产年初数=ACCT(”1101”,"","NC","”,0,1,1)交易性金融资产期末数=ACCT("1101",””,”Y","”,0,0,0)应收账款年初数=ACCT(”1122”,”","JC",”",0,1,1)-ACCT(”1231”,”","NC",”",0,1,1)+ACCT(”2203”,”",”JC”,"”,0,1,1)应收账款期末数=ACCT("1122",”","JY","”,0,0,0)—ACCT(”1231","","Y",””,0,0,0)+ACCT (”2203",”","JY","”,0,0,0)预付款项年初数=ACCT("1123","”,"JC","”,0,1,1)+ACCT("2202",”",”JC",”",0,1,1)预付款项期末数=ACCT(”1123",””,”JY","”,0,0,0)+ACCT(”2202","",”JY","",0,0,0)持有至到期投资年初数=ACCT(”1501","”,"NC","",0,1,1)-ACCT(”1502”,"",”NC”,"",0,1,1)持有至到期投资期末数=ACCT("1501",””,”Y",””,0,0,0)—ACCT("1502","","Y","”,0,0,0)长期应收款年初数=ACCT("1531","”,”NC",”",0,1,1)—ACCT(”1532","”,”NC”,”",0,1,1)长期应收款期末数=ACCT(”1531",””,”Y”,”",0,0,0)-ACCT("1532”,"”,”Y",”",0,0,0)长期股权投资年初数=ACCT(”1511”,”","NC”,"”,0,1,1)-ACCT("1512”,”",”NC","”,0,1,1)长期股权投资期末数==ACCT(”1511",””,”Y","",0,0,0)—ACCT(”1512”,"",”Y”,”",0,0,0)固定资产年初据=ACCT("1601”,"”,”NC",””,0,1,1)—ACCT("1602","”,"NC",””,0,1,1)-ACCT(”1603”,"",”NC”,”",0,1,1)固定资产期末据=ACCT(”1601",”",”Y","",0,0,0)—ACCT("1602”,"”,"Y","",0,0,0)—ACCT("1603”,”",”Y”,"”,0,0,0)无形资产年初数=ACCT("1701","",”NC”,”",0,1,1)-ACCT(”1702",”","NC",”",0,1,1)-ACCT(”1703”,"”,"NC”,"”,0,1,1)无形资产期末数=ACCT(”1701","",”Y",””,0,0,0)—ACCT("1702","","Y”,"",0,0,0)—ACCT(”1703”,””,”Y”,"”,0,0,0)应付账款年初数=ACCT("2202","”,”DC”,"",0,1,1)+ACCT(”1123",”",”DC”,”",0,1,1)应付账款期末数=ACCT(”2202","”,”DY”,"”,0,0,0)+ACCT(”1123",”",”DY","",0,0,0)预收款项年初=ACCT("2203”,””,”DC”,"”,0,1,1)+ACCT(”1122","”,"DC”,"",0,1,1)预收款项期末=ACCT("2203”,"","DY",”",0,0,0)+ACCT("1122”,"","DY",””,0,0,0)长期应付款年初数=ACCT(”2701”,"",”NC”,"”,0,1,1)-ACCT(”2702”,"","NC”,”",0,1,1)长期应付款期末数=ACCT(”2701”,"”,”Y”,"",0,0,0)-ACCT(”2702”,"”,”Y”,””,0,0,0)所有者权益年初数=SUM(I30:I31)-I32+I33+I34所有者权益期末数=SUM(H30:H31)—H32+H33+H34未分配利润=ACCT("4104”,"","NC”,"”,0,1,1)+ACCT("4103”,"","NC”,"”,0,1,1)未分配利润期末数=ACCT("4104”,"”,”y",””,0,0,0)+ACCT("4103",””,”y”,”",0,0,0)+ACCT("6001",”",”y","",0,0,0)+ACCT(”6051”,"”,”y","”,0,0,0)—ACCT(”6401","”,"y”,””,0,0,0)-ACCT(”6402”,”",”y”,"",0,0,0)—ACCT(”6403","”,"y”,"",0,0,0)—ACCT("6601",”","y”,”",0,0,0)—ACCT("6602",”",”y","",0,0,0)—ACCT(”6603",”","y”,””,0,0,0)-ACCT("6701”,"","y”,””,0,0,0)+ACCT(”6101”,"",”y","",0,0,0)+ACCT("6111","",”y",””,0,0,0)+ACCT("6301","","y”,"",0,0,0)-ACCT("6711”,"",”y",”",0,0,0)—ACCT("6801",”","y”,"",0,0,0)存货年初数=ACCT(”1401:1406”,”","NC","",0,1,1)—ACCT(”1471","”,"NC",””,0,1,1)+ACCT ("5001",””,"NC",””,0,1,1)+ACCT(”1408",”",”NC”,"",0,1,1)+ACCT("1411”,"”,”NC”,”",0,1,1)—ACCT(”1407”,”",”NC”,”",0,1,1)存货期末数==ACCT(”1401:1406",”",”Y",”",0,0,0)—ACCT(”1471","",”Y","",0,0,0)+ACCT (”5001",””,"Y","”,0,0,0)+ACCT(”1408",”",”Y",””,0,0,0)+ACCT("1411","",”Y","”,0,0,0)-ACCT(”1407”,"”,"Y","",0,0,0)利润表营业收入上期数==ACCT(”6001”,”",”SL”,”",-1.0,0,0)+ACCT(”6051”,"",”SL”,"",-1。

金蝶资产负债表公式设置

开发支出

商誉

长期待摊费用

递延所得税资产

其他非流动资产

非流动资产合计

资产总计

行次

年初数

期末数

1 2 3 4

=ACCT("1001:1012","C","",0,"1",0 =ACCT("1001:1012",

,"") =ACCT("1101","C","",0,"1",0,"") ==AACCCCTT((""11112212"",,""CC"",,"""",,00,,""11"",,00,,""""))-

资

产

流动资产:

货币资金

交易性金融资产

应收票据

应收账款

预付款项

应收利息

应收股利

其他应收款

存货

其中:库存商品

待摊费用 一年内到期的非流动资

产 其他流动资产

流动资产合计

非流动资产:

可供出售金融资产

持有至到期投资

长期应收款

长期股权投资

投资性房地产

固定资产

在建工程

工程物资

固定资产清理

生产性生物资产

油气资产

无形资产

53

54 55 56

=ACCT("4101","C","",0,"1",0, "="A)CCT("4101.01","C","",0,"1"

金蝶软件应交税费资产负债表公式设置

金蝶软件应交税费资产负债表公式设置

分别双击该单元格,输入以下公式后,出车!

▲(以下用3位科目代码举例,自可复制,粘贴过去,或修改为4位科目代码后,再回车!)

期初数(列)公式。

如:1)货币资金取数;2)单个科目取数公式,自行修改科目代码

=<101:102>.C@1

=<120>.C@1

期末数(列)公式。

如:1)货币资金取数;2)通常单个科目取数公式

=<101:102>

=<120>

金蝶软件应交税费资产负债表公式相关阅读延伸:

金蝶软件资产负债表公式怎么设置?

报表上方有个“向导”,点向导

1、选取科目

2、选好数据(选期初余额、期末余额、本期损益实际发生额)。

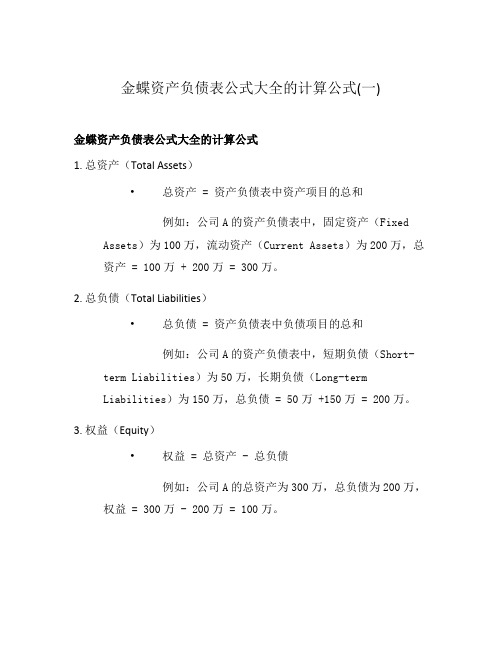

金蝶资产负债表公式大全的计算公式(一)

金蝶资产负债表公式大全的计算公式(一)金蝶资产负债表公式大全的计算公式1. 总资产(Total Assets)•总资产 = 资产负债表中资产项目的总和例如:公司A的资产负债表中,固定资产(Fixed Assets)为100万,流动资产(Current Assets)为200万,总资产 = 100万 + 200万 = 300万。

2. 总负债(Total Liabilities)•总负债 = 资产负债表中负债项目的总和例如:公司A的资产负债表中,短期负债(Short-term Liabilities)为50万,长期负债(Long-termLiabilities)为150万,总负债 = 50万 +150万 = 200万。

3. 权益(Equity)•权益 = 总资产 - 总负债例如:公司A的总资产为300万,总负债为200万,权益 = 300万 - 200万 = 100万。

4. 总营业收入(Total Revenue)•总营业收入 = 资产负债表中营业收入(Operating Revenue)的总和例如:公司A的资产负债表中,销售收入(Sales Revenue)为80万,其他营业收入(Other Operating Revenue)为20万,总营业收入 = 80万 + 20万 = 100万。

5. 总营业成本(Total Expenses)•总营业成本 = 资产负债表中营业成本(Cost of Goods Sold)的总和例如:公司A的资产负债表中,原材料成本(Raw Material Cost)为30万,人工成本(Labor Cost)为20万,总营业成本 = 30万 + 20万 = 50万。

6. 净利润(Net Profit)•净利润 = 总营业收入 - 总营业成本例如:公司A的总营业收入为100万,总营业成本为50万,净利润 = 100万 - 50万 = 50万。

7. 总资产周转率(Total Asset Turnover)•总资产周转率 = 总营业收入 / 总资产例如:公司A的总营业收入为100万,总资产为300万,总资产周转率 = 100万 / 300万 = 。

金蝶资产负债表预付账款公式

金蝶资产负债表预付账款公式

金蝶资产负债表预付账款公式

金蝶资产负债表是指金蝶集团的财务报表,用于反映公司的财务状况

和经营成果。

其中,预付账款是指公司预先支付的货物或服务的费用,但还未收到货物或服务的情况下的账款。

预付账款是金蝶资产负债表中的一个重要指标,其公式为:预付账款

= 预付货款 + 预付劳务款。

其中,预付货款指已预缴的货物费用,预

付劳务款指已预缴的服务费用。

预付账款的变化情况对公司的经营状况有着重要的影响。

如果预付账

款不断增加,说明公司对供应商的信用度在提高,但也可能造成流动

资金的紧张。

相反,如果预付账款不断减少,则说明公司的现金流状

况在变得更加充裕。

因此,对于公司来说,合理掌握预付账款的变化情况是非常重要的。

通过财务报表中的预付账款指标,可以及时调整企业的经营策略和流

动资金的使用。

金蝶资产负债表其他流动资产公式

金蝶资产负债表其他流动资产公式

【原创实用版】

目录

1.金蝶资产负债表概述

2.其他流动资产的定义与计算公式

3.金蝶资产负债表其他流动资产公式的应用实例

正文

一、金蝶资产负债表概述

金蝶资产负债表是一款企业管理软件中的财务报表工具,用于帮助企业进行财务管理、分析及决策。

资产负债表是企业三大财务报表之一,它反映了企业在某一特定时间点的财务状况,展示了企业的资产、负债和所有者权益。

通过分析资产负债表,企业可以了解自身的财务状况,以便做出更为明智的经营决策。

二、其他流动资产的定义与计算公式

其他流动资产是指企业在资产负债表日一年内 (含一年) 预计能够

变现或耗用的资产,以及预计在一年内 (含一年) 收回的资产。

这类资产通常包括预付款项、预收款项、存货、待摊费用等。

其他流动资产的计算公式为:

其他流动资产 = 预付款项 + 预收款项 + 存货 + 待摊费用

三、金蝶资产负债表其他流动资产公式的应用实例

假设某企业在资产负债表日,其预付款项为 20 万元,预收款项为 30 万元,存货为 40 万元,待摊费用为 50 万元。

那么,该企业的其他流动资产为:

其他流动资产 = 20 万元 + 30 万元 + 40 万元 + 50 万元 = 140 万

元

通过金蝶资产负债表其他流动资产公式,企业可以清晰地了解到其他流动资产的总额,从而更好地分析和调整企业的财务状况。

金蝶资产负债表其他流动资产公式

金蝶资产负债表其他流动资产公式

(原创版)

目录

1.金蝶资产负债表概述

2.其他流动资产的定义和作用

3.金蝶资产负债表其他流动资产公式

4.举例说明公式的应用

正文

一、金蝶资产负债表概述

金蝶资产负债表是一款财务软件,用于帮助企业进行财务管理和分析。

资产负债表是企业财务报表中的一种,它反映了企业在某一特定时间点的财务状况,主要包括资产、负债和所有者权益三个部分。

通过分析资产负债表,企业可以了解自己的资产、负债及权益状况,以便更好地制定经营策略和财务决策。

二、其他流动资产的定义和作用

其他流动资产是指企业在资产负债表日之前的一年内预计可以变现、但尚未归类的流动资产。

它主要包括短期投资、预付款项、应收票据、其他应收款等。

其他流动资产对于企业的短期偿债能力和运营能力具有重要意义,可以帮助企业更好地管理流动资产,提高资金使用效率。

第1页共1页。

金蝶资产负债表其他流动资产公式

金蝶资产负债表其他流动资产公式

摘要:

一、资产负债表概述

1.资产负债表的定义

2.资产负债表的作用

二、金蝶资产负债表其他流动资产项目

1.项目定义

2.计算公式

三、金蝶资产负债表其他流动资产项目的应用

1.企业如何运用其他流动资产

2.其他流动资产对企业的意义

四、资产负债表其他流动资产项目的注意事项

1.项目填列要求

2.项目分析方法

正文:

一、资产负债表概述

资产负债表是反映企业在一定时期内财务状况的重要报表,主要包括资产、负债和所有者权益三部分。

资产负债表可以帮助企业管理者、投资者和其他利益相关者了解企业的经营状况、财务实力以及偿债能力。

二、金蝶资产负债表其他流动资产项目

在金蝶资产负债表中,其他流动资产项目是一个重要的组成部分。

其他流

动资产是指企业在一年内可以转化为现金或消耗的资产,包括以下内容:其他流动资产= 存货+ 应收账款+ 预付款项+ 其他应收款+ 短期投资+ 一年内到期的非流动资产+ 其他流动资产

三、金蝶资产负债表其他流动资产项目的应用

企业应充分利用其他流动资产项目,优化资产结构,提高资产周转率,从而提高企业的经营效益。

例如,企业可以通过加快应收账款回收、控制存货水平、合理安排短期投资等方式,提高其他流动资产的运用效率。

四、资产负债表其他流动资产项目的注意事项

在填写其他流动资产项目时,企业应按照会计准则和报表编制要求,真实、准确地反映企业的财务状况。

同时,企业还应关注其他流动资产项目的变动情况,分析其对企业的财务状况和经营业绩的影响,为决策提供依据。

金蝶资产负债表其他流动资产公式

金蝶资产负债表其他流动资产公式【实用版】目录1.金蝶资产负债表概述2.其他流动资产的定义与公式3.金蝶资产负债表其他流动资产的计算方法4.金蝶资产负债表其他流动资产的填写规范5.金蝶资产负债表其他流动资产的注意事项正文一、金蝶资产负债表概述金蝶资产负债表是一款企业财务管理软件中的报表工具,用于反映企业在某一特定时间点的财务状况,包括企业的资产、负债和所有者权益。

资产负债表是企业财务报表的重要组成部分,对于企业管理者、投资者和其他利益相关者来说,具有重要的参考价值。

二、其他流动资产的定义与公式其他流动资产是指企业在一个营业周期内(通常为一年)可以变现、用于偿还债务或用于企业经营活动的资产。

其他流动资产的公式通常为:其他流动资产 = 流动资产总额 - 存货 - 应收账款 - 预付款项 - 应收利息 - 应收股利 - 其他应收款。

三、金蝶资产负债表其他流动资产的计算方法在金蝶资产负债表中,其他流动资产的计算方法与上述公式一致。

首先,需要计算出流动资产总额,然后分别减去存货、应收账款、预付款项、应收利息、应收股利和其他应收款,得出的其他流动资产的数值即为所求。

四、金蝶资产负债表其他流动资产的填写规范在填写金蝶资产负债表时,其他流动资产应按照实际情况进行填写。

需要注意的是,其他流动资产的填写应当准确、完整,以确保资产负债表的准确性。

此外,在填写其他流动资产时,还应遵循会计准则和税收法规的相关规定。

五、金蝶资产负债表其他流动资产的注意事项在填写金蝶资产负债表其他流动资产时,应注意以下几点:1.确保计算方法正确,避免因计算错误导致其他流动资产的数据不准确;2.仔细核对相关数据,确保其他流动资产的数据真实、完整;3.遵循会计准则和税收法规,避免因违规操作而产生的不良后果;4.定期对资产负债表进行分析,以便企业管理者及时了解企业财务状况,做出合理决策。

总之,金蝶资产负债表是企业财务管理的重要工具,其他流动资产作为资产负债表的组成部分,对于反映企业财务状况具有重要意义。

金蝶资产负债表公式设置

30

非流动资产合计

=SUM(C18:C34)

=SUM(D18:D34)

资产总计

=C16+C35

=D16+D35

负债和股东权益

行次

年初数

期末数

流动负债:

短期借款

31

交易性金融负债

32

应付票据

33 =ACCT("2201","C","",0,"1",0,"="A)CCT("2201","Y","",0,0,0,"")

在建工程

20 =ACCT("1604","C","",0,"1",0,"") =ACCT("1604","Y","",0,0,0,"")

工程物资

21

固定资产清理

22 =ACCT("1606","C","",0,"1",0,"") =ACCT("1606","Y","",0,0,0,"")

生产性生物资产

应收票据

3 =ACCT("1121","C","",0,"1",0,"") =ACCT("1121","Y","",0,0,0,"")

应收账款