ACCA F5 2010年12月真题答案

ACCA 2010 Dec Answer

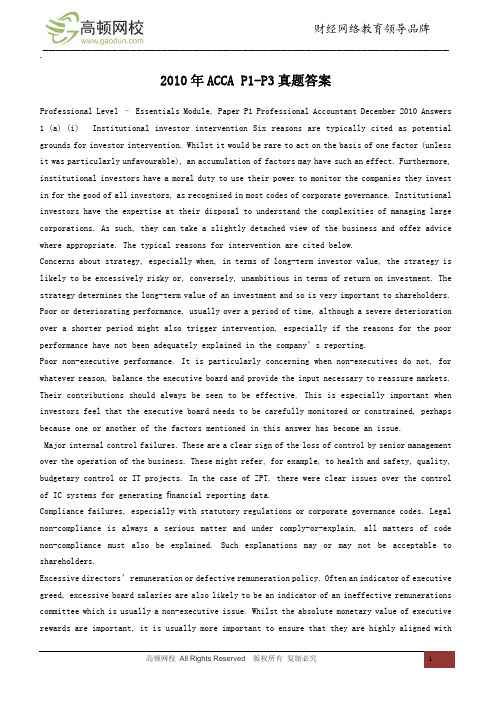

AnswersProfessional Level – Essentials Module, Paper P1Professional Accountant December 2010 Answers 1 (a) (i) Institutional investor interventionSix reasons are typically cited as potential grounds for investor intervention. Whilst it would be rare to act on the basis ofone factor (unless it was particularly unfavourable), an accumulation of factors may have such an effect. Furthermore,institutional investors have a moral duty to use their power to monitor the companies they invest in for the good of allinvestors, as recognised in most codes of corporate governance. Institutional investors have the expertise at their disposalto understand the complexities of managing large corporations. As such, they can take a slightly detached view of thebusiness and offer advice where appropriate. The typical reasons for intervention are cited below.Concerns about strategy, especially when, in terms of long-term investor value, the strategy is likely to be excessivelyrisky or, conversely, unambitious in terms of return on investment. The strategy determines the long-term value of aninvestment and so is very important to shareholders.deteriorating performance, usually over a period of time, although a severe deterioration over a shorter period orPoormight also trigger intervention, especially if the reasons for the poor performance have not been adequately explained inthe company’s reporting.Poor non-executive performance. It is particularly concerning when non-executives do not, for whatever reason, balancethe executive board and provide the input necessary to reassure markets. Their contributions should always be seen tobe effective. This is especially important when investors feel that the executive board needs to be carefully monitored orconstrained, perhaps because one or another of the factors mentioned in this answer has become an issue.Majorinternal control failures. These are a clear sign of the loss of control by senior management over the operation of the business. These might refer, for example, to health and safety, quality, budgetary control or IT projects. In the case ofZPT, there were clear issues over the control of IC systems for generating fi nancial reporting data.Compli ance fai lures, especially with statutory regulations or corporate governance codes. Legal non-compliance isalways a serious matter and under comply-or-explain, all matters of code non-compliance must also be explained. Suchexplanations may or may not be acceptable to shareholders.Excessive directors’ remuneration or defective remuneration policy. Often an indicator of executive greed, excessive boardsalaries are also likely to be an indicator of an ineffective remunerations committee which is usually a non-executive issue.Whilst the absolute monetary value of executive rewards are important, it is usually more important to ensure that theyare highly aligned with shareholder interests (to minimise agency costs).ethical performance, or lack of social responsibility. Showing a lack of CSR can be important in terms of the orPoorCSRcompany’s long-term reputation and also its vulnerability to certain social and environmental risks.[Tutorial note: the study texts approach this slightly differently.](ii) Case for interventionAfter the fi rst restatement, it was evident that three of the reasons for interventions were already present. Whilst one ofthese perhaps need not have triggered an intervention alone, the number of factors makes a strong case for an urgentmeeting between the major investors and the ZPT board, especially Mr Xu.Poor performance. The restated results were ‘all significantly below market expectations’. Whilst this need not initself have triggered an institutional investor intervention, the fact that the real results were only made public after aninitial results announcement is unfortunate. The obvious question to ask the ZPT board is why the initial results weremis-stated and why they had to be corrected as this points to a complete lack of controls within the business. A set ofresults well below market expectations always needs to be explained to shareholders.Internal control and potential compliance failures. There is ample evidence to suggest that internal controls in ZPT werevery defi cient, especially (and crucially) those internal controls over external fi nancial reporting. The case mentions, ‘noeffective management oversight of the external reporting process and a disregard of the relevant accounting standards’,both of which are very serious allegations. Linked to this, the investors need an urgent clarifi cation of the legal allegationsof fraud, especially in the light of the downward restatement of the results. Any suggestion of compliance failure isconcerning but fraud (down to intent rather than incompetence) is always serious as far as investors are concerned.Excessive remuneration in the form of the $20 million bonus. It is likely that this bonus was excessive even had theinitial results been accurate, but after the restatement, the scale of the bonus was evidently indefensible as it was basedon false fi gures. The fact that the chief executive is refusing to repay the bonus implies a lack of integrity, adding weightto the belief that there may be some underlying dishonesty. Furthermore, although the investors thought it excessive,the case describes this as within the terms of Mr Xu’s contract. A closer scrutiny of remunerations policy (and thereforenon-executive effectiveness) would be appropriate.(b) Absolutist and relativist perspectivesAbsolutism and relativismAn absolutist ethical stance is when it is assumed that there is an unchanging set of ethical principles which should always be obeyed regardless of the situation or any other pressures or factors that may be present. Typically described in universalist ways, absolutist ethics tends to be expressed in terms such as ‘it is always right to ...’, ‘it is never right to ...’ or ‘it is always wrong to ...’Relativist ethical assumptions are those that assume that real ethical situations are more complicated than absolutists allow for.It is the view that there are a variety of acceptable ethical beliefs and practices and that the right and most appropriate belief depends on the situation. The best outcome is arrived at by examining the situation and making ethical assessments based on the best outcomes in that situation.Evaluation of Shazia Lo’s behaviour – absolutist ethicsFirstly, Shazia Lo was correct to be concerned about the over-valuation of contracts at ZPT. As a qualified accountant, she should never be complicit in the knowing mis-statement of accounts or the misrepresentation of contract values. For a qualifi ed accountant bound by very high ethical and professional standards, she was right to be absolutist in her instincts even if not in her eventual behaviour.Secondly, she was also right to raise the issue with the fi nance director. This was her only legitimate course of action in the first instance and it would have been wrong, in an absolutist sense, to remain silent. Given that she was intimidated and threatened upon raising the issue, she was being absolutist in threatening to take the issue to the press (i.e. whistleblowing).It would be incompatible with her status as a professional accountant to be complicit in false accounting as she owed it to the ZPT shareholders, to her professional body and to the general public (the public interest) never to process accounting data she knows to be inaccurate. An effective internal audit process would be a source of information for this action.Evaluation of Shazia Lo’s behaviour – relativist ethicsIt is clear from Shazia Lo’s behaviour that despite having absolutist instincts, other factors caused her to assume a relativist ethic in practice.Her mother’s serious illness was evidently the major factor in overriding her absolutist principles with regard to complicity in the fraudulent accounting fi gures. It is likely she weighed her mother’s painful suffering against the need to be absolutist with regard to the mis-statement of contract values. In relativist situations, it is usually the case that one ‘good’ is weighed against another ‘good’. Clearly it is good (an absolute) to show compassion and sympathy toward her mother but this should not have caused her to accept the payment (effectively a bribe to keep silent). She may have reasoned that the continued suffering of her mother was a worse ethical outcome than the mis-statement of ZPT accounts and the fact that she received no personal income from the money (it all went to support her mother) would suggest that she acted with reasonable motives even though her decision as a professional accountant was defi nitely inappropriate. Given that accepting bribes is a clear breach of professional codes of ethics for accountants and other professionals, there is no legitimate defence of her decision and her behaviour was therefore wrong.(c) (i) Speech on importance of good corporate governance and consequences of failureIntroductionLadies and Gentlemen, I begin my remarks today by noting that we meet at an unfortunate time for business in this country. In the wake of the catastrophic collapse of ZPT, one of the largest telecommunications companies, we have also had to suffer the loss of one of our larger audit fi rms, JJC. This series of events has heightened in all of us an awareness of the vulnerability of business organisations to management incompetence and corruption.The consequences of corporate governance failures at ZPT.I would therefore like to remind you all why corporate governance is important and I will do this by referring to the failuresin this unfortunate case. Corporate governance failures affect many groups and individuals and as legislators, we owe it to all of them to ensure that the highest standards of corporate governance are observed.Firstly and probably most obviously, effective corporate governance protects the value of shareholders’ investment in a company. We should not forget that the majority of shareholders are not ‘fat cats’ who may be able to afford large losses.Rather, they are individual pension fund members, small investors and members of mutual funds. The hard-working voters who save for the future have their efforts undermined by selfi sh and arrogant executives who deplete the value of those investments. This unfairness is allowed to happen because of a lack of regulation of corporate governance in this country.The second group of people to lose out after the collapse of ZPT were the employees. It is no fault of theirs that their directors were so misguided and yet it is they who bear a great deal of the cost. I should stress, of course, that jobs were lost at JJC as well as at ZPT. Unemployment, even when temporary and frictional, is a personal misery for the families affected and it can also increase costs to the taxpayer when state benefi ts are considered.Thirdly, because of the collapse of ZPT, creditors have gone unpaid and customers have remained unserviced. Again, we should not assume that suppliers can afford to lose their receivables in ZPT and for many smaller suppliers, their exposure to ZPT could well threaten their own survival. Where the value of net assets is inadequate to repay the full value of payables, let alone share capital, there has been a failure in company direction and in corporate governance so I hope you will agree with me that effective management and sound corporate governance are vital.The loss of two such important businesses, ZPT and JJC, has caused great disturbance in the telecommunications and audit industries. As JJC lost its legitimacy to provide audit services and its clients moved to other auditors, the structure of the industry changed. Other auditors will eventually be able to absorb the work previously undertaken by JJC but clearly this will cause short-to-medium term capacity issues for those fi rms as they redeploy resources to make good on those new contracts. This was, I should remind you, both unnecessary and entirely avoidable.Linked to this point, I would remind colleagues that it is important for business in general and auditing in particular to be respected in society. The loss of auditors’ reputation caused by these events is very unfortunate as auditing underpinsour collective confi dence in business reporting. It would be wholly inappropriate for other auditors to be affected by thebehaviour of JJC or for businesses in general to be less trusted because of the events at ZPT. I very much hope that suchlosses of reputation and in public confi dence will not occur.Finally, we have all been dismayed by the case of Shazia Lo that was reported in the press. A lack of sound corporategovernance practice places employees such as Ms Lo in impossible positions. Were she to act as whistleblower shewould, by all accounts, have been victimised by her employers. Her acceptance of what was effectively a bribe to remainsilent brings shame both on Ms Lo and on those who offered the money. An effective audit committee at ZPT wouldhave offered a potential outlet for Ms Lo’s concerns and also provided a means of reviewing external audit and otherprofessional services at ZPT. This whole situation could, and would have been, avoided had the directors of ZPT managedthe company under an effective framework of corporate governance.(ii) The case for the mandatory external reporting of internal controls and risksI now turn to the issue of the mandatory external reporting of internal controls and risks. My reason for raising this as anissue is because this was one of the key causes of ZPT’s failure.My fi rst point in this regard is that disclosure allows for accountability. Had investors been aware of the internal controlfailures and business probity risks earlier, it may have been possible to replace the existing board before events deterioratedto the extent that they sadly did. In addition, however, the need to generate a report on internal controls annually will bringvery welcome increased scrutiny from shareholders and others. It is only when things are made more transparent thateffective scrutiny is possible.Secondly, I am fi rmly of the belief that more information on internal controls would enhance shareholder confi dence andsatisfaction. It is vital that investors have confi dence in the internal controls of companies they invest in and increasedknowledge will encourage this. It was, I would remind you, a lack of confi dence in ZPT’s internal controls and the strongsuspicion of fraud that caused the share price to collapse and the company to ultimately fail.Furthermore, compulsory external reporting on internal controls will encourage good practice inside the company. Theknowledge that their work will be externally reported upon and scrutinised by investors will encourage greater rigour inthe IC function and in the audit committee. This will further increase investor confi dence.T o those who might suggest that we should opt for a comply-or-explain approach to this issue, I would argue that thisis simply too important an issue to allow companies to decide for themselves or to interpret non-mandatory guidelines.It must be legislated for because otherwise those with poor internal controls will be able to avoid reporting on them. Byspecifying what should be disclosed on an annual basis, companies will need to make the audit of internal controls anintegral and ongoing part of their operations. It is to the contents of an internal control report that I now turn.Content of external report on internal controls(iii)I am unable, in a speech such as this, to go into the detail of what I would like to see in an external report on internalcontrols, but in common with corporate governance codes elsewhere, there are four broad themes that such a reportshould contain.Firstly, the report should contain a statement of acknowledgement by the board that it is responsible for the company’ssystem of internal control and for reviewing its effectiveness. This might seem obvious but it has been shown to bean important starting point in recogni si ng responsi bi li ty. It is only when the board accepts and acknowledges thisresponsibility that the impetus for the collection of data and the authority for changing internal systems is provided. The‘tone from the top’ is very important in the development of my proposed reporting changes and so this is a very necessarycomponent of the report.Secondly, the report should summarise the processes the board (or where appli cable, through i ts commi ttees) hasapplied in reviewing the effectiveness of the system of internal control. These may or may not satisfy shareholders, ofcourse, and weak systems and processes would be a matter of discussion at AGMs for non-executives to strengthen.reportprovide meaningful, high level information that does not give a misleading impression. Clearly,shouldtheThirdly,internal auditing would greatly increase the reliability of this information but a robust and effective audit committee wouldalso be very helpful.Finally, the report should contain information about any weaknesses in internal control that have resulted in error ormaterial losses. This would have been a highly material disclosure in the case of ZPT and the costs of non-disclosure ofthis was a major cause of the eventual collapse of the companyI very much hope that these brief remarks have been helpful in persuading colleagues to consider the need for increasedcorporate governance legislation. Thank you for listening.[Tutorial note: full speec h not required to gain full professional marks as the question asks for ‘sec tions’ of thespeech.]2 (a) Explain ‘sustainability’ and criticise the fi nance director’s understanding of sustainabilitySustainability is the ability of the business to continue to exist and conduct operations with no effects on the environment that cannot be offset or made good in some other way. The best working defi nition is that given by the Gro Harlem Brundtland, the former Norwegian prime minister in the Brundtland Report (1987) as activity that, ‘meets the needs of the present without compromising the ability of future generations to meet their own needs.’ Importantly, it refers to both the inputs and outputs of any organisational process. Inputs (resources) must only be consumed at a rate at which they can be reproduced, offset or insome other way not irreplaceably depleted. Outputs (such as waste and products) must not pollute the environment at a rate greater than can be cleared or offset. Recycling is one way to reduce the net impact of product impact on the environment. The business activities must take into consideration the carbon emissions, other pollution to water, air and local environment, and should use strategies to neutralise these impacts by engaging in environmental practices that will replenish the used resources and eliminate harmful effects of pollution. A number of reporting frameworks have been developed to help in accounting for sustainability including the notion of triple-bottom-line accounting and the Global Reporting Initiative (GRI). Both of these attempt to measure the social and environmental impacts of a business in addition to its normal accounting.The fi nance director has completely misunderstood the meaning of the term sustainable. He has assumed that it refers to the sustainability of the business as a going concern and not of the business’s place in the environment. Clearly, if a business has lasted 50 years then the business model adopted is able to be sustained over time and a healthy balance sheet enabling future business to take place ensures this. But this has no bearing at all on whether the business’s environmental footprint is sustainable which is what is meant by sustainability in the context of environmental reporting.(b)Stages in an environmental audit and the issues that JGP will have in developing these stagesEnvironmental auditing contains three stages.The first stage is agreei ng and establi shi ng the metri cs involved and deciding on what environmental measures will be included in the audit. This selection is important because it will determine what will be measured against, how costly the audit will be and how likely it is that the company will be criticised for ‘window dressing’ or ‘greenwashing’. JGP needs to decide, for example, whether to include supply chain metrics as Professor Appo suggested, which would be a much more challenging audit. Given that the board’s preference is to be as ‘thorough as possible’, it seems likely that JGP will include a wide range of measures and set relatively ambitious targets against those measures.The second stage is measuring actual performance against the metrics set in the first stage. The means of measurement will usually depend upon the metri c bei ng measured. Whilst many items will be capable of numerical and/or financial measurement (such as energy consumption or waste production), others, such as public perception of employee environmental awareness, will be less so. Given the board’s stated aim of providing a robust audit and its need to demonstrate compliance, this stage is clearly of great importance. If JGP wants to demonstrate compliance, then measures must be established so that compliance against target can be clearly shown. This is likely to favour quantitative measures.The third stage is reporti ng the levels of compli ance or vari ances. The issue here is how to report the i nformati on and how widely to distribute the report. The board’s stated aim is to provide as much information as possible ‘in the interests of transparency’. This would tend to signal the publication of a public document (rather than just a report for the board) although there will be issues on how to produce the report and at what level to structure it. The information demands of local communities and investors may well differ in their appetite for detail and the items being disclosed. Given that it was the desire to issue an environmental report that underpinned the proposed environmental audit, it is likely that JGP will opt for a high level of disclosure to offset the concerns of the local community and the growing number of concerned investors.(c) Defi ne ‘environmental risk’. Distinguish between strategic and operational risks and explain why the environmental risks atJGP are strategicDefi ne environmental riskAn environmental risk is an unrealised loss or liability arising from the effects on an organisation from the natural environment or the actions of that organisation upon the natural environment. Risk can thus arise from natural phenomena affecting the business such as the effects of climate change, adverse weather, resource depletion, and threats to water or energy supplies.Similarly, liabilities can result from emissions, pollution, waste or product liability.Strategic risksThese arise from the overall strategic positioning of the company in its environment. Some strategic positions give rise to greater risk exposures than others. Because strategic issues typically affect the whole of an organisation and not just one or more of its parts, strategic risks can potentially involve very high stakes – they can have very high hazards and high returns. Because of this, they are managed at board level in an organisation and form a key part of strategic management. Examples of strategic risks include those affecting products, markets, reputation, supply chain issues and other factors that can affect strategic positioning. In the case of JGP, reputation risk in particular is likely to be one of the most far-reaching risks, and hence one of the most strategic.Operational risksOperational risks refer to potential losses arising from the normal business operations. Accordingly, they affect the day-to-day running of operations and business systems in contrast to strategic risks that arise from the organisation’s strategic positioning.Operational risks are managed at risk management level (not necessarily board level) and can be managed and mitigated by internal control systems. Examples include those risks that, whilst important and serious, affect one part of the organisation and not the whole, such as machinery breakdown, loss of some types of data, injuries at work and building/estates problems.In the specifi c case of JGP, environmental risks are strategic for the following reasons.First,performanceaffects the way in which the company is viewed by some of its key stakeholders. The case environmentalmentions the local community (that supplies employees and other inputs) and investors. The threat of the withdrawal of support by the local community is clearly a threat capable of affecting the strategic positioning of JGP as its ability to attract a key resource input (labour) would be threatened. In addition, the case mentions that a ‘growing group of investors’ is concerned with environmental behaviour and so this could also have potential market consequences.as a chemical company, Professor Appo said that JGP has a ‘structural environmental risk’ which means that its Second,membership of the chemical industry makes it have a higher level of environmental risk than members of other industries.This is because of the unique nature of chemicals processing which can, as JGP found, have a major impact on one or more stakeholders and threaten a key resource (labour supply). Environmental risk arises from the potential losses from such things as emissions and hazardous leaks, pollution and some resource consumption issues. CEO Keith Miasma referred to this risk in his statement about the threat to JGP’s overall reputation. As a major source of potential reputation risk, environmental risk is usually a strategic risk for a chemical company such as JGP.3 (a) Confl ict of interestConfl ict of interestA confl ict of interest is a situation in which an individual has compromised independence because of another countervailinginterest which may or may not be declared. In the case of non-executive directors, shareholders have the right to expect each NED to act wholly in the shareholders’ interests whilst serving with the company. Any other factors that might challenge this sole fiduciary duty is likely to give rise to a conflict of interest. Does the director pursue policies and actions to benefit the shareholders or to benefi t himself in some other way?Confl icts of interest in the caseJohn has a longstanding and current material business relationship with KK Limited as CEO of its largest supplier. This creates an obvious incentive to infl uence future purchases from Soria Supplies over and above other competitor suppliers, even if the other suppliers are offering more attractive supply contracts as far as KK is concerned. It is in the interests of KK shareholders for inputs to be purchased from whichever supplier is offering the best in terms of quality, price and supply. This may or may not be offered by Soria Supplies. Similarly, a confl ict of interest already exists in that Susan Schwab, KK’s fi nance director, isa NED on the board of Soria Supplies. Soria has a material business relationship with KK and Susan Schwab has a confl ict ofinterest with regard to her duty to the shareholders of KK and the shareholders of Soria Supplies.His appointment, if approved, would create a cross directorship with Susan Schwab. As she was appointed to the board of Soria Supplies, any appointment from Soria’s board to KK’s board would be a cross directorship. Such arrangements have the ability to create a disproportionately close relationship between two people and two companies that may undermine objectivity and impartiality in both cases. In this case, the cross directorship would create too strong a link between one supplier (Soria Supplies) and a buyer (KK) to the detriment of other suppliers and thus potentially lower unit costs.John’s brother-in-law is Ken Kava, the chief executive of KK. Such a close family relationship may result in John supporting Ken when it would be more in the interests of the KK shareholders for John to exercise greater objectivity. There should be no relationships between board members that prevent all directors serving the best interests of shareholders and a family relationship is capable of undermining this objectivity. This is especially important in public listed companies such as KK Limited.(b)Advantages of appointing non-executives to the KK boardThe case discusses a number of issues that were raised as a result of the rapid expansion. An effective NED presence during this period would expect to bring several benefi ts.In the case of KK, the NEDs could provide essential input into two related areas: monitoring the strategies for suitability and for excessive risk. In monitoring the strategies for suitability, NEDs could have an important scrutinising and advising role to fulfi l on the ‘aggressive’ strategies pursued by KK. All strategy selection is a trade off between risk and return and so experience of strategy, especially in risky situations, can be very valuable.monitor the strategies for excessive risk. The strategy role of NEDs is important partly because of increasing alsoNEDscouldthe collective experience of the board to a wide range of risks. With KK pursuing an ‘aggressive’ strategy that involved the ‘increasingly complex operations’, risk monitoring is potentially of great importance for shareholders. There is always a balance between aggression in a growth strategy and caution for the sake of risk management. The fact that some of the other executive directors are both new to the company (resulting from the expansion) and less experienced means, according to the case, that they may be less able and willing to question Mr Kava. Clearly, an effective non-executive presence would be able to bring such scrutiny to the board. They may also place a necessary restraint on the strategic ambitions of Mr Kava.couldprovide expertise on the foreign investments including, in some cases, country-specifi c knowledge. It is careless Theyand irresponsible to make overseas investments based on incomplete intelligence. Experienced NEDs, some of whom may have done business in or with the countries in question, could be very valuable. Experienced NEDs capable of offering specifi c risk advice, possibly through the company’s committee structure (especially the risk committee) would be particularly helpful.Investors are reassured by an effective non-executive presence on a board. The fact that investors have expressed concerns over the strategy and risk makes this factor all the more important in this case. An experienced and effective NED presence would provide shareholders with a higher degree of confi dence in the KK board so that when large overseas investments were made, they would be more assured that such investments were necessary and benefi cial.。

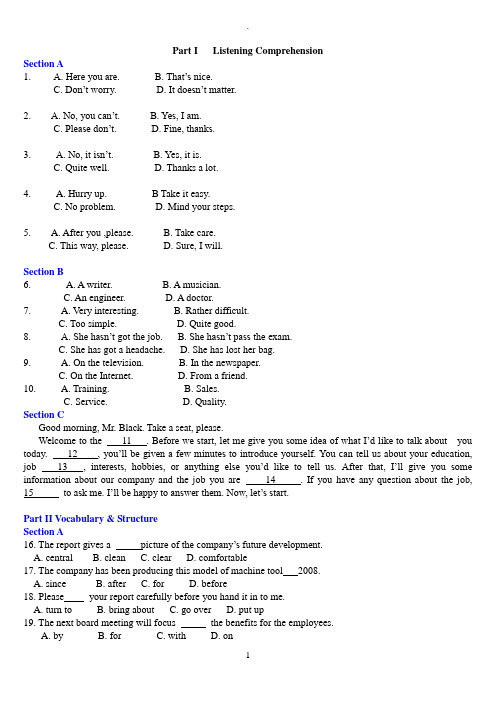

2010年12月高等学校英语应用能力考试B级真题及完整解析

Part I Listening ComprehensionSection A1. A. Here you are. B. That’s nice.C. Don’t worry.D. It doesn’t matter.2. A. No, you can’t. B. Yes, I am.C. Please don’t.D. Fine, thanks.3. A. No, it isn’t. B. Yes, it is.C. Quite well.D. Thanks a lot.4. A. Hurry up. B Take it easy.C. No problem.D. Mind your steps.5. A. After you ,please. B. Take care.C. This way, please.D. Sure, I will.Section B6. A. A writer. B. A musician.C. An engineer.D. A doctor.7. A. Very interesting. B. Rather difficult.C. Too simple.D. Quite good.8. A. She hasn’t got the job. B. She hasn’t pass the exam.C. She has got a headache.D. She has lost her bag.9. A. On the television. B. In the newspaper.C. On the Internet.D. From a friend.10. A. Training. B. Sales.C. Service.D. Quality.Section CGood morning, Mr. Black. Take a seat, please.Welcome to the 11 . Before we start, let me give you some idea of what I’d like to talk about you today. 12 , you’ll be given a few minutes to introduce yourself. You ca n tell us about your education, job 13 , interests, hobbies, or anything else you’d like to tell us. After that, I’ll give you some information about our company and the job you are 14 . If you have any question about the job, 15 to a sk me. I’ll be happy to answer them. Now, let’s start.Part II Vocabulary & StructureSection A16. The report gives a picture of the company’s future development.A. centralB. cleanC. clearD. comfortable17. The company has been producing this model of machine tool 2008.A. sinceB. afterC. forD. before18. Please your report carefully before you hand it in to me.A. turn toB. bring aboutC. go overD. put up19. The next board meeting will focus the benefits for the employees.A. byB. forC. withD. on20. Breakfast can be to you in your room for an additional charge.A. eatenB. servedC. usedD. made21. If more money had been invested, we a factory in Asia.A. will set upB. have set upC. would have set upD. had set up22. Even in small companies, computers are a(n) tool.A. naturalB. essentialC. carefulD. impossible23. We were excited to learn that the last month’s sales by 30%.A. had increasedB. increaseC. are increasingD. have increased24. your name and job title, the business card should also include your telephone number and address.A. As far asB. In addition toC.In spite ofD.As a result of25. Have you read our letter of December 18, in we complained about the quality of your product?A. thatB. whereC. whatD. whichSection B26. Could you tell me the (different) between American and British English in business writing?27. John is the (good) engineer we have ever hired in our department.28. The people there were really friendly and supplied us with a lot of (use) information.29. You’d better (give) me a call before you come to visit us.30. Greenpeace is an international (organize) that works to protect the environment.31. The final decision (make) by the team leader early next week.32. Have you ever noticed any (improve) in the work environment of our factory?33. We can arrange for your car to (repair) within a reasonable period of time.34. It was only yesterday that the chief engineer (email) us the details information about the project.35. We have received your letter of May 10th, (inform) us of the rise of the price.2008年12月说明:假定你是JKM公司的Thomas Black, 刚从巴黎(Paris)出差回来,请给在巴黎的Jane Costa小姐写一封感谢信。

2010年12月份ACCA考试真T(F7)

2010年12月份ACCA(国际注册会计师)考试真题(F7)ALL FIVE questions are compulsory and MUST be attempted1On1June2010,Premier acquired80%of the equity share capital of Sanford.The consideration consisted of two elements:a share exchange of three shares in Premier for every five acquired shares in Sanford and the issue of a$1006%loan note for every50 0shares acquired in Sanford.The share issue has not yet been recorded by Premier,but t he issue of the loan notes has been recorded.At the date of acquisition shares in Premier had a market value of$5each and the shares of Sanford had a stock market price of $3·50each.Below are the summarized draft financial statements of both companies.Statements of comprehensive income for the year ended30September2010Statements of financial position as at30September2010The following information is relevant:(i)At the date of acquisition,the fair values of Sanford‘s assets were equal to their c arrying amounts with the exception of its property.This had a fair value of$1·2million below its carrying amount.This would lead to a reduction of the depreciation charge(in cost of sales)of$50,000in the post-acquisition period.Sanford has not incorporated this value change into its entity financial statements.Premier‘s group policy is to revalue all properties to current value at each year end.On 30September2010,the value of Sanford’s property was unchanged from its value at ac quisition,but the land element of Premier‘s property had increased in value by$500,000 as shown in other comprehensive income.(ii)Sales from Sanford to Premier throughout the year ended30September2010had consistently been$1million per month.Sanford made a mark-up on cost of25%on these sales.Premier had$2million.(at cost to Premier)of inventory that had been supplied i n the post-acquisition period by Sanford as at30September2010.(iii)Premier had a trade payable balance owing to Sanford of$350,000as at30Sep tember2010.This agreed with the corresponding receivable in Sanford‘s books.(iv)Premier‘s investments include some available-for-sale investments that have increas ed in value by$300,000during the year.The other equity reserve relates to these invest ments and is based on their value as at30September2009.There were no acquisitions or disposals of any of these investments during the year ended30September2010.(v)Premier‘s policy is to value the non-controlling interest at fair value at the date of acquisition.For this purpose Sanford’s share price at that date can be deemed to be repr esentative of the fair value of the shares held by the non-controlling interest.(vi)There has been no impairment of consolidated goodwillRequired:(a)Prepare the consolidated statement of comprehensive income for Premier for the y ear ended30September2010.(b)Prepare the consolidated statement of financial position for Premier as at30Septe mber2010.The following mark allocation is provided as guidance for this question:(a)9marks(b)16marks(25marks)2The following trial balance relates to Cavern as at30September2010:The following notes are relevant:(i)Cavern has accounted for a fully subscribed rights issue of equity shares made on 1April2010of one new share for every four in issue at42cents each.The company pa id ordinary dividends of3cents per share on30November2009and5cents per share o n31May2010.The dividend payments are included in administrative expenses in the trial balance.(ii)The8%loan note was issued on1October2008at its nominal(face)value of $30million.The loan note will be redeemed on30September2012at a premium which gives the loan note an effective finance cost of10%per annum.(iii)Non-current assets:Cavern revalues its land and building at the end of each accounting year.At30Septembe r2010the relevant value to be incorporated into the financial statements is$41·8million. The building‘s remaining life at the beginning of the current year(1October2009)was 18years.Cavern does not make an annual transfer from the revaluation reserve to retaine d earnings in respect of the realization of the revaluation surplus.Ignore deferred tax on t he revaluation surplus.Plant and equipment includes an item of plant bought for$10million on1October 2009that will have a10-year life(using straight-line depreciation with no residual value).P roduction using this plant involves toxic chemicals which will cause decontamination costs to be incurred at the end of its life.The present value of these costs using a discount r ate of10%at1October2009was$4million.Cavern has not provided any amount for t his future decontamination cost.All other plant and equipment is depreciated at12·5%per annum using the reducing balance method.No depreciation has yet been charged on any non-current asset for the year ended30 September2010.All depreciation is charged to cost of sales.(iv)The available-for-sale investments held at30September2010had a fair value of $13·5million.There were no acquisitions or disposals of these investments during the yea r ended30September2010.(v)A provision for income tax for the year ended30September2010of$5·6million is required.The balance on current tax represents the under/over provision of the tax lia bility for the year ended30September2009.At30September2010the tax base of Caver n‘s net assets was$15million less than their carrying amounts.The movement on deferre d tax should be taken to the income statement.The income tax rate of Cavern is25%.Required:(a)Prepare the statement of comprehensive income for Cavern for the year ended30 September2010.(b)Prepare the statement of changes in equity for Cavern for the year ended30Septe mber2010.(c)Prepare the statement of financial position of Cavern as at30September2010.Notes to the financial statements are not required.The following mark allocation is provided as guidance for this question:(a)11marks(b)5marks(c)9marks(25marks)3Hardy is a public listed manufacturing company.Its summarized financial statement s for the year ended30September2010(and2009comparatives)are:I n c o m e s t a t e m e n t s f o r t h e y e a r e n d e d30S e p t e m b e r:Statements of financial position as at30September:The following information has been obtained from the Chairman's Statement and the notes to the financial statements:'Market conditions during the year ended30September2010proved very challenging d ue largely to difficulties in the global economy as a result of a sharp recession which has led to steep falls in share prices and property values.Hardy has not been immune from these effects and our properties have suffered impairment losses of$6million in the year.' The excess of these losses over previous surpluses has led to a charge to cost of sal es of$1·5million in addition to the normal depreciation charge.'Our portfolio of investments at fair value through profit or loss has been'marked to market'(fair valued)resulting in a loss of$1·6million(included in administrative expense s).'There were no additions to or disposals of non-current assets during the year.'In response to the downturn the company has unfortunately had to make a number o f employees redundant incurring severance costs of$1·3million(included in cost of sales) and undertaken cost savings in advertising and other administrative expenses.' 'The difficulty in the credit markets has meant that the finance cost of our variable r ate bank loan has increased from4·5%to8%.In order to help cash flows,the company made a rights issue during the year and reduced the dividend per share by50%.' 'Despite the above events and associated costs,the Board believes the company's unde rlying performance has been quite resilient in these difficult times.'Required:Analyze and discuss the financial performance and position of Hardy as portrayed by the above financial statements and the additional information provided.Your analysis should be supported by profitability,liquidity and gearing and other ap propriate ratios(up to10marks available).(25marks)4(a)IAS8Accounting Policies,Changes in Accounting Estimates and Errors contain s guidance on the use of accounting policies and accounting estimates.Required:Explain the basis on which the management of an entity must select its accounting p olicies and distinguish,with an example,between changes in accounting policies and chan ges in accounting estimates.(5marks)(b)The directors of Tunshill are disappointed by the draft profit for the year ended30 September2010.The company's assistant accountant has suggested two areas where she b elieves the reported profit may be improved:(i)A major item of plant that cost$20million to purchase and install on1October2 007is being depreciated on a straight-line basis over a five-year period(assuming no resi dual value).The plant is wearing well and at the beginning of the current year(1October 2009)the production manager believed that the plant was likely to last eight years in total (i.e.from the date of its purchase).The assistant accountant has calculated that,based on a n eight-year life(and no residual value)the accumulated depreciation of the plant at30Sep tember2010would be$7·5million($20million/8years x3).In the financial statements for the year ended30September2009,the accumulated depreciation was$8million($20mil lion/5years x2).Therefore,by adopting an eight-year life,Tunshill can avoid a depreciati on charge in the current year and instead credit$0·5million($8million–$7·5million)to the income statement in the current year to improve the reported profit.(5marks) (ii)Most of Tunshill's competitors value their inventory using the average cost(AVCO) basis,whereas Tunshill uses the first in first out(FIFO)basis.The value of Tunshill's in ventory at30September2010(on the FIFO basis)is$20million;however on the AVCO basis it would be valued at$18million.By adopting the same method(AVCO)as its co mpetitors,the assistant accountant says the company would improve its profit for the year ended30September2010by$2million.Tunshill‘s inventory at30September2009was reported as$15million,however on the AVCO basis it would have been reported as$1 3·4million.(5marks)Required:Comment on the acceptability of the assistant accountant‘s suggestions and quantify h ow they would affect the financial statements if they were implemented under IFRS.Ignor e taxation.Note:the mark allocation is shown against each of the two items above.(15marks)5Manco has been experiencing substantial losses at its furniture making operation wh ich is treated as a separate operating segment.The company‘s year end is30September. At a meeting on1July2010the directors decided to close down the furniture making op eration on31January2011and then dispose of its non-current assets on a piecemeal basis.Affected employees and customers were informed of the decision and a press announce ment was made immediately after the meeting.The directors have obtained the following i nformation in relation to the closure of the operation:(i)On1July2010,the factory had a carrying amount of$3·6million and is expecte d to be sold for net proceeds of$5million.On the same date the plant had a carrying a mount of$2·8million,but it is anticipated that it will only realize net proceeds of$500, 000.(ii)Of the employees affected by the closure,the majority will be made redundant at cost of$750,000,the remainder will be retrained at a cost of$200,000and given work in one of the company's other operations.(iii)Trading losses from1July to30September2010are expected to be$600,000an d from this date to the closure on31January2011a further$1million of trading losses are expected.Required:Explain how the decision to close the furniture making operation should be treated in Manco‘s financial statements for the years ending30September2010and2011.Your an swer should quantify the amounts involved.(10marks)。

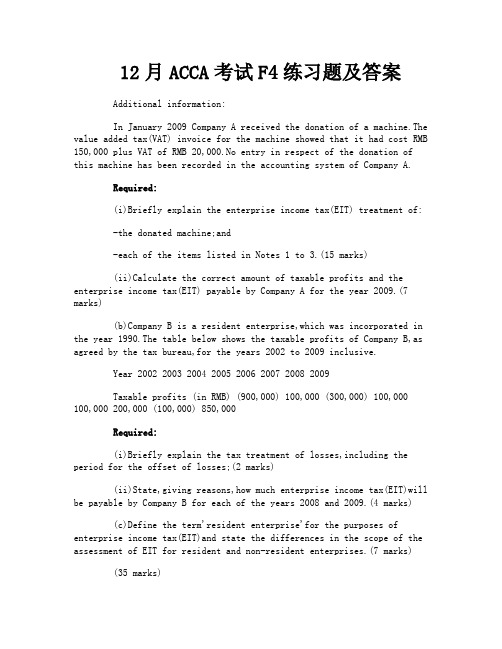

12月ACCA考试F4练习题及答案

12月ACCA考试F4练习题及答案Additional information:In January 2009 Company A received the donation of a machine.The value added tax(VAT) invoice for the machine showed that it had cost RMB 150,000 plus VAT of RMB 20,000.No entry in respect of the donation of this machine has been recorded in the accounting system of Company A.Required:(i)Briefly explain the enterprise income tax(EIT) treatment of:-the donated machine;and-each of the items listed in Notes 1 to 3.(15 marks)(ii)Calculate the correct amount of taxable profits and the enterprise income tax(EIT) payable by Company A for the year 2009.(7 marks)(b)Company B is a resident enterprise,which was incorporated in the year 1990.The table below shows the taxable profits of Company B,as agreed by the tax bureau,for the years 2002 to 2009 inclusive.Year 2002 2003 2004 2005 2006 2007 2008 2009Taxable profits (in RMB) (900,000) 100,000 (300,000) 100,000 100,000 200,000 (100,000) 850,000Required:(i)Briefly explain the tax treatment of losses,including the period for the offset of losses;(2 marks)(ii)State,giving reasons,how much enterprise income tax(EIT)will be payable by Company B for each of the years 2008 and 2009.(4 marks)(c)Define the term'resident enterprise'for the purposes of enterprise income tax(EIT)and state the differences in the scope of the assessment of EIT for resident and non-resident enterprises.(7 marks)(35 marks)2(a)Mr Zhang,a Chinese citizen,is a University professor.He had the following income for the month of January 2009:(1)Monthly employment income of RMB 18,000 and a bonus for the year 2008 of RMB 12,000.(2)Income of RMB 18,000 for publishing a book on 6 January 2009.One of the chapters of the book was published in a magazine as a four-day series commencing on 19 January 2009 for which Mr Zhang received income of RMB 1,000 per day.(3)A net gain of RMB 12,000 from trading in the A-shares market.(4)Income of RMB 4,800 for giving four separate seminars for Enterprise X.(5)A translation fee of RMB 5,200 from a media publisher.(6)Received RMB 300,000 from the sale of the property(50 square metres)that he had lived in for six years.Mr Zhang had acquired the property for RMB 180,000.(7)Gross interest income of RMB 6,000 from a bank deposit.(8)Received RMB 11,000 as insurance compensation.Required:Calculate the individual income tax(IIT)payable(if any)by Mr Zhang on each of his items of income for the month of January2009,clearly identifying any item which is tax exempt.(10 marks)(b)Mr Smith,who is a UK national,is employed by a UK construction company to work in Shanghai on a project that will last for a period of 18 consecutive months.Required:(i)State,giving reasons,whether Mr Smith will be a resident taxpayer or a non-resident taxpayer in the PRC and the scope of his individual income tax(IIT)assessment;(2 marks)(ii)List any THREE fringe benefits that can be provided to Mr Smith that will not be subject to individual income tax(IIT)in China;(3 marks)(iii)Briefly explain the requirements for the reporting and payment of the individual income tax(IIT)due for Mr Smith if he is paid RMB 30,000 per month.(5 marks)。

2010年12月份ACCA考试真T(F7)

2010年12月份ACCA(国际注册会计师)考试真题(F7)ALL FIVE questions are compulsory and MUST be attempted1 On 1 June 2010, Premier acquired 80% of the equity share capital of Sanford. The consideration consisted of two elements: a share exchange of three shares in Premier for every five acquired shares in Sanford and the issue of a $100 6% loan note for every 50 0 shares acquired in Sanford. The share issue has not yet been recorded by Premier, but t he issue of the loan notes has been recorded. At the date of acquisition shares in Premier had a market value of $5 each and the shares of Sanford had a stock market price of $3·50 each. Below are the summarized draft financial statements of both companies.Statements of comprehensive income for the year ended 30 September 2010Statements of financial position as at 30 September 2010The following information is relevant:(i)At the date of acquisition, the fair values of Sanford‘s assets were equal to their c arrying amounts with the exception of its property. This had a fair value of $1·2 million below its carrying amount. This would lead to a reduction of the depreciation charge (in cost of sales) of $50,000 in the post-acquisition period. Sanford has not incorporated this value change into its entity financial statements.Premier‘s group policy is to revalue all properties to current value at each year end.On 30 September 2010, the value of Sanford’s property was unchanged from its value at ac quisition, but the land element of Premier‘s property had increase d in value by $500,000 as shown in other comprehensive income.(ii)Sales from Sanford to Premier throughout the year ended 30 September 2010 had consistently been $1 million per month. Sanford made a mark-up on cost of 25% on these sales. Premier had $2 million. (at cost to Premier) of inventory that had been supplied i n the post-acquisition period by Sanford as at 30 September 2010.(iii)Premier had a trade payable balance owing to Sanford of $350,000 as at 30 Sep tember 2010. This agreed with the corre sponding receivable in Sanford‘s books.(iv)Premier‘s investments include some available-for-sale investments that have increas ed in value by $300, 000 during the year. The other equity reserve relates to these invest ments and is based on their value as at 30 September 2009.There were no acquisitions or disposals of any of these investments during the year ended 30 September 2010.(v)Premier‘s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose Sanf ord’s share price at that date can be deemed to be repr esentative of the fair value of the shares held by the non-controlling interest.(vi)There has been no impairment of consolidated goodwillRequired:(a) Prepare the consolidated statement of comprehensive income for Premier for the y ear ended 30 September 2010.(b) Prepare the consolidated statement of financial position for Premier as at 30 Septe mber 2010. The following mark allocation is provided as guidance for this question:(a) 9 marks(b) 16 marks(25 marks)2 The following trial balance relates to Cavern as at 30 September 2010:The following notes are relevant:(i)Cavern has accounted for a fully subscribed rights issue of equity shares made on1 April 2010 of one new share for every four in issue at 42 cents each. The company pa id ordinary dividends of3 cents per share on 30 November 2009 and 5 cents per share o n 31 May 2010.The dividend payments are included in administrative expenses in the trial balance.(ii)The 8% loan note was issued on 1 October 2008 at its nominal (face) value of $30 million. The loan note will be redeemed on 30 September 2012 at a premium which gives the loan note an effective finance cost of 10% per annum.(iii)Non-current assets:Cavern revalues its land and building at the end of each accounting year. At 30 Septembe r 2010 the relevant value to be incorporated into the financial statements is $41·8 million. The building‘s remaining life at the beginning of the current year (1 October 2009) was18 years. Cavern does not make an annual transfer from the revaluation reserve to retained earnings in respect of the realization of the revaluation surplus. Ignore deferred tax on t he revaluation surplus.Plant and equipment includes an item of plant bought for $10 million on 1 October 2009 that will have a 10-year life(using straight-line depreciation with no residual value).P roduction using this plant involves toxic chemicals which will cause decontamination costs to be incurred at the end of its life. The present value of these costs using a discount r ate of 10% at 1 October 2009 was $4 million. Cavern has not provided any amount for t his future decontamination cost. All other plant and equipment is depreciated at 12·5% per annum using the reducing balance method.No depreciation has yet been charged on any non-current asset for the year ended 30 September 2010.All depreciation is charged to cost of sales.(iv)The available-for-sale investments held at 30 September 2010 had a fair value of $13·5 million. There were no acquisitions or disposals of these investments during the yea r ended 30 September 2010.(v)A provision for income tax for the year ended 30 September 2010 of $5·6 million is required. The balance on current tax represents the under/over provision of the tax lia bility for the year ended 30 September 2009.At 30 September 2010 the tax base of Caver n‘s net assets was $15 million less than their carrying amounts. Th e movement on deferre d tax should be taken to the income statement. The income tax rate of Cavern is 25%.Required:(a)Prepare the statement of comprehensive income for Cavern for the year ended 30 September 2010.(b)Prepare the statement of changes in equity for Cavern for the year ended 30 Septe mber 2010.(c)Prepare the statement of financial position of Cavern as at 30 September 2010.Notes to the financial statements are not required.The following mark allocation is provided as guidance for this question:(a) 11 marks(b) 5 marks(c) 9 marks(25 marks)3 Hardy is a public listed manufacturing company. Its summarized financial statement s for the year ended 30 September 2010(and 2009 comparatives) are:I n c o m e s t a t e m e n t s f o r t h e y e a r e n d e d30S e p t e m b e r:Statements of financial position as at 30 September:The following information has been obtained from the Chairman's Statement and the notes to the financial statements:'Market conditions during the year ended 30 September 2010 proved very challenging d ue largely to difficulties in the global economy as a result of a sharp recession which has led to steep falls in share prices and property values. Hardy has not been immune from these effects and our properties have suffered impairment losses of $6 million in the year.' The excess of these losses over previous surpluses has led to a charge to cost of sal es of $1·5 million in addition to the normal depreciation charge.'Our portfolio of investments at fair value through profit or loss has been 'marked to market' (fair valued) resulting in a loss of $1·6 million (included in administrative expense s).'There were no additions to or disposals of non-current assets during the year.'In response to the downturn the company has unfortunately had to make a number o f employees redundant incurring severance costs of $1·3million (included in cost of sales) and undertaken cost savings in advertising and other administrative expenses.' 'The difficulty in the credit markets has meant that the finance cost of our variable r ate bank loan has increased from 4·5% to 8%.In order to help cash flows ,the company made a rights issue during the year and reduced the dividend per share by 50%.' 'Despite the above events and associated costs, the Board believes the company's unde rlying performance has been quite resilient in these difficult times.'Required:Analyze and discuss the financial performance and position of Hardy as portrayed by the above financial statements and the additional information provided.Your analysis should be supported by profitability, liquidity and gearing and other ap propriate ratios (up to 10 marks available).(25 marks)4 (a) IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors contain s guidance on the use of accounting policies and accounting estimates.Required:Explain the basis on which the management of an entity must select its accounting p olicies and distinguish, with an example, between changes in accounting policies and chan ges in accounting estimates. (5 marks)(b)The directors of Tunshill are disappointed by the draft profit for the year ended 30 September 2010.The company's assistant accountant has suggested two areas where she b elieves the reported profit may be improved:(i)A major item of plant that cost $20 million to purchase and install on 1 October 2 007 is being depreciated on a straight-line basis over a five-year period (assuming no resi dual value).The plant is wearing well and at the beginning of the current year(1 October 2009)the production manager believed that the plant was likely to last eight years in total (i.e. from the date of its purchase).The assistant accountant has calculated that, based on a n eight-year life(and no residual value)the accumulated depreciation of the plant at 30 Sep tember 2010 would be $7·5 million($20 million/8 years x 3).In the financial statements forthe year ended 30 September 2009,the accumulated depreciation was $8 million ($20 mill ion/5 years x 2).Therefore, by adopting an eight-year life, Tunshill can avoid a depreciatio n charge in the current year and instead credit $0·5 million($8 million –$7·5 million)to t he income statement in the current year to improve the reported profit.(5 marks) (ii)Most of Tunshill's competitors value their inventory using the average cost (AVCO) basis, whereas Tunshill uses the first in first out (FIFO) basis. The value of Tunshill's in ventory at 30 September 2010(on the FIFO basis) is $20 million; however on the AVCO basis it would be valued at $18 million. By adopting the same method (AVCO) as its co mpetitors, the assistant accountant says the company would improve its profit for the year ended 30 September 2010 by $2 million. Tunshill‘s inventory at 30 September 2009 was reported as $15 million, however on the AVCO basis it would have been reported as $1 3·4 million. (5 marks)Required:Comment on the acceptability of the assistant accountant‘s suggestions and quantify h ow they would affect the financial statements if they were implemented under IFRS. Ignor e taxation.Note: the mark allocation is shown against each of the two items above.(15 marks)5 Manco has been experiencing substantial losses at its furniture making operation wh ich is treated as a separate operating segment. The company‘s year end is 30 September . At a meeting on 1 July 2010 the directors decided to close down the furniture making op eration on 31 January 2011 and then dispose of its non-current assets on a piecemeal basis. Affected employees and customers were informed of the decision and a press announce ment was made immediately after the meeting. The directors have obtained the following i nformation in relation to the closure of the operation:(i)On 1 July 2010, the factory had a carrying amount of $3·6 million and is expected to be sold for net proceeds of $5 million. On the same date the plant had a carrying a mount of $2·8 million, but it is anticipated that it will only realize net proceeds of $500, 000.(ii)Of the employees affected by the closure, the majority will be made redundant at cost of $750,000,the remainder will be retrained at a cost of $200,000 and given work in one of the company's other operations.(iii)Trading losses from 1 July to 30 September 2010 are expected to be $600,000 an d from this date to the closure on 31 January 2011 a further $1 million of trading losses are expected.Required:Explain how the decision to close the furniture making operation should be treated in Manco‘s financial statements for the years ending 30 September 2010 and 2011. Your an swer should quantify the amounts involved. (10 marks)。

ACCA考试F4公司法与商法China真题2010年12月_真题-无答案

ACCA考试F4公司法与商法(China)真题2010年12月(总分100,考试时间180分钟)ALL TEN questions **pulsory and MUST be attempted** relation to the Civil Procedure Law of China:(a) explain the term exclusive jurisdiction; (2 marks)(b) state the major legal characteristics of exclusive jurisdiction, in terms of: (i) the basis of exclusive jurisdiction; and (4 marks) (ii) the effect of the rule of exclusive jurisdiction. (4 marks)** relation to the Property Law of China:(a) explain the term right of lien; (4 marks)(b) state THREE conditions to be met for a party to claim the right of lien. (6 marks)** relation to the Labour Contract Law of China:(a) state the various powers of the labour administration in exercising its supervisory and examining functions; (2 marks)(b) state any FOUR kinds of situations under which the labour administration may issue administrative orders to an employer for violations of Labour Contract Law. (8 marks)** relation to the Contract Law of China:(a) explain the term termination of contract; (2 marks)(b) explain and distinguish between termination of contract and dissolution of contract. (8 marks)** relation to the Company Law of China:(a) state the basic rules regarding the shareholders of: (i) a general limited **pany; (2 marks) (ii) a sole-person limited **pany and a wholly state-**pany; and (2 marks) (b) state the requirements for capital of: (i) a general limited **pany; (2 marks) (ii) a sole-person limited **pany; and (2 marks) (iii) a company with exclusive state-ownership. (2 marks)** relation to the Enterprises Bankruptcy Law of China, state the legal effect of the acceptance of an application for bankruptcy by the court:(a) in terms of the preservative measures against the assets of the debtor; (4 marks)(b) in terms of the enforcement procedure against the relevant debtor; (4 marks)(c) in terms of pending legal actions against a debtor. (2 marks)** relation to the Securities Law of China:(a) explain the term sponsor in underwriting securities; (2 marks)(b) state the objective of the legislation to set up the system of sponsorship in underwriting securities; (2 marks)(c) state the various legal liabilities of a sponsor, in providing professional services, for his wrongdoings or failure to perform his functions. (6 marks)8.In 2009 Mr Lee and the **mittee entered into a contract for the management of land, under which he obtained the right to manage the contracted piece of land in a small mountain for 30 years. The contract was duly registered with the relevant government authority in light of the Property Law.One day when Mr Lee was planting trees on the mountain, he accidentally found a small coal mine in the mountain. Having discovered this information many villagers rushed to the mountain to exploit coal for sale. Mr Lee demanded the villagers stop the exploitation of coal, on the ground that he has been a legitimate holder of the right of management of land. Therefore, he should be a lawful holder of right to the coal mine under the land. On the other hand, the villagers refused to accept Mr Lee’s position and insisted that Mr Lee’s right to management of land would not extend to natural resources under the land. They held that the coal mine should be **mon property of the villagers as a whole and they were entitled to dig coal.Since Mr Lee and the villagers could not reach a settlement themselves, they filed a lawsuit against each other before the court for the determination of right.Required:Answer the following questions in accordance with the relevant provisions of the Property Law of China, and give reasons for your answer:(a) describe what kind of property right Mr Lee has held regarding the mountain; (2 marks)(b) describe who should hold the ownership of the coal mine in the mountain; (4 marks)(c) state how the court should deal with the claim brought by Mr Lee for damages against villagers because some of the trees in the land were destroyed by villagers in digging coal. (4 marks)9.Natural Gas Company (Gas Company) and Yaowa Glass Company (Yaowa Company) entered into a supply contract. The major terms and conditions of the contract were that Gas Company would provide a minimum 4,000 of natural gas daily for a period of five years at a fixed price; it should give a written notice five days in advance where it reduces the quantity of supply; Yaowa Company would provide a sum of RMB 100,000 yuan as a deposit for the performance of the contract. Yaowa Company paid the deposit pursuant to the supply contract upon the conclusion of the contract.Gas Company has been in decline since the beginning of 2010. In order to achieve extra profit, Gas Company sold more natural gas to other customers at a higher price by reducing the quantity of supply to Yaowa Company. One day Gas Company suddenly stopped providing natural gas to Yaowa Company without a notice in advance, which resulted in serious damage to the equipment of the latter.Due to unsuccessful negotiation between the two parties, Yaowa Company intended to seek the assistance from the people’s court.Required:Answer the following questions in accordance with the relevant provisions of the Contract Law of China, and give your reasons for your answer:(a) explain the legal nature of the deposit under the contract law, and state whether a claim for a refund of twice the amount of the deposit should be supported by the court; (4 marks) (b) state whether a claim requiring specific performance of contract by Gas Company should be supported by the court where the Yaowa Company has already requested a refund of twice the amount of the deposit. (6 marks)10.Kingmart Joint Stock Company (Kingmart Company) was a listed joint **pany listing in Shanghai Securities Exchange, with total assets of RMB 500 million yuan; while Dahua LimitedLiability Company’s (Dahua Company) registered capital was RMB 160 million yuan. At the end of 2009 the board of directors of Kingmart Company adopted a special board of directors’ resolution to merge with Dahua Company in a form of merger by absorption. After **pletion of the merger plan Dahua Company would be dissolved.For the purpose of carrying forward the merger plan, Kingmart Company and Dahua Company should take some procedural steps before the merger plan could be implemented and settle the credit and/or debt of these **panies with other parties.Required:Answer the following questions in accordance with the relevant provisions of the Company Law, and give reasons for your answer:(a) state the relevant voting requirement by the general shareholders’ meeting; (3 marks)(b) state the relevant rules with respect to public notice; (3 marks)(c) state how to deal with Dahua Company’s debts of RMB 500,000 yuan owed to a local electricity plant. (4 marks)。

2010年ACCAP1-P3真题答案