上海交大国际投资作业

北外1603奥鹏远程教育---国际投资--- 参考答案

第一单元单选题1 今年来,国际投资发展最快的产业部门是( ))A. 第一产业B. 第二产业C. 第三产业D. 制造业 2 1914年以前,在全球投资中最大输出国是(A. 美国B. 法国C. 德国D. 英国3 总体来看,自20世纪80年代后半期以来,制造业在国际直接投资行业格局中的地位()A. 下降了B. 提高了C. 未发生显著变化D. 一会高一会低4 ( )是国际直接投资的主体A. 跨国公司B. 跨国金融机构C. 官方与半官方机构D. 个人投资者5 国际投资的根本目的是( )A. 政治利益B. 经济利益C. 实现价值增值D. 长期的战略性目标6 国际货币基金组织认为,视为对企业实施有效控制的股权比例一般是( )A. 10%B. 25%C. 35%D. 50%7 ( )是当今发展中国家中吸引外资最多的国家。

A. 中国B. 巴西C. 泰国D. 南非8 区分国际直接投资和国际间接投资的根本原则是( )A. 股权比例B. 有效控制C. 持久利益D. 战略关系9 根据投资主体类型,国际投资可分为( )A. 实物资产投资和无形资产投资B. 官方投资和半官方投资C. 对外投资和对内投资1 0 二次世界大战前,国际投资是以()为主A. 证券投资B. 实业投资C. 直接投资D. 私人投资 第一单元判断题1 国际投资一般而言较国内投资风险更大。

√2 统计表明,国际直接投资较国际间接投资波动性更大。

国际投资的发展对世界经济的影响有百利而无一害。

×3 ×4 近年来,发展中国家在吸收FDI 方面已超过发达国家,占据主要地位。

近年来,国际投资的发展很大程度上得益于政策的日益自由化。

中国援非建设不属于国际投资。

×5 √6 ×7 大三角地区是指:美国、北约、日本。

×8 自20世纪80年代后半期以来,初级产品部门在国际直接投资行业格局中的地位未发生显著变化。

无形资产包括生产诀窍、管理技术、厂房、商标专利等。

2022年上海交通大学专业课《金融学》科目期末试卷A(有答案)

2022年上海交通大学专业课《金融学》科目期末试卷A(有答案)一、选择题1、一国物价水平普遍上升,将会导致国际收支,该国的货币汇率。

()A.顺差:上升B.顺差;下降C.逆差;上升D.逆差;下降2、假设一张票据面额为80000元,90天到期,月贴现率为5%。

,则该张票据的实付贴现额为()A.68000B.78000C.78800D.800003、某公司以延期付款方式销售给某商场一批商品,该商场到期偿还欠款时,货币执行的是()职能。

A.流通手段B.支付手段C.购买手段D.贮藏手段4、中央银行进行公开市场业务操作的工具主要是()。

A.大额可转让存款单B.银行承兑汇票C.金融债券D.国库券5、下列不属于长期融资工具的是()。

A.公司债券B.政府债券C.股票D.银行票据6、10.如果复利的计息次数增加,则现值()A.不变B.增大C.减小D.不确定7、期权的最大特征是()。

A.风险与收益的对称性B.期权的卖方有执行或放弃执行期权的选择权C.风险与收益的不对称性D.必须每日计算益亏,到期之前会发生现金流动8、剑桥方程式重视的是货币的()。

A.媒介功能B.交易功能C.避险功能D.资产功能9、10.如果复利的计息次数增加,则现值()A.不变B.增大C.减小D.不确定10、以下的金融资产中不具有与期权类似的特征的是()。

A.可转债B.信用期权C.可召回债券D. 期货11、L公司刚支付了2.25元的股利,并预计股利会以5%每年的速度增长,该公司的风险水平对应的折现率为11%,该公司的股价应与以下哪个数值最接近?()A.20.45元B.21.48元C.37.50元D.39.38元12、下列属于直接金融工具的是()。

A.企业债券B.银行债券C.银行抵押贷款D.大额可转让定期存单13、公司将一张面额为10000元,3个月后到期的商业票据变现,若银行年贴现率为5%,应付金额为()。

A.125B.150C.9875D.980014、()最能体现中央银行是“银行的银行”。

《投资学》第三次作业及答案

《投资学》第三次作业1单选题1. 以下哪种方法可以改进有效投资边界(efficient frontier )?A. 增大投资的额度B. 降低投资的额度C. 不允许卖空D. 增加投资组合中股票的数量解答:D2. 下面哪种最可能是系统性风险(systematic risk )?(Berk ,第10章26题)A. 工厂因为台风而关闭的风险B. 经济下滑,对产品需求减少的风险C. 最好的雇员被挖走的风险D. 研发部门研发的新技术无法产品化的风险解答:B3. 下面哪个企业的beta 可能是最大的?A. 新东方B. 同仁堂C. 百度D. 中石油解答: 百度,高科技企业4. 假设市场风险溢价(market risk premium )为6.5%,无风险利率为5%,某投资项目的beta 为1.2,则投资该项目的资本成本(cost of capital )为(Berk ,第10章37题):A. 6.5%B. 12.8%C. 6.8%D. 7.8%解答:资本成本=([])12.8%f m f r E R r β+-=5. 假设你持有的风险资产(risky asset )和无风险资产的比例为7:3,风险资产的预期回报率为10%,标准差为20%,无风险资产的收益率为5%,则你所持有的资产组合收益率的标准差为多少?A. 20%B. 14%C. 6%D. 2%解答:BSD[R ]()0.720%14%xP P xSD R ==⨯=6. 如果投资者现在的资产全部由a 股票组成,并且只被允许选取另外一种股票组成资产组合,投资者将会选择哪种股票?已知每种股票的期望收益率均为8%,标准差为20%,corr(a,b)=0.85; corr(a,c)=0.60; corr(a,d)=0.45。

(Bodie ,第8章18题)A. bB. cC. dD. 需要更多信息解答:C7. 按照CAPM 模型,假定市场预期收益率=15%,无风险利率=8%,证券A 的预期收益率=17%,A 的beta 为1.25,则以下哪种说法是正确的?(注:阿尔法值指超额收益率)(Bodie ,第9章22题)A. 证券A 被高估1 参考书为Berk 英文第三版,Bodie 中文第八版B. 证券A是公平定价C. 证券A的阿尔法值为-0.25%D. 证券A的阿尔法值为0.25%解答:D。

上交大《物流案例与实践》教学资料包 课后习题答案 第十一章

第十一章物流企业课后习题答案要点案例一上海百大配送的物流末端服务案例(1)上海百大公司采取了哪些具体措施构建配送的网络体系?上海百大配送服务网络基本思路是:组织具有实战经验的专家队伍进行市场策划和开发;在全国主要大中城市设点布局并通过现代通讯和电脑技术组成网络;在市区内建立一系列属地配送点,用网络连接,当消费者通过电话、互联网、传真等形式提出服务请求时,由调度中心调度,配送点送货(服务)上门。

具体的做法有:①变传统的坐商为行商,缩短厂商和最终消费者的时空距离。

直投配送行业是为生产厂商和最终消费者提供信息平台和物流沟通渠道。

它可将大型配送中心及量贩店的货物送到百姓家中,也可直接为品牌商提供现成的市场营销网络。

②紧随高新技术发展,市场潜力具大。

直投配送亦为在世界范围内急剧发展的电子商务(电话、网上购物)做下游服务,解决其送货和结算问题。

③创造大量就业机会,降低人工成本。

④与现代信息技术紧密结合,节约时间和人工费用并降低管理成本。

上海百大配送通过与国家重点实验室的合作,设计开发出一套信息平台软件,可以大大缩短信息传输时间,提高自动化水平,减少管理层次,提高工作效率和降低差错率。

(2)上海百大配送的网络运作方式有何特点,并取得了哪些成效?上海百大配送直投配送网络是通过五个方面来运作的。

①做好基础管理工作。

上海百大配送在信息平台技术、管理技术、资金筹措,特别是干部队伍的培养等方面做了大量工作,积累了成功经验。

公司在不断探索以现代企业制度为核心的科学的法人治理结构和管理结构,一方面通过经营班子年薪制和期权制来吸引和稳定高级管理人才;另一方面,通过运用现代企业管理方法来强化企业的基础管理。

②积极向外扩展。

除了以昆明为发展基地建点运作外,上海百大配送首先抢滩上海,收购了上海特能市场推广有限公司,开创了云南企业收购上海企业的先河。

③发挥购并优势,进行低成本扩张。

上海百大配送的控股公司利用其丰富的人才资源和昆明百大的支持,成功地运作了原昆明自行车总厂的破产企业收购,积累了相当丰富的经验,特别是在下岗职工妥善安置、土地重组变现、国内过剩设备境外投资及企业产权重组、机制更新等方面形成了一套完整的资产重组模式和能力。

上海交大网络 《外贸函电》复习 整理版

Review For Final ExamI Multiple Choices1. If your samples meet our requirement, we will ___B_____ a large order. immediately.a. place youb. send youc. make youd. expect you2. Although we are ___A____ to open up business with you, we regret that it is impossible for us to all the reductionasked for, because we have already cut our price to the lowest point after closely examining our cost _______.a. anxious / calculationsb. desire / considerationc. wishing / evaluationd. longing / reduction3. With a view to supporting your sales we have specially prepared some samples of our new ___B_____ and aresending them to you under _______ cover.a. models / the sameb. designs / separatec. styles / anotherd. makes / other4. As __B_____ by you some time ago, we take pleasure in making you the following offer, which is _______ to youracceptance within seven days.a. requesting / dueb. requested / subjectc. your request / subjectedd. requests / valid5. ___D____ to this letter you will find our _______ in triplicate for jackets.a. Subject / sample invoiceb. Enclosed / bona fide holdersc. Applied / entrustmentd. Attached / proforma invoice6. The shipment _C______by your Credit No. 388 has been ready for some time, but the amendment to the _______credit has not yet reached us.a. mentioned / lastb. relevant / coveringc. covered / relevantd. covering / relevant7. In __A______ with your request, we will make an exception to our rules and accept delivery against D/P at sight.a. complianceb. accordancec. arrangementd. correspondence8. ___D___ you will find a cheque covering all commission due to you to _______.a. Attached / mentionb. Enclose / todayc. Enclosing with / updated. Enclosed / date9. It is not our intention to rush you into a decision, ,but as this article is in great __D_____, we would advise you_______ yourselves of our offer in your own interest.a. quantity / captureb. demand / makec. popularity / supplyd. demand / avail10. As a special sign of encouragement, we shall consider accepting payment By D/P. We trust this will greatly____D____ your efforts in pushing the sales of our products.a. expediteb. confirmc. amendd. facilitate11. Goods under your Order 690 are ready for __D_____. Unfortunately, we have not yet received your packing _______.Please also inform us of your shipping _______.a. instructions / marksb. requirements / transactionc. consignment / dated. dispatch /instructions/ marks12. We feel you may be interested in some of our other products and enclose some ___C____ booklets and a supply ofsales ________ for use with your customers.a. well-illustrating / informationb. excessive / promotionc. descriptive / literature\d. detailed / statements13. As soon as we receive your reply ____B______, we shall confirm supply of the goods at the prices stated in yourletter.a. in the positionb. in the affirmative\c. in the presentationd. in the establishment14. Our terms of payment are by confirmed, ___C____ letter of credit in our _________, available by draft at sight,reaching us one month ________ shipment.a. irrevocable / time / beforeb. acknowledgeable / bank / prior toc. irrevocable / favor / ahead of\d. revocable / notification / in advance15. We wish to point out that the ___D____ in the credit strictly conform to the terms stated in our S/C No. 655 in order toavoid _______ amendment.a. condition / lateb. provisions / consequentc. clauses / laterd. stipulations / subsequent\16. We are ___A____ your letter 26 June and have ______ acted on your instruction.a. in receipt of / duly\b. acknowledgement of / immediatelyc. in priority of / quicklyd. in arrangement of / considerabl17. We are airmailing you our S/C No. 080624 in ___B____, a copy of which is to be _______and returned to us for ourrecords.a. writing / leftb. duplicate / countersigned\c. copies / namedd. ;attest version / printed18. You will understand that the ___D____ of one of our standard sizes to your specifications means a _______adjustment of our production methods.a. change / quiteb. changed / difficultc. altering / considerabled. alteration / substantial \19. It seems clear that there is a good demand for your electronic products and as we believe you are not directly__B_____ in this area, we are writing to offer our service as your _____ agent.a. selling / exclusiveb. represented / sole \c. connected / generald. established / chief20. D/P calls for __A_____ payment against _______ of shipping documents.a. actual / transfer\b. immediate / handing inc. prompt / negotiationd. delayed / presentation21. The L/C will stay valid for at least 15 days beyond the ___C___ date of shipment.a. compliedb. conformedc. promised \d. authorized22. Please ___C____ shipment until you receive our further instructions.a. consignb. extendc. defer\d. compel23. We wish to advise you that the goods went ___A____ on the steamer “Yunnan” on August 8. They are to be _______at Copenhagen and are expected to reach your port in early September.a. forward / transshipped\b. out / dischargedc. westward / reloadedd. off / transshipping24. As ___C____ payments, we cannot do _______ than L/C at sight.a. concerns / moreb. to / lessc. regards / otherwise\d. for / rather25. Instead of __A_____”Manhattan Maru” as ______ advised, you are now required to ship the goods of this order onthe steam er “Calchas”.a. s. s. /previously \b. by the Boat / youc. on Ship / usuallyd. Steamer / we wereII. Questions about concepts (选择题型)1. Agency(1) Why shall a seller appoint an agent in a foreign country to which the goods are to be exported?KEY: An important reason for appointing an agent in a foreign country to which the goods are to be exported is that the agent knows the local condition and the local market. He also knows what goods are best suited to his area and what prices the market will bear.2. Insurance(1) How is the insurance value calculated?KEY: The insurance value is calculated as:cost of goods + amount of freight + insurance premium + a percentage of profit on the sale of goods(2) As far as foreign trade is concerned, what risks are covered under an insurance policy?KEY: So far as foreign trade is concerned the following three risks are covered under an insurance policy, namely, FPA, WPA and All Risks.3. Payment(1) What is the advantage of payment by L/C?KEY: Letter of credit is a reliable and safe method of payment, facilitating trade with unknown buyers and giving protection to both sellers and buyers.(2) Under what circumstances shall a seller agree to payment by D/A?KEY: Payment by D/A is accepted only when the financial standing of the importer is sound or where a previous course of business has inspired the exported to believe that the importer will be good for payment.4. Quotation, Offer and Counter-offer(1) What is to be included in a satisfactory quotation?KEY: A satisfactory quotation should include the following:(1) An expression of thanks for the enquiry.(2) Details of prices, discounts and terms of payment.(3) A statement of clear indication of what the prices cover ()e.g.: freight and insurance, etc.)(4) An undertaking as to date of delivery or time of shipment.(5) The period for which the quotation is valid.5. Shipment(1) What are the characteristics of liners shipping?KEY: Characteristics of Liner Shipping :(1) The liner has regular line, ports, sailing schedule and relatively fixed freight.(2) It is suitable for cargoes of small quantity(3) Loading and unloading charges are included in the freight.(4) Liner shipping is irrespective of demurrage and dispatch money.(5) It provides good service and simple procedures.6. Packing(1) Why does packing need more care in export trade than in homeKEY: Because export goods usually have to go a long way to reach the destination and sometimes have to go through the ordeal of transport, such as the roughest journey. If export goods are not packed in stronger and tight containers, they will reach the buyer either damaged or part missing.III Terms♦合法持证人bona fide holder ♦标签价格tag prices♦物权票据title documents ♦(汇票等)期限tenor♦委托人principal♦进款proceeds ♦大路货FAQ (Fair Average Quality) ♦循环信用证revolving L/C♦打包贷款packing loan♦通风集装箱ventilated container♦海上费用Marine Charges♦会签countersign♦偷窃、提货不着险TPND (Theft, Pilferage & Non-delivery)♦租船合同charter party♦包干运费lump sum freight♦独家代理sole agent / exclusive agent ♦成本加运费价CFR♦标签价tag price♦时价prevailing prices ♦救助费用Salvage charges ♦有利可图的价格remunerative priceIV Sentence Translation: (英汉互译)1. 我们愿意担任你们现行出口商品的代理,因为我们拥有一个广阔的国内市场。

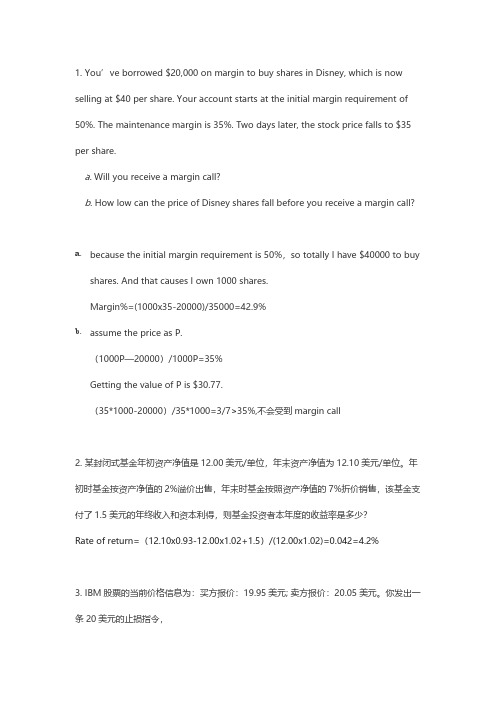

投资学作业(英文版)

1. You’ve borrowed $20,000 on margin to buy shares in Disney, which is now selling at $40 per share. Your account starts at the initial margin requirement of 50%. The maintenance margin is 35%. Two days later, the stock price falls to $35 per share.a. Will you receive a margin call?b. How low can the price of Disney shares fall before you receive a margin call?a.because the initial margin requirement is 50%,so totally I have $40000 to buyshares. And that causes I own 1000 shares.Margin%=(1000x35-20000)/35000=42.9%b.assume the price as P.(1000P—20000)/1000P=35%Getting the value of P is $30.77.(35*1000-20000)/35*1000=3/7>35%,不会受到margin call2. 某封闭式基金年初资产净值是12.00美元/单位,年末资产净值为12.10美元/单位。

年初时基金按资产净值的2%溢价出售,年末时基金按照资产净值的7%折价销售,该基金支付了1.5美元的年终收入和资本利得,则基金投资者本年度的收益率是多少?Rate of return=(12.10x0.93-12.00x1.02+1.5)/(12.00x1.02)=0.042=4.2%3. IBM股票的当前价格信息为:买方报价:19.95美元; 卖方报价:20.05美元。

国际投资学教程课后题答案(完整版)-图文

国际投资学教程课后题答案(完整版)-图文第一章1.名词解释:国际投资:是指以资本增值和生产力提高为目标的国际资本流动,是投资者将其资本投入国外进行的一阴历为目的的经济活动。

国际公共(官方)投资:是指一国政府或国际经济组织为了社会公共利益而进行的投资,一般带有国际援助的性质。

国际私人投资:是指私人或私人企业以营利为目的而进行的投资。

短期投资:按国际收支统计分类,一年以内的债权被称为短期投资。

长期投资:一年以上的债权、股票以及实物资产被称为长期投资。

产业安全:可以分为宏观和中观两个层次。

宏观层次的产业安全,是指一国制度安排能够导致较合理的市场结构及市场行为,经济保持活力,在开放竞争中本国重要产业具有竞争力,多数产业能够沈村冰持续发展。

中观层次上的产业安全,是指本国国民所控制的企业达到生存规模,具有持续发展的能力及较大的产业影响力,在开放竞争中具有一定优势。

资本形成规模:是指一个经济落后的国家或地区如何筹集足够的、实现经济起飞和现代化的初始资本。

2、简述20世纪70年代以来国际投资的发展出现了哪些新特点?(二)投资格局,1.“大三角”国家对外投资集聚化2.发达国家之间的相互投资不断增加3.发展中国家在吸引外资的同时,也走上了对外投资的舞台(三)投资方式,国际投资的发展出现了直接投资与间接投资齐头并进的发展局面。

(四)投资行业,第二次世界大战后,国际直接投资的行业重点进一步转向第二产业。

3.如何看待麦克杜格尔模型的基本理念?麦克杜格尔模型是麦克杜格尔在1960年提出来,后经肯普发展,用于分析国际资本流动的一般理论模型,其分析的是国际资本流动对资本输出国、资本输入国及整个世界生产和国民收入分配的影响。

麦克杜格尔和肯普认为,国际间不存在限制资本流动的因素,资本可以自由地从资本要素丰富的国家流向资本要素短缺的国家。

资本流动的原因在于前者的资本价格低于后者。

资本国际流动的结果将通过资本存量的调整使各国资本价格趋于均等,从而提高世界资源的利用率,增加世界各国的总产量和各国的福利。

国际金融学汇率专题计算题(含作业答案)

国际金融学汇率专题计算题(含作业答案)《国际金融学》第五章课堂练习及作业题一、课堂练习(一)交叉汇率的计算 1.某日某银行汇率报价如下:USD1=FF5.4530/50,USD1=DM1.8140/60,那么该银行的法国法郎以德国马克表示的卖出价为多少?(北京大学2022研)解:应计算出该银行的法国法郎以德国马克表示的套算汇率。

由于这两种汇率的方法相同,所以采用交叉相除的方法,即:USD1=DM1.8140/60 USD1=FF5.4530/50 可得:FF1=DM0.3325/30 所以该银行的法国法郎以德国马克表示的卖出价为:FF=DM0.3330。

2.在我国外汇市场上,假设2022年12月的部分汇价如下:欧元/美元:1.4656/66;澳元/美元:0.8805/25。

请问欧元与澳元的交叉汇率欧元/澳元是多少?(上海交大2022年考研题,数据有所更新)解:由于两种汇率的标价方法相同,所以交叉相除可得到交叉汇率。

欧元/美元:1.4655/66 澳元/美元:0.8805/25 1.6656 1.6606 可得:欧元/澳元:1.6606/56。

3、某日伦敦外汇市场上汇率报价如下:即期汇率1英镑等于1.6615/1.6635美元,三个月远期贴水50/80点,试计算美元兑英镑三个月的远期汇率。

(北京大学2022研)解:即期汇率1英镑等于1.6615/1.6635美元三个月远期贴水等于50/80点三个月英镑等于 (1.6615+0.0050)/(1.6635+0.0080)=1.6665/1.6715美元则1美元=英镑=0.5983/0.6001英镑 4.已知,在纽约外汇市场即期汇率1个月远期差价美元/澳元 1.1616/26 36—25 英镑/美元 1.9500/10 9-18 求1个月期的英镑兑澳元的1个月远期汇率是多少?(1)1个月期的美元/澳元、英镑/美元的远期汇率:美元/澳元:1.1580/1.1601 英镑/美元:1.9509/1.9528 (2)1个月期的英镑兑澳元的1个月远期汇率英镑/澳元的买入价:1.9509×1.1580 =2.2591 英镑/澳元的卖出价:1.9528×1.1601 =2.2654 5.已知:2022年7月21日,银行间外汇市场美元折合人民币的中间价为 USD 1 =RMB 8.2765;2022年12月21日银行间外汇市场美元对人民币汇率的中间价为:USD1 = RMB 7.8190,请问美元对人民币的贴水年率、人民币对美元的升水年率各是多少?解:(2)人民币对美元的升水年率 6. 已知:(1)2022年12月28日(年末交易日),银行间外汇市场美元折合人民币的中间价为 1USD =7.3046RMB,2022年12月31日银行间外汇市场美元折合人民币的中间价为 1USD =6.8346RMB。

《国际投资》第六版作业课后练习答案

第一章15/16/20第二章4/6/9/15/16/19/20第三章3/5/9/16/18第四章8/13/15/16/17第五章2/7/10/15/17第六章6/8/10/12/13文本:人参淫家Fish 汉化:fish&MonkEy协力排版:MonkEy 校对:无时间:无后期:无本汉化由马骝鱼汉化组制作,本作品来源于互联网供学习爱好者使用禁止用于商业盈利行为若因私自散布造成法律纠纷汉化组概不负责第一章15.问:假设在某一时点,巴克莱银行每英镑的美元标价为英镑对美元=1.4570。

兴业银行每美元的目标价位为美元对日元=128.17,米德银行每英镑的日元的套算汇率的标价为英镑对日元=183.a.不考虑买卖价差,此处是否存在套利机会b.加入存在套利机会,你要通过哪些步骤以获得套利利润?如果你有100万美元,你可以获利多少?解:a.根据题目可以求得美元对日元的汇率:£:¥= $:¥⨯ £:$ = 128.17 ⨯ 1.4570 = 186.74。

然而,米德银行的标价为£:¥=1:183,因此存在套利机会b.在存在£:¥=186.74的同时,米德银行汇率标价为£:¥=1:183,即英镑对日元价值在米德银行被相对低估,因此,你的套利步骤应建立为使用日元从米德银行购买英镑,有100万美元情况下,具体步骤如下:a. 在兴业银行售出美元以取得日元: 售出$1,000,000 以取得$1,000,000 ⨯ ¥128.17 / $ =¥128,170,000.b. 在米德银行出售日元以购买英镑:售出l ¥128,170,000 以购买¥128,170,000/(¥183 / £) =£700,382.51.c. 在巴克莱银行将英镑兑换为美元: 卖出£700,382.51 ,得到£700,382.51 ⨯ ($1.4570 /k, £) =$1,020,457.32.因此,获利为:$1,020,457.32 - $1,000,000 = $20,457.3216.吉姆擅长与套算汇率套利,在某一个时点,他注意到如下标价:以瑞士法郎标价的美元价值= 1.5971 瑞士法郎/美元以澳大利亚元标价的美元价值=1.8215 澳大利亚/美元以澳大利亚元标价的瑞士法郎价值=1.1450 澳大利亚元/瑞士法郎不考虑交易成本,基于这些标价,吉姆有套利机会吗?他应该怎样做来获取套利利润?他用100万美元可以套利多少?解:由题可知,澳元跟瑞士法郎之间的隐形汇率为SFr:A$ = $:A$ ⨯ SFr:$ = ($:A$) ÷ ($:SFr) = 1.8215/1.5971 = 1.1405。

国际投资学案例大全

关财务公司方面的接洽,上汽正式参股通用大宇使双方的战略联盟更紧密。

上汽集团作为通用汽车在中国及亚太地区重要的战略合伙伴的身份人股通用大宇,表明通用汽车与上汽的战略合作伙已跨出中国国界,走向世界。

2,是一种提高国内市场份额的巧妙方式山东大宇工程,是大宇汽车在破产之前和山东省方面合资建设的,总投资78亿元,主要生产轿车零部件。

按照原计划,山东大字工程生产的产品全部返销韩国,但随着大宇汽车的破产,该返销计划被迫终止,工程停产,78亿元的投资变成了废墟。

上海通用2001年就开始与山东烟台进行厂接触,真正谈判是在2002年年初。

上汽集团此次收购大宇10%的股份,伴随着通用重组大宇计划的进程,也为上汽和山东大宇的谈判铺平了道路。

因为根据重组大宇计划安排,重组计划包括债务重新安排、还债措施和业务拆分。

随着上汽、钟木参与收购大宇股份的落实,债务重新安排已经完成。

因此重点将是业务的拆分,即在新合资公司成立后把大宇的海外资产以工厂为单位卖掉。

正如前面提到的那样,从收购大宇的协议来看,通用的思路是选择大宇比自己强的业务来弥补自己相对薄弱的那部分业务。

通用收购韩国大宇在表面看来是一个大手笔,但是经过资产层层剥离后,除开大宇本土的部分产业,海外资产只要了一个越南的工厂。

就中国市场来看,通用在中国的市场占有额也是大宇不能企及的,所以通用对于大宇在中国的业务并不十分看重。

如果通用看中大宇的海外工厂,完全有能力在2002年4月收购时把它一并买下,并且像山东大宇这样的零部件工程和通用本身的业务范围存在着冲突。

所以,通过分析可以看出,山东大宇工程作为大宇惟一在华资产。

上汽集团参与收购大宇资产,最终目标将是中国市场,上汽集团此次的借船出海可以说是一举两得的行为。

(三)思考题1.上汽集团“借船出海”说明了什么?上海汽车工业集团“借船出海”,实施出海跨洋战略说明,近年来中园经济的飞速发展,使得中国已经开始踏上了—条对外直接投资的道路。

目前,中国的跨国兼并和收购行动非适度,有一个很好的战略性的开端。

上海交通大学金融学导论综合练习题

金融学导论综合练习题综合练习一一、判断题1。

俗话说的“不要把鸡蛋放在一个篮子里”体现的金融学原理是分散化投资可以降低风险。

()A。

正确2。

对于一个经济系统而言,金融体系必须是一个能自我平衡的体系,否则将会引发金融危机、经济危机乃至政治危机。

()A。

正确3。

20世纪90年代以来,传统的银行业务正在遭受来自证券业、保险和基金组织的侵蚀,世界金融体系越来越显得多元化,银行作为各国金融体系的信贷中心、结算中心和现金出纳中心的地位已不复存在.()B. 错误4. 钱、货币、通货、现金都是一回事,银行卡也是货币。

()B. 错误5。

所谓“流通中的货币"就是现金,即发挥支付手段职能的货币和发挥流通手段职能的货币的总和。

()B。

错误6。

信用货币虽然本身没有价值,但由于其能够发挥货币的职能,所以构成社会财富的组成部分。

()A。

正确7. 电子货币作为一种信用货币,预示着无现金社会的发展趋势,即完全没有货币的社会。

()B。

错误8. 目前,世界各国普遍以金融资产安全性的强弱作为划分货币层次的主要依据.()B。

错误9。

我国M1层次的货币口径是:M1=流通中现金+定期存款。

()B。

错误10. 在纸币本位制下,如果在同一市场上出现两种以上可流通纸币,会导致实际价值较低的货币排斥实际价值高的货币的“劣币驱逐良币”现象.()B。

错误11。

货币制度最基本的内容是确定货币名称和货币单位,货币名称和货币单位确定了,一国的货币制度也就确定了。

()B. 错误12。

金融市场被称为国民经济的“晴雨表”,这实际上指的就是金融市场的调节功能。

()B. 错误13. 资本市场是指以期限在1年以内的金融工具为交易对象的短期金融市场。

()B. 错误14。

金融产品的收益性与流动性一般是反向变动,收益性越强,流动性越差.()B. 错误15. 我们经常说高风险高收益,是说只要投资者承担高风险,就可以获得高收益。

()B. 错误二、单选题1。

在有效市场假说中,认为基本面分析是徒劳的、无用的市场是()。

国际投资学作业答案.

《国际投资学》作业集第一章国际投资概述一、名词解释1。

国际投资是各国官方机构、跨国公司、金融机构及居民个人等投资主体将其所拥有的货币资本或产业资本,经跨国流动形成实物资产、无形资产或金融资产,并通过跨国经营得以实现价值增值的经济行为.2. 跨国公司是指依赖雄厚的资本和先进的技术,通过对外直接投资在其他国家和地区设立子公司,从事国际化生产、销售活动的大型企业。

3。

经济全球化世界各国在全球范围内的经济融合二、简答题1. 国际投资的主要特点第一,投资主体单一化;第二,投资环境多样化;第三投资目标多元化;第四,投资运行复杂化。

2.跨国公司与国内企业比较有哪些特点?第一,生产经营活动的跨国化,这是跨国公司的最基本特征;第二,实行全球性战略;第三,公司内部一体化原则。

三、论述题1. 书 P35论述题第一题试述跨国公司近年来在中国的投资状况及迅速扩张的主要原因。

跨国公司进入中国的步伐明显加快, 这一趋势还将继续保持下去。

跨国公司研发投入明显增加, 跨国公司投资更倾向于独资方式, 中国政府的优惠政策,低廉的劳动力、广阔的市场等第二章国际直接投资理论一、名词解释1. 市场内部化是指企业为减少交易成本,减少生产和投资风险,而将该跨国界的各交易过程变成企业内部的行业。

2. 产品生命周期是产品的市场寿命,即一种新产品从开始进入市场到被市场淘汰的整个过程 3. 区位优势是指跨国公司在投资区位上具有的选择优势二、简答题1. 简述垄断优势理论的主要内容这一理论主要是回答一家外国企业的分支机构为什么能够与当地企业进行有效的竞争,并能长期生存和发展下去。

海默认为,一个企业之所以要对外直接投资,是因为它有比东道国同类企业有利的垄断优势,从而在国外进行生产可以赚取更多的利润。

这种垄断优势可以划分为两类:一类是包括生产技术、管理与组织技能及销售技能等一切无形资产在内的知识资产优势;一类是由于企业规模大而产生的规模经济优势.2。

国际生产折中论的主要内容对外投资主要是由所有权优势、内部化优势和区位优势这三个基本因素决定的。

国本国际投资学题库2022

国本国际投资学题库202210国本国际投资学习题库一、单项选择题1.下列国际投资方式中属于股权投资的是(C)。

A.技术授权B.管理合同C.合资经营D.合作经营2.下列关于证券组合有效集的条件正确的是(C)。

A.在既定风险水平下取得最大收益并且在既定收益率水平下承担风险最大B.在既定风险水平下取得最大收益或在既定收益率水平下承担风险最大C.在既定风险水平下取得最大收益并且在既定收益率水平下承担风险最小D.在既定风险水平下取得最大收益或在既定收益率水平下承担风险最小3.下列选项中不属于我国对外直接投资特点的是(B)A.我国对外投资规模总体规模偏小B.投资主体中大型国有企业占比逐渐上升C.我国的投资行业领域不断拓宽D.我国对外投资呈现向世界各地分散的趋势4.通过收购另一家已在海外证券市场上市的公司即空壳公司的全部或部分股份,取得上市公司的实际管理权,然后注入本国国内资产和业务,以达到海外间接上市目的的方式被称为(D)。

A.造壳上市B.换壳上市C.借壳上市D.买壳上市5.下列选项中不属于我国吸收外商直接投资特点的是(C)。

C.外资进入方式以跨国并购为主D.外商对华投资的独资化趋势日益明显6.将生产或经营过程中的某一个或几个环节交由其他实体完成的一种商业模式被称为(A)。

A.服务外包B.国际工程承包C.服务贸易D.产业转移7.下列选项中会增加国际投资风险的是(B)。

A.对东道国投资环境进行全面考察B.延长投资期限C.提高投资者的经营管理水平D.国际政治经济格局稳定8.外汇风险不包括(C)。

A.折算风险B.交易风险C.技术风险D.经济风险9.跨国公司规避国际业务中经营风险的方式不包括(D)。

A.改变生产流程或产品B.改变生产经营地点C.放弃对风险较大项目的投资D.风险自留10.国际工程承包的创新方式中BOT、TOT、ABS依次代表的是(B)A.移交—经营—建设、建设—经营—建设、资产证券化B.建设—经营—移交、移交—经营—移交、资产证券化C.移交—经营—建设、移交—经营—移交、资产证券化D.建设—经营—移交、建设—经营—建设、资产证券化11.由租赁公司融资,把承租人自行选定的机械、设备买进或租进,然后租给企业使用,企业按合同规定,以交租赁费的形式按期付给租赁公司的国际租赁方式称为(A)。

国际投资学案例分析

国际投资学案例分析简介:特斯拉是一家全球知名的电动车制造商,总部位于美国加州。

特斯拉在全球范围内积极寻找新的市场机会,其中包括中国。

本篇案例分析将探讨特斯拉在中国的投资情况,并分析其对特斯拉及中国市场带来的影响。

案例分析:1.特斯拉在中国市场的投资决策特斯拉于2024年进入中国市场,当时中国是全球最大的汽车市场之一、特斯拉决定在中国建立工厂,并加大在中国的生产和销售力度。

这一决策受到了中国政府对电动车市场的支持以及中国市场巨大的潜力的影响。

2.特斯拉在中国市场的挑战进入中国市场后,特斯拉面临着一系列的挑战。

首先,特斯拉在中国面临着激烈的竞争,包括来自本土企业的竞争。

其次,特斯拉在中国市场存在着供应链和物流等问题,需要与中国供应商和物流公司进行合作。

此外,特斯拉还需要适应中国市场的文化和消费习惯,例如中国消费者更加看重价格因素。

3.特斯拉在中国市场的成功尽管面临许多挑战,特斯拉在中国市场取得了一定的成功。

首先,特斯拉在中国建立了超过10个销售和服务中心,覆盖了主要城市。

其次,特斯拉在中国市场的销量持续增长,并成为中国最受欢迎的豪华电动车品牌之一、此外,特斯拉还积极与中国政府合作,推动电动车的发展。

4.特斯拉对中国市场的影响特斯拉的进入和发展对中国市场带来了多重影响。

首先,特斯拉的成功吸引了其他国际电动车制造商进入中国市场。

其次,特斯拉在中国市场推动了电动车行业的发展,中国政府对电动车市场的支持也得到了进一步加强。

此外,特斯拉在中国的生产基地为中国创造了就业机会,并促进了相关产业的发展。

结论:特斯拉在中国的投资是一个成功的案例,充分展示了如何在全球化背景下寻找新的市场机会并克服挑战。

特斯拉的成功对中国市场和电动车行业的发展都产生了积极影响。

这个案例也给其他企业提供了有益的经验教训,特别是在进入新的国际市场时需要考虑到文化、竞争和政府支持等因素。

国际投资(第六版)在线解答手册(即课后习题答案) M08_SOLN8117_06_SM_C08

Chapter 8Alternative Investments1. Let us compute the terminal value of $1 invested. The share class with the highest terminal value netof all expenses would be the most appropriate, because all classes are based on the same portfolio and thus have the same portfolio risk characteristics.a. Class A. $1 × (1 – 0.05) = $0.95 is the amount available for investment at t= 0, after paying thefront-end sales charge. Because this amount grows at 9% per year, reduced by annual expensesof 0.0125, the terminal value per $1 invested after one year is $0.95 × 1.09 × (1 − 0.0125) = $1.0226.Class B. Ignoring any deferred sales charge, after one year, $1 invested grows to $1 × 1.09 ×(1 – 0.015) = $1.0737. According to the table, the deferred sales charge would be 4%; therefore,the terminal value is $1.0737 × 0.96 = $1.0308.Class C. Ignoring any deferred sales charge, after one year, $1 invested grows to $1 × 1.09 ×(1 − 0.015) = $1.0737. According to the table, the deferred sales charge would be 1%; therefore,the terminal value is $1.0737 × 0.99 = $1.063.Class C is the best.b. Class A. The terminal value per $1 invested after three years is $0.95 × 1.093× (1 − 0.0125)3=$1.1847.Class B. Ignoring any deferred sales charge, after three years, $1 invested grows to $1 × 1.093 ×(1 − 0.015)3= $1.2376. The deferred sales charge would be 2%; therefore, the terminal value is$1.2376 × 0.98 = $1.2128.Class C. There would be no deferred sales charge. Thus, after three years, $1 invested grows to$1 × 1.093× (1 − 0.015)3= $1.2376.Class C is the best.c. Class A. The terminal value per $1 invested after five years is $0.95 × 1.095× (1 − 0.0125)5=$1.3726.Class B. There would be no deferred sales charge. So, the terminal value per $1 invested afterfive years is $1 × 1.095× (1 − 0.015)5= $1.4266.Class C. There would be no deferred sales charge. So, the terminal value per $1 invested afterfive years is $1 × 1.095× (1 − 0.015)5= $1.4266.Classes B and C are the best.d. Class A. The terminal value per $1 invested after 15 years is $0.95 × 1.0915× (1 − 0.0125)15=$2.8653.Class B. There would be no deferred sales charge. So, the terminal value per $1 invested after15 years is $1 × 1.0915× (1 − 0.015)6× (1 − 0.0125)9= $2.9706.Class C. There would be no deferred sales charge. So, the terminal value per $1 invested after15 years is $1 × 1.0915× (1 − 0.015)15= $2.9036.Class B is the best.42 Solnik/McLeavey • Global Investments, Sixth Edition2. Class A performs quite poorly unless the investment horizon is very long. The reason is the high salescharge of 5 percent on purchases. Even though the annual expenses for Class A are low, that is not enough to offset the high sales charge on purchases until a very long investment horizon. One could verify that Class A outperforms Class C for an investment horizon of 21 years or more.Class B performs worse than Class C at very short-term horizons because of its higher deferred sales charges. However, after its deferred sales charges disappear, the relative performance of Class B starts improving. After six years, Class B shares convert to Class A with its lower annual expenses.At longer horizons, Class B starts to outperform Class C due to its annual expenses, which are lower than those of Class C.Class C performs well at shorter investment horizons because it has no initial sales charge and it has a low deferred sales charge.3. The estimated model isHouse value in euros = 140,000 + (210 × Living area) + (10,000 × Number of bathrooms) +(15,000 × Fireplace) − (6,000 × Age)so, the value of the specific house is140,000 + (210 × 500) + (10,000 × 3) + (15,000 × 1) – (6,000 × 5) =€260,0004. a. The net operating income for the office building is gross potential rental income minus estimatedvacancy and collection costs, minus insurance and taxes, minus utilities, minus repairs andmaintenance.NOI = 350,000 − 0.04 × 350,000 − 26,000 − 18,000 − 23,000 = $269,000b. The capitalization rate of the first office building recently sold in the area isNOI/(Transaction price) = 500,000/4,000,000 = 0.125The capitalization rate of the second office building recently sold in the area isNOI/(Transaction price) = 225,000/1,600,000 = 0.141The average of the two capitalization rates is 0.133.Applying this capitalization rate to the office building under consideration, which has an NOI of $269,000, gives an appraisal value of:NOI/(Capitalization rate) = 269,000/0.133 = $2,022,5565. The after-tax cash flow for the property sale year is $126,000 + $710,000 = $836,000. At a cost ofequity of 18%, the present value of the after-tax cash flows in years 1 through 5 is as follows.$60,000/1.18 + $75,000/1.182+ $91,000/1.183+ $108,000/1.184 +36,000/1.185= $581,225 The investment requires equity of 0.15 × $3,000,000 = $450,000. Thus, the NPV = $581,225 −$450,000 = $131,225. The recommendation based on NPV would be to accept the project, because the NPV is positive.Chapter 8 Alternative Investments 43 6. a. The amount borrowed is 80% of $1.5 million, which is $1.2 million. The first year’s interest =9% of $1.2 million = $108,000. So,After-tax net income in year 1 = (NOI − Depreciation − Interest) × (1 − Marginal tax rate) =($170,000 − $37,500 − $108,000) × (1 − 0.30) = $17,150flow= After-tax net income + Depreciation − Principal repaymentcashAfter-taxand,= Mortgage payment − Interest = $120,000 − $108,000 = $12,000 Principalrepaymentso,After-tax cash flow in year 1 = $17,150 + $37,500 − $12,000 = $42,650.New NOI in year 2 = 1.04 × $170,000 = $176,800. We need to calculate the second year’sinterest payment on the mortgage balance after the first year’s payment. This mortgage balanceis the original principal balance minus the first year’s principal repayment, or $1,200,000 –$12,000 = $1,188,000. The interest on this balance is $106,920.So,= ($176,800 − $37,500 − $106,920) × (1 − 0.30) = $22,666incomeAfter-taxnet= $120,000 − $106,920 = $13,080repaymentPrincipalso,After-tax cash flow in year 2 = $22,666 + $37,500 − $13,080 = $47,086New NOI in year 3 = 1.04 × $176,800 = $183,872. We need to calculate the third year’s interestpayment on the mortgage balance after the second year’s payment. This mortgage balance is theoriginal principal balance minus the first two years’ principal repayments, or $1,200,000 −$12,000 − $13,080 = $1,174,920. The interest on this balance is $105,743.So,income= $183,872 − $37,500 − $105,743) × (1 − 0.30) = $28,440netAfter-tax= $120,000 − $105,743 = $14,257repaymentPrincipalso,After-tax cash flow in year 3 = $28,440 + $37,500 − $14,257 = $51,683b. Ending book value = Original purchase price − Total depreciation during three years =$1,500,000 − 3 × $37,500 = $1,387,500.The net sale price = $1,720,000 × (1 − 0.065) = $1,608,200Capital gains tax = 0.20 × ($1,608,200 − $1,387,500) = $44,140After-tax cash flow from property sale = Net sales price − Outstanding mortgage − Capitalgains taxand,= Original mortgage − Three years’ worth of principal repayments,mortgageOutstandingor$1,200,000 − ($12,000 + $13,080 + $14,257) = $1,160,63so,After-tax cash flow from the property sale = $1,608,200 − $1,160,663 − $44,140 = $403,39744 Solnik/McLeavey • Global Investments, Sixth Editionc. The total after-tax cash flow for the property sale year is $51,683 + $403,397 = $455,080. At acost of equity of 19%, the present value of the after-tax cash flows in years 1 through 3 is asfollows:$42,650/1.19 + $47,086/1.192+ $455,080/1.193= $339,142The investment requires equity of 0.20 × $1,500,000 = $300,000. Thus, the NPV = $339,142 −$300,000 = $39,142. The recommendation based on NPV would be to accept the project, because the NPV is positive.7. No, one would not suggest using real estate appraisal-based indexes in a global portfolio optimization.Real estate appraisal values are a smoothed series. One of the reasons for this smoothness is that the appraisals are done quite infrequently. Another reason is that the appraised values typically show relatively few changes. Due to these two reasons, an appraisal-based index understates volatility.This spuriously low volatility would inflate the attractiveness of real estate.8. Clearly, the two real estate indexes have very different price behaviors. Their correlation is almostnull. As expected, the NAREIT index exhibits a strong correlation with U.S. stocks because the REIT share prices are strongly influenced by the stock market. In contrast, the FRC index, which is much less volatile, is not highly correlated with the stock market.9. a. There are three possibilities.Project does not survive until the end of the eighth yearProject survives and the investor exits with a payoff of $25 millionProject survives and the investor exits with a payoff of $35 millionThere is an 80 percent chance that the project will not survive until the end of the eighth year.That is, there is a 20 percent chance that the project will survive, and the investor will exit theproject then. If the project survives, it is equally likely that the payoff at the time of exit will beeither $25 million or $35 million.The project’s NPV is the present value of the expected payoffs minus the required initialinvestment of $1.4 million.= 0.8 × $0 + 0.2 × [(0.5 × $25 million + 0.5 × $35 million)/1.28] − $1.4 million = NPV−$0.004592 million or −$4,592b. Because the expected NPV of the project is negative, the project should be rejected.10. The probability that the venture capital project survives to the end of the first year is (1 − 0.28),1 minus the probability of failure in the first year; the probability that it survives to the end ofsecond year is the product of the probability it survives the first year times the probability it survives the second year, or (1 − 0.28) (1 − 0.25). So, the probability that the project survives to end of the sixth year is (1 − 0.28) (1 − 0.25) (1 − 0.22) (1 − 0.18) (1 − 0.18) (1 − 0.10) = (0.72) (0.75) (0.78)(0.82) (0.82) (0.90) = 0.255, or 25.5%. The probability that the project fails is 1 − 0.255 = 0.745,or 74.5%.The net present value of the project, if it survives to the end of the sixth year and thus earns€60 million, is – €4.5 million +€60 million/1.226=€13.70 million. The net present value of the project if it fails is −€4.5 million. Thus, the project’s expected NPV is a probability-weightedaverage of these two amounts, or (0.255) (€13.70 million) + (0.745) (–€4.5 million) =€141,000.Based on the project’s positive net present value, VenCap should accept the investment.Chapter 8 Alternative Investments 4511. a. Fee = 1.5% + 15% × (35% − 5.5%) = 1.5% + 4.425% = 5.925%.= 35% − 5.925% = 29.1%Netreturnb. Because the gross return is less than the risk-free rate, the incentive fee is zero. The only feeincurred is the base management fee of 1.5%.= 5% − 1.5% = 3.5%.returnNetc. Again, the incentive fee is zero.=−6% − 1.5% =−7.5%.Netreturn12. a. Fixed fee = 1% of $2 billion = $20 million.If the return is 29%, new value of the fund would be $2 billion × 1.29 = $2.58 billion. This newvalue would be $2.58 billion − $2.1 billion = $0.48 billion above the high watermark. So, theincentive fee = 20% × $0.48 billion = $0.096 billion, or $96 million.Total fee = $20 million + $96 million = $116 millionb. Fixed fee = 1% of $2 billion = $20 million.If the return is 4.5%, new value of the fund would be $2 billion × 1.045 = $2.09 billion. Becausethis new value is below the high watermark of $2.1 billion, no incentive fee would be earned.Total fee = $20 millionc. Fixed fee = 1% of $2 billion = $20 million.If the return is −1.8%, no incentive fee would be earned.Total fee = $20 million13. Clearly, the high watermark provision has the positive implication for the investors that they wouldhave to pay the manager an incentive fee only when they make a profit. Further, the hedge fundmanager would need to make up any earlier losses before becoming eligible for the incentive feepayment. However, a negative implication is that the option-like characteristic of the high watermark provision (the incentive fee being zero everywhere below the benchmark and increasing above the benchmark) may induce risk-taking behavior when the fund is below the high watermark. Themanager may take more risky positions when the fund is below the high watermark in order to get to above the high watermark and earn an incentive fee. The worst case for the manager is a zeroincentive fee, regardless of how far below the benchmark the fund turns out to be. Another negative implication is that the incentive fees, if the fund exceeds the high watermark, are set quite high(typically at 20%), which reduces long-run asset growth.14. a. The hedge fund would sell short the overvalued shares and use the proceeds to buy theundervalued shares. The fund has €25 million −€1 million =€24 million to be used toward cashmargin deposit. Because the cash margin deposit requirement is 20%, the fund could take longand short positions totalling €24 million/0.20 =€120 million. So, the fund would do thefollowing:€1 million in cashK eep€24 million in a margin accountDeposit€120 million of overvalued stocks from a brokerBorrowSell the overvalued stocks for €120 millionUse the sale proceeds to purchase undervalued stocks for €120 million46 Solnik/McLeavey • Global Investments, Sixth Editionb. If the performances of both lists of stocks are as expected, there would be a gain of 7% on thelong position of €120 million and a gain of 7% on the short position of €120 million. So, the total gain would be 7%×€120 million × 2 =€16.8 million. Ignoring the return on invested cash of €1 million, and assuming that dividends on the long stocks will offset dividends on the short stocks, this translates to an annual return of (€16.8 million/€25 million) × 100 = 67.2%. The return is so high when the expectations are realized, because the position is highly levered.15. a. The Spanish firm will give two of its shares, which are worth €25, for three of the Italian firm’sshares, which are worth €24. Thus, the shares of the Italian firm are trading at a discount. Thereason for the discount is that there is a possibility that the merger may not go through. If themerger does not go through, the shares of the Italian firm are likely to fall back to the premerger announcement level. An investor currently buying shares of the Italian firm is taking the risk that the merger will not occur.b. The hedge fund will take a hedged position by selling two shares of the Spanish firm short forevery three shares of the Italian firm that it buys. So, the hedge fund will buy 250,000 shares ofthe Italian firm by selling (2/3) × 250,000 = 166,666.67, that is, 166,667 shares of the Spanishfirm. The proceeds from the short sale are 166,667 ×€12.50 =€2,083,338, which is €83,338more than the cost of buying the shares of the Italian firm, which is 250,000 ×€8 =€2,000,000.c. Because the merger did not go through and the stock price of the Italian firm fell, the hedge fundincurs a substantial loss. The loss is 250,000 × (€8 −€6.10) =€475,000.16. a. Net return on Fund A = 50% × (1 − 0.15) = 42.5%Net return on Fund B = 20% × (1 – 0.15) = 17%Net return on Fund C =−10%So, average net return = (42.5% + 17% − 10%)/3 = 16.5%= (50% + 20% − 10%)/3 = 20%.AveragereturngrossThus, the average gross return on the three hedge funds is the same as the percentage increase in the stock market index, and the average net return is lower.b. The publicity campaign launched by Global group illustrates the problem of survivorship bias inperformance measure of hedge funds. Although the average gross return on the three hedge funds is the same as the percentage increase in the stock market index, the performance reported byGlobal group seems much better because it is based on only the funds that survive. That is, theaverage performance reported by Global group is inflated.17. The measurement of the performance of the hedge funds suffers from survivorship bias. The 90 hedgefunds that the analyst has examined include only those funds that have survived during the last 10 years. Thus, any poorly performing funds that have been discontinued due to low return or highvolatility, or both, have been excluded. Accordingly, the average return on hedge funds hasbeen overstated, while the volatility has been understated. Consequently, the Sharpe ratio for the hedge funds has been overstated. Furthermore, the Sharpe ratio may be a misleading measure of risk-adjusted performance for hedge funds because of the optionality in their investment strategies.18. a. The construction of the index is okay in year 10 but not in the earlier years. By using today’sweights in construction of the index in earlier years, the exchange is over-weighing thosecommodities that have become important over the period, and have simultaneously gone up inprice.b. For each year, use the relative economic importance of the commodities in that year as theweights for that year. That is, use year one weights for the index calculated in year one, and so on.Chapter 8 Alternative Investments 4719. a. The expected return on gold, as theoretically derived by the CAPM, isE(Rgold) = 7% +βgold × 4%= 7% − 0.3 (4%) = 5.8%b. Given its negative beta, gold is likely to perform well when the overall market performs poorly.Thus, our investment in gold is likely to offset some of the loss on the rest of the portfolio.Investors should be willing to accept an overall lower expected return on gold because, in periodsof financial distress, gold tends to do well.。

成考上海大学国际金融

10、国际收支调节的资产组合平衡分析法的前提条件是货币和债券的组合比例取决于债券的收益和风险

你的答案: 对

第三章作业

1、外汇缓冲政策用于外汇缓冲的资产是你的答案: D

A、外汇

B、黄金

C、白银

D、黄金和外汇

2、国际收支的国际资金融通政策,主要调节你的答案: A

A、临时性的国际收支失衡

B、长期性的国际收支失衡

A、补偿性交易

B、调节性交易

C、自主性交易

D、事后交易

4、下面哪一种交易应该记录在国际收支平衡表的借方科目D

A、国际资本流入

B、出售国外有价证券

C、对外负债增加

D、官方储备资产增加

多选题

5、在国际收支概念中,居民包括你的答案: ABC

A、当地政府

B、居住满1年的个人

C、在当地注册的企业

D、国外驻军

E、外交使节

B、外汇储备

C、在IMF的储备头寸

D、特别提款权

2、与国际清偿力具有相同含义的是你的答案: C

C、平衡项目

D、统计误差

E、SDRs

判断题

9、国际收支是国际借贷的原因你的答案: 错

10、国际收支平衡表中的贸易交易,进口、出口均采用FOB价格你的答案: 对

第二章作业

1、在国际金本位制下,发生黄金外流的是由于该国你的答案: A

A、国际收支逆差

B、国内货币供给减少

C、物价水平下跌

D、本国商品在国外市场上的竞争能力提高

你的答案: 对

8、由于国民收入的变化所引起的国际收支不平衡,称为收入性不平衡。你的答案: 对

9、货币供应量的相应变动所引起的国际收支失衡,称为货币性失衡你的答案: 对

chapter 9投资作业-chapter 15习题

习题Chapter 93. You are a consultant to a large manufacturing corporation that is considering a project with the following net after-tax cash flows (in millions of dollars):The project’s beta is 1.8. Assuming that, what is the net present value of the project? What is the highest possible beta estimate for the project before its NPV becomes negative?4. Are the following true or false? Explain.a. Stocks with a beta of zero offer an expected rate of return of zero.b. The CAPM implies that investors require a higher return to hold highly volatile securities.c. You can construct a portfolio with beta of .75 by investing .75 of the investment budget in T-bills and the remainder in the market portfolio.In problems 13 to 15 assume that the risk-free rate of interest is 6% and the expected rate of return on the market is 16%.13. Ashare of stock sells for $50 today. It will pay a dividend of $6 per share at the end of the year. Its beta is 1.2. What do investors expect the stock to sell for at the end of the year?14. I am buying a firm with an expected perpetual cash flow of $1,000 but am unsure of its risk. If I think the beta of the firm is .5, when in fact the beta is really 1, how much more will I offer for the firm than it is truly worth?15. A stock has an expected rate of return of 4%. What is its beta?17. Suppose the rate of return on short-term government securities (perceived to be riskfree) is about 5%. Suppose also that the expected rate of return required by the market for a portfolio with a beta of 1 is 12%. According to the capital asset pricing model (security market line):a. What is the expected rate of return on the market portfolio?b. What would be the expected rate of return on a stock with beta=0?c. Suppose you consider buying a share of stock at $40. The stock is expected to pay $3 dividends next year and you expect it to sell then for $41. The stock risk has been evaluated at beta=-0.5. Is the stock overpriced or underpriced?21. The security market line depicts:a. A security’s expected return as a function of its systematic risk.b. The market portfolio as the optimal portfolio of risky securities.c. The relationship between a security’s return and the return on an index.d. The complete portfolio as a combination of the market portfolio and the risk-free asset.22. Within the context of the capital asset pricing model (CAPM), assume:• Expected return on the market =15%.• Risk-free rate _ 8%.• Expected rate of return on XYZ security =17%.• Beta of XYZ security =1.25.Which one of the following is correct?a. XYZ is overpriced.b. XYZ is fairly priced.c. XYZ’s alpha is=-0.25%.d. XYZ’s alpha is=0 .25%.The following table shows risk and return measures for two portfolios. answer question 26 and 2726. When plotting portfolio R on the preceding table relative to the SML, portfolio R lies:a. On the SML.b. Below the SML.c. Above the SML.d. Insufficient data given.27. When plotting portfolio R relative to the capital market line, portfolio R lies:a. On the CML.b. Below the CML.c. Above the CML.d. Insufficient data given.31. Karen Kay, a portfolio manager at Collins Asset Management, is using the capital asset pricing model for making recommendations to her clients. Her research department has developed the information shown in the following exhibit.a. Calculate expected return and alpha for each stock.b. Identify and justify which stock would be more appropriate for an investor who wants toi. add this stock to a well-diversified equity portfolio.ii. hold this stock as a single-stock portfolio.Chapter 111. A portfolio management organization analyzes 60 stocks and constructs a meanvariance efficient portfolio using only these 60 securities.a. How many estimates of expected returns, variances, and covariances are needed to optimize this portfolio?b. If one could safely assume that stock market returns closely resemble a single index structure, how many estimates would be needed?2. The following are estimates for two of the stocks in problem 1.The market index has a standard deviation of 22% and the risk-free rate is 8%.a. What is the standard deviation of stocks A and B?b. Suppose that we were to construct a portfolio with proportions:Stock A: .30Stock B: .45T-bills: .25Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio.4. Consider the two (excess return) index model regression results for A and B:a. Which stock has more firm-specific risk?b. Which has greater market risk?c. For which stock does market movement explain a greater fraction of return variability?d. Which stock had an average return in excess of that predicted by the CAPM?e. If rf were constant at 6% and the regression had been run using total rather than excess returns, what would have been the regression intercept for stock A ?Use the following data for problems 5 through 9. Suppose that the index model for stocks A and B is estimated from excess returns with the following results:5. What is the standard deviation of each stock?6. Break down the variance of each stock to the systematic and firm-specific components.7. What are the covariance and correlation coefficient between the two stocks?8. What is the covariance between each stock and the market index?9. Are the intercepts of the two regressions consistent with the CAPM? Interpret their values.15. Based on current dividend yields and expected growth rates, the expected rates of return on stocks A and B are 11% and 14%, respectively. The beta of stock A is .8, while that of stock B is 1.5. The T-bill rate is currently 6%, while the expected rate of return on the S&P 500 index is 12%. The standard deviation of stock A is 10% annually, while that of stock B is 11%.a. If you currently hold a well-diversified portfolio, would you choose to add either of these stocks to your holdings?b. If instead you could invest only in bills and one of these stocks, which stock would you choose? Explain your answer using either a graph or a quantitative measure of the attractiveness of the stocks.16. Assume the correlation coefficient between Baker Fund and the S&P 500 Stock Index is .70. What percentage of B aker Fund’s total risk is specific (i.e., nonsystematic)?a. 35%b. 49%c. 51%d. 70%17. The correlation between the Charlottesville International Fund and the EAFE Market Index is 1.0. The expected return on the EAFE Index is 11%, the expected return on Charlottesville International Fund is 9%, and the risk-free return in EAFE countries is 3%. Based on this analysis, the implied beta of Charlottesville International is:a. Negativeb. .75c. .82d. 1.00chapter 122. Which of the following most appears to contradict the proposition that the stock market is weakly efficient? Explain.a. Over 25% of mutual funds outperform the market on average.b. Insiders earn abnormal trading profits.c. Every January, the stock market earns abnormal returns.3. Suppose that, after conducting an analysis of past stock prices, you come up with the following observations. Which would appear to contradict the weak form of the efficient market hypothesis? Explain.a. The average rate of return is significantly greater than zero.b. The correlation between the return during a given week and the return during the following week is zero.c. One could have made superior returns by buying stock after a 10% rise in price and selling after a 10% fall.d. One could have made higher-than-average capital gains by holding stocks with low dividend yields.4. Which of the following statements are true if the efficient market hypothesis holds?a. It implies that future events can be forecast with perfect accuracy.b. It implies that prices reflect all available information.c. It implies that security prices change for no discernible reason.d. It implies that prices do not fluctuate.5. Which of the following observations would provide evidence against the semistrong form of the efficient market theory? Explain.a. Mutual fund managers do not on average make superior returns.b. You cannot make superior profits by buying (or selling) stocks after the announcement of an abnormal rise in dividends.c. Low P/E stocks tend to have positive abnormal returns.d. In any year approximately 50% of pension funds outperform the market.6. The semistrong form of the efficient market hypothesis asserts that stock prices:a. Fully reflect all historical price information.b. Fully reflect all publicly available information.c. Fully reflect all relevant information including insider information.d. May be predictable.7. Assume that a company announces an unexpectedly large cash dividend to its shareholders.In an efficient market without information leakage, one might expect:a. An abnormal price change at the announcement.b. An abnormal price increase before the announcement.c. An abnormal price decrease after the announcement.d. No abnormal price change before or after the announcement.8. Which one of the following would provide evidence against the semistrong form of the efficient market theory?a. About 50% of pension funds outperform the market in any year.b. All investors have learned to exploit signals about future performance.c. Trend analysis is worthless in determining stock prices.d. Low P/E stocks tend to have positive abnormal returns over the long run. Chapter 141. Which security has a higher effective annual interest rate?a. A 3-month T-bill selling at $97,645 with par value $100,000.b. A coupon bond selling at par and paying a 10% coupon semiannually.2. Treasury bonds paying an 8% coupon rate with semiannual payments currently sell at par value. What coupon rate would they have to pay in order to sell at par if they paid their coupons annually? (Hint: what is the effective annual yield on the bond?)3. Two bonds have identical times to maturity and coupon rates. One is callable at 105, the other at 110. Which should have the higher yield to maturity? Why?4. Consider a bond with a 10% coupon and with yield to maturity _ 8%. If the bond’s yield to maturity remains constant, then in 1 year, will the bond price be higher, lower, or unchanged? Why?5. Consider an 8% coupon bond selling for $953.10 with 3 years until maturity making annual coupon payments. The interest rates in the next 3 years will be, with certainty, . Calculate the yield to maturity and realized compound yield of the bond.6. Philip Morris may issue a 10-year maturity fixed-income security, which might include a sinking fund provision and either refunding or call protection.a. Describe a sinking fund provision.b. Explain the impact of a sinking-fund provision on:i. The expected average life of the proposed security.ii. Total principal and interest payments over the life of the proposed security.c. From the investor’s point of view, explain the rationale for demanding a sinking fund provision.7. Bonds of Zello Corporation with a par value of $1,000 sell for $960, mature in 5 years, and have a 7% annual coupon rate paid semiannually.a. Calculate the:i. Current yield.ii. Yield to maturity (to the nearest whole percent, i.e., 3%, 4%, 5%, etc.).iii. Realized compound yield for an investor with a 3-year holding period and a reinvestment rate of 6% over the period. At the end of 3 years the 7% coupon bonds with 2 years remaining will sell to yield 7%.b. Cite one major shortcoming for each of the following fixed-income yield measures:i. Current yield.ii. Yield to maturity.iii. Realized compound yield.9. A 20-year maturity bond with par value of $1,000 makes semiannual coupon payments at a coupon rate of 8%. Find the bond equivalent and effective annual yield to maturity of the bond if the bond price is:a. $950.b. $1,000.c. $1,050.12. Consider a bond paying a coupon rate of 10% per year semiannually when the market interest rate is only 4% per half year. The bond has 3 years until maturity.a. Find the bond’s price today and 6 months from now after the next coupon is paid.b. What is the total (6 month) rate of return on the bond?14. A bond with a coupon rate of 7% makes semiannual coupon payments on January15 and July 15 of each year. The Wall Street Journal reports the asked price for the bond on January 30 at 100:02. What is the invoice price of the bond? The coupon period has 182 days.20. A 30-year maturity, 8% coupon bond paying coupons semiannually is callable in 5 years at a call price of $1,100. The bond currently sells at a yield to maturity of 7% (3.5% per half-year).a. What is the yield to call?b. What is the yield to call if the call price is only $1,050?c. What is the yield to call if the call price is $1,100, but the bond can be called in 2 years instead of 5 years?22. A 2-year bond with par value $1,000 making annual coupon payments of $100 is priced at $1,000. What is the yield to maturity of the bond? What will be the realized compound yield to maturity if the 1-year interest rate next year turns out to be (a) 8%,(b) 10%26. Alarge corporation issued both fixed and floating-rate notes 5 years ago, with terms given in the following table:a. Why is the price range greater for the 9% coupon bond than the floatingrate note?b. What factors could explain why the floating-rate note is not always sold at par value?c. Why is the call price for the floating-rate note not of great importance to investors?d. Is the probability of call for the fixed-rate note high or low?e. If the firm were to issue a fixed-rate note with a 15-year maturity, what coupon rate would it need to offer to issue the bond at par value?f. Why is an entry for yield to maturity for the floating-rate note not appropriate?27. On May 30, 1999, Janice Kerr is considering one of the newly issued 10-year AAA corporate bonds shown in the following exhibit.a. Suppose that market interest rates decline by 100 basis points (i.e., 1%). Contrast the effect of this decline on the price of each bond.b. Should Kerr prefer the Colina over the Sentinal bond when rates are expected to rise or to fall?c. What would be the effect, if any, of an increase in the volatility of interest rates on the prices of each bond?Chapter 152. Which one of the following statements about the term structure of interest rates is true?a. The expectations hypothesis indicates a flat yield curve if anticipated futureshort-term rates exceed current short-term rates.b. The expectations hypothesis contends that the long-term rate is equal to the anticipated short-term rate.c. The liquidity premium theory indicates that, all else being equal, longer maturities will have lower yields.d. The liquidity preference theory contends that lenders prefer to buy securities at the short end of the yield curve.8. Suppose the following table shows yields to maturity of zero coupon U.S. Treasury securities as of January 1, 1996:a. Based on the data in the table, calculate the implied forward 1-year rate of interest at January 1, 1999.b. Describe the conditions under which the calculated forward rate would be an unbiased estimate of the 1-year spot rate of interest at January 1, 1999.c. Assume that 1 year earlier, at January 1, 1995, the prevailing term structure for U.S. Treasury securities was such that the implied forward 1-year rate of interest at January 1, 1999, was significantly higher than the corresponding rate implied by the term structure at January 1, 1996. On the basis of the pure expectations theory of the term structure, briefly discuss two factors that could account for such a decline in the implied forward rate.16. Below is a list of prices for zero-coupon bonds of various maturities.a. An 8.5% coupon $1,000 par bond pays an annual coupon and will mature in 3years. What should the yield to maturity on the bond be?b. If at the end of the first year the yield curve flattens out at 8%, what will be the1-year holding-period return on the coupon bond?21. The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year-maturity coupon bonds with coupon rates of 12% (paid annually) is 5.8%. What arbitrage opportunity is available for an investment banking firm? What is the profit on the activity?22. Suppose that a 1-year zero-coupon bond with face value $100 currently sells at $94.34, while a 2-year zero sells at $84.99. You are considering the purchase of a2-year-maturity bond making annual coupon payments. The face value of the bond is $100, and the coupon rate is 12% per year.a. What is the yield to maturity of the 2-year zero? The 2-year coupon bond?b. What is the forward rate for the second year?c. If the expectations hypothesis is accepted, what are (1) the expected price of the coupon bond at the end of the first year and (2) the expected holding-period return on the coupon bond over the first year?d. Will the expected rate of return be higher or lower if you accept the liquidity preference hypothesis?。

交大网络教育国际金融复习题 (1)

国际金融复习题判断题(10题10分)单选题(10题20分)名词解释(5题20分)简答题(4题20分)计算题(1题15分)论述题(1题15分)1.国际金融学是研究本国内部均衡和外部平衡实现问题的一门学科 ------ 错2.中国当前的经济增长方式以内涵型增长为主。

------ 错3.安倍经济学推出的是一种以邻为壑的经济政策。

------ 对4.国际收支是一个流量的事后的概念。

------ 对5. 5.在国际收支平衡表中,凡资产增加负债减少的项目应计入贷方;反之,则记为借方。

------ 错6.经常账户和资本与金融账户都属于自主性交易账户。

------ 错7.支出转换型政策主要包括汇率政策补贴和关税政策以及直接管制。

------ 对8.本国货币贬值会使本国国际收支改善本国贸易条件恶化。

------ 错9、直接标价法下数值变大,说明本国货币( B,外币升值,本币贬值)10.根据掉期率决定远期汇率的升贴水时,掉期率主要是针对美元的。

------ 对11.国际收支状况一定会影响到汇率。

------ 对12.根据利率平价说,利率相对较高的国家未来货币升水的可能性较大。

------ 对13.根据黏性价格的货币分析法,汇率发生超调的原因与资产价格的调整速度快于商品价格的调整速度有关。

12.本币贬值对经济产生扩张性的作用。

------ 错13.外部均衡就是国际收支平衡,只要采取了适当的手段消除了国际收支差额,就实现了外部均衡。

------ 错14.蒙代尔分配法则指出,应当用财政手段调节外部不平衡,用货币手段调节内部不平衡。

------ 错15.当内部经济出现衰退和失业增加、外部经济出现国际收支顺差时,采取扩张性的财政货币政策来实现内部均衡和外部平衡这两个目标的冲突。

------ 对16.根据本章介绍的内外均衡分析新框架,内部均衡和外部平衡的短期冲突,在一定程度上能够由市场经济的自动调节来消除。

------ 对17.在中期跨度内,劳动生产率增长和技术进步是经济增长的主要推动因素,在此过程中,为使内部均衡和外部平衡同时实现,需要本币贬值和物价上涨。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

3. 跨国并购的动因是什么?

答:①企业增长或发展的需要;②技术因素;③产品优势和产品差异;④政府的政策;⑤汇率;

⑥政治、经济稳定性;⑦劳动力成本和生产率差异;⑧银行追随顾客;⑨多样化经营;⑩确保原材料供应。

4. 什么是非股权经营?

答:非股权经营是指跨国公司在东道国企业中不参与股份,通过向东道国企业提供技术、管理、销售渠道等与股权没有直接联系的各项服务(无形资产)参与企业的经营活动,从中获取相应的利益与报酬。

在非股权参与方式中,跨国公司并不持有在东道国企业的股份,而只是通过与东道国的企业建立某些业务关系来取得某种程度的实际控制权,从而实现本公司的经营目标。

三、案例分析题

耐克公司是美国著名的运动鞋公司,它是1964 年由美国俄勒冈大学的长跑运动员费尔和他的教练波曼合伙组建的,两人初始投资是各300 美元,委托日本的一家鞋厂按波曼的设计试制了300 双球鞋。

最初的球鞋储存在费尔父亲家的地下室里,每逢比赛,由费尔和波曼带到田径运动场上去推销。

1972 年,奥运会田径预赛在美国俄勒冈举行,费尔和波曼说服了部分马拉松跑运动员穿着耐克鞋参赛。

结果,其中有四名进入预赛前七名,费尔和波曼趁机大做广告,耐克运动鞋从此声名大振,不断发展壮大。

耐克公司1994 年的销售额已经达到38 亿美元,产品销往81 个国家。

但特别值得我们注意的是从耐克的最初发迹到以后的成长发展,耐克公司本身并不制造球鞋,97%以上的耐克球鞋的生产采取在第三世界国家合同承包、加工返销的形式进行,其中2/3 是在韩国生产的,然后由耐克公司收购,由耐克公司独家在发达国家销售。

分析耐克公司成功的奥秘。

答:耐克公司赖以成长壮大的秘密不在于制造环节,而在于其对产品设计和广告营销环节的控制,这用价值链原理很容易解释。

因为在运功鞋行业,其制造环节料重工轻,规模经济效益有限,生产工艺成熟,而其研究和广告推销环节,固定成本高,产品的广告边际成本低,经济规模效应高,是应该关键控制的战略环节。

耐克球鞋在市场上主要是依靠其最佳设计和高档品牌为号召,不惜重金聘请了乔丹等顶级明星在美国电视节目收视率最高的黄金时间做广告,成功地塑造了耐克球鞋的高档名牌形象。

耐克这种“抓住设计,营销,外包生产制造”的价值链战略是其成功的奥秘所在。

这个案例给我们的重要启示是:通过价值链分析来剖析企业竞争优势,从而确定正确的经营战略是企业成功的关键之一。