国际结算chapter 7-documents.

国际结算chapter 7-documents

❖Some issues relating to documents under the credit 1.Ambiguity as to issuers of documents 单据签发

人 Terms such as "first class", "well known", "qualified",

---Article 3,UCP600

3

Documents Under the Credit

2.Original Documents and Copies 单据的 正本和副本

a. At least one original of each document stipulated in the credit must be presented.

6

【实战案例】关于信用证对副本的要求

当信用证有要求提供单据的副本时,出口商往往是漫不经 心的。例如:有个信用证的条款是这样的:“Full set of clean on board ocean B/L, 3 original and 2 N/N copies”. 对 于这三份正本提单,出口商不敢怠慢,做得很谨慎。但 是遇到2份 non –negotiable copies 时,那就很随意了。 在复印机上制成二份了事。而开证银行由此而提出的拒 付不在少数:“Photocopies of B/L presented instead

国际结算(中文)

国际结算概述

教学目的:通过本章的学习可以从整体上把握 本学科的基本内容。 教学重点:国际结算的概念、特征、研究内容, 国际结算中的银行等。 教学难点:国际结算的特征,国际结算中的银 行关系

第一章

国际结算概述

一、国际结算的含义与内容p151 二、国际结算的历史与发展p151-152 三、国际结算方式的具体内容 四、国际结算的基本要素(三要素:结算工具、结算

1.国际结算概述

2.国际结算票据

票据基本知识

汇票及案例

本票及案例

支票及案例

3.国际结算方式

汇款及案例

托收及案例

信用证及案例

银行保函、备用信用证及案例

4.国际结算单据

单据的基本知识

单据制作及范例

单据的审核及案例

5.国际非贸易结算资

Chapter 1. Introduction to International Settlement

国际结算中的单据

在国际贸易结算中,普遍实行“推定交货”— —又称象征性交货,是相对“实物交货”而言 的。实质就是货物单据化,以货物单据代表货 物所有权。国际贸易结算的实体和依据就是货 运单据。 国际结算的单据是指贸易结算中涉及的单据, 例如发票、包装单、货运单据、保险单、产地 证、函抄与汇票等单据。

Methods

Other methods Factoring Letter of guarantee Forfeiting

Documents

basic Invoice Additional Packing list Weight memo Certificate of Original All kinds of Certificates

国际结算CH7 Other Documents

Chapter 7 Other Documents7.1Introduction and learning objectives7.2Insurance documents7.3Financial and commercial documents, anddocuments for official purposes7.4Questions©Wang Shanlun7.1 Introduction and learning objectives Chapter 6 covered the examination of documents in relation to the carriage of goods in international trade. This chapter covers the study of the following documents:Insurance documentsFinancial documentsCommercial documentsOfficial documentsThis chapter also answers the following questions:How are goods insured during the journey from beneficiary to applicant?What is the value of goods transported?What is the nature of the goods transported?©Wang ShanlunLearning objectivesTo introduce documents, other than transport documents, as commonly seen in documentarycredits;To appreciate some of the requirements of merchants and countries of export and import.To give an insight into the practical aspects of checking the documents described in this chapter.©Wang Shanlun©Wang Shanlun7.2 Insurance documents Insurance policy, insurance certificate and cover note Insurance terms as commonly seen AverageFranchise or an excess (deductible) Deck shipmentClaim payable at …Warehouse-to-warehouse clause ©Wang Shanlun7.2 Insurance documents General requirementsOnly one insurance document should be submitted under a credit covering the same risks for the same shipment. There may, however, be the need, in certain circumstances, to spread the risk between insurers and, in such cases ISBP paragraph 174 states …An insurance document should not evidence cover for goods not requested in the credit.Insurance documents must appear to have been countersigned where there is a requirement for such on the face of the document.Insurance documents must be endorsed as required to assign the rights to the applicant or other party named in the credit. (ISBP Para.179/180)©Wang Shanlun A study of the applications of the provisions of UCP600 in insurance documents commonly stipulated in credits UCP600 Art.28 ISBP681 Para.170~180 Art.28(a) –issue and signature Art.28(a) –open cover Art.28(b) –originalsArt.28(c) –cover notesArt.28(e) –date of issuanceArt.28(f) –currency and minimum coverArt.28(g~j) –types of insurance coverCommon discrepancies that arise upon document checking1.The currency in which the insurance document is expressed is notthat of the credit.2.The amount of insurance is insufficient.3.The merchandise description is not consistent with the credit orinvoice description.4.The port of loading or place of taking in charge is not in accordancewith the credit.5.Specific risks as stipulated in the credit are not annotated in orcovered by the document.6.Certificates are not countersigned where such countersignature isrequired.7.The insurance policy is not endorsed in terms of the credit.8.The effective date for insurance is later than the date of shipment.9.All the originals shown on the document as issued are not presented.©Wang Shanlun7.3 Financial and commercial documents, and documents for official purposesFinancial documentsISBP681 Para.43~56Corrections and alterationsCalculation of maturityPayment at maturity©Wang ShanlunCommercial documentsCommercial invoiceIssued by The beneficiary of the credit.Content A description and value of goods and terms of sale and other detail as stipulated in the credit. It would be considered safe toshow the wording of the credit precisely and additional informationshould not be in conflict with such wording.Purpose To evidence the manner in which the drawing under the credit is made up and to evidence the sale of goods in the termsrequired by the credit.UCP600 Art.18, ISBP681 Para.57~67©Wang ShanlunCommercial documentsCertified invoiceIssued by The beneficiary of the credit.Content Similar to the commercial invoice, together with certification by the beneficiary or third party interms of the credit. eg, a beneficiary may be required tocertify that the contents are correct and in terms of thepro forma invoice.Purpose To satisfy a specific concern of the buyer in relation to the certification required.©Wang ShanlunCommercial documentsCertificate of analysisCertificate of weightInspection certificatePacking listWeight listUCP600 Art.14(f)©Wang ShanlunDocuments for official purposesCertificate of originISBP681 Para.181~185Consular invoiceLegalised invoiceExport licenceHealth certificateUCP600 Art.3, 14(d), 14(f)ISBP681 Para.13, 14, 15, 22, 41, 42©Wang ShanlunCommon discrepanciesDiscrepancies on financial documentsDraft not signed by the beneficiary.Draft signed but no indication of the name of the beneficiary.Draft not endorsed as required.Draft not drawn on the correct party.Amount is in excess of the credit.Words and figures do not agree.Tenor of draft shown incorrectly.©Wang ShanlunCommon discrepanciesDiscrepancies on commercial invoicesNot issued by the beneficiary.Not signed as required by the credit.Description of goods on invoice does not correspond with the description of goods shown on the credit.Invoice not visaed or legalized as required by the credit.Quantity of goods shipped exceeds tolerance of 5% in sub-article 30(b).Unit price not as stipulated in the credit.Partial shipment effected when credit prohibits part shipment.Shipping marks and numbers on invoice not consistent with marks and numbers on the transport documents.©Wang ShanlunCommon discrepanciesCertificate of originIndicates the origin of the goods to be other than as stipulated in the credit.Certificate not issued by party as stipulated in the credit.Certificate does not indicate that it has been legalized and visaed as required by the credit.Legalization not in terms of the credit.Data on document in conflict with other documents.©Wang Shanlun7.4 Questions1.Do you clearly understand the differences betweeninsurance policies, insurance certificates, declarationsunder open cover and cover notes?2.Why is it important to examine the insurance document toascertain where claims are payable if the credit stipulates claims payable at a particular city or country?3.Because document examiners cannot be expected to readthe entire text of the insurance document, can you recallthe elements for which you will look and which form yourown functional standard?©Wang Shanlun7.4 Questions4.On which parties are drafts usually drawn underdocumentary credits and on which party should they not be drawn?5.Which type of credit availability will never call forpresentation of a draft?6.Do you understand the impact and application of thevarious tolerances defined in article 30?7.Why must documents issued for official purposes beprecise regarding the issuer and data content?©Wang Shanlun。

国际结算(双语)第七章:银行保函 chapter7 Guarantee

Can be the primary ,and also can the issuing bank will take the be the secondary primary liability to effect payment. Under URDG758, the governing law and jurisdiction for letter of guarantee business are clearly indicated. UCP600 does not stipulate the governing laws or jurisdiction when disputes under letter of credit happens.

2. Differences

Bank Guarantee Documentary Letter of Credit

The undertaking of the issuing bank

The documents required for payment The liability for payment The law and custom

1. Commons • Both the Bank guarantee and documentary credit are settlement method used in international trade; • They are both issued at the request of the applicant, in favor of the beneficiary, promising the payment obligation when complying documents are presented. • The banks will only deal with documents, while not being responsible for the authenticity and effectiveness of the documents, banking credit replaces the commercial credit, which in a great degree facilitate the development of international transactions.

第七章 国际结算中的单据

(二)背面条款

1、首要条款 principle items 2、承运人的责任条款 liability of carrier 3、转运、包装与唛头条款 transhipment、package & marks 4、赔偿条款 compensation items 5、留置权条款 lien items

6、特殊货物条款 special goods

第七章 国际结算中的单据

Documents in International Settlement

u 单 据 概 述(General Introduction)

u 运输单据(Bill of Lading)

u信用证项下的跟单汇票(Drafts drawn

under a Letter of Credit)

(二)按货物是否已装船为标准划分: 已装船提单Shipped B/L or On board B/L : 承运人在货物确已装船后才签发的提单; 收妥备运提单Received for Shipment B/L : 承运人在收到货物但尚未装船期间,应托运人的要 求而签发的提单。

(三)按运输方式分:

直达提单Direct B/L :承运人签发的将货物从起运港装船 后直接运至目的港卸货的提单。

豁免作了规定,在一定程度上保护了货方的利益,但其内容有明

显偏袒船方利益的一面。

(二)《维斯比规则》(Visby Rules) 全称是《修改海牙规则的协定书》或《布鲁 塞尔协定书》。该规则于1977年6月正式生效,但 至今仍只有10多个国家承认该规则。《维斯比规

则》并未对《海牙规则》的基本原则作出实质性

修改,只是扩大了公约的适用范围,提高了货物 损害赔偿的最高限额,因而在更大程度上保护了 货方的利益。

国际结算第七章国际贸易结算中的单据

1、首文(Heading)部分。 主要写明基本情况:发票名称及号码、合约或定 单号码、发票制作日期和地点、运输工具、装货 地点、卸货地点等。

2、正文(Body)部分。 是说明履约情况的部分,主要是通过对货物和货 价的描述提供履约证明。

3、结文部分。 其最重要的内容是出口商的签章(exporter’s signature),信用证项下,必须是受益人签发发 票。除此之外,还可按需要标注进出口许可证号、 外汇批准号、税则号等内容,或证实性文句。

托运人 Shipper/Consignor

承运人 Carrier

收货人 Consignee

出口方/进口方 船方

进口方/第三方

被通知人 Notify Party

受让人 Transferee

持单人 Holder

进口方或其代理 接受转让方 收货方/受让人

(三)海运提单的作用

1、货物收据。它是承运人确认从托运人处收到货 物后签发的一纸证明。

1、按提单签发时货物是否确实已经装上货船,分为 “已装船提单”(Shipped on Board B/L)及“待运 提单”(Received for Shipment B/L) 。 2、按运输过程中是否转换运输工具或转换船只,分为 直达提单(Direct B/L)、转船提单 (Transshipment B/L)和联运提单(through B/L) 等。

就广义而言,发票包括商业发票、海关发票 、形式发 票、领事发票、样品发票、厂商发票、 证实发票等。

就狭义而言,通常是指商业发票。

商业发票的内容

1.首文部分

2.本文部分

发票名称

唛头

发票的抬头

商品描述

发票号码及日期 数量

合同号、信用证号等 单价及总价

国际结算7章

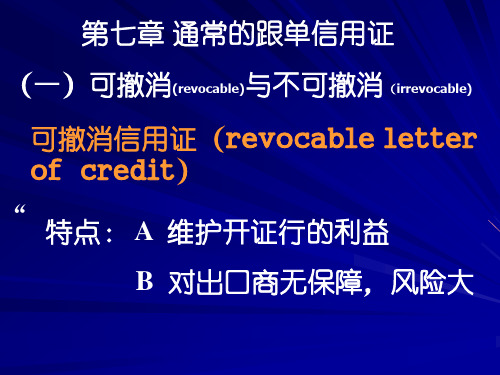

(一)可撤消(revocable)与不可撤消(irrevocable) 可撤消信用证(revocable letter of credit)

“

特点: A 维护开证行的利益 B 对出口商无保障,风险大

注意事项 : 1 不规定自由议付的使用方式 2 装运前一定要询问指定银行 3 可撤销信用证适于特殊贸易

假远期信用证(usance letter of credit payable at sight) 假远期信用证的功能条款 如usance drafts to be negotiated at sight basis and discounted by us (issuing bank) ,discount charges and acceptance commission are for importer`s account.

假远期L/C:

开证申请人远期付款而受益人即期收汇的L/C。

做法:1、合同中规定即期付款L/C 2、申请人开来L/C中规定汇票 制成远期,付款人为申请人 3、受益人作好单据与远期汇票 后寄至开证行,开证行审单合格后即期 付款

4、开证行通知申请人审单,申 请人审单后对远期汇票进行承兑就 可提走单据。 5、在汇票到期前,申请人将货 物卖出,资金回笼。在汇票到期时 将钱还给开证行。

在信用证上列有这样的文句,以示可撤销信用证

This credit is subject to cancellation or amendment at any time without prior notice to the beneficiary. This revocable credit may be cancelled by the issuing bank at any moment without prior notice .

国际结算与单证制作课件:第7章 国际结算中的单据

2022年2月16日星期三

(二)正文(body)部分

1 货物名称

2 货物规格

3 货物的包装、件数和数量

4 货物的重量

5 单价和发票金额

6 唛头及件号

2022年2月16日星期三

(三)结文(complementary clause)部分 1. 发票上加注各种证明 2.信用证要求多份发票时的正副 本发票

2022年2月16日星期三

2022/2/16

16

四、其他类型的发票

1. 海关发票 2. 领事发票 3. 厂商发票 4. 形式发票 5. 样品发票 6. 寄售发票 7. 证实发票

2022年2月16日星期三

第二节 货物运输单据 导入:

在一份采用海洋货物运输的CIF 合同中,出口企业如何履行货物运输 义务。

TOTAL NUMBER OF CONTAINERS SAY TOTAL PACKAGES IN ONE HUNDRED AND FIFTY ONLY (IN WORDS)

FREIGHT&CHARGES

REVENUE TONS RATE PER PREFPARIEDIGHTCPORLLEEPCATID

2.FULL SET OF CLEAN ON BOARD B/L ISSUED TO OUR ORDER, MARKED NOTIFYING APPLICANT AND FREIGHT PREPAID AND SHOWING FULL NAME AND ADDRESS OF THE RELATIVE SHIPPING AGENT IN EGYPT.

3.根据资料缮制提单

海运提单一般就是指港至港已装船提单(Port to port shipped on board marine bill of lading),习惯简称为 海运提单 .

国际结算(第七章)

第三节 保险单据

一、保险单据的定义 保险单据是保险人与投保人之间订立的保险合 同的证明文件,它是保险人对投保人的承保证 明,也是反映双方权利、义务关系的契约。

在被保险货物发生保险责任范围内的损失时,

保险单据是保险索赔和理赔的主要依据

二、保险单据的出单人 保险单据必须看似由保险公司或承保人或其代理人或代表 出具并签署。代理人或代表的签字必须表明其系代表保险 公司或承保人签字。 保险人(insurer)或称承保商(underwriter),也称保 险方,是指保险合同中经营保险业务的一方当事人。 保险代理人(insurance agent)又称保险代理商,是根据 代理合同向保险人收取代理手续费,并以保险人的名义为 保险人代办保险业务的人。

未列明,便构成不符。

(二)唛头

唛头(Mark)又称运输标志,是指为了使货物在装卸、 运输和保管的过程中便于承运人和收货人识别,而在货物 的运输包装上所标注的识别标志。 唛头通常包括主标志、目的港标志和件号标注,有时也会 加注原产地标志。 在审核发票唛头时,需要注意: 1. 信用证有唛头细节,则载有唛头的单据必须显示这些细 节,但额外信息可以接受,只要其与信用证的条款不相矛 盾。

(六)汇票中的对价条款 汇票中的对价条款(Value received for×××of ×××)通常填写交易货物的件 数及品名。 Value received for 200 pieces of mail box

(七)出票条款 出票条款(Drawn Clause)是信用证项下汇票必须加列

UCP600第3条关于日期计算是解释: on or about to、until· · · to、from、between

中文 第7章 国际结算

第一节

一、商品品质的含义

贴现:远期汇票的持票人可以选择持有汇票直到有效期取得票面金额或选择在 有效期前贴现汇票。贴现是指银行用低于票面金额的价格购买远期的已承兑的汇票。 贴现时,银行计算了票面金额的现值后把净款支付给汇票的持有人。由于汇票转让 日至到期日的利息要从票面金额中扣除,所以汇票的现值小于票面金额。例如,一 张6000美元的已承兑汇票,见票后90天付款。持票人要求银行于承兑当日贴现,如 贴现率为6%, 则贴现息计算如下:

2.本票和汇票的区别 ◎本票是支付“承诺”,然而汇票是支付“命令”。 ◎本票只涉及两个当事人:出票人和收款人,但汇票涉及三个基本当事人:出票人、受票 人和收款人。 ◎本票是没有承兑,因为本票的出票人就是其付款人,但是汇票能承兑。 ◎本票由出票人负全责,但汇票仅在承兑前由出票人负责,承兑后则由承兑人负责。 ◎本票只能开一式一份,但汇票能开一套两张。

23

第一节

三、支票

3.支票和汇票的不同点 ◎汇票的受票人可以是任何人,然而支票的受票人必须是银行。 ◎支票是即期付款的,没有承兑,但远期汇票可以“承兑”。 ◎出票人是支票的主债务人,但汇票的出票人仅在汇票承兑之前作为汇票的主 债务人,汇票承兑后,承兑人成了汇票的主要债务人。 ◎支票只能开一张,但汇票能开一套两张。

应用外语系 基础L平O台G课O程

国际贸易实务(双语版)

第7章

国际结算

广东轻工职业技术学院 应用外语系

1

国际结算

众所周知国际结算是国际贸易中最重要的,因为卖方最感兴趣的就是 赚钱。但是,由于地理界限、风俗习惯和贸易惯例的影响,国际结算是 复杂和困难的。因此好好理解不同的支付方式能帮助我们解决在国际贸 易中遇到的难题。本章讨论国际支付中涉及的票据、汇款和四种基本的 支付方式。

国际结算chapter 7-documents.

【实战案例】关于信用证对副本的要求 当信用证有要求提供单据的副本时,出口商往往是漫不经 心的。例如:有个信用证的条款是这样的:“Full set of clean on board ocean B/L, 3 original and 2 N/N copies”. 对 于这三份正本提单,出口商不敢怠慢,做得很谨慎。但 是遇到2份 non –negotiable copies 时,那就很随意了。 在复印机上制成二份了事。而开证银行由此而提出的拒 付不在少数:“Photocopies of B/L presented instead of N/N copies of B/L”. 正本提单显示有“Original”字样。而不可转让副本提单则 标注有“Copy- non – negotiable ”字样。ICC 有关案例曾 有这样的说明,必须根据信用证的具体要求提交相应的 副本。一套提单中的“non-negotiable copy”指的是一种 特定的副本提单,不象一般copy那样泛指任何副本。因 此,当信用证要求N/N copy时,提交一份包括 7 Photocopy 在内的普通副本是不能接受的。

Documents Under the Credit

1

Documents Under the Credit

Some issues relating to documents under the credit Documents

2

Documents Under the Credit

Some issues relating to documents under the credit 1.Ambiguity as to issuers of documents 单据签发 人 Terms such as "first class", "well known", "qualified", "independent", "official", "competent" or "local" used to describe the issuer of a document allow any issuer except the beneficiary to issue that document. ---Article 3,UCPd alterations 单据的修正 和变更

国际结算09级(11)

“Insufficiently packed” “Ironstrap loose or missing” “Rain Wet” “Packaging soiled by content” “Second-hand cases” “Content leaking” “Used Drums” “Three packages in damaged condition” “Short shipped five cases” “Two bags torn” “The Carrier shall not be responsible for rusty of the goods”

第一节 商业发票 (Commercial Invoice)

一、商业发票的概念 出口商向进口商开立的详细说明所装运货物的清单,是出、 进口商交接货物和结算货款的主要单据。 二、商业发票的主要作用 1. 是履约的证明文件 2. 是收付货款和记账凭证 3. 是报关纳税的依据 4. 代替汇票作为付款的依据 三、商业发票的基本内容 (一)首文(Heading)部分 1.发票名称 2.发票号码与日期

第二节 运输单据 (Transport Documents)

海运提单(Ocean/Marine Bill of Lading, B/L) 一、提单的含义 提单是承运人(Carrier)在收到货物后签发给托运人的一 种运输单据,确认已收到托运货物或已将托运货物装上指 定的船舶。 二、提单的性质和作用 1.是货物收据(Receipt for the Goods) 2.是运输合同或运输合同的证明(Contract of Carriage or Evidence of Contract of Carriage) 3.是物权凭证(Document of Title of the Goods) 三、提单的种类Fra bibliotek

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

【实战案例】关于信用证对副本的要求 当信用证有要求提供单据的副本时,出口商往往是漫不经 心的。例如:有个信用证的条款是这样的:“Full set of clean on board ocean B/L, 3 original and 2 N/N copies”. 对 于这三份正本提单,出口商不敢怠慢,做得很谨慎。但 是遇到2份 non –negotiable copies 时,那就很随意了。 在复印机上制成二份了事。而开证银行由此而提出的拒 付不在少数:“Photocopies of B/L presented instead of N/N copies of B/L”. 正本提单显示有“Original”字样。而不可转让副本提单则 标注有“Copy- non – negotiable ”字样。ICC 有关案例曾 有这样的说明,必须根据信用证的具体要求提交相应的 副本。一套提单中的“non-negotiable copy”指的是一种 特定的副本提单,不象一般copy那样泛指任何副本。因 此,当信用证要求N/N copy时,提交一份包括 7 Photocopy 在内的普通副本是不能接受的。

5

Documents Under the Credit

d. If a credit requires presentation of copies of documents, presentation of either originals or copies is permitted. e. If a credit requires presentation of multiple documents by using terms such as "in duplicate", "in two fold" or "in two copies", this will be satisfied by the presentation of at least one original and the remaining number in copies, except when the document itself indicates otherwise. 6

3

Documents Under the Credit

2.Original Documents and Copies 单据的 正本和副本 a. At least one original of each document stipulated in the credit must be presented. b. A bank shall treat as an original any document bearing an apparently original signature, mark, stamp, or label of the issuer of the document, unless the document itself indicates that it is not an original. 4

Documents Under the Credit

c. Unless a document indicates otherwise, a bank will also accept a document as original if it: i. appears to be written, typed, perforated or stamped by the document issuer’s hand; or ii. appears to be on the document issuer’s original stationery; or iii. states that it is original, unless the statement appears not to apply to the document presented.

Chapter Seven

Documents Under the Credit

1

Documents Under the Credit

Some issues relating to documents under the credit Documents

2

Documents Under the Credit

一般讲来,当信用证仅要求提交副本(copy)时,而未 明确要求是何种副本。如果提交复写副本,影印副本 或者电脑系统制作的副本均被认为是允许的。但是最 近中国银行收到一个拒付电,对方提出的拒付内容是 这样的“It’s remitted a copy of GSP Form A instead of photocopy”。也许开证行的本意是要求提供一份影印 副本,而实际受益人交来的是一式数联中的一个副本, 这样就被认为和信用证规定不相一致了。另有一个信 用证的规定是这样的:“Signed commercial invoice in five fold .”通常的做法是提交一份正本,其余为副本 即可。但是副本无须一定要签字,而这里的Signed一 词应被理解成副本发票也需要签字,这就要引起出口 商注意了。简言之,受益人在单据副本的制作和处理 上是不能粗心大意的,对于信用证的具体条款所规定 的内容一定要进行辨析。 8

Some issues relating to documents under the credit 1.Ambiguity as to issuers of documents 单据签发 人 Terms such as "first class", "well known", "qualified", "independent", etent" or "local" used to describe the issuer of a document allow any issuer except the beneficiary to issue that document. ---Article 3,UCP600