ACCA财务管理基础练习题及答案

ACCA《财务成本管理基础》练习题

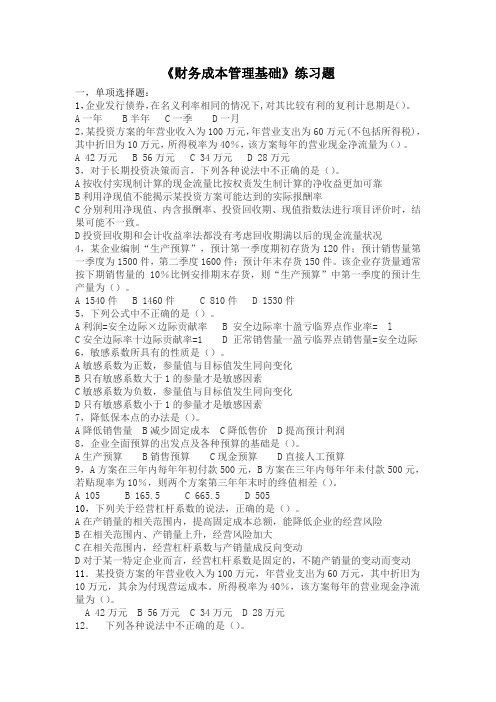

(注:表中制造费用、管理费用中的80%是固定 成本)

项目 销售收入 销售成本 其中:直接材料 生产工人计件工资 制造费用

销售税金及附加 (售价的4%) 门市销售计件工资 管理费用 税前利润

单位产品 10 7.725 4.025 0.575 3.125 0.4 0.5 1.00 0.375

全部产品(8万双) 800000 618000 322000 46000 250000 32000 40000 80000 30000

其中,制造费用中有一项是机器设备折旧 费,全年共180000元,按月平均分摊;其 余制造费用随产量而变动;销售税金及附 加按销售价格的2%计算得出;营业及管理 费用全部是固定成本,全年共120000元, 也是按月平均分摊。假设每月的产销量相 等,不考虑其它费用。

此时,销售经理收到一份特殊订单:5000盏 灯,每盏灯的价格是13元。他就这一订单 请示总经理,总经理抱怨说:“这价格确 实太低了!这个价格还不够弥补成本,更 何况为生产这盏灯还要花费2000元的设计 费!就算它不会对正常生产和销售产生影 响,我们也不能接受这笔订单。我们已经 亏损了,接受它,只会对企业造成更大的 亏损!”

年初东方宾馆直接来厂订货30000双,但 每双只出价7.5元,而且必须一次全部购置,否 则不要。此项业务不会影响市场上的正常需要 量。 对东方宾馆订货,厂长认为对方出价低于 每双的成本,而且还影响了正常生产能力,可 能造成亏损,不应接受。 生产科长算了一笔帐,认为即是减少正常 销售10000双,接收这笔订单仍然有利可图。 销售科长认为正常销售量应该保证,接受 这笔订单后,不足的生产能力可采取加班的方 法弥补。但每双要支付额外加班费1.8元,其它 费用不变。

案例分析1:

光明公司是一家灯具生产厂,全年的最大生 产能力是40000盏灯。该公司的总经理近日 心情不好,因为他才阅读了一份本年度1— —9月份的会计报表,如下:

ACCA财务管理基础练习题及答案

《财务成本管理基础》练习题一,单项选择题:1,企业发行债券,在名义利率相同的情况下,对其比较有利的复利计息期是()。

A一年 B半年 C一季 D一月2,某投资方案的年营业收入为100万元,年营业支出为60万元(不包括所得税),其中折旧为10万元,所得税率为40%,该方案每年的营业现金净流量为()。

A 42万元B 56万元C 34万元D 28万元3,对于长期投资决策而言,下列各种说法中不正确的是()。

A按收付实现制计算的现金流量比按权责发生制计算的净收益更加可靠B利用净现值不能揭示某投资方案可能达到的实际报酬率C分别利用净现值、内含报酬率、投资回收期、现值指数法进行项目评价时,结果可能不一致。

D投资回收期和会计收益率法都没有考虑回收期满以后的现金流量状况4,某企业编制“生产预算”,预计第一季度期初存货为120件;预计销售量第一季度为1500件,第二季度1600件;预计年末存货150件。

该企业存货量通常按下期销售量的10%比例安排期末存货,则“生产预算”中第一季度的预计生产量为()。

A 1540件B 1460件C 810件D 1530件5,下列公式中不正确的是()。

A利润=安全边际×边际贡献率 B 安全边际率十盈亏临界点作业率= lC安全边际率十边际贡献率=1 D 正常销售量一盈亏临界点销售量=安全边际6,敏感系数所具有的性质是()。

A敏感系数为正数,参量值与目标值发生同向变化B只有敏感系数大于1的参量才是敏感因素C敏感系数为负数,参量值与目标值发生同向变化D只有敏感系数小于1的参量才是敏感因素7,降低保本点的办法是()。

A降低销售量 B减少固定成本 C降低售价 D提高预计利润8,企业全面预算的出发点及各种预算的基础是()。

A生产预算 B销售预算 C现金预算D直接人工预算9,A方案在三年内每年年初付款500元,B方案在三年内每年年未付款500元,若贴现率为10%,则两个方案第三年年末时的终值相差()。

2021年ACCA考试模拟试题

2021年ACCA考试模拟试题:财务管理(1)1.在有限责任公司中,所有者的责任仅限于A.公司的债务B. 已发行普通股的市场价值C. 已发行普通股的票面价值D. 注册资本的价值2. 历史成本原则A. 不适用于资产负债表上的任何资产项目B.适用于资产负债表上某些负债项目C.适用于资产负债表上某些资产项目D. 适用于资产负债表上所有资产、负债项目3. 在进行财务比率分析时,假设货币价值A. 保持不变B. 变化可以预测C. 变化不可预测D. 不相关4. 企业评价投资项目时,计算全部现金流入量、现金流出量的现值,并将其进行比较,所得到的计算结果称为A. 回收期B.内部收益率C.会计报酬率D. 净现值5. 有4种评价投资的主要方法,其中考虑了货币时间价值的方法有A. 净现值法和内部收益率法B.内部收益率法和回收期法C.回收期法和会计报酬率法D. 会计报酬率法和净现值法6. 在存在资金限额的条件下,备选方案的排序应按下列哪种标准来进行A.现在已筹集到的资金的每元净现值B.尚需筹集的资金的每元净现值C. 尚需筹集的资金的每元内部收益率D.现在已筹集到的资金的每元内部收益率7. 在投资项目评价中,税款支出应A. 包含于现金流量之中B. 不包含在现金流量之中C. 包含于利润之中D.不包含在利润之中8. 抵押贷款是【】A. 一方以资产为担保借钱给另一方B.一种法律责任,以拥有的资产作担保的一项贷款C.一方向另一方借钱,并且以财产作担保,但不一定承担法律责任D.将款项支付给贷出方,其担保物是财产9. 营运资本应该【】A. 尽可能多B. 与企业的经营规模相适应C. 尽可能少D. 与长期资本一样多10. 存货周转率反映【】A. 商品销售的速度B. 商品付款的速度C. 客户购买存货付款的速度D. 购买商品的速度11. 一项兼并受到目标公司董事的反对,这项兼并称为【】A. 善意兼并B. 敌意兼并C. 横向兼并D. 企业的分立12. 给予现有普通股东购买新增发股票的权利是【】A. 发行可转换证券B. 发放贷款C. 发放奖金D. 发行优先认股权2021年ACCA考试模拟试题:财务管理(2)The following information should be used when answering questions 1, 2 and 3.ScenarioCAET have implemented a bespoke Human Resources (HR) system. The system has gone live but it has not proved very popular or successful, with users claiming that it only partly fulfils their requirements. A consultant has been hired toexamine their claims and to suggest how their concerns might be tackled.The consultant’s report has highlighted the role played by the Requirements Specification. He suggests that theRequirements Specification’s reliance on ambiguous textual specifications has led to problems of ill-defined and poorlycommunicated requirements. He claims that the‘analyst’s failure to use diagrammatic models has meant that manyrequirements were not fully understood before they were programmed. Specifications without diagrams are very difficult toquality assure.’ His report quotes several examples of textual specifications. Two specifications are reproduced below;Specification 1(field names are shown in italics)The system should hold information about Jobs (job number, job description, grade) and about the Departments (department name, department head) that these Jobs are in. A Department may have many Jobs allocated to it, but oneJob is only in one Department. When these Jobs become vacant they should be advertised in both Internal and Externalmedia. The information that must be stored isdate advertised, size of advertisement, noticeboard location(for internaladvertisement only),newsletter reference(for internal advertisement only),newspaper edition(for external advertisementonly) and cost of advertisement(for external advertisement only). Information about Applicants (applicant name, applicantaddress) is required, specifying which Job they are applying for and where they saw the Job advertised.Specification 2When an application form is received from an Applicant, a Clerk enters the information on the form into the system. As itis entered, it is validated against Job details to ensure that the Applicant is applying for a valid Job. Once details have beenentered they are stored on an Applicant database. Overnight a batch process is run to send an acknowledgement letter toeach Applicant. The date that the letter is sent is noted on the Applicant details held in the system.Redefinition ProjectThe consultant has suggested a Redefinition Project to address the problems encountered by the users. He says that,‘I am suggesting a mini-project with agreed Terms of Reference and a project plan. These problems need to be addressedin a planned manner’.The consultant is keen to stress that he does not wish to over-engineer the software solution. ‘We have to ensure that thetrade-off between time, cost and quality is appropriate for the delivered software’, he says, ‘the delivered software must beappropriately located on the time/cost/quality triangle.’1The consultant has recognised that ambiguous textual specification has contributed to the software’s problems. Heclaims that the ‘analyst’s failure to use diagrammatic models has meant that many requirements were not fullyunderstood before they were programmed.’ The implication is that the use of such diagrammatic models in analysiswould have solved many of the ambiguities of the specification.(a)Specification 1 in the scenario describes static structures, which could be modelled with a class model, entity-relationship model or logical data structure model.(i)Briefly explain the notation of EITHER a class model OR an entity-relationship model OR a logical datastructure model;(4 marks)(ii)Using this notation, model the information given in Specification 1. Note any assumptions you havemade or issues you would need to clarify with the user. Your answer should indicate the fields in eachentity/class.(6 marks)2021年ACCA考试模拟试题:财务管理(3) An organisation is reviewing the way that Information System (IS) projects are accounted for in the organisation. Atpresent the Information Systems department (which undertakes the IS projects) is a non-recharged cost centre.However, the organisation wishes to explore the advantages and disadvantages of other charging approaches.Four approaches are being considered(1)Non-rechargeable cost centre (current situation)(2)Recharged at cost(3)Recharged at a mark up (profit centre)(4)Setting up a separate IS companyRequired:FOR EACH of the FOUR approaches listed above:(i)briefly describe the principle of the approach;(1 mark)(ii)briefly describe ONE advantage of the approach;(2 marks)(iii)briefly describe ONE disadvantage of the approach.(2 marks)The mark allocation shown is for each approach, four approaches are listed.(20 marks)5(Designing Information Systems)An organisation wishes to purchase a software package to administer its workflow requirements. It is currently drawingup an Invitation to Tender (ITT) to send out to potential suppliers.Required:(a)Identify and briefly describe the contents of FOUR possible sections of the Invitation to Tender which will be sent to the potential suppliers.(12 marks)(b)Some of the managers are sceptical about the formal drawing up of an ITT. Project manager, Mary Mendes, claims ‘our approach is to select a software package from a well-established software house, show it to the usersand convince them that it is what they want. Ours is a much quicker approach than all this formal ITT stuff’.Explain the potential problems of Mary’s approach to software package selection and explain how these are overcome by a formal approach that includes the production of an ITT.(8 marks)(20 marks)46(Evaluating Information Systems)An examination board currently has a system where the following details are held about examinations. There are currently 1,000 examinations on file, set by 100 examiners. Each examiner has set 10 examinations. There is asimple computer file (called ASSESSMENT) containing 1,000 records. Each record has the following structure: ASSESSMENT fileField nameLength of fieldType of fieldExamination number4NumericExamination name30CharacterExaminer name30CharacterExaminer address50CharacterPassmark2Numeric2021年ACCA考试模拟试题:会计师与企业(1)Section A–BOTH questions are compulsory and MUST be attempted 1 Doric Co,a listed company,has two manufacturing divisions:parts and fridges.It has been manufacturing parts for domestic refrigeration and air conditioning systems for a number of years,which it sells to producers of fridges and air conditioners worldwide.It also sells around 50% of the parts it manufactures to its fridge production division.It started producing and selling its own brand of fridges a few years ago.After limited initial success,competition in the fridge market became very tough and revenue and profits have beendeclining.Without further investment there are currently few growth prospects in either the parts or the fridge divisions.Doric Co borrowed heavily to finance the development and launch of its fridges,and has now reached its maximum overdraft limit.The markets have taken a pessimistic view of the company and its share price has declined to 50c per share from a high of $2.85 per share around three years ago.Extracts from the most recent financial statements:A survey from the refrigeration and air conditioning parts market has indicated that there is potential for Doric Co to manufacture parts for mobile refrigerationunits used in cargo planes and containers.If this venture goes ahead then the parts division before-tax profits are expected to grow by 5% per year.The proposed venture would need an initial one-off investment of $50 million.Suggested proposalsThe Board of Directors has arranged for a meeting to discuss how to proceed and is considering each of the following proposals:1.To cease trading and close down the company entirely.2.To undertake corporate restructuring in order to reduce the level of debt and obtain the additional capital investment required to continue current operations.5.To close the fridge division and continue the parts division through a leveraged management buy-out,involving some executive directors and managers from the partsdivision.The new company will then pursue its original parts business as well as the development of the parts for mobile refrigeration business,described above.All the current and long-term liabilities will be initially repaid using the proceeds from the sale of the fridge division.The finance raised from the management buy-out will pay for any remaining liabilities,the additional capital investment required to continue operations and re-purchase the shares at a premium of 20%.The following information has been provided for each proposal:Cease tradingCorporate restructuringThe existing ordinary shares will be cancelled and ordinary shareholders will be issued with 40 million new $1 ordinary shares in exchange for a cash payment at par.The existing unsecured bonds will be cancelled and replaced with 270 million of $1 ordinary shares.The bond holderswill contribute $90 million in cash.All the shares will be listed and traded.The bank overdraft will be converted intoa secured ten-year loan with a fixed annual interest rate of 7%.The other unsecured loans will be repaid.In addition to this,the directors of the restructured company will get 4 million $1 share options for an exercise price of$1.10,which will expire in four years.An additional one-off capital investment of $80 million in machinery and equipment is necessary to increase sales revenue for both divisions by 7%,with no change to the costs.After the one-off 7% growth,sales will continue at the new level for the foreseeable future.It is expected that the Doric's cost of capital rate will reduce by 550 basis points following the restructuring from the current rate.Management buy-outThe parts division is half the size of the fridge division in terms of the assets and liabilitiesattributable to it.If the management buy-out proposal is chosen,a pro rata additional capital investment will be made to machinery and equipment on a one-off basis to increase sales revenue of the parts division by 7%.Salesrevenue will then continue at the new level for the foreseeable future.All liabilities categories have equal claim for repayment against the company's assets.It is expected that Doric's cost of capital rate will decrease by 100 basis points following the management buy-out from the current rate.The following additional information has been provided:Redundancy and other costs will be approximately $54 million if the whole company is closed,and pro rata for individual divisions that are closed.These costs have priority for payment before any other liabilities in case of closure.The taxation effects relating to this may be ignored.Corporation tax on profits is 20% and losses cannot be carried forward for tax purposes.Assume that tax is payable in the year incurred.All the non-current assets,including land and buildings,are eligible for tax allowable depreciation of 15% annually on the book values.The annual reinvestmentneeded to keep operations at their current levels is roughly equivalent to the tax allowable depreciation.The $50 million investment in the mobile refrigeration business is not eligible for any tax allowable depreciation.Doric's current cost of capital is 12%.Required:Prepare a report for the Board of Directors,evaluating the financial and non-financial impact of all the three proposals to Doric Co's main stakeholder groups,that includes:(i)An estimate of the return the debt holders and shareholders would receive in the event that Doric Co ceases trading and is closed down.(5 marks)(ii)An estimate of the income position and the value of Doric Co in the event that the restructuring proposal is selected.State any assumptions made.(8 marks)(iii)An estimate of the amount of additional finance needed and the value of Doric Co if the management buy-out proposal is selected.State any assumptions made.(8 marks)(iv)A discussion of the impact of each proposal on the existing shareholders,the unsecured bond holders,and the executive directors and managers involved in the management buy-out.Suggest which proposal is likely to be selected.(12 marks)Professional marks will be awarded in question 1 for the appropriateness and format of the report.(4 marks)(55 marks)2 Fubuki Co,an unlisted company based in Megaera,has been manufacturing electrical parts used in mobility vehicles for people with disabilities and the elderly,for many years.These parts are exported to various manufacturers worldwide but at present there are no local manufacturers of mobility vehicles in Megaera.Retailers in Megaera normally import mobility vehicles and sell them at an average price of $4,000 each.Fubuki Co wants to manufacture mobility vehicles locally and believes that it can sell vehicles of equivalent quality locally at a discount of 57.5% to the current average retail price.Although this is a completely new venture for Fubuki Co,it will be in addition to the company's corebusiness.Fubuki Co's directors expect to develop theproject for a period of four years and then sell it for $16 million to a private equity firm.Megaera's government has been positive about the venture and has offered Fubuki Co a subsidised loan of up to 80% of the investment funds required,at a rate of 200 basis points below Fubuki Co's borrowing rate.Currently Fubuki Co can borrow at 500 basis points above the five-year government debt yield rate.A feasibility study commissioned by the directors,at a cost of $250,000,has produced the following information.1.Initial cost of acquiring suitable premises will be $11 million,and plant and machinery used in the manufacture will cost $5 million.Acquiring the premises and installing the machinery is a quick process and manufacturing can commence almost immediately.2.It is expected that in the first year 1,500 unitswill be manufactured and sold.Unit sales will grow by 40% in each of the next two years before falling to an annual growth rate of 5% for the final year.After the first yearthe selling price per unit is expected to increase by 5% per year.5.In the first year,it is estimated that the total direct material,labour and variable overheads costs will be $1,200 per unit produced.After the first year,the direct costs are expected to increase by an annual inflation rate of 8%.4.Annual fixed overhead costs would be $2.5 million of which 60% are centrally allocated overheads.The fixed overhead costs will increase by 5% per year after the first year.5.Fubuki Co will need to make working capital available of 15% of the anticipated sales revenue for the year,at the beginning of each year.The working capital is expected to be released at the end of the fourth year when the project is sold.Fubuki Co's tax rate is 25% per year on taxable profits.Tax is payable in the same year as when the profits are earned.Tax allowable depreciation is available on the plant and machinery on a straight-line basis.It isanticipated that the value attributable to the plant and machinery after four years is $400,000 of the price at which the project is sold.No tax allowable depreciation is available on the premises.Fubuki Co uses 8% as its discount rate for new projects but feels that this rate may not be appropriate for this new type of investment.It intends to raise the full amount of funds through debt finance and take advantage of the government's offer of a subsidised loan.Issue costs are 4% of the gross finance required.It can be assumed that the debt capacity available to the company is equivalent to the actual amount of debt finance raised for the project.Although no other companies produce mobility vehicles in Megaera,Haizum Co,a listed company,produces electrical-powered vehicles using similar technology to that required for the mobility vehicles.Haizum Co's cost of equity is estimated to be 14% and it pays tax at 28%.Haizum Co has 15 million shares in issue trading at $2.55 each and $40 million bonds trading at $94.88 per $100.The five-year government debt yield is currently estimated at 4.5% and the market risk premium at 4%.Required:(a)Evaluate,on financial grounds,whether Fubuki Co should proceed with the project.(17 marks)(b)Discuss the appropriateness of the evaluation method used and explain any assumptions made in part(a)above.(8 marks)(25 marks)2021年ACCA考试模拟试题:会计师与企业(2)1 Bravado,a public limited company,has acquired two subsidiaries and an associate. The draft statements of financial position are as follows at 51 May 2009:Bravado Message Mixted$m $m $mAssets:Non-current assetsProperty,plant and equipment 265 250 161Investments in subsidiariesMessage 500Mixted 128Investment in associate - Clarity 20 Available-for-sale financial assets 51 6 5 - - -764 256 166- - -Current assets:Inventories 155 55 75Trade receivables 91 45 52Cash and cash equivalents 102 100 8- - -528 200 115- - -Total assets 1,092 456 279- - -Equity and liabilities:Share capital 520 220 100Retained earnings 240 150 80Other components of equity 12 4 7- - -Total equity 772 574 1872021年ACCA考试模拟试题:会计师与企业(3)On 1 June 2007,Bravado acquired 6% of the ordinary shares of Mixted. Bravado had treated this investment asavailable-for-sale in the financial statements to 51 May 2008 but had restated the investment at cost on Mixted becoming a subsidiary. On 1 June 2008,Bravado acquired a further 64% of the ordinary shares of Mixted and gained control of the company. The consideration for the acquisitions was as follows:Holding Consideration$m1 June 2007 6% 101 June 2008 64% 118- -70% 128- -Under the purchase agreement of 1 June 2008,Bravado is required to pay the former shareholders 50% of the profits of Mixted on 51 May 2010 for each of the financial years to 51 May 2009 and 51 May 2010. The fair value of this arrangement was estimated at $12 million at 1 June 2008 and at 51 May 2009 this value had not changed. This amount has not been included in the financial statements.At 1 June 2008,the fair value of the equity interestin Mixted held by Bravado before the business combination was $15 million and the fair value of the non-controlling interest in Mixted was $55 million. The fair value of the identifiable net assets at 1 June 2008 of Mixted was $170 million (excluding deferred tax assets and liabilities),and the retained earnings and other components of equity were $55 million and $7 million respectively. There had been no new issue of share capital by Mixted since the date of acquisition and the excess of the fair value of the net assets is due to an increase in the value of property,plant and equipment (PPE)。

2015年12月ACCA考试F9财务管理真题(SectionB部分)及标准答案

2015年12月ACCA考试F9财务管理真题(SectionB部)(总分100, 考试时间180分钟)Section BGemlo Co is planning an expansion of existing business operations costing $10 million in the(a) Calculate the debt/equity ratio of Gemlo Co based on market values and comment on your findings.(b) Gemlo Co agrees with a bank that its business expansion will be financed by a new issue of 8% loan notes. The company then announces to the stock market both this financing decision and the expected increase in profit before interest and tax arising from the business expansion. Required:Assuming the stock market is semi-strong form efficient, analyse and discuss the effect of the financing and profitability announcement on the financial risk and share price of Gemlo Co.Required:(a) Evaluate the proposed forward rate agreement as a way of managing the interest rate risk anticipated by GXJ Co.该题您未回答:х 该问题分值: -3forward exchange rates and future (expected) spot rates.receivable.It is expected that investing $20 million in the business will increase income by 5% over theRequired:(a) Assess the impact of financing the business expansion by the loan note issue on financial position, financial risk and shareholder wealth after one year, using appropriate measures.company could be used in investment appraisal and indicate briefly how its limitations as a discount rate could be overcome.(a) Using a nominal terms net present value approach, evaluate whether purchasing the newmachine is financially acceptable.。

ACCA财务会计习题-8页精选文档

一、复习思考题1.按2019年新颁会计准则,会计核算有哪些前提?其作用是什么?2.财务会计对会计信息质量保证的要求有哪些?3.财务会计工作规范体系包括哪些内容?具体如何实施?二、填空题1.财务会计的基本前提主要包括。

2.我国企业会计准则规定,企业的会计核算应当以为记帐基础。

3.会计提供信息要以为主要计量尺度。

4.我国企业会计准则规定,在我国境内的企业应以为记帐本位币5.会计要素的核算主要解决_____ 等三方面的问题。

6.反映财务状况的会计等式为;反映经营成果的会计等式为。

7.我国企业会计准则规定,企业应以作为会计年度。

8.会计期间通常一年,称为。

9.会计等式揭示了之间的关系,它是、和的理论依据。

10.企业会计制度根据企业生产经营活动的特点以及会计报表要素,将会计科目分为、、、与五大类。

11.实际工作中,常用的帐务处理程序有、、、与__________五种。

我国会计人员惯用的是和两种。

12.一项信息是否有相关性取决的因素包括、。

13.收益性支出在会计处理上计入要素项目,而资本性支出计入要素项目。

三、单选题1.会计主体与法律主体一般是()①两个不相关的概念②两个不能相互代替的概念③一致的④有区别的2.会计核算进行分期的主要目的是()①贯彻权责发生制②分阶段确定经营成果③贯彻一致性原则④贯彻谨慎性原则3.会计机构、会计人员对本单位实行会计监督所应负的责任是()①行政责任②本职工作责任③对厂长负责④法律责任4.我国企业会计准则、具体会计准则是由()负责制定①企业主管部门②财政部门③国务院④企业自身5.某企业的存货计价前年采用先进先出法,去年改用移动加权平均法,今年又改用加权平均法。

该企业的做法主要违背了()原则①客观性②谨慎性③可比性④配比原则复习思考题1.企业使用现金的范围是如何规定的,企业应如何加强对现金的控制管理?2.目前我国银行的结算方式有哪几种,哪些适合同城交易结算,哪些适合异地交易结算?3.什么是其他货币资金,会计报表中如何列示??〖根据下列业务编制会计分录〗1.开出现金支票一张提取现金2389元。

ACCAF1考试-会计师与企业(基础阶段)历年真题精选及详细解析1109-9

ACCAF1考试-会计师与企业(基础阶段)历年真题精选及详细解析1109-91.The IASB\'s Conceptual Framework for Financial Reporting gives six qualitative characteristics offinancial information. What are these six characteristics?A Relevance, Faithful representation, Comparability, Verifiabilit, Timeliness and UnderstandabilityB Accuracy, Faithful representation, Comparability, Verifiability, Timeliness and UnderstandabilityC Relevance, Faithful representation, Consistency, Verifiability, Timeliness and UnderstandabilityD Relevance, Comparability, Consistency, Verifiability, Timeliness and Understandability答案:A2. Listed below are some comments on accounting concepts.1 Financial statements always treat the business as a separate entity.2 Materiality means that only items having a physical existence may be recognised as assets.3 Provisions are estimates and therefore can be altered to make the financial results of a business more attractive to investors.Which, if any, of these comments is correct, according to the IASB\'s Conceptual Framework for Financial Reporting?A 1 onlyB 2 onlyC 3 onlyD None of them答案:A3. Listed below are some characteristics of financial information.1 Relevance2 Consistency3 Faithful representation4 AccuracyWhich of these are qualitative characteristics of financial information according to the IASB\'s Conceptual Framework for Financial Reporting?A 1and2onlyB 2 and 4 onlyC 3 and 4 onlyD 1 and 3 only答案:D4. Which ONE of the following statements describes faithful representation, a qualitative characteristic of faithful representation?A Revenue earned must be matched against the expenditure incurred in earning it.B Having information available to decision-makers in time to be capable of influencing their decisions.C The presentation and classification of items in the financial statements should stay the same from one period to the next.D Financial information should be complete, neutral and free from error5. According to the IASB\'s Conceptual Framework for Financial Reporting, which TWO of the following are part of faithful representation?1 It is neutral2 It is relevant3 It is presented fairly4 It is free from material errorA 1and2B 2and3C 1and4D 3and4。

ACCA《财务会计》真题及答案

ACCA《财务会计》真题及答案在xx年ACCA考试之际,为大家分享的是ACCA《财务会计》的真题及答案,希翼能匡助到大家!Cronin Auto Retail (CAR) is a car dealer that sellsused cars bought at auctions by its experienced team of buyers. Every car for sale is less than two years old and has a full service history. The pany concentrates on small family cars and, at any one time, there are about 120 on display at its purpose-built premises. The premises were acquired five years ago on a 25 year lease and they include a workshop, a small cafe and a children’s playroom. All vehicles are selected by one of five experienced buyers who attend auctions throughout the country. Each attendance costs CAR about $500 per day in staff and travelling costs and usually leads to the purchase of five cars. On average, each car costs CAR $10,000 and is sold to the customer for $12,000. The pany has a good sales and profitability record, although a recent economic recession has led the managing director to question ‘whether we are selling the righttype of cars. Recently, I wonder if we have been buyingcars that our team of buyers would like to drive, not what our customers want to buy?’ However, the personalselection of quality cars has been an important part of CAR’s business model and it is stressed in their marketing literature and website.Sales records show that 90% of all sales are to customers who live within two hours’ drive of CAR’s base. This is to be expected as there are many petitors and most customers want to buy from a garage that they can easily return the car to if it needs inspection, a service or repair. Consequently, CAR concentrates on display advertising in newspapers in this geographical area. It also has a customer database containing the records of people who have bought cars in the last three years. All customers receive a regular mail-shot, listing the cars for sale and highlighting any special offers or promotions. The pany has a website where all the cars are listed with a series of photographs showing each car from a variety of angles. The website also contains general information about the pany, special offers and promotions, and information about its service, maintenance and repair service.CAR is keen to expand the service and mechanical repair side of its business. It would particularly like customers who have purchased cars from them to bring them back for servicing or for any mechanical repairs that are subsequently required. However, although CAR holds basic spare parts in stock, it has to order many parts from specialist parts panies (called motor factors) or from the manufacturers directly. Mechanics have to raise paper requisitions which are passed to the procurement managerfor reviewing, agreeing and sourcing. Most parts are ordered from regular suppliers, but there is an increasing backlog and this can cause a particular problem if the customer’s car is in the garage waiting for the part to arrive. Customers are increasingly frustrated and annoyed by repairs taking much longer than they were led to expect. Another source of frustration is that the procurement manager only works from 10.00 to 16.00. The mechanics work on shifts and so the garage is staffed from 07.00 to 19.00. Urgent requisitions cannot be processed when the procurement manager is not at work. The backlog of requisitions is placing increased strain on the procurement manager who has recently made a number of clerical mistakes when raising a purchase order.Requests for stationery and other office supplies also go through the same requisitioning process, with orders placed with the office supplier who is offering the best current deal. Finding this deal can be time consuming and so employees are increasingly submitting requisitions earlier so that they can be sure that new supplies will be received in time.The managing director is aware of the problems of the requisitioning system but is reluctant to appoint a second procurement manager because he is trying to keep staff overheads down during a difficult trading period. He iskeen to address ‘more fundamental issues in the marketing and procurement processes’. He is particularly interested in how the ‘interactivity, intelligence, individualisation and independence of location offered by e-marketing media can help us at CAR’.(a) Evaluate how the principles of interactivity, intelligence, individualisation and independence oflocation mightbe applied in the e-marketing of the products and services of CAR. (16 marks)(b) Explain the principles of e-procurement and evaluate its potential application at CAR. (9 marks)(25 marks)(a) This question uses four of the ‘6 Is’ developed by McDonald and Wilson to explore the differences between traditional and e-marketing. Candidate answers do not have to be strictly classified within each of the factors identified below. In reality, suggestions will cross the boundaries of these factors.Interactivity concerns the development of a two-way relationship between the customer and the supplier. The traditional display advertising and mail-shots used by CAR are examples of ‘push media’ where the marketing message is broadcast to current and potential customers. Their current website continues this approach, with the stocklisting essentially representing a continually updated, but widely aessible, display advertisement. Supplementing mail-shots with e-mails could be immediately considered by CAR and would be a cheaper alternative to mail-shots. However, it still remains a ‘push technique’ with little dialogue with the customer.Here are three ideas that CAR could consider to improve the interactivity of its site. Other legitimate suggestions will also be given credit.(1) Encouraging potential buyers on their website to ask questions about any car that they are interested in. Both questions and answers are published. This may provide someone with the vital information that clinches the sale. It also creates a great enthusiasm around the car. Buyers may move quickly so that they do not lose the opportunity to buy the car. On e-bay, customers are encouraged to ‘ask a question’ of the seller and this often leads to long threads where the supplier and potential buyers interact.(2) Many buyers would like to test drive a car before they purchase it. CAR could provide the opportunity for customers to book a test drive over the Inter.(3) Once a purchase had been plete, CAR might encourage feedback which could be published on the website. In this instance, customers are actually providing information that is mercially useful to buyers. This may be in the form oftestimonials, or in the form of more structured feedback that e-bay encourages. Suppliers who have 100% positive feedback backed up by testimonials from previous buyers are powerfully reinforcing their marketing message.Intelligence is about identifying and understanding the needs of potential customers and how they wish to be municated with. It is traditionally the area of market research and marketing research. Currently CAR does very little research. It relies on a database that only consists of people who have actually bought cars from the pany. Collecting email addresses through promotions and interactivity initiatives (see above) provides a much greater pool of potential customers who can be kept up-to-date through email. It can also give CAR significant intelligence about the type of cars that they areinterested in and at what price. At present, the buyers for CAR use their experience when buying cars at auction and there is some concern that they buy what they would like to drive, not what the customers want to drive. It would be useful to support this experience with quantitative information about the type of cars potential buyers are really interested in. This may lead to a change in buying policy.Individualisation concerns the tailoring of marketing information to each individual, unlike traditional mediawhere the same message tends to be sent to everyone. Personalisation is a key element in building an effective relationship with the customer. In the context of CAR, individuals who have shown interest in a certain model or type of car may be selectively emailed when a similar car bees available. This approach may also be used for current customers. For example, someone who purchased a particular car two or three years ago might be e-mailed about an opportunity to upgrade to an updated model. For individualisation to be suessful, sufficient details must be collected through the intelligence and interactive facets of the‘6 Is’.Individualisation will also be key in offering relevant after-sales service. This may concern inviting customers to return their cars for servicing at the correct dates or offering services only appropriate to that type of car. For example, circulating details of air-conditioning renewal only to customers with air conditioned cars.Independence of location concerns the geographical location of the pany. Electronic media increases the geographical reach of a pany. For many panies this gives opportunities to sell into international markets which had previously been inaessible to them.This facet of the new media is unlikely to be appropriate to CAR. Most sales are to customers who are within two hours’ drive of the CAR premises. The modity nature of the cars that CAR are selling means that similar cars will be available throughout the country, often from garages that offer local service and support. Independence of location would be more significant if CAR was selling collectors or classic cars where each car is relatively rare and people are prepared to travel long distances to view the car they are interested in. Furthermore, the long term lease on CAR’s current premises makes it unlikely that they will be able to locate to a cheaper site and hence exploit the independence of location offered by the new media.(b) Procurement is concerned with purchasing goods or services for the organisation. It is concerned with sourcing items at the right price, delivered at the right time, to the right quality, in the right quantity and from the right source. Many contemporary definitions of procurement also include the inbound logistics required to get the product from the supplier to the customer.E-procurement looks at the opportunities presented by automating aspects of procurement to improve the performance of the five ‘rights’ identified above. There is a wide range of potential answers to this part of thequestion depending on the scope and focus of e-procurement selected by the candidate. Solutions may vary from the simple automation of part of the system, to re-thinking the way the pany does business.In the context of CAR, two distinct types of procurement can be identified. The first is production-related procurement and is directly related to the core activities of the organisation. This relates to the purchase of cars for sale and the purchase of parts required for servicing or repairing vehicles. The second is non-production procurement.CAR has always purchased its vehicles through experienced buyers attending auctions. On average this attendance costs the pany $500 per day, leading to the purchase (on average) of five cars. This purchasing cost of $100 per car represents 5% of the average profit margin on each car. This cost could be eliminated if cars were purchased through e-auctions, with bids made on-line. The risk here is that the cars bought were not of the right quality. CAR prides itself in the personal selection of its cars. However, it could be argued that cars which are less than two years old with a full service history are unlikely to have much wrong with them.The parts needed for servicing and mechanical repairs are ordered from motor factors or manufacturers. A numberof regular suppliers are retained, many in long-term relationships with CAR. This is known as systematic sourcing. Most of the problems here are caused by the needto pass requisitions for parts through a procurement manager. The first problem is the delay in the purchasing cycle. There is a backlog of requisitions that have to be reviewed, agreed and sourced by the procurement manager. This is particularly problematic when a customer’s car isin the garage awaiting a part. The customer is likely to be frustrated and annoyed by the delay, whilst the car is oupying garage space that could have been profitably usedfor a fee-paying job. The second problem is the cost of the paperwork and the processing time of the procurement manager associated with the purchase. The final problem is that purchases can only be made between 10.00 and 16.00 when the procurement manager is at work. Mechanics work07.00 to 19.00 and are frustrated that they cannot make orders outside the times the procurement manager is at work. Giving the mechanics the systems and authorisation to order parts (up to a certain value limit) from specifiedsuppliers over the Inter should deliver cost savings and speed up repairs and services. A direct ordering system should also reduce administrative errors and enhance customer goodwill. CAR might also use eprocurement to open up petitive bidding between potential suppliers; postingtheir requirements on their website and inviting peting bids. Parts could be sourced from a number of suppliers, taking advantage of the lowest prices for each part. This could be bined with just-in-time supply, reducing the cost of stock holding at CAR.Non-production procurement is concerned with ordering things such as stationery, paper, ink toner and other office supplies. Christa Degnan (quoted in Chaffney, E-Business and E-Commerce Management) suggested that for‘every dollar a pany earns in revenue, 50 cents to 55 cents is spent on indirect goods and services – things like office supplies and puter equipment. That half dollar represents an opportunity. By driving costs out of the purchasing process, panies can increase profits without having to sell more goods’. CAR is in this situation. It uses the same process for office supplies as it does for car parts. However, most office supplies are cheap, modity products where sometimes the cost of ordering the product exceeds the value of the purchased product, particularly where a cumbersome purchasing process is in place. With little differentiation between products, it is the availability and cost of the product that bee the most significant aspects in the procurement process. E-procurement should provide better information, identifyingalternative suppliers and allowing spot sourcing of office products to fulfil immediate need.Overall, e-procurement should reduce the administrative burden on the procurement manager, giving him or her the opportunity to concentrate on negotiating terms, agreements and product standardisation; more strategic tasks in the procurement process.。

初级审计师《财务管理基础》章节练习题及答案

初级审计师《财务管理基础》章节练习题及答案初级审计师《财务管理基础》章节练习题及答案1.财务管理的基本职能包括:A.财务预测职能B.财务监督职能C.财务预算职能D.财务核算职能E.财务分析职能答案:ACE财务管理的基本职能一般有财务预测、财务决策、财务预算、财务控制和财务分析五项职能。

2.下列说法中正确的有:A.贝塔系数是测度系统风险B.贝塔系数是测度总风险C.贝塔值只反映市场风险D.方差反映风险程度E.标准离差反映风险程度答案:ACDE贝塔系数是测度系统风险,贝塔系数是不能测度系非统风险,因此B错误。

P95。

3.下列表述中正确的有:A.投资组合的风险有系统风险和非系统风险B.系统风险是可以分散的C.非系统风险是可以分散的D.系统风险和非系统风险均可以分散E.系统风险和非系统风险均不可以分散答案:AC投资组合的风险有系统风险和非系统风险,非系统风险是可以分散的,系统风险是不可以分散的。

参考教材P93~95。

4.风险分散理论认为,整体市场风险具有的特征有:A.不能通过投资组合来回避B.该类风险来自于公司之外,如通货膨胀C.是一种特定的公司风险D.能通过投资组合来回避E.该类风险来自于公司,如盈利质量下降答案:AB整体市场风险是不能通过投资组合来回避,是来自于公司之外。

选项CDE是非系统风险的特点。

参考教材P95。

5.按照资本资产定价模式,影响投资组合必要报酬率的因素有:A.无风险收益率B.投资组合的贝塔系数C.市场平均报酬率D.财务杠杆系数E.综合杠杆系数答案:ABC按照资本资产定价模式,资组合必要报酬率=无风险收益率+投资组合的贝塔系数×(市场平均报酬率-无风险收益率),因此答案ABC正确。

参考教材P96。

6.下列说法正确的有:A.市场组合的贝塔系数等于1B.无风险资产的贝塔系数等于1C.无风险资产的贝塔系数等于0D.市场组合的贝塔系数等于0E.以上说法均不正确答案:AC市场组合的贝塔系数等于1;无风险资产的贝塔系数等于0。

西方财务管理试题及答案

西方财务管理试题及答案一、单项选择题(每题2分,共10分)1. 以下哪项不是企业财务管理的目标?A. 利润最大化B. 股东财富最大化C. 企业价值最大化D. 社会责任最大化答案:D2. 以下哪项不是财务杠杆的表现形式?A. 经营杠杆B. 财务杠杆C. 市场杠杆D. 综合杠杆答案:C3. 以下哪项不是企业筹资的渠道?A. 内部筹资B. 银行贷款C. 股票发行D. 政府补贴答案:D4. 以下哪项不是企业投资决策的基本原则?A. 净现值原则B. 内部收益率原则C. 等额年金原则D. 风险分散原则答案:C5. 以下哪项不是企业风险管理的方法?A. 风险转移B. 风险避免C. 风险接受D. 风险共享答案:D二、多项选择题(每题3分,共15分)1. 企业财务管理的内容包括哪些方面?A. 资金筹集B. 资金运用C. 资金分配D. 资金监督答案:ABCD2. 以下哪些因素会影响企业的财务杠杆效应?A. 企业的负债规模B. 企业的盈利水平C. 企业的资产结构D. 企业的市场地位答案:ABC3. 企业筹资方式包括哪些?A. 自有资金B. 银行借款C. 发行债券D. 发行股票答案:ABCD4. 企业投资决策需要考虑哪些因素?A. 投资回报率B. 投资风险C. 投资期限D. 投资规模答案:ABCD5. 企业风险管理包括哪些内容?A. 风险识别B. 风险评估C. 风险控制D. 风险转移答案:ABCD三、判断题(每题2分,共10分)1. 企业财务管理的目标是利润最大化。

答案:错误2. 财务杠杆效应是指企业通过增加负债来提高股东收益。

答案:正确3. 企业筹资的渠道只有内部筹资和外部筹资两种。

答案:错误4. 企业投资决策只需要考虑投资回报率,不需要考虑投资风险。

答案:错误5. 企业风险管理的目的是完全消除风险。

答案:错误四、简答题(每题5分,共20分)1. 简述企业财务管理的作用。

答案:企业财务管理的作用包括:(1)提高资金使用效率;(2)降低企业经营风险;(3)实现企业价值最大化;(4)支持企业战略发展。

2023年ACCA考试F1真题及答案

2023年ACCA考试F1真题及答案为了帮助准备ACCA考试的学生更好地备考,我们特别整理了2023年ACCA考试F1的真题及答案。

请注意,以下内容仅供参考和学习使用。

第一部分:2023年ACCA考试F1真题试卷一:ACCA F1 Financial Reporting and TaxationSection A - 选择题(共30分)1. XYZ 公司的现金流量报表中,下列项目属于现金流入的是:(A)销售商品收到的现金(B)购买固定资产支付的现金(C)取得长期贷款收到的现金(D)支付利润税款的现金2. 在现金流量报表中,投资活动的主要内容是:(A)经营性投资(B)筹资性投资(C)经济性投资(D)投机性投资3. ABC 公司在报告期内遭受亏损,亏损产生的主要原因是:(A)销售收入减少(B)成本费用增加(C)营运资金减少(D)折旧费用减少......Section B - 简答题(共70分)1. 问题:请简要解释远期汇率合同的基本原理。

答案:远期汇率合同是一种外汇交易形式,约定在未来某一特定日期以约定的汇率进行货币兑换。

它允许交易双方在未来锁定特定的汇率,以避免由于汇率波动所带来的风险。

2. 问题:简述巴鲁克公司如何应对经济衰退对其业务的影响。

答案:面对经济衰退,巴鲁克公司可以采取一些措施来应对。

首先,他们可以进行成本削减,减少不必要的开支,以保持盈利能力。

其次,他们可以寻找新的市场机会,例如拓展国际市场或开发新产品。

此外,他们还可以优化供应链,提高效率,降低生产成本。

最后,巴鲁克公司应加强财务管理,合理规划资金运作,确保资金的流动性和稳定性。

......第二部分:2023年ACCA考试F1答案Section A - 选择题1. 答案:(A)销售商品收到的现金2. 答案:(B)筹资性投资3. 答案:(B)成本费用增加......Section B - 简答题1. 答案:远期汇率合同的基本原理是约定未来某一特定日期以预先确定的汇率进行货币兑换的外汇交易方式。

ACCAF1考试-会计师与企业(基础阶段)历年真题精选及详细解析1109-11

ACCAF1考试-会计师与企业(基础阶段)历年真题精选及详细解析1109-111. A business can make a profit and yet have a reduction in its bank balance. Which ONE of the following might cause this to happen?A The sale of non-current assets at a lossB The charging of depreciation in the statement of profit or lossC The lengthening of the period of credit given to customersD The lengthening of the period of credit taken from suppliers 答案:C2. The profit made by a business in 20X7 was $35, ,400. The proprietor injected new capital of $10,200 during the year and withdrew a monthly salary of $500.If net assets at the end of 20x7 were $95,100, what was the proprietor\'s capital at the beginning of the year?A $50,000B $55, 500C $63,900D $134,700答案:B3. The profit earned by a business in 20X7 was $72 ,500. The proprietor injected new capital of $8,000 during the year and withdrew goods for his private use which had cost $2,200. If net assets at the beginning of 20X7 were $101,700, what were the closing net assets?A $35,000B $39, 400C $168, 400D $180,000答案:D4. A trader\'s net profit for the year may be computed by using which of the following formulae?A Opening capital + drawings -capital introduced -closing capitalB Closing capital + drawings -capital introduced -opening capitalC Opening capital -drawings + capital introduced -closing capitalD Opening capital -drawings -capital introduced -closing capital答案:B5. Which one of the following can the accounting equation can be rewritten as?A Assets + profit - drawings - liabilities = closing capitalB Assets - liabilities - drawings = opening capital + profitC Assets - liabilities - opening capital + drawings = profitD Assets - profit - drawings = closing capital - liabilities答案:C。

ACCA考试《财务成本管理》重点练习(2)

ACCA考试《财务成本管理》重点练习(2)一.上述的流动比率显示流动资产多于短期负债。

但是1.07:1的比率数值似乎低了一点。

假若变卖公司的流动资产,只能容许很小的折让,否则,所得金额亦不足偿还短期负债。

速动比率不考虑存货,所以是一个比较精确的变现能力测试。

0.57:1的速动比率亦是比较偏低,显示公司可能没有足够的资金来偿还它的债务。

当解释这些比率时,要紧记它们是基于资产负债表的帐面数值,所以只能代表某一时间的变现能力的状况。

较有效的方法是留意这些比率的走势。

若想了解将来的变现能力的状况,预测现金流量会是一有效方法。

同时,银行的透支是一主要的短期融资工具,银行是否继续支持,对公司是很重要的。

(6 分)(每个1 分,小计8分)(b) 企业的营运资金周期代表了由付款购货至销售收款之间的时期。

以一个批发商为例,营运资金周期如下:平均存货库存时间+ 平均应收款收帐时间- 平均应付帐清还时间营运资金周期愈长,此公司的融资需求愈大,而涉及的风险更高。

(5 分)(c) 营运资金周期如下:(* 每个? 分,# 每个1 分)(小计14 分)(b) 关于新手帐的可行性的报告致:万氏公司分部经理由:考生在评估新手帐的可行性时,净现值法被采用了。

这个方法适用于投资决策的原因如下:(i) 它与企业的假设目的,即增加财富,有着直接的关系。

(ii) 它把未来收入及支出折现,从而考虑到金钱的时间价值。

(iii) 它已考虑到所有有关的资料。

有别于回本期法,回本期法忽略了回本期以后的现金流量。

(iv) 它利用了根据长期融资提供者要求的回报所计算出来的贴现率。

(v) 相对来说,它是较易理解的,同时亦提供了清晰的决策原则及计算方法。

上述(a) 的计算显示电子手帐的净现值为正数。

如果接受建议,分部经理将可增加股东的财富。

因此,应对电子手帐的生产放行绿灯。

(6 分)(c) 在作出投资决策时,应认知到通胀可影响企业融资的成本和项目的未来现金流量。

ACCA考试管理会计(基础阶段)历年真题精选及详细解析1110-81

D.Top management prepare a budget with lttle or no input from operating staff

A.103 .3%

B.93.1%

C.89.7%

D.96.3%

答案:96.3%

Budgeted hours per unit = 4 (116,000 / 29,000)

Actual hours per unit = 4.15 (108,000 / 26,000)

Labour eff

Imposed budgets are prepared with insignificant input from operational levels. This way the management is able to prevent intentional creation of cost buffers or power revenue target setting at operational level.

One of the disadvantages of imposed budgeting is that it may hinder motivation so it will not increase operational managers\' commitment.

Imposed budgets are most effective in small organisations, not large organisations.

ACCA财务管理试题

ACCA财务管理试题1、企业溢价发行股票,实收款项超过股票面值的部分,应计入()。

[单选题] *A.主营业务收入B.资本公积(正确答案)C.盈余公积D.财务费用2、下列项目中,应计入营业外收入的有()。

[单选题] *A.处置交易性金融资产的收益B.固定资产盘盈C.接受捐赠(正确答案)D.无法收到的应收账款3、企业因解除与职工的劳动关系给予职工补偿而发生的职工薪酬,应借记的会计科目是()。

[单选题] *A.管理费用(正确答案)B.计入存货成本或劳务成本C.营业外支出D.计入销售费用4、企业购进货物用于集体福利时,该货物负担的增值税额应当计入()。

[单选题] *A.应交税费——应交增值税B.应付职工薪酬(正确答案)C.营业外支出D.管理费用5、下列固定资产当月应计提折旧的有()。

[单选题] *A.以经营租赁方式租出的汽车(正确答案)B.当月购入并投入使用的机器C.已提足折旧的厂房D.单独计价入账的土地6、会计期末,如果企业所持有的非专利技术的账面价值高于其可回收金额的,应按其差额计入()。

[单选题] *A.其他业务成本B.资产减值损失(正确答案)C.无形资产D.营业外支出7、企业为扩大生产经营而发生的业务招待费,应计入()科目。

[单选题] *A.管理费用(正确答案)B.财务费用C.销售费用D.其他业务成本8、某企业去年发生亏损235 000元,按规定可以用本年度实现的利润弥补去年全部亏损时,应当()。

[单选题] *A.借:利润分配——弥补亏损235 000 贷:利润分配——未分配利润235 000B.借:盈余公积235 000 贷:利润分配——未分配利润235 000C.借:其他应收款235 000 贷:利润分配——未分配利润235 000D.不做账务处理(正确答案)9、某企业自创一项专利,并经过有关部门审核注册获得其专利权。

该项专利权的研究开发费为15万元,其中开发阶段符合资本化条件的支出8万元;发生的注册登记费2万元,律师费1万元。

ACCA《财务成本管理基础》练习题

5,已知:某公司只销售一种产品,2009年单 位变动成本为12元/件,变动成本总额为 60000元,共获利润18000元,若该公司计 划于2010年维持销售单价不变,边际贡献 率仍维持2009年的60%,固定成本维持不 变。 要求:(1)计算2009年的保本点; (2)如果预计2010年实际可销售6000件, 预测2010年的安全边际; (2)若2010年的计划销售量比2000年提高 8%,则可获得多少利润?

7,某厂全年需要甲零件30000个,生产甲的 设备日产量100个,每天要领用60个,每次 调整准备成本800元;单位零件的变动生产 成本是5元/个,全年的单位甲零件储存成本 5元,请计算该厂甲零件的最优生产批量。

8.长江公司产销A产品,期初存货为0,本年度 计划产销10000件,相应的计划成本资料如 下:直接材料2元/件,直接人工3元/件,单 位变动制造费用3元/件,单位固定制造费用 4元/件,单位变动管理及营业费用1元/件, 单位固定管理及营业费用2元/件,单价20元/ 件;本年度实际生产了11000件(未突破相关 范围),卖出了9000件。 要求:请分别用完全成本法和变动成本法计算 本年度A产品的实际单位生产成本、生产成 本总额、期总经理的决定是否有利于企业?请给出

计算和说明。 2)请描述一种更有用的利润表形式。 3)如果公司不接受这笔订单,这笔订单将 会被竞争对手夺取,并会造成对正常销量 的影响,会使下个季度产销量降低20%,此 时企业应否接受该笔订单?

案例分析2:

某制鞋厂生产一种高级室内拖鞋,年生产能力为 100000双,根据销售预测编制的计划年度损益表 (简表)如下:

2017年12月ACCA考试P4高级财务管理真题及标准答案

2017骞?2鏈圓CCA鑰冭瘯P4楂樼骇璐㈠姟绠$悊鐪熼(鎬诲垎锛?25.00锛屽仛棰樻椂闂达細195鍒嗛挓)妗堜緥鍒嗘瀽棰?br/>Section A涓哄繀鍋氶锛孲ection B涓洪€夊仛棰樸€?/p>(鎬婚鏁帮細4锛屽垎鏁帮細125.00)Section A – This ONE question is compulsory and MUST be attemptedConejo Co is a listed company based in Ardilla and uses the $ as its currency. The company was formed around 20 years ago and was initially involved in cybernetics, robotics and artificial intelligence within the information technology industry. At that time due to the risky ventures Conejo Co undertook, its cash flows and profits were very varied and unstable. Around 10 years ago, it started an information systems consultancy business and a business developing cyber security systems. Both these businesses have been successful and have been growing consistently. This in turn has resulted in a stable growth in revenues, profits and cash flows. The company continues its research and product development in artificial intelligence and robotics, but this business unit has shrunk proportionally to the other two units.Just under eight years ago, Conejo Co was successfully listed on Ardilla’s national stock exchange, offering 60% of its share capital to external equity holders, whilst the original founding members retained the remaining 40% of the equity capital. The company remains financed largely by equity capital and reserves, with only a small amount of debt capital. Due to this, and its steadily growing sales revenue, profits and cash flows, it has attracted a credit rating of A from the credit rating agencies.At a recent board of directors (BoD) meeting, the company’s chief financial officer (CFO) argued that it was time for Conejo Co to change its capital structure by undertaking a financial reconstruction, and be financed by higher levels of debt. As part of her explanation, the CFO said that Conejo Co is now better able to bear the increased risk resulting from higher levels of debt finance; would be better protected from predatory acquisition bids if it was financed by higher levels of debt; and could take advantage of the tax benefits offered by increased debt finance. She also suggested that the expected credit migration from a credit rating of A to a credit rating of BBB, if the financial reconstruction detailed below took place, would not weaken Conejo Co financially.Financial reconstructionThe BoD decided to consider the financial reconstruction plan further before making a final decision. The financial reconstruction plan would involve raising $1,320 million ($1·32 billion) new debt finance consisting of bonds issued at their face value of $100. The bonds would be redeemed in five years’ time at their face value of $100 each. The funds raised from the issue of the new bonds would be used to implement one of the following two proposals:(i) Proposal 1: Either buy back equity shares at their current share price, which would be cancelled after they have been repurchased; or(ii) Proposal 2: Invest in additional assets in new business ventures.Conejo Co, Financial informationExtract from the forecast financial position for next yearConejo Co’s forecast after-tax profit for next year is $350 million and its current share price is $11 per share.The non-current liabilities consist solely of 5·2% coupon bonds with a face value of $100 each, which are redeemable at their face value in three years’ time. These bonds are currently trading at $107·80 per $100. The bond’s covenant stipulates that s hould Conejo Co’s borrowing increase, the coupon payable on these bonds will increase by 37 basis points.Conejo Co pays tax at a rate of 15% per year and its after-tax return on the new investment is estimated at 12%.Other financial informationCurrent government bond yield curveThe finance director wants to determine the percentage change in the value of Conejo Co’s current bonds, if the credit rating changes from A to BBB. Furthermore, she wants to determine the coupon rate at which the new bonds would need to be issued, based on the current yield curve and appropriate yield spreads given above.Conejo Co’s chief executive officer (CEO) suggested that if Conejo Co paid back the capital and interest of the new bond in fixed annual repayments of capital and interest through the five-year life of the bond, then the risk associated with the extra debt finance would be largely mitigated. In this case, it was possible that credit migration, by credit rating companies, from A rating to BBB rating may not happen. He suggested that comparing the duration of the new bond based on the interest payable annually and the face value in five years’ time with the duration of the new bond where the borrowing is paid in fixed annual repayments of interest and capital could be used to demonstrate this risk mitigation.Required:锛堝垎鏁帮細50锛?/p>(1).Discuss the possible reasons for the finance director’s suggestions that Conejo Co could benefit from higher levels of debt with respect to risk, from protection against acquisition bids, and from tax benefits. 锛堝垎鏁帮細7锛?/p>__________________________________________________________________________________________ 姝g‘绛旀锛?Increasing the debt finance of a company relative to equity finance increases its financial risk, and therefore the company will need to be able to bear the consequences of this increased risk. However, companies face both financial risk, which increases as the debt levels in the capital structure increase, and business risk, which is present in a company due to the nature of its business.In the case of Conejo Co, it could be argued that as its profits and cash flows have stabilised, the company’s business risk has reduced, in contrast to early in its life, when its business risk would have been much higher due to unstable profits and cash flows. Therefore, whereas previously Conejo Co was not able to bear high levels of financial risk, it is able to do so now without having a detrimental impact on the overall risk profile of the company. It could therefore change its capital structure and have higher levels of debt finance relative to equity finance.The predatory acquisition of one company by another could be undertaken for a number of reasons. One possible reason may be to gain access to cash resources, where a company which needs cash resources may want to take over another company which has significant cash resources or cash generative capability. Another reason may be to increase the debt capacity of the acquirer by using the assets of the target company. Where the relative level of debt finance is increased in the capital structure of a company through a financial reconstruction, like in the case of Conejo Co, these reasons for acquiring a company may be diminished. This is because the increased levels of debt would probably be secured against the assets of the company and therefore the acquirer cannot use them to raise additional debt finance, and cash resources would be needed to fund the higher interest payments.Many tax jurisdictions worldwide allow debt interest to be deducted from profits before the amount of tax payable is calculated on the profits. Increasing the amount of debt finance will increase the amount of interest paid, reducing the taxable profits and therefore the tax paid. Modigliani and Miller referred to this as the benefit of the tax shield in their research into capital structure, where their amended capital proposition demonstrated the reduction in the cost of capital and increase in the value of the firm, as the proportion of debt in the capital structure increases.)瑙f瀽锛?/div>(2).Prepare a report for the board of directors of Conejo Co which:(i) Estimates, and briefly comments on, the change in value of the current bond and the coupon rate required for the new bond, as requested by the CFO; (6 marks)(ii) Estimates the Macaulay duration of the new bond based on the interest payable annually and face value repayment, and the Macaulay duration based on the fixed annual repayment of the interest and capital, as suggested by the CEO; (6 marks)(iii) Estimates the impact of the two proposals on how the funds may be used on next year’s forecast earnings, forecast financial position, forecast earnings per share and on forecast gearing; (11 marks)(iv) Using the estimates from (b)(i), (b)(ii) and (b)(iii), discusses the impact of the proposed financial reconstruction and the proposals on the use of funds on:– Conejo Co;– Possible reaction(s) of credit rating companies and on the expected credit migration, including the suggestion made by the CEO;–Conejo Co’s equity holders;–Conejo Co’s current and new debt holders.(16 marks)Professional marks will be awarded in part (b) for the format, structure and presentation of the report. (4 marks)锛堝垎鏁帮細43锛?/p>__________________________________________________________________________________________ 姝g‘绛旀锛?Report to the board of directors (BoD), Conejo CoIntroductionThis report discusses whether the proposed financial reconstruction scheme which increases the amount of debt finance in Conejo Co would be beneficial or not to the company and the main parties affected by the change in the funding, namely the equity holders, the debt holders and the credit rating companies. Financial estimates provided in the appendices are used to support the discussion.Impact on Conejo CoBenefits to Conejo Co include the areas discussed in part (a) above and as suggested by the CFO. The estimate in appendix 3 assumes that the interest payable on the new bonds and the extra interest payable on the existing bonds are net of the 15% tax. Therefore, the tax shield reduces the extra amount of interest paid. Further, it is likely that because of the large amount of debt finance which will be raised, the company’s assets would have been used as collateral. This will help protect the company against hostile takeover bids. Additionally, proposal 2 (appendix 3) appears to be better than proposal 1, with a lower gearing figure and a higher earnings per share figure. However, this is dependent on the extra investment being able to generate an after-tax return of 12% immediately. The feasibility of this should be assessed further.Conejo Co may also feel that this is the right time to raise debt finance as interest rates are lower and therefore it does not have to offer large coupons, compared to previous years. Appendix 1 estimates that the new bond will need to offer a coupon of 3·57%, whereas the existing bond is paying a coupon of 5·57%.The benefits above need to be compared with potential negative aspects of raising such a substantial amount of debt finance. Conejo Co needs to ensure that it will be able to finance the interest payable on the bonds and it should ensure it is able to repay the capital amount borrowed (or be able to re-finance the loan) in the future. The extrainterest payable (appendix 3) will probably not pose a significant issue given that theprofit after tax is substantially more than the interest payment. However, the repayment of the capital amount will need careful thought because it is significant.The substantial increase in gearing, especially with respect to proposal 1 (appendix 3), may worry some stakeholders because of the extra financial risk. However, based on market values, the level of gearing may not appear so high. The expected credit migration from A to BBB seems to indicate some increase in risk, but it is probably not substantial.The BoD should also be aware of, and take account of, the fact that going to the capital markets to raise finance will require Conejo Co to disclose information, which may be considered strategically important and could impact negatively on areas where Conejo Co has a competitive advantage.Reaction of credit rating companiesCredit ratings assigned to companies and to borrowings made by companies by credit rating companies depend on the probability of default and recovery rate. A credit migration from A to BBB means that Conejo Co has become riskier in that it is more likely to default and bondholders will find it more difficult to recover their entire loan if default does happen. Nevertheless, the relatively lower increase in yield spreads from A to BBB, compared to BBB to BB, indicates that BBB can still be considered a relatively safe investment.Duration indicates the time it takes to recover half the repayments of interest and capital of a bond, in present value terms. Duration measures the sensitivity of bond prices to changes in interest rates. A bond with a higher duration would see a greater fluctuation in its value when interest rates change, compared to a bond with a lower duration. Appendix 2 shows that a bond which pays interest (coupon) and capital in equal annual instalments will have a lower duration. This is because a greater proportion of income is received earlier and income due to be received earlier is less risky. Therefore, when interest rates change, this bond’s value will change by less than the bond with the higher duration. The CEO is correct that the bond with equal annual payments of interest and capital is less sensitive to interest rate changes, but it is not likely that this will be a significant factor for a credit rating company when assigning a credit rating.A credit rating company will consider a number of criteria when assigning a credit rating, as these would give a more appropriate assessment of the probability of default and the recovery rate. These criteria include, for example, the industry within which the company operates, the company’s position within that industry, the company’s ability to generate profits in proportion to the capital invested, the amount of gearing, the quality of management and the amount of financial flexibility the company possesses. A credit rating company will be much less concerned about the manner in which a bond’s value fluctuates when interest rates change.Impact on equity holdersThe purpose of the financial reconstruction would be of interest to the equity holders. If, for example, Conejo Co selects proposal 1 (appendix 3), it may give equity holders an opportunity to liquidate some of their invested capital. At present, the original members of the company hold 40% of the equity capital and proposal 1 provides them with the opportunity to realise a substantial capital without unnecessary fluctuations in the share price.Selling large quantities of equity shares in the stock exchange may move the price of the shares down and cause unnecessary fluctuations in the share price.If, on the other hand, proposal 2 (appendix 3) is selected, any additional profits after the payment of interest will benefit the equity holders directly. In effect, debt capital is being used for the benefit of the equity holders.It may be true that equity holders may be concerned about the increased risk which higher gearing will bring, and because of this, they may need higher returns to compensate for thehigher risk. However, in terms of market values, the increased gearing may be of less concern to equity holders. Conejo Co should consider the capital structure of its competitors to assess what should be an appropriate level of gearing.Equity holders will probably be more concerned about the additional restrictive covenants which will result from the extra debt finance, and the extent to which these covenants will restrict the financial flexibility of Conejo Co when undertaking future business opportunities.Equity holders may also be concerned that because Conejo Co has to pay extra interest to debt holders, its ability to pay increasing amounts of dividends in the future could be affected. However, appendix 3 shows that the proportion of interest relative to after-tax profits is not too high and any concern from the equity holders is probably unfounded. Impact on debt holdersAlthough the current debt holders may be concerned about the extra gearing which the new bonds would introduce to Conejo Co, appendix 1 shows that the higher coupon payments which the current debt holders will receive would negate any fall in the value of their bonds due to the credit migration to BBB rating from an A rating. Given that currently Conejo Co is subject to low financial risk, and probably lower business risk, it is unlikely that the current and new debt holders would be overly concerned about the extra gearing. The earnings figures in appendix 3 also show that the after-tax profit figures provide a substantial interest cover and therefore additional annual interest payment should not cause the debt holders undue concern either.The curre nt and new debt holders would be more concerned about Conejo Co’s ability to pay back the large capital sum in five years’ time. However, a convincing explanation of how this can be achieved or a plan to roll over the debt should allay these concerns.The current and new debt holders may be concerned that Conejo Co is not tempted to take unnecessary risks with the additional investment finance, but sensible use of restrictive covenants and the requirement to make extra disclosures to the markets when raising the debt finance should help mitigate these concerns.ConclusionOverall, it seems that the proposed financial reconstruction will be beneficial, as it will provide opportunities for Conejo Co to make additional investments and/or an opportunity to reduce equity capital, and thereby increasing the earnings per share. The increased gearing may not look large when considered in terms of market values. It may also be advantageous to undertake the reconstruction scheme in a period when interest rates are low and the credit migration is not disadvantageous. However, Conejo Co needs to be mindful of how it intendsto repay the capital amount in five years’ time, the information it will disclose to the capital markets and the impact of any negative restrictive covenants.Report compiled by:DateAppendices:Appendix 1: Change in the value of the current bond from credit migration and coupon rate required from the new bond (Question (b) (i))Spot yield rates (yield curve) based on BBB ratingBond value based on BBB rating$5·57 x 1·0220–1+ $5·57 x 1·0251–2+ $105·57 x 1·0284–3= $107·81Current bond value = $107·80Although the credit rating of Conejo Co declines from A to BBB, resulting in higher spot yield rates, the value of the bond does not change very much at all. This is because theincrease in the coupons and the resultant increase in value almost exactly matches the fall in value from the higher spot yield rates.Coupon rate required from the new bondTake R as the coupon rate, such that:Take R as the coupon rate, such that:($R x 1·0220–1) + ($R x 1·0251–2) + ($R x 1·0284–3) + ($R x 1·0325–4) + ($R x 1·0362–5) + ($100 x 1·0362–5) = $1004·5665R + 83·71 = 100R = $3·57Coupon rate for the new bond is 3·57%.If the coupon payments on the bond are at a rate of 3·57% on the face value, it ensuresthat the present values of the coupons and the redemption of the bond at face value exactly equals the bond’s current face value, based on Conejo Co’s yield curve.Appendix 2: Macaulay durations (Question (b) (ii))Macaulay duration based on annual coupon of $3·57 and redemption value of $100 in year 5: [($3·57 x 1·0220–1x 1 year) + ($3·57 x 1·0251–2x 2 years) + ($3·57 x 1·0284–3 x 3 years) + ($3·57 x 1·0325–4x 4 years) + ($103·57 x 1·0362–5x 5 years)]/$100 = [3·49 + 6·79 + 9·85 + 12·57 + 433·50]/100 = 4·7 yearsMacaulay duration based on fixed annual repayments of interest and capital:Annuity factor: (3·57%, 5 years) = (1 –1·0357–5)/0·0357 = 4·51 approximatelyAnnual payments of capital and interest required to pay back new bond issue = $100/4·51 = $22·17 per $100 bond approximately[($22·17 x 1·0220–1 x 1 year) + ($22·17 x 1·0251–2x 2 years) + ($22·17 x 1·0284–3 x 3 years) + ($22·17 x 1·0325–4x 4 years) + ($22·17 x 1·0362–5x 5 years)]/$100 = [21·69 + 42·20 + 61·15 + 78·03 + 92·79]/100 = 3·0 yearsAppendix 3: Forecast earnings, financial position, earnings per share and gearing (Question (b) (iii))Adjustments to forecast earningsNotes:If gearing is calculated based on non-current liabilities/(non-current liabilities + equity) and/or using market value of equity, instead of as above, then this is acceptable as well. Proposal 1Additional interest payable is deducted from current assets, assuming it is paid in cash and this is part of current assets. Reserves are also reduced by this amount.Shares repurchased as follows: $1 x 120m shares deducted from share capital and $10 x 120m shares deducted from reserves. $1,320m, consisting of $11 x 120m shares, added to non-current liabilities.Proposal 2Treatment of additional interest payable is as per proposal 1Additional debt finance raised, $1,320 million, is added to non-current liabilities and to non-current assets, assuming that all this amount is invested in non-current assets to generate extra income.It is assumed that this additional investment generates returns at 12%, which is added to current assets and to profits (and therefore to reserves).(Explanations given in notes are not required for full marks, but are included to explain how the figures given in appendix 3 are derived)(Note: Credit will be given for alternative relevant presentation of financial positions and discussion))瑙f瀽锛?/div>Section B – TWO questions ONLY to be attemptedEview Cinemas Co is a long-established chain of cinemas in the country of Taria. Twenty years ago Eview Cinemas Co’s board decided to convert some of its cinemas into sports g yms, known as the EV clubs. The number of EV clubs has expanded since then. Eview Cinemas Co’s board brought in outside managers to run the EV clubs, but over the years there have been disagreements between the clubs’ managers and the board. The managers h ave felt that the board has wrongly prioritised investment in, and refurbishment of, the cinemas at the expense of the EV clubs.Five years ago, Eview Cinemas Co undertook a major refurbishment of its cinemas, financing this work with various types of debt, including loan notes at a high coupon rate of 10%. Shortly after the work was undertaken, Taria entered into a recession which adversely affected profitability. The finance cost burden was high and Eview Cinemas Co was not ableto pay a dividend for two years.The recession is now over and Eview Cinemas Co has emerged in a good financial position, as two of its competitors went into insolvency during the recession. Eview Cinemas Co’s board wishes to expand its chain of cinemas and open new, multiscreen cinemas in locations which are available because businesses were closed down during the recession.In two years’ time Taria is due to host a major sports festival. This has encouraged interest in sport and exercise in the country. As a result, some gym chains are looking to expand and have contacted Eview Cinemas Co’s board to ask if it would be interested in selling the EV clubs. Most of the directors regard the cinemas as the main business and so are receptive to selling the EV clubs.The finance director has recommended that the sales price of the EV clubs be based on predicted free cash flows as follows:1. The predicted free cash flow figures in $millions for EV clubs are as follows:2. After Year 4, free cash flows should be assumed to increase at 5·2% per annum.3. The discount rate to be used should be the current weighted average cost of capital, which is 12%.4. The finance director believes that the result of the free cash flow valuation will represent a fair value of the EV clubs’ business, but Eview Cinemas Co is looking to obtain a 25% premium on the fair value as the expected sales price.Other information supplied by the finance director is as follows:1. The predicted after-tax profits of the EV clubs are $454 million in Year 1. This can be assumed to be 40% of total after-tax profits of EV Cinemas Co.2. The expected proceeds which Eview Cinemas Co receives from selling the EV clubs will be used firstly to pay off the 10% loan notes. Part of the remaining amount from the sales proceeds will then be used to enhance liquidity by being held as part of current assets, so that the current ratio increases to 1·5. The rest of the remaining amount will be invested in property, plant and equipment. The current net book value of the non-current assets of the EV clubs to be sold can be assumed to be $3,790 million. The profit on the sale of the EV clubs should be taken directly to reserves.3. Eview Cinemas Co’s asset beta for the cinemas can be assumed to be 0·952.4. Eview Cinemas Co currently has 1,000 million $1 shares in issue. These are currently trading at $15·75 per share. The finance director expects the share price to rise by 10% once the sale has been completed, as he thinks that the stock market will perceive it to be a good deal.5. Tradeable debt is currently quoted at $96 per $100 for the 10% loan notes and $93 per $100 for the other loan notes. The value of the other loan notes is not expected to change once the sale has been completed. The overall pre-tax cost of debt is currently 9% and can be assumed to fall to 8% when the 10% loan notes are redeemed.6. The current tax rate on profits is 20%.7. Additional investment in current assets is expected to earn a 7% pre-tax return and additional investment in property, plant and equipment is expected to earn a 12% pre-tax return.8. The current risk-free rate is 4% and the return on the market portfolio is 10%.Eview Cinemas Co’s current summarised statement of financial position is shown below. The CEO wants to know the impact the sale of the EV clubs would have immediately on the statement of financial position, the impact on the Year 1 forecast earnings per share and on the weighted average cost of capital.Required:锛堝垎鏁帮細25锛?/p>(1).Calculate the expected sales price of the EV clubs and demonstrate its impact on Eview Cinemas Co’s statement of financial position, forecast earnings per share and weighted average cost of capital.锛堝垎鏁帮細17锛?/p>__________________________________________________________________________________________ 姝g‘绛旀锛?Proceeds from sales of EV clubsPresent value in Year 5 onwards = $490m x 1·052/(0·12 –0·052) x 0·636 = $4,821mTotal present value = $1,318m + $4,821m = $6,139mDesired sales proc eeds (25% premium) = $6,139m x 1·25 = $7,674mImpact on statement of financial position ($m)Profit on sale = $7,674m – $3,790m = $3,884mCurrent assets adjustment = $2,347m + $7,674m –($2,166m x 1·5) = $6,772mPPE adjustment = $6,772m – $3,200m = $3,572m)瑙f瀽锛?/div>(2).Evaluate the decision to sell the EV clubs.锛堝垎鏁帮細8锛?/p>__________________________________________________________________________________________ 姝g‘绛旀锛?Shareholders would appear to have grounds for questioning the sale of the EV clubs. It would mean that Eview Cinemas Co was no longer diversified into two sectors. Although shareholders can achieve diversification themselves in theory, in practice transaction costs and other issues may mean they do not want to adjust their portfolio.The increase in gym membership brought about by the forthcoming sports festival couldjustify the predicted increases in free cash flows made in the forecasts. Although increased earnings per share are forecast once the EV clubs are sold, these are dependent on Eview Cinemas Co achieving the sales price which it desires for the EV clubs and the predicted returns being achieved on the remaining assets.The proposed expansion of multiscreen cinemas may be a worthwhile opportunity, but the level of demand for big cinema complexes may be doubtful and there may also be practical problems like negotiating change of use. In Year 1 the EV clubs would be forecast to make a post-tax return on assets of (454/3,790) = 12·0% compared with 9·6% (12% x 0·8) on the additional investment in the cinemas.Investors may also wonder about the motives of Eview Cinema s Co’s board. Selling the EV clubs offers the board a convenient way of resolving the conflict with the management teamof the EV clubs and investors may feel that the board is trying to take an easy path by focusing on what they are comfortable with managing.There may be arguments in favour of the sale, however. The lower WACC will be brought about by a fall in the cost of equity as well as the fall in the cost of debt. A reduction in the complexity of the business may result in a reduction in central management costs.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

《财务成本管理基础》练习题一,单项选择题:1,企业发行债券,在名义利率相同的情况下,对其比较有利的复利计息期是()。

A一年B半年C一季D一月2,某投资方案的年营业收入为100万元,年营业支出为60万元(不包括所得税),其中折旧为10万元,所得税率为40%,该方案每年的营业现金净流量为()。

A 42万元B 56万元C 34万元D 28万元3,对于长期投资决策而言,下列各种说法中不正确的是()。

A按收付实现制计算的现金流量比按权责发生制计算的净收益更加可靠B利用净现值不能揭示某投资方案可能达到的实际报酬率C分别利用净现值、内含报酬率、投资回收期、现值指数法进行项目评价时,结果可能不一致。

D投资回收期和会计收益率法都没有考虑回收期满以后的现金流量状况4,某企业编制“生产预算”,预计第一季度期初存货为120件;预计销售量第一季度为1500件,第二季度1600件;预计年末存货150件。

该企业存货量通常按下期销售量的10%比例安排期末存货,则“生产预算”中第一季度的预计生产量为()。

A 1540件B 1460件C 810件D 1530件5,下列公式中不正确的是()。

A利润=安全边际×边际贡献率 B 安全边际率十盈亏临界点作业率= lC安全边际率十边际贡献率=1 D 正常销售量一盈亏临界点销售量=安全边际6,敏感系数所具有的性质是()。

A敏感系数为正数,参量值与目标值发生同向变化B只有敏感系数大于1的参量才是敏感因素C敏感系数为负数,参量值与目标值发生同向变化D只有敏感系数小于1的参量才是敏感因素7,降低保本点的办法是()。

A降低销售量B减少固定成本C降低售价D提高预计利润8,企业全面预算的出发点及各种预算的基础是()。

A生产预算B销售预算C现金预算D直接人工预算9,A方案在三年内每年年初付款500元,B方案在三年内每年年未付款500元,若贴现率为10%,则两个方案第三年年末时的终值相差()。

A 105B 165.5C 665.5D 50510,下列关于经营杠杆系数的说法,正确的是()。

A在产销量的相关范围内,提高固定成本总额,能降低企业的经营风险B在相关范围内、产销量上升,经营风险加大C在相关范围内,经营杠杆系数与产销量成反向变动D对于某一特定企业而言,经营杠杆系数是固定的,不随产销量的变动而变动11.某投资方案的年营业收入为100万元,年营业支出为60万元,其中折旧为10万元,其余为付现营运成本。

所得税率为40%,该方案每年的营业现金净流量为()。

A 42万元B 56万元C 34万元D 28万元12.下列各种说法中不正确的是()。

A按收付实现制计算的现金流量比按权责发生制计算的净收益更加可靠B利用净现值不能揭示某投资方案可能达到的实际报酬率C分别利用净现值、内含报酬率、现值指数法进行项目评价时,结果可能不一致。

D投资回收期和会计收益率法都没有考虑回收期满以后的现金流量状况13.下列公式中不正确的是()。

A利润=安全边际×边际贡献率B安全边际率十保本点作业率= lC安全边际率十边际贡献率=1 D正常销售量一保本点销售量=安全边际14.既对成本负责,又对收入、利润和投资负责的单位或部门,一般称为()。

A责任中心 B 投资中心 C 利润中心 D 成本中心15.下列表述中不正确的是()。

A净现值是未来现金流入的现值与未来现金流出的现值之间的差额B当净现值为零时,说明此时的贴现率为内含报酬率C当净现值大于零时,现值指数小于1D当净现值大于零时,说明该投资方案可行二,判断分析题:先判断正误,再说明理由:1,甲、乙两人比赛射击,每人射十次。

甲每次都在9环以上,乙射中靶心的比率在90%,所以,甲乙两人射击成绩一样优秀。

2,某公司1998年计划产销甲产品1万件,计划单位成本8元,计划固定成本总额3万元,计划实现利润1万元;1998年实际实现产销量12000件(未突破相关范围),单位成本和售价未变,实现利润12000元。

于是厂长认为计划完成情况很好。

3,通常利润中心被看成是一个可以用利润衡量其业绩的组织单位。

因此,凡是可以计算出利润的单位都是利润中心。

4.在其他条件不变的情况下,固定成本越大,经营杠杆系数就越小,所以,在产销量的相关范围内,降低固定成本,可以使利润提高,但无法降低企业的经营风险。

5,成本中心只对成本负责。

成本又可以分为可控成本和不可控成本,两者都属于成本中心的责任范围之内。

6,管理会计中,为决策需要,将成本分成各种不同类型。

属于相关成本的是历史成本、共同成本、可延缓成本、机会成本、重置成本等类型,属于无关成本的有不可避免成本、沉入成本等。

三,计算分析题1,某企业生产和销售甲、乙两种产品,产品的单价分别为2元和10元,边际贡献率分别为20%和10%,全年固定成本为45000元。

要求:(1)假设全年甲、乙两种产品分别销售 50000件和 30000件,计算下列指标:加权平均边际贡献率;企业保本点销售量;安全边际额;预计利润额。

(2)如果增加广告费5000元,可使甲产品销售量增加至60000件,而乙产品销售量减少到20000件,其他条件不变。

试计算此时的保本点,并说明采用这一广告措施是否合算。