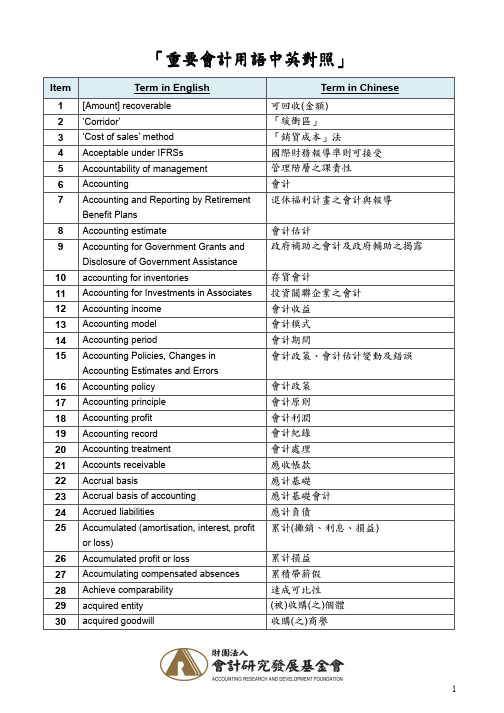

ifrs 重要会计词语英汉对照

IFRS-重要会计用语中英对照

存貨會計 投資關聯企業之會計 會計收益 會計模式 會計期間 會計政策、會計估計變動及錯誤

會計政策 會計原則 會計利潤 會計紀錄 會計處理 應收帳款 應計基礎 應計基礎會計 應計負債 累計(攤銷、利息、損益)

累計損益 累積帶薪假 達成可比性 (被)收購(之)個體 收購(之)商譽

date] 50 adjustment 51 Administrative expenses 52 Admission fees 53 Advance 54 adverse economic consequences 55 adverse event 56 After-tax amount 57 Agency 58 Aggregate 59 Aggregation 60 Agreement date 61 Agricultural activity 62 Agricultural produce 63 Agriculture 64 Allocation

4

「重要會計用語中英對照」

Item

Term in English

134 Bottom-up test 135 business 136 Business combination 137 business combination involving entities or

businesses under common control 138 Business Combinations 139 Business Combinations – “Date of

Term in Chinese

關聯企業 查核報告 核准(發布財務報表) 備供出售金融資產 資產負債表 資產負債表日 資產負債表負債法 銀行 銀行透支 破產 廉價購買 基本每股盈餘 認列基礎調整 結論基礎 基點 標竿處理 有利合約 效益/ 利益/ 福利 福利義務 對使用者之效益 最佳估計 偏誤 投標保證 買方報價/ 買價 買賣價差 具約束力之銷售協議 二項式 生物資產 生物轉化 Black-Scholes-Merton公式 董事會 分紅配股 分紅計畫 合約組合 帳面價值 借款成本

财务术语中英文对照大全

财务术语中英文对照大全一、会计与会计理论会计accounting决策人DecisionMaker投资人Investor股东Shareholder债权人Creditor财务会计FinancialAccounting管理会计ManagementAccounting成本会计CostAccounting私业会计PrivateAccounting公众会计PublicAccounting注册会计师CPACertifiedPublicAccountant国际会计准则委员会IASC美国注册会计师协会AICPA财务会计准则委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship合伙人企业Partnership公司Corporation会计目标AccountingObjectives会计假设AccountingAssumptions会计要素AccountingElements会计原则AccountingPrinciples会计实务过程AccountingProcedures财务报表FinancialStatements财务分析FinancialAnalysis会计主体假设Separate-entityAssumption货币计量假设Unit-of-measureAssumption持续经营假设Continuity(Going-concern)Assumption会计分期假设Time-periodAssumption资产Asset负债Liability业主权益Owner'sEquity收入Revenue费用Expense亏损Loss历史成本原则CostPrinciple收入实现原则RevenuePrinciple配比原则MatchingPrinciple全面披露原则Full-disclosure(Reporting)Principle客观性原则ObjectivePrinciple一致性原则ConsistentPrinciple可比性原则ComparabilityPrinciple重大性原则MaterialityPrinciple稳健性原则ConservatismPrinciple权责发生制AccrualBasis现金收付制CashBasis财务报告FinancialReport流动资产Currentassets流动负债CurrentLiabilities长期负债Long-termLiabilities投入资本ContributedCapital留存收益RetainedEarning------------------------------------------------------------二、会计循环会计循环AccountingProcedure/Cycle会计信息系统AccountinginformationSystem帐户Ledger会计科目Account会计分录Journalentry原始凭证SourceDocument日记帐Journal总分类帐GeneralLedger明细分类帐SubsidiaryLedger试算平衡TrialBalance现金收款日记帐Cashreceiptjournal现金付款日记帐Cashdisbursementsjournal销售日记帐SalesJournal购货日记帐PurchaseJournal普通日记帐GeneralJournal工作底稿Worksheet调整分录Adjustingentries结帐Closingentries---------------------------------------------------------- 三、现金与应收帐款银行存款Cashinbank库存现金Cashinhand流动资产Currentassets偿债基金Sinkingfund定额备用金Imprestpettycash支票Check(cheque)银行对帐单Bankstatement银行存款调节表Bankreconciliationstatement在途存款Outstandingdeposit在途支票Outstandingcheck应付凭单Voucherspayable应收帐款Accountreceivable应收票据Notereceivable起运点交货价F.O.Bshippingpoint目的地交货价F.O.Bdestinationpoint商业折扣Tradediscount现金折扣Cashdiscount销售退回及折让Salesreturnandallowance坏帐费用Baddebtexpense备抵法Allowancemethod备抵坏帐Baddebtallowance损益表法Incomestatementapproach资产负债表法Balancesheetapproach帐龄分析法Aginganalysismethod直接冲销法Directwrite-offmethod带息票据Interestbearingnote不带息票据Non-interestbearingnote出票人Maker受款人Payee本金Principal利息率Interestrate到期日Maturitydate本票Promissorynote贴现Discount背书Endorse拒付费Protestfeecom------------------------------------------------------------ 四、存货存货Inventory商品存货Merchandiseinventory产成品存货Finishedgoodsinventory在产品存货Workinprocessinventory原材料存货Rawmaterialsinventory起运地离岸价格F.O.Bshippingpoint目的地抵岸价格F.O.Bdestination寄销Consignment寄销人Consignor承销人Consignee定期盘存Periodicinventory永续盘存Perpetualinventory购货Purchase购货折让和折扣Purchaseallowanceanddiscounts存货盈余或短缺Inventoryoveragesandshortages分批认定法Specificidentification加权平均法Weightedaverage先进先出法First-in,first-outorFIFO后进先出法Lost-in,first-outorLIFO移动平均法Movingaverage成本或市价孰低法LowerofcostormarketorLCM市价Marketvalue重置成本Replacementcost可变现净值Netrealizablevalue上限Upperlimit下限Lowerlimit毛利法Grossmarginmethod零售价格法Retailmethod成本率Costratio------------------------------------------------------------ 五、长期投资长期投资Long-terminvestment长期股票投资Investmentonstocks长期债券投资Investmentonbonds成本法Costmethod权益法Equitymethod合并法Consolidationmethod股利宣布日Declarationdate股权登记日Dateofrecord除息日Ex-dividenddate付息日Paymentdate债券面值Facevalue,Parvalue债券折价Discountonbonds债券溢价Premiumonbonds票面利率Contractinterestrate,statedrate市场利率Marketinterestratio,Effectiverate普通股CommonStock优先股PreferredStock现金股利Cashdividends股票股利Stockdividends清算股利Liquidatingdividends到期日Maturitydate到期值Maturityvalue直线摊销法Straight-Linemethodofamortization实际利息摊销法Effective-interestmethodofamortization--------------------------------------------------------- 六、固定资产固定资产PlantassetsorFixedassets原值Originalvalue预计使用年限Expectedusefullife预计残值Estimatedresidualvalue折旧费用Depreciationexpense累计折旧Accumulateddepreciation帐面价值Carryingvalue应提折旧成本Depreciationcost净值Netvalue在建工程Construction-in-process磨损Wearandtear过时Obsolescence直线法Straight-linemethod(SL)工作量法Units-of-productionmethod(UOP)加速折旧法Accelerateddepreciationmethod双倍余额递减法Double-decliningbalancemethod(DDB)年数总和法Sum-of-the-years-digitsmethod(SYD)以旧换新Tradein经营租赁Operatinglease融资租赁Capitallease廉价购买权Bargainpurchaseoption(BPO)资产负债表外筹资Off-balance-sheetfinancing最低租赁付款额Minimumleasepayments-------------------------------------------------------- 七、无形资产无形资产Intangibleassets专利权Patents商标权Trademarks,Tradenames著作权Copyrights特许权或专营权Franchises商誉Goodwill开办费Organizationcost租赁权Leasehold摊销Amortization--------------------------------------------------------八、流动负债负债Liability流动负债Currentliability应付帐款Accountpayable应付票据Notespayable贴现票据Discountnotes长期负债一年内到期部分Currentmaturitiesoflong-termliabilities 应付股利Dividendspayable预收收益Prepaymentsbycustomers存入保证金Refundabledeposits应付费用Accrualexpense增值税valueaddedtax营业税Businesstax应付所得税Incometaxpayable应付奖金Bonusespayable产品质量担保负债Estimatedliabilitiesunderproductwarranties赠品和兑换券Premiums,couponsandtradingstamps或有事项Contingency或有负债Contingent或有损失Losscontingencies或有利得Gaincontingencies永久性差异Permanentdifference时间性差异Timingdifference应付税款法Taxespayablemethod纳税影响会计法Taxeffectaccountingmethod递延所得税负债法Deferredincometaxliabilitymethod------------------------------------------------------------ 九、长期负债长期负债Long-termLiabilities应付公司债券Bondspayable有担保品的公司债券SecuredBonds抵押公司债券MortgageBonds保证公司债券GuaranteedBonds信用公司债券DebentureBonds一次还本公司债券TermBonds分期还本公司债券SerialBonds可转换公司债券ConvertibleBonds可赎回公司债券CallableBonds可要求公司债券RedeemableBonds记名公司债券RegisteredBonds无记名公司债券CouponBonds普通公司债券OrdinaryBonds收益公司债券IncomeBonds名义利率,票面利率Nominalrate实际利率Actualrate有效利率Effectiverate溢价Premium折价Discount面值Parvalue直线法Straight-linemethod实际利率法Effectiveinterestmethod到期直接偿付Repaymentatmaturity提前偿付Repaymentatadvance偿债基金Sinkingfund长期应付票据Long-termnotespayable抵押借款Mortgageloan-------------------------------------------------- 十、业主权益权益Equity业主权益Owner'sequity股东权益Stockholder'sequity投入资本Contributedcapital缴入资本Paid-incapital股本Capitalstock资本公积Capitalsurplus留存收益Retainedearnings核定股本Authorizedcapitalstock实收资本Issuedcapitalstock发行在外股本Outstandingcapitalstock库藏股Treasurystock普通股Commonstock优先股Preferredstock累积优先股Cumulativepreferredstock非累积优先股Noncumulativepreferredstock完全参加优先股Fullyparticipatingpreferredstock部分参加优先股Partiallyparticipatingpreferredstock非部分参加优先股Nonpartiallyparticipatingpreferredstock现金发行Issuanceforcash非现金发行Issuancefornoncashconsideration股票的合并发行Lump-sumsalesofstock发行成本Issuancecost成本法Costmethod面值法Parvaluemethod捐赠资本Donatedcapital盈余分配Distributionofearnings股利Dividend股利政策Dividendpolicy宣布日Dateofdeclaration股权登记日Dateofrecord除息日Ex-dividenddate股利支付日Dateofpayment现金股利Cashdividend股票股利Stockdividend拨款appropriation------------------------------------------------------------ 十一、财务报表财务报表FinancialStatement资产负债表BalanceSheet收益表IncomeStatement帐户式AccountForm报告式ReportForm编制(报表)Prepare工作底稿Worksheet多步式Multi-step单步式Single-step----------------------------------------------------------- 十二、财务状况变动表财务状况变动表中的现金基础SCFP.CashBasis(现金流量表)财务状况变动表中的营运资金基础SCFP.WorkingCapitalBasis(资金来源与运用表)营运资金WorkingCapital全部资源概念All-resourcesconcept直接交换业务Directexchanges正常营业活动Normaloperatingactivities财务活动Financingactivities投资活动Investingactivities----------------------------------------------------------- 十三、财务报表分析财务报表分析Analysisoffinancialstatements比较财务报表Comparativefinancialstatements趋势百分比Trendpercentage比率Ratios普通股每股收益Earningspershareofcommonstock股利收益率Dividendyieldratio价益比Price-earningsratio普通股每股帐面价值Bookvaluepershareofcommonstock资本报酬率Returnoninvestment总资产报酬率Returnontotalasset债券收益率Yieldrateonbonds已获利息倍数Numberoftimesinterestearned债券比率Debtratio优先股收益率Yieldrateonpreferredstock营运资本WorkingCapital周转Turnover存货周转率Inventoryturnover应收帐款周转率Accountsreceivableturnover流动比率Currentratio速动比率Quickratio酸性试验比率Acidtestratio------------------------------------------------------------ 十四、合并财务报表合并财务报表Consolidatedfinancialstatements吸收合并Merger创立合并Consolidation控股公司Parentcompany附属公司Subsidiarycompany少数股权Minorityinterest权益联营合并Poolingofinterest购买合并Combinationbypurchase权益法Equitymethod成本法Costmethod------------------------------------------------------------十五、物价变动中的会计计量物价变动之会计Price-levelchangesaccounting一般物价水平会计Generalprice-levelaccounting货币购买力会计Purchasing-poweraccounting统一币值会计Constantdollaraccounting历史成本Historicalcost现行价值会计Currentvalueaccounting现行成本Currentcost重置成本Replacementcost物价指数Price-levelindex国民生产总值物价指数Grossnationalproductimplicitpricedeflator(orGNPdeflator) 消费物价指数Consumerpriceindex(orCPI)批发物价指数Wholesalepriceindex货币性资产Monetaryassets货币性负债Monetaryliabilities货币购买力损益Purchasing-powergainsorlosses资产持有损益Holdinggainsorlosses未实现的资产持有损益Unrealizedholdinggainsorlosses。

会计专业专业术语中英文对照

会计专业专业术语中英文对照一、会计与会计理论会计accounting决策人Decision Maker投资人Investor股东Shareholder债权人Creditor财务会计Financial Accounting管理会计Management Accounting本钱会计Cost Accounting私业会计Private Accounting公众会计Public Accounting注册会计师CPA Certified Public Accountant国际会计准那么委员会IASC美国注册会计师协会AICPA财务会计准那么委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship合伙人企业Partnership公司Corporation会计目标Accounting Objectives会计假设Accounting Assumptions会计要素Accounting Elements会计原那么Accounting Principles会计实务过程Accounting Procedures财务报表Financial Statements财务分析Financial Analysis会计主体假设Separate-entity Assumption货币计量假设Unit-of-measure Assumption持续经营假设Continuity(Going-concern) Assumption会计分期假设Time-period Assumption资产Asset负债Liability业主权益Owner's Equity收入Revenue费用Expense收益Ine亏损Loss历史本钱原那么Cost Principle收入实现原那么Revenue Principle配比原那么Matching Principle全面披露原那么Full-disclosure (Reporting) Principle 客观性原那么Objective Principle一致性原那么Consistent Principle可比性原那么parability Principle重大性原那么Materiality Principle稳健性原那么Conservatism Principle权责发生制Accrual Basis现金收付制Cash Basis财务报告Financial Report流动资产Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益Retained Earning二、会计循环会计循环Accounting Procedure/Cycle会计信息系统Accounting information System Ledger会计科目Account会计分录Journal entry原始凭证Source Document日记帐Journal总分类帐General Ledger明细分类帐Subsidiary Ledger试算平衡Trial Balance现金收款日记帐Cash receipt journal现金付款日记帐Cash disbursements journal销售日记帐Sales Journal购货日记帐Purchase Journal普通日记帐General Journal工作底稿Worksheet调整分录Adjusting entries结帐Closing entries三、现金与应收账款现金Cash银行存款Cash in bank库存现金Cash in hand流动资产Current assets偿债基金Sinking fund定额备用金Imprest petty cash支票Check(cheque)银行对帐单Bank statement银行存款调节表Bank reconciliation statement在途存款Outstanding deposit在途支票Outstanding check应付凭单Vouchers payable应收帐款Account receivable应收票据Note receivable起运点交货价目的地交货价商业折扣Trade discount 现金折扣Cash discount销售退回及折让Sales return and allowance坏帐费用Bad debt expense备抵法Allowance method备抵坏帐Bad debt allowance损益表法Ine statement approach资产负债表法Balance sheet approach帐龄分析法Aging analysis method直接冲销法Direct write-off method带息票据Interest bearing note不带息票据Non-interest bearing note出票人Maker受款人Payee本金Principal利息率Interest rate到期日Maturity date本票Promissory note贴现Discount背书Endorse拒付费Protest fee四、存货存货Inventory商品存货Merchandise inventory产成品存货Finished goods inventory在产品存货Work in process inventory原材料存货Raw materials inventory起运地离岸价格目的地抵岸价格寄销Consignment 寄销人Consignor承销人Consignee定期盘存Periodic inventory永续盘存Perpetual inventory购货Purchase购货折让和折扣Purchase allowance and discounts 存货盈余或短缺Inventory overages and shortages 分批认定法Specific identification加权平均法Weighted average先进先出法First-in, first-out or FIFO后进先出法Lost-in, first-out or LIFO移动平均法Moving average本钱或市价孰低法Lower of cost or market or LCM 市价Market value重置本钱Replacement cost可变现净值Net realizable value上限Upper limit下限Lower limit毛利法Gross margin method零售价格法Retail method本钱率Cost ratio五、长期投资长期投资Long-term investment长期股票投资Investment on stocks长期债券投资Investment on bonds本钱法Cost method权益法Equity method合并法Consolidation method股利宣布日Declaration date股权登记日Date of record除息日Ex-dividend date付息日Payment date债券面值Face value, Par value债券折价Discount on bonds债券溢价Premium on bonds票面利率Contract interest rate, stated rate市场利率Market interest ratio, Effective rate普通股mon Stock优先股Preferred Stock现金股利Cash dividends股票股利Stock dividends清算股利Liquidating dividends到期日Maturity date到期值Maturity value直线摊销法Straight-Line method of amortization实际利息摊销法Effective-interest method of amortization 六、固定资产固定资产Plant assets or Fixed assets原值Original value预计使用年限Expected useful life预计残值Estimated residual value折旧费用Depreciation expense累计折旧Accumulated depreciation帐面价值Carrying value应提折旧本钱Depreciation cost净值Net value在建工程Construction-in-process磨损Wear and tear过时Obsolescence直线法Straight-line method (SL)工作量法Units-of-production method (UOP)加速折旧法Accelerated depreciation method双倍余额递减法Double-declining balance method (DDB) 年数总和法Sum-of-the-years-digits method (SYD)以旧换新Trade in经营租赁Operating lease融资租赁Capital lease廉价购置权Bargain purchase option (BPO)资产负债表外筹资Off-balance-sheet financing最低租赁付款额Minimum lease payments七、无形资产无形资产Intangible assets专利权Patents商标权Trademarks, Trade names著作权Copyrights特许权或专营权Franchises商誉Goodwill开办费Organization cost租赁权Leasehold摊销Amortization八、流动负债负债Liability流动负债Current liability应付帐款Account payable应付票据Notes payable贴现票据Discount notes长期负债一年到期局部Current maturities of long-term liabilities 应付股利Dividends payable预收收益Prepayments by customers存入保证金Refundable deposits应付费用Accrual expense增值税value added tax营业税Business tax应付所得税Ine tax payable应付奖金Bonuses payable产品质量担保负债Estimated liabilities under product warranties 赠品和兑换券Premiums, coupons and trading stamps或有事项Contingency或有负债Contingent或有损失Loss contingencies或有利得Gain contingencies永久性差异Permanent difference时间性差异Timing difference应付税款法Taxes payable method纳税影响会计法Tax effect accounting method递延所得税负债法Deferred ine tax liability method 九、长期负债长期负债Long-term Liabilities应付公司债券Bonds payable有担保品的公司债券Secured Bonds抵押公司债券Mortgage Bonds保证公司债券Guaranteed Bonds信用公司债券Debenture Bonds一次还本公司债券Term Bonds分期还本公司债券Serial Bonds可转换公司债券Convertible Bonds可赎回公司债券Callable Bonds可要求公司债券Redeemable Bonds记名公司债券Registered Bonds无记名公司债券Coupon Bonds普通公司债券Ordinary Bonds收益公司债券Ine Bonds名义利率,票面利率Nominal rate实际利率Actual rate有效利率Effective rate溢价Premium折价Discount面值Par value直线法Straight-line method实际利率法Effective interest method到期直接偿付Repayment at maturity提前偿付Repayment at advance偿债基金Sinking fund长期应付票据Long-term notes payable抵押借款Mortgage loan十、业主权益权益Equity业主权益Owner's equity股东权益Stockholder's equity投入资本Contributed capital缴入资本Paid-in capital股本Capital stock资本公积Capital surplus留存收益Retained earnings核定股本Authorized capital stock实收资本Issued capital stock发行在外股本Outstanding capital stock库藏股Treasury stock普通股mon stock优先股Preferred stock累积优先股Cumulative preferred stock非累积优先股Noncumulative preferred stock完全参加优先股Fully participating preferred stock局部参加优先股Partially participating preferred stock非局部参加优先股Nonpartially participating preferred stock 现金发行Issuance for cash非现金发行Issuance for noncash consideration股票的合并发行Lump-sum sales of stock发行本钱Issuance cost本钱法Cost method面值法Par value method捐赠资本Donated capital盈余分配Distribution of earnings股利Dividend股利政策Dividend policy宣布日Date of declaration股权登记日Date of record除息日Ex-dividend date股利支付日Date of payment现金股利Cash dividend股票股利Stock dividend拨款appropriation十一、财务报表财务报表Financial Statement资产负债表Balance Sheet收益表Ine Statement式Account Form报告式Report Form编制〔报表〕Prepare工作底稿Worksheet多步式Multi-step单步式Single-step十二、财务状况变动表财务状况变动表中的现金根底SCFP.Cash Basis〔现金流量表〕财务状况变动表中的营运资金根底SCFP.Working Capital Basis 〔资金来源与运用表〕营运资金Working Capital全部资源概念All-resources concept直接交换业务Direct exchanges正常营业活动Normal operating activities财务活动Financing activities投资活动Investing activities十三、财务报表分析财务报表分析Analysis of financial statements比拟财务报表parative financial statements趋势百分比Trend percentage比率Ratios普通股每股收益Earnings per share of mon stock股利收益率Dividend yield ratio价益比Price-earnings ratio普通股每股帐面价值Book value per share of mon stock资本报酬率Return on investment总资产报酬率Return on total asset债券收益率Yield rate on bonds已获利息倍数Number of times interest earned债券比率Debt ratio优先股收益率Yield rate on preferred stock营运资本Working Capital周转Turnover存货周转率Inventory turnover应收帐款周转率Accounts receivable turnover流动比率Current ratio速动比率Quick ratio酸性试验比率Acid test ratio十四、合并财务报表合并财务报表Consolidated financial statements吸收合并Merger创立合并Consolidation控股公司Parent pany附属公司Subsidiary pany少数股权Minority interest权益联营合并Pooling of interest购置合并bination by purchase权益法Equity method本钱法Cost method十五、物价变动中的会计计量物价变动之会计Price-level changes accounting一般物价水平会计General price-level accounting货币购置力会计Purchasing-power accounting统一币值会计Constant dollar accounting历史本钱Historical cost现行价值会计Current value accounting现行本钱Current cost重置本钱Replacement cost物价指数Price-level index国民生产总值物价指数Gross national product implicit price deflator (or GNP deflator) 消费物价指数Consumer price index (or CPI)批发物价指数Wholesale price index货币性资产Monetary assets货币性负债Monetary liabilities货币购置力损益Purchasing-power gains or losses资产持有损益Holding gains or losses未实现的资产持有损益Unrealized holding gains or losses。

ifrs准则中英文对照

ifrs准则中英文对照

IFRS准则(International Financial Reporting Standards)是国际

财务报告准则,又称国际会计准则(International Accounting Standards),是世界各国财务报告标准的国际统一标准。

其目的是为了促进全球财务信息的透明度和比较性,提高投资者和利益相关方对

企业财务状况的理解和信任度。

IFRS准则的起源可以追溯到20世纪70年代,当时国际航空运输协会建立了一个财务报告委员会,专门负责制定全球标准财务报告准则。

1989年,国际会计准则委员会(IASB)成立,被授权制定IFRS准则

并推进其全球范围内的推广和实施。

IFRS准则适用于所有上市公司和银行,以及一些非盈利性组织。

其主

要特点是强调财务报告的透明度、可比性和真实性。

其中,最重要的

标准包括IAS 1 (财务报告),IAS 2(存货),IAS 7(现金流量表)和IAS 8(会计政策、会计估计和会计错误)。

IFRS准则的全球推广和实施,旨在促进全球财务信息的透明度和比较性,增强投资者和利益相关方对企业财务状况的理解和信任度。

同时,IFRS准则为企业提供了更好的机会,通过全球化的财务报告标准,获

得更多的国际投资和融资。

当然,IFRS准则在全球范围内的推广和实施也面临诸多挑战,如地域差异、语言障碍、文化差异等。

因此,IFRS准则的设计和实施需要各国政府、监管部门、投资者、企业和专业人士的共同努力和支持,以确保IFRS准则能够真正发挥其充分作用,为全球金融市场的稳定和发展做出更大的贡献。

会计中英文词汇对照

会计中英文词汇对照以下是会计中英文词汇对照(2024新准则):1. 资产 - Assets2. 负债 - Liabilities3. 所有者权益 - Equity4. 股东权益 - Shareholders' equity5. 应付账款 - Accounts payable6. 应收账款 - Accounts receivable7. 资产负债表 - Balance sheet9. 利润 - Profit10. 成本 - Cost11. 现金流量表 - Cash flow statement12. 营业利润 - Operating profit13. 净利润 - Net profit14. 资金流量 - Cash flow15. 凭证 - Voucher16. 会计准则 - Accounting standards17. 会计政策 - Accounting policies18. 会计师 - Accountant19. 年度报表 - Annual report20. 资本 - Capital21. 借方 - Debit22. 贷方 - Credit23. 折旧 - Depreciation24. 减值 - Impairment25. 公允价值 - Fair value26. 经营活动现金流量 - Cash flow from operating activities27. 投资活动现金流量 - Cash flow from investing activities28. 筹资活动现金流量 - Cash flow from financing activities29. 现金及现金等价物 - Cash and cash equivalents30. 投资 - Investment31. 融资 - Financing32. 业务周期 - Business cycle33. 长期负债 - Long-term liabilities34. 短期负债 - Short-term liabilities35. 固定资产 - Fixed assets36. 流动资产 - Current assets37. 其他应收款 - Other receivables38. 存货 - Inventory39. 预付账款 - Prepaid expenses。

国际会计准则会计科目中英对照

国际会计准则会计科目中英对照要说国际会计准则的会计科目中英对照,这事儿听起来是不是有点复杂?但其实你稍微了解一下,就能发现它并不难,甚至可以说挺有意思的。

想象一下,你去一家外国公司做生意,账本上有很多术语你不太明白,稍微转个弯,弄清楚它们的中英文对照,问题就迎刃而解了。

这就像你去外地旅游,碰到不懂的地方,发现一张“翻译单”就觉得一切都能轻松搞定了!要知道,了解这些会计术语可比你去超市找打折商品还省心呢。

看看什么是“资产”吧。

在中文里,资产就是公司拥有的有价值的东西,像现金、设备、库存等等。

那在英文里,资产可不是一眼就能看明白的东西哦。

它就叫“Assets”。

看!是不是简单得很?不过,资产又分很多种,流动资产(Current Assets)和非流动资产(NonCurrent Assets)就是其中两个大类。

流动资产你可以理解成那些一眼看得出来很快能变现的东西,比如现金、存货什么的。

非流动资产呢,就像是你家那台不怎么舍得卖的老电视,买了就很久都不会动的那种,换句话说,它就是那些长期使用的资产,像机器、厂房之类的。

再说说“负债”吧,负债,顾名思义就是公司欠别人的钱。

这可是每个公司都逃不掉的话题。

比如,你从银行贷款,或者向供应商赊账,负债就产生了。

这部分在英文里叫“Liabilities”,简直就是字面意思了,欠的东西得还嘛。

负债也分成短期负债和长期负债,就像你借了一些短期小额的钱,跟你借了十年的房贷不一样,短期负债(Current Liabilities)就是那种快要还掉的账,长期负债(NonCurrent Liabilities)嘛,大家就可以理解成更长时间才能偿还的债务了,反正每个月按期支付,稳稳的。

大家可能会好奇,资产和负债都弄明白了,那企业的“所有者权益”到底是啥?哎,这个其实就是公司老板心头的宝,所有者权益就是公司资产减去负债后的净值。

在英文里呢,叫“Equity”,大家记住这个词,以后听到就知道那是公司“净资产”的代名词。

财务术语中英对照

一、会计与会计理论会计accounting决策人Decision Maker投资人Investor股东Shareholder债权人Creditor财务会计Financial Accounting管理会计Management Accounting成本会计Cost Accounting私业会计Private Accounting公众会计Public Accounting注册会计师CPA Certified Public Accountant国际会计准则委员会IASC美国注册会计师协会AICPA财务会计准则委员会FASB管理会计协会IMA美国会计学会AAA税务稽核署IRS独资企业Proprietorship合伙人企业Partnership公司Corporation会计目标Accounting Objectives会计假设Accounting Assumptions会计要素Accounting Elements会计原则Accounting Principles会计实务过程Accounting Procedures财务报表Financial Statements财务分析Financial Analysis会计主体假设Separate-entity Assumption货币计量假设Unit-of-measure Assumption持续经营假设Continuity(Going-concern)Assumption会计分期假设Time-period Assumption资产Asset负债Liability业主权益Owner's Equity收入Revenue费用Expense收益Income亏损Loss历史成本原则Cost Principle收入实现原则Revenue Principle配比原则Matching Principle全面披露原则Full-disclosure (Reporting) Principle客观性原则Objective Principle 一致性原则Consistent Principle可比性原则Comparability Principle重大性原则Materiality Principle稳健性原则Conservatism Principle权责发生制Accrual Basis现金收付制Cash Basis财务报告Financial Report流动资产Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益Retained Earning二、会计循环会计循环Accounting Procedure/Cycle会计信息系统Accounting information System 帐户Ledger会计科目Account会计分录Journal entry原始凭证Source Document日记帐Journal总分类帐General Ledger明细分类帐Subsidiary Ledger试算平衡Trial Balance现金收款日记帐Cash receipt journal现金付款日记帐Cash disbursements journal 销售日记帐Sales Journal购货日记帐Purchase Journal普通日记帐General Journal工作底稿Worksheet调整分录Adjusting entries结帐Closing entries三、现金与应收帐款现金Cash银行存款Cash in bank库存现金Cash in hand流动资产Current assets偿债基金Sinking fund定额备用金Imprest petty cash支票Check(cheque)银行对帐单Bank statement银行存款调节表Bank reconciliation statement 在途存款Outstanding deposit在途支票Outstanding check应付凭单Vouchers payable应收帐款Account receivable应收票据Note receivable起运点交货价F.O.B shipping point目的地交货价F.O.B destination point商业折扣Trade discount现金折扣Cash discount销售退回及折让Sales return and allowance坏帐费用Bad debt expense备抵法Allowance method备抵坏帐Bad debt allowance损益表法Income statement approach资产负债表法Balance sheet approach帐龄分析法Aging analysis method直接冲销法Direct write-off method带息票据Interest bearing note不带息票据Non-interest bearing note出票人Maker受款人Payee本金Principal利息率Interest rate到期日Maturity date本票Promissory note贴现Discount背书Endorse拒付费Protest fee com四、存货存货Inventory商品存货Merchandise inventory产成品存货Finished goods inventory在产品存货Work in process inventory原材料存货Raw materials inventory起运地离岸价格F.O.B shipping point目的地抵岸价格F.O.B destination寄销Consignment寄销人Consignor承销人Consignee定期盘存Periodic inventory永续盘存Perpetual inventory购货Purchase购货折让和折扣Purchase allowance and discounts 存货盈余或短缺Inventory overages and shortages 分批认定法Specific identification加权平均法Weighted average先进先出法First-in, first-out or FIFO后进先出法Lost-in, first-out or LIFO 移动平均法Moving average成本或市价孰低法Lower of cost or market or LCM 市价Market value重置成本Replacement cost可变现净值Net realizable value上限Upper limit下限Lower limit毛利法Gross margin method零售价格法Retail method成本率Cost ratio五、长期投资长期投资Long-term investment长期股票投资Investment on stocks长期债券投资Investment on bonds成本法Cost method权益法Equity method合并法Consolidation method股利宣布日Declaration date股权登记日Date of record除息日Ex-dividend date付息日Payment date债券面值Face value, Par value债券折价Discount on bonds债券溢价Premium on bonds票面利率Contract interest rate, stated rate市场利率Market interest ratio, Effective rate普通股Common Stock优先股Preferred Stock现金股利Cash dividends股票股利Stock dividends清算股利Liquidating dividends到期日Maturity date到期值Maturity value直线摊销法Straight-Line method of amortization实际利息摊销法Effective-interest method of amortization六、固定资产固定资产Plant assets or Fixed assets原值Original value预计使用年限Expected useful life预计残值Estimated residual value折旧费用Depreciation expense累计折旧Accumulated depreciation帐面价值Carrying value应提折旧成本Depreciation cost净值Net value在建工程Construction-in-process磨损Wear and tear过时Obsolescence直线法Straight-line method (SL)工作量法Units-of-production method (UOP)加速折旧法Accelerated depreciation method双倍余额递减法Double-declining balance method (DDB)年数总和法Sum-of-the-years-digits method (SYD) 以旧换新Trade in经营租赁Operating lease融资租赁Capital lease廉价购买权Bargain purchase option (BPO)资产负债表外筹资Off-balance-sheet financing最低租赁付款额Minimum lease payments七、无形资产无形资产Intangible assets专利权Patents商标权Trademarks, Trade names著作权Copyrights特许权或专营权Franchises商誉Goodwill开办费Organization cost租赁权Leasehold摊销Amortization--------------------------------------------------------八、流动负债负债Liability流动负债Current liability应付帐款Account payable应付票据Notes payable贴现票据Discount notes长期负债一年内到期部分Current maturities of long-term liabilities应付股利Dividends payable预收收益Prepayments by customers存入保证金Refundable deposits应付费用Accrual expense增值税value added tax营业税Business tax应付所得税Income tax payable应付奖金Bonuses payable 产品质量担保负债Estimated liabilities under product warranties赠品和兑换券Premiums, coupons and trading stamps或有事项Contingency或有负债Contingent或有损失Loss contingencies或有利得Gain contingencies永久性差异Permanent difference时间性差异Timing difference应付税款法Taxes payable method纳税影响会计法Tax effect accounting method递延所得税负债法Deferred income tax liability method九、长期负债长期负债Long-term Liabilities应付公司债券Bonds payable有担保品的公司债券Secured Bonds抵押公司债券Mortgage Bonds保证公司债券Guaranteed Bonds信用公司债券Debenture Bonds一次还本公司债券Term Bonds分期还本公司债券Serial Bonds可转换公司债券Convertible Bonds可赎回公司债券Callable Bonds可要求公司债券Redeemable Bonds记名公司债券Registered Bonds无记名公司债券Coupon Bonds普通公司债券Ordinary Bonds收益公司债券Income Bonds名义利率,票面利率Nominal rate实际利率Actual rate有效利率Effective rate溢价Premium折价Discount面值Par value直线法Straight-line method实际利率法Effective interest method到期直接偿付Repayment at maturity提前偿付Repayment at advance偿债基金Sinking fund长期应付票据Long-term notes payable抵押借款Mortgage loan十、业主权益权益Equity业主权益Owner's equity股东权益Stockholder's equity投入资本Contributed capital缴入资本Paid-in capital股本Capital stock资本公积Capital surplus留存收益Retained earnings核定股本Authorized capital stock实收资本Issued capital stock发行在外股本Outstanding capital stock库藏股Treasury stock普通股Common stock优先股Preferred stock累积优先股Cumulative preferred stock非累积优先股Noncumulative preferred stock完全参加优先股Fully participating preferred stock 部分参加优先股Partially participating preferred stock非部分参加优先股Nonpartially participating preferred stock现金发行Issuance for cash非现金发行Issuance for noncash consideration股票的合并发行Lump-sum sales of stock发行成本Issuance cost成本法Cost method面值法Par value method捐赠资本Donated capital盈余分配Distribution of earnings股利Dividend股利政策Dividend policy宣布日Date of declaration股权登记日Date of record除息日Ex-dividend date股利支付日Date of payment现金股利Cash dividend股票股利Stock dividend拨款appropriation十一、财务报表财务报表Financial Statement资产负债表Balance Sheet收益表Income Statement帐户式Account Form报告式Report Form编制(报表)Prepare 工作底稿Worksheet多步式Multi-step单步式Single-step十二、财务状况变动表财务状况变动表中的现金基础SCFP.Cash Basis (现金流量表)财务状况变动表中的营运资金基础SCFP.Working Capital Basis(资金来源与运用表)营运资金Working Capital全部资源概念All-resources concept直接交换业务Direct exchanges正常营业活动Normal operating activities财务活动Financing activities投资活动Investing activities十三、财务报表分析财务报表分析Analysis of financial statements比较财务报表Comparative financial statements趋势百分比Trend percentage比率Ratios普通股每股收益Earnings per share of common stock股利收益率Dividend yield ratio价益比Price-earnings ratio普通股每股帐面价值Book value per share of common stock资本报酬率Return on investment总资产报酬率Return on total asset债券收益率Yield rate on bonds已获利息倍数Number of times interest earned债券比率Debt ratio优先股收益率Yield rate on preferred stock营运资本Working Capital周转Turnover存货周转率Inventory turnover应收帐款周转率Accounts receivable turnover流动比率Current ratio速动比率Quick ratio酸性试验比率Acid test ratio十四、合并财务报表合并财务报表Consolidated financial statements吸收合并Merger创立合并Consolidation控股公司Parent company附属公司Subsidiary company少数股权Minority interest权益联营合并Pooling of interest购买合并Combination by purchase权益法Equity method成本法Cost method十五、物价变动中的会计计量物价变动之会计Price-level changes accounting一般物价水平会计General price-level accounting货币购买力会计Purchasing-power accounting统一币值会计Constant dollar accounting历史成本Historical cost现行价值会计Current value accounting现行成本Current cost重置成本Replacement cost物价指数Price-level index国民生产总值物价指数Gross national productimplicit price deflator (or GNP deflator)消费物价指数Consumer price index (or CPI)批发物价指数Wholesale price index货币性资产Monetary assets货币性负债Monetary liabilities货币购买力损益Purchasing-power gains or losses资产持有损益Holding gains or losses未实现的资产持有损益Unrealized holding gains orlossesaccountant genaral 会计主任account balancde 结平的帐户account bill 帐单account books 帐account classification 帐户分类account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐Accounting period(会计期间)are related to specific time periods ,typically one year(通常是一年)资产负债表:balance sheet 可以不大写b利润表:income statements (or statements of income)利润分配表:retained earnings现金流量表:cash flows2、人员的称谓助理Assistant秘书secretary前台接待小姐Receptionist文员clerk ,如会计文员为Accounting Clerk主任supervisor经理Manager总经理GM,General Manager入场费admission运费freight小费tip学费tuition价格,代价charge制造费用Manufacturing overhead材料费Materials管理人员工资Executive Salaries奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees总监Director总会计师Finance Controller高级Senior 如高级经理为Senior Manager营业费用Operating expenses代销手续费Consignment commission charge运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license plate tax(VVULPT)土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost帐目名词一、资产类Assets流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents外埠存款Other city Cash in bank银行本票Cashier''s cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments - stock债券Short-term investments - corporate bonds基金Short-term investments - corporate funds其他Short-term investments - other短期投资跌价准备Short-term investments falling price reserves应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable 库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrappage低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process - outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investment长期股权投资Long-term investment on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investment on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investments depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备Bcreditor''s rights investment depreciation reserves委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves 机器设备减值准备Machinery equipment depreciation reserves 工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or income待处理固定资产损溢Wait deal fixed assets loss or income 二、负债类Liability短期负债Current liability短期借款Short-term borrowing应付票据Notes payable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应付账款Account payable预收账款Deposit received代销商品款Proxy sale goods revenue应付工资Accrued wages应付福利费Accrued welfarism应付股利Dividends payable应交税金Tax payable应交增值税value added tax payable进项税额Withholdings on VAT已交税金Paying tax转出未交增值税Unpaid VAT changeover减免税款Tax deduction销项税额Substituted money on VAT出口退税Tax reimbursement for export进项税额转出Changeover withnoldings on VAT出口抵减内销产品应纳税额Export deduct domestic sales goods tax转出多交增值税Overpaid VAT changeover未交增值税Unpaid VAT应交营业税Business tax payable应交消费税Consumption tax payable应交资源税Resources tax payable应交所得税Income tax payable应交土地增值税Increment tax on land value payable应交城市维护建设税Tax for maintaining and building citiespayable应交房产税Housing property tax payable应交土地使用税Tenure tax payable应交车船使用税Vehicle and vessel usage license platetax(VVULPT) payable应交个人所得税Personal income tax payable其他应交款Other fund in conformity with paying其他应付款Other payables预提费用Drawing expense in advance其他负债Other liabilities待转资产价值Pending changerover assets value预计负债Anticipation liabilities长期负债Long-term Liabilities长期借款Long-term loans一年内到期的长期借款Long-term loans due within one year一年后到期的长期借款Long-term loans due over one year应付债券Bonds payable债券面值Face value, Par value债券溢价Premium on bonds债券折价Discount on bonds应计利息Accrued interest长期应付款Long-term account payable应付融资租赁款Accrued financial lease outlay一年内到期的长期应付Long-term account payable due within one year一年后到期的长期应付Long-term account payable over one year专项应付款Special payable一年内到期的专项应付Long-term special payable due within one year一年后到期的专项应付Long-term special payable over one year递延税款Deferral taxes三、所有者权益类OWNERS'' EQUITY资本Capita实收资本(或股本) Paid-up capital(or stock)实收资本Paicl-up capital实收股本Paid-up stock已归还投资Investment Returned公积资本公积Capital reserve资本(或股本)溢价Cpital(or Stock) premium接受捐赠非现金资产准备Receive non-cash donate reserve股权投资准备Stock right investment reserves拨款转入Allocate sums changeover in外币资本折算差额Foreign currency capital其他资本公积Other capital reserve盈余公积Surplus reserves法定盈余公积Legal surplus任意盈余公积Free surplus reserves法定公益金Legal public welfare fund储备基金Reserve fund企业发展基金Enterprise expension fund利润归还投资Profits capitalizad on return of investment利润Profits本年利润Current year profits利润分配Profit distribution其他转入Other chengeover in提取法定盈余公积Withdrawal legal surplus提取法定公益金Withdrawal legal public welfare funds提取储备基金Withdrawal reserve fund提取企业发展基金Withdrawal reserve for business expansion提取职工奖励及福利基金Withdrawal staff and workers'' bonus andwelfare fund利润归还投资Profits capitalizad on return of investment应付优先股股利Preferred Stock dividends payable提取任意盈余公积Withdrawal other common accumulation fund应付普通股股利Common Stock dividends payable转作资本(或股本)的普通股股利Common Stock dividends change toassets(or stock)未分配利润Undistributed profit四、成本类Cost生产成本Cost of manufacture基本生产成本Base cost of manufacture辅助生产成本Auxiliary cost of manufacture制造费用Manufacturing overhead材料费Materials管理人员工资Executive Salaries奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees季节性停工损失Loss on seasonality cessation劳务成本Service costs五、损益类Profit and loss收入Income业务收入OPERATING INCOME主营业务收入Prime operating revenue产品销售收入Sales revenue服务收入Service revenue其他业务收入Other operating revenue材料销售Sales materials代购代售包装物出租Wrappage lease出让资产使用权收入Remise right of assets revenue返还所得税Reimbursement of income tax其他收入Other revenue投资收益Investment income短期投资收益Current investment income长期投资收益Long-term investment income计提的委托贷款减值准备Withdrawal of entrust loans reserves补贴收入Subsidize revenue国家扶持补贴收入Subsidize revenue from country其他补贴收入Other subsidize revenue营业外收入NON-OPERATING INCOME非货币性交易收益Non-cash deal income现金溢余Cash overage处置固定资产净收益Net income on disposal of fixed assets出售无形资产收益Income on sales of intangible assets固定资产盘盈Fixed assets inventory profit 罚款净收入Net amercement income支出Outlay业务支出Revenue charges主营业务成本Operating costs产品销售成本Cost of goods sold服务成本Cost of service主营业务税金及附加Tax and associate charge营业税Sales tax消费税Consumption tax城市维护建设税Tax for maintaining and building cities资源税Resources tax土地增值税Increment tax on land value5405 其他业务支出Other business expense销售其他材料成本Other cost of material sale其他劳务成本Other cost of service其他业务税金及附加费Other tax and associate charge费用Expenses营业费用Operating expenses代销手续费Consignment commission charge运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license platetax(VVULPT)土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost营业外支出Nonbusiness expenditure捐赠支出Donation outlay减值准备金Depreciation reserves非常损失Extraordinary loss处理固定资产净损失Net loss on disposal of fixed assets 出售无形资产损失Loss on sales of intangible assets固定资产盘亏Fixed assets inventory loss债务重组损失Loss on arrangement罚款支出Amercement outlay所得税Income tax以前年度损益调整Prior year income adjustment______________________________________________________________________________________________________________Welcome To Download !!!欢迎您的下载,资料仅供参考!-可编辑修改-。

会计术语中英对照

一、会计与会计理论会计 accounting决策人 Decision Maker投资人 Investor国际会计准则委员会 IASC美国注册会计师协会 AICPA财务会计准则委员会 FASB管理会计协会 IMA 美国会计学会 AAA税务稽核署 IRS独资企业 Proprietorship合伙人企业 PartnershipAssumption货币计量假设Unit-of-measure Assumption持续经营假设 Continuity(Going-concern) Assumption会计分期假设 Time-period Assumption 资产 Asset负债 Liability业主权益 Owner's Equity客观性原则 Objective Principle一致性原则 Consistent Principle可比性原则 Comparability Principle 重大性原则 Materiality Principle 稳健性原则 Conservatism Principle 权责发生制 Accrual Basis现金收付制 Cash Basis财务报告 Financial Report帐户 Ledger会计科目 Account会计分录 Journal entry原始凭证 Source Document日记帐 Journal总分类帐 General Ledger明细分类帐 Subsidiary Ledger 试算平衡 Trial Balance三、现金与应收帐款现金 Cash银行存款 Cash in bank库存现金 Cash in hand 流动资产 Current assets偿债基金 Sinking fund定额备用金 Imprest petty cash支票 Check(cheque)目的地交货价 F.O.B destination point商业折扣 Trade discount现金折扣 Cash discount销售退回及折让Sales return andallowance坏帐费用 Bad debt expense 备抵法 Allowance method备抵坏帐 Bad debt allowance利息率 Interest rate到期日 Maturity date本票 Promissory note贴现 Discount 背书 Endorse拒付费 Protest fee com四、存货存货 Inventory定期盘存 Periodic inventory永续盘存 Perpetual inventory购货 Purchase购货折让和折扣 Purchase allowance anddiscounts存货盈余或短缺 Inventory overages and shortages分批认定法 Specific identification下限 Lower limit毛利法 Gross margin method零售价格法 Retail method 成本率 Cost ratio五、长期投资长期投资 Long-term investment长期股票投资 Investment on stocks债券折价 Discount on bonds债券溢价 Premium on bonds票面利率Contract interest rate, stated rate市场利率Market interest ratio, Effective rate普通股 Common Stock优先股 Preferred Stock固定资产 Plant assets or Fixed assets 原值 Original value预计使用年限 Expected useful life预计残值 Estimated residual value 折旧费用 Depreciation expense累计折旧 Accumulated depreciation帐面价值 Carrying value应提折旧成本 Depreciation costbalance method (DDB)年数总和法Sum-of-the-years-digits method (SYD)以旧换新 Trade in经营租赁 Operating lease融资租赁 Capital lease廉价购买权Bargain purchase option (BPO)开办费 Organization cost租赁权 Leasehold摊销 Amortization 八、流动负债负债 Liability流动负债 Current liability应付帐款 Account payable营业税 Business tax应付所得税 Income tax payable应付奖金 Bonuses payable产品质量担保负债Estimatedliabilities under product warranties赠品和兑换券Premiums, coupons and trading stamps或有事项 Contingency九、长期负债长期负债 Long-term Liabilities应付公司债券 Bonds payable有担保品的公司债券 Secured Bonds 抵押公司债券 Mortgage Bonds 保证公司债券 Guaranteed Bonds 信用公司债券 Debenture Bonds 一次还本公司债券 Term Bonds实际利率 Actual rate有效利率 Effective rate溢价 Premium折价 Discount面值 Par value直线法 Straight-line method实际利率法 Effective interest method 到期直接偿付 Repayment at maturity缴入资本 Paid-in capital股本 Capital stock资本公积 Capital surplus留存收益 Retained earnings 核定股本 Authorized capital stock实收资本 Issued capital stock发行在外股本 Outstanding capital stock 库藏股 Treasury stockparticipating preferred stock现金发行 Issuance for cash非现金发行Issuance for noncash consideration股票的合并发行 Lump-sum sales of stock 发行成本 Issuance cost成本法 Cost method面值法 Par value method股票股利 Stock dividend拨款 appropriation十一、财务报表财务报表 Financial Statement 资产负债表 Balance Sheet收益表 Income Statement帐户式 Account Form报告式 Report Form基础(资金来源与运用表)营运资金 Working Capital全部资源概念 All-resources concept直接交换业务 Direct exchanges正常营业活动Normal operating activities财务活动 Financing activities股利收益率 Dividend yield ratio价益比 Price-earnings ratio普通股每股帐面价值Book value per share of common stock 资本报酬率 Return on investment总资产报酬率 Return on total asset债券收益率 Yield rate on bonds已获利息倍数 Number of times interest速动比率 Quick ratio酸性试验比率 Acid test ratio十四、合并财务报表合并财务报表Consolidated financialstatements吸收合并 Merger创立合并 Consolidation控股公司 Parent company一般物价水平会计 General price-level accounting货币购买力会计Purchasing-power accounting统一币值会计Constant dollar accounting历史成本 Historical cost现行价值会计 Current value accounting 现行成本 Current costGNP货币购买力损益 Purchasing-power gains or losses资产持有损益 Holding gains or losses未实现的资产持有损益Unrealizedholding gains or losses。

FRM英语学习词汇表

FRM英语词汇表a payment or serious payments 一次或多次付款abatement 扣减absolute and unconditional payments 绝对和无条件付款accelerated payment 加速支付acceptance date 接受日acceptance 接受accession 加入accessories 附属设备accountability 承担责任的程度accounting benefits 会计利益accounting period 会计期间accounting policies 会计政策accounting principle 会计准则accounting treatment 会计处理accounts receivables 应收账款accounts 账项accredited investors 经备案的投资人accumulated allowance 累计准备金acknowledgement requirement 对承认的要求acquisition of assets 资产的取得acquisitions 兼并Act on Product Liability (德国)生产责任法action 诉讼actual ownership 事实上的所有权additional filings 补充备案additional margin 附加利差additional risk 附加风险additions (设备的)附件adjusted tax basis 已调整税基adjustment of yield 对收益的调整administrative fee 管理费Administrative Law(美国)行政法advance notice 事先通知advance 放款adverse tax consequences 不利的税收后果advertising 做广告affiliated group 联合团体affiliate 附属机构African Leasing Association 非洲租赁协会after-tax rate 税后利率aggregate rents 合计租金aggregate risk 合计风险agreement concerning rights of explore natural resources 涉及自然资源开发权的协议agreement 协议aircraft registry 飞机登记air<I>frame</I> (飞机的)机身airports 机场airworthiness directives (飞机的)适航指令alliances 联盟allocation of finance income 财务收益分配allowance for losses on receivables 应收款损失备抵金alternative uses 改换用途地使用amenability to foreign investment 外国投资的易受控制程度amendment 修改American Law Institute 美国法学会amortization of deferred loan fees and related consideration 递延的贷款费和相关的报酬的摊销amortization schedule 摊销进度表amortize 摊销amount of recourse 求偿金额amount of usage 使用量AMT (Alternative Minimum Tax) (美国)可替代最低税analogous to 类推为annual budget appropriation 年度预算拨款appendix (契约性文件的)附件applicable law 适用法律applicable securities laws 适用的证券法律applicable tax life 适用的应纳税寿命appraisal 评估appraisers 评估人员appreciation 溢价appropriation provisions 拨款条例appropriation 侵占approval authority 核准权approval 核准approximation 近似arbitrary and artificially high value (承租人违约出租人收回租赁物时法官判决的) 任意的和人为抬高的价值arbitration 仲裁arm's length transaction 公平交易arrangement 安排arrest 扣留Article 2A 美国统一商法典关于法定融资租赁的条款articles of incorporation 公司章程AsiaLeaae 亚洲租赁协会assess 评估asset manager 设备经理asset risk insurance 资产风险保险asset securitization 资产证券化asset specificity 资产特点asset tracking 资产跟踪asset-backed financing 资产支持型融资asset-based lessor 立足于资产的出租人asset-oriented lessor (经营租赁中的)资产导向型出租人asset 资产assignee 受让人assignment 让与association 社团at the expiry 期限届满时ATT (automatic transfer of title) 所有权自动转移attachments 附着物attributes 属性auction sale 拍卖audits 审计authenticate 认证authentication 证实authority 当局authorize 认可availability of fixed rate medium-term financing 固定利率中期融资可得到的程度available-for-sale securities 正供出售证券average life 平均寿命average managed net financed assets 所管理的已筹资金资产净额平均值aviation authority 民航当局backed-up servicer 替补服务者backhoe 反铲装载机balance sheet date 资产负债表日bandwidth 带宽bank affiliates 银行的下属机构bank quote 银行报价bankruptcy cost 破产成本bankruptcy court 破产法院bankruptcy law 破产法bankruptcy proceedings 破产程序bankruptcy 破产bareboat charterer 光船承租人bargain renewal option 廉价续租任择权basic earnings per share 每股基本收益basic rent 基本租金(各期应付的租金)beneficiaries 受益人big-ticket items 大额项目bill and collect 开票和收款binding agreement 有约束力的协议blind vendor discount 卖主暗扣bluebook 蓝皮书(美国二手市场设备价格手册)book income 账面收入book loses 账面亏损borrower 借款人BPO(bargain purchase option)廉价购买任择权bridge facility 桥式融通bridge 桥梁broker fee 经纪人费brokers 经纪人build-to-suit leases(租赁物由承租人)承建或承造的租赁协议bulldozer 推土机bundled additional services 捆绑(在一起的)附加服务bundling 捆绑(服务)business acquisition 业务收购business and occupation tax 营业及开业许可税business generation 业务开发business trust 商业信托by(e)-laws 细则byte 字节cable TV network 有线电视网络cable 电缆cancelability 可撤销性cancelable 可撤销的capacity 资格capital allocation 资本分派capital constraint 资金掣肘capital contribution 出资额capital cost 资本费用capital expenditure 基建费用capital lease 融资租赁协议capital market 资本市场capitalize 资本化captive finance company 专属金融公司captives 专属公司carrying amount 维持费用carrying value 账面结存价值case law 案例法cash collatera1 现金抵押cash election 现金选择cash flow coverage ratio 现金流偿债能力比率cash flow 现金流cash receipts and cash applications 现金收入及现金运用casualty value 要因价值(指租赁物毁坏或灭失时承租人应付的赔偿金额)casualty 灾变、事故CAT(computer-added tomograph)依靠电脑的层析X 射线摄影机category 种类causal sale 偶然销售ceiling 上限cellular(mobile)移动通信central authority 中央集权certificate of acceptance 接受证书、验收证书certificate of participation 共享证书certificate 证书charitable trust 公益信托chattel mortgage 动产抵押chattel paper 动产文据checking account 存款支票户checklists 审核内容清单circuit board 线路板civil and commercial law 民商法Civil Code(德国)民法典civil law country(欧洲大陆各国的)大陆法系国家claim 权利要求classes 级别classification criteria 归类标准classification determination 类别的确定classification indicators 分类指标classification of leases 租赁协议分类classification opinion 分类观点classification process 归类过程clawback (用附加税)填补(福利开支)client 顾客clinic 诊所collateral agent 副代理人collateral tracking system 抵押物跟踪制度collateral value 抵押物价值collateralized by third party medical receivables due 以第三方到期医疗应收款作为质押collateral 抵押物collect and disburse 收取和支付collectibility 可收回程度collection 托收comfort level 方便程度commerce clause 商务条款commercial risk 商业风险commercial terms 商业条款commissions 佣金commitment 承诺common carriage 通用车队common law country(英美等)海洋法系国家common trust 共同信托commonality 通用性compensate 补偿competitive risk 竞争风险competitor 竞争者complex finance leases 复杂的融资租赁comprehensive income 综合收入comptroller 审计官computer 计算机conceptual difference 概念上的差别concession period 持有特许权的期间concession 让步、特许conclusion 结论conditional sales agreement 附条件销售协议conditions of usage 使用条件conduit structure 管道结构(的公司)confidentiality 保密性configure 改装conflict 冲突connectivility(信息传递中的)可连通性consensual or non-consensual lien 同意或非经同意的留置权consent 同意consideration 对价consolidation 合并constructive acceptance of collateral 抵押物的指定接受constructive sale 推定出售consulting and advisory services 咨询及顾问服务Consumer Credit Act(德国)消费者信用法consumer price index 消费者价格指数consumer secured transaction 消费者有担保交易consumer transaction 消费者交易consumption tax 消费税container 集装箱contingent rental 随机租金contingent rents 随机租金continuation beyond the termination date 终止日后的接续continuous and close customer contact 同客户持续而紧密的接触contract maintenance(对设备的)合同维修contract origination 合同开发contract pool 合同池contract portfolio 合同组合contract sales 合同出售contracting cost 缔约成本contracting states 缔约国contracts for services 服务合同contractual provisions 合同条款contributions 出资Convention on the Recognition and Enforcement of Foreign Arbitral Award 承认和执行外国仲裁裁决公约convention 公约converted subordinated notes 可转换次级票据convincing case 有说服力的案例core <I>frame</I>work 核心框架corporate aircraft 公务(飞)机corporate debt market 公司债市场corporate guarantees 公司担保corporate income tax 公司所得税corporation 公司correlation 相关性cost of capital 资金成本cost of funds 筹资成本cost of sale 销售成本coterminous rate 同期利率counsel 律师counterclaim 反诉counterpart 副本course of dealing and usage of trade 交易习惯和贸易惯例covenants 契约coverage(保险中的)险别crane 起重机credit and liquidity enhancement 信用及流动性增级credit card receivables 信用卡应收款credit card 信用卡credit development 信用变化credit enhancement 信用增级credit history and profile 信用记录和规模credit rating 信用等级credit risk allocation and management 信用风险的分摊及管理credit risk 信用风险credit underwriting process 信用担保程序credit-based lessor 立足于信用的出租人credit-oriented lessor(经营租赁中的)信贷导向型出租人creditors 债权人creditworthiness 信誉criterion(衡量用的)标准critical goals 关键性目标cross-border funding 跨境融资currency risk 货币风险current and non-current liabilities 当期及非当期负债current ratio 流动比率current realization 即期实现cushion 缓冲customer contact 客户联系customer's purchase cycle 客户的购买周期customers 客户cable TV network 有线电视网络cable 电缆cancelability 可撤销性cancelable 可撤销的capacity 资格capital allocation 资本分派capital constraint 资金掣肘capital contribution 出资额capital cost 资本费用capital expenditure 基建费用capital lease 融资租赁协议capital market 资本市场capitalize 资本化captive finance company 专属金融公司captives 专属公司carrying amount 维持费用carrying value 账面结存价值case law 案例法cash collatera1 现金抵押cash election 现金选择cash flow coverage ratio 现金流偿债能力比率cash flow 现金流cash receipts and cash applications 现金收入及现金运用casualty value 要因价值(指租赁物毁坏或灭失时承租人应付的赔偿金额)casualty 灾变、事故CAT(computer-added tomograph)依靠电脑的层析X 射线摄影机category 种类causal sale 偶然销售ceiling 上限cellular(mobile)移动通信central authority 中央集权certificate of acceptance 接受证书、验收证书certificate of participation 共享证书certificate 证书charitable trust 公益信托chattel mortgage 动产抵押chattel paper 动产文据checking account 存款支票户checklists 审核内容清单circuit board 线路板civil and commercial law 民商法Civil Code(德国)民法典civil law country(欧洲大陆各国的)大陆法系国家claim 权利要求classes 级别classification criteria 归类标准classification determination 类别的确定classification indicators 分类指标classification of leases 租赁协议分类classification opinion 分类观点classification process 归类过程clawback (用附加税)填补(福利开支)client 顾客clinic 诊所collateral agent 副代理人collateral tracking system 抵押物跟踪制度collateral value 抵押物价值collateralized by third party medical receivables due 以第三方到期医疗应收款作为质押collateral 抵押物collect and disburse 收取和支付collectibility 可收回程度collection 托收comfort level 方便程度commerce clause 商务条款commercial risk 商业风险commercial terms 商业条款commissions 佣金commitment 承诺common carriage 通用车队common law country(英美等)海洋法系国家common trust 共同信托commonality 通用性compensate 补偿competitive risk 竞争风险competitor 竞争者complex finance leases 复杂的融资租赁comprehensive income 综合收入comptroller 审计官computer 计算机conceptual difference 概念上的差别concession period 持有特许权的期间concession 让步、特许conclusion 结论conditional sales agreement 附条件销售协议conditions of usage 使用条件conduit structure 管道结构(的公司)confidentiality 保密性configure 改装conflict 冲突connectivility(信息传递中的)可连通性consensual or non-consensual lien 同意或非经同意的留置权consent 同意consideration 对价consolidation 合并constructive acceptance of collateral 抵押物的指定接受constructive sale 推定出售consulting and advisory services 咨询及顾问服务Consumer Credit Act(德国)消费者信用法consumer price index 消费者价格指数consumer secured transaction 消费者有担保交易consumer transaction 消费者交易consumption tax 消费税container 集装箱contingent rental 随机租金contingent rents 随机租金continuation beyond the termination date 终止日后的接续continuous and close customer contact 同客户持续而紧密的接触contract maintenance(对设备的)合同维修contract origination 合同开发contract pool 合同池contract portfolio 合同组合contract sales 合同出售contracting cost 缔约成本contracting states 缔约国contracts for services 服务合同contractual provisions 合同条款contributions 出资Convention on the Recognition and Enforcement of Foreign Arbitral Award 承认和执行外国仲裁裁决公约convention 公约converted subordinated notes 可转换次级票据convincing case 有说服力的案例core <I>frame</I>work 核心框架corporate aircraft 公务(飞)机corporate debt market 公司债市场corporate guarantees 公司担保corporate income tax 公司所得税corporation 公司correlation 相关性cost of capital 资金成本cost of funds 筹资成本cost of sale 销售成本coterminous rate 同期利率counsel 律师counterclaim 反诉counterpart 副本course of dealing and usage of trade 交易习惯和贸易惯例covenants 契约coverage(保险中的)险别crane 起重机credit and liquidity enhancement 信用及流动性增级credit card receivables 信用卡应收款credit card 信用卡credit development 信用变化credit enhancement 信用增级credit history and profile 信用记录和规模credit rating 信用等级credit risk allocation and management 信用风险的分摊及管理credit risk 信用风险credit underwriting process 信用担保程序credit-based lessor 立足于信用的出租人credit-oriented lessor(经营租赁中的)信贷导向型出租人creditors 债权人creditworthiness 信誉criterion(衡量用的)标准critical goals 关键性目标cross-border funding 跨境融资currency risk 货币风险current and non-current liabilities 当期及非当期负债current ratio 流动比率current realization 即期实现cushion 缓冲customer contact 客户联系customer's purchase cycle 客户的购买周期customers 客户damage 损害dampening effect 削弱性效应data transfer 数据转换data transmission 数据传输DDC (dedicated contract carriage)指定车型及司机的合同车队dealer lessors 供应商出租人debt capital 债务资本debt covenant 债务契约debt instruments 债务证书debt issuance costs 债务发行成本debt maturities 债务期限debt securities 债务证券debt service 债息debt-equity ratios 自有资金负债率debt-equity treatment 债务-权益处理debtor 债务人debt-to-equity ratio 权益负债率decay(机械设备的)腐蚀declarations 声明dedicated capacity carriage 指定最低运输量的合同车队dedicated carriage 一应俱全的车厢deductibility 可抵扣程度deduction 扣减default 违约defeasance structures 带有废止条款的结构defense 抗辩deficiency claim 损失索赔deficiency 损失、缺陷definitional maze 定义上的暧昧不明definition 定义deflation 通货紧缩deinstallation 拆卸delay in delivery 延迟交付delinquencies 拖欠delivery and acceptance process 交付及验收程序denunciation 退出deposit account 押金账项deposit taker 存款接受者deposition 处置depreciated value 折余价值depreciation allowance 折旧提存depreciation benefit 折旧好处depreciation deductions 折旧抵扣depreciation expense 折旧费用depreciation period 折旧期间deregulation 解除管制derivative financial instruments 衍生的金融工具designated location 指定的位置detention 扣押detraction 减损developed and mature market 发达而成熟的市场diagnostic equipment 诊断设备differentiation 差别化digitization 数字化diluted earning per share 每股稀释后收益direct and consequential damage 直接和间接损失direct financing lease 直接融资租赁direct tax 直接税disaster recovery services(电脑租赁的)救灾服务disclaimer 免责disclosure items 披露项目discount rate 折现率discounted present value 折现值discretion 自由酌情处理discrimination 差别待遇disguised credit sale 变相信贷销售disguised purchaser of the leased asset 经过伪装的租赁资产买入人(指融资租赁的承租人)dispute resolution process 争议解决程序dissolution 解散distinction 区别distinctive triangular relationship 特有的三边关系distribution 分配diverse nuances 多样化的细微差别diversification 多样化diversity 多样性dividends 红利documentation 文件制作及提供domestic law 国内法double taxation agreement 双重课税协议double tax 双重税double-dip tax leases(租赁一方为美国法人而另一方不是美国法人时的)双重所有权租赁协议down payment 定金down time 窝工时间downgraded 信用等级下降downward sloped interest expense line 趋降的利息费用曲线draftsmanship(合同文本的)起草due diligence 应有的审慎durability 耐久性duration of delay 拖延的持续时间duress 胁迫early buyout 提前买断early termination 提前结束earnings before minority interest 少数权益前收益earnings pattern 收益模型EBO (early buyout)提前买断economic benefits 经济利益economic climate 经济气候economic life 经济寿命economic ownership 经济上的所有权education 教育effective date 生效日effective ownership 有效的所有权effective waiver of defenses(对)抗辩的有效放弃effectiveness 有效性electronic mail 电子邮件eligibility 合格性embedded 嵌入emerging lease markets 新兴租赁市场employee benefit plans 雇员福利计划enactment 实施encumbrance 留置权end-of-term consequences 期末结果end-of-term process 期末程序ends up 倒闭end-users 最终用户enforceable 强制性的enforcing remedies 实施补救engine 发动机enhanced equipment trust certificate 增级的设备信托证书enter into force 生效entitlement 权利资格Environmental Liability Act(德国)环境责任法EPS(earning per share)每股收益率equalizing 等量化equipment cost 设备成本equipment defects 设备瑕疵equipment identification 设备认定equipment leasing industry 设备租赁业equipment risk allocation and management 设备风险的分担及管理Equipment Schedule 设备清单equitable owner 衡平法上的所有权人equity capital 权益资本equity contribution 权益出资equity in net loss of invests 投资净损失中的权益equity insertion 权益嵌入(指经营租赁的出租人在购置用于租赁的货物时要更多地依赖其自有资金)equity investor 权益投资人equity securities 权益证券ERISA(Employee Retirement Income and Security Act)(美国)雇员退休收入及担保法escalation clauses 自动调整条款essential use 实质性使用estate(房地产)产业estimated remaining period 估计的剩余期间estimated residual 估计的余值estimates 估计ETO(early termination option)(对)提前结束(的)任择权evolution 演变excess cash 过剩现金excess deduction 超额扣减exchange 交换excise tax 许可证税exclusive remarketing firms(只处置某类设备的)专业性再处置公司executory cost 执行成本exempt assets 免税资产exempt entity 免税机构exercisable 可行使的exercise price 行使(某项权利,例如购买任择权时的)价格exhaustion 损耗Exhibit(契约性文件的)附件EXIM bank(美国)进出口银行expenditure 开支expertise 专长expiration of the initial lease term 初始租赁期限的届满exposure to residual asset value 所承担的资产残值风险express warranty 明示的担保extended retention of possession 对占有的延伸提留extension 延期external reporting risk 财务报告引起的外部风险FAA(Federal Aviation Administration)(美国)联邦航空署face value 面值factoring company 代理融通公司fair market value leases 公允市值租赁(指租金按租赁市场的常见数额来确定)fair market value transactions 公允市值交易fair value 公允价值fair wear and tear 合理磨损FASB(Federal Accounting Standards Board) 13(美国)财务会计标准委员会第13 号说明:租赁FASIT (financial asset securitizationinvestment trust)金融资产证券化投资信托fatal illness 绝症features 装置federal income tax 联邦所得税Federal Tax Court(德国)联邦税务法庭federally guaranteed mortgage 联邦保证抵押fee receivable 应收费fee subordination 附加费fee-based financing services 以收费为基础的融资服备Felalease 拉美租赁协会fiber optics 光纤fiduciary responsibilities 受托责任filing 备案finance and other income 财务及其它收入finance charges 财务费用finance companies 金融公司、财务公司finance lease laws 融资租赁法律finance lease 融资租赁协议financial assets 金融资产financial bottom line 财务底线financial components 财务成份financial distortion 财务失真financial institution 金融机构financial instruments 金融证书,金融工具financial leasing transaction 融资租赁交易financial leasing 融资租赁financial lessor 融资出租人financial performance 财务业绩financial ratios 财务比率financial reality 财务现实financial reporting risk(因财务失真所导致的)财务报告风险financial statement appearance 资产负债表的表现financial terms 融资条件financiers 融资人financing source 融资来源finding 认定firm term 确定的条款first amendment leases 首期更改租赁协议five different <I>frame</I>works(作为租赁交易宏观环境的)五个不同的框架fixed investment trust 固定投资信托fixed purchase option 固定价格购买任择权fixed rate 固定利率fixed wire 有线(通信)fixture filing 固定备案flexibility 灵活性floating lease accrued interest receivable 浮动租赁应计的应收利息fluctuation 波动FMRV(fair market rental value)公允的租金市值footnote disclosure 通过附注披露foreclosure disposition 扣押抵债处置foreclosure 了结抵押(抵押权人按规定拍卖抵押物以受偿)forklift 叉车form report 格式报告forward rate agreement 远期利率协议forward start swaps 远期掉期four criteria(区别融资租赁和经营租赁的)四项标准fractional interest 零散权益franchise 特许权fraud 欺诈free standing derivative instruments 自力支撑的衍生工具from cradle to grave 从摇篮到坟墓(指自始至终全程服务)front-end payment 前端支付FSL(full-service lease)全程服务租赁fuel use tax 燃料使用税full commitment 全额承诺full disclosure 充分披露full-payout versus non-full-payout 全额支付还是非全额支付full-payout 全额支付full-service lease 全套服务租赁fund appropriation 拨款fund risk 筹资风险funding resources 筹资渠道funding risk 筹资风险furnish 供应future cash flow 未来的现金流future lease payment 未来租赁付款GAAP(generally acceptedaccounting principle)公认会计准则gains 收益gear ratio 资本充足率gearing 资本充足率general intangible 一般无形物geographic distance 地理上的距离German Insolvency Act 德国破产法global leasing industry 全球租赁业global survey 全球调查globalization 全球化goods 货物goodwill 商誉governmental agency 政府(指定的)代理机构governmental body 政府机构governmental fund 政府基金governmental taking 政府征用GPTD(gross profit tax deferral)毛利税递延grantor trust 委托人信托grantors 委托人grantor 授予人growth rate 增长率guaranteed residual value 有担保的残值guarantee 担保hallmark 印记hardware 硬件harmonization(在有着不同法规情况下的)协调headings 标题health care merchant fund incorporation 保健商融资公司health care receivables 保健应收款health care services 保健服务healthcare provider 保健提供者heavy maintenance 大修hedge against inflation 抵御通涨hedge 套期保值helicopters 直升机hell-or high water clauses 绝对责任条款high technology leasing 高技术租赁hire purchase agreement 租购协议hire purchase contracts 租购合同hirer 租入人holders 持有人homogeneity 同质性hospitalization(到)医院治疗hours of use(设备的)使用小时hurdle rate 最低可接受费率IAS(International Accounting Standard) 17 国际会计准则17 租赁IDC(initial direct costs)初始直接费用identification 确认idle capacity 闲置的能力IFC(International Finance Corporation)国际金融公司illness 疾病illustration 演示immaterial items 非实质性事项immediately available fund 立即可以得到的资金impairment of assets 资产减损implementation 执行implicit interest rate 隐含利率implied acceptance 默认接受implied warranty or guarantee 暗示的担保in-bound leases 进口租赁inception of the lease 租赁协议开始日income and expense recognition 收入和支出的确认income statement 损益表income tax 所得税incremental borrowing rate of interest 新增借款利率incurrance of an obligation 义务的承担indebtedness 欠款indemnification 赔偿indemnify 保护indenture trustee 契约受托人independent director 独立董事indexed rate 指数利率(指跟着某个基准利率走的利率)index 指数indirect bank leasing 间接的银行租赁indirect tax 间接税individual lessees 个人承租人industrialization 工业化industry dynamics 行业动向industry lingo 行话(行业内的暗语)information 信息infrastructure 基础设施infringement 侵权in-house expertise(该公司)自有的专长initial accounting 初始的会计处理initial case law 初始判例法initial lease term 初始的租期innovation 创新in-place remarketing 原地再处置input tax 投入税insider transaction 内部交易insolvency 破产inspection findings 检验结果inspection report 检验报告inspection 检验inspector 检验员institutional finance 机构融资instrument 工具、文据insurance carrier 承保人insurance claims 保险索赔insurance coverage 保险类别insurance <I>function</I>保险功能insurance policy 保险单intangible assets 无形资产intangible benefit 无形权益intellectual property right 知识产权intelligence gathering 情报收集intentional or grossly negligent act 故意的或严重疏忽的作为interest and fee income 利息和收费收入interest component of scheduled payments 排定进度付款的利息部分interest rate spreads 利差interest rate swaps 利率掉期interim real estate financing 不动产过渡性融资interim rent 暂行租金(在租金首付日应付的租金)intermediate twin-aisle 中程双过道(指飞机)internal preference(所披露的信息严重扭曲时的)内部参考international financial leasing of equipment 国际设备融资租赁international leasing community 国际租赁界international registration requirement plan(飞机的)国际登记计划要求internationalization 国际化Internet 互联网interperiod tax allocation 各期之间的税收分配invasion 侵犯inventory 盘存、存货清册investment company 投资公司investment grade credit rating 投资等级信用评级investment return 投资回报investors 投资人invoice 发票IOSCO(International Organization of Securities Commissions)证券委员会国际组织IRC(Internal Revenue Code)(美国)国内税收法irrevocable 不可撤销的IRS(Internal Revenue Service)(美国)国内税务局issue notes 出立票据issuer 发行人IT assets 信息技术资产item 项目job qualification sheet 职业资格证judge 法官judgement 裁决judicial arena 司法场所judicially-assisted repossession 司法协助重新占有junk bonds 垃圾债券jurisdictions 司法管辖区label 标记landing gear(飞机的)起落架landing 着陆language(合同中的)用语large ticket asset 大额资产lease application 租赁申请lease fee 租赁费(对租金中所含收益部分的形容)lease for movables 动产租赁协议lease inception 起租日lease intended as security 担保意向租赁lease liabilities 租赁负债lease lines of credit 租赁信贷限额lease manager 租赁协议管理人lease portfolio 租赁协议组合lease registry 租赁协议登记lease tax 租赁税lease termination payment(为)提前结束(租赁协议而作的)支付lease term 租赁期限lease versus purchase 租还是买leased assets 租赁资产leased equipment 租赁设备leased items 租赁物件leased property 租赁财产leasehold 租赁、租借lease-in/lease-out(美国特有的为享受税收待遇而在美国企业同外国企业之间订立的)租入租出租赁协议lease-purchase financing 租购融资leases 租赁协议Leaseurope 欧洲租赁协会leasing activities 租赁业务leasing agreement 租赁协议leasing arrangement 租赁安排leasing company 租赁公司leasing professionals 租赁专业人员leasing regulation 对租赁的管制leasing systems(手工的或电脑的)租赁业务管理系统leasing's share of GDP 租赁占国内生产总值的份额leasing 租赁legal arrangement 法律安排legal consequences 法律后果legal entity 法人legal fees 法律费legal form 法律形式legal issue 法律课题legal ownership 法定所有权legal owner 法定所有权人legal right 法定权利legal risk 法律风险legal status 法律地位legal title 法定所有权legal treatment 法律处理legally empowered 法律授权的legitimate business purpose 合法的营业目的lenders 放款人lenient terms 宽松条款lessee intent 承租人的意向lessee 承租人lessor's internal staff 出租人的内部人员lessor 出租人letter of credit 信用证level of collateral 抵押水平leverage borrowings 杠杆借款leverage ratio 资本充足率leveraged lease 杠杆租赁levy 扣押liabilities 负债liberal depreciation rules 自由折旧规则license 特许licensing agreements 许可证协议licensing of lease activity 对租赁业务的许可lien date 留置日lien 留置权life-limited parts(飞机上)限制其使用小时的部件limitation of liability 责任限度limited ability 有限能力limited liability company 有限责任公司liquidated damage 损失赔偿金liquidator 清算人liquidity facility 流动性融通liquidity support 流动性支持liquidity 现金支付能力litigation 诉讼loans disguised as leases 伪装成租赁的贷款loan-type financing 贷款型融资loan 贷款lobby effort 游说努力local law 当地法律local statues 当地法规local tax 地方税location 所在地lock box account 锁箱账户lock box collection and sweep arrangement(银行的)锁箱和自动转存安排locomotive(铁路)机车long term rental contract 长期出租合同loss containment 亏损防堵loss ratio 赔付率losses 损失lost sales losses 出租人为了再处置收回的租赁物而失去出租新的租赁物的机会所带来的损失MACRS depreciation(美国的)加速成本回收的折旧maintain reserves(飞机租赁中承租人承担的)保养准备金maintenance contract 维修保养合同maintenance interval(飞机发电机的)维修间隔期maintenance policies and procedures 保养方针及程序make-whole premium 凑整升水managerial reporting risk(财务报告导致的)管理层报告的风险manipulation of accounting principles 对会计准则的巧妙运用manufacturer subsidy(来自)制造商(的)补贴marginal tax rate 边际税率market friction 市场摩擦market imperfection 市场的不完善market participants 市场参与者market penetration 市场渗透率market rates of interest 市场利率market share 市场份额market size 市场规模market stability 市场稳定性marketplace 市场环境master lease illustration 租赁协议正文master lease 主租赁协议material facts 重要事实maturity 到期日means 手段measurement criteria 衡量标准mechanism 机制memory <I>function</I>备忘功能mercantile-type sale 商业性销售merchantability 适销性(经营租赁协议中的暗示保证)merges 合并merit review process 事实真相检查程序middle-market leasing 中级市场租赁MIGA(Multilateral Investment Guarantee Agency)多边投资担保署minimum capital 最低资本minimum lease payments receivable 应收最小租赁付款minimum lease terms 最短租赁期限minimum rental rate 最低租金费率mirror-in/mirror-out principle(飞机返还时的维修状况同交付时)一模一样的原则mismatches 不匹配mitigate 缓解(风险)mobility 移动性model 模式modem“猫”(调制解调器)modification 更改monetary policy 货币政策money-over-money lease 钱到钱的租赁(租赁业内对融资租赁的俗称)monitoring 监控monoline insurer 单一险种保险人monopolies 垄断部门monopoly 垄断month-to-month rentals(期满但租赁物未退还时的)逐月收取的租金moratorium 延缓履行mortgage loan placement 抵押贷款安排motor carrier fee 机动车费MPD(maintenance planning document)维修计划书MRI(magnetic resonance imaging)核磁共振成象multiple jurisdiction 涉及多个司法管辖区的multi-years lease commitment 多年的租赁款项承付municipal trade tax 地方贸易税named owner 指名的所有权人。

会计专业专业术语中英文对照

会计专业专业术语中英文对照一、会计与会计理论会计accountingn XXX投资人XXX股东XXX债权人Creditor财务会计Financial Accounting管理会计Management Accounting成本会计Cost Accounting私业会计Private Accounting公众会计Public Accounting注册会计师XXXIASCXXXAICPA财务会计准则委员会FASBXXXIMAXXXAAA税务稽核署IRS独资企业Proprietorship合资人企业Partnershipn会计目标Accounting Objectives管帐假定Accounting ns会计要素Accounting Elements会计原则Accounting Principles管帐实务进程Accounting res财政报表Financial Statements财政分析Financial Analysis会计主体假设Separate-entity n货币计量假设Unit-of-measure n持续经营假设Continuity(Going-concern) d n资产Asset负债Liability业主权益Owner's XXX支出Revenue费用XXXe亏损Loss支出完成原则Revenue Principle配比原则Matching Principle全面披露原则Full-disclosure (Reporting) Principle客观性原则Objective Principle一致性原则Consistent Principle可比性原则Comparability Principle严重性原则Materiality Principle稳健性原则Conservatism Principle权责产生制Accrual Basis现金收付制Cash Basis财务报告Financial Report流动资产Current assets流动负债Current Liabilities长期负债Long-term Liabilities投入资本Contributed Capital留存收益Retained Earning二、会计循环会计循环Accounting re/Cycle管帐信息体系Accounting n System帐户Ledger管帐科目Account会计分录Journal entry原始凭证Source Document日记帐Journal总分类帐General XXX明细分类帐Subsidiary Ledger试算均衡Trial Balance现金收款日记帐Cash receipt journal现金付款日志帐Cash disbursements journal销售日志帐Sales Journal购货日记帐Purchase Journal通俗日志帐General Journal事情初稿Worksheet调整分录Adjusting entries结帐Closing entries三、现金与应收账款现金Cash银行存款Cash in bank库存现金Cash in hand活动资产Current assets偿债基金Sinking fund定额备用金Imprest petty cash支票Check(cheque)银行对帐单Bank statement银行存款调节表XXX在途存款Outstanding deposit在途支票Outstanding check应对笔据Vouchers payable应收帐款Account receivable应收单子Note receivable起运点交货价F.O.B shipping point目的地交货价XXX point贸易扣头Trade discount现金扣头Cash discount销售退回及折让Sales return and allowance坏帐费用Bad XXX备抵法Allowance method备抵坏帐Bad debt allowance损益表法XXX资产欠债表法Balance sheet approach帐龄分析法Aging analysis method直接冲销法Direct write-off method带息单子Interest bearing note不带息单子Non-interest bearing note出票人XXX受款人XXX本金Principal利息率Interest rate到期日Maturity date本票Promissory note贴现Discount背书Endorse拒付费Protest fee com 四、存货存货Inventory商品存货XXX产制品存货Finished XXX 在产品存货XXX原资料存货XXX起XXX shipping point目的地抵岸价格XXX寄销Consignment寄销人Consignor承销人Consignee按期盘存XXX永续盘存XXX购货Purchase购货折让和折扣Purchase allowance and discounts存货盈余或短缺XXX分批认定法Specific n加权平均法Weighted average先进先出法First-in。

ifrs准则中英文对照

IFRS准则中英文对照引言IFRS(国际财务报告准则,International Financial Reporting Standards)是由国际会计准则理事会(IASB,International Accounting Standards Board)颁布的一套国际财务报告准则。

IFRS准则的广泛应用对全球金融市场的稳定和信息透明度起到了重要作用。

IFRS准则的主要内容1. 会计准则的制定1.1 IFRS准则的目的和使用对象•IFRS准则的目的是为了提供用户对企业财务状况、经营绩效和现金流量的准确和公允的信息。

•IFRS准则适用于所有报告目标是全面提供信息的企业,包括上市公司、金融机构和非营利组织等。

1.2 IFRS准则的基本原则•公平表示原则:企业应按照公平表示原则编制财务报表,以反映其真实的财务状况和经营绩效。

•业务实质重于法律形式:企业应根据业务实质进行会计处理,而不仅仅依据法律形式。

•以预测结果为导向:企业应根据预计的经济利益和损益发生即时原则进行会计处理。

2. 财务报表要求2.1 资产负债表•资产负债表应按照资产、负债和股东权益的分类和顺序编制。

•资产负债表中的项目应根据其预计使用周期和流动性进行分类。

2.2 利润表•利润表中的项目应按照其性质和功能进行分类。

•利润表应明确列示企业期间内实现的收入、费用、损益和所得税等信息。

2.3 现金流量表•现金流量表应明确列示现金流入和流出的项目。

•现金流量表分为经营活动、投资活动和筹资活动三个部分。

IFRS准则与国内会计准则的差异IFRS准则与国内会计准则在以下方面存在差异: 1. 会计处理原则:IFRS准则更注重企业财务信息的公允价值,而国内会计准则更注重成本法计量。

2. 财务报告要求:IFRS准则对财务报表的格式和内容有更为详细的规定,包括分类和顺序等;而国内会计准则在这方面规定较为简略。

3. 对业务组合和资产处置的处理:IFRS 准则对业务组合和资产处置有更为详细的规定,而国内会计准则在这方面规定较为模糊。

国际会计准则XXXX《重要会计用语中英对照》