investment_appraisal(1)

财会英语 Financial management

01

foreign currency risk 外汇 风险

0 2 interest rate risk 利率风险

控制的两种方法

forward exchange contracts 远期合约

foreign currency derivatives 衍生品

IRR (the internal rate of return method)内部

收益率(NPV=0)

payback period 回 收期

Maximize shareholders' wealth 股东权益最大化 3. Business finance 企业融 资

soures of finance 融资来 源

1

cash operating cycle 现金运营周期

2

Liquidity ratios 流动性 比率: overcapitalization 投资过热 / overtrading 过度交易

3

Liquidity ratios 流动性比率: over-capitalization 投资过热 / overtrading 过度交易

0 2 2. Investment appraisal 投资评 估

03Biblioteka 3. Business finance 资

企业融

0 4 4. Cost of capital 资本成本

05

5. Risk management 风险 管理

Maximize shareholders' wealth 股东权益最大化

Maximize shareholders' wealth 股东权益最大化 2. Investment appraisal 投资评估

投资的英语单词

投资的英语单词投资指的是特定经济主体为了在未来可预见的时期内获得收益或是资金增值,在一定时期内向一定领域投放足够数额的资金或实物的货币等价物的经济行为。

那么你知道投资的英语单词是什么吗?下面来学习一下吧。

投资英语单词1:investment投资英语单词2:invest投资的英语例句:他访问了泰国与新加坡,以期招揽投资。

He visited Thailand and Singapore to tout for investment.但可口可乐也应当进行这样的投资吗?But should coke be the one making that investment?他们有投资新技术的远见。

They had the foresight to invest in new technology.有充分的证据表明这种投资能够促进增长。

The evidence that such investment promotes growth is strong.公司宣布了一份投资和管理补偿的双重计划。

The company announced a double-barreled investment and management-compensation plan.人们买房投资的强烈意愿People's desire to buy a house as an investment德国空前的繁荣是建立在明智的投资基础之上的。

Germany's unparalleled prosperity is based on wise investments.华尔街一家投资银行的虚假交易计划A phantom trading scheme at a Wall Street investment bank公司正在减少投资,缩减产品系列。

Firms are cutting investment and pruning their product ranges.这家公司不自量力地轻率投资。

IPAA投资项目分析评价软件简介

IPAA投资项目分析评价软件简介一、IPAA投资项目分析评价软件(Investment Project Analysis & Appraisal以下简称IPAA软件)由北京华智博宇咨询有限公司的投资项目分析评价专家和计算机技术人员开发研制。

IPAA软件依据和符合国家发展改革委员会、国家建设部《建设项目经济评价方法与参数》2006年第三版和财政部有关财务税收制度的规定,借鉴和吸取国外项目分析评价软件技术与经验。

在设计思路、功能设置、应用范围、自动高效、性能价格比、方便实用等多方面已达到国内领先水平。

通过建立项目时的行业选择自动转换,实现了使用一套软件进行各行业投资项目、各类型投资项目、各种产出类型投资项目的财务评价、经济评价和多项目多方案分析比选。

IPAA软件2006年底投入实际应用。

IPAA软件已在工业、农业、林业、矿业、建材、电力、交通、城市基础设施、房地产、金融、设计、咨询等行业和大专院校应用。

在2009年依据国家有关设备增值税规定,IPAA软件增加了投资中设备涉及增值税的有关自动处理程序;完善了改扩建项目的分析,在原有多项目多方案比选的基础上,增加增量现金流量表和增量分析;完善了多项目多方案比选;完善了经济评价,增加了矿山类项目有关科目的自动处理;增加了IPAA软件主要操作视频演示,完善了房地产项目分析评价功能。

北京华智博宇咨询有限公司的投资项目分析评价专家长期从事投资项目评价方法技术研究、长期从事投资项目分析评价以及项目咨询实际工作。

承担国家发展改革委员会(原国家计委)、国家建设部《建设项目经济评价方法与参数》1987年1版、1993年2版、2006年3版的研究制定编写工作;具有数百个各类投资项目可行性研究、项目评价以及评估的丰富实践经验;曾于1993-1995年与清华大学合作,主持研制开发IPEA、IPAS投资项目经济评价软件;在全国范围培训各行业从事投资项目可行性研究与分析评价人员5000多人。

常用会计英语词汇

常用会计英语词汇基本词汇1. account 账户,报表2. accounting postulate 会计假设3. accounting valuation 会计计价4. accountability concept 经营责任概念5. accountancy 会计职业6. accountant 会计师7. accounting 会计8. agency cost 代理成本9. accounting bases 会计基础10. accounting manual 会计手册11. accounting period 会计期间12. accounting policies 会计方针13. accounting rate of return 会计报酬率14. accounting reference date 会计参照日15. accounting reference period 会计参照期间16. accrual concept 应计概念17. accrual expenses 应计费用18. acid test ratio 速动比率(酸性测试比率)19. acquisition 收购20. acquisition accounting 收购会计21. adjusting events 调整事项22. administrative expenses 行政管理费23. amortization 摊销24. analytical review 分析性复核25. annual equivalent cost 年度等量成本法26. annual report and accounts 年度报告和报表27. appraisal cost 检验成本28. appropriation account 盈余分配账户29. articles of association 公司章程细则30. assets 资产31. assets cover 资产担保32. asset value per share 每股资产价值33. associated company 联营公司34. attainable standard 可达标准35. attributable profit 可归属利润36. audit 审计37. audit report 审计报告38. auditing standards 审计准则39. authorized share capital 额定股本40. available hours 可用小时41. avoidable costs 可避免成本42. back-to-back loan 易币贷款43. backflush accounting 倒退成本计算44. bad debts 坏帐45. bad debts ratio 坏帐比率46. bank charges 银行手续费47. bank overdraft 银行透支48. bank reconciliation 银行存款调节表49. bank statement 银行对账单50. bankruptcy 破产51. basis of apportionment 分摊基础52. batch 批量53. batch costing 分批成本计算54. beta factor B (市场)风险因素B55. bill 账单56. bill of exchange 汇票57. bill of lading 提单58. bill of materials 用料预计单59. bill payable 应付票据60. bill receivable 应收票据61. bin card 存货记录卡62. bonus 红利63. book-keeping 薄记64. Boston classification 波士顿分类65. breakeven chart 保本图66. breakeven point 保本点67. breaking-down time 复位时间68. budget 预算69. budget center 预算中心70. budget cost allowance 预算成本折让71. budget manual 预算手册72. budget period 预算期间73. budgetary control 预算控制74. budgeted capacity 预算生产能力75. business center 经营中心76. business entity 营业个体77. business unit 经营单位78. by-product 副产品79. called-up share capital 催缴股本80. capacity 生产能力81. capacity ratios 生产能力比率82. capital 资本83. capital assets pricing model 资本资产计价模式84. capital commitment 承诺资本85. capital employed 已运用的资本86. capital expenditure 资本支出87. capital expenditure authorization 资本支出核准88. capital expenditure control 资本支出控制89. capital expenditure proposal 资本支出申请90. capital funding planning 资本基金筹集计划91. capital gain 资本收益92. capital investment appraisal 资本投资评估93. capital maintenance 资本保全94. capital resource planning 资本资源计划95. capital surplus 资本盈余96. capital turnover 资本周转率97. card 记录卡98. cash 现金99. cash account 现金账户100. cash book 现金账薄101. cash cow 金牛产品102. cash flow 现金流量103. cash flow budget 现金流量预算104. cash flow statement 现金流量表105. cash ledger 现金分类账106. cash limit 现金限额107. CCA 现时成本会计108. center 中心109. changeover time 变更时间110. chartered entity 特许经济个体111. cheque 支票112. cheque register 支票登记薄113. classification 分类114. clock card 工时卡115. code 代码116. commitment accounting 承诺确认会计117. common cost 共同成本118. company limited by guarantee 有限担保责任公司119. company limited by shares 股份有限公司120. competitive position 竞争能力状况121. concept 概念122. conglomerate 跨行业企业123. consistency concept 一致性概念124. consolidated accounts 合并报表125. consolidation accounting 合并会计126. consortium 财团127. contingency plan 应急计划128. contingent liabilities 或有负债129. continuous operation 连续生产130. contra 抵消131. contract cost 合同成本132. contract costing 合同成本计算133. contribution centre 贡献中心134. contribution chart 贡献图135. control 控制136. control account 控制账户137. control limits 控制限度138. controllability concept 可控制概念139. controllable cost 可控制成本140. conversion cost 加工成本141. convertible loan stock 可转换为股票的贷款142. corporate appraisal 公司评估143. corporate planning 公司计划144. corporate social reporting 公司社会报告145. cost 成本146. cost account 成本账户147. cost accounting 成本会计148. cost accounting manual 成本手册149. cost adjustment 成本调整150. cost allocation 成本分配151. cost apportionment 成本分摊152. cost attribution 成本归属153. cost audit 成本审计154. cost benefit analysis 成本效益分析155. cost center 成本中心156. cost driver 成本动因157. cost of capital 资本成本158. cost of goods sold 销货成本159. cost of non-conformance 非相符成本160. cost of sales 销售成本161. cost reduction 成本降低162. cost structure 成本结构163. cost unit 成本单位164. cost-volume-profit analysis(CVP) 本量利分析165. costing 成本计算166. credit note 贷项通知167. credit report 信贷报告书168. creditor 债权人169. creditor days ratio 应付账款天数率170. creditors ledger 应付账款分类账171. critical event 关键事项172. critical path 关键路线173. cumulative preference shares 累积优先股174. current asset 流动资产175. current cost accounting 现时成本会计176. current liabilities 流动负债177. current purchasing power accounting 现时购买力会计178. current ratio 流动比率179. cut-off 截止180. CVP 本量利分析181. cycle time 周转时间182. debenture 债券183. debit note 借项通知184. debit capacity 举债能力185. debt ratio 债务比率186. debtor 债务人;应收账款187. debtor days ratio 应收账款天数率188. debtors ledger 应收账款分类账189. debtor' age analysis 应收账款账龄分析190. decision driven costs 决策连动成本191. decision tree 决策树192. defects 次品193. deferred expenditure 递延支出194. deferred shares 递延股份195. deferred taxation 递延税款196. delivery note 交货单197. departmental accounts 部门报表198. departmental budget 部门预算199. depreciation 折旧200. dispatch note 发运单201. development cost 开发成本202. differential cost 差别成本203. direct cost 直接成本204. direct debit 直接借项205. direct hours yield 直接小时产出率206. direct labour cost percentage rate 直接人工成本百分比207. direct labour hour rate 直接人工小时率208. directs on indirect work 间接工作事项上的工时209. discount rate 贴现率210. discounted cash flow 现金流量贴现211. discretionary cost 酌量成本212. distribution cost 摊销成本213. diversions 移用214. diverted hours 移用小时215. diverted hours ratio 移用工时比率216. dividend 股利217. dividend cover 股利产出率218. dividend per share 每股股利219. dog 疲软产品220. double entry accounting 复式会计221. double-entry book-keeping 复式薄记222. doubtful debts 可疑债务223. down time 停工时间224. dynamic programming 动态规划225. earning per share 每股盈利226. earning ratio 市盈率227. economic order quantity(EOQ) 经济订购批量228. efficient market hypothesis 有效市场假设229. efficiency ration 效率性比率230. element of cost 成本要素231. entity 经济个体232. environmental audit 环境审计233. environmental impact assessment 环境影响评价234. EOQ 经济订购批量235. equity 权益236. equity method of accounting 权益法会计计算237. equity share capital 权益股本238. equivalent units 当量239. event 事项240. exceptional items 例外事项241. expected value 期望值242. expenditure 支出243. expenses 费用244. external audit 外部审计245. external failure cost 外部损失成本246. extraordinary items 非常事项247. factory goods 让售商品248. factoring 应收帐款让售249. fair value 公允价值250. feedback 反馈251. FIFO 先近先出法252. final accounts 年终报表253. finance lease 融资租赁254. financial accounting 财务会计255. financial accounts calendar adjustment 财务报表的日历时间调整256. financial management 财务管理257. financial planning 财务计划258. financial statement 财务报表259. finished goods 完成品260. fixed asset 固定资产261. fixed overhead 固定制造费用262. fixed asset turnover 固定资产周转率263. fixed assets register 固定资产登记薄264. fixed cost 固定成本265. flexed budget 变动限额预算266. flexible budget 弹性预算267. float time 浮动时间268. floating charge 流动抵押269. flow of funds statement 资金流量表270. forecasting 预测271. founder's shares 发起人股份272. full capacity 满负荷生产能力273. function costing 职能成本计算274. functional budget 职能预算275. fund accounting 基金会计276. fundamental accounting concept 基础会计概念277. fungible assets 可互换资产278. futuristic planning 远景计划279. gap analysis 间距分析280. gearing 举债经营比率(杠杆)281. goal congruence 目标一致性282. going concern concept 持续经营概念283. goods received note 商品收讫单284. goodwill 商誉285. gross dividend yield 总股息产出率286. gross margin 总边际287. gross profit 毛利润288. gross profit percentage 毛利润百分比289. group 企业集团290. group accounts 集团报表291. high-geared 高结合杠杆(比例)292. hire purchase 租购293. historical cost 历史成本294. historical cost accounting 历史成本会计295. hours 小时296. hurdle rate 最低可接受的报酬率297. ideal standard 理想标准298. idle capacity ration 闲置生产能力比率299. idle time 闲置时间300. impersonal accounts 非记名账户301. imprest system 定额备用制度302. income and expenditure account 收益和支出报表303. incomplete records 不完善记录304. incremental cost 增量成本305. incremental yield 增量产出率306. indirect cost 间接成本307. indirect hours 间接小时308. insolvency 无力偿付309. intangible asset 无形资产310. integrated accounts 综合报表311. interdependency concept 关联性概念312. interest cover 利息保障倍数313. interlocking accounts 连锁报表314. internal audit 内部审计315. internal check 内部牵制316. internal control system 内部控制体系317. internal failure cost 内部损失成本318. internal rate of return(IRR) 内含报酬率319. inventory 存货320. investment 投资321. investment center 投资中心322. invoice register 发票登记薄323. issued share capital 已发行股本324. job 定单325. job card 工作卡326. job costing 工作成本计算327. job sheet 工作单328. joint cost 联合成本329. joint products 联产品330. joint stock company 股份公司331. joint venture 合资经营332. journal 日记账333. just-in-time(JIT) 适时制度334. just-in-time production 适时生产335. just-in-time purchasing 适时购买336. key factor 关键因素337. labour 人工338. labour transfer note 人工转移单339. leaning curve 学习曲线340. ledger 分类账户341. length of order book 定单平均周期342. letter of credit 信用证343. leverage 举债经营比率344. liabilities 负债345. life cycle costing 寿命周期成本计算346. LIFO 后近先出法347. limited liability company 有限责任公司348. limiting factor 限制因素349. line-item budget 明细支出预算350. liner programming 线性规划351. liquid assets 变现资产352. liquidation 清算353. liquidity ratios 易变现比率354. loan 贷款355. loan capital 借入资本356. long range planning 长期计划357. lost time record 虚耗时间记录358. low geared 低结合杠杆(比例)359. lower of cost or net realizable value concept 成本或可变净价孰低概念360. machine hour rate 机器小时率361. machine time record 机器时间记录362. managed cost 管理成本363. management accounting 管理会计364. management accounting concept 管理会计概念365. management accounting guides 管理会计指导方针366. management audit 管理审计367. management buy-out 管理性购买产权368. management by exception 例外管理原则369. margin 边际370. margin of safety ration 安全边际比率371. margin cost 边际成本372. margin costing 边际成本计算373. mark-down 降低标价374. mark-up 提高标价375. market risk premium 市场分险补偿376. market share 市场份额377. marketing cost 营销成本378. matching concept 配比概念379. materiality concept 重要性概念380. materials requisition 领料单381. materials returned note 退料单382. materials transfer note 材料转移单383. memorandum of association 公司设立细则384. merger 兼并385. merger accounting 兼并会计386. minority interest 少数股权387. mixed cost 混合成本388. net assets 净资产389. net book value 净账面价值390. net liquid funds 净可变现资金391. net margin 净边际392. net present value(NPV) 净现值393. net profit 净利润394. net realizable value 可变现净值395. net worth 资产净值396. network analysis 网络分析397. noise 干捞398. nominal account 名义账户399. nominal share capital 名义股本400. nominal holding 代理持有股份401. non-adjusting events 非调整事项402. non-financial performance measurement 非财务业绩计量403. non-integrated accounts 非综合报表404. non-liner programming 非线性规划405. non-voting shares 无表决权的股份406. notional cost 名义成本407. number of days stock 存货周转天数408. number of weeks stock 存货周转周数409. objective classification 客体分类410. obsolescence 陈旧411. off balance sheet finance 资产负债表外筹资412. offer for sale 标价出售413. operating budget 经营预算414. operating lease 经营租赁415. operating statement 营业报表416. operation time 操作时间417. operational control 经营控制418. operational gearing 经营杠杆419. operating plans 经营计划420. opportunity cost 机会成本421. order 定单422. ordinary shares 普通股423. out-of-date cheque 过期支票424. over capitalization 过分资本化425. overhead 制造费用426. overhead absorption rate 制造费用分配率427. overhead cost 制造费用428. overtrading 超过营业资金的经营429. paid cheque 已付支票430. paid-up share capital 认定股本431. parent company 母公司432. pareto distribution 帕累托分布433. participating preference shares 参与优先股434. partnership 合伙435. payable ledger 应付款项账户436. payback 回收期437. payments and receipts account 收入和支出报表438. payments withheld 保留款额439. payroll 工资单440. payroll analysis 工资分析441. percentage profit on turnover 利润对营业额比率442. period cost 期间成本443. perpetual inventory 永续盘存444. personal account 记名账户445. PEPT 项目评审法446. petty cash account 备用金账户447. petty cash voucher 备用金凭证448. physical inventory 实地盘存449. planning 计划450. planning horizon 计划时限451. planning period 计划期间452. policy cost 政策成本453. position audit 状况审计454. post balance sheet events 资产负债表编后事项455. practical capacity 实际生产能力456. pre-acquisition losses 购置前损失457. pre-acquisition profits 购置前利润458. preference shares 优先股459. preference creditors 优先债权人460. preferred creditors 优先债权人461. prepayments 预付款项462. present value 现值463. prevention cost 预防成本464. price ratio 市盈率465. prime cost 主要成本466. prime entry-books of 原始分录登记薄467. principal budget factor 主要预算因素468. prior charge capital 优先股469. prior year adjustments 以前年度调整470. priority base budgeting 优先顺序体制的预算471. private company 私人公司472. pro-forma invoice 预开发票473. problem child 问号产品474. process costing 分步成本计算475. process time 加工时间476. product cost 产品成本477. Product life cycle 产品寿命周期478. production cost 生产成本479. production cost of sales 售货成本480. production volume ratio 生产业务量比率481. profit center 利润中心482. profit per employee 每员工利润483. profit retained for the year 年度利润留存484. profit to turnover ratio 利润对营业额比率485. profit-volume graph 利量图486. profitability index 盈利指数487. programming 规划488. project evaluation and review technique 项目评审法489. projection 预计490. promissory note 本票491. prospectus 募债说明书492. provisions for liabilities and charges 偿债和费用准备493. prudent concept 稳健性概念494. public company 公开公司495. purchase order 订购单496. purchase requisition 请购单497. purchase ledger 采购账户498. quality related costs 质量有关成本499. queuing time 排队时间500. rate 率501. ratio 比率502. ration pyramid 比率金字塔503. raw material 原材料504. receipts and payments account 收入和支付报表505. receivable ledger 应收款项账户506. redeemable shares 可赎回股份507. redemption 赎回508. registered share capital 注册资本509. rejects 废品510. relevancy concept 相关性概念511. relevant costs 相关成本512. relevant range 相关范围513. reliability concept 可靠性概念514. replacement price 重置价格515. report 报表516. reporting 报告517. research cost, applied 应用性研究成本518. research cost, pure or basic 理论或基础研究成本519. reserves 留存收益520. residual income 剩余收益521. responsibility center 责任中心522. retention money 保留款额523. return on capital employed 运用资本报酬率524. returns 退回525. revenue 收入526. revenue center 收入中心527. revenue expenditure 收益支出528. revenue investment 收入性投资529. right issue 认股权发行530. rolling budget 滚动预算531. rolling forecast 滚动预测532. sales ledger 销售分类账533. sales order 销售定单534. sales per employee 每员工销售额535. scrap 废料536. scrip issue 红股发行537. secured creditors 有担保的债权人538. segmental reporting 分部报告539. selling cost 销售成本540. semi-fixed cost 半固定成本541. semi-variable cost 半变动成本542. sensitivity analysis 敏感性分析543. service cost center 服务成本中心544. service costing 服务成本计算545. set-up time 安装时间546. shadow prices 影子价格547. share 股票548. share capital 股份资本549. share option scheme 购股权证方案550. share premium 股票溢价551. sight draft 即期汇票552. single-entry book-keeping 单式薄记553. sinking fund 偿债基金554. slack time 松弛时间555. social responsibility cost 社会责任成本556. sole trader 独资经营者557. source and application of funds statement 资金来源和运用表558. special order costing 特殊定单成本计算559. staff costs 职工成本560. statement of account 营业账单561. statement of affairs 财务状况表562. statutory body 法定实体563. stock 存货564. stock control 存货控制565. stock turnover 存货周转率566. stocktaking 盘点存货567. stores requisition 领料申请单568. strategic business unit 战略性经营单位569. strategic management accounting 战略管理会计570. strategic planning 战略计划571. strategy 战略572. subjective classification 主体分类573. subscribed share capital 已认购的股本574. subsidiary undertaking 子公司575. sunk cost 沉没成本576. supply estimate 预算估计577. supply expenditure 预算支出578. suspense account 暂记账户579. SWOT analysis 长处和短处,机会和威胁分析580. system 制度,体系581. tactical planning 策略计划582. tactics 策略583. take-over 接收584. tangible asset 有形资产585. tangible fixed asset statement 有形固定资产表586. target cost 目标成本587. terotechnology 设备综合工程学588. throughput accounting 生产量会计589. time 时间590. time sheet 时间记录表591. total assets 总资产592. total quality management 全面质量管理593. total stocks 存货总计594. trade creditors 购货客户(应付账款)595. trade debtors 销货客户(应收账款)596. trading profit and loss account 营业损益表597. transfer price 转让价格598. transit time 中转时间599. treasurership 财务长制度600. trail balance 试算平衡表601. turnover 营业额602. uncalled share capital 未催缴股本603. under capitalization 不足资本化604. under or over-absorbed overhead 少吸收或多吸收的制造费用605. uniform accounting 统一会计606. uniform costing 统一成本计算607. unissued share capital 未发行股本608. value 价值609. value added 增值610. value analysis 价值分析611. value for money audit 经济效益审计612. vote 表决613. voucher 凭证614. waiting time 等候时间615. waste 废品(料)616. wasting asset 递耗资产617. weighted average cost of capital 资本的加权平均成本618. weighted average price 加权平均价格619. with resource 有追索权620. without recourse 无追索权621. working capital 营运资本622. write-down 减值623. zero base budgeting 零基预算624. zero coupon bond 无息债券625. Z score 破产预测计分法。

投资用英语怎么说

投资用英语怎么说投资指的是特定经济主体为了在未来可预见的时期内获得收益或是资金增值,在一定时期内向一定领域投放足够数额的资金或实物的货币等价物的经济行为。

那么你知道投资用英语怎么说吗?下面来学习一下吧。

投资的英语说法1:invest投资的英语说法2:investment投资的相关短语:投资者 investor ; financier ;投资人 Investors ;accredited investors ; informal investor投资公司Investment Company ; Investment Companies ; Standard Life Investments ;另类投资Alternative investment ; haha alternative investment ; Alternative Asset ; investment投资管理asset management ; Investment Management ; Fund management ; Fund managers投资学Investment ; Investment Principles ; Theory of Investment ; Investment science投资报酬Return on investment ; return ; Return above investment ; Return aboard investment投资的英语例句:1. He hoped to strike it rich by investing in ginseng.他希望通过投资人参发大财。

2. Investment could dry up and that could cause the economy to falter.投资可能会中断,而这会引起经济衰退。

3. Investment remains tiny primarily because of theexorbitant cost of land.投资仍然微乎其微,主要原因在于土地成本过高。

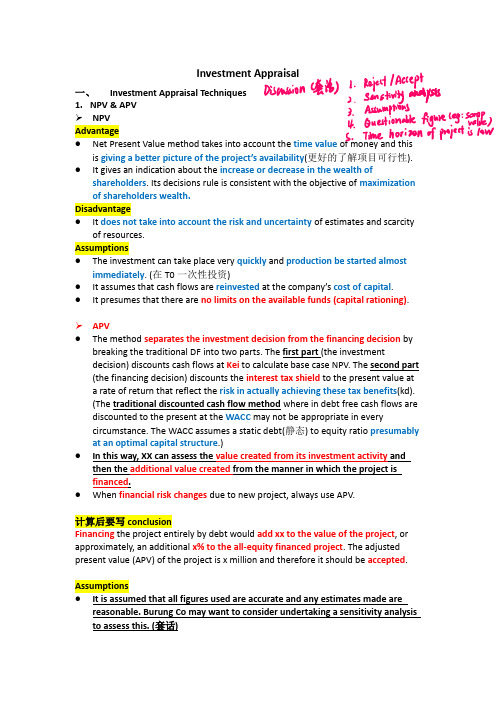

ACCA AFM Investment Appraisal投资决策笔记

Investment Appraisal一、Investment Appraisal Techniques1.NPV & APV➢NPVAdvantage●Net Present Value method takes into account the time value of money and thisis giving a better picture of the project’s availability(更好的了解项目可行性).●It gives an indication about the increase or decrease in the wealth ofshareholders. Its decisions rule is consistent with the objective of maximization of shareholders wealth.Disadvantage●It does not take into account the risk and uncertainty of estimates and scarcityof resources.Assumptions●The investment can take place very quickly and production be started almostimmediately. (在T0一次性投资)●It assumes that cash flows are reinvested at the company’s cost of capital.●It presumes that there are no limits on the available funds (capital rationing).➢APV●The method separates the investment decision from the financing decision bybreaking the traditional DF into two parts. The first part (the investmentdecision) discounts cash flows at Kei to calculate base case NPV. The second part (the financing decision) discounts the interest tax shield to the present value ata rate of return that reflect the risk in actually achieving these tax benefits(kd).(The traditional discounted cash flow method where in debt free cash flows are discounted to the present at the WACC may not be appropriate in everycircumstance. The WACC assumes a static debt(静态) to equity ratio presumably at an optimal capital structure.)●In this way, XX can assess the value created from its investment activity andthen the additional value created from the manner in which the project isfinanced.●When financial risk changes due to new project, always use APV.计算后要写conclusionFinancing the project entirely by debt would add xx to the value of the project, or approximately, an additional x% to the all-equity financed project. The adjusted present value (APV) of the project is x million and therefore it should be accepted. Assumptions●It is assumed that all figures used are accurate and any estimates made arereasonable. Burung Co may want to consider undertaking a sensitivity analysis to assess this. (套话)●It is assumed that XX’s asset beta and all-equity financed discount rate representthe business risk of the project. 可比公司’s entire business may not be similar to the project, and it may undertake other lines of business.(可比公司的asset beta可能是不同业务商业风险加权得到的,可比公司不一定只有一个和该项目一样的业务)●It is assumed that the initial working capital required will form part of the fundsborrowed but that the subsequent working capital requirements will beavailable from the funds generated by the project. (第一年的WC算在债务筹集的资本中,之后WC投入假设来源于每年赚的钱)2.IRR & MIRR➢IRRThe minimum return that projects can generate or the cost of capital at which NPV is ZERO.Advantage●Risk can be incorporated into decision making by adjusting the company’s targetdiscount rate.Disadvantage●IRR assumes that all the cash flows are reinvested in the project at calculatedIRR.●multiple answers●IRR is a relative measure and it does not consider the size of the project.➢MIRR (=project’s return)Modified internal rate of return (MIRR) provides the same result as IRR but it assumes that positive cash flows are reinvested at the firm's cost of capital/WACC (IRR assumes reinvested at IRR).Advantage●MIRR assumes reinvestment of cash flows at cost of capital which is morerealistic in case of having a very high IRR.●single answerDisadvantage●MIRR is also a relative measure so it still does not consider size of the project.二、Incorporating risk into investment appraisal1.Probability analysis (expected value)Can be applied to potential cash flows of projects but is not useful for one-off calculations. If several uncertain variables have been estimated using probability analysis, it is important to note that the potential for inaccuracy in the final NPV calculation is increased.2.(Discounted) paybackA measure of how long it takes to recover the cost of an investment.3.SimulationAn analysis of how changes in more than 1 variable may affect the NPV of a project.3.Sensitivity analysisAn analysis of what % change in one variable (eg: sales) would be needed for the NPV of a project to fall to zero.XX would appear to have some scope可以调整的空间to reduce the XX in order to guarantee the success of the product launch.4.DurationProject duration● A measure of average time to cover the PV of investment returns.●It is the weighted (weight: PV of CF/total CF) average time required to obtaincash flows from the return phase of project.●Duration captures both the time value of money and the whole life of the cashflows of a project.●Projects with higher durations carry more risks. If duration of the project islarge portion of the total life of the project – this means the most of the returns from the project will be recovered in later years.5.Value at risk●The likely change in the value of an investment.●VAR=1,471,000It can be X% confident that the present value will not fall by more than€1,471,000 over its life.AdvantageComparing VAR of different assets and portfolios, the VAR provides an indication of the potential riskiness of a project.DisadvantageIt should be noted that the VAR calculations indicate that the investments involve different risk. However, the cash flows are discounted at the same rate (NPV), which they should not be, since the risk differs between them.由计算VAR得出两个项目风险不同,但NPV的折现率是相同的❖NPV&IRR&MIRR&VAR指标选择Where projects are mutually exclusive, the IRR can give an incorrect answer.IRR&MIRR&NPVIRR assumes that returns are re-invested at the IRR, whereas NPV and the modified IRR assume that they are re-invested at the cost of capital (discount rate). The cost of capital is a more realistic assumption as this is the minimum return required by investors in a company. NPV(项目收益率绝对值)与MIRR(相对值)是一致的VAR&NPV●The VAR provides an indication of the potential riskiness of a project.●It should be noted that the VAR calculations indicate that the investmentsinvolve different risk. However, the cash flows are discounted at the same rate (NPV), which they should not be, since the risk differs between them.●When risk is also taken into account, the choice between the projects is not clearcut and depends on company’s attitude to risk and return.套话必备This is before taking into account additional uncertainties such as trading in an area in which XX is not familiar.6.Option pricingBlack Scholes model (BSOP)The Black-Scholes model values options before the expiry date and takes account of all the determinants that effect the value of option.Assumptions and Limitations●No Transaction Costs or taxes●The real option is a European-style option, which can only be exercised on thedate that the option expires.●Investor can borrow at the risk-free rate●Risk free rate and share price volatility is constant over the periodNET PRESENT VALUE (NPV) AND REAL OPTIONS●When making decisions, following investment appraisals of projects, net presentvalue assumes that a decision must be made immediately or not at all, and once made, it cannot be changed. Real options, on the other hand, recognise that many investment appraisal decisions have some flexibility.●NPV captures just the intrinsic value, whereas real option captures both intrinsicvalue and time value. Real options view risks and uncertainties as opportunities.By incorporating the value of any real options available into an investment appraisal decision, entity will be able to assess the full value of a project.三、Cost of capitalThe cost of the different forms of capital reflect their risk; in the event of a company being unable to pay its debts and going into liquidation, ordinary shareholders rank after preference shareholders, who in turn rank after the providers of debt finance. 1)Project specific costs of capitalEquity beta: reflect both business risk and financial risk.Asset beta (beta u/i): only reflect business risk.To understand the level of business risk, the equity beta needs to be adjusted by stripping out the effect of gearing to create an ungeared or asset beta (business risk).❖商业风险加权思想背景:不一定能找到只做单一行业的proxy company,proxy的biz risk由不同行业的biz risk按业务占比加权组成举例:About 15% of its business is in the luxury transport (target business) market and Reka Co’s equity beta is 1·6. It is estimated that the asset beta of the non-luxury transport industry is 0·80.分析:1.Equity beta-ungeared得到asset beta= 0.892.总asset beta 0.89=15%(target business)*target beta a+85%*0.83.target beta a = 1.4Assumption:It is assumed that the asset beta is a weighted average of the asset betas of business 1 and business 2, using non-current assets invested in each business unit as a fair representation of the size of each business unit.2)Theories of capital structureTraditional theory-WACC●There is an optimal capital structure at which the company’s WACC is at itsminimum.●Traditional theory suggests that using some debt will lower WACC, but if gearingrises above an acceptable level then the cost of equity will rise dramatically causing the WACC to rise.●WACC Assumptions-In the long-term the company will maintain its existing capital structure (ie financial risk is unchanged)-The project has the same risk as the company (ie business risk is unchanged). Modigliani & Miller (M&M) theoryWithout taxM&M demonstrated that, ignoring tax, the use of debt simply transfers more risk to shareholders, and that this makes equity more expensive so that the use of debt does not reduce finance costs.With taxM&M then introduced the effect of corporation tax to demonstrate that if debt also saves corporation tax then it does reduce finance costs, which benefits shareholders.Key AssumptionKd will remain constant at all level of gearing because there is no financial distress cost.MM formula3)The cost of equitya.Dividend growth model(P0=D1/(Ke-g)) (考试不给)*Assumption: Dividend growth can be estimated and is constant.Estimating ‘g’-Use historic growth-Use current re-investment levels ‘g=br’‘b’=1-payout%, ‘r’=Earnings /equity(ROE)权益净利率(每一单位净资产赚的钱) b.CAPM:Ke = Rf+β(Rm-Rf)(Un)Systematic risk-Rational, risk averse investors will spread their investment across a wide range of securities in order to reduce their exposure to risk.-Unsystematic (or specific) risk is gradually eliminated as the investor increases the diversity of the portfolio until a point where it need not be considered (the “well-diversified portfolio”).-Systematic (or 'market') risk is caused by factors which affect all industries and businesses to some extent.CAPM AssumptionCAPM assumes that investors have a broad range of investments, and are worried about how a fall in the stock market as a whole would affect their investments.βfactorCommercial databases monitor the sensitivity of firms to a stock market downturn by calculating the average fall in the return on a share each time there is a 1% fall in the stock market as a whole. 当市场每波动1%,个股收益的波动值Limitations of the CAPM-Estimating market return幸存者偏差Achieved by estimating comparing movements in the stock market as a whole; this will be volatile and will overstate the returns achieved because it will not pick up the firms that have failed and have dropped out of the stock market. 测算时只使用现在尚存的公司,而没有记录已经倒闭的公司-Estimating the beta factorBeta values are historic and will not give an accurate measure of risk if the firm has recently changed its gearing or its strategy. 测算使用历史数据但如果现在公司财务结构/业务行业/战略改变将会有一定偏差c.MM formula4)Cost of debtredeemable debt: 内插法use IRR (interest payment可抵税)preference shares:D/P0 (no tax relief)Bond credit spread: kd=Rf + basis pointConvertible loan notes (2018/Mar&Jun Q2)Advantages●The conversion rights mean that these directors will benefit if the share priceincreases, aligning their interests with shareholders.●The conversion terms also mean that the loan notes will not necessarily have tobe repaid in a few years’ time. This may be significant if the entity does not have the cash available for redemption then.●The option to convert is an advantage for convertible loan note holders. Theywould often effectively pay for this option by receiving a lower rate of interest on the loan notes.Drawbacks●The convertible loan notes would be treated as debt, increasing gearing, whichmay concern the other shareholders. The interest on the convertible loan notes will be payable before dividends and may leave less money for distribution to shareholders.●(Case related) Shareholders may doubt whether the higher interest burden onthe convertible loan notes compared with the subsidised loan is compensated for by the lower costs of Tippletine Co not having to fulfil the government’srequirements. The other shareholders may be concerned by the interest rate on the convertible notes being Tippletine Co’s normal cost of borrowing正常可转债的利率应低于普通债,这里利率没有变低,怀疑是否有利益关系.●Shareholders would want to assess how likely conversion would be, that is howlikely it would be the share price will rise above $2·75. The option to convert may also change the balance of shareholdings, giving the directors who held thenotes a greater percentage of share capital and possibly more influence overTippletine Co. The other shareholders may be unhappy with this.●The shareholders may also have reservations about the loan note holders havingthe option to redeem(强制赎回) if Tippletine Co’s share price is low. Thisreduces the risk of providing the finance from the loan note holders’ viewpoint.However, if the share price is low, Tippletine Co’s financial results and cash flows may be poor and it may struggle to redeem the loan notes.●Shareholders may also be concerned that there is no cap the other way, allowingTippletine Co to force conversion(强制转换) if the share price reaches a highenough level.四、International investment appraisal - NPV1.Issues for MNCs (跨国公司)Government requirementsIndividual countries have imposed their own restrictions from time to time by, for example, reserving保留certain shareholdings for their own nationals or by l imiting the transference of profits or royalties.Mobility of capital 流动性changes in the economythat political action will affect the position and value of a company.●Confiscation political riskThis is the risk of loss of control over the foreign entity trough intervention of the local government.●Financial political risk-Restrictions on local borrowing.-Restrictions on sending back capital, dividends or other remittances.Dealing with political risk-Negotiations with host government: obtain a concession agreement-Insurance-Production strategies: It may be necessary to strike a balance between using local sources and producing directly.Exchange control regulationsCultural risksCultural risks affect the products and services produced and the way organizations are managed and staffed. Businesses should take cultural issues into account when deciding where to sell abroad, and how much to centralize activities.2.FDI优缺点3.Assumptions in international NPV calculation4.Risk in projectsTransaction exposure is the risk of adverse exchange rate movements occurring in the course of normal international trading transactions.(Hedging using a variety of financial products.)Translation exposure(折算风险) arises from differences in the currencies in which assets and liabilities are denominated.These effects become most obvious when consolidated group accounts are prepared and the values of assets denominated in foreign currency are translated into the home currency. (集团在外国的资产编入合并报表时要用汇率折算,价值会变化)Such risk can be reduced if assets and liabilities denominated in particular currencies can be held in balanced amounts. (调整资产和负债结构)Economic exposure refers to changes in the exchange rate which adversely affecting the international competitiveness. This is different from transaction risk only in that it is of long term in nature and the amount of exposure cannot be certain yet. Thus, transaction risk may be view as a short-term economic exposure.Every firm will be affected by this exposure, regardless of whether it deals directly with foreign currency transaction or not.The project NPV is initially calculated using forecast exchange rates, where a change over the project life will increase or decrease NPV and hence the gain to SH. Purchasing power parity (PPP:h-ex) predicts that the exchange rates between two currencies depend on the relative difference in the rates of inflation in each country. Therefore, if one country has a higher rate of inflation compared to another, then its currency is expected to depreciate over time.5.Transfer pricingWith taxThe transfer price is the price charged by one part of a company when supplying goods or services to another part of the company (oversea subsidiary).By manipulating the transfer prices charged, it may be possible to minimise the overall taxation cost for the group. Therefore, the transfer price policy may be unsuccessful, as most governments require the transfer price to be set on an ‘arm’s length’ basis(公正客观-market value).Although the above may decrease the taxation the profits will end up in oversea subsidiary. If the currency of subsidiary is weak relative to the holding company, then loss from the depreciation may be more than tax saving.With performance evaluationSetting the transfer price at market price should enable a fair assessment of the performance of both the buying and selling divisions. However, this may distort performance in that the costs of internal sales may be lower than external sales. For example, administration costs should be lower and there should be no costs of bad debts. These cost savings should be shared between the two divisions to give a fair picture.In theory, using market price should mean that the central treasury function has tointervene less. However, in reality, there may be complications that require central intervention. The market price may be difficult to determine or may fluctuate wildly, and central treasury may have to decide which price to use. If it is decided that an allowance should be made for costs of internal transfer being lower, central treasury may have to determine what this should be as it may vary significantly between products and divisions.。

财务成本管理英语完整版

财务成本管理英语完整版财务成本管理英语 HEN system office room 【HEN16H-HENS2AHENS8Q8-HENH1688】INVESTMENT APPRAISAL[对应中⽂教材2008年财务成本管理第五章:投资管理](已动⽤资本回报率)or ARR(会计收益率)(Accounting Rate of Return)(回收期法)Payback period=Initial payment/Annual cash inflow, payback is not always an exact number of yearsMost common formula:ROCE=EBIT (after depreciation)/ initial capital costsC NPV(净现值法)(1) Basic assumptions:·cash outlay occurs in year 0 (now).·cash flows occur at the end of the year.·if a cash flow occurs at the beginning of a year, it is assumed to occur at the end of the previous year.D IRR(内含报酬率法)(1)Basic principle: IRR is the cost of capital at which the NPV is zero, if the expected IRR is higher than a target rate of return; the project is financially worth undertaking.(2)Selection between IRR and NPV: when a choice has to be made between mutually exclusive projects, in such case the NPV should be selected, because higher NPV can maximize sharehold er’s wealth.DefinitionThe discount rat which, when applied to the cash flows of a project, gives an NPV of zero.OrThe break-even interest rate for a project.It is the maximum rate of interest that you could afford to pay on a project without making a loss.FeaturesAdvantages -Takes into account the time value of money-Relative measure-More readily understood than NPVDisadvantages -May not be unique – projects can have more than one IRR- May rank projects incorrectly – for mutually exclusive projects or whenFunds are short supply- Cannot cope with changing rates of interestThe method of calculation depends upon whether or not the project has even cash flows.Even cash flowsConsider an investment of £ that generates net cash earnings of £10m for 5yearsThe IRR is the discount rate that gives a NPV of zero. This means that the IRR is theRate that will discount five installments of £10m to a present value of £. This in turnMeans that the IRR is the discount rate for which the 5year annuity factor is . A The project’s IRR has been found via a cumulative discount factor (annuity factor) givenBy:Annuity factorat the IRR=for the life of the projectUneven cash flowsThese have to be found by trial and error or by estimating using two present values.Where:A=lower rate chosen=NPV at rate AB=higher rate=NPV at rate BIt helps to get A and B as close t o the true IRR as possible, but it doesn’t matter whetherthe resultant NPVs are positive, negative or one of each.Some students prefer to use a common sense approach rather than a formula. Seeing by nowMuch NPV has fallen (from to) as the discount rate has risen from A to B, They find how much more the discount rate needs to rise to bring the NPV to zero.Whether the formula is used or common sense, the calculation assumes a linear relationshipBetween NPV and discount rate. In fact the relationship is not linear, hence the calculationIs only approximate and (unless you have been lucky when guessing which discount rates touse)you should not quote IRR’s calculated in this way to many, not toany,decimal places –unless the examiner asks you.IRR of a perpetuityThe present value of a perpetuity is the annual cash flow divided by the discount rate(expressed as a decimal. From this it follows that:the IRR of a perpetuity ==100Perpetuity: 永续年⾦Method of presentationA simple calculation such as those for Woods can be done on a single line. For larger projectstwo possibilities exist:(i) the cash budget approach(ii) the tabular approach.(1)Cash budget approachTime 0 1 2 3£’000£’000£’000£’000Investment (X)—— XAdvertising (X)(X) - -Working capital (X)- - XMaterials (X)(X)(X)-Labour —(X)(X)(X)Overheads —(X)(X)(X)Revenue ———X————Net cash flow (X)(X)(X) X————y% Discount factor 1 X X XPresent value (X)(X)(X)XNet present value (£’000)XThe cash budget approach is suitable for short projects with lots of different cash flows Which change from year to year.(2) Tabular approachTime Cash flow y% Discount Present value£’000£’000£’0000 Investment (X) 1 (X)0 and 1 Advertising (X)X (X)0 Working capital (X) 1 (X)0-9 Materials (X) 1 (X)1-10 Labour and overheads (X)X (X)1-10 Revenue X X X 10 Sales proceeds X X X10 WC recovery X X X—Net present value (£’000)XThe tabular approach is suitable for long projects with lots of different cash flows that are The same from year to year (enabling annuity factors to be used).Picking the right figuresWhen carrying out discounted cash flow analysis it is important to select the right figures. Ignore:costs – amounts that have already been spent– not a cash flowvalues – not a cash flow–incremental fixed costs (look out for the words “reapportioned fixed overheads”)costs – taken into account by the discounting processInclude:Those cash flows that are specifically received or incurred as a result of the acceptance of the project(future–incremental–cash flows).Asset replacement decisionFactors to be considered when making replacement decision are as follows:·capital cost of new equipment;·operating costs, increased repair and maintenance costs;loss of productivity;lower of quality and quantity of output;One application of discounted cash flow is to make decisions concerned with the replacement ofMachinery. This applies to short – life assets that will need to be replaced in perpetuity (. motorCars or photocopiers). As a machine gets older, it is likely to cost more to keep it running and itsScrap value will decrease. The aim is to find the optimal replacement cycle for the machine,. how often it should be replaced - before it becomes uneconomic to own.A simple approach would involve finding the total cost of keeping an asset for 1,2,3 years, etc,Then finding an average annual cost.DCF VersionNow, each possible replacement cycle is treated as a project (1-year, 2-year, or 3-year project).You calculate the NPV of each project (rather than just the total cost).Instead of dividing the NPV’s by 1,2,or 3, they’re divided by the 1,2, or 3-year annuity factorTo find an equivalent annual cost.Equivalent annual cost =。

财务会计专用英语

常用会计类英语词汇汇总根本词汇(1)account 账户,报表(2)accounting postulate 会计假设(3)accounting valuation 会计计价(4)accountability concept 经营责任概念(5)accountancy 会计职业(6)accountant 会计师(7)accounting 会计(8)agency cost 代理本钱(9)accounting bases 会计根底(10)accounting manual 会计手册(11)accounting period 会计期间(12)accounting policies 会计方针(13)accounting rate of return 会计报酬率(14)accounting reference date 会计参照日(15)accounting reference period 会计参照期间(16)accrual concept 应计概念(17)accrual expenses 应计费用(18)acid test ratio 速动比率(酸性测试比率)(19)acquisition 收购(20)acquisition accounting 收购会计(21)adjusting events 调整事项(22)administrative expenses 行政管理费(23)amortization 摊销(24)analytical review 分析性复核(25)annual equivalent cost 年度等量本钱法(26)annual report and accounts 年度报告和报表(27)appraisal cost 检验本钱(28)appropriation account 盈余分配账户(29)articles of association 公司章程细那么(30)assets 资产(31)assets cover 资产担保(32)asset value per share 每股资产价值(33)associated company 联营公司(34)attainable standard 可达标准(35)attributable profit 可归属利润(36)audit 审计(37)audit report 审计报告(38)auditing standards 审计准那么(39)authorized share capital 额定股本(40)available hours 可用小时(41)avoidable costs 可防止本钱(42)back-to-back loan 易币贷款(43)backflush accounting 倒退本钱计算(44)bad debts 坏帐(45)bad debts ratio 坏帐比率(46)bank charges 银行手续费(47)bank overdraft 银行透支(48)bank reconciliation 银行存款调节表(49)bank statement 银行对账单(50)bankruptcy 破产(51)basis of apportionment 分摊根底(52)batch 批量(53)batch costing 分批本钱计算(54)beta factor B (市场)风险因素B(55)bill 账单(56)bill of exchange 汇票(57)bill of lading 提单(58)bill of materials 用料预计单(59)bill payable 应付票据(60)bill receivable 应收票据(61)bin card 存货记录卡(62)bonus 红利(63)book-keeping 薄记(64)Boston classification 波士顿分类(65)breakeven chart 保本图(66)breakeven point 保本点(67)breaking-down time 复位时间(68)budget 预算(69)budget center 预算中心(70)budget cost allowance 预算本钱折让(71)budget manual 预算手册(72)budget period 预算期间(73)budgetary control 预算控制(74)budgeted capacity 预算生产能力(75)business center 经营中心(76)business entity 营业个体(77)business unit 经营单位(78)by-product 副产品(79)called-up share capital 催缴股本(80)capacity 生产能力(81)capacity ratios 生产能力比率(82)capital 资本(83)capital assets pricing model 资本资产计价模式(84)capital commitment 承诺资本(85)capital employed 已运用的资本(86)capital expenditure 资本支出(87)capital expenditure authorization 资本支出核准(88)capital expenditure control 资本支出控制(89)capital expenditure proposal 资本支出申请(90)capital funding planning 资本基金筹集方案(91)capital gain 资本收益(92)capital investment appraisal 资本投资评估(93)capital maintenance 资本保全(94)capital resource planning 资本资源方案(95)capital surplus 资本盈余(96)capital turnover 资本周转率(97)card 记录卡(98)cash 现金(99)cash account 现金账户(100)cash book 现金账薄(101)cash cow 金牛产品(102)cash flow 现金流量(103)cash flow budget 现金流量预算(104)cash flow statement 现金流量表(105)cash ledger 现金分类账(106)cash limit 现金限额(107)CCA 现时本钱会计(108)center 中心(109)changeover time 变更时间(110)chartered entity 特许经济个体(111)cheque 支票(112)cheque register 支票登记薄(113)classification 分类(114)clock card 工时卡(115)code 代码(116)commitment accounting 承诺确认会计(117)common cost 共同本钱(118)company limited by guarantee 有限担保责任公司(119)company limited by shares 股份(120)competitive position 竞争能力状况(121)concept 概念(122)conglomerate 跨行业企业(123)consistency concept 一致性概念(124)consolidated accounts 合并报表(125)consolidation accounting 合并会计(126)consortium 财团(127)contingency plan 应急方案(128)contingent liabilities 或有负债(129)continuous operation 连续生产(130)contra 抵消(131)contract cost 合同本钱(132)contract costing 合同本钱计算(133)contribution centre 奉献中心(134)contribution chart 奉献图(135)control 控制(136)control account 控制账户(137)control limits 控制限度(138)controllability concept 可控制概念(139)controllable cost 可控制本钱(140)conversion cost 加工本钱(141)convertible loan stock 可转换为股票的贷款(142)corporate appraisal 公司评估(143)corporate planning 公司方案(144)corporate social reporting 公司社会报告(145)cost 本钱(146)cost account 本钱账户(147)cost accounting 本钱会计(148)cost accounting manual 本钱手册(149)cost adjustment 本钱调整(150)cost allocation 本钱分配(151)cost apportionment 本钱分摊(152)cost attribution 本钱归属(153)cost audit 本钱审计(154)cost benefit analysis 本钱效益分析(155)cost center 本钱中心(156)cost driver 本钱动因(157)cost of capital 资本本钱(158)cost of goods sold 销货本钱(159)cost of non-conformance 非相符本钱(160)cost of sales 销售本钱(161)cost reduction 本钱降低(162)cost structure 本钱构造(163)cost unit 本钱单位(164)cost-volume-profit analysis(CVP) 本量利分析(165)costing 本钱计算(166)credit note 贷项通知(167)credit report 信贷报告书(168)creditor 债权人(169)creditor days ratio 应付账款天数率(170)creditors ledger 应付账款分类账(171)critical event 关键事项(172)critical path 关键路线(173)cumulative preference shares 累积优先股(174)current asset 流动资产(175)current cost accounting 现时本钱会计(176)current liabilities 流动负债(177)current purchasing power accounting 现时购置力会计(178)current ratio 流动比率(179)cut-off 截止(180)CVP 本量利分析(181)cycle time 周转时间(182)debenture 债券(183)debit note 借项通知(184)debit capacity 举债能力(185)debt ratio 债务比率(186)debtor 债务人;应收账款(187)debtor days ratio 应收账款天数率(188)debtors ledger 应收账款分类账(189)debtor' age analysis 应收账款账龄分析(190)decision driven costs 决策连动本钱(191)decision tree 决策树(192)defects 次品(193)deferred expenditure 递延支出(194)deferred shares 递延股份(195)deferred taxation 递延税款(196)delivery note 交货单(197)departmental accounts 部门报表(198)departmental budget 部门预算(199)depreciation 折旧(200)dispatch note 发运单(201)development cost 开发本钱(202)differential cost 差异本钱(203)direct cost 直接本钱(204)direct debit 直接借项(205)direct hours yield 直接小时产出率(206)direct labour cost percentage rate 直接人工本钱百分比(207)direct labour hour rate 直接人工小时率(208)directs on indirect work 间接工作事项上的工时(209)discount rate 贴现率(210)discounted cash flow 现金流量贴现(211)discretionary cost 酌量本钱(212)distribution cost 摊销本钱(213)diversions 移用(214)diverted hours 移用小时(215)diverted hours ratio 移用工时比率(216)dividend 股利(217)dividend cover 股利产出率(218)dividend per share 每股股利(219)dog 疲软产品(220)double entry accounting 复式会计(221)double-entry book-keeping 复式薄记(222)doubtful debts 可疑债务(223)down time 停工时间(224)dynamic programming 动态规划(225)earning per share 每股盈利(226)earning ratio 市盈率(227)economic order quantity(EOQ) 经济订购批量(228)efficient market hypothesis 有效市场假设(229)efficiency ration 效率性比率(230)element of cost 本钱要素(231)entity 经济个体(232)environmental audit 环境审计(233)environmental impact assessment 环境影响评价(234)EOQ 经济订购批量(235)equity 权益(236)equity method of accounting 权益法会计计算(237)equity share capital 权益股本(238)equivalent units 当量(239)event 事项(240)exceptional items 例外事项(241)expected value 期望值(242)expenditure 支出(243)expenses 费用(244)external audit 外部审计(245)external failure cost 外部损失本钱(246)extraordinary items 非常事项(247)factory goods 让售商品(248)factoring 应收帐款让售(249)fair value 公允价值(250)feedback 反应(251)FIFO 先近先出法(252)final accounts 年终报表(253)finance lease 融资租赁(254)financial accounting 财务会计(255)financial accounts calendar adjustment 财务报表的日历时间调整(256)financial management 财务管理(257)financial planning 财务方案(258)financial statement 财务报表(259)finished goods 完成品(260)fixed asset 固定资产(261)fixed overhead 固定制造费用(262)fixed asset turnover 固定资产周转率(263)fixed assets register 固定资产登记薄(264)fixed cost 固定本钱(265)flexed budget 变动限额预算(266)flexible budget 弹性预算(267)float time 浮动时间(268)floating charge 流动抵押(269)flow of funds statement 资金流量表(270)forecasting 预测(271)founder's shares 发起人股份(272)full capacity 满负荷生产能力(273)function costing 职能本钱计算(274)functional budget 职能预算(275)fund accounting 基金会计(276)fundamental accounting concept 根底会计概念(277)fungible assets 可互换资产(278)futuristic planning 远景方案(279)gap analysis 间距分析(280)gearing 举债经营比率(杠杆)(281)goal congruence 目标一致性(282)going concern concept 持续经营概念(283)goods received note 商品收讫单(284)goodwill 商誉(285)gross dividend yield 总股息产出率(286)gross margin 总边际(287)gross profit 毛利润(288)gross profit percentage 毛利润百分比(289)group 企业集团(290)group accounts 集团报表(291)high-geared 高结合杠杆(比例)(292)hire purchase 租购(293)historical cost 历史本钱(294)historical cost accounting 历史本钱会计(295)hours 小时(296)hurdle rate 最低可承受的报酬率(297)ideal standard 理想标准(298)idle capacity ration 闲置生产能力比率(299)idle time 闲置时间(300)impersonal accounts 非记名账户(301)imprest system 定额备用制度(302)income and expenditure account 收益和支出报表(303)incomplete records 不完善记录(304)incremental cost 增量本钱(305)incremental yield 增量产出率(306)indirect cost 间接本钱(307)indirect hours 间接小时(308)insolvency 无力偿付(309)intangible asset 无形资产(310)integrated accounts 综合报表(311)interdependency concept 关联性概念(312)interest cover 利息保障倍数(313)interlocking accounts 连锁报表(314)internal audit 内部审计(315)internal check 内部牵制(316)internal control system 内部控制体系(317)internal failure cost 内部损失本钱(318)internal rate of return(IRR) 内含报酬率(319)inventory 存货(320)investment 投资(321)investment center 投资中心(322)invoice register 发票登记薄(323)issued share capital 已发行股本(324)job 定单(325)job card 工作卡(326)job costing 工作本钱计算(327)job sheet 工作单(328)joint cost 联合本钱(329)joint products 联产品(330)joint stock company 股份公司(331)joint venture 合资经营(332)journal 日记账(333)just-in-time(JIT) 适时制度(334)just-in-time production 适时生产(335)just-in-time purchasing 适时购置(336)key factor 关键因素(337)labour 人工(338)labour transfer note 人工转移单(339)leaning curve 学习曲线(340)ledger 分类账户(341)length of order book 定单平均周期(342)letter of credit 信用证(343)leverage 举债经营比率(344)liabilities 负债(345)life cycle costing 寿命周期本钱计算(346)LIFO 后近先出法(347)limited liability company 有限责任公司(348)limiting factor 限制因素(349)line-item budget 明细支出预算(350)liner programming 线性规划(351)liquid assets 变现资产(352)liquidation 清算(353)liquidity ratios 易变现比率(354)loan 贷款(355)loan capital 借入资本(356)long range planning 长期方案(357)lost time record 虚耗时间记录(358)low geared 低结合杠杆(比例)(359)lower of cost or net realizable value concept 本钱或可变净价孰低概念(360)machine hour rate 机器小时率(361)machine time record 机器时间记录(362)managed cost 管理本钱(363)management accounting 管理会计(364)management accounting concept 管理会计概念(365)management accounting guides 管理会计指导方针(366)management audit 管理审计(367)management buy-out 管理性购置产权(368)management by exception 例外管理原那么(369)margin 边际(370)margin of safety ration 平安边际比率(371)margin cost 边际本钱(372)margin costing 边际本钱计算(373)mark-down 降低标价(374)mark-up 提高标价(375)market risk premium 市场分险补偿(376)market share 市场份额(377)marketing cost 营销本钱(378)matching concept 配比概念(379)materiality concept 重要性概念(380)materials requisition 领料单(381)materials returned note 退料单(382)materials transfer note 材料转移单(383)memorandum of association 公司设立细那么(384)merger 兼并(385)merger accounting 兼并会计(386)minority interest 少数股权(387)mixed cost 混合本钱(388)net assets 净资产(389)net book value 净账面价值(390)net liquid funds 净可变现资金(391)net margin 净边际(392)net present value(NPV) 净现值(393)net profit 净利润(394)net realizable value 可变现净值(395)net worth 资产净值(396)network analysis 网络分析(397)noise 干捞(398)nominal account 名义账户(399)nominal share capital 名义股本(400)nominal holding 代理持有股份(401)non-adjusting events 非调整事项(402)non-financial performance measurement 非财务业绩计量(403)non-integrated accounts 非综合报表(404)non-liner programming 非线性规划(405)non-voting shares 无表决权的股份(406)notional cost 名义本钱(407)number of days stock 存货周转天数(408)number of weeks stock 存货周转周数(409)objective classification 客体分类(410)obsolescence 陈旧(411)off balance sheet finance 资产负债表外筹资(412)offer for sale 标价出售(413)operating budget 经营预算(414)operating lease 经营租赁(415)operating statement 营业报表(416)operation time 操作时间(417)operational control 经营控制(418)operational gearing 经营杠杆(419)operating plans 经营方案(420)opportunity cost 时机本钱(421)order 定单(422)ordinary shares 普通股(423)out-of-date cheque 过期支票(424)over capitalization 过分资本化(425)overhead 制造费用(426)overhead absorption rate 制造费用分配率(427)overhead cost 制造费用(428)overtrading 超过营业资金的经营(429)paid cheque 已付支票(430)paid-up share capital 认定股本(431)parent company 母公司(432)pareto distribution 帕累托分布(433)participating preference shares 参与优先股(434)partnership 合伙(435)payable ledger 应付款项账户(436)payback 回收期(437)payments and receipts account 收入和支出报表(438)payments withheld 保存款额(439)payroll 工资单(440)payroll analysis 工资分析(441)percentage profit on turnover 利润对营业额比率(442)period cost 期间本钱(443)perpetual inventory 永续盘存(444)personal account 记名账户(445)PEPT 工程评审法(446)petty cash account 备用金账户(447)petty cash voucher 备用金凭证(448)physical inventory 实地盘存(449)planning 方案(450)planning horizon 方案时限(451)planning period 方案期间(452)policy cost 政策本钱(453)position audit 状况审计(454)post balance sheet events 资产负债表编后事项(455)practical capacity 实际生产能力(456)pre-acquisition losses 购置前损失(457)pre-acquisition profits 购置前利润(458)preference shares 优先股(459)preference creditors 优先债权人(460)preferred creditors 优先债权人(461)prepayments 预付款项(462)present value 现值(463)prevention cost 预防本钱(464)price ratio 市盈率(465)prime cost 主要本钱(466)prime entry-books of 原始分录登记薄(467)principal budget factor 主要预算因素(468)prior charge capital 优先股(469)prior year adjustments 以前年度调整(470)priority base budgeting 优先顺序体制的预算(471)private company 私人公司(472)pro-forma invoice 预开发票(473)problem child 问号产品(474)process costing 分步本钱计算(475)process time 加工时间(476)product cost 产品本钱(477)Product life cycle 产品寿命周期(478)production cost 生产本钱(479)production cost of sales 售货本钱(480)production volume ratio 生产业务量比率(481)profit center 利润中心(482)profit per employee 每员工利润(483)profit retained for the year 年度利润留存(484)profit to turnover ratio 利润对营业额比率(485)profit-volume graph 利量图(486)profitability index 盈利指数(487)programming 规划(488)project evaluation and review technique 工程评审法(489)projection 预计(490)promissory note 本票(491)prospectus 募债说明书(492)provisions for liabilities and charges 偿债和费用准备(493)prudent concept 稳健性概念(494)public company 公开公司(495)purchase order 订购单(496)purchase requisition 请购单(497)purchase ledger 采购账户(498)quality related costs 质量有关本钱(499)queuing time 排队时间(500)rate 率(501)ratio 比率(502)ration pyramid 比率金字塔(503)raw material 原材料(504)receipts and payments account 收入和支付报表(505)receivable ledger 应收款项账户(506)redeemable shares 可赎回股份(507)redemption 赎回(508)registered share capital 注册资本(509)rejects 废品(510)relevancy concept 相关性概念(511)relevant costs 相关本钱(512)relevant range 相关范围(513)reliability concept 可靠性概念(514)replacement price 重置价格(515)report 报表(516)reporting 报告(517)research cost, applied 应用性研究本钱(518)research cost, pure or basic 理论或根底研究本钱(519)reserves 留存收益(520)residual income 剩余收益(521)responsibility center 责任中心(522)retention money 保存款额(523)return on capital employed 运用资本报酬率(524)returns 退回(525)revenue 收入(526)revenue center 收入中心(527)revenue expenditure 收益支出(528)revenue investment 收入性投资(529)right issue 认股权发行(530)rolling budget 滚动预算(531)rolling forecast 滚动预测(532)sales ledger 销售分类账(533)sales order 销售定单(534)sales per employee 每员工销售额(535)scrap 废料(536)scrip issue 红股发行(537)secured creditors 有担保的债权人(538)segmental reporting 分部报告(539)selling cost 销售本钱(540)semi-fixed cost 半固定本钱(541)semi-variable cost 半变动本钱(542)sensitivity analysis 敏感性分析(543)service cost center 效劳本钱中心(544)service costing 效劳本钱计算(545)set-up time 安装时间(546)shadow prices 影子价格(547)share 股票(548)share capital 股份资本(549)share option scheme 购股权证方案(550)share premium 股票溢价(551)sight draft 即期汇票(552)single-entry book-keeping 单式薄记(553)sinking fund 偿债基金(554)slack time 松弛时间(555)social responsibility cost 社会责任本钱(556)sole trader 独资经营者(557)source and application of funds statement 资金来源和运用表(558)special order costing 特殊定单本钱计算(559)staff costs 职工本钱(560)statement of account 营业账单(561)statement of affairs 财务状况表(562)statutory body 法定实体(563)stock 存货(564)stock control 存货控制(565)stock turnover 存货周转率(566)stocktaking 盘点存货(567)stores requisition 领料申请单(568)strategic business unit 战略性经营单位(569)strategic management accounting 战略管理会计(570)strategic planning 战略方案(571)strategy 战略(572)subjective classification 主体分类(573)subscribed share capital 已认购的股本(574)subsidiary undertaking 子公司(575)sunk cost 漂浮本钱(576)supply estimate 预算估计(577)supply expenditure 预算支出(578)suspense account 暂记账户(579)SWOT analysis 长处和短处,时机和威胁分析(580)system 制度,体系(581)tactical planning 策略方案(582)tactics 策略(583)take-over 接收(584)tangible asset 有形资产(585)tangible fixed asset statement 有形固定资产表(586)target cost 目标本钱(587)terotechnology 设备综合工程学(588)throughput accounting 生产量会计(589)time 时间(590)time sheet 时间记录表(591)total assets 总资产(592)total quality management 全面质量管理(593)total stocks 存货总计(594)trade creditors 购货客户(应付账款)(595)trade debtors 销货客户(应收账款)(596)trading profit and loss account 营业损益表(597)transfer price 转让价格(598)transit time 中转时间(599)treasurership 财务长制度(600)trail balance 试算平衡表(601)turnover 营业额(602)uncalled share capital 未催缴股本(603)under capitalization 缺乏资本化(604)under or over-absorbed overhead 少吸收或多吸收的制造费用(605)uniform accounting 统一会计(606)uniform costing 统一本钱计算(607)unissued share capital 未发行股本(608)value 价值(609)value added 增值(610)value analysis 价值分析(611)value for money audit 经济效益审计(612)vote 表决(613)voucher 凭证(614)waiting time 等候时间(615)waste 废品(料)(616)wasting asset 递耗资产(617)weighted average cost of capital 资本的加权平均本钱(618)weighted average price 加权平均价格(619)with resource 有追索权(620)without recourse 无追索权(621)working capital 营运资本(622)write-down 减值(623)zero base budgeting 零基预算(624)zero coupon bond 无息债券(625)Z score 破产预测计分法。

Investment_appraisal_1

Cash flows and relevant costs

• For all methods of investment appraisal, with the exception of ROCE, only relevant cash flows should be considered. These are:

14

Accounting profits and cash flows

• In capital investment appraisal it is more appropriate to evaluate future cash flows than accounting profits, because:

– Future – Incremental – Cash-based.

Ignore:

– Sunk costs, committed costs, non-cash items, allocated costs.

17

Relevant costs

• The only cash flows that should be taken into consideration in capital investment appraisal (with the exception of ROCE) are:

13

Advantages and disadvantages of ROCE

Advantages include: • Simplicity – easily understood and easily calculated. • Expressed in percentage terms – familiar to managers and accountants. Disadvantages include: • No account is taken of project life – therefore ignores the time value of money. • No account is taken of timing of cash flows – therefore ignores the time value of money. • It varies depending on accounting policies – accounting policies will have a direct impact on profits and how much of the project costs are capitalised – therefore profits are subjective and ROCE’s may not be comparable. • It may ignore working capital. • It does not measure absolute gain (ie ROCE is calculated as a percentage). • There is no definitive investment signal – the decision of whether or not to invest still remains subjective as the ROCE is subjective.

财务报表分析-英文

Introduction and Basic Concepts

Business Partnership Vision Strategy Budget Forecast

Others Treasury M&A Risk Management Insurance Auditing Compliance Hedging ….

Introduction and Basic Concepts

Minimize Working Capital Maintain Strong Cash Flow

Pay Debts As They Are Due Increase Liquidity

Maintain Strong Financial Position

Introduction and Basic Concepts

导言及基本概念 Introduction and Basic Concepts Introduction Finance Organization Finance Activity Other topics

This training will allow you to understand: Finance Function Concept of Financial KPIs (Revenue, DM, DL, VOH, FOH, SG&A, OI, OCF, EBITDA, DOH, DSO, DPO, Incremental, etc.) BS, P&L and Cash Flow Statements Concepts of Financial Statement Evaluation and Investment Appraisal

Project Investment Feasibility Studies Project Appraisal【外文翻译】

本科毕业论文外文翻译外文文献译文标题:项目投资评估及可行性研究资料来源: 经济学家杂志作者:阿道夫摘要:工程可行性研究投资占据着举足轻重的地位和作用,在投资项目选择和可行性研究的基础上分析了可行性研究的重要作用,从而得出了对中国投资项目的可行性研究报告的一些建议。

可行性研究报告是从事一种经济活动(投资)之前,双方要从经济、技术、生产、供销直到社会各种环境、法律等各种因素进行具体调查、研究、分析,确定有利和不利的因素、项目是否可行,估计成功率大小、经济效益和社会效果程度,为决策者和主管机关审批的上报文件。

首先,投资项目的选择及可行性研究。

按照世界银行的说法,投资项目需要在一定期限内完成关于投资目标、政策、制度等复杂方面的计划。

项目是一次性的,所以它没有工作是重复的,不可以在后续操作中使其得以纠正。

错误所造成的损失在项目中是非常大的, 该项目是有风险的,但这并不意味着可以放松项目的选择,而是要在一开始就要求在选择项目时严格分析。

对于一个国家,一个公司或其他投资者来说,他们经常面临许多的投资机会,因此需要仔细选择各种各样的投资机会,只有选择合适的投资项目,以确保有限的资金将会用在关键领域,从而保证项目成功的基础上,有较高的投资的基础。

项目的选择是一个很重要的项目决策。

可行性研究在20世纪的美国开发和在田纳西河流域实施了30年的,形成了一套完整的科学研究方法,在世界各地各个领域已经广泛运用于项目决策。

要做可行性研究,我们必须先对项目的可行性研究和项目评估的关系进行认识。

可行性研究及项目评估都是分析示范性项目是否以实际工作为目的,两个都是密切相关的,有很多的共同之处,但也有其自身的特点,所以要了解两者之间的差异和相似之处。

从两者的关系来看,可行性研究及项目评估在项目开发的周期,两者都处于工程前期阶段, 是重要的准备工作。

两个项目对投资质量有着重要的影响。

可行性研究及项目评估,都是应用学科,两者的基本理论和内容基本相同,无论从经济评价指标计算的基本原理,或分析的内容都是相同的。

常见大学课程名称翻译