个人理财英文版第二章

个人理财英文版第一章

1-12

Goal-Setting Guidelines Effective Goals should be:

– Realistic – Stated

in specific, measurable

terms – Based on a time frame – Action-oriented

1-13

Assess Personal and Financial Opportunity Costs of Financial Decisions

• Opportunity cost = what you give up making a choice

Objective 3

– The trade-off of a decision

– Not always measurable in dollars; may be time – Consider lost opportunities resulting from your decisions

– /

1-7

Financial Planning in Our Economy Global Factors

• U.S economy affected by foreign investors and competition from foreign companies • Level of imports/exports affects available supply of dollars • Level of foreign investment affects domestic money supply • Money supply affects consumer interest rates

个人理财英文版第二章

• Insolvency:

N–eIntabWilityotrotphay debts when due – Liabilities far exceed assets

2-14

Sample Balance Sheet

2-15

Ways to Increase Net Worth

Documents re: purchase and sale of real estate Copies of tax returns and supporting data

Indefinitely

As long as you own them Indefinitely

7 years minimum 10 years better

RATIO

Calculation

Interpretation

Debt Ratio

Liabilities divided by net worth

Low debt is best

Curent Ratio Liquidity Ratio

Liquid assets divided by current liabilties

Money Management Troubles & Debt

Getting out of debt:

2-5

An Organized Personal Financial Records System

Provides a basis for:

• Handling daily business affairs, such as bill paying • Planning and measuring financial

英语听力材料:个人理财

★⽆忧考英语听⼒频道为⼤家整理的英语听⼒材料:个⼈理财。

更多阅读请查看本站频道。

第⼀部分新鲜⽣活Unit10 Personal Finance 个⼈理财A silvedess mon goes fast ihrough the market.⾝上⽆钱,市场疾⾏Dialouge 2A:You look at bit dull today. What's up?A:你今天看起来不那么⾼兴,怎么了?B:Well, my mum lost her job yesterday.B:嗯,我妈昨天把⼯作给丢了。

A:I'm sorry to hear that. Well,l heard that registered urban unem-ployment rate reached 4 percent this year,with more than half be-ing women.A:真抱歉,我该问的。

嗯,我听说今年城镇居民的失业率达到4%,⽽其中⼀半以上都是⼥的。

B:The supply outstrips the demand in the job market and women are in a disadvantageous position as a whole.B:⼈才市场供⼤于求,⼥性总的来说还是处于劣势。

A:Yeah,it's true. What is she going to do?A:确实是那样。

有什么办法吗?B:Well,she is thinking of doing some household cleaning or baby-sitting in the community.B:嗯,我妈打算去⼩区⾥给⼈打扫卫⽣或看孩⼦什么的。

A:That's not bad. It could be a short-term altemative. Your mum can look for another one when the market improves. Things will work out eventually.A:那也不错。

公司理财精要9版-英文-第二章课件

significant loss of value. • Liquid firms are less likely to experience financial distress • But liquid assets typically earn a lower return • Trade-off to find balance between liquid and illiquid assets

$ 400 $ 600 LTD

$ 500 $ 500

700 1,000 SE

600 1,100

1,100 1,600

1,100 1,600

公司理财精要9版-英文-第二章

2-11

Income Statement

• If the balance sheet is like a snapshot, the income statement is like a video recording of what the people did between two snapshot.

公司理财精要9版-英文-第二章

2-3

2.1 The Balance Sheet

• An accountant’s snapshot of the firm。 • It is a convenient means of organization and

summarizing what a fir m owns(its assets), what a firm owes(its liabilities), and the difference between the two(the firm’s equity) at a given point in time. • Assets are listed in order of decreasing liquidity • Balance Sheet Identity(特性)

个人理财英文作文答案

个人理财英文作文答案下载温馨提示:该文档是我店铺精心编制而成,希望大家下载以后,能够帮助大家解决实际的问题。

文档下载后可定制随意修改,请根据实际需要进行相应的调整和使用,谢谢!并且,本店铺为大家提供各种各样类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,如想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by theeditor. I hope that after you download them,they can help yousolve practical problems. The document can be customized andmodified after downloading,please adjust and use it according toactual needs, thank you!In addition, our shop provides you with various types ofpractical materials,such as educational essays, diaryappreciation,sentence excerpts,ancient poems,classic articles,topic composition,work summary,word parsing,copyexcerpts,other materials and so on,want to know different data formats andwriting methods,please pay attention!I need to save some money. For example, I can cut down on eating out and shopping.It's important to have a budget. That way I know where my money is going.Investing can be a good idea. But I have to learn more about it first.Sometimes I think about buying a lottery ticket. Maybe I'll get lucky.Credit cards can be handy, but I have to be careful not to overspend.I should review my financial situation regularly. See if I'm on the right track.。

个人理财英文版第二章

Benefits

1. Recap your current financial position in relation to the value of items you own and amounts you owe

2-11

Balance Sheet

A financial statement that reports what an individual or family owns and owes as of a specific date:

• ቤተ መጻሕፍቲ ባይዱlso called:

–Net worth statement –Statement of financial position

4. Connect money management activities with saving for personal financial goals

2-2

Objective 1

Identify the Main Components of Wise Money Management

• Money management = day-to-day financial activities necessary to manage current personal economic resources, while working toward long-term financial security

How much of earnings goes to sevice debt; less than 20% recommended

个人理财英文作文

个人理财英文作文英文回答:Personal Finance: A Comprehensive Guide to Mastering Your Money。

As Benjamin Franklin famously said, "A penny saved is a penny earned." Managing personal finances effectively is a crucial aspect of financial independence and overall well-being. It involves understanding your income, expenses, savings, investments, and financial goals. By embracing responsible financial habits, you can take control of your financial destiny and achieve your aspirations.Step 1: Track Your Income and Expenses。

The foundation of personal finance is understandingyour cash flow. You can use a budgeting app, spreadsheet,or simply a notebook to track every dollar that comes inand goes out. Categorize your expenses (e.g., housing, food,transportation) to identify areas where you can cut back.Step 2: Create a Budget。

个人理财英语

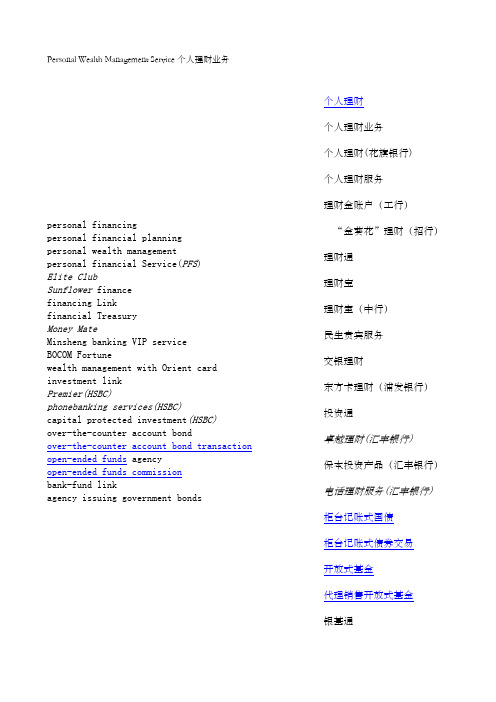

Personal Wealth Management Service个人理财业务personal financingpersonal financial planningpersonal wealth managementpersonal financial Service(PFS)Elite ClubSunflower financefinancing Linkfinancial TreasuryMoney MateMinsheng banking VIP serviceBOCOM Fortunewealth management with Orient card investment linkPremier(HSBC)phonebanking services(HSBC)capital protected investment(HSBC)over-the-counter account bondover-the-counter account bond transaction open-ended funds agencyopen-ended funds commissionbank-fund linkagency issuing government bonds 个人理财个人理财业务个人理财(花旗银行)个人理财服务理财金账户(工行)“金葵花”理财(招行)理财通理财宝理财室(中行)民生贵宾服务交银理财东方卡理财(浦发银行)投资通卓越理财(汇丰银行)保本投资产品(汇丰银行)电话理财服务(汇丰银行)柜台记账式国债柜台记账式债券交易开放式基金代理销售开放式基金银基通代理发行国债visible treasury certificateBearer treasury certificateindividual Credit Servicesafekeeping agencycustodial box servicesafe deposit box serviceassets managementaround-clock service of account management network settlementbank-securities linkbank-securities account transferMoney Linkaccount transfer via money linkbank-insurance link(bonus participated insurance) open-ended fundsbank-fund linkopen-ended funds commission 凭证式国债无记名式国债个人资信服务代理保管业务保管箱服务保管箱业务资产管理24小时到账处理业务网络结算业务银证通银证转账银证通(浦发银行)银证转账(浦发银行)银保通(分红保险)开放式基金银基通代理销售开放式基金capital accountdeposit(Margin) accountcounter Transfertelephone Banking self-service transfer service a letter of entrustment for transferentrusting transfer and deduction shareholders’ magnetic cardnetwork settlementdomestic payment settlement service 资金账户保证金账户柜台转账电话银行自助转账old-age pension fund social security fund bond fundinvestment fund close-ended fund open-ended fund 转账委托书委托转账代缴费股东磁卡网络结算业务国内支付结算业务养老基金社会保险基金债券基金投资基金封闭式基金开放式基金Savings Deposit储蓄存款业务savings depositdemand deposit(current deposit)current deposit passbookcurrent checkbook deposittime or demand optional depositcall deposittime deposit(term deposit)large sum fixed depositgeneral fixed depositfloating time rate depositlump-sum deposit and withdrawaltime deposit of lump-sum deposit and withdrawaltime deposits of lump-sum depositing and lump-sum withdrawalinstallment fixed depositstime deposit of small savings for lump-sum withdrawal interest withdrawal for a principal depositedpeincipal-receiving and interest withdrawing time deposit time saving big money and small drawingsavings / time optional deposits 活期储蓄存款活期储蓄存款活期存折活期支票定活两便存款通知存款定期存款大额定期存款普通定期存款定期浮息选择存款整存整取整存整取定期储蓄整存整取定期存款零存整取零存整取定期储蓄存本取息存本取息定期储蓄整存零取定期储蓄定活两便存款seven-day notice depositpersonal settlement accounts avings account(HSBC)f ixed deposit account(HSBC)renminbi account(HSBC)children account(HSBC)statement savings account(HSBC)interest bearing savings account(HSBC)interest bearing chequeing account(HSBC) advance withdrawal and loss-reporting business deposits by correspondencedeposit collections in different places personal checksdeposit certificate loss reportingloss reporting for personal checkssavings certificatepersonal call depositinterbank deposit and withdrawaleducation deposit 七天通知存款个人结算账户储蓄账户(汇丰银行)定期存款账户(汇丰银行)人民币账户(汇丰银行)儿童账户(汇丰银行)结单储蓄账户(汇丰银行)生息储蓄账户(汇丰银行)生息支票账户(汇丰银行)提前支取与挂失业务通信存款储蓄存款异地托收个人支票储蓄存款挂失个人支票挂失定期存单个人通知存款通存通兑教育储蓄存款procedures of loss reporting deposit certificate loss reporting interim loss reportingcurrent All-In-One passbookfixed All-In-One passbookmultiple function debit card Deposit Plus(HSBC)挂失业务存单挂失临时挂失活期一本通定期一本通多功能借记卡双利存款(汇丰银行)Personal Consumer Credit个人消费信贷housing mortgage loanindividual business house loan house refurbishing loan. individual housing loanshousing loans on own account housing loans on authorization individual combined housing loans CITIC Happy Family 住房抵押贷款个人商业用房贷款房屋装修贷款个人住房贷款auto loansloan for refurbishing houseconsumer durables loanpersonal loan secured by CDs/treasury bonds individual consumption loanpetty consumer creditindividual unsecured loanconsumption credit for individual clients individual consumption loansecured loansmall amount private loans 自营性住房贷款委托住房贷款个人住房组合贷款中信家家乐汽车消费贷款家居装修贷款大额耐用消费品贷款个人存单质押贷款个人消费信贷小额信用消费贷款个人信用贷款个人消费信贷业务个人消费信贷抵押放款(担保放款) 小额贷款individual auto loanindividual comprehensive consumer loanindividual large-denomination durable commodities loan personal pledge loantravel and vacation loansonline personal pledge loaninsurance certificate pledge loandeposit certificate pledge loancertificates of deposit(CDs)individual comprehensive consumer loanindividual large-denomination durable commodities loan state educational loancommercial educational loanoverseas study loaneducational loans 个人汽车消费贷款个人综合消费贷款个人大额耐用消费品贷款个人质押贷款旅游度假贷款网上个人质押贷款保单质押贷款存单质押贷款大额存单个人综合消费贷款个人大额耐用消费品贷款国家助学贷款商业助学贷款留学贷款教育助学贷款Foreign Exchange for Corporate公司外汇业务forex deposit for enterprisecurrent forex deposit for enterprisetime foreign fxchange deposit for enterprise call forex deposit for enterpriseforex creditforex working capital loanforex temporary loansforex short-term loansforex medium-term loansforex revolving loansforex loans with repayment in Installments forex fixed asset loanforex fixed asset investmentforex business development and expansion forex technical innovationforex fixed asset acquisition 单位外汇存款业务活期对公外汇存款定期对公外汇存款通知对公外汇存款外汇贷款业务外汇流动资金贷款外汇临时流动资金贷款外汇短期流动资金贷款外汇中期流动资金贷款外汇流动资金循环贷款外汇整贷零偿外汇固定资产贷款外汇固定资产投资贷款外汇开发扩建贷款外汇技改贷款外汇固定资产收购贷款International Finance国际融资业务forex merger&acquisition loanproject financeBOT(build, operate, transfer)BT(build, transfer)export buyer’s creditsyndicated loanon-lending project financeinternational commercial loanimport buyer’s creditforeign government loanforeign government mixed loanloan from international financial organizations forex transferred loanf inancing business of featuresbills discountcredit linew orldwide creditexport seller's creditfinance leasepurchase of the accounts receivableexternal labor service contract loan 外汇兼并收购贷款项目融资建设经营转让建设转让出口买方信贷银团贷款外汇转贷款项目融资国际商业贷款融资进口买方信贷融资外国政府贷款融资外国政府混合贷款融资国际金融组织贷款融资外汇转贷款特色融资业务票据贴现授信额度统一大授信出口卖方信贷融资租赁应收账款收购对外劳务承包贷款distribution passportstart-up winneri nternational financing and guarantee business trust servicesinternational debt offeringforeign exchange guaranteeguarantee for loantender guaranteeperformance bondadvanced payment guaranteepayment guaranteeverification payment guaranteetechnical verification payment guarantee deferred payment guaranteelease guaranteeimport bills for collectionexport bills for collectionpurchasing collection bills 一路通创业宝国际融资及担保信托业务境外发债融资外汇担保业务借款担保投标担保履约担保预付款退款担保付款担保验货付款保函技术交易验收付款保函延期付款担保租赁担保进口代收出口托收出口托收买单packing loan under L/Ctransferable L/Cnegotiating export bills打包放款(信用证项下)discounting billssecured ladingopening letter of guaranteeforeign exchange payment and clearing service settlement clearance for foreign exchange pusiness banking facilityforeign exchange rate risks coverguarantee and attestationinter-bank foreign currency borrowings and lendings asset portfolio managementoffshore banking businesstrade financinggeneral banking facilitiesPacking Creditimport bills purchaseexport(0utward) bill purchaseforeign currency bill discountforeign exchange bills purchasebills discountingForfaitingFactoringnon-trade finance 转让信用证议付出口信用证单据(银行承兑)汇票贴现担保提货开立保函外汇清算业务外汇业务清算授信外汇保值避险担保和见证金融机构间外汇拆借理财策划离岸金融业务贸易融资综合授信打包放款进口押汇出口押汇外币票据贴现买入外币票据票据贴现福费廷(包买票据)保理业务非贸易融资Bank Card银行卡业务peony credit cardpeony international card peony MoneyLink cardpeony IC(Smart) cardpeony proprietary cardpeony photo cardpeony co-branding cardLong cardsavings carddebit cardanimal cardaccount transfer cardpre-paid consumption card special-purpose cardco-branded cardGreat Wall credit cardGreat Wall international card Great Wall credit card in RMB pacific cardgold cardordinary cardThe World’s Sunflower development cardMinsheng cardOrient cardLady cardVisa cardMaster cardDiner’s cardAmerican Express cardMillion cardJCB cardFederal card 牡丹信用卡牡丹国际卡牡丹灵通卡牡丹智能卡牡丹专用卡牡丹彩照卡牡丹联名卡龙卡储蓄卡借记卡生肖卡转账卡储值卡专用卡联名卡(认同卡)长城信用卡长城国际卡长城人民币信用卡太平洋卡金卡普通卡金葵花卡发展卡民生卡东方卡真情卡(广发银行)维萨卡万事达卡大莱卡运通卡百万卡(日本)JCB卡(日本)发达卡(香港)Terms of Post and Title岗位职务词汇board of directorschairman of the boardchair of board of directors chief executive officer directormanaging directorauthorized officermanager and head of China desk general manager(GM)director generalchief controllerdeputy general manager(DGM) chief executive officer(CEO) chief financial officer(CFO) chief market officer(CMO)top manager 董事会,理事会董事长董事长董事长董事总裁,常务董事代理行长中国事务部经理兼主管managerfinance director financial manager chief accountant chief cashierchief clerkhead clerkhead of department head tellerchief accountant chief of finance sales director sales manager directing staff top management middle management lower management 总经理总监总稽核副总经理首席执行官首席财务总监首席市场总监总经理经理,主任财务经理,财务处(科)长财务经理会计主任,总会计师,财务处长出纳主任主任办事员首席办事员部门主任出纳主任总会计,会计主任财务主任营业副经理;销售处(科)长销售经理领导人员最高管理层基层管理manager of bank managerial staffofficer, official financial adviser financial accountant financial administrator financial executive auditing officers controlleraccountant in charge accountantconsultantmanagement consultant managing agentassistant accountant assistant general manager assistant manager managing partner administrative staff office staffoperation staff accounting clerkbank clerkoffice clerkstatistical clerkpay clerkstaffclerkcashiertellercustomerclient 银行经理人管理人员高级职员财务顾问财务会计员财务主管人财务主管审计人员主管会计;审计员主管会计师会计师,会计员顾问业务顾问经理人的代理助理会计师协理,副总经理,副总裁副理,协理办事员管理人员,行政人员办公室职员簿记员银行职员办事员统计员出纳员职员办事员出纳员出纳员顾客,客户顾客,客户Intermediary Business(1)中间业务remittance servicesdomestic remittanceremittance agencyremittance expresscommom remittanceurgent remittanceremittance by draftcash remittancebank promissory note(bank check) checkcheck Bookagency servicesfund agency serviceBank-fund LinkBank-futures LinkFortuneLink 汇兑业务国内汇兑代理汇兑汇款直通车普通汇款加急汇款票汇(汇票汇款) 汇款银行本票支票支票簿代理业务基金代理业务银基通银期通财富通bond agency servicebonds settlement agencyinsurance agency servicefinancing agencysafekeeping agencycollection and payment agencysettlement agencysalary payment agency(payroll agency service) wages(old-aged pension) distribution agency public utility fee levying agencyissuing government bonds agencycommission collection of telephone fee commission collection of telephone fee for Unicom commission collection of electricity charge commission collection of insurance premium payment through telephone bankingpayment through mobile phone bankingnetwork payment settlement agencyagency collection and paymentcommission payment on consignmentpayment in cashcharge withholding service 债券代理业务债券结算代理保险代理业务代理理财代理保管代理收付代理结算代发工资(业务)代发工资(养老金)业务代理公用事业收费代理发行国债代收电话费业务代收联通话费业务代收电费业务代收保险费电话银行缴费手机银行缴费代收付业务网上支付结算代理委托缴费现金缴费缴费业务fee collection expresscommission security business agency securities fund clearing commission tax withholding commission insuranceagency signing of the banker’s bill forward settlement 缴费通代理证券业务代理证券资金清算代理税收业务代理保险业务代签银行汇票期货结算业务client service centercustomer service hotlinebearer treasury certificatevisible treasury certificatebearer treasury certificate with fixed denominationproof of payment(payment vouchers)a letter of entrustment for transfer agency collection and paymentagency collection and deductionpublic utility Feeentrusting transfer and deduction agency issuing government bondsforeign exchange trading agency automated transferdeposit(margin) account 客户服务中心客户服务热线无记名式国债凭证式国债固定面额无记名式国债支付凭证转账委托书代收代缴费公用事业费委托转账代交费代理发行国债代理外币买卖自动转账保证金账户bill consultancyreal-time funds transferringcounter transfersettlement businessdomestic settlement servicedraft for collectioncollection and acceptioncommission receptionon-line Settlementon-line Shoppingsecurities and capital settlement agency commission collection and payment agency client bar code automatic inquiry system payment and settlement agencyforward settlement 票据查询实时资金汇划柜台转账结算业务国内结算业务托收汇票托收承付委托收款网上结算网上购物代理证券资金清算代理收付业务客户条形码自动查询支付结算业务代理期货结算业务notes clearingcharged bond trading on the counter treasury billstreasury bondsbook-entry treasury billvisible treasury certificate investment bankingmerchant bankingconsultancy-specific financial service funds trusteeshipcash-based settlementpaper-based settlementelectronic-based settlement transferring settlementaccounting settlement business 柜台记账式债券交易国库券长期国债凭证式国债凭证式国债投资银行业务商人银行业务咨询性金融业务基金托管现金清算票据清算电子清算转账结算会计结算业务。

个人理财英文版第一章

• Increased control of your financial affairs

• Improved personal relationships • Sense of freedom from financial

– Marital status, household size, employment

– Exhibit 1-1 (page 5)

• Major events:

– Graduation, marriage, divorce – Birth or adoption of child – Career or health changes

1. Identify social and economic influences on personal financial goals and decisions

2. Develop personal financial goals 3. Assess personal and financial

opportunity costs associated with financial decisions 4. Implement a plan for these decisions

1-2

Financial Planning

• Process of managing your money to achieve personal economic satisfaction

– Business, labor & government

公司理财罗斯英文原书第九版第二章

Financial Statements and Cash Flow

McGraw-Hill/Irwin

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

Key Concepts and Skills

Usually a separate section reports the amount of taxes levied on income.

$86 $43 $43

2-13

U.S.C.C. Income Statement

Total operating revenues Cost of goods sold Selling, general, and administrative expenses Depreciation Operating income Other income Eห้องสมุดไป่ตู้rnings before interest and taxes Interest expense Pretax income Taxes Current: $71 Deferred: $13 Net income Retained earnings: Dividends: $2,262 1,655 327 90 $190 29 $219 49 $170 84

Deferred taxes Long-term debt Total long-term liabilities $117 471 $588 $104 458 $562

Total assets

$1,879

$1,742

Stockholder's equity: Preferred stock $39 $39 Common stock ($1 par value) 55 32 Capital surplus 347 327 Accumulated retained earnings 390 347 Less treasury stock (26) (20) Total equity $805 $725 Total liabilities and stockholder's equity $1,879 $1,742

个人理财英文

An Organized Personal Financial Records System

Provides a basis for:

• Handling daily business affairs, such as bill paying

• Planning and measuring financial progress

4. Connect money management activities with saving for personal financial goals

2-2

Objective 1

Identify the Main Components of Wise Money Management

• Money management = day-to-day financial activities necessary to manage current personal economic resources, while working toward long-term financial security

• Daily spending and saving decisions = central to financial planning

– Must be coordinated with needs, goals, and personal situations

2-3

Components of Money Management

account numbers – Citizenship and military papers – Adoption and custody papers – Serial numbers and photos of valuables – CDs and credit and banking account numbers – Mortgage papers and titles – List of insurance policy numbers – Stock and bond certificates – Coins and other collectibles – Copy of will

how to become wealthy英语作文

如何变得富有英语作文1英文作文:Becoming rich is a goal that many people aspire to. But how can we achieve it? Well, hard work is definitely the key. Let me tell you about my friend Tom. He is an ordinary office worker. At first, he was just like everyone else, doing his daily tasks and not thinking much about the future. But one day, he realized that he wanted more out of life. So, he decided to work hard and improve himself. He started taking online courses in his spare time to learn new skills. He would stay late at the office to finish his tasks perfectly. He even volunteered for extra projects. His efforts didn't go unnoticed. Gradually, his boss began to notice his dedication and hard work. One day, a big project came up. Tom took the initiative and worked overtime for weeks to make sure everything was done perfectly. In the end, the project was a huge success. And as a result, Tom got a promotion and a significant pay raise. Another example is my neighbor, Lisa. She had a great idea for a business. She didn't let fear hold her back. Instead, she took a risk and started her own company. It was not easy at first. She faced many challenges and setbacks. But she never gave up. She kept working hard, coming up with innovative ideas and improving her products. Slowly but surely, her business started to grow. Now, she is very successful and wealthy. In conclusion, becoming rich is not something that happens overnight. It takes hard work, determination, and a willingness to take risks. We can all learn from people like Tom and Lisa. If we are willing to put in the effort, we too can achieve our dreams of becoming rich.中文翻译:变得富有是许多人渴望实现的目标。

公司理财英文版第二章

US Corporation Income Statement – Table 2.2

Insert new Table 2.2 here (US Corp Income Statement)

2-19

Hale Waihona Puke Income Statement Analysis

• There are three things to keep in mind when analyzing an income statement:

2-13

• Which one of the following is included in a firm's market value but yet is excluded from the firm's accounting value? A. real estate investment B. good reputation of the company C. equipment owned by the firm D. money due from a customer E. an item held by the firm for future sale

• Which one of the following accounts is the most liquid? A. inventory B. building C. accounts receivable D. equipment E. land

• Which one of the following represents the most liquid asset? A. $100 account receivable that is discounted and collected for $96 today B. $100 of inventory which is sold today on credit for $103 C. $100 of inventory which is discounted and sold for $97 cash today D. $100 of inventory that is sold today for $100 cash E. $100 accounts receivable that will be collected in full next week

个人理财英文版第一章汇编

• The Federal Reserve

– “.. Sets the nation’s monetary policy to promote the objectives of maximum employment, stable prices and moderate long-term interest rates.”

• “Compounding”

1-19

Future Value

Example

Future Value Original Amount in Savings

=

+

Interest Earned

$100 deposited for 1 year at 6% per year Future Value = $100 + ($100 X .06 X 1) Future Value = $100 + $6 = $106

1-12

Goal-Setting Guidelines Effective Goals should be:

– Realistic – Stated

in specific, measurable

terms – Based on a time frame – Action-oriented

1-13

Objective 3

1-9

Financial Planning in Our Economy Interest Rates Interest Rate = the cost of money – Affected by supply and demand – Risk premium:

公司理财原版英文课件Chap020

There are two methods for selecting an underwriter

Competitive Negotiated

20-9

Firm Commitment Underwriting

The issuing firm sells the entire issue to the underwriting syndicate. The syndicate then resells the issue to the public. The underwriter makes money on the spread between the price paid to the issuer and the price received from investors when the stock is sold. The syndicate bears the risk of not being able to sell the entire issue for more than the cost. This is the most common type of underwriting in the United States.

关于理财的一个人自我介绍一句话

关于理财的一个人自我介绍一句话英文回答:Hi there! My name is John and I am passionate about personal finance and investment. I believe that financial planning is essential for achieving long-term financial goals and securing a comfortable future. With my expertise in financial management and investment strategies, I can help individuals and families make informed decisions to grow their wealth and protect their assets.One of the key aspects of my approach to financial planning is diversification. As the saying goes, "Don't put all your eggs in one basket." I firmly believe in spreading investments across different asset classes and industries to minimize risk and maximize returns. By diversifying, one can potentially benefit from the growth of various sectors and mitigate the impact of any downturns in a particular market.For example, let's say an individual has a substantial amount of savings and decides to invest it all in the stock market. While the stock market may offer great returns, it is also subject to volatility and downturns. If the market experiences a significant drop, this person's entire investment could be at risk. However, by diversifying their portfolio and allocating a portion of their savings to other investment options such as bonds, real estate, or mutual funds, they can reduce the impact of any single investment's poor performance.Another important principle I follow is the power of compounding. As the famous investor Warren Buffett once said, "My wealth has come from a combination of living in America, some lucky genes, and compound interest." Compounding allows investments to grow exponentially over time, as the returns generated are reinvested to generate even more returns. By starting early and consistently contributing to investments, individuals can take advantage of compounding to build substantial wealth over the long term.To illustrate this, let's consider two individuals, Alex and Ben. Alex starts investing $1,000 per month at the age of 25 and continues until retirement at 65, earning an average annual return of 8%. Ben, on the other hand, waits until the age of 35 to start investing and contributes $2,000 per month until retirement at 65, also earning an average annual return of 8%. Despite contributing more money each month, Ben ends up with a smaller retirement fund compared to Alex due to the power of compounding. This example highlights the importance of starting early and harnessing the power of time in investment growth.中文回答:大家好!我叫John,对个人理财和投资充满热情。

公司理财(罗斯)第2章(英文)

2-2

Sources of Information

Annual reports Wall Street Journal Internet

2.1 The Balance Sheet 2.2 The Income Statement 2.3 Net Working Capital 2.4 Financial Cash Flow 2.5 The Statement of Cash Flows 2.6 Financial Statement Analysis 2.7 Summary and Conclusions

McGraw-Hill/Irwin Corporate Finance, 7/e 2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

2-6

Debt versus Equity

Generally, when a firm borrows it gives the bondholders first claim on the firm’s cash flow. Thus shareholder’s equity is the residual difference between assets and liabilities.

Total assets

McGraw-Hill/Irwin Corporate Finance, 7/e

$1,879

$1,742

2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

如何更好的理财英文作文

如何更好的理财英文作文英文回答:How to Improve Your Financial Management.Improving your financial management is crucial for securing your financial future and achieving your financial goals. Here are some effective strategies:1. Create a Budget and Track Your Expenses:Establish a detailed budget that outlines your income and expenses. Regularly track your spending to identify areas where you can reduce expenses or allocate funds more efficiently.2. Set Financial Goals:Define specific financial goals, both short-term (e.g., saving for a down payment) and long-term (e.g., retirement).Setting goals provides motivation and keeps you focused on your financial journey.3. Reduce Unnecessary Expenses:Analyze your expenses and eliminate unnecessary spending on non-essential items. Consider cutting back on dining out, entertainment, or impulse purchases.4. Increase Your Income:Explore ways to earn additional income through a side hustle, part-time job, or investing. Increasing your income can accelerate your financial progress.5. Save and Invest Regularly:Make saving and investing a priority. Set up automatic transfers from your checking to your savings or investment accounts. Diversify your investments to minimize risk.6. Seek Professional Advice:If managing your finances feels overwhelming, consider consulting a financial advisor. They can provide personalized guidance and help you develop a comprehensive financial plan.7. Educate Yourself:Continuously educate yourself about personal finance. Read books, attend workshops, or consult reputable online resources to enhance your financial literacy.8. Use Technology:Utilize budgeting apps, investment platforms, and other financial tools to simplify your financial management. These tools can help you stay organized and make informed decisions.9. Practice Financial Discipline:Develop financial discipline by sticking to your budget,avoiding impulse spending, and making responsible decisions about your money.10. Review and Adjust Regularly:Your financial situation and goals may change over time. Regularly review your budget, financial goals, and investments, and adjust your strategies as needed.中文回答:如何提高你的理财能力。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2-16

Evaluating Financial Progress Ratios

RATIO Debt Ratio Curent Ratio Calculation Interpretation Liabilities divided by Low debt is best net worth Liquid assets divided High is desirable by current liabilties Number of months Liquid assets divided expenses canbe paid in by monthly expenses an emergency; high is desirable

2-6

Records in Your Home File

• Items you refer to often

– – – – – – – – – – Personal and employment records Money management records Tax records Financial services records Credit records Consumer purchase and auto records Housing records Insurance records Investment records Estate planning and retirement records

Total cash received during the time period

-

Cash outlays during the time period

=

Cash surplus or deficit

2-18

The Cash Flow Statement

Inflows and Outflows

2-7

What to Keep in a Safe Deposit Box

• Records and items that would be hard to replace:

– Birth, marriage and death certificates – List of checking, savings and financial institution account numbers – Citizenship and military papers – Adoption and custody papers – Serial numbers and photos of valuables – CDs and credit and banking account numbers – Mortgage papers and titles – List of insurance policy numbers – Stock and bond certificates – Coins and other collectibles – Copy of will

Items of Value (what you own)

-

Amounts owed (what you owe)

=

Net Worth (your wealth)

2-12

Components of a Balance Sheet

• Step 1 – List items of value

Liquid assets – Real estate – Personal possessions – Investment assets • Step 2 – Determine amounts owed – Current liabilities (< 1 year) – Long term liabilities • Step 3 - Compute your net worth.

2-17

The Cash Flow Statement

Inflows and Outflows

• •

Cash flow statement = personal income and expenditure statement Summary of cash receipts and payments for a given period

2-11

Balance Sheet

A financial statement that reports what an individual or family owns and owes as of a specific date: • Also called: – Net worth statement – Statement of financial position

Liquidity Ratio

Monthly credit How much of earnings Debt-payments payments divided by goes to sevice debt; less Ratio take-home pay than 20% recommended Savings Ratio Monthly savings divided by gross income 5-10% recommended

2-8

Records on Your Personal Computer*

•

•

• •

•

Current and past budgets Summary of checks written and other banking transactions Past income tax returns prepared with tax preparation software Account summaries and investment performance results Computerized versions of wills, estate plans, and other documents

Chapter 2

Money Management Skills

McGraw-Hill/Irwin

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Money Management Skills

Chapter Objectives 1. Identify the main components of wise money management 2. Create a personal balance sheet and cash flow statement 3. Develop and implement a personal budget 4. Connect money management activities with saving for personal financial goals

2-5

An Organized Personal Financial Records System

Provides a basis for:

• Handling daily business affairs, such as

• • •

•

bill paying Planning and measuring financial progress Completing required tax reports Making effective investment decisions Determining available resources for current and future buying

Step 1 - Record Income

– Net income from employment (Net Pay) – Savings and investment income – Other sources

Step 2 - Record cash outflows

– Fixed and variable expenses

2-2ቤተ መጻሕፍቲ ባይዱ

Objective 1

Identify the Main Components of Wise Money Management

• Money management = day-to-day financial activities necessary to manage current personal economic resources, while working toward long-term financial security • Daily spending and saving decisions = central to financial planning

2-13

–

Net Worth

• •

•

•

Assets - Liabilities = Net Worth Measurement of current financial position Net worth ≠ cash available Insolvency:

–

Inability to pay debts when due – Liabilities far exceed assets

2-10

Create a Personal Balance Sheet and Cash Flow Statement

Objective 2

Benefits

1. Recap your current financial position in

relation to the value of items you own and amounts you owe 2. Measure progress toward financial goals 3. Maintain information on financial activities 4. Provide information for preparing tax forms or applying for credit