个人理财外文翻译文献翻译

推动个人理财的应用研究【外文翻译】

外文翻译原文Promoting Applied Research in Personal FinanceMaterial Source:Handbook of Consumer Finance ResearchAuthor: Sharon A.BurnsThe purpose of this chapter is to briefly summarize the role that a national professional association plays in bringing quality research to professional financial counselors and educators.This chapter also includes a brief,non-exhaustive review of personal finance research.A research agenda from the perspective of financial counselors and educators is proffered.Most national associations exist to assemble like-minded professionals who serve a similar population or provide the same or similar products or services in various geographic markets.Four national associations serve personal finance practitioners:the Association for Financial Counseling and Planning Education (AFCPE),the Financial Planning Association(FPA),the National Association of Personal Financial Advisors(NAPFA)and the CFP Board of Standards.The first three serve as professional associations for the purpose of enhancing the capacity of individual professionals to be successful.The purpose of the CFP Board of Standards is to develop and maintain the standards of the Certified Financial Planner designation.In the field of financial counseling,AFCPE serves the role of certifying body as well.Other associations either serve professionals in smaller geographic markets,or personal finance is one of several components or topics addressed by the membership.Four associations are comprised primarily of researchers and academicians.These include the Financial Services Academy(FSA),American Council on Consumer Interests(ACCI),the Eastern Family Economics and Resource Management Association(EFERMA) and its sister organization,Western Family Economics Association(WFEA).Members of the FSA research financial services and personal finance topics.ACCI members primarily study consumer behavior and economic issues with some focus on personal finance topics.The latter two groupsfocus heavily on personal finance topics,and participants are primarily graduate students and university faculty.Many associations serve to address,in whole or in part,personal finance by enhancing the capacity of their members to provide counsel and advice to individuals and families,or research personal finance decisions.The Association for Financial Counseling and Planning Education(AFCPE)is unique because its membership rolls include both university academicians and researchers,educators and counselors,all of whom focus on improving the financial well-being of individuals and families.History of the Association for Financial Counseling andPlanning EducationIn early 1983,Tahira Hira and Jerry Mason,two faculty members from leading universities,discussed the need for an organization that “promoted the interests and supported the needs of financial counselors”.The faculty members’professional work focused on these issues and their instructional efforts aimed to prepare students to serve consumers as financial and credit counselors.In the autumn of 1983,over 60 invited participants attended a conference in Provo,Utah,focusing on financial counseling.The conference agenda included discussions exploring the possibility of forming a new association of university faculty and cooperative extension educators.Additional talks centered on providing university students with curricula appropriate to serving as professional financial counselors.Out of this meeting,and during a subsequent conference in 1984,the Association for Financial Counseling and Planning Education was born.It was not long before association leaders realized that the work of their members had more value in the larger context of increasing the financial well-being of consumers.This motivated association leaders to develop networks with professionals in a variety of occupations who helped individuals and families develop sound financial management practices.Members of the credit counseling industry and those counseling military members were specifically interested in the association because the synergy among academicians,researchers and practitioners could result in providing more successful programming and counseling to their clients.During the early 1990s,association leaders identified the need to certify professionals who were providing one-to-one financial counseling or group financial education.Such a certification would(1)develop a corps of professionals to assistindividuals and families with personal financial issues,(2)enhance and develop best practices,(3)encourage consistency across the range of financial counseling services and(4)signal to the public that an individual financial counseling professional met independently developed standards.A committee of academic researchers,university-based faculty,cooperative extension educators and credit counseling industry leaders convened to develop industry standards,curriculum and examination requirements.The work of researchers and academicians was particularly helpful in identifying the greatest personal financial obstacles and risks consumers faced and best practices in delivering educational programming and counseling to the individual client.AFCPE’s mission includes building the capacity of its practicing(counseling and educator)members to serve their clientele well.While the practitioners’work is very important to individuals and families,it is most likely to be successful when the practitioner employs strategies and practices confirmed through well-designed and implemented research programs.Conversely,researchers should look to practitioners to assist them in developing and prioritizing research questions and projects.An examination of research and its applicability to the provision of personal finance education and counseling programs to individuals and families is important in increasing the likelihood that programming will result in successful financial management practices.Relating Research to PracticeOver the course of several years,it has become abundantly clear to AFCPE’s staff and board of directors that the future of financial counseling and education depends upon the interdependency of research and practice.One current focus of the AFCPE strategic plan includes building this capacity and interweaving research programs and practice outcomes.In 2006,the association embarked on a“listening”tour of sorts.Several forums were used to gather information about the current state and future needs of financial education and counseling.These included a survey of members and a conference workshop.In the 2006 survey,AFCPE memb ers were asked to choose the“one”financial message consumers most need to hear from counselors and educators.The three most popular responses were(1)prepare a spending plan,(2)reduce debt and (3)save.During a workshop held at its annual conference in 2009 regarding the future of financial counseling and financial education,participants worked in teams to assemble“then”and“now”posters regarding financial messages,programs,researchand program delivery.The Current State of Personal Finance Research The papers provide a good synopsis of the history of research in the field of personal finance.They summarize or employ theories that form the basis for personal finance research,review data that has historically been available to or used by researchers,address Internet delivery of financial vehicles and services and examine consumer finance as it relates to specific populations or settings.A perusal of research published in the past 5 years in six journals related to personal finance shows that the overwhelming majority of papers related to personal finance or financial counseling,and planning focused on(1)the relationship between specific demographic or social characteristics(e.g.,life cycle stage,income)and a particular financial behavior(e.g.,selecting a certain type of loan,saving money),(2)knowledge(e.g.,about credit cards,savings,vehicles)and a particular financial behavior or(3)optimal behaviors(e.g.,when to take Social Security benefits,assume investment risk or a particular mortgage).Israelsen and Hatch noted the lack of family financial management research in two leading family studies journals.Until recently,studies published in economics and finance journals focused heavily on the economic issues of the marketplace,individual decision making not directly related to financial decisions or corporate finance topics.Studies related to personal financial management behaviors are beginning to appear in these publications and other journals related to psychology and social work.The Journal of Behavioral Economics and Journal of Economic Psychology are dedicated to publishing research related to the interaction between economics and all types of behaviors and market choices.Many of the studies published in journals regarding personal finance analyze data collected through large national surveys.The reliance on information from large data sets is practical for several reasons including availability,accessibility,cost and the opportunity to study large populations.Other projects employed localized surveys studying the choices of certain populations.Inherently,these are specific and not necessarily applicable to large populations.One common element in most of these works is a description of the behaviors of a particular group of respondents and an examination of the differences or similarities(often,demographic)betweens respondents who behaved one way rather than another.Few published papers in personal finance research involve the collection andanalysis of motivation data;satisfaction with and/or success of specific delivery methods of financial education,counseling or messages;or development of diagnostic tools for practitioner or educator use.However,the results of several research projects did provide results that could easily translate into useful information for a practitioner.A good example of studies that provide results for use in research and practices include Lyons,Cude,Lawrence,and Gutter’s(2005)project investigating online research methodologies,the results of which are useful in designing survey research programs.A paper written by Mayer,Huh,and Cude(2005)examined the role of cues in assessing web site credibility.The results offer direction in successfully providing financial information to consumers via the Internet.Two papers supported the use of one-to-one counseling.Collins(2007)studied the financial counseling process and its effects on mortgage default.Elliehausen,Lundquist,and Staten(2007) examined the impact of credit counseling on the subsequent behavior of borrowers.Three research papers considered the psychological and emotional aspects of financial management.The Clarke,Heaton,Israelsen,and Eggett(2005)and Pinto,Pacente,and Mansfield(2005)research examined how financial information,roles and responsibilities were passed from one generation to another and the effect on behavior.A paper studying the link between psychological type using a well-known personality profile scale and financial decision-making was presented by McKenna,Hyllegard,and Linder(2003).Two papers related to diagnosing financial distress and risk tolerance resulted in counseling tools that can be employed by practitioners to better serve their clients.ConclusionDuring the past decade,for a variety of reasons,a marked increase in improving the financial literacy of Americans has developed.The media,policymakers and changing landscape of retirement plan programs have all contributed to the increased ernment entities,financial institutions and their foundations,community and social organizations and specialized financial education foundations serve the public interest through educational programming and research initiatives.The field of personal finance research can play a significant role in fulfilling the needs of consumers,practitioners and policymakers.But,it is at crossroads.While it is interesting to know what people know and do,it is more important that practitioners understand what motivates a consumer to implement planned behaviorsthat increase the potential for long-term financial stability and security.In addition,studies that confirm best practices in terms of marketing and delivering financial education and counseling programs and common financial messages would be quite useful to practitioners.Policymakers rely on quality research to inform issues and outcomes.Professional organizations,such as AFCPE,serve the personal finance profession best by uniting professionals with a diversity of perspectives to focus on common issues.Researchers,practitioners and educators,working together,can producen great outcomes from a well-designed national research program.The ultimate goal of a collaborative,interdisciplinary research program is to enhance the long-term financial security and stability of individuals and families.译文推动个人理财的应用研究资料来源:金融消费者手册期刊作者:夏恩本文的目的在于简要总结全国性专业协会在引进关于专业金融顾问和教育工作者的优质研究的作用。

个人理财英文版第一章

1-12

Goal-Setting Guidelines Effective Goals should be:

– Realistic – Stated

in specific, measurable

terms – Based on a time frame – Action-oriented

1-13

Assess Personal and Financial Opportunity Costs of Financial Decisions

• Opportunity cost = what you give up making a choice

Objective 3

– The trade-off of a decision

– Not always measurable in dollars; may be time – Consider lost opportunities resulting from your decisions

– /

1-7

Financial Planning in Our Economy Global Factors

• U.S economy affected by foreign investors and competition from foreign companies • Level of imports/exports affects available supply of dollars • Level of foreign investment affects domestic money supply • Money supply affects consumer interest rates

个人理财规划外文翻译文献编辑

文献信息:文献标题:A Study of Personal Financial Planning Process and Socio-Economic Decision-Making in Households(个人理财规划过程与家庭社会经济决策研究)国外作者:S Shah,AS Bhatt文献出处:《Social Science Electronic Publishing》,2016字数统计:英文2308单词,13376字符;中文4089汉字外文文献:A Study of Personal Financial Planning Process andSocio-Economic Decision-Making in Households Abstract In the current era, planning of finance is assuming extreme importance as myriad financial products are available and individuals’ demands are increasing. Personal financial planning is a process which outlines one’s financial objectives and takes financial decisions in a manner that his goals are achieved. The process of financial planning and decision-making in household has been studied independently by various researchers. However, these are essentially intertwined in nature. In view of this, the researchers have undertaken the task of understanding whether individuals followed the Personal Financial Planning process consciously and whether this was linked to household decision-making, especially in the social and economic areas. This paper also examines gender inequality in household decision-making and how household decision-making evolves with time. The study was conducted in the Ahmedabad district of Gujarat, and a sample size of 196 respondents was selected on judgmental basis to meet the objective of the study. The response rate was 78% (n=150) which is considered to be acceptable for a research study. The sample size was equally split between males and females. The survey was carried out in June- July, 2014.Analysis has been done by using Analysis of Variance(ANOV A), Binary Logistic Regression and Chi-square.It was found that age influences components of Personal financial planning (PFP) like determining one’s financial objectives, knowledge of finance, satisfaction regarding current economic status, and retirement planning. Likewise, gender, income, education, profession and marital status affect various components of PFP. It was also found that household economic and social decisions were related to income and investment of the respondent. Further, it could be inferred that in a household, males held more bargaining power in taking economic decisions, while females exerted more influence in taking social decisions.Key-words: Personal financial planning, financial objective, household economic decisions, household social decisions1.IntroductionHousehold financial management is that activity which is concerned with planning and controlling finances of individuals and households. The concept ‘personal financial management’ is of immense interest to researchers, academicians and policy formulators in the context of global economic crisis and financial inclusion in developing countries. As in the case of a nation or business institution, finance plays a crucial role in the life of an individual, to rich or poor. Mobilisation of finance and its wise and efficient deployment play a strategic role in the well-being of a nation or institution and at the most in the case of a person who is the base or starting point of any economic activity. Personal finance as a branch of economics deals with budgeting, saving, investing, borrowing, lending, insuring, and diversifying.Personal financial planning denotes the process of determining whether and how an individual can meet life goals through the proper management of financial sources.(CFP Board, 2005) Financial literacy and financial well-being are mutually related with each other (UNDP and PFIP, 2010). Financial well-being is the ability to have wealth to serve life - to have the financial means to comfortably attain whatever personal goals one has to enjoy an acceptable lifestyle. Sociological research data indicate that fourfactors strongly predict happiness and overall well-being in most cultures: health, economic status, employment, and family relationships. People are happier when they are healthy, employed, married or in a committed relationship, and financially secure. There is a relationship between an individual’s ability to do something (competence) and well-being (both self-perceived happiness and economic well-being). Well- being is, at least in part, a product of competent behaviour enacted consistently over time. Financial capability and financial competence therefore influence a person’s well-being. The opportunity accorded to people to engage with the formal financial system and how well they manage the money they have will influence their standard of living and the standard of living of those for whom they are responsible.Like never before, researchers, public authorities, community groups, industry associations and international organisations, are initiating financial literacy programmes and want to understand how people can become financially literate, or in other words, have the knowledge, understanding, skills and competence to deal with everyday financial matters and make the right choices for their needs.2.Literature Review2.1.Financial Literacy & PlanningVery few articles and research papers were found those have founded identical theories of personal financial planning. The term personal finance is having its root in micro-economics, finance and behavioral science as this area originated from home economics to various finance theories to behavioral finance. An Individual, as a consumer, is a rational being who tries to use his or her money income to derive the utmost amount of consummation or utility from it. Consumers want to get "the most for their money" or, to exceed their total utility as per ‘Maximisation of utility’ theory. Money is scarce in nature and due to this, consumers tend to be rational in their purchasing decisions. A consumer would spend his money on the best possible purpose or product and only when needed that guarantees optimum utility or a complete sense of satisfaction.Considering the importance of financial literacy, in RBI-OECD Workshop onFinancial Literacy, Bengaluru, in March, 2010 Sri Pranabkumar Mukerjee, Hon’ble Minister for Finance in his speech narrated “Financial literacy and education plays a crucial role in financial inclusion.” He further added that research and existing literature in financial literacy have typically associated an individual’s knowledge of economics and finance with his financial decisions related to savings, spending, borrowing, retirement planning, or portfolio choice. Today, financial competence has become essential due to complex choices and, while the policies need to enable access, the responsibility for saving and investing for the future primarily lies with the individuals. Another study by Miller M., Godfrey N., Levesque B. and Stark E. (2009) discussed the importance of financial literacy for consumers in developing countries, especially in the context of the global financial crisis.The authors stated that financial literacy was an active process, in which communicating information was only the beginning: empowering consumers to take action to improve their financial well-beingwas the ultimate goal. This study presented empirical evidence on thevalue of financial literacy programs and made a case for further research in determining the most effective financial literacy tools, programs and public policies, especially in the context of developing countries. Lusardi A. (2001), a world famous financial literacy scholar and academician, in her article ‘Financial literacy around the world: an overview’ stated that in an increasingly risky and globalised market-place, people must be able to make well-informed financial decisions.2.2.Socio-Economic decisions in householdHousehold decision-making affects many choices with important consequences including the distribution of income, allocation of resources, allocation of time, purchase of goods, and fertility decisions. If there is gender inequality in household decision making then this affects the economic well-being of women and children in the household. Blood and Wolfe (1960) in their study based on households in the Detroit area of the United States, found that comparative resources of the wife and husband were more important determinants in decision-making and power than social norms. The spouse with the greater resource base was more likely to have more decision making power. Similar studies done in lower and middle-income countriesreported different results. Research in Yugoslavia and Greece found that husband’s socio-economic resources were negatively related to his power (Buric and Zecevic 1967, Safilios- Rothschild 1967). A study conducted in India by Rammu (1988) which included urban, dual and single income earning households found that the more resources the partner brought into the marriage, in terms of education, income and occupational status, the more decision-making power he/she possessed. He also found that women who were gainfully employed exercised greater authority in all spheres of decision-making compared to women engaged in domestic housework only. However, even employed women did not succeed in negotiating a noticeable change in the allocation of domestic housework, perhaps a consequence of the timeless social norm of women doing housework. In one more study conducted in Venezuela (Lawrence and Mancini 1998) focused on decision-making concerning four subjects: purchase of household goods, change in residence, household finances and children’s education. The study found that while a majority of households made decisions jointly, more women made decisions concerning the purchase of household goods and children’s education compared to men, while men dominated decisions concerning household finances and change in residence.The process of financial planning and decision-making in household has been studied independently in the previous researches. However, these are essentially intertwined and if one wants to achieve life goals, financial literacy is a necessity. In view of this, the researches undertook the task of understanding whether individuals followed the Personal Financial Planning (PFP) process consciously and whether this was linked to household decision-making, especially in the social and economic areas. Further, there is a dearth of research related to this topic especially in Gujarat state of India. Hence, the researchers carried out the study in Gujarat.3.Research MethodologyOn the basis of review of literature and evidences from psychological studies, the present study has been planned with the following objectives:1)To analyse the effect of demographic variables on household financial planning2)To find out the relationship between financial planning decisions and economic and social decisions3)To find out the gender impact on economic and social decisionsThe study was conducted in the Ahmedabad district of Gujarat, and a sample size of 196 respondents was selected on judgmental basis to meet the objectives of the study. The total number of questionnaires distributed was 196. We received 176 questionnaires, but some of them had one or more missing responses. Such questionnaires were discarded and were not considered for further analysis. The final sample size after discarding the questionnaires with missing responses was 150. Thus the response rate was 78% which is considered to be acceptable for a research study. The respondents carried equal number of males and females. The survey was carried out in June-July, 2014. The profile of the respondents with respect to demographics like age, gender, qualification, income, marital status and household investments has been presented in the data analysis section.The research design for the study is descriptive in nature. The questionnaire constructed for the study included several questions which were continuous and categorical in nature. The survey consisted of questions that covered demographics, financial attitude towards personal financial planning, preferences for investment avenues, and purposes for investment.Definition of ConstructsThe components of personal financial planning were obtained through literature review regarding how individuals consider each component in their household financial planning decisions.•Financial Objective: Financial objectives are life goals converted into monetary terms. They can be categorised based on time period- Short term, Medium term and Long term financial objectives.•Knowledge: Knowledge of financial products, terms, financial services and financial markets required for personal financial management.•Satisfaction: Satisfaction in context to personal financial components viz. obtaining, saving, borrowing, investment planning.•Tax efficiency: Proper management of financial resources to avail various rebates and concessions thereby reducing tax liability.•Insurance Coverage: Adequate insurance coverage of life, health and property against risks associated.•Retirement Income: Availability of sufficient corpus to maintain the same standard of living in non-earning years.Data Analysis ApproachAnalysis is done using SPSS software 19.0 and Microsoft excel.Description of Analytical Tools•To find out the impact of the demographical variables on household financial planning, One-Way Analysis of Variance (ANOV A) has been applied for each component identified through literature review and each demographic variable viz. gender, age, income, education, profession and marital status.•To find out the association between financial and socio-economic decisions, Chi square has been applied.•To further analyse the gender impact on economic and social decisions Bivariate Logistic regression is applied where gender is taken as predictor variable and decision taker as outcome variable.4.Managerial ImplicationsThere is significant association between gender and financial objective, knowledge of finance and retirement planning, wherein males agree more to having knowledge and adequate retirement planning.•The older age group (40 – 60 years) disagree more as compared to other age groups when it comes to satisfaction, financial objective, knowledge and retirement planning processes of financial planning.•The higher income group (above 8 lacs) disagree more when it comes to deriving satisfaction from the current PFP, however, the low income group agreed more to tax efficiency as they fall in the tax exempted category.•The non-employed group had less knowledge of the formal financial planning process as compared to the salaried and business groups, and the business class significantly differed from other two groups for retirement planning component.•The marital status is related to several components of PFP, viz. financial objective, knowledge, tax efficiency, and insurance coverage and the categories differ among themselves marginally for these components. However, the divorced category was found to be lacking on the financial objectives and satisfaction part.Looking at the above findings, it became increasingly clear that the typical target group for conducting financial literacy programs would consist of young and middle-aged, females who are home-makers. But the next question was whether they are influential in household decision- making. If they are not typical decision-makers, the training shall not impact the actual decisions taken in the household. Hence, a few significant economic and social decisions of the household were identified and the role of females was studied. The analysis indicated that males play a dominant role in taking economic decisions while females play a leading role in taking social decisions of the household. Hence, the financial literacy programs while targeting the above-mentioned group should especially capture the process of PFP, with a focus on social decisions taken in the household.中文译文:个人理财规划过程与家庭社会经济决策研究摘要在当前时代,随着金融产品的大量激增,以及个人需求的不断上升,理财规划开始变得非常重要。

个人理财英文版第二章

• Insolvency:

N–eIntabWilityotrotphay debts when due – Liabilities far exceed assets

2-14

Sample Balance Sheet

2-15

Ways to Increase Net Worth

Documents re: purchase and sale of real estate Copies of tax returns and supporting data

Indefinitely

As long as you own them Indefinitely

7 years minimum 10 years better

RATIO

Calculation

Interpretation

Debt Ratio

Liabilities divided by net worth

Low debt is best

Curent Ratio Liquidity Ratio

Liquid assets divided by current liabilties

Money Management Troubles & Debt

Getting out of debt:

2-5

An Organized Personal Financial Records System

Provides a basis for:

• Handling daily business affairs, such as bill paying • Planning and measuring financial

关于个人理财的英语作文

关于个人理财的英语作文The Essentials of Personal Finance Management.Personal finance management is a crucial skill that everyone should possess. It involves managing one's income, expenses, savings, investments, and financial risks to achieve short-term and long-term financial goals. With the increasing complexity of financial products and services,it has become even more important to have a sound understanding of personal finance to ensure financial stability and growth.Budgeting and Saving.The foundation of personal finance management is budgeting. Creating a budget helps individuals track their income and expenses, identify areas where they can save money, and allocate funds towards their financial goals. A budget should be realistic and should take into account all fixed expenses such as rent, utilities, and transportation,as well as variable expenses like food, entertainment, and healthcare. By subtracting total expenses from total income, individuals can determine their disposable income, whichcan then be used for savings and investments.Saving money is essential for building a financial cushion to cover unexpected expenses or emergencies. It is recommended to save at least 10-20% of one's income, depending on personal financial goals and circumstances. There are various saving options available, such as bank accounts, bonds, and mutual funds, and it is important to choose the one that best suits one's needs and risk tolerance.Investing for Growth.Investing is another crucial aspect of personal finance management. By investing, individuals can grow theirsavings and achieve their financial goals faster. There are various investment options available, ranging from low-risk options like bank deposits and bonds to higher-risk options like stocks and cryptocurrencies. The choice of investmentshould be based on personal risk tolerance, financial goals, and time horizon.It is important to remember that investing involves risks, and it is crucial to diversify one's portfolio to mitigate these risks. Diversification means investing in multiple asset classes and markets to reduce the impact of any single asset's performance on the overall portfolio.Insurance and Risk Management.Insurance is another important aspect of personal finance management. It helps individuals protect themselves and their families from financial losses caused by unexpected events like accidents, illnesses, or natural disasters. There are various types of insurance available, such as life insurance, health insurance, and property insurance, and it is important to choose the ones that best suit one's needs and budget.In addition to insurance, it is also important to havea financial plan for emergencies. This plan should includea contingency fund to cover unexpected expenses and a financial backup plan in case of job loss or otherfinancial emergencies.Conclusion.Personal finance management is a lifelong process that requires continuous monitoring and adjustment. By budgeting, saving, investing, and managing risks, individuals can achieve their financial goals and build a secure financial future. It is important to stay informed about financial products and services, stay disciplined with one'sfinancial plan, and seek professional advice when needed.By taking control of their personal finance, individualscan enjoy a financially stable and secure life.。

3篇关于《个人理财的重要性》的英语六级作文

1.篇一:The Importance of Personal Financial ManagementPersonal financial management plays a pivotal role in shaping individuals' long-term financial well-being. Through prudent budgeting, saving, and investment, individuals can establish financial stability, achieve their financial goals, and effectively navigate unexpected expenses or economic downturns. Furthermore, sound financial management enables individuals to build a financial safety net, plan for future expenses such as education, homeownership, and retirement, and make informed decisions about borrowing and debt management. By cultivating a habit of responsible financial management, individuals can enhance their financial resilience and reduce their vulnerability to financial hardships. Moreover, effective personal financial management fosters a sense of empowerment and control over one’s financial future. Therefore, developing financial literacy and embracing the discipline of personal financial management are essential for individuals to secure their financial well-being and pursue their aspirations.2.篇二:Empowering Individuals through Personal Financial ManagementThe practice of personal financial management empowers individuals to take charge of their financial destinies and build a secure future. By cultivating habits of budgeting, saving, and investing, individuals can forge a path towards financial freedom and independence. Effective financial management enables individuals to weather economic uncertainties, pursue educational and career opportunities, and achieve their personal and professional aspirations. Moreover, it instills a sense of discipline and responsibility, fostering a proactive approach towards financial decision-making. Through the prudent management of income, expenses, and investments, individuals can secure their financial well-being, mitigate financial risks, and withstand unexpected financial challenges. Therefore, promoting financial literacy and advocating for the importance of personal financial management is crucial in equipping individuals with the tools and knowledge to navigate the complexities of the modern financial landscape.3.篇三:Cultivating Financial Resilience through Personal Financial ManagementPersonal financial management is indispensable in cultivating financial resilience and security. Individuals who actively engage in budgeting, saving, and investing are better equipped to weather financial uncertainties, seize opportunities, and pursue their long-term financial goals. Effective financial management enables individuals to build a robust financial foundation, plan for contingencies, and make informed financial decisions. By embracing disciplined financial practices, individuals can mitigate the risks of debt, financial hardship, and unexpected expenses. Additionally, sound financial management fosters a mindset of preparedness and forward-thinking, enablingindividuals to navigate financial challenges with confidence. Therefore, promoting a culture of financial literacy and empowering individuals with the tools and knowledge for personal financial management is crucial in bolstering financial resilience and fostering a more secure financial future for individuals and families.。

个人理财英文作文

个人理财英文作文英文回答:Personal Finance: A Comprehensive Guide to Mastering Your Money。

As Benjamin Franklin famously said, "A penny saved is a penny earned." Managing personal finances effectively is a crucial aspect of financial independence and overall well-being. It involves understanding your income, expenses, savings, investments, and financial goals. By embracing responsible financial habits, you can take control of your financial destiny and achieve your aspirations.Step 1: Track Your Income and Expenses。

The foundation of personal finance is understandingyour cash flow. You can use a budgeting app, spreadsheet,or simply a notebook to track every dollar that comes inand goes out. Categorize your expenses (e.g., housing, food,transportation) to identify areas where you can cut back.Step 2: Create a Budget。

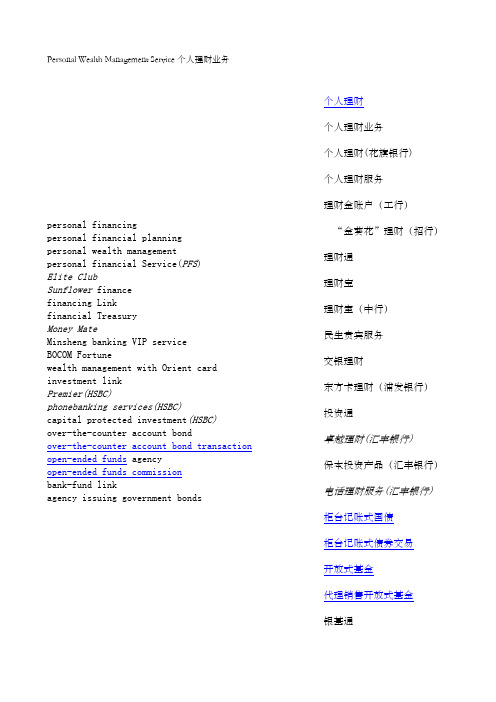

个人理财英语

Personal Wealth Management Service个人理财业务personal financingpersonal financial planningpersonal wealth managementpersonal financial Service(PFS)Elite ClubSunflower financefinancing Linkfinancial TreasuryMoney MateMinsheng banking VIP serviceBOCOM Fortunewealth management with Orient card investment linkPremier(HSBC)phonebanking services(HSBC)capital protected investment(HSBC)over-the-counter account bondover-the-counter account bond transaction open-ended funds agencyopen-ended funds commissionbank-fund linkagency issuing government bonds 个人理财个人理财业务个人理财(花旗银行)个人理财服务理财金账户(工行)“金葵花”理财(招行)理财通理财宝理财室(中行)民生贵宾服务交银理财东方卡理财(浦发银行)投资通卓越理财(汇丰银行)保本投资产品(汇丰银行)电话理财服务(汇丰银行)柜台记账式国债柜台记账式债券交易开放式基金代理销售开放式基金银基通代理发行国债visible treasury certificateBearer treasury certificateindividual Credit Servicesafekeeping agencycustodial box servicesafe deposit box serviceassets managementaround-clock service of account management network settlementbank-securities linkbank-securities account transferMoney Linkaccount transfer via money linkbank-insurance link(bonus participated insurance) open-ended fundsbank-fund linkopen-ended funds commission 凭证式国债无记名式国债个人资信服务代理保管业务保管箱服务保管箱业务资产管理24小时到账处理业务网络结算业务银证通银证转账银证通(浦发银行)银证转账(浦发银行)银保通(分红保险)开放式基金银基通代理销售开放式基金capital accountdeposit(Margin) accountcounter Transfertelephone Banking self-service transfer service a letter of entrustment for transferentrusting transfer and deduction shareholders’ magnetic cardnetwork settlementdomestic payment settlement service 资金账户保证金账户柜台转账电话银行自助转账old-age pension fund social security fund bond fundinvestment fund close-ended fund open-ended fund 转账委托书委托转账代缴费股东磁卡网络结算业务国内支付结算业务养老基金社会保险基金债券基金投资基金封闭式基金开放式基金Savings Deposit储蓄存款业务savings depositdemand deposit(current deposit)current deposit passbookcurrent checkbook deposittime or demand optional depositcall deposittime deposit(term deposit)large sum fixed depositgeneral fixed depositfloating time rate depositlump-sum deposit and withdrawaltime deposit of lump-sum deposit and withdrawaltime deposits of lump-sum depositing and lump-sum withdrawalinstallment fixed depositstime deposit of small savings for lump-sum withdrawal interest withdrawal for a principal depositedpeincipal-receiving and interest withdrawing time deposit time saving big money and small drawingsavings / time optional deposits 活期储蓄存款活期储蓄存款活期存折活期支票定活两便存款通知存款定期存款大额定期存款普通定期存款定期浮息选择存款整存整取整存整取定期储蓄整存整取定期存款零存整取零存整取定期储蓄存本取息存本取息定期储蓄整存零取定期储蓄定活两便存款seven-day notice depositpersonal settlement accounts avings account(HSBC)f ixed deposit account(HSBC)renminbi account(HSBC)children account(HSBC)statement savings account(HSBC)interest bearing savings account(HSBC)interest bearing chequeing account(HSBC) advance withdrawal and loss-reporting business deposits by correspondencedeposit collections in different places personal checksdeposit certificate loss reportingloss reporting for personal checkssavings certificatepersonal call depositinterbank deposit and withdrawaleducation deposit 七天通知存款个人结算账户储蓄账户(汇丰银行)定期存款账户(汇丰银行)人民币账户(汇丰银行)儿童账户(汇丰银行)结单储蓄账户(汇丰银行)生息储蓄账户(汇丰银行)生息支票账户(汇丰银行)提前支取与挂失业务通信存款储蓄存款异地托收个人支票储蓄存款挂失个人支票挂失定期存单个人通知存款通存通兑教育储蓄存款procedures of loss reporting deposit certificate loss reporting interim loss reportingcurrent All-In-One passbookfixed All-In-One passbookmultiple function debit card Deposit Plus(HSBC)挂失业务存单挂失临时挂失活期一本通定期一本通多功能借记卡双利存款(汇丰银行)Personal Consumer Credit个人消费信贷housing mortgage loanindividual business house loan house refurbishing loan. individual housing loanshousing loans on own account housing loans on authorization individual combined housing loans CITIC Happy Family 住房抵押贷款个人商业用房贷款房屋装修贷款个人住房贷款auto loansloan for refurbishing houseconsumer durables loanpersonal loan secured by CDs/treasury bonds individual consumption loanpetty consumer creditindividual unsecured loanconsumption credit for individual clients individual consumption loansecured loansmall amount private loans 自营性住房贷款委托住房贷款个人住房组合贷款中信家家乐汽车消费贷款家居装修贷款大额耐用消费品贷款个人存单质押贷款个人消费信贷小额信用消费贷款个人信用贷款个人消费信贷业务个人消费信贷抵押放款(担保放款) 小额贷款individual auto loanindividual comprehensive consumer loanindividual large-denomination durable commodities loan personal pledge loantravel and vacation loansonline personal pledge loaninsurance certificate pledge loandeposit certificate pledge loancertificates of deposit(CDs)individual comprehensive consumer loanindividual large-denomination durable commodities loan state educational loancommercial educational loanoverseas study loaneducational loans 个人汽车消费贷款个人综合消费贷款个人大额耐用消费品贷款个人质押贷款旅游度假贷款网上个人质押贷款保单质押贷款存单质押贷款大额存单个人综合消费贷款个人大额耐用消费品贷款国家助学贷款商业助学贷款留学贷款教育助学贷款Foreign Exchange for Corporate公司外汇业务forex deposit for enterprisecurrent forex deposit for enterprisetime foreign fxchange deposit for enterprise call forex deposit for enterpriseforex creditforex working capital loanforex temporary loansforex short-term loansforex medium-term loansforex revolving loansforex loans with repayment in Installments forex fixed asset loanforex fixed asset investmentforex business development and expansion forex technical innovationforex fixed asset acquisition 单位外汇存款业务活期对公外汇存款定期对公外汇存款通知对公外汇存款外汇贷款业务外汇流动资金贷款外汇临时流动资金贷款外汇短期流动资金贷款外汇中期流动资金贷款外汇流动资金循环贷款外汇整贷零偿外汇固定资产贷款外汇固定资产投资贷款外汇开发扩建贷款外汇技改贷款外汇固定资产收购贷款International Finance国际融资业务forex merger&acquisition loanproject financeBOT(build, operate, transfer)BT(build, transfer)export buyer’s creditsyndicated loanon-lending project financeinternational commercial loanimport buyer’s creditforeign government loanforeign government mixed loanloan from international financial organizations forex transferred loanf inancing business of featuresbills discountcredit linew orldwide creditexport seller's creditfinance leasepurchase of the accounts receivableexternal labor service contract loan 外汇兼并收购贷款项目融资建设经营转让建设转让出口买方信贷银团贷款外汇转贷款项目融资国际商业贷款融资进口买方信贷融资外国政府贷款融资外国政府混合贷款融资国际金融组织贷款融资外汇转贷款特色融资业务票据贴现授信额度统一大授信出口卖方信贷融资租赁应收账款收购对外劳务承包贷款distribution passportstart-up winneri nternational financing and guarantee business trust servicesinternational debt offeringforeign exchange guaranteeguarantee for loantender guaranteeperformance bondadvanced payment guaranteepayment guaranteeverification payment guaranteetechnical verification payment guarantee deferred payment guaranteelease guaranteeimport bills for collectionexport bills for collectionpurchasing collection bills 一路通创业宝国际融资及担保信托业务境外发债融资外汇担保业务借款担保投标担保履约担保预付款退款担保付款担保验货付款保函技术交易验收付款保函延期付款担保租赁担保进口代收出口托收出口托收买单packing loan under L/Ctransferable L/Cnegotiating export bills打包放款(信用证项下)discounting billssecured ladingopening letter of guaranteeforeign exchange payment and clearing service settlement clearance for foreign exchange pusiness banking facilityforeign exchange rate risks coverguarantee and attestationinter-bank foreign currency borrowings and lendings asset portfolio managementoffshore banking businesstrade financinggeneral banking facilitiesPacking Creditimport bills purchaseexport(0utward) bill purchaseforeign currency bill discountforeign exchange bills purchasebills discountingForfaitingFactoringnon-trade finance 转让信用证议付出口信用证单据(银行承兑)汇票贴现担保提货开立保函外汇清算业务外汇业务清算授信外汇保值避险担保和见证金融机构间外汇拆借理财策划离岸金融业务贸易融资综合授信打包放款进口押汇出口押汇外币票据贴现买入外币票据票据贴现福费廷(包买票据)保理业务非贸易融资Bank Card银行卡业务peony credit cardpeony international card peony MoneyLink cardpeony IC(Smart) cardpeony proprietary cardpeony photo cardpeony co-branding cardLong cardsavings carddebit cardanimal cardaccount transfer cardpre-paid consumption card special-purpose cardco-branded cardGreat Wall credit cardGreat Wall international card Great Wall credit card in RMB pacific cardgold cardordinary cardThe World’s Sunflower development cardMinsheng cardOrient cardLady cardVisa cardMaster cardDiner’s cardAmerican Express cardMillion cardJCB cardFederal card 牡丹信用卡牡丹国际卡牡丹灵通卡牡丹智能卡牡丹专用卡牡丹彩照卡牡丹联名卡龙卡储蓄卡借记卡生肖卡转账卡储值卡专用卡联名卡(认同卡)长城信用卡长城国际卡长城人民币信用卡太平洋卡金卡普通卡金葵花卡发展卡民生卡东方卡真情卡(广发银行)维萨卡万事达卡大莱卡运通卡百万卡(日本)JCB卡(日本)发达卡(香港)Terms of Post and Title岗位职务词汇board of directorschairman of the boardchair of board of directors chief executive officer directormanaging directorauthorized officermanager and head of China desk general manager(GM)director generalchief controllerdeputy general manager(DGM) chief executive officer(CEO) chief financial officer(CFO) chief market officer(CMO)top manager 董事会,理事会董事长董事长董事长董事总裁,常务董事代理行长中国事务部经理兼主管managerfinance director financial manager chief accountant chief cashierchief clerkhead clerkhead of department head tellerchief accountant chief of finance sales director sales manager directing staff top management middle management lower management 总经理总监总稽核副总经理首席执行官首席财务总监首席市场总监总经理经理,主任财务经理,财务处(科)长财务经理会计主任,总会计师,财务处长出纳主任主任办事员首席办事员部门主任出纳主任总会计,会计主任财务主任营业副经理;销售处(科)长销售经理领导人员最高管理层基层管理manager of bank managerial staffofficer, official financial adviser financial accountant financial administrator financial executive auditing officers controlleraccountant in charge accountantconsultantmanagement consultant managing agentassistant accountant assistant general manager assistant manager managing partner administrative staff office staffoperation staff accounting clerkbank clerkoffice clerkstatistical clerkpay clerkstaffclerkcashiertellercustomerclient 银行经理人管理人员高级职员财务顾问财务会计员财务主管人财务主管审计人员主管会计;审计员主管会计师会计师,会计员顾问业务顾问经理人的代理助理会计师协理,副总经理,副总裁副理,协理办事员管理人员,行政人员办公室职员簿记员银行职员办事员统计员出纳员职员办事员出纳员出纳员顾客,客户顾客,客户Intermediary Business(1)中间业务remittance servicesdomestic remittanceremittance agencyremittance expresscommom remittanceurgent remittanceremittance by draftcash remittancebank promissory note(bank check) checkcheck Bookagency servicesfund agency serviceBank-fund LinkBank-futures LinkFortuneLink 汇兑业务国内汇兑代理汇兑汇款直通车普通汇款加急汇款票汇(汇票汇款) 汇款银行本票支票支票簿代理业务基金代理业务银基通银期通财富通bond agency servicebonds settlement agencyinsurance agency servicefinancing agencysafekeeping agencycollection and payment agencysettlement agencysalary payment agency(payroll agency service) wages(old-aged pension) distribution agency public utility fee levying agencyissuing government bonds agencycommission collection of telephone fee commission collection of telephone fee for Unicom commission collection of electricity charge commission collection of insurance premium payment through telephone bankingpayment through mobile phone bankingnetwork payment settlement agencyagency collection and paymentcommission payment on consignmentpayment in cashcharge withholding service 债券代理业务债券结算代理保险代理业务代理理财代理保管代理收付代理结算代发工资(业务)代发工资(养老金)业务代理公用事业收费代理发行国债代收电话费业务代收联通话费业务代收电费业务代收保险费电话银行缴费手机银行缴费代收付业务网上支付结算代理委托缴费现金缴费缴费业务fee collection expresscommission security business agency securities fund clearing commission tax withholding commission insuranceagency signing of the banker’s bill forward settlement 缴费通代理证券业务代理证券资金清算代理税收业务代理保险业务代签银行汇票期货结算业务client service centercustomer service hotlinebearer treasury certificatevisible treasury certificatebearer treasury certificate with fixed denominationproof of payment(payment vouchers)a letter of entrustment for transfer agency collection and paymentagency collection and deductionpublic utility Feeentrusting transfer and deduction agency issuing government bondsforeign exchange trading agency automated transferdeposit(margin) account 客户服务中心客户服务热线无记名式国债凭证式国债固定面额无记名式国债支付凭证转账委托书代收代缴费公用事业费委托转账代交费代理发行国债代理外币买卖自动转账保证金账户bill consultancyreal-time funds transferringcounter transfersettlement businessdomestic settlement servicedraft for collectioncollection and acceptioncommission receptionon-line Settlementon-line Shoppingsecurities and capital settlement agency commission collection and payment agency client bar code automatic inquiry system payment and settlement agencyforward settlement 票据查询实时资金汇划柜台转账结算业务国内结算业务托收汇票托收承付委托收款网上结算网上购物代理证券资金清算代理收付业务客户条形码自动查询支付结算业务代理期货结算业务notes clearingcharged bond trading on the counter treasury billstreasury bondsbook-entry treasury billvisible treasury certificate investment bankingmerchant bankingconsultancy-specific financial service funds trusteeshipcash-based settlementpaper-based settlementelectronic-based settlement transferring settlementaccounting settlement business 柜台记账式债券交易国库券长期国债凭证式国债凭证式国债投资银行业务商人银行业务咨询性金融业务基金托管现金清算票据清算电子清算转账结算会计结算业务。

外文文献翻译(我国商业银行个人理财业务的战略研究与发展现状)讲课教案

The Development Status and Strategy Research of Commercial Banks’Personal Financial ManagementBusiness in ChinaAbstract: The personal financial management business in our country is in the initial stage,compared to the developed one in western,there’s still a long way to go,Therefore,the commercial banks in china need to review and study to estimate market direction;build excellence brand image and special services;Increase of innovation;change the products from single to comprehensive;Establish and perfect financial management business’management system in o rder to promote the development of personal financial business in our management country.Keywords:Commercial banks,Personal financial management,Strategy1 IntroductionThe commercial banks are facing the new situation:the increasing danger in traditional business.the margin of the interest rate’s turning increasingly narrowed and foreign bank’s competition.These banks should think deeply to find why that business develop so slowly and then put forward a feasible plan.The personal financial management business is not only an important carrier for commercial banks to advance Comprehensive management strategy but also a major way of improving Intermediary business income.That business in our country is in the initial stage.compared to the developed one in western,there’s still a long way to go.Therefore.the commercial banks in china need to review and study to estimate market direction;build excellence brand image and special services;Increase of innovation;change the products from single to comprehensive;Establish and perfect financial management business’management system in order to promote the development of personal financial management business in our country.Meanwhile.the commercial banks are facing the new situation:the increasing danger in traditional business.the margin of the interest rate’s turning increasingly narrowed and foreign bank’s competition.These banks should think deeply to fend why that bus;mess develop so slowly and then put forward a feasible plan.Among all the businesses in commercial banks.personal financial management business has the advantages of huge market capacity,low risk,widerange of business,and stable income.For those advantages the personal financial m anagement business becomes commercial banks’main business and vital profits source.In western developed country,this kind of business almost gets into every family.Its business income has been account for bank’s 30%.Compared to the developed one in western.there’s still a long way to go but it has a bright market expectation.However,our country’s personal financial management business is limited by some factors,for instance,the financial legal system,financial supervision system and the development of financial market.As a result.it brings some problems that need to be done while developing rapidly.2 The Development Situation,Trait and Existing Problem of Individual Manage Matters Operation in Commercial Bank of China2.1 The development situation of individual money matters operation in commercial bank of ChinaManage money matters operation refers to commercial bank uses professional advantages like various kinds of financial knowledge,professional technique and wide fund credibility and according t o clients’financial position and investment requirement,provide clients with professional service activities,such as financial analysis.financial planning,investment counselor and assets management.Recently,as the fast developing economy of china and the accumulating property of citizens,the need of manage money matters operation becomes stronger and stronger.There are several reasons:first of all,when people’s properties accumulate to some degree,they concern more about how to effectively keep and increase the value of their properties.Second,as the pushing on housing,education and medical treatment marketing revolution proceeding,families need the help of financial mechanism service to create a complete risk safeguard mechanism.On the other hand,we have already been in aging stage,thus it has become many people’s real need to accumulate part of their pension through manage money matters.Under the circumstances.individual money matters operation of commercial bank develops quickly.But according to individual money matters operation situation of every commercial bank.there are still many problems that make it hard to develop individual money matters operation.2.2 The trait of individual money matters operation in commercial bank of ChinaAs the individual money matters operation of commercial bank has just started,financial mechanism and laws and regulations systems are special,so compared to western developed countries,we have our own traits.Fiduciary loan product becomes the 1eader of manage money matters market Recently,invest people pay more attention to the risk situation of product when they choose manage money matters product.At the same time,because the CBRC(china banking regulatory commission) adds its strength to manage money matters operation in commercial bank,the breed structure of manage money matters product changed a lot in general.Since 2009,fiduciary loan product increased largely and become the leader in all kinds of banking manage money matters product for its clear investment, simple structure,various deadline,stable income.Public beneficial and creative product is the value of manage money matters product afoot. During the wenchuan earthquake in 2008,some banks give quickly reflect to the calamity and push out public beneficial and creative manage money matters product.This kind of manage money matters product was themed as benevolent and cares,which greatly widen the developing thought of banking manage money matters operation and validly promote brand value and social image of the bank.3 The Reasons Why We Have Problems in Personal Financial Business in Our National Commercial BanksThe reason why we have so many problems in personal financial business in our national commercial banks is not just because of one single element,but because of many aspects.The reason that we still take separate operation in practice .The policies and regulations.idea of supervision and measures in China still not keep pace with the development of era;we still rely on separate operation and separate management to keep watching to the financial risk.But this kind of operation mode increases the cost of processing personal financial business in commercial banks.and it is hard to make good results.The reason why all the products have the same quality.As it is limited by the idea,the analysis of personal finance business from our commercial banks are not totally correct,there still exists some deficiencies to theresearch of clients,as a result.nearly all the financial products are the same.The reason why we have a shortage of high—quality financial manager The capability of training finance managers in our country is still undeveloped and the mentality relatively falls behind with developing countries,so most of excellent managers choose to enter foreign banks, and it will be reasonable that the managers couldn’t reach the requirements in national commercial banks.The reason why we are lack of the consciousness of financial management .As we are developing our economy in recent years, it results in a lack of financial culture and financial consciousness.Firstly, people just have some egg money;they can hardly adjust to the life style which adds the finance management into it.Secondly, the influence of traditional concept and shortage of understanding the personal financial business in banks result in the lack of financial consciousness and the deficiency of sense of identity and safety.The reason why we are lake of cultivation Our national commercial banks are limited by system, thinking, technique and objective environment and some influences so that our national commercial banks’s cultivation stagnates, in some high—profited area,we couldn’t keep the pace.And if we don’t solve the problem of lack of cultivation,it is hard for us to complete with foreign banks.4 The Questions Exit in Individual Managing Financial Services in Commercial Bank of ChinaA good financial planner should know everything about a product and have a good knowledge of security, bank,insurance。

个人理财英文版第一章

• Increased control of your financial affairs

• Improved personal relationships • Sense of freedom from financial

– Marital status, household size, employment

– Exhibit 1-1 (page 5)

• Major events:

– Graduation, marriage, divorce – Birth or adoption of child – Career or health changes

1. Identify social and economic influences on personal financial goals and decisions

2. Develop personal financial goals 3. Assess personal and financial

opportunity costs associated with financial decisions 4. Implement a plan for these decisions

1-2

Financial Planning

• Process of managing your money to achieve personal economic satisfaction

– Business, labor & government

理财的好处英语作文带翻译

Financial management is a crucial skill that everyone should possess, as it helps individuals to understand and control their financial situation, plan for the future, and achieve their financial goals. Here are some of the benefits of financial management:1. Control Over Finances: It allows individuals to have a clear picture of their income, expenses, assets, and liabilities. This control helps in making informed decisions about spending and saving.2. Budgeting: Effective financial management involves creating a budget that allocates funds for various needs and goals. This helps in living within ones means and avoiding overspending.3. Savings: By understanding where money is going, one can identify areas to cut back and save more. Savings can be used for emergencies, future investments, or to achieve personal financial goals.4. Debt Management: Proper financial management helps in reducing and managing debt. It involves understanding the terms of loans and credit, and making timely payments to avoid interest accumulation.5. Investment Opportunities: With a solid financial foundation, one can explore various investment opportunities that align with their risk tolerance and financial goals. This can lead to wealth creation over time.6. Retirement Planning: Financial management is essential for planning a comfortable retirement. It involves saving and investing in a way that ensures a steady income during retirement years.7. Financial Security: By managing finances well, individuals can achieve a sense of financial security, which reduces stress and allows for a more peaceful life.8. Education and Training: Financial management skills can be learned and improved over time. Continuous learning helps in adapting to changing economic conditions and personal circumstances.9. Legacy Planning: For those who have dependents or wish to leave a legacy, financial management ensures that there are plans in place for the distribution of assets after ones passing.10. Economic Stability: On a larger scale, when individuals manage their finances well, itcontributes to the economic stability of the community and the country.In conclusion, financial management is not just about making money but also about making the most of the money one has. It empowers individuals to take control of their financial future and live a life that is in line with their values and aspirations.理财的好处英语作文翻译:理财是一项每个人都应该具备的关键技能,它帮助个人了解和控制自己的财务状况,为未来做计划,并实现他们的财务目标。

银行个人理财战略中英文对照外文翻译文献

银行个人理财战略中英文对照外文翻译文献(文档含英文原文和中文翻译)原文:The Development Status and Strategy Research of Commercial Banks’Personal Financial ManagementBusiness in ChinaAbstract: The personal financial management business in our country is in the initial stage,compared to the developed one in western,there’s still a long way to go,Therefore,the commercial banks in china need to review and study to estimate market direction;build excellence brand image and special services;Increase of innovation;change the products from single to comprehensive;Establish and perfect financial management business’management system in order to promote the development of personal financial business in our management country.Keywords:Commercial banks,Personal financial management,Strategy1 IntroductionThe commercial banks are facing the new situation:the increasing danger in traditional business.the margin of the interest rate’s turning increasingly narrowed and foreign bank’s competition.These banks should think deeply to find why that business develop so slowly and then put forward a feasible plan.The personal financial management business is not only an important carrier for commercial banks to advance Comprehensive management strategy but also a major way of improving Intermediary business income.That business in our country is in the initial stage.compared to the developed one in western,there’s still a long way to go.Therefore.the commercial banks in china need to review and study to estimate market direction;build excellence brand image and special services;Increase of innovation;change the products from single to comprehensive;Establish and perfect financial management business’management system in order to promote the development of personal financial management business in our country.Meanwhile.the commercial banks are facing the new situation:the increasing danger in traditional business.the margin of the interest rate’s turningincreasingly narrowed and foreign bank’s competition.These banks should think deeply to fend why that bus;mess develop so slowly and then put forward a feasible plan.Among all the businesses in commercial banks.personal financial management business has the advantages of huge market capacity,low risk,wide range of business,and stable income.For those advantages the personal financial management business becomes commercial banks’main business and vital profits source.In western developed country,this kind of business almost gets into every family.Its business income has been account for ba nk’s 30%.Compared to the developed one in western.there’s still a long way to go but it has a bright market expectation.However,our country’s personal financial management business is limited by some factors,for instance,the financial legal system,financial supervision system and the development of financial market.As a result.it brings some problems that need to be done while developing rapidly.2 The Development Situation,Trait and Existing Problem of Individual Manage Matters Operation in Commercial Bank of China2.1 The development situation of individual money matters operation in commercial bank of ChinaManage money matters operation refers to commercial bank uses professional advantages like various kinds of financial knowledge,professional technique and wide fund credibility and according to clients’financial position and investment requirement,provide clients with professional service activities,such as financial analysis.financial planning,investment counselor and assets management.Recently,as the fast developing economy of china and the accumulating property of citizens,the need of manage money matters operation becomes stronger and stronger.There are several reasons:first of all,when people’s properties accumulate to some degree,they concern more about how to effectively keep and increase the value of their properties.Second,as the pushing on housing,education and medical treatment marketing revolution proceeding,families need the help of financial mechanism service to create a complete risk safeguard mechanism.On the other hand,we have already been in aging stage,thus it has become many people’s real need to accumulate part of their pension through manage money matters.Under thecircumstances.individual money matters operation of commercial bank develops quickly.But according to individual money matters operation situation of every commercial bank.there are still many problems that make it hard to develop individual money matters operation.2.2 The trait of individual money matters operation in commercial bank of ChinaAs the individual money matters operation of commercial bank has just started,financial mechanism and laws and regulations systems are special,so compared to western developed countries,we have our own traits.Fiduciary loan product becomes the 1eader of manage money matters market Recently,invest people pay more attention to the risk situation of product when they choose manage money matters product.At the same time,because the CBRC(china banking regulatory commission) adds its strength to manage money matters operation in commercial bank,the breed structure of manage money matters product changed a lot in general.Since 2009,fiduciary loan product increased largely and become the leader in all kinds of banking manage money matters product for its clear investment, simple structure,various deadline,stable income.Public beneficial and creative product is the value of manage money matters product afoot. During the wenchuan earthquake in 2008,some banks give quickly reflect to the calamity and push out public beneficial and creative manage money matters product.This kind of manage money matters product was themed as benevolent and cares,which greatly widen the developing thought of banking manage money matters operation and validly promote brand value and social image of the bank.3 The Reasons Why We Have Problems in Personal Financial Business in Our National Commercial BanksThe reason why we have so many problems in personal financial business in our national commercial banks is not just because of one single element,but because of many aspects.The reason that we still take separate operation in practice .The policies and regulations.idea of supervision and measures in China still not keep pace with the development of era;we still rely on separate operation and separate management to keep watching to the financial risk.But this kind of operation mode increases thecost of processing personal financial business in commercial banks.and it is hard to make good results.The reason why all the products have the same quality.As it is limited by the idea,the analysis of personal finance business from our commercial banks are not totally correct,there still exists some deficiencies to the research of clients,as a result.nearly all the financial products are the same.The reason why we have a shortage of high—quality financial manager The capability of training finance managers in our country is still undeveloped and the mentality relatively falls behind with developing countries,so most of excellent managers choose to enter foreign banks, and it will be reasonable that the managers couldn’t reach the requirements in national commercial banks.The reason why we are lack of the consciousness of financial management .As we are developing our economy in recent years, it results in a lack of financial culture and financial consciousness.Firstly, people just have some egg money;they can hardly adjust to the life style which adds the finance management into it.Secondly, the influence of traditional concept and shortage of understanding the personal financial business in banks result in the lack of financial consciousness and the deficiency of sense of identity and safety.The reason why we are lake of cultivation Our national commercial banks are limited by system, thinking, technique and objective environment and some influences so that our national commercial banks’s cultivation stagnates, in some high—profited area,we couldn’t keep the pace.And if we don’t solve the problem of lack of cultivation,it is hard for us to complete with foreign banks.4 The Questions Exit in Individual Managing Financial Services in Commercial Bank of ChinaA good financial planner should know everything about a product and have a good knowledge of security, bank,insurance。

银行个人理财战略中英文对照外文翻译文献

银行个人理财战略中英文对照外文翻译文献(文档含英文原文和中文翻译)原文:The Development Status and Strategy Research of Commercial Banks’Personal Financial ManagementBusiness in ChinaAbstract: The personal financial management business in our country is in the initial stage,compared to the developed one in western,there’s still a long way to go,Therefore,the commercial banks in china need to review and study to estimate market direction;build excellence brand image and special services;Increase of innovation;change the products from single to comprehensive;Establish and perfect financial management business’management system in order to promote the development of personal financial business in our management country.Keywords:Commercial banks,Personal financial management,Strategy1 IntroductionThe commercial banks are facing the new situation:the increasing danger in traditional business.the margin of the interest rate’s turning increasingly narrowed and foreign bank’s competition.These banks should think deeply to find why that business develop so slowly and then put forward a feasible plan.The personal financial management business is not only an important carrier for commercial banks to advance Comprehensive management strategy but also a major way of improving Intermediary business income.That business in our country is in the initial stage.compared to the developed one in western,there’s still a long way to go.Therefore.the commercial banks in china need to review and study to estimate market direction;build excellence brand image and special services;Increase of innovation;change the products from single to comprehensive;Establish and perfect financial management business’management system in order to promote the development of personal financial management business in our country.Meanwhile.the commercial banks are facing the new situation:the increasing danger in traditional business.the margin of the interest rate’s turningincreasingly narrowed and foreign bank’s competition.These banks should think deeply to fend why that bus;mess develop so slowly and then put forward a feasible plan.Among all the businesses in commercial banks.personal financial management business has the advantages of huge market capacity,low risk,wide range of business,and stable income.For those advantages the personal financial management business becomes commercial banks’main business and vital profits source.In western developed country,this kind of business almost gets into every family.Its business income has been account for ba nk’s 30%.Compared to the developed one in western.there’s still a long way to go but it has a bright market expectation.However,our country’s personal financial management business is limited by some factors,for instance,the financial legal system,financial supervision system and the development of financial market.As a result.it brings some problems that need to be done while developing rapidly.2 The Development Situation,Trait and Existing Problem of Individual Manage Matters Operation in Commercial Bank of China2.1 The development situation of individual money matters operation in commercial bank of ChinaManage money matters operation refers to commercial bank uses professional advantages like various kinds of financial knowledge,professional technique and wide fund credibility and according to clients’financial position and investment requirement,provide clients with professional service activities,such as financial analysis.financial planning,investment counselor and assets management.Recently,as the fast developing economy of china and the accumulating property of citizens,the need of manage money matters operation becomes stronger and stronger.There are several reasons:first of all,when people’s properties accumulate to some degree,they concern more about how to effectively keep and increase the value of their properties.Second,as the pushing on housing,education and medical treatment marketing revolution proceeding,families need the help of financial mechanism service to create a complete risk safeguard mechanism.On the other hand,we have already been in aging stage,thus it has become many people’s real need to accumulate part of their pension through manage money matters.Under thecircumstances.individual money matters operation of commercial bank develops quickly.But according to individual money matters operation situation of every commercial bank.there are still many problems that make it hard to develop individual money matters operation.2.2 The trait of individual money matters operation in commercial bank of ChinaAs the individual money matters operation of commercial bank has just started,financial mechanism and laws and regulations systems are special,so compared to western developed countries,we have our own traits.Fiduciary loan product becomes the 1eader of manage money matters market Recently,invest people pay more attention to the risk situation of product when they choose manage money matters product.At the same time,because the CBRC(china banking regulatory commission) adds its strength to manage money matters operation in commercial bank,the breed structure of manage money matters product changed a lot in general.Since 2009,fiduciary loan product increased largely and become the leader in all kinds of banking manage money matters product for its clear investment, simple structure,various deadline,stable income.Public beneficial and creative product is the value of manage money matters product afoot. During the wenchuan earthquake in 2008,some banks give quickly reflect to the calamity and push out public beneficial and creative manage money matters product.This kind of manage money matters product was themed as benevolent and cares,which greatly widen the developing thought of banking manage money matters operation and validly promote brand value and social image of the bank.3 The Reasons Why We Have Problems in Personal Financial Business in Our National Commercial BanksThe reason why we have so many problems in personal financial business in our national commercial banks is not just because of one single element,but because of many aspects.The reason that we still take separate operation in practice .The policies and regulations.idea of supervision and measures in China still not keep pace with the development of era;we still rely on separate operation and separate management to keep watching to the financial risk.But this kind of operation mode increases thecost of processing personal financial business in commercial banks.and it is hard to make good results.The reason why all the products have the same quality.As it is limited by the idea,the analysis of personal finance business from our commercial banks are not totally correct,there still exists some deficiencies to the research of clients,as a result.nearly all the financial products are the same.The reason why we have a shortage of high—quality financial manager The capability of training finance managers in our country is still undeveloped and the mentality relatively falls behind with developing countries,so most of excellent managers choose to enter foreign banks, and it will be reasonable that the managers couldn’t reach the requirements in national commercial banks.The reason why we are lack of the consciousness of financial management .As we are developing our economy in recent years, it results in a lack of financial culture and financial consciousness.Firstly, people just have some egg money;they can hardly adjust to the life style which adds the finance management into it.Secondly, the influence of traditional concept and shortage of understanding the personal financial business in banks result in the lack of financial consciousness and the deficiency of sense of identity and safety.The reason why we are lake of cultivation Our national commercial banks are limited by system, thinking, technique and objective environment and some influences so that our national commercial banks’s cultivation stagnates, in some high—profited area,we couldn’t keep the pace.And if we don’t solve the problem of lack of cultivation,it is hard for us to complete with foreign banks.4 The Questions Exit in Individual Managing Financial Services in Commercial Bank of ChinaA good financial planner should know everything about a product and have a good knowledge of security, bank,insurance。

理财的好处英语作文带翻译

理财的好处英语作文带翻译Title: The Benefits of Financial Management。