新个税英文解释 New IIT rate

税务专用英语

税务词汇营业税:business tax or turnover tax消费税:excise tax or consumption tax增值税:value added tax关税:custom duty印花税:stamp tax土地增值税:land appreciation tax or increment tax on land value个人所得税:individual income tax企业所得税:income tax on corporate business外商投资企业所得税:income tax on foreign investment enterprises城市维护建设税:city maintenance construction tax资源税:resource tax房产税:house property tax土地使用税:land use tax车船使用税:operation tax of vehicle and ship耕地占用税:farmland use tax教育费附加:extra charges of education fundsState Administration for Taxation 国家税务总局Yangzhou Taxation Training College of State Administration of Taxation国家税务总局扬州税务进修学院Local Taxation bureau 地方税务局外汇管理局:Foreign Exchange Control Board海关:customs财政局:finance bureau统计局:Statistics Bureau工商行政管理局:Administration of Industry and Commerce出入境检验检疫局:Administration for EntryExit Inspection and Quarantine中国证监会:China Securities Regulatory Commission (CSRS)劳动和社会保障部:Ministry of Labour and Social Securitytax returns filing 纳税申报tax payable 应交税金the assessable period for tax payment 纳税期限the timing of tax liability arising 纳税义务发生时间consolidate reporting 合并申报the local competent tax authority 当地主管税务机关精选文库the outbound business activity 外出经营活动Tax Inspection Report 纳税检查报告tax avoidance 逃税tax evasion 避税tax base 税基refund after collection 先征后退withhold and remit tax 代扣代缴collect and remit tax 代收代缴income from authors remuneration 稿酬所得income from remuneration for personal service 劳务报酬所得income from lease of property 财产租赁所得income from transfer of property 财产转让所得contingent income 偶然所得resident 居民non-resident 非居民tax year 纳税年度temporary trips out of 临时离境flat rate 比例税率withholding income tax 预提税withholding at source 源泉扣缴State Treasury 国库tax preference 税收优惠the first profit-making year 第一个获利年度refund of the income tax paid on the reinvested amount 再投资退税export-oriented enterprise 出口型企业technologically advanced enterprise 先进技术企业Special Economic Zone 经济特区accountant genaral 会计主任account balancde 结平的帐户account bill 帐单account books 帐account classification 帐户分类account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款精选文库account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐accept 受理accounting software 会计核算软件affix 盖章application letter 申请报告apply for reimbursement 申请退税apply for a hearing 申请听证apply for nullifying the tax registration 税务登记注销apply for reimbursement of tax payment 申请退税ask for 征求audit 审核author’s remuneration 稿酬;稿费averment 申辩bill/voucher 票证bulletin 公告bulletin board 公告牌business ID number 企业代码business license 营业执照call one’s number 叫号carry out/enforce/implement 执行check 核对check on the cancellation of the tax return 注销税务登记核查checking the tax returns 审核申报表city property tax 城市房地产税company-owned 公司自有的conduct an investigation/investigate 调查construction contract 建筑工程合同]cconsult; consultation 咨询<consulting service/advisory service 咨询服务contact 联系contract 承包copy 复印;副本deduct 扣除精选文库delay in filing tax returns 延期申报(缴纳)税款describe/explain 说明document 文件;资料examine and approve 审批extend the deadline for filing tax returns 延期税务申报feedback 反馈file tax returns(online) (网上)纳税申报fill out/in 填写foreign-owned enterprise 外资企业hearing 听证ID(identification) 工作证`Identical with the original 与原件一样IIT(Individual income tax) 个人所得税Implementation 稽查执行income 收入;所得inform/tell 告诉information desk 咨询台inspect 稽查inspection notice 稽查通知书instructions 使用说明invoice book(purchase) 发票购领本invoice 发票invoice tax control machine 发票税控机legal person 法人代表letter of settlement for tax inspection 稽查处理决定书list 清单local tax for education 教育地方附加费lunch breakmake a supplementary payment 补缴make one’s debut in handling tax affairs 初次办理涉税事项manuscript 底稿materials of proof 举证材料material 资料modify 修改modify one’s tax return 税务变更登记Nanjing Local Taxation Bureau 南京市地方税务局Notice 告知nullify 注销精选文库office building 办公楼office stationery 办公用品on-the-spot service 上门服务on-the-spot tax inspection 上门稽查opinion 意见original value 原值pay an overdue tax bill 补缴税款pay 缴纳penalty 处罚penalty fee for overdue payment 滞纳金penalty fee 罚款personal contact 面谈post/mail/send sth by mail 邮寄procedure/formality 手续proof material to backup tax returns 税收举证资料purchase 购领real estate 房产receipt 回执;反馈单record 记录reference number 顺序号register outward business administration 外出经营登记relevant materials of proof 举证资料rent 出租reply/answer 答复sell and pay foreign exchange 售付汇service trade 服务业settlement 处理settle 结算show/present 出示special invoice books of service trade 服务业发票stamp 公章submit a written application letter 提供书面申请报告supervision hotline 监督电话tax inspection bureau 稽查局tax inspection permit 税务检查证tax inspection 税务稽查tax law 税法tax officer 办税人精选文库tax payable/tax applicable 应缴税tax payment assessment 纳税评估tax payment receipt 完税凭证tax payment 税款tax rate 税率tax reduction or exemption 减免税tax registration number 纳税登记号tax registration certificate 税务登记证tax registration 税务登记tax related documents 涉税资料tax return/tax bill 税单tax return forms and the acknowledgement of receipt 申报表回执tax returns 纳税申报表tax voucher 凭证the accounting software 会计核算软件the acknowledgement of receipt 送达回证the application for an income refund 收入退还清单the author’s remuneration 稿费the business ID number 企业代码the certificate for outward business administration 外出经营管理证明the certificate for exchange of invoice 换票证the deadline 规定期限the inspection statement/report 检查底稿the legal person 法人代表the letter of statement and averment 陈述申辩书the online web address for filling tax returns 纳税申报网络地址the penalty fee for the overdue tax payment 税款滞纳金the penalty notice 处罚告知书the real estate 房产the registration number of the tax returns 纳税登记号the special invoice of service trade 服务业专用发票the special nationwide special invoice stamp 发票专用章the special nationwide invoice stamp 发票专用章the State Administration of Taxation 国家税务局supervision of taxation 税收监督tax inspection department 税务稽查局tax inspection permit 税务检查证tax officer 办税人员精选文库tax return form 纳税申报表格tax voucher application for the sale and purchase of foreign exchange 售付汇税务凭证申请审批表the use of invoice 发票使用trading contract 购销合同transportation business 运输业under the rate on value method 从价urban house-land tax 城市房地产税V AT(value-added tax, value added tax) 增值税Written application letter 书面申请报告资产负债表:balance sheet 可以不大写b利润表:income statements (or statements of income)利润分配表:retained earnings现金流量表:cash flows。

新个税介绍及简单案例说明修订版

新个税介绍及简单案例说明修订版IBMT standardization office【IBMT5AB-IBMT08-IBMT2C-ZZT18】新个税介绍及简单案例说明新个税法将于2019年1月1日起施行,2018年10月1日起施行最新起征点和税率。

以下是根据相关法规整理的新个税测算的要点,分享给各位同事参考。

一、居民与非居民概念在中国境内有住所,或者无住所而一个纳税年度内在中国境内居住满一百八十三天的个人,为居民个人,其从中国境内和境外取得的所得,依照本法规定缴纳个人所得税。

在中国境内无住所又不居住,或者无住所而一个纳税年度内在中国境内居住不满一百八十三天的个人,为非居民个人,其从中国境内取得的所得,依照本法规定缴纳个人所得税。

居民个人和非居民个人的概念比较二、所得项目的基本分类1.个人所得纳税项目分类根据新法规定,个人所得税应税项目分为9个明细项目,即:工资、薪金所得;劳务报酬所得;稿酬所得;特许权使用费所得;经营所得;利息、股息、红利所得;财产租赁所得;财产转让所得;偶然所得。

根据新个税的计算方式,将个税分为三类:(1)综合所得:具体包括工资、薪金所得;劳务报酬所得;稿酬所得;特许权使用费所得四个项目所得。

(2)经营所得:将经营所得一项实行单独的计算。

(3)特定所得:新法对利息、股息、红利所得;财产租赁所得;财产转让所得;偶然所得四项归类一起,采用比例税率,但没有归集名称,根据其都是针对特定性质的所得项目的特点,简称为特定所得。

2.税率的基本适用(1)综合所得,适用百分之三至百分之四十五的超额累进税率;(2)经营所得,适用百分之五至百分之三十五的超额累进税率;(3)特定所得,适用比例税率,税率为百分之二十。

三、综合所得的计算表新个税法将个人所得税纳税人分为居民个人和非居民个人两大类,且计税有所不同。

1.居民个人居民个人的综合所得,是以自公历1月1日起至12月31日止的每一纳税年度进行计税,并在日常由扣缴义务人按月(如基本的工资薪金等按月发放的个人所得)或者按次(如稿酬等)进行扣缴税款。

个税起征点

个税起征点基本释义personal income tax exemptionindividual income tax threhold双语例句1 提高个税起征点能否实现藏富于民?Will people get benefit from rising tax levy point of IIT?2 珠海现行的个税起征点是多少?Zhuhai months of the current tax threshold is how much?3 提高个税起征点的说法当然也不是空穴来风。

In raising the tax threshold to say, of course, is not groundless.4 只简单调整工资薪金所得起征点,实非个税的全面改革。

Simply adjust the threshold derived from wages and salaries, is not a tax overhaul.5 从这个意义上来说,提高个税起征点,账不能像我这么算。

In this sense, improve tax threshold, so my account can not count.6 由于涉及法律修改,个税起征点的调整将必须经过人大常委会的审议。

Due to legal changes to a tax adjustment of the threshold will be subject to consideration of the NPC Standing Committee.7 近日关于修改《个人所得税法》的消息中,个税起征点的确定令人瞩目。

Recently on the revision of the "law on personal income tax, " the source, a tax threshold for determining spectacular.8 对此,我的看法是,减税势在必行,但个税起征点的提高却不必冀望过高。

税收的单词

税收的单词一、“tax”(税收;征税;税)1. 中文翻译与英语解释- 中文翻译为“税收;征税;税”。

- 英语解释:A sum of money demanded by a government for its support or for specific facilities or services, levied upon incomes, property, sales, etc.(政府为了维持自身运转或提供特定设施与服务而对收入、财产、销售等征收的一笔钱。

)2. 词干(词根)、前缀、后缀的使用情况- “tax”本身是一个词根,来源于拉丁语“taxare”,意思是“评估、估算”。

- 可以加前缀,例如“detax”(免税,这是一个非标准用法,但可以理解为“de - ”表示“去除”,去除税收的意思)。

- 加后缀,“taxation”(名词,税收;征税,“ - ation”是名词后缀,表示行为、状态等);“taxable”(形容词,应纳税的,“ - able”是形容词后缀,表示“可……的”);“taxpayer”(名词,纳税人,“ - payer”表示“支付者”)。

3. 不同词式的造句与翻译- tax(名词)- The government has increased the tax on cigarettes.(政府已经提高了香烟税。

)- 这家公司必须缴纳高额的企业税。

The company has to pay a high corporate tax.- 他们正在抗议新的财产税。

They are protesting against the new property tax.- tax(动词)- The authorities decided to tax luxury goods at a higher rate.(当局决定对奢侈品征收更高的税率。

)- 政府不应该过度征税穷人。

The government should not over - tax the poor.- 他们计划对进口汽车征税。

IIT-filing-return-个人所得税纳税申报表(中英文版)教学文稿

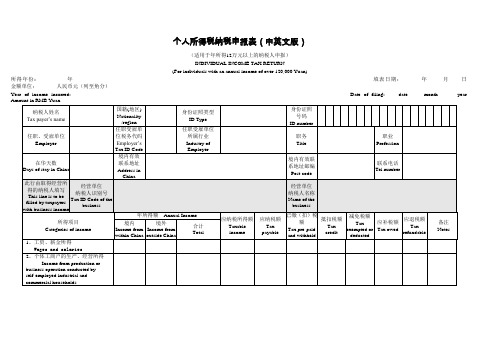

个人所得税纳税申报表(中英文版)(适用于年所得12万元以上的纳税人申报)INDIVIDUAL INCOME TAX RETURN(For individuals with an annual income of over 120,000 Yuan)所得年份: 年填表日期:年月日金额单位:人民币元(列至角分)Year of income incurred: Date of filing: date month year Amount in RMB Yuan章):Signature of responsible tax officer : Filing date: Time: Year/Month/Date Responsible tax offic填表须知一、本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二、负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三、填写本表应当使用中文,也可以同时用中、外两种文字填写。

四、本表各栏的填写说明如下:(一)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职、受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职、受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职、受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

浅析新时期个人所得税纳税筹划外文资料及翻译(可编辑)

浅析新时期个人所得税纳税筹划外文资料及翻译Superficial analysis of the design of new ear personal income taxBy Jody BlazekAbstractWith China's economic development, personal income increased dramatically, followed by personal income tax burden will increase significantly. Personal income tax planning it caused widespread concern. So the premise of how the tax law, through planning, reduce the tax burden, the article introduced in detail the significance of personal income tax planning and the necessity, personal income tax planning major tax-related items.Keywords: Individual income tax; tax planning; significance; necessity; major tax-related itemsWith the economy growing, gradually raise the living standards of our people, the sources and forms of personal income are becoming increasingly diverse, more and more people become personal income taxpayers. Accordingly, revenue from personal income tax in the proportion also showed a rising trend year by year, to maintain the vitalinterests of the perspective of reducing the tax burden, personal income tax planning more and more taxpayers are highly valued. So how to make the taxpayers under the premise of not against the law, reduce the tax burden as much as possible, to gain imum benefit has become an important research content, the personal income tax planning has become increasingly important.The significance of personal income tax planning and the necessity Many taxpayers from the past secretly or unconsciously adopt various methods to reduce their tax burden, development of active tax planning through to reduce the tax burden. However, in some tax planning ideas and knowledge are often opportunistic together. At the same time some people puzzled: "Tax Planning in the premise is not illegal, but the plan itself is not a violation of the spirit of national legislation and tax policy-oriented it? Desirable tax planning it?" In this context, the correct income tax guide taxpayers on tax planning and tax of the economic development of the more important practical significance, great deal of research necessary.1. Personal income tax planning is conducive to long-term development units.2. Helps to reduce the unit's tax expenditures.3. Helps to reduce the individual's own tax evasion, tax evasion and other illegal acts occur, and enhance tax awareness and realizationof tax honesty.Third, personal income tax planning for tax-related itemsPlanning ideas. First of all, develop a reasonable tax avoidance scheme. Is through the study of the current tax law, income of individuals expected in the near future to make the revenue arrangements, through the time and amount of income, payment, and reaches purpose of reducing the amount of nominal income, thus reducing tax level to reduce the tax burden or exempt taxes. Second, take reasonable tax avoidance strategy. Personal income tax planning can be reasonable to consider the following aspects: improving the level of employee benefits and reduce the nominal income; equilibrium level of wage income each month; can deduct the cost of seizing all opportunities and make full use; use of tax incentives.2. The main tax-related project planning application.1 wage and salary income planning. Progressive tax rates from the nine tables can be seen over, because of the wage and salary income is taken over nine progressive tax rate, so the higher the income, the higher the tax rate applicable to the tax burden heavier. In the periphery of each level, the income may be only a difference of a dollar, but the personal income tax borne by the tax burden will be very different. However, by taking some of the legitimate means of planning, can avoid such an unfair place. There are many specific methods, are:Equilibrium income method. Personal income tax with progressiverates usually, if the taxpayer's taxable income the more, the highest marginal tax rate applicable to the higher, so the average taxpayer's income tax rate and effective tax rate may increase. Therefore, the total income of the taxpayer a period of time given the circumstances, its contribution to the income of each tax period should be balanced, not ups and downs, in order to avoid increasing the tax burden of taxpayers. For example: a staff of 1,500 yuan monthly salary, the company usually taken to the payment of wages, end of year performance-based management approach to implement the pay award. Assuming that the end of the year employees 12 month and get a bonus of 6,000 yuan, then the employee's personal income tax to be paid throughout the year as [1500 +6000 - 2000] × 20% - 375 725 dollars. If the company will be 500 yuan per month by year-end awards along with the payment of wages, the wages of employees for 2000 yuan a month, the annual income for tax purposes.Use of employee benefits planning. Tax payable Taxable income × Applicable tax rate - quick deduction. In the file under the conditions of constant tax rates, reducing their income by way of making their use a lower tax rate, while the tax base is also smaller. Approach is feasible and units agreed to change their payment method of wages and salaries, which some of the units to provide the necessary benefits, such enterprises to provide shelter, it is reasonable tax personal income tax effective way. Enterprises can also provide holiday travel allowance,provide staff welfare facilities, free lunches, etc., to offset their wage and salary income.Cost difference between using the standard deduction. Tax law, deduct the cost of wage and salary income amounted to 2,000 yuan, labor income from more than 4,000 yuan a single 20% of the costs incurred. In some cases, the wage and salary income and income from remuneration for separately, and in some cases the wages and salaries combined with the services will save the tax return, and thus its tax planning to have some possibilities.Cases, Lee February 2006 A company from wages and salaries of 1,000 yuan, the unit wage is too low, the same month in the B Lee to find a part-time company achieved income of 5,000 yuan. If Li and B company does not have fixed employment relationship, in accordance with tax law, wage and salary income and income from remuneration for personal income tax should be calculated separately. A company has made from the wages, salaries did not exceed the deduction limit, do not pay taxes. Obtained from the B company taxable amount of remuneration: 5000 × 1 - 20% × 20% 800 yuan, the Wang in February were 800 individual income tax to be paid; if Mr. Lee and the existence of a fixed B Company the employment relationship, the two should be combined by income wage and salary income to pay personal income tax: 5000 +1000- 2000 × 15% - 125 475 million.Clearly, in this case, the use of wage and salary income tax payablecalculated is wise, therefore, Lee B should be signed with a fixed employment contract, will the income from B Company to the way wages and salaries paid to Lee.2 income from remuneration planning. On income from remuneration of a 20% rate applies, but for the case of a one-time implementation of high income plus collection, in effect amounts to three levels of progressive rates. Income from remuneration has its own characteristics, the following for its characteristics, the analysis of tax planning. Number of planning law. With different wage and salary income, income from remuneration for taxation is based on the number of the standard, rather than months, so the number of times to determine the income tax paid, which is critical to planning for the labor income tax return as a factor when the first considerationRemuneration is based on the standard number of times, deducted a fee each time, so that within one month, the number of labor remuneration paid more the more deductible expenses, the tax should be paid less. So when the taxpayers in the provision of services, reasonable arrangements for tax time, the number of monthly remuneration received, you can deduct legal fees many times, reducing the amount of taxable income each month to avoid the higher tax rates apply, so that their net increased.For example: a public listed company of an expert advisory services, according to the contract, each of the listed company of the expertadvisory fees paid 60,000 yuan. If a tax declaration by a person if their taxable income as follows:One-time reporting taxable income 6-6 × 20% 4.8 million Tax payable 4.8 × 20% × 1 +50% 1.44 millionIf it is 3 times per month, every 2 million tax returns, the amount of tax payable as follows:Payable monthly reporting 2 - 2 * 20% 1.6 millionTax payable 1.6 × 20% 0.32 millionMonthly tax payable 0.32 * 3 0.94 millionWhen comparing the two tax saving 1.44-0.94 0.5 millionCosts offset method. That by reducing the nominal income from remuneration in the form of planning, will cost the taxpayers should be replaced by the owners, to achieve the reduction in nominal labor compensation purposes. Wage and salary income conversion method. Through the wage and salary income into income from remuneration, pay personal income tax by labor income, is more conducive to reducing tax expenditures.Example: Mr. Song is a senior engineer, May 2008 to obtain a company income of 63,700 yuan of wages. Song and the company if the existence of a stable employment relationship, according wage and salary income tax, the tax payable 63700-2000 × 35% -6375 15220 yuan. If the Song and the company a stable employment relationship does not exist, this income istaxed according to perjury.Amount of tax payable 63700 × 1-20% × 40% -7000 13384 yuan. If he can save taxes 1,836 yuan.Summary:As China's economic development, the personal income tax impact on our lives will become increasingly large, and its position will become increasingly important. Making tax planning, each taxpayer must be the extent permitted by laws and regulations reasonably expected taxable income, which is the basic premise. On the basis of protection of interests of the taxpayers through the tax planning to imize personal income tax for the improvement and popularity, with significant practical significance.浅析新时期个人所得税纳税筹划By Jody Blazek摘要随着中国经济的发展,个人收入也急剧增加,随之而来的个人所得税负担也就明显加重。

个人所得税培训课件2024更新PPT

个人

公民个人

依法登记为个体工商的公民

个人独资企业投资者

合伙企业自然人合伙人

境内无住所又不居住或者境内无住所居住一年累计不满183天

类型

具体情况

纳税义务

居民纳税人

二者满足其一:1、境 内有住所;2、境内无 住所但居住,一年内累 计满18二者满足其一:1、境 内有住所;2、境内无 住所但居住,一年内累 计满183天

查遗补缺

汇总收支

按年查账

多退少补

计算公式

全部工资薪资税前收入 全部劳务报酬税前收入x (1-20%) 全部特许权使用税前收入x (1-20%)

全部稿酬税前收入x (1-20%) x (1-30%)

每年60000元 三险一金

子女教育支出 继续教育支出 大病医疗支出 住房贷款利息

住房租金收入 赡养老人支出 婴幼儿照护费用

第二章节

个人应知应会点

The individual should know the point

什么是个税

征税对象:个人

偶然的、临时的, 货币、有价证券、

实物

关于”个人“的身份

个人

居民/非居民 纳税人

类型

自然人 个体工商业户 个人融资企业 合伙企业 非居民纳税人 判断标准

住所标准/居住时间 标准

个人自行申报指南

一、实名注册(未注册用户)

1、下载“个人所得税”APP 2、下载完成后打开APP,可选择大厅注册码 注册、人脸识别认证注册。

个人自行申报指南

二、找回密码(已注册用户)

1、 找回密码需进行身份验证,先填写本人注册时的正确的身份证件信息,然后输入随机验证码。 2、完成上述内容,点击页面“下一步” 3、选择“验证方式”,目前有“通过已绑定的手机号码验证”和“通过本人银行卡进行验证“二 选其一。注意:如果选择“通过本人银行卡进行验证”前提是要原先在APP端或WEP端里面添加过 银行卡才可操作。 4、输入“短信验证码”,点击“下一步 5、设置新密码,然后点击“保存”码修改成功。注意:密码规则必须要由大写、小写字数字组合, 必须8位以上。

IIT filing return 个人所得税纳税申报表(中英文版)

个人所得税纳税申报表(中英文版)(适用于年所得12万元以上的纳税人申报)INDIVIDUAL INCOME TAX RETURN(For individuals with an annual income of over 120,000 Yuan)所得年份: 年填表日期:年月日金额单位:人民币元(列至角分)Year of income incurred: Date of filing: date month year Amount in RMB Yuan章):Signature of responsible tax officer : Filing date: Time: Year/Month/Date Responsible tax offic填表须知一、本表根据《中华人民共和国个人所得税法》及其实施条例和《个人所得税自行纳税申报办法(试行)》制定,适用于年所得12万元以上纳税人的年度自行申报。

二、负有纳税义务的个人,可以由本人或者委托他人于纳税年度终了后3个月以内向主管税务机关报送本表。

不能按照规定期限报送本表时,应当在规定的报送期限内提出申请,经当地税务机关批准,可以适当延期。

三、填写本表应当使用中文,也可以同时用中、外两种文字填写。

四、本表各栏的填写说明如下:(一)所得年份和填表日期:申报所得年份:填写纳税人实际取得所得的年度;填表日期,填写纳税人办理纳税申报的实际日期。

(二)身份证照类型:填写纳税人的有效身份证照(居民身份证、军人身份证件、护照、回乡证等)名称。

(三)身份证照号码:填写中国居民纳税人的有效身份证照上的号码。

(四)任职、受雇单位:填写纳税人的任职、受雇单位名称。

纳税人有多个任职、受雇单位时,填写受理申报的税务机关主管的任职、受雇单位。

(五)任职、受雇单位税务代码:填写受理申报的任职、受雇单位在税务机关办理税务登记或者扣缴登记的编码。

(六)任职、受雇单位所属行业:填写受理申报的任职、受雇单位所属的行业。

个人所得税最新法(英文版)

第15章个人所得税法Chapter 15 Individual Income Tax•Who are the individuals liable to Individual Income Tax?•What is the income from sources within China?•What is the income from sources outside China?•What income earned by an individual is subject to Individual Income Tax?•How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?•What does wage, salary income include specifically?•How are salaries and wages assessed for Individual Income Tax payable?•How is the “additional deduction for expenses”regulated for wages and salaries? •How to compute the income tax payable on the bonus income on the year-end in one payment?•How to compute the income tax payable on the income of welfare in kind?•How to compute the income tax payable on the income stock options of employees of enterprises?•How is severance pay taxed?•How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?•What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?•How to calculate the taxable income of individual Industrial and Commercial Households?•What are the rules concerning deductions for Individual Industrial and Commercial Households?•How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?•How do single proprietorship enterprises compute and pay income tax payable on their production and business income?•How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?•How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return from their investment?•How is income from contracted or leased operation of enterprises or institutions assessed for Individual Income Tax?•How is income from remuneration for personal service assessed for Individual Income Tax payable?•How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?•What expenses are not allowed for deductions for Individual Industrial and Commercial Households?•What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?•How to deduct the expenses concerning intangible assets used by Individual Industrial and Commercial Households?•How do Individual Industrial and Commercial Households compute their income tax payable?•How additional income tax is levied on remuneration income that is excessively high at one payment?•How is author’s remuneration income assessed for Individual Income Tax payable? •How is income from royalties assessed for Individual Income Tax payable?•How is income from lease of property assessed for Individual Income Tax payable? •How is income from transfer of property assessed for Individual Income Tax payable?•How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?•What do the interest, dividend, bonus, contingent income and/ or other income include specifically?•How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?•How to compute the income tax payable on income derived by two individuals or more together?•How is donation income assessed for Individual Income Tax payable?•How to compute the income tax payable in case that the employers bear the Individual Income Tax for the taxpayers?•How is income derived from sources outside China assessed for Individual Income Tax payable?•What are the main exemptions for Individual Income Tax?•What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State?•What are the main reductions for Individual Income Tax?•What are the rules concerning the mode, time and places for Individual Income Tax payment?•How to report and pay income tax on wages and salaries income?•How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?•How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?•How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?•How to report and pay income tax on income earned by taxpayers from sources outside China?Example1 British professor Henry came to China at invitation for teaching of one year. During that period , he left China twice for business trip and vocation for respectively 15 days and 30 days.According to Chinese tax law, the two leaves were temporary absence from China and each leave was not over 30 days and the accumulative time period was less than 90 days. Therefore ,Henry resided in China for one full year in one tax year, he became resident taxpayer of Chinese Individual Income Tax.Example2 One clerk Mr. Liu has its monthly salary of 2400 yuan, bonus of 700 yuan, other taxable allowances of 500 yuan and the deductible social insurance expenses of 600 yuan. Try to compute the Individual Income Tax payable.Taxable income of the month = 2400 yuan + 700 yuan + 500 yuan–2000 yuan–600 yuan = 1000 yuanTax payable for the month = 1000 yuan ×10% - 25 yuan = 75 yuanExample3 Mr. Jiang earns wage,bonus of 2000 yuan to 3000 yuan each month and has paid the income tax already. At the year end,he obtains one lump-sum bonus of 9000 yuan.Try to compute the income tax payable.9600 yuan ÷12 = 800 yuanThe applicable tax rats is 10% and the quick deduction is 25 yuanThe income tax payable = 9600 yuan ×10% - 25 yuan = 935 yuanExample4 Mr. Lin ears wage and salary of 1900 yuan each month .At the year end, he gets one lump-sum bonus of 2500 yuan.Try to compute his income tax payable.[2500 yuan — (2000 yuan—1900 yuan)]÷12 = 200 yuanThe applicable tax rats is 5% and qiuck deduction is 0.Mr. Lin’s income tax payable = [2500 yuan —(2000 yuan —1900 yuan)]×5%= 120 yuanExample5 One Individual Industrial Household Mr. Qian has revenue of 1,000,000 yuan from business operation for the tax year. The cost and expenses are 800,000 yuan. Try to compute the income tax payable by Mr. Qian.Taxable income = 1,000,000 yuan - 800,000 yuan = 200,000 yuanIndividdual Income Tax payable = 200,000 yuan ×35% - 6750 yuan = 63,250 yuanExample6 One contractor Mr. Huang has derived 100,000 yuan from contracted operation. The deductible expenses allowed are 24,000 yuan. Try to compute the income tax payable.Annual taxable income = 100,000 yuan - 24,000 yuan = 76,000 yuanAnnual income tax payable = 76,000 yuan ×35% - 6750 yuan = 19850 yuanExample7 One engineer Mr. Zhao has received the payment of 50,000 yuan from Company A for designing and at the mean time received a payment of 3000 yuan from company B for advisory services. Try to compute the Individual Income Tax payable of Mr. Zhao.a. The income tax payable for the payment of designing services = 50,000 yuan ×(1 –20%)×30% - 2000 yuan = 10,000 yuanb. The income tax payable for the payment of advisory services = (3000 yuan –800 yuan) ×20% = 440 yuanc. The total income tax payable: 10,000 yuan + 440 yuan = 10,440 yuanExample8 Actor Zhao got remuneration of 60,000 yuan for one performance. The performing company borne Individual Income Tax for him. Try to the tax payable .Taxable incom = (60,000 yuan –7000 yuan)×(1 – 20%)÷[1 – 40%×(1 –20%)] = 62352.94 yuanTax payable = 62352.94 yuan ×40% - 7000 yuan = 17941.18 yuanExample9 One auther Mr. Zhou receives one payment for remuneration of 20,000 yuan on his work. Try to compute the tax payable.Taxable income = 20,000 yuan ×(1–20%) = 16,000 yuanThe statutory income tax payable = 16,000 yuan ×20% = 3,200 yuanThe statutory tax reduction amount = 3,200 yuan ×30% = 960 yuanThe actual Individual Income Tax payable = 3,200 yuan–960 yuan = 2,240 yuanExample10 Professor Li provides the use right of his patent to one company and receives one payment of 100,000 yuan. Try to calculated the incom tax payable.Taxable income = 100,000 yuan ×(1–20%)=80,000 yuanIndividual Income Tax payable = 80,000 yuan ×20% = 16,000 yuanExample11 One citizen Mr. Gu receives dividends of 6,000 yuan from the listed company in one payment. Try to calculated the income tax payable.Income tax payable = 6,000 yuan ×50%×20% = 600 yuanExample12 Some one leases his house to other person for business operation and receives house rental income of 6,500 yuan for the current month . The expenses of taxes, Educational Surcharge and repaining expenses are 1,500 yuan. Try to compute the amount of Individual Income Tax payable.Taxable income = (6,500 yuan–1,500 yuan)×(1–20%) = 4,000 yuanAmount of tax payable = 4,000 yuan ×20% = 800 yuanExample13 Mr. Fang sells a house with the original value of 200,000 yuan and receives 400,000 yuan for the sale. The deductible tax paid related to the sale and the expenses are 100,000 yuan. Try to compute the income tax payable.Taxable income = 400,000 yuan –200,000 yuan –100,000 yuan = 100,000 yuanIncome tax payable = 100,000 yuan ×20% = 20,000 yuanExample14 One citizen Mr. Cai won 100,000 yuan from social welfare lottery. Try to calculate the income tax payable .Tax payable = 100,000 yuan ×20% = 20,000 yuan例题15 某纳税人在同一纳税年度,从A、B两国取得应税收入,其中:在A国一公司任职,取得工资、薪金收入69600元(平均每月5800元),因提供一项专利技术使用权,一次取得特许权使用费收入30000元,该两项收入在A国缴纳个人所得税5200元;因在B国出版著作获得稿酬收入15000元,并在B国缴纳该项收入的个人所得税1720元。

《个人所得税新解》课件

减征个人所得税的优惠政策

对在中国境内无住所的个人,其在中国境内工作期间 取得的由中国境内企业或个人雇主支付和由中国境外 企业或个人雇主支付的工资薪金所得均有不同的计算 方法。

单击此处添加正文,文字是您思想的提一一二三四五 六七八九一二三四五六七八九一二三四五六七八九文 ,单击此处添加正文,文字是您思想的提炼,为了最 终呈现发布的良好效果单击此4*25}

入者的税率。

引入专项扣除

根据居民的生活成本和 负担情况,引入专项扣 除,降低居民的实际税

负。

加强税收征管

加强个人所得税的税收 征管,打击偷税漏税行

为,确保税收公平。

感谢您的观看

THANKS

提高税收效率

改革个人所得税制度,简 化税制,降低税收成本, 提高税收效率。

适应经济发展

随着经济发展和收入水平 的提高,个人所得税的起 征点和税率需要进行调整 ,以适应经济发展。

个人所得税改革的方向和目标

降低中低收入者的税负

01

通过提高起征点、降低税率等方式,减轻中低收入者的税负。

加大对高收入者的税收调节力度

减征个人所得税的优惠政策

• 在中国境内的外商投资企业和外国企业中工作的外籍人员,应聘在中国境内的企业、事业单位、社会团体、国家机关中工 作的外籍专家,在中国境内有住所而在中国境外任职或者受雇取得工资、薪金所得的个人,国务院财政、税务主管部门确 定的其他人员,在1个纳税年度中,一次所得畸高的,按应纳税所得额确定征税,实行按月或按次分项计算纳税义务人应纳 税额,并根据分项所得与最高月工资薪金收入限额的比例确定各项所得一次应纳个人所得税的额度。

01

02

03

查账征收

纳税人自行申报应税所得 ,税务机关核定应纳税所 得额。

个税汇算清缴相关英语

个税汇算清缴相关英语

English:

Individual income tax final settlement refers to the process of reconciling the annual income, deducting allowable deductions and calculating the tax payable or refundable for the whole year. It usually takes place at the end of the tax year or when an individual terminates their employment or leaves China. The final settlement is an important step in the individual income tax process and must be completed accurately and in a timely manner to ensure compliance with tax laws.

中文翻译:

个人所得税的最终结算是指调节全年收入、扣除允许的扣除项目并计算整年的应纳税额或可退税额的过程。

通常在税年结束时或个人终止就业或离开中国时进行。

最终结算是个人所得税流程中的重要步骤,必须准确并及时完成,以确保遵守税法。

新《企业所得税法》变化解读(Interpretation of new enterprise income tax law change)

新《企业所得税法》变化解读(Interpretation of new enterpriseincome tax law change)One of the major amendments to draft the law:Of concern, after 10 years of motion in the enterprise income tax law of People's Republic of China revised several times during the session (hereinafter referred to as the "new law") will be officially implemented in January 1, 2008. The emphasis is on the comparison between the old and the new terms, and the following are the following: the content of the amendment and its implications for practice.A total of eight chapters, sixty articles of corporate income tax law, and then submitted to the people's Congress at the time of the draft comparison, in the layout of the text has been greatly modified and changed. The number of chapters and the layout of the "three minus two points" adjustment, the terms of the "delete seven points, two" changes.Cut out the three chapters of the original independent "income", "deduction" and "asset tax treatment", and decompose the taxable income and taxable amount into independent two chapters. To become now the "General Provisions", "taxable income", "tax payable", "tax" and "withholding", "special tax adjustments", "collection and management" and "Supplementary Provisions" of eight parts.The provisions of the amendment are listed and analyzed as follows: (1) fifth: the calculation of taxable income should be based on the principle of accrual basis. This article is from(94) financial law document No. third. Besides the accrual basis, the principle of accounting includes the principle of dividing capital expenditure and income expenditure. In the calculation of taxable income, the accrual basis is not the general principle, nor the only principle. (two) ninth: the processing enterprises of large-scale machinery and equipment, ship manufacturing, and engaged in construction, installation, assembly engineering or business services, duration across the tax year, the tax year shall be in accordance with the progress of the project or the amount of work completed to determine income. This provision is still derived from the document of the specified number. First of all, this is a clause about the time of tax payment for labor income. It is not a direction to establish the taxable income from the legal level. But the scope and types of taxable income listed in the enterprise income tax law are many. It will be a smaller one written in French practice, not only is too one-sided and care for this and lose that and it is easy to fantastic. (three) twenty-fifth: the calculation formula for the taxable amount of enterprise income tax is: tax payable = tax payable amount * applicable tax rate - tax relief - allowable tax credits. The deletion of this clause may have at least two aspects: one is not in conformity with the general expression habit of French; the other is that the expression of oneself is not accurate; two. (four) thirteenth: all assets of an enterprise include fixed assets, intangible assets, long-term expenses to be amortized, investment assets, inventories, etc., and are usually priced at historical cost. The prototype of this article comes from document [2000]84 of national tax administration. Although the tax law may also allow inconsistent with the accounting system and standards, but so to face the legal provisions, the relevant provisionsof a will and level, legal effectiveness than the accounting system of the "fighting", two is already with the reality and the future of the assets accounting measurement principles conflict. (five) article fourteenth: when the assets of the enterprise reorganization are recognized as gains or losses, the relevant assets shall be determined according to the value of the re confirmation.This article comes from the national tax code No. [1997]97 and is related to the order No. sixth of the State Administration of taxation. But the concept of "enterprise reorganization" mentioned at first is very vague, and it is also a complicated problem. Because of the reform of the enterprise, the tax problem is not only phased, but also difficult to regulate and clear a lot of problems through the law. (six) twenty-second: in addition to the twenty-sixth article of this law, enterprise income tax should be calculated formula of taxable income for the taxable income of a total income of a non taxable income tax income deduction allowed to compensate for losses of the previous year. The greatest deficiency of this should be similar to the analysis of (three) mentioned above. (seven) article sixty-second: if the provisions of the existing laws and administrative regulations concerning the enterprise income tax are inconsistent with the provisions of this law, they shall be implemented in accordance with the provisions of this law. Retaining this article means preserving the bureaucratic style of "habitual action". Since new laws have been enacted, it is tantamount to denying what is contrary to the new law.The so-called "two points", that is, a draft of the CentralPlains to express a tax rate terms are divided into the current fourth and twenty-eighth.The revision on the substance and the changes in the following ten aspects: (1) the most striking additions "in compliance with the conditions of the environmental protection, energy and water saving project income" and "eligible technology transfer income two to enjoy the enterprise income tax exemption or reduction projects; (2) new the country needs to focus on supporting high-tech enterprises, reduced to 15% a preferential tax rate; (3) the public welfare donation for the deduction of two percentage points. (4) the abolition of the "business organizations within the enterprise between pay rents and royalties, interest payments between business organizations and non bank within the enterprise and between enterprises pay management fees shall not be stipulated in the tax deduction; (5) the enterprise will transfer the assets of" transfer costs "out in outside the scope of the tax deduction will be unified; (6) involved" investors to pay the income from equity investment "was renamed" such as dividend and bonus paid to the investors equity investment gains in the draft." (7) due to the adjustment of tax and tax levied "additional fines" approach to the "additional interest"; (8) remove the enterprise income tax calculated said; (9) the autonomous prefectures and autonomous counties, reduction or exemption of enterprise income tax authority; (10) in the "processing the part exceeding the limit of tax credit", the deletion of the original draft of current "no credit, nor as expense deduction".Two: the change of taxpayer's definition and its influenceComparing the new law with the enterprise income tax regulations (hereinafter referred to as the regulations), which neither has any sections nor only 20 clauses, is quite a contrast. Realization is a major change to the taxpayers of enterprise income tax.The definition of taxpayer has realized "four unification"". First, the internal and external tax system is unified; two, the tax treatment between domestic capital is unified. The unification and merger of two sets of internal and external income tax systems are well known. But the other little concern is that the new law has abolished financial and insurance companies' corporate income taxes,The provisions in accordance with the relevant provisions (article eighteenth of the Ordinance). That is, the new law is no longer allowed to be treated separately because of the different accounting systems implemented; three, it unifies the classification of taxpayers. The new law will unify the total income of different types of enterprise income tax payers, which is defined as the difference between resident taxpayers and non resident taxpayers; four, it is consistent with the definition mechanism of individual income tax payers. The implementation of corporate tax system is the direction of the reform of enterprise income tax system. Therefore, the provisions of "independent economic accounting" as the standard for the determination of taxpayers in the current domestic tax law have been abolished. The concept of "resident enterprise" and "non resident enterprise" are introduced. The measures for combining the standards of registration place andthe standards of the actual management institution have been put into effect. And so on, not only in line with international practice, but also in line with the needs of economic globalization.These unified and normative, in the collection and management practice level, in addition to the end of the definition and division of domestic and foreign enterprises, in the practice of corporate income tax, it also has the following practical significance:(1) abolishing the "three conditions" can solve the dispute between taxpayers. The current regulations on the definition of corporate income tax obligations on the expression of, one hand tied the use of "enterprise", "organization" two terms, on the one hand, the examples of the practice, the taxpayer of enterprise income tax to determine the hidden danger. Therefore, in addition to standard regulations in the rules to separate accounting provisions of the "three conditions" (refers to the taxpayer and have opened in the bank settlement account; establish independent books and prepare financial statements; independently calculated the profit and loss conditions of enterprises or organizations). For this approach, the new law first did not simply make "organization" pens, but instead added it to "other revenue taking" organizations. The reason is simple. Second, there is no list of the types of firms. The author believes that bread here contains two levels of meaning. First of all, the enterprise income tax law should be bound by the enterprise and the company law and the relevant laws and regulations of the enterprise content and denotation consistent. Even in the broad sense of the enterprise, it isnot defined by the tax law. The tax law is not likely to give an exhaustive description of the form or nature of an enterprise. Secondly, since it is called "enterprise", we should agree that it has independent accounting or is regarded as independent accounting. That is, as long as they belong to lawfully established enterprises or other organizations that obtain income, they should be included in the scope of the enterprise income tax taxpayers. As for the enumerated Guoshuihan [1998]677 document in the form or the phenomenon does not have "three conditions", has no need to spend effort in that, for enterprises, mainly to deal with the tax authorities should adopt different collection methods.(two) the "new standard" can end the dispute over outstanding tax affairs. Here refers to the enterprise organization change is mainly for China in the special period for enterprises that relatively frequent problems of merger, division and leasing business involving taxpayer. For enterprises such as the national tax administration [1998]97 and the national tax document [1997]8, the merged and retained enterprises, the merged enterprises and the enterprises established after the separation are separately stated,And all or part of the lease and the lease business, the future of whether it is the enterprise income tax taxpayers only two standards. That is, the standard of registration place and the standard of the actual management institution". That is to say, no matter how the enterprise change in the organizational form, as long as there is in the change after the enterprise is set up in China Chinese territory in accordance with laws and regulations, or a foreign (regional) law was established butthe actual enterprise management institutions in the territory of China, belong to our resident enterprises. Enterprise income tax shall be paid in accordance with the law. Whether or not the registration is made separately and whether the actual management organization has changed or not is the basic criterion for paying or not paying the enterprise income tax after the change of the form or mode of operation of the enterprise mentioned above. That is not to be registered and the original enterprise should continue to fulfill all of the obligations of corporate income tax; for re registration and re registration of the enterprise registered enterprise for enterprise income tax. It is not difficult to deal with the so-called "outstanding tax affairs" after the taxpayer has been appointed from the legal principle".(three) make clear the principle that "general tax shall not be consolidated", and resolve the dispute over the subject of Taxation of the enterprise income tax in the group. In the ninth chapter of the new law, the three chapter, "fifty-five chapters" and "fifty-sixth articles", are used in the chapter of "collection and management", which makes clear rules for the subject of income tax including group enterprises, including fifty-fourth items. That is, the resident enterprise set up the business institutions does not have the qualifications of a legal person in China territory, and non resident enterprises in China China set up two or more than two agencies and offices shall, after the examination and approval or can be aggregated to calculate and pay enterprise income tax, and other non regulations between enterprises (State Department), shall not be subject to enterprise income tax.(four) to supplement the conditional restriction of "obtaining income", which can appease the dispute of tax payment among other organizations. The new refinement as "other income" and the revision of sole proprietorship enterprises and partnership enterprises are excluded, to identify social organizations and institutions, intermediary organizations and industry associations is to become the corporate income tax taxpayers to provide a ruler. Of course, the "income" here should be combined with the sixth and seven of the new laws.Three: the tax rate has been reduced, reduced and reduced, which can prevent malicious tax avoidanceThe new tax rate, compared with the current tax law, is five smaller in number. That is to say, the income tax rates of current domestic and foreign enterprises are both 33%. 24%, the implementation of the preferential tax rate of 15% and the domestic profit enterprises are carried out respectively 27%, 18% preferential care for some special areas of foreign enterprise unified multi file rate coexistence is reduced, combined and reduced to 25%, 20% and 15%. And given different nature and significance. 25% is the basic tax rate of enterprise income tax, 20% is the limited tax rate, and the 15% is preferential tax rate. Reduced nominal tax rate, in addition to conducive to fair competition, but also effectively put an end to the use of "tax rate difference" to steal, flee, tax avoidance of the black hole. Specific performance is as follows: first, basically can dispel the "false foreign capital" really "domestic capital" motivation; two is to eradicate in the current period before tax income to do the hidden dangers.The current domestic profit enterprises are the implementation of 27%, 18% of the second rate and "take care of the year on business losses can be offset by the year income, tax shall be determined according to the amount of income after the losses, the number of enterprises to avoid" high rate "and" low tax "in mind.Number four: high density, generous revision of taxable income and income taxThe taxable income tax and the income tax amount have the "sub core" status and function for any tax subject to income tax. The size of the amount of income tax taxpayers paid to the state enterprises, in addition to the "core" of "tax on total income" and "non taxable income" and "expenditure" and "deduction" base elements of man-made or expanded or reduced to the provisions. In this regard, the new law shows the characteristics of high-density increase and big revision.The increase in density is reflected in the terms of the new law, the amount of added information, and the capacity of the information contained. The new law adds forty clauses to the bill. Among them, the provisions of the taxable income, the hard increase in terms of twelve. Both the absolute quantity of the increase and the quantity of the original clause or the total number of articles of the new law are among the best. The terms are entirely new are as follows: (1) increase the tax revenue concept and object (seventh, funding, according to collect and incorporated into the financial management of administrative fees, government funds, the provisions of the State Council and other non taxable income). (2) a supplement to the pre taxdeduction of "expenditure" principle (article eighth: enterprise of actual income and relevant and reasonable expenses, including the costs, expenses, taxes, losses and other expenses, granted when calculating the taxable income amount deducted). (3) specification of the charitable donation title and unified its pre tax deduction rate (ninth, charitable donations incurred by enterprises within 12% of the total annual profit, is permitted to be deducted). (4) add six new clauses to unify and standardize the provisions concerning tax treatment of assets in the relevant administrative regulations and normative documents, and raise them to the level of the law. Such as: eleventh, in calculating taxable income, enterprises in accordance with the provisions of the depreciation of fixed assets, may be deducted. Not including the calculation of fixed assets depreciation, housing, outside the building is not put into use; fixed assets under operating leases; fixed assets leased by means of financing lease; has been in full from the depreciation of fixed assets still in use; fixed assets that are irrelevant to business activities; separate valuation as fixed assets recorded in the land; the calculation of depreciation of fixed assets shall not be deducted; the twelfth, when calculating the taxable income amount, the amortization of intangible assets of enterprises in accordance with the provisions of the calculation, the deductible. No amortized expense calculation of intangible assets: self development expenditure has be deducted from the taxable income of the intangible assets in the calculation; goodwill; irrelevant to business activities or other intangible assets; intangible assets amortization expense deduction; and thirteenth,For the long-term prepaid expenses project in accordance withthe provisions of amortization deduction four: expenditures for rebuilding fixed assets depreciation in full; the rebuilding of a rented fixed asset expenditures; heavy repair expenses of fixed assets; the other shall be treated aslong-term deferred expenses; the fourteenth, the assets of foreign investment enterprises in the cost calculation when the amount of taxable income shall not be deducted; the fifteenth, using or selling stock, in accordance with the provisions of the calculation of inventory cost, to be deducted from the taxable income; the sixteenth, the transfer of the net assets of enterprises, to the taxable income deduction. (5) the loss of newly added overseas business institutions shall not be deducted from the profits of the domestic business institutions (seventeenth articles). (6) an increase of non resident enterprises in the amount of taxable income in terms of the scope of the project (nineteenth, the amount of taxable income includes dividends, bonuses and other equity investment income and interest, rents and royalties, the total income taxable income; methods according to the provisions of the preceding two items to transfer property income, the total income after the deduction of the net value of the property as taxable income; other income calculation). (12) grant the authority of the Department of Finance and taxation of the State Council in formulating the specific scope and standards of income and deductions, and the specific measures for the tax treatment of assets (Twentieth articles).The big revision is reflected in the rewriting of the four terms relating to the original column: the first amendment is the new law, giving the true explanation of the amount of tax payable. Expressed as a formula: tax payable = total income - non taxableincome - tax-free income - amounts deducted - allowable annual loss amount for the previous year. The term "total amount of income minus the amount of deductible items" as defined in the column is the statement that the taxable income is clearly not justified. The second amendment is to supplement, decompose and standardize the scope and content of the total income. One is to increase the total income including "monetary and non monetary form to obtain income from all sources"; two is the production, operating income is divided into income sales of goods and provide labor income of two, corresponding to the value-added tax and business tax; the three is the "rental income" and the "dividend income" were renamed the "rental income" and "dividends, bonuses and other equity investment income; four is the new" donations income "of A. Retained the original single row of "transfer of property income", "royalties income", "interest income" and other income. The third amendment is a significant change in projects that cannot be deducted before tax. Embodied in the "three increase", "two" and "three removed". Increase the "investors to pay the dividends, bonuses and other equity investment proceeds", "enterprise income tax" and "unverified reserve spending" three projects "; the original fines for illegal business operations and the confiscation of property loss" and "the tax arrears, penalties and fines of two integration is divided into" tax payment "and" fines, fines and confiscation of property loss "; from" capital expenditure "and" intangible assets, the development expenditure "and" losses due to natural disasters or accidents are part of the compensation of "three types of expenditure.In addition, the original "more than the state allows to deductpublic welfare, relief donations, and non public, relief donations" expression, unified specification attributed to the "Ninth provisions of this law," other than donations". There are only two pre tax deductions for sponsorship expenditure and other expenses not related to income. The project shall not be deducted the terms while still is eight, the content has changed a lot. The fourth amendment is reflected in the handling of losses arising from the tax year. On the one hand, the new law defines the position of "allowing losses to be carried forward". If it is not allowed to carry over the losses, how can we make up for it? On the one hand with the longest limit node in turn instead to make up for the said limit. Such amendments not only conform to the actual situation, but also eliminate the problem of inadequate expression of the original regulations.There are only three terms for the taxable income. Among them, twenty-second of the taxable income of the conceptual expression, compared with the regulations, belongs to the new clause. Articles twenty-third and twenty-fourth shall be subject to the revision of the original regulation twelfth. For the treatment of income tax paid from overseas income, the new law first changes "deducted" into "credit"". More logical. Secondly, to exceed the prescribed limit of tax credit part first clear: in the following five years, each year the limit of tax credit that should balance the tax credits to offset. At the same time, take the list of specified objects can enjoy the credits, including resident enterprises from Chinese overseas taxable income and non resident enterprises in the territory of Chinese establishments or places, have occurred in Chinese overseas but with the agency, places the taxable income. Third, the "resident enterprise as an example from theforeign enterprises directly or indirectly controlled by the share from Chinese overseas dividends, bonuses and other equity investment income, with a separate clause (twenty-fourth) to be clear. That is, the premise that the overseas income tax may be exempted is that the income tax has been paid abroad. Otherwise, we can not enjoy the twenty-third stipulated credit policy.。

个人利息所得税

中华人民共和国主席令

第八十五号

《全国人民代表大会常务委员会关于修改〈中华人民共和国个人所得税法〉的决定》已由中华人民共和国第 十届全国人民代表大会常务委员会第三十一次会议于2007年12月29日通过,现予公布,自2008年3月1日起施行。

中华人民共和国主席

2007年12月29日

中华人民共和国个人所得税法

起征调整

十届全国人大常委会第三十一次会议于2007年12月29日表决通过了关于修改个人所得税法的决定。根据决定, 2008年税率

个人所得税根据不同的征税项目,分别规定了三种不同的税率:

1.工资、薪金所得,适用9级超额累进税率,按月应纳税所得额计算征税。该税率按个人月工资、薪金应税 所得额划分级距,最高一级为45%,最低一级为5%,共9级。

英文名称

personal income tax

概念诠释

个人所得税是调整征税机关与自然人(居民、非居民人)之间在个人所得税的征纳与管理过程中所发生的社 会关系的法律规范的总称。个人所得税法,就是有关个人的所得税的法律规定。

发展历程

国家对本国公民、居住在本国境内的个人的所得和境外个人来源于本国的所得征收的一种所得税。在有些国 家,个人所得税是主体税种,在财政收入中占较大比重,对经济亦有较大影响。

中华人民共和国第十届全国人民代表大会常务委员会第十八次会议于2005年10月27日通过《全国人民代表大 会常务委员会关于修改〈中华人民共和国个人所得税法〉的决定》,自2006年1月1日起施行。

纳税对象

我国个人所得税的纳税义务人是在中国境内居住有所得的人,以及不在中国境内居住而从中国境内取得所得 的个人,包括中国国内公民,在华取得所得的外籍人员和港、澳、台同胞。

个人利息所得税 (一)居民纳税义务人 在中国境内有所住所,或者无住所而在境内居住满1年的个人,是居民纳税义务人,应当承担无限纳税义务, 即就其在中国境内和境外取得的所得,依法缴纳个人所得税。 (二)非居民纳税义务人 在中国境内无住所又不居住或者无住所而在境内居住不满一年的个人,是非居民纳税义务人,承担有限纳税 义务,仅就其从中国境内取得的所得,依法缴纳个人所得税。