Chapter_04________The Value of Common Stocks

Chapter 04 Channels of Distribution

Limited-function wholesalers:

Rack Jobbers/Rack merchandisers 货架批 发商add non-food lines to grocery stocks Cash and Carry Wholesalers 付款提货批发 商serve small groceries and other stores that buy in

bulky:庞大的

5

工商导论· 第四章 分销渠道

Common Channels of Distribution

Retailers 零售商 intermediaries who sell goods or

services to consumers and represent the final link between producers and end-users. Store retailing includes:

工商导论· 第四章 分销渠道

11

Textual Analysis-7

They earn commissions on their own sales and they also create commissions for the “upliners” who recruited them. In turn, they receive commissions from any “downliners” they recruit to sell. When you have hundreds of downliners, the commissions can be quite sizable. (p35) 他们根据他们的销售量提成,他们给录用他们的上线 交佣金。相反,他们可以从他们录用的下线提取佣金。 当你有上百个下线,佣金可是相当可观的。

Chapter 4 Comparison and Contrast

in spite of /despite 尽管, 不管 conversely 相反地 differ from 和…不同 … to the contrary 相反 的… even though/if 即使 yet 还,仍旧,依然 in contrast to 和…形成对 比 anyway/anyhow 总之,无 论如何

A Special form of comparison — analogy Analogy is tracing a striking likeness between unlike things. Electricity is transferred from one place to another in much the same manner as water. A water pipe performs the same function as a length of wire. The pipe carries water to its point of use in the same manner as wire carries electricity to its point of use. A blown fuse(熔断的保险丝 )results from the same thing as a burst water pipe. Both give out due to extreme pressure applied to the walls of the carrier. A switch is to electricity what a faucet (水龙头)is to water. Both of them control the flow of the substance. Since electricity and water have some common properties, understanding the job of the plumber will help understanding the work of the electrician.

简明教程Chapter 4

NP=noun phrase AP=adjective phrase VP=verb phrase PP=preposition phrase S=sentence or clause

Bracketing

• Bracketing is not as common in use, but it is an economic notation in representing the constituent/phrase structure of a grammatical unit.

2.4 Coordination and Subordination

• Endocentric constructions fall into two main types, depending on the relation between constituents:

Coordination

• Coordination is a common syntactic pattern in English and other languages formed by grouping together two or more categories of the same type with the help of a conjunction such as and, but and or .

1.1 Relations of Position

• For language to fulfill its communicative function, it must have a way to mark the grammatical roles of the various phrases that can occur in a clause. • The boy kicked the ball NP1 NP2 Subject Object

chapter_two_The_Political_system_of_America

the head of each department is the Secretary. There are the departments of State, Treasury, Defense, Justice, Interior, Agriculture, Commerce, Labor, Health and Human Resources, Housing and Urban Development, Transportation, Energy, and

Created: November 15, 1777 Ratified: March 1, 1781 Authors: Continental Congress Signers: Continental Congress Purpose: Constitution for the United States, later replaced by the creation of the current United States Constitution

3. Bill of Rights

It is the first 10 amendments to the U.S. Constitution,

confirming the fundamental rights of American citizens. The new United States of America adopted them on December 15, 1791. These amendments limit the powers of the federal government, protecting the rights of all citizens, residents and visitors on United States territory.

国际商务习题

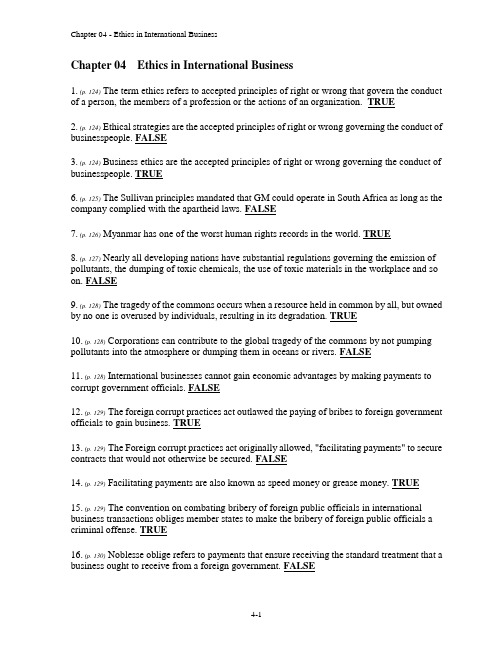

Chapter 04 Ethics in International Business1. (p. 124) The term ethics refers to accepted principles of right or wrong that govern the conduct of a person, the members of a profession or the actions of an organization. TRUE2. (p. 124) Ethical strategies are the accepted principles of right or wrong governing the conduct of businesspeople. FALSE3. (p. 124) Business ethics are the accepted principles of right or wrong governing the conduct of businesspeople. TRUE6. (p. 125) The Sullivan principles mandated that GM could operate in South Africa as long as the company complied with the apartheid laws. FALSE7. (p. 126) Myanmar has one of the worst human rights records in the world. TRUE8. (p. 127) Nearly all developing nations have substantial regulations governing the emission of pollutants, the dumping of toxic chemicals, the use of toxic materials in the workplace and so on. FALSE9. (p. 128) The tragedy of the commons occurs when a resource held in common by all, but owned by no one is overused by individuals, resulting in its degradation. TRUE10. (p. 128) Corporations can contribute to the global tragedy of the commons by not pumping pollutants into the atmosphere or dumping them in oceans or rivers. FALSE11. (p. 128) International businesses cannot gain economic advantages by making payments to corrupt government officials. FALSE12. (p. 129) The foreign corrupt practices act outlawed the paying of bribes to foreign government officials to gain business. TRUE13. (p. 129) The Foreign corrupt practices act originally allowed, "facilitating payments" to secure contracts that would not otherwise be secured. FALSE14. (p. 129) Facilitating payments are also known as speed money or grease money. TRUE15. (p. 129) The convention on combating bribery of foreign public officials in international business transactions obliges member states to make the bribery of foreign public officials a criminal offense. TRUE16. (p. 130) Noblesse oblige refers to payments that ensure receiving the standard treatment that a business ought to receive from a foreign government. FALSE17. (p. 130) Social responsibility refers to the idea that businesspeople should consider the social consequences of economic actions when making business decisions and that there should be a presumption in favor of decisions that have both good economic and social consequences. TRUE19. (p. 131) The ethical obligations of a multinational corporation toward employment conditions, human rights, environmental pollution and the use of power are always clear cut. FALSE21. (p. 132-133) An individual with a strong sense of personal ethics is less likely to behave in an unethical manner in a business setting. TRUE22. (p. 133) Expatriate managers may experience more than the usual degree of pressure to violate their personal ethics. TRUE23. (p. 134) A firm's organizational culture refers to the values and norms that are shared among employees of an organization. TRUE24. (p. 135) The Enron debacle indicates that an organizational culture can legitimize behavior that a society would judge as unethical. TRUE25. (p. 136) According to the Friedman doctrine, the only social responsibility of business is to increase profits, so long as the company stays within the rules of law. TRUE26. The Friedman doctrine is the belief that ethics are nothing more than a reflection of culture and therefore, a firm should adopt the ethics of the culture in which it is operating. F27.Cultural relativism is the belief that ethics are nothing more than a reflection of culture and therefore, a firm should adopt the ethics of the culture in which it is operating. TRUE28.According to the righteous moralist if a manager of a multinational sees that firms from other nations are not following ethical norms in a host nation, that manager should not either. F 29. (p. 138) The naive immoralist claims that a multinational's home country standards of ethics are the appropriate ones for companies to follow in foreign countries. FALSE30. (p. 138) Most moral philosophers see value in utilitarian and Kantian approaches to business ethics. TRUE31. (p. 138) The utilitarian approaches to ethics hold that the moral worth of actions or practices is determined by their consequences. TRUE32.It, typically is fairly easy to measure the benefits, costs and risks of a course of action. F33. An advantage of utilitarianism is that the philosophy allows for the consideration of justice. FALSE34. (p. 139) Rights theories recognize that human beings have fundamental rights and privileges that transcend national boundaries and cultures. TRUE35. (p. 140) A just distribution is one that is considered fair and equitable. TRUE36. (p. 141) According to Rawls, inequalities can be just if the system that produces inequalities is to the advantage of everyone. TRUE37. (p. 142) Talking with prior employers regarding someone's reputation is a good way to discerna potential employee's ethical predisposition. TRUE38. (p. 143) Building an organization culture that places a high value on ethical behavior requires incentive and reward systems. TRUE39. (p. 144) A firm's stakeholders are individuals or groups that have an interest, claim or stake in the company, what it does and how well it performs. T40. (p. 145-146) Companies can strengthen the moral courage of employees by committing themselves to retaliate against employees who exercise moral courage, say no to superiors or otherwise complain about unethical actions. FALSE41. (p. 124) The accepted principles of right or wrong governing the conduct of businesspeople are best known as A. Business measures B. Business ethics42. (p. 124) Identify the incorrect statement regarding ethical issues in international business.A. They are often rooted in the fact that political systems, law, economic development and culture of nations vary significantlyB. Human rights and environmental regulations are some of the common ethical issuesC. Ethical practices of all nations are similar in natureD. Managers in multinational firms need to be particularly sensitive to differences in business practices because they work across national borders43. (p. 125) To guard against abuse of employment practices in other nations, multinationals should do all of the following exceptA. Establish minimal acceptable standards that safeguard the basic rights and dignity of employeesB. Adhere to working conditions of the host country if they are clearly inferior to those in a multinational's home nationC. Audit foreign subsidiaries and subcontractors on a regular basis to make sure established standards are metD. Take action to correct unacceptable behavior46. (p. 126) Identify the incorrect statement pertaining to foreign multinationals doing business in countries with repressive regimes.A. Inward investment by multinationals can be a force for economic, political and social progress that ultimately improves the rights of people in repressive regimesB. No multinational does business with nations that lack the democratic structures and human rights records of developed nationsC. Multinational investment cannot be justified on ethical grounds in some regimes due to their extreme human rights violationsD. Multinationals adopting an ethical stance can, at times, improve human rights in repressive regimes47. (p. 127) Identify the incorrect statement about environmental regulations.A. Environmental regulations are often lacking in developing nationsB. Environmental regulations are similar across developed and developing nationsC. Developed nations have substantial regulations governing the emission of pollutants, the dumping of toxic chemicals, etcD. Inferior environmental regulations in host nations, as compared to home nation, can lead to ethical issues48. (p. 128) Everyone benefits from the atmosphere and oceans but no one is specifically responsible for them. In this sense, the atmosphere and oceans can be referred to as a(n)B. Global commonsC. Joint assetD. Global reserve49. (p. 128) The _____ occurs when a resource is shared by all, but owned by no one is overused by individuals, resulting in its degradation.A. Tragedy of the commonsB. Noblesse obligeC. Ethical dilemmaD. Friedman system50. (p. 129) Which of the following observations is true of the Foreign Corrupt Practices Act?A. The act outlawed the paying of bribes to foreign government officials to gain businessB. There is enough evidence that it put U.S. firms at a competitive disadvantageC. The act originally allowed for "facilitating payments."D. The Nike case was the impetus for the 1977 passage of this act51. (p. 129) The Convention on Combating Bribery of Foreign Public Officials in International Business Transactions excludesA. Speed payments to secure contracts that would otherwise not be securedB. Grease payments to gain exclusive preferential treatmentC. Facilitating payments made to expedite routine government actionD. Payments to government officials for special privileges52. (p. 129) Grease paymentsA. Are not the same as facilitating payments or speed moneyB. are facilitating payments made to expedite routine government actionC. Are payments to gain exclusive preferential treatmentsD. Can be used to secure contracts that would otherwise not be secured53. (p. 129) Facilitating payments areA. Permitted under the amended Foreign Corrupt Practices ActB. A direct violation of the Foreign Corrupt Practices ActC. Permitted so long as they designed only to gain exclusive preferential treatmentD. Used to secure contracts that would otherwise not be secured54. (p. 130) The idea that businesspeople should consider the social consequences of economic actions when making business decisions and that there should be a presumption in favor of decisions that have both good economic and social consequences is known asA. Business ethicsB. Noblesse obligeC. Ethical dilemmaD. Social responsibility55. (p. 130) Which of the following, in a business setting is taken to mean benevolent behavior that is the responsibility of successful enterprises.A. Sullivan's principlesB. Ethical dilemmaC. Tragedy of the commonsD. Noblesse oblige57. (p. 132) _____ are generally accepted principles of right and wrong governing the conduct of individuals.A. Ethical dilemmasB. Noblesse obligesC. Personal ethicsD. Business measures58. (p. 132) Ethical dilemmas exist because of all of the following reasons exceptA. Many real-world decisions are complex and difficult to frameB. Decisions may involve first, second and third-order consequences that are hard to quantifyC. Doing the right thing or knowing what the right thing might be is often far too easyD. They are situations in which none of the available alternatives seem ethically acceptable59. (p. 132) Which of the following is not likely to lead to unethical behavior?A. An organizational culture that de-emphasizes business ethicsB. A process that does not incorporate ethical considerations into business decision-makingC. A strong personal ethical code governing the conduct of an individualD. Pressure from the parent company to meet unrealistic performance goals60. (p. 133) Ethical behavior is likely to be determined by all of the following, except A. Decision making processes B. Organization culture C. Leadership D. Realistic performance goals61. (p. 133) Expatriate managers may experience more than the usual degree of pressure to violate their personal ethics because of all of the following reasons exceptA. They are away from their ordinary social context and supporting cultureB. They are psychologically and geographically closer to the parent companyC. They may be based in a culture that does not place the same value on ethical norms important in the manager's home countryD. They may be surrounded by local employees who have less rigorous ethical standards62. (p.63. (p. 136) All of the following approaches to business ethics are discussed by scholars primarilyto demonstrate that they offer inappropriate guidelines for ethical decision making in a multinational enterprise exceptA. Friedman doctrineB. Cultural relativismC. Kantian ethicsD. Naive moralist64. (p. 136) According to _____ the social responsibility of business is to increase profits, so longas the company stays within the rules of law. A. The naive immoralistB. The righteous moralistC. Cultural relativismD. The Friedman doctrine65. (p. 136) The Friedman doctrine suggests thatA. Ethics are nothing more than the reflection of cultureB. A multinational's home-country standards of ethics are inappropriate to follow in foreign countriesC. Businesses should not undertake social expenditures beyond those mandated by the law and required for the efficient running of a businessD. If a manager of a multinational sees that firms from other nations are not following ethical norms in a host nation, that manager should not either66. (p. 136) Identify the incorrect statement pertaining to the Friedman doctrine.A. It states that the only social responsibility of business is to increase profits, so long as the company stays within the rules of lawB. It argues that businesses should undertake social expenditures beyond those mandated by the lawC. It believes that maximizing profits is the way to maximize the returns that accrue to firms stockholdersD. Managers of the firm should not make decisions regarding social investments on behalf ofthe stockholders67. (p. 137) Cultural relativism suggests thatA. Ethics are nothing more than the reflection of culture and that a firm should adopt the ethicsof the culture in which it is operatingB. The only social responsibility of business is to increase profitsC. Managers of a firm should not make decisions regarding social investmentsD. A multinational's home-country standards of ethics are always appropriate to follow in foreign countries68. (p. 137) Identify the incorrect statement pertaining to cultural relativism.A. It argues that a firm should adopt the ethics of the culture in which it is operatingB. At its extreme, it suggests that if a culture supports slavery, it is OK to use slave labor in a countryC. It embraces the idea that universal notions of morality transcend different culturesD. It believes that ethics are nothing more than the reflection of a culture69. (p. 137) Child labor is permitted and widely employed in Country X. A multinational company entering Country X decides to employ minors in its subsidiary, even though it is against the multinational's home country ethics. Which of the following approaches to business ethics would justify the actions of the multinational company?A. Righteous moralistB. Cultural relativismC. The justice theoryD. The rights theory70. (p. 137) The idea that universal notions of morality transcend different cultures is implicitly rejected by A. The righteous moralist B. The naive immoralist C. The Friedman doctrineD. Cultural relativism71. (p. 137) The righteous moralist suggests thatA. Ethics are nothing more than the reflection of cultureB. A multinational's home-country standards of ethics are the appropriate ones for companies to follow in foreign countriesC. The social responsibility of business is to increase profits, so long as the company stays within the rules of lawD. If a manager of a multinational sees that firms from other nations are not following ethical norms in a host nation, that manager should not either72. (p. 137) Which of the following statement about the righteous moralist approach is not true?A. It claims that a multinational's home-country standards of ethics are the appropriate ones for companies to follow in foreign countriesB. It is typically associated with managers from developing nationsC. Its proponents often go too far in advocating that the appropriate thing to do is adopt home-country standardsD. It can create practical problems73. (p. 137) The righteous moralist approach to business ethics is typically associated with managers from A. Third world nations B. Underdeveloped nations C. Developing nationsD. Developed nations74. (p. 138) The _____ approach asserts that if a manager of a multinational sees that firms from other nations are not following ethical norms in a host nation, that manager should not either.A. Cultural relativismB. Friedman doctrineC. Righteous moralistD. Naive immoralist75. (p. 138) The naive immoralist suggests thatA. Ethics are nothing more than the reflection of cultureB. A multinational's home-country standards of ethics are the appropriate ones for companies to follow in foreign countriesC. The social responsibility of business is to increase profits, so long as the company stays within the rules of lawD. If firms in a host nation do not follow ethical norms then the manager of a multinational should also not follow ethical norms there76. (p. 138) According to the _____ approach to business ethics, the moral worth of actions or practices is determined by their consequences.A. UtilitarianB. Cultural relativismC. Friedman doctrineD. Naive immoralist77. (p. 138) The utilitarian approach to business ethics suggests thatA. People should be treated as ends and never purely as means to the ends of othersB. The moral worth of actions or practices is determined by their consequencesC. People have dignity and need to be treated as suchD. Human beings have fundamental rights and privileges that transcend national cultures78. (p. 138) Which of the following approaches is committed to the maximization of good and the minimization of harm?A. The righteous moralistB. Cultural relativismC. Friedman doctrineD. Utilitarianism79. (p. 139) Tools to assess actions such as cost-benefit analysis and risk assessment are rooted in the _____ philosophy.A. Utilitarian approachB. Kantian approachC. Friedman doctrineD. Naive immoralist80. (p. 139) According to the _____ approach, the best decisions are those that produce the greatest good for the greatest number of people.A. Naive immoralistB. Friedman doctrineC. UtilitarianD. Kantian81. (p. 139) The Kantian approach to ethics suggests thatA. Human beings have fundamental rights and privileges that transcend national boundariesB. The moral worth of actions or practices is determined by their consequencesC. People should be treated as ends and never purely as means to the ends of othersD. Ethics are nothing more than the reflection of culture82. (p. 139) The utilitarian approach to business ethics has been criticized because of all of the following reasons, exceptA. The measurement of benefits, costs and risks is often not possible due to limited knowledgeB. The philosophy omits the consideration of justiceC. The philosophy advocates the greatest good for the greatest number of people, but such actions may result in the unjustified treatment of a minorityD. It holds that the moral worth of actions or practices is determined by their consequences83. (p. 139) Rights theories suggest thatA. Human beings have fundamental rights and privileges that transcend national boundariesB. The moral worth of actions or practices is determined by their consequencesC. People should be treated as ends never purely as means to the ends of othersD. Minimum levels of morally acceptable behavior should be established84. (p. 140) Identify the approach that most moral philosophers favor and that forms the basis for current models of ethical behavior in international businesses.A. Friedman doctrineB. Cultural relativismC. The righteous moralistD. Rights theory85. (p. 140) The Universal Declaration of Human Rights, related to employment, upholds all of the following, exceptA. Just and favorable work conditionsB. Equal pay for equal workC. Prohibition of trade unionsD. Protection against unemployment86. (p. 140) Article 1 of the United Nations' Universal Declaration of Human Rights states: "All human beings are born free and equal in dignity and rights." This best echoesA. Cultural relativismB. Friedman doctrineC. The righteous moralist approachD. Kantian ethics87. (p. 140) A(n) _____ is any person or institution that is capable of moral action such as a government or corporation.A. Moral agentB. UtilitarianC. Righteous moralistD. Naive immoralist88. (p. 140) Justice theories of business ethics focus onA. The moral worth of actions or practicesB. Minimum levels of morally acceptable behaviorC. Fundamental rights and privileges that transcend national boundariesD. The attainment of a just distribution of economic goods and services89. (p. 141) The notion that all economic goods and services should be distributed equally except when an unequal distribution would work to everyone's advantage was developed byA. David HumeB. John RawlsC. Jeremy BenthamD. John Stuart Mill90. (p. 141) Under the veil of ignorance, everyone is imagined to be ignorant ofA. All of his or her particular characteristicsB. Fundamental rights and privilegesC. The moral worth of actions or practicesD. The minimum levels of morally acceptable behavior91. (p. 141) According to John Rawls,A. Each person be permitted the maximum amount of basic liberty compatible with a similar liberty for othersB. Freedom of speech and assembly is the single most important component in a justice systemC. Equal basic liberty is only possible in a pure market economyD. Inequalities in a justice system are not to be tolerated under any circumstance92. (p. 141) Rawls' philosophy that inequalities are justified if they benefit the position of the least-advantaged person is known as theA. Inequality principleB. Equity principleC. Difference principleD. Indifference principle93. (p. 142) Managers of international business can do all of the following to make sure ethical issues are considered in business decisions, exceptA. Favor hiring and promoting people with a well-grounded sense of personal ethicsB. Build an organizational culture that places a high value on ethical behaviorC. Make sure that leaders within the business do not articulate the rhetoric of ethical behaviorD. Develop moral courage95. (p. 143) To build an organization culture that values ethical behavior, a company should do all of the following, exceptA. Not sanction people who do not engage in ethical behaviorB. Articulate values that emphasize ethical valuesC. Make sure that key business decisions not only make good economic sense, but are also ethicalD. Place a high value on ethical behavior by providing incentives and reward systems96. (p. 144) External stakeholdersA. Are individuals or groups who own the businessB. Include all employees, the board of directors and stockholdersC. Typically, comprises customers, suppliers, lenders, etcD. Are individuals or groups who work for the business97. (p. 144) Internal stakeholdersA. Are individuals or groups who work for or own the businessB. Do not have any claim on a firm or its activitiesC. Typically comprises customers, suppliers, lenders, governments, unions, etcD. Are individuals, except employees, board of directors and stockholders that have some claim on the firm98. (p. 144) _____ means standing in the shoes of a stakeholder and asking how a proposed decision might impact that stakeholder.A. Veil of ignoranceB. Difference principleC. Moral imaginationD. Noblesse oblige99. (p. 145) Establishing _____ involves a business' resolve to place moral concerns ahead of other concerns in cases where either the fundamental rights of stakeholders or key moral principles have been violated.A. A veil of ignoranceB. A difference principleC. Moral imaginationD. Moral intent 100. (p. 145) _____ enables managers to walk away from a decision that is profitable, but unethical.A. Noblesse obligeB. Moral courageC. Difference principleD. Friedman doctrine101. (p. 124) What are business ethics? What is the relationship between business ethics and an ethical strategy?Business ethics are the accepted principles of right or wrong governing the conduct of businesspeople. An ethical strategy is a strategy or course of action that does not violate those accepted principles.102. (p. 124-13) What is considered normal practice in one country may be considered unethical in others. Discuss.Chapter 04 - Ethics in International BusinessMany of the ethical issues and dilemmas in international business are rooted in the fact that political systems, law, economic development and culture vary significantly from nation to nation. Therefore, what might be considered a normal business practice in one country may constitute unethical behavior in another country. Managers in a multinational company need to be sensitive to these differences and choose the ethical action in those circumstances where variation across societies creates the potential for ethical problems. In the international business setting, the most common ethical issues involve employment practices, human rights, environmental regulations, corruption and the moral obligation of multinational corporations.4-11。

新编简明英语语言学教程04Chapter-4-gram

The criteria on which categories are determined

确定词的范畴的标准

Meaning (意义) Inflection (屈折变化) Distribution(分布)

11

Word categories often bear some relationship with its meaning. e.g.

9

Major lexical categories play a very important role in sentence formation. They differ from minor lexical categories in that they are often assumed to be the heads around which phrases are built.

14

‘s; -ed, -ing; -er, -est… Although inflection is very helpful in determining a

word’s category, it does not always suffice. Some words do not take inflections. Moisture, fog, sheep; Frequent, intelligent Note: The most reliable criterion of determining a word’s category is its distribution.

因此, 一个词的分布情况与其意义和屈折变化 能力的信息一起对于确定它的句法范畴有帮助.

16

Phrase categories and their structures

医学专业英语上册(第四章)chapter 4 musculoskeletal system

50

Axial skeleton

The axial skeleton includes the bones in the head, neck, spine, chest and trunk of the body. These bones form the central axis for the whole body and protect many of the internal organs such as the brain, lungs, and heart. The head or skull is divided into two parts consisting of the cranium and facial bones. These bones protect the brain and special sense organs from injury. The cranium covers the brain and the facial bones surround the mouth, nose, and eyes. Muscles for chewing and head movements are attached to the cranial bones. The cranium consists of the frontal , parietal , temporal, ethmoid , sphenoid , and occipital bones. The facial bones are the mandible , maxilla , zygomatic , vomer, palatine , nasal , and lacrimal bones. The cranial and facial bones are illustrated in Figure 3.1 and described in Table 3.1. Figure 3.1 The cranial and facial bones (seen from the lateral part)

Part One Chapter Four Langland 朗兰

Chapter Four: Langland朗兰I. Piers the Plowman and Its Author耕者皮尔斯和它的作者Piers the Plowman shows the existence of English Popular literature in the Middle Age.耕者皮尔斯表明了中世纪流行文学的存在。

7000 lines, written by William LanglandII.A Picture of Feudal EnglandThe poem sets forth a series of wonderful dreams.这首诗描写了一系列奇妙的梦境。

1. The Exposure of the Ruling Classes对统治阶级的揭露“They leapt away to London.To be clerks of the King’s Bench and despoil the land.”2. The Story of the Cat and Rats猫和老鼠的故事If the cat was killed, another would come in its place.Let that cat be.The cat is the symbol of the ruling class.3. The Marriage of Lady Meed贿赂夫人的婚姻Three major characters: Lady Meed, the King, Conscience4. The Condition of the Peasants农民的境况5. The Search for Truth寻找真理6. The Class Nature of Piers皮尔斯的阶级本质7. Social Significance社会意义III. Artistic Feature艺术特点习题Choose the best answer.1._____ defeated the English troops at Hastings.A. Angles, Saxons and JutesB. Germanic peoplesC. Danish VikingsD. NormansD【史称诺曼征服Norman Conquest】Choose the best answer.2.The Anglo-Saxon period ended in ____.A. 1017B. 1042C. 1016D. 1066D【同第一题。

Chapter 04-The Path of least resistance

(Chapter 4)(The Path of Least Resistance)A Lesson from the GhettoRecently I was traveling from New York’s La Guardia Airport to Manhattan. My cabdriver chose to avoid the congested traffic on the East River Drive. His route brought me through my old neighborhood in East Harlem.I had moved there after getting a master’s degree from the Boston Conservatory of Music. What a contrast that was, cultural Boston and “culturally deprived” East Harlem. For a musician just if for the New York music scene, East 110th Street between Second and Third Avenue was just the right price in those days.Most of us have a talent for selective memory. We remember the past as containing many more good experiences than bad ones. (My grandmother had it just the other way around.) And so, as I studied my old turf, I was flooded with wonderful memories of my ghetto days. Suddenly I was brought back to the present by an extraordinary example of ghetto art, graffiti.This art from developed years ago. Its origin was the wanton vandalizing of property. When I lived in East Harlem, graffiti was not yet an art form. Just kids, spray cans, and walls. Mostly the kids used the walls to express their hostility by painting expletives in large, sloppy letters. Occasionally a kid would express his romantic tendencies with great declarations of love; Jose’ loves Judy.Over the years the letters became more artistic and then developed into complex artistic creations. The young artists became competitive with each other. Originality and craft became the norm. The bravado of youthful energy came to beexpressed in painting rather than in gang warfare. Bold designs gave way to bolder designs. The color was strong, direct, primary.The city became the canvas. These artists would stalk at night and paint on whatever surface they found. They used up the available walls quickly and then found the perfect symbol of their art: subway cars- owned by the society the artists were separate from, vital to the movement of the populace, gray, drab, dilapidated, lifeless and institutional.The graffiti writers would break into the railway yards and spend the night painting subway cars. Then the Transit Authority would spread their works to a mass audience throughout the city. Influenced by each other’s work, the artists’creations got better. The authorities became alarmed and put armed guards around the railway yards. But by that time the highbrow art world had taken notice. Some of the best ghetto artists were sought out by art dealers. The artists switched to real canvasses. A fad rose and fell in short order.Gallery success might have been temporary, but the artists kept on painting, growing, and developing. New artists emerged, pushing the art form further and further still. Later the city of Tokyo would invite one of the best artists to come to Japan and paint long murals on their subway cars.What a story. Too strange to be fiction. If someone had told you twenty-five years ago that somebody in New York City the “culturally deprived,”undereducated children of welfare would rise up, not in violence, but in art and in dance (break dancing) and in poetry (rap), you might have asked to examine that person’s sugar cube for traces of LSD.What caught my eye and captured my imagination that day in East Harlem was a new evolutionary step in graffiti art. It was the choice of colors. Pastels. No longer the bright, bold, shouting colors of a few years ago, but colors that were soft, translucent, subtle, and penetrating.Somewhere in the destructive life of the inner city, a young artist is think about color. Experimenting with quinacri-done violet and cerulean blue. Mixing and blending opposite colors to create illusions of space and dimension. And somehow, because of this, I experience hope for our civilization.There is a profound lesson here. It is partly about the human spirit. We have been led to believe that the circumstances of our life determine our ability to express ourselves. That for us to explore new dimensions of our being, our conditions need to be favorable. If that were true, how could such creativity, originality, and vitality come from such humble and adverse beginnings as the ghetto? How is it that it was from there, and not there sacred institutions of academia, that new thought, born of what is highest in humanity, developed and grew? Perhaps our true is that of creators, who can bring forth new life out of any set of circumstance.Creating Is Not a Product of the CircumstancesCreating is completely different from reacting or responding to the circumstances you are in. The process of creating is not generated by the circumstances in which you find yourself, but the creation itself.It is popular to think of creativity as a product of your environment, culture, or other circumstances that foster the creative process. An example of this notion was the corporate fad, popular just a few years ago, of “engineer environments” that weresupposed to the conducive for creating. But a quick survey of the history of creativity will make it obvious that people have created in a wide range of circumstances, from convenient ones to difficult ones.As you begin to consider what you want to create in your life. It is good for you to know that the circumstances that presently exist are not the determining factor of the results you desire to create. You are not limited by them, eve though it may seem you are entrenched in them.Because creating is so essentially different from the creative-responsive orientation to which you have been exposed, it may seem ridiculous to consider life to be any different from what you have experienced before. You may be reading these words with the suspicion that this is yet another pep talk designed to inspire you to a new way of life. Or you may think that creating is possible only for the artist, that the creative process is limited to painting, music, filmmaking, poetry, or the other arts.Even though the most obvious expression of the creative process is found in the arts, it is in no way limited to the arts. Almost all of your life’s desires can be the subject of the creative process. There need be no separation from the creative process as practiced in the arts and the same creative process as practiced in other human endeavors. In addition, the art is a perfect arena for learning the special ability and skill of creating.It is wise to learn about the creative process from those practitioners who know the most about it and who have used it to bring the highest fruits of the creative process into being. This is a different skill from what you have learned in school, at home, or at work, and yet it is one of the most important skills to develop in your life.Pablo Casals, one of the greatest cellists of our century, did not limit his concept of creating his music.I have always regarded manual labor as creative and looked withrespect- and, yes, wonder- at people who work with their hands. Itseems to me that heir creativity is no less than that of a violinist orpainter.And psychologist Carl Rogers has written:The action of the child inventing a few game with his playmates;Einstein formulating a theory of relativity; the housewife devising anew sauce for the meat; a young author writing his first novel; all ofthese are, in terms of our definition, creative, and there is no attempt toset them in some order of more or less creative.When one does not consciously know the skill of creating, it is common to suppose the creative process a product of the unconscious, or of mysticism. Then the creative process becomes a search for the formula that will tap your hidden powers. Because your “normal” self seems not to be the possessor of such powers, you might assume they must lie somewhere else.In the story of Dumbo the elephant, a mouse convinces Dumbo that he can fly because of a “magic” feather. Dumbo tries out the feature and finds he can fly. But one day he loses his feather and thinks he has lost the ability. The mouse confesses that the story of the magic feather was a hoax and that Dumbo’s ability to fly was his own. Dumbo discovers he can fly without benefit of feather.Many of the theories about the creative process are similar to Dumbo’s magicfeather. In these theories the power to create what you want depends on a magical talisman that will enable you to unlock your hidden powers once and for all.To some jungle tribes who have not had contact with modern civilization,the jet planes they see flying overhead take on a magical meaning. These planes are seen as gods or at least vehicles of gods.It is common to assume that the unknown is unknowable, or at lease unknowable by normal means. It is our inexperience and ignorance that can make the creative process seem as if it is an outcome of magical operations, the same kind of inexperience and ignorance a jungle tribe may have about modern aviation. But, in fact, creating is a skill that can be learned and developed. Like any skill, you learn by practice and hands-on experience. You can learn to create by creating.The StepsThe steps in the creative process are simple to describe, but they do not constitute a formula. Instead, each step represents certain types of actions. Some aspects of the creative process are active, some are more passive. Different aspects call for different skills. You ma have developed some of these skills already and find that other skills are not as easy at first. Each time you create a new result, you are involved in a unique creation. While your ability will develop over time with experience, every new creation has its own individual process.In this chapter I will outline the basic steps of creating. In later chapters I will develop these steps so that you will be able to begin to experiment with them in your own life. Think of the following as an overview of the creative process rather than as a formula to adopt.1.Conceive of the result you want to create.Creators start at the end. First have an idea of what they want to create. Sometimes this idea is general, and sometimes it is specific. Before you can create what you want to create, you must know what you are after, what you want to bring into being. Your original concept may be clear, or it may be simply a rough draft. Either will work well. Some creators like to improvise as they create, so they begin with a general concept. A painter may not know exactly how the final painting may look, but he or she has enough of a concept to make adjustments during the creative process so that the painting in progress will come closer and closer to what the artist wants. Other painters know exactly what the final painting will look like before they pick up a brush. Georgia O’Keeffe said, “I don’t start until I’m almost entirely clear. It is a waste of time and paint if I don’t. I’ve wasted a lot of canvasses, so be pretty clear.”Knowing what you want is itself skill. Our traditional educational system does not encourage you to know what you want. Instead you are encouraged to choose the “correct” response from narrow choices that life seems to offer. Frequently this has little relationship to what you really want. Because of this, many people develop an ambivalence toward what they want. And why not? It is hard to be enthusiastic about the choices most people are left with. But as you develop your own creative process, conceiving of the results you want will become meaningful and interesting.2.Know what currently exists.If you were painting a painting, you would need to know the current state ofthe painting as it developed. This would be important knowledge. If you did not know what you had created so far, it would be impossible for you to add more brushstrokes or change what you had done so as to bring the painting you wanted into being.Knowing what currently exists is another skill. While this may sound deceptively simple, in fact most of us have been encouraged to view reality with particular biases. Some people make reality seem better than it is, some make it seem worse than it is, and some minimize how good or bad it can be. One of the most important abilities creators have is the ability to be objective about their own creation. There is a notion, popular in many university philosophy departments, that you can never really view reality objectively. But in the same university, the art department teachers those students to draw portraits of models. This drawing skill helps students learn first to see, and then represent, what they are looking at. Even though each art student may have his or her own style of portraiture, anyone from the philosophy department could identify the model by looking at any of the drawings of the model.In music conservatories students are taught to identify rhythms, harmonies, and intervals by hearing them. This skill is called ear training. This is another skill in which students are taught to identify and represent reality correctly. When they write down the music that was played, it is not a matter of “interpretation.” If the student correctly identifies what was played, he or she gets an A. Students who do not correctly identify what is played get less than an A. Music students learn how concrete the perception of music can be. This is another example of training designed to enhance the ability to view reality objectively.In a similar way, you need to develop the skill of viewing reality objectively.For many people reality is an acquired taste. At first glance you may have uncomfortable and disturbing experiences. If you were in a problem-solving mode, you would take action to restore feelings of balance and well-being. The most common way people do this is by misrepresenting reality. They may lie, rationalize, or distract themselves from what is going on. But as you learn to master your own creative process, you develop a capacity for truth. Good, bad, or indifferent, you will still want to know accurately what is going on.3.Take actionOnce you know what you want and what you currently have, the next step is to take action. But what kind of action do you take? Creating is a matter of invention rather than of convention. Education emphasizes convention, so you may have had little experience with inventing. Inventing is another skill that can be developed. When you take an action that is designed to bring your creation into being, the action may either work or not work. If the action works, you can continue taking it or discontinue taking it. Sometimes it will be useful to continue, sometimes it will not be useful to continue. You will know what to do by watching the changes in the current state of the result. All the actions, the ones that work and the ones that do not work, help to create the final result. This is because creating itself is a learning process, learning what works and what does not work. The stock-in-trade of a creator are the abilities to experiment and to evaluate one’s experiments.Invention is not all trail and error. As you invent actions to bring your creations into being, you begin to develop an instinct for the actions that work best. Creators are able to develop an economy of means. This generally happens over time, and themore you create, the more chance you have to develop your own instincts.Some of the actions you take will help you move directly to the result you want, but most will not. The art of creating is often found in your ability to adjust or correct what you have done so far. Many people have been encouraged to “get it right the first time”or, even worse, to “be perfect.”This policy can lead to profound inexperience in the adjustment process. Instead of making the most of what you have done so far, in order to bring creation into existence, you may be tempted to give up anytime the circumstances seem against you. Sometimes people encourage others to “stay with it”and develop “determination and fortitude”in reaction to habitual quitting. But this manipulation hardly ever works. Without an ever-increasing ability to adjust the actions you take, trying to “stay with it”can seem like banging your head against a wall. After sincere attempts to “stay with it” fail and fail again, the path of least resistance is to quit. You may have thought your habitual giving up was a serious character flaw. But this is probably not the case. It is not fortitude, willpower, or determination that enables you to continue the creative process, but learning as you go.4. Learn the rhythms of the creative process.There are three distinct phases of the creative process: germination, assimilation, and completion. Each phase has its own energy and class of actions.Germination begins with excitement and newness. Partly this germinational energy comes from the unusualness of the new activity.Assimilation is often the least obvious phase of the process. In this phase the initial “thrill is gone.” This phase moves from a focus on internal action to a focus onexternal action. In this phase you live with your concept of what you want to create and internalize it. It becomes part of you. Because of this, you are able to generate energy to use in your experiments and learning. The drama of the first blush of germination is over, but this new, quiet energy of assimilation helps you form the result.Completion is the third stage of creation. This stage has a similar energy to germination, but new it is applied to a creation that is more tangible. In this phase you use the energy not only to bring to final completion the result you are creating but also to position yourself for your next creation. In other words, this stage leads also to the germination of your next creation.5. Creating momentumMany of the theories describing creativity these days have a tone of “beginners luck.”For professional creators there is a different tone, that of ever-increasing momentum. Not only is the creative process a reliable method for producing the results you want, it also contains seeds of its own development. Who do you think has a greater chance for successfully creating the results they want: those who have done it for years, or those who are novices? It is true that some first-time novelists write masterpieces, but this is the exception, not the rule. Even Mozart, perhaps the most gifted composer in history, developed and grew in his art. The music he wrote in his thirties was far more advanced than what he wrote in his twenties or in his teens. The more music he wrote, the more he was able to write. His increasing experience gave him the momentum typical of the creative process. If you begin to create the results you want today, you are more prepared to create the results you want ten yearsfrom now. Each new creation gives you added experience and knowledge of your own creative process. You will naturally increase your ability to envision what you want and your ability to bring those results into being.。

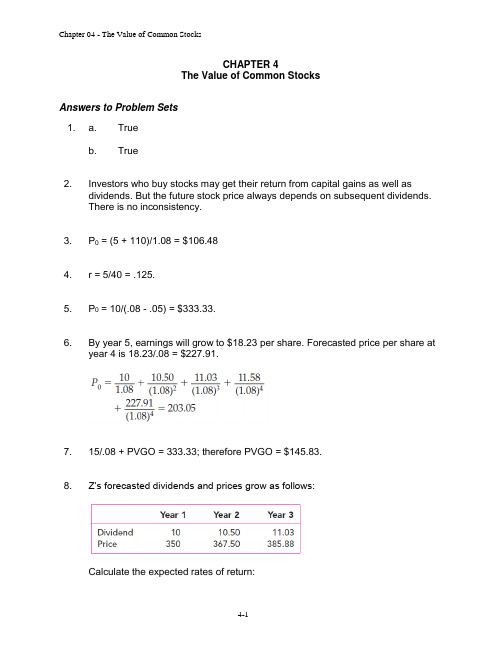

Principles of Corporate Finance 英文第十版习题解答Chap004

CHAPTER 4The Value of Common StocksAnswers to Problem Sets1. a. Trueb. True2. Investors who buy stocks may get their return from capital gains as well asdividends. But the future stock price always depends on subsequent dividends.There is no inconsistency.3. P0 = (5 + 110)/1.08 = $106.484. r = 5/40 = .125.5. P0 = 10/(.08 - .05) = $333.33.6. By year 5, earnings will grow to $18.23 per share. Forecasted price per share atyear 4 is 18.23/.08 = $227.91.7. 15/.08 + PVGO = 333.33; therefore PVGO = $145.83.8. Z’s forecasted dividends and prices grow as follows:Calculate the expected rates of return:From year 0 to 1: 08.33.333)33.333350(10=-+From year 1 to 2: 08.350)35050.367(50.10=-+From year 2 to 3:08.50.367)50.36788.385(03.11=-+Double expects 8% in each of the first 2 years. Triple expects 8% in each of the first 3 years.9. a. Falseb. True.10. PVGO = 0, and EPS 1 equals the average future earnings the firm could generate under no-growth policy.11. Free cash flow is the amount of cash thrown off by a business after allinvestments necessary for growth. In our simple examples, free cash flow equals operating cash flow minus capital expenditure. Free cash flow can be negative if investments are large.12. The value at the end of a forecast period. Horizon value can be estimated using the constant-growth DCF formula or by using price –earnings or market – book ratios for similar companies.13. If PVGO = 0 at the horizon date H , horizon value = earnings forecasted for H + 1 divided by r .14. Newspaper exercise, answers will vary15.Expected Future Values Present Values Horizon Period (H) Dividend (DIV t ) Price (P t ) Cumulative Dividends FuturePrice Total0 100.00 100.00100.001 10.00 105.00 8.70 91.30 100.002 10.50 110.25 16.64 83.36 100.003 11.03 115.76 23.88 76.12 100.004 11.58 121.55 30.50 69.50 100.00 10 15.51 162.89 59.74 40.26 100.00 20 25.27 265.33 83.79 16.21 100.00 50 109.21 1,146.74 98.94 1.06 100.00 100 1,252.39 13,150.13 99.99 0.01 100.00Assumptions 1. Dividends increase at 5% per year compounded. 2. Capitalization rate is 15%.16.$100.000.10$10r DIV P 1A ===$83.33.0400.10$5g r DIV P 1B =-=-=⎪⎭⎫⎝⎛⨯++++++=67665544332211C 1.1010.10DIV 1.10DIV 1.10DIV 1.10DIV 1.10DIV 1.10DIV 1.10DIV P $104.501.1010.1012.441.1012.441.1010.371.108.641.107.201.106.001.105.00P 6654321C =⎪⎭⎫⎝⎛⨯++++++=At a capitalization rate of 10%, Stock C is the most valuable. For a capitalization rate of 7%, the calculations are similar. The results are:P A = $142.86 P B = $166.67 P C = $156.48Therefore, Stock B is the most valuable.17. a. $21.90.027500.095 1.0275$1.35$1.35g r DIV DIV P 100=-⨯+=-+=b.First, compute the real discount rate as follows:(1 + r nominal ) = (1 + r real ) ⨯ (1 + inflation rate)1.095 = (1 + r real ) ⨯ 1.0275(1 + r real ) = (1.095/1.0275) – 1 = .0657 = 6.57%In real terms, g = 0. Therefore:$21.900.0657$1.35$1.35g r DIV DIV P 100=+=-+= 18.a. Plowback ratio = 1 – payout ratio = 1.0 – 0.5 = 0.5Dividend growth rate = g= Plowback ratio × ROE = 0.5 × 0.14 = 0.07 Next, compute EPS 0 as follows:ROE = EPS 0 /Book equity per share 0.14 = EPS 0 /$50 ⇒ EPS 0 = $7.00Therefore: DIV 0 = payout ratio × EPS 0 = 0.5 × $7.00 = $3.50 EPS and dividends for subsequent years are:YearEPS DIV0 $7.00$7.00 × 0.5 = $3.501 $7.00 × 1.07 = $7.4900 $7.4900 × 0.5 = $3.50 × 1.07 = $3.74502 $7.00 × 1.072 = $8.0143 $8.0143 × 0.5 = $3.50 × 1.072 = $4.0072 3 $7.00 × 1.073 = $8.5753 $8.5753 × 0.5 = $3.50 × 1.073 = $4.28774 $7.00 × 1.074 = $9.1756$9.1756 × 0.5 = $3.50 × 1.074 = $4.58785 $7.00 × 1.074 × 1.023 = $9.3866 $9.3866 × 0.5 = $3.50 × 1.074 × 1.023 = $4.6933EPS and dividends for year 5 and subsequent years grow at 2.3% per year, as indicated by the following calculation:Dividend growth rate = g = Plowback ratio × ROE = (1 – 0.08) × 0.115 = 0.023b.⎪⎭⎫ ⎝⎛⨯++++=45443322110 1.11510.115DIV 1.115DIV 1.115DIV 1.115DIV 1.115DIV P $45.651.1010.023-0.1154.6931.1154.5881.1154.2881.1154.0071.1153.74544321=⎪⎭⎫⎝⎛⨯++++=The last term in the above calculation is dependent on the payout ratioand the growth rate after year 4.19. a.11.75%0.11750.0752008.5g P DIV r 01==+=+=b.g = Plowback ratio × ROE = (1 − 0.5) × 0.12 = 0.06 = 6.0%The stated payout ratio and ROE are inconsistent with the security analysts’ forecasts. With g = 6.0% (and assuming r remains at 11.75%) then:pesos 147.830.06- 0.11758.5g r DIV P 10==-=20.The security analyst’s forecast is wrong because it a ssumes a perpetual constant growth rate of 15% when, in fact, growth will continue for two years at this rate and then there will be no further growth in EPS or dividends. The value of the company’s stock is the present value of the expected divi dend of $2.30 to be paid in 2020 plus the present value of the perpetuity of $2.65 beginning in 2021. Therefore, the actual expected rate of return is the solution for r in the following equation:r)r(1$2.65r 1$2.30$21.75+++=Solving algebraically (using the quadratic formula) or by trial and error, we find that: r = 0.1201= 12.01% 21.a.An Incorrect Application . Hotshot Semiconductor’s earnings anddividends have grown by 30 percent per year since the firm’s founding ten years ago. Current stock price is $100, and next year’s dividend is projected at $1.25. Thus:31.25%.31250.3001001.25g P DIV r 01==+=+=This is wrong because the formula assumes perpetual growth; it is notpossible for Hotshot to grow at 30 percent per year forever.A Correct Application. The formula might be correctly applied to the Old Faithful Railroad, which has been growing at a steady 5 percent rate for decades. Its EPS 1 = $10, DIV 1 = $5, and P 0 = $100. Thus:10.0%.100.0501005g P DIV r 01==+=+=Even here, you should be careful not to blindly project past growth into thefuture. If Old Faithful hauls coal, an energy crisis could turn it into a growth stock.b.An Incorrect Application. Hotshot has current earnings of $5.00 per share. Thus:5.0%.0501005P EPS r 01====This is too low to be realistic. The reason P 0 is so high relative to earningsis not that r is low, but rather that Hotshot is endowed with valuable growth opportunities. Suppose PVGO = $60:PVGO rEPS P 10+=60r5100+=Therefore, r = 12.5%A Correct Application. Unfortunately, Old Faithful has run out of valuable growth opportunities. Since PVGO = 0:PVGO r EPS P 10+=0r10100+=Therefore, r = 10.0%22.gr NPVr EPS price Share 1-+= Therefore:0.15)(r NP V r E P S Ραα1αα-+=α0.08)(r NP V r E P S Ρββββ1β-+=The statement in the question implies the following:⎪⎪⎭⎫⎝⎛-+->⎪⎪⎭⎫ ⎝⎛-+-0.15)(r NPV r EPS 0.15)(r NPV 0.08)(r NPV r EPS 0.08)(r NPV αααα1ααββββ1ββ Rearranging, we have:β1βββα1αααE P S r 0.08)(r NP V E P S r0.15)(r NP V ⨯-<⨯- a.NPV α < NPV β, everything else equal.b. (r α - 0.15) > (r β - 0.08), everything else equal.c.0.08)(r NP V 0.15)(r NP V ββαα-<-, everything else equal. d. β1βα1αE P S r E P S r <, everything else equal. 23.a.Growth-Tech’s stock price should be:23.81.08)0(0.12$1.24(1.12)1(1.12)$1.15(1.12)$0.60(1.12)$0.50P 332$=⎪⎪⎭⎫ ⎝⎛-⨯+++=b.The horizon value contributes:$22.07.08)0(0.12$1.24(1.12)1)P V(P 3H =-⨯=c.Without PVGO, P 3 would equal earnings for year 4 capitalized at 12 percent:$20.750.12$2.49= Therefore: PVGO = $31.00 – $20.75 = $10.25d.The PVGO of $10.25 is lost at year 3. Therefore, the current stock price of $23.81 will decrease by:$7.30(1.12)$10.253= The new stock price will be: $23.81 – $7.30 = $16.5124.a.Here we can apply the standard growing perpetuity formula with DIV 1 = $4, g = 0.04 and P 0 = $100:8.0%.080.040$100$4g P DIV r 01==+=+=The $4 dividend is 60 percent of earnings. Thus:EPS 1 = 4/0.6 = $6.67Also:PVGO rEPS P 10+=PVGO 0.08$6.67$100+=PVGO = $16.63b.DIV 1 will decrease to: 0.20 ⨯ 6.67 = $1.33However, by plowing back 80 percent of earnings, CSI will grow by 8 percent per year for five years. Thus: Year 1 2 3 4 5 6 7, 8 . . . DIV t 1.33 1.44 1.55 1.68 1.81 5.88 Continued growth at EPS t6.677.207.788.409.079.80 4 percentNote that DIV 6 increases sharply as the firm switches back to a 60 percent payout policy. Forecasted stock price in year 5 is:$147.0400.085.88g r DIV P 65=-=-=Therefore, CSI’s stock price will increase to:$106.211.081471.811.081.681.081.551.081.441.081.33P 54320=+++++=25.a.First, we use the following Excel spreadsheet to compute net income (or dividends) for 2009 through 2013:2009 2010 2011 2012 2013 Production (million barrels) 1.8000 1.6740 1.5568 1.4478 1.3465 Price of oil/barrel 65 60 55 50 52.5 Costs/barrel 25 25 25 25 25 Revenue 117,000,000 100,440,000 85,625,100 72,392,130 70,690,915 Expenses 45,000,000 41,850,000 38,920,500 36,196,065 33,662,340 Net Income (= Dividends) 72,000,000 58,590,000 46,704,600 36,196,065 37,028,574Next, we compute the present value of the dividends to be paid in 2010,2011 and 2012:=++=320 1.0936,196,0651.0946,704,6001.0958,590,000P $121,012,624 The present value of dividends to be paid in 2013 and subsequent yearscan be computed by recognizing that both revenues and expenses can be treated as growing perpetuities. Since production will decrease 7%per year while costs per barrel remain constant, the growth rate of expenses is: –7.0%To compute the growth rate of revenues, we use the fact that production decreases 7% per year while the price of oil increases 5% per year, so that the growth rate of revenues is:[1.05 × (1 – 0.07)] – 1 = –0.0235 = –2.35%Therefore, the present value (in 2012) of revenues beginning in 2013 is:45$622,827,4(-0.0235)-0.0970,690,915PV 2012==Similarly, the present value (in 2012) of expenses beginning in 2013 is:25$210,389,6(-0.07)-0.0933,662,340P V 2012==Subtracting these present values gives the present value (in 2012) of net income, and then discounting back three years to 2009, we find that the present value of dividends paid in 2013 and subsequent years is: $318,477,671The total value of the company is:$121,012,624 + $318,477,671 = $439,490,295Since there are 7,000,000 shares outstanding, the present value per share is:$439,490,295 / 7,000,000 = $62.78b. EPS 2009 = $72,000,000/7,000,000 = $10.29 EPS/P = $10.29/$62.78 = 0.16426.[Note: In this problem, the long-term growth rate, in year 9 and all later years, should be 8%.]The free cash flow for years 1 through 10 is computed in the following table:Year1 2 3 4 5 6 7 8 9 10 Asset value 10.00 12.00 14.40 17.28 20.74 23.12 25.66 28.36 30.63 33.08 Earnings 1.20 1.44 1.73 2.07 2.49 2.77 3.08 3.40 3.68 3.97 Investment 2.00 2.40 2.88 3.46 2.38 2.54 2.69 2.27 2.45 2.65 Free cash flow -0.80-0.96-1.15-1.380.100.230.381.131.23 1.32 Earnings growth from previous period20.0% 20.0% 20.0% 20.0% 20.0% 11.5% 11.0% 10.5%8.0%8.0%Computing the present value of the free cash flows, following the approach from Section 4.5, we find that the present value of the free cash flows occurring in years 1 through 7 is:654321 1.100.231.100.101.101.38-1.101.15-1.100.96-1.100.80-PV +++++==+71.100.38-$2.94 The present value of the growing perpetuity that begins in year 8 is:29.10.08)0(0.101.1343(1.10)1PV 7$=⎪⎪⎭⎫ ⎝⎛-⨯= Therefore, the present value of the business is:-$2.94 + $29.10 = $26.16 million27.From the equation given in the problem, it follows that:bROE )/(r b1ROE )(b r b)(1ROE BVP S P 0--=⨯--⨯= Consider three cases:ROE < r ⇒ (P 0/BVPS) < 1 ROE = r ⇒ (P 0/BVPS) = 1 ROE > r ⇒ (P 0/BVPS) > 1Thus, as ROE increases, the price-to-book ratio also increases, and, when ROE = r, price-to-book equals one. 28.Assume the portfolio value given, $100 million, is the value as of the end of the first year. Then, assuming constant growth, the value of the contract is given by the first payment (0.5 percent of portfolio value) divided by (r – g). Also:r = dividend yield + growth rateHence:r – growth rate = dividend yield = 0.05 = 5.0%Thus, the value of the contract, V, is:million $100.05million$1000.005V =⨯=For stocks with a 4 percent yield:r – growth rate = dividend yield = 0.04 = 4.0%Thus, the value of the contract, V, is:Chapter 04 - The Value of Common Stocks 4-11 million $12.50.04million $1000.005V =⨯=29. If existing stockholders buy newly issued shares to cover the $3.6 millionfinancing requirement, then the value of Concatco equals the discounted value of the cash flows (as computed in Section 4.5): $18.8 million.Since the existing stockholders own 1 million shares, the value pershare is $18.80.Now suppose instead that the $3.6 million comes from new investors, who buy shares each year at a fair price. Since the new investors buy shares at a fair price, the value of the existing stockholders’ shares must remain at $18.8 million. Since existing stockholders expect to earn 10% on their investment, the expected value of their shares in year 6 is:$18.8 million × (1.10) 6 = $33.39 millionThe total value of the firm in year 6 is:$1.59 million / (0.10 – 0.06) = $39.75 millionCompensation to new stockholders in year 6 is:$39.75 million – $33.39 million = $6.36 millionSince existing stockholders own 1 million shares, then in year 6, newstockholders will own:($6.36 million / $33.39 million) × 1,000,000 = 190,300 sharesShare price in year 6 equals:$39.75 million / 1.1903 million = $33.39。

财务管理(英语)-教学大纲