西方财务会计选择判断题

财务分析模拟题1

障倍数

13.企业风险较低的资产结构是( )。

A.稳健型结构 B.保守型结构 C.平衡型结构 D.风险型结

构

14.假设某企业在物价下跌时将存货计价方法由先进先出法改

为后进先出法,则这项会计政策变化对利润的影响是( )。

A.利润增加 B.利润减少 C.利润不变 D.不

一定15.下列现金流量比率中,最能够反映盈利质量的指标是

A.市盈率 B.利息保障倍数 C.剩余收益 D.资本积累率

二、多项选择题:

1.下列分析技术中,用于动态分析的有:( )。

A.结构分析 B.水平分析

C.趋势分析

D.比率分析 E.专题分析

2.企业的内部信息主要包括( )。

A.会计信息 B.统计信息与业务信息 C.预算

信息

D.计划信息

E.国家经济政策与法规信息

A.120% B.100% C.80% D.83.33%

10.主营业务利润率的标准值区段等级表如下:

标准系 优秀 良好 平均值 较低值 较差值

数 (1) (0.8) (0.6) (0.4) (0.2)

指标值 20% 16% 10% 6%

4%

某企业主营业务利润率的实际值为13%,该指标的

权数是14分,财务效益类指标的权数是40分,该类

( )。

A.流动比率 B.现金充分性比率 C.盈余现金保障倍数 D.现

金毛利率

16.销售品种构成变动之所以影响产品销售利润率,是因为(

)。

A.各产品价格不同

B. 各产品利润率不同

C.各产品单位成本不同 D. 各产品单位利润不

同

17.财务分析的最基本、最重要的方法是( )。

A.比率分析法 B.连环替代法 C.差额计算法 D.趋势分析

财务会计期末考试题及答案

财务会计期末考试题及答案一、单项选择题(每题2分,共20分)1. 会计的基本假设包括会计主体、持续经营、货币计量和以下哪一项?A. 会计分期B. 历史成本C. 权责发生制D. 公允价值答案:A2. 企业在编制财务报表时,应遵循的会计信息质量要求是?A. 相关性B. 可靠性C. 可比性D. 所有选项答案:D3. 以下哪项不是会计要素?A. 资产B. 负债C. 所有者权益D. 利润答案:D4. 对于固定资产的折旧,通常采用的方法是?A. 直线法B. 双倍余额递减法C. 年数总和法D. 所有选项答案:D5. 企业在进行利润分配时,应首先提取的是?A. 法定公积金B. 任意公积金C. 公益金D. 职工福利基金答案:A...(此处省略其他单项选择题)二、多项选择题(每题3分,共15分)1. 会计信息的质量要求包括以下哪些方面?A. 可靠性B. 相关性C. 及时性D. 可理解性答案:ABCD2. 会计政策变更的会计处理方法包括?A. 追溯调整法B. 未来适用法C. 直接调整法D. 重述法答案:AB3. 以下哪些属于财务报表的组成部分?A. 资产负债表B. 利润表C. 现金流量表D. 所有者权益变动表答案:ABCD...(此处省略其他多项选择题)三、判断题(每题1分,共10分)1. 会计的基本职能是核算和监督。

()答案:正确2. 会计分期是将企业持续经营的生产经营活动划分为若干个相等的会计期间。

()答案:正确3. 会计要素中的收入和费用应当在发生时确认。

()答案:错误...(此处省略其他判断题)四、简答题(每题5分,共10分)1. 简述会计信息的使用者及其信息需求。

答案:会计信息的使用者包括投资者、债权人、政府及其相关部门、企业管理者等。

投资者需要会计信息来评估企业的盈利能力、财务状况和风险,以做出投资决策;债权人需要了解企业的偿债能力和财务状况,以评估贷款风险;政府需要会计信息进行税收征管、经济政策制定等;企业管理者则需要会计信息进行日常经营决策和战略规划。

西方财务会计课后习题答案

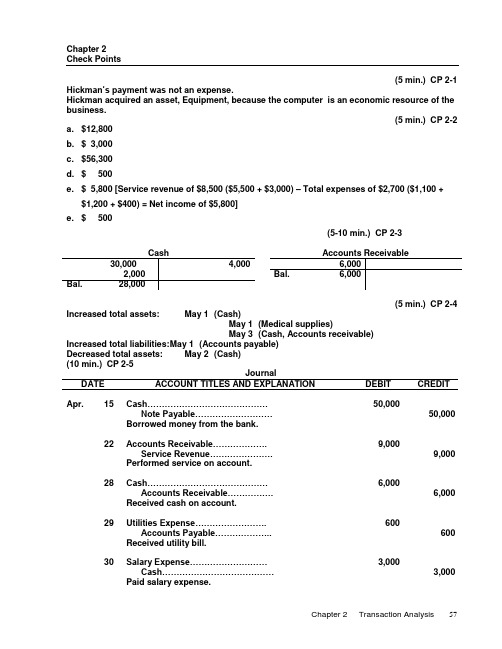

Chapter 2Check Points(5 min.) CP 2-1 Hickman’s payment was not an expense.Hickman acquired an asset, Equipment, because the computer is an economic resource of the business.(5 min.) CP 2-2a. $12,800b. $ 3,000c. $56,300d. $ 500e. $ 5,800 [Service revenue of $8,500 ($5,500 + $3,000) – Total expenses of $2,700 ($1,100 +$1,200 + $400) = Net income of $5,800]e. $ 500(5-10 min.) CP 2-3Cash Accounts Receivable 30,000 4,000 6,0002,000 Bal. 6,000Bal. 28,000(5 min.) CP 2-4 Increased total assets: May 1 (Cash)May 1 (Medical supplies)May 3 (Cash, Accounts receivable)Increased total liabilities: M ay 1 (Accounts payable)Decreased total assets: May 2 (Cash)(10 min.) CP 2-5JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Apr. 15 Cash……………………………………50,000Note Payable………………………50,000 Borrowed money from the bank.22 Accounts Receivable……………….9,000Service Revenue………………….9,000 Performed service on account.28 Cash……………………………………6,000Accounts Receivable…………….6,000 Received cash on account.29 Utilitie s Expense (600)Accounts Payable (600)Received utility bill.30 Salary Expense………………………3,000Cash…………………………………3,000 Paid salary expense.Chapter 2 Transaction Analysis 5730 Interest Expense (300)Cash (300)Paid interest expense.(10-15 min.) CP 2-6Req. 1JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Supplies………………………………..2,000Accounts Payable…………………2,000 Purchased supplies on account.Accounts Payable (500)Cash (500)Paid cash on account.Req. 2Accounts Payable500 2,000Bal. 1,500Req. 3Biaggi’s business owes $1,500, as shown in the Accounts Payable account.(10-15 min.) CP 2-7Req. 1JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Accounts Receivable………………..1,200Service Revenue…………………..1,200 Performed service on account.Cash (500)Accounts Receivable (500)Received cash on account.Req. 2Cash Accounts Receivable Service Revenue500 1,200 500 1,200 Bal. 500 Bal. 700 Bal. 1,200 Req. 3a. The Center earned $1,200: S ervice Revenueb. Total assets $1,200: C ash………………….. $ 500Accounts receivable. 700Total assets…………. $1,20058Financial Accounting 6/e Solutions Manual(10 min.) CP 2-8Old NavyTrial BalanceDecember 31, 20X8ACCOUNT DEBIT CREDITMillionsCash……………………….…...$ 2Other assets (9)Accounts payable……………$ 1Other liabilities (2)Stockholders’ equity (2)Revenues (30)Expenses……………………... 24 ___Total……………………….……$35 $35Old Navy’s net income:$6 million ($30 – $24)(10 min.) CP 2-9 1. Total assets = $53,800 ($33,300 + $2,000 + $500 +$18,000)2. Total liabilities = $1003. Total stockholders’ equity = $53,700 ($53,800 – $100)4. Net income = $5,800 ($8,500 – $1,100 – $1,200 – $400)(10 min.) CP 2-101. Total debits = $121,600 ($58,600 + $81,000 – $18,000)Total credits = $ 58,600Difference = $ 63,000 ($121,600 – $58,600)$63,000 / 9 = $7,000 (an integer), which suggests either atransposition or a slide2. Total debits = $76,600 ($58,600 + $20,000 – $2,000)Total credits = $58,600Difference = $18,000 ($76,600 – $58,600)$18,000 / 9 = $2,000 (original amount of accountsreceivable)3. Total debits = $56,600 ($58,600 – $ 2,000)Total credits = $60,600 ($58,600 + $ 2,000)Difference = $ 4,000 ($60,600 – $56,600)$4,000 / 2 = $2,000 (original amount of accounts receivable)Chapter 2 Transaction Analysis 59(5 min.) CP 2-12Cash Computer Equipment250,000 100,000Accounts Payable Common Stock100,000 250,000Total debits = $350,000 ($250,000 + $100,000)Total credits = $350,000 ($100,000 + $250,000)Exercises(10-15 min.) E 2-1 TO: Home OfficeFROM: Store ManagerDuring the first week, I borrowed $320,000 on a note payable. I used the store’s beginning cash plus the borrowed money to purchase land, a building, copy equipment, and supplies. After all these transactions, the store’s balance sheet appears as follows:Kinko’sOklahoma City StoreBalance SheetDateASSETS LIABILITIESCash $ 80,000* Note payable $320,000 Supplies 10,000Copy equipment 60,000 STOCKHOLDERS’ EQUITYLand 90,000 Common stock 40,000 Building 120,000 Total liabilities and ________ Total assets $360,000 stockholders’ equity $360,000 _____*$40,000 + $320,000 – $90,000 – $120,000 – $60,000 – $10,000 = $80,000(5-10 min.) E 2-2 a. Issuance of stockRevenue transactionb. Purchase of asset on accountBorrow moneyc. Purchase of asset for cashSale of asset for cashCollection of an account receivabled. Payment of dividends to ownersExpense transactione. Pay a liability60Financial Accounting 6/e Solutions Manual(10-20 min.) E 2-4 Req. 1Analysis of TransactionsASSETS = LIABILITIES + STO CKHOLDERS’ EQUITYDate Cash + AccountsReceivable +MedicalSupplies + Land =AccountsPayable +NotePayable +CommonStock +RetainedEarningsType of Stockholders’Equity TransactionOct. 6 40,000 40,000 Issued stock9 (30,000) 30,00012 2,000 2,00015 Not a transaction of the business.15-31 4,000 4,000 8,000 Service revenue 15-31 (1,400) (1,400) Salary expense (1,000) (1,000) Rent expense(300) (300) Utilities expense31 500 (500)31 10,000 10,00031 (1,500) (1,500)Bal. 20,300 4,000 1,500 30,000 500 10,000 40,000 5,30055,800 55,800Chapter 2 Transaction Analysis 61(continued) E 2-4 Req. 2a. $55,800b. $4,000c. $10,500 ($500 + $10,000)d. $45,300 ($55,800 – $10,500, or $40,000 + $5,300)e. $5,300 (Revenue, $8,000 minus total expenses of $2,700, equals net income, $5,300.)62Financial Accounting 6/e Solutions Manual(10-15 min.) E 2-5JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Oct. 6 Cash………………………………………..40,000Common Stock……………………….40,000 Issued stock to owner.9 Land………………………………………...30,000Cash…………………………………….30,000 Purchased land.12 Medical Supplies…………………………2,000Accounts Payable……………………2,000 Purchased supplies on account.15 Not a transaction of the business.15-31 Cash………………………………………..4,000Accounts Receivable……………………4,000Servi ce Revenue……………………..8,000 Performed service for cash and on account.15-31 Salary Expense…………………………..1,400Rent Expense……………………………..1,000Utilities Expense (300)Cash…………………………………….2,700 Paid expenses.31 Cash (500)Medical Supplies (500)Sold supplies.31 Cash………………………………………..10,000Note Payable…………………………..10,000 Borrowed money.31 Accounts Payable……………………….1,500Cash…………………………………….1,500 Paid on account.(10-15 min.) E 2-6 Req. 1Total assets = $145 million ($100 + $60 – $55 + $35 + $26 – $21)Req. 2Company owes $41 million [$60 – $55 + $35 + $22 – $21]Req. 3Net income = $4 million ($26 – $22)Chapter 2 Transaction Analysis 63(10-20 min.) E 2-7 Req. 1 (journal entries)JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Aug. 1 Cash……………………………………………19,500Common Stock…………………………...19,500 Issued common stock to owner.2 Office Supplies (800)Accounts Payable (800)Purchased office supplies on account.4 Land……………………………………………14,000Cash………………………………………..14,000 Paid cash for land.6 Cash……………………………………………2,000Service Revenue…………………………2,000 Performed services for cash.9 Accounts Payable (100)Cash (100)Paid cash on account.17 Accounts Receivable……………………….1,200Service Revenue…………………………1,200 Performed service on account.23 Cash (900)Accounts Receivable (900)Received cash on account.31 Salary Expense………………………………1,000Rent Expense (500)Cash………………………………………..1,500 Paid cash expenses.(continued) E 2-7Req. 2Ending cash = $6,800($19,500 – $14,000 + $2,000 – $100 + $900 – $1,500)Expects to collect on account = $300 ($1,200 – $900)Total liabilities = $700 ($800 – $100)Net income (profit) = $1,700 ($2,000 + $1,200 – $1,000 – $500)64Financial Accounting 6/e Solutions Manual(20-30 min.) E 2-8 Req. 1Cash Accounts ReceivableAug. 1 19,500 Aug. 4 14,000 Aug. 17 1,200 Aug. 23 9006 23 2,0009009311001,500Aug. 31 300Aug. 31 6,800Office Supplies LandAug. 2 800 Aug. 4 14,000Aug. 31 800 Aug. 31 14,000Accounts Payable Common StockAug. 9 100 Aug. 2 800 Aug. 1 19,500 Aug. 31 700 Aug. 31 19,500 Service Revenue Salary ExpenseAug. 6 2,000 Aug. 31 1,00017 1,200 Aug. 31 1,000Aug. 31 3,200Rent ExpenseAug. 31 500Aug. 31 500(continued) E 2-8Req. 2Coaxial Electronic Systems, Inc.Trial BalanceAugust 31, 20X6ACCOUNT DEBIT CREDITCash…………………………...$ 6,800Accounts receivable (300)Office supplie s (800)Land…………………………...14,000Accounts payable…………..$ 700Common stock………………19,500Service revenue……………..3,200Salary expense………………1,000Rent expense (500)Total…………………………...$23,400 $23,400Req. 3Total a ssets ($6,800 + $300 + 800 + $14,000)……..$21,900Total liabilities (700)Total stockholders’ equity ($21,900 –$700)………$21,200Chapter 2 Transaction Analysis 65(10-15 min.) E 2-9JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT1. Cash…………………………………..10,000Common Stock…………………..10,000 Issued common stock.2. Cash…………………………………..7,000Note Payable……………………..7,000 Borrowed money; signed note payable.3. Land…………………………………..31,000Cash………………………………..8,000Note Payable……………………..23,000 Purchased land by paying cashand signing a note payable.4. Supplies (600)Accounts Payable (600)Purchased supplies on account.5. Cash (100)Su pplies (100)Sold supplies for cash.6. Equipment……………………………6,000Cash………………………………..6,000 Paid cash for equipment.7. Accounts Payable (300)Cash (300)Paid cash on account.Cash balance = $2,800 ($10,000 + $7,000 – $8,000 + $100 – $6,000 – $300)Company owes $30,300 ($7,000 + $23,000 + $600 – $300)(10-20 min.) E 2-10Req. 1Whirlpool Appliance ServiceTrial BalanceJune 30, 20X6ACCOUNT DEBIT CREDIT Cash…………………………...$ 9,000Accounts receivable………..15,500Building……………………….40,250Land…………………………...29,000Accounts payable………….. $ 4,300Note payable………………… 13,000Common stock……………… 48,800Retained earnings………….. 21,350*Dividends……………………..6,000Service revenue…………….. 22,00066Financial Accounting 6/e Solutions ManualSalary expense………………8,000Utilities expense…………….1,400Delivery expense (300)Total…………………………...$109,450 $109,450 *Total debits…………………………………………$109,450 Total credits, ex cluding retained earnings…… (88,100) Retained earnings…………………………………$ 21,350 (continued) E 2-10Req. 2Whirlpool Appliance ServiceIncome StatementMonth Ended June 30, 20X6Service revenue………………...$22,000Salary expense…………………$8,000Ut ilities expense………………..1,400Delivery expense (300)Total expenses…………………. 9,700Net income………………………$12,300 (15-25 min.) E 2-11Car Connection, Inc.Trial BalanceDecember 31, 20X3ACCOUNT DEBIT CREDIT Cash…………………………...$ 4,600*Accounts receivable……….. 12,600*Inventory……………………... 17,000Supplies (600)Land…………………………... 55,000Accounts payable…………..$13,100*Common stock………………48,300*Sales revenue……………….. 35,700Cost of goods sold…………. 3,900Salary expense……………… 1,700Rent expense (800)Utilities expense……………. 900* _______Total…………………………...$97,100 $97,100_____*Explanations:Cash: $4,200 + $400 = $4,600Accounts Receivable: $13,000 – $400 = $12,600Accounts Payable: $12,000 + $1,000 – $100 + $200 = $13,100Common Stock: $47,900 + $400 = $48,300Utilities Expense: $700 + $200 = $900(5-15 min.) E 2-12 Cash Accounts Receivable(a) 12,500 (b) 1,500 (f) 8,300(d) 1,800 Bal. 8,300(e) 400(g) 2,000Bal. 6,800Office Supplies Office Furniture(c) 800 (a) 9,000Bal. 800 Bal. 9,000Accounts Payable Common Stock(e) 400 (c) 800 (a) 21,500Bal. 400 Bal. 21,500 Dividends Service Revenue(g) 2,000 (f) 8,300 Bal. 2,000 Bal. 8,300 Salary Expense Rent Expense(d) 1,800 (b) 1,500Bal. 1,800 Bal. 1,500(10-20 min.) E 2-13Req. 1LaVell Oxford, AttorneyTrial BalanceJuly 31, 20X8ACCOUNT DEBIT CREDITCash…………………………...$ 6,800Accounts receivable………..8,300Office supplies (800)Office furniture………………9,000Accounts payable…………..$ 400Common stock………………21,500Dividends……………………..2,000Service revenue……………..8,300Salary expense………………1,800Rent expense……………….. 1,500Total…………………………...$30,200 $30,200Req. 2The business performed well during July. The result of operations was net income of $5,000, as shown by the income statement accounts:Service revenue………………….$ 8,300Salary expense………..$1,800Rent expense…………. 1,500Total expenses……………….. (3,300)Net income……………………….. $ 5,000(20-30 min.) E 2-14Reqs. 1 and 3Cash Accounts ReceivableDec. 2 7,000 Dec. 2 500 Dec. 18 1,7009 800 3 3,00012 200Bal. 4,100Supplies EquipmentDec. 5 300 Dec. 3 3,000Furniture Accounts PayableDec. 4 3,600 Dec. 4 3,6005 300Bal. 3,900 Common Stock DividendsDec. 2 7,000Service Revenue Rent ExpenseDec. 9 800 Dec. 2 50018 1,700Bal. 2,500Utilities Expense Salary ExpenseDec. 12 200(continued) E 2-14Req. 2JournalDATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Dec. 2 Cash……………………………………..7,000Common Stock……………………..7,0002 Rent Expense (500)Cash (500)3 Equipment……………………………...3,000Cash………………………………….3,0004 Furniture………………………………..3,600Accounts Payable………………….3,6005 Supplies (300)Accounts Payable (300)9 Cash (800)Service Revenue (800)12 Utilities Expense (200)Cash (200)18 Accounts Receivable…………………1,700Service Revenue…………………...1,700 (continued) E 2-14Req. 4Matthew Rogers, Certified Public Accountant, P.C.Trial BalanceDecember 18, 20XXACCOUNT DEBIT CREDIT Cash…………………………...$ 4,100Accounts receivable………..1,700Supplies (300)Equipment……………………3,000Furniture……………………...3,600Accounts payable…………..$ 3,900Common stock………………7,000Dividends……………………..—Service revenue……………..2,500Rent expense (500)Utilities expense (200)Salary expense………………—Total…………………………...$13,400 $13,400(20-40 min.) E 2-15a. Net income for March – Given as follows:Retained EarningsFeb. 28 Bal. 7,000MarchMarch dividends 15,800 net income X = $19,300Mar. 31 Bal. 10,500$7,000 + X – $15,800 = $10,500X = $19,300b. Total cash paid during March:CashFeb. 28 Bal. 11,600March receipts 81,200 March payments X = $87,800Mar. 31 Bal. 5,000$11,600 + $81,200 – X = $ 5,000X = $87,800 (continued) E 2-15c. Cash collections from customers during March:Accounts ReceivableFeb. 28 Bal. 24,300March saleson account 49,400 March collections X = $47,000 Mar. 31 Bal. 26,700$24,300 + $49,400 – X = $26,700X = $47,000d. Cash paid on a note payable during March:Note PayableFeb. 28 Bal. 13,900 March MarchX =17,500 payments on note X new borrowing 25,000Mar. 31 Bal. 21,400 $13,900 + $25,000 – X = $21,400X = $17,500(20-30 min.) E 2-16Req. 1Road Runner, Inc.Trial BalanceDecember 31, 20X5Cash…………………………...$ 4,200Accounts receivable………..7,200Supplies (800)Land…………………………...34,000Accounts payable…………..$ 5,800Note payable…………………5,000Common stock………………20,000Retained earnings…………..7,300Service revenue……………..9,100Salary expense………………3,400Advertising expense………. 900 _______Totals………………………….$50,500 $47,200Out of balanceby $3,300The correct balance of Accounts Receivable is $3,900 ($7,200 – $3,300). After this correction, total debits will be $47,200 ($50,500 – $3,300), the same as total credits.(continued) E 2-16Req. 2Road Runner, Inc.Trial BalanceDecember 31, 20X5Cash ($4,200 –$400)……………………$ 3,800Accounts receivable($7,200 –$3,300 + $7,000)..............10,900 Supplies.. (800)Land ($34,000 + $80,000)………………114,000Accounts payable ($5,800 + $2,000)…$ 7,800 Note payable ($5,000 + $80,000)……...85,000 Common stock…………………………..20,000 Retained earnings………………………7,300 Service revenue ($9,100 + $7,000)……16,100 Salary expense ($3,400 + $400)………3,800Advertising expense ($900 + $2,000). 2,900Tot als……………………………………...$136,200 $136,200Req. 3a. Total assets = $129,500 ($3,800 + $10,900 + $800 + $114,000).b. Road Runner is profitable, as indicated by the excess of revenue ($16,100) over totalexpenses ($6,700 = $3,800 + $2,900).(10-15 min.) E 2-17San Francisco:Income statement June July Medical expense…………..$40,000 $ -0- Balance sheet June 30 July 31 Cash…………………………$55,000 $23,000*Accounts payable…………40,000 8,000** Bay Area:Income statement June July Service revenue…………..$40,000 $ -0- Balance sheet June 30 July 31 Cash………………………… $ -0- $32,000Accounts receivable……..40,000 8,000**Explanation:San Francisco’s expense is Bay Area’s revenue.San Francisco’s cash payment is Bay Area’s cash receipt.San Francisco’s account payable is Bay Area’s account receivable. __________*$55,000 – $32,000 = $23,000**$40,000 – $32,000 = $ 8,000。

财务会计练习题(二)

财务会计练习题(二)姓名:学号一、判断题1、先进先出法在定期盘存制和永续盘存制下核算的结果是相同的(T)2、根据收入实现原则,收入的确认应当与现金的收取时间保持一致(F)3、注销应收账款时,在直接转销法下,既会影响流动资产总额,也会影响当期净收益(T)4、注销应收账款时,在备抵法下,既不会影响流动资产总额,也不会影响当期净收益(T)5、在永续盘存制下,存货的溢缺都隐含在存货的销售成本中,无法单独反映(F)6、存货发出计价方法的选择可能会影响公司当年收益,但不会影响公司年末总资产(F)7、固定资产的折旧是指将固定资产的原始成本扣除净残值之后在其估计有效使用年限内摊配为费用的过程(T)8、在固定资产使用的早期,与直线法相比,采用加速折旧法核算出来的净收益、资产总额、所有者权益均较低。

(T)9、借贷方出现现金账户的会计分录不可能会是调整分录(T)10、无论是采用后进先出法还是先进先出法,在两种盘存制下核算的结果都是相同的(F)11、收付实现制下,收入和费用的确认,分别应与现金的收取与支出时间保持一致(T)12、公司将资本性支出作为收益性支出进行确认,会减少公司当年利润(T)13、期末会计人员忘记计提坏帐准备,将会高估资产、收益和股东权益(T)14、利得和损失一定会影响当期损益(F)15、企业在一定期间发生亏损,但企业在这一会计期间的所有者权益不一定减少(T)16、因商业折扣在销售发生时已发生,企业应按扣除商业折扣前的净额确认销售收入(T)二、单项选择题1、下列各项中,应计入坏账准备贷方的有(D)。

A.发生的坏账款B.应收账款的收回C.冲减多提的坏账准备D.收回已转销的坏账2.下列项目中,不属于本企业存货范围的是(A)。

A.受托代销的商品B.购入并自行加工的材料C.库存商品D.委托外部加工的材料3、企业收回代购货方垫付的运杂费时,应贷记(C)账户。

A.银行存款B.其他应收款C.应收账款D.其他业务收入4、在物价持续上涨期间,采用(A)使得当期利润最少。

财务会计考试试题及答案

财务会计考试试题及答案一、单项选择题(每题2分,共20分)1. 会计的基本职能是()。

A. 核算和监督B. 预测和决策C. 计划和控制D. 组织和协调答案:A2. 会计要素中,反映企业财务状况的是()。

A. 资产B. 负债C. 所有者权益D. 收入答案:C3. 会计核算的基本原则是()。

A. 历史成本原则B. 权责发生制原则C. 配比原则D. 持续经营原则答案:B4. 以下哪项不是会计信息质量要求()。

A. 可靠性B. 相关性C. 及时性D. 可比性答案:C5. 资产负债表中,资产的排列顺序是()。

A. 按流动性大小B. 按金额大小C. 按取得时间D. 按重要性答案:A6. 利润表中,利润的计算公式是()。

A. 收入 - 费用B. 资产 - 负债C. 所有者权益 - 负债D. 收入 - 成本答案:A7. 以下哪项不是会计政策变更()。

A. 存货计价方法的变更B. 固定资产折旧方法的变更C. 会计估计的变更D. 会计差错的更正答案:C8. 会计估计变更的会计处理方法是()。

A. 追溯调整法B. 未来适用法C. 重述法D. 差额调整法答案:B9. 以下哪项不是会计差错更正的方法()。

A. 追溯重述法B. 未来适用法C. 差额调整法D. 重述法答案:B10. 会计报表附注中,不需要披露的信息是()。

A. 会计政策和会计估计变更B. 重要会计估计的不确定性C. 会计差错更正D. 企业未来的经营计划答案:D二、多项选择题(每题3分,共15分)1. 以下哪些属于会计核算的内容()。

A. 资产的取得B. 负债的清偿C. 收入的确认D. 费用的支付答案:ABC2. 会计信息质量要求包括()。

A. 可靠性B. 及时性C. 相关性D. 可理解性答案:ABCD3. 以下哪些属于会计政策变更()。

A. 存货计价方法的变更B. 固定资产折旧方法的变更C. 会计估计的变更D. 会计差错的更正答案:AB4. 以下哪些属于会计差错更正的方法()。

财务会计试题5

一、单项选择题(本题型共10 题。

答案正确的,每题得 1 分。

本题型共10 分。

)1.企业在对会计要素计量时普通应采用()。

BA.公允价值B.历史成本C.重置成本D.现值E、可变现净值2.某公司采用应收账款余额百分比法按5‰的比例计提坏账准备,该公司年末应收账款余额为120 000 元, “坏账准备”科目贷方期初余额为200 元,则本年应计提的坏账准备为()。

CA.600 元B.800 元C.400 元D.200 元3.在物价持续上涨且当期有多次购进和发出业务的情况下,能够肯定发出存货成本最低的计价方法是()。

BA.个别计价法B.先进先出法C.挪移加权平均法D.月末一次加权平均法4.企业2005 年以50 000 元取得一项专利权,在2022 年1 月10 日以30 000 元出售,款已存银行。

假定营业税率为5%(不考虑其它税费),至出售前累计摊销20 000 元(未提减值准备)。

则下列处理符合现行规定的是()。

BA.借记“营业外支出”1 500 元B.借记“其他业务成本”1 500 元C.借记“营业外支出”20 000 元D.借记“其他业务成本”20 000 元5.下列资产中,确认其减值损失时不应贷记“××减值准备”科目的是()。

A.无形资产B.持有至到期投资C.可供出售金融资产D.长期股权投资6.按现行会计准则的规定,下列各项中不能作为收入确认的是()。

A. 出租固定资产的租金收入B. 出售固定资产的价款收入C.长期债券投资的利息收入D. 出租包装物的租金收入E.处置投资性房地产的价款收入7.下列税金中,应计入固定资产入账价值的是()。

A.房产税B.土地使用税C. 印花税D.耕地占用税E.车船使用税8.某企业2022 年用银行存款偿还银行的各种借款本金共计500 万元,支付的借款利息计50 万元,摊销利息调整金额计10 万元。

则该企业在编制现金流量表时,“偿还债务支付的现金”项目应填列的金额为()万元。

财务会计英文版选择判断题练习

14 Chapters’ MCQChapter 11. The functions of an accounting system include all of the following except to:a. gather marketing data.b. handle routine bookkeeping tasks.c. structure information so that it can be used to evaluate performance of a business.d. analyze transactions.--------------------------------------------------------------------------------2 Accounting information is useful for several kinds of decisions. For which decision situation would accounting information NOT be useful?a. Bankers evaluating the riskiness of loans.b. Corporate managers controlling costs.c. Production managers evaluating the quality of materials used in manufacturing.d. Corporate managers setting prices.--------------------------------------------------------------------------------3 The primary users of external financial reports are:a. those who direct day-to-day operations of a business enterprise.b. individuals who have an economic interest in the firm but who are not part of management.c. managers of an enterprise who plan, implement plans, and control costs.d. none of the above.--------------------------------------------------------------------------------4 Which primary financial statement shows a business enterprise's resources, obligations, and equities?a. Statement of cash flowsb. Balance sheetc. Income statementd. Statement of retained earnings--------------------------------------------------------------------------------5 Which primary financial statement shows a business enterprise's excess of revenues over expenses?a. Statement of cash flowsb. Balance sheetc. Income statementd. Statement of retained earnings--------------------------------------------------------------------------------6 Which of the following is NOT true of the Securities and Exchange Commission (SEC)?a. The SEC is charged with protecting investors from losing money.b. Congress has given the SEC specific legal authority to establish accounting standards.c. As a result of the accounting scandals of 2001-2002, the SEC was given more authority to set standards.d. The SEC could take over the role of standard setting in accounting if the FASB loses credibility.7 Which of the following is NOT true regarding the International Accounting Standards Board (IASB)?a. IASB standards are gaining increasing acceptance throughout the world.b. The purpose of the IASB is to harmonize conflicting accounting standards of various countries.c. The accounting standards produced by the IASB are referred to as International Financial Reporting Standards (IFRS's) Note: the 200 country reference was not cited in the text.d. The IASB standards are accepted in the United States.--------------------------------------------------------------------------------8 Several organizations have developed codes of ethics for accountants. Which of the following organizations did NOT develop a code of ethics for accountants?a. American Institute of Certified Public Accountants (AICPA)b. Institute of Management Accountants (IMA)c. Securities Exchange Commission (SEC)d. All of the above developed a code of ethics for accountants.--------------------------------------------------------------------------------9 Technology has impacted accounting in many ways. Which of the following is NOTa change in accounting due to technology?a. Technology has replaced judgment.b. Technology has allowed users access to more than just summarized data.c. Technology allows more detailed information to be gathered.d. Technology has reduced the likelihood of errors in accounting data.Chapter 21.Obligations to pay cash, transfer other assets, or provide services are:a. assets.b. liabilities.c. equities.d. expenses.--------------------------------------------------------------------------------2 The interrelationships among the financial statements is called:a. disclosure.b. articulation.c. recognition.d. reconciliation.--------------------------------------------------------------------------------3 The statement of financial position is also known as the:a. statement of cash flows.b. balance sheet.c. income statement.d. retained earnings statement.--------------------------------------------------------------------------------4 Which of the following is NOT normally considered to be an asset?a. Retained earningsb. Cashc. Buildingsd. Accounts receivable--------------------------------------------------------------------------------5 If a company has $15,000 in assets and $10,000 in equities, then liabilities are:a. $25,000.b. $10,000.c. $5,000.d. $0.--------------------------------------------------------------------------------6 Assets consumed through business operations are called:a. liabilities.b. expenses.c. equities.d. net income.--------------------------------------------------------------------------------7 Gross profit is calculated as:a. Sales - Cost of goods sold.b. Sales - Operating expenses.c. Sales - All expenses.d. Sales - Income tax expense.--------------------------------------------------------------------------------8 When preparing a statement of cash flows, activities associated with buying and selling assets are:a. operating activities.b. investing activities.c. financing activities.d. revenue activities.--------------------------------------------------------------------------------9 If a corporation has assets of $250,000, liabilities of $70,000, and capital stock of $120,000, what is the amount of retained earnings?a. $30,000b. $0c. $60,000d. $140,000--------------------------------------------------------------------------------10 The idea that the business will continue to operate for the foreseeable future is known as the:a. arm's-length transaction assumption.b. entity concept.c. going concern assumption.d. monetary measurement concept.--------------------------------------------------------------------------------11 The idea that a business is considered to be separate from its individual owners is known as the:a. arm's-length transaction assumption.b. entity concept.c. going concern assumption.d. monetary measurement concept.--------------------------------------------------------------------------------12 In order for the data of a transaction to be accurately represented, an assumption must be made that the transaction was conducted between buyer and seller with no bias toward either party. This concept is called the:a. arm's-length transaction assumption.b. entity concept.c. going concern assumption.d. monetary measurement concept. chapter 31 When owners invest money in their business, the effect on the accounting equation is that the investment:a. increases assets and decreases owners' equity.b. increases assets and increases liabilities.c. decreases assets and decreases owners' equity.d. increases assets and increases owners' equity.--------------------------------------------------------------------------------2 The purchase of inventory on credit:a. increases assets and decreases liabilities.b. increases liabilities and decreasesassets.c. increases assets and increases liabilities.d. decreases assets and decreases liabilities.--------------------------------------------------------------------------------3 A revenue account is increased with:a. debits.b. credits.c. equities.d. none of the above.--------------------------------------------------------------------------------4 A company's retained earnings balance is increased by:a. net income.b. expenses.c. investments by owners.d. the declaration and payment of dividends.--------------------------------------------------------------------------------5 Which of the following accounts would normally have a debit balance?a. Revenuesb. Expensesc. Liabilitiesd. Owner's Equity--------------------------------------------------------------------------------6 When transactions are posted from the book of original entry, they are posted to the:a. general journal.b. general ledger.c. work sheets.d. trial balance.--------------------------------------------------------------------------------7 Bosso Company repaid a note payable of $20,000 and the interest due of $400. The journal entry to record this transaction would include a:a. debit to cash.b. credit to notes payable.c. debit to interest expense.d. credit to interest revenue.--------------------------------------------------------------------------------8 The journal entry to record the payment of wages in the amount of $52,000 to workers could include a:a. debit to wages expense.b. credit to accounts payable.c. debit to cash.d. credit to wages expense.--------------------------------------------------------------------------------9 The entry to record the collection of cash from customers would include a:a. debit to accounts receivable.b. debit to sales revenue.c. credit to cash.d. debit to cash.--------------------------------------------------------------------------------10 When a company earns revenue from sales to customers, the effects on the accounting equation may be:a. assets are increased, equities are decreased.b. assets are decreased, equities are decreased.c. assets are decreased, equities are increased.d. assets are increased, equities are increased.--------------------------------------------------------------------------------11 Wagner Inc. had a beginning cash balance of $14,000 on January 1, 2005. During January, the company recorded debits of $23,000 and credits of $25,000 to the cash account. The ending cash balance on January 31 would be a:a. debit balance of $16,000.b. credit balance of $16,000.c. debit balance of $12,000.d. credit balance of $12,000.--------------------------------------------------------------------------------12 On March 1, 2005, the Cruston Company had a beginning balance in the accounts payable account of $30,000. During March, the company recorded debits of $52,000 and credits of $47,000 to accounts payable. The ending accounts payable balance on March 31 would be a:a. debit balance of $35,000.b. credit balance of $35,000.c. debit balance of $25,000.d. credit balance of $25,000.--------------------------------------------------------------------------------13 The term "compound entry" means that the journal entry has:a. more than two accounts involved in the entry.b. a debit amount greater than the credit amount.c. a credit amount greater than the debit amount.d. a debit amount less than a credit amount.--------------------------------------------------------------------------------14 After preparing its trial balance, the Wright-Way Company found that total debits equaled total credits. This equality would assure the company that:a. there are no errors in the accounting records.b. no transactions were omitted from the accounting records.c. no transactions were recorded incorrectly.d. the accounting equation is in balance.Chapter 41 The idea that the expenses incurred to generate revenue for a given period should be matched against that revenue is called the:a. revenue recognition principle. 收入确认原则The idea that revenues should be recorded when 1the earnings process has been substantially completed and 2cash has either been collected or collectibility is reasonably assured.b. realization concept.c. time period concept. The idea that the life of a business is divided into distinct and relatively short time periods so that accounting information can be timelyd. matching principle. 配比原则the concept that all costs and expense incurred in generating revenues must be recognized in the same reporting period as the related revenues--------------------------------------------------------------------------------2 The process of dividing a company's operations into separate and distinct time periods so that reports can be prepared on a timely basis is the:a. fiscal year concept. --------------b. revenue recognition principle.c. matching concept.d. time period concept.3 During 2005, the Latrex Corporation had cash and credit sales of $47,000 and $45,500 respectively. The company also collected accounts receivable of $26,700 and incurred expenses of $68,500, 80 percent of which were paid during the year. In addition, Latrex paid $24,000 for a 12-month building rental, beginning on July 1, 2005. Latrex's accrual-basis (权责发生制)net income (loss) for 2005 was: a. $12,000. b. $25,700.c. $0.d. $38,700. --------------------------------------------------------------------------------4 No matter the type of adjusting entry , which of the following accounts would not be affected by an adjusting entry?a. Cashb. Unearned revenuec. Rent expensed. Prepaid insurance--------------------------------------------------------------------------------5 A revenue that is collected before it has been earned is called a(n):a. accrued revenue. 应计收入,是指已实现但尚未收到款项的收入。

财务会计 英文选择题

1. In which of the following depreciation methods are the depreciation costs the highest in the first year of the asset's life?Choose onea. decreasing residue methodb. production method of depreciationc. under none of the above depreciation methodsd. linear depreciation methodA2. Are not external users of accounting information:Choose onea. tax authoritiesb. suppliersc. trade unionsd. potential investorse. managersf. current creditorsE3.Which of the following does NOT belong to the minimum required information to be presented on the face of the statement of comprehensive income in accordance with International Financial Reporting Standards?Choose onea. the dividends distributed during the yearb. tax costsc. components of other comprehensive incomed. incomee. total comprehensive income for the periodf. profit or loss from discontinued operationsg. financial costsF4. The variable overhead costs are:Choose onea. those direct and indirect (indirect) costs that directly depend on changes in production volume, such as direct and indirect laborb. all major technological costs of productionc. any additional production costsd. those indirect costs that change directly or almost directly depending on changes in production volume, such as indirect labor and indirect materialse. those direct costs that change directly or almost directly depending on changes in production volume, such as direct labor and direct materialsD5.Which of the following is NOT a criterion for classifying a liability as current?Choose onea. the liability is held primarily for commercial purposesb. the liability is expected to be settled within 12 m after the end of the reporting periodc. the enterprise has no unconditional right to postpone the settlement of the obligation by at least 12 months after the end of the reporting periodd. the liability is expected to be settled within the normal operating cycle of the entitye. there is no correct answerE6. At the end of the reporting period it is established that the provision accrued during the previous reporting period was overestimated by BGN 20,000. What accounting item should be drawn up in this case?Choose onea. Debit account "Provisions for warranty service" 20 000, Credit account "Other income" 20 000b. Debit account "Provisions for warranty service" 20 000, Credit account "Sales revenues" 20 000c. Debit account "Provisions for warranty service" 20 000, Credit account "Other expenses" 20 000d. Debit account "Expenses for provisions" (20 000), Credit account "Provisions for warranty service" (20 000) - by the red reversal methodD7.Which of the following is NOT an outgoing cash flow from investing activities for a manufacturing enterprise?Choose onea. Repurchase of own sharesb. Cash payments for the purchase of a software productc. Loan granted to a subsidiaryd. Cash payments for the purchase of investments in associatese. All of the above are cash outflows from investing activitiesf. Advance paid for the purchase of a machineE8. The accounting of the impairment of materials is as follows:Choose onea. We debit the account "Expenses for impairment of inventories" and credit the account "Impairment of materials", but with negative amountsb. We debit the account "Impairment of materials" and credit the account "Expenses for impairment of inventories"c. We debit the "Materials" account and credit the "Materials Impairment" accountd. We debit the account "Impairment of materials" and credit the account "Expenses for impairment of inventories", but with negative amountse. We debit the account "Expenses for impairment of inventories" and credit the account "Impairment of materials"f. We debit the account "Impairment of materials" and credit the account "Other expenses"B9. The initial malt on the account "Provisions for warranty service" is BGN 12,000. The accrued expenses for provisions during the reporting period are BGN 45,000. the following accounting item is drawn up:Choose onea. Debit account "Costs for provisions" 60 000, Credit account "Provisions for warranty service"60 000b. Debit account "Provisions for warranty service" 45 000, Debit account "Other expenses" 15 000, Credit account "Cash" 60 000c. Debit account "Provisions for warranty service" 57 000, Debit account "Expenses for provisions" 3 000, Credit account "Cash" 60 000d. Debit account "Expenses for provisions" 60 000, Credit account "Cash" 60 000e. Debit account "Provisions for warranty service" 60 000, Credit account "Cash" 60 000f. Debit account "Provisions for warranty service" 45 000, Debit account "Expenses for provisions"15 000, Credit account "Cash" 60 000F10.Which of the following is NOT a component of equity?Choose onea. fixed capitalb. legal reservesc. revaluation reserved. uncovered loss from previous yearse. financing for the acquisition of a tangible fixed assetf. premium reserveE11. What accounting item is compiled for reporting a received bank loan in the amount of BGN 120,000. Upon concluding the loan agreement, the enterprise has paid a management fee for the bank's tariff in the amount of BGN 6,300?Choose onea. Dt s / ka Skonto by financial instruments 6 300 and Dt s / ka Current account in BGN 113 700; Long-term bank loans received 120,000b. Dt s / ka Current account in BGN 120,000; Kt s / ka Long-term bank loans received 120 100c. Dt s / ka Received long-term bank loans 120,000; Kt s / ka Skonto by financial instruments 6 300 and Kt s / ka Current account in BGN 113 700d. Dt s / ka Current account in BGN 113,700; Long-term bank loans received 113,700C12. For which inventory do special accounting regulations apply, given its characteristics? Choose onea. unfinished construction under construction contractsb. delivery of goods by importc. unfinished delivery of auxiliary materialsd. combustible materialse. productsf. work in progressA13.Which of the following statements concerning the exchange of a tangible fixed asset for another asset is true?Choose onea. The cost of acquiring the asset received is equal to the carrying amount of the leased asset, less any payments made by the enterprise, plus the payment received by the company that leases the asset to the enterprise.b. If the asset is acquired for exchange with another non-monetary asset or with a combination of monetary and non-monetary assets, then the acquisition cost is the fair value of the leased assetc. If the asset is acquired in exchange for another non-monetary asset or a combination of monetary and non-monetary assets, then the acquisition cost is the fair value of the asset received if the transaction is of a non-commercial natured. A transaction is considered to be of a commercial nature if the cash flow scheme associated with the asset received, in terms of time, amount and risk, coincides with the cash flow scheme of the leased asset.e. If the fair value of the asset received cannot be determined, then the cost of acquisition is equal to the carrying amount of the leased asset, adjusted for cash payments.f. All these statements are not trueE14.Which of the following is NOT incoming cash flow from operating activities?Choose onea. Cash receipts from sale of productsb. Cash receipts of an insurance company from insurance premiumsc. Dividends received from holding companiesd. Cash receipts from commissionse. Interest received on loans from a financial institutionf. All specified cash inflows are from core businessC15.Which of the following methods for writing off inventories and determining the cost of sales is NOT eligible under International Financial Reporting Standards?Choose onea. last incoming, first outgoing priceb. all the listed assessment methods are acceptablec. method of specific identificationd. first incoming, first outgoing pricee. floating weighted average priceA16. The cancellation of impairment of materials reported in previous reporting periods may occur as:Choose onea. We debit the account "Impairment losses" and credit the account "Impairment of materials"b. We debit the "Materials" account and credit the "Materials Impairment" accountc. We debit the account "Impairment of materials" and credit the account "Other income"d. We debit the account "Impairment of materials" and credit the account "Recovered impairment"e. We debit the "Materials" account and credit the "Impairment losses" accountf. We debit the account "Impairment of materials" and credit the account "Impairment costs", but with negative amountsg. We debit the account "Impairment of materials" and credit the account "Materials"F17.If the fair value less costs to sell of an item of property, plant and equipment exceeds its carrying amount, it:Choose onea. its value in use must be determinedb. the present value of the deferred sale value must also be calculatedc. the asset is not impaired and it is not necessary to determine its value in used. it must be assumed that the asset is impairedC18. Research costs incurred by the enterprise:Choose onea. should be recognized as an intangible assetb. they must be recorded as current expenses for the period in which they are incurredc. should be accounted for as a reduction in development costsd. must be accounted for as an expense for future periodsB19.Which of the following information should NOT be disclosed in the notes to the financial statements based on International Financial Reporting Standards?Choose onea. management's estimates to determine accounting estimatesb. the basis for the preparation of the financial statements of the enterprisec. selected accounting policies of the enterprised. the total amount of dividends offered or declared prior to the approval of the financial statements for publication that were not recognized as a distribution of equity to owners for the periode. information required by International Financial Reporting Standards that is not presentedelsewhere in the financial statementsf. each of the above information must be disclosedg. the valuation base (s) used in the preparation of the financial statementsh. the judgments made by management in the process of implementing its accounting policiesD20. The issue of 95,000 ordinary shares with a nominal value of BGN 1 per share and an issue value of BGN 1.10 / share by an enterprise shall be accounted for with the following accounting item:Choose onea. Dt s / ka Share capital 95 000 and Dt s / ka Reserve from issue of shares 9 500; Kt Current account in BGN 104,500b. Dt s / ka Share capital 95 000; Kt s / ka Reserve from issue of shares 95 000c. Dt s / ka Current account in BGN 104,500; Kt s / ka Share capital 95 000 and Kt s / ka Reserve from issue of shares 9 500d. Dt s / ka Current account in BGN 104,500; Kt s / ka Share capital 104 500C21.Which of the following is NOT included in the group of cash and cash equivalents?Choose onea. all of the above are includedb. current account balancesc. cashd. investments in quarterly government securitiese. quarterly bank depositf. long-term blocked fundsF22.Which of the following statements concerning property, plant and equipment is NOT true? Choose onea. Borrowing costs are always capitalized in the amount of the property, plant and equipment acquiredb. Spare parts are usually accounted for as inventories and current consumption is accounted for when usedc. If appropriate, the entity may group insignificant assets separately and apply the criteria for recognizing property, plant and equipment to their total value.d. Tangible fixed assets acquired for security or environmental reasons may be recognized as separate property, plant and equipment.e. The costs of major inspections must be added (capitalized) to the carrying amount of property, plant and equipment if the recognition criteria are met.f. If basic spare parts and service equipment are used during more than one reporting period or only in connection with a tangible fixed asset, they are reported as property, plant and equipment.g. Expenses related to the daily maintenance of property, plant and equipment are recognized ascurrent for the period in which they are incurred.A23.Which of the following is not a non-current asset under International Financial Reporting Standards?Choose onea. investments in associatesb. income for future periodsc. facilitiesd. software productse. investment propertyf. improvements on the groundB24.Which of the following does not fall within the scope of financial accounting?Choose onea. there is no correct answerb. annual accounting closingc. preparation of financial statementsd. presentation of financial statementse. current accountingf. preparation of the annual budget of revenues and expendituresF25. Which of the following accounting items will be used to report the printer purchased for the needs of the marketing department, worth BGN 2,400, incl. 20% VAT, as the threshold for capitalization of properties, machinery and equipment is BGN 2,200:Choose onea. Dt s / ka Expenses for materials - assets below the value threshold 2 000 and Dt s / ka VAT purchases 400; Kt s / ka Current account in BGN 2,400b. Dt s / ka Material costs - assets below the value threshold 2,000; Kt s / ka Current account in BGN 2,000c. Dt s / ka Printer 2,000; Kt s / ka Current account in BGN 2,000d. Dt s / ka Expenses for acquisition of tangible fixed assets 2 400; Kt s / ka Current account in BGN 2,400A26.In most business transactions leading to a trade receivable, it is initially assessed:Choose onea. based on the exchange price agreed between the two parties to the transactionb. at its value in usec. at its reproductive valued. at its net realizable valuee. at its recoverable amountf. at its current value at the date of saleA27.Which statement about the net realizable value of inventories is NOT true?Choose onea. Net realizable value is always determined based on the market price of inventoriesb. For each subsequent period a new estimate of the net realizable value is madec. The impairment to net realizable value takes place on separate items of inventoriesd. The determination of net realizable value is based on an approximate accounting estimatee. The net realizable value depends on the contracts concluded by the enterprise, if anyf. When the conditions that led to the depreciation of inventories below their cost are no longer present, the previous value of the impaired inventories is re-adopted.g. The net realizable value is an indicator of the recoverable amount of inventories, given their liquidityh. The net realizable value depends on the selling expenses, which are specific and may be different for different companiesA28.Bulgarian accounting legislation does NOT include:Choose onea. Independent Financial Audit Actb. Accountancy Actc. Value Added Tax Actd. National accounting standardse. Law on the Public Offering of Securitiesf. Corporate Income Tax Actg. International Financial Reporting StandardsG29. The delivery value of purchased inventories does NOT include:Choose onea. finishing costsb. loading and unloading costsc. transport costsd. customs duties and taxese. purchase pricef. overhead costsg. commissions paid in connection with the purchaseF30.Which of the following does NOT belong to the minimum required information to be presented on the face of the statement of changes in equity in accordance with International Financial Reporting Standards?Choose onea. all of the above belong to the minimum required informationb. correction of significant errors from previous periods, if anyc. share capitald. revaluation reservee. retained earnings / uncovered lossf. premiums from the issue of shares / unitsg. reserves from recalculations in foreign currencyA31.Which of the following costs is not included in the cost of an asset in the group of property, plant and equipment?Choose onea. installation costsb. all listed costs are included in the acquisition price (cost)c. the estimated costs of dismantling and removing the asset and restoring the sited. delivery costse. the costs of site preparationf. import dutiesg. the cost of training staff to work with the asseth. purchase priceG32. Development costs incurred by the enterprise:Choose onea. are recognized as an asset and the cost of research is added to themb. are recognized as an asset only if they meet certain criteriac. are recognized as current expenses for the period in which they are incurredd. are recognized as a loss because the expected economic benefit against them is uncertaine. are recognized as deferred expensesB33.Which of the following costs are included in the cost of inventories?Choose onea. selling expensesb. non-production costs incurred in connection with bringing the inventories in the required conditionc. administrative costsd. input materials outside the norme. warehouse costsf. costs of exchange rate changesB34. An enterprise issues 10,000 ordinary shares with a nominal value of BGN 1 per share. The issue value is BGN 1.10 per share. The following accounting item must be prepared for theaccounting reflection of the issue:Choose onea. Cash debit account 11,000, Fixed capital credit account 10,000, Issue premiums credit account 1,000b. Debit account "Cash" 11 000, Credit account "Fixed capital" 10 000, Credit account "Additional capital" 1 000c. Cash debit account 10,000, Issue premiums debit account 1,000, Fixed capital credit account 11,000d. Cash debit account 11 000, Credit account "Income from operations with financial assets" 1 000, Credit account "Fixed capital" 10 000e. Debit account "Cash" 11 000, Credit account "Fixed capital" 11 000A35.Which of the following statements is NOT true?Choose onea. It is required to preserve the presentation and classification of the items in the financial statements during the reporting periodsb. Each significant class of related items must be presented separately in the financial statementsc. Revenues and expenses can be reimbursed only under certain conditionsd. All statements are truee. Instead of one statement of comprehensive income for the period, companies may submit two statements - a profit or loss statement for the year and a statement of comprehensive income.f. Comparative information for the previous reporting period is required for all digital informationg. The financial statements are presented at least once a yearh. The financial review by the management of the company is an integral part of its financial statements prepared on the basis of International Financial Reporting Standards.H36. The purchased machine is included in the fixed tangible assets of the enterprise under inventory number 124 and is accounted for at the acquisition price of BGN 96,400. The accounting of this business operation is:Choose onea. Dt s / ka Costs for acquisition of a machine 96 400; Kt s / ka Machine 96 400b. Dt s / ka Costs for acquisition of a machine 96 400; Kt s / ka Suppliers 96 400c. Dt s / ka Machine 96 400; Kt s / ka Costs for acquiring a machine 96 400d. Dt s / ka Machine 96 400; Kt s / ka Delivery 96 400C37.Which of the following accounting items are accrued dividends for BGN 3,700 in connection with the owned investments of the enterprise in subsidiaries:Choose onea. Dt s / ka Dividend receivables 3,700; Kt s / ka Dividend income 3,700b. Dt s / ka Dividend income 3,700; Kt s / ka Dividend receivables 3,700c. Dt s / ka Investments in subsidiaries 3,700; Kt s / ka Dividend income 3,700d. Dt s / ka Dividend receivables 3,700; Kt s / ka Investments in subsidiaries 3 700A38.Which of the following statements about the differences between financial (FS) and management accounting (MB) is NOT true?Choose onea. All statements are trueb. FS and MB solve different tasksc. FS and MB use different methodologies and procedural techniquesd. All statements are wronge. FS and MB use the same classification and analyticity of the reporting objectsf. The FS and the MB apply the same accounting methodg. FS and MB have the same subjectE39. The management of Jasmine AD prepares a draft financial statement on January 17, which is submitted for approval by the Board of Directors on February 25. The Board of Directors authorized the report for issue on February 25. Shareholders approve the financial statements on March 17. On March 5, a major customer of the company was declared bankrupt. In this regard, the company has taken one of the following actions:Choose onea. adjusts the disclosures in the financial statements in connection with the event and takes action to authorize the report for issuanceb. does not take any action related to the financial statementsc. adjusts the financial statement by depreciating the receivable from the client and warns the Board of Directors of the adjustments maded. adjusts the financial statement by depreciating the receivable from the client and takes new actions for re-authorization of the financial statement for issuancee. there is no correct answerD40. The accounting of the actual costs incurred for warranty service requires the compilation of the following accounting item:Choose onea. Debit account "Guarantee service provisions", Credit account "Cash"b. Debit account "Costs for provisions", Credit account "Provisions for warranty service"c. Debit account "Provisions for warranty service", Credit account "Expenses for provisions"d. Debit account "Cash", Credit account "Provisions for warranty service"e. All listed accounting items are wrongf. Debit account "Guarantee service provisions", Credit account "Other income"A41.Which of the following statements about inventories is NOT true?Choose onea. There are difficulties in quantitative measurement of inventories due to the various costs that form their value (cost)b. The classification of inventories must be consistent with the nature of the enterprise's operationsc. A problem in practice is the write-off of inventories when used in the activity, as there is a difference between the physical flow of inventories and value movements (flows)d. Inventories must be presented in the financial statements at the higher of their delivery value (cost) and their net realizable value.e. Inventories are directly related to liquidity and turnover, which characterize the production activity of the enterprisef. Inventories are material goods and they are materially responsibleD42.Which of the following statements concerning intangible assets is NOT true?Choose onea. Intangible assets are stated in the statement of financial position at their carrying amountb. When amortizing intangible assets, the straight-line method is mandatoryc. The cost of acquiring an intangible asset does not include the cost of training staff to work with the assetd. Intangible assets are subject to impairmente. Subsequent measurement of intangible assets may take place at historical cost or at revalued (fair) valueB43.Which of the following is NOT an incoming cash flow from financing activities for a manufacturing enterprise?Choose onea. Cash proceeds from bond issueb. All of these are cash inflows from financing activitiesc. Bank loan receivedd. Funding received under a European programe. Cash proceeds from the issue of sharesf. Payment received on the principal of a loan granted to an associateB44.Which of the listed assets is NOT included in the group of inventories?Choose onea. goodsb. materialsc. goods on the roadd. productse. semi-finished productsf. all of the listed assets are includedF45.Which of the following factors should not be taken into account when determining the useful life of property, plant and equipment?Choose onea. the expected use of the asset by the enterpriseb. the expected physical depletion of the assetc. the technical obsolescence of the assetd. the depreciable value of the assete. legal or other restrictions on the use of the assetf. the commercial obsolescence of the assetD46. On 01.09.2019 Maritza OOD received a loan in the amount of BGN 320,000. The loan is repayable in 16 equal quarterly installments. The first installment is due on December 1, 2019. All installments are made on the due date. How should the balance of the debt be presented as of 31.12. 2020 in the statement of financial position as of that date?Choose onea. as a non-current liability of BGN 80,000 and a current liability of BGN 140,000.b. there is no correct answerc. as a non-current liability BGN 220,000.d. as a non-current liability of BGN 140,000 and a current liability of BGN 80,000.e. as a current liability BGN 220,000.D47. The increase of the fixed capital cannot take place:Choose onea. against in-kind contribution of a partnerb. against the destruction of repurchased sharesc. through a new issue of sharesd. against repayment of an obligation of the enterprise to a suppliere. at the expense of retained earnings from previous yearsf. against the conversion of bonds into sharesD48.Which of the following is NOT an outflow of cash from operating activities?Choose onea. Cash payments of benefits from an insurance companyb. Dividends paidc. Cash payments to staffd. Cash payments to suppliers of goodse. Corporate tax paidf. Loans from a financial institutionF49.Which accounting item reflects a shareholder's contribution to the company's capital in the form of a building worth BGN 98,000, corresponding to subscribed but unpaid shares of the company?Choose onea. Dt s / ka Building 98 000; Kt s / ka Receivables on subscribed share contributions 98 000b. Dt s / ka Building 98 000; Kt s / ka Fixed capital 98 000c. Dt s / ka Share capital 79 000; Kt s / ka Building 98 000d. Dt s / ka Receivables on subscribed share contributions 98 000; Kt s / ka Building 98 000D50.Which of the following costs are included in the cost of inventories?Choose onea. warehouse costsb. costs of exchange rate changesc. non-production costs incurred in connection with bringing the inventories in the required conditiond. selling expensese. administrative costsf. input materials outside the normC。

财务会计判断题

11

企业转让无形资产时,无论采用何种转让方式,都应将转让收入计入其他业务收入,并注销已转让无形资产的账面价值。( )

12

虽然商誉能在较长的时期内使企业获得经济利益,但企业自创的商誉在会计上不予确认。( )

11

11

特准储备物资属于企业的存货。()

12

企业采购原材料取得的现金折扣应冲减其采购成本。()

12

企业的原材料无论是按实际成本计价核算还是按计划成本计价核算,其记入生产成本的原材料成本最终均应为所耗用材料的实际成本。( )

{

11

一次摊销的低值易耗品,领用时将其全部价值一次计入有关成本费用,报废时,将其残料价值冲减有关成本费用。( )

¥

12

按现行会计制度规定,企业和事业单位以原材料对外投资时,应交纳的增值税均应计入投资成本。( )

11

已经宣告的股票股利在尚未分派给股东之前,形成企业的一项负债。()

12

企业报销职工医药费、支付的福利补助费、发放的退休金等对职工个人支付的款项,均应通过“应付工资”科目核算。( )

12

企业在建工程领用本企业生产的产品,应按产品的售价转账,计入在建工程成本。()

会计核算的可比性原则要求同一会计主体在不同时期尽可能采用相同的会计程序和会计处理方法,以便于不同会计期间会计信息的纵向比较。( )

12

会计主体同法律主体是统一的,因此,会计主体只能是独立法人,不能是非法人。 ( )

-

12

权责发生制原则要求企业根据一定期间收入和费用之间存在的因果关系,来确认本期的收入和费用。( )

11

按照企业会计制度规定,法定盈余公积和公益金均可用于弥补亏损。( )

财务会计判断题

企业按年末应收款项余额的一定比例计算的坏账准备金额,应等于年末结账后“坏账准备”科目的余额。( )

11

在存在现金折扣的情况下,若采用总价法核算,应收账款应按销售收入扣除预计的现金折扣后的金额确认。( )

12

应收票据的利息收入,一般可在实际收款时确认;金额较大的,应按权责发生制原则在票据到期前的各期期末确认。( )

财务会计判断题(175道)

题目标题(1) 必填(题干11为“对” 12为“错”)

标准ห้องสมุดไป่ตู้案

会计主体是进行会计核算的基本前提。一个企业可以根据具体情况,确定一个或若干个会计主体,作为会计核算的基础。( )

11

会计核算的谨镇原则,一般是指对可能发生的损失和费用应当合理预计,对可能实现的收益不预计。( )

11

11

企业销售产品收到购货单位开出并承兑的商业汇票,不论应收票据是否带息,均按票据的票面金额登记入账。( )

11

按照企业会计制度规定,所有企业的应收账款和应收票据均可以提取坏账准备。( )

12

企业坏账不论采用直接转销法还是备抵法核算,当已确认并转销的坏账以后又收回时,均应通过“应收账款”账户核算。( )

11

短期股票投资持有期间所赚得的现金股利,应当在实际收到时确认为投资收益。( )

12

长期股权投资由权益法改按成本法核算时,应按原投资的公允价值作为投资成本。()

12

企业以购买股票的形式进行短期投资或长期投资时,如果购买的股票价格中含有已经宣告但尚未支付的股利,应以支付价款扣除该股利后的数额作为“短期投资”或“长期股权投资”的成本入账。( )

12

明确会计主体可确定会计核算的范围。( )

11

要求同一企业前后各期提供相互可比的会计信息的原则是可比性原则。( )

财务会计往年试题及答案

财务会计往年试题及答案一、单项选择题(每题2分,共20分)1. 会计的基本职能是()。

A. 核算和监督B. 预测和决策C. 计划和控制D. 分析和评价答案:A2. 会计核算的基本前提是()。

A. 会计主体B. 持续经营C. 会计分期D. 货币计量答案:B3. 资产负债表中资产的排列顺序是()。

A. 从高到低B. 从低到高C. 按照流动性D. 按照重要性答案:C4. 会计信息质量要求中,要求企业应当合理确认、计量利得和损失,并在财务报表中反映的是()。

A. 可靠性B. 相关性C. 及时性D. 谨慎性答案:A5. 企业对外提供的财务报表至少应当包括()。

A. 资产负债表B. 利润表C. 现金流量表D. 所有者权益变动表答案:A6. 企业在确定收入确认时点时,通常采用的标准是()。

A. 风险和报酬的转移B. 所有权的转移C. 控制权的转移D. 经济利益的流入答案:B7. 企业在编制现金流量表时,下列项目中属于经营活动产生的现金流量的是()。

A. 销售商品、提供劳务收到的现金B. 取得投资收益收到的现金C. 处置固定资产、无形资产和其他长期资产收回的现金净额D. 吸收投资收到的现金答案:A8. 企业在进行存货计价时,可以采用的方法有()。

A. 先进先出法B. 加权平均法C. 移动平均法D. 以上都是答案:D9. 企业在计算应纳税所得额时,下列支出中不得扣除的是()。

A. 合理的工资薪金支出B. 广告费和业务宣传费C. 税收滞纳金D. 公益性捐赠支出答案:C10. 企业在进行长期股权投资核算时,下列方法中适用于对子公司投资的是()。

A. 成本法B. 权益法C. 公允价值计量D. 历史成本法答案:A二、多项选择题(每题3分,共15分)11. 会计核算的一般原则包括()。

A. 客观性原则B. 相关性原则C. 可比性原则D. 重要性原则答案:ABCD12. 会计要素包括()。

A. 资产B. 负债C. 所有者权益D. 收入、费用和利润答案:ABCD13. 企业在进行固定资产折旧时,可以采用的方法有()。

财务会计练习题

财务会计练习题(二)姓名:学号一、判断题1、先进先出法在定期盘存制和永续盘存制下核算的结果是相同的()2、根据收入实现原则,收入的确认应当与现金的收取时间保持一致()3、注销应收账款时,在直接转销法下,既会影响流动资产总额,也会影响当期净收益()4、注销应收账款时,在备抵法下,既不会影响流动资产总额,也不会影响当期净收益()5、在永续盘存制下,存货的溢缺都隐含在存货的销售成本中,无法单独反映()6、存货发出计价方法的选择可能会影响公司当年收益,但不会影响公司年末总资产()7、固定资产的折旧是指将固定资产的原始成本扣除净残值之后在其估计有效使用年限内摊配为费用的过程()8、在固定资产使用的早期,与直线法相比,采用加速折旧法核算出来的净收益、资产总额、所有者权益均较低。

()9、借贷方出现现金账户的会计分录不可能会是调整分录()10、无论是采用后进先出法还是先进先出法,在两种盘存制下核算的结果都是相同的()11、收付实现制下,收入和费用的确认,分别应与现金的收取与支出时间保持一致()12、公司将资本性支出作为收益性支出进行确认,会减少公司当年利润()13、期末会计人员忘记计提坏帐准备,将会高估资产、收益和股东权益()14、利得和损失一定会影响当期损益()15、企业在一定期间发生亏损,但企业在这一会计期间的所有者权益不一定减少()16、因商业折扣在销售发生时已发生,企业应按扣除商业折扣前的净额确认销售收入()二、单项选择题1、下列各项中,应计入坏账准备贷方的有()。

A.发生的坏账款B.应收账款的收回C.冲减多提的坏账准备D.收回已转销的坏账2.下列项目中,不属于本企业存货范围的是()。

A.受托代销的商品B.购入并自行加工的材料C.库存商品D.委托外部加工的材料3、企业收回代购货方垫付的运杂费时,应贷记()账户。

A.银行存款B.其他应收款C.应收账款D.其他业务收入4、在物价持续上涨期间,采用()使得当期利润最少。

财务会计试题(含答案)

财务会计试题(含答案)一、单项选择题(每题2分,共20分)1. 企业的财务会计报告主要包括()。

A. 资产负债表、利润表、现金流量表和所有者权益变动表B. 资产负债表、利润表、现金流量表和财务情况说明书C. 资产负债表、利润表、现金流量表和附注D. 资产负债表、利润表、现金流量表和会计政策说明书答案:C2. 企业采用权责发生制核算时,下列业务中应当确认为收入的是()。

A. 销售商品,货款尚未收到B. 销售商品,货款已经收到C. 提供劳务,收到劳务报酬D. 预收账款发出商品答案:A3. 下列各项中,不属于流动资产的是()。

A. 现金B. 银行存款C. 短期投资D. 长期股权投资答案:D4. 下列属于应付职工薪酬核算范围的是()。

A. 工资B. 福利费C. 社会保险费D. 所有选项均属于应付职工薪酬核算范围答案:D5. 企业计提的坏账准备,应当计入()。

A. 管理费用B. 销售费用C. 资产减值损失D. 利润分配答案:C6. 企业发行股票,支付的佣金、手续费等费用,应当计入()。

A. 应付股利B. 资本公积C. 管理费用D. 所有者权益答案:B7. 企业采用成本模式进行投资性房地产核算,下列表述正确的是()。

A. 投资性房地产应当按成本计量,不计提折旧或摊销B. 投资性房地产应当按成本计量,计提折旧或摊销C. 投资性房地产应当按公允价值计量,不计提折旧或摊销D. 投资性房地产应当按公允价值计量,计提折旧或摊销答案:A8. 下列属于企业应付债券的是()。

A. 短期借款B. 长期借款C. 应付票据D. 应付债券答案:D9. 企业确认的营业外收入主要包括()。

A. 非流动资产处置利得B. 非货币性资产交换利得C. 债务重组利得D. 所有选项均属于营业外收入答案:D10. 下列属于企业长期股权投资核算范围的是()。

A. 投资企业能够对被投资单位施加重大影响的投资B. 投资企业能够对被投资单位实施控制的investmenC. 投资企业对被投资单位不具有控制、共同控制或重大影响的股权投资D. 投资企业对被投资单位具有共同控制的投资答案:A二、多项选择题(每题3分,共30分)1. 企业的财务会计报告主要包括()。

会计判断试题及答案

会计判断试题及答案一、单项选择题1. 根据会计准则,下列哪项不是会计要素?A. 资产B. 负债C. 所有者权益D. 利润答案:D2. 企业在编制财务报表时,应遵循以下哪项原则?A. 权责发生制B. 收付实现制C. 历史成本原则D. 公允价值原则答案:A3. 以下哪项不是会计信息质量要求?A. 可靠性B. 相关性C. 可比性D. 可操作性答案:D4. 会计政策变更时,应如何处理?A. 立即调整所有相关账目B. 追溯调整法C. 未来适用法D. 忽略不计答案:B5. 企业对外投资的收益,应如何进行会计处理?A. 直接计入当期利润B. 计入投资收益C. 计入其他业务收入D. 计入营业外收入答案:B二、多项选择题6. 以下哪些属于会计核算的基本前提?A. 会计主体B. 持续经营C. 货币计量D. 会计分期答案:ABCD7. 会计估计变更时,应如何进行会计处理?A. 追溯调整B. 立即调整C. 未来适用D. 忽略不计答案:CD8. 以下哪些属于会计信息披露的要求?A. 真实性B. 完整性C. 及时性D. 可理解性答案:ABCD9. 会计报表包括哪些?A. 资产负债表B. 利润表C. 现金流量表D. 所有者权益变动表答案:ABCD10. 以下哪些属于会计核算的基本原则?A. 权责发生制B. 历史成本原则C. 谨慎性原则D. 重要性原则答案:ABCD三、判断题11. 会计核算中,所有资产的计价都应采用公允价值。

(错误)12. 企业在编制财务报表时,必须遵循权责发生制原则。

(正确)13. 会计政策变更时,必须采用追溯调整法。

(错误)14. 会计信息披露要求中,及时性是指信息披露必须在事件发生后的第一时间内完成。

(正确)15. 会计报表的编制必须遵循历史成本原则。

(错误)四、简答题16. 简述会计信息的可靠性要求。

答案:会计信息的可靠性要求是指会计信息应当真实、准确、完整地反映企业的财务状况和经营成果。

企业在编制财务报表时,应当遵循会计准则和相关法规,确保所提供的信息真实可靠,不得有虚假记载、误导性陈述或重大遗漏。

(财务会计)会计基础选择题和判断题及答案

一、单项选择题(每小题1分。

共30分,在每小题的四个备选答案中选出一个正确答案,并将正确答案的序号填在题干的括号内。

错选、不选或多选均不得分)第1题:会计的基本职能是( )。

A.记账、算账和报账B.核算和监督C.预测、决策和分析D.监督和管理[答案]:B[解析]:会计的基本职能是核算和监督,除了基本职能外还具有预测、决策和分析等职能。

第2题:下列项目不属于费用要素的是( )。

A.制造费用B.管理费用C.长期待摊费用D.财务费用[答案]:C[解析]:制造费用、管理费用和财务费用都属于费用要素,而长期待摊费用属于资产。

第3题:下列经济业务引起资产与负债同时减少的是( )。

A.收到投资者投入的设备一台,价值8万元B.购人材料一批,价值5万元,货款未付C.以银行存款归还以前欠货款6万元D.生产甲产品领用材料费5400元[答案]:C[解析]:以银行存款归还前欠货款一方面引起了银行存款的减少,银行存款为资产,另一方面引起了应付账款的减少,应付账款属于负债,其余三项都不是。

第4题:下列账户中,期末一般没有余额的是( )。

A.“生产成本”账户B.“应交税金”账户C.“制造费用”账户D.“累计折旧”账户[答案]:C[解析]:“制造费用”属于应计人生产成本的间接费用,期末时应转入“生产成本”科目,结转后无余额。

第5题:某会计账户的期初借方余额为5000元,本期贷方发生额为l2000元。

期末借方余额为8400元,则本期借方发生额为( )。

A.8600元B.15400元C.1400元D.14500元[答案]:B[解析]:因为期初借方余额+本期借方发生额一本期贷方发生额=期末借方余额,所以该账户的本期借方发生额=8400+12000-5000=15400元。

第6题:下列属于外来原始凭证的是( )。

A.收料单B.收款的收据C.出差后的车票D.经济合同[答案]:C[解析]:外来原始凭证是指在经济业务发生或完成时,从其他单位或个人直接取得的原始凭证,出差后的车票是从外单位取得的,属于外来凭证,其他均为自制的凭证。

财务会计期末判断题

财务会计期末判断题您的姓名: [填空题] *_________________________________5、企业一般按月提取折旧,当月增加的当月照提,当月减少的当月不提。

[判断题] *对错(正确答案)6、已达到预定可使用状态的固定资产,无论是否交付使用,都应计提折旧。

[判断题] *对(正确答案)错3、企业购入无形资产,只能按买价作为购入无形资产的实际成本。

[判断题] *对错(正确答案)4、无形资产的摊销不考虑残值。

[判断题] *对(正确答案)错5、生产车间使用的专利权在按月摊销时,应借记“制造费用”账户。

[判断题] *对错(正确答案)6、企业为出租无形资产所发生的相关费用,应于发生时借记“销售费用”账户。

[判断题] *对错(正确答案)7、无论固定资产是融资租入还是经营租入,其租入方均需计提折旧。

[判断题] *对错(正确答案)8、固定资产的后续支出,包括企业对固定资产进行维护、改建、扩建或者改良等所发生的支出。

[判断题] *对(正确答案)错1、存货的成本就是存货的采购成本。

[判断题] *对错(正确答案)4、存货是企业的一项流动资产。

[判断题] *对(正确答案)错5、存货按实际成本计价是指每种存货的收发结存,都按收发结存时的市场价格计价。

[判断题] *对错(正确答案)7、无形资产成本在取得的当月开始摊销,处置无形资产的当月不再摊销。

[判断题] *错8、无形资产的研发支出应全部记入该项无形资产的成本。

[判断题] *对错(正确答案)6、存货清查的目的,主要是进行总账和明细账的核对,做到账账相符。

( ×)。

[填空题]_________________________________7、当企业外购材料出现“付款在前,收料在后”情况时,应当及时反映已付出的购料款,并将其记入“应付账款”账户的贷方。

[判断题] *对错(正确答案)8、“在途物资”账户是材料按计划成本计价核算时设置的,用以反映材料采购的实际成本。

《财务会计》习题及参考答案

《财务会计》习题及参考答案一、判断题(正确的在括号后打“√”错误的在括号后打“×”)1.在进行现金核对时,库存现金实有数,包括借条、收据等在内,必须与现金日记帐的帐面余额相符合。

(×)2.同城或异地的商品交易,劳务供应均可采用银行本票方式进行结算。

(×)3.我国的会计核算以人民币为记帐本位币,因此,企业的现金是指库存的人民币现金,不包括外币。

(×)4.带息应收票据应于收到或开出或承兑时,以其票面金额与应计利息的合计数入帐。

(×)5.一切应收款项均可预先估计坏帐损失。

(×)6.企业对于已转为坏帐损失的应收帐款已放弃了追索权。

(×)7.已确认并已转销的坏帐损失,以后又收回的,仍然应通过“应收帐款”科目核算,并冲减“坏帐准确”科目。

(√)8.企业按年末应收帐款余额的一定比例计算出的坏帐准备,等于年末计入“管理费用——坏帐损失”科目的金额。

(×)9.预付货款可以在“应付帐款”科目核算,因此,预付货款可以减少企业的负债。

(×)10.企业发生的预付货款业务也可不通过“预付帐款”科目,而在“应付帐款”科目中进行核算,但在会计期末编制报表时应将二者分开报告。

(√)11.应收票据贴现的的实收金额一定小于票据面值。

(×)12.票据贴现所得一定小于票据面值。

(×)13.“预付帐款”科目的贷方登记企业收到订购物品时应结转的预付款项。

(√)14.存货是指已经完成全部生产过程并验收入库可对外销售的产品。

(×)15.所有企业采购存货时支付的增值税不得记入存货成本。

(×)16.帐面结存法下定期或不定期的盘点,目的是核对帐实,而不是取得存货的实际结存数。

(√)17.生产过程中用于包装产品作为产品组成部分的包装物的价值应构成产品的生产成本。

(√)18.企业购进原材料已验收入库,但结算凭证尚未到达,货款尚未支付,则月末应将这批材料按暂估价入帐,待下月收到结算凭证并支付货款时,将其实际采购成本与暂估价的差额记入“材料成本差异”科目。

财务会计考试题判断

财务会计考试题判断1. "出售无形资产取得收益会导致经济利益的流入,所以它属于会计准则所定义的“收入”范畴。

对错(正确答案)2. "判断一项会计事项是否具有重要性,主要取决于会计准则的规定,而不是取决于会计人员的职业判断。

所以同-个事项在某一企业具有重要性,在另一企业则也具有重要性。

对错(正确答案)3. "企业必须拥有其所有权的资源才能作为资产予以确认,所以租赁期内的融资租入固定资产,承租人没有其所有权,故不作为固定资产核算,只在备查账簿登记。

对错(正确答案)4. "企业为减少本年度亏损而调减计提资产减值准备金额,体现了会计核算的谨慎性原则。

对错(正确答案)5. "实质重于形式要求企业应当按照交易或者事项的经济实质进行会计确认、计量和报告,不应仅以交易或者事项的法律形式为依据。

对(正确答案)错6. "库存现金是指企业为了备付日常零星开支而保管的现金,包括人民币和外币。

对(正确答案)错7. "支票的提示付款期限为10天,自出票的次日起算。

对错(正确答案)8. "银行本票的提示付款期,自出票日起最长不得超过2个月,在付款期内银行本票见票即付。

对(正确答案)错9. "商业汇票只有在银行开立存款账户的法人及其他组织之间,而且具有真实的交易关系或债权债务关系才能使用。

对(正确答案)错10. "采用托收承付结算方式办理结算的款项必须是商品交易及因商品交易而产生的劳务供应的款项,包括代销、寄销和赊销商品的款项。

对错(正确答案)11. "已确认为坏账的应收账款,意味着企业放弃了其追索权。

对错(正确答案)12. "坏账损失采用直接转销法虽然简便易行,但却不符合收入与费用相配合的原则。

对(正确答案)错13. "采用直接转销法核算坏账损失,当坏账实际发生时,直接将坏账损失计入当期损益.对(正确答案)错14. "用账龄分析法估计坏账损失是基于这种观点:账款拖欠的时间越长,发生坏账的可能性就越大,应提取的坏账准备金额就越多。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

1.Generally accepted accounting principles (GAAP) are formulated by the ( )A. Securities and Exchange Commission (SEC)B. Financial Accounting Standards Board (FASB)C. Institute of Management Accountants (IMA)D. American Institute of Certified Public Accountants (AICPA)2.Which accounting concept or principle specifically states that we should record transactions at amounts that can be verified?A. Entity conceptB. Cost principleC. Reliability principleD. Going-concern concept3.Fossil is famous for fashion wristwatches and leather goods. At the end of a recent year, Fossil’s total assets added up to﹩381 million, and owner s’ equity was ﹩264 million. How much did Fossil owe creditors?A. Cannot determine from the data givenB. ﹩381 millionC. ﹩264 millionD. ﹩117 million 4.Assume that Fossil sold watches for ﹩50,000 to a department store on account. How would this transaction affect Fossil’s accounting equation?A. Increase both assets and owner s’ equity by ﹩50,000B. Increase both assets and liabilities by ﹩50,000C. Increase both liabilities and owners’ equity by ﹩50,000D. No effect on the accounting equation because the effects cancel out 5.The financial statement that reports assets, liabilities, and owner’s equity is the:A. Income statement.B. Owner’s equity statement.C. Balance sheet.D. Statement of cash flow.6.The left side of an account is used to record ( )A. DebitsB. CreditsC. Debit or credit, depending on the type of accountD. Increases 7.Accounts that normally have debit balance are: ( )A. Assets, expenses, and revenuesB. Assets, expenses, and owner’s capital.C. A ssets, liabilities, and owner’s drawings.D. Assets, owner’s drawings, and expenses.8.The time period assumption states that: ( )A. Revenue should be recognized in the accounting period in which it is earned.B. Expenses should be matched with revenues.C. The economic life of a business can be divided into artificial time periods.D. The fiscal year should be correspond with the calendar year. 9.In a work sheet, net income is entered in the following columns: ( )A. Income statement (Dr) and balance sheet (Dr).B. Income statement (Cr) and balance sheet (Dr).C. Income statement (Dr) and balance sheet (Cr).D. Income statement (Cr) and balance sheet (Cr).10.An account that will have a zero balance after closing entries have been journalized and posted is: ( )A. Service Revenue.B. Advertising Supplies.C. Prepaid Insurance.D. Accumulated Depreciation.11.Gross profit will result if: ( )A. Operating expenses are less than net income.B. Sales revenues are greater than operating expenses.C. Sales revenues are greater than cost of goods sold.D. Operating expenses are greater than cost of goods sold.12.A credit sale of ﹩750 is made on June 13, terms 2/10, net/30. A return of ﹩50 is granted on June 16. The amount received as payment in full on June 23 is:( )A. ﹩700.B. ﹩686.C. ﹩685.D. ﹩750.13.When special journals are used: ( )A. All purchase transactions are recorded in the purchases journal.B. All cash received, except from cash sales, is recorded in the cashreceipts journal.C. All cash disbursements are recorded in the cash payments journal.D. A general journal is not necessary.14.The statement of cash flows classifies cash receipts and cash payments by the following activities: ( )A. Operating and nonoperating.B. Investing, financing, and operating.C. Financing, operating, and nonoperating.D. Investing, financing, and nonoperating.15.Net income is ﹩132,000. During the year, accounts payable increased ﹩10,000, inventory decreased ﹩6,000, and accounts receivable increased ﹩12,000. Under the indirect method, net cash provided by operations is: ( )A. ﹩102,000.B. ﹩112,000.C. ﹩124,000.D. ﹩136,000.16.The cost principle states that ( )A. Assets should be initially recorded at cost and adjusted when the marketvalue changes.B. Activities of an entity are to be kept separate and distinct from its owner.C. Assets should be recorded at their cost.D. Only transaction data capable of being expressed in terms of money beincluded in the accounting records.17.Net income will result during a time period when:A. Assets exceed liabilities.B. Assets exceed revenues.C. Expenses exceed revenues.D. Revenues exceed expenses.18.Performing services on account will have the following effects on the components of the basic accounting equation:A. Increase assets and decrease owner’s equity.B. Increase assets and increase owner’s equity.C. Increase assets and increase liabilities.D. Increase liabilities and increase owner’s equity.19.As of December 31, 2007, Stoneland Company has assets of ﹩3,500 and owner’s equity of ﹩2,000. What are the liabilities for Stoneland Company as of December 31, 2007?A. ﹩1,500B. ﹩1,000.C. ﹩2,500.D. ﹩2,000. 20.On the last day of the period, Genesis Company buys a ﹩900 machine on credit. This transaction will affect the:A. Income statement only.B. Income statement and owner’s equity statement only.C. Balance sheet only.D. Income statement, owner’s equity statement, and balance sheet. 21.The right side of an account is used to record ( )A. DebitsB. CreditsC. Debit or credit, depending on the type of accountD. Increases. 22.Which of the following statements about a journal is false?A. It is not a book of original entry.B. It provides a chronological record of transac t ions.C. It helps to locate errors because the debit and credit amounts for each entry can be readily compared.D. It discloses in one place the complete effect of a transaction.23.One of the following statements about the accrual basis of accounting is false. That statement is: ( )A. Events that change a company’s financial statements are recorded in the periods in which the events occur.B. Revenue is recognized in the period in which it is earned.C. This basis is in accord with generally accepted accounting principles.D. Revenue is recorded only when cash is received, and expense is recorded only when cash is paid.24.When a net loss has occurred, Income Summary is: ( )A. Debited and Owner’s Capital is credited.B. Credited and Owner’s capital is debited.C. Debited and Owner’s Drawing is credited.D. Credited and Owner’s Drawing is debited.25.Current assets are listed: ( )A. By liquidity.B. By importance.C. By longevity.D. Alphabetically.26.If sales revenues are ﹩400,000, cost of goods sold is ﹩310,000, and operating expenses are ﹩60,000, the gross profit is: ( )A. ﹩30,000.B. ﹩90,000.C. ﹩340,000.D. ﹩400,000. 27.If beginning inventory is ﹩60,000, cost of goods purchased is ﹩380,000, and ending inventory is ﹩50,000, cost of goods sold is: ( )A. ﹩390,000.B. ﹩370,000.C. ﹩330,000.D. ﹩420,000. 28.Which of the following statements is correct?A. The sales discount column is included in the cash receipts journal.B. The purchases journal records all purchases of merchandise whether for cash or onaccount.C. The cash receipts journal records sales on account.D. Merchandise returned by the buyer is recorded by the seller in the purchases journal.29.An example of a cash flow from an operating activity is: ( )A. Payment of cash to lenders for interest.B. Receipt of cash from the sale of capital stock.C. Payment of cash dividends to the company’s stockholders.D. None of the above.30.The beginning balance in accounts receivable is ﹩44,000. The ending balance is ﹩42,000. Sales during the period are ﹩129,000. Cash receipts from customers are: ( )A. ﹩127,000.B. ﹩129,000.C. ﹩131,000.D. ﹩141,000.31.Generally,revenue is recorded by a business enterprise at a point when :( )A、M anagement decides it is appropriate to do soB、T he product is available for sale to consumersC、A n exchange has taken place and the earning process is virtually completeD、A n order for merchandise has been received32.Why are certain costs capitalized when incurred and then depreciated or amortized over subsequent accounting periods?( )A、T o reduce the income tax liabilityB、T o aid management in making business decisionsC、T o match the costs of production with revenue as earnedD、T o adhere to the accounting concept of conservatism33.What accounting principle or concept justifies the use of accruals and deferrals?( )A、G oing concernB、M aterialityC、C onsistencyD、S table monetary unit34.An accrued expense can best be described as an amount ( )A、P aid and currently matched with revenueB、P aid and not currently matched with revenueC、N ot paid and not currently matched with revenueD、N ot paid and currently matched with revenue35.Continuation of a business enterprise in the absence of contrary evidence is an example of the principle or concept of ( )A、B usiness entityB、C onsistencyC、G oing concernD、S ubstance over form36.、In preparing a bank reconciliation,the amount of checks outstanding would be:( )A、a dded to the bank balance according to the bank statement.B、d educted from the bank balance according to the bank statement.C、a dded to the cash balance according to the deposi tor’s records.D、d educted from the cash balance according to the depositor’s records.37.Journal entries based on the bank reconciliation are required for:( )A、a dditions to the cash balance according to the depositor’s records.B、d eductions from the cash bala nce according to the depositor’s records.C、B oth A and BD、N either A nor B38.A petty cash fund is :( )A、u sed to pay relatively small amounts。