会计稳健性外文翻译---会计稳健性的第一篇:解释和意义

会计准则外文文献翻译-财务会计专业

会计准那么外文文献及翻译-财务会计专业(含:英文原文及中文译文)文献出处:Buschhüter M, Striegel A. IAS 37 – Provisions, Contingent Liabilities and Contingent Assets[M]// Kommentar Internationale Rechnungslegung IFRS. Gabler, 2021:955-974.英文原文Accounting Standard (AS) 37Contingent Liabilities and Contingent AssetsBuschhüter M, Striegel AThis International Accounting Standard was approved by the IASC Board in July 1998 and became effective for financial statements covering periods beginning on or after 1 July 1999.Introduction1. IAS 37 prescribes the accounting and disclosure for all provisions, contingent liabilities and contingent assets, except:(a) those resulting from financial instruments that are carried at fair value;(b) those resulting from executory contracts, except where the contract is onerous. Executory contracts are contracts under which neither party has performed any of its obligations or both parties have partially performed their obligations to an equal extent;(c) those arising in insurance enterprises from contracts with policyholders;(d) those covered by another International Accounting Standard. Provisions2. The Standard defines provisions as liabilities of uncertain timing or amount. A provision should be recognised when, and only when:(a) an enterprise has a present obligation (legal or constructive) as a result of a past event; (b) it is probable (i.e. more likely than not) that an outflow of resources embodying economic benefits will be required to settle the obligation;(c) a reliable estimate can be made of the amount of the obligation. The Standard notes that it is only in extremely rare cases that a reliable estimate will not be possible.3. The Standard defines a constructive obligation as an obligation that derives from an enterprise's actions where:(a) by an established pattern of past practice, published policies or a sufficiently specific current statement, the enterprise has indicated to other parties that it will accept certain responsibilities; (b) as a result, the enterprise has created a valid expectation on the part of those other parties that it will discharge those responsibilities.4. In rare cases, for example in a law suit, it may not be clear whether an enterprise has a present obligation. In these cases, a past event is deemed to give rise to a present obligation if, taking account of all available evidence, it is more likely than not that a present obligation exists at thebalance sheet date. An enterprise recognises a provision for that present obligation if the other recognition criteria described above are met. If it is more likely than not that no present obligation exists, the enterprise discloses a contingent liability, unless the possibility of an outflow of resources embodying economic benefits is remote.5. The amount recognized as a provision should be the best estimate of the expenditu required to settle the present obligation at the balance sheet date, in other words, the amount that an enterprise would rationally pay to settle the obligation at the balance sheet date or to transfer it to a third party at that time.6. The Standard requires that an enterprise should, in measuring a provision: (a) take risks and uncertainties into account. However, uncertainty does not justify the creation of excessive provisions or a deliberate overstatement of liabilities;(b) discount the provisions, where the effect of the time value of money is material, using a pre-tax discount rate (or rates) that reflect(s) current market assessments of the time value of money and those risks specific to the liability that have not been reflected in the best estimate of the expenditure. Where discounting is used, the increase in the provision due to the passage of time is recognised as an interest expense;(c) take future events, such as changes in the law and technological changes, into account where there is sufficient objective evidence thatthey will occur; and(d) not take gains from the expected disposal of assets into account, even if the expected disposal is closely linked to the event giving rise to the provision.7. An enterprise may expect reimbursement of some or all of the expenditure required to settle a provision (for example, through insurance contracts, indemnity clauses or suppliers' warranties). An enterprise should:(a) recognise a reimbursement when, and only when, it is virtually certain that reimbursement will be received if the enterprise settles the obligation. The amount recognised for the reimbursement should not exceed the amount of the provision; and(b) recognise the reimbursement as a separate asset. In the income statement, the expense relating to a provision may be presented net of the amount recognised for a reimbursement. 8. Provisions should be reviewed at each balance sheet date and adjusted reflect thecurrent best estimate. If it is no longer probable that an outflow of resources embodying economic benefits will be required to settle the obligation, the provisioshould be reversed.9. A provision should be used only for expenditures for which the provision was originally recognised.Provisions - Specific Applications10. The Standard explains how the general recognition and measurement requirements for provisions should be applied in three specific cases: future operating losses; onerous contracts; and restructurings. Contingent Liabilities11. An enterprise should not recognise a contingent liability. , unless the12. A contingent liability is disclosed, as required by paragraph 86possibility of an outflow of resources embodying economic benefits is remote.13. Where an enterprise is jointly and severally liable for an obligation, the part of tobligation that is expected to be met by other parties is treated as a contingentThe enterprise recognises a provision for the part of the obligation for which an outflow of resources embodying economic benefits is probable, except in the extremely rare circumstances where no reliable estimate can be made.14. Contingent liabilities may develop in a way not initially expected. Therefore, theare assessed continually to determine whether an outflow of resources embodying probable. If it becomes probable that an outflow of economic benefits has become future economic benefits will be required for an item previously dealt with as a contingent liability, a provision is recognised in the financial statements of the period in which the change in probability occurs (except in the extremely rare circumstances where no reliable estimate can be made).Contingent Assets15. An enterprise should not recognise a contingent asset.16. Contingent assets usually arise from unplanned or other unexpected events that give rise to the possibility of an inflow of economic benefits to the enterprise. An example is a claim that an enterprise is pursuing through legal processes, where the outcome is uncertain. 17. Contingent assets are not recognised in financial statements since this may result in the recognition of income that may never be realised. However, when the realisation of income is virtually certain, then the related asset is not a contingent asset and its recognition is appropriate. 18. A contingent asset is disclosed, as required by paragraph 89 economic benefits is probable.19. Contingent assets are assessed continually to ensure that developments are appropriately reflected in the financial statements. If it has become virtually certain that an inflow of economic benefits will arise, the asset and the related income are recognised in the financial statements of the period in which the change occurs. If an inflow of economic benefits has become probable, an enterprise discloses the contingent asset.Measurement20. The amount recognised as a provision should be the best estimate of the expenditure required to settle the present obligation at the balance sheet date.21. The best estimate of the expenditure required to settle the present obligation is the amount that an enterprise would rationally pay to settle the obligation at the balance sheet date or to transfer it to a third party at that time. It will often be impossible or prohibitively expensive to settle or transfer an obligation at the balance sheet date. However, the estimate of the amount that an enterprise would rationally pay to settle or transfer the obligation gives the best estimate of the expenditure required to settle the present obligation at the balance sheet date. 22. The estimates of outcome and financial effect are determined by the judgement of the management of the enterprise, supplemented by experience of similar transactions and, in some cases, reports from independent experts. The evidence considered23. Uncertainties surrounding the amount to be recognised as a provision are dealt with by various means according to the circumstances. Where the provision being measured involves a large population of items, the obligation is estimated by weighting all possible outcomes by their associated probabilities. The name for thistatistical method of estimation is 'expected value'. The provision will therefore be different depending on whether the probability of a loss of a given amount is, for example, 60 per cent or 90 per cent. Where there is a continuous range of possible outcomes, and each point in that range is as likely as any other, the mid-point of thrange is used. 24. Where a single obligation is beingmeasured, the individual most likely outcome may be the best estimate of the liability. However, even in such a case, the enterprise considers other possible outcomes. Where other possible outcomes are either mostly higher or mostly lower than the most likely outcome, the best estimate will be a higher or lower amount. For example, if an enterprise has to rectify a serious fault in a major plant that it has constructed for a customer, the individual most likely outcome may be for the repair to succeed at the first attempt at a cost of1,000, but a provision for a larger amount is made if there is a significant chance that further attempts will be necessary.25. The provision is measured before tax, as the tax consequences of the provision, , Income Taxes. and changes in it, are dealt with under IAS 12,Income Taxes.Risks and Uncertainties26. The risks and uncertainties that inevitably surround many events and the best estimate of a circumstances should be taken into account in reachin the best estmeate of a provision.27. Risk describes variability of outcome. A risk adjustment may increase the amount at which a liability is measured. Caution is needed in making judgements under conditions of uncertainty, so that income or assets are not overstated and expenses or liabilities are not understated. However, uncertainty does not justify the creation of excessive provisions or adeliberate overstatement of liabilities. For example, if the projected costs of a particularly adverse outcome are estimated on a prudent basis, that outcome is not then deliberately treated as more probable than is realistically the case. Care is needed to avoid duplicating adjustments for risk and uncertainty with consequent overstatement of a provision. Present Value28. Where the effect of the time value of money is material, the amount ofa provision should be the present value of the expenditures expected to be required to settle the obligation.29. The discount rate (or rates) should be a pre-tax rate (or rates) that reflect(s) current market assessments of the time value of money and the risks specific to the liability. The discount rate(s) should not reflect risks for which future cash flow estimates have been adjusted. Future Events 30. Future events that may affect the amount required to settle an obligation should be reflected in the amount of a provision where there is sufficient objective evidence that they will occur.31. Expected future events may be particularly important in measuring provisions. For example, an enterprise may believe that the cost of cleaning up a site at the end of its life will be reduced by future changes in technology. The amount recognised reflects a reasonable expectation of technically qualified, objective observers, taking account of all available evidence as to the technology that will be available at the time of theclean-up. Thus it is appropriate to include, for example, expected cost reductions associated with increased experience in applying existing technology or the expected cost of applying existing technology to a larger or more complex clean-up operation than has previously been carried out. However, an enterprise does not anticipate the new technology for cleaning up unless it is supported by development of a completel sufficient objective evidence.32. The effect of possible new legislation is taken into consideration in measuring an existing obligation when sufficient objective evidence exists that the legislation is virtually certain to beenacted. The variety of circumstances that arise in practice makes it impossible to specify a single event that will provide sufficient, objective evidence in every case. Evidence is required both of what legislation will demand and of whether it is virtually certain to be enacted and implemented in due course. In many cases sufficient objective evidence will not exist until the new legislation is enacted.Expected Disposal of Assets33. Gains from the expected disposal of assets should not be taken into account in measuring a provision.34. Gains on the expected disposal of assets are not taken into account in measuring a provision, even if the expected disposal is closely linked to the event giving rise to the provision. Instead, an enterprise recognisesgains on expected disposals of assets at the time specified by the International Accounting Standard dealing with the assets concerned. Reimbursements35. Where some or all of the expenditure required to settle a provision is expected to be reimbursed by another party, the reimbursement should be recognised when, and only when, it is virtually certain that reimbursement will be received if the enterprise settles the obligation. The reimbursement should be treated as a separate asset. The amount recognised for the reimbursement should not exceed the amount of the provision.36. In the income statement, the expense relating to a provision may be presented net of the amount recognised for a reimbursement.37. Sometimes, an enterprise is able to look to another party to pay part or all of the expenditure required to settle a provision (for example, through insurance contracts, indemnity clauses or suppliers' warranties). The other party may either reimburse amounts paid by the enterprise or pay the amounts directly.38. In most cases the enterprise will remain liable for the whole of the amount in question so that the enterprise would have to settle the full amount if the third party failed to pay for any reason. In this situation, a provision is recognised for the full amount of the liability, and a separate asset for the expected reimbursement is recognised when it is virtuallycertain that reimbursement will be received if the enterprise settles the liability.39. In some cases, the enterprise will not be liable for the costs in question if the third party fails to pay. In such a case the enterprise has no liability for those costs and they are not included in the provision.40. As noted in paragraph 29,severally liable is a contingent liability to the extent that it is expected that the obligation will be settled by the other parties.Changes in Provisions41. Provisions should be reviewed at each balance sheet date and adjusted to reflect the current best estimate. If it is no longer probable that an outflow of resources embodying economic benefits will be required to settle the obligation, the provision should be reversed.42. Where discounting is used, the carrying amount of a provision increases in each period to reflect the passage of time. This increase is recognised as borrowing cost.Use of Provisions43. A provision should be used only for expenditures for which the provision was originally recognised.44. Only expenditures that relate to the original provision are set against it. Setting expenditures against a provision that was originally recognised for another purpose would conceal the impact of two different events.Future Operating Losses45. Provisions should not be recognised for future operating losses.46. Future operating losses do not meet the definition of a liability in paragraph 10.the general recognition criteria set out for provisions in paragraph 1447. An expectation of future operating losses is an indication that certain assets of the operation may be impaired. An enterprise tests these assets for impairment under IAS 36, Impairment of Assets.Onerous Contracts48. If an enterprise has a contract that is onerous, the present obligation under the contract should be recognised and measured as a provision. 49. Many contracts (for example, some routine purchase orders) can be cancelled without paying compensation to the other party, and therefore there is no obligation. Other contracts establish both rights and obligations for each of the contracting parties. Where events make such a contract onerous, the contract falls within the scope of this Standard and a liability exists which is recognised. Executory contracts that are not onerous fall outside the scope of this Standard. 50. This Standard defines an onerous contract as a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it. The unavoidable costs under a contract reflect the least net cost of exiting from the contract, which is the lower ofthe cost of fulfilling it and any compensation or penalties arising from failure to fulfil it.51. Before a separate provision for an onerous contract is established, an enterprise recognises any impairment loss that has occurred on assets dedicated to that contract(see IAS 36, Impairment of Assets). Restructuring52. The following are examples of events that may fall under the definition of restructuring: (a) sale or termination of a line of business; (b) the closure of business locations in a country or region or the relocation of business activities from one country or region to another; (c) changes in management structure, for example, eliminating a layer of management; (d) fundamental reorganisations that have a material effect on the nature and focus of the enterprise's operations.53. A provision for restructuring costs is recognised only when the general recognition are met. Paragraphs 72-83 set out how criteria for provisions set out in paragraph 14the general recognition criteria apply to restructurings.54. A constructive obligation to restructure arises only when an enterprise:(a) has a detailed formal plan for the restructuring identifying at least: (i) the business or part of a business concerned;(ii) the principal locations affected;(iii) the location, function, and approximate number of employees whowill be compensated for terminating their services;(iv) the expenditures that will be undertaken;(v) when the plan will be implemented;(b) has raised a valid expectation in those affected that it will carry out the restructuring by starting to implement that plan or announcing its main features to those affected by it. . Evidence that an enterprise has started to implement a restructuring plan would be provided, 55for example, by dismantling plant or selling assets or by the public announcement of the main features of the plan. A public announcement of a detailed plan to restructure constitutes a constructive obligation to restructure only if it is made in such a way and in sufficient detail (i.e. setting out the main features of the plan) that it gives rise to valid expectations in other parties such as customers, suppliers and employees (or their representatives) that the enterprise will carry out the restructuring.56. For a plan to be sufficient to give rise to a constructive obligation when communicated to those affected by it, its implementation needs to be planned to begin as soon as possible and to be completed in a timeframe that makes significant changes to the plan unlikely. If it is expected that there will be a long delay before the restructuring begins or that the restructuring will take an unreasonably long time, it is unlikely that the plan will raise a valid expectation on the part of others that theenterprise is at present committed to restructuring, because the timeframe allows opportunities for the enterprise to change its plans.57. A management or board decision to restructure taken before the balance sheet date does not give rise to a constructive obligation at the balance sheet date unless the enterprise has, before the balance sheet date:(a) started to implement the restructuring plan;(b) announced the main features of the restructuring plan to those affected by it in a sufficiently specific manner to raise a valid expectation in them that the enterprise will carry out the restructuring. In some cases, an enterprise starts to implement a restructuring plan, or announces its main features to those affected, only after the balance sheet date. Disclosure may be , Events After the Balance Sheet Date, if the restructuring is of required under IAS 10 such importance that its non-disclosure would affect the ability of the users of the financial statements to make proper evaluations and decisions.58. Although a constructive obligation is not created solely by a management decision, an obligation may result from other earlier events together with such a decision. For example, negotiations with employee representatives for termination payments, or with purchasers for the sale of an operation, may have been concluded subject only to board approval. Once that approval has been obtained and communicated to the other parties, the enterprise has a constructive obligation to restructure, if theconditions of paragraph 72 are met.. 59. In some countries, the ultimate authority is vested in a board whose membership gement (e.g. employees) includes representatives of interests other than those of managment.or notification to such representatives may be necessary before the board decision is taken. Because a decision by such a board involves communication to these representatives, it may result in a constructive obligation to restructure.60. No obligation arises for the sale of an operation until the enterprise is committed to the sale, i.e. there is a binding sale agreement.61. Even when an enterprise has taken a decision to sell an operation and announced that decision publicly, it cannot be committed to the sale until a purchaser has been identified and there is a binding sale agreement. Until there is a binding sale agreement, the enterprise will be able to change its mind and indeed will have to take another course of action if a purchaser cannot be found on acceptable terms. When the sale of an operation is envisaged as part of a restructuring, the assets of the operation , Impairment of Assets. When a sale is only are reviewed for impairme-ent under IAS 36part of a restructuring, a constructive obligation can arise for the other parts of the restructuring before a binding sale agreement exists.62. A restructuring provision should include only the direct expenditures arising form the restrict-uring,which are those that are both:(a) necessarily entailed by the restructuring; and(b) not associated with the ongoing activities of the enterprise.63. A restructuring provision does not include such costs as:(a) retraining or relocating continuing staff;(b) marketing; or(c) investment in new systems and distribution networks.These expenditures relate to the future conduct of the business and are not liabilities for restructuring at the balance sheet date. Such expenditures are recognised on the same basis as if they arose independently of a restructuring.64. Identifiable future operating losses up to the date of a restructuring are not included in a provision, unless they relate to an onerous contract as defined in paragraph 10. , gains on the expected disposal of assets are not taken65. As required by paragraph 51into account in measuring a restructuring provision, even if the sale of assets is envisaged as part of the restructuring.Disclosure66. For each class of provision, an enterprise should disclose:(a) the carrying amount at the beginning and end of the period;(b) additional provisions made in the period, including increases toexisting provisions; (c) amounts used (i.e. incurred and charged against the provision) during the period; (d) unused amounts reversed during the period; and(e) the increase during the period in the discounted amount arising from the passage of time and the effect of any change in the discount rate. Comparative information is not required67. An enterprise should disclose the following for each class of provision:(a) a brief description of the nature of the obligation and the expected timing of any resulting outflows of economic benefits;(b) an indication of the uncertainties about the amount or timing of those outflows. Where necessary to provide adequate information, an enterprise should disclose the major assumptions made concerning future events, as addressed in paragraph 48(c) the amount of any expected reimbursement, stating the amount of any asset that has been recognised for that expected reimbursement.68. Unless the possibility of any outflow in settlement is remote, an enterprise should disclose for each class of contingent liability at the balance sheet date a brief description of the nature of the contingent liability and, where practicable:;(a) an estimate of its financial effect, measured under paragraphs 36(b) an indication of the uncertainties relating to the amount or timing of any outflow; (c) the possibility of any reimbursement.69. In determining which provisions or contingent liabilities may be aggregated to form a class, it is necessary to consider whether the nature of the items is sufficiently similar for a single statement about them to fulfil the requirements of paragraphs 85(a)and (b) and 86(a) and (b). Thus, it may be appropriate to treat as a single class of provision amounts relating to warranties of different products, but it would not be appropriate to treat as a single class amounts relating to normal warranties and amounts that are subject to legal proceedings.70. Where a provision and a contingent liability arise from the same set of -86 in a circumstances, an enterprise makes the disclosures required by paragraphs 84 that shows the link between the provision and the contingent liability.71. Where an inflow of economic benefits is probable, an enterprise should disclose a brief description of the nature of the contingent assets at the balance sheet date, and, where practicable, an estimate of their financial effect, measured using the principles set out for provisions in paragraphs 3672. It is important that disclosures for contingent assets avoid giving misleading ndications of the likelihood of income arising.73 In extremely rare cases, disclosure of some or all of the information required by paragraphs 84-89 can be expected to prejudice seriously the position of the enterprise a dispute with other parties on the subject matterof the provision, contingent or contingent asset. In such cases, an enterprise need not disclose the information, but should disclose the general nature of the dispute, together with the fact that, and reason why, the information has not been disclosed. Transitional Provisions74. The effect of adopting this Standard on its effective date (or earlier) should be reported as an adjustment to the opening balance of retained earnings for the period in which the Standard is first adopted. Enterprises are encouraged, but not required, to adjust the opening balance of retained earnings for the earliest period presented and to restate comparative information. If comparative information is not restated, this fact should be disclosed. , Net Profit or Loss for the75. The Standard requires a different treatment from IAS 8requires Period, Fundamental Errors and Changes in Accounting Policies. IAS 8comparative information to be restated (benchmark treatment) or additional pro forma comparative information on a restated basis to be disclosed (allowed alternative reatment) unless it is impracticable to do so.。

会计稳健性

▪ 赵春光(2004)讨论了会计盈余稳健性的变化趋势,发现在 1999、2000和2001年有所提高。

▪ 陈旭东和黄登仕(2006)使用1993-2003年间我国上市公司 数据发现,会计稳健性在1998年后逐渐增强,2001年以 后上市公司的会计具有稳健性。

三、会计稳健性在我国的应用与发展

▪ 第一阶段:从无到有的突破阶段(1985年~ 1997年)

▪ 1985年7月1目,我国实施了《中外合资企业会计制度》, 是新中国成立以来第一部借鉴国际会计惯例制定的全新 的会计制度。它提出了稳健性原则,如存货以成本与可 变现净值孰低法计价等。

▪ 1992年l1月16日,财政部颁布了《企业会计准则》,初 步建立了适应市场经济发展的企业会计制度体系。基本 会计准则提出了会计核算的12项原则,其中规定“会计 核算应当遵循谨慎性原则的要求,合理核算可能发生的 损失和费用”,这是我国首次就稳健性原则(谨慎性原则) 明确提出要求。同时,在行业会计制度中稳健性原则主 要体现在三个方面:即存货计价方法采用后进先出法、 应收账款计提坏账准备、固定资产折旧采用加速折旧法。

6

▪ 会计稳健性的分类: (根据其性质的差异)

▪ 非条件稳健性(Unconditional Conservatism)也称为独立 稳健性(Independent Conservatism),这种稳健性意味着 会计处理方法在资产或负债形成的时候就已经确定了,不会 再根据其后的经营环境而变化,它一般会导致不可确认的商 誉存在,使得股东权益的账面价值低于其市场价值。如有关 研究开发的费用化处理,以及大部分固定资产使用加速折旧 法等。它是一个总体的偏见,和当期的消息没有关系。

会计盈余的稳健性_发现与启示

会计盈余的稳健性_发现与启示会计盈余的稳健性: 发现与启示摘要: 会计盈余的稳健性是衡量一家企业财务健康状况的重要指标。

本文通过分析会计盈余的稳健性,探讨了稳健性的定义、原则以及影响因素,并深入探讨了它对企业的重要意义与启示。

一、稳健性的定义与原则会计盈余的稳健性是指企业对不利信息持保守态度,即在缺乏充分证据时不予承认预期盈利,但对于预期亏损则要提前进行计提。

稳健性原则强调谨慎态度,根据风险与利益的不对称性,确保财务报告表达真实、合理、可靠的信息。

二、稳健性的影响因素1. 企业规模:通常情况下,较大规模的企业更注重会计盈余的稳健性,因为它们面临着更大的风险。

2. 行业特点:某些行业如金融、房地产等风险更高,会计盈余的稳健性要求更高。

3. 法律法规要求:不同国家和地区对会计准则有不同的规定,一些国家对稳健性有着更为严格的要求。

三、稳健性的重要意义1. 提供可靠信息:稳健性原则保证了财务报告的可靠性和真实性,投资者和相关利益关系方可以凭借稳健性原则提供的信息做出明智的决策。

2. 防止财务欺诈:稳健性原则能够防止企业虚构盈余数据、操纵财务报告,有效减少企业间的不公平竞争。

3. 保护投资者利益:只有真实可靠的财务信息才能提供对投资者利益的保护,而会计盈余的稳健性则是实现这一目标的重要手段。

四、稳健性的启示1. 加强企业治理:企业应加强内部控制,确保财务报告的准确性和可靠性,保证会计盈余的稳健性。

2. 提高透明度:定期披露企业财务信息,提高信息透明度,为投资者提供充分的信息,增强市场的有效运作。

3. 加强监管:政府和监管部门应加强对企业财务报告的监管,确保企业遵守会计准则,保护投资者和市场的利益。

4. 提高会计人员专业素养:会计人员应具备高度的职业道德和专业技能,保证会计盈余的准确计算和稳健识别。

结论: 会计盈余的稳健性是确保财务报告可靠性和投资者利益保护的重要原则。

企业应根据自身情况加强会计盈余的稳健性管理,加强透明度、监管以及会计人员的专业素养,才能实现稳健健康的财务状况综上所述,会计盈余的稳健性对于确保财务报告的可靠性和投资者利益保护至关重要。

会计稳健性的研究综述_佟玲

&FOREIGNENTREPRENEURS2014年4月刊(总第456期)CHINESE一、引言近年来,伴随着我国证券市场的发展,会计稳健性在会计实务中的重视程度逐步增加,这将很大程度上影响企业的会计稳健性水平。

市场经济条件下,企业生产经营过程中不可避免地会遭遇风险,实施谨慎原则,能够使企业在风险实际发生之前对其加以防范并化解,可以说,谨慎地选择会计政策,对企业的经营决策有正向的引导作用,使利益相关者的切身利益得以保护,并提高企业的竞争力。

二、会计稳健性的内涵与分类首先从定义上看,Bliss(1924)会计师将稳健原则表述为“预见所有可能的损失,但不预期任何不确定的收益”。

国际会计准则委员会在其概念框架中将稳健性定义如下:“谨慎性是在不确定的条件下,需要运用判断做出必要的估计中包含一定程度的审慎,比如资产或收益不可高估,负债或费用不可低估。

”稳健性是会计确认与计量的传统和原则。

稳健性意味着会计人员在确认好消息的时候对可验证性的要求更高,所以稳健性就意味着对损失和收益确认的非对称性,即会计人员对于损失(坏消息)要及时确认而对于收益(好消息)直到有充分的证据时才予以确认。

会计实务也一直深受稳健性原则的影响,例如存货计价中的成本与市价孰低原则以及资产减值的处理都有着稳健性的烙印。

Basu(1997)认为,稳健性对会计实务的影响至少有500年以上的历史;Sterling(1970)将稳健性作为会计实务中最有影响力的原则之一。

一般而言,稳健性意味着资产的账面价值低于其市场价值(因为存在着没有确认的商誉)。

在学术界,根据性质的差异将稳健性分为两种不同的类别’:条件稳健性和非条件稳健性。

首先非条件稳健性,也称为独立稳健性,这种稳健性意味着会计处理方法在资产或负债形成的时候就己经确定了,不会再根据其后的经营环境而变化,它一般会导致不可确认的商誉存在。

关于非条件稳健性的例子有研究支出的费用化处理,以及大部分固定资产使用加速折旧法,以及对净现值为正的项目使用历史成本等。

浅谈稳健性原则在会计中的运用

成本和市 价进行 比较 , 认市价下跌而 不确认市 价上涨 ; 确 存货 跌价准 备则是期末 的时候对存 货的计价 采用成本和 可变净 现 值孰 低法 , 避免在市场 经济下 , 存货的价格 变化 导致 存货 的价 值减少 ; 长期投资 、 资产 、 固定 无形资产减值 准备则需要在期末 值 , 需要计提相应 的减值准备 ; 建工程减值 准备 则是对长 则 在 准备 ; 而对企业 的委托贷款 本金需要进行 定期检 查 , 按本金和

- _ _ _ - ● - - ● _ _ - _ _ _ - _ _ _ _ ●-

_ l● __ __ __ -

CO NTEM RARYECO NO O P

℃S

●■■■●

企业会计准 则中对 固定 资产 的折 旧方法有 直线 法和加速 折 旧法 , 如果企业选择加速折 旧方法就会导致 其在固定资产使 用 的前几年 多计提折 旧 , 而减少 企业 前几 年的利 润 , 从 也加快 了物 资的淘汰 和推陈 出新 , 科技不断 发展 、 产力不 断发展 在 生 的形 势下 , 采用加 速折旧 法也 是谨慎原 则的 考虑 , 也考 虑了 固

本文以企业 稳健 『 生原则的运用 为对象 , 探讨 其具体的运用

目前稳健性 原则的运用和客观性原 则 、 比性原则 等还 存 可 在一定的冲突 。 例如稳健性原则和可比性原则的冲突体 现在 可 比性原 则要 求会 计核算要按照规定 的会 计处理方法进行 , 到 做 口径一致 , 但是稳健性原则则 要求企业可 以根 据 自身的具体 情 况变化改变核算 的 口径和方法 , 者有一定 的冲突 。国家要 完 二

保 持足够 的警惕 , 以应付外 界的变化 , 将风 险和损失 缩小到可 接受 的范围。

认或有资产。 或有负债一旦变成损失就会影响到企业的偿债能 力 , 认或有负债能 够全面反映 企业的负债 情况 , 确 减少 企业的

会计四大假设介绍英语作文

会计四大假设介绍英语作文The accounting profession is built upon four fundamental assumptions, which serve as the foundation for financial reporting. These assumptions provide a framework for accountants to prepare and present financial statements in a consistent and reliable manner. Let's take a closer look at each of these four major assumptions.1. Going Concern Assumption: This assumption assumes that a business will continue to operate indefinitely unless there is evidence to the contrary. It implies that the company will not be forced to liquidate its assets or cease operations in the near future. By assuming the going concern, accountants can prepare financial statements that reflect the long-term nature of a business.2. Monetary Unit Assumption: The monetary unit assumption states that financial transactions should be recorded and reported in a common unit of currency. This assumption allows for the aggregation and comparison offinancial information across different entities and time periods. By using a common unit of currency, such as the US dollar or the euro, accountants can provide meaningful and comparable financial information to users of financial statements.3. Time Period Assumption: The time period assumption divides the life of a business into distinct and meaningful intervals for reporting purposes. This assumption allows accountants to prepare financial statements for specific periods, such as monthly, quarterly, or annually. By reporting financial information on a regular basis, stakeholders can assess the performance and financial position of a business over time.4. Historical Cost Assumption: The historical cost assumption requires that assets and liabilities be recorded at their original cost at the time of acquisition. This assumption implies that the value of assets and liabilities remains constant over time, unless there is evidence to suggest otherwise. While this assumption may not reflect the current market value of assets and liabilities, itprovides a reliable and objective basis for financial reporting.These four major assumptions play a crucial role in shaping the way financial information is prepared and presented. They provide a common language and framework for accountants to communicate financial information to stakeholders. By understanding and applying these assumptions, accountants can ensure the reliability and comparability of financial statements, ultimately enhancing the transparency and trustworthiness of the accounting profession.。

第九讲 会计稳健性

5.或有事项的确认和计量 《企业会计准则第13号——或有事项》第四条规定: “与或有事项相关的义务同时满足下列条件,应当确认 为预计负债: (1)该义务是企业承担的现时义务; (2)该义务的履行很可能导致经济利益流出企业; (3)该义务的金额能够可靠地计量。”同时第十三条 还规定:“企业不应当确认或有负债和或有资产。”

会计稳健性

小组分工:

陆明月负责第一、二部分 周娟负责第三、四部分 许庆玥负责第五部分

会计稳健性

(一)什么是会计稳健性 (二)会计稳健性与通常的会计谨慎性是何关系

(三)会计稳健性研究的重要意义何在

(四)如何度量会计的稳健性 (五)哪些因素会影响会计稳健性

一.什么是会计稳健性

(一)会计稳健性定义的发展历程 (二)实证研究中的会计稳健性定义 (三)条件稳健性和无条件稳健性

陆明月负责第一二部分周娟负责第三四部分许庆玥负责第五部分一什么是会计稳健性二会计稳健性与通常的会计谨慎性是何关系三会计稳健性研究的重要意义何在四如何度量会计的稳健性五哪些因素会影响会计稳健性一会计稳健性定义的发展历程二实证研究中的会计稳健性定义三条件稳健性和无条件稳健性1basu1997认为稳健性对会计实务的影响至少有500年以上的历史

回目录

2. 模型法 (1) 收益变化模型 稳健性意味着收益比损失更具有持续性。因为财务 报告不确认未被证实的资产价值增长 ( 经济收益) , 而是在未来期间现金流实现时才将其包含在会计收益中, 表现为公司正的收益或收益变化较为持续。而当发生损 失时, 公司及时确认表现为收益为负或负的变化, 这种 负的收益或收益变化是暂时的, 以后会出现反转。Basu、 Ball和Shivakumar用如下模型予以计量:

回目录

四.如何度量会计的稳健性

什么是会计稳健性

什么是会计稳健性稳健性原则是企业〔会计〕核算中运用的一项重要原则,《企业会计制度》和已发布的具体会计准则充分体现了这一原则。

稳健性原则又称慎重性原则,是指在处理企业不确定的经济业务时,应持慎重的态度。

那你知道什么是会计稳健性吗?接下来我告诉你什么是会计稳健性。

什么是会计稳健性:凡是可以预见的损失和费用都应予以记录和确认,而没有十足把握的收入则不能予以确认和入账。

在市场经济条件下,企业不可避免地会碰到风险,实施慎重原则,就能在风险实际发生之前化解风险,并防范风险,有利于企业做出正确的经营决策,有利于保护所有者和债权人的利益、提升企业在市场上的竞争力。

会计稳健性存在条件:会计的不确定性是指在一种或几种状况和境况下的最终结果是得利或损失,只有在发生或没发生一个或几个不确定的将来事项时,才干加以确认的会计信息。

在我们现在的社会中,由于科学技术的不断进步,经济的飞速发展,信息的传播速度也越来越快,致使会计领域中信息的不确定性问题也越来越复杂。

但会计不确定性问题产生的原因可以归纳为两个,一个是外因即由于会计系统外部环境的不断变化而产生的会计信息的不确定性如企业的承诺,以及与银行有关的资金借贷往来等信用,信用作为企业经营中一种必要的融通工具和交易保证,它是企业会计不确定性产生的一个重要原因;由于企业在外币业务中汇兑期限的不同而发生的汇兑损益,企业无形资产的摊销,合同生效的长短等也都会引起企业资产因时间的关系而不断的变化;企业在生产经营中,为了谋取超额的经济利益,就必定会存在着一定的风险性,由于这种风险性的存在,企业的会计信息中也就自然的存在着一种不确定性;另外,企业的生存与发展总是和社会,环境分不开的,那么会计信息就一定会受到税率例率、物价变动指数、通货膨胀等因素的影响,而使企业的资产不断发生变化。

另一个原因为内因,即指由于会计系统内部的信息加工过程中存在的不确定性问题而引起的会计信息的不确定性,如在会计人员确实认,计量、记录和报告中,因自身业务水平或职业道德素养的限制,而使企业的会计信息不断的发生变化。

韩德睿-会计102-外文翻译

毕业设计(论文)外文资料翻译系:经济系专业:会计学姓名:韩德睿学号: 1005180222 外文出处:SME and Entrepreneurship Financing: The Roleof Credit Guarantee Schemes and Mutual Guarantee Societies in supporting finance for small and medium-sized enterprises附件: 1.外文资料翻译译文;2.外文原文。

附件1:外文资料翻译译文中小企业与创业融资:信用担保计划及互助担保社团在给予小型和中小型企业金融支持中的作用最终报告内容提要1.在许多国家,信用担保计划(CGSs)代表了一个解决中小企业融资缺口的重要政策工具,同时也缓解了公共财政的负担。

因为没有足够的担保抵押能力,有限或者空的信用记录,以及经常缺乏必要的专业知识去编制精细复杂的财务报表,中小企业和创业企业通常被限制获得信贷。

公司与潜在放贷人之间存在的信息不对称,意味着后者对借款者来说具有默认情况下的高风险属性,而且,在没有足够的抵押品的情况下,最终导致一个对信贷需求部分或否定的反应。

信用担保机制是一种常用的针对这种市场失灵情况的办法。

通过给予一部分所要求的贷款担保保护,CGS可以降低贷款人的风险,并且有利于向那些有信用约束的企业提供融资。

2.在一些经合组织国家,信用担保计划已经成为决策者在近来的金融危机中改善中小企业和企业家融资渠道的工具。

在一些非经合组织国家,信用担保制度也成为拓展信贷市场,改善金融包容性的机制,并迅速的发展起来。

公共担保工具的扩展,以及对私人担保计划的扶持,通过提供资金或共同担保,引发了对对监测和评估的更大需求。

同时,也有必要去区分从广泛使用的信用担保产生并成为他们的日常运作的反周期工具,进而成为金融体系的结构要素所带来的特定挑战。

3.目前的研究目的是通过几个方面的调查如所有制结构和资金,法律和监管框架,以及包括服务类型,资格标准,担保分配处理和信贷风险管理在内的计划的运作特点,来提高对信用担保的作用,影响和可持续性的认识。

浅析会计稳健性原则

浅析会计稳健性原则作者:孙晓雯来源:《财经界·学术版》2015年第06期摘要:本文首先简要介绍了会计稳健性的含义,并首次从微观和宏观两方面简要阐述了会计稳健性的重要意义,然后重点阐述了稳健性在实际运用中存在的主要问题,并提出了几点建议,为今后进一步研究和运用稳健性原则,保证会计信息的真实性和客观性,能够提供一定的参考。

关键词:会计稳健性原则应用一、会计稳健性的含义会计稳健性在业内一直没有统一的定义,本文通过对以往文献资料的翻阅对比,将会计稳健性的含义描述为:会计人员在不确定的会计环境下,充分估计可能发生的风险和损失,在对会计信息作出判断时,要以不高估资产或收益,也不低估负债或费用为原则,保持必要的谨慎,从而对会计要素的确认和计量作出恰当合理的估计。

二、运用会计稳健性原则的重要意义会计稳健性原则的意义我们可以从两个方面来看,一个是微观层面的意义,即对个别企业的影响;一个是宏观层面的意义,即对整个国家经济的影响:一是在微观层面上,稳健性在整个会计核算工作中的适度运用,是对历史成本法计量不足的补充,它可以降低企业各契约方的违约可能性,提高会计核算的质量,降低企业的代理成本,满足内部经营决策的需要,有利于保护各投资方的利益,帮助企业规避各种经营与投资风险,强化企业的整体竞争实力;二是在宏观层面上,会计稳健性是社会主义市场经济发展的必然产物,符合当前我国的实际情况,它的适度运用有利于我国树立稳定可靠的财政来源,有利于稳定物价,降低经济的不稳定性,保障社会主义市场经济健康有序的发展。

三、稳健性原则在实际运用中存在的主要问题(一)稳健性原则的相关条款缺乏一定的可操作性当前,由于我国的会计准则和会计政策规定还不够细致完善,会计核算方法不统一,缺乏一定的可操作性,导致企业在进行会计核算时,利用会计政策的漏洞,虚增、虚减利润来达到自己的目的。

如对存货的计量,是采用先进先出法还是后进先出法。

(二)税法规定限制了稳健性原则的运用当前,企业在计算应纳所得税额时,无论企业的财务会计如何核算,均按税法规规定执行。

(完整版)哈佛分析框架外文文献及翻译

经营分析与估值克雷沙·G.帕利普保罗·M.希利摘自书籍“Business Analysis and Valuation”第五版第一章节1.简介本章的目的是勾勒出一个全面的财务报表分析框架。

因为财务报表提供给公共企业经济活动最广泛使用的数据,投资者和其他利益相关者依靠财务报告评估计划企业和管理绩效率。

各种各样的问题可以通过财务状况及经营分析解决,如下面的示例所示:一位证券分析师可能会对问:“我的公司有多好?这家公司是否符合我的期望?如果没有,为什么不呢?鉴于我对公司当前和未来业绩的评估,该公司的股票价值是多少?”一位信贷员可能需要问:“这家公司贷款给这家公司有什么贷款?公司管理其流动性如何?公司的经营风险是什么?公司的融资和股利政策所产生的附加风险是什么?“一位管理顾问可能会问:“公司经营的行业结构是什么?该策略通过在工业各个企业追求的是什么?不同企业在行业中的相对表现是什么?”公司经理可能会问:“我的公司是正确的估值的投资者吗?是我们在通信程序中有足够的投资者来促进这一过程?”财务报表分析是一项有价值的活动,当管理者在一个公司的战略和各种体制因素完成后,他们不可能完全披露这些信息。

在这一设置中,外部分析师试图通过分析财务报表数据来创建“中端信息”,从而获得有价值的关于该公司目前业绩和未来前景的展望。

了解财务报表分析所做的贡献,这是很重要的理解在资本市场的运作,财务报告的作用,形成财务报表制度的力量。

因此,我们首先简要说明这些力量,然后我们讨论的步骤,分析师必须执行,以提取信息的财务报表,并提供有价值的预测。

2.从经营活动到财务报表企业管理者负责从公司的环境中获取物理和财务资源,并利用它们为公司的投资者创造价值。

当公司在资本成本的超额投资时,就创造了价值。

管理者制定经营战略,实现这一目标,并通过业务活动实施。

企业的经营活动受其经济环境和经营战略的影响。

经济环境包括企业的产业、投入和产出的市场,以及公司经营的规章制度。

1-4. 会计稳健性对企业融资活动的影响:来自日本的证据

The Effect of Accounting Conservatism on Corporate Financing Activity:Evidence from JapanSouhei IshidaGraduate School of Commerce and Management, Hitotsubashi Universitycd132001@g.hit-u.ac.jp3 August, 2014AbstractThis study examines how two types of conservatism―unconditional conservatism and conditional conservatism―affect Japanese firms’ financing activity, in particu lar, borrowing money from banks. This study obtained the two main findings. First, firms practicing a higher level of unconditional conservatism borrow more money from banks under the condition of facing a funding shortfall. Second, the degree of their conditional conservatism does not significantly relate with the degree of proceeds from loans. These results are robust to the endogeneity problem between conservatism and firms’ borrowing activity. In addition, I find that firms having a strong relationship with the main bank benefit from unconditional conservatism and conditional conservatism is useful for firms having a weak relationship with the main bank. This paper reveals that the economic consequences of conservatism vary across institutional factors and suggests the possibility that the nature of conservatism has been misjudged by focusing only on the accounting system when considering its economic consequences.Keywords: Accounting Conservatism; Corporate Financing Activity; Loan; Main Bank1.IntroductionThis study examines how two types of conservatism―unconditional conservatism and conditional conservatism―affect Japanese firms’ financing activity, in particular, borrowing money from banks.Conservatism has a long history. For example, conservatism is said to have influenced accounting practice for at least 500 years (Basu 1997). Conservatism became an American accounting principle in 1938 (Sanders et al. 1938), and was described in Japanese accounting principles in 1949 (ESB 1949). However, there has been a global movement for the elimination of conservatism. In 2005, the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) published a joint paper discussing conservatism as part of the conceptual framework project, which stated that the common conceptual framework should not include conservatism among the desirable qualitative characteristics of accounting information (FASB 2005). The process of accounting standards convergence, in turn, led their attitudes to influence those of the Accounting Standards Board of Japan (ASBJ) (Yaekura 2007).On the other hand, many researchers have analyzed the economic rationality of conservatism and reported that it improves the efficiency of contracting (Watts 2003). However, these papers suffer from two problems. First, the conservatism examined by previous research is not always the same as that eliminated by the bodies in charge of setting standards. While many previous studies focus on “conditional” conservatism and analyze it’s rationality (García Lara et al. 2014; Iyengar and Zampeli 2010; LaFond and Roychowdhury 2008; Nikoleav 2010; Wittenberg-Moerman 2008), Kanamori (2009) reveals that the conservatism eliminated by standards setting bodies is not conditional conservatism but rather “unconditional” conservatism1. Therefore, academic research cannot contribute to setting standards without drawing a distinction between conditional conservatism and unconditional conservatism and examining the economic consequences of each.The second, problem is the external validity of previous research. As stated above, many studies have focused on conservatism. Many of these argue that unconditional conservatism does not 1Kanamori (2009) examines accounting standards published by FASB from 1973 to 2002 and finds that approximately 40% of published accounting standards exclude unconditional conservatism.improve contracting efficiency, unlike conditional conservatism (Bauwhede 2007; Ball and Shivakumar 2005; Qiang 2007; Zhang 2008). However, because these studies analyze U.S. listed companies, questions can be raised about the validity of generalizing these findings to firms based in other countries. Wysoki (2011) argues that an accounting system is interrelated to other institutional factors and the economic consequences of accounting systems can vary across these institutional factors. This suggests the possibility that the nature of the economic consequences have been misjudged by focusing only on accounting systems.Using a large sample of Japanese listed firms during 2003–2012, I analyze how both unconditional conservatism and conditional conservatism affected corporate borrowing activity from banks. Japanese financial system is centered on banks, which develop a long-term and close relationship with their borrowers (Hiroda 2012). This traditional Japanese system is known as the main bank system, and has possibly lead conservatism to have consequences different from those observed in other countries.This study obtained the two main findings. First, firms practicing a higher level of unconditional conservatism borrow more money from banks under the condition of facing a funding shortfall. Second, the degree of their conditional conservatism does not significantly relate with the degree of proceeds from loans. These results are robust to the endogeneity problem between conservatism and firms’ borrowing activity.In addition, I find that firms having a strong relationship with the main bank benefit from unconditional conservatism and conditional conservatism is useful for firms having a weak relationship with the main bank.This paper greatly contributes to the literature. First, this study reveals that firms benefit from unconditional conservatism in Japan. Previous research argues that conditional conservatism benefits firms through improving their debt-contracting efficiency, unlike unconditional conservatism. I provide evidence different from that found by this previous research.Second, this study reveals that the economic consequences of conservatism vary across the degrees of firms’ relationships with the main bank. Wysoki (2011) argues that the accounting system is interrelated to other institutional factors, and therefore the economic consequences of theaccounting system can vary across different institutional factors. This study followed through on this possibility to examine if the economic consequences of the accounting system have been misjudged by focusing only on the accounting system itself. Thus, this study contributes to literature on the new institutional accounting regime.Finally, this study focuses on proceeds from long-term loans payable. Using interest rate and credit rating, previous studies examine the economic rationality of conservatism for debt contracting (Bauwhede 2007; Nakamura 2008; Zhang 2008). However, I cannot directly analyze the relationship between conservatism and debt contracts using these items because I was unable to identify when these items are decided. On the other hand, data on proceeds from long-term loans payable are a readily available form of cash flow statement that permits identification of when firms borrow money from banks. Therefore, this study provides direct evidence for the link between conservatism and debt contracts. In addition, my approach opens the possibility of application to other studies.The remainder of this paper proceeds as follows. Section 2 reviews the literature and presents the hypotheses. Section 3 provides a detailed research design and sampling methodology. Section 4 provides the main results, and Section 5 reports additional results. Section 6 provides the conclusion.2.Literature Review and Hypotheses(1)Unconditional Conservatism and Conditional ConservatismThis section reviews previous research and provides the hypotheses. First, I provide a simple explanation of conservatism and define both unconditional conservatism and conditional conservatism.Conservatism is defined as a downward bias in the accounting of net asset value relative to economic net asset value resulting from the asymmetric recognition of economic value in accounting income (Beaver and Ryan 2005; Ruch and Taylor 2011). Based on this definition, conservatism manifests itself in two approaches. One that recognizes expenses earlier and other that recognizes revenue later. However, many previous studies present only the former as an example of conservatism. Examples of conservatism include (i) lower cost or market for inventory, (ii)impairment for long-lived tangible and intangible assets, (iii) immediate expensing of the cost of internally generated intangible assets, and (iv) accelerated amortization of long-lived assets (Edwards 1989; Ryan 2006; Sanders et al. 1983). Because revenue is generally recognized on a realization basis and conservatism has no room for the recognition of revenue, many previous studies may regard recognizing expenses earlier as an example of conservatism. Based on this view, whether a firm is conservative depends entirely on the timing of recognizing expenses.Recent studies point out two ways in which conservatism can be utilized in terms of recognizing expenses. One is recognizing expenses at the time when the value decreases, whereas the other is recognizing them before the value decreases. Consider, for example, the recognition of goodwill expenses. They can be recognized in two ways: (i) amortization and (ii) impairment2. Although impairment accounting recognizes the expenses when the value of goodwill declines, amortization accounting recognizes expenses before the value of goodwill declines. Given that revenue recognition is based on a realization basis, both these methods underestimate accounting of net asset value. However, because a time lag exists between impairment and amortization in terms of the timing of recognizing expenses, the timings of underestimating accounting of net asset values differs between these two methods. Recent studies focus on these timing differences and call the conservatism of recognizing expenses when the value declines as “conditional conservatism” and the conservatism of recognizing expenses before the value declines as “unconditional conservatism” (Beaver and Ryan 2005).(2)Conservatism and Contracting Efficiency3On the basis of Basu (1997), many studies attempted to reveal the economic rationality of 2Under U.S. general accounting principles (GAAP) and IFRS, goodwill most not be amortized and should be regularly tested for impairment (IFRS 3; Topic 350). On the other hand, goodwill must be amortized within 20 years under Japanese GAAP and be regularly tested for impairment (Corporate Accounting Standards 21).3Because many previous studies do not draw a distinction between unconditional conservatism and conditional conservatism, I categorize these studies into “unconditional conservatism” research and “conditional conservatism” research based on the measurements they use. If these studies use the measurements proposed by Ball and Shivakumar (2005), Basu (1997), Callen et al. (2009), and Khan and Watts (2009), I categorize them as “conditional conservatism” research. On the other hand, if they use the measurements proposed by Ahmed et al. (2002), Beaver and Ryan (2000), Giner and Rees (2001), and Penman and Zhang (2002), I categoriz e them as “unconditional conservatism” research.conditional conservatism. A review of recent papers revealed broad agreement with the opinion that conditional conservatism improves contracting efficiency.Shareholders and creditors often contract with a firm manager on the basis of accounting numbers. However, because information asymmetry exists between the manager and shareholders/creditors, the manager has incentive to bias earnings and equity upward by recognizing losses later to maximize his or her own welfare. This is likely to impair both shareholder and creditor wealth. Watts (2003) argues that (conditional) conservatism improves contracting efficiency to offset this upward bias.Recent empirical research finds that both shareholders and creditors demand conditionally conservative accounting by firms. For example, Qiang (2007) focuses on U.S. firms and shows that higher debt equity ratio induces a greater level of conditional conservatism. In addition, using a sample of U.S. firms, Nikolaev (2010) reports that reliance on covenants in public debt contracts is positively associated with the degree of timely loss recognition (i.e., conditional conservatism). On the other hand, LaFond and Roychowdhury (2008) examine (conditional) conservatism from the shareholders’ perspective. They use U.S. firms and show that (conditional) conservatism increases in the presence of agency problems between managers and shareholders. Iyengar and Zampeli (2010) also analyze the relationship between (conditional) conservatism and the sensitivity of executive pay to accounting performance. Using a sample of U.S. firms, they find that the sensitivity of executive pay to accounting performance is higher for firms that report (conditionally) conservative accounting earnings.Furthermore, some studies provide evidence that firms share in the shareholder and creditor benefits arising from conditional conservatism. For instance, Bauwhede (2007) examines U.S. firms and finds evidence that the credit ratings of firms in industries with more conditional conservatism are significantly more favorable. Using a sample of U.S. firms, Zhang et al. (2008) also show that (conditionally) conservative borrowers are more likely to violate debt covenants following a negative price shock and that lenders offer lower interest rates to more (conditionally) conservative borrowers. Wittenberg-Moerman (2008) focuses on U.S. firms and reports that timely lossrecognition (i.e., conditional conservatism) reduces the bid–ask spread in the secondary loan market. In addition, García Lara et al. (2014) examine U.S. firms and find that increase in firm-level conditional conservatism leads to a future decrease in the bid–ask spread and in stock returns volatility.In summary, many earlier studies provide evidence that conditional conservatism improves contracting efficiency. At the same time, the economic rationality of unconditional conservatism is questioned. For example, Ball and Shivakumar (2005) argue that unconditional conservatism does not function so as to improve contracting efficiency. Although unconditional conservatism biases both earnings and equity downward, this downward bias occurs independently of any economic value reduction. Thus, unconditional conservatism does not provide fresh insight into contracting, while on the other hand, it introduces noise into decisions based on accounting information and reduces contracting efficiency. Consistent with Ball and Shivakumar (2005), Qiang (2007) shows that a higher debt equity ratio induces a lower unconditional conservatism level. In addition, Bauwhede (2007) finds that the credit ratings of firms in industries with more unconditional conservatism are significantly less favorable. Zhang et al. (2008) also show that more (unconditional) conservative borrowers are less likely to violate debt covenants following a negative price shock and that the degree of (unconditional) conservatism is positively related to interest rates4.(3)Shareholder Governance vs. Stakeholder GovernanceWhile many empirical studies focusing on U.S. firms reveal the economic rationality of conditional conservatism in contracting, they suggest that unconditional conservatism has no benefits. However, cross-national studies provide evidence that contrasts with these previous findings.Cross-national studies include Ball et al. (2000) and Giner and Rees (2001). If conditional (unconditional) conservatism homogenously improves (reduces) contracting efficiency between countries, then countries should exhibit homogeneous demand for conservatism. However, Ball et al.4However, their result for unconditional conservatism is not statistically significant.(2000) compare the degrees of (conditional) conservatism among seven countries (Australia, C anada, the UK, the U.S., France, Germany, and Japan), and show that discrepancies exist in the degree of (conditional) conservatism among countries: accounting income in shareholder governance countries (Australia, Canada, the UK, and the U.S.) recognize losses in a more timely manner than stakeholder governance countries (France, Germany, and Japan). Furthermore, Giner and Rees (2001) compare the degrees of (unconditional) conservatism among three counties (France, Germany, and the UK) and find that the degree of (unconditional) conservatism in stakeholder governance countries (France and Germany) is higher than that in shareholder governance country (the UK).These studies suggest that the economic consequences of conservatism are likely to vary across countries―corporate governance types. Under shareholder governance, a firm’s ownership is widely dispersed, and the information asymmetry between managers and shareholder/creditors increases. While managers essentially have incentives to disclose good news, they are apt to hold back bad information to maximize their own welfare. Because managers try to hide bad news as information asymmetry increase, shareholder/creditors demand conditional conservatism by firms to counteract this tendency.In contrast, under stakeholder governance, a firm’s ownership includes founder families, the bank, and employees, and is often highly concentrated. These stakeholders are also actively involved in managing the company. Thus, they can reduce information asymmetry via informal communication with managers. This decreases the demand for conditional conservatism found in the stakeholder governance model. On the other hand, the stakeholder governance model generates different demand for firms from the shareholder governance model. Under stakeholder governance, because firm’s ownership is highly concentrated on sta keholders and they develop long-term relationships with the firm, they cannot easily transfer their ownership to somebody else. Therefore, shareholders are concerned with the firm’s long-term financial viability (Ding et al. 2008; Hiroda 2012).Ding et al. (2008) and Sanders et al. (1938) suggest that (unconditional) conservatism is possible to satisfy their demand. Accounting income is related to payments such as employee compensation,executive compensation, dividends, and tax. Because unconditional conservatism biases accounting income downward, it can reduce payments related to accounting income. Therefore, unconditional conservatism overcomes doubts over firms’long-term financial viability. Biddle et al. (2012) provide evidence supporting this opinion, finding that unconditional conservatism mitigates ex ante bankruptcy risk and reduces incidence of real bankruptcy by enhancing firms’ cash holding s.(4)Role of Conservatism in JapanSome previous studies suggest that the economic rationality of conservatism can vary across corporate governance types. Using a sample of Japanese firms, I examine if unconditional conservatism and conditional conservatism have economic rationality in Japan.Japan’s financial system is centered on banks, which develop long-term and close relationships with borrowers (Hiroda 2012). Hiroda (2012) examines the relationship between the main financing bank and a firm, showing that 97.8% of Japanese firms did not switch their main financing bank during the period of 1995–2000. He also reports that 94.3% of firms did not switch during 2000–2005, and 95.1% did not switch during 2005–2010. This traditional Japanese system is known as the main bank system and is categorized as a stakeholder governance model. Main banks cannot easily transfer funds from clients to others firms because they develop a long-term relationship with the clients. They demand long-term financial viability for firms via unconditional conservatism. Usui (2004) provides evidence consistent with this viewpoint. Using a sample of Japanese firms, he finds that a higher debt equity ratio induces a higher (unconditional) conservatism level.Furthermore, main banks can share the benefits from unconditional conservatism with their borrower firms. For instance, Nakamura (2008) focuses on Japanese firms and shows that a firm’s degree of unconditional conservatism is negatively related with interest rates. Although this finding is highly suggestive, scrupulous attention is required to interpret them because I am unable to identify when the interest rates listed in the financial statements are determined. Therefore, his study cannot directly analyze whether unconditional conservatism benefits firms. I focus on proceeds from long-term loans payable in order to examine the economic consequences of unconditionalconservatism because it is an easily available form of cash flow statement that allows identification of when firms borrow money from banks. From the above discussions, I develop the first hypothesis: H1: firms with a higher degree of unconditional conservatism borrow more money from banks.As stated above, recent studies suggest that conditional conservatism improves debt contracting and benefits firms via lower debt costs under the shareholder governance model (Bauwhede 2007; Wittenberg-Moerman 2008; Zhang 2008). On the other hand, there is a high possibility that it provides little benefit to firms under the stakeholder governance model such as Japan’s main bank system. Main banks can reduce information asymmetry via informal communication with managers because they are actively involved in firm management. In addition, conditional conservatism is not likely to contribute to a firm’s long-term financial viability in the following respects. First, losses due to conditional conservatism are unlikely to be deductible because such losses are based on unrealized decreases in market value rather than realized losses from transactions (Qiang 2007). Therefore, conditional conservatism cannot reduce payments related to tax. Second, some surveys show that managers do not reduce dividends due to transitory losses as a result of such conditional conservatism (Brav et al. 2005; Hanaeda and Serita 2009). These findings suggest that conditional conservatism does not contribute to a firm’s long-term financial viability. Biddle et al. (2012) also provides evidence that conditional conservatism cannot reduce real bankruptcy rates though it does reduces ex ante bankruptcy risk. From the above discussions, I develop the second hypothesis. In addition, I focus on proceeds from long-term loans payable to compare with the consequences of unconditional conservatism and identify the relationship between conditional conservatism and debt contracting:H2: Degree of conditional conservatism is not related to firm borrowings from banks.3.Research Design(1)Unconditional Conservatism MeasurementFollowing previous studies, I use the measurement developed by Beaver and Ryan (2000) as aproxy for unconditional conservatism. They estimate the following fixed effect model: Book_to_Market i,t= αt+ αi+ Σ2j = 0βjReturn i,t − j+ εi,t,,(1) where i indexes the firm, and t indexes the year. Book_to_Market i,t is the ratio of the book value of equity to market value of equity at the end of period t. Return i,t − j is the 12-month buy-and-hold return from the beginning of period t − j (j = 0–2). αt is the time effect while αi denotes the firm effect and captures the degree of unconditional conservatism.Because αi is the firm effect, its calculation requires a certain length of estimation period. My study uses an estimation period three years. Specifically, I estimate Eq. (1) using a sample from period t − 2 to t and obtain the unconditional conservatism measurement at the end of period t. Higher αi represents lower unconditional conservatism. I refer to αi multiplied by −1 as UCC i,t. Higher UCC i,t represents higher unconditional conservatism.(2)Conditional Conservatism MeasurementI use the measurement developed by Khan and Watts (2009) as a proxy for conditional conservatism. In contrast, many previous studies use the measurement developed by Basu (1997) as a proxy for conditional conservatism. Basu (1997) estimates the following pooling regression model:X i,t = β1 + β2D i,t + β3R i,t + β4D i,t * R i,t + εi,t,,(2) where X i,t is calculated as net income for period t divided by the market value of equity at the beginning of period t. R i,t denotes 12-month buy-and-hold returns beginning from nine months before the end of period t. D i,t denotes a dummy variable equal to 1 if R i,t < 0, and 0 otherwise. β3 captures the timeliness of gain recognition in earnings. β4 captures the incremental timeliness of loss recognition in earnings relative to the gain and degree of conditional conservatism.Although many previous studies estimate Eq. (2) to measure conditional conservatism, it is not sufficient to enable estimation of firm-year measurements. To estimate the timeliness of gain recognition in the earnings measurement and conditional conservatism measurement at the firm-year level, Khan and Watts (2009) specify that both these elements of timeliness are linear functions ofthree firm-specific characteristics (size, market to book, and leverage):G_SCORE i,t = β3 = γ1 + γ2Size i,t + γ3Market_to_Book i,t + γ4Leverage i,t,(3) C_SCORE i,t = β4 = λ1 + λ2Size i,t + λ3Market_to_Book i,t + λ4Leverage i,t,(4) where Size i,t is firm size and the natural log of market value of equity at the end of period t. Market_to_Book i,t is the ratio of the market value of equity to the book value of equity at the end of period t. Leverage i,t is the leverage and ratio of interest-bearing debt to the market value of equity at the end of period t.C_SCORE i,t is the firm-year measurement of conditional conservatism, and G_SCORE i,t is the firm-year measurement of the timeliness of gain recognition in earnings. Coefficients γ and λare constant across firms but vary over time because they are estimated each year. Thus, C_SCORE i,t and G_SCORE i,t vary across firms through a cross-sectional variation in firm-year characteristics and over time through an intertemporal variation in γand λas well as firm-year characteristics. However, Eqs. (3) and (4) are not regression models. To estimate γ and λ, I substitute Eqs. (3) and (4) into Eq. (2) to obtain Eq. (5) , which is then estimated annually:X i,t= β1+ β2D i,t+ β3R i,t(γ1+ γ2Size i,t+ γ3Market_to_Book i,t+ γ4Leverage i,t) + β4D i,t * R i,t(λ1 + λ2Size i,t+ λ3Market_to_Book i,t + λ4Leverage i,t) + (μ1Size i,t+ μ2Market_to_Book i,t+ μ3Leverage i,t + μ4D i,t * Size i,t + μ5D i,t * Market_to_Book i,t + μ6D i,t * Leverage i,t) + εi,t,, (5) Because Eq. (5) includes interaction terms between returns and firm-specific characteristics, firm-specific characteristics must be controlled for separately. Therefore, I include the terms in the last parenthesis of Eq. (5). I substitute γ and λ resulting from the estimation of Eq. (5) and firm-specific characteristics into Eq. (4) each year to obtain the firm-year measurement of conditional conservatism (C_SCORE i,t). I refer to C_SCORE i,t as CC i,t. A higher value of CC i,t represents a firm having a higher conditional conservatism.(3)Standardization of Conservatism MeasurementsI estimate the firm-year measurements of unconditional conservatism and conditionalconservatism as stated above. However, some previous studies point out that these measurements include noise (DeFond et al. 2012; Louis et al. 2012; Zhang 2008). Following these studies, I rank these measurements in ascending order and divide the obtained values by the maximum value of the ranked measurements to reduce this noise. I refer to the unconditional (constitutional) conservatism measurement obtained from this procedure as STUCC i,t (STCC i,t). STUCC i,t (STCC i,t) takes a value between 0 and 1, and the higher value represents higher unconditional (conditional) conservatism. Table1 presents an example of this procedure.(4)Empirical ModelI analyze if unconditional conservatism and conditional conservatism are useful for firms trying to get loans from banks. It is very important for this analysis that the condition where firms intend to collect money with debt is identified. Unless firms achieve the intended aim by conservative accounting, it is not necessarily appropriate to suggest that an accounting system, such as conservatism, provides benefits to firms.Theories explaining corporate financing activity include tradeoff theory and pecking order theory. Some previous studies show that the pecking order model explains considerably more about corporate financing activity than the tradeoff model (Sakai 2009; Shyam-Sunder and Myers 1999). Following these findings, I identify the condition where firms intend to collect money with debt on the basis of pecking order theory. Pecking order theory is modeled as follows:DEBT i,t= α1+ β1GAP i,t+ εi,t= α1+ β1{(DIV i,t + X i,t + ⊿W i,t− C i,t) ÷ A i,t − 1} + εi,t,(6) where DEBT i,t is proceeds from long-term debt and calculated as proceeds from bond issue plus proceeds from long-term loans payable for period t divided by total assets at the end of period t − 15. GAP i,t is the funding gap and is calculated as aggregate investment (DIV i,t + X i,t + ⊿W i,t) minus 5Sakai (2009), and Shyam-Sunder and Myers (1999) incorporate only proceeds from long-term debt into the model as a dependent variable because only long-term financing activity becomes a problem in the context of traditional capital structure theory. However, short-term debt outstanding is adjusted by ⊿W i,t on the right side of Eq. (6).。

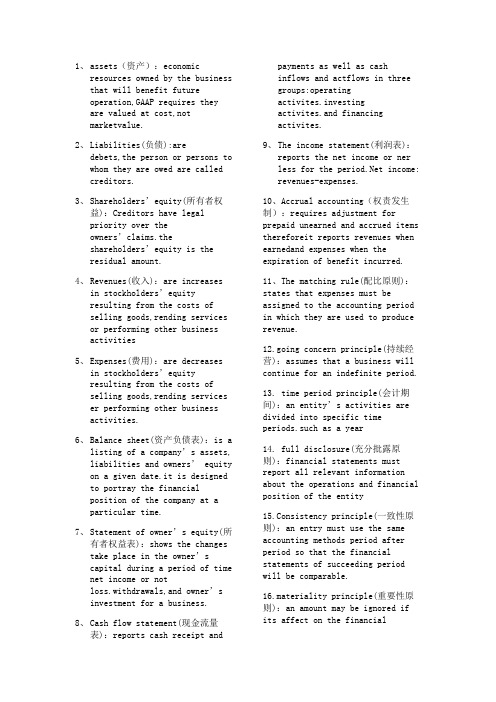

会计英语名词解释

1、assets(资产):economicresources owned by the business that will benefit futureoperation,GAAP requires theyare valued at cost,notmarketvalue.2、Liabilities(负债):aredebets,the person or persons to whom they are owed are calledcreditors.3、Shareholders’equity(所有者权益):Creditors have legalpriority over theowners’claims.theshareholders’equity is theresidual amount.4、Revenues(收入):are increasesin stockholders’equityresulting from the costs ofselling goods,rending servicesor performing other businessactivities5、Expenses(费用):are decreasesin stockholders’equityresulting from the costs ofselling goods,rending serviceser performing other businessactivities.6、Balance sheet(资产负债表):is alisting of a company’s assets, liabilities and owners’ equity on a given date.it is designedto portray the financialposition of the company at aparticular time.7、Statement of owner’s equity(所有者权益表):shows the changestake place in the owner’scapital during a period of time net income or notloss.withdrawals,and owner’sinvestment for a business.8、Cash flow statement(现金流量表):reports cash receipt andpayments as well as cashinflows and actflows in threegroups:operatingactivites.investingactivites.and financingactivites.9、The income statement(利润表):reports the net income or nerless for the income: revenues-expenses.10、Accrual accounting(权责发生制):requires adjustment for prepaid unearned and accrued items thereforeit reports revenues when earnedand expenses when the expiration of benefit incurred.11、The matching rule(配比原则):states that expenses must be assigned to the accounting period in which they are used to produce revenue.12.going concern principle(持续经营):assumes that a business will continue for an indefinite period.13. time period principle(会计期间):an entity’s activities are divided into specific time periods.such as a year14. full disclosure(充分批露原则):financial statements must report all relevant information about the operations and financial position of the entity15.Consistency principle(一致性原则):an entry must use the same accounting methods period after period so that the financial statements of succeeding period will be comparable.16.materiality principle(重要性原则):an amount may be ignored if its affect on the financialstatements is not important to its users.17.conservatism principle(稳健性原则):the least optimistic estimate should be selected when two estimates of amounts to be received or paid are aboutequality likely;it is better to understate than over values.18.busniness entity principle(会计主体):each entity must keep accounting records and people reports that are distinct from those of the owner and any other entity.19.。

关于会计的英文文献原文(带中文翻译)

The Optimization Method of Financial Statements Based on Accounting Management TheoryABSTRACTThis paper develops an approach to enhance the reliability and usefulness of financial statements. International Financial Reporting Standards (IFRS) was fundamentally flawed by fair value accounting and asset-impairment accounting. According to legal theory and accounting theory, accounting data must have legal evidence as its source document. The conventional “mixed attribute” accounting system should be re placed by a “segregated” system with historical cost and fair value being kept strictly apart in financial statements. The proposed optimizing method will significantly enhance the reliability and usefulness of financial statements.I.. INTRODUCTIONBased on international-accounting-convergence approach, the Ministry of Finance issued the Enterprise Accounting Standards in 2006 taking the International Financial Reporting Standards (hereinafter referred to as “the International Standards”) for reference. The Enterprise Accounting Standards carries out fair value accounting successfully, and spreads the sense that accounting should reflect market value objectively. The objective of accounting reformation following-up is to establish the accounting theory and methodology which not only use international advanced theory for reference, but also accord with the needs of China's socialist market economy construction. On the basis of a thorough evaluation of the achievements and limitations of International Standards, this paper puts forward a stand that to deepen accounting reformation and enhance the stability of accounting regulations.II. OPTIMIZA TION OF FINANCIAL STATEMENTS SYSTEM: PARALLELING LISTING OF LEGAL FACTS AND FINANCIAL EXPECTA TIONAs an important management activity, accounting should make use of information systems based on classified statistics, and serve for both micro-economic management and macro-economic regulation at the same time. Optimization of financial statements system should try to take all aspects of the demands of the financial statements in both macro and micro level into account.Why do companies need to prepare financial statements? Whose demands should be considered while preparing financial statements? Those questions are basic issues we should consider on the optimization of financial statements. From the perspective of "public interests", reliability and legal evidence are required as qualitative characters, which is the origin of the traditional "historical cost accounting". From the perspective of "private interest", security investors and financial regulatory authoritieshope that financial statements reflect changes of market prices timely recording "objective" market conditions. This is the origin of "fair value accounting". Whether one set of financial statements can be compatible with these two different views and balance the public interest and private interest? To solve this problem, we design a new balance sheet and an income statement.From 1992 to 2006, a lot of new ideas and new perspectives are introduced into China's accounting practices from international accounting standards in a gradual manner during the accounting reform in China. These ideas and perspectives enriched the understanding of the financial statements in China. These achievements deserve our full assessment and should be fully affirmed. However, academia and standard-setters are also aware that International Standards are still in the process of developing .The purpose of proposing new formats of financial statements in this paper is to push forward the accounting reform into a deeper level on the basis of international convergence.III. THE PRACTICABILITY OF IMPROVING THE FINANCIAL STATEMENTS SYSTEMWhether the financial statements are able to maintain their stability? It is necessary to mobilize the initiatives of both supply-side and demand-side at the same time. We should consider whether financial statements could meet the demands of the macro-economic regulation and business administration, and whether they are popular with millions of accountants.Accountants are responsible for preparing financial statements and auditors are responsible for auditing. They will benefit from the implementation of the new financial statements.Firstly, for the accountants, under the isolated design of historical cost accounting and fair value accounting, their daily accounting practice is greatly simplified. Accounting process will not need assets impairment and fair value any longer. Accounting books will not record impairment and appreciation of assets any longer, for the historical cost accounting is comprehensively implemented. Fair value information will be recorded in accordance with assessment only at the balance sheet date and only in the annual financial statements. Historical cost accounting is more likely to be recognized by the tax authorities, which saves heavy workload of the tax adjustment. Accountants will not need to calculate the deferred income tax expense any longer, and the profit-after-tax in the solid line table is acknowledged by the Company Law, which solves the problem of determining the profit available for distribution.Accountants do not need to record the fair value information needed by security investors in the accounting books; instead, they only need to list the fair value information at the balance sheet date. In addition, because the data in the solid line table has legal credibility, so the legal risks of accountants can be well controlled. Secondly, the arbitrariness of the accounting process will be reduced, and the auditors’ review process will be greatly simplified. The independent auditors will not have to bear the considerable legal risk for the dotted-line table they audit, because the risk of fair value information has been prompted as "not supported by legalevidences". Accountants and auditors can quickly adapt to this financial statements system, without the need of training. In this way, they can save a lot of time to help companies to improve management efficiency. Surveys show that the above design of financial statements is popular with accountants and auditors. Since the workloads of accounting and auditing have been substantially reduced, therefore, the total expenses for auditing and evaluation will not exceed current level as well.In short, from the perspectives of both supply-side and demand-side, the improved financial statements are expected to enhance the usefulness of financial statements, without increase the burden of the supply-side.IV. CONCLUSIONS AND POLICY RECOMMENDATIONSThe current rule of mixed presentation of fair value data and historical cost data could be improved. The core concept of fair value is to make financial statements reflect the fair value of assets and liabilities, so that we can subtract the fair value of liabilities from assets to obtain the net fair value.However, the current International Standards do not implement this concept, but try to partly transform the historical cost accounting, which leads to mixed using of impairment accounting and fair value accounting. China's accounting academic research has followed up step by step since 1980s, and now has already introduced a mixed-attributes model into corporate financial statements.By distinguishing legal facts from financial expectations, we can balance public interests and private interests and can redesign the financial statements system with enhancing management efficiency and implementing higher-level laws as main objective. By presenting fair value and historical cost in one set of financial statements at the same time, the statements will not only meet the needs of keeping books according to domestic laws, but also meet the demand from financial regulatory authorities and security investorsWe hope that practitioners and theorists offer advices and suggestions on the problem of improving the financial statements to build a financial statements system which not only meets the domestic needs, but also converges with the International Standards.基于会计管理理论的财务报表的优化方法摘要本文提供了一个方法,以提高财务报表的可靠性和实用性。

国际会计准则中英文对照外文翻译文献

中英文对照外文翻译文献(文档含英文原文和中文翻译)译文:译文(一)世界贸易的飞速发展和国际资本的快速流动将世界经济带入了全球化时代。

在这个时代, 任何一个国家要脱离世界贸易市场和资本市场谋求自身发展是非常困难的。