Accountability and fiscal equalization

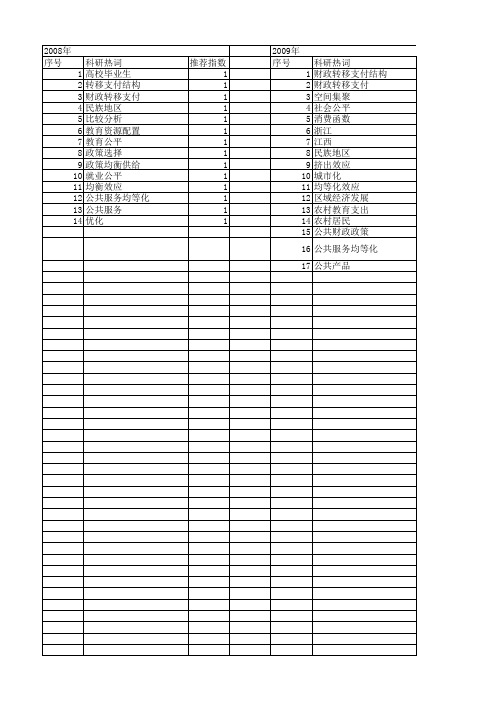

【国家社会科学基金】_均等化效应_基金支持热词逐年推荐_【万方软件创新助手】_20140805

推荐指数 5 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

2014年 序号 1 2 3 4 5 6 7 8 9 10 11

2014年 科研热词 转移支付 非税收入 门槛效应 资产动态 财政自给 财力差异 经济增长 税收收入 消费平滑 气候变化 中国农村贫困陷阱 推荐指数 2 1 1 1 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

科研热词 推荐指数 转移支付 1 财政支出结构 1 财政均等化 1 粘蝇纸效应 1 社会调查 1 社会公正 1 横向财政失衡 1 核密度估计 1 政府间转移支付制度 1 收入分配 1 均等化效应测度 1 可替换效应 1 公共服务均等化 1 中央转移支付体系 1 transfer payments 1 structure of fiscal expenditure 1 fungibility effect 1 flypaper effect 1 fiscal equalization 1

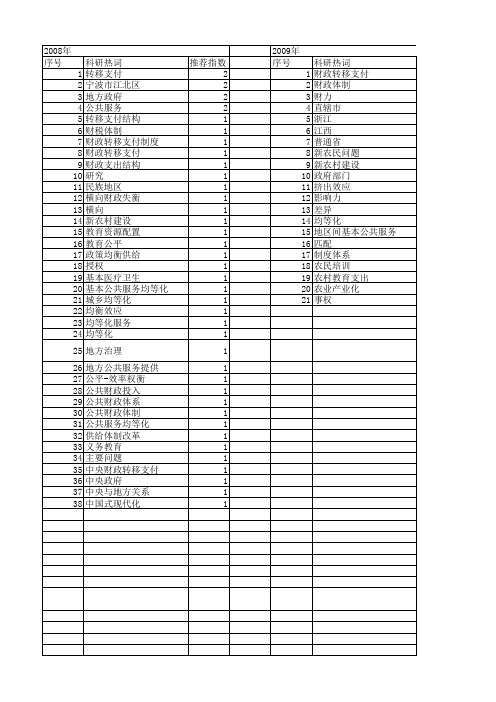

2013年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

科研热词 转移支付 税收返还 均等化 高管薪酬 集聚 金融发展 财税改革 财政转移支付 财政分权 财政体制 评估 衔接 行业异质性 薪酬差距 科技进步 社会保障 理论依据 新型城镇化 教育服务均等化 政策协同效应 政府行为 技术溢出 扶贫开发 居民消费 外商直接投资 基本公共服务均等化 城市化 城市公共品供给 城乡人口迁移 地方政府债务 区域差异 区域发展 区域创新能力 农村低保 公共服务均等化 全球生产网络 企业绩效 企业特征 gmm模型 fdi

英文速读资料金融时报

经济预测,欲望永不眠辞旧迎新的时候,人们为何总期望经济学家做预测呢?预测成绩怎样?这是FT"卧底经济学家"蒂姆·哈福德有趣的解答。

An insatiable desire to peer into the futureThe wonderful thing about forecasts is that they all sound very profound--------------------------It’s that time of year again. Time for you to make your predictions for 2013.You’re kidding, right? You’re asking an economist for predictions?Just my little joke. But surely you’re not a propereconomist if you can’t make a few predictions. Isn’t that the whole point of the economic profession – to make dozens of mutually contradictory forecasts with impunity?Well, the impunity is a topic worth discussing. But the economics profession could do with a few more disagreements, I think. In 1995, FT columnist John Kay examined the record of British economic forecasters from 1987 to 1994. He discovered that they tended to all say much the same thing. The only dissenter was reality: economic growth often fell outside the range of all 34 forecasts.So economists are terrible forecasters. What else is new?It isn’t just economists who are terrible forecasters. Take the quantitative analysts responsible for Goldman Sachs’s notorious “25 standard deviation” episode – presumably physicists or mathematicians.25 standard deviation?At the beginning of the financial crisis, the chief financial officer of Goldman Sachs explained that the firm was seeing “25 standard deviation moves, several days in a row” – a statement that, translated into English, means “according to our models, what we’re seeing is very unlucky”.How unlucky?Oh, the sort of bad luck you see once every 28, 900, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000,000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000 years, given certain assumptions about what Goldman might have meant. For reference the universe is about 14,000,000,000 years old. The alternative to the “very unlucky” hypothesis, of course, is that the quantitative models didn’t produce very good forecasts.Well, that’s a forecast so bad that I can’t believe an economist wasn’t involved somewhere.You may be right. But I can give you another example: the 300-odd experts recruited by Philip Tetlock, the psychologist, for his epic study of forecasting in political science. Prof Tetlo ck’s conclusions are wide-ranging and painstaking, but if I can be forgiven an excessively brief summary, he finds that all sorts of people with plausible claims to expertise –diplomats, political advisers, journalists and academics –produce lame forecasts of political and economic events.Nate Silver seems to be able to forecast just fine.Well, yes, notwithstanding the politically motivated “Nate Silver can’t add up” school of criticism, Mr Silver, and other statisticians such as Drew Linzer and Sam Wang, successfully forecast the outcome of the US elections in some detail. Contrasted against a background of bloviation, it was impressive. But if psephology is Exhibit A in the Museum of Successful Social Science Forecasts, let’s reflect on how modest our ambitions must have become: US elections are frequently repeated, with behaviour that shows considerable historical persistence, and an astonishing amount of detailed quantitative data are available. The elections take place at a fixed date, according to well-understood rules, and with a narrowly defined space of possible outcomes. It’s easy to see that forecasting a win for Barack Obama, while better than forecasting a win for Mitt Romney, is not quite as hard as successfully predicting if and when Greece will leave the eurozone.You’re pretty quick with the excuses.No excuses. We just can’t see into the future. I don’t thinkthat’s any surprise, nor an embarrassment. The question is why there’s such a hunger for social science predictions, when the practice is so transparently pointless.It’s a test of expertise.If so, then monkeys are as expert as professors of political economy. I wouldn’t want to be quite so cynical. I think forecasting in a complex world is a poor test of expertise because luck is the overwhelming success factor.So why do we love predictions?No idea. Here’s one guess: saying “the UK economy will recover strongly in 2012” or “President Assad will be out of office by June” compresses a vast amount of expertise and analysis into a few words.But the words are probably meaningless.Yes. But it’s Christmas. Actually studying the situation in detail is far too much like hard work真是费神的事. Thewonderful thing about a forecast is that both the forecaster and his audience feel that something profound has been expressed. And nobody will remember the forecast anyway.It’s time of …….time for; but surely you…..if you …….; Isn’t that the whole point of …….Well, but……..I think.So…… what else is new?It isn’t just , presumably……;But if I can be forgivenWell yes,notwithstandingAs hard asIf and whenIf so….共和党旗手埃里克·坎托年轻的国会共和党领袖坎托是个野心勃勃和勤奋异常的人,FT华盛顿分社社长马利德(Richard McGregor)认为他是共和党的新旗手。

Accountingprinciples会计原理(英文)

Accountingprinciples会计原理(英文)Accounting Principles Used to Prepare theFinancial StatementsTable of Content1.Introduction (1)2. Analysis of eight accounting principles (1)2.1 Time Period Assumption (1)2.2 Principle of Historical Cost (2)2.3 Full Disclosure Principle (2)2.4 Matching principle (3)2.5 Going Concern Principle (4)2.6 Revenue Recognition Principle (4)2.7 Materiality (5)2.8 Conservatism (5)3.Conclusion (6)References (7)1.IntroductionThe goal of financial statements is to provide users with accounting information relevant to the enterprise financial position, operation outcome, cash flow etc., reflect managers’ performance of fiduciary responsibilities,so as to help financial statement users make proper economic decisions. In this paper, the author will explain eight different accounting principles used to prepare the financial statements with suitable examples or illustration.2. Analysis of eight accounting principles2.1 Time Period AssumptionThe concept of Time Period refers to that accounting information should be collected and handled following timeperiods (Zeff, 2012). Time Period Assumption is a necessary supplement of Going Concern Assumption. This principle lays a foundation for other accounting principles such as Cost Principle and Matching Principle. Assuming an accounting entity should endlessly operate a business, logically the provision of accounting information needs to have regulated time period, which is the premise for accounting to perform effect (Schipper, 2003).The principle of Time Period Assumption manually divides the constant production and operation activities of an enterprise into various time periods, calculate economic activities and report operation outcome by stages (Zeff, 2012). It is because stakeholders need to timely know the financial condition and operation outcome of the enterprise, thus the enterprise should regularly provide accounting information as the basis of decision-making.Clarifying the basic premise of accounting time period has great importance to accounting, Due to the time period, the differences between this period and other period exist, thus generates the differences between accrual basis and cash basis, different types of accounting entities have the benchmark of keeping accounts, and further the accounting methods such as accounts receivable, accounts payable, accrual, deferral, prepaid and so on.In China’s accounting practice, an accounting year refers t o January 1st to December 31st (Zeff, 2012). For example, Financial Statements of 2012 reflects the financialinformation from January 1st 2012 to December 31st 2012. Financial statements which less than one year are called mid-term statements. Mid-term statements are mainly embodied assemi-annual statements and quarterly statements.2.2 Principle of Historical CostPrinciple of Historical Cost means that the recording of accounting elements should use the acquisition cost when economic businesses took place as the standard to measure (Weygandt et al, 2010). The main content of this principle is that all kinds of assets gained by an enterprise should use the primitive cost (actual cost) occurred when purchasing or building to record, and make it as the basis of share and transfer cost (White, 2006). When price of commodities changes, enterprises cannot adjust its accounting value except for state policy changes. Valuation according to actual cost can avoid randomness, make accounting information reliable and easy to know and compare.Principle of Historical Cost is mainly used to determine the cost of assets on the account book. For example, an enterprise spent $5 million buying an office building on January 1st 2010, thus when recording,the actual cost of the building is $5 million. Suppose that till January 1st 2013, the market price of this office building increased to $8 million, at that moment, there is no need to adjust the original recorded value, the original actual cost or the historical cost should be still on the account book. It should be noticed that, it does not mean that recorded value cannot be adjusted. For instance, this enterprise will sell the building, so assets appraisal will be conducted. This is a special case (White, 2006).2.3 Full Disclosure PrincipleFull Disclosure Principle refers to that in order to achieve the just reflection of an enterprise’s economic events and the influence, all necessary information should be fully provided and should be easy for users to understand (Weygandt et al, 2010).The goal of full disclosure is to meet users’ demand fo r decision-making. Full Disclosure Principle has several aspects of meaning.Firstly, comprehensiveness of disclosure. Comprehensiveness means any information which has influence on use rs’ decision-making or reflects economic events should bedisclosed. Horizontally, any information which reflects production and operation condition should be disclosed. Vertically, not only the surface but also the in-depth information should be recorded. Accounting information is mainly provided by financial statements, this kind of regular and unified format has some limitations. The Notions as the supplementary information become more important with the guidance of Full Disclosure Principle (Schipper, 2003). Secondly, the properness of disclosure. Over-disclosure will make users confused. Therefore major programmes should be disclosed in-detail, while less-important programmes can be disclosed less, so as to let users effectively use the information. Thirdly, the effectiveness of disclosure. Understandable is the connection between decision-makers and the effectiveness of decisions.Besides, information should meet the common demands of different users. Lastly, the promptness of disclosure requires obligators to disclose information in specific ways according to laws and regulations.2.4 Matching principleMatching Principle means the income of a certain time period or a certain accounting object should match the corresponding cost, so as to correctly calculate the net profit or loss of the accounting entity during the time period (Weygandt et al, 2010). Matching Principle as a requirement of accountingelements confirmation, is used to determine profits. Economic activities accounting entity will bring some certain income and also spend corresponding costs. Income and cost are the unity of the opposites, profits is the result. Matching Principle is based on Benefit Principle. Direct costs with causal relations and indirect costs without causal relations must be distinguished according to the Matching Principle. Direct costs should be directly matched with income to decide the loss or profit, while indirect costs firstly make apportionment among all products and income with proper standard, and than determine the loss or profit through matching revenues and expenses (Weygandt et al, 2010).Therefore, the Matching Principle has three aspects of meaning. Firstly, income of a product must match the cost of the product. Secondly, income of a time period must match the cost of the time period. Thirdly, income of a department must match thecost of the department.2.5 Going Concern PrincipleGenerally, going concern refers to one enterprise can maintain constant business operation in the foreseeable future (usually 12 months in a year), without intention or risk of bankruptcy (Efendi et al, 2007). In this case, the asset value of the enterprise can be remained, it also has the ability to pay its debt, income potential of going concern can improve the overall value of the enterprise. If an enterprise suffers long-term losses or investment error, insolvency may occur. In severe cases, enterprises cannot go concern, thus assets cannot be recorded according to fair value, but should be investment depreciation according to market price(Zeff, 2012).For instance, an enterprise uses $150000 to buy anequipment and predicts that the equipment can be used for five years and brings the enterprise $40000 every year. Based on Going Concern Principle, the enterprise will not go bankrupt in 5 years. Therefore, the $150000 investment can be regained in 5 years with $30000 cost annually, thus the equipment can gain $10000 per year. However without such assumption, accounting cannot be conducted normally. If the enterprise goes broke after 4 years, the equipment cost must be regained in four years, thus every year should bear $37500, there will be only $2500 profit.Without the assumption, accounting will have no certain time range, thus cannot complete. Similarly, production and operation activities cannot be organized neither (Ryan et al, 2002). 2.6 Revenue Recognition PrincipleRevenue recognition means the time when revenue is recorded. Revenue recognition should solve two problems, one is timing, the other is measuring (Ryan et al, 2002). Revenue recognition mainly includes the recognition of product sales revenue and service revenue. Besides, it also includes the revenue that gain from offering other to use the assets of the enterprise, such as interest, use fee and dividend. This principle must meet four basic premises: definability, accountability, relativity and reliability (Weygandt et al, 2010). Meanwhile, it must conform to some common standards.In No.5 financial accounting concept of morality released by Financial Accounting Standards Board (FASB), according to Revenue Principle, revenue is usuallyrecognized when revenue is realized or realizable, or is earned (Schipper, 2003). Therefore, revenue of selling products is generally recognized on the sales date. Service revenue is confirmed when completing the duty of offering services.Revenue gained from allowing others to use the corporate is gradually recognized with the time passes or the procedure of asset use. While the International Accounting Standards Board (IASB) emphasizes on defining revenue timing from the basic standard that whether the important risks and rewards have been transferred to the buyers (Schipper, 2003).2.7 MaterialityThe Materiality principle has several features. Firstly, the core is one cannot omit or misrepresent important information, the standard of judging importance is to see whether it will influence the decisions of users. Secondly, the concept is proposed from the perspective of information users, main users include investors, shareholders etc. Thirdly, judgment of materiality cannot be separated from the enterprise environment, different enterprises or the same enterprise in different period, the standards may differ (Weygandt et al, 2010). Lastly, judgment of importance cannot neglect its own nature. Some information does not reach the importance, but the nature is serious, thus it has conformed to the requirement of materiality, so it should be disclosed.In terms of the application of this principle, firstly, it can be used in the recognition of post balance sheet events. Matters need to be adjusted or explained means information which reaches to the materiality standard and can influence decision-making should be handled specifically. Secondly, it can be used in making mid-term financial statements. The aim is to improve the promptness of information, therefore it does not require the enterprises to provide complete information like annual financial statements (Weygandt et al, 2010). In addition, the principle can also used in recognition of segmental reporting, trade disclosureof related parties and disclosure of notes to financial statements.2.8 ConservatismThe principle of Conservatism refers to that when dealing with the uncertaineconomic businesses of the enterprises, people should hold the cautious attitude. That is to say, all predictable loss and cost should be recorded and confirmed, while income without 100% certainty cannot be recognized and recorded. In market economy conditions, enterprise inevitably will face risks,implementing the Conservatism principle can help enterprises resolute or prevent risks before the risks come. It is beneficial for enterprises to make correct operation decisions, protect interest of owners and stakeholders, improve enterprises’ competence in market.This principle has both advantages and disadvantages. It has the information features demanded by stakeholders, which can protect their interest so as to avoid unnecessary loss. It is also an effective management method in principle making institutions and a standard when accounting staff deal with the uncertain items. However, it may reduce the quality of accounting information because it has much judgment and estimation. It also brings some convenience for information counterfeiters and managers’ short-term behaviors.3.ConclusionUnder modern corporate system, ownership and managing right of enterprises are separate. Only through accounting information can users precisely judge whether the investment is used scientifically and appropriately. In order to prepare good financial statements, various accounting principles should be adopted, therefore, it is important for accounting professionalsto have a comprehensive understanding of various accounting principles and their applications.References:Efendi, J., Srivastava, A., & Swanson, E. P. (2007). Why do corporate managers misstate financial statements? The role of option compensation and other factors. Journal of Financial Economics, 85(3), 667-708.Ryan, B., Scapens, R. W., & Theobald, M. (2002). Research method and methodology in finance and accounting.Schipper, K. (2003). Principles-based accounting standards. Accounting Horizons, 17(1), 61-72.Weygandt, J. J., Kimmel, P. D., KIESO, D., & Elias, R. Z. (2010). Accounting principles. Issues in Accounting Education, 25(1), 179-180.White, G. (2006). THE ANALYSIS AND USE OF FINANCIAL STATEMENTS, (With CD). Wiley. Com. 33-55.Zeff, S. (2012). Forging accounting principles in five countries: A history and an analysis of trends. 21-46.。

[翻译米整理]银行业英语词汇

![[翻译米整理]银行业英语词汇](https://img.taocdn.com/s3/m/c0ceaad9d5bbfd0a79567327.png)

loan-deposit ratio存放款比率self-owned capital ratio自有资本比率output-capital ratio产出与资本的比率ratio of profit to capital收益同资本的比率turnover of account receivable应收帐款周转率ratio of doubtful loans to total loans坏帐比率fixed assets ratio固定资产比率fixed assets turnover ratio固定资产周转率current ratio流动比率turnover ratio of working capital流动资本周转率liquidity of bank银行资产流动性payment reserve支付准备internal reserves内部准备金graduated reserve requirement分级法定准备金ratio of cash reserves to deposits存款支付准备率initial reserve初期准备金offset reserve坏帐准备金allowance for doubtful debt备抵呆帐款项reserve requirements法定存款准备金reserve ratio法定存款准备金比率required reserve ratio法定准备率minimum reserve ratio法定最低准备比率additional reserve追加准备金guaranteed fund保证准备金reserve margin准备金比率unbalance finance赤字财政red balance赤字差额repressed inflation抑制性通货膨胀shortage of financial resources财源短缺galloping inflation恶性通货膨胀monetary and financial crisis货币金融危机inflationary trends通货膨胀趋势monetary stringency银根奇紧slack of finance银根松缓stagflation滞胀demand pull inflation需求拉动通货膨胀demand shift inflation需求变动型通货膨胀latent inflation潜在的通货膨胀inflationary spiral螺旋式上升的通货膨胀neutrality of the central bank中央银行的中立性counter-inflation policy反通货膨胀对策open market policy公开市场政策deficit-covering finance赤字财政fiscal and monetary policy财政金融政策harmony of fiscal and monetary policies财政政策和金融政策的协调monetary device金融调节手段monetary action金融措施measures for monetary ease金融缓和措施easy credit放松信贷monetary and credit control货币信用管理deficit covering弥补赤字restrictive lending policy贷款紧缩政策over-loan position贷款超额credit control instrument信用调节手段restrictive monetary policy紧缩通货膨胀credit extending policy融资方针ultra-cheap money policy超低息政策financial transaction金融业务monetary market金融市场financial unrest金融动荡financial crisis金融危机financial system金融体系financial world金融界policy of discount window窗口指导政策open market operation公开市场业务accrued bond interest应计债券利息accrued dividend应计股利active securities热头股票,活跃的证券baby bond小额债券bear operation卖空行为black market黑市black money黑钱bond fund债券基金call for funds控股、集资call market活期存款市场capital market信贷市场、资本市场capital resources资本来源capital surplus资本盈余capital transfer资本转移capital turnover rate资本周转率cash audit现金审核cash basis现金制cash basis accounting现金收付会计制cash budget现金预算cash flow资金流动cash holdings库存现金cash payment现金支付cash position头寸cash resources(reserves)现金准备common fund共同基金common trust fund共同信托基金current fund流动基金deposit turnover存款周转率derived deposit派生存款designated currency指定货币discount market贴现市场discounted cash flow净现金量due from other funds应收其他基金款due to other funds应付其他基金款equalization fund(外汇)平衡基金farm subsidies农产品补贴fund资金、基金fund account基金帐户fund allocation基金分配fund appropriation基金拨款fund balance基金结存款fund for relief救济基金fund for special use专用基金fund in trust信托基金fund liability基金负债fund obligation基金负担fund raising基金筹措funds statement资金表general fund普通基金gross cash flow现金总流量hedge fund套利基金hoarded money储存的货币legal tender法定货币monetary aggregates货币流通额monetary area货币区monetary assets货币性资产monetary base货币基础monetary circulation货币流通monetary ease银根松动monetary stringency银根紧monetary unit货币单位money collector收款人money credit货币信用money down付现款money equivalent货币等价money-flow analysis货币流量分析near money准货币neutral money中介货币provident fund准备基金public audit公开审计public money公款short-term funds短期资金sinking fund偿债基金soft currency软币subsidy account补助金帐户transfer to reserve account转到准备金帐户transferable money可转帐货币trust bank信托银行trust fund信托基金withdrawal from circulation(货币)回笼withdrawal of bank notes钞票回笼withdrawal of funds资金回收banker's bank中央银行banks with business dealing with the central bank中央银行的往来银行foreign banks外国银行local bank地方银行overseas branches国外分行foreign correspondent国外代理银行nationalized bank国有化银行national bank国家银行bank of the government政府的银行city bank城市银行credit union信用合作社operating bank营业银行consortium bank银团银行ordinary bank普通银行our bank开户银行establishing bank开证银行intermediary bank中间银行certifying bank付款保证银行paying bank付款银行appointed bank外汇指定银行correspondent代理行main bank主要银行remitting bank汇出银行remittance bank汇款银行negotiating bank议付银行issue bank发行银行bank of deposit存款银行rediscount bank再贴现银行agent for collection托收代理银行collecting bank托收银行mortgage bank抵押银行selling bank卖方银行requesting bank委托开证银行transmitting bank转证银行trustee bank受托银行domestic correspondent国内通汇银行loan bank放款银行accepting bank承兑银行confirming bank保兑银行discounting bank贴现银行creditor bank债权银行debtor bank借方银行advising bank通知银行acceptance bank票据承兑行clearing bank清算银行presenting bank提示银行affiliated bank联行long-term credit bank长期信用银行specialized foreign exchange bank外汇专业银行member bank会员银行fringe bank边缘银行export and import bank进出口银行managing bank of a syndicate财团的经理银行non-member bank非会员银行credit bank信贷银行chartered bank特许银行special bank特殊银行side-work bank兼业银行overseas bank海外银行popularity bank庶民银行banker's association银行协会infrastructure bank基本建设投资银行reserving bank储备银行savings bank储蓄银行multinational bank跨国银行world bank世界银行Asian Development Fund(ADB)亚洲开发银行Euro-bank欧洲银行International Investment Bank(IIB)国际投资银行interest subsidy利息补贴interest restriction利息限制legal interest法定利息public deposit政府存款derivative deposit派生存款special deposit特种存款reserve deposit准备存款bank deposit银行存款reserve account准备金帐户Bank of Communications交通银行Development Bank开发银行the Construction Bank of China中国建设银行the People's Bank of China中国人民银行Industrial and Commercial Bank of China中国工商银行Agricultural Bank of China中国农业银行China Investment Bank中国投资银行Bank of China中国银行the International Trust and Investment Corporation of China(ITICC)中国国际信托投资公司advice of drawing提款通知书draw提款drawee bank付款银行drawing account提款帐户fixed savings withdrawal定期储蓄提款run on a bank银行挤兑outward remittance汇出汇款postal remittance邮政汇款remittance by draft汇票汇款remittance charges汇费telegraphic transfer(T/T)电汇collection of trade charges托收货款collection on clean bill光票托收collection on documents跟单托收collecting bank托收银行letter transfer信汇deposit rate存款利率external account对外帐户fixed deposit(=time deposit)定期存款fixed deposit by installment零存整取imprest bank account定额银行存款专户large deposit大额存款nominal deposit名义存款non-resident account非居民存款account charges账户费用"account current(A/C,a/c)"往来帐户amount in figures小写金额amount in words大写金额application form for a banking account银行开户申请书bank balance存款余额Certificate of Deposits(CDs)大额定期存款单certificate of balance存款凭单checking account支票帐户。

【国家社会科学基金】_省级财政转移支付_基金支持热词逐年推荐_【万方软件创新助手】_20140809

2012年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

科研热词 推荐指数 转移支付 7 财政分权 7 政府间关系 5 财政支出结构 1 财政均等化 1 粘蝇纸效应 1 省直管县 1 省 1 激励效应 1 横向财政失衡 1 政府间转移支付制度 1 政府间财政转移支付 1 政府规模 1 城市扩张 1 均等化效应测度 1 地方税收收入体系 1 土地出让 1 可替换效应 1 “利维坦”假说 1 transfer payments 1 structure of fiscal expenditure 1 fungibility effect 1 flypaper effect 1 fiscal eq科研热词 1 财政分权 2 蒂伯特分权定理 3 基础教育

推荐指数 1 1 1

2009年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

科研热词 转移支付 财政转移支付 财政体制 财力 省级财政转移支付 案例 效率 政策悖论 均衡效应 匹配 农村基层组织 农村公共品 公平 事权 不均等 一事一议

推荐指数 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

2010年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

科研热词 财政分权 转移支付 财政转移支付 财政教育投入 财政支出竞争 财力均等化 激励机制 激励效应 有效性 政治平衡 基本公共服务均等化 均等化 地方官员 公共预算 公共品供给 公共卫生服务 中央财政转移支付

推荐指数 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

2011年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

财政转移支付体系优化与完善研究

财政转移支付体系优化与完善研究第一章引言财政转移支付是指中央政府将部分财政收入转移给地方政府的一种财政行为。

它扮演着促进地方经济发展、调整地区间贫富差距、保障基本公共服务等重要角色。

然而,在现实中,财政转移支付体系仍然存在诸多问题,如资金分配不均、使用效率低下等。

因此,本文拟围绕财政转移支付体系优化与完善展开研究,旨在为如何更好地实现财政转移支付的目标提供一些建议。

第二章财政转移支付的意义与原则财政转移支付对于推动我国地区经济发展具有重要意义。

首先,财政转移支付能够促进资源优化配置,弥补地方财政收入不足的缺陷。

其次,财政转移支付可以用于调整地区间贫富差距,消除地区间的不平衡发展现象。

再次,财政转移支付是保障基本公共服务的重要手段,可以确保全国范围内每个地区都能够享受到公平合理的公共服务。

第三章财政转移支付体系存在的问题然而,在现实中,财政转移支付体系仍然存在一系列问题。

首先,资金分配不均问题严重,一些贫困地区长期以来都在面临财政困难。

其次,地方政府对转移支付资金使用不规范,导致资金浪费和效率低下。

再次,由于缺乏有效的监管机制,一些地方政府存在滥用转移支付资金的问题。

第四章财政转移支付体系优化建议为了解决现有财政转移支付体系存在的问题,应采取一系列的优化措施。

首先,建立更加公平合理的财政转移支付分配机制,确保贫困地区能够获得更多的转移支付资金。

其次,加强地方政府对转移支付资金的监管,确保资金使用的规范和高效。

第三,完善财政转移支付资金的分配标准,根据地区实际情况和需求合理确定资金分配比例。

第四,加强各级政府之间的合作,推动地区间的资源共享和互利合作。

第五章国际财政转移支付经验借鉴国际上一些国家的财政转移支付经验可以为我们优化财政转移支付体系提供借鉴。

例如,加拿大的Equalization Program通过计算各个省份的财力差距,来确定转移支付的金额,确保各个省份的财政收入相对平衡。

澳大利亚的Fiscal Equalization Scheme通过调整地区间的税收差异,来实现资源的均衡配置。

【国家社会科学基金】_地方公共服务均等化_基金支持热词逐年推荐_【万方软件创新助手】_20140809

科研热词 基本公共服务 财政转移支付 财政均等化 民族地区 公共服务均等化 公共服务 非营利组织 需求因素 转移支付 财政问题 财政转移支付制度 财政能力 财政改革 财政支出比重 财政分权 财政体制 西部地区 统筹城乡 系统 省管县 生态脆弱地区 有效供给 新公共服务理论 教育经费 政府职能 平均化 对策建议 基础教育援助 均衡效应 均等化 地方政府 可持续发展 区域外部性 制度创新 分税制 内涵 公共财政 公共产品 供需缺口 供给因素 体制改革 云南

2013年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52

科研热词 均等化 基本公共服务 公共服务均等化 转移支付 基本公共服务均等化 地方政府 公共服务体系 顶层设计 财政转移支付 经验借鉴 税收返还 政治激励机制 政府间财政关系 形式与实质法治 城乡一体化 公共服务供给 集聚 身份制度 财政转移支付制度 财政投入 财政分权 财政关系 财政保障 财政体制改革 财力 评价指标体系 行政运行机制 融入城镇 老龄化 综合指数法 税收负担 社区化 社会管理 社会满意度 社会服务 社会公平 省级地方政府 现状 环境质量 环境管理体制 环境基本公共服务 环境保护 环保机构 照护体系 热钱流出 满意度 深化改革 民生财政 民生体育 根本转变 新生代农民工 新型城镇化

2008年 序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38

政府间财政关系公共经济学中国人民大学郭庆旺解析

算中确定 8. 省/地方税种的税率或税基只能在上级政府规

定的范围内变化 9. 上级政府规定税率和第税10基页/共41页

权重

1 0.8 0.6 0.5 0.4

0.3

0.2

0.1 0

2. 地方政府公共支出占国家公共支出的比 重

• 第一,伴随着改革开放和社会主义市场经济体制的建立,我 国地方政府公共支出比重明显提高,从20世纪80年代平均 56.8%,上升到90年代平均69.7%,到本世纪初再创新高, 达到70.2%,比80年代初上升了23.6%。这表明,我国财政 分权程度越来越高。

机动车辆: 牌照税 驾驶证税

营业税

消费税

财产税

土地税

使用费

中央、省 中央

中央 省、地方 省、地方

中央、省 省、地方 省、地方

中央 中央、省、地方 中央、省、地方 地方

省 省 省 省

省 省 中央、省、地方

税率决定主体 中央 中央 中央、省、地方

中央、省 中央、省 中央

中央 省、地方 省、地方

中央、省 省、地方 省、地方

2024/2/11

第20页/共41页

(二)公共物品的层次性

• 全国性公共物品应由中央政府提供 • 区域性公共物品应由省(或直辖市、自治区)提供 • 地方性公共物品应由地方政府(市、县)提供 • 对于那些具有明显利益外溢的公共物品,或由上级政府提供,或由临近上下两级政府分担提供

2024/2/11

第21页/共41页

(三)基本原则

• 经济效率原则(economic efficiency principle) ——规模经济原则(principle of the economies of scale) ——政府间竞争原则(principle of intergovernmental competition) ——公共定价原则(principle of public pricing)

国际经济学_中英名词解释

国际经济学中英名词解释Absolute advantage: The greater efficiency that one nation may have over another in the production of a commodity. This was the basis for trade for Adam Smith.绝对优势Law of comparative advantage: The less efficient nation should specialize in and export the commodity in which its absolute disadvantage is smaller (this is the commodity of its comparative advantage), and should import the other commodity.比较优势原理Ad valorem tariff: A tariff expressed as a fixed percentage of the value of a traded commodity.从价税Specific tariff:从量税A tariff expressed as a fixed sum per unit of a traded commodity.Capital-intensive commodity: The commodity with the higher capital-labor ratio at all relative factor prices.资本密集型商品Labor-intensive commodity:The commodity with the higher labor-capital ratio (L/K) at all relative factor prices.劳动密集型产品Capital inflow: An increase of foreign assets in the nation or a reduction in the nation’s assets abroad.资本流入Capital outflow: A decrease of foreign assets in the nation or an increases the nation’s assets abroad.资本流出Community indifference curve: The curve that shows the various combinations of two commodities yielding equal satisfaction to the community or nation. Community indifference curves are negatively sloped, convex from the origin, and should not across.社会无差异曲线Consumer surplus: The difference between what consumers are willing to pay for a specific amount of a commodity and what they actually pay for it.消费者剩余Producer surplus: The revenue producers receive over and above the minimum amount required to induce them to supply the good.生产者剩余Current account: The account that includes all sales and purchases of currently produced goods and services, income on foreign investments, and unilateral transfers.经常项目Credit transactions:Transactions that involve the receipt of payments from foreigners. These include the export of goods and services, unilateral transfers from foreigners, and capital inflow.贷方交易Debit transactions: Transactions that involve payments to foreigners. These include the import of goods and services, unilateral transfers to foreigners, and capital outflows.借方交易Deficit in the balance of payments:The excess of debits over credits in the current and capital accounts, or autonomous transactions, equal to the net credit balance in the official reserve account, or accommodating transactions.国际收支逆差Factor abundance: The factor of production available in greater proportion and at a lower relative price in one nation than in another nation.要素丰裕度General equilibrium analysis: The study of the interdependence that exists among all markets in the economy.一般均衡分析General equilibrium model: An economic model that studies the behavior of all producers, and traders simultaneously.一般均衡模型Heckscher-Ohlin(H-O) theory: 赫克歇尔—俄林理论The theory that postulates that(1)a nation exports commodities intensive in its relatively abundant and cheap factor and(2)international trade brings about equalization in returns to homogeneous factors across countries.Infant-industry argument: The argument that temporary trade protection is needed to set up an industry and to protect it during its infancy against competition from more established and efficient foreign firms.幼稚工业保护税Marginal rate of substitution,MRS: The amount of one commodity that a nation could give up in exchange for one extra unit of a second commodity and still remain on the same indifference curve. It is given by the slope of the community indifference curve at the point of consumption and declines as the nation consumes more of the second commodity.边际替代率Marginal rate of transformation,MRT:The amount of one commodity that a nation must give up to produce each additional unit of another commodity. This is another name for the opportunity cost of a commodity and is given by the slope of the production frontier at the point of production.边际转换率Opportunity cost theory: The theory that the cost of a commodity is the amount of a second commodity that must be given up to release just enough resources to produce one more unit of the firstcommodity.机会成本理论Dumping:The export of a commodity at below cost or at a lower price than sold domestically.倾销Persistent dumping:The continuous tendency of a domestic monopolist to maximize total profits by selling the commodity at a lower price abroad than domestically, also called international price discrimination.持久性倾销Predatory dumping: The temporary sale of commodity at a lower price abroad in order to drive foreign producers out of business, after which prices are raised to take advantage of the newly acquired monopoly power abroad.掠夺性倾销Sporadic dumping:偶尔倾销The occasional sale of a commodity at a lower price abroad than domestically in order to sell an unforeseen and temporary surplus of the commodity abroad without having to reduce domestic prices.Product cycle model:The hypothesis, advanced by Vernon, that new products introduced by industrial nations and produced with skilled labor eventually become standardized and can be produced in other nations with less skilled labor.产品周期模型Production possibility frontier:A curve showing the various alternative combinations of two commodities that a nation can produce by fully utilizing all of its resources with the best technology available to it.生产可能性边界Purchasing-power parity(PPP) theory:The theory that postulates that the change in the exchange rate between two currencies is proportional to the change in the ratio in the two countries’ general price levels.购买力平价理论Rate of effective protection:The tariff calculated on the domestic value added in the production of a commodity.有效保护率Relative purchasing-power parity theory:Postulates that the change in the exchange rate over a period of time should be proportional to the relative change in the price levels in the two nations. This version of the PPP theory has some value.相对购买力平价Small-country case:The situation where trade takes place at the pretrade-relative commodity prices in the large nation so that the small nation receives all of the benefits from trade.小国情况Specific tariff:A tariff expressed as a fixed sum per unit of a traded commodity.特别关税Terms of trade:The ratio of the index price of a nation’s export to its import commodities.贸易条件Free-trade area:自由贸易区Remove all tariff and nontariff barriers among members and maintain its own trade restrictions against outsiders.Customs union:关税同盟Removes all barriers on trade among members and harmonizes trade policies toward the rest of the world.The best example is the European Union(EU).Common market:共同市场Removes all barriers on trade among members,harmonizes trade policies toward the rest of the world,and also allows the free movement of labor and capital among member nations.An example is the European Union(EU)since January 1,1993. Economic union:经济同盟A supranational institution harmonize and administer national,social,taxation,and fiscal policies.Dumping:倾销The export of a commodity at below cost or at a lower price than sold domestically.Direct investments:直接投资Real investments in factories,capitalgoods,land,and inventories where both capital and management are involved and the investor retains control over the use of the invested capital.Interdependence: 相互依赖The (economic) relationships among nation.Increasing opportunity costs: 机会成本递增The increasing amounts of one commodity that a nation must give up to release just enough resources to produce each additional unit of another commodity.This is reflected in a production frontier that is concave from the origin.Income terms of trade:收入贸易条件The ratio of the price index of the nation’s exports to the price index of its imports times the index of the nation’s volume of exports.Immiserizing growth:悲惨性增长The situation where a nation’s terms of trade deteriorate so much as a result of growth that the nation is worse off after growth than before,even if growth without trade tends to improve the nation’s welfare.Leontief paradox:里昂惕夫之谜The empirical finding that U.S import substitutes were more K intensive than U.S exports.This is contrary to the H-O trade model,which predicts that,as the most K-abundant nation,the United States should import L-intensive products andexport K-intensive products.Multinational corporations(MNCs):跨国公司Firms that own,control,or manage production and distribution facilities in several countries.Optimum tariff:最有关税The rate of tariff that maximizes the benefit resulting from improvement in the nation's terms of trade against the negative effect resulting from reduction in the volume of trade. Pattern of trade:贸易模式The commodities exported and imported by each nation.Production possibility frontier:生产可能性曲线A curve showing the various alternative combinations of two commodities that a nation can produce by fully utilizing all of its resources with the best technology available to it.Prohibitive tariff:禁止性关税A tariff sufficiently high to stop all international trade so that the nation returns to autarky. Preferential trade arrangements:优惠贸易安排The loosest from of economic integration;provides lower barriers to trade among participating nations than on trade with nonparticipating nations.An example is the British Commonwealth Preference Scheme.Stolper-Samuelson theorem: 施托尔珀-萨缪尔森定理It postulates that free international trade reduces the real income of the nation's relatively scarce factor and increases the real income of the nation's relatively abundant factor.Terms of trade:贸易条件The ratio of the index price of a nation's export to its import commodities.Trade creation:贸易创造Occurs when some domestic production in a member of the customs union is replaced by lower-cost imports from another member nation.This increases welfare.Trade diversion:贸易转移Occurs when lowercost imports from outside the union are replaced by higher-cost imports from another union member.Byitself,this reduces welfare.Transfer pricing:转移价格The overpricing or underpricing of products in the intrafirm trade of multinational corporations in an attempt to shift income and profits from high-to low-tax nations.。

ACCA F1 重点词汇大全

ACCA F1 重点词汇大全1. Accountablity 责任2. Accounting 会计3. Activist 积极分子4. Ad hoc 临时5. Advocacy 辩护6. Agency theory 代理理论7. Aggregate demand 总需求8. Aggregate supply 总供给9. Apprisal 评估10. Artefact 人工11. Asset 资产12. Audit 审计13. Audit committee 审计委员会14. Audit trail 审计追踪15. Authority 权威16. Back-up 备份17. Balance of payment 国际收支平衡18. Bargaining power 讨价还价能力19. Belief 信仰20. Bonus scheme 奖金制度21. Boundaryless 无边界组织22. Budget 预算23. Business cycle 商业周期24. Business strategy 商业战略25. Capital 资本26. Capital expenditure 资本性支出27. Capital market 资本市场28. Centralization 集权29. Coach 教练30. Coercive 强迫31. Committee 委员会32. Competence 称职33. Compliance 遵守34. Confidentiality 保密性35. Conflict of interest 利益冲突36. Consensus 一致37. Consumer price index (CPI) 居民消费价格指数38. Consumer surplus 消费者剩余39. Contingency 权变40. Corporate 合作41. Corporate social responsibility (CSR) 企业社会责任42. Code of ethics 行为规范43. Cyclical unemployment 周期性失业44. Data 数据45. Decentralization 分权46. Delayering 简化管理结构47. Delegation 授权48. Demand 需求49. Demand curve 需求曲线50. Deontology 义务论51. Depression 萧条52. Direct discrimination 直接歧视53. Dismissal 辞退54. Diversity 多样性55. Dorming 调整期56. Double-entry bookkeeping 复式记账法57. Egoism 利己主义58. Elasticity 弹性59. Empowerment 授权60. Entrepreneurial 企业家61. Environmental footprint 环境脚印62. Equilibrium price 平衡价格63. Ethics 道德64. Exchange rate 汇率65. Executive director 执行董事66. External 外部67. Feedback 反馈68. Fiduciary responsibility 诚信义务69. Finance function 财务部70. Financial accounting 财务会计71. Financial statement 财务报表72. Firm 企业73. Fiscal policy 财政政策74. Flat organization 扁平结构75. Fraud 舞弊76. Frictional unemployment 摩擦性失业77. Generally Accepted Accounting Practice (GAAP) 美国通用会计准则78. Governance principle 治理原则79. Grievance 委屈80. Gross Domestic product 国内生产总值81. Gross National product 国民生产总值82. Group thinking 团队思维83. Hawthorne Study 霍桑实验84. Hollow organization 中空组织85. Honesty 诚实86. Hospitablity 热情87. Human Resourse Management (HRM) 人力资源管理88. Hygiene 保健89. Imperfect competition 不完全竞争90. Inbound logistic 向内运输91. Incentive 刺激92. Income 收入93. Induction 入职培训94. Inferior good 劣质产品95. Inflation 通货膨胀96. Inseparability 不可分割97. Intangibility 无形98. Integrity 诚实99. Intellectual 智商100. Interest rate 利率101. Internal audit 内审102. Internal control 内控103. International Accounting Standard Board (IASB) 国际会计准则理事会104. International Federation of Accountant (IFAC) 国际会计师联合会105. Interpersonal 人际106. Interview 面试107. Intimidation 恐吓108. Intrinsic 内部109. Job enlargement 工作扩大化110. Job enrichment 工作丰富化111. Job rotation 工作轮岗制112. Joint committee 联合委员会113. Judgement 判决114. Leadership 领导力115. Learning process 学习过程116. Liablity 负债117. Limited liability 有限责任118. Litigation 诉讼119. Lowballing 虚报低价120. Macroeconomic 宏观经济121. Management 管理122. Marginal utility 边际效益123. Market 市场124. Matrix 矩阵125. Mentor 导师126. Middle line 企业中层127. Microeconomic 微观经济128. Minimum wage 最低工资标准129. Module 模块130. Monetary policy 货币政策131. Money laundering 洗钱132. Monopolistic competition 垄断竞争133. Monopoly 垄断134. Morale 士气135. Motivation 激励136. Mourning 悲哀137. Multiplier effect 乘数效应138. Nomination committee 提名委员会139. Non-current asset 固定资产140. Non-governmental organization 非政府组织141. Norm 原则142. Objectivity 客观143. Offshore 离岸144. Oligopoly 寡头垄断145. Operational 运营146. Organization 组织147. Outbound logistic 向外运输148. Output 输出149. Oursource 外包150. Overhead 间接成本151. Ownership 所有权152. Partnership 合伙制153. Password 密码154. Payable 应付账款155. Payroll 工资156. Perception 感知157. Performance management 业绩管理158. Personality 性格159. Political 政治160. Price mechanism 定价机制161. Priortization 优先162. Privacy 隐私163. Probity 诚实164. Process 流程165. Procurement 采购166. Product life cycle 产品生命周期167. Professional 专业168. Profit 利润169. Project 项目170. Public sector 公共部门171. Purchasing 采购172. Quality control 质量控制173. Rate of unemployment 失业率174. Rational 理性175. Raw material 原材料176. Receivable 应收账款177. Recession 衰退178. Recovery 恢复179. Recruit 招聘180. Redundancy 裁员181. Relativism 相对主义182. Reputation 声誉183. Remuneration 薪酬184. Resignation 辞职185. Reward 奖励186. Retail Price Index (RPI) 居民消费价格指数187. Sarbanes-Oxley Act 萨班斯法案188. Scalar chain 层级链189. Selection 选拔190. Share capital 实收资本191. Shareholder 股东192. Social class 社会层级193. Sole trader 个体户194. Span of control 控制维度195. Spreadsheet 电子表格196. Stagflation 停滞性通货膨胀197. Stakeholder 企业利益相关者198. Strategy 战略199. Substitute 替代品200. Supervision 监督201. Supply 供给202. Synergy 协作203. Taxation 税务204. Team building 团队建设205. Teeming and lading 拆东墙补西墙206. Theorist 理论家207. Transparancy 透明208. Treasury 财政209. Uncertainty 不确定性210. Unemployment 失业211. Utilitarianism 功利主义212. Valence 效价213. Value chain 价值链214. Variable 变量215. Victimisation 受害216. Whistleblow 告密者217. Working capital 营运资本218. World Trade Organization (WTO) 世界贸易组织由东亚国际ACCA金牌讲师——孔令裔精心整理。

主权财富基金排名

主权财富基金排名根据美国主权财富基金研究所(Sovereign Wealth Fund Institute )2012年7月发布的数据,世界上排名为Country Fund Name Assets$BillionInception OriginUAE – Abu Dhabi Abu Dhabi InvestmentAuthority$627 1976 OilNorway Government Pension Fund– Global$593 1990 OilChina SAFE Investment Company $567.9** 1997 Non-Commodity Saudi Arabia SAMA Foreign Holdings $532.8 n/a OilChina China InvestmentCorporation$439.6 2007 Non-CommodityKuwait Kuwait InvestmentAuthority$296 1953 OilChina – HongKongHong Kong MonetaryAuthority Investment Portfolio $293.3 1993 Non-CommoditySingapore Government of SingaporeInvestment Corporation$247.5 1981 Non-CommoditySingapore Temasek Holdings $157.5 1974 Non-Commodity Russia National Welfare Fund $149.7 2008 OilChina National SocialSecurity Fund $134.5 2000 Non-CommodityQatar Qatar InvestmentAuthority$100 2005 OilAustralia Australian Future Fund $80 2006 Non-CommodityUAE – Dubai Investment Corporationof Dubai$70 2006 OilUAE – AbuDhabiInternationalPetroleum Investment Company$65.3 1984 OilLibya Libyan InvestmentAuthority$65 2006 OilKazakhstan Kazakhstan NationalFund$58.2 2000 OilAlgeria Revenue Regulation Fund $56.7 2000 Oil UAE – Abu Dhabi Mubadala DevelopmentCompany$48.2 2002 OilSouth Korea Korea Investment $43 2005 Non-CommodityCorporationUS – Alaska Alaska Permanent Fund $40.3 1976 OilMalaysia Khazanah Nasional $36.8 1993 Non-Commodity Azerbaijan State Oil Fund $30.21999 OilIreland National PensionsReserve Fund$302001 Non-Commodity Brunei Brunei InvestmentAgency$301983 OilFrance Strategic InvestmentFund$282008 Non-Commodity US – Texas Texas Permanent SchoolFund$24.41854 Oil & Other Iran Oil Stabilisation Fund $231999 OilNew Zealand New ZealandSuperannuation Fund $15.92003 Non-Commodity Canada Alberta’s HeritageFund$15.11976 Oil Chile Social and EconomicStabilization Fund$152007 Copper US – New Mexico New Mexico StateInvestment Council$14.31958 Non-Commodity Brazil Sovereign Fund ofBrazil$11.32008 Non-Commodity East Timor Timor-Leste PetroleumFund$10.22005 Oil & Gas Bahrain Mumtalakat HoldingCompany$9.12006 Non-Commodity Oman State General ReserveFund$8.21980 Oil & Gas Peru Fiscal StabilizationFund $7.11999 Non-Commodity BotswanaPula Fund$6.91994 Diamonds & Minerals Mexico Oil RevenuesStabilization Fund of Mexico$6.02000 Oil Saudi Arabia Public Investment Fund $5.32008 OilChina China-AfricaDevelopment Fund $5.02007 Non-Commodity US – Wyoming Permanent WyomingMineral Trust Fund$4.71974 Minerals Chile Pension Reserve Fund $4.42006CopperTrinidad & Tobago Heritage andStabilization Fund $2.9 2000 OilUS – Alabama Alabama Trust Fund $2.5 1985 Oil & Gas Italy Italian Strategic Fund $1.4 2011 Non-Commodity UAE – Ras Al Khaimah RAK InvestmentAuthority$1.2 2005 OilNigeria Nigerian SovereignInvestment Authority $1 2011 OilPalestine Palestine InvestmentFund$0.8 2003 Non-CommodityVenezuela FEM $0.8 1998 OilVietnam State CapitalInvestment Corporation $0.5 2006 Non-CommodityKiribati Revenue EqualizationReserve Fund$0.4 1956 PhosphatesGabon Gabon Sovereign WealthFund$0.4 1998 OilIndonesia Government InvestmentUnit$0.3 2006 Non-CommodityMauritania National Fund forHydrocarbon Reserves$0.3 2006 Oil & GasUS – North Dakota North Dakota LegacyFund$0.1 2011 Oil & GasEquatorial Guinea Fund for FutureGenerations $0.08 2002 OilUAE – Federal Emirates InvestmentAuthority n/a 2007 OilOman Oman Investment Fund n/a 2006 Oil UAE – Abu Dhabi Abu Dhabi InvestmentCounciln/a 2007 OilPapua New Guinea Papua New GuineaSovereign Wealth Fund n/a 2011 GasMongolia Fiscal Stability Fund n/a 2011 Minerals Total Oil & Gas Related $2,863.9 Total Other $2,155.2 TOTAL $5,019.1All figures quoted are from official sources, or, where the institutions concerned do not issue statistics of their assets, from other publicly available sources. Some of these figures are best estimates as market values change day to day.Recent Sovereign Wealth Fund Market Size by QuarterSep2007 Dec2007Mar2008Jun2008Sep2008Dec2008Mar2009Jun2009Sep2009Dec2009Mar2013,265 3,259 3,427 3,916 4,054 4,140 3,749 3,790 3,914 4,022 4,052Jun2010 Sep201Dec201Mar2011Jun2011Sep2011Dec2011Mar2012Jun20124,107 4,154 4,406 4,551 4,731 4,847 4,830 4,995 5,019 Source: /view/1174598.htm。

英美概况总复习题目汇总

1. What are the functions of the Bank of England?Answer: Britain's central bank, working in close contact with the government for the control of monetary policy and for giving directives to commercial banks. It is the only note issuing bank in England and Wales. It is also responsible for keeping the exchange rate of British Pound against other currencies within certain limits by operating an Exchange Equalization Account.2. Which are the major political parties now in Britain?Answer: Although there are so many different parties in the United Kingdom, British politics is after all a battle between Conservative and Labor.The Conservative Party believes firmly in private enterprises and free competition. But it did not undo the social legislations passed by the Labor Government. The Labor Party, which is in power now, has traditionally drawn support from the trade unions. It has embraced socialist ideas, supported governmental control of important industries and advocated more equal distribution of the wealth.Among some the key issues around which are the two parties fight are foreign policy and economic policy. Pro-Americanism is thus at the center of British foreign policy for both Conservative and Labor governments, though the opposition always accuses the party in power of being too pro-American.The battle between the two parties over economic policy centers on nationalization and privatization. The Conservatives have been very firm in their belief in free-trade and marketeconomy, while the Labor Party, owing to its socialist origin, has always emphasized the importance of government involvement in the national economy and the role of the state as provider of welfare benefits to citizens.3. What is a welfare state?Answer: The welfare state includes Stoical Security, the National Health Service, the Housing Program, education, and personal services.4. As the Head of State, does the monarch exercise political powers?Answer: The monarch played an active role in making political decisions, but now the monarch functions only as the symbol of the country's unity and formal Head of State.5. Which branch of the Parliament plays a more important role in the law-marking process? Why?Answer: The most important function of the House of Commons is to make laws, known as Act of Parliament. Although both houses are involved in the law making process, the House of Commons has primacy axation Andover the House of Lords, especially in the processing of "money bills" that concern t public expenditure.6. What’s the relationship between the Parliament and the Cabinet in UK?Answer: Parliament is the law-making body of the United Kingdom. The Prime Minister is usually the leader of the majority party in Parliament. After each general election, the monarch would ask the leader of the winning party to be the Prime Minister and form a new Cabinet. The Cabinet is at the center of the British political system. It is the supreme decision-making body in British government. Cabinet members are chosen by the Prime Minister from members of his own political party in Parliament.7. How many stages is education in the U.K divided into and what are they?Answer: primary, secondary, further education, higher education.8. What are the basic characteristics of British foreign policy after World Wall П?Answer: After World Wall П, Britain adopted an isolationist policy toward Europe but cooperated very closely with the United States in the Cold War.9. Which river is the longest in Canada?Answer: Mackenzie is the longest river in Canada.10. What religion is the most dominant in Canada?Answer: Roman Catholicism.11. What are the indigenous people of Canada?Answer: They are the Indians and the Intuits12. What are the most important sectors in the Canadian economy?Answer:The most important sectors in the Canadian economy are manufacturing industry,IT industry, chemical industry, services, minerals industry , foreign trade, forestry and forest industry, paper industry, agriculture, fishery, energy industry.13. Who were the WASPs?Answer: The WASPs were the White Anglo-Saxon Protestants from England who began to immigrate to America in 1607 and played an important role in winning America's independence from Britain.14. What are the main principles of government in the United States?Answer: The principles of federalism, the separation of powers and the rule of law are the main principles of government in the United States.15. What is the Bill of Rights?Answer:The Bill of Rights belong to the amendment. Amendments can be added to the Constitution when proposed by two thirds of the total members of Congress and ratified by threefourths of all the states.The first ten amendments are known as the Bill of Rights which was ratified in 1791. It listed the rights of the people which the government can not deprive, including the right to freedom of speech and religion, the right to bear arms, the right to jury trial, and the right to security of person and property. The Bill of Rights has since been regarded as the fundamental protection of individual rights against arbitrary power of the government.16. How is the president of the United States elected?Answer: The president of the United States is elected for a term of four years by Electoral College. The presidential candidate who gets the majority of electoral votes becomes the president. The presidential election is a fight between the Republican Party and the Democratic Party. The presidential election is done in four stages: first, each of the major party conducts state primary elections to elect delegates to the party convention. The second stage is the party conventions. The third stage is the general election. And the fourth stage is the general vote which is usually held in early November.17. How do the three branches of government check against each other?Answer: No one of the legislative, executive, judicial branches may dominate the others.18. What are the different types of institutions that providehigher education?Answer: There are universities and colleges, vocational and technical institutes.19. What are the most popular forms of American music and how did they develop?Answer: The most popular forms of American music are Jazz, rock and roll and western and country music. Music is an important part of every American’ life Americans use music, especially popular music to convey cultural and social information and to express their emotions. American popular music is often regarded as a symbol of rebellion of the youth against tradition. A famous popular music event in 1969, the Woodstock Art and Fair drew a crowd of 300000 young people .so the Young people is important factors of development.20. Why do Americans love sports?Answer:①Because Americans are very conscious about health and regard outdoor activities as a way to keep healthy and fit;②Because sports are used to express their interests in keeping fit;③Because sports also allow them to engage in mass culture and occupy their leisure time.21. Why did Americans adopt a policy of neutrality at the beginning of both world wars?Answer: Because American's isolationist policy toward European, and American did not want to be involved in European entanglement and stay out of any European conflicts, since the wars too far to affect American.22. How did Australia start as a nation?Answer: Modern Australia has its origin in the 18th century when the Europeans went there. It became a national state on the first day of the 20th century. However, the Aborigine people had lived there for about 60,000 years before the Europeans got there. They were nomadic hunters and food-gatherers, living in extended family groups formed into tribes. Before the Europeans went there, their population was somewherebetween 600,000 and one million. But about to half of the population died after the Europeans got there and exposed them to diseases such as small pox and measles, againstwhich they had no immunity. This rendered the localpopulation powerless against the Europeans when the latter began to arrive in arrive in large numbers in the late 18thcentury.23. Who are the New Zealanders?Answer: The Maori people are natives of the New Zealander. They are Polynesian in origin and probably came to settle in New Zealand in canoes about the 9th to 13th century AD.24. When and why did the British assume authority over New Zealand?Answer: In the 1830s, the British saw it as a way to solve the English economic problem by transferring English capital and surplus labor to New Zealand and create a new English society there.25. Why has sheep been so important to New Zealand?Answer: Because wool export became the founding stone of New Zealand’s economy.26. What is the Conservative Party’s solution to the economic problems in the 1970s? Was it successful? (Answer in Page14) Answer: In 1970s the Conservative Party denationalized most of the industries controlled by the government for the purpose of stimulating private competition.It has achieved some success but unemployment is still high.27. What are the elements that form the national government of the United Kingdom?Answer: The British government comprises the monarch, the parliament and the executive branch led by the prime minister.28. What is the fundamental government policy for education in the United Kingdom?Answer: Compulsory for all children between the ages of 5 and 16 is the fundamental government policy for education in the United Kingdom.29. What is Tony Blair’s “the Third Way”?Answer: Tony Blair’s the “Third Way” which was different from both the old Labor Party’s commitment to the nationalization of the economy and its close relationship with the trade unions and the Conservative Party’s emphasis of extreme individualism and its rejection of community. He is committed to long term economic stability and fiscal transparency. In order to separate politics and economic policy, he made the Bank of England independent. In social policy, the Blair government changed the old Labor Pa rty’s practice of using tax system, public expenditure and price control to reduce inequality and has put emphasis on minimum wage, and supplementing low wages. It also emphasizes individual responsibility.30. What are the differences between the Conservative Party and the Labor Party in their principles? (Chapter13: Britain in the 20th Century)Answer: The Labor Party adopted the principle of Welfare State, full employment and government control of economic development. But the Conservative Party adopted the privatization of state-owned industries and free labor market.。

复旦大学经济学考研参考书目

承载梦想,启航未来

贸易政策分析包括基本政策工具和措施及其衡量、国际贸易政策 效应分析、国际 贸易政策的动因分析、区域经济一体化分析、国际 贸易多边体制分析等内容。

一、李嘉图模型 (一)绝对优势和比较优势 (二)封闭经济和开放经济下的生产可能性边界 (三)超额需 求和国际市场均衡 (四)绝对优势和实际工资水平 (五)贸易利得的分配 二、赫克歇尔-俄林模型(H-O 模型)

生具备这些相关课程或内容模块的本科生阶段知识及能力水平。 模块一:世界经济和国别经济 基本要求:该模块要求考生掌握国际经济关系的演变与特点;掌 握经济全球 化与区域经济体一体化发展趋势及规律;掌握国际贸易 与投资协定的发展、内容 与主要特点。 一、引进外资与东道国(母)经济发展 (一)外商直接投资 (二)国际间接投资 (三)中国外资经济 发展战略与外资经济发展的国际经验 二、经济全球化与区域经济一体化 (一)经济全球化理论与实践 (二)区域经济一体化理论与实 践 (三)经济全球化与区域经济一体化的关系 三、国际贸易与投资 协定 (一)多边国际贸易协定的逻辑 (二)双边与区域国际贸易与 投资协定 (三)国际贸易与投资协定中的劳工与环境问题 (四)主 要的国际贸易与投资协定 模块二:国际贸易 基本要求:该模块主要包括两部分内容,即国际贸易纯理论与国 际贸易政策。 国际贸易纯理论包括新古典贸易理论、新贸易理论和异质性企业 贸易理论。国际

(五)斯托珀尔-萨缪尔森定理(Stolper-Samuelson theorem, 简称 SS 定

理) (六)要素禀赋与国际贸易的实证分析 三、特定要素模型 (一)特定要素模型 (二)赫克歇尔-俄林模型中定理的变型 (三)特定要素模型的实证分析

承载梦想,启航未来

四、新贸易理论 (一)垄断竞争模型下的规模报酬递增 (二)寡头垄断模型下的规模报酬递增 (三)新贸易理论的贸易利得来源 (四)新贸易理论下的引力模型 (五)新贸易理论下的实证分析 五、异质性企业贸易理论(又称为新-新贸易理论) (一)地理与贸易成本 (二)企业异质性与企业的出口行为 (三)异质性企业贸易理论的贸易利得 (四)异质性企业贸易理论下的引力模型 (五)对于异质性企业贸易理论的实证检验 六、生产要素贸易 (一)在商品贸易上增加生产要素贸易 (二)生产要素贸易的短期和长期均衡 (三)要素贸易与商品贸易之间的替代关系 (四)要素贸易与商品贸易之间的互补关系 七、国际贸易政策措施及其衡量 (一)国际贸易政策措施 (二)国际贸易政策措施的衡量 八、国际贸易政策原理及其经验分析

中美的会计准则制度差异英语作文

中美的会计准则制度差异英语作文The accounting standards and systems in China and the United States exhibit notable differences, reflecting the unique economic, regulatory, and cultural environments in each country. These variations can impact financial reporting practices, investor confidence, and overall transparency in financial markets. In this essay, I will outline some of the key differences between the accounting standards and systems in China and the United States.One of the major differences between China and the United States lies in the regulatory frameworks governing accounting standards. In the United States, the Financial Accounting Standards Board (FASB) is responsible for establishing and updating Generally Accepted Accounting Principles (GAAP), which are followed by most U.S. companies. On the other hand, China follows the Chinese Accounting Standards (CAS) issued by the Ministry of Finance, which are more closely aligned with International Financial Reporting Standards (IFRS).Another key difference is the level of enforcement and scrutiny of accounting standards. In the United States, the Securities and Exchange Commission (SEC) plays a significant role in regulating financial reporting and ensuring compliance with GAAP. There are strict regulatory requirements for public companies to maintain transparency and accountability in their financial reporting. In China, the regulatory environment is still evolving, and there have been concerns about the enforcement of accounting standards and the quality of financial information disclosed by Chinese companies.Additionally, cultural factors can influence accounting practices in China and the United States. In China, there may be a greater emphasis on maintaining harmonious relationships and preserving reputation, which could impact the transparency and accuracy of financial reporting. In contrast, the United States has a more litigious culture, which may lead to greater scrutiny and accountability in financial reporting practices.Overall, the differences between the accounting standards and systems in China and the United States highlight the importance of understanding the unique regulatory, cultural, and economic factors that shape financial reporting practices in each country. As global markets become increasingly interconnected, it is crucial for companies, investors, and regulators to navigate these differences and promote transparency and integrity in financial reporting across borders.。

国际经济名词解释英文重点总结

1、Absolute trade theory(main idea)绝对贸易理论:the greater efficiency that one nation may have over another in the production of a commodity. conclusion: Both countries have absolute advantage in one commodity commodity’’s production because the natural or acquired advantage. If each nation specializes in the production of the commodity of its absolute advantage and exchanges part of its output for the commodity of its absolute disadvantage, both nations benefit from the trade.2、▲Absorption approach :一、一、Overview of The Absorption Approach: Overview of The Absorption Approach:1)1) The absorption approach was put forward by Alexander in 1952. 2)2) This approach emphasizes changes in real domestic income and absorption as adeterminant of a nation determinant of a nation’’s balance of payments.3)3) The balance of trade is viewed as the difference between what the economyproduces and what it absorbs for domestic use.二、二、Absorption : Absorption :1) A nation nation’’sabsorption falls into three categories, consumption (c), investment (i), government purchase (g).2) The domestic absorption (a)a a 符号:符号:“比等号再多一道”“比等号再多一道” c + i + g c + i + g1、▲Balance of payments equilibrium and adjustment :Balance of payments equilibrium is a state that the debits equals to the credits in the autonomous transactions. This would simply mean that their stocks of international reserves are unchanging. 2、▲Balance of payments equilibrium and disequilibrium : (一)(一)Balance of payments equilibrium: is a state that the debits equals to the Balance of payments equilibrium: is a state that the debits equals to the credits in the autonomous transactions. This would simply mean that their stocks of international reserves are unchanging.(二)(二)Disequilibrium Disequilibrium in balance of payments payments::1)Deficit in the balance of payments: the excess of debits over credits in the autonomous transactions. Deficit countries will experience reserve asset losses. 2) Surplus in the balance of payments: the excess of credits over debits in the autonomous transactions. surplus countries will experience reserve asset accumulation.3、▲Basic theories of the balance of payments:1) The Elasticity Approach to Balance-of-Payments2) The absorption approach to the balance of payments3) The monetary approach to the balance of payments1、Comparative trade theory 比较贸易理论:(main (main points)A points)A points)A country has a comparative country has a comparative advantage in producing a goods if the opportunity cost of producing that goods in terms of other goods is lower in that country than it is in other countries. basic ideas: Even if a nation has an absolute disadvantage in the production of both goods, a basis for mutually beneficial trade may still exist.In this case, countries should specialize where they have their greatest absolute advantage (if they have absolute advantage in both goods) or in their least absolute disadvantage (if they have absolute advantage in neither goods). (两利相权取其重,两害相权取其轻)两害相权取其轻)2、Competitive advantage of nations :美国美国 20C80 20C80 20C80、、90年代迈克尔年代迈克尔--波特认为:具有比较优势的国家未必具有竞争优势。

财政与税务系课程介绍(中英对照)

财政与税务系课程介绍(中英对照)序号:1课程编码:17001030、17001020课程名称:财政学学分:3周学时:3开课系部:财政与税务系预修课程:微观经济学修读对象:本科生课程简介:本课程主要讲授财政学的基本理论、基本知识和基本管理技能,以财政支出和财政收入为核心。

主要内容包括:财政的概念、财政职能、财政支出的规模和结构、财政收入的规模和结构、税收原理、国债原理、国债规模与国债市场、国家预算管理体制、财政赤字、财政政策和开放经济下的财政问题。

通过教学,使学生掌握财政学的基本原理和理论,为其它专业课的学习打下基础。

拟用教材:《财政学》,陈共编著,中国人民大学出版社,2004年3月第四版参考教材:《财政学教程》,聂庆轶、陈业俊编著,立信会计出版社,2005年12月第二版Course Code:17001030、17001020Course Name:Public FinanceCredit:3 creditsLesson Hours:3h per weekDepartment:Finance & Taxation DepartmentAnterior Course:MicroeconomicsObjective Students:Undergraduate StudentsSummary of the Course:The course introduces the basic theory, knowledge and managing skill, in which thepublic expenditure and revenue is the kernel. It mainly includes the concept andfunctions of public finance, the scale and structure of public expenditure and revenue,basic theory of taxation, basic theory and scale of national debt, national debt market,managerial system of national budget, fiscal deficit, fiscal policy and fiscal issues in theopen economy. The course aims to help students learn the basic theory of public financeso as to build good base of future relevant course learning.Teaching Material:Public Finance by Chen Gong, Remin University of China Press,fourth edition,March, 2004Reference:A course of Public Finance by Nie Qingyi and Chen Yejun, Lixin Accounting Press,second edition, Dec 2005序号:2课程编码:17002020课程名称:税收学学分:2周学时:2开课系部:财政与税务系预修课程:微观经济学、宏观经济学、财政学修读对象:本科生课程简介:本课程主要讲授税收的基本原理和我国现行税收制度概况。

浅析美国与卢森堡税收协定的利益限制条款

浅析美国与卢森堡税收协定的利益限制条款浅析美国与卢森堡税收协定的利益限制条款来源:《税务研究》2015年02期作者:吴青伦内容提要:为防⽌滥⽤税收协定⽽出台的协定利益限制条款,规定⼗分繁复。

本⽂以美国与卢森堡税收协定为例,分析利益限制条款的应⽤机制(特别是各种主要测试,如合格居民测试、所有权与税基侵蚀测试、公开公司测试和衍⽣利益测试等客观测试,积极商业测试、税局裁量条款测试和运营总部测试等主观测试),以期在国际税收竞合上寻求⼀个平衡点。

关键词:协定利益限制条款税收协定反滥⽤税收协定商业实质为了防⽌滥⽤税收协定和消除其他国家认为美国会⽤国内税法推翻协定的疑虑,从1970年代末期,美国开始在谈判税收协定的过程中,引进利益限制条款(Limitation on Benefits Clause),也就是著名的LOB条款,并将其纳⼊1981年的美国税收协定范本第16条。

如今,美国对外签订的⼤多数税收协定都包含有LOB条款。

不过,LOB条款就好⽐是国际税法⾥的⼋阵图,即便是实务⼯作者对该条款也时常有雾⾥看花的感觉。

但⽬前看来,LOB条款这套杀⼿锏的警⽰效果倒是不差,因此,其他国家也开始仿效,例如印度和⽇本。

本⽂将以美国与卢森堡税收协定(以下简称“美卢税收协定”)为例,简要梳理LOB条款的主要应⽤要点。

⼀般来说,LOB条款的应⽤机制,主要可以分为客观测试(objective tests)和主观测试(subjectivetests)两⼤类。

客观测试,主要是检验居民的某些攸关的实际情况,如股权结构和税基扣除情形,通过者就可以不论是哪项所得,来享受完整的协定利益。

⽽主观测试则是重视背后的运营动机。

不过,⼀旦涉及所谓的三⽅交易(triangular case)或不对称所得(disproportionate part of theincome),相关的协定利益还是会受到限制,甚⾄完全被否决。

⼀、客观测试(⼀)合格居民测试正如美卢税收协定第24条第1款所规定,此协定下的所有利益,必须是该条第2款所定义的合格居民(qualifiedresident)才能享受。

经济学最全词典中英对照

经济学词典提供经济学词典.向他致敬!Ability-to-pay principle(of taxation)(税收的)支付能力原则按照纳税人支付能力确定纳税负担的原则。

纳税人支付能力依据其收人或财富来衡量。

这一原则并不说明某经济状况较好的人到底该比别人多负担多少。

Absolute advantage(in international trade)(国际贸易中的)绝对优势A国所具有的比B国能更加有效地(即单位投入的产出水平比较高等)生产某种商品的能力。

这种优势并不意味着A国必然能将该商品成功地出口到B国。

因为B国还可能有一种我们所说的比较优势或曰比较利益(comparative advantage)。

Accelerator principle 加速原理解释产出率变动同方向地引致投资需求变动的理论。

Actual,cyc1ical,and structual budget 实际预算、周期预算和结构预算实际预算的赤字或盈余指的是某年份实际记录的赤字或盈余。

实际预算可划分成结构预算和周期预算。

结构预算假定经济在潜在产出水平上运行,并据此测算该经济条件下的政府税入、支出和赤字等指标。

周期预算基于所预测的商业周期(及其经济波动)对预算的影响。

Adaptive expectations 适应性预期见预期(expectations)。

Adjustable peg 可调整钉住一种(固定)汇率制度。

在该制度下,各国货币对其他货币保持一种固定的或曰“钉住的”汇率。

当某些基本因素发生变动、原先汇率失去合理依据的时候,这种汇率便不时地趋于凋整。

在1944-1971年期间,世界各主要货币都普遍实行这种制度,称为“布雷顿森林体系”。

Administered(or inflexible)prices 管理(或非浮动)价格特指某类价格的术语。

按照有关规定,这类价格在某一段时间内、在若干种交易中能够维持不变。

(见价格浮动,price flexibility)Adverse selection 逆向选择一种市场不灵。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。